A Dynamic Multi-Objective Duopoly Game with Capital Accumulation and Pollution

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Model

3. Open-Loop Nash Equilibria

3.1. Optimality Conditions

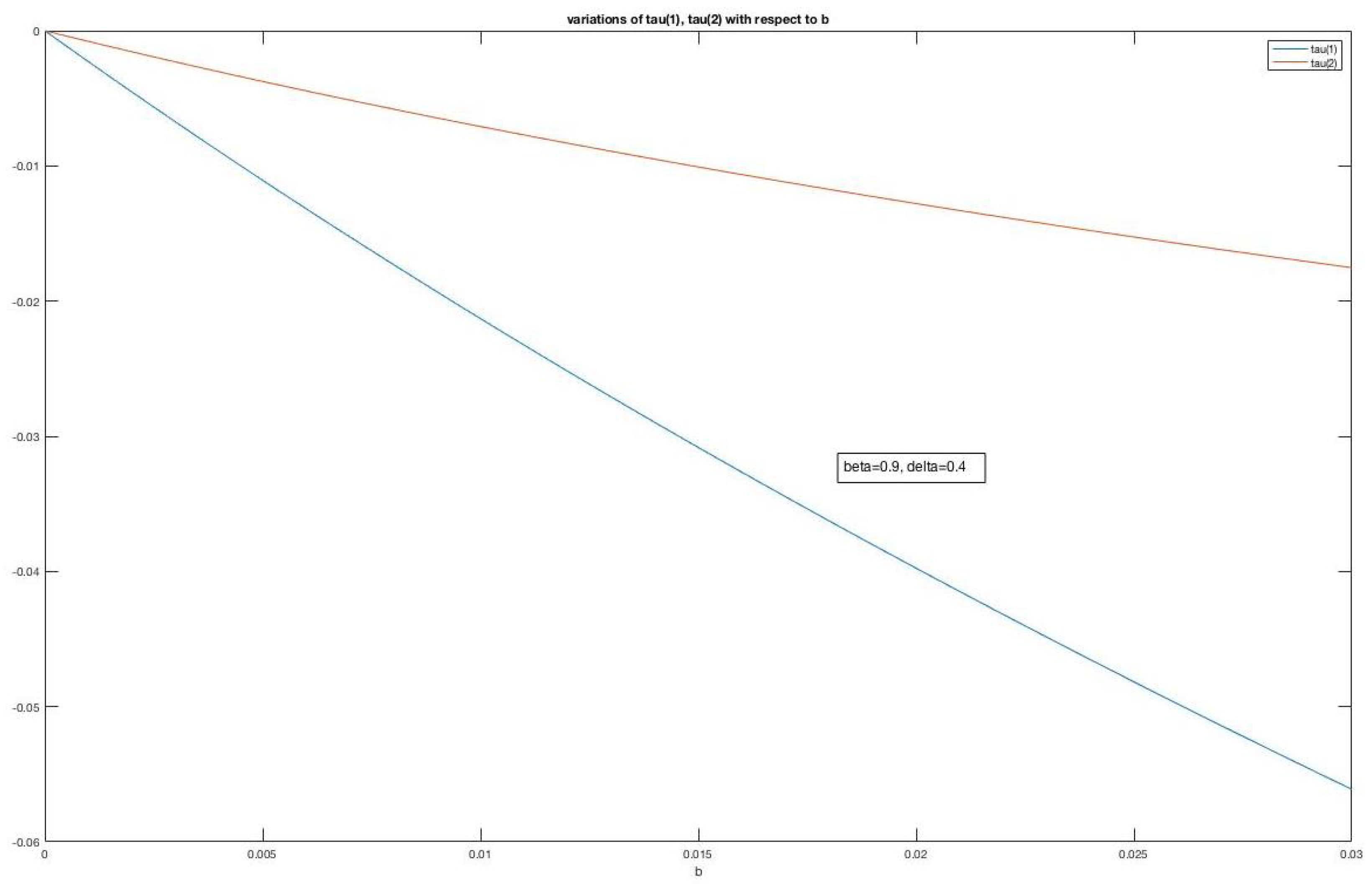

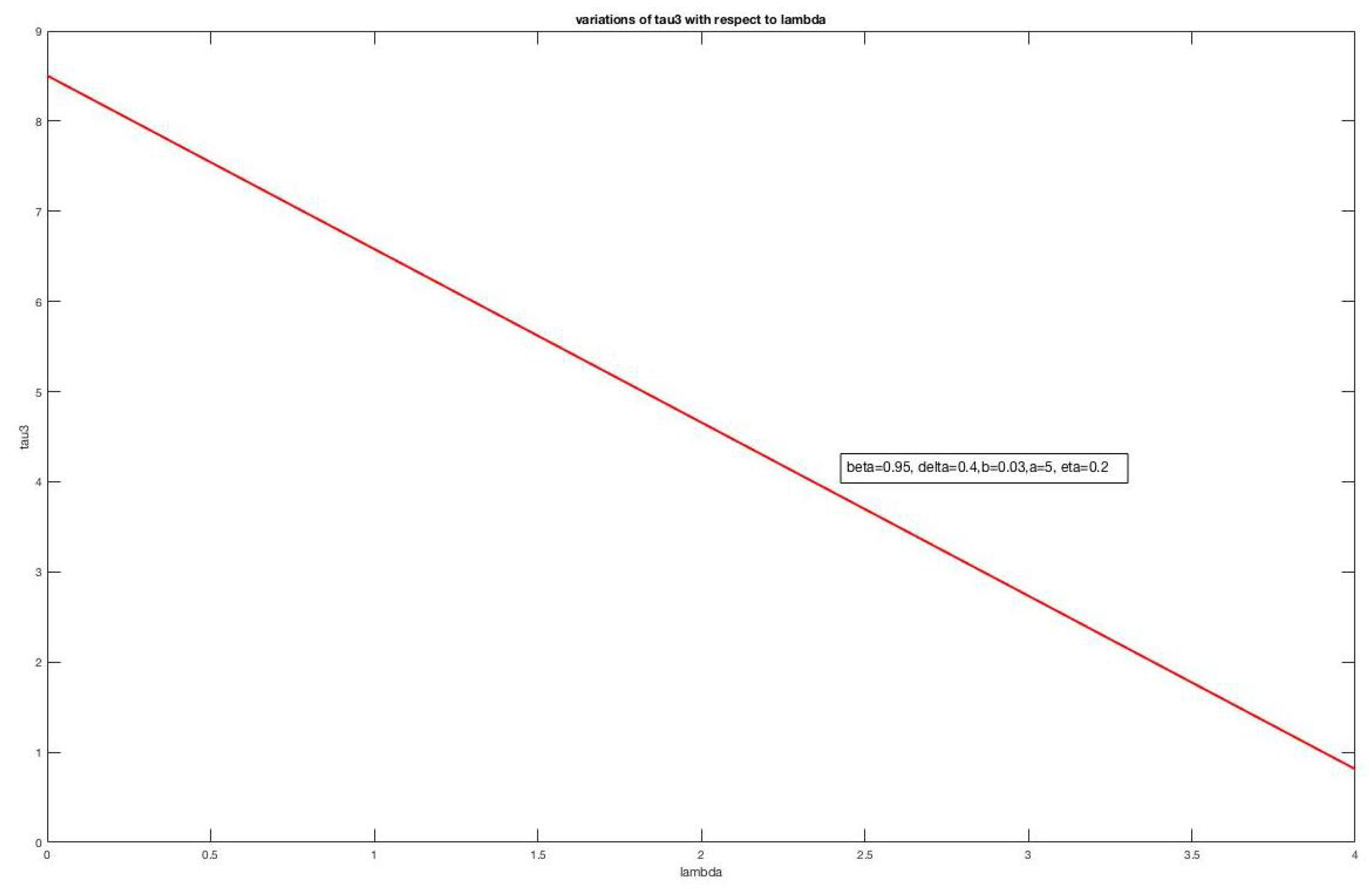

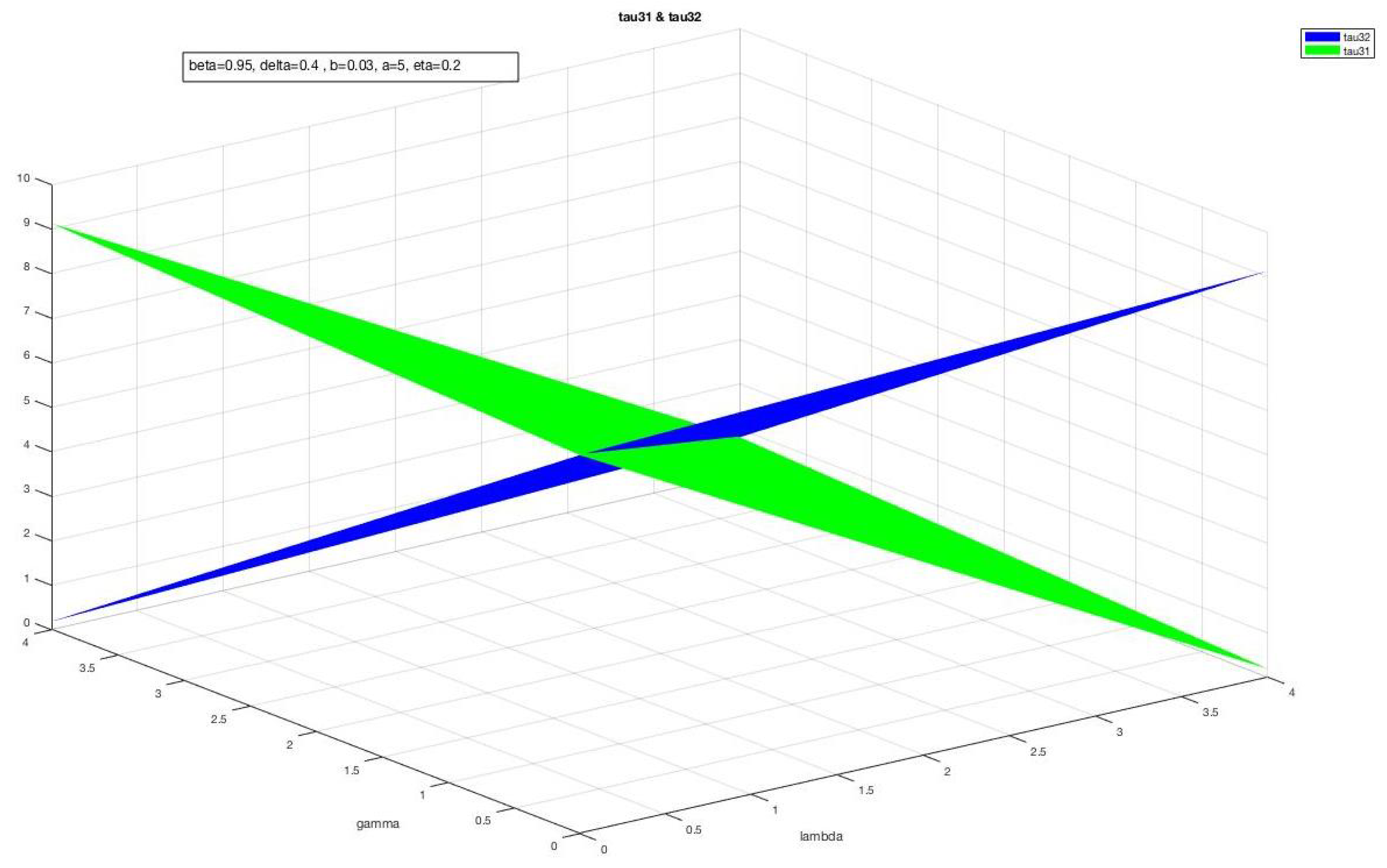

3.2. Sensitivity Analysis

4. Feedback Nash Equilibria

4.1. Necessary Conditions for a Feedback Nash Equilibrium

4.2. Symmetric and Partially Symmetric Nash Equilibria

4.2.1. Existence and Properties of Symmetric Feedback Nash Equilibria

4.2.2. Existence and Properties of Partially Symmetric Equilibria

5. Cooperative Equilibrium

6. Comparison

6.1. Comparing the Open-Loop and the Feedback Nash Analysis in the Completely Symmetric Case

6.2. Cooperative vs. Non-Cooperative Open-Loop Equilibria

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Wirl, F.; Feichtinger, G.; Kort, P.M. Individual Firm and Market Dynamics of CSR Activities. J. Econ. Behav. Organ. 2013, 86, 169–182. [Google Scholar] [CrossRef]

- Lambertini, L.; Palestini, A.; Tampieri, A. CSR in an Asymmetric Duopoly with Environmental Externality. South. Econ. J. 2016, 83, 236–252. [Google Scholar] [CrossRef]

- Yanase, A. Corporate Environmentalism in Dynamic Oligopoly. Strateg. Behav. Environ. 2013, 3, 223–250. [Google Scholar] [CrossRef]

- Feichtinger, G.; Lambertini, L.; Leitmann, G.; Wrzaczek, S. R & D for Green Technologies in a Dynamic Oligopoly: Schumpeter, Arrow and Inverted U’s. Eur. J. Oper. Res. 2016, 249, 1131–1138. [Google Scholar]

- Rettieva, A. Equilibria in Dynamic Multicriteria Games. Int. Game Theory Rev. 2017, 19, 1750002. [Google Scholar] [CrossRef]

- Rettieva, A. Dynamic Multicriteria Games with Finite Horizon. Mathematics 2018, 6, 156. [Google Scholar] [CrossRef] [Green Version]

- Kuzyutin, D.; Gromova, E.; Pankratova, Y. Sustainable Cooperation in Multicriteria Multistage Games. Oper. Res. Lett. 2018, 46, 557–562. [Google Scholar] [CrossRef]

- Kuzyutin, D.; Smirnova, N.; Gromova, E. Long-Term Implementation of the Cooperative Solution in a Multistage Multicriteria Game. Oper. Res. Perspect. 2019, 6, 100107. [Google Scholar] [CrossRef]

- Crettez, B.; Hayek, N. A Dynamic Multi-objective Duopoly Game with Environmentally Concerned Firms. Int. Game Theory Rev. 2021, 2150008. [Google Scholar] [CrossRef]

- Reynolds, S.S. Investment, Preemption and Commitment in an Infinite Horizon Model. Int. Econ. Rev. 1987, 28, 69–88. [Google Scholar] [CrossRef]

- Bhaumik, A.; Roy, S.K.; Li, D.-F. Analysis of Triangular Intuitionistic Fuzzy Matrix Games Using Robust Ranking. J. Intell. Fuzzy Syst. 2017, 33, 327–336. [Google Scholar] [CrossRef]

- Roy, S.K.; Bhaumik, A. Intelligent Water Management: A Triangular Type-2 Intuitionistic Fuzzy Matrix Games Approach. Water Resour Manag. 2018, 32, 949–968. [Google Scholar] [CrossRef]

- Bhaumik, A.; Roy, S.K.; Weber, G.W. Hesitant interval-valued intuitionistic fuzzy-linguistic term set approach in Prisoners’ dilemma game theory using TOPSIS: A case study on Human-trafficking. Cent. Eur. J. Oper. Res. 2020, 28, 797–816. [Google Scholar] [CrossRef]

- Bhaumik, A.; Roy, S.K.; Li, D.F. (α, β, γ)-cut set based ranking approach to solving bi-matrix games in neutrosophic environment. Soft Comput. 2021, 25, 2729–2739. [Google Scholar] [CrossRef]

- Roy, S.K.; Maiti, S.K. Reduction methods of type-2 fuzzy variables and their applications to Stackelberg game. Appl. Intell. 2020, 50, 1398–1415. [Google Scholar] [CrossRef]

- Lambertini, L. Differential Games in Industrial Economics; Cambridge University Press: Cambridge, UK, 2018. [Google Scholar]

- Qu, S.; Ji, Y. The Worst-Case Weighted Multi-Objective Game with an Application to Supply Chain Competitions. PLoS ONE 2016, 11, e0147341. [Google Scholar] [CrossRef] [PubMed]

- Hayek, N. Infinite-Horizon Multiobjective Optimal Control Problems for Bounded Processes. Discret. Contin. Dyn. Syst. Ser. S 2018, 11, 1121. [Google Scholar] [CrossRef] [Green Version]

- Dawid, H.; Kopel, M.; Kort, P.M. New Product Introduction and Capacity Investment by Incumbents: Effects of Size on Strategy. Eur. J. Oper. Res. 2013, 230, 133–142. [Google Scholar] [CrossRef]

- Cabo, F.; Martín-Herràn, G.; Martínez-García, M.P. Non-constant Discounting, Social Welfare and Endogenous Growth with Pollution Externalities. Environ. Resour. Econ. 2020, 76, 369–403. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Crettez, B.; Hayek, N.; Kort, P.M. A Dynamic Multi-Objective Duopoly Game with Capital Accumulation and Pollution. Mathematics 2021, 9, 1983. https://doi.org/10.3390/math9161983

Crettez B, Hayek N, Kort PM. A Dynamic Multi-Objective Duopoly Game with Capital Accumulation and Pollution. Mathematics. 2021; 9(16):1983. https://doi.org/10.3390/math9161983

Chicago/Turabian StyleCrettez, Bertrand, Naila Hayek, and Peter M. Kort. 2021. "A Dynamic Multi-Objective Duopoly Game with Capital Accumulation and Pollution" Mathematics 9, no. 16: 1983. https://doi.org/10.3390/math9161983

APA StyleCrettez, B., Hayek, N., & Kort, P. M. (2021). A Dynamic Multi-Objective Duopoly Game with Capital Accumulation and Pollution. Mathematics, 9(16), 1983. https://doi.org/10.3390/math9161983