Mean-Value-at-Risk Portfolio Optimization Based on Risk Tolerance Preferences and Asymmetric Volatility

,

,

Abstract

:1. Introduction

2. The Mechanism Framework

2.1. Autoregressive-Moving-Average (ARMA) Model

2.2. Glosten–Jagannathan–Runkle–Generalized Autoregressive Conditional Heteroscedasticity (GJR-GARCH) Model

2.3. Statistical Tests

2.3.1. Stationarity Test

2.3.2. Distribution Fit Test

2.3.3. Independence Test

2.3.4. Heteroscedasticity Test

2.3.5. Asymmetry Test

2.4. Mean-Value-at-Risk (Mean-VaR) Portfolio Optimization Model with Investor’s Risk Tolerance

3. Application of Mechanism

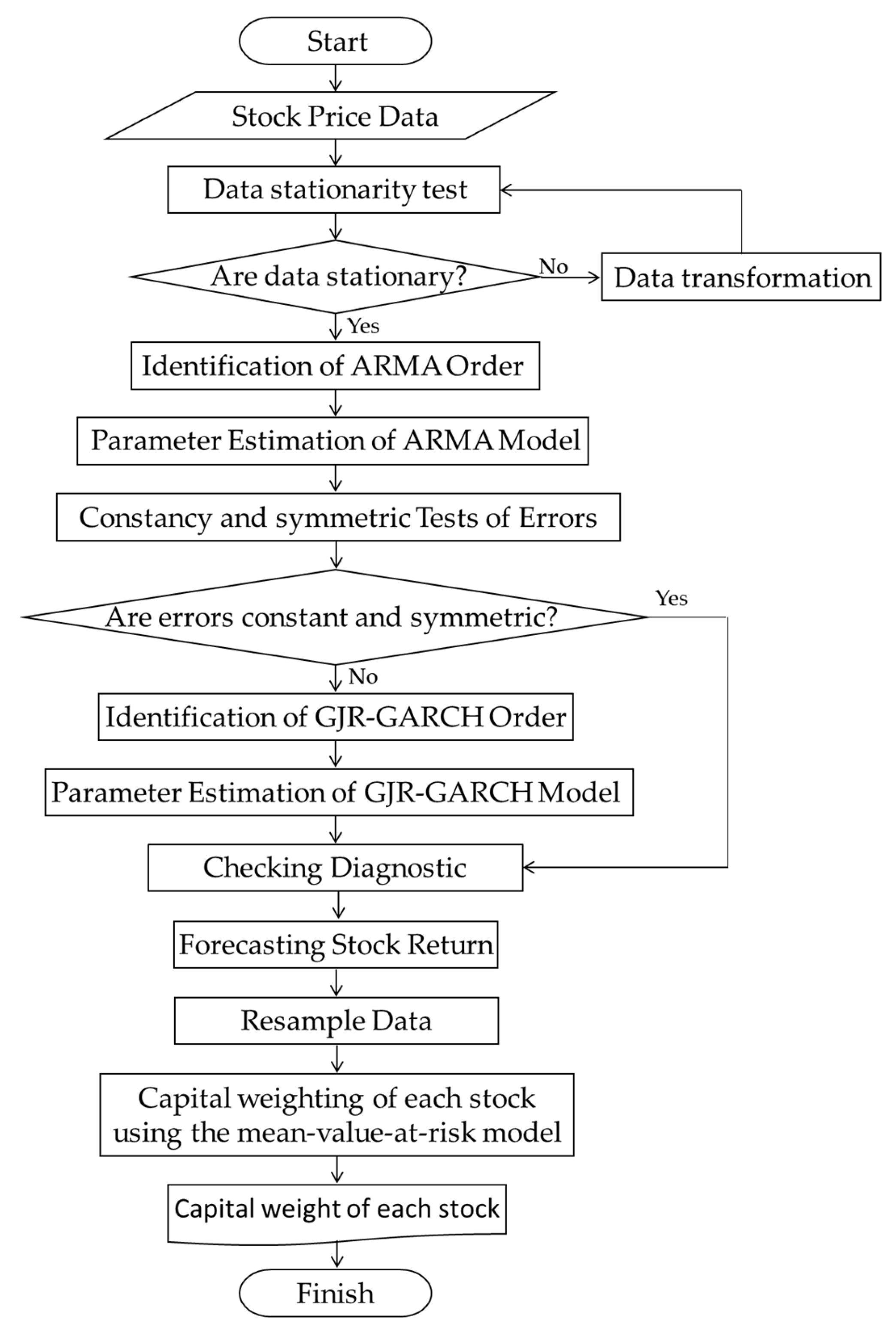

3.1. Algorithm to Apply Mechanism on Real Data

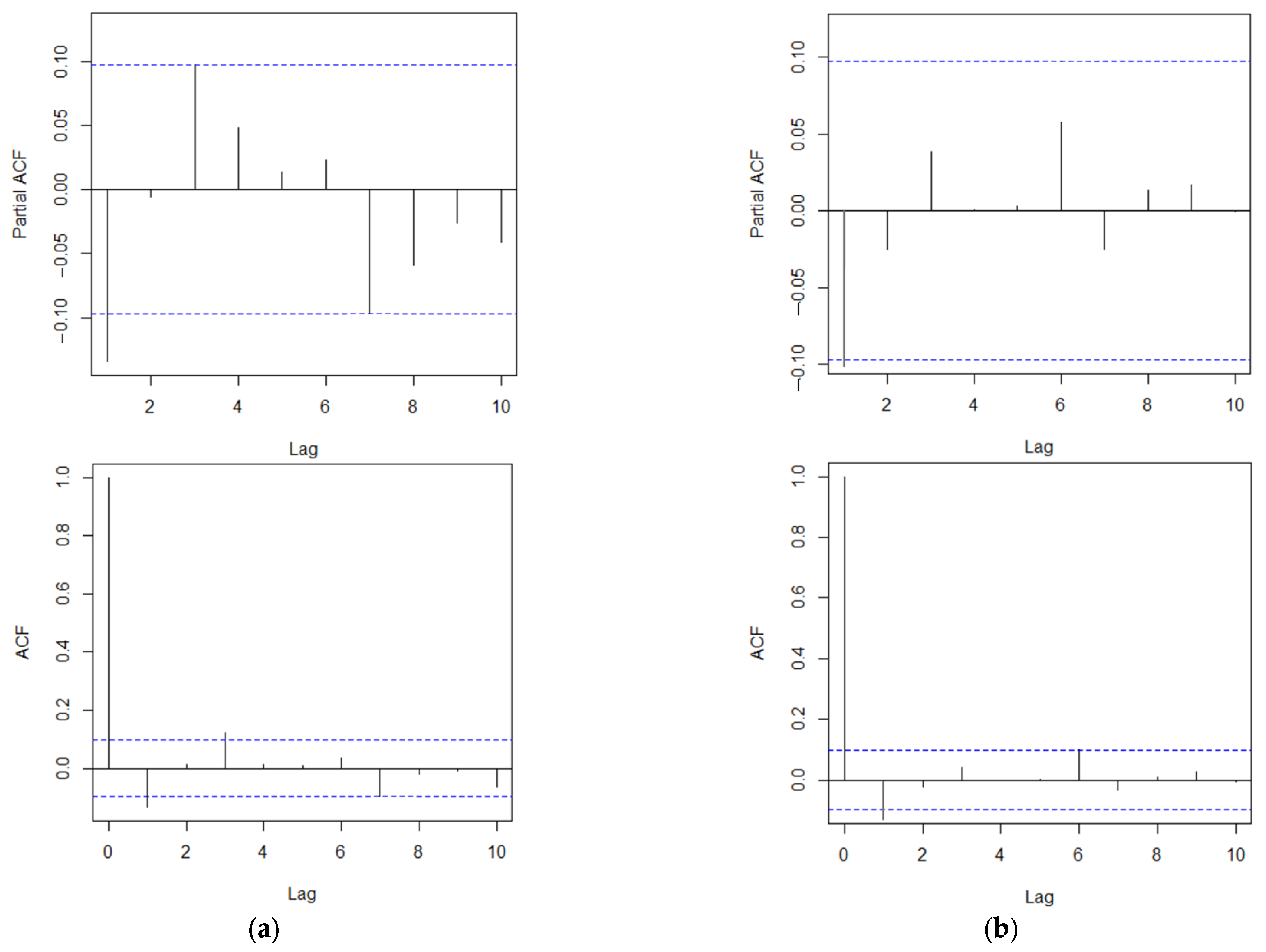

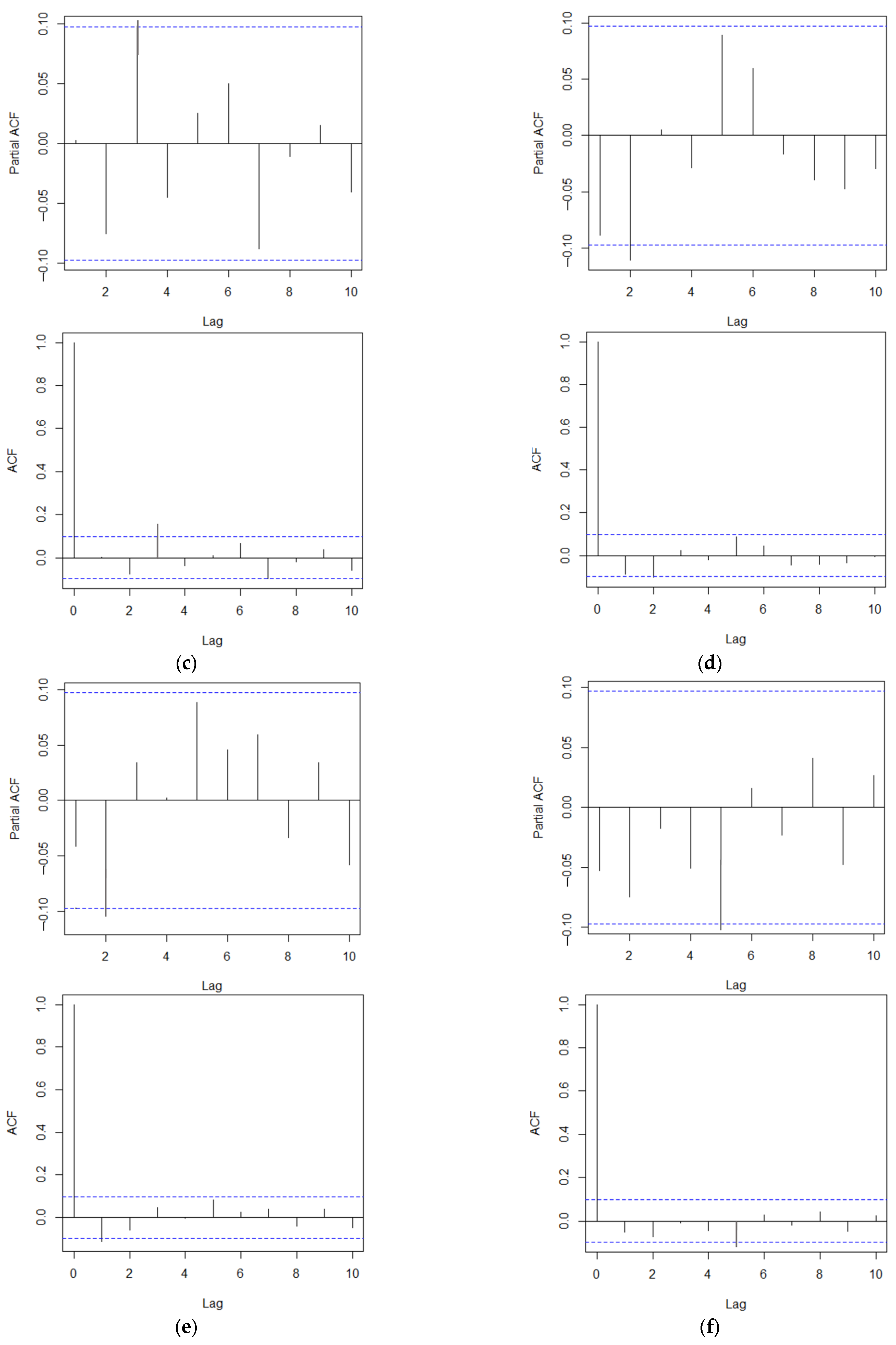

- Check the stationarity of each return data for each stock. The examination in this study was carried out using the Dicky–Fuller test (see Section 2.3.1). If the data is stationary, the experiment continues to the next stage, whereas if vice versa, the data is transformed first, e.g., into logarithmic form and data differentiation transformation.Identify orders from the ARMA model. Identification of AR and MA orders in this research is carried out using partial-autocorrelation and auto-correlation function diagrams, respectively.

- Estimate the parameters of the ARMA model. This assessment in this study was carried out using the maximum likelihood (ML) method.

- Check the classic assumptions in the ARMA model, one of which is the assumption of constant and symmetry of random errors. This study’s constant and symmetry checks were carried out using Glejser and cross-correlation (CC) tests, respectively. If the assumptions of constant and symmetry of random errors are met, the experiment continues to stage g, whereas if otherwise, the experiment continues to stage e.

- Identify orders from the GJR-GARCH model. The identification in this study was carried out through the Akaike information criterion (AIC) value. The order with the smallest AIC value is selected.

- Estimate the parameters of the GJR-GARCH model. This assessment in this study was carried out using the maximum likelihood (ML) method. Once this is completed, an ARMA-GJR-GARCH model of each stock data is obtained.

- Diagnostically test errors in the ARMA-GJR-GARCH model.

- Forecast the return of each stock for the next day using each model.

- Resample data by inputting the forecast results of each stock return into the data itself individually.

- Determine the vector of the mean of return and the covariance matrix from the resampled stock return data.

- Determine the optimal capital weight of each stock using Equation (25).

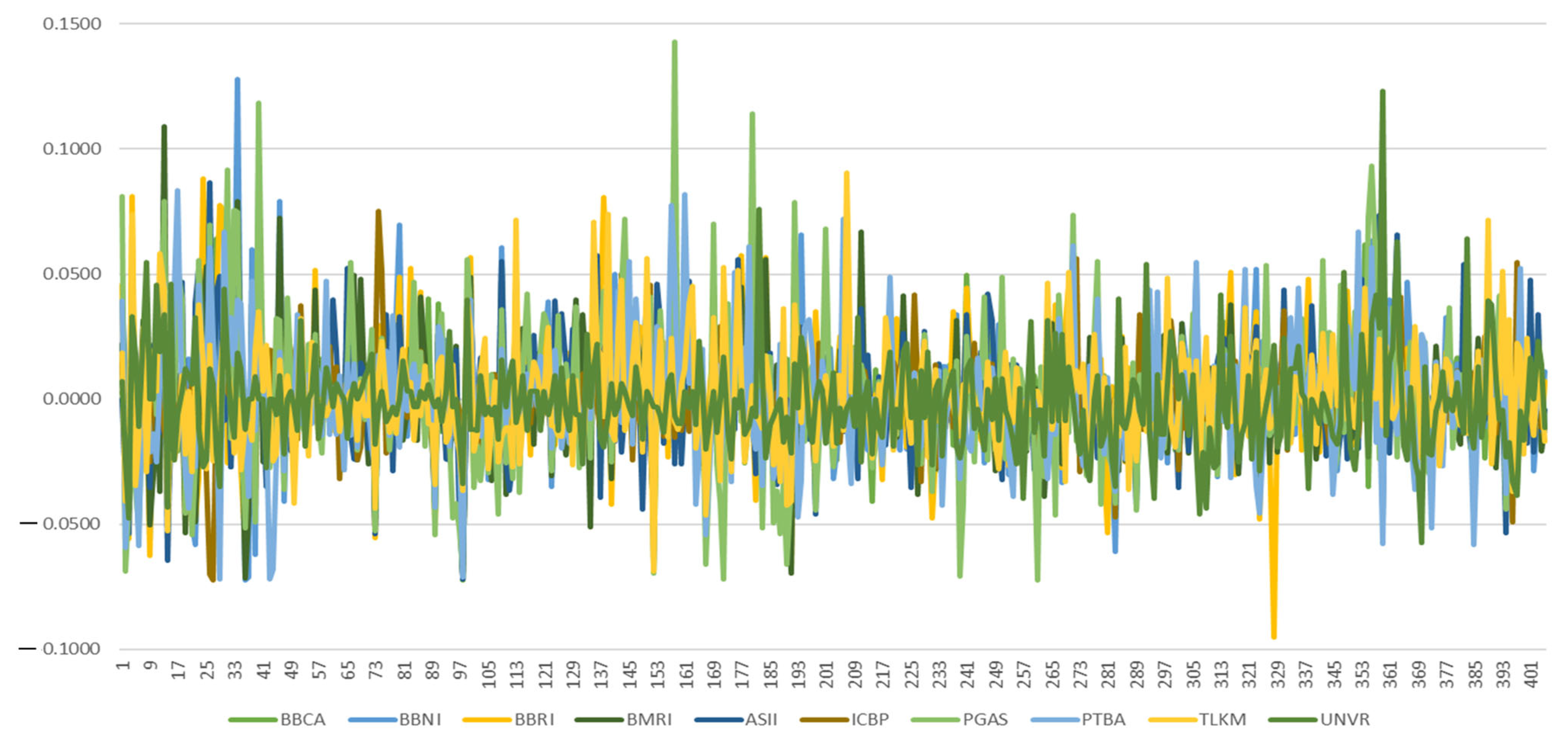

3.2. Data Description

- PT. Bank Central Asia Tbk. is coded as BBCA

- PT. Bank Negara Indonesia Tbk. is coded as BBNI.

- PT. Bank Rakyat Indonesia Tbk. is coded as BBRI.

- PT. Bank Mandiri Tbk. is coded as BMRI.

- PT. Astra International Tbk. is coded as ASII.

- PT. Indofood CBP Sukses Makmur Tbk. is coded as ICBP.

- PT. Perusahaan Gas Negara Tbk. is coded as PGAS.

- PT. Bukit Asam Tbk. is coded as PTBA.

- PT. Telekomunikasi Indonesia Tbk. is coded as TLKM.

- PT. Unilever Indonesia Tbk. is coded as UNVR.

3.3. Stationarity Test of Data

3.4. Order Identification and Parameter Estimation of the ARMA Model

3.5. Checking the Constancy and Symmetry Assumptions of Error Variance in the ARMA Model

3.6. GJR-GARCH Modeling of Each Stock Return

3.7. Error Diagnostic Test and Accuracy Check of ARMA-GJR-GARCH Model

3.8. Forecasting Mean of Return One Day Ahead

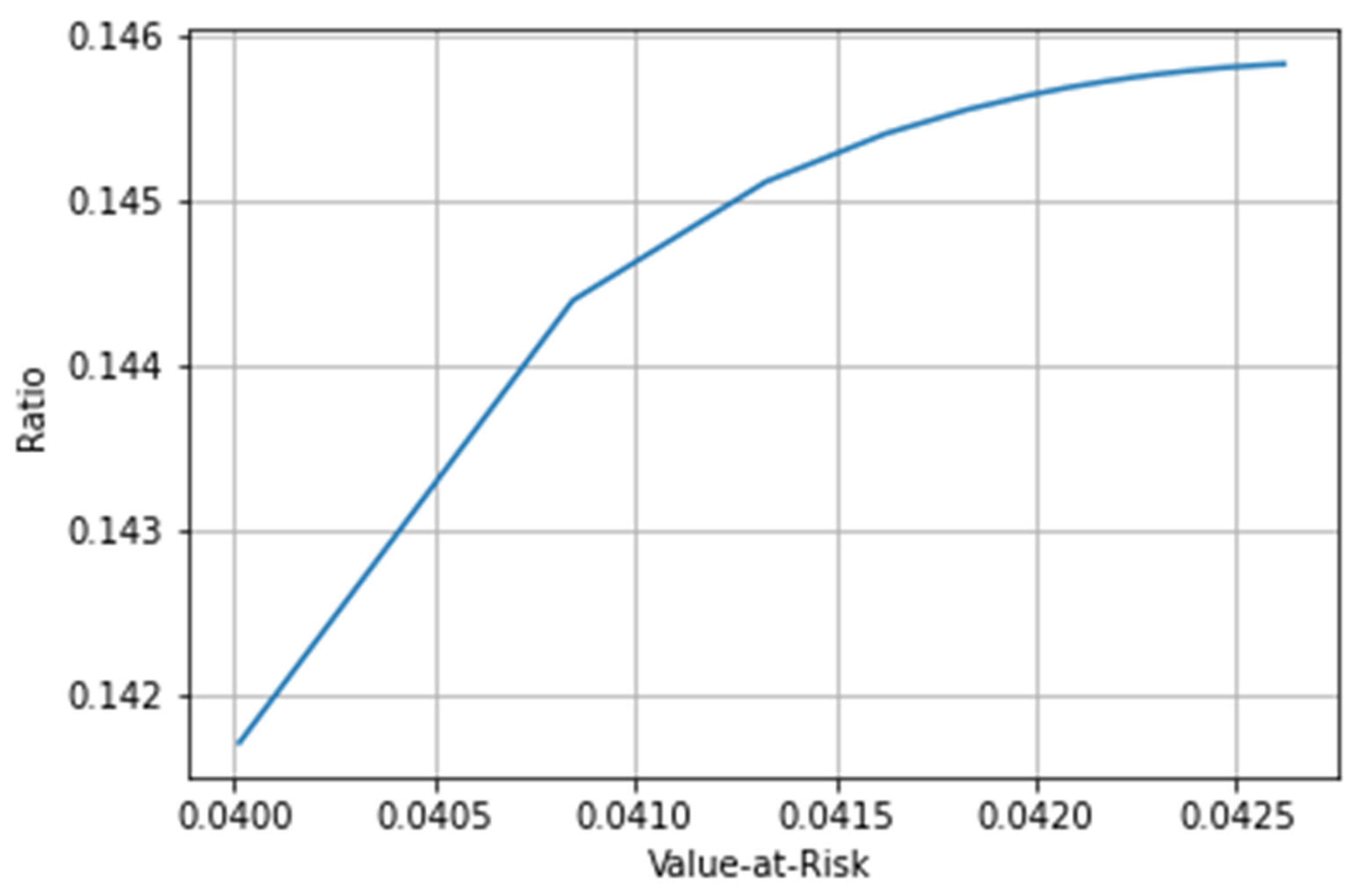

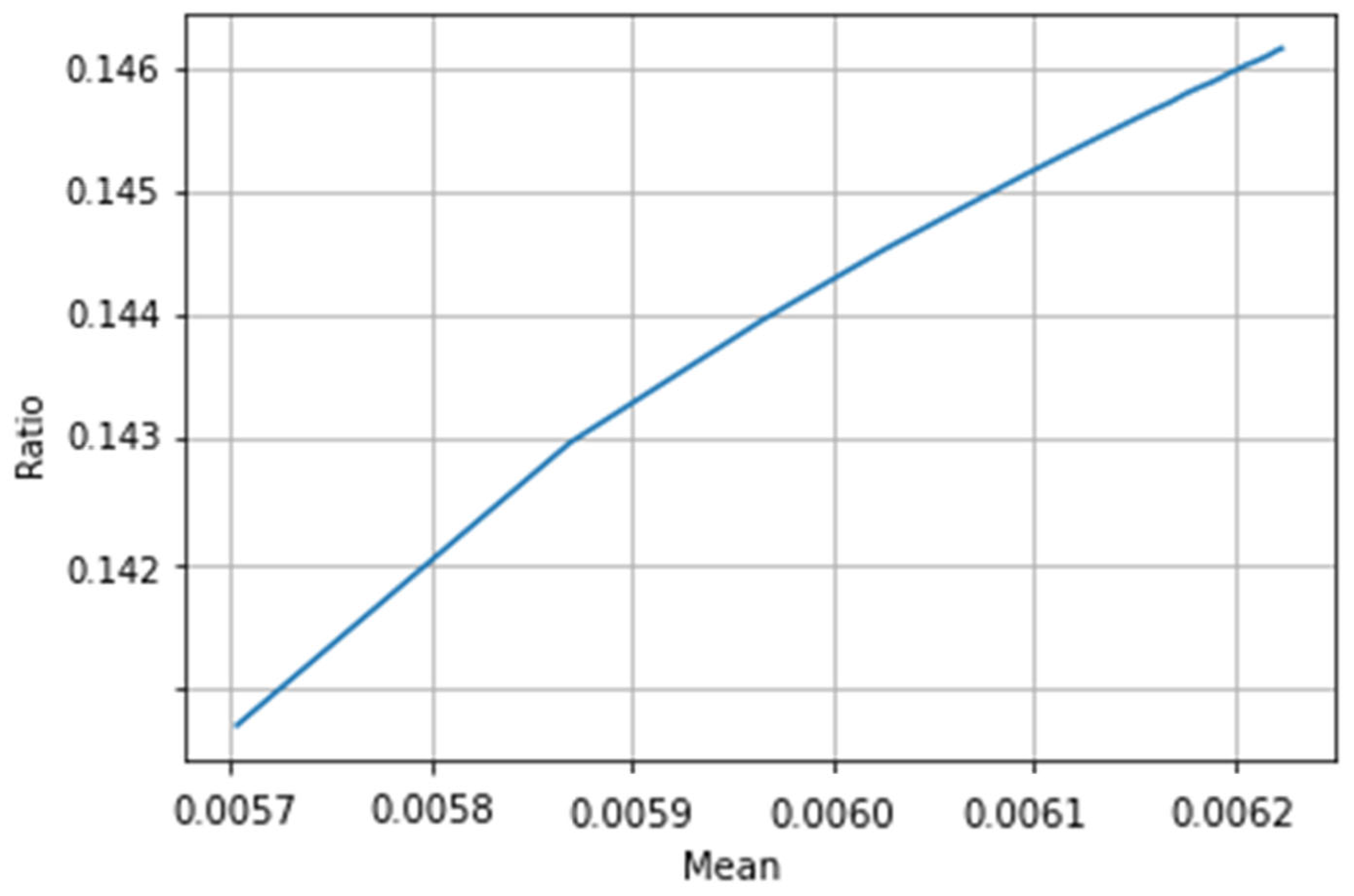

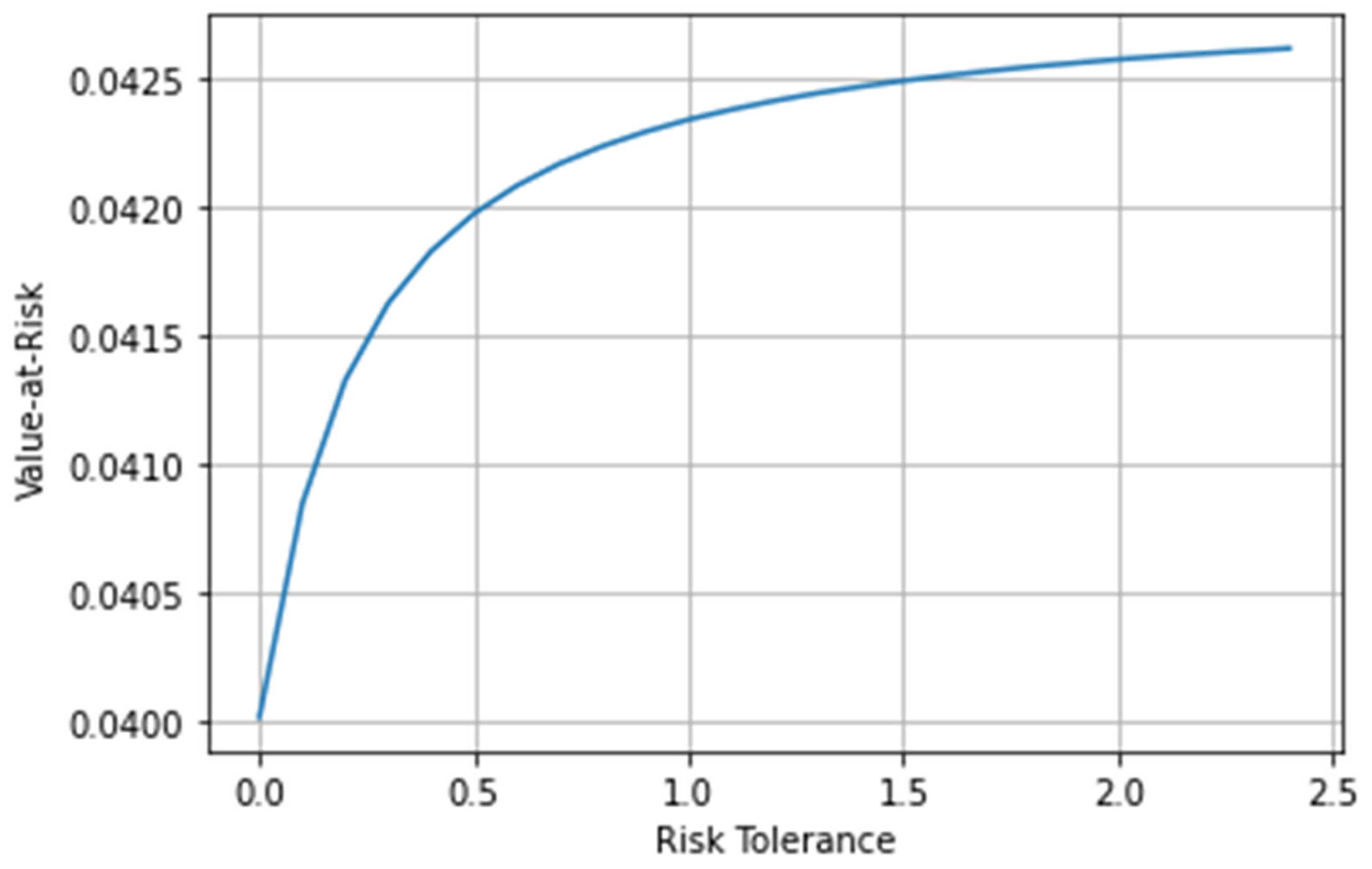

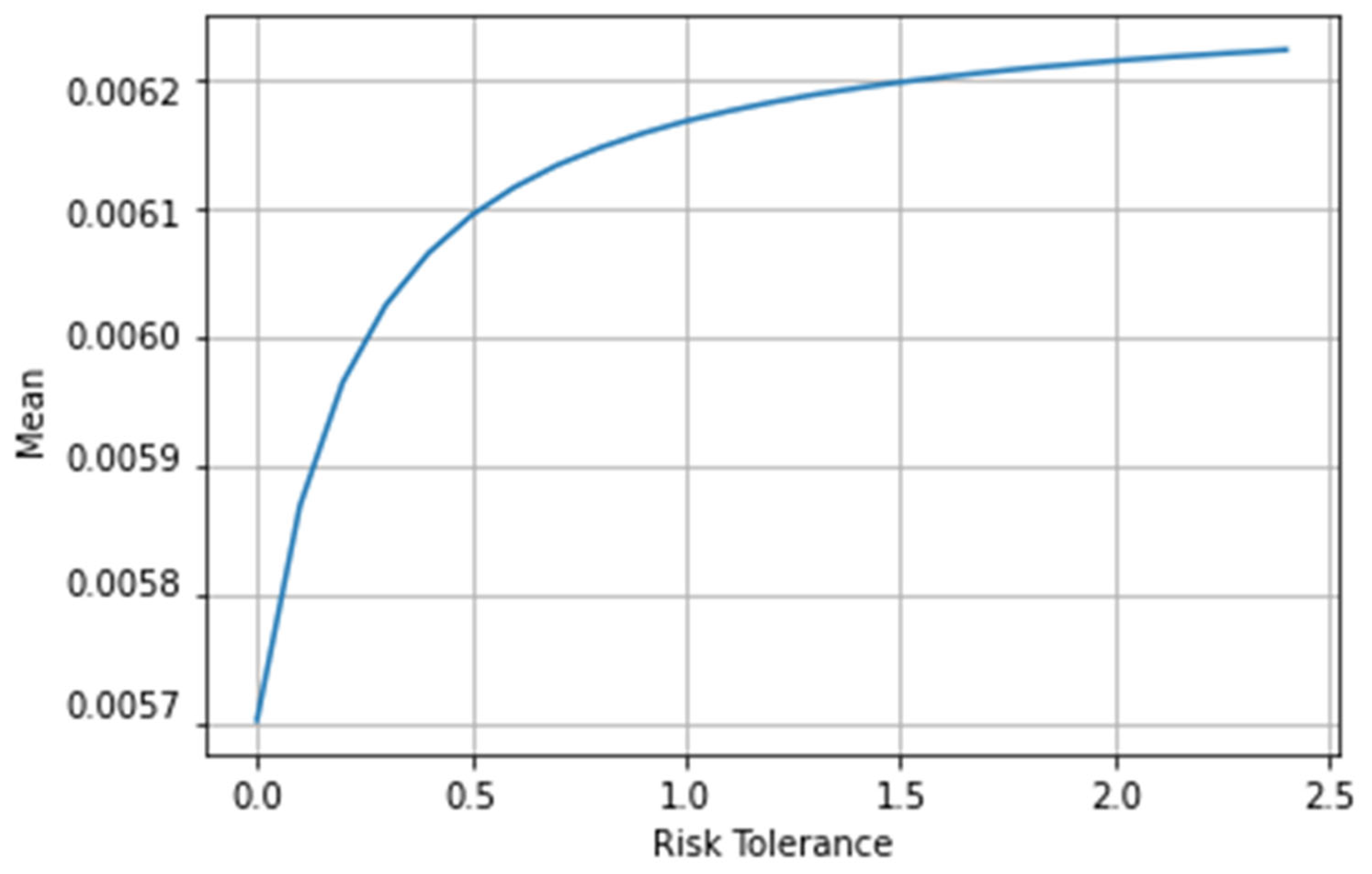

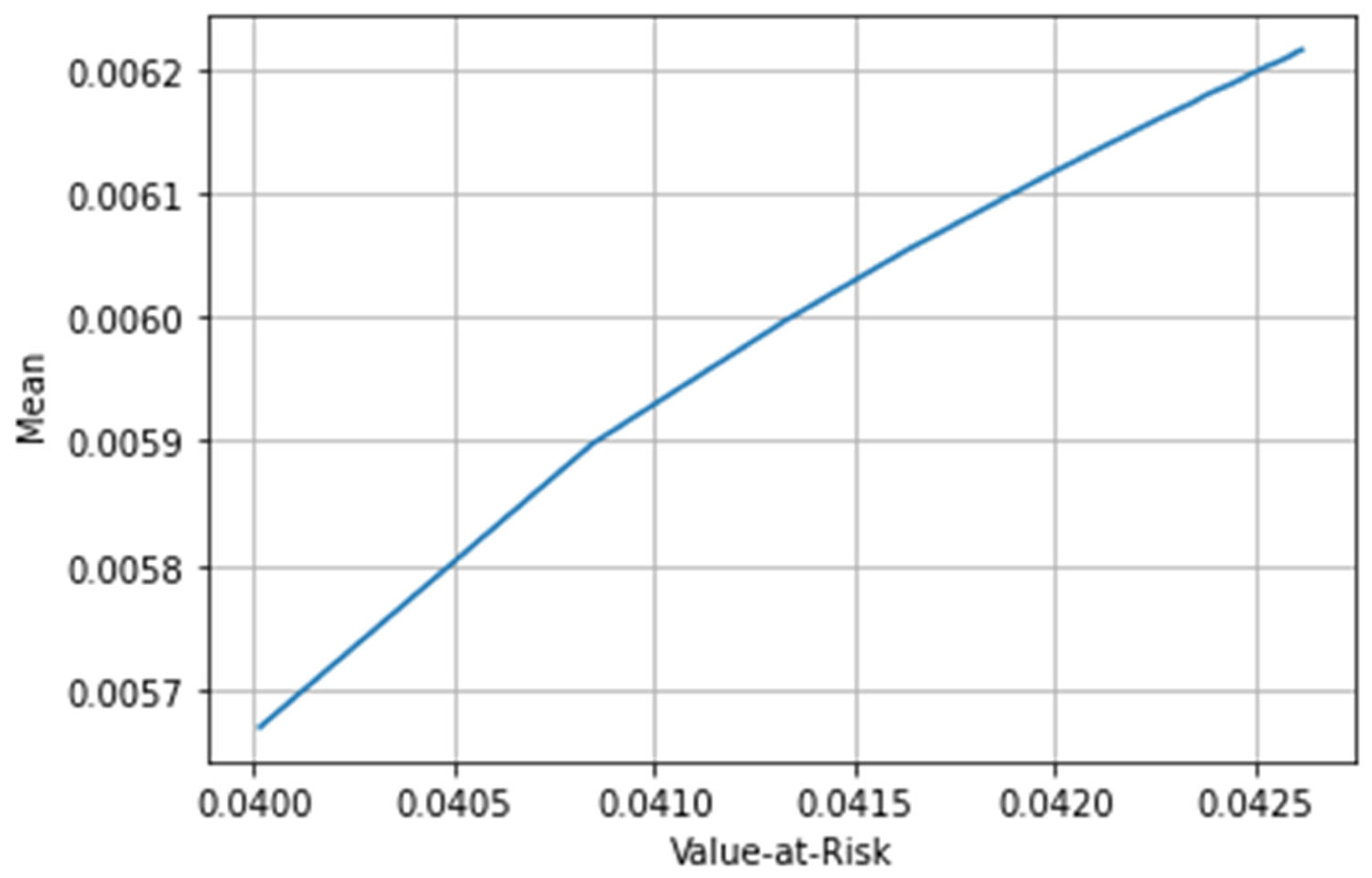

3.9. Portfolio Optimization Process

3.10. Discussion

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 0 | 0.721239 | 0.062561 | 0.099212 | 0.006589 | 0.006513 | 0.028736 | 0.028792 | 0.003542 | 0.037460 | 0.005355 | 1 | 0.005670 | 0.040015 | 0.141701 |

| 0.72 | 0.771480 | 0.047017 | 0.081043 | 0.004297 | 0.005117 | 0.019538 | 0.032824 | 0.002062 | 0.032430 | 0.004191 | 1 | 0.005898 | 0.040846 | 0.144393 |

| 1.44 | 0.793396 | 0.040237 | 0.073118 | 0.003298 | 0.004508 | 0.015526 | 0.034582 | 0.001416 | 0.030237 | 0.003683 | 1 | 0.005997 | 0.041327 | 0.145115 |

| 2.16 | 0.805673 | 0.036439 | 0.068678 | 0.002738 | 0.004167 | 0.013279 | 0.035567 | 0.001054 | 0.029007 | 0.003398 | 1 | 0.006053 | 0.041626 | 0.145408 |

| 2.88 | 0.813523 | 0.034010 | 0.065839 | 0.002379 | 0.003948 | 0.011842 | 0.036197 | 0.000823 | 0.028222 | 0.003216 | 1 | 0.006088 | 0.041829 | 0.145554 |

| 3.6 | 0.818976 | 0.032323 | 0.063867 | 0.002131 | 0.003797 | 0.010844 | 0.036635 | 0.000662 | 0.027676 | 0.003090 | 1 | 0.006113 | 0.041975 | 0.145637 |

| 4.32 | 0.822984 | 0.031083 | 0.062418 | 0.001948 | 0.003685 | 0.010110 | 0.036956 | 0.000544 | 0.027274 | 0.002997 | 1 | 0.006131 | 0.042084 | 0.145690 |

| 5.04 | 0.826054 | 0.030134 | 0.061308 | 0.001808 | 0.003600 | 0.009548 | 0.037203 | 0.000454 | 0.026967 | 0.002926 | 1 | 0.006145 | 0.042170 | 0.145724 |

| 5.76 | 0.828481 | 0.029383 | 0.060430 | 0.001697 | 0.003533 | 0.009104 | 0.037398 | 0.000382 | 0.026724 | 0.002870 | 1 | 0.006156 | 0.042238 | 0.145748 |

| 6.48 | 0.830447 | 0.028774 | 0.059719 | 0.001607 | 0.003478 | 0.008744 | 0.037555 | 0.000324 | 0.026527 | 0.002824 | 1 | 0.006165 | 0.042294 | 0.145766 |

| 7.2 | 0.832073 | 0.028271 | 0.059131 | 0.001533 | 0.003433 | 0.008446 | 0.037686 | 0.000276 | 0.026365 | 0.002786 | 1 | 0.006172 | 0.042341 | 0.145779 |

| 7.92 | 0.833440 | 0.027848 | 0.058636 | 0.001471 | 0.003395 | 0.008196 | 0.037795 | 0.000236 | 0.026228 | 0.002755 | 1 | 0.006179 | 0.042380 | 0.145789 |

| 8.64 | 0.834605 | 0.027488 | 0.058215 | 0.001418 | 0.003362 | 0.007982 | 0.037889 | 0.000202 | 0.026111 | 0.002728 | 1 | 0.006184 | 0.042414 | 0.145797 |

| 9.36 | 0.835610 | 0.027177 | 0.057852 | 0.001372 | 0.003335 | 0.007798 | 0.037970 | 0.000172 | 0.026010 | 0.002704 | 1 | 0.006188 | 0.042444 | 0.145804 |

| 10.08 | 0.836486 | 0.026906 | 0.057535 | 0.001332 | 0.003310 | 0.007638 | 0.038040 | 0.000146 | 0.025923 | 0.002684 | 1 | 0.006192 | 0.042469 | 0.145809 |

| 10.8 | 0.837256 | 0.026668 | 0.057257 | 0.001297 | 0.003289 | 0.007497 | 0.038102 | 0.000124 | 0.025846 | 0.002666 | 1 | 0.006196 | 0.042492 | 0.145813 |

| 11.52 | 0.837938 | 0.026457 | 0.057010 | 0.001266 | 0.003270 | 0.007372 | 0.038156 | 0.000104 | 0.025777 | 0.002650 | 1 | 0.006199 | 0.042512 | 0.145816 |

| 12.24 | 0.838546 | 0.026269 | 0.056790 | 0.001238 | 0.003253 | 0.007261 | 0.038205 | 0.000086 | 0.025717 | 0.002636 | 1 | 0.006202 | 0.042530 | 0.145819 |

| 12.96 | 0.839093 | 0.026100 | 0.056592 | 0.001213 | 0.003238 | 0.007161 | 0.038249 | 0.000070 | 0.025662 | 0.002624 | 1 | 0.006204 | 0.042547 | 0.145822 |

| 13.68 | 0.839586 | 0.025947 | 0.056414 | 0.001190 | 0.003224 | 0.007071 | 0.038289 | 0.000055 | 0.025612 | 0.002612 | 1 | 0.006206 | 0.042561 | 0.145824 |

| 14.4 | 0.840033 | 0.025809 | 0.056252 | 0.001170 | 0.003212 | 0.006989 | 0.038324 | 0.000042 | 0.025568 | 0.002602 | 1 | 0.006208 | 0.042575 | 0.145826 |

| 15.12 | 0.840441 | 0.025683 | 0.056105 | 0.001151 | 0.003200 | 0.006914 | 0.038357 | 0.000030 | 0.025527 | 0.002592 | 1 | 0.006210 | 0.042587 | 0.145828 |

| 15.84 | 0.840814 | 0.025567 | 0.055970 | 0.001134 | 0.003190 | 0.006846 | 0.038387 | 0.000019 | 0.025490 | 0.002584 | 1 | 0.006212 | 0.042598 | 0.145829 |

| 16.56 | 0.841156 | 0.025461 | 0.055846 | 0.001119 | 0.003180 | 0.006783 | 0.038415 | 0.000009 | 0.025455 | 0.002576 | 1 | 0.006214 | 0.042608 | 0.145830 |

| 17.28 | 0.841472 | 0.025364 | 0.055732 | 0.001104 | 0.003172 | 0.006725 | 0.038440 | −0.000001 | 0.025424 | 0.002568 | 1 | 0.006215 | 0.042618 | 0.145831 |

References

- Black, F.; Litterman, R. Global Portfolio Optimization. Financ. Anal. J. 1992, 48, 28–43. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized Autoregressive Conditional Heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Charles, A.; Darné, O. The Accuracy of Asymmetric GARCH Model Estimation. Int. Econ. 2019, 157, 179–202. [Google Scholar] [CrossRef]

- Xiong, J.; Zhou, X.Y. Mean-Variance Portfolio Selection under Partial Information. SIAM J. Control Optim. 2007, 46, 156–175. [Google Scholar] [CrossRef]

- Su, Y.C.; Huang, H.C.; Lin, Y.J. GJR-GARCH Model in Value-at-Risk of Financial Holdings. Appl. Financ. Econ. 2011, 21, 1819–1829. [Google Scholar] [CrossRef]

- Kalayci, C.B.; Ertenlice, O.; Akbay, M.A. A Comprehensive Review of Deterministic Models and Applications for Mean-Variance Portfolio Optimization. Expert Syst. Appl. 2019, 125, 345–368. [Google Scholar] [CrossRef]

- Al Janabi, M.A.M. Multivariate Portfolio Optimization under Illiquid Market Prospects: A Review of Theoretical Algorithms and Practical Techniques for Liquidity Risk Management. J. Model. Manag. 2021, 16, 288–309. [Google Scholar] [CrossRef]

- Nur Aini, N.S.; Lutfi, L. The Influence of Risk Perception, Risk Tolerance, Overconfidence, and Loss Aversion towards Investment Decision Making. J. Econ. Bus. Account. Ventur. 2019, 21, 401. [Google Scholar] [CrossRef]

- Pak, O.; Mahmood, M. Impact of Personality on Risk Tolerance and Investment Decisions. Int. J. Commer. Manag. 2015, 25, 370–384. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Khandakar, Y. Automatic Time Series Forecasting: The Forecast Package for R. J. Stat. Softw. 2008, 27, 1–22. [Google Scholar] [CrossRef]

- Fu, R.; Zhang, Z.; Li, L. Using LSTM and GRU Neural Network Methods for Traffic Flow Prediction. In Proceedings of the 2016 31st Youth Academic Annual Conference of Chinese Association of Automation (YAC), Wuhan, China, 1–13 November 2016; pp. 324–328. [Google Scholar]

- Sukono, S.; Parmikanti, K.; Lisnawati, L.; Gw, S.H.; Saputra, J. Mean-Var Investment Portfolio Optimization Under Capital Asset Pricing Model (CAPM) with Nerlove Transformation: An Empirical Study Using Time Series Approach. Ind. Eng. Manag. Syst. 2020, 19, 498–509. [Google Scholar] [CrossRef]

- Suganthi, L.; Samuel, A.A. Energy Models for Demand Forecasting—A Review. Renew. Sustain. Energy Rev. 2012, 16, 1223–1240. [Google Scholar] [CrossRef]

- Valipour, M.; Banihabib, M.E.; Behbahani, S.M.R. Comparison of the ARMA, ARIMA, and the Autoregressive Artificial Neural Network Models in Forecasting the Monthly Inflow of Dez Dam Reservoir. J. Hydrol. 2013, 476, 433–441. [Google Scholar] [CrossRef]

- Vaibhava Lakshmi, R.; Radha, S. Time Series Forecasting for the Adobe Software Company’s Stock Prices Using ARIMA (BOX-JENKIN’) Model. J. Phys. Conf. Ser. 2021, 2115, 012044. [Google Scholar] [CrossRef]

- Hidayana, R.A.; Napitupulu, H.; Sukono, S. An Investment Decision-Making Model to Predict the Risk and Return in Stock Market: An Application of ARIMA-GJR-GARCH. Decis. Sci. Lett. 2022, 11, 235–246. [Google Scholar] [CrossRef]

- Dritsaki, C. An Empirical Evaluation in GARCH Volatility Modeling: Evidence from the Stockholm Stock Exchange. J. Math. Financ. 2017, 07, 366–390. [Google Scholar] [CrossRef]

- Zhang, L.; Zoli, E. Leaning against the Wind: Macroprudential Policy in Asia. J. Asian Econ. 2016, 42, 33–52. [Google Scholar] [CrossRef]

- Yin, R.; Newman, D.H.; Siry, J. Testing for Market Integration among Southern Pine Regions. J. For. Econ. 2002, 8, 151–166. [Google Scholar] [CrossRef]

- Ma, Z.-G.; Ma, C.-Q. Pricing Catastrophe Risk Bonds: A Mixed Approximation Method. Insur. Math. Econ. 2013, 52, 243–254. [Google Scholar] [CrossRef]

- Ghasemi, A.; Zahediasl, S. Normality Tests for Statistical Analysis: A Guide for Non-Statisticians. Int. J. Endocrinol. Metab. 2012, 10, 486–489. [Google Scholar] [CrossRef]

- Liu, Q.; Liu, X.; Jiang, B.; Yang, W. Forecasting Incidence of Hemorrhagic Fever with Renal Syndrome in China Using ARIMA Model. BMC Infect. Dis. 2011, 11, 218. [Google Scholar] [CrossRef] [PubMed]

- Sukono; Juahir, H.; Ibrahim, R.A.; Saputra, M.P.A.; Hidayat, Y.; Prihanto, I.G. Application of Compound Poisson Process in Pricing Catastrophe Bonds: A Systematic Literature Review. Mathematics 2022, 10, 2668. [Google Scholar] [CrossRef]

- Tadesse, K.B.; Dinka, M.O. Application of SARIMA Model to Forecasting Monthly Flows in Waterval River, South Africa. J. Water Land Dev. 2017, 35, 229–236. [Google Scholar] [CrossRef]

- Mohajerin Esfahani, P.; Kuhn, D. Data-Driven Distributionally Robust Optimization Using the Wasserstein Metric: Performance Guarantees and Tractable Reformulations. Math. Program. 2018, 171, 115–166. [Google Scholar] [CrossRef]

- Kolm, P.N.; Tütüncü, R.; Fabozzi, F.J. 60 Years of Portfolio Optimization: Practical Challenges and Current Trends. Eur. J. Oper. Res. 2014, 234, 356–371. [Google Scholar] [CrossRef]

- Xidonas, P.; Steuer, R.; Hassapis, C. Robust Portfolio Optimization: A Categorized Bibliographic Review. Ann. Oper. Res. 2020, 292, 533–552. [Google Scholar] [CrossRef]

- Guo, Y.; Zhou, W.; Luo, C.; Liu, C.; Xiong, H. Instance-Based Credit Risk Assessment for Investment Decisions in P2P Lending. Eur. J. Oper. Res. 2016, 249, 417–426. [Google Scholar] [CrossRef]

- Ponsich, A.; Jaimes, A.L.; Coello, C.A.C. A Survey on Multiobjective Evolutionary Algorithms for the Solution of the Portfolio Optimization Problem and Other Finance and Economics Applications. IEEE Trans. Evol. Comput. 2013, 17, 321–344. [Google Scholar] [CrossRef]

- Kon, S.J. Models of Stock Returns—A Comparison. J. Financ. 1984, 39, 147. [Google Scholar] [CrossRef]

- Prakash, A.J.; Chang, C.-H.; Pactwa, T.E. Selecting a Portfolio with Skewness: Recent Evidence from US, European, and Latin American Equity Markets. SSRN Electron. J. 2003, 27, 1375–1390. [Google Scholar] [CrossRef]

- Rockafellar, R.T.; Uryasev, S. Optimization of Conditional Value-at-Risk. J. Risk 2000, 2, 21–41. [Google Scholar] [CrossRef]

- Rockafellar, R.T.; Uryasev, S. Conditional Value-at-Risk for General Loss Distributions. J. Bank. Financ. 2002, 26, 1443–1471. [Google Scholar] [CrossRef]

- Gaivoronski, A.; Pflug, G. Value-at-Risk in Portfolio Optimization: Properties and Computational Approach. J. Risk 2005, 7, 1–31. [Google Scholar] [CrossRef]

- Pérignon, C.; Smith, D.R. The Level and Quality of Value-at-Risk Disclosure by Commercial Banks. J. Bank. Financ. 2010, 34, 362–377. [Google Scholar] [CrossRef]

- Purwandari, T.; Riaman; Hidayat, Y.; Sukono; Ibrahim, R.A.; Hidayana, R.A. Selecting and Weighting Mechanisms in Stock Portfolio Design Based on Clustering Algorithm and Price Movement Analysis. Mathematics 2023, 11, 4151. [Google Scholar] [CrossRef]

- Lwin, K.T.; Qu, R.; MacCarthy, B.L. Mean-VaR Portfolio Optimization: A Nonparametric Approach. Eur. J. Oper. Res. 2017, 260, 751–766. [Google Scholar] [CrossRef]

- Sukono; Sidi, P.; bin Bon, A.T.; Supian, S. Modeling of Mean-VaR Portfolio Optimization by Risk Tolerance When the Utility Function Is Quadratic. In Proceedings of the 2016 2nd International Conference on Applied Statistics (ICAS II), West Java, Indonesia, 27–28 September 2016; p. 020035. [Google Scholar]

- Lin, X.; Floudas, C.A.; Kallrath, J. Global Solution Approach for a Nonconvex MINLP Problem in Product Portfolio Optimization. J. Glob. Optim. 2005, 32, 417–431. [Google Scholar] [CrossRef]

- Cesarone, F.; Scozzari, A.; Tardella, F. An Optimization–Diversification Approach to Portfolio Selection. J. Glob. Optim. 2020, 76, 245–265. [Google Scholar] [CrossRef]

| Code | Conclusion | |||

|---|---|---|---|---|

| BBCA | −15.1522 | −3.4251 | Stock return data are stationary | |

| BBNI | −14.8121 | |||

| BBRI | −15.2115 | |||

| BMRI | −16.4812 | |||

| ASII | −16.0417 | |||

| ICBP | −15.6242 | |||

| PGAS | −15.4219 | |||

| PTBA | −14.8221 | |||

| TLKM | −18.8046 | |||

| UNVR | −14.2247 |

| No. | Code | ARMA Order | ARMA Model |

|---|---|---|---|

| 1. | BBCA | ARMA (1,3) | |

| 2. | BBNI | ARMA (1,1) | |

| 3. | BBRI | ARMA (3,3) | |

| 4. | BMRI | ARMA (2,2) | |

| 5. | ASII | ARMA (2,1) | |

| 6. | ICBP | ARMA (5,5) | |

| 7. | PGAS | ARMA (1,2) | |

| 8. | PTBA | ARMA (1,5) | |

| 9. | TLKM | ARMA (3,3) | |

| 10. | UNVR | ARMA (2,3) |

| Code | ARMA Model | Probability | Conclusion |

|---|---|---|---|

| BBCA | ARMA (1,3) | 0.0004 | There is heteroscedasticity in the ARMA model’s error variance. |

| BBNI | ARMA (1,1) | 0.0000 | |

| BBRI | ARMA (3,3) | 0.0000 | |

| BMRI | ARMA (2,2) | 0.0000 | |

| ASII | ARMA (2,1) | 0.0000 | |

| ICBP | ARMA (5,5) | 0.0000 | |

| PGAS | ARMA (1,2) | 0.0000 | |

| PTBA | ARMA (1,5) | 0.0002 | |

| TLKM | ARMA (3,3) | 0.0000 | |

| UNVR | ARMA (2,3) | 0.0160 |

| Code | GJR-GARCH (1,1) Model |

|---|---|

| BBCA | |

| BBNI | |

| BBRI | |

| BMRI | |

| ASII | |

| ICBP | |

| PGAS | |

| PTBA | |

| TLKM | |

| UNVR |

| Code | Conclusion | ||

|---|---|---|---|

| BBCA | 0.0564 | 0.0675 | The error of each ARMA-GJR-GARCH model is normally distributed |

| BBNI | 0.0653 | ||

| BBRI | 0.0429 | ||

| BMRI | 0.0461 | ||

| ASII | 0.0593 | ||

| ICBP | 0.0663 | ||

| PGAS | 0.0641 | ||

| PTBA | 0.0673 | ||

| TLKM | 0.0419 | ||

| UNVR | 0.0578 |

| Code | Conclusion | ||

|---|---|---|---|

| BBCA | 45.3311 | 46.1943 | The error of each ARMA-GJR-GARCH model is independent of the others |

| BBNI | 45.1821 | 48.6024 | |

| BBRI | 43.1391 | 43.7730 | |

| BMRI | 36.2593 | 46.1943 | |

| ASII | 43.3852 | 47.3999 | |

| ICBP | 31.3604 | 38.8851 | |

| PGAS | 46.9329 | 47.3999 | |

| PTBA | 38.8132 | 43.7730 | |

| TLKM | 39.9226 | 43.7730 | |

| UNVR | 44.9590 | 44.9853 |

| Code | MAE | RMSE |

|---|---|---|

| BBCA | 0.0139 | 0.0209 |

| BBNI | 0.0169 | 0.0245 |

| BBRI | 0.0158 | 0.0237 |

| BMRI | 0.0234 | 0.0327 |

| ASII | 0.0163 | 0.0229 |

| ICBP | 0.0116 | 0.0177 |

| PGAS | 0.0219 | 0.0312 |

| PTBA | 0.0184 | 0.0274 |

| TLKM | 0.0144 | 0.0203 |

| UNVR | 0.0136 | 0.0207 |

| Code | ) | ) |

|---|---|---|

| BBCA | 0.00661 | 0.00107 |

| BBNI | 0.00026 | 0.00523 |

| BBRI | 0.00030 | 0.00382 |

| BMRI | 0.00205 | 0.04064 |

| ASII | 0.00026 | 0.05490 |

| ICBP | −0.00133 | 0.01291 |

| PGAS | 0.00081 | 0.02410 |

| PTBA | −0.00129 | 0.08080 |

| TLKM | 0.00326 | 0.01180 |

| UNVR | 0.00227 | 0.07700 |

| Model | Mean of Return |

|---|---|

| ARMA-GJR-GARCH mean-VaR | 0.006214 |

| Mean variance | 0.005514 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hidayat, Y.; Purwandari, T.; Sukono; Prihanto, I.G.; Hidayana, R.A.; Ibrahim, R.A. Mean-Value-at-Risk Portfolio Optimization Based on Risk Tolerance Preferences and Asymmetric Volatility. Mathematics 2023, 11, 4761. https://doi.org/10.3390/math11234761

Hidayat Y, Purwandari T, Sukono, Prihanto IG, Hidayana RA, Ibrahim RA. Mean-Value-at-Risk Portfolio Optimization Based on Risk Tolerance Preferences and Asymmetric Volatility. Mathematics. 2023; 11(23):4761. https://doi.org/10.3390/math11234761

Chicago/Turabian StyleHidayat, Yuyun, Titi Purwandari, Sukono, Igif Gimin Prihanto, Rizki Apriva Hidayana, and Riza Andrian Ibrahim. 2023. "Mean-Value-at-Risk Portfolio Optimization Based on Risk Tolerance Preferences and Asymmetric Volatility" Mathematics 11, no. 23: 4761. https://doi.org/10.3390/math11234761

APA StyleHidayat, Y., Purwandari, T., Sukono, Prihanto, I. G., Hidayana, R. A., & Ibrahim, R. A. (2023). Mean-Value-at-Risk Portfolio Optimization Based on Risk Tolerance Preferences and Asymmetric Volatility. Mathematics, 11(23), 4761. https://doi.org/10.3390/math11234761