The Role of E-Accounting Adoption on Business Performance: The Moderating Role of COVID-19

,

,

,

,  ,

,  , ,

, ,

Abstract

1. Introduction

2. Literature Review and Hypotheses Development

2.1. Information Quality

2.2. System Quality

2.3. Service Quality (SQ)

2.4. E-Accounting Usage

2.5. User Satisfaction

2.6. Moderating the Effect of COVID-19 on the Relationship between E-Accounting Usage and Business Performance

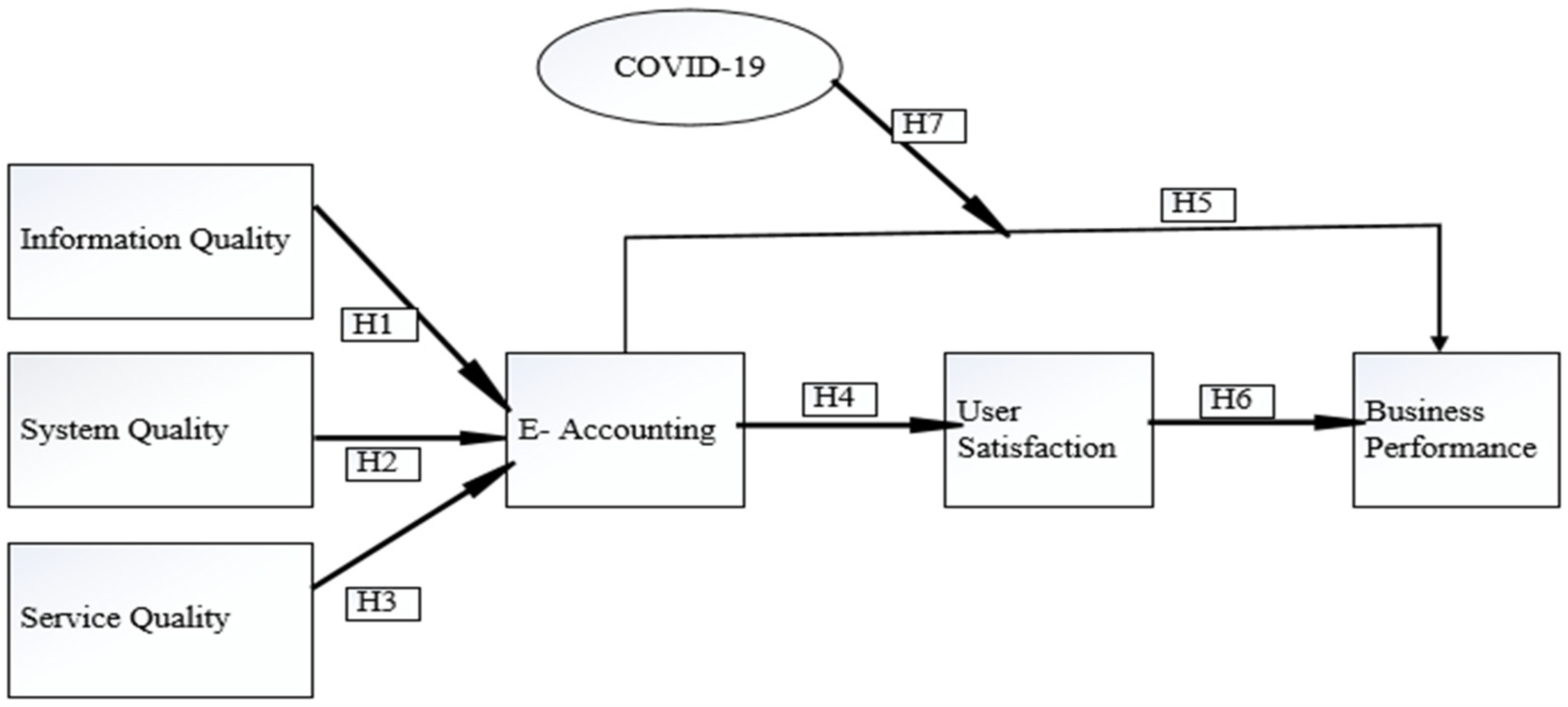

3. Theoretical Underpinning and Framework

3.1. DeLone and McLean IS Success Model (DM ISSM)

3.2. Theoretical Framework

4. Methodology

Measurement Development and Data Collection

5. Analysis

5.1. Internal Consistency Reliability

5.2. Discriminant Validity

6. Discussion and Implications

7. Conclusions, Limitations, and Recommendations for Future Studies

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

| Information Quality (InfQ) | Items | Reference |

| InfQ1 | Information from the E-accounting is always timely | Lin et al. (2006) |

| InfQ2 | data provided by the E-accounting is useful | |

| InfQ3 | information provided by the E-accounting is accurate | |

| InfQ4 | Information from the E-accounting is easy to understand and related to decision-making | |

| System Quality (SysQ) | Items | Reference |

| SysQ1 | E-accounting user interface can be easily adapted to one’s personal approach. | Lin et al. (2006) |

| SysQ2 | E-accounting is easy to use. | |

| SysQ3 | E-accounting responds quickly enough. | |

| SysQ4 | E-accounting is always up and running as necessary. | |

| Service Quality (SerQ) | Items | Reference |

| SerQ1 | The information I receive from the IS department is accurate. | (Petter et al. 2008; Alzoubi 2011) |

| SerQ2 | Training provided by the IS department improves my quality of work. | |

| SerQ3 | The IS department solves my problems and provide me prompt service. | |

| E-accounting Use | Items | Reference |

| Use1 | E-accounting is used frequently. | (Rajan and Baral 2015) |

| Use2 | I spend most of time per day using E-accounting for job-related work. | |

| Use3 | I depend highly on E-accounting use. | |

| E-accounting USat | Items | Reference |

| USat1 | I am satisfied with the SysQ. | (Hsu et al. 2015) |

| USat1 | I am satisfied with the InfQ. | |

| USat1 | I am satisfied with the SerQ. | |

| Business Performance | Items | Reference |

| BP1 | I believe that E-accounting can increase my hotels operational performance. | |

| BP 2 | I believe that E-accounting can increase the profitability of my hotel. | Laitinen (2014) |

| BP3 | I believe that E-accounting can increase our financial performance. | |

| BP4 | I believe that E-accounting can provide us with more accurate data. | |

| COVID-19 | ||

| COVID1 | COVID-19 has had an adverse impact on our business. | (Song et al. 2022) |

| COVID2 | COVID-19 has made daily work even more challenging. | |

| COVID3 | COVID-19 has added to concerns about their future development. | |

| COVID4 | COVID-19 has inspired our business to take the initiative to expand businesses. | |

| COVID5 | COVID-19 has caused me to work longer hours. | |

| COVID6 | COVID-19 has made work more demanding. |

References

- Alalwan, Jaffar, Manoj A. Thomas, and H. Roland Weistroffer. 2014. Decision support capabilities of enterprise content management systems: An empirical investigation. Decision Support Systems 68: 39–48. [Google Scholar] [CrossRef]

- Aliedan, Meqbel, Abu Elnasr Sobaih, Mansour Alyahya, and Ibrahim Elshaer. 2022. Influences of Distributive Injustice and Job Insecurity Amid COVID-19 on Unethical Pro-Organisational Behaviour: Mediating Role of Employee Turnover Intention. International Journal of Environmental Research and Public Health 19: 7040. [Google Scholar] [CrossRef]

- Al-Dalaien, Borhan Omar Ahmad, and Bader Omar Ahmad Dalayeen. 2018. Investigating the Impact of Accounting Information System on the Profitability of Jordanian Banks. Research Journal of Finance and Accounting 9: 110–18. [Google Scholar]

- Al-Frijat, Yaser Saleh. 2014. The impact of accounting information systems used in the income tax department on the effectiveness of tax audit and collection in Jordan. Journal of Emerging Trends in Economics and Management Sciences 5: 19–25. [Google Scholar]

- Al-Hiyari, Ahmad, Mohammed Hamood Hamood Al-Mashregy, Nik Kamariah Nik Mat, and Jamal Mohammed Esmail Alekam. 2013. Factors that affect accounting information system implementation and accounting information quality: A survey in University Utara Malaysia. American Journal of Economics 3: 27–31. [Google Scholar]

- Almaiah, Mohammed Amin, Ali Al-Rahmi, Fahad Alturise, Lamia Hassan, Abdalwali Lutfi, Mahmaod Alrawad, Salem Alkhalaf, Waleed Mugahed Al-Rahmi, Saleh Al-sharaieh, and Theyazn H. H. Aldhyani. 2022a. Investigating the Effect of Perceived Security, Perceived Trust, and Information Quality on Mobile Payment Usage through Near-Field Communication (NFC) in Saudi Arabia. Electronics 11: 3926. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Ali Mugahed Al-Rahmi, Fahad Alturise, Mahmaod Alrawad, Salem Alkhalaf, Abdalwali Lutfi, Waleed Mugahed Al-Rahmi, and Ali Bani Awad. 2022b. Factors influencing the adoption of internet banking: An integration of ISSM and UTAUT with price value and perceived risk. Frontiers in Psychology 13: 919198. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Fahima Hajjej, Abdalwali Lutfi, Ahmad Al-Khasawneh, Rami Shehab, Shaha Al-Otaibi, and Mahmaod Alrawad. 2022c. Explaining the Factors Affecting Students’ Attitudes to Using Online Learning (Madrasati Platform) during COVID-19. Electronics 11: 973. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Fahima Hajjej, Abdalwali Lutfi, Ahmad Al-Khasawneh, Tayseer Alkhdour, Omar Almomani, and Rami Shehab. 2022d. A Conceptual Framework for Determining Quality Requirements for Mobile Learning Applications Using Delphi Method. Electronics 11: 788. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Fahima Hajjej, Rima Shishakly, Abdalwali Lutfi, Ali Amin, and Ali Bani Awad. 2022e. The Role of Quality Measurements in Enhancing the Usability of Mobile Learning Applications during COVID-19. Electronics 11: 1951. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Khadija Alhumaid, Abid Aldhuhoori, Noha Alnazzawi, Ahmad Aburayya, Raghad Alfaisal, Said A. Salloum, Abdalwali Lutfi, Ahmed Al Mulhem, Tayseer Alkhdour, and et al. 2022f. Factors Affecting the Adoption of Digital Information Technologies in Higher Education: An Empirical Study. Electronics 11: 3572. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Raghad Alfaisal, Said A. Salloum, Fahima Hajjej, Rima Shishakly, Abdalwali Lutfi, Mahmaod Alrawad, Ahmed Al Mulhem, Tayseer Alkhdour, and Rana Saeed Al-Maroof. 2022g. Measuring Institutions’ Adoption of Artificial Intelligence Applications in Online Learning Environments: Integrating the Innovation Diffusion Theory with Technology Adoption Rate. Electronics 11: 3291. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Raghad Alfaisal, Said A. Salloum, Fahima Hajjej, Sarah Thabit, Fuad Ali El-Qirem, Abdalwali Lutfi, Mahmaod Alrawad, Ahmed Al Mulhem, Tayseer Alkhdour, and et al. 2022h. Examining the Impact of Artificial Intelligence and Social and Computer Anxiety in E-Learning Settings: Students’ Perceptions at the University Level. Electronics 11: 3662. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Raghad Alfaisal, Said A. Salloum, Shaha Al-Otaibi, Omar Said Al Sawafi, Rana Saeed Al-Maroof, Abdalwali Lutfi, Mahmaod Alrawad, Ahmed Al Mulhem, and Ali Bani Awad. 2022i. Determinants influencing the continuous intention to use digital technologies in Higher Education. Electronics 11: 2827. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Raghad Alfaisal, Said Salloum, Shaha Al-Otaibi, Rima Shishakly, Abdalwali Lutfi, Mahmaod Alrawad, Ahmed Al Mulhem, Ali Bani Awad, and Rana Saeed Al-Maroof. 2022j. Integrating Teachers’ TPACK Levels and Students’ Learning Motivation, Technology Innovativeness, and Optimism in an IoT Acceptance Model. Electronics 11: 3197. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Shaha Al-Otaibi, Abdalwali Lutfi, Omar Almomani, Arafat Awajan, Adeeb Alsaaidah, Mahmoad Alrawad, and Ali Bani Awad. 2022k. Employing the TAM Model to Investigate the Readiness of M-Learning System Usage Using SEM Technique. Electronics 11: 1259. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Sarra Ayouni, Fahima Hajjej, Abdalwali Lutfi, Omar Almomani, and Ali Bani Awad. 2022l. Smart Mobile Learning Success Model for Higher Educational Institutions in the Context of the COVID-19 Pandemic. Electronics 11: 1278. [Google Scholar] [CrossRef]

- Al-Mugheed, Khaild, Nurhan Bayraktar, Mohammad Al-Bsheish, Adi AlSyouf, Badr K. Aldhmadi, Mu’taman Jarrar, and Moath Alkhazali. 2022. Effectiveness of game-based virtual reality phone application and online education on knowledge, attitude and compliance of standard precautions among nursing students. PLoS ONE 17: e0275130. [Google Scholar] [CrossRef] [PubMed]

- Alrawad, Mahmaod, Abdalwali Lutfi, Sundus Alyatama, Ibrahim Elshaer, and Mohammed Amin Almaiah. 2022. Perception of Occupational and Environmental Risks and Hazards among Mineworkers: A Psychometric Paradigm Approach. International Journal of Environmental Research and Public Health 19: 3371. [Google Scholar] [CrossRef] [PubMed]

- Alrawad, Mahmaod, Abdalwali Lutfi, Sundus Alyatama, Adel Al Khattab, Sliman S. Alsoboa, Mohammed Amin Almaiah, Mujtaba Hashim Ramadan, Hussin Mostafa Arafa, Nazar Ali Ahmed, Adi Alsyouf, and et al. 2023. Assessing customers perception of online shopping risks: A structural equation modeling–based multigroup analysis. Journal of Retailing and Consumer Services 71: 103188. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan F. 2019. The Effect of Peer Influence on Sales Tax Compliance among Jordanian SMEs. International Journal of Academic Research in Business and Social Sciences 9: 710–21. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, and Hijattulah Abdul-Jabbar. 2020a. Moderating role of patriotism on sales tax compliance among Jordanian SMEs. International Journal of Islamic and Middle Eastern Finance and Management 13: 389–415. [Google Scholar] [CrossRef]

- Alshira’h, Ahmad Farhan, Moh Alsqour, Abdalwali Lutfi, Adi Alsyouf, and Malek Alshirah. 2020b. A Socio-Economic Model of Sales Tax Compliance. Economies 8: 88. [Google Scholar] [CrossRef]

- Alshirah, Malek, Abdalwali Lutfi, Ahmad Alshirah, Mohamed Saad, Nahla Mohamad El Sayed Ibrahim, and Fathallah Mohammed. 2021a. Influences of the environmental factors on the intention to adopt cloud based accounting information system among SMEs in Jordan. Accounting 7: 645–54. [Google Scholar] [CrossRef]

- Alshirah, Malek Hamed, Ahmad Farhan Alshira’h, and Abdalwali Lutfi. 2021b. Political connection, family ownership and corporate risk disclosure: Empirical evidence from Jordan. Meditari Accountancy Research 30: 1241–64. [Google Scholar] [CrossRef]

- Alshirah, Malek Hamed, Ahmad Farhan Alshira’h, and Abdalwali Lutfi. 2021c. Audit committee’s attributes, overlapping memberships on the audit committee and corporate risk disclosure: Evidence from Jordan. Accounting 7: 423–40. [Google Scholar] [CrossRef]

- Alsmadi, Ayman Abdalmajeed, Mohammad Salem Oudat, and Hafnida Hasan. 2020. Islamic finance value versus conventional finance, dynamic equilibrium relationships analysis with macroeconomic variables in the jordanian economy: An ardl approach. Change Management 130: 1–14. [Google Scholar]

- Alsmadi, Ayman Abdalmajeed, Mais Sha’ban, and Omran Ahmad Al-Ibbini. 2019. The Relationship between E-banking Services and Bank Profit in Jordan for the Period of 2010–2015. Proceedings of the 2019 5th International Conference on E-Business and Applications, Bangkok, Thailand, February 25–28; pp. 70–74. Available online: https://dl.acm.org/doi/proceedings/10.1145/3317614 (accessed on 3 December 2022).

- Alsmadi, Ayman Abdalmajeed, and Mohammad Salem Oudat. 2019. The effect of foreign direct investment on financial development: Empirical evidence from Bahrain. Ekonomski pregled 70: 22–40. [Google Scholar] [CrossRef]

- Alsmadi, Ayman Abdalmajeed, and Marwan Alzoubi. 2022. Green economy: Bibliometric analysis approach. International Journal of Energy Economics and Policy 12: 282–89. [Google Scholar] [CrossRef]

- Alsmadi, Ayman Abdalmajeed, Najed Alrawashdeh, Ala’a Fouad Al-Dweik, and Mohammed Al-Assaf. 2022. Cryptocurrencies: A bibliometric analysis. International Journal of Data and Network Science 6: 619–28. [Google Scholar] [CrossRef]

- Alsyouf, Adi, and Awanis Ku Ishak. 2018. Understanding EHRs continuance intention to use from the perspectives of UTAUT: Practice environment moderating effect and top management support as predictor variables. International Journal of Electronic Healthcare 10: 24–59. [Google Scholar] [CrossRef]

- Alsyouf, Adi, Abdalwali Lutfi, Mohammad Al-Bsheish, Mu’taman Jarrar, Khalid Al-Mugheed, Mohammed Amin Almaiah, Fahad Nasser Alhazmi, Ra’ed Masa’deh, Rami J. Anshasi, and Abdallah Ashour. 2022a. Exposure Detection Applications Acceptance: The Case of COVID-19. International Journal of Environmental Research and Public Health 19: 7307. [Google Scholar] [CrossRef] [PubMed]

- Alsyouf, Adi, Awanis Ku Ishak, Abdalwali Lutfi, Fahad Nasser Alhazmi, and Manaf Al-Okaily. 2022b. The Role of Personality and Top Management Support in Continuance Intention to Use Electronic Health Record Systems among Nurses. International Journal of Environmental Research and Public Health 19: 11125. [Google Scholar] [CrossRef] [PubMed]

- Alsyouf, Adi, Ra’ed Masa’deh, Moteb Albugami, Mohammad Al-Bsheish, Abdalwali Lutfi, and Nizar Alsubahi. 2021. Risk of Fear and Anxiety in Utilising Health App Surveillance Due to COVID-19: Gender Differences Analysis. Risks 9: 179. [Google Scholar] [CrossRef]

- Alzoubi, Ali. 2011. The effectiveness of the accounting information system under the enterprise resources planning (ERP). Research Journal of Finance and Accounting 2: 10–19. [Google Scholar]

- Anggadini, Sri Dewi. 2015. The effect of top management support and internal control of the accounting information systems quality and its implications on the accounting information quality. Information Management and Business Review 7: 93–102. [Google Scholar] [CrossRef]

- Arora, Monika, and Anand Kumar. 2022. An Empirical Study on Make-or-buy Decision Making. International Journal of Education and Management Engineering 12: 19–28. [Google Scholar] [CrossRef]

- Arshah, Ruzaini Abdullah, Mohammad Ishak Desa, and Ab Razak Che Hussin. 2012. Establishing important criteria and factors for successful integrated information system. Global Journal on Technology 2: 311–17. [Google Scholar]

- Azazz, Alaa M. S., and Ibrahim A. Elshaer. 2022. Amid COVID-19 pandemic, entrepreneurial resilience and creative performance with the mediating role of institutional orientation: A quantitative investigation using structural equation modeling. Mathematics 10: 2127. [Google Scholar] [CrossRef]

- Bani-Khalid, Tareq, Ahmad Farhan Alshira’h, and Malek Hamed Alshirah. 2022. Determinants of Tax Compliance Intention among Jordanian SMEs: A Focus on the Theory of Planned Behavior. Economies 10: 30. [Google Scholar] [CrossRef]

- Bhattacherjee, Anol. 2001. Understanding information systems continuance: An expectation-confirmation model. MIS Quarterly 25: 351–70. [Google Scholar] [CrossRef]

- Bokhari, Rahat. 2005. The relationship between system usage and user satisfaction: A meta-analysis. Journal of Enterprise Information Management 18: 211–34. [Google Scholar] [CrossRef]

- Chang, Yun-ke, Xue Zhang, Intan Azura Mokhtar, Schubert Foo, Shaheen Majid, Brendan Luyt, and Yin-leng Theng. 2012. Assessing students’ information literacy skills in two secondary schools in Singapore. Journal of Information Literacy 6: 19–34. [Google Scholar] [CrossRef]

- Chou, Huey-Wen, Hsiu-Hua Chang, Yu-Hsun Lin, and Shyan-Bin Chou. 2014. Drivers and effects of post-implementation learning on ERP usage. Computers in Human Behavior 35: 267–77. [Google Scholar] [CrossRef]

- Chou, Jui-Sheng, and Jhih-Hao Hong. 2013. Assessing the impact of quality determinants and user characteristics on successful enterprise resource planning project implementation. Journal of Manufacturing Systems 32: 792–800. [Google Scholar] [CrossRef]

- Cohen, Jo. 1992. Statistical power analysis. Current Directions in Psychological Science 1: 98–101. [Google Scholar] [CrossRef]

- Cullen, Andrea J., and Margaret Taylor. 2009. Critical success factors for B2B e-commerce use within the UK NHS pharmaceutical supply chain. International Journal of Operations & Production Management 29: 1156–85. [Google Scholar]

- Daoud, Hazar, and Mohamed Triki. 2013. Accounting information systems in an ERP environment and tunisian firm performance. International Journal of Digital Accounting Research 13: 1–35. [Google Scholar] [CrossRef]

- Das, Ashok. 1989. Integrable Models. Singapore: World Scientific, vol. 30. [Google Scholar]

- Dehghanpouri, Houriyeh, Zeynab Soltani, and Reza Rostamzadeh. 2020. The impact of trust, privacy and quality of service on the success of E-CRM: The mediating role of customer satisfaction. Journal of Business & Industrial Marketing 35: 1831–47. [Google Scholar]

- DeLone, William, and Ephraim McLean. 1992. Information systems success: The quest for the dependent variable. Information Systems Research 3: 60–95. [Google Scholar] [CrossRef]

- DeLone, William, and Ephraim McLean. 2003. The DeLone and McLean model of information system success: A ten-year update. Journal of Management Information Systems 19: 3–9. [Google Scholar]

- Duarte, Paulo Alexandre, and Mário Lino Raposo. 2010. A PLS model to study brand preference: An application to the mobile phone market. In Handbook of Partial Least Squares: Springer Handbooks of Computational Statistics. Berlin/Heidelberg: Springer, pp. 449–84. [Google Scholar]

- Eid, Mustafa Ismail Mustafa, and Hani I. Abbas. 2017. User Adaptation and ERP Benefits: Moderation Analysis of User Experience with ERP. Kybernetes 46: 530–49. [Google Scholar] [CrossRef]

- Elshaer, Ibrahim, and Samar Saad. 2022. Learning from Failure: Building Resilience in Small-and Medium-Sized Tourism Enterprises, the Role of Servant Leadership and Transparent Communication. Sustainability 14: 15199. [Google Scholar] [CrossRef]

- Fadelelmoula, Ashraf Ahmed. 2018. The effects of the critical success factors for ERP implementation on the comprehensive achievement of the crucial roles of information systems in the higher education sector. Interdisciplinary Journal of Information, Knowledge, and Management 13: 21–44. [Google Scholar] [CrossRef] [PubMed]

- Fitrios, Ruhul. 2016. Factors that influence accounting information system implementation and accounting information quality. International Journal of Scientific & Technology Research 5: 192–98. [Google Scholar]

- Ghobakhloo, Morteza, Adel Azar, and Sai Hong Tang. 2019. Business Value of Enterprise Resource Planning Spending and Scope: A Post-Implementation Perspective. Kybernetes 48: 967–89. [Google Scholar] [CrossRef]

- Ghobakhloo, Morteza, and Sai Hong Tang. 2015. Information system success among manufacturing SMEs: Case of developing countries. Information Technology for Development 21: 573–600. [Google Scholar] [CrossRef]

- Hair, Joseph, Jeffrey Risher, Marko Sarstedt, and Christian Ringle. 2019. When to use and how to report the results of PLS-SEM. European Business Review 31: 2–24. [Google Scholar] [CrossRef]

- Hambali, Atika Jauharia Hatta. 2020. The success of e-filing adoption during COVID 19 pandemic: The role of collaborative quality, user intention, and user satisfaction. Journal of Economics, Business, and Accountancy Ventura 23: 57–68. [Google Scholar] [CrossRef]

- Hamdan, Mousa, and Naser Al-Hajri. 2021. The effect of information systems success factors on user satisfaction in accounting information systems. Management Science Letters 11: 2045–52. [Google Scholar] [CrossRef]

- Heo, Jaeho, and Ingoo Han. 2003. Performance measure of information systems (IS) in evolving computing environments: An empirical investigation. Information & Management 40: 243–56. [Google Scholar]

- Hou, Chung-Kuang. 2013. Measuring the impacts of the integrating information systems on decision-making performance and organisational performance: An empirical study of the Taiwan semiconductor industry. International Journal of Technology, Policy and Management 13: 34–66. [Google Scholar] [CrossRef]

- Hsu, Pei-Fang, HsiuJu Rebecca Yen, and Jung-Ching Chung. 2015. Assessing ERP post-implementation success at the individual level: Revisiting the role of service quality. Information & Management 52: 925–42. [Google Scholar]

- Hurt, Robert. 2013. Accounting Information Systems: Basic Concepts and Current Issues, 3rd ed. New York: McGraw-Hill. [Google Scholar]

- Hwang, Yujong, Mohanned Al-Arabiat, Dong-Hee Shin, and Younghwa Lee. 2016. Understanding information proactiveness and the content management system adoption in pre-implementation stage. Computers in Human Behavior 64: 515–23. [Google Scholar] [CrossRef]

- Idris, Kamil Md, and Rosli Mohamad. 2016. The influence of technological, organizational and environmental factors on accounting information system usage among Jordanian small and medium-sized enterprises. International Journal of Economics and Financial Issues 6: 240–48. [Google Scholar]

- Ifinedo, Princely, Birger Rapp, Airi Ifinedo, and Klas Sundberg. 2010. Relationships among ERP post-implementation success constructs: An analysis at the organizational level. Computers in Human Behavior 26: 1136–48. [Google Scholar] [CrossRef]

- Jaafreh, Ali Bakhit. 2017. Evaluation information system success: Applied DeLone and McLean information system success model in context banking system in KSA. International Review of Management and Business Research 6: 829–45. [Google Scholar]

- Jaber, Mustafa Musa, Thamer Alameri, Mohammed Hasan Ali, Adi Alsyouf, Mohammad Al-Bsheish, Badr K. Aldhmadi, Sarah Yahya Ali, Sura Khalil Abd, Saif Mohammed Ali, Waleed Albaker, and et al. 2022. Remotely Monitoring COVID-19 Patient Health Condition Using Metaheuristics Convolute Networks from IoT-Based Wearable Device Health Data. Sensors 22: 1205. [Google Scholar] [CrossRef] [PubMed]

- Jiang, James, Gary Klein, and Suzanne Crampton. 2000. A note on SERVQUAL reliability and validity in information system service quality measurement. Decision Sciences 31: 725–44. [Google Scholar] [CrossRef]

- Jaoua, Fakher, Hussein Almurad, Ibrahim Elshaer, and Elsayed S. Mohamed. 2022. E-Learning Success Model in the Context of COVID-19 Pandemic in Higher Educational Institutions. International Journal of Environmental Research and Public Health 2022: 2865. [Google Scholar] [CrossRef] [PubMed]

- Kharuddin, Saira, Soon-Yau Foong, and Rosmila Senik. 2015. Effects of decision rationality on ERP adoption extensiveness and organizational performance. Journal of Enterprise Information Management 28: 658–79. [Google Scholar] [CrossRef]

- Khassawneh, Abd Alwali Lutfi. 2014. The influence of organizational factors on accounting information systems (AIS) effectiveness: A study of Jordanian SMEs. International Journal of Marketing and Technology 4: 36. [Google Scholar]

- Laitinen, Erkki. 2014. Influence of cost accounting change on performance of manufacturing firms. Advanced Account 30: 230–40. [Google Scholar] [CrossRef]

- Li, Yanxing, and Jinghai Wang. 2021. Evaluating the Impact of Information System Quality on Continuance Intention toward Cloud Financial Information System. Frontiers in Psychology 12: 713353. [Google Scholar] [CrossRef]

- Lin, Hsiu-Fen. 2010. An investigation into the effects of IS quality and top management support on ERP system usage. Total Quality Management 21: 335–49. [Google Scholar] [CrossRef]

- Lin, Hua-Yang, Ping-Yu Hsu, and Ping-Ho Ting. 2006. ERP systems success: An integration of IS success model and balanced scorecard. Journal of Research and Practice in Information Technology 38: 215–28. [Google Scholar]

- Lutfi, Abdalwali. 2020. Investigating the moderating effect of Environment Uncertainty on the relationship between institutional factors and ERP adoption among Jordanian SMEs. Journal of Open Innovation: Technology, Market, and Complexity 6: 91. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali. 2021. Understanding Cloud Based Enterprise Resource Planning Adoption among SMEs in Jordan. Journal of Theoretical and Applied Information Technology 99: 5944–53. [Google Scholar]

- Lutfi, Abdalwali. 2022a. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 10: 75. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali. 2022b. Understanding the Intention to Adopt Cloud-based Accounting Information System in Jordanian SMEs. The International Journal of Digital Accounting Research 22: 47–70. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Adi Alsyouf, Mohammed Amin Almaiah, Mahmaod Alrawad, Ahmed Abdullah Khalil Abdo, Akif Lutfi Al-Khasawneh, Nahla Ibrahim, and Mohamed Saad. 2022a. Factors Influencing the Adoption of Big Data Analytics in the Digital Transformation Era: Case Study of Jordanian SMEs. Sustainability 14: 1802. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Manaf Al-Okaily, Hamza Alqudah, Mohamed Saad, Nahla Ibrahim, and Osama Abdelmaksoud. 2022b. Antecedents and Impacts of Enterprise Resource Planning System Adoption among Jordanian SMEs. Sustainability 14: 3508. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Akif Lutfi Al-Khasawneh, Mohammed Amin Almaiah, Adi Alsyouf, and Mahmaod Alrawad. 2022c. Business Sustainability of Small and Medium Enterprises during the COVID-19 Pandemic: The Role of AIS Implementation. Sustainability 14: 5362. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Akif Lutfi Al-Khasawneh, Mohammed Amin Almaiah, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Adi Alsyouf, Mahmaod Alrawad, Ahmad Al-Khasawneh, Mohamed Saad, and Rommel Al Ali. 2022d. Antecedents of Big Data Analytic Adoption and Impacts on Performance: Contingent Effect. Sustainability 14: 15516. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Maryam Ashraf, Waqas Ahmad Watto, and Mahmaod Alrawad. 2022e. Do Uncertainty and Financial Development Influence the FDI Inflow of a Developing Nation? A Time Series ARDL Approach. Sustainability 14: 12609. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Saleh Zaid Alkilani, Mohamed Saad, Malek Hamed Alshirah, Ahmad Farhan Alshirah, Mahmaod Alrawad, Malak Akif Al-Khasawneh, Nahla Ibrahim, Abeer Abdelhalim, and Mujtaba Hashim Ramadan. 2022f. The Influence of Audit Committee Chair Characteristics on Financial Reporting Quality. J. Risk Financial Managagement 15: 563. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Manaf Al-Okaily, Adi Alsyouf, and Mahmaod Alrawad. 2022g. Evaluating the D&M IS Success Model in the Context of Accounting Information System and Sustainable Decision Making. Sustainability 14: 8120. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Mohamed Saad, Mohammed Amin Almaiah, Abdallah Alsaad, Ahmad Al-Khasawneh, Mahmaod Alrawad, Adi Alsyouf, and Akif Lutfi Al-Khasawneh. 2022h. Actual Use of Mobile Learning Technologies during Social Distancing Circumstances: Case Study of King Faisal University Students. Sustainability 14: 7323. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali Saleh, Nafeth Alkelani, Malak Akif Al-Khasawneh, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Mohammed Amin Almaiah, Mahmaod Alrawad, Adi Alsyouf, Mohamed Saad, and Nahla Ibrahim. 2022i. Influence of Digital Accounting System Usage on SMEs Performance: The Moderating Effect of COVID-19. Sustainability 14: 15048. [Google Scholar] [CrossRef]

- Lutfi, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2017. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. Journal of Advanced Research in Business and Management Studies 6: 24–38. [Google Scholar]

- Lutfi, Abdalwali, Manaf Al-Okaily, Adi Alsyouf, Abdallah Alsaad, and Abdallah Taamneh. 2020. The Impact of AIS Usage on AIS Effectiveness among Jordanian SMEs: A Multi Group Analysis of the Role of Firm Size. Global Business Review 21: 1–19. [Google Scholar] [CrossRef]

- Lutfi, Abdalwali, Mahmaod Alrawad, Adi Alsyouf, Mohammed Amin Almaiah, Ahmad Al-Khasawneh, Akif Lutfi Al-Khasawneh, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Mohamed Saad, and Nahla Ibrahim. 2023. Drivers and impact of big data analytic adoption in the retail industry: A quantitative investigation applying structural equation modeling. Journal of Retailing and Consumer Services 70: 103129. [Google Scholar] [CrossRef]

- Marble, Robert. 2003. A system implementation study: Management commitment to project management. Information & Management 41: 111–23. [Google Scholar]

- Negash, Solomon, Terry Ryan, and Magid Igbaria. 2003. Quality and effectiveness in web-based customer support systems. Information & Management 40: 757–68. [Google Scholar]

- Nelson, Ryan, Peter Todd, and Barbara Wixom. 2005. Antecedents of information and system quality: An empirical examination within the context of data warehousing. Journal of Management Information Systems 21: 199–235. [Google Scholar] [CrossRef]

- Nguyen, Hieu Tat, and Anh Nguyen. 2020. Determinants of accounting information systems quality: Empirical evidence from Vietnam. Accounting 6: 185–98. [Google Scholar] [CrossRef]

- Okon, Edet Eyibio, Evans Otuza, and Samuel Dada. 2021. Effect of Human Resource in Accounting Information System on Management Decision-Making in Seventh—Day Adventist Institutions in Eastern Nigeria. Advances in Social Sciences Research Journal 8: 1–11. [Google Scholar] [CrossRef]

- Ouiddad, Ahmed, Chafik Okar, Razane Chroqui, and Imane Beqqali Hassani. 2018. Does the adoption of ERP systems help improving decision-making? A systematic literature review. Paper presented at 2018 IEEE International Conference on Technology Management, Operations and Decisions (ICTMOD), Marrakech, Morocco, November 21–23; Piscataway: IEEE, pp. 61–66. [Google Scholar]

- Petter, Stacie, and Ephraim McLean. 2009. A meta-analytic assessment of the DeLone and McLean IS success model: An examination of IS success at the individual level. Information & Management 46: 159–66. [Google Scholar]

- Petter, Stacie, William DeLone, and Ephraim McLean. 2008. Measuring information systems success: Models, dimensions, measures, and interrelationships. European Journal of Information Systems 17: 236–63. [Google Scholar] [CrossRef]

- Purwati, Astri Ayu, Zainol Mustafa, and Mazzlida Mat Deli. 2021. Management Information System in Evaluation of BCA Mobile Banking Using DeLone and McLean Model. Journal of Applied Engineering and Technological Science (JAETS) 2: 70–77. [Google Scholar] [CrossRef]

- Quintero, José Melchor Medina, Esther García Pedroche, and María Isabel de la Garza Ramos. 2009. Influence of the implementation factors in the information systems quality for the user satisfaction. Journal of Information Systems and Technology Management 6: 25–44. [Google Scholar] [CrossRef]

- Rajan, Christy Angeline, and Rupashree Baral. 2015. Adoption of ERP system: An empirical study of factors influencing the usage of ERP and its impact on end user. IIMB Management Review 27: 105–17. [Google Scholar] [CrossRef]

- Ramli, A. 2013. The impact of external factors on accounting information system (AIS) usage. Journal of Entrepreneurship and Business (JEB) 1: 1–14. [Google Scholar]

- Ritchi, Hamzah, Noer Fitri Evayanti, and Prima Yusi Sari. 2020. A study on information systems success: Examining user satisfaction of accounting information system: (A Study on whole City/Regency Governments of West Java Province). Bina Ekonomi 24: 1–14. [Google Scholar] [CrossRef]

- Saad, Mohamed, Abdalwali Lutfi, Mohammed Amin Almaiah, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Hamza Alqudah, Akif Lutfi Alkhassawneh, Adi Alsyouf, Mahmaod Alrawad, and Osama Abdelmaksoud. 2022. Assessing the Intention to Adopt Cloud Accounting during COVID-19. Electronics 11: 4092. [Google Scholar] [CrossRef]

- Sabah, Mohammed Ihsan Ahmed, Umi Kartini Rashid, Juzaimi Nasuredin, Nawzad Majeed Hamawandy, Hemn Adl Wali A. L. Bewani, and Diyar bdulmajeed Jamil. 2021. The Effect of Delone and Mclean’s Information System Success Model on The Job Performance of Accounting Managers in Iraqi Banks. Journal of Contemporary Issues in Business and Government 27: 6305–20. [Google Scholar]

- Saarinen, Timo. 1996. An expanded instrument for evaluating information system success. Information & management 31: 103–18. [Google Scholar]

- Sekaran, Uma, and Roger Bougie. 2010. Research Methods for Business, 5th ed. West Sussex: John Wiley & Sons. [Google Scholar]

- Sekaran, Uma, and Roger Bougie. 2013. Research Methods for Business: A Skill-Building Approach. West Sussex: John Willey & Sons Ltd. [Google Scholar]

- Shagari, Shamsudeen Ladan, Akilah Abdullah, and Rafeah Mat Saat. 2015. The influence of system quality and information quality on Accounting Information System (AIS) effectiveness in Nigerian bank. International Postgraduate Business Journal 58: 58–74. [Google Scholar]

- Scherer, Ronny, Fazilat Siddiq, and Jo Tondeur. 2019. The technology acceptance model (TAM): A meta-analytic structural equation modeling approach to explaining teachers’ adoption of digital technology in education. Computers & Education 128: 13–35. [Google Scholar]

- Sobaih, Abu Elnasr E., Ahmed Hasanein, and Ibrahim A. Elshaer. 2022. Higher Education in and after COVID-19: The Impact of Using Social Network Applications for E-Learning on Students’ Academic Performance. Sustainability 14: 5195. [Google Scholar] [CrossRef]

- Song, Jianmin, Senmao Xia, Demetris Vrontis, Arun Sukumar, Bing Liao, Qi Li, Kun Tian, and Nengzhi Yao. 2022. The Source of SMEs’ Competitive Performance in COVID-19: Matching Big Data Analytics Capability to Business Models. Information Systems Frontiers 24: 1167–87. [Google Scholar] [CrossRef]

- Syahidi, Aulia Akhrian, and Arifin Noor Asyikin. 2018. Strategic planning and implementation of academic information system (AIS) based on website with D&M model approach. IOP Conference Series: Materials Science and Engineering 407: 012101. [Google Scholar]

- Tajuddin, Muhammad. 2015. Modification of DeLon and Mclean Model in the Success of Information System for Good University Governance. Turkish Online Journal of Educational Technology-TOJET 14: 113–23. [Google Scholar]

- Thong, James, and Chee-Sing Yap. 1996. Information systems effectiveness: A user satisfaction approach. Information Processing & Management 32: 601–10. [Google Scholar]

- Trice, Andrew, and Michael Treacy. 1988. Utilization as a dependent variable in MIS research. ACM SIGMIS Database: The Database for Advances in Information Systems 19: 33–41. [Google Scholar] [CrossRef]

- Urbach, Nils, and Frederik Ahlemann. 2010. Structural equation modeling in information systems research using partial least squares. Journal of Information Technology Theory and Application 11: 5–40. [Google Scholar]

- Wade, Michael, and John Hulland. 2004. The resource-based view and information systems research: Review, extension, and suggestions for future research. MIS Quarterly 28: 107–42. [Google Scholar] [CrossRef]

- Wixom, Barbara, and Peter Todd. 2005. A theoretical integration of user satisfaction and technology acceptance. Information Systems Research 16: 85–102. [Google Scholar] [CrossRef]

- Xie, Ying, Colin James Allen, and Mahmood Ali. 2014. An integrated decision support system for ERP implementation in small and medium sized enterprises. Journal of Enterprise Information Management 27: 358–84. [Google Scholar] [CrossRef]

- Xu, Jingjun, Izak Benbasat, and Ronald Cenfetelli. 2013. Integrating service quality with system and information quality: An empirical test in the e-service context. MIS Quarterly 37: 777–94. [Google Scholar] [CrossRef]

- Yakubu, Nasiru, and Salihu Dasuki. 2018. Assessing eLearning systems success in Nigeria: An application of the DeLone and McLean information systems success model. Journal of Information Technology Education: Research 17: 183–203. [Google Scholar] [CrossRef] [PubMed]

- Zybin, Serhii, and Yana Bielozorova. 2021. Risk-based Decision-making System for Information Processing Systems. International Journal of Information Technology and Computer Science 13: 1–18. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Cronbach Alpha | Composite Reliability | AVEs |

|---|---|---|---|

| Information Quality | 0.909 | 0.929 | 0.738 |

| System Quality | 0.819 | 0.878 | 0.649 |

| Service Quality | 0.906 | 0.927 | 0.731 |

| COVID-19 | 0.773 | 0.854 | 0.549 |

| E-accounting Use | 0.910 | 0.941 | 0.838 |

| User Satisfaction | 0.939 | 0.957 | 0.850 |

| Business Performance | 0.780 | 0.858 | 0.616 |

| Constructs | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|---|

| 1 | Business Performance | 0.788 | ||||||

| 2 | Information Quality | 0.456 | 0.861 | |||||

| 3 | Service Quality | 0.278 | 0.530 | 0.854 | ||||

| 4 | System Quality | 0.444 | 0.659 | 0.558 | 0.809 | |||

| 5 | E-accounting Use | 0.450 | 0.495 | 0.431 | 0.519 | 0.900 | ||

| 6 | User Satisfaction | 0.549 | 0.615 | 0.548 | 0.579 | 0.554 | 0.923 | |

| 7 | COVID-19 | 0.372 | 0.306 | 0.247 | 0.659 | 0.280 | 0.088 | 0.832 |

| Hyp. | Relationships of Factors | Sta. Beta | t-Values | p-Values | Results |

|---|---|---|---|---|---|

| H1 | Information Quality–E-accounting | 0.233 | 1.961 | 0.050 | Supported |

| H2 | System Quality–E-accounting | 0.285 | 2.089 | 0.037 | Supported |

| H3 | Service Quality–E-accounting | 0.142 | 1.281 | 0.201 | Not supported |

| H4 | E-accounting–User Satisfaction | 0.251 | 2.648 | 0.007 | Supported |

| H5 | E-accounting Use–Business Performance | 0.215 | 2.112 | 0.036 | Supported |

| H6 | User Satisfaction–Business Performance | 0.441 | 5.056 | 0.000 | Supported |

| H7 | COVID-19–E-accounting–Business Performance | 0.204 | 4.991 | 0.000 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lutfi, A.; Alkelani, S.N.; Alqudah, H.; Alshira’h, A.F.; Alshirah, M.H.; Almaiah, M.A.; Alsyouf, A.; Alrawad, M.; Montash, A.; Abdelmaksoud, O. The Role of E-Accounting Adoption on Business Performance: The Moderating Role of COVID-19. J. Risk Financial Manag. 2022, 15, 617. https://doi.org/10.3390/jrfm15120617

Lutfi A, Alkelani SN, Alqudah H, Alshira’h AF, Alshirah MH, Almaiah MA, Alsyouf A, Alrawad M, Montash A, Abdelmaksoud O. The Role of E-Accounting Adoption on Business Performance: The Moderating Role of COVID-19. Journal of Risk and Financial Management. 2022; 15(12):617. https://doi.org/10.3390/jrfm15120617

Chicago/Turabian StyleLutfi, Abdalwali, Saleh Nafeth Alkelani, Hamza Alqudah, Ahmad Farhan Alshira’h, Malek Hamed Alshirah, Mohammed Amin Almaiah, Adi Alsyouf, Mahmaod Alrawad, Abdelhameed Montash, and Osama Abdelmaksoud. 2022. "The Role of E-Accounting Adoption on Business Performance: The Moderating Role of COVID-19" Journal of Risk and Financial Management 15, no. 12: 617. https://doi.org/10.3390/jrfm15120617

APA StyleLutfi, A., Alkelani, S. N., Alqudah, H., Alshira’h, A. F., Alshirah, M. H., Almaiah, M. A., Alsyouf, A., Alrawad, M., Montash, A., & Abdelmaksoud, O. (2022). The Role of E-Accounting Adoption on Business Performance: The Moderating Role of COVID-19. Journal of Risk and Financial Management, 15(12), 617. https://doi.org/10.3390/jrfm15120617