Climate-Related Regulations and Financial Markets: A Meta-Analytic Literature Review

Abstract

1. Introduction

2. Literature Review and Hypotheses Development

2.1. Environmental Regulation

2.2. Climate-Related Disclosure

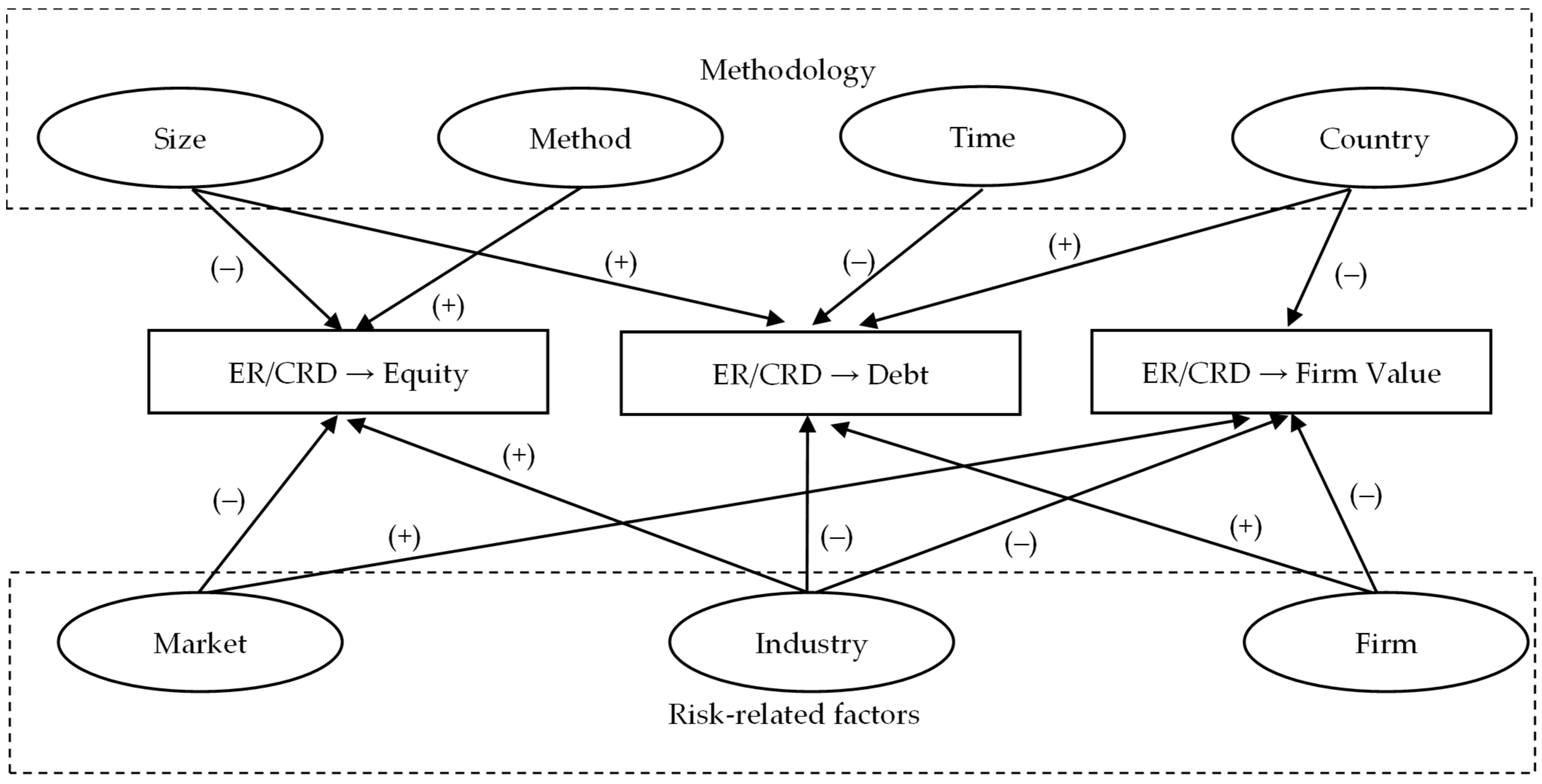

2.3. The Theoretical Model

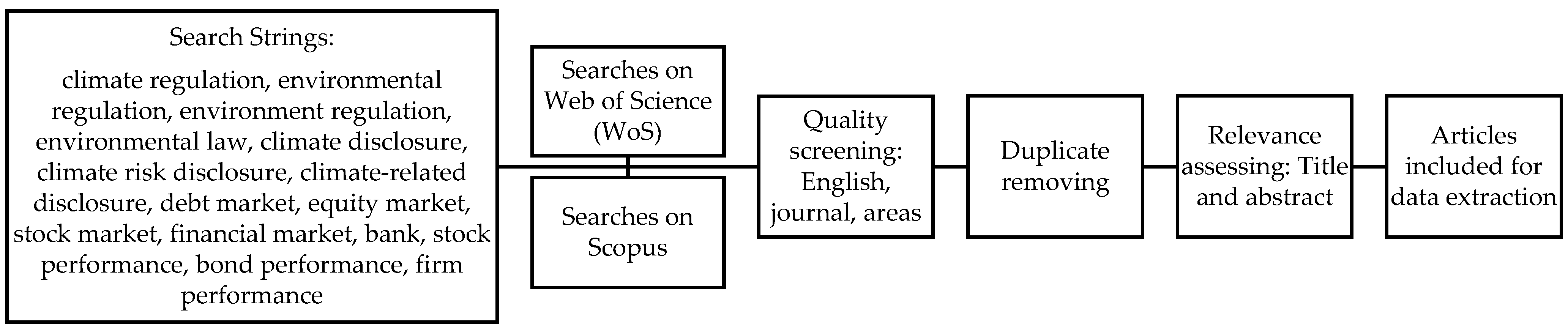

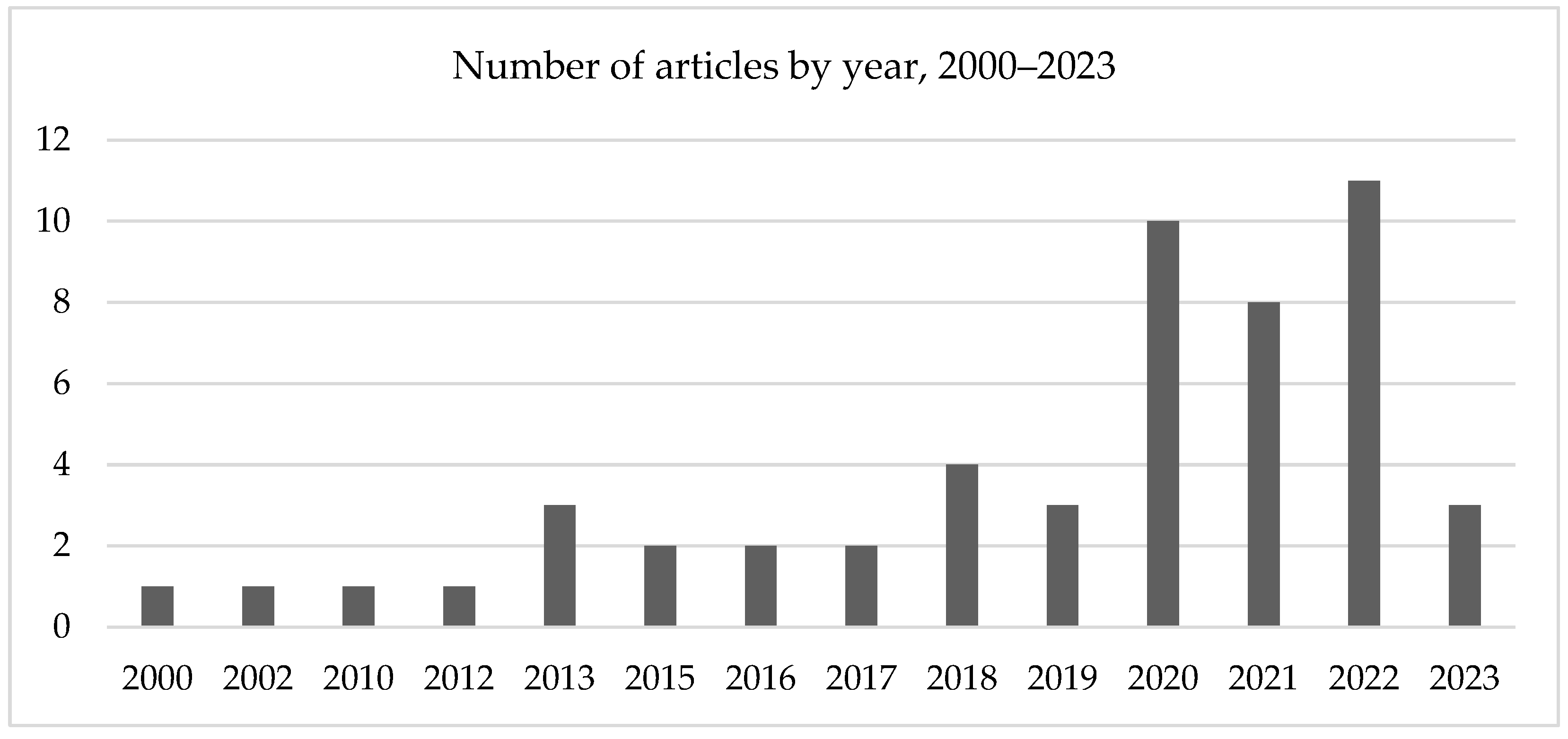

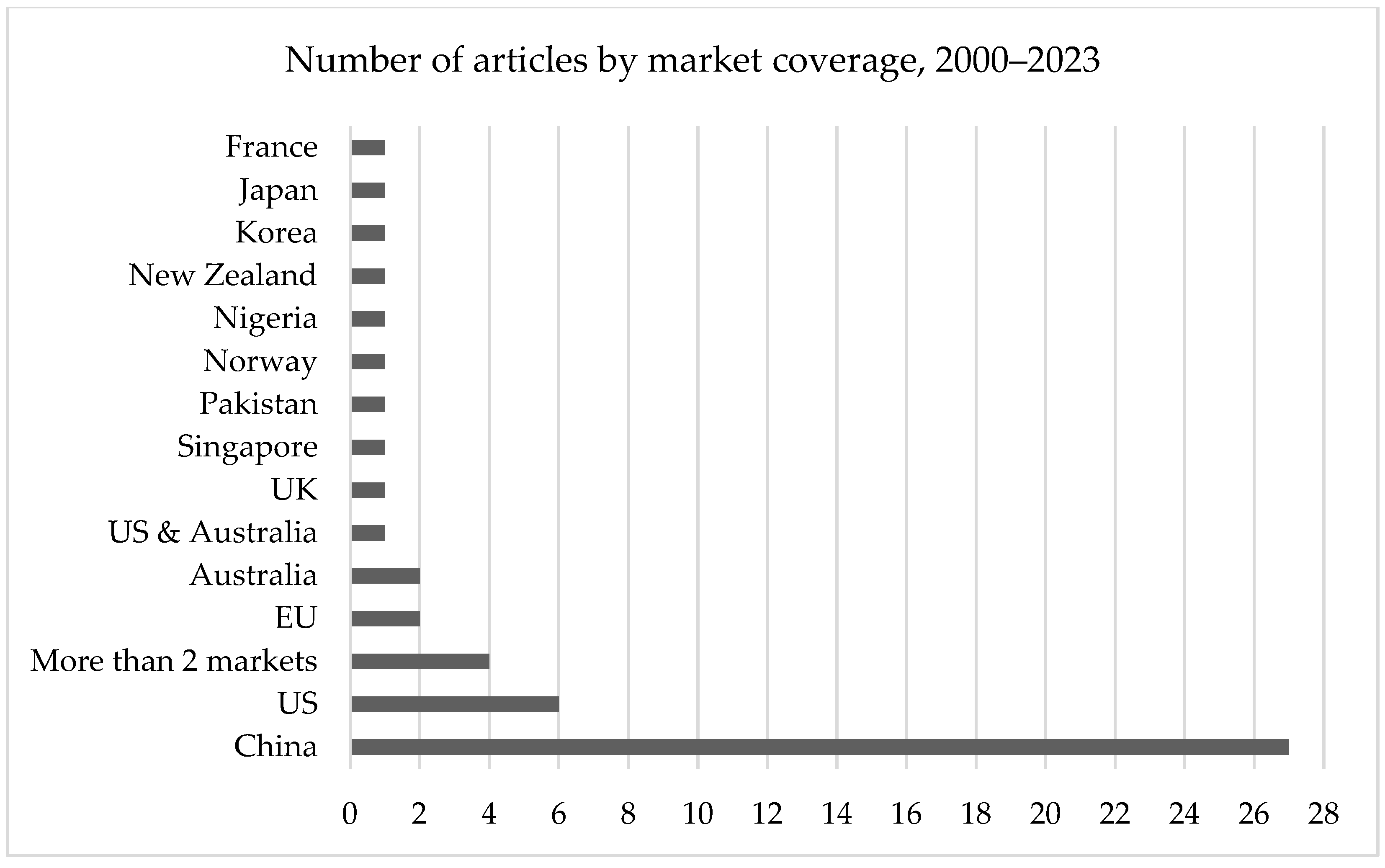

3. Methodology

4. Results

4.1. Reliability and Regression Path Analysis

4.2. Meta-Analysis Structural Equation Modelling Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Al-Tuwaijri, Sulaiman, Theodore E. Christensen, and K. E. Hughes, II. 2004. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Accounting, Organizations and Society 29: 447–71. [Google Scholar] [CrossRef]

- Amar, Jeanne, Samira Demaria, and Sandra Rigot. 2022. Enhancing Financial Transparency to Mitigate Climate Change: Toward a Climate Risks and Opportunities Reporting Index. Environmental Modeling & Assessment 27: 425–39. [Google Scholar] [CrossRef]

- Antoniuk, Yevheniia. 2022. The effect of climate disclosure on stock market performance: Evidence from Norway. Sustainable Development 31: 1008–26. [Google Scholar] [CrossRef]

- Bai, Caiquan, Chen Feng, Kerui Du, Yuansheng Wang, and Yuan Gong. 2020. Understanding spatial-temporal evolution of renewable energy technology innovation in China: Evidence from convergence analysis. Energy Policy 143: 111570. [Google Scholar] [CrossRef]

- Birindelli, Giuliana, and Helen Chiappini. 2021. Climate change policies: Good news or bad news for firms in the European Union? Corporate Social Responsibility and Environmental Management 28: 831–48. [Google Scholar] [CrossRef]

- Boulatoff, Catherine, Carol Boyer, and Stephen J. Ciccone. 2012. Voluntary Environmental Regulation and Firm Performance: The Chicago Climate Exchange. The Journal of Alternative Investments 15: 114–22. [Google Scholar] [CrossRef]

- Bowan, Megan, and Daniel Wiseman. 2020. Finance Actors and Climate-Related Disclosure Regulation: Logic Limits and Emerging Accountability. In Climate Finance: Insurance, Finance and the Regulation of Harmscapes. London: Routledge, pp. 153–78. [Google Scholar]

- Charkham, Jonathan P. 1992. Corporate governance: Lessons from abroad. European Business Journal 4: 8. [Google Scholar]

- Clarkson, Peter, Xiaohua Fang, Yue Li, and Gordon D. Richardson. 2010. The relevance of environmental disclosure for investors and other stakeholder groups: Are such disclosures incrementally informative? Accounting Research 22: 41–47. [Google Scholar] [CrossRef]

- Colombelli, Alessandra, Claudia Ghisetti, and Francesco Quatraro. 2020. Green technologies and firms’ market value: A micro-econometric analysis of European firms. Industrial and Corporate Change 29: 855–75. [Google Scholar] [CrossRef]

- Dhaliwal, Dan, Oliver Zhen Li, Albert Tsang, and Yong George Yang. 2014. Corporate social responsibility disclosure and the cost of equity capital: The roles of stakeholder orientation and financial transparency. Journal of Accounting and Public Policy 33: 328–55. [Google Scholar] [CrossRef]

- Diltz, J. David. 2002. U.S. equity markets and environmental policy. The case of electric utility investor behavior during the passage of the Clean Air Act Amendments of 1990. Environmental and Resource Economics 23: 379–401. [Google Scholar] [CrossRef]

- Dowell, Glen, Stuart Hart, and Bernard Yeung. 2000. Do corporate global environmental standards create or destroy market value? Management Science 46: 1059–74. [Google Scholar] [CrossRef]

- Dwivedi, Yogesh K., Nripendra P. Rana, Anand Jeyaraj, Marc Clement, and Michael D. Williams. 2019. Re-examining the Unified Theory of Acceptance and Use of Technology (UTAUT): Towards a revised theoretical model. Information Systems Frontiers 21: 719–34. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1970. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Fan, Haichao, Yuchao Peng, Huanhuan Wang, and Zhiwei Xu. 2021. Greening through finance? Journal of Development Economics 152: 102683. [Google Scholar] [CrossRef]

- Fard, Amirhossein, Siamak Javadi, and Incheol Kim. 2020. Environmental regulation and the cost of bank loans: International evidence. Journal of Financial Stability 51: 100797. [Google Scholar] [CrossRef]

- Freedman, Martin, and Bikki Jaggi. 1982. Pollution disclosures, pollution performance and economic performance. Omega 10: 167–76. [Google Scholar] [CrossRef]

- Gans, Will, and Beat Hintermann. 2013. Market Effects of Voluntary Climate Action by Firms: Evidence from the Chicago Climate Exchange. Environmental and Resource Economics 55: 291–308. [Google Scholar] [CrossRef]

- Guo, Mengmeng, Yicheng Kuai, and Xiaoyan Liu. 2020. Stock market response to environmental policies: Evidence from heavily polluting firms in China. Economic Modelling 86: 306–16. [Google Scholar] [CrossRef]

- Hair, Joe F., Jr., Lucy M. Matthews, Ryan L. Matthews, and Marko Sarstedt. 2017. PLS-SEM or CB-SEM: Updated guidelines on which method to use. International Journal of Multivariate Data Analysis 1: 107. [Google Scholar] [CrossRef]

- He, Yu, and Huan Zheng. 2022. Do environmental regulations affect firm financial distress in China? Evidence from stock markets. Applied Economics 54: 4384–401. [Google Scholar] [CrossRef]

- Hew, Teck-Soon, and Sharifah Latifah Sye Kadir. 2017. The drivers for cloud-based virtual learning environment: Examining the moderating effect of school category. Internet Research 27: 942–73. [Google Scholar]

- Hew, Teck-Soon, Lai-Ying Leong, Keng-Boon Ooi, and Alain Yee-Loong Chong. 2016. Predicting drivers of mobile entertainment adoption: A two-stage sem-artificial-neural-network analysis. Journal of Computer Information Systems 56: 352–70. [Google Scholar] [CrossRef]

- Horváthová, Eva. 2010. Does environmental performance affect financial performance? A meta-analysis. Ecological Economics 70: 52–59. [Google Scholar] [CrossRef]

- Huang, Bihong, Maria Teresa Punzi, and Yu Wu. 2021. Do banks price environmental transition risks? Evidence from a quasi-natural experiment in China. Journal of Corporate Finance 69: 101983. [Google Scholar] [CrossRef]

- Huang, Bihong, Maria Teresa Punzi, and Yu Wu. 2022. Environmental regulation and financial stability: Evidence from Chinese manufacturing firms. Journal of Banking & Finance 136: 106396. [Google Scholar] [CrossRef]

- Hu, Guoqiang, Xiaoqi Wang, and Yu Wang. 2021. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Economics 98: 105134. [Google Scholar] [CrossRef]

- Ismagilova, Elvira, Emma L. Slade, Nripendra P. Rana, and Yogesh K. Dwivedi. 2020. The effect of electronic word of mouth communications on intention to buy: A meta-analysis. Information Systems Frontiers 22: 1203–26. [Google Scholar] [CrossRef]

- Javeed, Sohail Ahmad, Rashid Latief, and Lin Lefen. 2020. An analysis of relationship between environmental regulations and firm performance with moderating effects of product market competition: Empirical evidence from Pakistan. Journal of Cleaner Production 254: 120197. [Google Scholar] [CrossRef]

- Khanna, Madhu, and Lisa A. Damon. 1999. EPA’s voluntary 33/50 program: Impact on toxic releases and economic performance of firms. Journal of Environmental Economics and Management 37: 1–25. [Google Scholar] [CrossRef]

- Kleimeier, Stefanie, and Michael Viehs. 2021. Pricing carbon risk: Investor preferences or risk mitigation? Economics Letters 205: 109936. [Google Scholar] [CrossRef]

- Kong, Gaowen, Shuai Wang, and Yanan Wang. 2022. Fostering firm productivity through green finance: Evidence from a quasi-natural experiment in China. Economic Modelling 115: 105979. [Google Scholar] [CrossRef]

- Lee, Chien-Chiang, Yu-Fang Chang, and En-Ze Wang. 2022. Crossing the rivers by feeling the stones: The effect of China’s green credit policy on manufacturing firms’ carbon emission intensity. Energy Economics 116: 106413. [Google Scholar] [CrossRef]

- Lee, Ki-Hoon, Bum-Jin Park, Hakjoon Song, and Keun-Hyo Yook. 2017. The Value Relevance of Environmental Audits: Evidence from Japan. Business Strategy and the Environment 26: 609–25. [Google Scholar] [CrossRef]

- Leong, Lai-Ying, Teck-Soon Hew, Keng-Boon Ooi, and June Wei. 2020. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. International Journal of Information Management 51: 1–24. [Google Scholar] [CrossRef]

- Leong, Lai-Ying, Teck-Soon Hew, Keng-Boon Ooi, Bhimaraya Metri, and Yogesh K. Dwivedi. 2023. Extending the Theory of Planned Behavior in the Social Commerce Context: A Meta-Analytic SEM (MASEM) Approach. Information Systems Frontiers 25: 1847–79. [Google Scholar] [CrossRef]

- Leong, Lai-Ying, Teck-Soon Hew, Keng-Boon Ooi, Voon-Hsien Lee, and Jun-Jie Hew. 2019. A hybrid SEM-neural network analysis of social media addiction. Expert Systems with Applications 133: 296–316. [Google Scholar] [CrossRef]

- Li, Meng, Liye Dong, Jing Luan, and Pengfei Wang. 2020. Do environmental regulations affect investors? Evidence from China’s action plan for air pollution prevention. Journal of Cleaner Production 244: 118817. [Google Scholar] [CrossRef]

- Lin, Boqiang, and Nan Wu. 2023. Climate risk disclosure and stock price crash risk: The case of China. International Review of Economics & Finance 83: 21–34. [Google Scholar] [CrossRef]

- Liu, Xinghe, Enxian Wang, and Danting Cai. 2018. Environmental Regulation and Corporate Financing—Quasi-Natural Experiment Evidence from China. Sustainability 10: 4028. [Google Scholar] [CrossRef]

- Lu, Shiyu, and Bo Cheng. 2022. Does environmental regulation affect firms’ ESG performance? Evidence from China. Managerial and Decision Economics 44: 2004–9. [Google Scholar] [CrossRef]

- Ma, Yechi, Yezhou Sha, Zilong Wang, and Wenjing Zhang. 2023. The effect of the policy mix of green credit and government subsidy on environmental innovation. Energy Economics 118: 106512. [Google Scholar] [CrossRef]

- Meng, Jia, and ZhongXiang Zhang. 2022. Corporate environmental information disclosure and investor response: Evidence from China’s capital market. Energy Economics 108: 105886. [Google Scholar] [CrossRef]

- Nerger, Gian-Luca, Toan Luu Duc Huynh, and Mei Wang. 2021. Which industries benefited from Trump environmental policy news? Evidence from industrial stock market reactions. Research in International Business and Finance 57: 101418. [Google Scholar] [CrossRef]

- Odoemelam, Ndubuisi, and Regina Okafor. 2018. The Influence of Corporate Governance on Environmental Disclosure of Listed Non-Financial Firms in Nigeria. Indonesian Journal of Sustainability Accounting and Management 2: 25. [Google Scholar] [CrossRef]

- Paré, Guy, Marie-Claude Trudel, Mirou Jaana, and Spyros Kitsiou. 2015. Synthesizing information systems knowledge: A typology of literature reviews. Information and Management 52: 183–99. [Google Scholar] [CrossRef]

- Pham, Huy Nguyen Anh, Vikash Ramiah, and Imad Moosa. 2020. The effects of environmental regulation on the stock market: The French experience. Accounting and Finance 60: 3279–304. [Google Scholar] [CrossRef]

- Pham, Huy, Van Nguyen, Vikash Ramiah, Priyantha Mudalige, and Imad Moosa. 2019. The Effects of Environmental Regulation on the Singapore Stock Market. Journal of Risk and Financial Management 12: 175. [Google Scholar] [CrossRef]

- Porter, Michael. 1990. Effect of environmental regulation on firm outcomes. Harvard Business Review 40: 1–20. [Google Scholar]

- Ramiah, Vikash, Belinda Martin, and Imad Moosa. 2013. How does the stock market react to the announcement of green policies? Journal of Banking and Finance 37: 1747–58. [Google Scholar] [CrossRef]

- Ramiah, Vikash, Huy Nguyen Anh Pham, Ian Wang, Van Ngoc Tuong Dang, Jose Francisco Veron, and Hung Duong. 2017. The financial consequences of abolishing a carbon trading system. Applied Economics Letters 24: 936–39. [Google Scholar] [CrossRef]

- Ramiah, Vikash, Jacopo Pichelli, and Imad Moosa. 2015a. Environmental regulation, the Obama effect and the stock market: Some empirical results. Applied Economics 47: 725–38. [Google Scholar] [CrossRef]

- Ramiah, Vikash, Jacopo Pichelli, and Imad Moosa. 2015b. The Effects of Environmental Regulation on Corporate Performance: A Chinese Perspective. Review of Pacific Basin Financial Markets and Policies 18: 1550026. [Google Scholar] [CrossRef]

- Ramiah, Vikash, Thomas Morris, Imad Moosa, Michael Gangemi, and Louise Puican. 2016. The effects of announcement of green policies on equity portfolios Evidence from the United Kingdom. Managerial Auditing Journal 31: 138–55. [Google Scholar] [CrossRef]

- Rana, Nripendra P., Yogesh K. Dwivedi, and Michael D. Williams. 2015. A meta-analysis of existing research on citizen adoption of e-government. Information Systems Frontiers 17: 547–63. [Google Scholar] [CrossRef]

- Rassier, Dylan G., and Dietrich Earnhart. 2010. Does the porter hypothesis explain expected future financial performance? The effect of clean water regulation on chemical manufacturing firms. Environmental and Resource Economics 45: 353–77. [Google Scholar] [CrossRef]

- Shane, Philip B., and Barry H. Spicer. 1983. Market Response to Environmental Information Produced outside the Firm. The Accounting Review 58: 521–38. [Google Scholar]

- Shao, Hanhua, Yuansheng Wang, Yao Wang, and Yuanjia Li. 2022. Green credit policy and stock price crash risk of heavily polluting enterprises: Evidence from China. Economic Analysis and Policy 75: 271–87. [Google Scholar] [CrossRef]

- Shu, Hao, and Weiqiang Tan. 2023. Does carbon control policy risk affect corporate ESG performance? Economic Modelling 120: 106148. [Google Scholar] [CrossRef]

- Solomon, Aris, and Linda Lewis. 2002. Incentives and disincentives for corporate environmental disclosure. Business Strategy and the Environment 11: 154–69. [Google Scholar] [CrossRef]

- Sun, Junxiu, Feng Wang, Haitao Yin, and Bing Zhang. 2019. Money Talks: The Environmental Impact of China’s Green Credit Policy. Journal of Policy Analysis and Management 38: 653–80. [Google Scholar] [CrossRef]

- Templier, Mathieu, and Guy Paré. 2018. Transparency in literature reviews: An assessment of reporting practices across review types and genres in top IS journals. European Journal of Information Systems 27: 503–50. [Google Scholar] [CrossRef]

- Tian, Yuan, Alexandr Akimov, Eduardo Roca, and Victor Wong. 2016. Does the carbon market help or hurt the stock price of electricity companies? Further evidence from the European context. Journal of Cleaner Production 112: 1619–26. [Google Scholar] [CrossRef]

- Wang, Jiayi, and Ping Lei. 2020. A new tool for environmental regulation? The connection between environmental administrative talk policy and the market disciplinary effect. Journal of Cleaner Production 275: 124162. [Google Scholar] [CrossRef]

- Wang, Yanbing, Michael S. Delgado, Neha Khanna, and Vicki L. Bogan. 2019. Good news for environmental self-regulation? Finding the right link. Journal of Environmental Economics and Management 94: 217–35. [Google Scholar] [CrossRef]

- Wellalage, Nirosha Hewa, and Vijay Kumar. 2021. Environmental performance and bank lending: Evidence from unlisted firms. Business Strategy and the Environment 30: 3309–29. [Google Scholar] [CrossRef]

- Wen, Fenghua, Nan Wu, and Xu Gong. 2020. China’s carbon emissions trading and stock returns. Energy Economics 86: 104627. [Google Scholar] [CrossRef]

- Wirth, Carolyn, Jing Chi, and Martin Young. 2013. The Economic Impact of Capital Expenditures: Environmental Regulatory Delay as a Source of Competitive Advantage? Journal of Business Finance and Accounting 40: 115–41. [Google Scholar] [CrossRef]

- Wong, Choy-Har, Garry Wei-Han Tan, Siew-Phaik Loke, and Keng-Boon Ooi. 2014. Mobile TV: A new form of entertainment? Industrial Management and Data Systems 114: 1050–67. [Google Scholar] [CrossRef]

- Wu, Jiming, and Hongwei Du. 2012. Toward a better understanding of behavioral intention and system usage constructs. European Journal of Information Systems 21: 680–98. [Google Scholar] [CrossRef]

- Xiao, Han, and KeMin Wang. 2020. Does environmental labeling exacerbate heavily polluting firms’ financial constraints? Evidence from China. China Journal of Accounting Research 13: 147–74. [Google Scholar] [CrossRef]

- Xu, Guangdong, Wenming Xu, and Shudan Xu. 2018. Does the establishment of the Ministry of Environmental Protection matter for addressing China’s pollution problems? Empirical evidence from listed companies. Economics of Governance 19: 195–224. [Google Scholar] [CrossRef]

- Yang, Gangqiang, Ziyu Ding, Haisen Wang, and Lingli Zou. 2022a. Can environmental regulation improve firm total factor productivity? The mediating effects of credit resource allocation. Environment, Development and Sustainability 25: 6799–27. [Google Scholar] [CrossRef]

- Yang, Jingyi, Daqian Shi, and Wenbo Yang. 2022b. Stringent environmental regulation and capital structure: The effect of NEPL on deleveraging the high polluting firms. International Review of Economics and Finance 79: 643–56. [Google Scholar] [CrossRef]

- Yang, Minhua, Vikash Ramiah, Imad Moosa, and Yu He. 2018. Narcissism, political tenure, financial indicators and the effectiveness of environmental regulation. Applied Economics 50: 2325–38. [Google Scholar] [CrossRef]

- Yao, Liming, Ying Luo, Yile Wang, and Haiyue Liu. 2022. Market response to the hierarchical water environment regulations on heavily polluting firm: Evidence from China. Water Resources and Economics 39: 100201. [Google Scholar] [CrossRef]

- Zhang, Xuehui, Jianhua Tan, and Kam C. Chan. 2021. Environmental law enforcement as external monitoring: Evidence from the impact of an environmental inspection program on firm-level stock price crash risk. International Review of Economics & Finance 71: 21–31. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Author(s) | Title | Sample |

|---|---|---|---|

| 1 | Dowell et al. (2000) | Do corporate global environmental standards create or destroy market value? | 89 US listed firms, 1994–1997 |

| 2 | Diltz (2002) | U.S. equity markets and environmental policy. The case of electric utility investor behavior during the passage of the clean air act amendments of 1990 | 97 US electric companies |

| 3 | Rassier and Earnhart (2010) | Does the porter hypothesis explain expected future financial performance? The effect of clean water regulation on chemical manufacturing firms | US Chemical Manufacturing Industry, 1995–2000 |

| 4 | Boulatoff et al. (2012) | Voluntary environmental regulation and firm performance: The Chicago climate exchange | 68 Chicago companies, 2003–2009 |

| 5 | Gans and Hintermann (2013) | Market effects of voluntary climate action by firms: Evidence from the Chicago climate exchange | 32 Chicago companies, 1991–2009 |

| 6 | Ramiah et al. (2013) | How does the stock market react to the announcement of green policies? | 1770 Australian listed firms, 2005–2011 |

| 7 | Wirth et al. (2013) | The economic impact of capital expenditures: Environmental regulatory delay as a source of competitive advantage? | 55 New Zealand listed firms, 1991–2007 |

| 8 | Ramiah et al. (2015a) | The effects of environmental regulation on corporate performance: A Chinese perspective | 97 industries in China, 2001–2011 |

| 9 | Ramiah et al. (2015b) | Environmental regulation, the Obama effect and the stock market: some empirical results | US and International Equity Portfolios, 1997–2011 |

| 10 | Ramiah et al. (2016) | The effects of announcement of green policies on equity portfolios: Evidence from the United Kingdom | 2132 UK stocks, 2002–2012 |

| 11 | Tian et al. (2016) | Does the carbon market help or hurt the stock price of electricity companies? Further evidence from the European context | EU Electricity Generation Industry, 2005–2012 |

| 12 | Lee et al. (2017) | The value relevance of environmental audits: Evidence from Japan | 266 Japanese manufacturing firms, 2010–2013 |

| 13 | Ramiah et al. (2017) | The financial consequences of abolishing a carbon trading system | 1875 Australian listed firms, 2009–2015 |

| 14 | Liu et al. (2018) | Environmental regulation and corporate financing—Quasi-natural experiment evidence from China | 4521 Chinese listed firms |

| 15 | Odoemelam and Okafor (2018) | The influence of corporate governance on environmental disclosure of listed non-financial firms in Nigeria | 86 Nigerian non-financial listed firms |

| 16 | Xu et al. (2018) | Does the establishment of the Ministry of Environmental Protection matter for addressing China’s pollution problems? Empirical evidence from listed companies | 309 Chinese listed firms in polluting industries |

| 17 | Yang et al. (2018) | Narcissism, political tenure, financial indicators and the effectiveness of environmental regulation | 758 listed firms in the US and Australia, 1989–2015 |

| 18 | Pham et al. (2019) | The effects of environmental regulation on the Singapore stock market | 37 Industries in Singapore, 2006–2018 |

| 19 | Sun et al. (2019) | Money talks: The environmental impact of China’s green credit policy | 17 cities in China, 2000–2007 |

| 20 | Wang et al. (2019) | Good news for environmental self-regulation? Finding the right link | Listed on the New York Stock Exchange, 2005–2014 |

| 21 | Bai et al. (2020) | Understanding spatial-temporal evolution of renewable energy technology innovation in China: Evidence from convergence analysis | Energy companies in 30 Chinese provinces, 1997–2005 |

| 22 | Colombelli et al. (2020) | Green technologies and firms’ market value: A micro-econometric analysis of European firms | Listed firms in France, Germany, Italy, the Netherlands and the UK, 2002–2011 |

| 23 | Fard et al. (2020) | Environmental regulation and the cost of bank loans: International evidence | 27 countries, 1990–2014 |

| 24 | Guo et al. (2020) | Stock market response to environmental policies: Evidence from heavily polluting firms in China | 609 Chinese listed firms from heavily polluting industries |

| 25 | Javeed et al. (2020) | An analysis of relationship between environmental regulations and firm performance with moderating effects of product market competition: Empirical evidence from Pakistan | 147 Pakistan manufacturing listed firms, 2008–2017 |

| 26 | Li et al. (2020) | Do environmental regulations affect investors? Evidence from China’s action plan for air pollution prevention | 2045 stocks on SSE and SZSE before 2012 |

| 27 | Pham et al. (2020) | The effects of environmental regulation on the stock market: the French experience | 797 French stocks, 2003–2013 |

| 28 | Wang and Lei (2020) | A new tool for environmental regulation? The connection between environmental administrative talk policy and the market disciplinary effect | 63 environmental administrative interviews (China), 2014–2018 |

| 29 | Wen et al. (2020) | China’s carbon emissions trading and stock returns | 52 stocks on SZSE, 2009–2018 |

| 30 | Xiao and Wang (2020) | Does environmental labeling exacerbate heavily polluting firms’ financial constraints? Evidence from China | 2426 non-financial firms on the SSE and SZSE, 2004–2013 |

| 31 | Birindelli and Chiappini (2021) | Climate change policies: Good news or bad news for firms in the European Union | EU firms, 2013–2018 |

| 32 | Fan et al. (2021) | Greening through finance? | Firms in 31 Chinese provinces, 2009–2015 |

| 33 | Hu et al. (2021) | Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China | China A-share listed firms, 2007–2016 |

| 34 | Huang et al. (2021) | Do banks price environmental transition risks? Evidence from a quasi-natural experiment in China | Non-financial firms in six prefecture-level cities in Jiangsu, China |

| 35 | Kleimeier and Viehs (2021) | Pricing carbon risk: Investor preferences or risk mitigation? | 2267 loans, 2009–2016 |

| 36 | Nerger et al. (2021) | Which industries benefited from Trump environmental policy news? Evidence from industrial stock market reactions | 49 industries in the US |

| 37 | Wellalage and Kumar (2021) | Environmental performance and bank lending: Evidence from unlisted firms | 3915 companies in 7 developing countries 1, 2018–2019 |

| 38 | Zhang et al. (2021) | Environmental law enforcement as external monitoring: Evidence from the impact of an environmental inspection program on firm-level stock price crash risk | 6527 Chinese firms, 2014–2018 |

| 39 | Antoniuk (2022) | The effect of climate disclosure on stock market performance: Evidence from Norway | 56 Norwegian stocks |

| 40 | He and Zheng (2022) | Do environmental regulations affect firm financial distress in China? Evidence from stock markets | 2499 A shares on SSE and SZSE, 1999–2018 |

| 41 | Huang et al. (2022) | Environmental regulation and financial stability: Evidence from Chinese manufacturing firms | 817 firms in Sichuan, China, 2004–2007 |

| 42 | Kong et al. (2022) | Fostering firm productivity through green finance: Evidence from a quasi-natural experiment in China | 3544 Chinese A-share firms, 2014–2020 |

| 43 | Lee et al. (2022) | Crossing the rivers by feeling the stones: The effect of China’s green credit policy on manufacturing firms’ carbon emission intensity | 140,839 manufacturing Chinese firms in heavily polluting industries, 2004–2009 |

| 44 | Lu and Cheng (2022) | Does environmental regulation affect firms’ ESG performance? Evidence from China | 212,224 Chinese A-share firms, 2011–2018 |

| 45 | Meng and Zhang (2022) | Corporate environmental information disclosure and investor response: Evidence from China’s capital market | All Chinese A-share firms, 2004–2020 |

| 46 | Shao et al. (2022) | Green credit policy and stock price crash risk of heavily polluting enterprises: Evidence from China | All Chinese A-share firms, 2009–2014 |

| 47 | Yang et al. (2022a) | Can environmental regulation improve firm total factor productivity? The mediating effects of credit resource allocation | 13,319 Chinese A-share firms, 2011–2018 |

| 48 | Yang et al. (2022b) | Stringent environmental regulation and capital structure: The effect of NEPL on deleveraging the high polluting firms | 17819 Chinese listed firms, 2009–2018 |

| 49 | Yao et al. (2022) | Market response to the hierarchical water environment regulations on heavily polluting firm: Evidence from China | 242 Chinese high-water-polluting listed firms, 2010–2019 |

| 50 | Ma et al. (2023) | The effect of the policy mix of green credit and government subsidy on environmental innovation | 1602 Chinese A-share firms, 2009–2016 |

| 51 | Shu and Tan (2023) | Does carbon control policy risk affect corporate ESG performance? | Chinese A-share industrial firms, 2010–2019 |

| 52 | Lin and Wu (2023) | Climate risk disclosure and stock price crash risk: The case of China | Chinese A-share listed firms, 2016–2021 |

| Variable | Abbreviation | Construct |

|---|---|---|

| Environmental regulation | Reg | Environmental regulation = 1 Climate-related disclosure = 2 |

| Financial performance | Perform | Equity = 1 Debt = 2 Value = 3 Mixed = 4 |

| Sample size effect | Size | Less than 1000 = 1 From 1000 to 9999 = 2 From 10,000 to 99,999 = 3 More than 99,999 = 4 |

| Method effect | Method | Event study methodology = 1 Ordinary Least Square estimate = 2 Difference-in-differences method = 3 Mixed method = 4 |

| Time effect (Data frequency) | Time | Yearly = 1 Quarterly = 2 Monthly = 3 Daily = 4 |

| Country effect | Country | One country = 1 Two countries = 2 Three countries = 3 More than three countries = 4 |

| Market development effect | Market | Developing = 1 Developed = 2 Mixed = 3 |

| Industry effect consideration | Industry | No = 0 Yes = 1 |

| Firm effect | Firm | No = 1 Firm age = 2 Firm size = 3 Firm age and size = 4 |

| Panel A—Climate-Related Disclosure | Cronbach’s Alpha | |||||||||

| All Size | ||||||||||

| Variable | Obs | Mean | Std. Dev. | Min | Max | Obs = 6 | ||||

| perform | 6 | 1.166667 | 0.408248 | 1 | 2 | 0.768 | ||||

| sample | 6 | 8281.667 | 13392.52 | 86 | 34,658 | 0.8005 | ||||

| method | 6 | 2.833333 | 1.32916 | 1 | 4 | 0.7541 | ||||

| time | 6 | 2 | 1.549193 | 1 | 4 | 0.836 | ||||

| country | 6 | 1.333333 | 0.816497 | 1 | 3 | 0.768 | ||||

| market | 6 | 1.666667 | 0.816497 | 1 | 3 | 0.7164 | ||||

| industry | 6 | 0.666667 | 0.516398 | 0 | 1 | 0.7664 | ||||

| firm | 6 | 2.333333 | 1.032796 | 1 | 3 | 0.8539 | ||||

| Test scale reliability coefficient = mean Cronbach’s alpha (standardized items) | 0.8092 | |||||||||

| Panel B—Environmental Regulation | Cronbach’s alpha | |||||||||

| All size | size = 1 | size = 2 | size = 3 | size = 4 | ||||||

| Variable | Obs | Mean | Std. dev. | Min | Max | Obs = 46 | Obs = 14 | Obs = 17 | Obs = 10 | Obs = 5 |

| perform | 46 | 1.978261 | 1.183012 | 1 | 4 | 0.617 | 0.6372 | 0.8551 | 0.7670 | 0.8621 |

| sample | 46 | 82756.63 | 300,460 | 30 | 1,704,437 | 0.6894 | 0.7503 | 0.8349 | 0.7087 | 0.8075 |

| method | 46 | 2.760870 | 1.232608 | 1 | 4 | 0.6127 | 0.6464 | 0.8601 | 0.6626 | 0.8268 |

| time | 46 | 2.369565 | 1.466041 | 1 | 4 | 0.5815 | 0.6424 | 0.8381 | 0.7347 | 0.7997 |

| country | 46 | 1.478261 | 1.09014 | 1 | 4 | 0.6176 | 0.6751 | 0.8474 | 0.6885 | 0.7942 |

| market | 46 | 1.413043 | 0.540621 | 1 | 3 | 0.5736 | 0.7257 | 0.8088 | 0.6389 | 0.7942 |

| industry | 46 | 0.543478 | 0.50361 | 0 | 1 | 0.6071 | 0.6919 | 0.8306 | 0.7238 | 0.8268 |

| firm | 46 | 2.108696 | 1.120085 | 1 | 4 | 0.6279 | 0.6130 | 0.8143 | 0.7753 | 0.8882 |

| Test scale reliability coefficient = mean Cronbach’s alpha (standardized items) | 0.6489 | 0.7054 | 0.8544 | 0.7431 | 0.8464 | |||||

| Path | k | Beta Coefficient | Significant | % of Sig. Path | Sample Size | Total Sample Size | Average Sample Size | |||

|---|---|---|---|---|---|---|---|---|---|---|

| Min | Max | Sig. | n.s. | Min | Max | |||||

| CRD → Perform (Equity) | 4 | −0.018 | 0.001 | 4 | 0 | 100.00% | 222 | 34,658 | 47,337 | 11,834 |

| ER → Perform (Equity) | 15 | −7.384 | 11.830 | 12 | 3 | 80.00% | 55 | 1,704,437 | 1,796,114 | 112,257 |

| ER → Perform (Debt) | 11 | −0.050 | 0.837 | 11 | 0 | 100.00% | 68 | 1,114,880 | 1,783,383 | 162,126 |

| ER → Perform (Firm value) | 14 | −3.060 | 2.644 | 13 | 1 | 92.86% | 30 | 31,770 | 106,133 | 8164 |

| ER/CRD–Equity Relationship | ER/CRD–Debt Relationship | ER/CRD–Value Relationship | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coeff. | Std. Err. | z | p | Coeff. | Std. Err. | z | p | Coeff. | Std. Err. | z | p | |

| size | −0.672 | 0.192 | −3.50 | 0.000 | 1.011 | 0.189 | 5.34 | 0.000 | −0.234 | 0.213 | −1.10 | 0.273 |

| method | 0.582 | 0.242 | 2.41 | 0.016 | −0.476 | 0.291 | −1.64 | 0.102 | −0.241 | 0.192 | −1.26 | 0.209 |

| time | 0.030 | 0.249 | 0.12 | 0.903 | −0.445 | 0.214 | −2.08 | 0.038 | −0.123 | 0.173 | −0.71 | 0.476 |

| country | 0.026 | 0.196 | 0.13 | 0.895 | 0.772 | 0.348 | 2.22 | 0.026 | −0.751 | 0.302 | −2.49 | 0.013 |

| market | −0.480 | 0.201 | −2.39 | 0.017 | 0.207 | 0.379 | 0.55 | 0.586 | 0.813 | 0.258 | 3.15 | 0.002 |

| industry | 0.815 | 0.165 | 4.95 | 0.000 | −0.655 | 0.217 | −3.02 | 0.003 | −0.585 | 0.210 | −2.78 | 0.005 |

| firm | −0.053 | 0.167 | −0.32 | 0.751 | 0.690 | 0.204 | 3.38 | 0.001 | −0.649 | 0.144 | −4.50 | 0.000 |

| _cons | 1.358 | 0.971 | 1.40 | 0.162 | −2.089 | 1.721 | −1.21 | 0.225 | 2.749 | 1.329 | 2.07 | 0.039 |

| var(e.) | 0.490 | 0.135 | 0.320 | 0.124 | 0.285 | 0.103 | ||||||

| obs. | 20 | 12 | 14 | |||||||||

| Fit statistic | ||||||||||||

| Likelihood ratio | ||||||||||||

| chi2_ms(0) | 0.000 | 0.000 | 0 | |||||||||

| p > chi2 | ||||||||||||

| chi2_bs(7) | 14.266 | 13.688 | 17.562 | |||||||||

| p > chi2 | 0.047 | 0.057 | 0.014 | |||||||||

| Population error | ||||||||||||

| RMSEA | 0.000 | 0.000 | 0.000 | |||||||||

| 90% CI, lower | 0.000 | 0.000 | 0.000 | |||||||||

| 90% CI, upper | 0.000 | 0.000 | 0.000 | |||||||||

| pclose | 1.000 | 1.000 | 1.000 | |||||||||

| Information criteria | ||||||||||||

| AIC | 415.067 | 178.490 | 230.195 | |||||||||

| BIC | 424.029 | 182.855 | 235.947 | |||||||||

| Baseline comparison | ||||||||||||

| CFI | 1.000 | 1.000 | 1.000 | |||||||||

| TLI | 1.000 | 1.000 | 1.000 | |||||||||

| Size of residuals | ||||||||||||

| SRMR | 0.000 | 0.000 | 0.000 | |||||||||

| CD | 0.510 | 0.680 | 0.715 | |||||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ho, L.T.; Gan, C.; Zhao, Z. Climate-Related Regulations and Financial Markets: A Meta-Analytic Literature Review. J. Risk Financial Manag. 2024, 17, 398. https://doi.org/10.3390/jrfm17090398

Ho LT, Gan C, Zhao Z. Climate-Related Regulations and Financial Markets: A Meta-Analytic Literature Review. Journal of Risk and Financial Management. 2024; 17(9):398. https://doi.org/10.3390/jrfm17090398

Chicago/Turabian StyleHo, Linh Tu, Christopher Gan, and Zhenzhen Zhao. 2024. "Climate-Related Regulations and Financial Markets: A Meta-Analytic Literature Review" Journal of Risk and Financial Management 17, no. 9: 398. https://doi.org/10.3390/jrfm17090398

APA StyleHo, L. T., Gan, C., & Zhao, Z. (2024). Climate-Related Regulations and Financial Markets: A Meta-Analytic Literature Review. Journal of Risk and Financial Management, 17(9), 398. https://doi.org/10.3390/jrfm17090398