Integrating ESG into Corporate Strategy: Unveiling the Moderating Effect of Digital Transformation on Green Innovation through Employee Insights

Abstract

1. Introduction

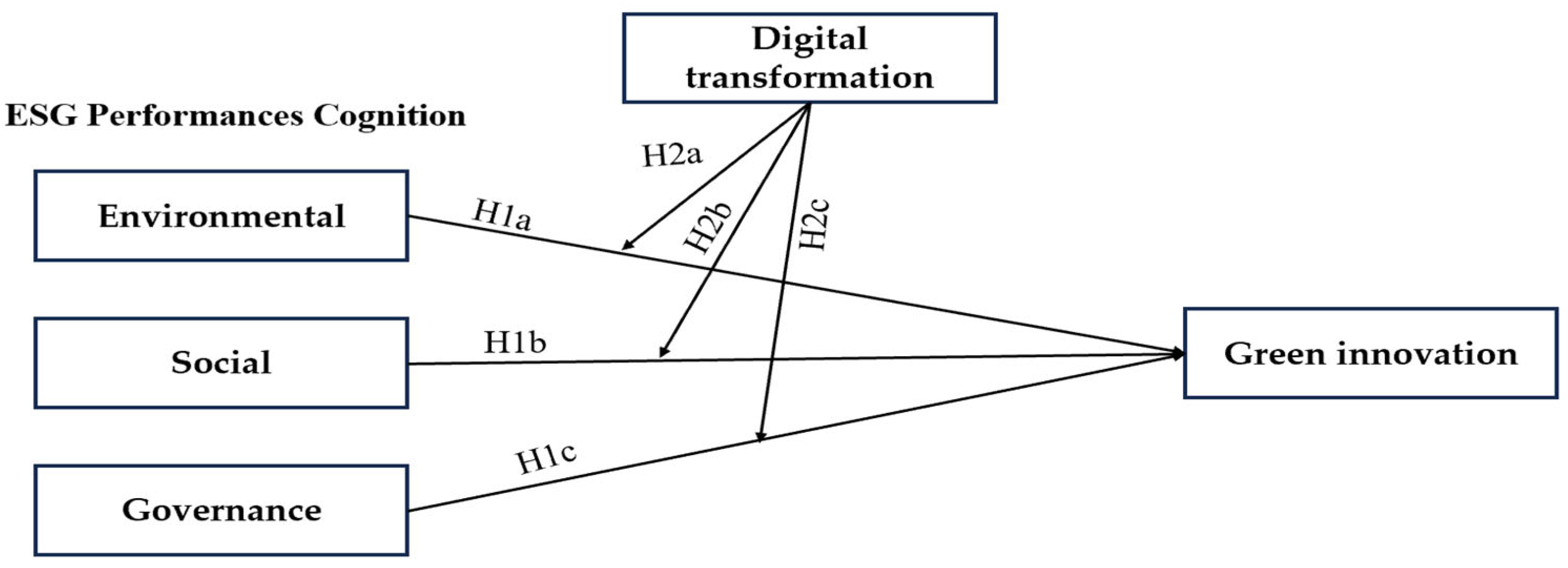

2. Theoretical Background and Hypothesis

2.1. ESG

2.2. Digital Transformation

2.3. ESG and Green Innovation

2.4. The Moderating Effect of DT

3. Methods

3.1. Sample and Data Collection

3.2. Measurement of Variables

4. Results

4.1. Measurement Reliability and Validity Assessment

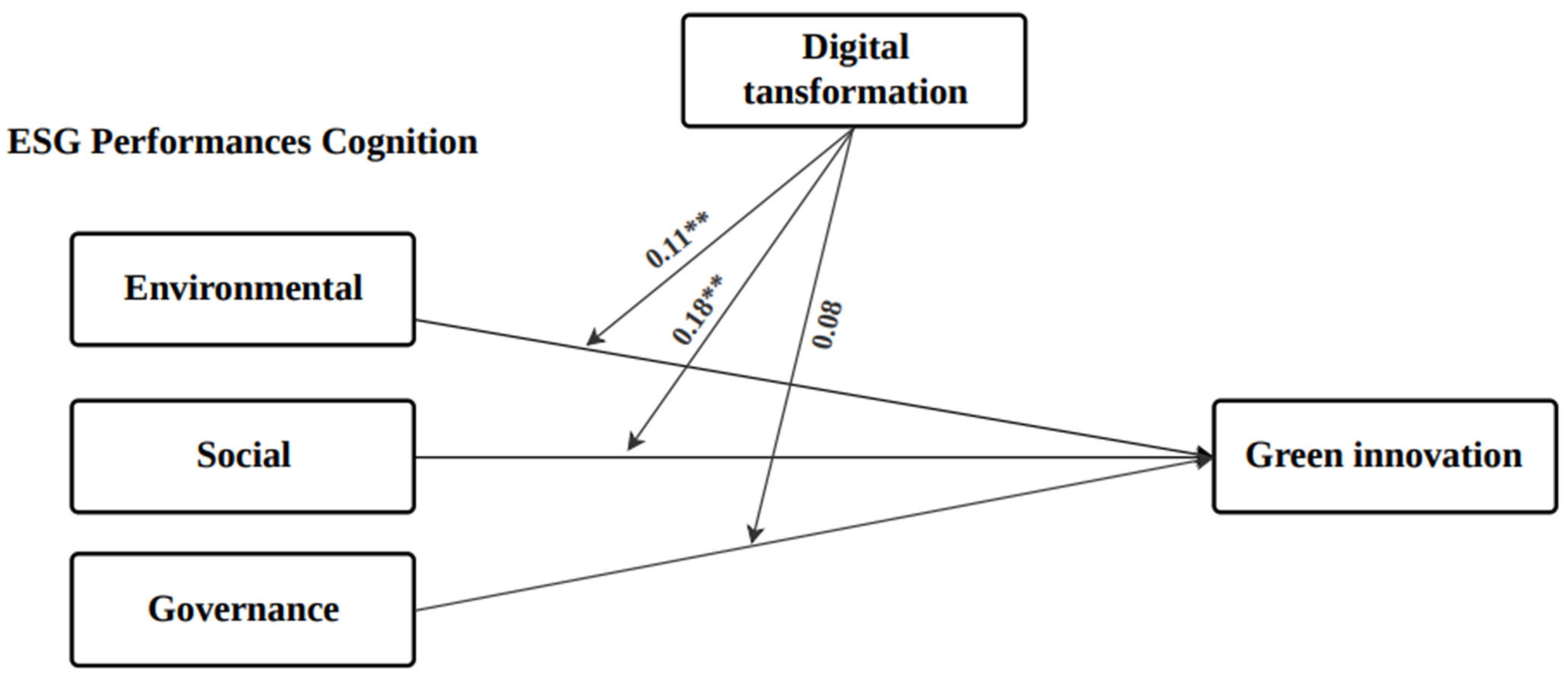

4.2. Hypothesis Testing

5. Discussion

5.1. Theoretical and Practical Implications

5.2. Limitations

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Lin, B.; Ma, R. Green technology innovations, urban innovation environment and CO2 emission reduction in China: Fresh evidence from a partially linear functional-coefficient panel model. Technol. Forecast. Soc. Chang. 2022, 176, 121434. [Google Scholar] [CrossRef]

- Adedoyin, F.F.; Satrovic, E.; Kehinde, M.N. The anthropogenic consequences of energy consumption in the presence of uncertainties and complexities: Evidence from World Bank income clusters. Environ. Sci. Pollut. Res. 2022, 29, 23264–23279. [Google Scholar] [CrossRef]

- Awan, A.G. Relationship between environment and sustainable economic development: A theoretical approach to environmental problems. Int. J. Asian Soc. Sci. 2013, 3, 741–761. [Google Scholar]

- Chopra, S.S.; Senadheera, S.S.; Dissanayake, P.D.; Withana, P.A.; Chib, R.; Rhee, J.H.; Ok, Y.S. Navigating the Challenges of Environmental, Social, and Governance (ESG) Reporting: The Path to Broader Sustainable Development. Sustainability 2024, 16, 606. [Google Scholar] [CrossRef]

- Thao, V.T.T.; Tien, N.H.; Anh, D.B.H. Sustainability Issues in Social Model of Coporate Social Responsibility Theoretical Analysis and Practical Implication. J. Adv. Res. Manag. 2019, 10, 17–29. [Google Scholar]

- Steyn, B.; Niemann, L. Strategic role of public relations in enterprise strategy, governance and sustainability—A normative framework. Public Relat. Rev. 2014, 40, 171–183. [Google Scholar] [CrossRef]

- Hoang, T.G.; Nguyen, G.N.T.; Le, D.A. Developments in financial technologies for achieving the Sustainable Development Goals (SDGs): FinTech and SDGs. In Disruptive Technologies and Eco-Innovation for Sustainable Development; IGI Global: Hershey, PA, USA, 2022; pp. 1–19. [Google Scholar] [CrossRef]

- Zhang, X.; Song, Y.; Zhang, M. Exploring the relationship of green investment and green innovation: Evidence from Chinese corporate performance. J. Clean. Prod. 2023, 412, 137444. [Google Scholar] [CrossRef]

- Schunk, D.H.; DiBenedetto, M.K. Motivation and social cognitive theory. Contemp. Educ. Psychol. 2020, 60, 101832. [Google Scholar] [CrossRef]

- Bandura, A. Social cognitive theory of self-regulation. Organ. Behav. Hum. Decis. Process. 1991, 50, 248–287. [Google Scholar] [CrossRef]

- Khaw, K.W.; Alnoor, A.; Al-Abrrow, H.; Tiberius, V.; Ganesan, Y.; Atshan, N.A. Reactions towards organizational change: A systematic literature review. Curr. Psychol. 2023, 42, 19137–19160. [Google Scholar] [CrossRef] [PubMed]

- Serikakhmetova, A.B.; Adambekova, A.A. Corporate Social Responsibility in the Context of ESG: Development and Current Trends. Farabi J. Soc. Sci. 2022, 8, 24–32. [Google Scholar] [CrossRef]

- Han, X.; Zheng, Y. Driving Elements of Enterprise Digital Transformation Based on the Perspective of Dynamic Evolution. Sustainability 2022, 14, 9915. [Google Scholar] [CrossRef]

- Guo, L.; Xu, L. The effects of digital transformation on firm performance: Evidence from China’s manufacturing sector. Sustainability 2021, 13, 12844. [Google Scholar] [CrossRef]

- Long, H.; Feng, G.-F.; Chang, C.-P. How does ESG performance promote corporate green innovation? Econ. Chang. Restruct. 2023, 56, 2889–2913. [Google Scholar] [CrossRef]

- Wang, X.; Luan, X.; Zhang, S. Research and Development Investment, ESG Performance, and Market Value of Enterprises: The Moderating Effect of Corporate Digitalization. Sci. Res. 2023, 41, 896–904. [Google Scholar]

- Fang, L.; Li, Z. Corporate digitalization and green innovation: Evidence from textual analysis of firm annual reports and corporate green patent data in China. Bus. Strategy Environ. 2024. [Google Scholar] [CrossRef]

- Wang, Z.; Chu, E.; Hao, Y. Towards sustainable development: How does ESG performance promotes corporate green transformation. Int. Rev. Financ. Anal. 2024, 91, 102982. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strategy Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Ahmad, N.; Mobarek, A.; Roni, N.N. Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis. Cogent Bus. Manag. 2021, 8, 1900500. [Google Scholar] [CrossRef]

- Wang, D.; Luo, Y.; Hu, S.; Yang, Q. Executives’ ESG cognition and enterprise green innovation: Evidence based on executives’ personal microblogs. Front. Psychol. 2022, 13, 1053105. [Google Scholar] [CrossRef] [PubMed]

- Sultana, S.; Zulkifli, N.; Zainal, D. Environmental, social and governance (ESG) and investment decision in Bangladesh. Sustainability 2018, 10, 1831. [Google Scholar] [CrossRef]

- Doni, F.; Johannsdottir, L. Environmental social and governance (ESG) ratings. In Climate Action; Springer: Cham, Switzerland, 2020; pp. 435–449. [Google Scholar] [CrossRef]

- Kandpal, V.; Jaswal, A.; Gonzalez, E.D.R.S.; Agarwal, N. Corporate Social Responsibility (CSR) and ESG Reporting: Redefining Business in the Twenty-First Century. In Sustainable Energy Transition: Circular Economy and Sustainable Financing for Environmental, Social and Governance (ESG) Practices; Springer Nature: Cham, Switzerland, 2024; pp. 239–272. [Google Scholar] [CrossRef]

- Wang, M.L.; Phillips-Fein, K. Environmental, Social, and Corporate Governance: A History of ESG Standardization from 1970s to the Present. Undergraduate. Senior Thesis, Columbia University, New York, NY, USA, 2023. [Google Scholar]

- Bialkowski, J.; Starks, L.T.; Wagner, M. Who cares wins: The rise of socially responsible investing. PRI Acad. Netw. Week 2021, 1–52. [Google Scholar]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Jebe, R. The convergence of financial and ESG materiality: Taking sustainability mainstream. Am. Bus. Law J. 2019, 56, 645–702. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Financ. 2021, 66, 101889. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research progress and future prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Luo, W.; Tian, Z.; Fang, X.; Deng, M. Can good ESG performance reduce stock price crash risk? Evidence from Chinese listed companies. Corp. Soc. Responsib. Environ. Manag. 2023. [Google Scholar] [CrossRef]

- Lian, Y.; Li, Y.; Cao, H. How does corporate ESG performance affect sustainable development: A green innovation perspective. Front. Environ. Sci. 2023, 11, 430. [Google Scholar] [CrossRef]

- Kraus, S.; Jones, P.; Kailer, N.; Weinmann, A.; Chaparro-Banegas, N.; Roig-Tierno, N. Digital transformation: An overview of the current state of the art of research. Sage Open 2021, 11, 21582440211047576. [Google Scholar] [CrossRef]

- Vial, G. Understanding digital transformation: A review and a research agenda. In Managing Digital Transformation; Routledge: London, UK, 2021; pp. 13–66. [Google Scholar] [CrossRef]

- Gouvea, R.; Li, S.; Montoya, M. Does transitioning to a digital economy imply lower levels of corruption? Thunderbird Int. Bus. Rev. 2022, 64, 221–233. [Google Scholar] [CrossRef]

- Ghasemaghaei, M.; Calic, G. Assessing the impact of big data on firm innovation performance: Big data is not always better data. J. Bus. Res. 2020, 108, 147–162. [Google Scholar] [CrossRef]

- Chen, W.; Zhu, C.; Cheung, Q.; Wu, S.; Zhang, J.; Cao, J. How does digitization enable green innovation? Evidence from Chinese listed companies. Bus. Strategy Environ. 2024. [Google Scholar] [CrossRef]

- Razzaq, A.; Yang, X. Digital finance and green growth in China: Appraising inclusive digital finance using web crawler technology and big data. Technol. Forecast. Soc. Chang. 2023, 188, 122262. [Google Scholar] [CrossRef]

- Ren, Y.; Li, B. Digital transformation, green technology innovation and enterprise financial performance: Empirical evidence from the textual analysis of the annual reports of listed renewable energy enterprises in China. Sustainability 2022, 15, 712. [Google Scholar] [CrossRef]

- Tang, L.; Jiang, H.; Hou, S.; Zheng, J.; Miao, L. The Effect of Enterprise Digital Transformation on Green Technology Innovation: A Quantitative Study on Chinese Listed Companies. Sustainability 2023, 15, 10036. [Google Scholar] [CrossRef]

- Li, D.; Shen, W. Can corporate digitalization promote green innovation? The moderating roles of internal control and institutional ownership. Sustainability 2021, 13, 13983. [Google Scholar] [CrossRef]

- Burki, U. Green supply chain management, green innovations, and green practices. In Innovative Solutions for Sustainable Supply Chains; Springer: Cham, Switzerland, 2018; pp. 81–109. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Sharma, S. A contingent resource-based view of proactive corporate environmental strategy. Acad. Manag. Rev. 2003, 28, 71–88. [Google Scholar] [CrossRef]

- Abdallah, A.B.; Al-Ghwayeen, W.S.; Al-Amayreh, E.M.; Sweis, R.J. The Impact of Green Supply Chain Management on Circular Economy Performance: The Mediating Roles of Green Innovations. Logistics 2024, 8, 20. [Google Scholar] [CrossRef]

- Harrison, J.S.; Bosse, D.A.; Phillips, R.A. Managing for stakeholders, stakeholder utility functions, and competitive advantage. Strateg. Manag. J. 2010, 31, 58–74. [Google Scholar] [CrossRef]

- Li, Z.; Huang, Z.; Su, Y. New media environment, environmental regulation and corporate green technology innovation: Evidence from China. Energy Econ. 2023, 119, 106545. [Google Scholar] [CrossRef]

- Liu, H.; Lyu, C. Can ESG ratings stimulate corporate green innovation? Evidence from China. Sustainability 2022, 14, 12516. [Google Scholar] [CrossRef]

- Tan, Y.; Zhu, Z. The effect of ESG rating events on corporate green innovation in China: The mediating role of financial constraints and managers’ environmental awareness. Technol. Soc. 2022, 68, 101906. [Google Scholar] [CrossRef]

- Song, W.; Yu, H. Green innovation strategy and green innovation: The roles of green creativity and green organizational identity. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 135–150. [Google Scholar] [CrossRef]

- Papademetriou, C.; Ragazou, K.; Garefalakis, A.; Passas, I. Green human resource management: Mapping the research trends for sustainable and agile human resources in SMEs. Sustainability 2023, 15, 5636. [Google Scholar] [CrossRef]

- Zona, F.; Zamarian, M. The behavioral agency model and innovation investment: Examining the combined effects of CEO and board ownership. Group Organ. Manag. 2022, 47, 647–678. [Google Scholar] [CrossRef]

- Naveed, K.; Voinea, C.L.; Roijakkers, N. Board Gender Diversity, Corporate Social Responsibility Disclosure, and Firm’s Green Innovation Performance: Evidence from China. Front. Psychol. 2022, 13, 892551. [Google Scholar] [CrossRef] [PubMed]

- Belloc, F. Corporate governance and innovation: A survey. J. Econ. Surv. 2012, 26, 835–864. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Dong, J.Q.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Nadkarni, S.; Prügl, R. Digital transformation: A review, synthesis and opportunities for future research. Manag. Rev. Q. 2021, 71, 233–341. [Google Scholar] [CrossRef]

- Lombardi, R.; Secundo, G. The digital transformation of corporate reporting–a systematic literature review and avenues for future research. Meditari Account. Res. 2021, 29, 1179–1208. [Google Scholar] [CrossRef]

- Nambisan, S.; Wright, M.; Feldman, M. The digital transformation of innovation and entrepreneurship: Progress, challenges and key themes. Res. Policy 2019, 48, 103773. [Google Scholar] [CrossRef]

- Zhang, C.; Wang, Y. Is enterprise digital transformation beneficial to shareholders? Insights from the cost of equity capital. Int. Rev. Financ. Anal. 2024, 92, 103104. [Google Scholar] [CrossRef]

- Sun, C.; Zhang, Z.; Vochozka, M.; Vozňáková, I. Enterprise digital transformation and debt financing cost in China’s A-share listed companies. Oeconomia Copernic. 2022, 13, 783–829. [Google Scholar] [CrossRef]

- Huang, Y.; Lau, C. Can digital transformation promote the green innovation quality of enterprises? Empirical evidence from China. PLoS ONE 2024, 19, e0296058. [Google Scholar] [CrossRef]

- Rai, A.; Patnayakuni, R.; Seth, N. Firm performance impacts of digitally enabled supply chain integration capabilities. MIS Q. 2006, 30, 225–246. [Google Scholar] [CrossRef]

- Qi, H.J.; Cao, X.Q.; Liu, Y.X. The impact of digital economy on corporate governance-based on the perspective of information asymmetry and managers’ irrational behavior. Reform 2020, 4, 50–64. [Google Scholar]

- Zhidong, T.; Xun, Z.; Jun, P.; Jianhua, T. The Value of Digital Transformation: From the Perspective of Corporate Cash Holdings. J. Financ. Econ. 2022, 48, 64–78. [Google Scholar]

- Zhu, J.; Huang, F. Transformational leadership, organizational innovation, and ESG performance: Evidence from SMEs in China. Sustainability 2023, 15, 5756. [Google Scholar] [CrossRef]

- Westerman, G.; Bonnet, D.; McAfee, A. Leading Digital: Turning Technology into Business Transformation; Harvard Business Press: Boston, MA, USA, 2014. [Google Scholar]

- Chang, C.H.; Chen, Y.S. Green organizational identity and green innovation. Manag. Decis. 2013, 51, 1056–1070. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Idowu, A.; Ohikhuare, O.M.; Chowdhury, M.A. Does industrialization trigger carbon emissions through energy consumption? Evidence from OPEC countries and high industrialised countries. Quant. Financ. Econ. 2023, 7, 165–186. [Google Scholar] [CrossRef]

- Friedman, H.L.; Heinle, M.S.; Luneva, I. A Theoretical Framework for ESG Reporting to Investors. Available SSRN 3932689 2021. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3932689 (accessed on 2 January 2024).

- Hanelt, A.; Bohnsack, R.; Marz, D.; Marante, C.A. A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. J. Manag. Stud. 2021, 58, 1159–1197. [Google Scholar] [CrossRef]

- Li, C.; Long, G.; Li, S. Research on measurement and disequilibrium of manufacturing digital transformation: Based on the text mining data of A-share listed companies. Data Sci. Financ. Econ. 2023, 3, 30–54. [Google Scholar] [CrossRef]

- Lee, G.; Shao, B.; Vinze, A. The role of ICT as a double-edged sword in fostering societal transformations. J. Assoc. Inf. Syst. 2018, 19, 1. [Google Scholar] [CrossRef]

- Pang, R.Z.; Liu, D.G. The paradox of digitalization and innovation: Does digitalization promote corporate innovation—An explanation based on open innovation theory. South Econ. 2022, 41, 97–117. [Google Scholar]

- Ai, Y.; Chi, Z.; Sun, G.; Zhou, H.; Kong, T. The research on non-linear relationship between enterprise digital transformation and stock price crash risk. N. Am. J. Econ. Financ. 2023, 68, 101984. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Categories | N | % | |

|---|---|---|---|

| Gender | Male | 145 | 45.9 |

| Female | 171 | 54.1 | |

| Age | 20~30 years | 102 | 32.3 |

| 30~40 years | 129 | 40.8 | |

| 40~50 years | 49 | 15.5 | |

| 50 years~ | 36 | 11.4 | |

| Education | High school | 16 | 5.1 |

| College | 103 | 32.6 | |

| Bachelor | 167 | 52.8 | |

| Master & Doctor | 30 | 9.5 | |

| Career | ~5 years | 80 | 25.3 |

| 5~10 years | 126 | 39.9 | |

| 11~20 years | 67 | 21.2 | |

| 20 years~ | 43 | 13.6 | |

| Industry | Manufacturing | 27 | 8.5 |

| Finance and insurance | 54 | 17.2 | |

| Entertainment, culture and sports | 25 | 7.9 | |

| Retail, wholesale and service | 49 | 15.5 | |

| Real estate | 33 | 10.4 | |

| IT and computer services | 35 | 11.1 | |

| Energy | 16 | 5.1 | |

| Health and social security | 27 | 8.5 | |

| Transportation | 27 | 8.5 | |

| Education | 23 | 7.3 | |

| Firm ownership | State-owned enterprise | 107 | 33.9 |

| Private enterprise | 142 | 44.9 | |

| Foreign enterprise | 62 | 19.6 | |

| Others | 5 | 1.6 | |

| Variable | Items | Source |

|---|---|---|

| ESG (E) | For example, questions such as… My firm is proactive in utilizing energy-efficient, low-carbon equipment and goods. My firm uses fuels and renewable energy. My firm has successfully implemented a comprehensive energy-saving system and measures for energy conservation, complete resource recycling, green offices, etc. My firm has created an excellent environmental management system and organization management system for environmental protection. … | [65] |

| ESG (S) | For example, questions such as… My firm is proactive in utilizing energy-efficient, low-carbon equipment and goods. My firm uses fuels and renewable energy. My firm has successfully implemented a comprehensive energy-saving system and measures for energy conservation, complete resource recycling, green offices, etc. My firm has created an excellent environmental and organization management system for environmental protection. | |

| ESG (G) | The method for disclosing information at my firm is effective. My firm fully considers the interests of stakeholders. My firm has an effective anti-risk response system. My firm operates with moral integrity. My firm has an effective anti-bribery system in place to get rid of corruption. … | |

| DT | My firm uses social media and analytics technology to understand our customers better. My firm markets our items using digital platforms like social media and the internet. My firm uses data analytics to make better operational decisions. My firm uses digital technology to improve product performance and service quality. My firm has introduced fresh, digitally-based business models. … | [66] |

| GI | My firm selects materials that result in the least pollution when undertaking product development or design. When undertaking product development or design, my firm selects materials for its goods that use the least amount of energy and resources. The production procedure used by my firm efficiently lowers the release of waste or harmful materials. Waste and emissions generated during the firm’s manufacturing processes are recycled or reused. My firm’s production method efficiently reduces the amount of water, energy, coal, and oil used. … | [67] |

| Items | 1 | 2 | 3 | 4 | 5 | Cronbach α |

|---|---|---|---|---|---|---|

| ESG15 | 0.787 | 0.183 | 0.125 | 0.099 | 0.069 | 0.948 |

| ESG11 | 0.775 | 0.196 | 0.107 | 0.102 | 0.153 | |

| ESG12 | 0.769 | 0.127 | 0.208 | 0.078 | 0.055 | |

| ESG9 | 0.762 | 0.125 | 0.176 | 0.210 | 0.119 | |

| ESG10 | 0.752 | 0.171 | 0.127 | 0.133 | 0.122 | |

| ESG17 | 0.749 | 0.154 | 0.108 | 0.094 | 0.160 | |

| ESG16 | 0.747 | 0.159 | 0.142 | 0.110 | 0.102 | |

| ESG8 | 0.738 | 0.141 | 0.156 | 0.158 | 0.092 | |

| ESG14 | 0.737 | 0.207 | 0.043 | 0.061 | 0.121 | |

| ESG13 | 0.734 | 0.168 | 0.215 | 0.084 | 0.134 | |

| ESG18 | 0.730 | 0.155 | 0.129 | 0.104 | 0.158 | |

| ESG7 | 0.723 | 0.182 | 0.159 | 0.164 | 0.134 | |

| DT6 | 0.146 | 0.774 | 0.139 | 0.144 | 0.135 | 0.944 |

| DT8 | 0.169 | 0.765 | 0.177 | 0.066 | 0.198 | |

| DT9 | 0.176 | 0.765 | 0.140 | 0.129 | 0.147 | |

| DT3 | 0.162 | 0.765 | 0.215 | 0.146 | 0.115 | |

| DT1 | 0.219 | 0.762 | 0.140 | 0.134 | 0.063 | |

| DT2 | 0.185 | 0.758 | 0.144 | 0.091 | 0.174 | |

| DT7 | 0.175 | 0.756 | 0.126 | 0.141 | 0.170 | |

| DT10 | 0.191 | 0.755 | 0.117 | 0.139 | 0.165 | |

| DT5 | 0.200 | 0.740 | 0.157 | 0.078 | 0.105 | |

| DT4 | 0.211 | 0.733 | 0.207 | 0.062 | 0.156 | |

| GI8 | 0.117 | 0.227 | 0.800 | 0.155 | 0.137 | 0.938 |

| GI5 | 0.205 | 0.090 | 0.777 | 0.169 | 0.156 | |

| GI6 | 0.189 | 0.174 | 0.776 | 0.219 | 0.152 | |

| GI2 | 0.128 | 0.193 | 0.771 | 0.170 | 0.129 | |

| GI7 | 0.230 | 0.140 | 0.761 | 0.129 | 0.172 | |

| GI4 | 0.182 | 0.214 | 0.740 | 0.194 | 0.159 | |

| GI1 | 0.220 | 0.209 | 0.729 | 0.135 | 0.229 | |

| GI3 | 0.209 | 0.248 | 0.716 | 0.140 | 0.142 | |

| ESG4 | 0.202 | 0.132 | 0.101 | 0.790 | 0.100 | 0.906 |

| ESG3 | 0.201 | 0.130 | 0.159 | 0.777 | 0.090 | |

| ESG5 | 0.145 | 0.100 | 0.184 | 0.773 | 0.196 | |

| ESG6 | 0.163 | 0.143 | 0.223 | 0.757 | 0.113 | |

| ESG1 | 0.125 | 0.198 | 0.232 | 0.743 | 0.092 | |

| ESG2 | 0.137 | 0.162 | 0.187 | 0.743 | 0.136 | |

| ESG23 | 0.204 | 0.200 | 0.146 | 0.154 | 0.785 | 0.911 |

| ESG21 | 0.206 | 0.227 | 0.220 | 0.095 | 0.756 | |

| ESG22 | 0.116 | 0.222 | 0.268 | 0.078 | 0.752 | |

| ESG24 | 0.182 | 0.146 | 0.099 | 0.182 | 0.748 | |

| ESG20 | 0.196 | 0.203 | 0.218 | 0.088 | 0.743 | |

| ESG19 | 0.169 | 0.202 | 0.185 | 0.177 | 0.730 | |

| KMO = 0.960, p = 0.000 | ||||||

| Items | Estimate | S.E. | C.R. | AVE | CR | |

|---|---|---|---|---|---|---|

| ESG18 | 0.764 | 1.000 | 0.616 | 0.951 | ||

| ESG17 | 0.775 | 0.983 | 0.066 | 14.825 | ||

| ESG16 | 0.773 | 1.034 | 0.070 | 14.778 | ||

| ESG15 | 0.807 | 1.052 | 0.068 | 15.562 | ||

| ESG14 | 0.754 | 0.973 | 0.068 | 14.349 | ||

| ESG13 | 0.783 | 1.000 | 0.067 | 15.007 | ||

| ESG12 | 0.792 | 1.010 | 0.066 | 15.212 | ||

| ESG11 | 0.809 | 1.079 | 0.069 | 15.621 | ||

| ESG10 | 0.790 | 1.015 | 0.067 | 15.185 | ||

| ESG9 | 0.812 | 1.058 | 0.067 | 15.687 | ||

| ESG8 | 0.779 | 0.980 | 0.066 | 14.915 | ||

| ESG7 | 0.777 | 1.019 | 0.068 | 14.878 | ||

| ESG1 | 0.771 | 1.000 | 0.631 | 0.911 | ||

| ESG2 | 0.778 | 1.037 | 0.071 | 14.599 | ||

| ESG3 | 0.805 | 1.116 | 0.073 | 15.210 | ||

| ESG4 | 0.801 | 1.112 | 0.073 | 15.127 | ||

| ESG5 | 0.804 | 1.124 | 0.074 | 15.194 | ||

| ESG6 | 0.805 | 1.114 | 0.073 | 15.209 | ||

| ESG24 | 0.764 | 1.000 | 0.656 | 0.920 | ||

| ESG23 | 0.836 | 1.132 | 0.071 | 15.912 | ||

| ESG22 | 0.812 | 1.082 | 0.070 | 15.367 | ||

| ESG21 | 0.839 | 1.136 | 0.071 | 15.980 | ||

| ESG20 | 0.815 | 1.047 | 0.068 | 15.434 | ||

| ESG19 | 0.793 | 1.029 | 0.069 | 14.926 | ||

| DT1 | 0.812 | 1.000 | 0.662 | 0.951 | ||

| DT2 | 0.816 | 1.009 | 0.058 | 17.253 | ||

| DT3 | 0.829 | 1.039 | 0.059 | 17.663 | ||

| DT4 | 0.806 | 1.020 | 0.060 | 16.955 | ||

| DT5 | 0.788 | 0.974 | 0.059 | 16.407 | ||

| DT6 | 0.812 | 1.025 | 0.060 | 17.142 | ||

| DT7 | 0.815 | 1.015 | 0.059 | 17.209 | ||

| DT8 | 0.826 | 1.037 | 0.059 | 17.570 | ||

| DT9 | 0.819 | 1.049 | 0.060 | 17.342 | ||

| DT10 | 0.815 | 1.049 | 0.061 | 17.214 | ||

| GI1 | 0.831 | 1.000 | 0.688 | 0.946 | ||

| GI2 | 0.823 | 0.953 | 0.053 | 18.033 | ||

| GI3 | 0.801 | 0.929 | 0.054 | 17.280 | ||

| GI4 | 0.830 | 0.948 | 0.052 | 18.255 | ||

| GI5 | 0.830 | 0.971 | 0.053 | 18.279 | ||

| GI6 | 0.859 | 0.986 | 0.051 | 19.313 | ||

| GI7 | 0.827 | 0.982 | 0.054 | 18.167 | ||

| GI8 | 0.834 | 0.991 | 0.054 | 18.385 | ||

| Model Fit Summary | CMIN/DF = 1.100 < 2 p < 0.001 comparative fit index [CFI] = 0.992, Tucker–Lewis’s index [TLI] = 0.992, incremental fit index [IFI] = 0.992, goodness-of-fitness index [GFI] = 0.890 [NFI] = 0.920, [RMSEA] = 0.018 < 0.08. | |||||

| Mean | S.D. | ESG(E) | ESG(S) | ESG(G) | DT | GI | |

|---|---|---|---|---|---|---|---|

| ESG(E) | 3.3539 | 0.96171 | 1 | ||||

| ESG(S) | 3.3816 | 0.92628 | 0.417 ** | 1 | |||

| ESG(G) | 3.4652 | 0.97193 | 0.411 ** | 0.449 ** | 1 | ||

| DT | 3.3854 | 0.95444 | 0.402 ** | 0.482 ** | 0.495 ** | 1 | |

| GI | 3.3619 | 10.01368 | 0.490 ** | 0.471 ** | 0.511 ** | 0.492 ** | 1 |

| Hypothesis | Estimate | S.E. | C.R. | p | |||

|---|---|---|---|---|---|---|---|

| B | β | ||||||

| H1a | ESG(E) → Green innovation | 0.342 | 0.307 | 0.062 | 5.550 | *** | |

| H1b | ESG(S) → Green innovation | 0.257 | 0.242 | 0.056 | 4.556 | *** | |

| H1c | ESG(G) → Green innovation | 0.413 | 0.387 | 0.061 | 6.790 | *** | |

| Model Fit Summary | CMIN/DF = 1.571 < 2, p < 0.001 comparative fit index [CFI] = 0.965, Tucker–Lewis’s index [TLI] = 0.963, incremental fit index [IFI] = 0.965, Goodness-of-fitness index [GFI] = 0.878, [NFI] = 0.910 [RMSEA] = 0.042 < 0.08 | ||||||

| Variables | Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|---|

| β | t | β | t | β | t | |

| ESG(E) mean centering | 0.275 *** | (5.444) | 0.244 *** | (4.845) | 0.221 *** | (4.403) |

| ESG(S) mean centering | 0.223 *** | (4.323) | 0.169 *** | (3.200) | 0.147 ** | (2.808) |

| ESG(G) mean centering | 0.298 *** | (5.799) | 0.239 *** | (4.508) | 0.192 *** | (3.681) |

| DT mean centering | 0.194 *** | (30.613) | 0.195 *** | (30.749) | ||

| ESG(E) × DT | 0.108 ** | (2.100) | ||||

| ESG(S) × DT | 0.177 ** | (3.343) | ||||

| ESG(G) × DT | −0.076 | (−1.484) | ||||

| R2 | 0.392 | 0.416 | 0.458 | |||

| △R2 | 0.386 | 0.409 | 0.446 | |||

| F statistics | 67.042 *** | 55.488 *** | 37.208 *** | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, Q.; Li, Y.; Hong, A. Integrating ESG into Corporate Strategy: Unveiling the Moderating Effect of Digital Transformation on Green Innovation through Employee Insights. Systems 2024, 12, 148. https://doi.org/10.3390/systems12050148

Sun Q, Li Y, Hong A. Integrating ESG into Corporate Strategy: Unveiling the Moderating Effect of Digital Transformation on Green Innovation through Employee Insights. Systems. 2024; 12(5):148. https://doi.org/10.3390/systems12050148

Chicago/Turabian StyleSun, Qiang, Yannan Li, and Ahreum Hong. 2024. "Integrating ESG into Corporate Strategy: Unveiling the Moderating Effect of Digital Transformation on Green Innovation through Employee Insights" Systems 12, no. 5: 148. https://doi.org/10.3390/systems12050148

APA StyleSun, Q., Li, Y., & Hong, A. (2024). Integrating ESG into Corporate Strategy: Unveiling the Moderating Effect of Digital Transformation on Green Innovation through Employee Insights. Systems, 12(5), 148. https://doi.org/10.3390/systems12050148