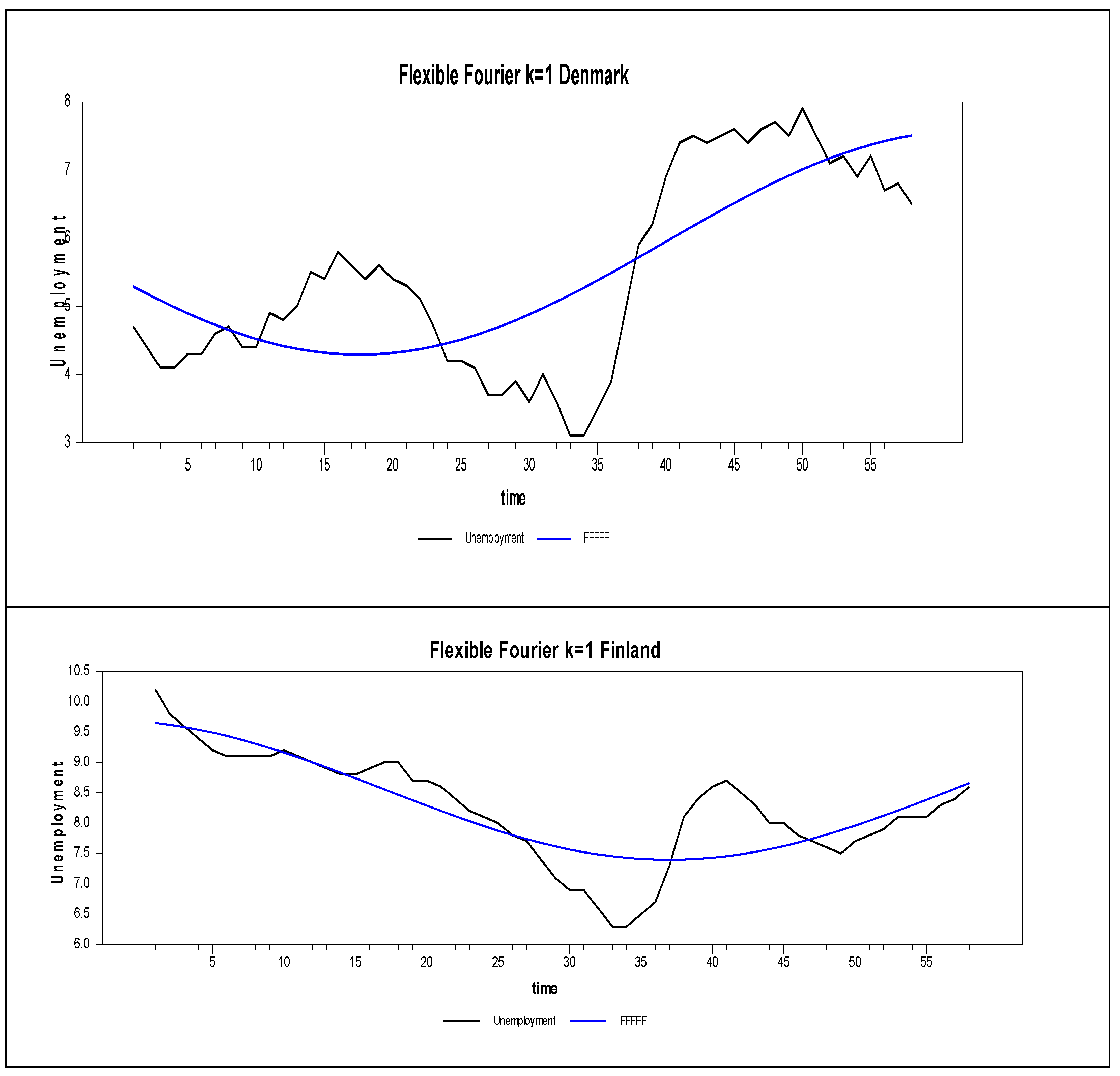

2.1. Common Correlated Estimator in Panel Unit Root Testing

In this part, we introduce a practical way to refine the CCE estimator of [

8]. In the author’s well-known paper, he introduces an auxiliary regression to remedy cross-sectional dependency. In line with [

8], we consider the following heterogeneous panel ADF regression:

where

is the unobserved common factor assumed to be a stationary process,

is factor loadings, and

is the individual specific error terms. For the moment, we assume that idiosyncratic error terms

are independently distributed across both

and

.

The common factor

can be proxied by the cross-sectional mean of

and

following [

8,

27]. To see this, first re-write Equation (1) as follows:

Taking the cross-section average of both sides, we obtain the following equation:

Assuming that

does not vanish, the common factor

can be written as

which suggests that the common factor can be proxied by a linear combination of

and

. Therefore, in order to filter out the effects of the common factor, we run the following modified test regression:

Then, the test of the null hypothesis of the unit root ( in Equation (1) above) is based on ratio of the OLS estimate of in Equation (6).

In Equation (1) and hence in Equation (6), it was assumed that the error terms are not serially correlated. In order to allow for serial correlation in the error terms, we ran the following augmented regression:

and we compute the test statistic from Equation (7) (see [

8]).

Ref. [

28] demonstrated that the CCE estimator provides consistent and asymptotically normal estimates of slope coefficients in panel data models, even with a multifactor error structure. In this section, we aim to explore additional properties by using the CSD test to determine whether the CCE estimator truly remedies the CSD issue. To carry out this, we employ the

test from [

30]. First, we need to verify if this test performs well across different levels of CSD.

2.2. The Behavior or Performance of the Test

In this section, we first conduct a Monte Carlo study to test whether the

test works properly with DGP given in Equation (3). The features of this DGP are described in [

8,

27], where CSD is introduced into the panel data using a factor structure, as shown in Equation (3). First, we compute the

test directly on the DGP to verify if the test detects CSD. In the second stage, we use the same DGP but apply the factor structure to remedy the CSD during the testing process. We expect to observe severe CSD in the first Monte Carlo setup and no CSD in the second. If these expectations hold, the

test can be used to assess the CCE estimator proposed by [

8,

27]. Previous studies [

28] have shown that the CCE estimator effectively remedies CSD and produces unbiased estimates. While our analysis complements theirs, our findings suggest a new direction for developing a more efficient estimator. In the final stage, we propose a new estimator based on these new insights.

The Monte Carlo design used in this study can be summarized as follows: First, we generate data using Equation (3) with factor loadings

ranging from −1.0 to 3.0, as suggested by the authors of [

8,

27], who classify this range as strong CSD. In our study, we compute the

test for each factor loading in this interval at 0.1 increments. These computations are performed for

and

. For each point, we calculate the

test 1000 times to examine the distribution and the minimum and maximum values of the test. For example, with

and

, we generate 40 intervals representing the probability of detecting CSD when imposed or, conversely, detecting no CSD. For

and

values as described, this results in 360 cells (

), which can be displayed in 27 tables for each

and

. To simplify interpretation, we present the results visually through figures. In these figures, we also include the 10% significance interval for the z-test, ranging from −2.0 to 2.0.

We consider the following panel regression model,

for

cross-sectional units and

time periods. The sample estimate of the pair-wise correlation of the residuals is given by

where

is the OLS estimates of

defined as

. Ref. [

30] suggests that the

test statistic can be computed as

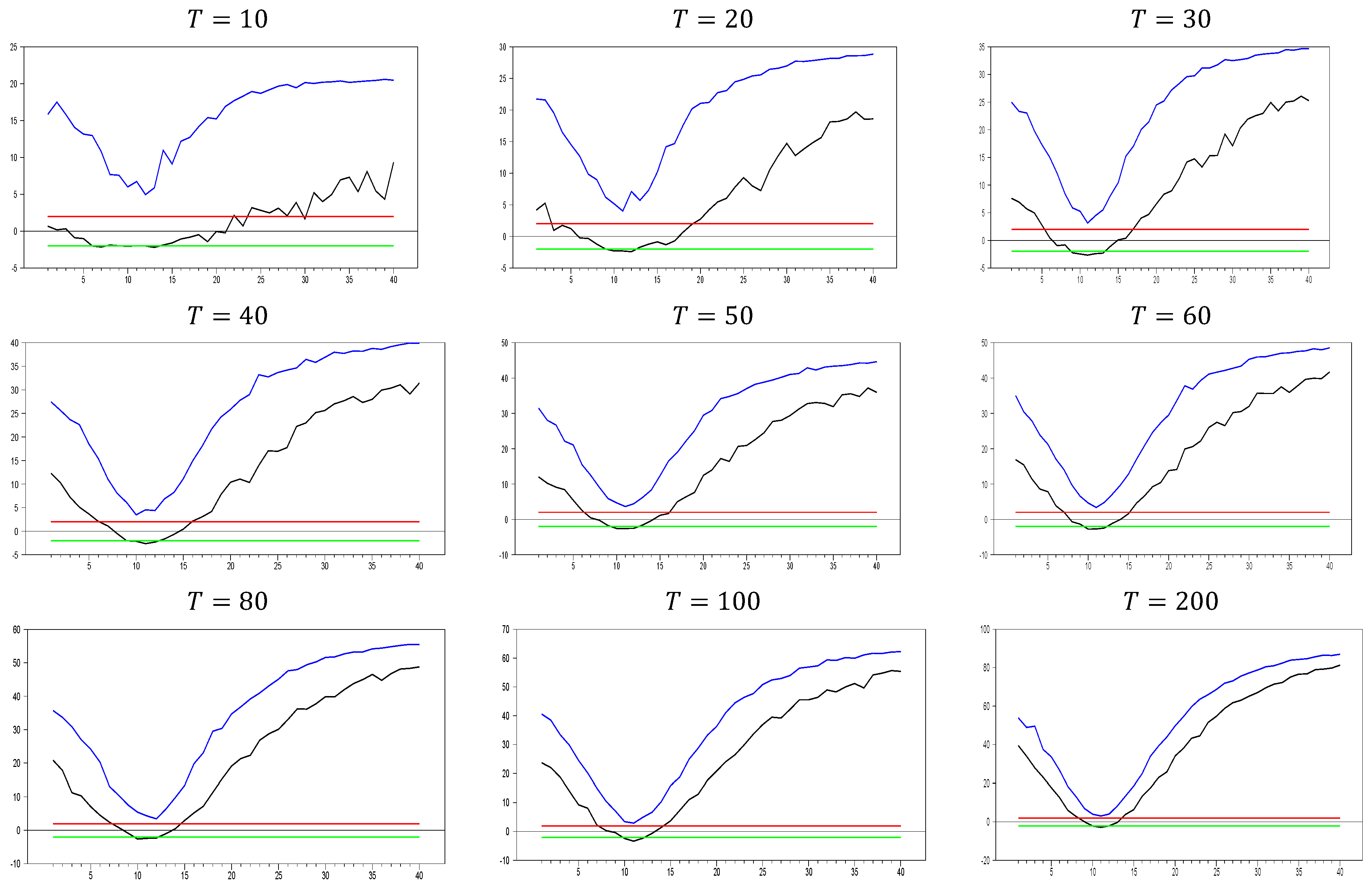

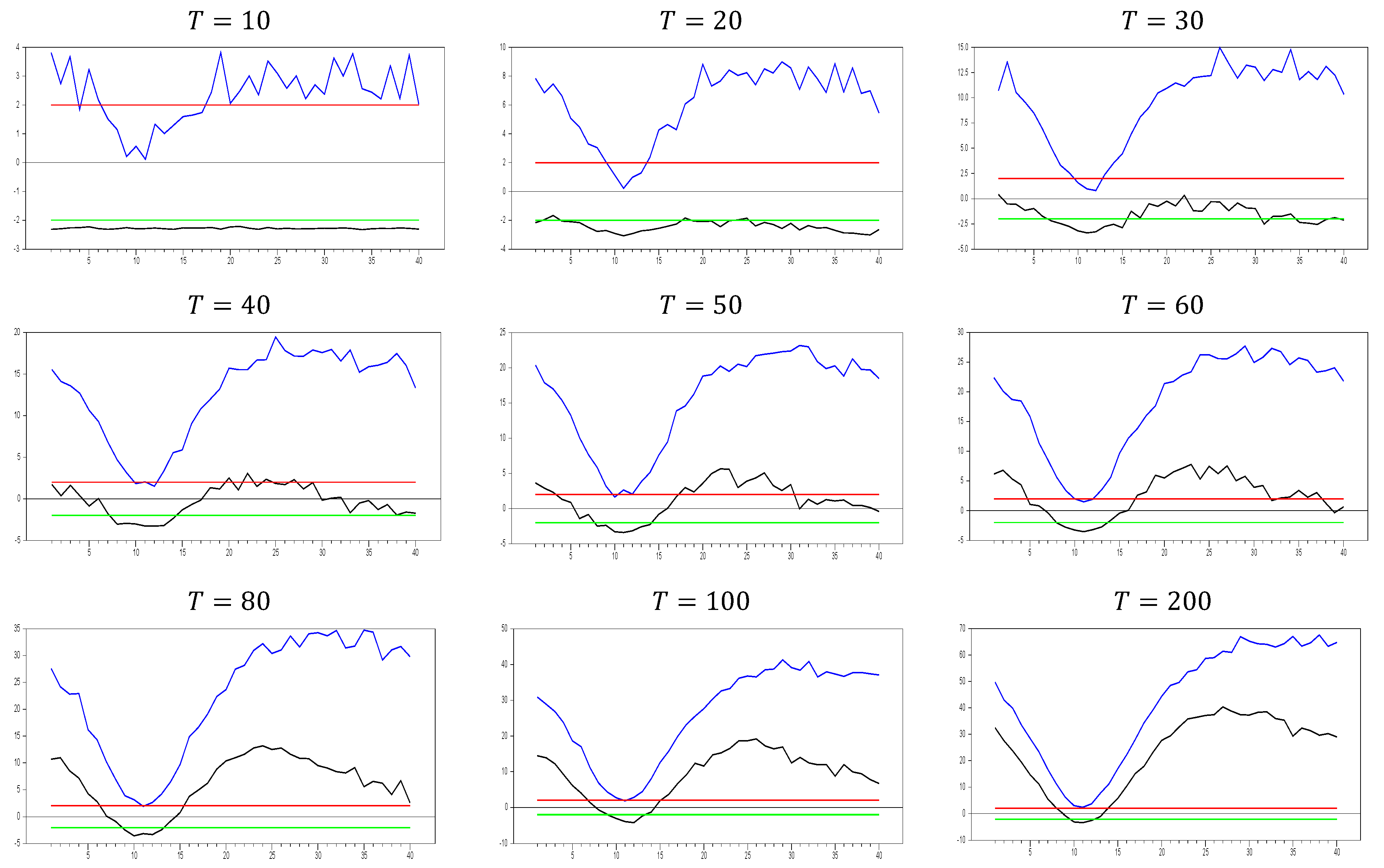

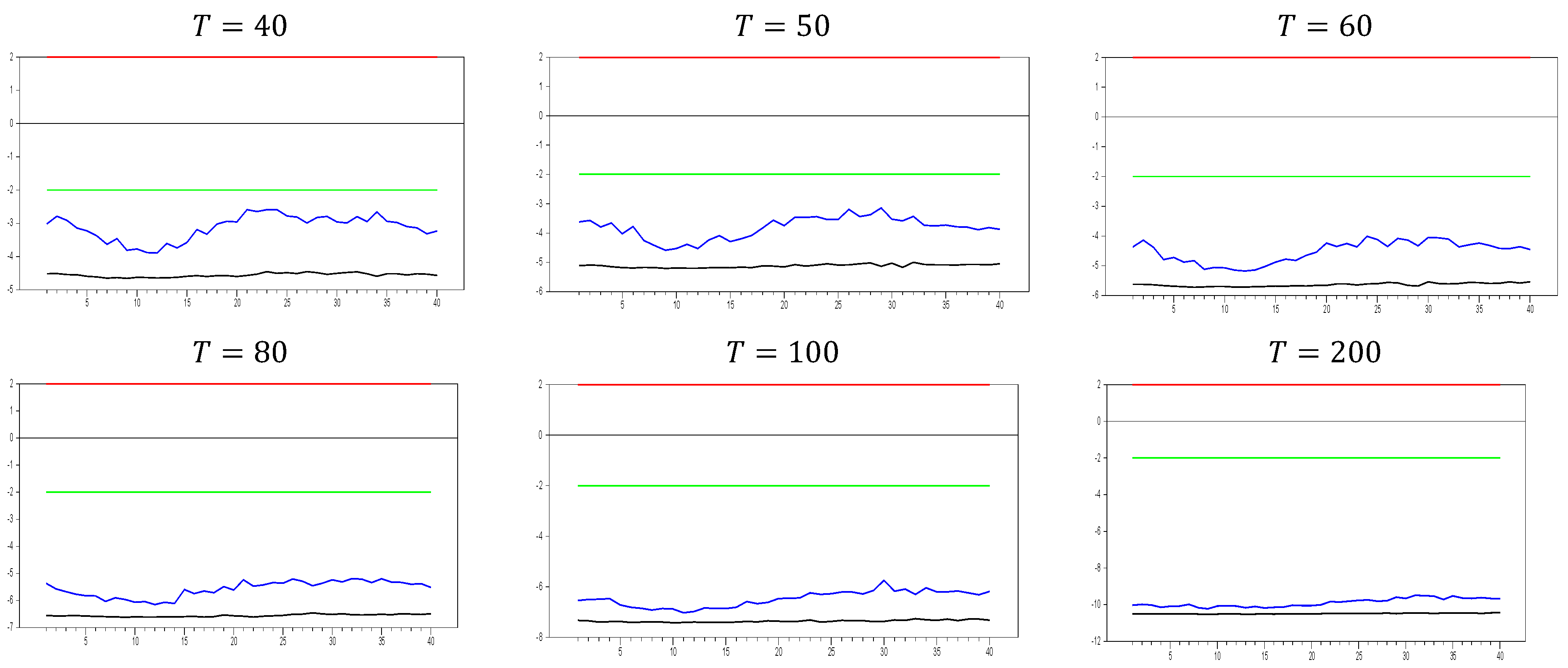

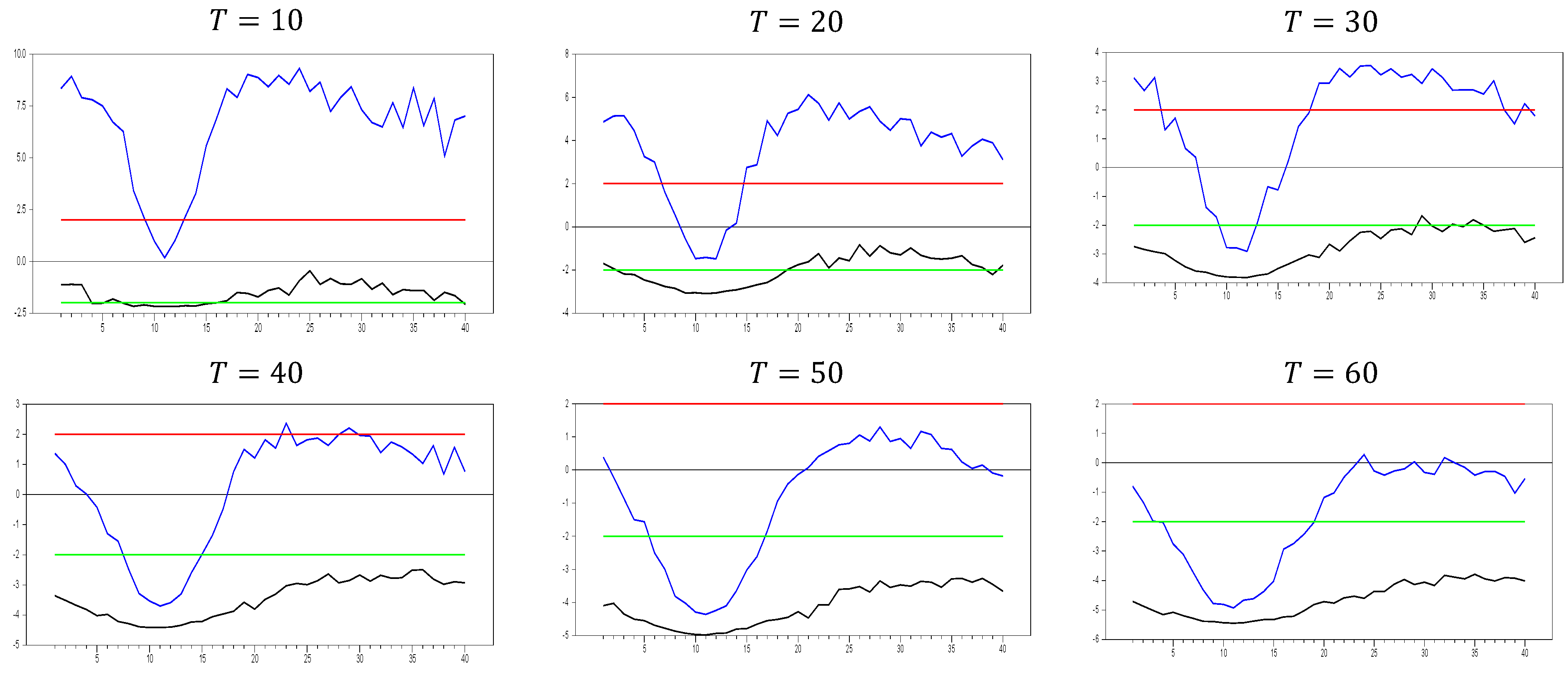

2.2.1. The Behavior of the Without Imposing the CCE Estimator

For the first Monte Carlo study, we use the DGP from Equation (3) without imposing any remedy. The results are shown in

Figure 1,

Figure 2 and

Figure 3.

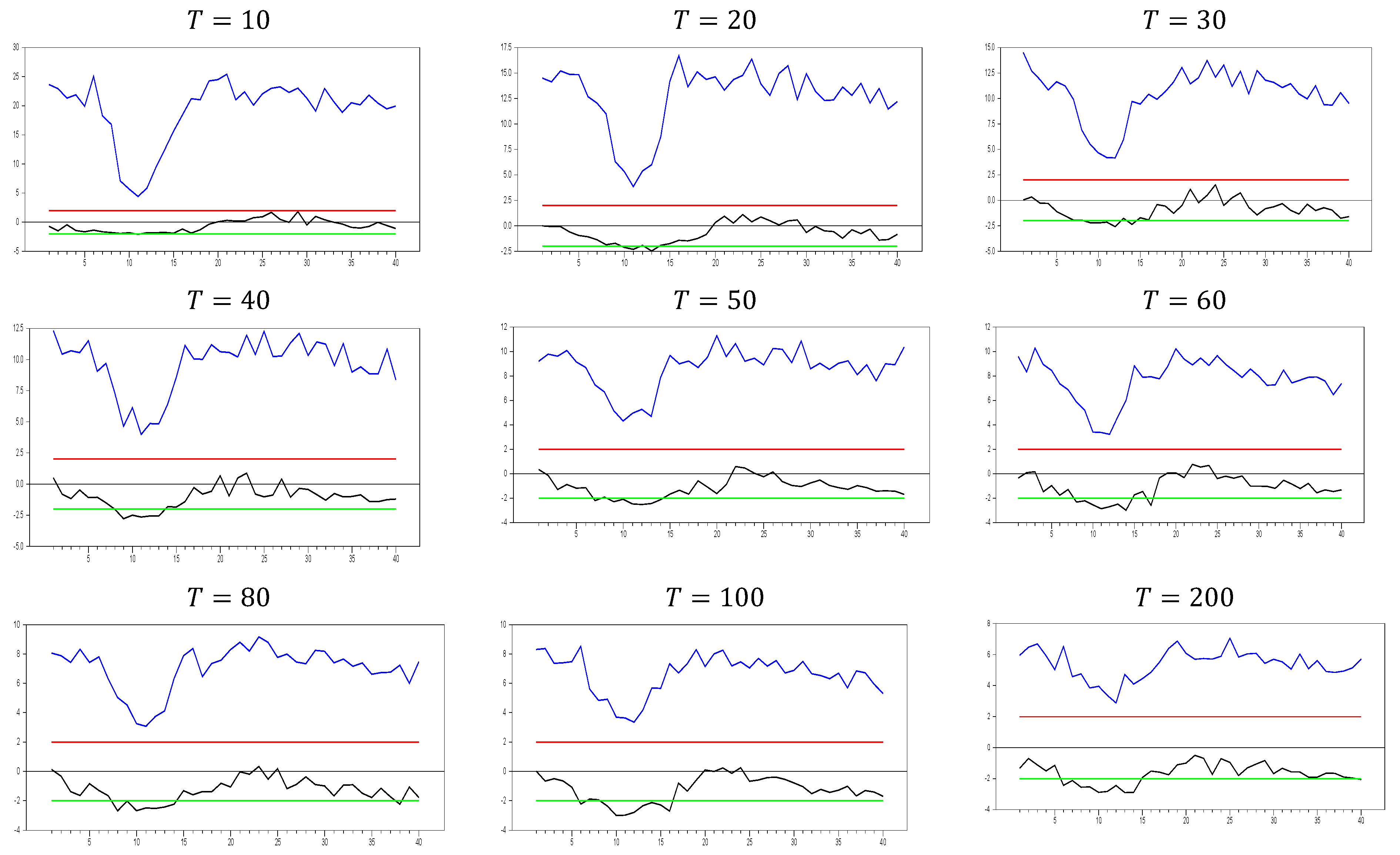

As shown in

Figure 1, the

test effectively captures CSD for

. The test becomes more sensitive as the

dimension increases. This can be observed in the figures, where for

, the maximum

test value approaches 20.0, while for

, it increases to around 50. A similar pattern is seen for the minimum values. As

increases, the initially u-shaped

test results become skewed, with the tangency points of the curve shortening. This indicates that the

test detects CSD for smaller factor loadings as

grows. For

, the range of test statistics is approximately (

0.1, 0.4), indicating almost no CSD, while for

, the range is wider at (−1.0, 2.4). These results suggest that it is not straightforward to categorize the range (0.0, 0.2) as weak CSD, as some effects are still present when

increases. However, our primary goal is to confirm whether the

test is working or not. Based on

Figure 1, we conclude that it works well for small

values.

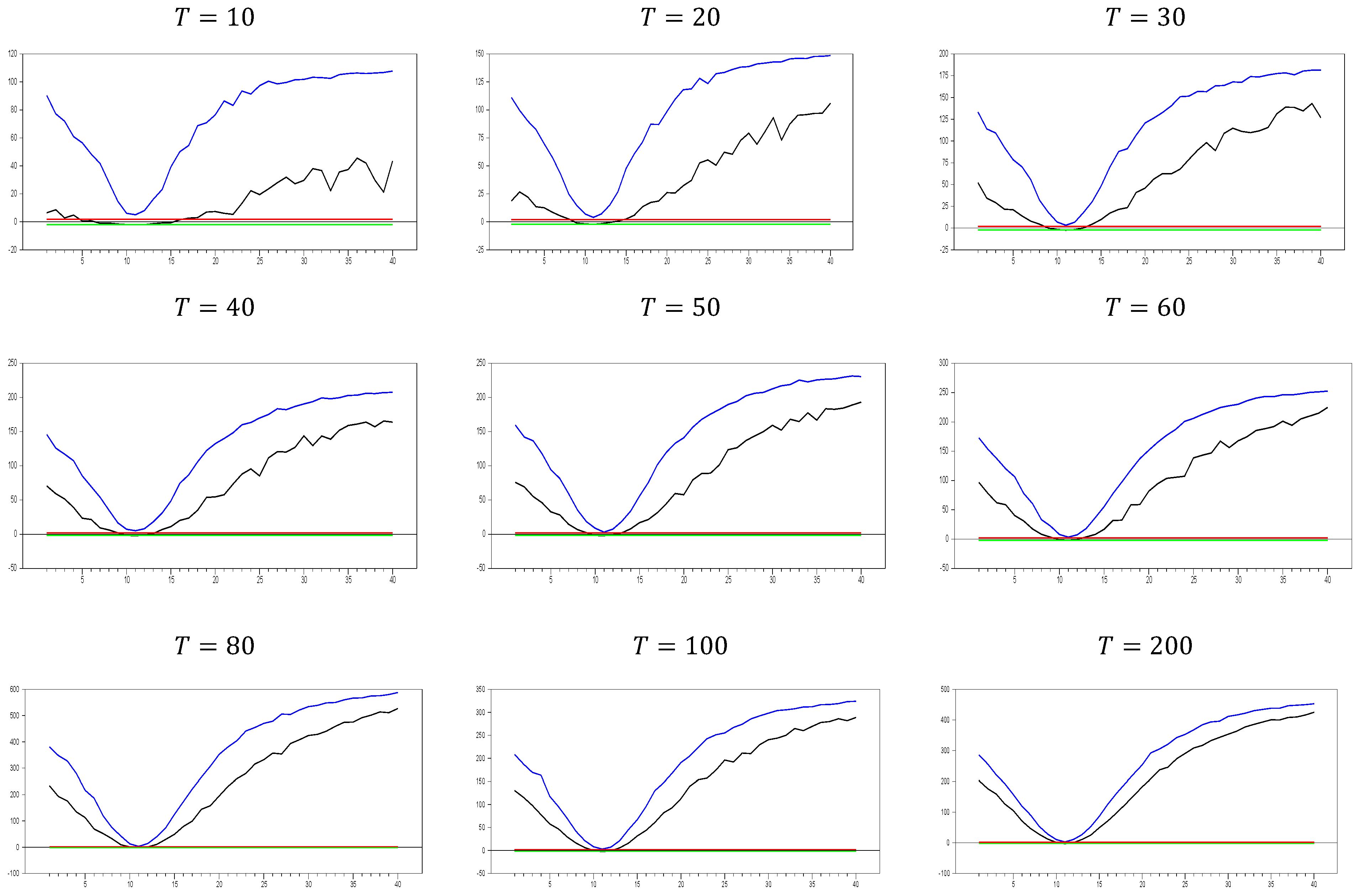

We now move on to test the performance with a larger

value, selecting

, and the corresponding results are given in

Figure 2. As shown in

Figure 2, the pattern observed is consistent with that in

Figure 1. This confirms that increasing the

dimension does not cause any issues with the

test results. Therefore, these simulation results provide evidence of the test’s consistency in small samples. As the

dimension increases, both the maximum and minimum values of the

test also increase. For example, with

and

, the maximum

test value approaches 20.0, but for

and

, this maximum value rises to approximately 100.0. Similarly, for

0 and

, the maximum value is around 50, while for

and

, it increases to 450.0. A similar pattern is observed for the minimum values. Furthermore, as the

dimension increases, the tangency points of the u-shaped figure become shorter, indicating that the

test detects CSD for smaller factor loadings.

For

and

, the test produces a range of (−0.1, 0.4), indicating almost no CSD, while for

and

, the range narrows to (0.0, 0.1). Once again, this confirms that it is difficult to classify the range (0.0, 0.2) as weak CSD for all values of

and

, as claimed by [

8,

27]. However, for large values of

and

, factor loadings in the range

can indeed be categorized as weak CSD.

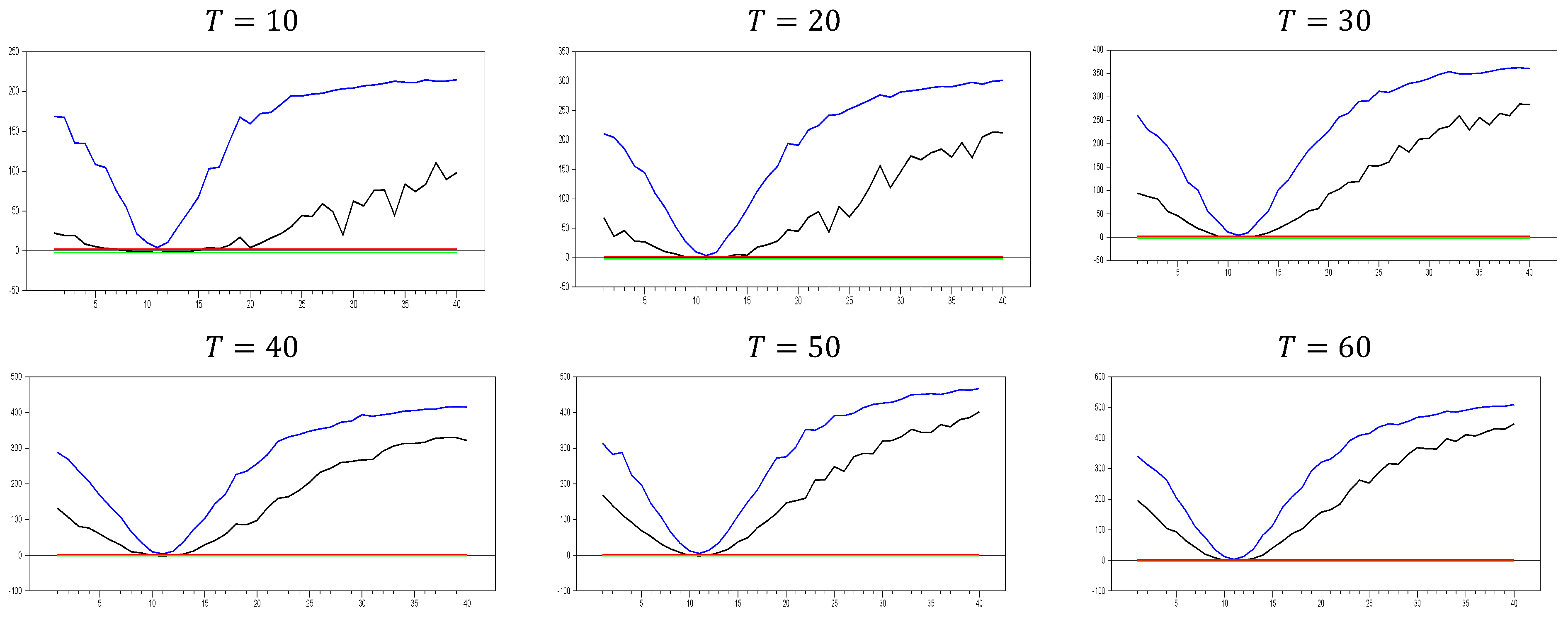

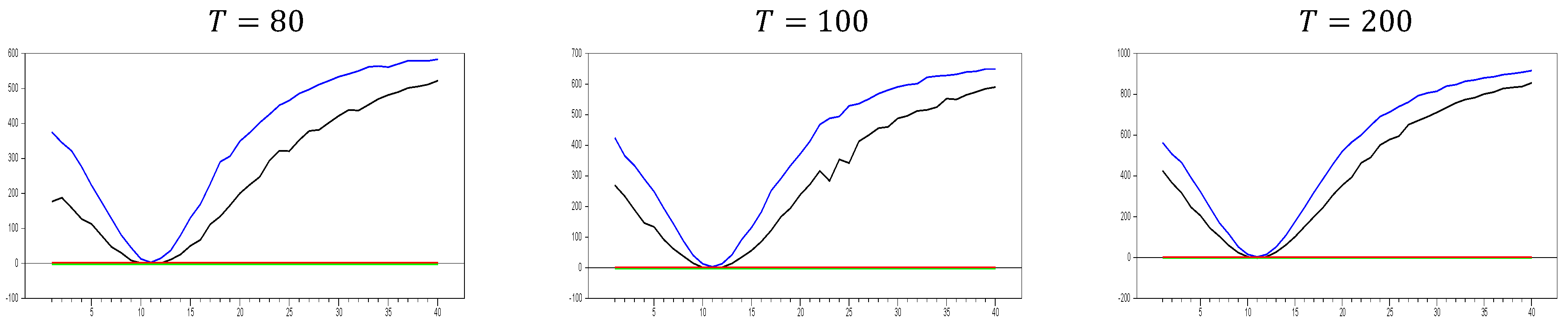

Up until here in

Figure 2 and

Figure 3, we have deal with

and

with

. In order to see the large sample features, we performed simulations for

and

.

Figure 4 shows the behavior of the

test in large samples.

Figure 4 confirms the expected pattern of

Figure 1,

Figure 2 and

Figure 3. All the explanations for the comparison of

Figure 1,

Figure 2 and

Figure 3 are valid. Hence, these simulation results provide evidence of the consistency of the test for catching CSD in small samples.

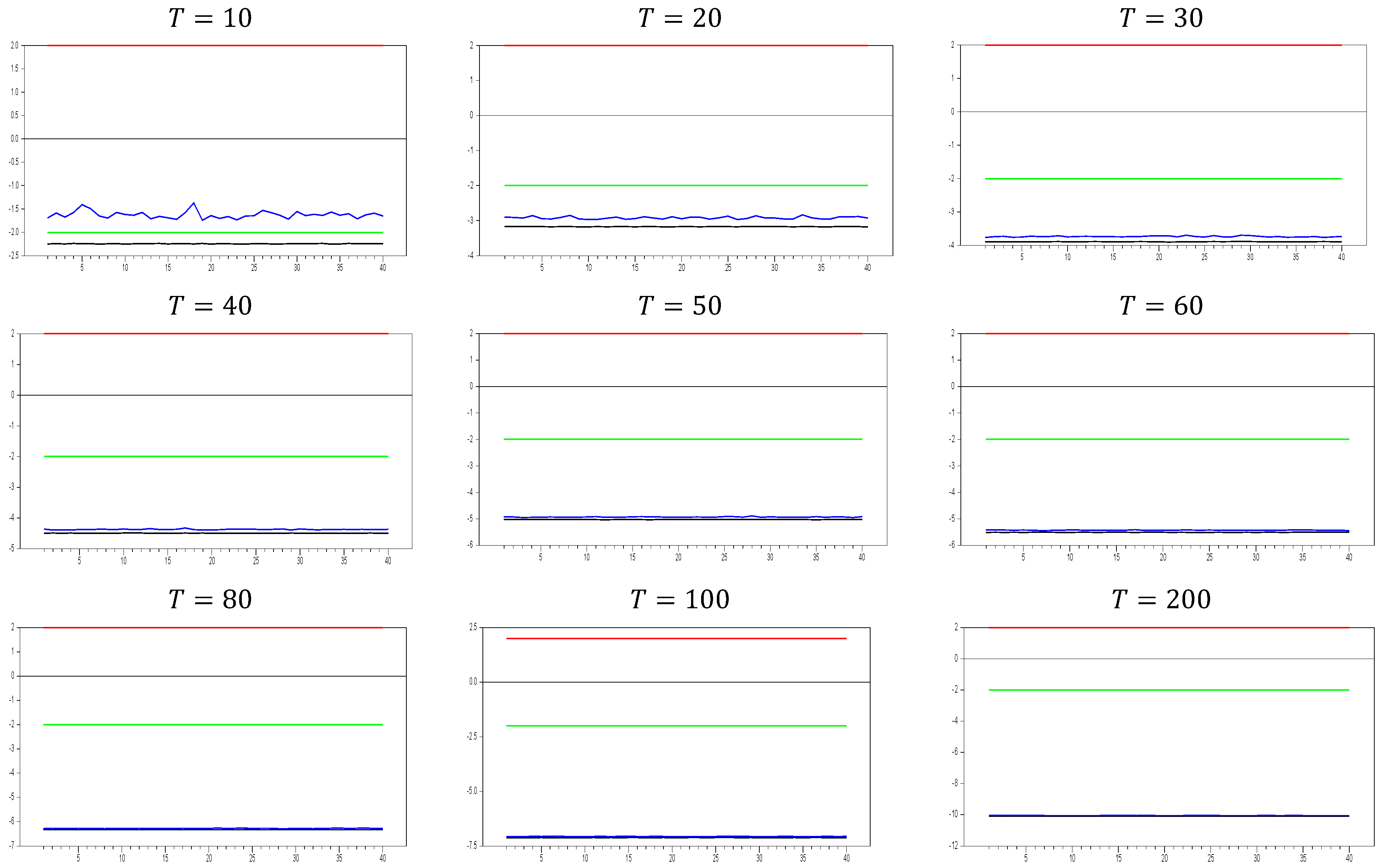

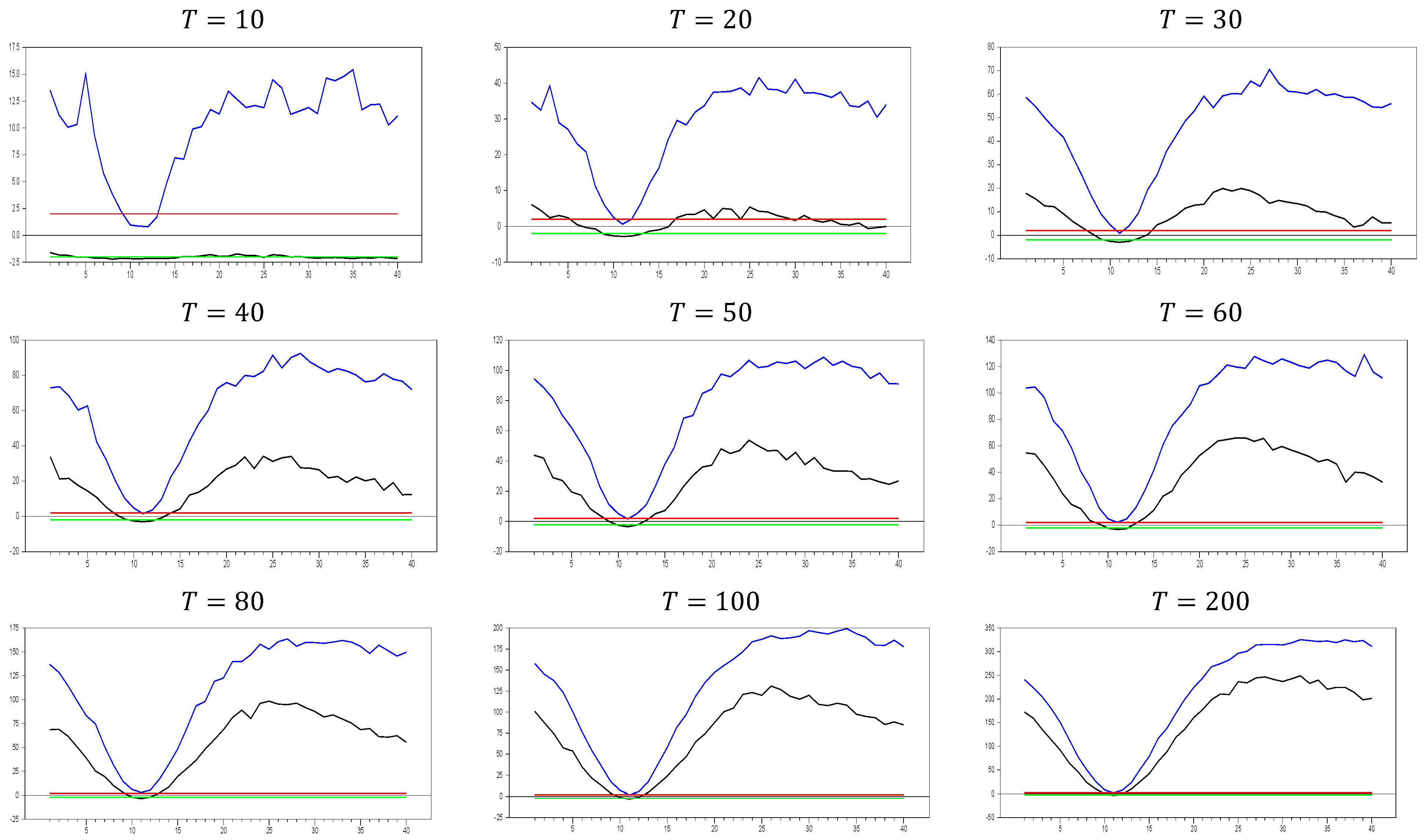

2.2.2. The Behavior of the with Imposing the Factor Variable

We now investigate the consistency of the

test by imposing a factor variable into the testing process, which induces CSD in the DGP. If the

test is working correctly, the inclusion of the factor variable should eliminate the CSD, and the

test should indicate no remaining CSD. The resulting

values will fall between the z-test thresholds of −2.0 and 2.0, as shown in the graphics. The first results are given in

Figure 5 for

.

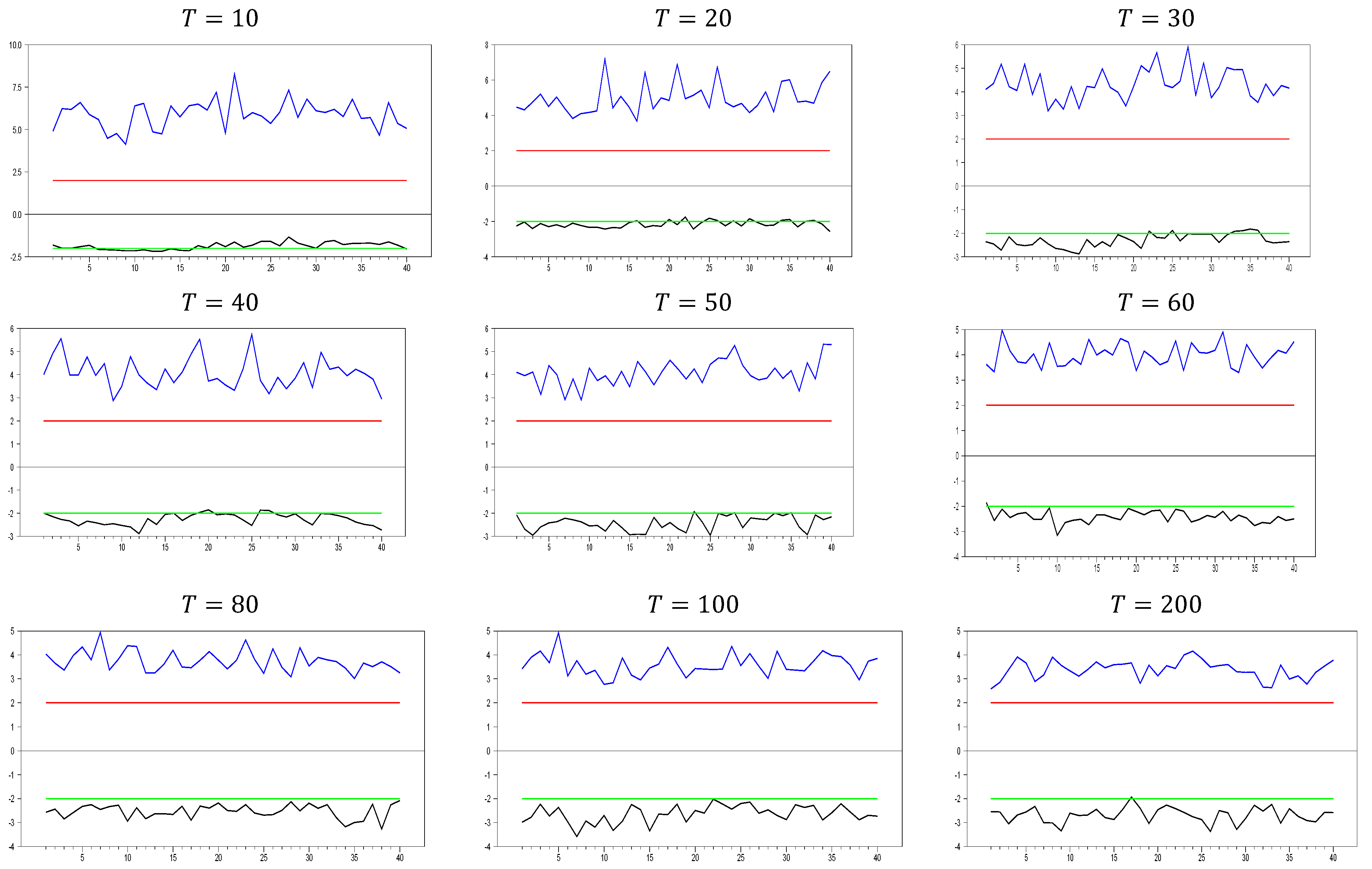

From

Figure 5, we observe that the calculated minimum and maximum values fall within the 10% significance level of the z-test, confirming that the

test successfully captures the CSD imposed in the DGP of Equation (3). This result meets our expectations and provides a benchmark for evaluating proxies used to remedy CSD. A valid proxy should follow this pattern for small

and

dimensions. If the test shows no CSD for any factor loading, the proxy can be considered an efficient factor variable. In

Figure 5, we can see how increasing the

dimension affects the results. The test statistics range between approximately −2.0 and 7.0 for

, and between −3.0 and 4.0 for

. As

increases, the band of calculated test statistics narrows and shifts downward, with the maximum values decreasing more significantly than the minimum values. This suggests that while the original factor effectively remedies CSD, it still has some limitations in handling very small probabilities. To better understand the

test’s behavior, it would be useful to analyze the results with a larger

dimension.

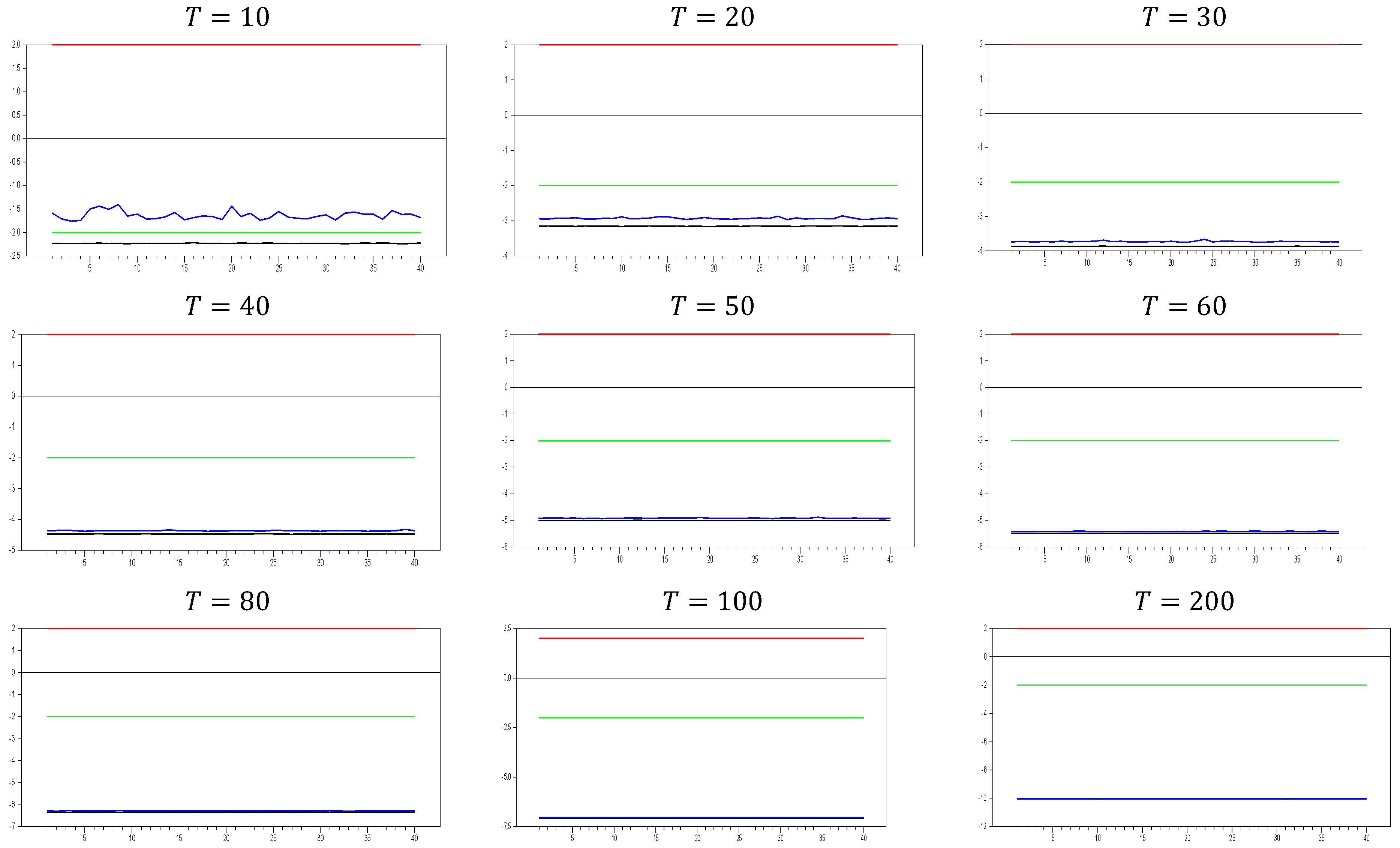

From

Figure 6, we can observe that for

and

, the calculated

test statistics range between approximately −1.5 and 15.0, compared to a range of −2.0 to 7.0 for

and

. As

increases, the band of the

test statistics shifts upward and widens, with the maximum values increasing more than the minimum values. When

and

, the band narrows to a range of −2.0 to 4.0, whereas for

and

, the range is approximately −3.0 to 4.0. This narrowing of the band as both

and

increase suggests that the original factor more effectively remedies CSD in the DGP. These simulations highlight the power of the

test, which proves to be highly effective in detecting CSD based on the test results. The second set of simulations further demonstrates the effectiveness of the method in remedying CSD, building on the first simulation’s results. Therefore, we can conclude that both simulations confirm the power of the

test and the method used to remedy CSD.

To explore this further, we now examine the impact of increasing the

dimension in

Figure 7. In

Figure 7, a new phenomenon emerges. When the factor loadings are low, the original factor remedies CSD more effectively than at higher factor loadings. This behavior may also appear in approximation methods like the CCE estimator.

Up until here in

Figure 5,

Figure 6 and

Figure 7, we have deal with

,

and

with

. To explore the behavior in larger samples, we conducted a simulation with

and

.

Figure 8 illustrates how the

test performs in remedying CSD using the original factor in these large-sample settings.

We now have solid benchmark simulations to assess whether the proxy variables are effective. The results from the first simulation help us evaluate whether the proxy can remedy part of CSD. The second set of simulations further demonstrates the efficiency of the proposed method in addressing CSD.

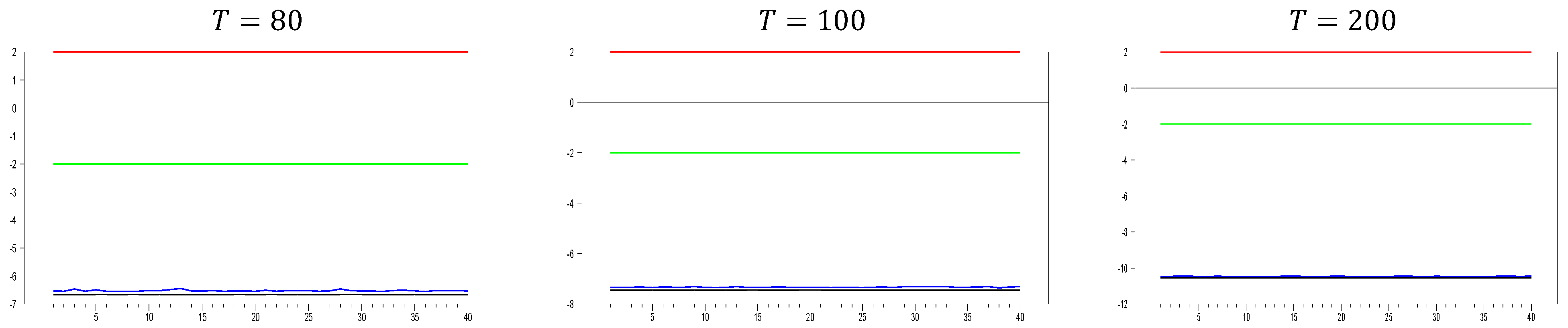

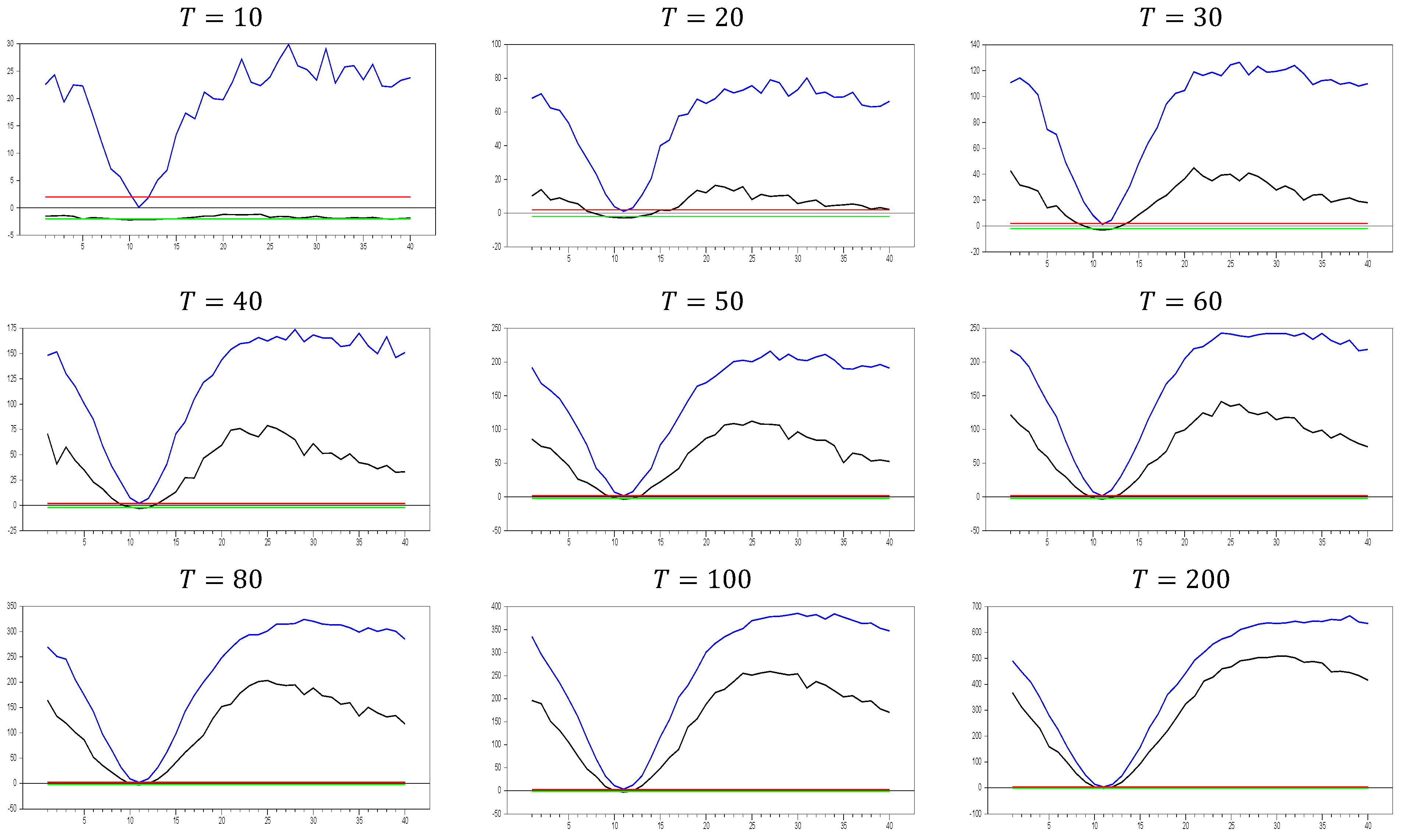

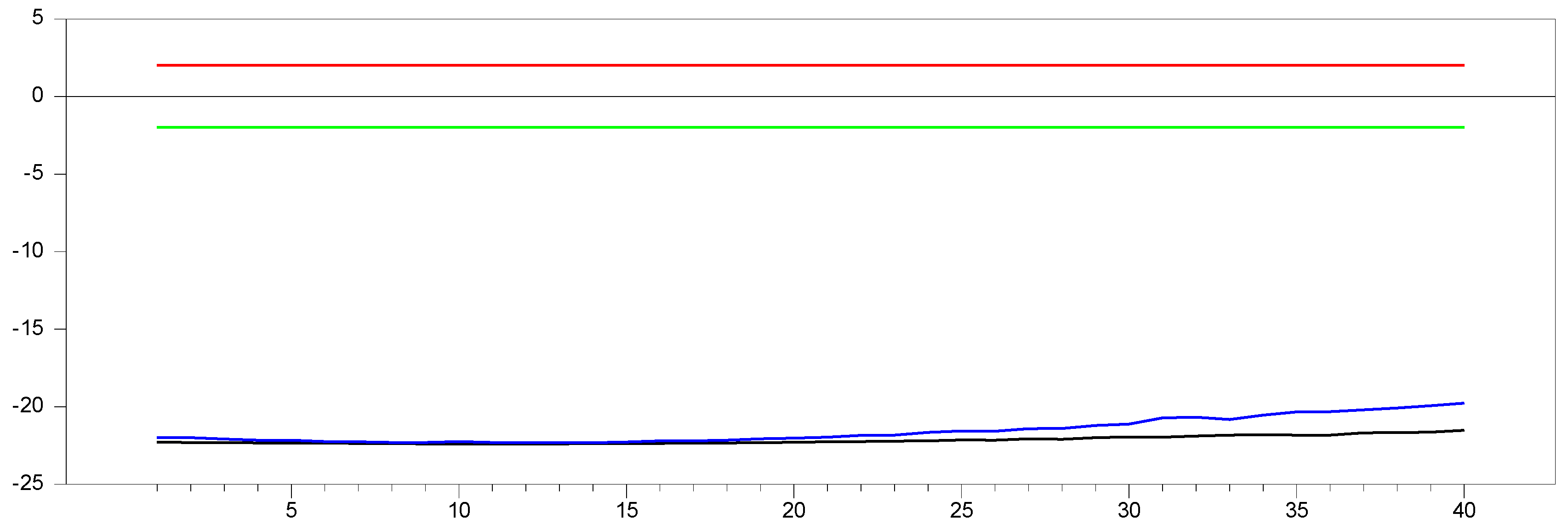

2.2.3. The Behavior of the with Imposing the CCE Estimator

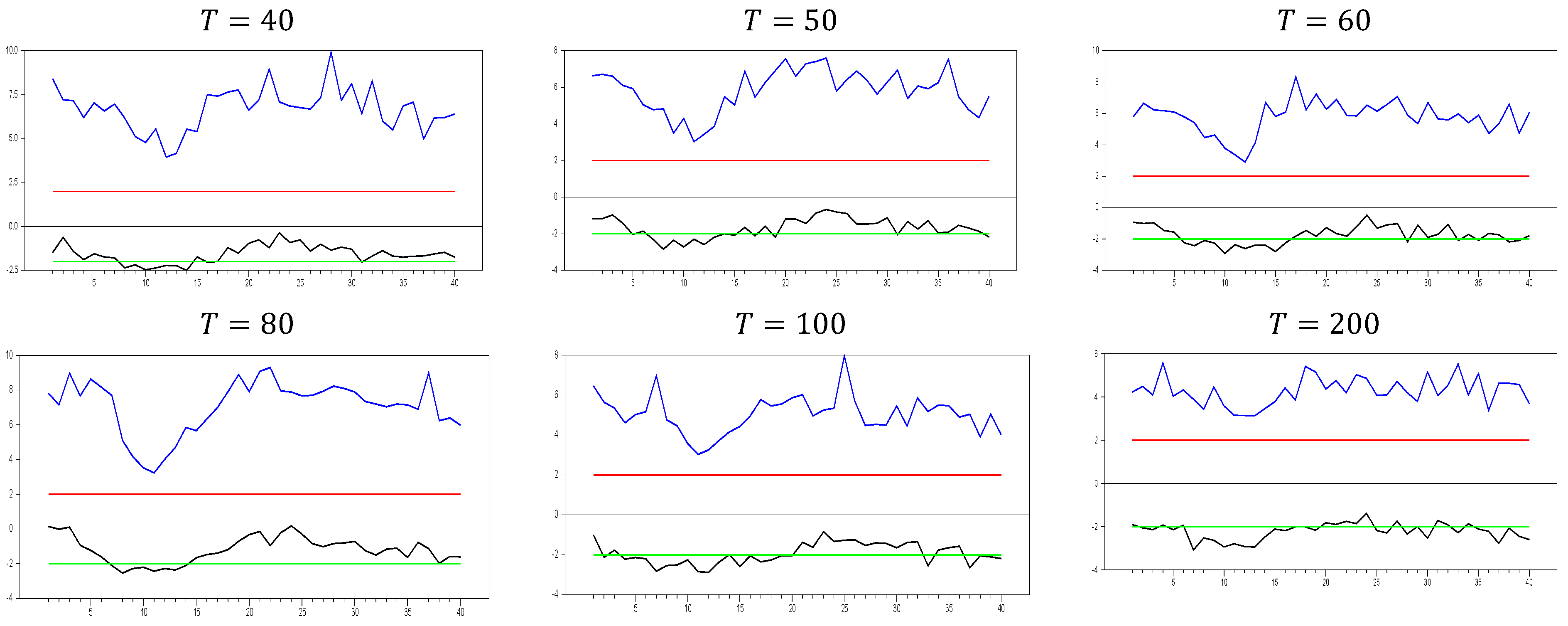

In light of these arguments, we can assess performances of the CCE estimator proposed by [

8,

27]. In

Figure 9, we observe some unexpected results for what would typically be considered a good proxy. However, only for

and

do we see the expected results for a proxy that remedies CSD, as indicated by simulations 1 and 2. The computed

values range between approximately −2.4 and −1.5, demonstrating that the CCE estimator effectively remedies CSD. Additionally, for

, the computed values quickly move out of the CSD rejection region, and the band between the minimum and maximum

values narrows as the

dimension increases. By

, the minimum and maximum values of the

test are approximately

10.25 and −10.15, respectively. Now, we can further explore the effects of increasing the

dimension.

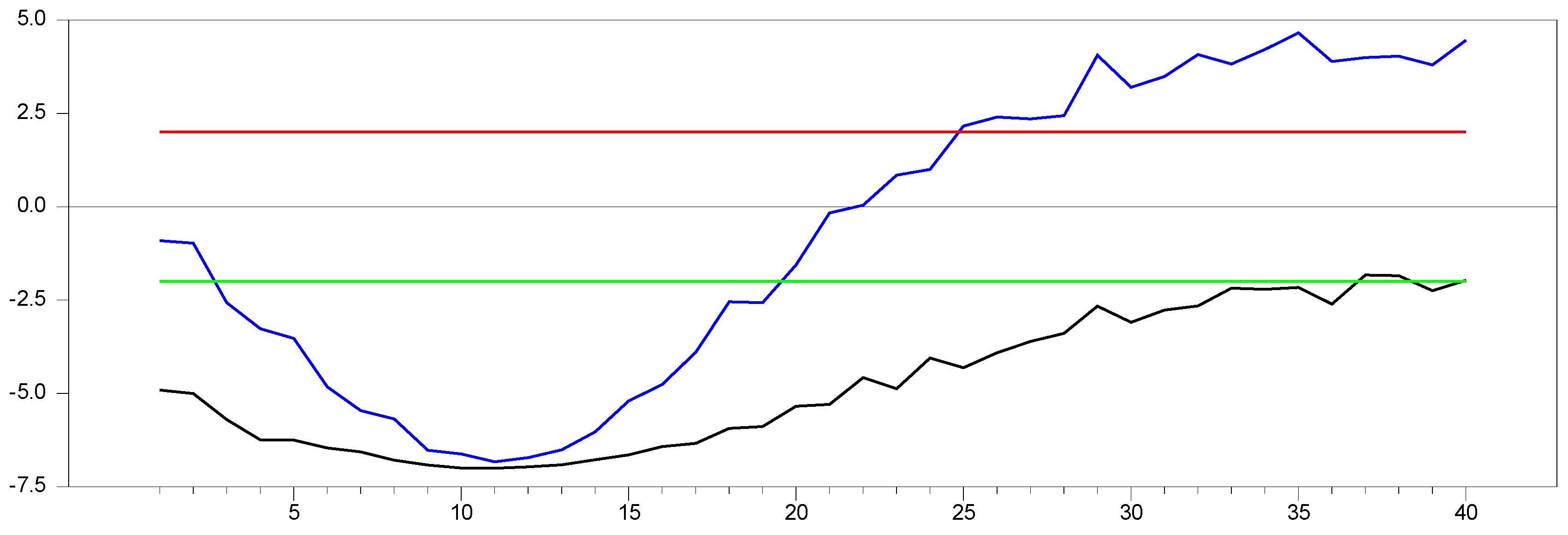

In

Figure 10, we observe that only for

and

we obtain the expected results for a good proxy that remedies CSD, as indicated by simulations 1 and 2. The computed

values range between approximately −2.2 and −1.4, confirming that the CCE estimator effectively remedies CSD. However, as the

dimension increases, the band between the minimum and maximum

values narrows. For

and

, the minimum and maximum

values for

are approximately

and

, respectively. These results show that increasing

reduces the

test values and narrows the band, while increasing

further narrows the range. The key finding from these simulations, in line with simulations 1 and 2, is that the CCE estimator remedies CSD most effectively when

is small. However, as

increases, the proxies

and

correct the factor’s effect in the residual term but introduce additional CSD in the opposite direction. These simulations focus solely on CSD, so we cannot yet determine how they impact bias reduction in the

parameter in Equation (3). Nonetheless, there remains scope for developing a better estimator for addressing CSD in panel unit root testing, in line with the approaches of [

8,

27]. Before further investigating this, it is beneficial to examine the effects of increasing both

and

dimensions.

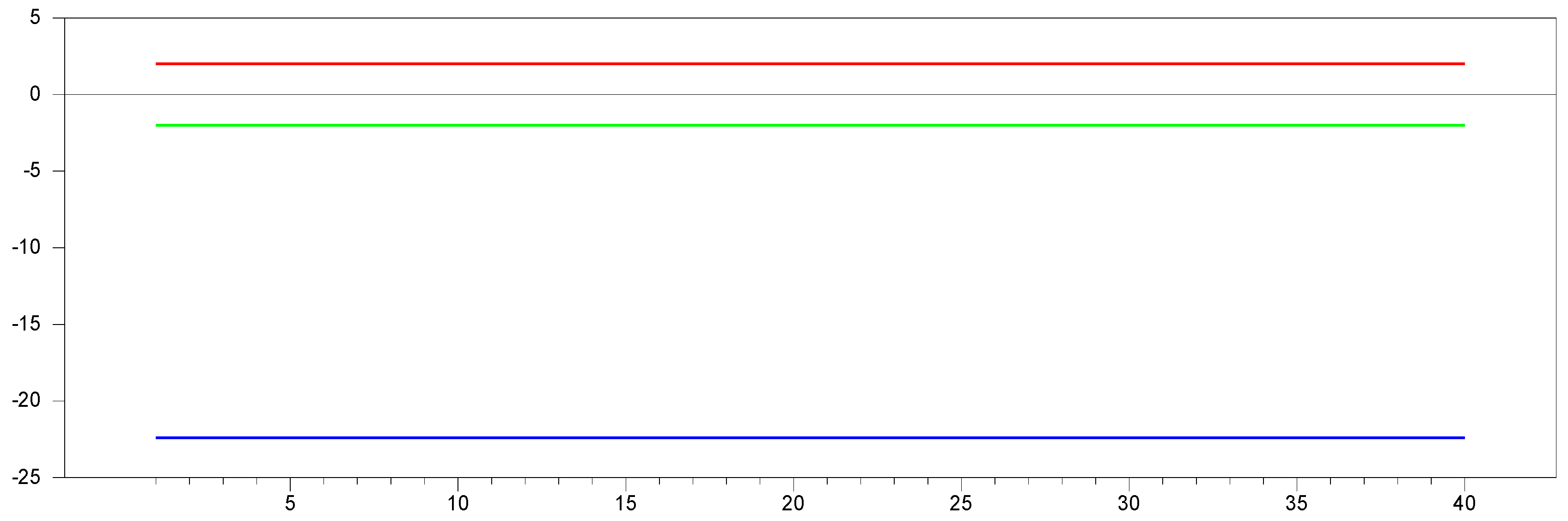

In

Figure 11, we observe that the results are similar to those in

Figure 9 and

Figure 10. The only difference is that for

and

, no band appears, and the minimum and maximum values are fixed at 10.0. This indicates that the bands in

Figure 11 are narrower than those in

Figure 9 and

Figure 10. To further explore the behavior in large samples, we conducted a simulation for

and

.

Figure 12 illustrates how the

test performs when remedying CSD using the CCE estimator proposed by [

27] in large samples. In

Figure 12, we observe that as the

dimension increases, the

test values reach 22.0. Additionally, increasing both the

and

dimensions together eliminate the band between the minimum and maximum values of the

test.

2.3. The Refinement of the Common Correlated Estimator by Using the Test Results

In light of these findings, we now can investigate for a more efficient estimator for remedying CSD in small samples.

Proposition 1. and

proxies can be expressed by

.

Proof. with some algebra can show that

where

and

is taken:

Now, we can re-write Equation (12),

Showing that

we prove that

□

Using this variable,

, may provide a more effective proxy factor to address cross-sectional dependency compared to [

27]’s CCE estimator. In the CCE estimator, we use two variables to proxy the factor; now, we have only one parameter to estimate, which may increase the efficiency.

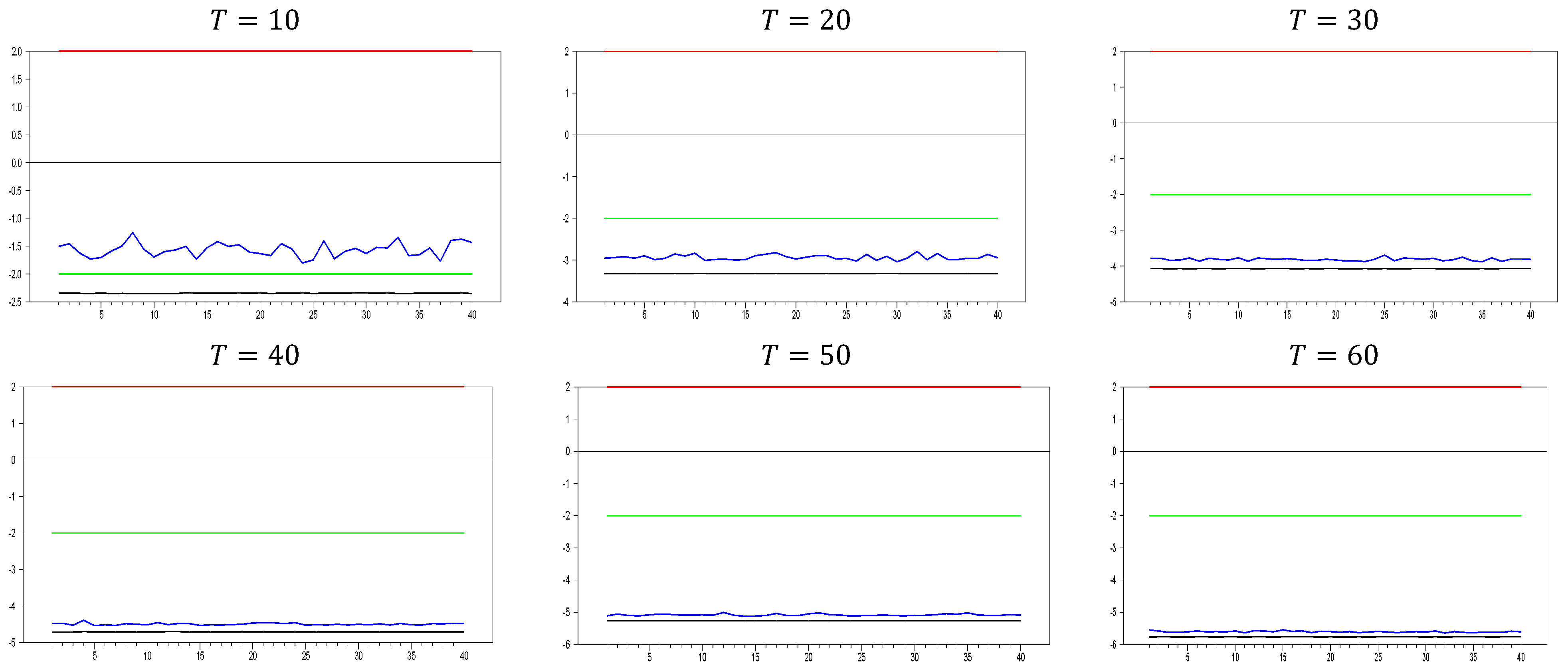

Figure 13 clearly demonstrates that, for small

values, the newly proposed estimator or proxy closely mimics the original factor variable. Specifically, for

and

, the new proxy closely replicates the original factor variable based on the

test results shown in

Figure 5. However, as the

dimension increases, both the minimum and maximum

test values rise, and the band widens. By

, the

test results for the proxy estimator indicate that it no longer provides an effective remedy. To further examine the effect of increasing the

dimension, we performed a simulation for

. The results are shown in

Figure 14.

Figure 14 shows that the effectiveness of the newly proposed estimator in remedying CSD diminishes as the

dimension increases. Thus, we can conclude that this proxy is only effective for very small

dimensions.

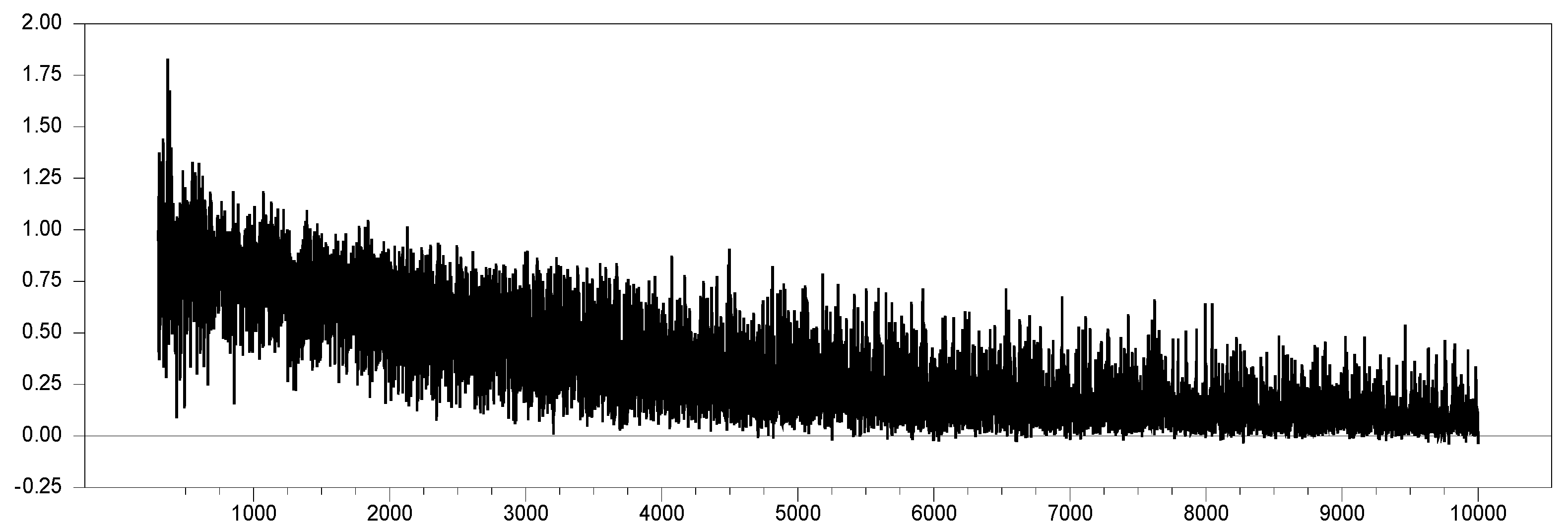

To further examine the impact of increasing the

dimension, we conducted a simulation for

. The results are presented in

Figure 15. Fortunately, as seen in

Figure 15, the

test results for

and

show that the test values converge to 1000.0, while the new estimator’s

test values converge to 600.0. This indicates that the new estimator remedies part of the CSD, but a significant portion of the induced CSD still remains, leading to biased estimates. Additionally, the

test values start to decrease around a factor loading of

, opposite to the trend in

Figure 15. Therefore, it may be useful to examine the behavior of the

test for higher factor loadings.

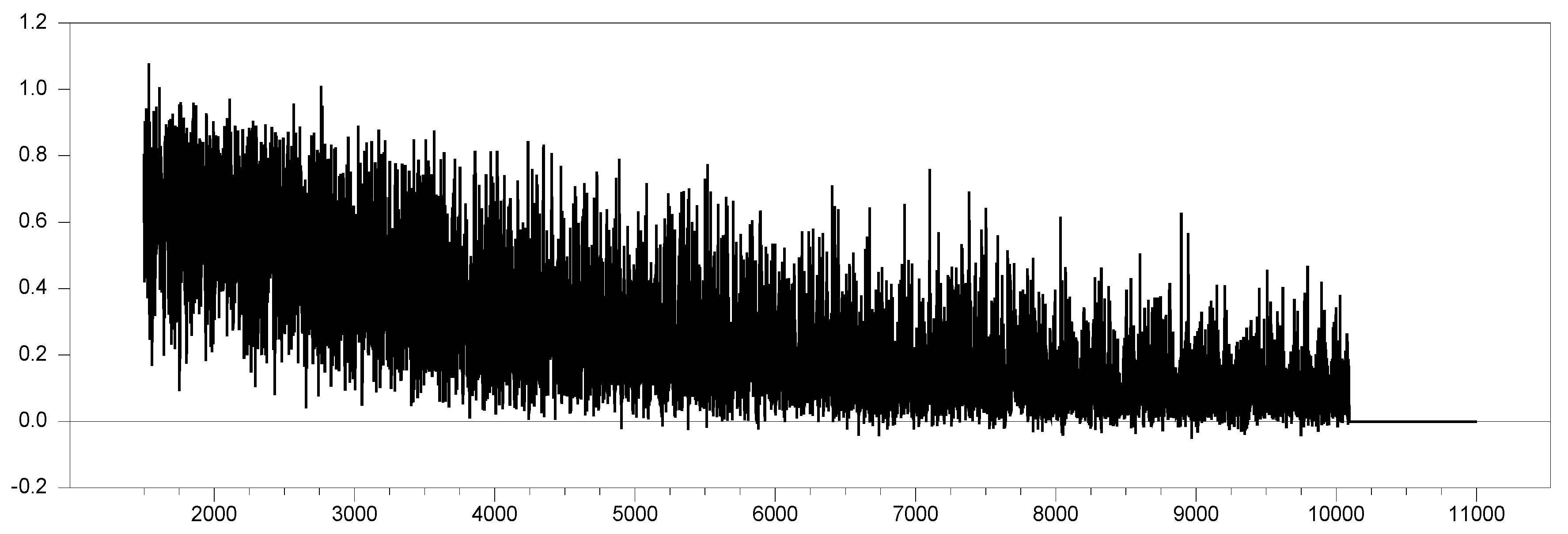

Figure 16 presents the simulation results for

and

with factor loadings ranging from

in 0.1 increments. As the factor loadings increase, the new proxy

adjusts within the range of

. To better understand the behavior without any remedy applied, we simulated the same values, as shown in

Figure 17 below.

Comparing

Figure 16 and

Figure 17, we can observe that the

proxy remedies CSD across all factor loadings and converges to the results obtained by the original factor variable. To further examine the parameter estimates of both the original factor and the

variable, we performed simulations for

and

within the factor loading range

. The simulated values are shown in

Figure 18 below (the simulations were performed by the 50-entity 100 factor loading interval for 10 trials; hence, the simulated values are 50,000).

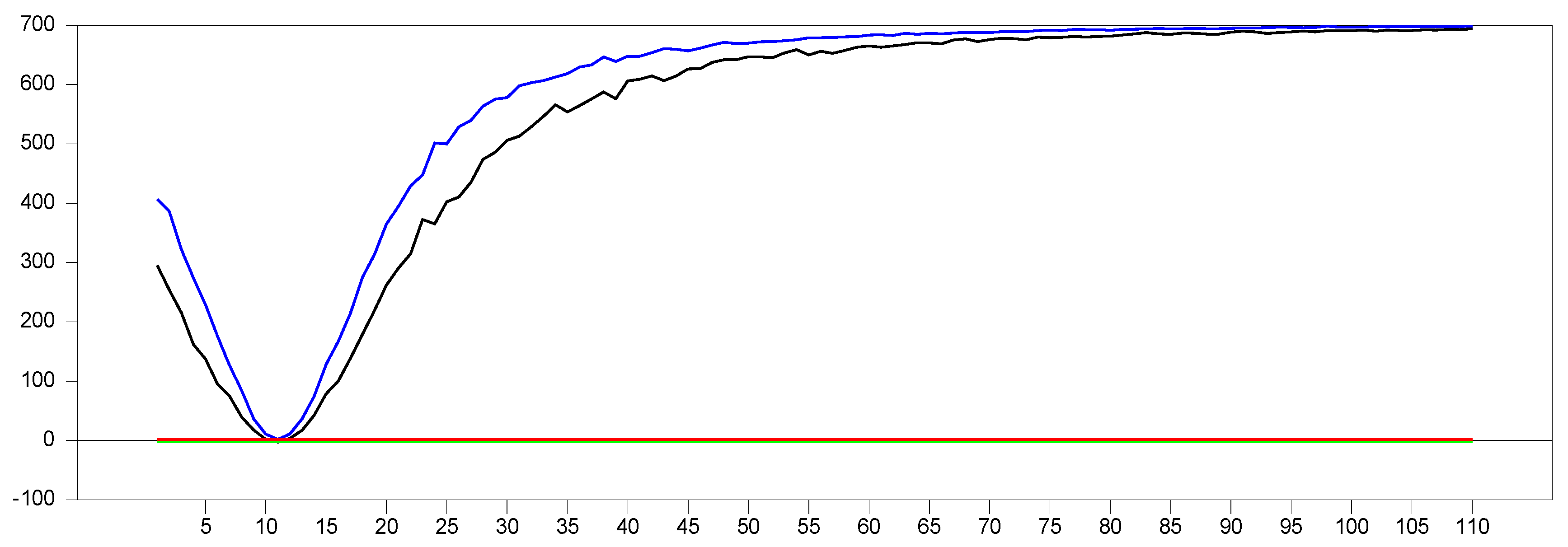

Each 10,000-point interval corresponds to a factor loading of

. After

, the parameters become equal, marking the turning point in

Figure 17, where the estimated parameter values for the original factor variable and the proxy converge, effectively remedying the CSD. The same pattern is observed in the CCE estimation. We subtracted the parameter value of

from the original factor’s parameter value within the same factor loading range.

Figure 19 below summarizes the results of the Monte Carlo study.

These two simulation results shed light on an issue. From

Figure 19, we can see that the difference between the parameters ranges from −0.04 to 0.06 until the factor loading reaches

, after which the difference becomes nearly zero, and it finally reaches 0.0 at

, as shown in

Figure 18. The difference obtained using the

parameter in

Figure 18 is quite large compared to the CCE estimator for the factor loading range

, where the CCE estimator consistently performs better. However, after

, the performance of the

proxy improves. Moreover, based on

Figure 13,

Figure 14 and

Figure 15, we observe that the

proxy performs better in small samples with

. These results suggest that there is a transformation that remedies CSD more effectively than the CCE estimator for small samples, particularly for factor loadings in the range

. However, we also recognize that while

or

is necessary for remedying CSD, they are not sufficient without incorporating

. Using

and

(as in the CCE estimator) together remedies CSD across all factor loadings but introduces a negative significant

test result, indicating that some CSD remains in the estimation process in panel unit root testing. Based on the simulation results from the original factor variable, we identified the behavior of an effective proxy with respect to the

test. Any proxy that meets these criteria can be used as an efficient proxy for factor variables.

In

Figure 20, we demonstrate that as the factor loadings increase in 0.1 increments, [

27]’s CCE estimator, denoted as

, and our proposed estimator,

, become equal, meaning

. Starting from a factor loading of 0.0 and increasing to 10.0, we find that at a factor loading of 1.0,

and

are approximately equal. At this point, the

test shows very low dependence when using our proposed estimator.

Based on the arguments and simulations presented, we propose a new estimator that may prove to be more efficient in small sample sizes. Our newly proposed method is outlined as follows:

Step 1. Run the below regression:

Step 2. Estimate the

and

from Equation (20), and compute the new variable:

Step 3. Use this new variable as a dependent variable and obtain the panel unit root test:

In the first step, we remove the CSD effect from residual term

with [

27]’s CCE method. Now, we are left with more CS independent data. However, still, some CSD prevails as we showed in the above simulations. In the second step, we impose some more CSD into the dependent variable by adding the

variable into the filtered dependent variable. And in the final stage, we use

as a proxy, which is indirectly equal to

. Therefore, we use [

8]’s method and Proposition 1 together. Our simulation results are given in

Figure 21,

Figure 22 and

Figure 23.

The newly proposed estimator behaves similarly to the CCE estimator for . All characteristics, such as the decrease in test values as the dimension increases and the narrowing of the band, follow the same pattern. However, while the lower bound of the test aligns in both methods, the upper bound converges more slowly than in the CCE estimator. This slower convergence of the upper bound makes the new estimator perform better than the CCE estimator in terms of the test.

In the second step, we increase the

dimension again to assess its impact. The results of these simulations are shown in

Figure 22 below. The new proxy method exhibits very similar behavior to the original factor variable for

, further supporting its effectiveness as a good proxy. In particular, for small

dimensions (

to

), the method performs as well as the original factor. However, for low levels of CSD, such as

, this method does not remedy CSD, which can be seen as a favorable characteristic. Similarly to the CCE estimator, the

test shows a negative sign, indicating that the method introduces some CSD. Additionally, as

increases, the upper and lower bounds of the computed values converge to those of the CCE estimator. As

grows, the

test results follow the same trend as the CCE estimator. For instance, with

and

0, the lower bound of the

test reaches 10.0, while the upper bound also becomes closer to the CCE estimator. This convergence is a positive attribute for deriving the asymptotic properties of the new estimator, showing that as

and

approach infinity, the new test aligns with the same asymptotic properties. The following simulation results are obtained for

.

From

Figure 23, we can clearly observe that for

and

, the newly proposed method closely approximates the original factor variable. These simulation results indicate that our proposed method performs similarly to the original factor as

increases while

is fixed. Additionally, we conducted simulations for two scenarios: one where both

and

approach infinity, and another where

is fixed and

is large.

Figure 24 shows that as

and

approach infinity, the new method converges toward the CCE method in remedying CSD.

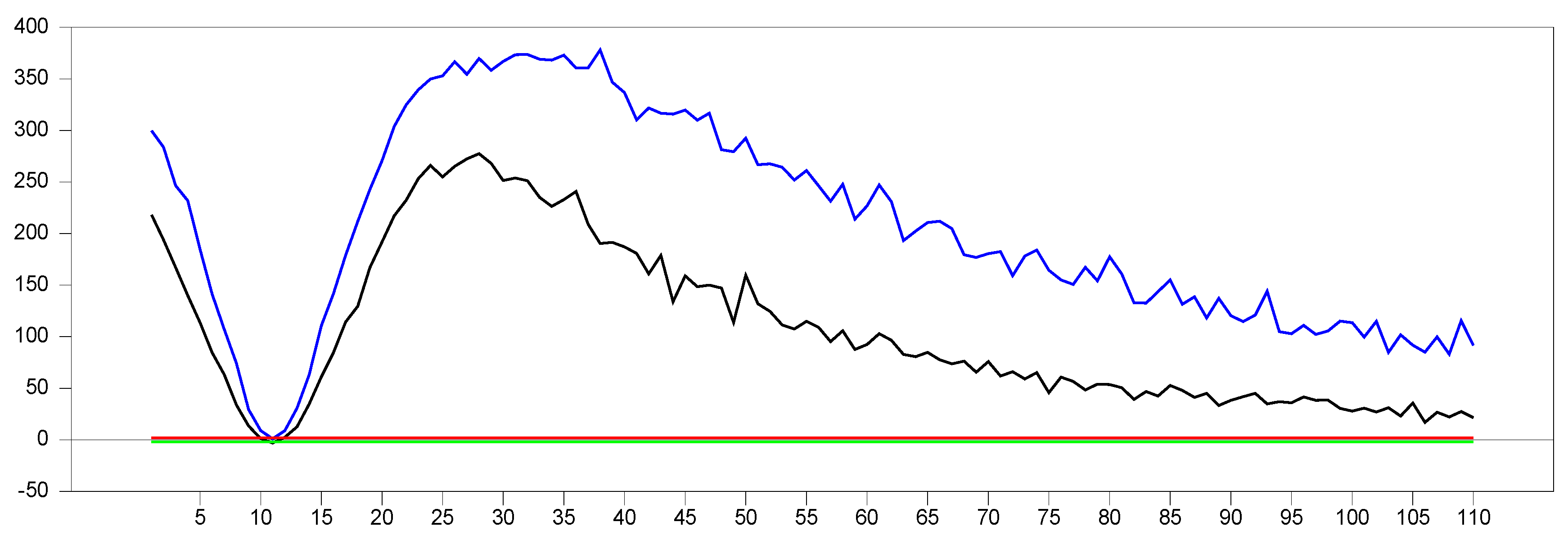

However, when

is fixed and

approaches infinity, the newly proposed method serves as a better proxy for the original variable. The results for this case are presented in

Figure 25.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}