1. Introduction

The question of how to promote high-quality development of corporations has aroused great attention from the Chinese government. High-quality development refers to the new concept of “innovation, coordination, greenness, openness, and sharing” put forward by the Party Central Committee with General Secretary Xi Jinping. The aim is to improve supply quantity and quality, to meet the needs of consumption upgrades, to drive innovation, and to promote efficient, balanced, and sustainable development [

1]. High-quality development of corporations is not only driven by incentive policies, but also affected by constraints, among which environmental regulations are particularly critical.

On the one hand, the setting of environmental regulations may increase the expenditure on pollution-controlling equipment, which crowds out productive investment and decreases productivity/financial performance [

2,

3,

4]. This weakens the level of high-quality development. On the other hand, environmental regulation may motivate firms to innovate, which leads to the coordination between environment and economy [

5,

6,

7]. For these contradictory viewpoints, investigating the effects of environmental regulation on high-quality development of corporations not only contributes to the strategy of carbon neutrality and peak carbon emissions, but also improves the firm’s competitiveness and its high-quality development.

Previous studies can be grouped into the following: the first is the connotation and features of high-quality development, such as innovation, coordination, greenness, openness, and sharing [

8], economic development path and economic structure with strong dynamic characteristics, economic development strategies and economic structure and drivers [

9,

10], and technological progress and worker quality [

11].

The second is a measure of high-quality development. High-quality development indicators are generally constructed to cover dimensions, such as innovation and green development. For example, Wei and Li measured the level of China’s high-quality economic development, which included the dimensions of economic structure, innovation drive, resource allocation, market mechanism, regional coordination, product services, infrastructure, ecological civilization, and economic outcomes. Similar cases were included in the studies by Li et al. [

12] and Huang et al. [

13].

The third focuses on the drivers of high-quality development, including ecological and environmental policies [

14,

15], technological innovation [

16,

17,

18], and the degree of openness [

19,

20,

21,

22,

23].

The fourth is the relationship between environmental regulations and corporate technological innovation (or productivity) based on theories of neoclassical tradition or innovation compensation. The former theory posits that the production cost increased by environmental governance has a crowding-out effect on a firm’s technological innovation, that is, environmental regulations reduce technical efficiency (or technological innovation) [

24,

25,

26,

27,

28] or weaken corporate performance [

4,

29,

30]. Innovation compensation emphasizes that regulated firms can improve their resource allocation and technological progress [

31,

32]. The literature on Mainland China [

33,

34,

35,

36,

37], Taiwan [

38], and India [

39] confirm the innovation compensation hypothesis. However, there are few studies that prove the uncertainty effect of environmental regulation on technological innovation or firm profitability [

40,

41].

To summarize, although a number of studies have provided valuable investigations into the connotation, measurement, and drivers of high-quality development, and the micro effects of environmental regulation, relatively little is known about the relationship between environment regulation and high-quality development of corporations. In particular, environmental regulation may show the greatest effects on energy-intensive firms with the features of high energy consumption and severe pollution, although the existing literature lacks analysis of this specific type of firm. For these reasons, we calculated the indexes of high-quality development of corporations using entropy weighting for the five dimensions of efficiency, innovation, openness, greenness, and social responsibility. Then, using the responsibility system for environmental protection targets (RSEPT) as a measure of environmental regulation, we have developed a difference-in-differences model to reveal its dampening effect on corporate high-quality development.

Our study contributes to several strands. It extends the study of high-quality development. Previous studies that related to high-quality development mainly covered the macro/medium scope, but we focused on corporate high-quality development by synthesizing it into a single indictor.

Our study also contributes to the effect of environmental regulations by considering the RSEPT. Different from the previous studies that focused on the socio-economic development, structural transformation, firm technological innovation, and production efficiency affected by environmental regulation, our paper, for the first time, considers the effect of RSEPT, which is one of the specific, key forms of environmental regulation.

Finally, we propose that environmental regulation for energy-intensive firms under the background of carbon neutrality should be prudent and orderly. Most prior studies suggested that environmental regulation promoted a firm’s economic development through technological innovation, but our paper fails to prove the positive role of environmental regulation on energy-intensive firms. Therefore, environmental regulation policies should be implemented cautiously and orderly instead of radically.

The remainder of this paper is organized as follows.

Section 2 outlines institutional background and research hypotheses.

Section 3 introduces the methodology and variables.

Section 4 investigates the effects of RSEPT on the high-quality development of energy-intensive firms. This section also examines the mediating mechanism from the perspective of efficiency of capital allocation.

Section 5 and

Section 6 show the robustness tests and discussion, respectively.

Section 7 provides a conclusion and policy implications.

2. Institutional Background and Research Hypotheses

2.1. Institutional Background

In China, environmental issues have aroused great concern since the end of the 1980s, as the first Law of the People’s Republic of China on Environmental Protection was formally promulgated in 1989. Following both the successive promulgation of “China’s 21st Century Agenda” and “the Ninth Five-Year Plan (1996–2000) for National Economic and Social Development and the Long-range” in 1994 and 1996, respectively, and General Secretary Hu Jintao’s comments on the relationship between economic development and environmental protection in 2003, China has moved from a strategy of sustainable development to a scientific outlook on development. Before 2006, although China had implemented a number of environmental pollution control policies, such as the “Regulations on the Environmental Management of Construction Projects” (1998), “The Atmospheric Pollution Prevention and Control Law of the People’s Republic of China” (2000), “The Law of the People’s Republic of China on Environmental Impact Assessment” (2003), and “Interim Measures on Cleaner Production Audits” (2004), the policy which caused the transition from environmental objectives with soft constraints to ones with hard constraints was RSEPT.

At the end of December 2005, The State Council developed the policy of “Environmental Performance Assessment”. In March 2006, “The 11th Five-Year Plan for National Economic and Social Development of the People’s Republic of China” proposed for the first time that environmental indicators, such as pollutant emissions and energy consumption per unit of GDP, should be included in the assessment process for political promotion of local government officials. Subsequently, a series of national institutions also issued specific assessment documents, and the leaders of each province signed responsibility documents for environmental protection targets. Local governments further required the key polluting firms in each city, district, and county under its jurisdiction to report pollution data on time and to make them public regularly. The reported data and assessment results served as one of the important criteria for political promotion or dismissal of leaders.

For the first time, China put forward the concept of high-quality development at the 19th National Congress of the Communist Party of China, and followed it up with the enactment of successive policies, such as “Opinions on Promoting the High-quality Development of National High-tech Industrial Development Zone” (2020), Several Policies to Promote the High-quality Development of Integrated Circuit Industry and Software Industry in the New Period” (2020), “Policies and Measures for High-quality Development Promoting the Private Economy” (2021), “Promoting High-quality Development of Digital Culture Industry” (2021), and other policies to provide support for high-quality development. However, current policies focus on high-quality development at the macro/industrial level. The definition and evaluation of high-quality indicators for firms that were originally defined in “Corporate High-quality Evaluation Indicators” was not enacted until 2021.

2.2. Research Hypothesis

The relationship between environmental regulation and corporate high-quality development can be expressed using the theories titled “cost effect” and “innovation compensation effect”. According to the cost effect theory, environmental regulation policies limit emission standards or emissions of pollutants. To meet the technological standards, firms increase the innovation costs in upgrading environment protection equipment. Additionally, firms raise the innovation costs due to environmental taxes, or additional sewage charges levied by the governments. If the firm has limited capital, the increased investment in environmental protection will cause a “crowding out” effect on technological innovation and input of production factors, which leads to a decline in that firm’s income [

42]. Environmental regulation policies may also restrict both the production and scope of operation of energy-intensive firms, thus reducing production efficiency and market share [

43]. Some studies show that environmental regulation has a stronger dampening effect on imports and exports of energy-intensive firms [

44]. In terms of corporate social responsibility, the environmental governance cost of energy-intensive firms is higher than that of other types of firms, which may lead to lowered profits and reduced wages for workers [

45]. Moreover, although energy-intensive firms may disclose more accounting information under environmental regulation pressure, they may also adopt negative earnings management to avoid paying taxes or for other reasons. Energy-intensive firms will attract sympathy from the government due to these poor management operating conditions [

46,

47]. Due to this, environmental regulations may cause firms to reduce their contribution to social responsibility, which would affect their high-quality development.

The innovation compensation theory states that, although firms are forced to bear more costs due to environmental constraints, they may also be stimulated to innovate. The innovations will increase productivity and profitability of firms, which offsets the costs caused by environmental regulation [

6]. The innovation compensation theory, which is supported by a number of empirical studies, is also known as the “Porter Hypothesis”. Environmental regulations stipulate specific standards for pollutant discharge that encourage a firms’ self-supervision. Firms seek a better market share [

48] and export international competitiveness [

49] by improving their own technical standards. Finally, in terms of corporate social responsibility to the employees, environmental regulations cause contradictory effects on employee wages. The formulation of short-term environmental regulation policies may reduce employee wages due to a firm’s motivation to reduce costs, but long-term environmental regulation policies promote green development and provide people with more employment opportunities [

50]. In terms of corporate social responsibility to the government, environmental regulations stimulate energy-intensive firms to adopt more transparent disclosure of their environmental information, which reduce the motivation to avoid corporate taxes [

51]. The policies that enable firms to adopt initiatives to assume their social responsibility to pay taxes contributes to corporate high-quality development.

Motivated by the reasons given above, we propose our first competing hypotheses:

Hypothesis 1 (H1a). The RSEPT promotes high-quality development of energy-intensive firms.

Hypothesis 1 (H1b). The RSEPT dampens high-quality development of energy-intensive firms.

As one of the main initiatives of environmental regulation, RSEPT may affect the efficiency of capital allocation by corporations. Some studies have documented the environmental laws and regulations that significantly restrain excessive management of capital by firms [

52]. Through “green cleaning” behavior, firms can enjoy low loan interest rates for environmental governance, reduce pollution control costs, and, therefore, allocate firms’ internal resources more rationally [

53]. However, the contradictory viewpoint suggests that the positive externality of environmental protection can hardly bring direct benefits to the capital allocation of firms. While implementing environmental regulation policies, the collection of environmental taxes and related fines and the setting of energy consumption standards may cause a crisis of confidence between consumers and investors. This will lead to tight commercial credit and financing difficulties [

54], further distorting the efficiency of capital allocation [

55]. According to Jiang and Li [

56], local officials may deliberately change their environmental governance decisions so that firms can benefit from their own political interests. To achieve “short-term performance”, the government may invest in projects that benefit officials rather than consumers, which easily result in excessive investment, redundant construction, and overcapacity. Combining environmental assessment with the promotions assessment of officials reduces the efficiency of capital allocation and further dampens corporate high-quality development.

Hence, we propose the following hypothesis:

Hypothesis 2 (H2). The efficiency of corporate capital allocation mediates the effects of RSPET on high-quality development of energy-intensive firms.

7. Conclusions and Policy Recommendations

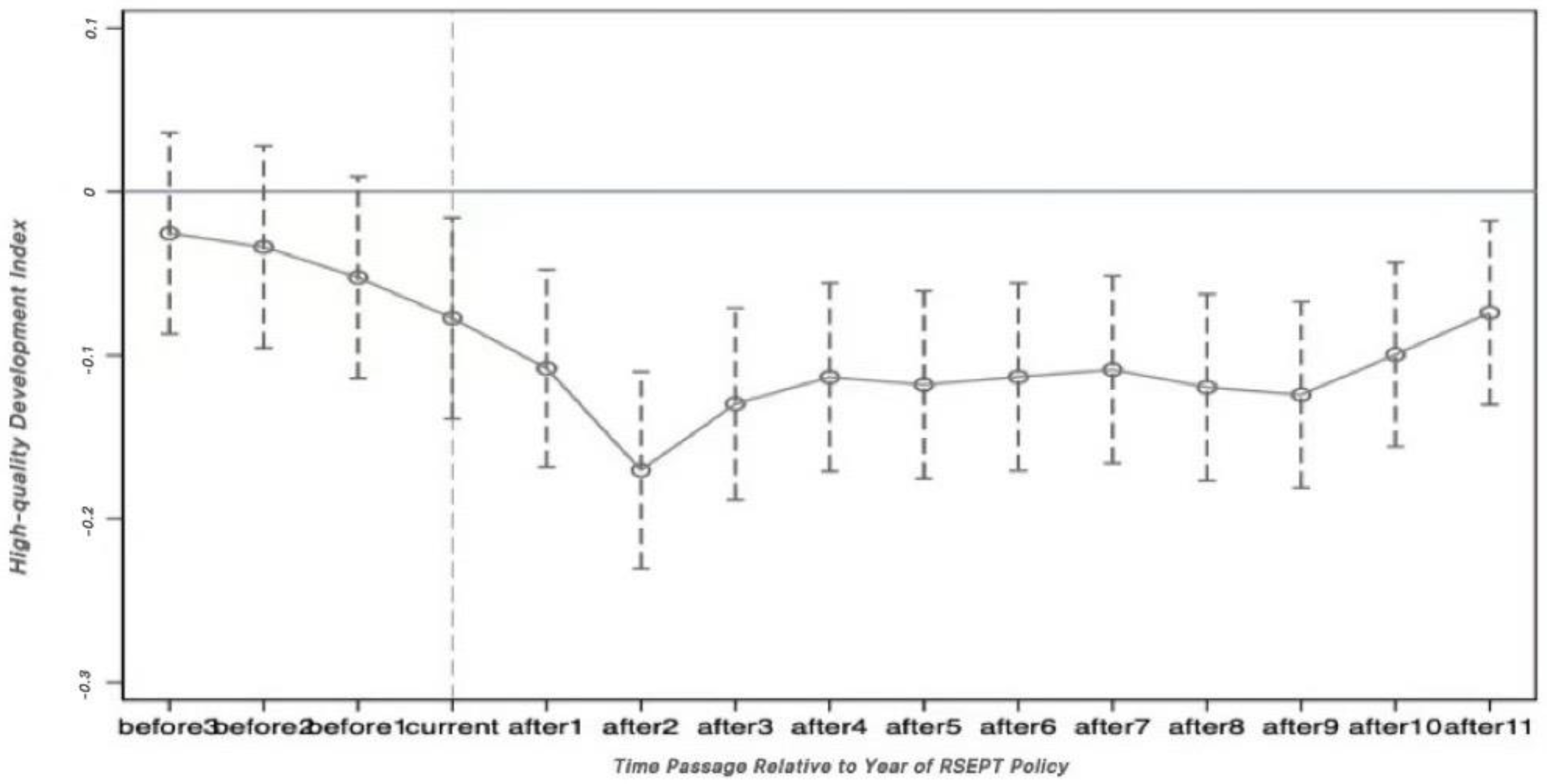

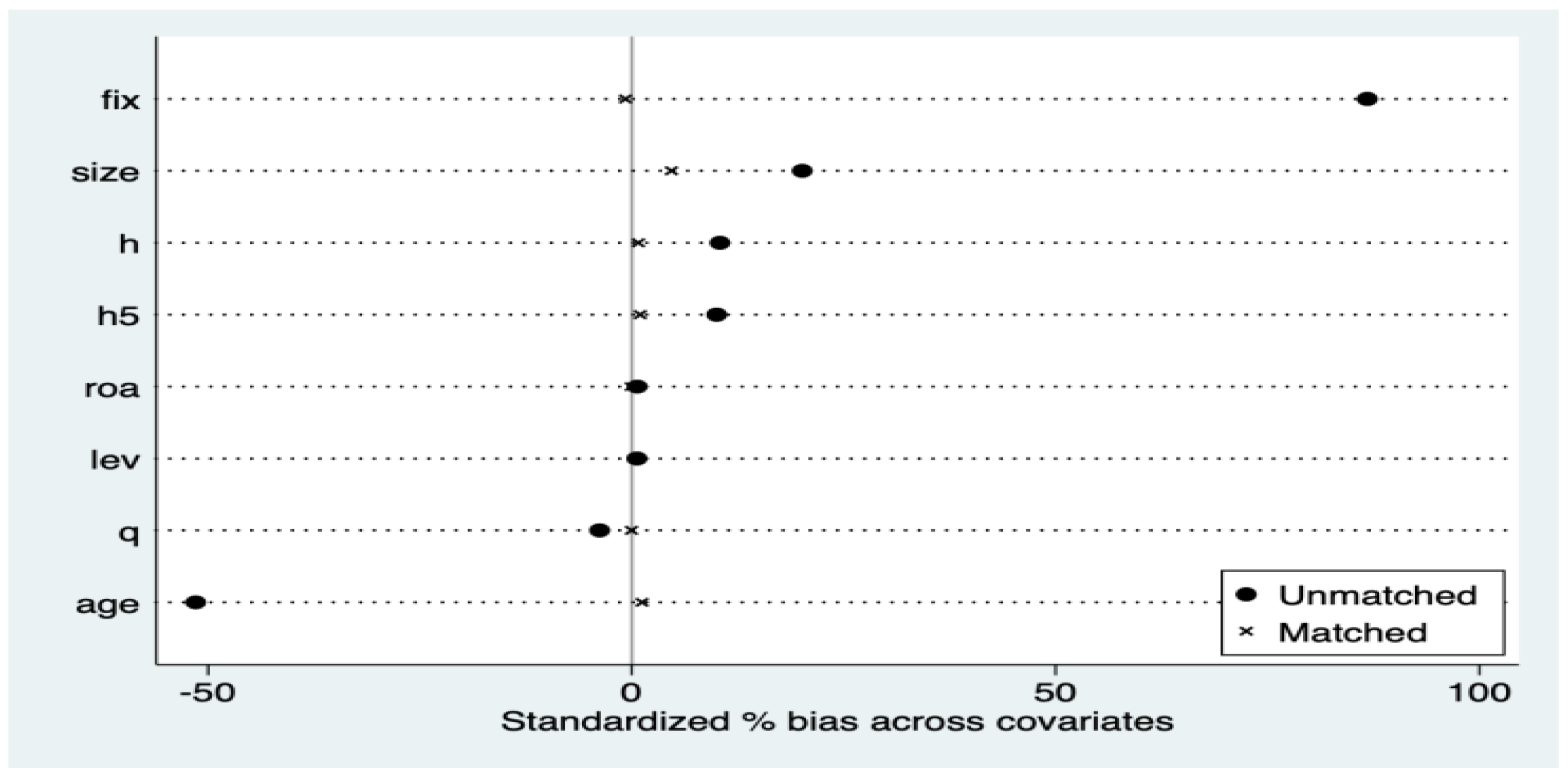

We provide a new insight into the relationship between the corporate high-quality development and RSEPT using a sample of energy-intensive firms from 2003 to 2018. We first calculate the indexes for corporate high-quality development using entropy weighting for the five dimensions of efficiency, innovation, openness, greenness, and social responsibility. Then, we develop a difference-in-differences model to reveal that RSEPT dampens high-quality development of corporations, as the estimated coefficient is −0.0420 with a t-statistic of −2.9384. This effect is significant in the year of policy implementation and is more pronounced in the subsequent two years. In contrast with negative and significant effect of private firms (t = −5.6514), the high-quality development of state-owned firms shows no correlation with environmental policy constraints. RSEPT inhibits the corporate high-quality development by reducing the capital allocation efficiency, with the coefficient of −0.32 (t = −3.8183).

Our findings in this study point to the following policy implications:

First, we need to understand the connotation of a high-quality development system and to formulate diversified regulatory policies. The level of energy-intensive firms’ high-quality development index in China is relatively low, and the number of firms with high-quality development values greater than the average accounted for only 34.7% of the total sample. Therefore, to better enhance the high-quality development of energy-intensive firms, the government should focus on policies that address issues of innovation, coordination, greenness, openness, and sharing.

Second, RSEPT should not be implemented aggressively. Given that RSEPT dampens corporate high-quality development, the goals of carbon peaking and carbon neutrality should be executed steadily while balancing corporate sustainability. This probably contributes to the reasons that strict policy standards or the hush implementation process may cause a reduction in yields or even suspension of production. The electricity brownout events that occurred recently in northeast China underlay the results of excessively stringent environmental regulation policies. To weaken this negative impact, the government can further supplement other incentives policies, such as credit and tax incentives, to relieve some of the pressures caused by the environmental policy.

Third, the policies may also target the high-quality development of private energy-intensive firms. Private firms have encountered ownership discrimination and tight budget constraints in China and, for private firms compared with state-owned firms, this may underlay the more pronounced negative effects of regulatory policies on corporate high-quality development. Therefore, we should investigate the high-quality index scores and address the drawbacks in a timely fashion.

Fourth, corporate internal governance should be designed to improve high-quality development. Corporate governance includes strategies such as protecting the stakeholder’s interests, information disclosure of major issues, and strengthening the supervision of the executives. Under the constraints of environmental regulations, these strategies can be implemented to promote high-quality development by efficient resource allocation.

In the future, we aim to examine the effects of RSEPT by classifying the energy-intensive industries into six sub-industries. Moreover, China has formulated a strategy of carbon peak and carbon neutralization, thus forming a new environmental regulation policy. Therefore, we will introduce the scenario analysis to simulate the effects of new kinetic factors on the high-quality development of firms under the “Dual Carbon” strategy.

{kind=link}

{kind=link}