The Role of Sustainability Resources of Large Greenhouse Gas Emitters: The Case of Corporations in Alberta, Canada

Abstract

:1. Introduction

2. Materials and Methods

2.1. Specified Gas Emitters Regulation (SGER)

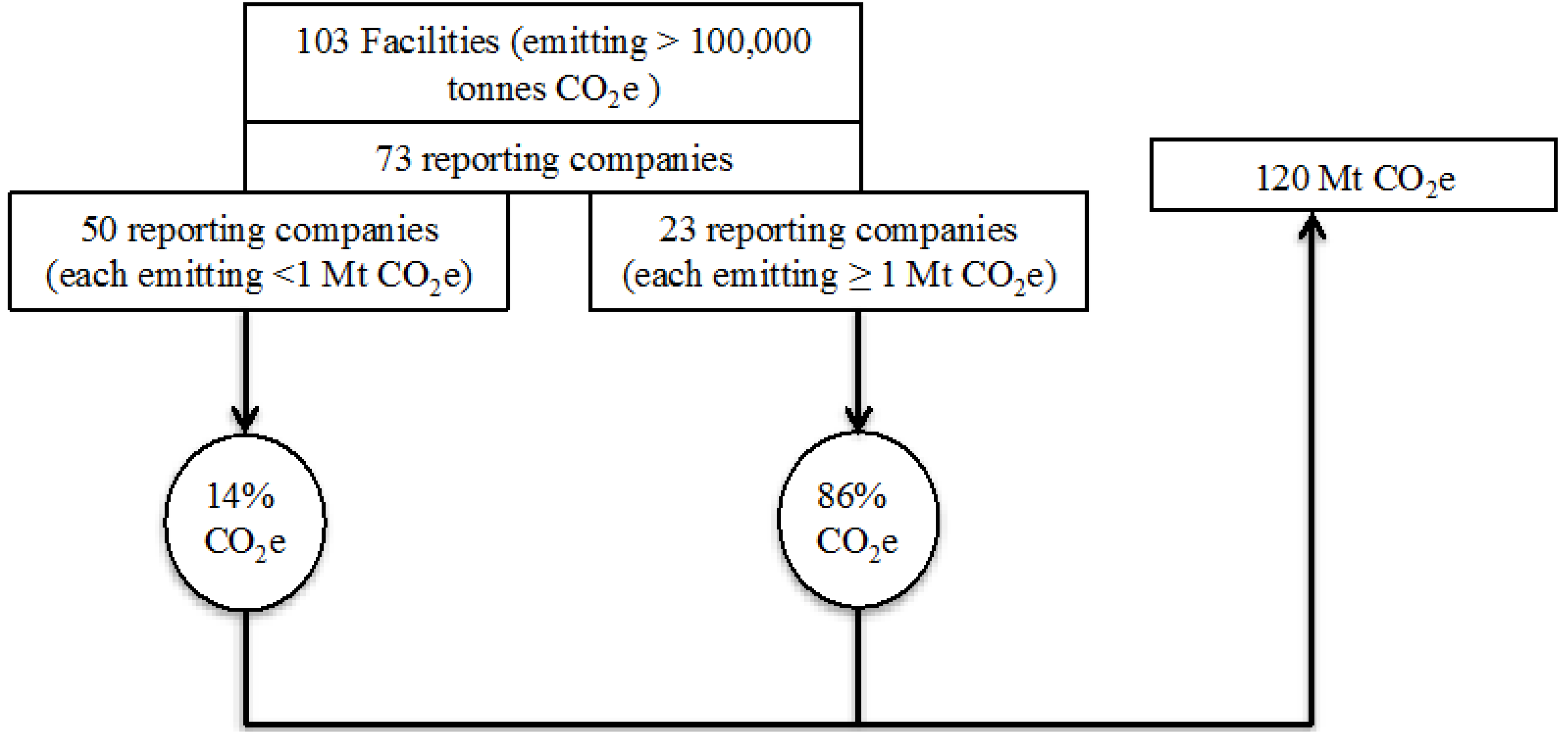

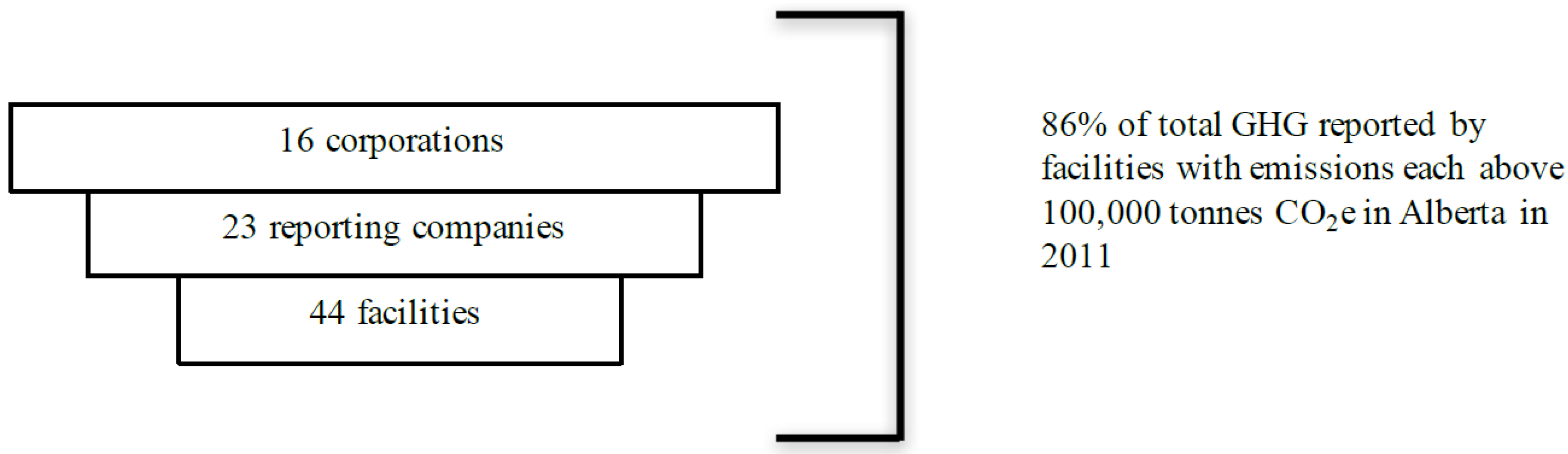

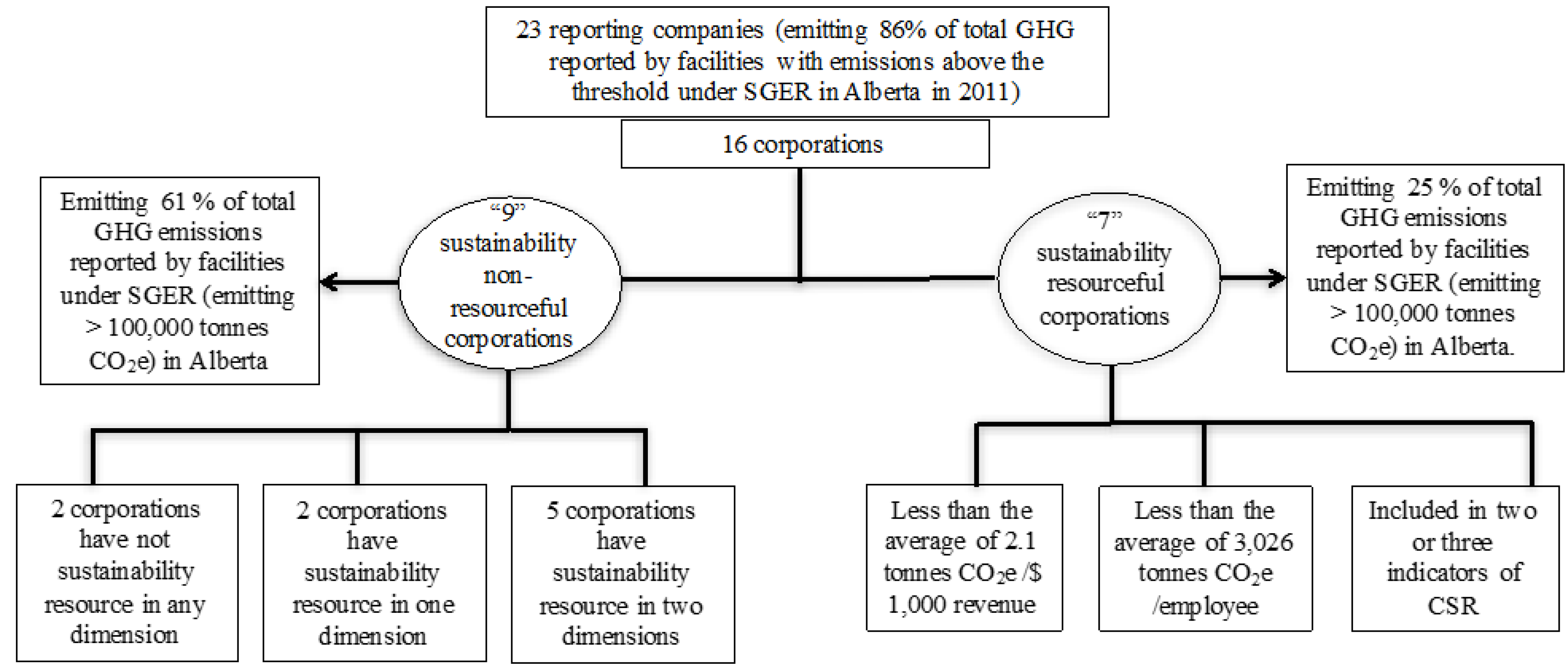

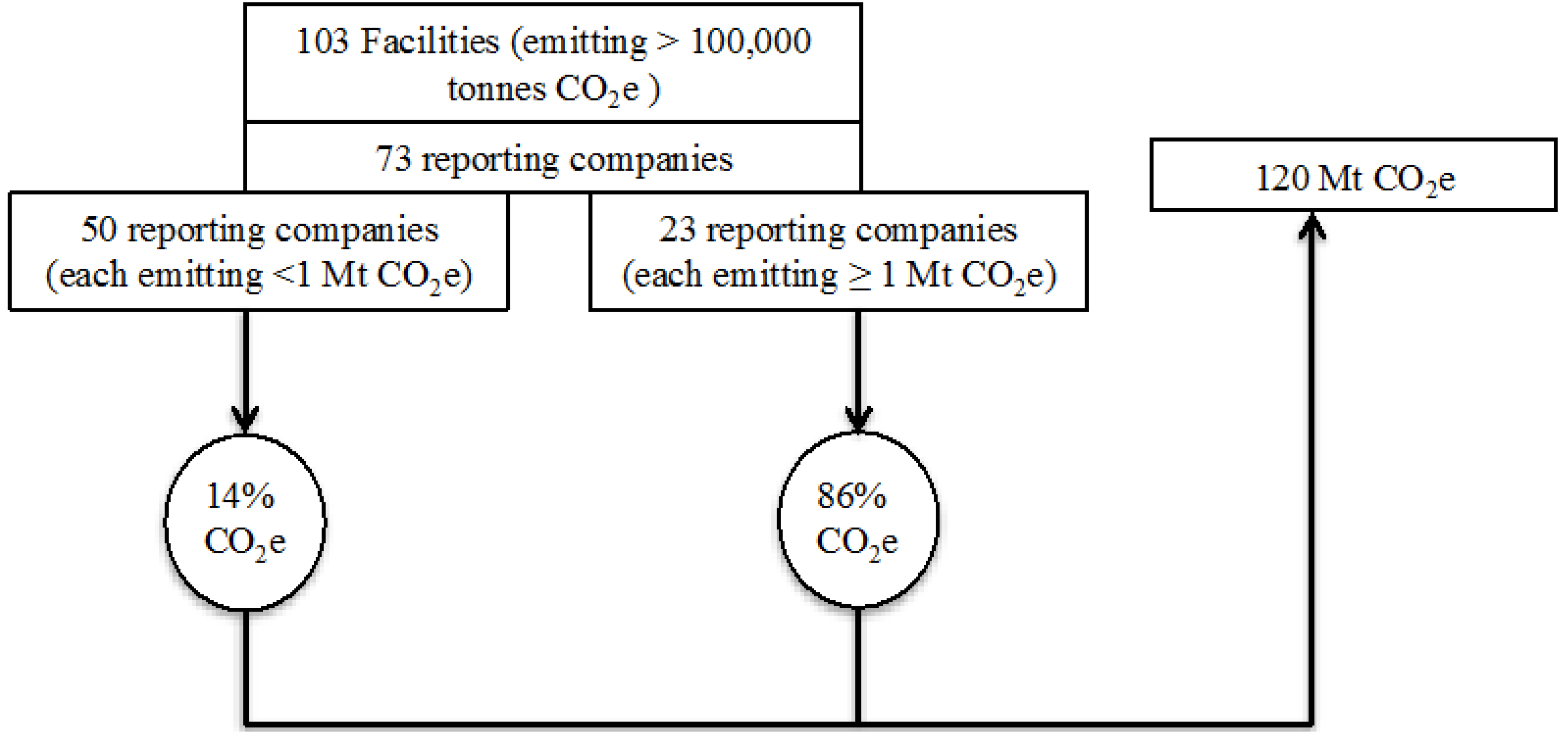

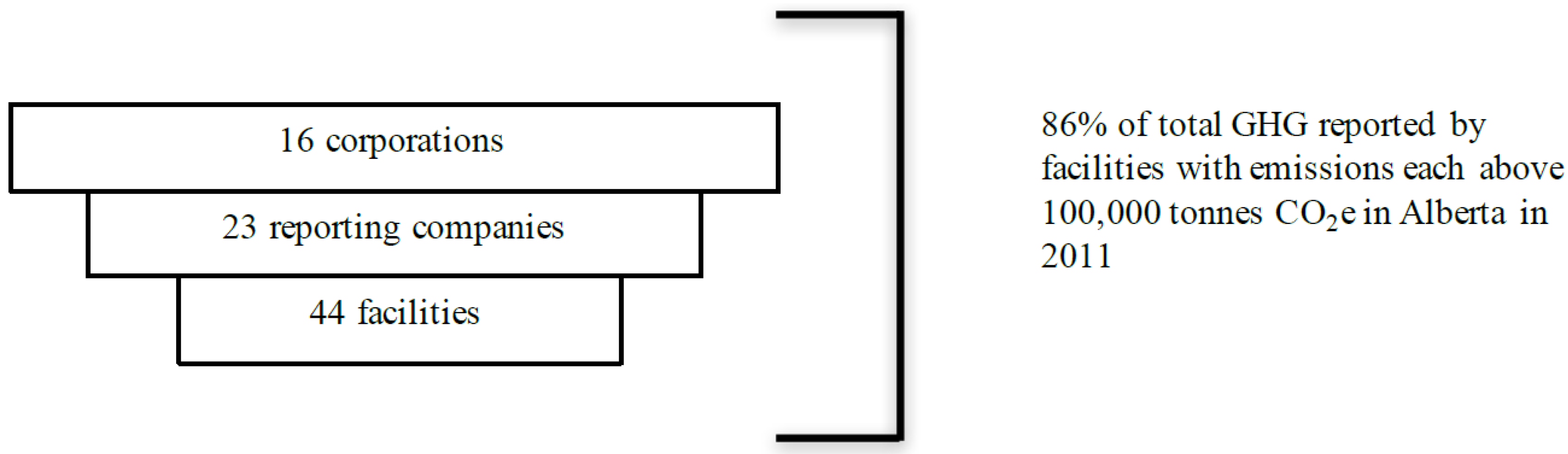

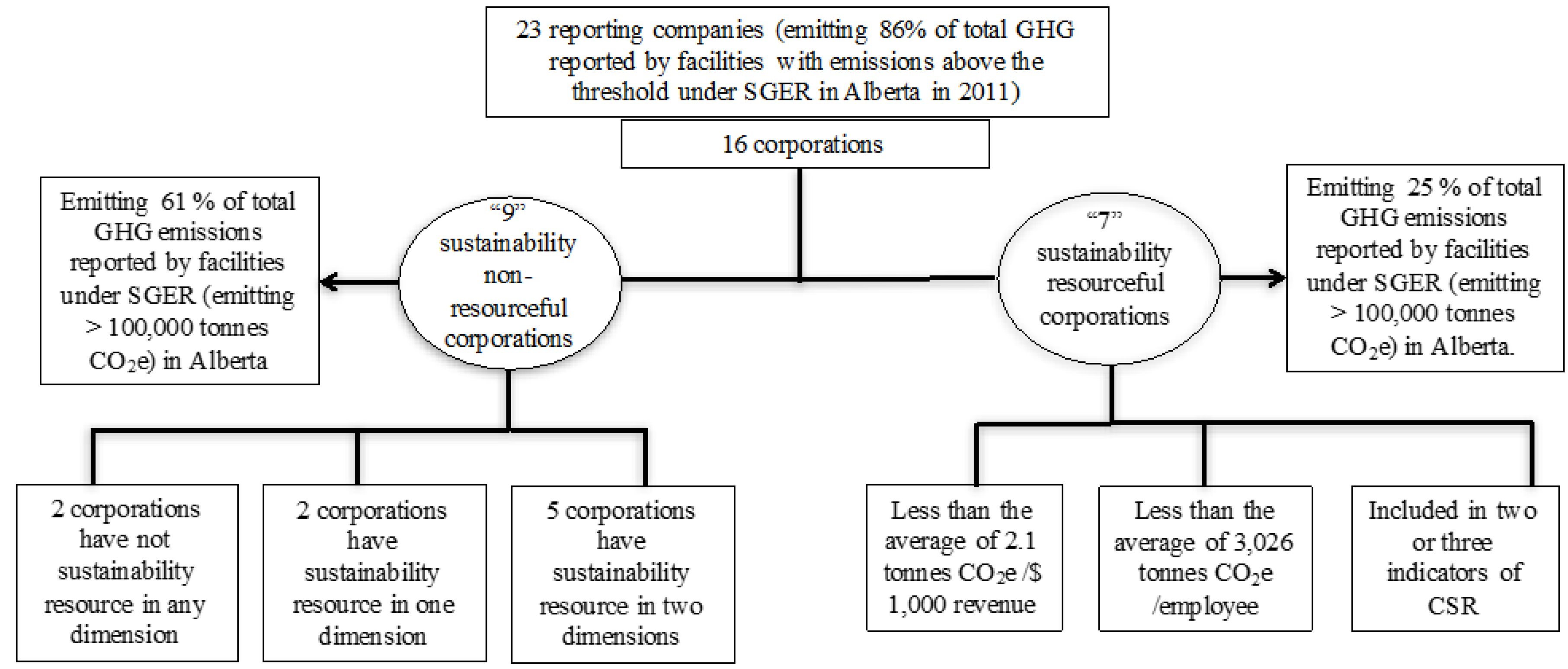

2.2. Companies Analyzed

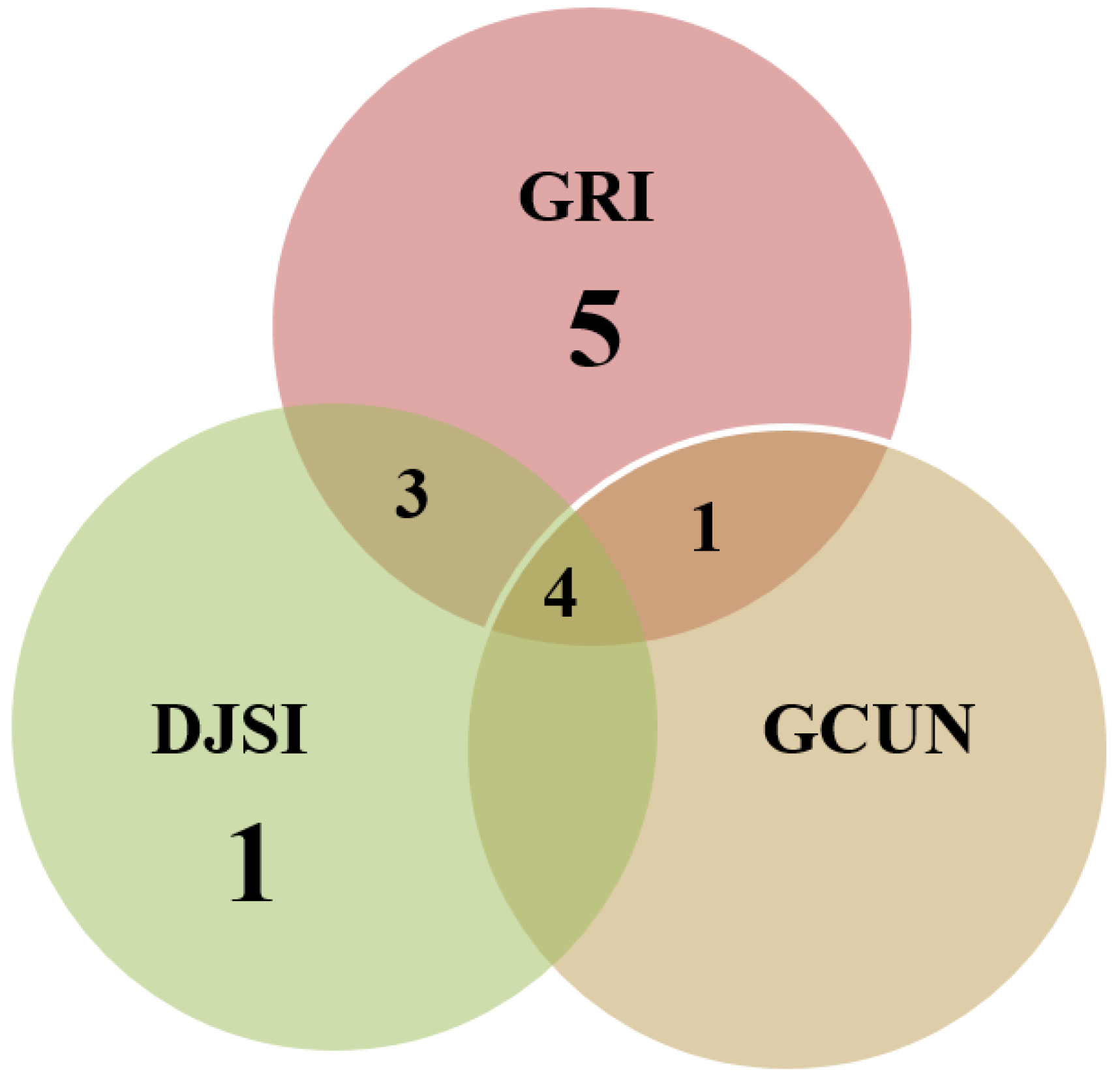

2.3. Sustainability-Driven Resources

- (1)

- Working with the Global Reporting Initiative (GRI) and using the third generation guidelines in sustainability reporting. The GRI is a leading organization in the sustainability field, which has developed sustainability reporting guidelines as a way to increase the social, environmental and economic performance of companies. Companies working with GRI use the sustainability reporting guidelines to communicate their sustainable performance [34].

- (2)

- Being listed on the Global and/or North American Dow Jones Sustainability Index (DJSI). These are a family of indexes that evaluate the sustainability performance of the largest 2500 companies listed on the Dow Jones Global Total Stock Market Index. To be included in this index, companies are assessed based on their long-term environmental, economic and social management plans [35,36].

- (3)

- Participation in the Global Compact United Nations (GCUN) and reporting in line with its principles. This is a global agreement or compact developed by the United Nations with businesses to align their operations with ten universally accepted principles in the areas of human rights, labor, the environment and anti-corruption. Members companies in this network support the compact and report in line with its principles [37].

3. Results

4. Discussion

4.1. Costs to Large Emitters

4.2. Incentivizing In-House Cleaner Production

- Offset credits are not achieving real reductions in emissions from the largest GHG emitters in Alberta; facilities using this option can continue their business-as-usual operations while generating their usual emissions and simply buy offset credits. In addition, according to a report from Pembina Institute, 82% of offset credits used for compliance with the SGER during 2008–2010 came from projects that started before the policy was announced [45]. Since January 2012, however, the Government of Alberta has removed this allowance for historic reductions to generate offset credits from the recent version of the Climate Change and Emissions Management Act [46]. In addition, projects can start generating offset credits from the time they got approved even before they start operating and achieving actual emission reductions. Therefore, this will not benefit Alberta’s 2020 target if the actual emission reductions from projects will start after 2020. Moreover, since 2011, the efficiency of the offset system has become worse with the allowance for double-counting of offset credits for one tonne of emission reductions associated with Carbon Capture and Storage projects [47]. As observed by Bramley et al. [47], this will introduce offset credits used by other companies to comply with the SGER that are not related to real reductions in emissions.

- Money paid to obtain fund credits and collected by the CCEM fund is oriented to deliver long-term emission reductions, which may not benefit Alberta’s 2020 target [48].

- -

- Some studies have suggested increasing the carbon levy of $15/tonne in order to create an incentive for large emitters to reduce emissions through internal improvements [47,48]. This scenario has been recently discussed by the IISD, with an increase of emissions intensity to 24% [41]. The modeling used by the IISD report has shown that most compliance options used by companies with this scenario will stay the same: cogeneration, offsets and fund credits. This model covers only oil and gas sector emissions, which is approximately 45% of the SGER emissions. In this case, the increase in emissions intensity will put pressure on offset market to satisfy demand. When there is no offset credit supply available in the market, facilities would choose the fund credit. Moreover, in addition to the long-term emission reductions that the fund credit can only achieve, 40% of this money would go to royalty and tax interaction for the province and federal government [41]. Therefore, doubling the fund credit or even increasing the emissions intensity will not create an incentive for large GHG emitters in Alberta to make internal emission reductions. However, this increase would be a good incentive if it is high enough to make cleaner production mechanisms competitive. However, determining the amount of this increase needs further research and is out of the scope of this paper.

- -

- On the other hand, some environmentalists have criticized the weak incentive provided by the SGER carbon pricing as it is based on emissions intensity targets [45,47,49]. They have suggested that a carbon tax charged on every tonne of emissions, irrespective of whether it is less or more than the 100,000 tonne per year, increases the incentive for large GHG emitters to make internal emission reductions. This comparison between the two carbon pricing approaches and the emissions reduction incentive they provide was the main discussion of an article by Leach [50]. The results of the analysis undertaken by Leach [50] have shown that the average cost of emissions with the SGER is weak compared to a carbon tax on all emissions. However, the SGER carbon price still provides a strong incentive for facilities in some ways. For example, the SGER provides a stronger incentive for improving productivity per unit of emissions than a carbon tax [50]. According to Leach [50], there is no big difference in the value of emissions cost between the two scenarios as other groups assume. Therefore, even this change will not create a stronger incentive for facilities than the current one to make internal improvements in their production processes.

5. Conclusions

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Government of Alberta. Climate Change and Emissions Management Act: Specified Gas Emitters Regulation; Alberta Regulation 139/2007; Alberta’s Queen’s Printer: Edmonton, AB, Canada, 2007. Available online: http://www.qp.alberta.ca/documents/Regs/2007_139.pdf (accessed on 5 September 2014).

- Rorie, M. An integrated theory of corporate environmental compliance and overcompliance. Crime Law Soc. Chang. 2015, 64, 65–101. [Google Scholar] [CrossRef]

- Thornton, D.; Kagan, R.A.; Gunningham, N. When social norms and pressures are not enough: Environmental performance in the trucking industry. Law Soc. Rev. 2009, 43, 405–437. [Google Scholar] [CrossRef]

- Kagan, R.A.; Thornton, D.; Gunningham, N. Explaining corporate environmental performance: How does regulation matter? Law Soc. Rev. 2003, 37, 51–90. [Google Scholar] [CrossRef]

- Gunningham, N.; Kagan, R.A.; Thornton, D. Social License and Environment Protection: Why Businesses Go beyond Compliance; Center for the Study of Law and Society Jurisprudence and Social Policy Program: Berkeley, CA, USA, 2002; Available online: http://www.escholarship.org/uc/item/35j962b3 (accessed on 11 January 2017).

- Gunningham, N.; Kagan, R.A.; Thornton, D. Social license and environmental protection: Why businesses go beyond compliance. Law Soc. Inq. 2004, 29, 307–342. [Google Scholar] [CrossRef]

- Gunningham, N.; Thornton, D.; Kagan, R.A. Motivating management: Corporate compliance in environmental protection. Law Policy 2005, 27, 289–316. [Google Scholar] [CrossRef]

- Beg, N.; Morlot, J.C.; Davidson, O.; Afrane-Okesse, Y.; Tyani, L.; Denton, F.; Sokona, Y.; Thomas, J.P.; La Rovere, E.L.; Parikh, J.K.; et al. Linkages between climate change and sustainable development. Clim. Policy 2002, 2, 129–144. [Google Scholar] [CrossRef]

- Cohen, S.; Demeritt, R.J.; Rothman, D. Climate change and sustainable development: Towards dialogue. Glob. Environ. Chang. 1998, 8, 341–371. [Google Scholar] [CrossRef]

- Munasinghe, M.; Swart, R. Primer on Climate Change and Sustainable Development: Facts, Policy and Analysis Applications; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2005. [Google Scholar]

- Swart, R.; Robinson, J.; Cohen, S. Climate change and sustainable development: Expanding the options. Clim. Policy 2003, 3, 19–40. [Google Scholar] [CrossRef]

- Winkler, H.; Spalding-Fecher, R.; Mwakasonda, S.; Davidson, O. Sustainable development policies and measures: Starting from development to tackle climate change. In Building on the Kyoto Protocol: Options for Protecting the Climate; Baumert, K.A., Blanchard, O., Llosa, S., Perkaus, J.P., Eds.; World Resources Institute: Washington, DC, USA, 2002; pp. 61–88. [Google Scholar]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Buysse, K.; Verbeke, A. Proactive environmental strategies: A stakeholder management perspective. Strateg. Manag. J. 2003, 24, 453–470. [Google Scholar] [CrossRef]

- Sharma, S.; Vredenburg, H. Proactive corporate environmental strategy and the development of competitively valuable organizational capabilities. Strateg. Manag. J. 1998, 19, 729–753. [Google Scholar] [CrossRef]

- Rueda-Manzanares, A.; Aragon-Correa, J.A.; Sharma, S. The influence of stakeholders on environmental strategy of service firms: The moderating effects of complexity, uncertainty and munificence. Br. J. Manag. 2008, 19, 185–203. [Google Scholar] [CrossRef]

- Backman, C.A.; Verbeke, A.; Schulz, R.A. The drivers of corporate climate change strategies and public policy: A new resource-based view perspective. Bus. Soc. 2015. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Aragon-Correa, J.A.; Leyva-de la Hiz, D.I. The influence of technology differences on corporate environmental patents: A resource-based versus an institutional view of green innovations. Bus. Strategy Environ. 2016, 25, 421–434. [Google Scholar] [CrossRef]

- Hart, S.L.; Dowell, G. A natural-resource-based view of the firm: Fifteen years after. J. Manag. 2011, 37, 1464–1479. [Google Scholar]

- Alberta Environment and Sustainable Resource Development (AESRD). Technical Guidance for Completing Specified Gas Compliance Reports; AESRD, Government of Alberta: Edmonton, AB, Canada, 2014. Available online: http://aep.alberta.ca/climate-change/guidelines-legislation/specified-gas-emitters-regulation/documents/TechGuidanceCompletingSpecGasComplianceRpts-Feb2014.pdf (accessed on 1 September 2014).

- The World Bank. CO2 Emissions (Metric Tons per Capita). 2016. Available online: http://data.worldbank.org/indicator/EN.ATM.CO2E.PC/countries/1W-CA?display=graph (accessed on 16 March 2016).

- The Conference Board of Canada. How Canada Performs, Provincial and Territorial Ranking, Environment, Greenhouse Gas (GHG) Emissions. 2017. Available online: http://www.conferenceboard.ca/hcp/provincial/environment/ghg-emissions.aspx (accessed on 3 January 2017).

- Environment Canada. Canada’s Emissions Trends. 2014. Available online: http://ec.gc.ca/ges-ghg/E0533893-A985-4640-B3A2-008D8083D17D/ETR_E%202014.pdf (accessed on 21 January 2015). [Google Scholar]

- National Round Table on the Environment and the Economy (NRT). Reality Check: The State of Climate Progress in Canada; 2020 Climate Change Plans; NRT: Ottawa, ON, Canada, 2012. Available online: http://publications.gc.ca/collections/collection_2012/trnee-nrtee/En134-57-2012-eng.pdf (accessed on 5 September 2014).

- McCrank, N.; Ross, A.L. Temperature Check: Alberta Makes Big Move on Carbon Emissions, Financial Post. 2015. Available online: http://business.financialpost.com/fp-comment/temperature-check-alberta-makes-big-move-on-carbon-emissions (accessed on 7 September 2015).

- Leach, A.; Adams, A.; Cairns, S.; Coady, L.; Lambert, G. Climate Leadership Report to Minister. 2015. Available online: http://alberta.ca/documents/climate/climate-leadership-report-to-minister.pdf (accessed on 23 December 2015).

- Wheler, J.; Storey, B.J. 2013 Large Final Emitter Update. Air and Climate Change Policy Branch, Environment and Sustainable Resource Development. 2014. Available online: http://esrd.alberta.ca/focus/alberta-and-climate-change/regulating-greenhouse-gas-emissions/alberta-based-offset-credit-system/offset-credit-system-protocols/documents/FinalEmitterUpdate-Presentation-2013.pdf (accessed on 27 December 2015).

- Partington, P.J.; Demerse, C. Context for Climate Action in Canada; Pembina Institute: Drayton Valley, AB, Canada, 2013; Available online: http://www.pembina.org/reports/climate-context-20131009.pdf (accessed on 5 January 2015).

- Alberta Environment and Sustainable Resource Development (AESRD). Information Centre, 2011 Facility Table; AESRD, Government of Alberta: Edmonton, AB, Canada, 2012. Available online: http://environment.gov.ab.ca/info/posting.asp?assetid=8851&subcategoryid=53 (accessed on 1 September 2014).

- Furrer, O. Corporate Level Strategy: Theory and Applications; Routledge: New York, NY, USA, 2011. [Google Scholar]

- McDonough, W.; Braungart, M. Cradle to Cradle: Remaking the Way We Make Things; MacMillan: New York, NY, USA, 2010; p. 18. [Google Scholar]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Commitment to corporate social responsibility measured through global reporting initiative reporting: Factors affecting the behavior of companies. J. Clean. Prod. 2014, 81, 244–254. [Google Scholar] [CrossRef]

- Karius, O. Dow Jones Sustainability Indexes. In Corporate Governance of Sustainability: A Co-Evolutionary View on Resource Management; Bleischwitz, R., Ed.; Edward Elgar Publishing: Cheltenham, UK, 2007; pp. 209–227. [Google Scholar]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Sethi, S.P.; Schepers, D.H. United Nations Global Compact: The promise-performance gap. J. Bus. Ethnics 2014, 122, 193–208. [Google Scholar] [CrossRef]

- United States Environmental Protection Agency (EPA). Design Principles, United States Environmental Protection Agency (EPA), Climate Leaders Greenhouse Gas Inventory Protocol. 2005. Available online: http://www.epa.gov/climateleadership/documents/resources/design-principles.pdf (accessed on 6 April 2015). [Google Scholar]

- WRI/WBCSD. The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard; WRI (World Resources Institute)/WBCSD (World Business Council for Sustainable Development): Washington, DC, USA, 2004. Available online: http://www.ghgprotocol.org/files/ghgp/public/ghg-protocol-revised.pdf (accessed on 6 April 2015).

- Department for Environment, Food and Rural Affairs (DEFRA). Guidance on How to Measure and Report Your Greenhouse Gas Emissions; DEFRA: London, UK, 2009. Available online: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/69282/pb13309-ghg-guidance-0909011.pdf (accessed on 6 April 2015).

- Sawyer, D. Regulating Carbon Emissions in Canada: A Timbit with That Double-Double? Costs and Emissions Reductions of Renewed Carbon Policy in Alberta; Policy Brief; The International Institute for Sustainable Development: Winnipeg, MB, Canada, 2014; Available online: http://www.iisd.org/sites/default/files/publications/costs_emission_reductions_renewed_carbon_policy_alberta.pdf (accessed on 15 December 2014).

- European Union (EU). The EU Emissions Trading System (EU ETS). 2013. Available online: http://ec.europa.eu/clima/publications/docs/factsheet_ets_en.pdf (accessed on 6 April 2015).

- Stern, N. Stern Review: The Economics of Climate Change. 2006. Available online: http://mudancasclimaticas.cptec.inpe.br/~rmclima/pdfs/destaques/sternreview_report_complete.pdf (accessed on 29 March 2015).

- McGariggle, P. Cogeneration and Carbon Management: Key Issues in the Design of Carbon Management Policies and Regulations in Alberta. 2014. Available online: http://cmcghg.com/wp-content/uploads/2014/01/Cogeneration-Carbon-Presentation_FINAL-copy.pdf (accessed on 20 January 2015).

- Huot, M.; Fischer, L.; Lemphers, N. Oil Sands and Climate Change: How Canada’s Oil Sands Are Standing in the Way of Effective Climate Action; Pembina Institute: Drayton Valley, AB, Canada, 2011; Available online: http://www.pembina.org/reports/us-oilsands-and-climate-briefing-note-201109b.pdf (accessed on 23 November 2014).

- Alberta Environment. Technical Guidance for Offset Projects Developers; Specified Gas Emitters Regulation; Government of Alberta: Edmonton, AB, Canada, 2011. Available online: http://environment.gov.ab.ca/info/library/7915.pdf (accessed on 29 January 2015).

- Bramley, M.; Huot, M.; Dyer, S.; Horne, M. Responsible Action? An Assessment of Alberta’s Greenhouse Gas Policies; Pembina Institute: Drayton Valley, AB, Canada, 2011; Available online: http://www.pembina.org/reports/responsible-action.pdf (accessed on 1 February 2015).

- Partington, P.J.; Horne, M.; Demerse, C. Getting on Track for 2020: Recommendations for Greenhouse Gas Regulations in Canada’s Oil and Gas Sector; Pembina Institute: Drayton Valley, AB, Canada, 2013; Available online: http://www.pembina.org/reports/getting-on-track-to-2020.pdf (accessed on 31 January 2015).

- Demersey, C.; Bramley, M. Choosing Greenhouse Gas Emission Reductions Policies in Canada; Pembina Institute: Drayton Valley, AB, Canada, 2008; Available online: http://www.pembina.org/reports/pembina-td-final.pdf (accessed on 5 January 2015).

- Leach, A. Policy Forum: Alberta’s Specified Gas Emitters Regulation. Can. Tax J. 2012, 60, 881–898. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Tonnes of CO2e per Thousand Dollars Revenue | <2.1 (Good Standing) | >2.1 (Weak Performance) |

|---|---|---|

| Number of corporations | 12 | 4 |

| Tonnes of CO2e Emitted Per-Employee | <3026 (Good Standing) | >3026 (Weak Performance) |

|---|---|---|

| Number of corporations | 13 | 3 |

| Compliance Mechanisms | Percentage of Facilities Complying (Number of Facilities) |

|---|---|

| Achieving and exceeding the 12% reduction through internal improvements or recognition of cogeneration (and generating EPCs) | 30% (6) |

| EPCs Submitted | 10% (2) |

| Offset Credits Submitted | 35% (7) |

| Funds Credits Purchased ($15/Tonne) | 5% (1) |

| EPCs submitted + Offset Credits Submitted | 5% (1) |

| Funds Credits Purchased + Offset Credits Submitted | 5% (1) |

| Fund Credits + Offset Credits + EPCs submitted | 10% (2) |

| Compliance Mechanisms | Percentage of Facilities Complying (Number of Facilities) |

|---|---|

| Achieving and exceeding the 12% reduction through internal improvements or recognition of cogeneration (and generating EPCs) | 28% (5) |

| Offset Credits Submitted | 6% (1) |

| Funds Credits Purchased ($15/Tonne) | 22% (4) |

| EPCs submitted + Offset Credits Submitted | 17% (3) |

| Funds Credits Purchased + Offset Credits Submitted | 11% (2) |

| Fund Credits + Offset Credits + EPCs submitted | 17% (3) |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hannouf, M.; Assefa, G. The Role of Sustainability Resources of Large Greenhouse Gas Emitters: The Case of Corporations in Alberta, Canada. Sustainability 2017, 9, 182. https://doi.org/10.3390/su9020182

Hannouf M, Assefa G. The Role of Sustainability Resources of Large Greenhouse Gas Emitters: The Case of Corporations in Alberta, Canada. Sustainability. 2017; 9(2):182. https://doi.org/10.3390/su9020182

Chicago/Turabian StyleHannouf, Marwa, and Getachew Assefa. 2017. "The Role of Sustainability Resources of Large Greenhouse Gas Emitters: The Case of Corporations in Alberta, Canada" Sustainability 9, no. 2: 182. https://doi.org/10.3390/su9020182

APA StyleHannouf, M., & Assefa, G. (2017). The Role of Sustainability Resources of Large Greenhouse Gas Emitters: The Case of Corporations in Alberta, Canada. Sustainability, 9(2), 182. https://doi.org/10.3390/su9020182