Dynamic Connectedness and Portfolio Diversification during the Coronavirus Disease 2019 Pandemic: Evidence from the Cryptocurrency Market

Abstract

:1. Introduction

2. Materials and Methods

2.1. Data

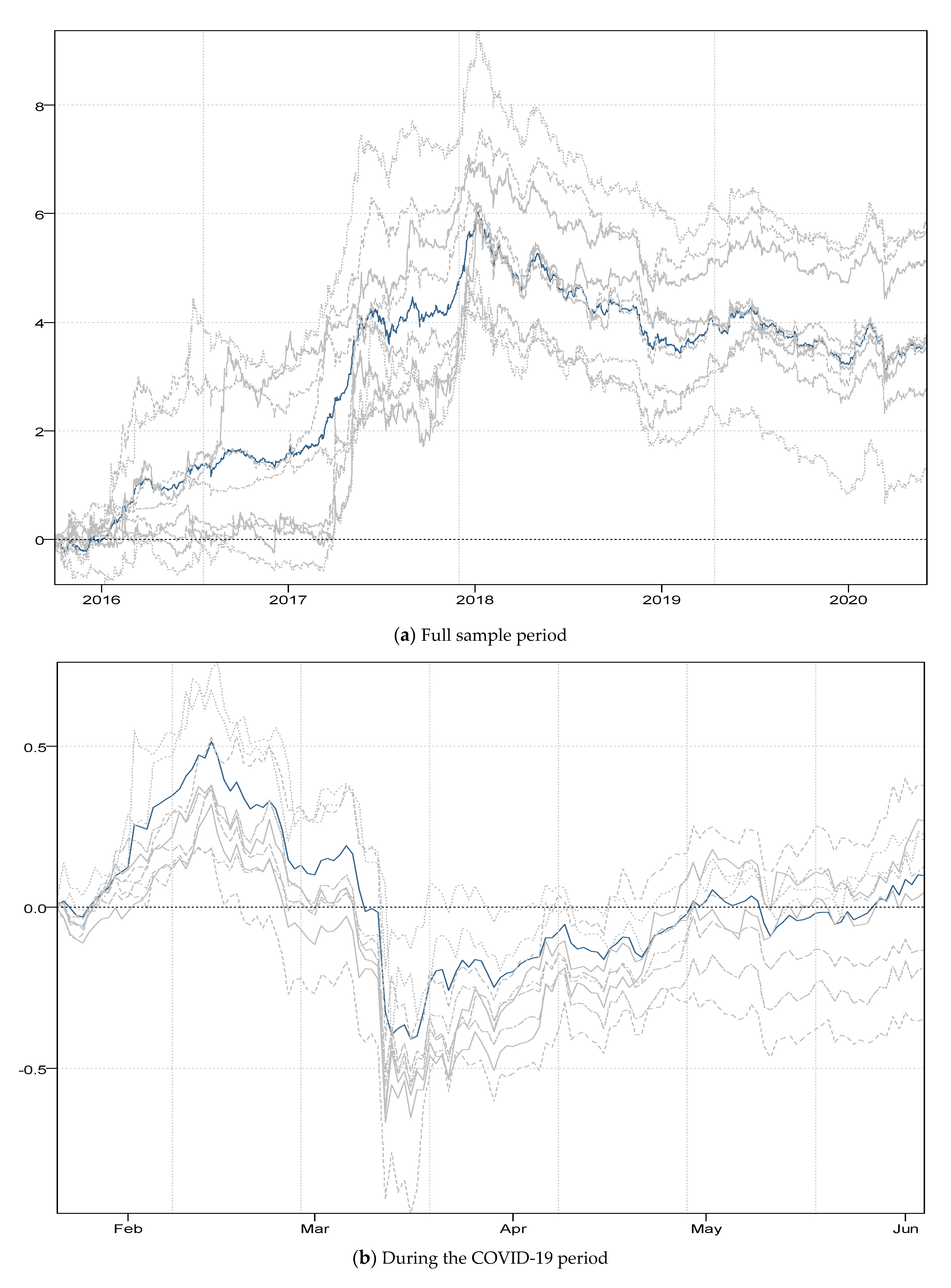

2.2. Econometric Methods

3. Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| USD | US dollars |

| TVP-VAR | time-varying parameter vector autoregression |

| COVID-19 | coronavirus disease 2019 |

| HE | hedge effectiveness index |

References

- Ji, Q.; Bouri, E.; Keung, C.; Lau, M.; Rauboud, D. Dynamic connectedness and integration in cryptocurrency markets. Int. Rev. Financ. Anal. 2019, 63, 257–272. [Google Scholar] [CrossRef]

- Brauneis, A.; Mestel, R. Price discovery of cryptocurrencies: Bitcoin and beyond. Econ. Lett. 2018, 165, 58–61. [Google Scholar] [CrossRef]

- Aggarwal, M.D. Do bitcoins follow a random walk model? Res. Econ. 2019, 73, 15–22. [Google Scholar] [CrossRef]

- Bundi, N.; Wildi, M. Bitcoin and market-(in)efficiency: A systematic time series approach. Digit. Financ. 2019, 1, 47–65. [Google Scholar] [CrossRef] [Green Version]

- Chaim, P.; Laurini, M. Is bitcoin a bubble? Phys. A 2019, 517, 222–232. [Google Scholar] [CrossRef]

- Zargar, F.N.; Kumar, D. Informational inefficiency of bitcoin: A study based on high-frequency data. Res. Int. Bus. Financ. 2019, 47, 344–353. [Google Scholar] [CrossRef]

- Tran, V.; Leirvik, T. Efficiency in the markets of crypto-currencies. Financ. Res. Lett. 2020, 35, 101382. [Google Scholar] [CrossRef]

- Ahelegbey, D.F.; Giudici, P.; Mojtahedi, F. Tail risk measurement in crypto-asset markets. Int. Rev. Financ. Anal. 2021, 73, 101604. [Google Scholar] [CrossRef]

- Caporale, G.M.; Zekokh, T. Modelling volatility of cryptocurrencies using Markov-switching GARCH models. Res. Int. Bus. Financ. 2019, 48, 143–155. [Google Scholar] [CrossRef]

- Katsiampa, P.; Corbet, S.; Lucey, B. Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Financ. Res. Lett. 2019, 29, 68–74. [Google Scholar] [CrossRef] [Green Version]

- Palamalai, S.; Maity, B. Return and volatility spillover effects in leading cryptocurrencies. Glob. Econ. J. 2019, 19, 1950017. [Google Scholar] [CrossRef]

- Moratis, G. Quantifying the spillover effect in the cryptocurrency market. Financ. Res. Lett. 2020, 38, 101534. [Google Scholar] [CrossRef]

- Bouri, E.; Jalkh, N.; Molnár, P.; Roubaud, D. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Appl. Econ. 2017, 49, 5063–5073. [Google Scholar] [CrossRef]

- Bouri, E.; Molnár, P.; Azzi, G.; Roubaud, D.; Hagfors, L.I. On the hedge and safe haven properties of bitcoin: Is it really more than a diversifier? Financ. Res. Lett. 2017, 20, 192–198. [Google Scholar] [CrossRef]

- Corbet, S.; Meegan, A.; Larkin, C.; Lucey, B.; Yarovaya, L. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Econ. Lett. 2018, 165, 28–34. [Google Scholar] [CrossRef] [Green Version]

- Demir, E.; Bilgin, M.H.; Karabulut, G.; Doker, A.C. The relationship between cryptocurrencies and COVID-19 pandemic. Eurasian Econ. Rev. 2020, 10, 349–360. [Google Scholar] [CrossRef]

- Demiralay, S.; Golitsis, P. On the dynamic equicorrelations in cryptocurrency market. Q. Rev. Econ. Financ. 2021, 80, 524–533. [Google Scholar] [CrossRef]

- González, M.D.L.O.; Jareño, F.; Skinner, F.S. Asymmetric interdependencies between large capital cryptocurrency and gold returns during the COVID-19 pandemic crisis. Int. Rev. Financ. Anal. 2021, 76, 101773. [Google Scholar] [CrossRef]

- Guesmi, K.; Saadi, S.; Abid, I.; Ftiti, Z. Portfolio diversification with virtual currency: Evidence from bitcoin. Int. Rev. Financ. Anal. 2019, 63, 431–437. [Google Scholar] [CrossRef]

- Jiang, Y.; Wu, L.; Tian, G.; Nie, H. Do cryptocurrencies hedge against EPU and the equity market volatility during COVID-19?—New evidence from quantile coherency analysis. J. Int. Financ. Mark. Inst. Money 2021, 72, 101324. [Google Scholar] [CrossRef]

- Stensås, A.; Nygaard, M.F.; Kyaw, K.; Treepongkaruna, S. Can bitcoin be a diversifier, hedge or safe haven tool? Cogent Econ. Financ. 2019, 7, 1593072. [Google Scholar] [CrossRef]

- Gopinath, G. The Great Lockdown: Worst Economic Downturn Since the Great Depression. IMF Blog. Available online: https://blogs.imf.org/2020/04/14/the-great-lockdown-worst-economic-downturn-since-the-great-depression (accessed on 14 April 2020).

- Akhtaruzzaman, M.; Boubaker, S.; Lucey, B.M.; Sensoy, A. Is gold a hedge or safe haven asset during COVID-19 crisis? Econ. Model. 2021, 105588, forthcoming. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Financ. Res. Lett. 2020, 35, 101554. [Google Scholar] [CrossRef]

- Goodell, J.W.; Goutte, S. Co-movement of COVID-19 and bitcoin: Evidence from wavelet coherence analysis. Financ. Res. Lett. 2021, 38, 101625. [Google Scholar] [CrossRef]

- Liu, H.Y.; Manzoor, A.; Wang, C.Y.; Zhang, L.; Manzoor, Z. The COVID-19 outbreak and affected countries stock markets response. Int. J. Environ. Res. Public Health 2020, 17, 2800. [Google Scholar] [CrossRef] [Green Version]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 Pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Vidal-Tomás, D. Transitions in the cryptocurrency market during the COVID-19 pandemic: A network analysis. Financ. Res. Lett. 2021, 101981, forthcoming. [Google Scholar] [CrossRef]

- Yarovaya, L.; Brzeszczynski, J.; Goodell, J.W.; Lucey, B.M.; Lau, C.K. Rethinking financial contagion: Information transmission mechanism during the COVID-19 pandemic. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 36, 101528. [Google Scholar] [CrossRef]

- Conlon, T.; Mcgee, R. Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Financ. Res. Lett. 2020, 35, 101607. [Google Scholar] [CrossRef] [PubMed]

- Kouttmos, D. Return and volatility spillovers among cryptocurrencies. Econ. Lett. 2018, 173, 122–127. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Kroner, K.F.; Ng, V.K. Modeling asymmetric comovement of asset returns. Rev. Financ. Stud. 1998, 11, 817–844. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Chatziantoniou, I.; Gabauer, D. Minimum Connectedness Portfolios and the Market for Green Bonds: Advocating Socially Responsible Investment (SRI) Activity. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Antonakakis, N.; Chatziantoniou, I.; Gabauer, D. Cryptocurrency market contagion: Market uncertainty, market complexity, and dynamic portfolios. J. Int. Financ. Mark. Inst. Money 2019, 61, 37–51. [Google Scholar] [CrossRef] [Green Version]

- Diebold, F.X.; Yılmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econom. 2014, 182, 119–134. [Google Scholar] [CrossRef] [Green Version]

- Koop, G.; Pesaran, M.H.; Potter, S.M. Impulse response analysis in nonlinear multivariate models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Chatziantoniou, I.; Gabauer, D. EMU risk-synchronisation and financial fragility through the prism of dynamic connectedness. Q. Rev. Econ. Financ. 2021, 79, 1–14. [Google Scholar] [CrossRef]

- Gabauer, D. Dynamic measures of asymmetric & pairwise connectedness within an optimal currency area: Evidence from the ERM I system. J. Multinatl. Financ. Manag. 2021, 60, 100680. [Google Scholar]

- Kroner, K.F.; Sultan, J. Time-varying distributions and dynamic hedging with foreign currency futures. J. Financ. Quant. Anal. 1993, 28, 535–551. [Google Scholar] [CrossRef]

- Ederington, L.H. The hedging performance of the new futures markets. J. Financ. 1979, 34, 157–170. [Google Scholar] [CrossRef]

- Antonakakis, N.; Cunado, J.; Filis, G.; Gabauer, D.; de Gracia, F.P. Oil and asset classes implied volatilities: Investment strategies and hedging effectiveness. Energy Econ. 2020, 91, 104762. [Google Scholar] [CrossRef]

- Bonga-Bonga, L.; Umoetok, E. The effectiveness of index futures hedging in emerging markets during the crisis period of 2008-2010: Evidence from South Africa. Appl. Econ. 2016, 48, 3999–4018. [Google Scholar] [CrossRef] [Green Version]

- Batten, J.A.; Kinateder, H.; Szilagyi, P.G.; Wagner, N.F. Hedging stock with oil. Energy Econ. 2021, 93, 104422. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Mean | S.D. | Minimum | Maximum | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| XLM | 0.219 | 7.725 | −41.49 | 69.84 | 1.822 | 19.35 |

| ETH | 0.341 | 6.350 | −56.56 | 30.06 | −0.253 | 10.07 |

| XEM | 0.335 | 7.835 | −36.29 | 87.06 | 1.810 | 18.61 |

| BTC | 0.218 | 4.113 | −47.05 | 22.40 | −0.899 | 15.86 |

| XRP | 0.210 | 6.999 | −63.65 | 100.8 | 2.544 | 40.46 |

| LTC | 0.161 | 5.714 | −45.87 | 55.67 | 1.194 | 17.22 |

| XMR | 0.300 | 6.479 | −48.43 | 59.63 | 0.827 | 13.10 |

| DASH | 0.205 | 5.944 | −47.45 | 42.56 | 0.543 | 10.81 |

| BTS | 0.075 | 7.434 | −49.43 | 51.67 | 0.683 | 11.89 |

| Full Sample Period | COVID-19 Period | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | 5% | 95% | HE | Prob. | Mean | S.D. | 5% | 95% | HE | Prob. | |

| XLM | 0.1 | 0.04 | 0.03 | 0.17 | 0.72 | 0 | 0.05 | 0.06 | 0 | 0.14 | 0.49 | 0 |

| ETH | 0.06 | 0.07 | 0 | 0.17 | 0.58 | 0 | 0 | 0 | 0 | 0 | 0.63 | 0 |

| XEM | 0.14 | 0.03 | 0.09 | 0.18 | 0.73 | 0 | 0.22 | 0.02 | 0.17 | 0.25 | 0.46 | 0.01 |

| BTC | 0.1 | 0.07 | 0 | 0.23 | 0 | 0 | 0.03 | 0.03 | 0 | 0.08 | 0.41 | 0.37 |

| XRP | 0.14 | 0.05 | 0.08 | 0.24 | 0.66 | 0 | 0.14 | 0.07 | 0.04 | 0.24 | 0.36 | 0.09 |

| LTC | 0.09 | 0.06 | 0 | 0.17 | 0.48 | 0 | 0 | 0 | 0 | 0.01 | 0.53 | 0.01 |

| XMR | 0.07 | 0.06 | 0 | 0.15 | 0.6 | 0 | 0.08 | 0.03 | 0 | 0.12 | 0.51 | 0 |

| DASH | 0.13 | 0.05 | 0.05 | 0.24 | 0.52 | 0 | 0.19 | 0.03 | 0.14 | 0.21 | 0.6 | 0 |

| BTS | 0.17 | 0.08 | 0.01 | 0.26 | 0.69 | 0 | 0.29 | 0.03 | 0.27 | 0.36 | 0.69 | 0.01 |

| Full Sample Period | COVID-19 Period | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | 5% | 95% | HE | p Value | Mean | S.D. | 5% | 95% | HE | p Value | |

| XLM/ETH | 0.38 | 0.27 | 0 | 0.89 | 0.52 | 0 | 0.84 | 0.26 | 0.21 | 1 | −0.01 | 0.94 |

| XLM/XEM | 0.5 | 0.3 | 0 | 1 | 0.31 | 0 | 0.43 | 0.42 | 0 | 1 | 0.22 | 0.15 |

| XLM/BTC | 0.14 | 0.17 | 0 | 0.49 | 0.72 | 0 | 0.47 | 0.35 | 0 | 0.99 | 0.06 | 0.7 |

| XLM/XRP | 0.27 | 0.3 | 0 | 0.95 | 0.4 | 0 | 0.19 | 0.34 | 0 | 1 | 0.21 | 0.18 |

| XLM/LTC | 0.34 | 0.25 | 0 | 0.79 | 0.49 | 0 | 0.49 | 0.39 | 0 | 1 | 0.07 | 0.66 |

| XLM/XMR | 0.43 | 0.26 | 0 | 0.84 | 0.49 | 0 | 0.38 | 0.41 | 0 | 1 | 0.05 | 0.76 |

| XLM/DASH | 0.36 | 0.27 | 0 | 0.91 | 0.56 | 0 | 0.53 | 0.41 | 0 | 1 | 0.05 | 0.77 |

| XLM/BTS | 0.5 | 0.19 | 0.16 | 0.85 | 0.37 | 0 | 0.53 | 0.12 | 0.32 | 0.71 | 0.04 | 0.83 |

| ETH/XLM | 0.62 | 0.27 | 0.11 | 1 | 0.29 | 0 | 0.16 | 0.26 | 0 | 0.79 | 0.26 | 0.08 |

| ETH/XEM | 0.62 | 0.27 | 0.13 | 1 | 0.24 | 0 | 0.29 | 0.34 | 0 | 0.85 | 0.4 | 0 |

| ETH/BTC | 0.15 | 0.2 | 0 | 0.55 | 0.6 | 0 | 0.29 | 0.38 | 0 | 1 | 0.31 | 0.03 |

| ETH/XRP | 0.41 | 0.31 | 0 | 1 | 0.4 | 0 | 0.03 | 0.12 | 0 | 0.23 | 0.42 | 0 |

| ETH/LTC | 0.47 | 0.31 | 0 | 1 | 0.37 | 0 | 0.13 | 0.3 | 0 | 1 | 0.21 | 0.16 |

| ETH/XMR | 0.55 | 0.26 | 0.04 | 1 | 0.29 | 0 | 0.14 | 0.3 | 0 | 1 | 0.25 | 0.09 |

| ETH/DASH | 0.44 | 0.29 | 0 | 1 | 0.34 | 0 | 0.3 | 0.36 | 0 | 1 | 0.09 | 0.59 |

| ETH/BTS | 0.57 | 0.2 | 0.23 | 0.94 | 0.32 | 0 | 0.48 | 0.15 | 0.17 | 0.69 | 0.14 | 0.38 |

| XEM/XLM | 0.5 | 0.3 | 0 | 1 | 0.33 | 0 | 0.57 | 0.42 | 0 | 1 | 0.17 | 0.28 |

| XEM/ETH | 0.38 | 0.27 | 0 | 0.87 | 0.5 | 0 | 0.71 | 0.34 | 0.15 | 1 | 0.13 | 0.44 |

| XEM/BTC | 0.13 | 0.19 | 0 | 0.53 | 0.71 | 0 | 0.53 | 0.43 | 0 | 1 | 0.1 | 0.55 |

| XEM/XRP | 0.32 | 0.26 | 0 | 0.87 | 0.47 | 0 | 0.48 | 0.38 | 0 | 1 | 0.21 | 0.17 |

| XEM/LTC | 0.34 | 0.27 | 0 | 0.85 | 0.52 | 0 | 0.65 | 0.4 | 0 | 1 | 0.06 | 0.72 |

| XEM/XMR | 0.43 | 0.26 | 0 | 0.88 | 0.49 | 0 | 0.62 | 0.37 | 0 | 1 | 0.09 | 0.6 |

| XEM/DASH | 0.35 | 0.27 | 0 | 0.92 | 0.54 | 0 | 0.68 | 0.34 | 0.06 | 1 | 0.1 | 0.52 |

| XEM/BTS | 0.49 | 0.21 | 0.11 | 0.85 | 0.37 | 0 | 0.57 | 0.14 | 0.28 | 0.74 | 0.03 | 0.86 |

| BTC/XLM | 0.86 | 0.17 | 0.51 | 1 | 0 | 1 | 0.53 | 0.35 | 0.01 | 1 | −0.08 | 0.66 |

| BTC/ETH | 0.85 | 0.2 | 0.45 | 1 | 0.04 | 0.37 | 0.71 | 0.38 | 0 | 1 | −0.1 | 0.6 |

| BTC/XEM | 0.87 | 0.19 | 0.47 | 1 | −0.06 | 0.2 | 0.47 | 0.43 | 0 | 1 | 0.02 | 0.9 |

| BTC/XRP | 0.76 | 0.25 | 0.26 | 1 | 0.05 | 0.24 | 0.3 | 0.39 | 0 | 1 | 0.03 | 0.88 |

| BTC/LTC | 0.85 | 0.25 | 0.24 | 1 | −0.07 | 0.15 | 0.49 | 0.41 | 0 | 1 | −0.1 | 0.59 |

| BTC/XMR | 0.88 | 0.17 | 0.53 | 1 | 0.01 | 0.91 | 0.38 | 0.45 | 0 | 1 | −0.06 | 0.75 |

| BTC/DASH | 0.8 | 0.22 | 0.36 | 1 | 0.07 | 0.16 | 0.52 | 0.38 | 0 | 1 | −0.06 | 0.75 |

| BTC/BTS | 0.76 | 0.16 | 0.49 | 1 | 0.1 | 0.03 | 0.55 | 0.07 | 0.46 | 0.65 | 0.23 | 0.12 |

| XRP/XLM | 0.73 | 0.3 | 0.05 | 1 | 0.27 | 0 | 0.81 | 0.34 | 0 | 1 | 0 | 1 |

| XRP/ETH | 0.59 | 0.31 | 0 | 1 | 0.5 | 0 | 0.97 | 0.12 | 0.77 | 1 | −0.01 | 0.95 |

| XRP/XEM | 0.68 | 0.26 | 0.13 | 1 | 0.34 | 0 | 0.52 | 0.38 | 0 | 1 | 0.06 | 0.71 |

| XRP/BTC | 0.24 | 0.25 | 0 | 0.74 | 0.67 | 0 | 0.7 | 0.39 | 0 | 1 | −0.06 | 0.72 |

| XRP/LTC | 0.53 | 0.31 | 0 | 1 | 0.46 | 0 | 0.85 | 0.31 | 0.04 | 1 | 0 | 0.98 |

| XRP/XMR | 0.63 | 0.28 | 0.05 | 1 | 0.47 | 0 | 0.81 | 0.27 | 0.12 | 1 | −0.01 | 0.93 |

| XRP/DASH | 0.52 | 0.27 | 0.06 | 1 | 0.51 | 0 | 0.85 | 0.25 | 0.19 | 1 | 0 | 1 |

| XRP/BTS | 0.6 | 0.21 | 0.2 | 0.96 | 0.36 | 0 | 0.6 | 0.15 | 0.24 | 0.78 | −0.17 | 0.36 |

| LTC/XLM | 0.66 | 0.25 | 0.21 | 1 | 0.06 | 0.17 | 0.51 | 0.39 | 0 | 1 | 0.15 | 0.35 |

| LTC/ETH | 0.53 | 0.31 | 0 | 1 | 0.22 | 0 | 0.87 | 0.3 | 0 | 1 | 0.01 | 0.97 |

| LTC/XEM | 0.66 | 0.27 | 0.15 | 1 | 0.1 | 0.02 | 0.35 | 0.4 | 0 | 1 | 0.19 | 0.23 |

| LTC/BTC | 0.15 | 0.25 | 0 | 0.76 | 0.44 | 0 | 0.51 | 0.41 | 0 | 1 | 0.13 | 0.44 |

| LTC/XRP | 0.47 | 0.31 | 0 | 1 | 0.19 | 0 | 0.15 | 0.31 | 0 | 0.96 | 0.27 | 0.06 |

| LTC/XMR | 0.61 | 0.27 | 0.08 | 1 | 0.2 | 0 | 0.35 | 0.36 | 0 | 1 | 0.01 | 0.96 |

| LTC/DASH | 0.49 | 0.3 | 0 | 1 | 0.23 | 0 | 0.52 | 0.36 | 0.01 | 1 | −0.04 | 0.81 |

| LTC/BTS | 0.61 | 0.16 | 0.41 | 0.92 | 0.23 | 0 | 0.53 | 0.14 | 0.21 | 0.69 | −0.02 | 0.91 |

| XMR/XLM | 0.57 | 0.26 | 0.16 | 1 | 0.27 | 0 | 0.62 | 0.41 | 0 | 1 | 0.09 | 0.61 |

| XMR/ETH | 0.45 | 0.26 | 0 | 0.96 | 0.32 | 0 | 0.86 | 0.3 | 0 | 1 | 0.01 | 0.95 |

| XMR/XEM | 0.57 | 0.26 | 0.12 | 1 | 0.25 | 0 | 0.38 | 0.37 | 0 | 1 | 0.17 | 0.27 |

| XMR/BTC | 0.12 | 0.17 | 0 | 0.47 | 0.6 | 0 | 0.62 | 0.45 | 0 | 1 | 0.12 | 0.47 |

| XMR/XRP | 0.37 | 0.28 | 0 | 0.95 | 0.39 | 0 | 0.19 | 0.27 | 0 | 0.88 | 0.22 | 0.14 |

| XMR/LTC | 0.39 | 0.27 | 0 | 0.92 | 0.38 | 0 | 0.65 | 0.36 | 0 | 1 | −0.04 | 0.83 |

| XMR/DASH | 0.38 | 0.28 | 0 | 0.98 | 0.3 | 0 | 0.66 | 0.3 | 0.16 | 1 | −0.05 | 0.79 |

| XMR/BTS | 0.54 | 0.19 | 0.24 | 0.9 | 0.34 | 0 | 0.56 | 0.16 | 0.2 | 0.77 | −0.04 | 0.84 |

| DASH/XLM | 0.64 | 0.27 | 0.09 | 1 | 0.26 | 0 | 0.47 | 0.41 | 0 | 1 | 0.25 | 0.1 |

| DASH/ETH | 0.56 | 0.29 | 0 | 1 | 0.25 | 0 | 0.7 | 0.36 | 0 | 1 | 0.01 | 0.96 |

| DASH/XEM | 0.65 | 0.27 | 0.08 | 1 | 0.2 | 0 | 0.32 | 0.34 | 0 | 0.94 | 0.33 | 0.02 |

| DASH/BTC | 0.2 | 0.22 | 0 | 0.64 | 0.55 | 0 | 0.48 | 0.38 | 0 | 1 | 0.27 | 0.06 |

| DASH/XRP | 0.48 | 0.27 | 0 | 0.94 | 0.32 | 0 | 0.15 | 0.25 | 0 | 0.81 | 0.37 | 0.01 |

| DASH/LTC | 0.51 | 0.3 | 0 | 1 | 0.28 | 0 | 0.48 | 0.36 | 0 | 0.99 | 0.1 | 0.52 |

| DASH/XMR | 0.62 | 0.28 | 0.02 | 1 | 0.17 | 0 | 0.34 | 0.3 | 0 | 0.84 | 0.14 | 0.38 |

| DASH/BTS | 0.59 | 0.18 | 0.25 | 0.91 | 0.32 | 0 | 0.53 | 0.16 | 0.15 | 0.7 | 0.13 | 0.42 |

| BTS/XLM | 0.5 | 0.19 | 0.15 | 0.84 | 0.32 | 0 | 0.47 | 0.12 | 0.29 | 0.68 | 0.41 | 0 |

| BTS/ETH | 0.43 | 0.2 | 0.06 | 0.77 | 0.5 | 0 | 0.52 | 0.15 | 0.31 | 0.83 | 0.28 | 0.06 |

| BTS/XEM | 0.51 | 0.21 | 0.15 | 0.89 | 0.29 | 0 | 0.43 | 0.14 | 0.26 | 0.72 | 0.44 | 0 |

| BTS/BTC | 0.24 | 0.16 | 0 | 0.51 | 0.72 | 0 | 0.45 | 0.07 | 0.35 | 0.54 | 0.59 | 0 |

| BTS/XRP | 0.4 | 0.21 | 0.04 | 0.8 | 0.43 | 0 | 0.4 | 0.15 | 0.22 | 0.76 | 0.43 | 0 |

| BTS/LTC | 0.39 | 0.16 | 0.08 | 0.59 | 0.55 | 0 | 0.47 | 0.14 | 0.31 | 0.79 | 0.32 | 0.03 |

| BTS/XMR | 0.46 | 0.19 | 0.1 | 0.76 | 0.5 | 0 | 0.44 | 0.16 | 0.23 | 0.8 | 0.34 | 0.02 |

| BTS/DASH | 0.41 | 0.18 | 0.09 | 0.75 | 0.56 | 0 | 0.47 | 0.16 | 0.3 | 0.85 | 0.33 | 0.02 |

| Full Sample Period | COVID-19 Period * | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | 5% | 95% | HE | p value | Mean | S.D. | 5% | 95% | HE | p value | |

| ETH/XLM | 0.45 | 0.29 | −0.03 | 0.9 | 0.17 | 0 | 1.05 | 0.17 | 0.82 | 1.38 | 0.8 | 0 |

| XEM/XLM | 0.57 | 0.27 | 0.17 | 1.01 | 0.23 | 0 | 0.73 | 0.21 | 0.45 | 1.06 | 0.65 | 0 |

| BTC/XLM | 0.32 | 0.2 | 0.03 | 0.61 | 0.15 | 0 | 0.83 | 0.13 | 0.6 | 1 | 0.7 | 0 |

| XRP/XLM | 0.59 | 0.24 | 0.22 | 0.95 | 0.32 | 0 | 0.8 | 0.15 | 0.63 | 1.13 | 0.82 | 0 |

| LTC/XLM | 0.47 | 0.27 | 0.08 | 0.87 | 0.17 | 0 | 0.91 | 0.16 | 0.69 | 1.21 | 0.79 | 0 |

| XMR/XLM | 0.49 | 0.25 | 0.07 | 0.87 | 0.25 | 0 | 0.86 | 0.18 | 0.62 | 1.23 | 0.75 | 0 |

| DASH/XLM | 0.43 | 0.28 | 0.04 | 0.87 | 0.16 | 0 | 0.9 | 0.22 | 0.64 | 1.45 | 0.65 | 0 |

| BTS/XLM | 0.22 | 0.24 | −0.04 | 0.72 | 0.02 | 0.69 | −0.02 | 0.02 | −0.05 | 0.01 | −0.12 | 0.5 |

| XLM/ETH | 0.61 | 0.4 | −0.01 | 1.12 | 0.26 | 0 | 0.8 | 0.09 | 0.63 | 0.95 | 0.81 | 0 |

| XEM/ETH | 0.6 | 0.38 | 0.02 | 1.1 | 0.26 | 0 | 0.66 | 0.19 | 0.41 | 0.91 | 0.71 | 0 |

| BTC/ETH | 0.41 | 0.26 | −0.03 | 0.8 | 0.34 | 0 | 0.79 | 0.18 | 0.44 | 1.02 | 0.67 | 0 |

| XRP/ETH | 0.55 | 0.34 | 0.04 | 1.03 | 0.31 | 0 | 0.71 | 0.09 | 0.55 | 0.89 | 0.87 | 0 |

| LTC/ETH | 0.58 | 0.36 | 0 | 1.05 | 0.3 | 0 | 0.84 | 0.1 | 0.68 | 1.04 | 0.89 | 0 |

| XMR/ETH | 0.62 | 0.28 | 0.15 | 1.01 | 0.32 | 0 | 0.78 | 0.12 | 0.6 | 1.01 | 0.85 | 0 |

| DASH/ETH | 0.58 | 0.33 | 0.08 | 1.04 | 0.29 | 0 | 0.81 | 0.14 | 0.61 | 1.07 | 0.69 | 0 |

| BTS/ETH | 0.23 | 0.26 | −0.01 | 0.82 | 0.02 | 0.68 | 0.03 | 0.02 | 0.01 | 0.05 | −0.33 | 0.1 |

| XLM/XEM | 0.57 | 0.34 | 0.11 | 1.05 | 0.25 | 0 | 0.89 | 0.28 | 0.49 | 1.33 | 0.63 | 0 |

| ETH/XEM | 0.45 | 0.28 | 0.03 | 0.91 | 0.12 | 0.01 | 1.05 | 0.34 | 0.59 | 1.59 | 0.64 | 0 |

| BTC/XEM | 0.31 | 0.21 | 0.04 | 0.67 | 0.21 | 0 | 0.84 | 0.28 | 0.51 | 1.27 | 0.6 | 0 |

| XRP/XEM | 0.43 | 0.27 | 0.06 | 0.87 | 0.08 | 0.09 | 0.78 | 0.2 | 0.45 | 1.08 | 0.6 | 0 |

| LTC/XEM | 0.43 | 0.28 | 0.05 | 0.88 | −0.02 | 0.72 | 0.95 | 0.24 | 0.52 | 1.32 | 0.7 | 0 |

| XMR/XEM | 0.45 | 0.26 | 0.05 | 0.87 | 0.16 | 0 | 0.84 | 0.22 | 0.46 | 1.19 | 0.63 | 0 |

| DASH/XEM | 0.43 | 0.28 | 0.04 | 0.9 | 0.16 | 0 | 0.9 | 0.24 | 0.56 | 1.26 | 0.56 | 0 |

| BTS/XEM | 0.17 | 0.23 | −0.05 | 0.67 | −0.01 | 0.84 | −0.04 | 0.02 | −0.08 | −0.01 | −0.06 | 0.74 |

| XLM/BTC | 0.83 | 0.44 | 0.12 | 1.54 | 0.34 | 0 | 0.91 | 0.23 | 0.73 | 1.33 | 0.7 | 0 |

| ETH/BTC | 0.81 | 0.5 | −0.13 | 1.51 | 0.46 | 0 | 1.14 | 0.44 | 0.81 | 2.02 | 0.78 | 0 |

| XEM/BTC | 0.89 | 0.44 | 0.2 | 1.64 | 0.33 | 0 | 0.76 | 0.27 | 0.43 | 1.33 | 0.59 | 0 |

| XRP/BTC | 0.71 | 0.43 | 0.08 | 1.33 | 0.34 | 0 | 0.82 | 0.31 | 0.56 | 1.59 | 0.7 | 0 |

| LTC/BTC | 1.03 | 0.31 | 0.53 | 1.55 | 0.45 | 0 | 0.97 | 0.36 | 0.68 | 1.75 | 0.75 | 0 |

| XMR/BTC | 0.94 | 0.43 | 0.21 | 1.49 | 0.45 | 0 | 0.97 | 0.38 | 0.66 | 1.8 | 0.78 | 0 |

| DASH/BTC | 0.78 | 0.44 | 0.09 | 1.45 | 0.39 | 0 | 0.95 | 0.41 | 0.59 | 2 | 0.63 | 0 |

| BTS/BTC | 0.28 | 0.35 | −0.08 | 1.04 | 0.01 | 0.91 | −0.03 | 0.02 | −0.06 | 0 | −0.05 | 0.79 |

| XLM/XRP | 0.86 | 0.33 | 0.38 | 1.34 | 0.44 | 0 | 1.06 | 0.16 | 0.78 | 1.3 | 0.87 | 0 |

| ETH/XRP | 0.6 | 0.34 | 0.06 | 1.11 | 0.2 | 0 | 1.23 | 0.18 | 0.95 | 1.56 | 0.87 | 0 |

| XEM/XRP | 0.64 | 0.34 | 0.13 | 1.11 | 0.21 | 0 | 0.84 | 0.18 | 0.63 | 1.15 | 0.7 | 0 |

| BTC/XRP | 0.39 | 0.25 | 0.02 | 0.81 | 0.17 | 0 | 0.97 | 0.23 | 0.52 | 1.3 | 0.69 | 0 |

| LTC/XRP | 0.57 | 0.35 | 0.08 | 1.11 | 0.14 | 0 | 1.07 | 0.14 | 0.84 | 1.26 | 0.86 | 0 |

| XMR/XRP | 0.58 | 0.32 | 0.09 | 1.06 | 0.19 | 0 | 0.97 | 0.11 | 0.73 | 1.14 | 0.8 | 0 |

| DASH/XRP | 0.5 | 0.33 | 0.05 | 1.08 | 0.16 | 0 | 1.01 | 0.15 | 0.7 | 1.24 | 0.63 | 0 |

| BTS/XRP | 0.24 | 0.27 | −0.06 | 0.83 | 0.11 | 0.02 | 0.01 | 0.03 | −0.02 | 0.06 | −0.17 | 0.37 |

| XLM/LTC | 0.65 | 0.31 | 0.14 | 1.16 | 0.31 | 0 | 0.89 | 0.13 | 0.7 | 1.1 | 0.82 | 0 |

| ETH/LTC | 0.6 | 0.36 | −0.01 | 1.11 | 0.45 | 0 | 1.07 | 0.13 | 0.82 | 1.28 | 0.89 | 0 |

| XEM/LTC | 0.64 | 0.35 | 0.09 | 1.22 | 0.29 | 0 | 0.77 | 0.18 | 0.55 | 1.12 | 0.74 | 0 |

| BTC/LTC | 0.55 | 0.18 | 0.24 | 0.86 | 0.45 | 0 | 0.86 | 0.19 | 0.48 | 1.12 | 0.74 | 0 |

| XRP/LTC | 0.57 | 0.32 | 0.08 | 1.09 | 0.32 | 0 | 0.8 | 0.1 | 0.66 | 0.99 | 0.86 | 0 |

| XMR/LTC | 0.63 | 0.28 | 0.09 | 1.02 | 0.36 | 0 | 0.88 | 0.12 | 0.68 | 1.09 | 0.84 | 0 |

| DASH/LTC | 0.56 | 0.32 | 0.06 | 1.09 | 0.34 | 0 | 0.9 | 0.13 | 0.72 | 1.16 | 0.69 | 0 |

| BTS/LTC | 0.17 | 0.24 | −0.07 | 0.7 | 0.02 | 0.68 | 0.01 | 0.02 | −0.01 | 0.04 | −0.25 | 0.19 |

| XLM/XMR | 0.59 | 0.35 | 0.11 | 1.08 | 0.27 | 0 | 0.94 | 0.16 | 0.7 | 1.19 | 0.78 | 0 |

| ETH/XMR | 0.57 | 0.26 | 0.13 | 0.96 | 0.3 | 0 | 1.11 | 0.16 | 0.85 | 1.4 | 0.85 | 0 |

| XEM/XMR | 0.54 | 0.31 | 0.08 | 1.01 | 0.21 | 0 | 0.75 | 0.19 | 0.53 | 1.11 | 0.65 | 0 |

| BTC/XMR | 0.4 | 0.21 | 0.05 | 0.74 | 0.32 | 0 | 0.95 | 0.23 | 0.5 | 1.27 | 0.67 | 0 |

| XRP/XMR | 0.47 | 0.3 | 0.07 | 0.91 | 0.25 | 0 | 0.8 | 0.08 | 0.69 | 0.95 | 0.8 | 0 |

| LTC/XMR | 0.52 | 0.28 | 0.07 | 0.94 | 0.27 | 0 | 0.97 | 0.12 | 0.78 | 1.2 | 0.84 | 0 |

| DASH/XMR | 0.56 | 0.28 | 0.11 | 0.99 | 0.31 | 0 | 0.92 | 0.14 | 0.74 | 1.17 | 0.64 | 0 |

| BTS/XMR | 0.18 | 0.24 | −0.06 | 0.73 | 0.03 | 0.54 | 0.03 | 0.02 | 0 | 0.07 | −0.22 | 0.25 |

| XLM/DASH | 0.58 | 0.37 | 0.08 | 1.12 | 0.23 | 0 | 0.84 | 0.16 | 0.53 | 1.08 | 0.62 | 0 |

| ETH/DASH | 0.61 | 0.3 | 0.13 | 1.02 | 0.34 | 0 | 0.99 | 0.17 | 0.75 | 1.3 | 0.71 | 0 |

| XEM/DASH | 0.61 | 0.32 | 0.14 | 1.14 | 0.24 | 0 | 0.7 | 0.17 | 0.48 | 0.95 | 0.58 | 0 |

| BTC/DASH | 0.4 | 0.24 | 0.04 | 0.77 | 0.34 | 0 | 0.8 | 0.21 | 0.4 | 1.13 | 0.51 | 0 |

| XRP/DASH | 0.47 | 0.32 | 0.08 | 0.92 | 0.24 | 0 | 0.72 | 0.1 | 0.56 | 0.91 | 0.65 | 0 |

| LTC/DASH | 0.55 | 0.32 | 0.07 | 1 | 0.3 | 0 | 0.86 | 0.11 | 0.68 | 1 | 0.69 | 0 |

| XMR/DASH | 0.65 | 0.26 | 0.22 | 1.01 | 0.35 | 0 | 0.8 | 0.12 | 0.62 | 0.94 | 0.66 | 0 |

| BTS/DASH | 0.16 | 0.23 | −0.09 | 0.71 | 0 | 0.92 | 0.02 | 0.02 | −0.01 | 0.05 | −0.18 | 0.33 |

| XLM/BTS | 0.23 | 0.28 | −0.04 | 0.69 | 0.12 | 0.01 | −0.02 | 0.03 | −0.06 | 0.01 | −0.01 | 0.96 |

| ETH/BTS | 0.16 | 0.15 | −0.01 | 0.43 | 0.11 | 0.02 | 0.03 | 0.06 | 0.01 | 0.08 | 0 | 0.99 |

| XEM/BTS | 0.17 | 0.22 | −0.06 | 0.53 | 0.07 | 0.13 | −0.03 | 0.03 | −0.07 | 0 | −0.01 | 0.98 |

| BTC/BTS | 0.08 | 0.1 | −0.03 | 0.27 | 0.07 | 0.13 | −0.02 | 0.02 | −0.05 | 0 | −0.01 | 0.96 |

| XRP/BTS | 0.15 | 0.19 | −0.06 | 0.5 | 0.07 | 0.16 | 0 | 0.03 | −0.02 | 0.03 | −0.01 | 0.97 |

| LTC/BTS | 0.09 | 0.13 | −0.07 | 0.31 | 0.03 | 0.52 | 0.01 | 0.04 | −0.02 | 0.05 | −0.01 | 0.98 |

| XMR/BTS | 0.13 | 0.15 | −0.06 | 0.37 | 0.07 | 0.11 | 0.03 | 0.05 | 0 | 0.07 | 0 | 1 |

| DASH/BTS | 0.1 | 0.13 | −0.07 | 0.33 | 0.04 | 0.4 | 0.02 | 0.04 | −0.01 | 0.06 | 0 | 0.98 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nasreen, S.; Tiwari, A.K.; Yoon, S.-M. Dynamic Connectedness and Portfolio Diversification during the Coronavirus Disease 2019 Pandemic: Evidence from the Cryptocurrency Market. Sustainability 2021, 13, 7672. https://doi.org/10.3390/su13147672

Nasreen S, Tiwari AK, Yoon S-M. Dynamic Connectedness and Portfolio Diversification during the Coronavirus Disease 2019 Pandemic: Evidence from the Cryptocurrency Market. Sustainability. 2021; 13(14):7672. https://doi.org/10.3390/su13147672

Chicago/Turabian StyleNasreen, Samia, Aviral Kumar Tiwari, and Seong-Min Yoon. 2021. "Dynamic Connectedness and Portfolio Diversification during the Coronavirus Disease 2019 Pandemic: Evidence from the Cryptocurrency Market" Sustainability 13, no. 14: 7672. https://doi.org/10.3390/su13147672

APA StyleNasreen, S., Tiwari, A. K., & Yoon, S.-M. (2021). Dynamic Connectedness and Portfolio Diversification during the Coronavirus Disease 2019 Pandemic: Evidence from the Cryptocurrency Market. Sustainability, 13(14), 7672. https://doi.org/10.3390/su13147672