Financial Applications on Fractional Lévy Stochastic Processes

Abstract

:1. Introduction and Notations

An Example of a Lévy Process: Lévy Stable Processes (LSP)

2. The Stochastic Model and Deterministic Representation

3. Numerical Discretization of the Fractional PDE

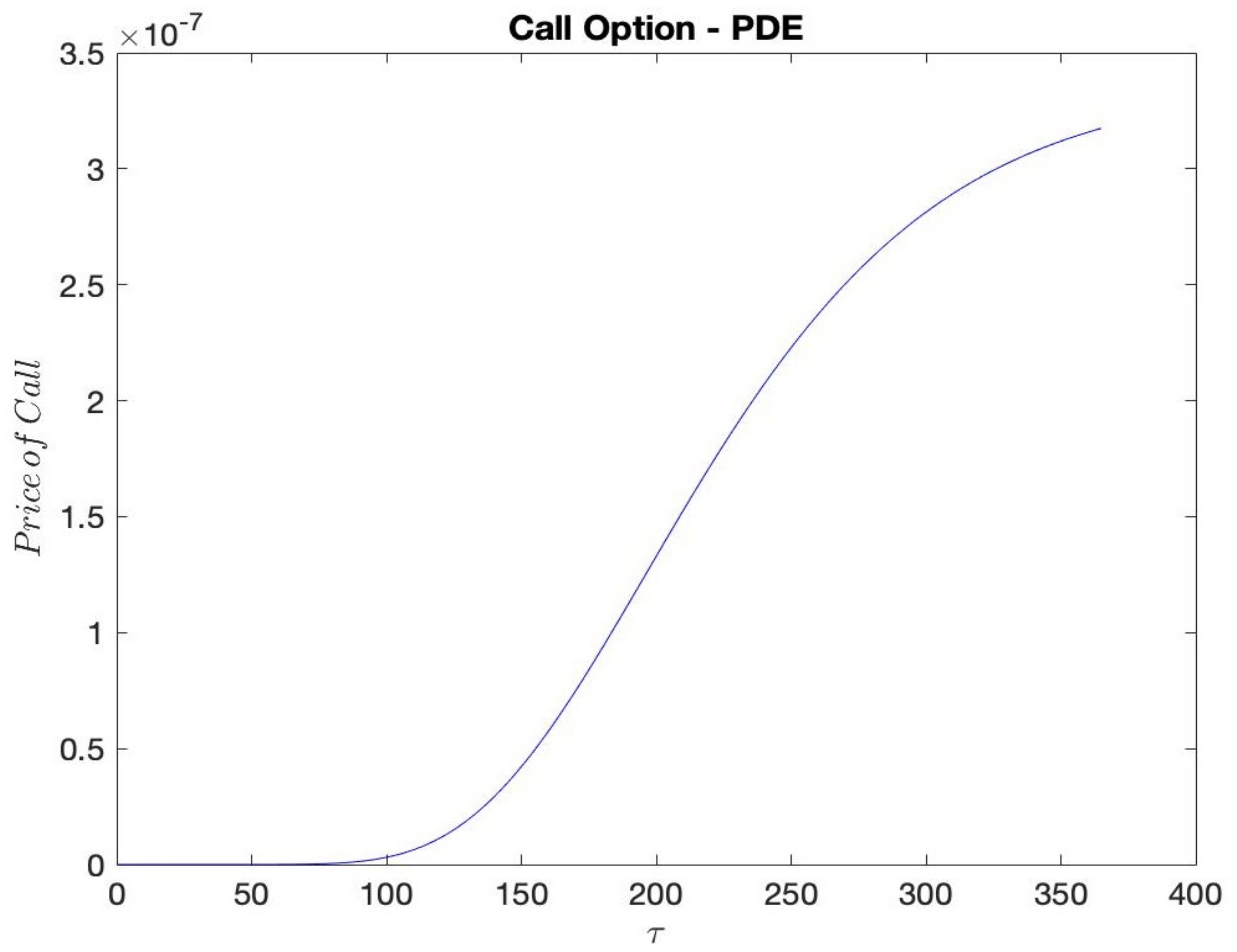

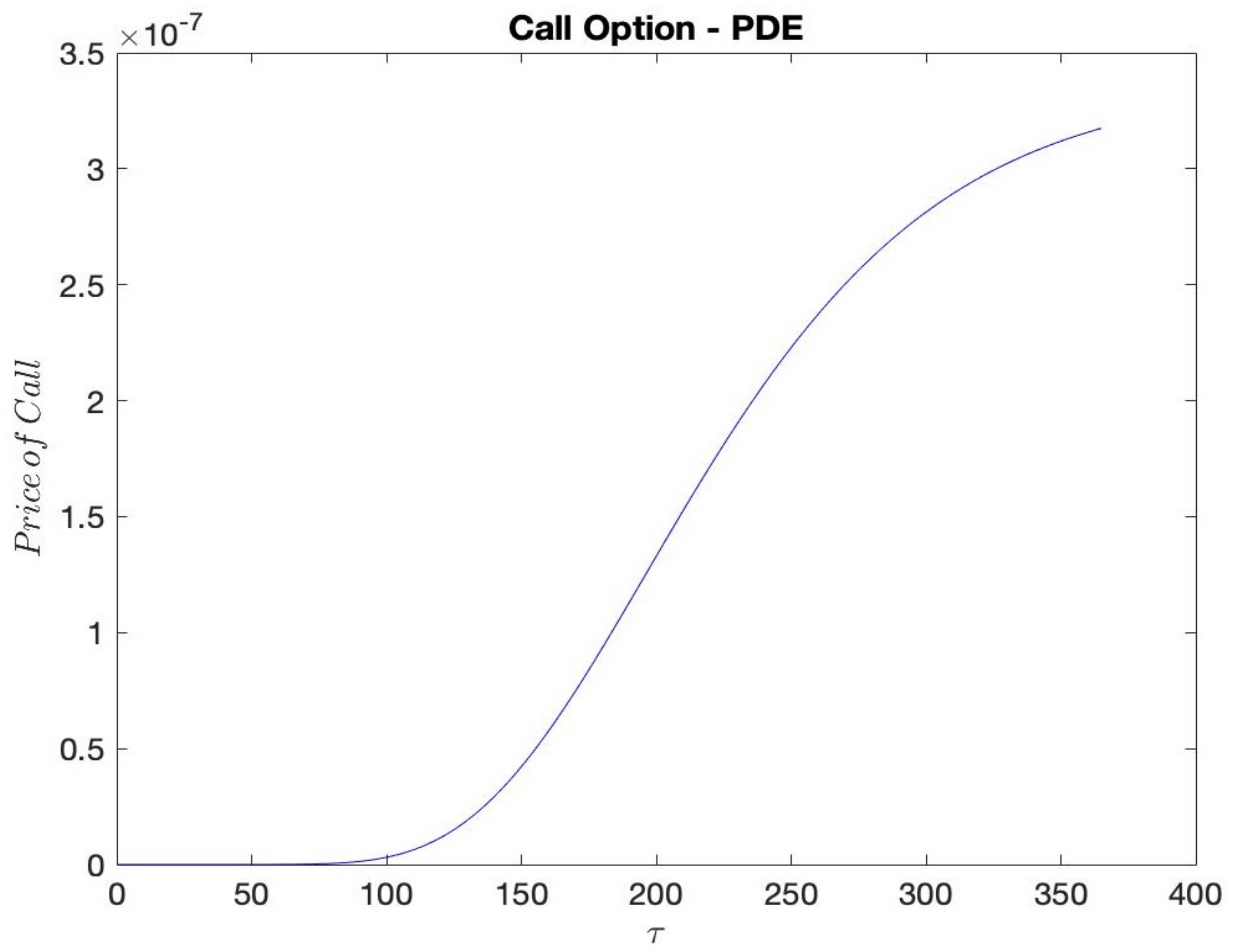

- For a call option, the payoff is defined by . Since we must truncate the spatial domain in order to make it workable from a numerical point of view, we will use the following boundary conditions and where and .

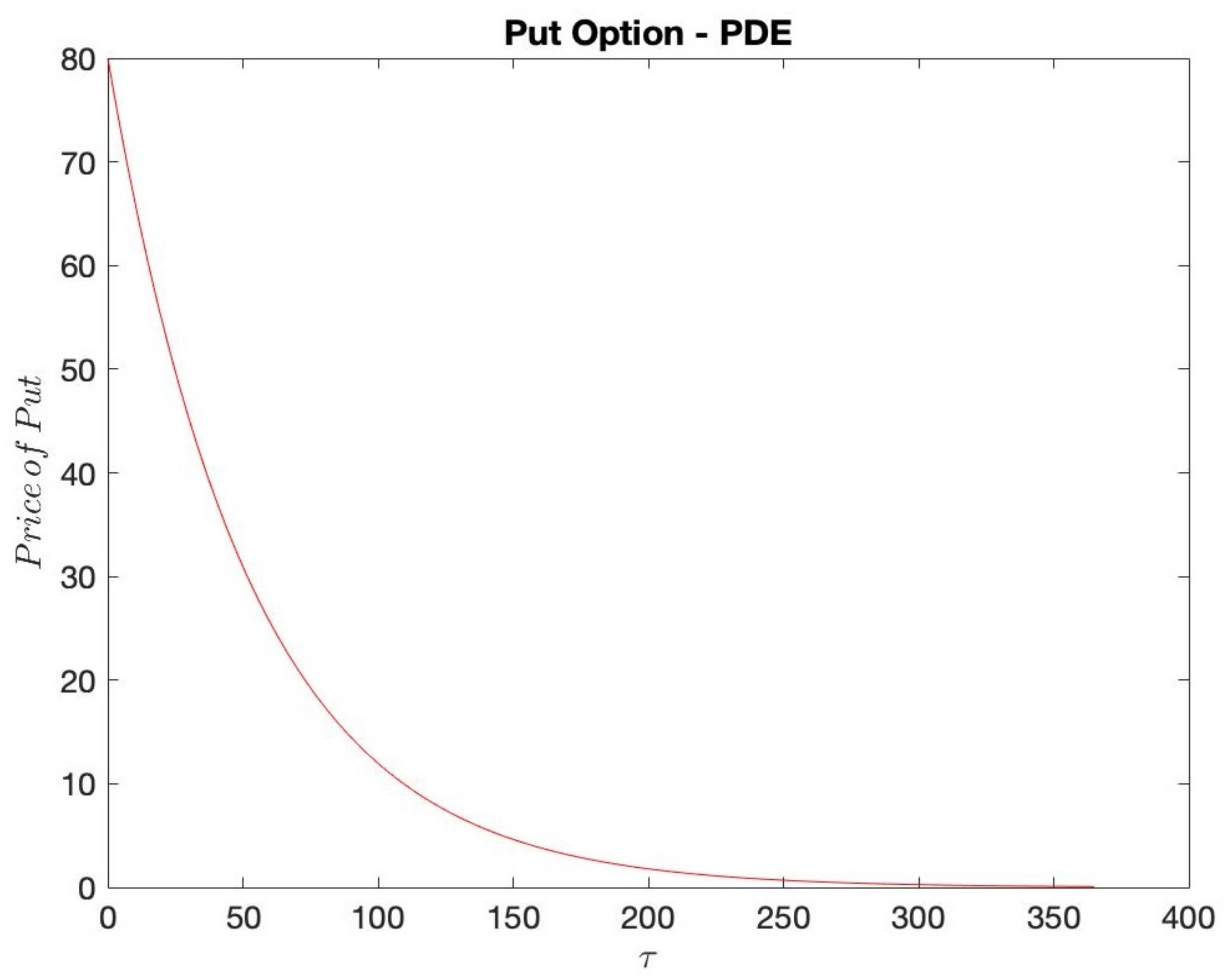

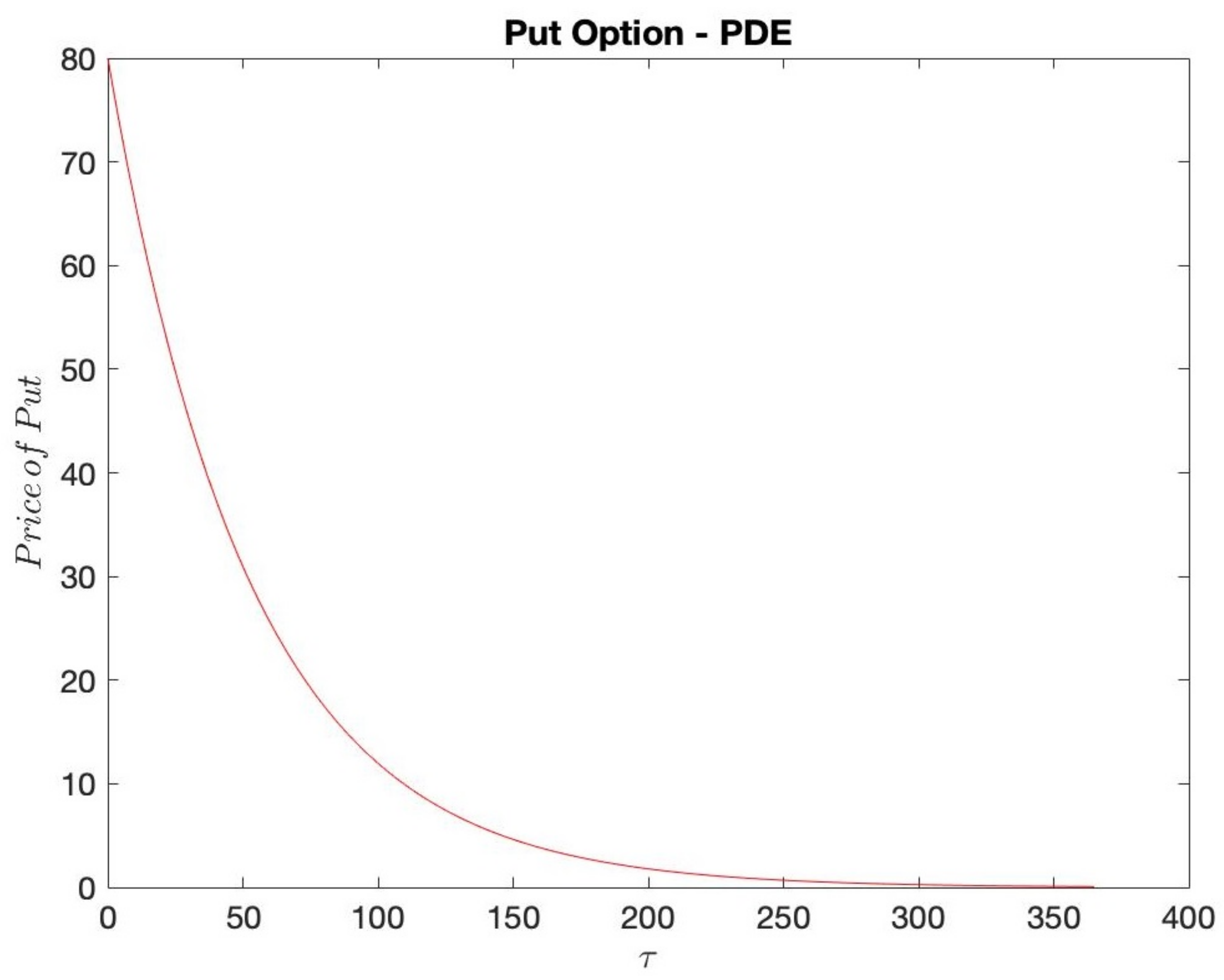

- For a put option, the payoff is defined by and we will use the following conditions and where and .

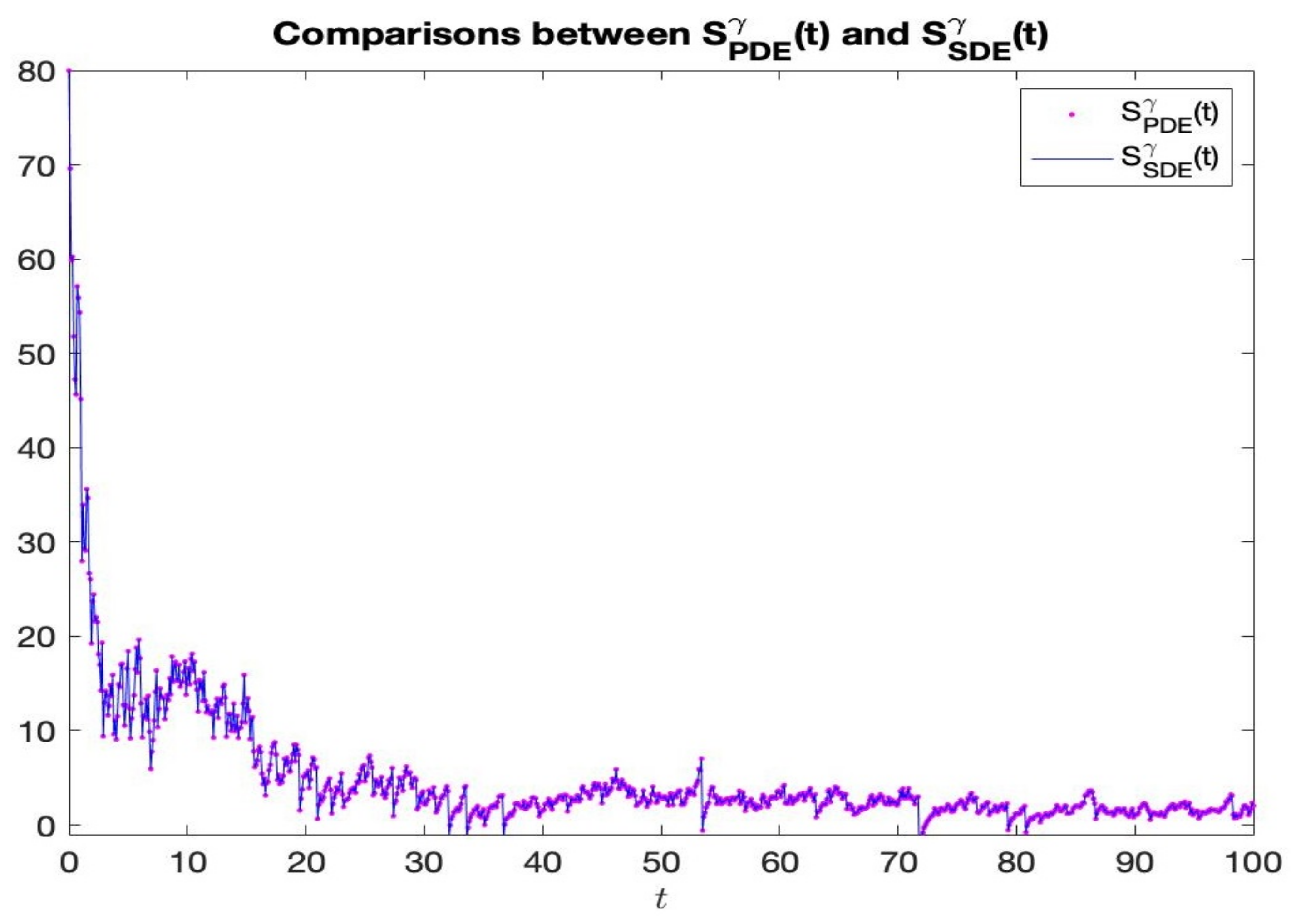

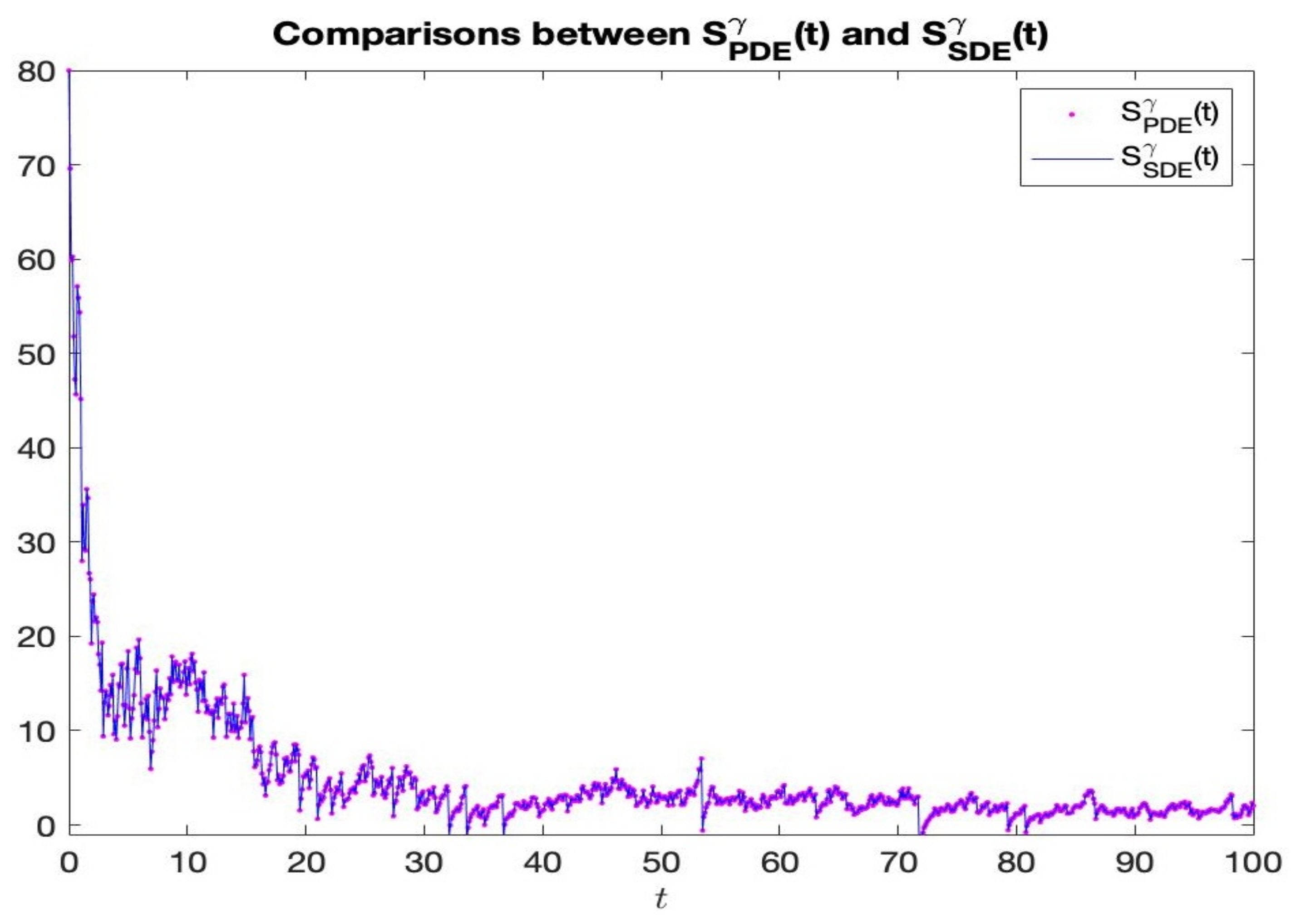

4. Numerical Simulations and Discussions

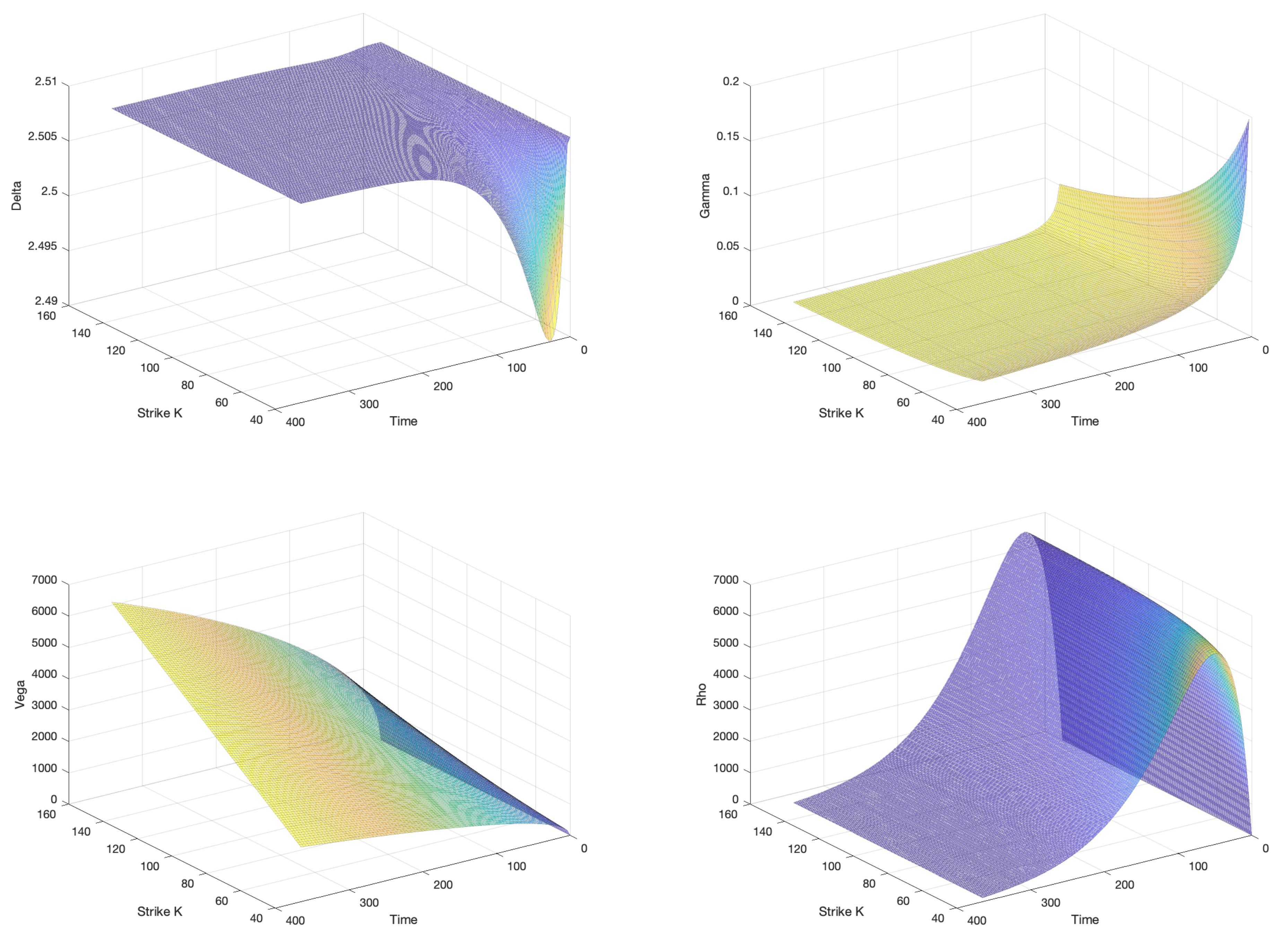

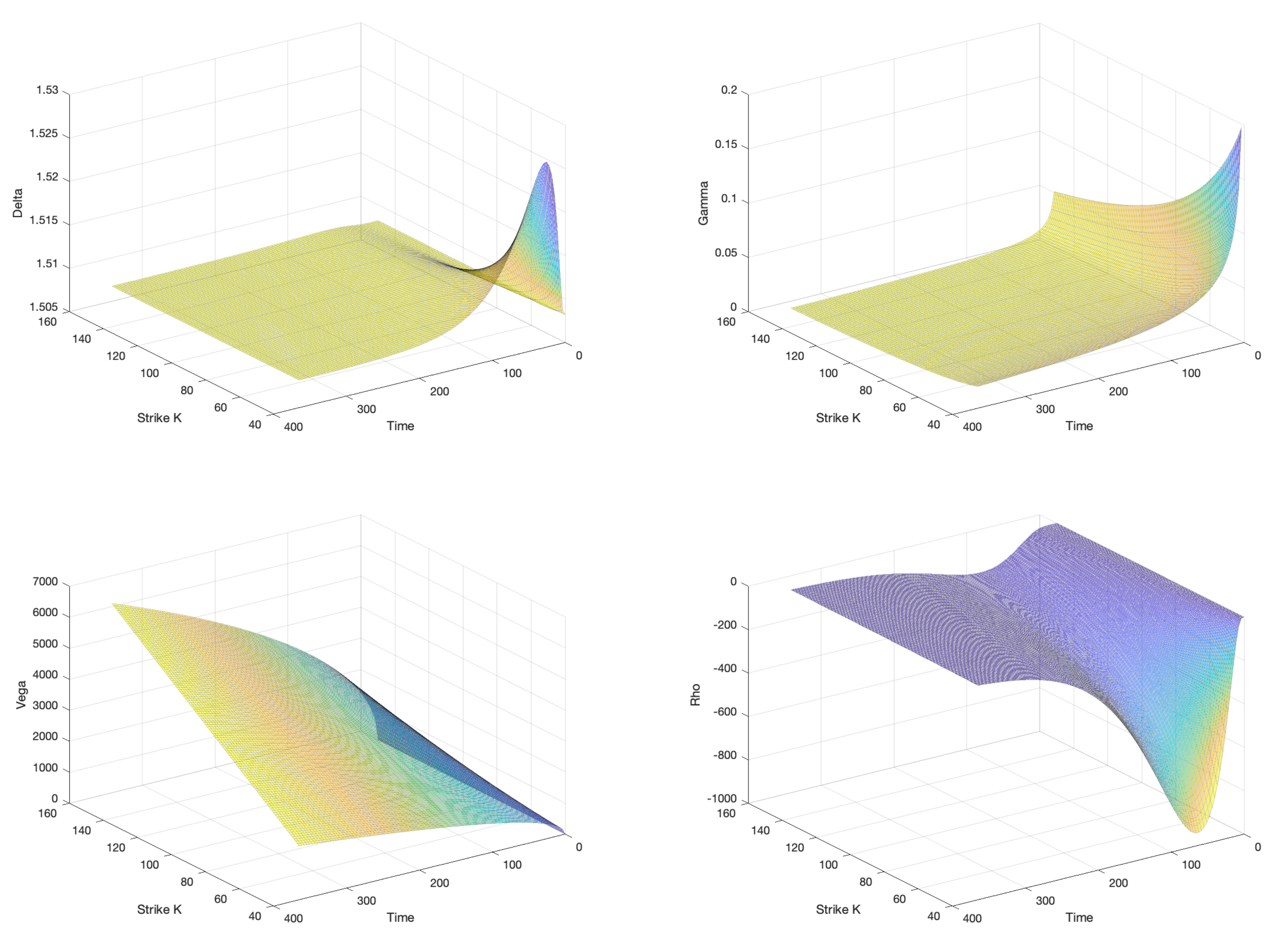

Approximation of Lévy Model Greeks

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Raible, S. Lévy Processes in Finance: Theory, Numerics, and Empirical Facts. Ph.D. Thesis, University of Freiburg, Freiburg im Breisgau, Germany, 2000. [Google Scholar]

- Schoutens, W. Lévy Processes in Finance, 1st ed.; Wiley Series in Probability and Statistics; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Eberlein, E. Fourier—Based Valuation Methods in Mathematical Finance. In Quantitative Energy Finance; Benth, F.E., Kholodnyi, V.A., Laurence, P., Eds.; Springer: Berlin/Heidelberg, Germany, 2014; pp. 85–114. [Google Scholar]

- Cartea, A.; del-Castillo-Negrete, D. Fractional Diffusion Models of Option Prices in Markets with Jumps; Elsevier: Amsterdam, The Netherlands, 2006. [Google Scholar]

- Abouagwa, M.; Li, J. Stochastic fractional differential Equations driven by Lévy noise under Carathéodory conditions. J. Math. Phys. 2019, 60, 022701. [Google Scholar] [CrossRef]

- Wu, P.; Yang, Z.; Wang, H.; Song, R. Time fractional stochastic differential equations driven by pure jump Lévy noise. J. Math. Anal. Appl. 2021, 504, 125–412. [Google Scholar] [CrossRef]

- Cont, R.; Voltchkova, E. Finite difference methods for option pricing in jump diffusion and exponential Lévy models. SIAM J. Numer. Anal. 2005, 43, 1596–1626. [Google Scholar] [CrossRef]

- Shokrollahi, F.; Kılıçman, A.; Ibrahim, N.A. Greeks and Partial Differential Equations for some Pricing Currency Option Models. Malays. J. Math. Sci. 2015, 9, 417–442. [Google Scholar]

- Chen, W.; Xu, X.; Zhu, S.P. Analytical pricing European-style option under the modified Black-Scholes equation with a partial-fractional derivative. Quartely Appl. Math. 2014, 72, 597–611. [Google Scholar] [CrossRef]

- Aljedhi, R.A.; Kılıçman, A. Fractional Partial Differential Equations Associated with Lévy Stable Process. Mathematics 2020, 8, 508. [Google Scholar] [CrossRef] [Green Version]

- Demirci, E.; Ozalp, N. A method for solving differential equations of fractional order. J. Comput. Appl. Math. 2012, 236, 2754–2762. [Google Scholar] [CrossRef] [Green Version]

- Shen, S.; Liu, F.; Chen, J.; Turner, I.; Anh, V. Numerical techniques for the variable order time fractional diffusion equation. Appl. Math. Comput. 2012, 218, 10861–10870. [Google Scholar] [CrossRef] [Green Version]

- Jumarie, G. Derivation and solutions of some farctional Black-Scholes equations in space and time. J. Comput. Math. Appl. 2010, 59, 1142–1164. [Google Scholar] [CrossRef] [Green Version]

- Yuste, S.B. Weighted average finite difference methods for fractional diffusion equations. J. Comput. Phys. 2006, 216, 264–274. [Google Scholar] [CrossRef] [Green Version]

- Lubich, C. Discretized Fractional Calculus. SIAM J. Math. Anal. 1986, 17, 704–719. [Google Scholar] [CrossRef]

- De Olivera, F.; Mordecki, E. Computing Greeks for Lévy Models: The Fourier Transform Approach. arXiv 2014, arXiv:1407.1343. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Strike K | r | q | m | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 100 | 80 | 1 | 10 |

| Strike K | Call Price with SDE | Call Price with FPDE | |

|---|---|---|---|

| 80 | |||

| 100 | |||

| 110 |

| Strike K | Put Price with SDE | Put Price with FPDE | |

|---|---|---|---|

| 80 | |||

| 100 | |||

| 110 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aljethi, R.A.; Kılıçman, A. Financial Applications on Fractional Lévy Stochastic Processes. Fractal Fract. 2022, 6, 278. https://doi.org/10.3390/fractalfract6050278

Aljethi RA, Kılıçman A. Financial Applications on Fractional Lévy Stochastic Processes. Fractal and Fractional. 2022; 6(5):278. https://doi.org/10.3390/fractalfract6050278

Chicago/Turabian StyleAljethi, Reem Abdullah, and Adem Kılıçman. 2022. "Financial Applications on Fractional Lévy Stochastic Processes" Fractal and Fractional 6, no. 5: 278. https://doi.org/10.3390/fractalfract6050278

APA StyleAljethi, R. A., & Kılıçman, A. (2022). Financial Applications on Fractional Lévy Stochastic Processes. Fractal and Fractional, 6(5), 278. https://doi.org/10.3390/fractalfract6050278