Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies

Abstract

1. Introduction

1.1. Definitions of Corporate Sustainability, Corporate Social Responsibility and Sustainable Development

- corporate sustainability in the sense that is synonymous with CSR;

- corporate sustainability in the sense that is not synonymous with CSR;

- CSR as a factor ensuring corporate sustainability;

- corporate sustainability is the observance of moral standards;

- corporate sustainability is a strategy implemented by executives;

- corporate sustainability is determined by many indicators and characteristics of a company (economic growth, product quality, business reputation, organizational structure, stakeholder relationships, environmental protection and others) simultaneously;

- the triune concept of corporate sustainability (based on TBL);

- corporate sustainability as a driver of economic results;

- corporate sustainability as a consequence of achieving particular results that are measured using instruments developed by organizations (for example, the Dow Jones Sustainability Index, the Shanghai Stock Exchange Sustainable Development Industry Index).

1.2. Methods Focused on Collection of Environmental Information and Calculation of Environmental Indicators

1.3. Methods Focused on Assessment of Social Welfare, Calculation of Social Indicators and Indicators of Social Efficiency

- Social Impact Assessment (SIA), which is a method for considering social impacts and a way to assess the impact of certain projects on society (roads, industrial facilities, mines, dams, ports, airports and others);

- Among methods for assessing social effectiveness, based mainly on a qualitative data analysis, it is worth noting SRA (Social Return Assessment);

- The LBG model allows assessing the value and achievements of corporate investment into the community, as well as properly report to stakeholders. This model presents a matrix, which can be used to summarize and obtain quantitative information on the results of work with local communities. Dividing corporate activity into elements, the matrix offers a detailed study of various types of resource inputs, determines immediate or intermediate results/products (outputs) and, ultimately, presents the nature and degree of environment impacts (LBG Model 2017).

1.4. Methods Based on a Comprehensive Assessment of CSR

- The SROI (Social Return on Investment) is based on the SCBA method and allows calculation of social efficiency of investments (social return on investment) (Emerson et al. 2000; Lingane and Olsen 2004). Social results are determined given the interests of stakeholders and are assessed by using subjective and objective indicators that most fully reflect the results obtained (A Guide 2012). This method does not use any sustainable indicators or results selected for specific conditions, company or project. However, this approach is focused on projects and does not allow assessing effectiveness of CSR of an operating company.

- The SCBA (Social Costs-Benefit Analysis) is a tool of the welfare economy and it assesses social costs-benefits. As a rule, it is used to justify a state support of large socially significant projects (Wells 1975). It is supposed to make monetary assessment of private and external social costs (including environmental ones) (Manning et al. 2016). The disadvantage of this method in assessing CSR is that it cannot take into account qualitative results to the full extent.

- The DEA (Data Envelopment Analysis) is used to evaluate CSR activities in order to determine effectiveness of management decisions based on profitability criterion. This method presents only final ratings.

- Since 1991 the KLD (Dowling 2013) index has been one of the most widely-used company analysis indices in seven areas: product quality and safety, relations with employees, corporate management, relations with the local community, human rights, environment, diversity, thus covering all main directions of SD. The method links social and financial indicators and demonstrates only final ratings.

- Econometric Impact Index, offered by Smith O’Brien, allows assessing the total impact of the company on the local community. This index can be used both by the companies and local authorities involved in assessing the impact of those companies on the local community, including expanding or reducing production, pricing policy, tax payments and the impact on decision-making in regional development.

1.5. Methods for Assessing Corporate Sustainability with a Comprehensive Assessment of Corporate Activities in Environmental, Social and Economic Areas

- The ISS-oekom corporate rating (ISS-oekom Universe) includes assessment of more than 3900 companies; Oekom Corporate Ratings assess companies by using 100 social, managerial and environmental criteria (ISS-oekom 2019) weighted, aggregated and presented as a score, which makes up the background of rating of the companies;

- ESG ratings are based on assessing the optimal set of special indicators reflecting the level of the company’s impact on the natural and social environment, as well as the degree of corporate exposure to social and managerial risks (ESG Rating 2020);

- DJSI Index (The Dow Jones Sustainability Index) is a set of indicators for assessing sustainability of large public companies-stock market players, selected under the corporate sustainability assessment made by RobecoSAM agency. DJSI indices are global benchmarks based on a set of criteria for assessing environmental, social and economic capacities of companies (JSI/CSA 2020), including weighting factors. The content and number of indicators within each criterion, as well as their weight factors can be adjusted in accordance with the recommendations of RobecoSAM;

- The RobecoSAM agency methods are used not only to evaluate DJSI, but also to assess sustainable development of companies given their industrial profile. In this case, assessment uses specific industry criteria. For example, for mineral companies, economic criterion included payment transparency, environmental one—mineral waste mgmt., water related risks, biodiversity, social one—asset closure mgmt, community impact, stakeholder engagement (Corporate 2018).

- 5.

- Fortune ranking is based on comparison with the “top companies” and presents the final ranking data. It limits the ability of companies to self-evaluate and analyze internal effects, relies on fixed indicators not ranked by their significance, that is, it does not count for effectiveness as a reason of certain social investments;

- 6.

- The 2008 World Business Council for Sustainable Development (WBCSD) Guidelines together with the International Finance Corporation (IFC) define universal framework principles for identifying, measuring, assessing and prioritizing social effects, as well as indicators by value chain elements (WBCSD 2017).

- (a)

- method for assessing basic performance indicators (BPI), developed by the Russian Union of Industrialists and Entrepreneurs (RUIE) under the Global Reporting Initiative (GRI) and intended for preparing corporate non-financial reports (social, sustainable development, environmental ones) and for corporate management systems in order to organize monitoring, control and assessment of key performance results. Basic performance indicators include 48 indicators in economic, social and environmental areas of the company (Global 2014);

- (b)

- The Social Reporting of Enterprises and Organizations Registered in the Russian Federation. Guidelines Standard prepared by the Chamber of Industry and Commerce under AA 1000 and GRI principles (Prokopov and Feoktistova 2008).

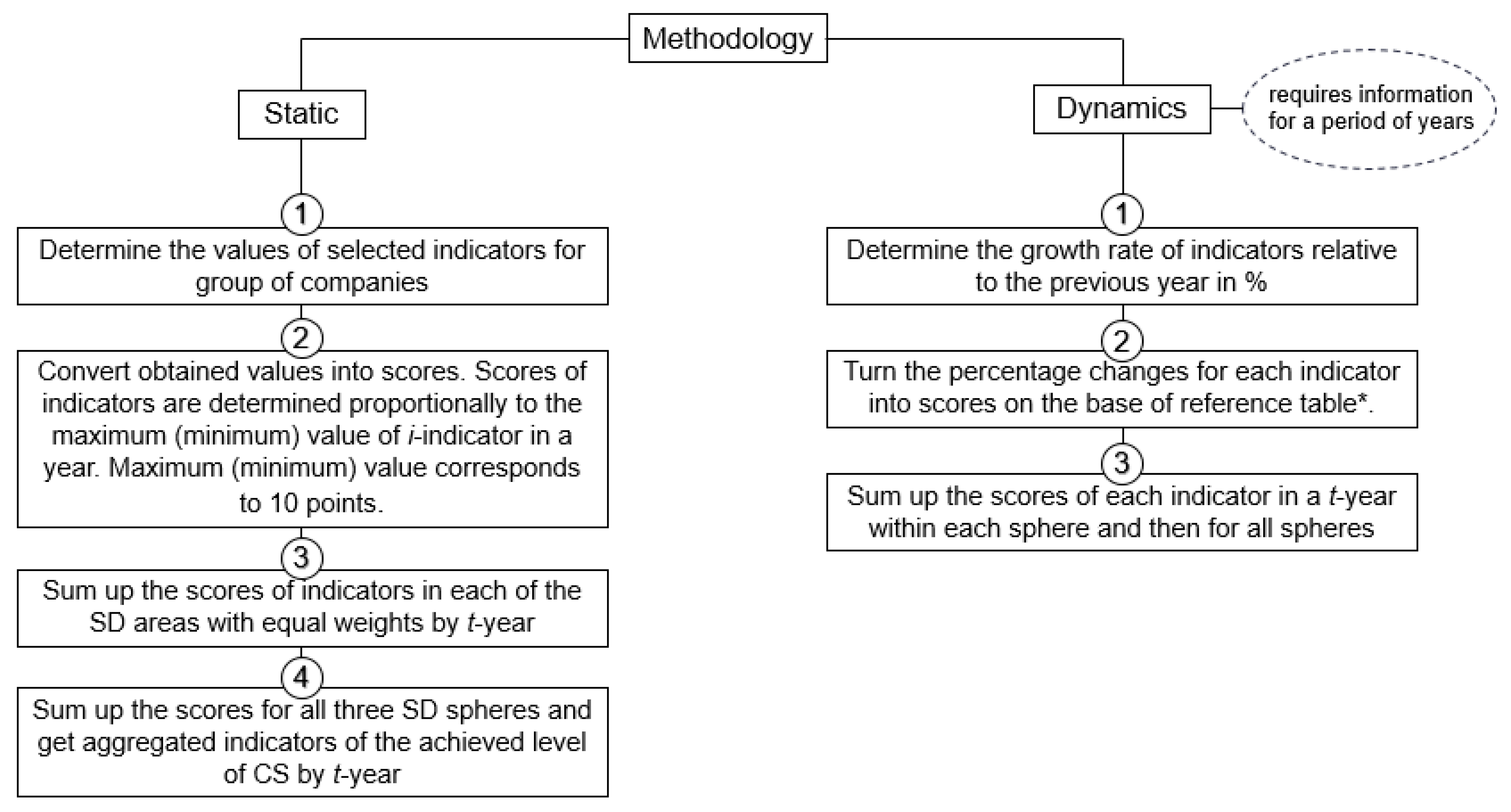

2. Methodology

- International methods for assessing CS and social performance

- Methods for assessing CS and social performance with the industry specifics

- Methods and approaches for assessing social performance

- Russian rating methods for assessing CS and social performance

- Individual researchers’ methods of assessing companies’ performance.

3. Results

- indicators that should be minimized: energy consumption per unit, water consumption, production waste, occupational injury frequency rate;

- indicators that should be maximized: average cost-to-revenue ratio, revenues, oil and gas reserve life, investment in environmental protection and costs associated with supporting local communities.

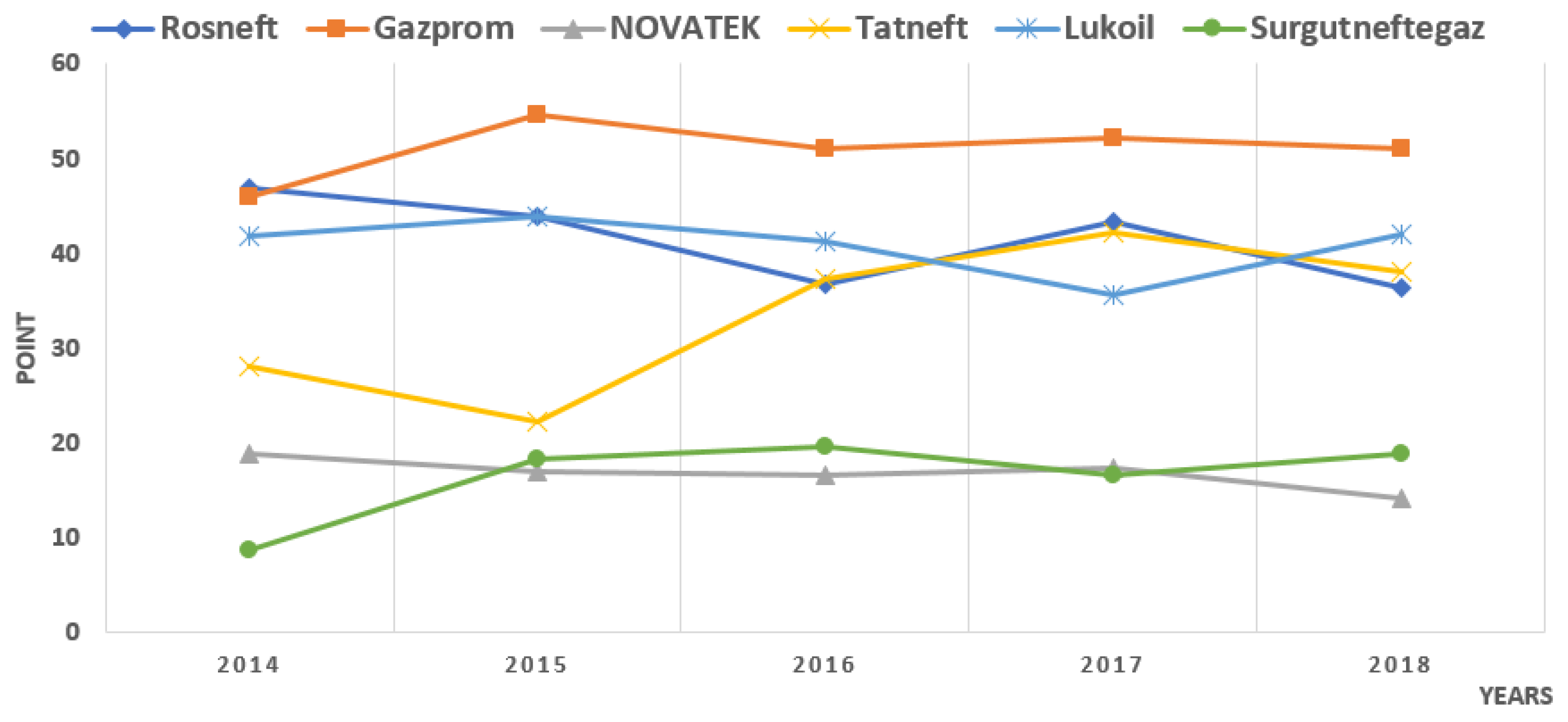

3.1. Calculating the Aggregate CS Index

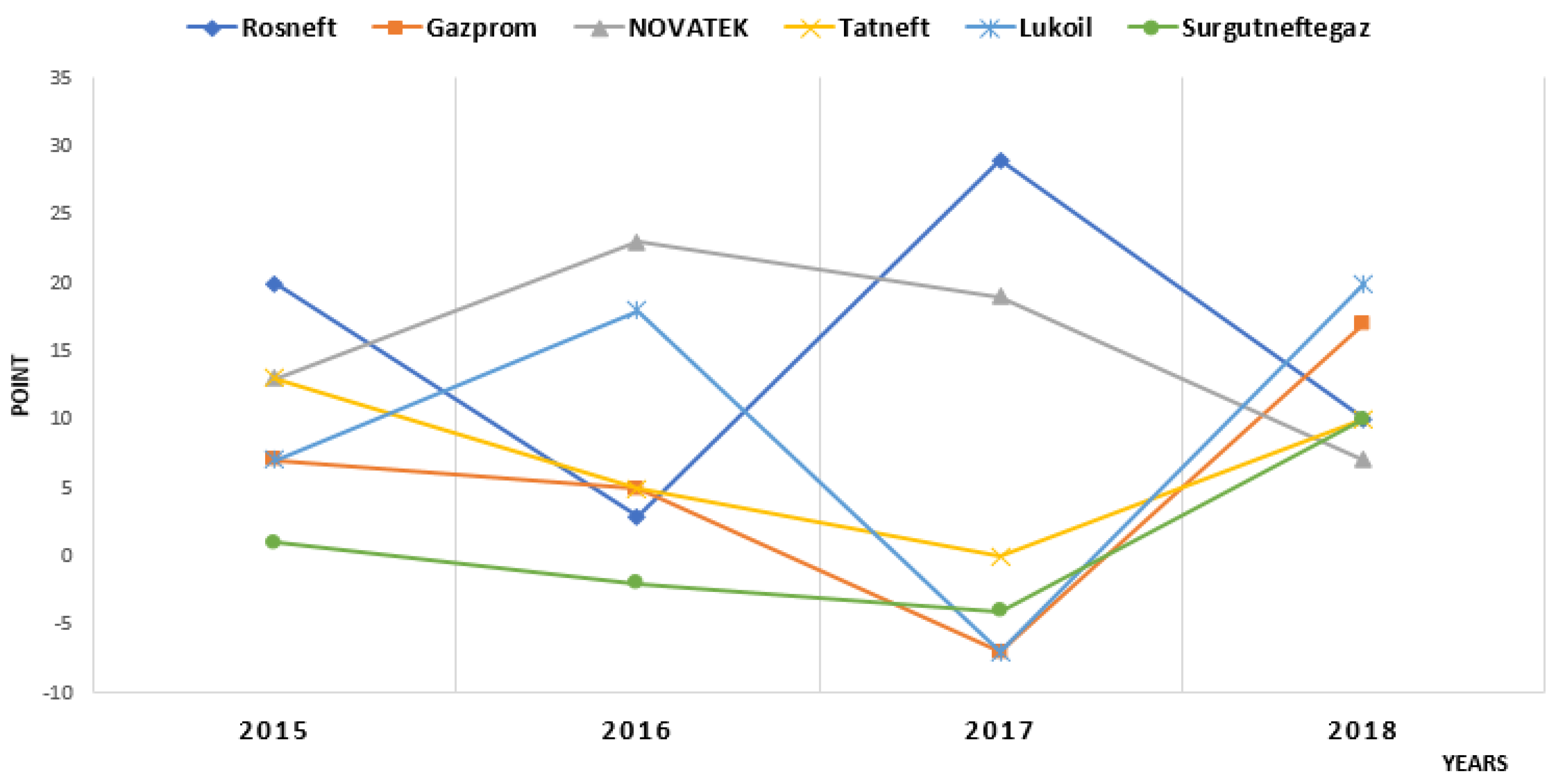

3.2. Assessment of Changes in Companies’ CS Indicators

- (1)

- PJSC Gazprom (2018-the level of CSR-41)

- (2)

- PJSC Lukoil (2018, the level of CSR-38)

- (3)

- PJSC NK Rosneft (2018-the level of CSR-32)

- (4)

- PJSC Tatneft (2018-the level of CSR-31)

- (5)

- PJSC Surgutneftegas (2018-the level of CSR-18)

- (6)

- PJSC NOVATEK (2018-the level of CSR-8)

4. Discussion

- By the area of research—the methods are aimed at study and assessment of corporate activity areas. Based on this criterion, there are methods focused on assessing environmental sustainability or social component of SD in the CSR system, methods of integrated (socio-environmental) assessment of CSR, integrated methods for assessing CSD combined with the analysis of environmental, social and economic components.

- By the objectives—the methods are aimed at monitoring of the situation in the areas of research; assessment of social and environmental results of projects or activities of the companies; making company ratings (comparative assessment).

- By applicable assessment criteria and indicators—the methods for making assessment criteria and indicators include: -quantitative indicators, for example, emissions in assessing environmental impact; cost performance indicators of companies; quantitative indicators for business areas of the company; quality indicators for assessing social and environmental effects; aggregate indicators (indices); score-rating indicators.

- By sources of information for CS assessment—secondary sources (open); primary sources (special surveys of companies); primary sources (special surveys for local communities).

- By rapid and detailed assessment of CS—rapid assessment generates an overall idea of socially responsible activities of the company confirmed by facts and non-financial reports and serves as an informational background for subsequent analysis, identification of potential risks and making informed decisions. The list of rapid assessment indicators includes the most important indicators characterizing social, economic and environmental role of the company.

5. Conclusions

- The main shortcomings of certain CS assessment methods are their static nature; lack of relation of social–environmental results to economic indicators characterizing a dynamic development of the company; lack of feedback from the companies; lack of count for industry specifics and differences in the level of disclosure and quality of information.

- For oil and gas companies, the set of CS indicators should include indicators reflecting business in harsh climatic conditions, increased injuries, generation of a large amount of various wastes, exploitation of mineral resources, vast economic impact of companies on the regional development, value of GDP and budgets.

- The method for CS assessment of mining companies is developed taking into account the stakeholder approach, institutional theory, the resource approach and the new theory of corporate sustainability.

- Analysis of CS indicators allows determining the place of CSR in the system of corporate values, identify the relations between CSR and corporate sustainability, explore the nature of relations with external stakeholders of mining companies and main directions of social programs, analyze the results achieved and the dynamics of the main performance indicators in CS. Comparing mining companies in terms of values and changes in CS indicators by industry reveals problems and creates incentives for further sustainable development of companies.

- The relevance of the study aimed at assessing corporate sustainable development in oil and gas companies operating stems from the fact that they have significant impact on the environment, the development of areas where they operate and the social landscape, which is accompanied by specific technological, macroeconomic and regulatory conditions for the development of oil and gas fields. Analysis of the integrated reporting showed that the volume of corporate social responsibility of mining companies is different and is characterized by different indicators that reflect the impact of companies on the society: impact on the social, environmental and economic sphere. In the voluntary reporting on sustainable development of the mining companies, CSR monitoring indicators are distributed in the following areas: participation in development, communities, human rights, environmental protection, economic impact, staff development, labor relations and management.

- Taking into account the purpose of this work to develop a methodology for assessing the CSR of oil and gas companies, the authors proposed the principles and method of assessment. The methodological principles are focused on the specifics of the industry and the long-term development of the company. The methodology contains indicators that allow to assess the impact in three areas (economy, ecology and environment) and characterize the prospects for long-term development of the company (by analyzing revenue, profitability and natural resource assets). The aggregate CS index is meant for ranking companies in relation to the best one in the industry. Assessment of changes in companies’ CS indicators determines the dynamics of indicators relative to previous periods for the company.

6. Patents

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Actual Figures | Points | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | PJSC NK Rosneft | PJSC Gazprom | PJSC NOVATEK | PJSC Tatneft | PJSC Lukoil | PJSC Surgutneftegas | PJSC NK Rosneft | PJSC Gazprom | PJSC NOVATEK | PJSC Tatneft | PJSC Lukoil | PJSC Surgutneftegas |

| Economic | ||||||||||||

| average product profitobility, % | ||||||||||||

| 2014 | 19.2 | 1.54 | 14.53 | 20.5 | 11.4 | - | 9.37 | 0.75 | 7.09 | 10 | 5.56 | 0 |

| 2015 | 23.8 | 5 | 10.6 | 19.1 | 9.7 | - | 10 | 2.1 | 4.45 | 8.03 | 4.08 | 0 |

| 2016 | 25 | 6 | 29.29 | 18.3 | 15 | 76 | 3.29 | 0.79 | 3.85 | 2.41 | 1.97 | 10 |

| 2017 | 22.6 | 4 | 16.23 | 18.2 | 8.1 | 16.6 | 10 | 1.77 | 7.18 | 8.05 | 3.58 | 7.35 |

| 2018 | 24.8 | 8 | 15.68 | 23.2 | 10.25 | 54.7 | 4.53 | 1.46 | 2.87 | 4.24 | 1.87 | 10 |

| revenue, billion rubles | ||||||||||||

| 2014 | 5503 | 5589.8 | 357.6 | 476.36 | 1710 | - | 9.84 | 10 | 0.64 | 0.85 | 3.06 | 0 |

| 2015 | 5150 | 6073.3 | 475.3 | 552.712 | 1877 | 1020.8 | 8.48 | 10 | 0.78 | 0.91 | 3.09 | 1.68 |

| 2016 | 4988 | 6111.1 | 537.5 | 580.127 | 5227 | 1002.6 | 8.16 | 10 | 0.88 | 0.95 | 8.55 | 1.64 |

| 2017 | 6011 | 6546.1 | 583 | 681.159 | 5936.7 | 1175 | 9.18 | 10 | 0.89 | 1.04 | 9.07 | 1.79 |

| 2018 | 8238 | 8224.2 | 832 | 910.534 | 8035.9 | 1556 | 10 | 9.98 | 1.01 | 1.11 | 9.75 | 1.89 |

| availability of mineral resources, years | ||||||||||||

| 2014 | 16.6 | 51.6 | 27.5 | 32 | 20.6 | 0 | 3.21 | 10 | 5.33 | 6.15 | 4 | 0 |

| 2015 | 18.2 | 49.6 | 24.6 | 32 | 18.9 | 0 | 3.67 | 10 | 4.96 | 6.45 | 3.81 | 0 |

| 2016 | 19.3 | 54.1 | 23.8 | 30.4 | 20.4 | 0 | 3.57 | 10 | 4.4 | 5.62 | 3.77 | 0 |

| 2017 | 19.4 | 49.5 | 29.4 | 30 | 19 | 0 | 3.92 | 10 | 5.94 | 6.06 | 3.84 | 0 |

| 2018 | 19.9 | 47.5 | 28.8 | 31.4 | 18.9 | 0 | 4.19 | 10 | 6.06 | 6.61 | 3.98 | 0 |

| Social | ||||||||||||

| frequency factor of industrial injuries | ||||||||||||

| 2014 | 0.33 | 0.18 | 0.4 | 0.1 | 0.13 | - | 3.03 | 5.56 | 2.5 | 10 | 7.69 | 0 |

| 2015 | 0.327 | 0.17 | 0.5 | 0.3 | 0.28 | - | 5.2 | 10 | 3.4 | 5.67 | 6.07 | 0 |

| 2016 | 0.21 | 0.16 | 0.3 | 0.14 | 0.21 | - | 6.67 | 8.75 | 4.67 | 10 | 6.67 | 0 |

| 2017 | 0.36 | 0.11 | 1.27 | 0.1 | 0.19 | - | 2.78 | 9.09 | 0.79 | 10 | 5.26 | 0 |

| 2018 | 0.41 | 0.17 | 0.79 | 0.14 | 0.19 | - | 3.41 | 8.24 | 1.77 | 10 | 7.37 | 0 |

| increased costs of local community support, million rubles | ||||||||||||

| 2014 | 8000 | 46,429 | 727 | 135.87 | 290.6 | - | 1.72 | 10 | 0.16 | 0.03 | 0.06 | 0 |

| 2015 | 9000 | 32,485 | 1000 | 165.7 | 304.9 | - | 2.77 | 10 | 0.31 | 0.05 | 0.09 | 0 |

| 2016 | 11,000 | 35,516 | 1324 | 195.65 | 304.3 | - | 3.1 | 10 | 0.37 | 0.06 | 0.09 | 0 |

| 2017 | 19,000 | 34,461 | 1377 | 281.64 | 341.9 | - | 5.51 | 10 | 0.4 | 0.08 | 0.1 | 0 |

| 2018 | 23,000 | 42,789 | 2000 | 257 | 384 | - | 5.38 | 10 | 0.47 | 0.06 | 0.09 | 0 |

| costs and investment into environmental protection, billion rubles | ||||||||||||

| 2014 | 36.93 | 48.98 | 0.63 | 5.8 | 59 | 18.58 | 6.26 | 8.3 | 0.11 | 0.98 | 10 | 3.15 |

| 2015 | 44.65 | 49.71 | 0.77 | 5.7 | 48 | 17.89 | 8.98 | 10 | 0.15 | 1.15 | 9.66 | 3.6 |

| 2016 | 47.14 | 57.47 | 1.19 | 13.29 | 53 | 17.73 | 8.2 | 10 | 0.21 | 2.31 | 9.22 | 3.09 |

| 2017 | 67.24 | 70.82 | 2.06 | 13.63 | 23 | 21.1 | 9.49 | 10 | 0.29 | 1.92 | 3.25 | 2.98 |

| 2018 | 45.61 | 68.96 | 2.4 | 11.68 | 58 | 17.4 | 6.61 | 10 | 0.35 | 1.69 | 8.41 | 2.52 |

| Environmental | ||||||||||||

| water consumption per unit of production/activity; m3/tons | ||||||||||||

| 2014 | 1.159 | 4.895 | 1.347 | - | 0.4 | 1.49 | 3.45 | 0.82 | 2.97 | 0 | 10 | 2.68 |

| 2015 | 1.467 | 4.511 | 1.716 | - | 0.5 | 1.63 | 3.41 | 1.11 | 2.91 | 0 | 10 | 3.07 |

| 2016 | 1.679 | 4.538 | 2.701 | 1.018 | 0.6 | 1.65 | 3.57 | 1.32 | 2.22 | 5.89 | 10 | 3.64 |

| 2017 | 2.26 | 4.523 | 2.779 | 1.005 | 0.5 | 1.418 | 2.21 | 1.11 | 1.8 | 4.98 | 10 | 3.53 |

| 2018 | 2.28 | 4.28 | 2.993 | 1.134 | 0.5 | 1.408 | 2.19 | 1.17 | 1.67 | 4.41 | 10 | 3.55 |

| mass of waste generated, thousand tons | ||||||||||||

| 2014 | 208 | 4831 | - | - | 1437 | 716.1 | 10 | 0.43 | 0 | 0 | 1.45 | 2.9 |

| 2015 | 5393 | 4954 | - | - | 1015 | 725.8 | 1.35 | 1.47 | 0 | 0 | 7.15 | 10 |

| 2016 | 5377 | 4289 | - | 92.7 | 1033 | 714 | 0.17 | 0.22 | 0 | 10 | 0.9 | 1.3 |

| 2017 | 6325 | 4130 | - | 80.1 | 1434 | 837.66 | 0.13 | 0.19 | 0 | 10 | 0.56 | 0.96 |

| 2018 | 7155 | 3555 | - | 78.6 | 1529 | 824.49 | 0.11 | 0.22 | 0 | 10 | 0.51 | 0.95 |

| Year | PJSC NK Rosneft | PJSC Gazprom | PJSC NOVATEK | PJSC Tatneft | PJSC Lukoil | PJSC Surgutneftegas |

|---|---|---|---|---|---|---|

| Economic | ||||||

| 2014 | 22.42 | 20.75 | 13.06 | 17 | 12.62 | 0 |

| 2015 | 22.15 | 22.1 | 10.19 | 15.9 | 10.98 | 1.68 |

| 2016 | 15.02 | 20.79 | 9.13 | 8.98 | 14.29 | 11.64 |

| 2017 | 23.1 | 21.77 | 14.01 | 15.15 | 16.49 | 9.14 |

| 2018 | 18.72 | 21.44 | 9.94 | 11.96 | 15.6 | 11.89 |

| Total | 101.41 | 106.85 | 56.33 | 68.48 | 69.98 | 34.35 |

| Social | ||||||

| 2014 | 11.01 | 23.86 | 2.76 | 11.01 | 17.75 | 3.15 |

| 2015 | 16.95 | 30 | 3.86 | 6.86 | 15.82 | 3.6 |

| 2016 | 17.97 | 28.75 | 5.25 | 12.37 | 15.97 | 3.09 |

| 2017 | 17.79 | 29.09 | 1.48 | 12.01 | 8.61 | 2.98 |

| 2018 | 15.4 | 28.24 | 2.59 | 11.75 | 15.87 | 2.52 |

| Total | 79.12 | 139.94 | 15.94 | 54 | 74.02 | 15.34 |

| Environmental | ||||||

| 2014 | 13.45 | 1.25 | 2.97 | 0 | 11.45 | 5.59 |

| 2015 | 4.75 | 2.57 | 2.91 | 0 | 17.15 | 13.07 |

| 2016 | 3.75 | 1.54 | 2.22 | 15.89 | 10.9 | 4.93 |

| 2017 | 2.34 | 1.3 | 1.8 | 14.98 | 10.56 | 4.48 |

| 2018 | 2.3 | 1.39 | 1.67 | 14.41 | 10.51 | 4.5 |

| Total | 26.59 | 8.05 | 11.57 | 45.28 | 60.57 | 32.57 |

| Actual Figures | Growth Rate (Points) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | Rosneft | Gazprom | NOVATEK | Tatneft | Lukoil | Surgutneftegaz | Rosneft | Gazprom | NOVATEK | Tatneft | Lukoil | Surgutneftegaz |

| Economic | ||||||||||||

| average product profitobility, % | ||||||||||||

| 2014 | 19.2 | 1.54 | 14.53 | 20.5 | 11.4 | - | - | - | - | - | - | - |

| 2015 | 23.8 | 5 | 10.6 | 19.1 | 9.7 | - | 0.24 | 2.25 | −0.27 | −0.07 | −0.15 | - |

| 2016 | 25 | 6 | 29.29 | 18.3 | 15 | 76 | 0.05 | 0.20 | 1.76 | −0.04 | 0.55 | - |

| 2017 | 22.6 | 4 | 16.23 | 18.2 | 8.1 | 16.6 | −0.10 | −0.33 | −0.45 | −0.01 | −0.46 | −0.78 |

| 2018 | 24.8 | 8 | 15.68 | 23.2 | 10.25 | 54.7 | 0.10 | 1.00 | −0.03 | 0.27 | 0.27 | 2.30 |

| revenue, billion rubles | ||||||||||||

| 2014 | 5503 | 5589.8 | 357.6 | 47.36 | 1710 | - | - | - | - | - | - | - |

| 2015 | 5150 | 6073.3 | 475.3 | 552.712 | 1877 | 1020.8 | −0.06 | 0.09 | 0.33 | 0.16 | 0.10 | - |

| 2016 | 4988 | 6111.1 | 537.5 | 580.127 | 5227 | 1002.6 | −0.03 | 0.01 | 0.13 | 0.05 | 1.78 | −0.02 |

| 2017 | 6011 | 6546.1 | 583 | 681.159 | 5936.7 | 1175 | 0.21 | 0.07 | 0.08 | 0.17 | 0.14 | 0.17 |

| 2018 | 8238 | 8224.2 | 832 | 910.534 | 8035.9 | 1556 | 0.37 | 0.26 | 0.43 | 0.34 | 0.35 | 0.32 |

| availability of mineral resources, years | ||||||||||||

| 2014 | 16.6 | 51.6 | 27.5 | 32 | 20.6 | 0 | - | - | - | - | - | - |

| 2015 | 18.2 | 49.6 | 24.6 | 32 | 18.9 | 0 | 0.10 | −0.04 | −0.11 | 0.00 | −0.08 | - |

| 2016 | 19.3 | 54.1 | 23.8 | 30.4 | 20.4 | 0 | 0.06 | 0.09 | −0.03 | −0.05 | 0.08 | - |

| 2017 | 19.4 | 49.5 | 29.4 | 30 | 19 | 0 | 0.01 | −0.09 | 0.24 | −0.01 | −0.07 | - |

| 2018 | 19.9 | 47.5 | 28.8 | 31.4 | 18.9 | 0 | 0.03 | −0.04 | −0.02 | 0.05 | −0.01 | - |

| Social | ||||||||||||

| frequency factor of industrial injuries | ||||||||||||

| 2014 | 0.33 | 0.18 | 0.4 | 0.1 | 0.13 | - | - | - | - | - | - | - |

| 2015 | 0.327 | 0.17 | 0.5 | 0.3 | 0.28 | - | −0.01 | −0.06 | 0.25 | 2.00 | 1.15 | - |

| 2016 | 0.21 | 0.16 | 0.3 | 0.14 | 0.21 | - | −0.36 | −0.06 | −0.40 | −0.53 | −0.25 | - |

| 2017 | 0.36 | 0.11 | 1.27 | 0.1 | 0.19 | - | 0.71 | −0.31 | 3.23 | −0.29 | −0.10 | - |

| 2018 | 0.41 | 0.17 | 0.79 | 0.14 | 0.19 | - | 0.14 | 0.55 | −0.38 | 0.40 | 0.00 | - |

| increased costs of local community support, million rubles | ||||||||||||

| 2014 | 8000 | 46,429 | 727 | 135.87 | 290.6 | - | - | - | - | - | - | - |

| 2015 | 9000 | 32,485 | 1000 | 165.7 | 304.9 | - | 0.13 | −0.30 | 0.38 | 0.22 | 0.05 | - |

| 2016 | 11,000 | 35,516 | 1324 | 195.65 | 304.3 | - | 0.22 | 0.09 | 0.32 | 0.18 | 0.00 | - |

| 2017 | 19,000 | 34,461 | 1377 | 281.64 | 341.9 | - | 0.73 | −0.03 | 0.04 | 0.44 | 0.12 | - |

| 2018 | 23,000 | 42,789 | 2000 | 257 | 384 | - | 0.21 | 0.24 | 0.45 | −0.09 | 0.12 | - |

| costs and investment into environmental protection, billion rubles | ||||||||||||

| 2014 | 36.93 | 48.98 | 0.63 | 5.8 | 59 | 18.58 | - | - | - | - | - | - |

| 2015 | 44.65 | 49.71 | 0.77 | 5.7 | 48 | 17.89 | 0.21 | 0.01 | 0.22 | −0.2 | −0.19 | −0.04 |

| 2016 | 47.14 | 57.47 | 1.19 | 13.29 | 53 | 17.73 | 0.06 | 0.16 | 0.55 | 1.33 | 0.10 | −0.01 |

| 2017 | 67.24 | 70.82 | 2.06 | 13.63 | 23 | 21.1 | 0.43 | 0.23 | 0.73 | 0.03 | −0.57 | 0.19 |

| 2018 | 45.61 | 68.96 | 2.4 | 11.68 | 58 | 17.4 | −0.32 | −0.03 | 0.17 | −0.14 | 1.52 | −0.18 |

| Environmental | ||||||||||||

| water consumption per unit of production/activity; m3/tons | ||||||||||||

| 2014 | 1.159 | 4.895 | 1.347 | - | 0.4 | 1.49 | - | - | - | - | - | - |

| 2015 | 1.467 | 4.511 | 1.716 | - | 0.5 | 1.63 | 0.27 | −0.08 | 0.27 | - | 0.25 | 0.09 |

| 2016 | 1.679 | 4.538 | 2.701 | 1.018 | 0.6 | 1.65 | 0.14 | 0.01 | 0.57 | - | 0.20 | 0.01 |

| 2017 | 2.26 | 4.523 | 2.779 | 1.005 | 0.5 | 1.418 | 0.35 | 0.00 | 0.03 | −0.01 | −0.17 | −0.14 |

| 2018 | 2.28 | 4.28 | 2.993 | 1.134 | 0.5 | 1.408 | 0.01 | −0.05 | 0.08 | 0.13 | 0.00 | −0.01 |

| mass of waste generated, thousand tons | ||||||||||||

| 2014 | 208 | 4831 | - | - | 1437 | 716.1 | - | - | - | - | - | - |

| 2015 | 5393 | 4954 | - | - | 1015 | 725.8 | 24.93 | 0.03 | - | - | −0.29 | 0.01 |

| 2016 | 5377 | 4289 | - | 92.7 | 1033 | 714 | 0.00 | −0.13 | - | - | 0.02 | −0.02 |

| 2017 | 6325 | 4130 | - | 80.1 | 1434 | 837.66 | 0.18 | −0.04 | - | −0.14 | 0.39 | 0.17 |

| 2018 | 7155 | 3555 | - | 78.6 | 1529 | 824.49 | 0.13 | −0.14 | - | −0.02 | 0.07 | −0.02 |

References

- A Guide. 2012. A Guide to Social Return on Investment. Available online: http://www.socialvalueuk.org/app/uploads/2016/03/The%20Guide%20to%20Social%20Return%20on%20Investment%202015.pdf (accessed on 28 June 2020).

- Berman, Shawn, Andrew C. Wicks, Suresh Kotha, and Thomas M. Jones. 1999. Does stakeholder orientation matter? The relationship between stakeholder management models and firm performance. Academy of Management Journal 42: 488–506. [Google Scholar]

- Blagov, Yu E. 2011. Corporate Social Responsibility: The Evolution of the Concept, 2nd ed. Saint Petersburg: Higher School of Management Publishing House. 272p. [Google Scholar]

- Borzakov, D. V. 2016. Control and Assessment of Corporate Social Responsibility in the Management of Organizations. Ph.D. dissertation, Voronezh South-West State University, Voronezh, Russia. [Google Scholar]

- Carayannis, Elias G., Alina Ilinova, and Alexey Cherepovitsyn. 2021. The Future of Energy and the Case of the Arctic Offshore: The Role of Strategic Management. Journal of Marine Science and Engineering 9: 134. [Google Scholar] [CrossRef]

- CDP. 2015. Climate Change. Information Request. Available online: https://www.cpr.ca/en/about-cp-site/Documents/cdp-program-submission-2015.pdf (accessed on 28 June 2020).

- Cherepovitsyn, Aleksey E., Svetlana A. Lipina, and Olga O. Evseeva. 2018. Innovative approach to the development of mineral raw materials of the arctic zone of the Russian federation. Journal of Mining Institute 232: 438. [Google Scholar]

- Corporate. 2018. Corporate Sustainability Assessment & Corporate Public Reporting Annelies Poolman. Available online: https://zebra-group.ru/download/ru/news/news-70/news-image-id-70-content-1.pdf (accessed on 7 March 2021).

- Dowling Grahame. 2013. The Curious Case of Corporate Tax Avoidance: Is it Socially Irresponsible? Journal of Business Ethics 124: 173–84. [Google Scholar]

- Drucker, Peter F. 1984. The new meaning of corporate social responsibility. California Management Review 26: 53–63. [Google Scholar] [CrossRef]

- Emerson, Jed, Jay Wachowicz, and Suzi Chun. 2000. Social Return Social Return on Investment: On Investment. Exploring Exploring Aspects of Aspects of Value Creation Value Creation in the Nonprofit in the Nonprofit Sector. Available online: https://hbswk.hbs.edu/archive/social-return-on-investment-sroi-exploring-aspects-of-value-creation (accessed on 28 June 2020).

- Endovickij, D. A., I. V. Panina, and M. V. Ponkratova. 2017. Analiz sushchnosti korporativnoj ustojchivosti kak reakcii na civilizacionnye izmeneniya. Ekonomicheskij Analiz: Teoriya i Praktika 16: 1043–60. [Google Scholar]

- Endovitsky, D. A., L. M. Nikitina, and D. V. Borzakov. 2014. Assessment of corporate social responsibility of Russian companies based on a comprehensive analysis of non-financial reporting. Economic Analysis: Theory and Practice 8: 2–10. [Google Scholar]

- Epstein, Marc J., and Marie-Jose Roy. 2003. Making the business case for sustainability. Linking social and environmental actions to financial performance. Journal of Corporate Citizenship 9: 79–96. [Google Scholar] [CrossRef]

- ESG. 2019. Expert Views on ESG Ratings. Available online: https://sustainability.com/our-work/reports/rate-raters-2019 (accessed on 7 March 2021).

- ESG Factors in Investment, MIRBIS. 2019. Available online: https://www.pwc.ru/ru/sustainability/assets/pwc-responsible-investment.pdf (accessed on 7 March 2021).

- ESG Rating. 2020. Available online: https://www.msci.com/esg-ratings (accessed on 28 June 2020).

- Freeman, Edward. 1984. Stakeholder Management: A Stakeholder Approach. Marshfield: Pitman Publishing, p. 292. [Google Scholar]

- Global. 2014. Global Competitiveness Report 2013–2014. Available online: http://www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2013-14.pdf (accessed on 28 June 2020).

- GOST R 54598.1. 2015. Management of Sustainable Development. Part 1. Guide 2016. Available online: http://docs.cntd.ru/document/1200127235 (accessed on 28 June 2020).

- GOST R ISO 20121. 2014. Systems of Management of a Sustainable Development. Requirements and Practical Guidance on Management of Stability of Events. Available online: http://docs.cntd.ru/document/1200113801 (accessed on 28 June 2020).

- GOST R ISO 9004. 2010. Managing for the Sustained Success of an Organization. A Quality Management Approach. Available online: http://docs.cntd.ru/document/gost-r-iso-9004-2010 (accessed on 28 June 2020).

- Halme, Minna, and Juha Laurila. 2009. Philanthropy, integration or innovation? Exploring the financial and societal outcomes of different types of corporate responsibility. Journal of Business Ethics 84: 325–39. [Google Scholar] [CrossRef]

- Ilinova, A., A. Chanysheva, and V. Solovyova. 2020. Arctic oil and gas offshore projects: How to forecast their future. Paper presented at IOP Conference Series: Earth and Environmental Science, St. Petersburg, Russia, March 18–19. [Google Scholar]

- International Integrated Reporting Council (‘IIRC’). 2021. Available online: https://integratedreporting.org/wp-content/uploads/2021/01/InternationalIntegratedReportingFramework.pdf (accessed on 7 March 2021).

- ISS-oekom. 2019. Corporate Rating. Available online: https://www.aiib.org/en/treasury/_common/_download/oekomCompanyReport_2019-5-3.pdf (accessed on 28 June 2020).

- Ivanova, D. 2020. Risk management and its contribution to sustainable development of mining enterprises. Scientific and Practical Studies of Raw Material Issues 2020: 182–91. [Google Scholar]

- Ivashkovskaya, I. V. 2009. Modelirovanie Stoimosti Kompanii. In Strategicheskaya Otvetstvennost’ Sovetov Direktorov. Moscow: INFRA-M. [Google Scholar]

- Johnson, H. 2003. Does it pay to be good? Social responsibility and financial performance. Business Horizons 46: 34–40. [Google Scholar] [CrossRef]

- Kanaeva, O. A. 2018. Social’nye imperativy ustojchivogo razvitiya. Vestnik SPbGU. Ekonomika 34: 26–58. [Google Scholar]

- Kirsanova, Natalia, Olga Lenkovets, and Muhammad Hafeez. 2020. Issue of Accumulation and Redistribution of Oil and Gas Rental Income in the Context of Exhaustible Natural Resources in Arctic Zone of Russian Federation. Journal of Marine Science and Engineering 8: 1006. [Google Scholar] [CrossRef]

- Klimova, Nina I., Dina Kh Krasnoselskaya, and Dilya R. Khamzina. 2018. An empirical study on the relationships between sales revenue of oil company and industry specific and exogenous characteristics. Journal of Applied Economic Sciences 8: 2261–68. [Google Scholar]

- Larsena, Sanne Vammen, Anne Merrild Hansen, and Helle Nedergaard Nielsen. 2018. The role of EIA and weak assessments of social impacts in conflicts over implementation of renewable energy policies. Energy Policy 115: 43–53. [Google Scholar] [CrossRef]

- LBG Model. 2017. The LBG Model—A GLOBAL VALUE Tool Showcase. Technical Report. Available online: https://www.researchgate.net/publication/323935384_The_LBG_Model_-_a_GLOBAL_VALUE_tool_showcase (accessed on 28 June 2020).

- Leadership GRI SRS. 2013. Available online: https://www.globalreporting.org/standards/gri-standards-download-center/consolidated-set-of-gri-standards/ (accessed on 7 March 2021).

- Lingane, Alison, and Sara Olsen. 2004. Guidelines for social return on investment. California Management Review 46: 116–35. [Google Scholar] [CrossRef]

- Lipina, Svetlana A., Lina K. Bocharova, and Lyubov A. Belyaevskaya-Plotnik. 2018. Analysis of Government Support Tools for Mining Companies in the Russian Arctic Zone. Zapiski Gornogo Instituta 230: 217–22. [Google Scholar] [CrossRef]

- Litvinenko, Vladimir S., Pavel S. Tsvetkov, Mikhail V. Dvoynikov, and Georgii V. Buslaev. 2020. Barriers to implementation of hydrogen initi-atives in the context of global energy sustainable development. Journal of Mining Institute 244: 428–38. [Google Scholar] [CrossRef]

- Manning, Matthew, Shane D. Johnson, Nick Tilley, Gabriel T. W. Wong, and Margarita Vorsina. 2016. Cost-Benefit Analysis (CBA) Economic Analysis and Efficiency in Policing, Criminal Justice and Crime Reduction: What Works? Berlin/Heidelberg: Springer, pp. 35–50. [Google Scholar]

- Margolis, Joshua D., and James P. Walsh. 2003. Misery Loves Companies: Rethinking Social Initiatives by Business. Administrative Science Quarterly 48: 268–305. [Google Scholar] [CrossRef]

- Montiel, Ivan, and Javier Delgado-Ceballos. 2014. Defining and Measuring Corporate Sustainability: Are We There Yet? Organization and Environment 27: 113–39. [Google Scholar] [CrossRef]

- National Register. 2020. National Register of Corporate Non-Financial Reports. Available online: https://рспп.рф/activity/social/registr/ (accessed on 7 March 2021).

- Nedosekin, Aleksei O., Elena I. Rejshahrit, and Aleksandr N. Kozlovskiy. 2019. Strategic Approach to Assessing Economic Sustainability Objects of Mineral Resources Sector of Russia. Journal of Mining Institute 237: 354–60. [Google Scholar] [CrossRef]

- Novikova, Natalya. 2020. Pipeline Neighbors: How Can We Avoid Conflicts? Resources 9: 13. [Google Scholar] [CrossRef]

- Pence, I. Sh, and S. A. Furs. 2008. Corporate Governance in Modern Russian Industry: State and Factors of Improvement. Moscow: LLC “Nedra Communications Ltd.”, p. 120. [Google Scholar]

- Ponomarenko, Tatyana, Marina Nevskaya, and Oksana Marinina. 2020. An Assessment of the Applicability of Sustainability Measurement Tools to Resource-Based Economies of the Commonwealth of Independent States. Sustainability 12: 5582. [Google Scholar] [CrossRef]

- Prokopov, F., and E. Feoktistova. 2008. Bazovye Indikatory Rezul’tativnosti. Rekomendacii po Ispol’zovaniyu v Praktike Upravleniya i -Korporativnoj Nefinansovoj Otchetnosti. Moscow: RSPP. 68p. [Google Scholar]

- Rahdari, Amir Hossein, and Ali Asghar Anvary Rostamy. 2015. Designing a general set of sustainability indicators at the corporate level. Journal of Cleaner Production 108: 757–71. [Google Scholar] [CrossRef]

- Rate the Raters. 2020. Investor Survey and Interview Results. Available online: https://sustainability.com/wp-content/uploads/2020/03/sustainability-ratetheraters2020-report.pdf (accessed on 7 March 2021).

- RepRisk Provides ESG. 2014. Intelligence for Dow Jones Sustainability Indices. Institutional Asset Manager. Available online: https://www.businesswire.com/news/home/20140910005040/en/RepRisk-ESG-Intelligence-Dow-Jones-Sustainability-Indices (accessed on 28 June 2020).

- Rudakov, Marat, Elena Gridina, and Jürgen Kretschmann. 2021. Kretschmann, Risk-based thinking as a basis for efficient occupational safety management in the mining industry. Sustainability 13: 470. [Google Scholar] [CrossRef]

- Saprykina, O. A. 2012. Multilevel assessment of the company’s performance in the field of corporate social responsibility. Transport business in Russia. Management 5: 74–78. [Google Scholar]

- Sklyar, E. N., and I. O. Zverkovich. 2007. Metodicheskie aspekty upravleniya razvitiem sotsialnogo potentsiala promyshlennyh predpriyatiy. Creative Economy 1: 74–81. [Google Scholar]

- Smol, Marzena, Paulina Marcinek, Joanna Duda, and Dominika Szołdrowska. 2020. Importance of Sustainable Mineral Resource Management in Implementing the Circular Economy (CE) Model and the European Green Deal Strategy. Resource 9: 55. [Google Scholar] [CrossRef]

- Szewrański, Szymon, and Jan K. Kazak. 2020. Socio-Environmental Vulnerability Assessment for Sustainable Management. Sustainability 12: 7906. [Google Scholar] [CrossRef]

- Tulaeva, Svetlana A., Maria S. Tysiachniouk, Laura A. Henry, and Leah S. Horowitz. 2019. Horowitz. Globalizing Extraction and Indigenous Rights in the Russian Arctic: The Enduring Role of the State in Natural Resource Governance. Resources 8: 179. [Google Scholar] [CrossRef]

- Vasilev, Yurii, Polina Vasileva, and Anna Tsvetkova. 2019. International review of public perception of ccs technologies. Paper presented at 19th International Multidisciplinary Scientific GeoConference SGEM, Albena, Bulgaria, June 28–July 7, vol. 19, pp. 415–22. [Google Scholar] [CrossRef]

- WBCSD. 2017. Measuring Impact Framework. Available online: https://www.wbcsd.org/Programs/People/Social-Impact/Resources/WBCSD-Measuring-Impact (accessed on 28 June 2020).

- Wells, Louis T., Jr. 1975. Social Cost/Benefit Analysis for MNCs, Harvard Business Review. Available online: https://hbr.org/1975/03/social-costbenefit-analysis-for-mncs (accessed on 28 June 2020).

- Wong, Christina, Aiste Brackley, and Erika Petroy. 2019. Rate the Raters 2019: Expert Views on ESG Ratings February. Available online: https://www.sustainability.com/globalassets/sustainability.com/thinking/pdfs/sa-ratetheraters-2019-1.pdf (accessed on 7 March 2021).

| Attributes | Stakeholder Theory | Corporate Social Performance | Corporate Citizenship |

|---|---|---|---|

| Object | The relationships between the company and its key stakeholders | The company’s activities in relation to its stakeholders | The relationship between the company and society |

| Essence | Identifying and taking into account the interests of parties involved, i.e., those who can influence the company’s activities or be influenced by the side effects of the company’s main activities | The company’s ability to understand its impact on society and respond to the needs of stakeholders in the economic, social and environmental spheres | An integrated approach that includes not only legal rights and obligations but also additional responsibilities that lie beyond the company’s boundaries and exist in the economic, social and environmental dimensions |

| Principles | The corporation is involved in resource mobilization in order to create well-being for its stakeholders and competitive advantages for itself | The underlying links between the principles of corporate social responsibility, corporate social performance and corporate strategy: 1. risk minimization, 2. profit maximization, 3. accountability to and responsibility for stakeholders | Companies take the position of a social institution and, having become a “good corporate citizen”, share a number of social functions with the government. They contribute to sustainable development at the regional or even global level. |

| Implementation methods | It is not required to meet the social interests of all the company’s stakeholders. The management should not pay too much attention to minor stakeholders who cannot influence the company’s sustainability in the mid-term | Three strategies of stakeholder communication: information strategy, response strategy and involvement strategy | Identification of socially anchored competences, elimination of contradictions between the interests of the company and society in terms of social, environmental, ethical and economic aspects |

| Principal authors | Freeman R.E., S. Ramakrishna Velamuri, Brian Moriarty, Preston L., Post J. | Sethi S. P., Wood D.J., Carroll A. B. | Logsdon J.M., Wood D.J., Carroll A. B., Matten D., Crane A., Chapple W. |

| Kinds of Methodologies | Methods |

|---|---|

| Russian methodologies (ratings) for assessing CS and social performance | Basic indicators of RSPP (Methodology of the Russian Union of Industrialists and Entrepreneurs) |

| RSPP indices (Interfax-Era methodology) | |

| CCI Social Reporting Standard (Chamber of Commerce and Industry) | |

| Fundamental efficiency ratings (compiled by the environmental and energy rating agency Interfax-ERA) | |

| Methodology for assessing energy efficiency class from E to A ++ (RERA) (RUSSIAN ENERGY RATING AGENCY) | |

| Russian Regional Network for Integrated Reporting (RRS) | |

| Employer Attractiveness Rating NRA (National Rating Agency) | |

| International methodologies for assessing CS and social performance | Dow Jones Sustainability Index (мeтoдoлoгия RobecoSam). |

| FTSE4GOOD | |

| Global 100 Index methodology. | |

| Global Reporting Initiative (GRI) methodology. | |

| Bloomberg ESG Index methology. | |

| DEA (Data Envelopment Analysis) | |

| KLD (Kinder, Lydenberg and Domini) | |

| Econometric Impact Index (economic benefit index) proposed by Smith O‘Brien. | |

| Carbon Disclosure Project (CDP) (carbon reporting and performance leaders: Carbon Disclosure Leadership Index, CDLI; Carbon Performance Leadership Index, CPLI) | |

| Methodologies for assessing CS and social performance with industry specifics | Oil and Gas Industry Guidance on Voluntary Sustainability Reporting. IPIECA/API (in the field of oil, gas production) |

| Rating agency Tomorrow’s Value Rating (TVR) (oil, gas) | |

| Equitable Origin has released the EO100 Standard (in the field of oil, gas) | |

| Rating of openness of oil and gas companies in the field of environmental responsibility (organized by KREON Group) | |

| Rating of the openness of mining and metallurgical companies in Russia in the field of environmental responsibility | |

| Methodologies and approaches for assessing social performance: | SIA (Social Impact Assessment), |

| SRA (Social Return Assessment), | |

| SCBA (Social Costs-Benefit Analysis), | |

| SVA (Stakeholder Value Added) | |

| Total Impact Measurement and Management (PWC-developer, approach to assessing the impact of business on the economy, society and the environment, as well as the tax contribution of the company) | |

| Coalition for Environmentally Responsible Economies (CERES) | |

| Institute for Social and Ethical Responsibility (ISEA) | |

| Social Reporting Standards | AA1000 KCO Institute of Social and Ethical Accountability |

| SA8000 Social Accountability International | |

| Social Responsibility Guide ISO 26000 | |

| Methodologies of Russian researchers for assessing performance (more than 100) | Borzakov; Skliar E., Zverkovich I.; Penc I., Saprikina O.; D. A. Endovitsky, Ponomarenko T.V., Marinina O.A. etc. |

| Sphere/Indicator | Information Source | Desired Trend |

|---|---|---|

| Social sphere | ||

| - occupational injury frequency rate | CSR and SD reports | →min |

| - growth in costs associated with supporting local communities, RUB USD, EUR) billion | CSR and SD reports | →max |

| - environmental protection costs, RUB (USD, EUR) billion | CSR and SD reports | →max |

| Environmental sphere | ||

| - energy consumption per unit, RUB/RUB; RUB/t ($, €) | CSR and SD reports | →min |

| - water consumption per unit, m3/t; m3/RUB ($, €) | CSR and SD reports | →min |

| - production waste, million tons | CSR and SD reports | →min |

| Economic sphere | ||

| - average cost-to-revenue ratio | Annual report | →max |

| - revenues, RUB billion (USD, EUR) | Financial report | →max |

| - oil and gas reserve life, years | Annual report | →max |

| Percentage change | 1–10 | 11–20 | 21–30 | 31–40 | 41–50 | 51–60 | 61–70 | 71–80 | 81–90 | 91–100 |

| Point ) | 1 (−1) | 2 (−2) | 3 (−3) | 4 (−4) | 5 (−5) | 6 (−6) | 7 (−7) | 8 (−8) | 9 (−9) | 10 (−10) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ponomarenko, T.; Marinina, O.; Nevskaya, M.; Kuryakova, K. Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies. Economies 2021, 9, 58. https://doi.org/10.3390/economies9020058

Ponomarenko T, Marinina O, Nevskaya M, Kuryakova K. Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies. Economies. 2021; 9(2):58. https://doi.org/10.3390/economies9020058

Chicago/Turabian StylePonomarenko, Tatyana, Oksana Marinina, Marina Nevskaya, and Kristina Kuryakova. 2021. "Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies" Economies 9, no. 2: 58. https://doi.org/10.3390/economies9020058

APA StylePonomarenko, T., Marinina, O., Nevskaya, M., & Kuryakova, K. (2021). Developing Corporate Sustainability Assessment Methods for Oil and Gas Companies. Economies, 9(2), 58. https://doi.org/10.3390/economies9020058