1. Introduction

Developing countries are highly dependent on export earnings to satisfy their import requirements and for the development of their economy [

1,

2]. Consequently, instability of such proceeds will significantly influence output by constraining input and production planning. Furthermore, fluctuations in quantity and price of exports could create a serious problem in balance-of-payments, national income, investment, as well as the overall growth of less developed countries [

2]. Susceptibility to this problem is high in SSA (Sub-Saharan African) countries as their international trades are mainly based on exporting primary agricultural commodities, whey they possess comparative advantages due to cheap labor [

3].

Similarly, in Ethiopia, the export structure is highly concentrated to a few traditional agricultural commodities, such as coffee, hides, skins, oilseeds, and pulses. Over a long period of time, coffee was the dominant export earning commodity, followed by non-coffee commodities such as hides, skins, oilseeds, pulses, and chat. Over two-thirds of the export earnings were obtained from the export of these few commodities [

4]. However, since the mid-1990s, the relative importance of these commodities, particularly coffee, in total export revenue has declined drastically. Coffee’s contribution to export earnings declined to 45% in 2003, from a high of 70% in the mid-1990s, due to the high volatility of coffee prices. This would have a detrimental effect on the economic planning and economic development of the country. From this, it can be understood that export earnings instability was one of the chronic economic problems facing Ethiopia. Since the 1970s, many other Less Developed Countries (LDC) have also experienced strong volatility and declines in the international prices of their primary commodities exports [

5]. Therefore, high dependence on a few agricultural export commodities added with the high volatility of prices left the countries’ export earnings extremely vulnerable.

In countries like Ethiopia, that mainly depend on primary agricultural commodities for their export earnings, vertical diversification through establishing agricultural processing industries which produce value-added quality export products is difficult. However, diversification horizontally into the export of non-traditional high-value agricultural commodities was one of the possible ways to reduce over-reliance on a few low-value traditional products and tackle the problem of export income instability.

Consequently, due to the declining export earnings from traditional exports, horticulture and other non-traditional, high-value, agricultural export expansions represent an important area of potential income growth [

5]. In this regard, Ethiopia was considered to have the potential to achieve trade gains in these sub-sectors [

6]. This is because Ethiopia has diverse agro-ecological zones that can easily fit the production of different agricultural export commodities, with minimum adjustment to the existing production systems [

1,

7]. As a result, promoting the production and export of horticultural products (fruits, vegetables, and flowers) has caught the attention of the federal government of Ethiopia. These high-value and labor-intensive cash crops can contribute to the fast and successful diversification of the export base towards non-traditional agricultural commodities to attain export earnings stability.

Production of horticultural products is a new sector in Ethiopia, as the production of these crops has been undertaken for decades. The sector comprises of large state farms supplying fruits and vegetables to the local market and for export [

8]. Fruit and vegetable crops with a significant potential for domestic consumption, export markets, and industrial processing are produced in the country [

6]. In this regard, the Ethiopian government, sector organizations, and donors have played a great role to identify potential for the further development of the fruits and vegetable sector in Ethiopia, both for the domestic and export market [

8].

The export destination of Ethiopia’s fruits and vegetables are mostly neighboring countries like Djibouti, Sudan, and Somalia. High-value fresh vegetables were exported to the United Kingdom, the United Arab Emirates, and the Netherlands, which may create an opportunity for the improvement of the fruit and vegetable sectors in the country [

6]. According to statistics in Reference [

9], in 2004/2005, export income generated from the subsector was 28.55 million USD. In 2015/16, the sector provided employment opportunities for approximately 183,000 persons and generated earnings of about 274.62 million USD, making the sector the fifth largest foreign revenue generator for the country.

Given Ethiopia’s endowment of natural resources and other competitive advantages, the export performance was still low despite the existence of blooming prospects for the development of the sub-sector. Consequently, although export diversification through horticultural produce was advocated as an alternative export promotion strategy, the performance of this sector has been generally unsatisfactory. In this regard, knowledge of the determinants of industry’s development has paramount importance. However, so far different empirical works [

2,

3,

10,

11,

12,

13,

14,

15] have mostly emphasized the export performance of traditional export commodities, with less consideration on examining the factors affecting the export performance of the horticulture sub-sector. Some others had tried to describe [

4,

16] and analyze the production and marketing aspects [

1] of the sector in a limited part of the country. Effective policy intervention to promote the performance of this potential and promising sub-sector needs knowledge of the determinants of the industry’s development. Consequently, the objective of this study was to assess factors affecting the export performance of the Ethiopian horticulture sub-sector, which in turn will enable the sector to be competitive in the global horticulture market and stabilize export earnings of the country.

3. Literature Review

Analyzing the export performance of the horticultural sub-sector, with a special focus on the determinants of horticultural exports, had attracted the attention of both policymakers and researchers in different parts of the world, particularly in developing countries. This is because the export of horticultural products provides a good opportunity to diversify the export base of many developing countries, which are mainly dependent on exports of tea, coffee, and cocoa [

18]. This, in turn, will reduce dependence on a narrow range of primary products by developing countries.

The prospects for export diversification in Ethiopia were assessed empirically to investigate the main determinants of the country’s exports (dominated by traditional commodities). Using the Error Correction Model (ECM), the estimation of the export determination model revealed that the real exchange rate was the significant determinant of the country’s exports in the long-run [

1]. The findings of this study were inconsistent with the results of Reference [

11]. However, the work of many researchers in different part of the world had confirmed that the real exchange rate was among the most important determinants of export performance [

3,

18,

19,

20,

21,

22,

23,

24]. In addition, the study by Reference [

10] had also stressed the existence of promising opportunities for export diversification in the country. References [

3] and [

11] had also stressed the need and importance for diversifying the export base of the country and breaking away from the export of traditional agricultural commodities.

The study by Reference [

2] analyzed Ethiopia’s export earnings instability by employing country-specific models, taking advantage of a sufficiently large sample period from 1962 to 2008. The study tried to identify the contributions of major traditional agricultural export commodities, such as coffee, hides, skins, oilseeds, and pulses. Attempts have also been made to make comparisons between the sub-periods of the Imperial, Derg, and Post-Derg periods, since these sub-periods experienced distinct trade and foreign policies. The study finds that the Post-Derg period was characterized by a higher level of instability and diversification of exports. This calls for the reconsideration of the direction of the diversification policy towards commodities that are negatively correlated with the traditional export commodities of the country.

The study by Reference [

11] examined the performance and trend of merchandise (and manufacturing) exports, and its determinants during the period from 1981–2008 in Ethiopia. The findings of the study indicated that merchandise export volumes were significantly influenced by gross capital formation (proxy for production capacity) and share of trade in GDP (proxy for trade liberalization). In addition, manufacturing exports supply was found to be negatively and significantly affected by foreign income and positively affected by gross capital formation. The impact of foreign income was also revealed as negative in References [

21,

25]. However, many empirical works had obtained a positive impact of trading partners’ income on the export performance of the exporting country [

20,

26,

27].

Using cross-sectional data, Reference [

16] also described the export performance of fruit and vegetable exporters and found that the sector was in its infancy and there was much to be done to increase gains from the sector. Ethiopian fruit and vegetable exporters were challenged by the lack of managerial and technical skills, and lack of commitment by employees, respectively. Externally, fruit and vegetable exporters were hindered by lack of credit facilities, supply of inputs, followed by lack of infrastructure. Finally, it was recommended that policymakers should design different schemes to enhance export performance, especially of fruits and vegetables. However, for the effectiveness of policy measures, an empirical work on the factors affecting the export performance of sub-sectors is still missing.

In the empirical work, Reference [

18] analyzed the export performance of the horticultural sub-sector in Kenya. The findings of the study indicated that agricultural GDP and real interest rates were the important factors that influenced horticultural exports from Kenya. Agricultural GDP had a positive influence on Kenyan horticultural exports, whilst real interest rates had a negative influence on horticultural exports. The implication of the findings were that since real interest rates had a negative relationship with horticultural exports, an increase in real interest rates would lead to a decrease in Kenya’s horticultural exports by increasing the cost of borrowing. In addition, it was emphasized that the significance of the cost of borrowing in influencing horticultural exports can be attributed to the fact that the horticultural sub-sector is relatively more capital intensive, compared to other agricultural sub-sectors. A significant amount of capital is required to set up greenhouses, cooling facilities, pack houses, irrigation systems, as well as the purchase of fertilizers, agrochemicals, and other inputs. The result was consistent with the findings of Reference [

28], wherein real interest rates were found to have a significant impact on the volume of cotton exports.

Using the cointegration test, Reference [

28] examined factors that affected tobacco and cotton exports in Zambia. The results of the study revealed that the factors that affected the growth of exports were crop specific. For instance, foreign direct investment had a significant impact on the volume of tobacco exports, both in the short-run and long-run, though tobacco exports were more responsive to movements in this factor in the long-run, than in the short-run. Consequently, policy measures like scaling up incentives in the form of tax holidays, should be taken to attract foreign direct investment. This result was consistent with References [

21,

25]. Furthermore, Reference [

29] stated that the impact of foreign direct investment (FDI) depends on its motive, whereby export-oriented FDI will promote the export performance of the exported commodities. In addition, the uni-directional Granger causality of agricultural exports to the share of agricultural gross domestic product for both tobacco and cotton in Zambia, implied that the two sectors should be prioritized in terms of increased budgetary allocations, which will raise agricultural GDP and drive the economy towards export diversification [

28].

4. Econometric Method

4.1. Description of Data

The study used time series data from References [

9,

17,

30]. Data on real exchange rates, foreign direct investment, real GDP of Ethiopia, real GDP of trading partners, price, and real interest rates were obtained from References [

27], whilst data on horticultural exports was obtained from References [

9,

17]. These data were analyzed using Eviews Version 9.0 (IHS Global Inc., Englewood, CO, USA).

4.2. Cointegration Test

Cointegration is a powerful way of detecting the presence of long-run relationships or steady-state equilibrium between variables [

31]. Different cointegration techniques were developed to determine the long-run relationships between the time series [

32,

33,

34]. In all these cointegration techniques, the most important restriction is that all the series must be of the same ordered integrations. However, a recently developed cointegration approach, namely the autoregressive-distributed lag (ARDL), also known as the bounds test, eliminates this restriction [

35]. The ARDL approach allows the regressors to be stationary in levels (I (0)) or the first-differenced (I (1)). Owing to this convenience, the ARDL method has been used in many empirical works, and it was also used to obtain the long-run relationship among the series in this study. The long-run ARDL equation was specified as follows:

where exp: represents horticultural exports, FDI: foreign direct investment, ER: real effective exchange rate, RGDP: real GDP of Ethiopia, FGDP: foreign GDP, Price: world average price of fresh fruits and vegetables, DU

t: Dummy variable representing the Structural break (

Tb (break year) = 2005 in this case), and RIR: real interest rate.

The F-test was employed to test co-integration among the variables, where the null hypothesis that the betas were jointly equal to zero (i.e.,

) was tested. Reference [

32] provided critical

F-values; one for the lower bound and the other for the upper bound, for testing whether there was co-integration. If the computed

F-value was less than the

F-value for the lower bound, then the null hypothesis cannot be rejected. If the computed

F-value exceeded the

F-value for the upper bound, then the null hypothesis of no co-integration was rejected, otherwise the test was inconclusive.

To select the lag values

m,

n,

o,

p,

q, and

r in Equation (1), model selection criteria, such as AIC, SIC, Hannan-Quinn information criteria, Adjusted R-squared were used. The short-run dynamics of the variables was described by employing the Error Correction Model (ECM) [

24]. The ECM representation was specified as follows:

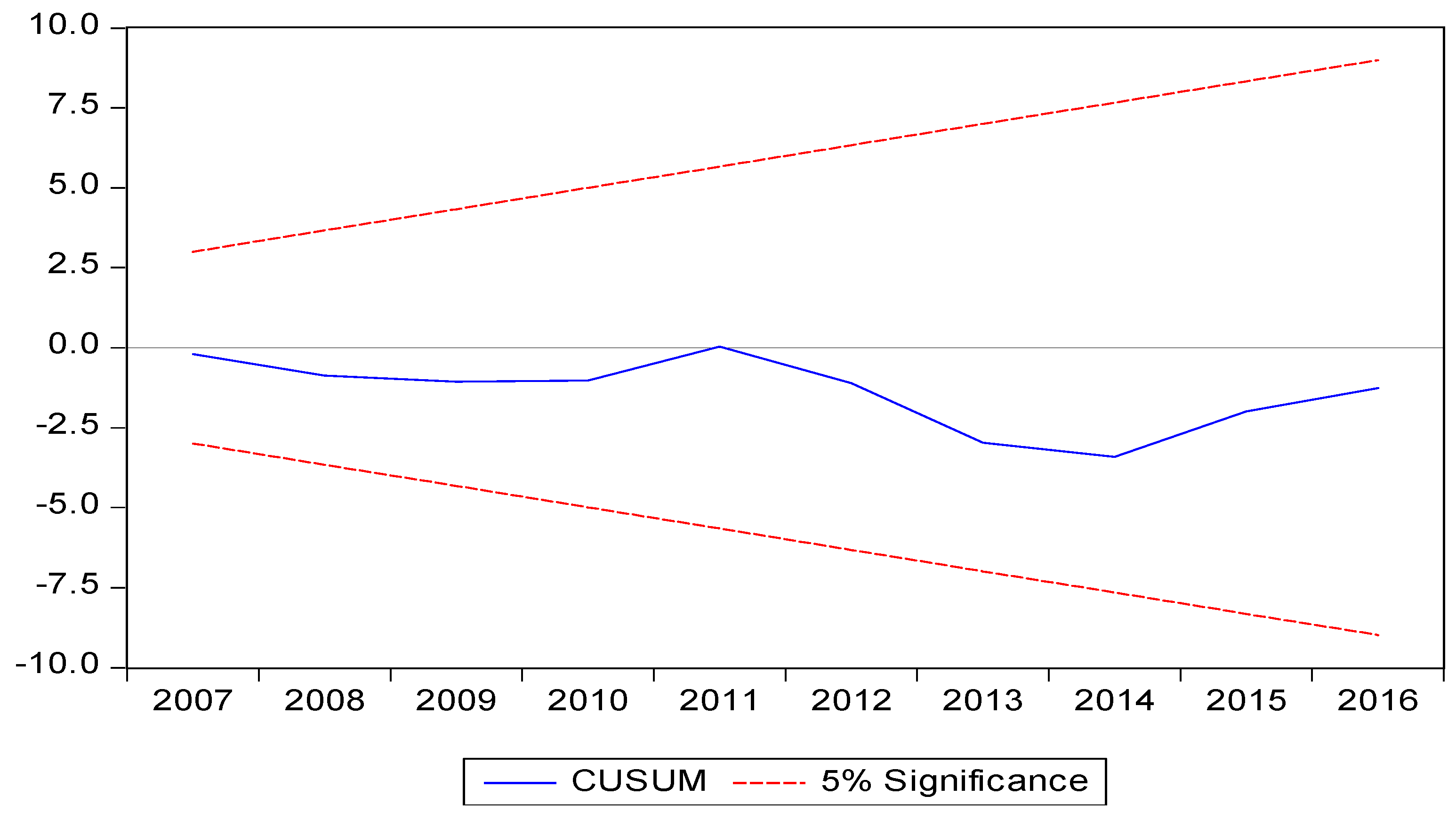

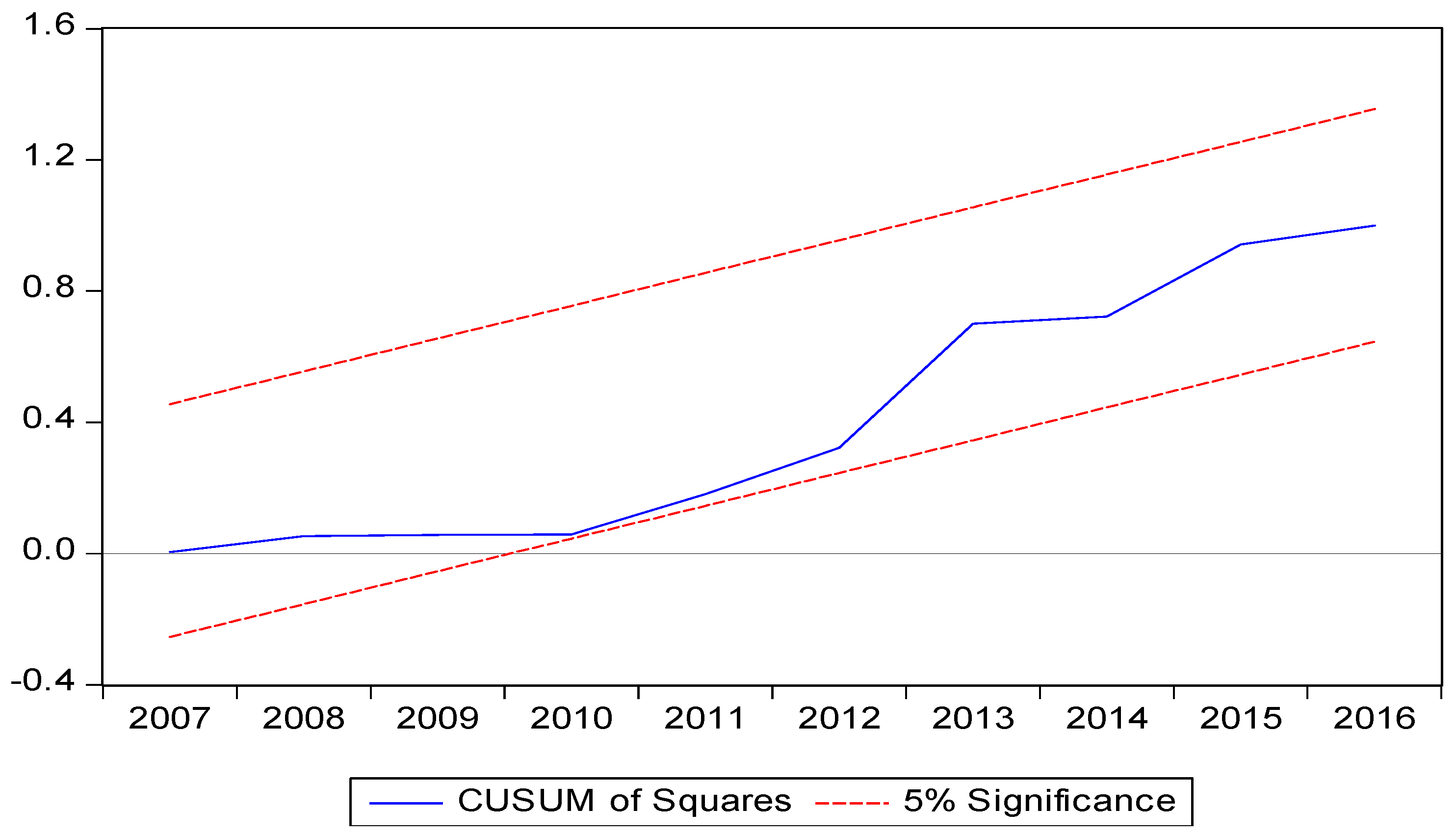

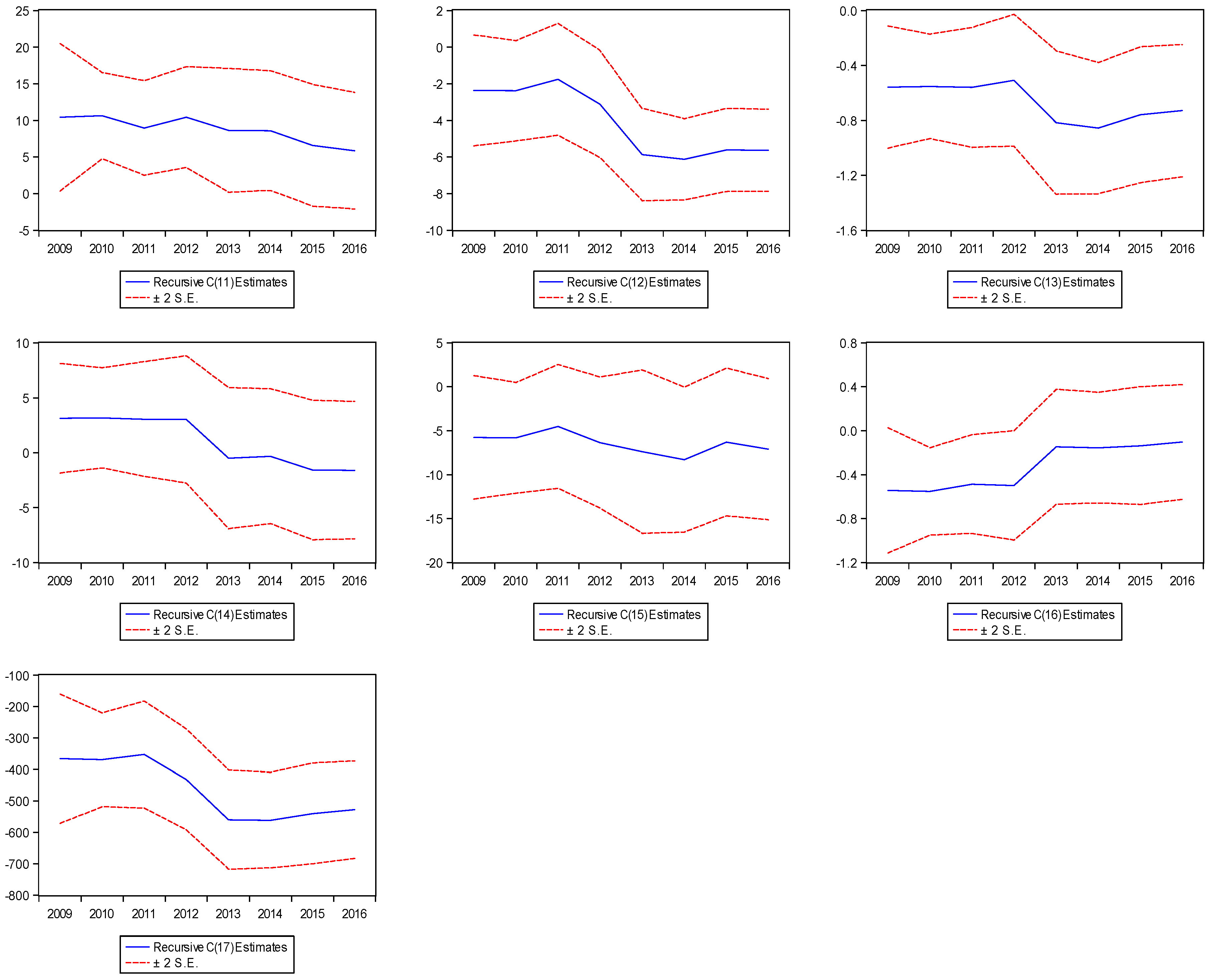

The coefficient of the ECMt−1, λ in Equation (2) shows the speed of adjustment of a parameter, indicating how quickly the series can come back to its long-run equilibrium. The sign of the coefficient must be negative and significant. Diagnostic tests which include serial correlation and heteroscedasticity tests were conducted to ensure the acceptability of the model. In addition, cumulative sum (CUSUM), the cumulative sum of squares (CUSUMQ), and recursive coefficient estimates were also applied to the series to assess stability of the coefficients and this was illustrated using graphics.

4.3. Independent Variables Included in the Model and their Expected Signs

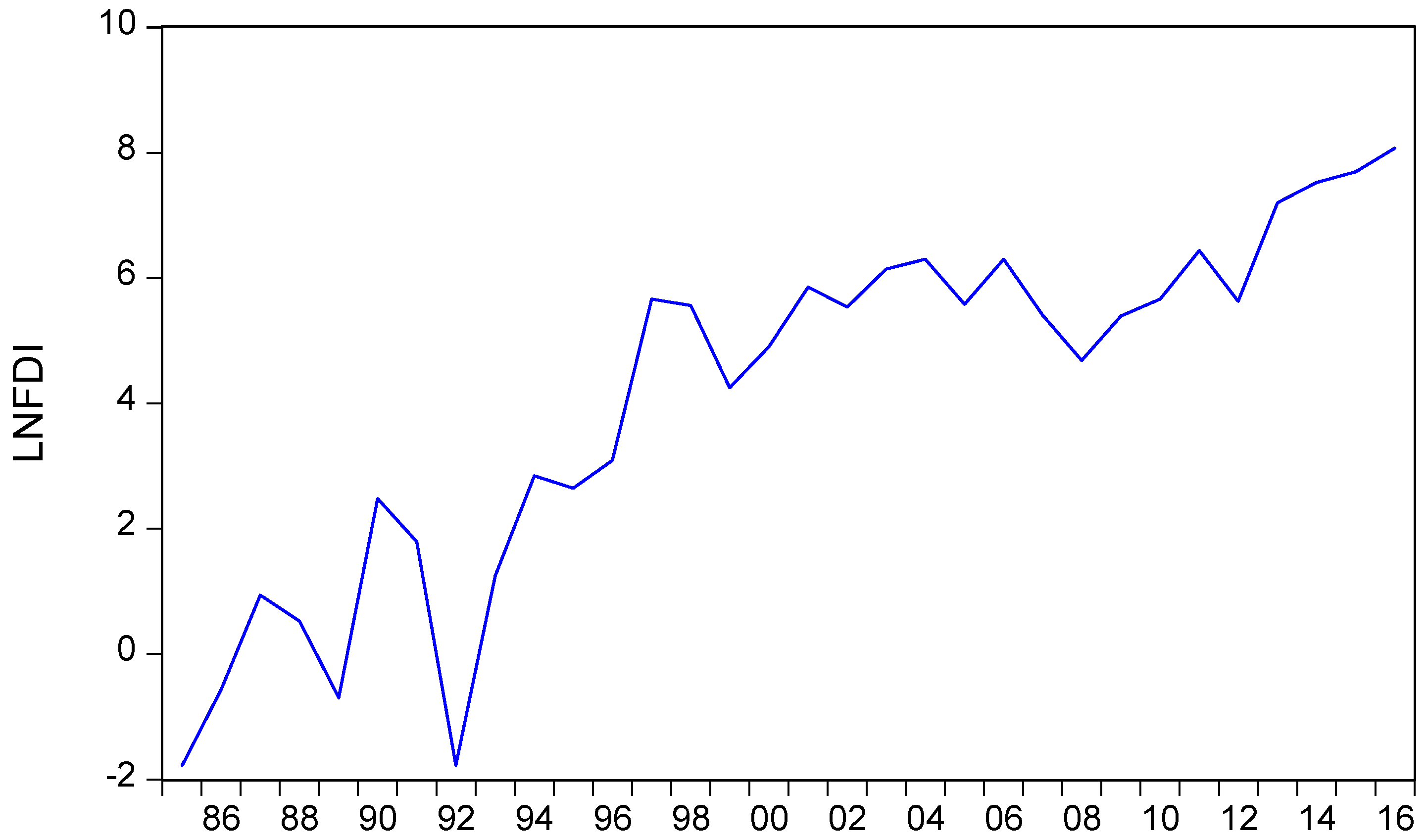

Foreign direct investment (FDI): It was defined as new investment made by foreign investors in horticultural sub-sectors. The results of the reviewed literature show varied results with regards to the impact of FDI on export performance. However, in Ethiopia, the government have given due attention to attract foreign investors into this potential sub-sector. Consequently, the expected sign of FDI in this study was expected to be positive.

ER: the real effective exchange rate was defined as the product of the nominal effective exchange rate and domestic consumer price index divided by the foreign consumer price index. An increase in the real effective exchange rate (depreciation) makes the exports cheap in the international market, thereby increasing the exports of the country. The opposite happens when it increases. Consequently, in this study, the expected sign of the real effective exchange rate was positive.

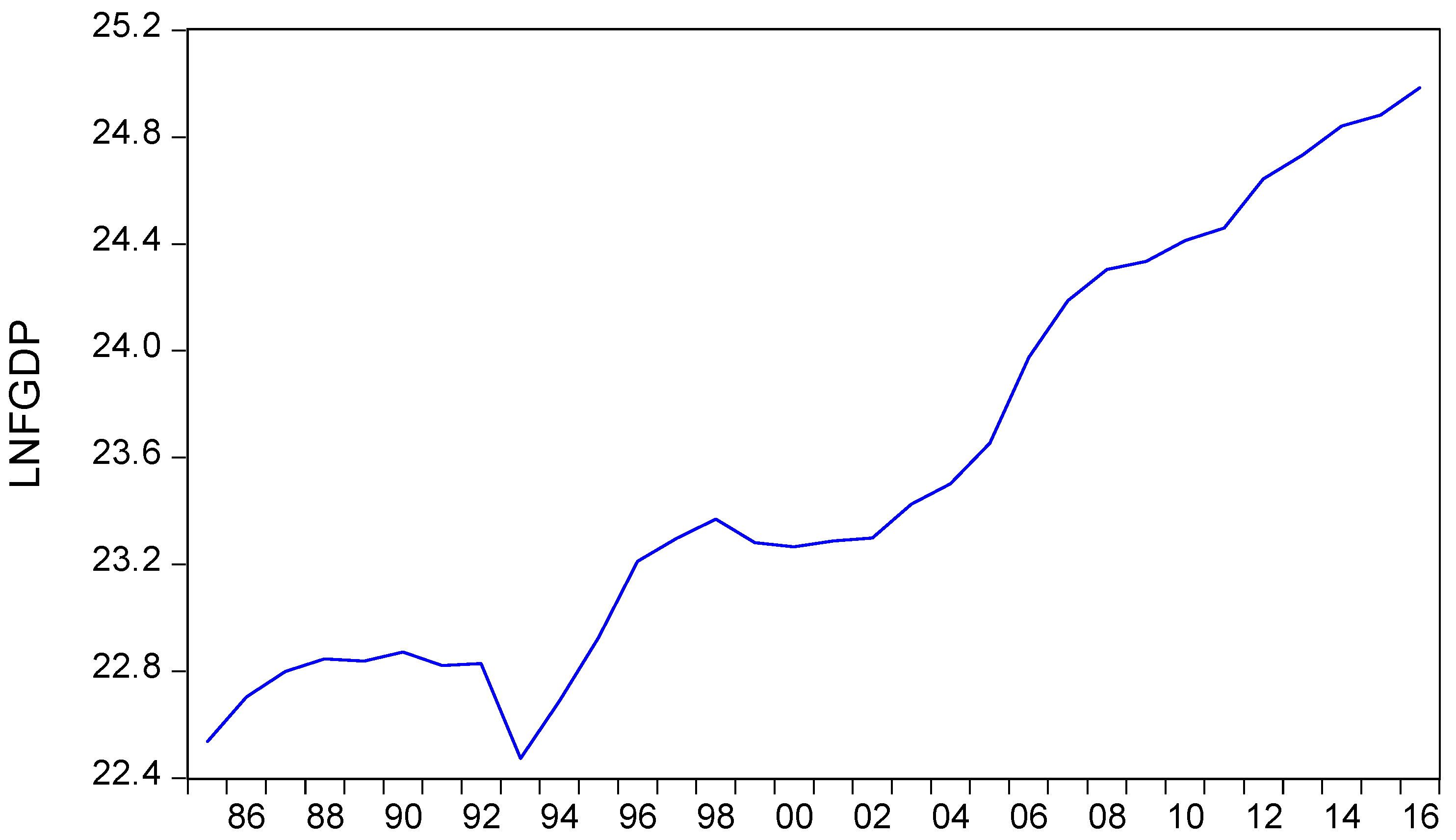

FGDP: Foreign GDP was defined as the average real GDPs of the major importers of horticultural crops. Diversification of both commodities exported and importing countries were considered by many as an important means of improving export performance in developing economies. Consequently, foreign income was hypothesized to influence horticulture export performance positively.

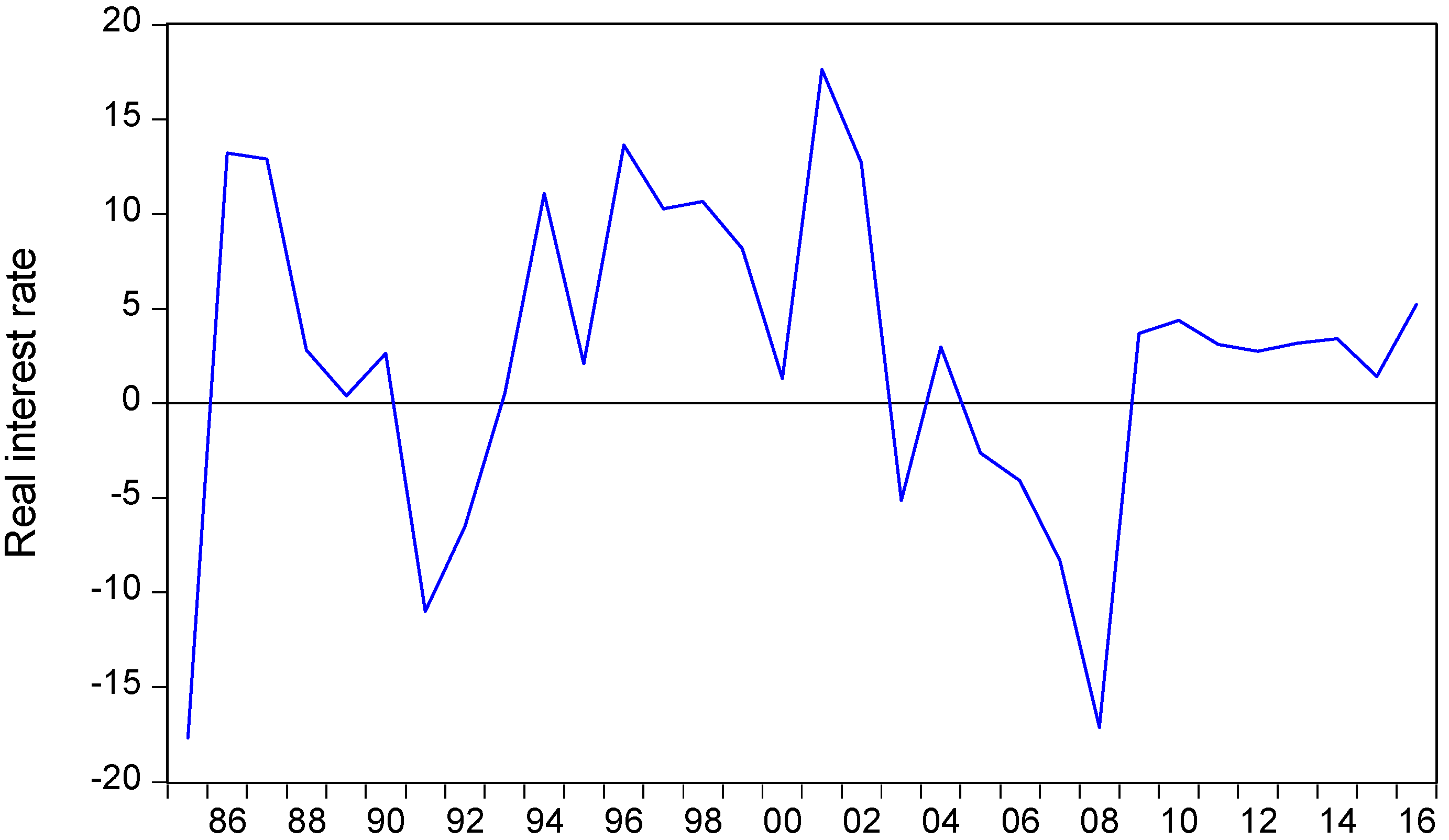

RIR: Real interest rate was defined as the nominal lending rate adjusted for inflation. The higher the interest rate, the lower the investment in production of horticultural crops and the less will be the volume of exports. Consequently, a negative relationship was expected between horticultural exports and the real interest rate.

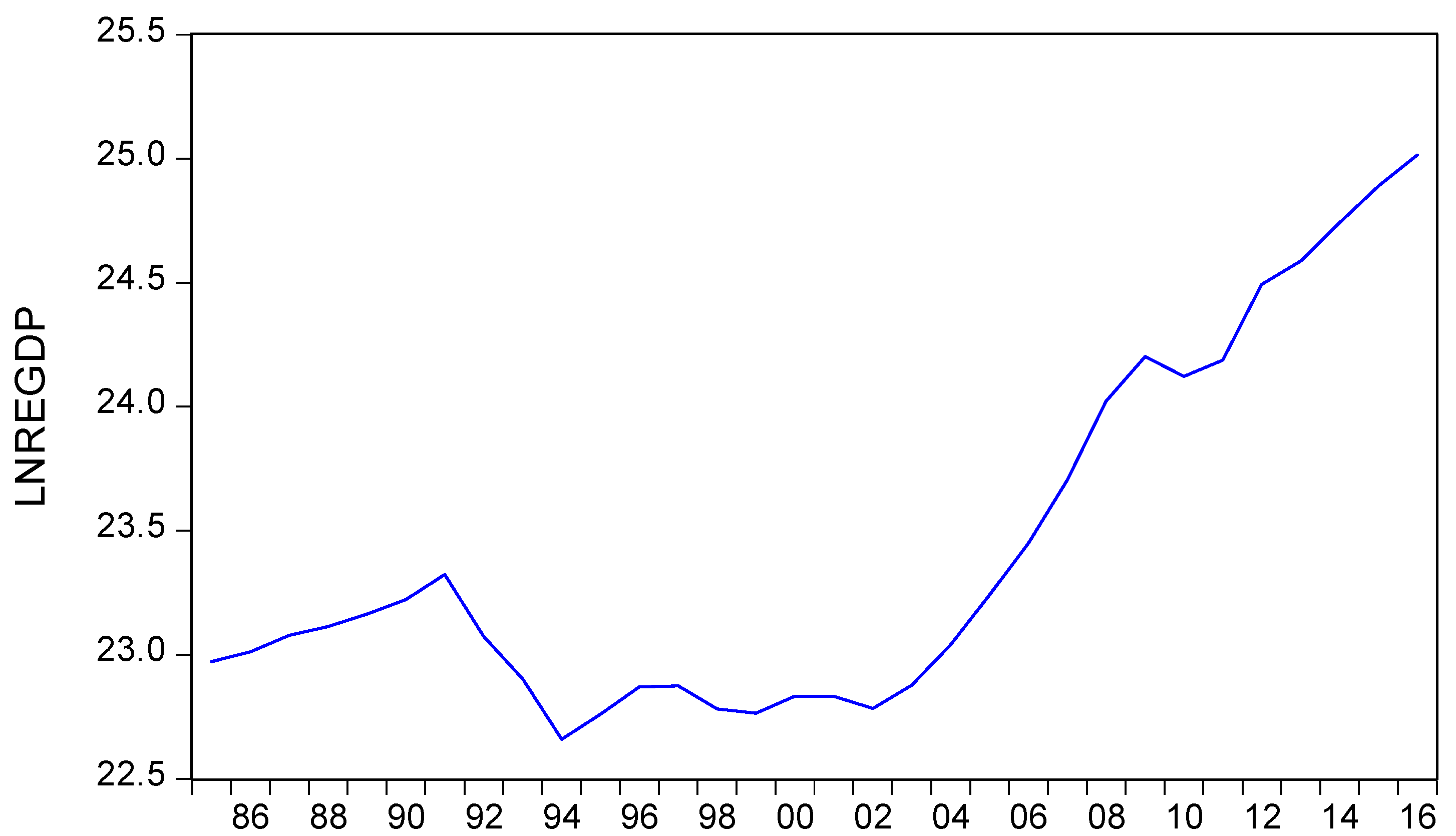

RGDP: It was defined as the real GDP of the exporting country which was Ethiopia in this case. The higher the real GDP of the country, the higher will be its export performance. Consequently, real GDP of the exporting country was expected to influence export performance positively.

PRICE: It was the average world price of fresh fruits and vegetables (dollars/kg) sourced from the World Bank and FAO statistics. It was hypothesized to have positive effects on horticultural export performance, since increases in output prices will lead to increased revenues.

BREAK: This was a dummy variable included in the model to capture the impact of the structural break that occurred in 2005. It was expected to have a positive impact on the export performance of the horticultural sub-sectors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}