Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors?

Abstract

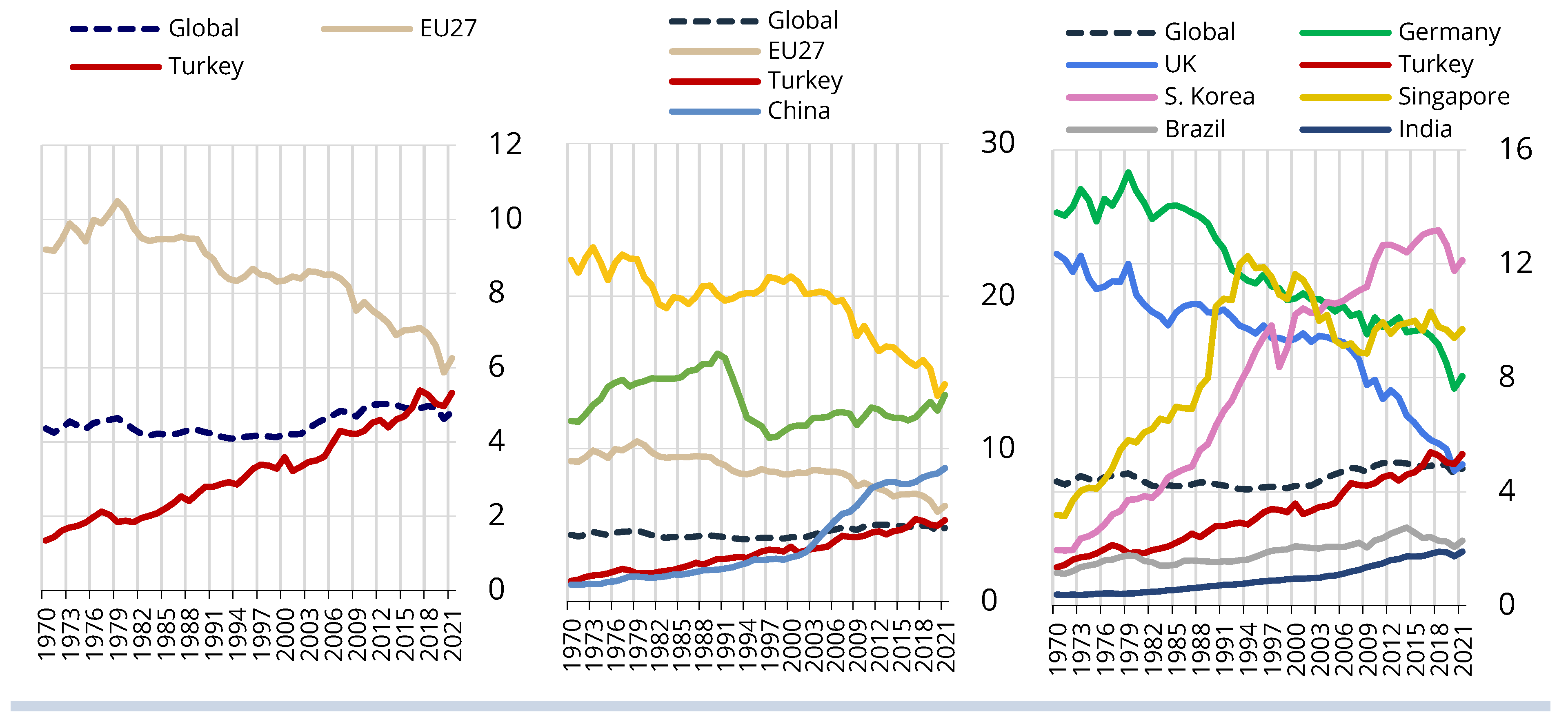

1. Introduction

2. Related Literature

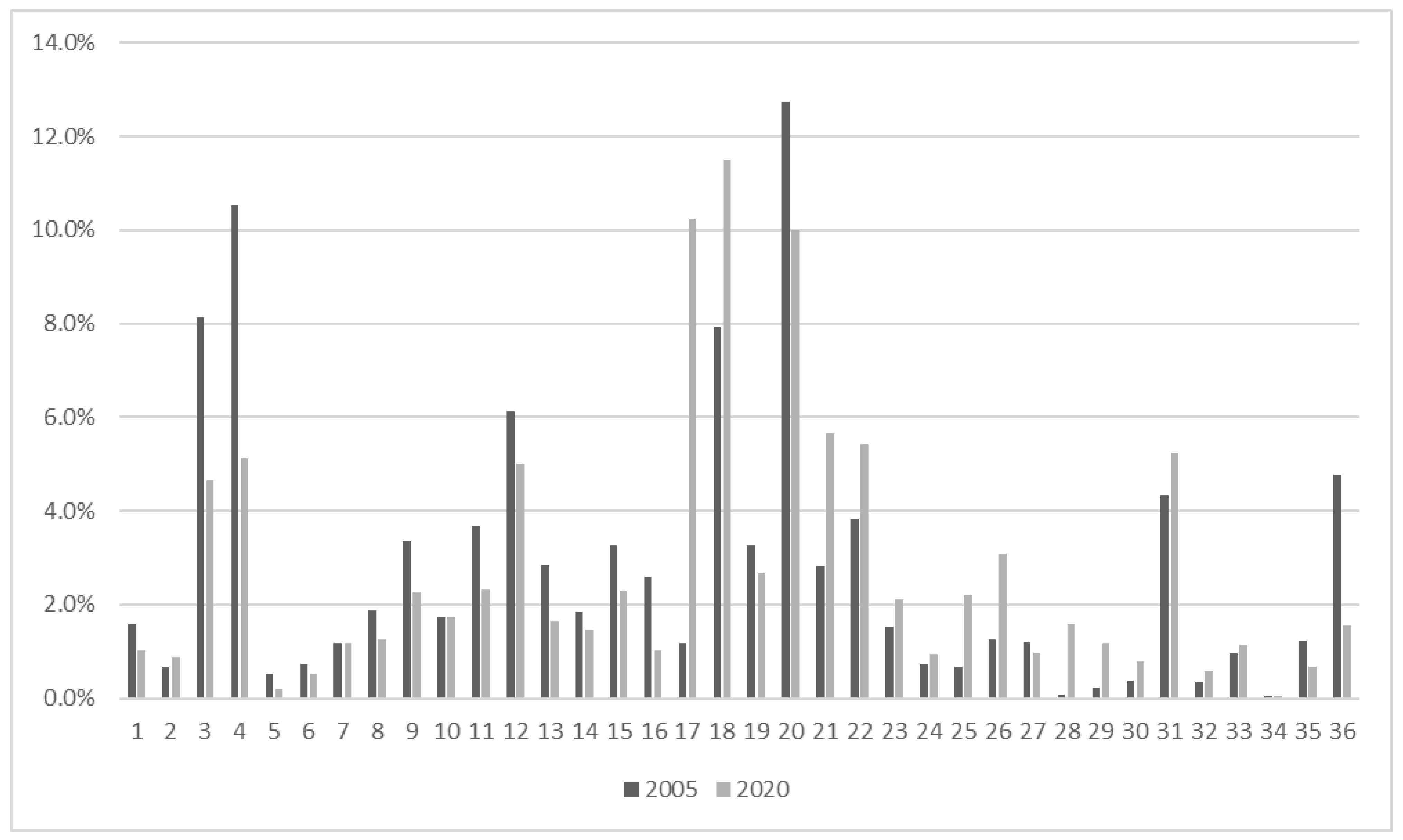

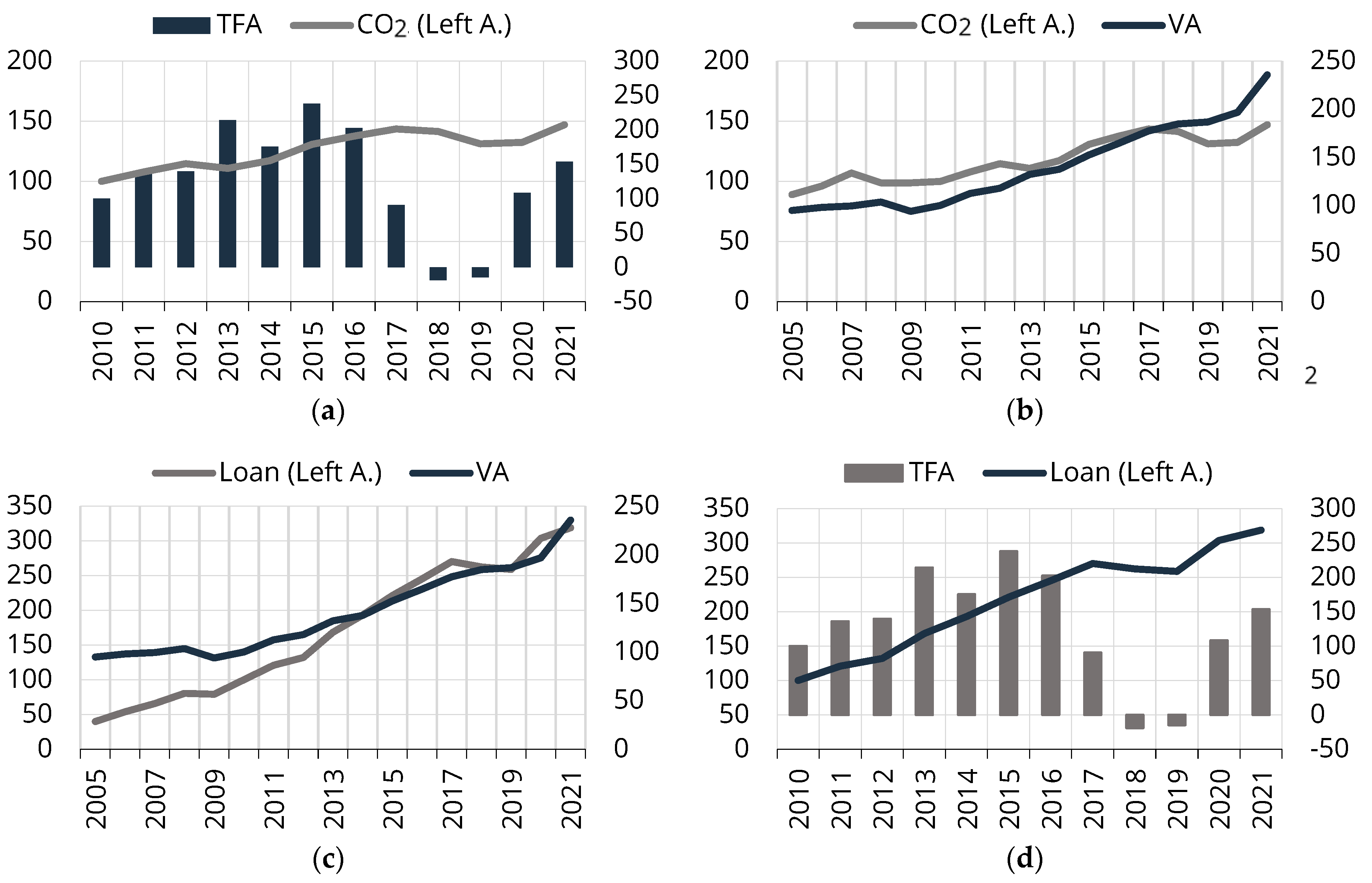

3. Data and Empirical Design

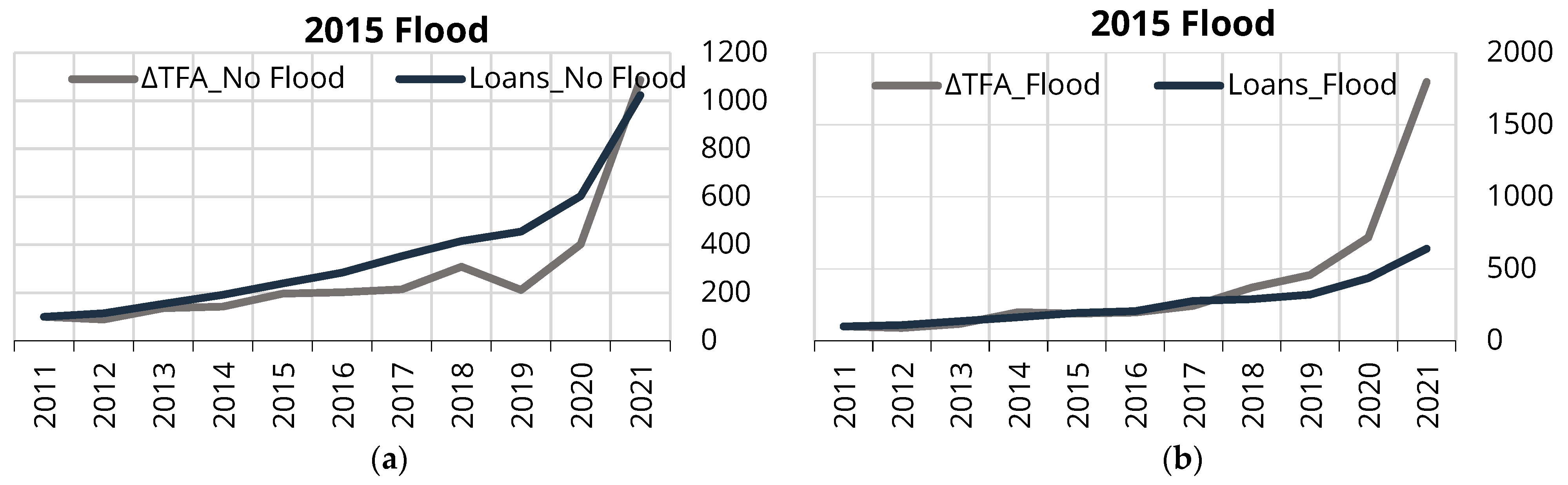

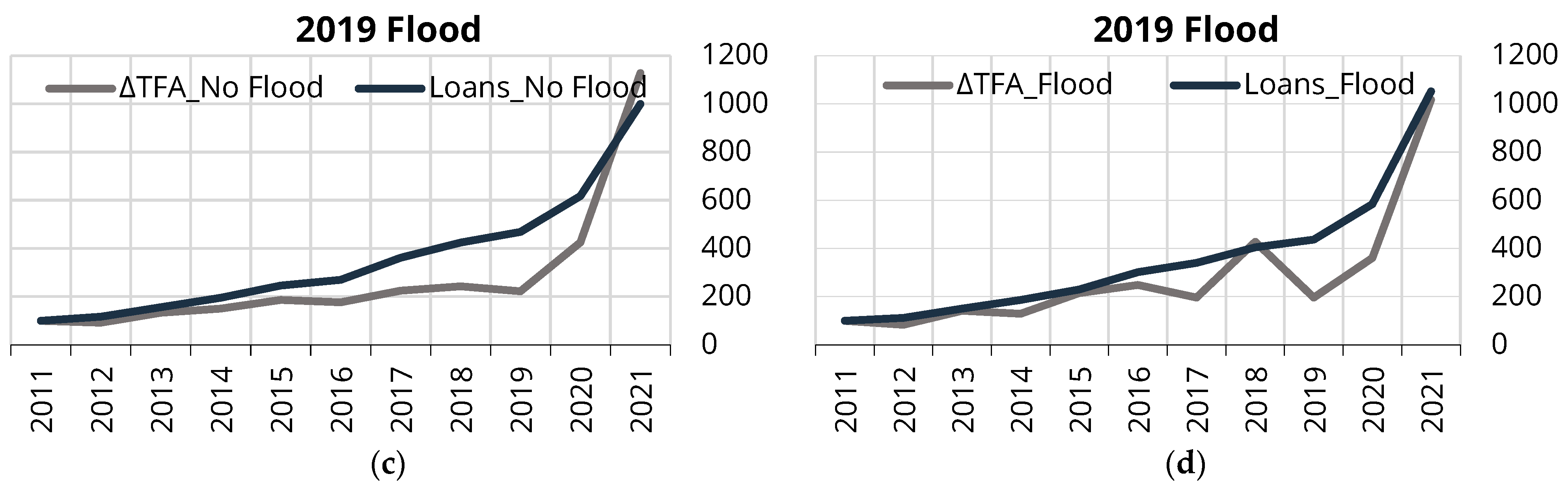

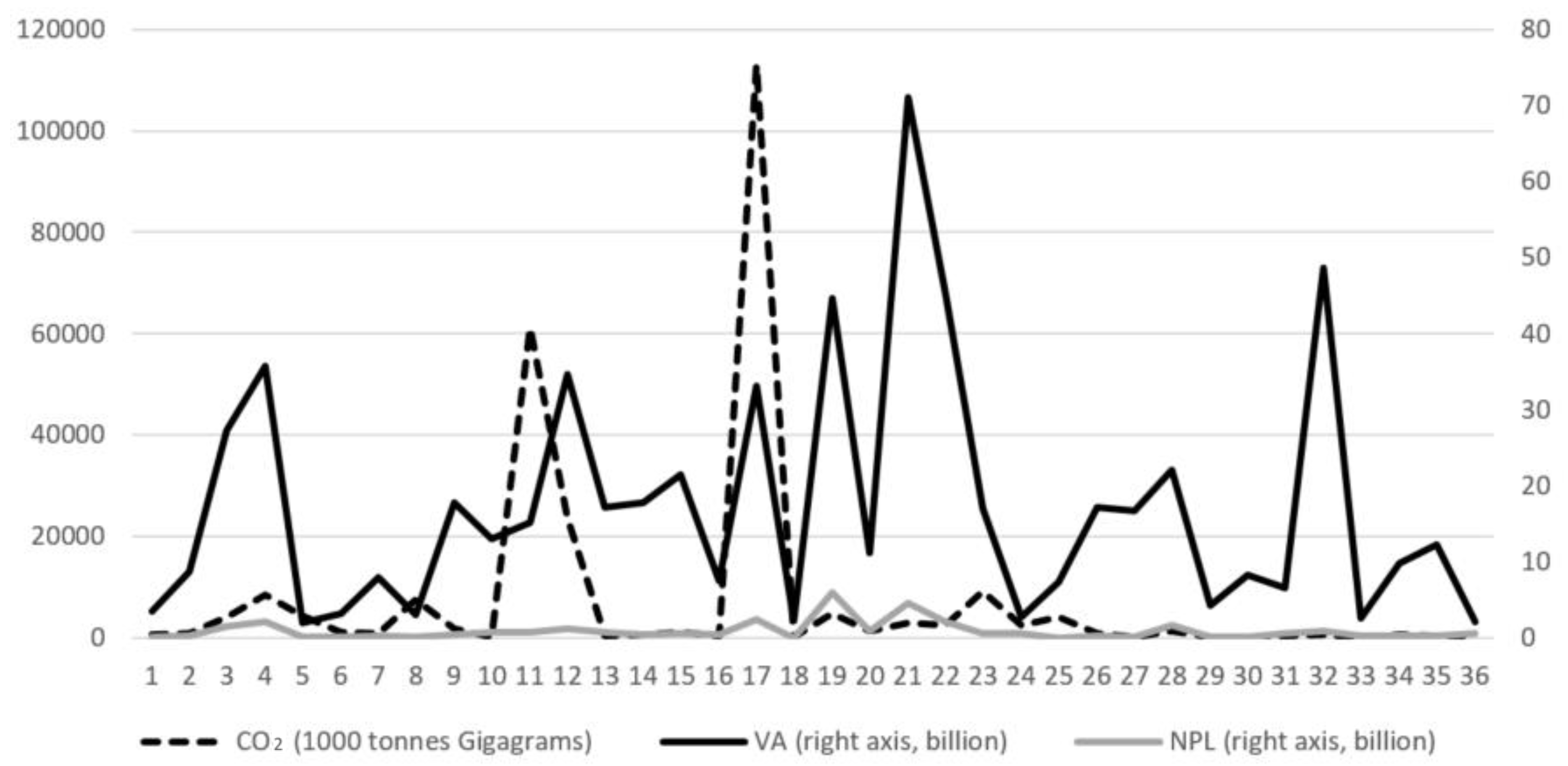

4. Results

5. Robustness Checks

6. Concluding Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No | Name | NACE Codes |

|---|---|---|

| 1 | Extracting of Mines Product Energy | 05 + 06 |

| 2 | Extracting of Mines Not Product Energy | 07 + 08 + 09 |

| 3 | Food, Beverage and Tobacco Industry. | 10 + 11 + 12 |

| 4 | Textile and Textile Products Industry | 13 + 14 |

| 5 | Leather and Leather Products Industry | 15 |

| 6 | Wood and Wood Products Industry | 16 |

| 7 | Paper Raw Materials and Paper Products Industry | 17 + 18 |

| 8 | Nuclear Fuel and Refined Petroleum and Coke Coal Industry | 19 |

| 9 | Chemical Products Industry | 20 + 21 |

| 10 | Rubber and Plastic Products Industry | 22 |

| 11 | Other Mines Excluding Metal Industry | 23 |

| 12 | Main Metal Industry | 24 + 25 |

| 13 | Machine and Equipment Industry | 28 + 33 |

| 14 | Electrical and Optical Devices Industry | 26 + 27 |

| 15 | Transportation Vehicles Industry | 29 + 30 |

| 16 | Manufacturing Industry Not Classified in Other Places | 31 + 32 |

| 17 | Electric, Gas and Water Resources | 35 + 36 |

| 18 | Construction | 41 + 42 + 43 |

| 19 | Retail Sale of Motor Vehicles and Its Fuel Oil | 45 |

| 20 | Wholesale Trade and Brokerage | 46 |

| 21 | Retail Trade and Personal Products | 47 |

| 22 | Hotels + Restaurants + Other Tourism | 55 + 56 |

| 23 | Railroad Transportation + Road Transportation + Road Haulage | 49 |

| 24 | Maritime Transportation | 50 |

| 25 | Air Transportation | 51 |

| 26 | Other Transportation Activities | 52 + 79 |

| 27 | Communication | 53 + 61 |

| 28 | Real Estate Brokerage | 68 |

| 29 | Rent (Vehicle, Machine, Device) | 77 |

| 30 | Computer and Related Activities | 62 + 63 |

| 31 | Research, Consulting, Advertising and Other Activities | 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80 + 81 + 82 |

| 32 | Education | 85 |

| 33 | Health and Social Services | 86 + 87 + 88 |

| 34 | Arranging of Drainage and Waste | 37 + 38 + 39 |

| 35 | Cultural, Entertainment and Sporting Activities | 58 + 59 + 60 + 90 + 91 + 92 + 93 |

| 36 | Other Personal Services | 95 + 96 |

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 4.320293 | (35,485) | 0.0000 |

| Cross-section Chi-square | 146.545302 | 35 | 0.0000 |

| Period F | 3.197548 | (14,485) | 0.0001 |

| Period Chi-square | 47.674382 | 14 | 0.0000 |

| Cross-Section/Period F | 3.984000 | (49,485) | 0.0000 |

| Cross-Section/Period Chi-square | 182.661206 | 49 | 0.0000 |

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 0.252735 | (35,486) | 1.0000 |

| Cross-section Chi-square | 9.740217 | 35 | 1.0000 |

| Period F | 3.233234 | (14,486) | 0.0001 |

| Period Chi-square | 48.088536 | 14 | 0.0000 |

| Cross-Section/Period F | 1.104600 | (49,486) | 0.2971 |

| Cross-Section/Period Chi-square | 57.020053 | 49 | 0.2015 |

| Test Cross-Section and Period Fixed Effects | |||

|---|---|---|---|

| Effects Test | Statistic | d.f. | Prob. |

| Cross-section F | 1.700013 | (35,485) | 0.0086 |

| Cross-section Chi-square | 62.488746 | 35 | 0.0029 |

| Period F | −0.000000 | (14,485) | 1.0000 |

| Period Chi-square | 0.000000 | 14 | 1.0000 |

| Cross-Section/Period F | 1.214295 | (49,485) | 0.1595 |

| Cross-Section/Period Chi-square | 62.488746 | 49 | 0.0933 |

| Part 1 | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Sector (NACE2) | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

| 05 + 06 | 684 | 827 | 956 | 574 | 603 | 572 | 485 | 555 | |

| 07 + 08 + 09 | 1026 | 1240 | 1434 | 862 | 905 | 858 | 728 | 833 | |

| 10 + 11 + 12 | 2595 | 2522 | 1987 | 1973 | 1068 | 1467 | 3999 | 4239 | |

| 13 + 14 | 13,813 | 17,402 | 20,013 | 9416 | 10,148 | 9570 | 6654 | 8112 | |

| 15 | 6907 | 8701 | 10,006 | 4708 | 5074 | 4785 | 3327 | 4056 | |

| 16 | 1691 | 2113 | 2433 | 1206 | 1292 | 1220 | 891 | 1073 | |

| 17 + 18 | 189 | 202 | 239 | 245 | 247 | 235 | 1031 | 1014 | |

| 19 | 5821 | 5954 | 6065 | 6704 | 4797 | 5594 | 6606 | 6570 | |

| 20 + 21 | 1272 | 871 | 885 | 1022 | 911 | 1082 | 1931 | 2166 | |

| 22 | 125 | 135 | 157 | 155 | 156 | 151 | 162 | 188 | |

| 23 | 38,410 | 40,506 | 41,404 | 48,061 | 47,630 | 55,771 | 61,920 | 65,640 | |

| 24 + 25 | 23,288 | 22,546 | 21,361 | 17,032 | 17,157 | 20,093 | 21,338 | 24,394 | |

| 26 + 27 | 615 | 767 | 882 | 437 | 468 | 443 | 323 | 398 | |

| 28 + 33 | 863 | 1065 | 1224 | 648 | 687 | 654 | 504 | 630 | |

| 29 + 30 | 1761 | 2216 | 2548 | 1206 | 1299 | 1226 | 857 | 1053 | |

| 31 + 32 | 381 | 433 | 479 | 265 | 279 | 267 | 222 | 277 | |

| 35 + 36 | 79,816 | 84,995 | 101,325 | 106,013 | 107,365 | 101,542 | 111,975 | 112,906 | |

| 37 + 38 + 39 | 104 | 113 | 132 | 131 | 129 | 122 | 132 | 153 | |

| 41 + 42 + 43 | 6178 | 7618 | 8760 | 4666 | 4942 | 4703 | 3644 | 4507 | |

| 45 | 681 | 732 | 829 | 771 | 766 | 766 | 790 | 1065 | |

| 46 | 1025 | 1108 | 1262 | 1174 | 1166 | 1158 | 1200 | 1625 | |

| 47 | 1028 | 1112 | 1265 | 1173 | 1164 | 1157 | 1198 | 1634 | |

| 49 | 5944 | 6289 | 6767 | 6371 | 6407 | 6368 | 6548 | 8572 | |

| 50 | 1299 | 1462 | 1597 | 1541 | 1630 | 1678 | 2233 | 1618 | |

| 51 | 4077 | 4497 | 5996 | 5203 | 5134 | 2868 | 3347 | 3728 | |

| 52 + 79 | 291 | 313 | 357 | 339 | 338 | 334 | 349 | 449 | |

| 53 + 61 | 42 | 45 | 51 | 48 | 47 | 47 | 49 | 66 | |

| 55 + 56 | 419 | 452 | 518 | 490 | 488 | 481 | 503 | 654 | |

| 58 + 59 + 60 + 90 + 91 + 92 + 93 | 31 | 33 | 38 | 35 | 35 | 34 | 36 | 48 | |

| 62 + 63 | 26 | 28 | 32 | 30 | 30 | 30 | 31 | 42 | |

| 68 | 230 | 247 | 286 | 278 | 278 | 271 | 288 | 350 | |

| 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80+ 81 + 82 | 270 | 291 | 333 | 311 | 309 | 306 | 318 | 426 | |

| 77 | 27 | 30 | 34 | 32 | 31 | 31 | 32 | 44 | |

| 85 | 67 | 72 | 83 | 79 | 79 | 77 | 81 | 104 | |

| 86 + 87 + 88 | 122 | 131 | 152 | 152 | 152 | 147 | 158 | 182 | |

| 95 + 96 | 80 | 86 | 98 | 91 | 90 | 90 | 93 | 127 | |

| part 2 | |||||||||

| Sector (NACE2) | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

| 05 + 06 | 468 | 482 | 469 | 483 | 508 | 521 | 497 | 471 | 522 |

| 07 + 08 + 09 | 701 | 723 | 703 | 724 | 762 | 781 | 745 | 707 | 784 |

| 10 + 11 + 12 | 4337 | 4114 | 5163 | 5824 | 5836 | 5996 | 6057 | 6713 | 7288 |

| 13 + 14 | 5756 | 5544 | 5078 | 4950 | 5078 | 5209 | 5103 | 4732 | 5074 |

| 15 | 2878 | 2772 | 2539 | 2475 | 2539 | 2604 | 2552 | 2366 | 2537 |

| 16 | 801 | 787 | 736 | 731 | 756 | 775 | 753 | 704 | 764 |

| 17 + 18 | 1034 | 1178 | 1258 | 1389 | 1279 | 1325 | 1345 | 1577 | 1628 |

| 19 | 5836 | 5798 | 8214 | 10,889 | 11,590 | 9017 | 10,957 | 10,636 | 10,570 |

| 20 + 21 | 1789 | 2026 | 2373 | 2037 | 1940 | 2733 | 2244 | 2148 | 3299 |

| 22 | 195 | 210 | 215 | 231 | 244 | 248 | 236 | 230 | 260 |

| 23 | 67,287 | 69,586 | 70,734 | 75,973 | 79,591 | 76,978 | 64,536 | 77,199 | 83,897 |

| 24 + 25 | 23,384 | 23,803 | 27,837 | 27,527 | 27,185 | 28,690 | 26,678 | 27,516 | 31,625 |

| 26 + 27 | 306 | 301 | 284 | 285 | 294 | 300 | 292 | 276 | 301 |

| 28 + 33 | 524 | 526 | 509 | 522 | 540 | 549 | 534 | 513 | 565 |

| 29 + 30 | 760 | 735 | 678 | 665 | 682 | 699 | 685 | 639 | 687 |

| 31 + 32 | 235 | 245 | 239 | 248 | 253 | 260 | 255 | 249 | 266 |

| 35 + 36 | 108,349 | 118,537 | 119,578 | 126,667 | 136,600 | 140,540 | 130,433 | 123,361 | 139,520 |

| 37 + 38 + 39 | 153 | 158 | 162 | 175 | 185 | 187 | 179 | 176 | 199 |

| 41 + 42 + 43 | 3728 | 3751 | 3620 | 3712 | 3847 | 3911 | 3801 | 3640 | 4008 |

| 45 | 1185 | 1257 | 1762 | 1851 | 1878 | 1746 | 1729 | 1708 | 1898 |

| 46 | 1807 | 1920 | 6511 | 6449 | 6253 | 4885 | 5040 | 4832 | 5175 |

| 47 | 1822 | 1935 | 4658 | 4696 | 4618 | 3817 | 3881 | 3759 | 4080 |

| 49 | 9648 | 10,261 | 12,015 | 12,644 | 13,252 | 12,658 | 12,321 | 11,925 | 13,353 |

| 50 | 1164 | 1357 | 5223 | 4838 | 3594 | 2694 | 3210 | 3761 | 3709 |

| 51 | 3754 | 4090 | 4227 | 4304 | 4921 | 4905 | 4371 | 1651 | 2098 |

| 52 + 79 | 489 | 521 | 1565 | 1556 | 1517 | 1210 | 1240 | 1190 | 1279 |

| 53 + 61 | 74 | 79 | 268 | 266 | 258 | 201 | 208 | 199 | 213 |

| 55 + 56 | 715 | 762 | 3350 | 3282 | 3159 | 2386 | 2480 | 2359 | 2504 |

| 58 + 59 + 60 + 90 + 91 + 92 + 93 | 54 | 57 | 238 | 234 | 225 | 171 | 178 | 170 | 181 |

| 62 + 63 | 47 | 49 | 78 | 81 | 82 | 74 | 73 | 72 | 80 |

| 68 | 371 | 398 | 408 | 440 | 464 | 469 | 449 | 441 | 498 |

| 69 + 70 + 71 + 72 + 73 + 74 + 75 + 78 + 80+ 81 + 82 | 472 | 502 | 1146 | 1158 | 1142 | 954 | 967 | 936 | 1019 |

| 77 | 48 | 51 | 74 | 77 | 78 | 72 | 72 | 71 | 78 |

| 85 | 114 | 121 | 1803 | 1726 | 1627 | 1117 | 1195 | 1118 | 1158 |

| 86 + 87 + 88 | 188 | 202 | 1345 | 1300 | 1242 | 900 | 943 | 886 | 930 |

| 95 + 96 | 141 | 150 | 815 | 794 | 759 | 559 | 587 | 557 | 587 |

| Dependent Variable: ∂(LOANS)st Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −41,463,726 *** (13,721,062) | −16,497,319 * (9,209,414) | −38,423,098 *** (14,648,789) | −11,491,869 (9,801,190) |

| ∂(LOANS)st−1 | 0.010111 (0.054857) | 0.016993 (0.053439) | 0.211454 *** (0.054000) | 0.225946 *** (0.051767) |

| ∂(NPLRATIOst) | −34,652,631 *** (6,660,165) | −32,452,880 *** (6,466,236) | −30,232,937 *** (6,956,792) | −28,174,752 *** (6,761,418) |

| ∂(VAst) | −0.000161 * (8.95 × 10−5) | −0.000246 *** (8.90 × 10−5) | −5.14 × 10−5 (9.17 × 10−5) | −0.000116 (9.12 × 10−5) |

| ∂(CO2)st−1 | −35.75991 (125.7362) | 41.36008 (93.01380) | 48.24618 (126.9419) | 155.6697 * (87.35823) |

| ∂(CO2)st−1*D2015 | −39.27358 (144.2516) | −87.87949 (149.9677) | ||

| ∂(CO2)st−1*D2019 | −39.62631 (143.0178) | −255.0271 * (139.1890) | ||

| ∂(INVSETst) | 5323.494 (18,710.76) | 27,662.49 *** (9011.493) | 82,076.65 *** (16,530.13) | 52,748.22 *** (8349.350) |

| ∂(INVSETst)*D2015 | 45,044.03 ** (19,336.54) | −18,205.09 (18,518.94) | ||

| ∂(INVSETst)*D2019 | 122,649.0 *** (23,063.40) | 103,114.8 *** (23,421.08) | ||

| D2015 | −1,014,612 ** (510,482.8) | −445,570.6 (539,281.5) | ||

| D2019 | −254,285.7 (404,927.4) | 158,201.6 (427,720.5) | ||

| ∂(GDP)t−1 | −2.029624 (3.662386) | −0.666831 (3.913548) | −7.146751 * (3.867557) | −3.707346 (4.160369) |

| ∂(Real Interb Rate)t−1 | −24,234.40 (20,961.12) | −16,771.28 (21,989.76) | −34,846.14 (22,369.49) | −35,458.57 (23,361.85) |

| Log(TotEquity)t−1 | 3,721,902 *** (1,204,335) | 1,516,435 (803,081.2) | 3,403,082 *** (1,285,616) | 1,049,656 (854,422.0) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.36 | 0.39 | 0.26 | 0.31 |

| F-statistic | 6.18 *** | 7.07 *** | 15.07 *** | 18.44 *** |

| DW | 2.25 | 2.30 | 2.20 | 2.29 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −0.003872 (0.003780) | 0.005587 ** (0.002602) | −0.003694 (0.003637) | 0.005493 ** (0.002507) |

| ∂(LOANSst−1/VAst−1) | −0.504135 *** (0.072589) | −0.499060 *** (0.071241) | −0.478311 *** (0.067748) | −0.473509 *** (0.066053) |

| ∂(CO2st−1/VAst−1) | 31.11498 (79.53593) | 52.08928 (62.17235) | 28.87092 (73.53356) | 38.85587 (57.60055) |

| ∂(CO2st−1/VAst−1)*D2015 | 43.48320 (107.9941) | 31.57589 (102.5113) | ||

| ∂(CO2st−1/VAst−1)*D2019 | 7.508978 (121.9143) | 5.730307 (109.3602) | ||

| ∂(NPLst/VAst) | 4.758286 *** (0.815275) | 4.658038 *** (0.806216) | 4.888359 *** (0.766911) | 4.795813 *** (0.758947) |

| ∂(INVSETst) | 5.38 × 10−6 (5.21 × 10−6) | 3.52 × 10−6 (2.56 × 10−6) | 6.72 × 10−6 * (4.04 × 10−6) | 4.31 × 10−6 ** (2.08 × 10−6) |

| ∂(INVSETst)*D2015 | −3.84 × 10−6 (5.41 × 10−6) | −7.62 × 10−6 (6.23 × 10−6) | −4.92 × 10−6 (4.64 × 10−6) | −7.95 × 10−6 (5.70 × 10−6) |

| ∂(INVSETst)*D2019 | ||||

| D2015 | −0.000193 (0.000141) | −0.000177 (0.000134) | ||

| D2019 | 0.000284 ** (0.000114) | 0.000284 *** (0.000109) | ||

| ∂(GDP)t−1 | −1.62 × 10−9 * (9.52× 10−10) | 1.95× 10−10 (1.10 × 10−9) | −1.63 × 10−9 * (9.17 × 10−10) | 1.76× 10−10 (1.06 × 10−9) |

| ∂(Real Interb Rate)t−1 | −1.41 × 10−5 ** (5.77 × 10−6) | −2.08 × 10−5 *** (6.14 × 10−6) | −1.43 × 10−5 ** (5.56 × 10−6) | −2.10 × 10−5 *** (5.91 × 10−6) |

| Log(TotEquity)t−1 | 0.000352 (0.000332) | −0.000483 ** (0.000227) | 0.000335 (0.000319) | −0.000475 ** (0.000218) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.22 | 0.23 | 0.28 | 0.28 |

| F-statistic | 3.73 *** | 3.82 *** | 17.53 *** | 17.92 *** |

| DW | 2.07 | 2.07 | 2.07 | 2.06 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

| Dependent Variable: ∂ (LOANSst/TOTLOANSst) Estimation Method: Panel Least Squares | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| C | −0.015573 (0.012601) | −0.002837 (0.011065) | −0.020570 * (0.012170) | −0.002113 (0.011239) |

| ∂(LOANSst−1/TOTLOANSst−1) | −0.209425 *** (0.047336) | −0.203547 *** (0.047232) | −0.134295 *** (0.045599) | −0.099946 ** (0.045284) |

| ∂(NPLst/TOTNPLt) | 0.073013 *** (0.020396) | 0.076663 *** (0.020875) | 0.088379 *** (0.018991) | 0.103292 *** (0.019516) |

| ∂(VAst/VASUMt) | 0.165689 *** (0.051201) | 0.157052 *** (0.050820) | 0.153404 *** (0.049317) | 0.137420 *** (0.049625) |

| ∂(CO2st−1/CO2TOTt−1) | −0.158698 ** (0.062298) | −0.158176 *** (0.044900) | −0.179905 *** (0.058853) | −0.198917 *** (0.043629) |

| ∂(CO2st−1/CO2TOTt−1)*D2015 | 0.061692 (0.074892) | 0.061078 (0.072416) | ||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | 0.098271 (0.076753) | 0.114919 (0.077133) | ||

| ∂(INVSETst/INVTOTt) | 0.020870 ** (0.008541) | −0.000539 ** (0.000254) | 0.027712 *** (0.007150) | −0.000524 ** (0.000247) |

| ∂(INVSETst/INVTOTt)*D2015 | −0.021427 ** (0.008526) | −0.028296 *** (0.007151) | ||

| ∂(INVSETst/INVTOTt)*D2019 | −0.006173 ** (0.002898) | −0.004603 (0.002830) | ||

| ∂(GDP)t−1 | −9.97× 10−10 (5.48 × 10−9 ) | −9.14× 10−10 (5.49 × 10−9 ) | −1.32× 10−9 (5.49 × 10−9 ) | −6.81× 10−10 (5.58 × 10−9 ) |

| ∂(Real Interb Rate)t−1 | 2.37 × 10−6 (3.40 × 10−5) | 3.22 × 10−6 (3.41 × 10−5) | 3.14 × 10−6 (3.41 × 10−5) | 2.40 × 10−6 (3.46 × 10−5) |

| Log(TotEquity)t−1 | 0.001322 (0.001080) | 0.000252 (0.000952) | 0.001746 * (0.001044) | 0.000188 (0.000967) |

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 432 | 432 | 432 | 432 |

| Adjusted R-squared | 0.13 | 0.13 | 0.13 | 0.10 |

| F-statistic | 2.44 *** | 2.41 *** | 7.16 *** | 5.76 *** |

| DW | 1.95 | 1.93 | 1.93 | 1.94 |

| Cross-section fixed effects | Yes | Yes | No | No |

| Period fixed effects | No | No | No | No |

References

- Aslan, C.; Bulut, E.; Cepni, O.; Yilmaz, M.H. Does climate change affect bank lending behavior? Econ. Lett. 2022, 220, 110859. [Google Scholar] [CrossRef]

- Cortés, K.R.; Strahan, P.E. Tracing out capital flows: How financially integrated banks respond to natural disasters. J. Financ. Econ. 2017, 125, 182–199. [Google Scholar] [CrossRef]

- Brei, M.; Mohanb, P.; Strobl, E. The impact of natural disasters on the banking sector: Evidence from hurricane strikes in the Caribbean. Q. Rev. Econ. Financ. 2019, 72, 232–239. [Google Scholar] [CrossRef]

- Ivanov, I.T.; Macchiavelli, M.; Santos, J. Bank lending networks and the propagation of natural disasters. Financ. Manag. 2020, 51, 903–927. [Google Scholar] [CrossRef]

- Faiella, I.; Natoli, F. Natural Catastrophes and Bank Lending: The Case of Food Risk in Italy; Bank of Italy Occasional Paper; Bank of Italy: Rome, Italy, 2018; Volume 457. [Google Scholar]

- Li, S.; Wu, X. How does climate risk affect bank loan supply? Empirical evidence from China. Econ. Chang. Restruct. 2023, 56, 2169–2204. [Google Scholar] [CrossRef]

- Berger, A.N.; Guedhami, O.; Kim, H.H.; Li, X. Economic Policy Uncertainty and Bank Liquidity Hoarding. J. Financ. Intermediation Forthcom. 2022, 49, 100893. [Google Scholar] [CrossRef]

- Lee, C.-C.; Wang, C.-W.; Thinh, B.-T.; Xu, Z.-T. Climate risk and bank liquidity creation: International evidence. Int. Rev. Financ. Anal. 2022, 82, 102198. [Google Scholar] [CrossRef]

- Do, Q.A.; Phan, V.; Nguyen, D.T. How do local banks respond to natural disasters? Eur. J. Financ. 2023, 29, 754–779. [Google Scholar] [CrossRef]

- Hosono, K.; Miyakawa, D.; Uchino, T.; Hazama, M.; Ono, A.; Uchida, H.; Uesugi, I. Natural Disasters, Damage to Banks, and Firm Investment. Int. Econ. Rev. 2016, 57, 1335–1370. [Google Scholar] [CrossRef]

- David, M.A. How do international financial flows to developing countries respond to natural disasters? Int. Monet. Fund 2010, 11, 1850243. [Google Scholar] [CrossRef]

- Berg, G.; Schrader, J. Access to credit, natural disasters, and relationship lending. J. Financ. Intermediat. 2012, 21, 549–568. [Google Scholar] [CrossRef]

- Islam, M.N.; Wheatley, C.M. Impact of Climate Risk on Firms’ Use of Trade Credit: International Evidence. Int. Trade J. 2020, 35, 40–59. [Google Scholar] [CrossRef]

- Horvath, G. Natural catastrophes and financial depth: An empirical analysis. J. Financ. Stab. 2021, 53, 100842. [Google Scholar] [CrossRef]

- Li, S.; Li, Q.; Lu, S. The impact of climate risk on credit supply to private and public sectors: An empirical analysis of 174 countries. Environ. Dev. Sustain. 2022, 26, 2443–2465. [Google Scholar] [CrossRef] [PubMed]

- Sun, H.; Bless, K.E.; Sun, C.; Kporsu, A.K. Institutional quality, green innovation and energy efficiency. Energy Policy 2019, 135, 111002. [Google Scholar] [CrossRef]

- Fatica, S.; Panzica, R.; Rancan, M. The pricing of green bonds: Are financial institutions special? J. Financ. Stab. 2021, 54, 100873. [Google Scholar] [CrossRef]

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corp. Soc. Responsib. Environ. Manag. 2019, 26, 529–547. [Google Scholar] [CrossRef]

- Kacperczyk, M.; Peydró, J. Carbon Emissions and the Bank-Lending Channel. 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3915486 (accessed on 20 December 2023).

- Mésonnier, J. Banks’ Climate Commitments and Credit to Brown Industries: New Evidence for France. Banque de France Working Paper 743. 2019. Available online: https://ssrn.com/abstract=3502681 (accessed on 12 November 2023).

- Delis, M.D.; de Greiff, K.; Ongena, S. Being Stranded on the Carbon Bubble? Climate Policy Risk and the Pricing of Bank Loans; Swiss Finance Institute Research Paper Series 18-10; Swiss Finance Institute: Zürich, Switzerland, 2018. [Google Scholar]

- Giannetti, M.; Jasova, M.; Lomiouti, M.; Mendicino, C. “Glossy Green” Banks: The Disconnect between Environmental Disclosures and Lending Activities. ECB Working Paper. 2023. Available online: https://ssrn.com/abstract=4668588 (accessed on 30 December 2023).

- Verga, G.; Soana, M.G. Supply and demand in the European credit market during the recent crisis. Appl. Financ. Econ. 2012, 22, 1355–1366. [Google Scholar] [CrossRef]

- Mueller, I.; Sfrappini, S. Climate Change-Related Regulatory Risks and Bank Lending. ECB Working Paper No. 2022/2670. 2022. Available online: https://ssrn.com/abstract=4144358 (accessed on 2 October 2023).

- Loayza, N.V.; Olaberria, E.; Rigolini, J.; Christiaensen, L. Natural Disasters and Growth: Going beyond the Averages. World Dev. 2012, 40, 1317–1336. [Google Scholar] [CrossRef]

- Gan, J. Collateral, debt capacity, and corporate investment: Evidence from a natural experiment. J. Financ. Econ. 2007, 85, 709–734. [Google Scholar] [CrossRef]

- Kasap, Y.; Şensöğüt, C.; Ören, Ö. Efficiency change of coal used for energy production in Turkey. Resour. Policy 2020, 65, 101577. [Google Scholar] [CrossRef]

| Year | Start Date | End Date | Total Affected | Total Deaths | Disaster Description (Group-Subgroup-Type-Subtype) | Origin | Provinces |

|---|---|---|---|---|---|---|---|

| 2009 | 7 September 2009 | 10 September 2009 | 35.060 | 40 | Natural–Hydrological–Flood–Flash flood | Heavy rains | Istanbul, Tekirdag |

| 2019 | 17 August 2019 | 17 August 2019 | 15.001 | 1 | Natural–Hydrological–Flood–Flash flood | Istanbul | |

| 2015 | 30 January 2015 | 2 February 2015 | 6.508 | 8 | Natural–Hydrological–Flood–Riverine flood | Edirne | |

| 2007 | 16 November 2007 | 21 November 2007 | 2.251 | 1 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Mugla, Tekirdag, Edirne |

| 2007 | 27 May 2007 | 1 June 2007 | 763 | 13 | Natural–Hydrological–Flood–Riverine flood | Heavy rain | Agri, Van, Bitlis, Gaziantep |

| 2020 | 11 June 2020 | 12 June 2020 | 751 | 1 | Natural–Hydrological–Flood–Flash flood | Ankara | |

| 2020 | 7 January 2020 | 9 January 2020 | 302 | 2 | Natural–Meteorological–Storm–Convective storm | Mersin, Antalya | |

| 2008 | 1 August 2008 | 5 August 2008 | 302 | 2 | Natural–Climatological–Wildfire–Forest fire | Drought, high winds, heat waves, human factors | Antalya |

| 2017 | 27 July 2017 | 27 July 2017 | 270 | 0 | Natural–Meteorological–Storm–Convective storm | Istanbul | |

| 2019 | 17 July 2019 | 18 July 2019 | 227 | 7 | Natural–Hydrological–Flood–Flash flood | Duzce | |

| 2010 | 27 August 2010 | 27 August 2010 | 219 | 13 | Natural–Hydrological–Landslide–Landslide | Torrential rains | Rize |

| 2007 | 3 August 2007 | 3 August 2007 | 188 | 2 | Natural–Hydrological–Flood–Riverine flood | Heavy rain | Erzurum |

| 2020 | 4 February 2020 | 5 February 2020 | 125 | 41 | Natural–Hydrological–Landslide–Avalanche | Van | |

| 2018 | 8 July 2018 | 8 July 2018 | 124 | 24 | Natural–Hydrological–Landslide–Landslide | Heavy rains | Tekirdag |

| 2009 | 10 July 2009 | 16 July 2009 | 118 | 7 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Artvin, Sinop, Ordu, Bartin |

| 2019 | 18 June 2019 | 20 June 2019 | 80 | 10 | Natural–Hydrological–Flood–Flash flood | Heavy rains | Trabzon |

| 2020 | 21 June 2020 | 23 June 2020 | 79 | 7 | Natural–Hydrological–Flood–Flash flood | Bursa | |

| 2009 | 25 January 2009 | 25 January 2009 | 17 | 11 | Natural–Hydrological–Landslide–Avalanche | High temperatures | Gumushane |

| 2011 | 8 October 2011 | 11 October 2011 | 11 | 8 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Antalya, Denizli, Manisa |

| 2020 | 22 August 2020 | 23 August 2020 | 16 | 16 | Natural–Hydrological–Flood | Samsun, Rize, Trabzon, Giresun | |

| 2015 | 25 August 2015 | 25 August 2015 | 9 | 9 | Natural–Hydrological–Flood–Flash flood | Pouring rainfall | Artvin |

| 2013 | 28 January 2013 | 28 January 2013 | 7 | 7 | Natural–Hydrological–Landslide–Landslide | Heavy rains | Sirnak |

| 2012 | 4 July 2012 | 4 July 2012 | 13 | 13 | Natural–Hydrological–Flood–Riverine flood | Heavy rains | Samsun |

| 2009 | 21 November 2009 | 22 November 2009 | 4 | 4 | Natural–Hydrological–Landslide–Landslide | Torrential rain | Trabzon, Giresun |

| 2007 | 31 May 2007 | 31 May 2007 | 3 | 3 | Natural–Meteorological–Extreme temperature–Heat wave | Burdur, Sinop |

| Main Variable | Unit | Definition | Mean | Median | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|---|---|

| Sector Loan | Billion TL | Change in stock loan amount on sectoral basis | 5.77 | 1.78 | 12.82 | −31.85 | 133.61 |

| Total Loans | Billion TL | Change in total loan amount of the banks | 207.67 | 152.41 | 251.23 | 9.68 | 1019.12 |

| Sector NPL | Billion TL | Change in non-performing loan amount on sectoral basis | 0.21 | 0.03 | 0.84 | −1.20 | 11.66 |

| Total NPL | Billion TL | Change in non-performing loan amount of the banks | 7.55 | 2.84 | 12.66 | −0.84 | 48.43 |

| Interest Rate | % | Interbank rate | 10.3 | 7.5 | 5.6 | 1.6 | 22.5 |

| Sector CO2 | Gigagram | CO2 emissions on a sectoral basis | 7407 | 949 | 21,480 | 26 | 140,540 |

| Total CO2 | Gigagram | CO2 emissions of all sectors | 266,665 | 259,496 | 41,317 | 201,198 | 332,638 |

| Sector Value Added | Billion TL | Value added at factor costs at sectoral basis | 20.6 | 9.7 | 30.2 | 0.2 | 300.8 |

| Total Value Added | Billion TL | Total value added at factor costs | 743.0 | 499.1 | 641.0 | 191.7 | 2670.6 |

| Sector Investment | Million TL | Change in tangible fixed assets on sectoral basis | 6 | 3 | 15 | −77 | 157 |

| Total Investment | Million TL | Change in tangible fixed assets on sectoral basis | 231 | 243 | 134 | −28 | 425 |

| NPL Ratio | % | Non-Performing Loans/(Performing Loans + Non-Performing Loans) | 3.5 | 2.8 | 2.8 | 0.1 | 20.3 |

| Dependent Variable: ∂(LOANS)st Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 1,005,112 *** (100,785.4) | 991,454.6 *** (100,132.7) | 965,255.3 *** (101,005.5) | 1,066,647 *** (139,911.3) | 976,731.0 *** (132,534.1) |

| ∂(LOANS)st−1 | −0.091259 * (0.049359) | −0.087288 * (0.049578) | −0.075999 (0.049346) | −0.119598 ** (0.055060) | −0.101683 * (0.054946) |

| ∂(NPLRATIOst) | −17,718,942 *** (525,708) | −17,854,382 *** (5,262,147) | −17,933,414 *** (5,248,747) | −21,906,659 *** (6,810,829) | −22,097,838 *** (6,755,282) |

| ∂(VAst) | 0.000335 *** (5.56 × 10−5) | 0.000340 *** (5.57 × 10−5) | 0.000332 *** (5.55 × 10−5) | 0.000292 *** (6.84 × 10−5) | 0.000247 *** (7.07 × 10−5) |

| ∂(CO2)st−1 | −216.0735 * (117.7448) | −110.0905 (70.42866) | −29.11581 (64.38706) | −68.02901 (121.2411) | 44.26970 (91.21884) |

| ∂(CO2)st−1*D2009 | 145.5409 (128.1418) | ||||

| ∂(CO2)st−1*D2015 | 29.11072 (95.41738) | −5.165647 (139.5781) | |||

| ∂(CO2)st−1*D2019 | −183.1634 (113.4169) | −133.2022 (139.1307) | |||

| ∂(INVSETst) | 843.9425 (18,111.17) | 18,437.52 ** (9088.077) | |||

| ∂(INVSETst)*D2015 | 27,911.93 (18,755.62) | ||||

| ∂(INVSETst)*D2019 | 58,867.41 ** (24,444.92) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.41 | 0.41 | 0.41 | 0.42 | 0.43 |

| F-statistic | 7.87 *** | 7.83 *** | 7.91 *** | 6.88 *** | 7.09 *** |

| DW | 2.01 | 2.00 | 2.03 | 2.12 | 2.15 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 8.53 × 10−5 *** (2.46 × 10−5) | 8.56 × 10−5 *** (2.45 × 10−5) | 8.51 × 10−5 *** (2.44 × 10−5) | 4.23 × 10−5 (3.24 × 10−5) | 5.26 × 10−5 * (3.16 × 10−5) |

| ∂(LOANSst−1/VAst−1) | −0.451685 *** (0.053234) | −0.459013 *** (0.059666) | −0.454011 *** (0.057582) | −0.475886 *** (0.067968) | −0.475805 *** (0.066809) |

| ∂(CO2st−1/VAst−1) | 12.43697 (72.93898) | 15.32679 (39.46820) | 19.52034 (36.04436) | 32.74124 (73.91078) | 33.82579 (57.93156) |

| ∂(CO2st−1/VAst−1)*D2009 | 10.94941 (82.41471) | ||||

| ∂(CO2st−1/VAst−1)*D2015 | 23.24363 (77.48787) | 18.28062 (102.4731) | |||

| ∂(CO2st−1/VAst−1)*D2019 | 14.16365 (95.37290) | 2.758186 (109.1711) | |||

| ∂(NPLst/VAst) | 4.737733 *** (0.718856) | 4.711741 *** (0.725115) | 4.739007 *** (0.718443) | 4.794958 *** (0.802638) | 4.824973 *** (0.795534) |

| ∂(INVSETst) | 6.36 × 10−6 (4.06 × 10−6) | 3.25 × 10−6 (2.12 × 10−6) | |||

| ∂(INVSETst)*D2015 | −5.48 × 10−6 (4.65 × 10−6) | ||||

| ∂(INVSETst)*D2019 | −8.01 × 10−6 (5.94 × 10−6) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.27 | 0.27 | 0.27 | 0.29 | 0.29 |

| F-statistic | 12.24 *** | 12.25 *** | 12.24 *** | 11.22 *** | 11.26 *** |

| DW | 2.01 | 2.00 | 2.00 | 2.07 | 2.07 |

| Cross-section fixed effects | No | No | No | No | No |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

| Dependent Variable: ∂ (LOANSst/TOTLOANSst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 6.85 × 10−17 (0.000169) | 6.14 × 10−17 (0.000169) | 6.42 × 10−17 (0.000170) | −0.000170 (0.000196) | 5.69 × 10−5 (0.000178) |

| ∂(LOANSst−1/TOTLOANSst−1) | −0.042625 (0.040316) | −0.046170 (0.040253) | −0.045051 (0.040466) | −0.204685 *** (0.047102) | −0.203399 *** (0.047053) |

| ∂(NPLst/TOTNPLt) | 0.035152 ** (0.015715) | 0.034309 ** (0.015701) | 0.032515 ** (0.015779) | 0.072634 *** (0.020357) | 0.076668 *** (0.020797) |

| ∂(VAst/VASUMt) | 0.164782 *** (0.044940) | 0.147882 *** (0.044866) | 0.154642 *** (0.044674) | 0.165827 *** (0.051108) | 0.157072 *** (0.050630) |

| ∂(CO2st−1/CO2TOTt−1) | 0.126020 (0.101152) | −0.002633 (0.035753) | −0.026245 (0.031419) | −0.163950 *** (0.062048) | −0.158202 *** (0.044733) |

| ∂(CO2st−1/CO2TOTt−1)*D2009 | −0.177371 * (0.107436) | ||||

| ∂(CO2st−1/CO2TOTt−1)*D2015 | −0.085170 (0.058408) | 0.067780 (0.074602) | |||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | −0.044083 (0.073076) | 0.098526 (0.076463) | |||

| ∂(INVSETst/INVTOTt) | 0.015440 ** (0.007369) | −0.000540 ** (0.000253) | |||

| ∂(INVSETst/INVTOTt)*D2015 | −0.016004 ** (0.007356) | ||||

| ∂(INVSETst/INVTOTt)*D2019 | −0.006031 ** (0.002854) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 540 | 540 | 540 | 432 | 432 |

| Adjusted R-squared | 0.09 | 0.09 | 0.09 | 0.13 | 0.13 |

| F-statistic | 2.36 *** | 2.34 *** | 2.29 *** | 2.58 *** | 2.60 *** |

| DW | 2.12 | 2.11 | 2.12 | 1.95 | 1.93 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | No | No | No | No | No |

| Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | |||

| Dependent Variable: | ∂ (LOANSst) | ∂(LOANSst/VAst) | ∂(LOANSst/ TOTLOANSt) | ||

| C | 898,103.8 *** (145,082.7) | C | 1.37 × 10−5 (3.80 × 10−5) | C | 1.61 × 10−5 (0.000198) |

| ∂(LOANSst−1) | −0.117976 ** (0.053186) | ∂(LOANSst−1/VAst−1) | −0.496480 *** (0.067319) | ∂(LOANSst−1/TOTLOANSt−1) | −0.188929 *** (0.046938) |

| ∂(CO2st−1) | −77.75375 (63.80037) | ∂(CO2st−1/VAst−1) | 52.64141 (59.30989) | ∂(NPLst/TOTNPLt) | 0.070529 *** (0.020464) |

| ∂(NPLRATIOst) | −33,554,090 *** (6,287,561) | ∂(NPLst/VAst) | 4.729198 *** (0.815984) | ∂(VAst/VASUMt) | 0.158392 *** (0.050984) |

| ∂(VAst) | 0.000393 *** (5.89 × 10−5) | ∂(INVSETst) | 2.51 × 10−6 (2.43 × 10−6) | ∂(CO2st−1/CO2TOTt−1) | −0.121864 *** (0.036567) |

| ∂(INVSETst) | 28,248.57 *** (8601.873) | TOTAFFNATt−1 | 7.66 × 10−9 ** (2.99× 10−9 ) | ∂(INVSETst/INVTOTt) | −0.000580 ** (0.000254) |

| TOTAFFNATt−1 | −2.722095 (10.88668) | TOTAFFNATt−1 | −1.65 × 10−20 (1.76 × 10−8 ) | ||

| Sample | 2010–2021 | 2010–2021 | 2010–2021 | ||

| Total Observations | 432 | 432 | 432 | ||

| Adjusted R-squared | 0.39 | 0.20 | 0.12 | ||

| F-statistic | 7.84 *** | 3.72 *** | 2.47 *** | ||

| DW | 2.14 | 2.09 | 1.95 | ||

| Cross-section fixed effects | Yes | Yes | Yes | ||

| Period fixed effects | No | No | No | ||

| Dependent Variable: ∂ (LOANSst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 1,092,092 *** (140,590.8) | 1,068,805 *** (138,616.2) | 1,015,951 *** (140,072.9) | 1,149,411 *** (187,123.8) | 908,797.3 *** (181,217.5) |

| ∂(LOANS)st−1 | 0.003449 (0.073509) | 0.012864 (0.073652) | 0.031653 (0.072868) | −0.027864 (0.080772) | 0.025108 (0.080575) |

| ∂(NPLRATIOst) | −34,802,255 *** (9,037,145) | −34,920,261 *** (9,052,856) | −34,805,955 *** (8,985,677) | −40,894,632 *** (11,521,580) | −42,803,859 *** (11,256,562) |

| ∂(VAst) | 0.000303 *** (6.76 × 10−5) | 0.000309 *** (6.77 × 10−5) | 0.000299 *** (6.72 × 10−5) | 0.000216 ** (8.39 × 10−5) | 0.000125 (8.91 × 10−5) |

| ∂(CO2)st−1 | −208.8401 * (113.7210) | −120.0343 * (67.53861) | −42.76500 (62.26676) | −83.50744 (113.3827) | 37.63014 (86.16163) |

| ∂(CO2)st−1*D2009 | 110.3091 (123.9884) | ||||

| ∂(CO2)st−1*D2015 | 5.678624 (91.78015) | −21.99148 (130.5297) | |||

| ∂(CO2)st−1*D2019 | −200.0598 * (107.8083) | −101.4600 (130.8603) | |||

| ∂(INVSETst) | −2825.639 (18,865.37) | 23,917.77 ** (11,782.84) | |||

| ∂(INVSETst)*D2015 | 43,432.39 ** (19,928.26) | ||||

| ∂(INVSETst)*D2019 | 96,716.82 *** (30,686.03) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.52 | 0.52 | 0.53 | 0.55 | 0.57 |

| F-statistic | 9.17 *** | 9.11 *** | 9.34 *** | 8.49 *** | 9.08 *** |

| DW | 1.93 | 1.91 | 1.95 | 2.15 | 2.22 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

| Dependent Variable: ∂ (LOANSst/VAst) Estimation Method: Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | 0.000108 ** (4.73 × 10−5) | 0.000108 ** (4.68 × 10−5) | 0.000106 ** (4.66 × 10−5) | 6.06 × 10−5 (6.29 × 10−5) | 7.52 × 10−5 (6.27 × 10−5) |

| ∂(LOANSst−1/VAst−1) | −0.482353 *** (0.077711) | −0.499834 *** (0.088875) | −0.489796 *** (0.084620) | −0.517171 *** (0.102294) | −0.507906 *** (0.099394) |

| ∂(CO2st−1/VAst−1) | 0.034946 (101.3000) | 17.01365 (54.20721) | 25.07819 (49.66097) | 27.33130 (102.4462) | 42.38499 (80.96355) |

| ∂(CO2st−1/VAst−1)*D2009 | 37.65671 (114.5524) | ||||

| ∂(CO2st−1/VAst−1)*D2015 | 53.10270 (108.4535) | 53.81078 (143.8399) | |||

| ∂(CO2st−1/VAst−1)*D2019 | 43.97011 (130.8802) | 6.109926 (153.6854) | |||

| ∂(NPLst/VAst) | 5.249556 *** (1.108305) | 5.179697 *** (1.121878) | 5.256845 *** (1.107102) | 5.062516 *** (1.242459) | 5.185369 *** (1.223347) |

| ∂(INVSETst) | 4.60 × 10−6 (6.22 × 10−6) | 3.10 × 10−6 (3.90 × 10−6) | |||

| ∂(INVSETst)*D2015 | −4.92 × 10−6 (7.68 × 10−6) | ||||

| ∂(INVSETst)*D2019 | −1.24 × 10−5 (1.08 × 10−5) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.29 | 0.29 | 0.29 | 0.29 | 0.29 |

| F-statistic | 7.10 *** | 7.11 *** | 7.10 *** | 6.20 *** | 6.27 *** |

| DW | 2.02 | 2.00 | 2.01 | 2.06 | 2.07 |

| Cross-section fixed effects | No | No | No | No | No |

| Period fixed effects | Yes | Yes | Yes | Yes | Yes |

| Dependent Variable: ∂ (LOANSst/TOTLOANSt) Panel Least Squares | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| C | −7.27 × 10−5 (0.000230) | −7.60 × 10−5 (0.000231) | −6.88 × 10−5 (0.000231) | −0.000193 (0.000267) | −2.75 × 10−5 (0.000237) |

| ∂(LOANSst−1/TOTLOANSst−1) | 0.037549 (0.057682) | 0.028030 (0.057683) | 0.032655 (0.057911) | −0.102445 (0.071716) | −0.109850 (0.068636) |

| ∂(NPLst/TOTNPLt) | −0.005619 (0.023577) | −0.008645 (0.023576) | −0.013111 (0.023787) | −0.008070 (0.029148) | −0.000803 (0.029555) |

| ∂(VAst/VASUMt) | 0.211107 *** (0.053668) | 0.188687 *** (0.053622) | 0.195376 *** (0.053291) | 0.193403 *** (0.059897) | 0.179784 *** (0.058161) |

| ∂(CO2st−1/CO2TOTt−1) | 0.138469 (0.097496) | −0.007488 (0.034973) | −0.018523 (0.031271) | −0.140547 ** (0.060907) | −0.110679 ** (0.04489) |

| ∂(CO2st−1/CO2TOTt−1)*D2009 | −0.189784 (0.104224) | ||||

| ∂(CO2st−1/CO2TOTt−1)*D2015 | −0.066906 (0.057572) | 0.065822 (0.072479) | |||

| ∂(CO2st−1/CO2TOTt−1)*D2019 | −0.068727 (0.071192) | 0.019273 (0.073653) | |||

| ∂(INVSETst/INVTOTt) | 0.005097 (0.008220) | −0.000203 (0.000275) | |||

| ∂(INVSETst/INVTOTt)*D2015 | −0.005304 (0.008195) | ||||

| ∂(INVSETst/INVTOTt)*D2019 | −0.010148 *** (0.003597) | ||||

| Sample | 2007–2021 | 2007–2021 | 2007–2021 | 2010–2021 | 2010–2021 |

| Total Observations | 270 | 270 | 270 | 216 | 216 |

| Adjusted R-squared | 0.20 | 0.19 | 0.19 | 0.15 | 0.17 |

| F-statistic | 4.01 *** | 3.90 *** | 3.87 *** | 2.53 *** | 2.90 *** |

| DW | 2.09 | 2.09 | 2.10 | 1.88 | 1.90 |

| Cross-section fixed effects | Yes | Yes | Yes | Yes | Yes |

| Period fixed effects | No | No | No | No | No |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Forte, A.; Sahan, S.; Silipo, D.B. Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors? Sustainability 2024, 16, 3943. https://doi.org/10.3390/su16103943

Forte A, Sahan S, Silipo DB. Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors? Sustainability. 2024; 16(10):3943. https://doi.org/10.3390/su16103943

Chicago/Turabian StyleForte, Antonio, Selay Sahan, and Damiano B. Silipo. 2024. "Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors?" Sustainability 16, no. 10: 3943. https://doi.org/10.3390/su16103943

APA StyleForte, A., Sahan, S., & Silipo, D. B. (2024). Do Natural Disasters Reduce Loans to the More CO2-Emitting Sectors? Sustainability, 16(10), 3943. https://doi.org/10.3390/su16103943