Abstract

In this paper, a framework is presented for the evaluation of smart grid environment which is called the three-layer model. This three-layer model comprises three specific categories, or ‘layers’, namely, the stakeholder, market and technologies layers. Each layer is defined and explored herein, using an extensive literature study regarding their key elements, their descriptions and an overview of the findings from the literature. The assumption behind this study is that a solid understanding of each of the three layers and their interrelations will help in more effective assessment of residential smart grid pilots in order to better design products and services and deploy smart grid technologies in networks. Based on our review, we conclude that, in many studies, social factors associated with smart grid pilots, such as markets, social acceptance, and end-user and stakeholder demands, are most commonly defined as uncertainties and are therefore considered separately from the technical aspects of smart grids. As such, it is recommended that, in future assessments, the stakeholder and market layers should be combined with the technologies layer so as to enhance interaction between these three layers, and to be able to better evaluate residential smart energy systems in a multidisciplinary context.

1. Introduction

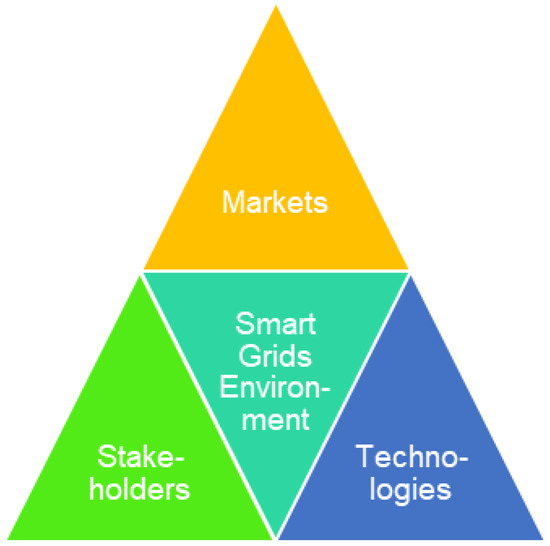

For the successful deployment of residential smart grids, it is evident that interdisciplinary information about energy technologies, energy markets and the needs of various types of stakeholders must be identified, merged, and implemented in practice. Therefore, in this paper, the results of an in-depth literature study are presented, aimed at elaborating a framework for gathering knowledge and developing understanding about residential smart energy systems. This framework, called the three-layer model, comprises three layers: stakeholders, the market, and technologies [1]. Each layer is defined below. The framework originates from the European research program, ERA-Net Smart Grids Plus, in which it is considered to provide a common context for interdisciplinary smart grid research (see Figure 1) [2]. According to the International Energy Agency (IEA), a smart grid is defined as “an electricity network that uses digital and other advanced technologies to monitor and manage the transport of electricity from all generation sources in that (local) network to meet the varying electricity demands of end-users” [3].

Figure 1.

Three-layer research model for smart grids environments (adapted from ERA-Net Smart Grids Plus [1,2]).

In this paper, we focused on the specific category of smart grid environment known as residential smart grids and their pilot projects for experimenting with diverse features. Residential smart grids are located in the low voltage grid, usually in the built environment, and involve tens to hundreds of households that are equipped with smart energy products and services.

Our definition of smart energy products and services (SEPS) includes all the products and services that have the ability to support the active participation of end users by efficiently and reliably managing their energy systems and balancing the mismatch between electricity demand and supply [4].

1.1. Layers

Below each layer of the model is briefly described in order to provide a general understanding for the reader.

1.1.1. Stakeholders Layer

In this layer stakeholders cover a diverse group of entities, ranging from individual end-users, communities, network operators, and aggregators to (local) governmental organizations. Stakeholders interact with smart grids through an interest or concern. Some features of smart grids, such as demand side management (DSM) and exchange of energy with other end users (peer-to-peer trading) involve individual end-user type stakeholders of the type of individual end users, whereas other features—such as a high penetration of renewable energy at a local level, as well as electric mobility [2,4,5,6]—involve stakeholders of a more organizational character such as network operators and governmental organizations.

1.1.2. Markets Layer

This layer comprises all the financial and business-related aspects of smart grids. Energy market structures, the micro-economics of energy technologies and energy billing belong to the markets layer. Also factors such as investments, net present value (NPV), levelized costs of electricity (LCoE), electricity tariffs and pricing mechanisms, fall into this category [7,8].

1.1.3. Technologies Layer

The technologies layer covers all the technological aspects of smart grids [9,10,11,12] related to energy technologies and information and communications technology (ICT), among which, but not exclusively, smart grid networks, distributed energy resources (DER) such as photovoltaic (PV) systems, wind turbines, micro-combined heat and power (μCHP) [13,14], energy storage systems [15], home energy management systems (HEMSs), DSM [16], demand shifting [17], demand and supply forecasting algorithms, electric vehicles (EVs), EV charging stations, stationary fuel cells, and hydrogen fuel cell electric vehicles (FCEVs) [18].

1.1.4. Flexibility

In addition to the three layers, special attention is given to ‘flexibility’ in this paper, as it is a main characteristic of future energy systems. It is defined as a “general concept of elasticity of resource deployment providing ancillary services for the grid stability and/or market optimisation” according to CENELEC [19]. In other words, electrical flexibility is the ability of a system to deploy its resources to respond to changes in net load, where the net load is defined as the remaining system load not served by variable generation [20]. Because the intermittent nature of renewable energy generation may threaten the stability of the overall system, smart grids can provide the flexibility needed for the correct operation of the energy system.

1.2. Aim

The main aim of this review was to emphasize the importance of each of the three layers and the current knowledge of each layer, to show the number of research activities in the different disciplines, and make an attempt to define the key elements of residential smart grids for sustainable energy and flexibility. To this end, a thorough review of the literature was performed. Compared to other established frameworks—such as the Transactive Energy [21], the Universal Smart Energy Framework (USEF) [22], and the Energy Flexibility Platform & Interface [23] —our review approaches energy transition at the residential level, using the theoretical three-layer model framework. We take into consideration each layer and their interrelations, suggesting cooperation among disciplines and parties, from their very beginnings and into the design phase. The main advantage of our approach is that we distinguish among the various disciplines in order to allocate knowledge and barriers for each layer in residential smart grid projects. This is a different approach than most of the stochastic or techno-economical models [24,25]. In this way, we aimed to decrease the uncertainties and increase active involvement at the residential level, making stakeholders and prosumers (consumers that also generate energy) part of the energy transition, and to stimulate feedback from end-users to designers. The research approach is presented in Section 2, with insights from the literature regarding the three layers then being presented (Section 3) and discussed (Section 4). The paper is summarized in the Conclusions (Section 5).

2. Research Approach

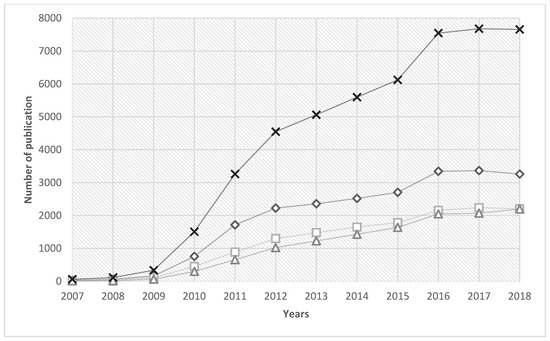

Our research consisted of reviewing journal papers, conference papers, reports and websites of interest to smart grids in the framework of technologies, markets, and stakeholders. The term ‘smart grid’ was used for the first time in 1966 [26]. Caution should be taken because at that time the term ‘smart grid’ was related to radio wave transmissions instead of electricity grids. The first official definition of a smart grid was approved by the US Congress in 2007, and signed into law in the same year [27]. According to a search in Scopus, which took place in November 2018, since 2007, there have been more than 100,000 papers published mentioning the term ‘smart grid’. We found it most significant to consider articles that mentioned ‘smart grid’ in the abstract, title or keywords in our literature study. We found around 40,000 works, 92% of them being conference papers (64%) and articles (28%). The literature study is summarized in Figure 2, and pertains to the years and different layers proposed above.

Figure 2.

Yearly number of publications found in Scopus using the search term ’smart grid’ and the three layers classification.

Up to 2012, the number of papers was exponentially increasing for all areas of research into smart grids. Since 2012, the increasing annual number of publications on smart grid topics has led to a massive volume of more than 4000 publications per year, represented by a linear increase between 2012 and 2015. Around 5600 publications were published in 2016, which is very similar to 2017. At the beginning of November 2018, the number of publications in 2018 had already reached 5200. Although the year has not ended yet, we did include 2018 in our results (Figure 2). Based on affiliation, most of the publications originated from the EU (37.5%), the USA (22%), China (19%), and other countries (21%). The trends are similarly exponential before 2012 for almost all regions, and for all disciplines. After 2012, the number of publications stabilized around 1000 publications per year for the USA and China, although trends in EU countries vary considerably. The Joint Research Centre of the European Commission database and reports indicate that 953 smart grid projects have been funded in the EU since 2007, by 2900 different organizations, involving 5900 participants, and with investments of around €5 billion [28]. This diversity in projects and participants, gave the EU the lead in the number of scientific publications. For the USA, the number of projects announced on government websites was limited to only 119. As such, the related budget ($4.5 billion) indicates that projects funded in the USA were mostly larger-scale projects than in the EU [29]. For China, pilot projects were expected to be even more concentrated, as today there are 15 smart city pilots, with an expected $7.4 billion of investments by 2020 [30].

A further analysis was needed in order to categorize papers in terms of the three layers proposed of the framework, aimed at highlighting the trends in weight of research directed towards each layer. The boundaries between the disciplines are difficult to clarify. A classification based on which journal the publication appeared, and it led to relatively very small number of papers for the market (Business, Management, and Accounting: 2.6%) and stakeholders (Social Sciences Journals: 4.2%) layers. Therefore, we searched in Scopus using the keywords that we used to define the layers. Multidisciplinary studies were taken into consideration so publications dealing with than one layer were mentioned in both corresponding layers. Therefore, the sum of the publication for each layer is greater than the total number of papers. It appears that markets and stakeholder layers’ tendencies are very close to each other. A possible explanation could be that many social scientific studies on users were critical of the market layer’s scientific contributions or insights, and those papers thus represent critiques. Another explanation could be that user behavior, stakeholder investments and expectancies played a major role in the market layer, considering the dependency of energy price on demand. The technologies layer showed at least 50% more publications than the other layers regardless of the year of publication.

3. Findings for Each of the Three Layers

3.1. Stakeholders Layer

Looking at the stakeholders layer, the main focus is on residential customers and prosumers [31,32,33]. It was found that users, as they are described in the more recent research, not only have different labels—such as customers, consumers, prosumers and end users—but are also assumed to behave differently from each other [4,34,35,36]. The most prevalent type reported on in the literature is the consumer, who is supposed to adapt to new developments in the energy system, such as smart grids. The prosumers are seen as users who consume and (co-)produce energy, who are sometimes also seen as potential active players on energy markets through aggregators [37,38]. The prosumers’ most important attribute is their ‘proactiveness’ inside the new energy system, which differs from passive consumers, who merely have to accept or adopt smart grids, and end users. Furthermore, based on the papers that focused on user experiences, with special attention paid to demand side management, it appears that the issue of the acceptance of smart grids is widely discussed. Only a few studies built on evaluations of real life experiences based on smart grid projects [39,40], whilst most studies focused on future scenarios and (online) surveys [32,40,41,42] (see report [43] for further details).

In particular, end-users’ knowledge with regard to smart grids, is shown to both enhance acceptance and to create confusion [33,44,45]. The literature review shows that from current smart grid projects and the reference framework USEF, the following other main stakeholder groups can be distinguished in smart grid environments: business customers, aggregators, balancing responsible parties, balancing service providers (BSPs), suppliers, distribution system operators (DSOs), transmission system operators (TSOs), governments, and other regulators (Table 1) [8].

Table 1.

Stakeholders in smart grids environments and descriptions of their roles (adapted from [8])

The role descriptions shown in Table 1 indicate stakeholders’ roles and their interactions with the markets or technologies layers. Our study also shows that the future roles of other stakeholders, other than the residential customers, are foremost mentioned in policy reports with a special focus on the role of the DSOs, which are generally public organizations. Mostly, their concerns are reliability and equity among the residential energy consumers, and not the development of new markets. From these reports, it seems that uncertainties still exist with regards to market structures (monopoly versus competition), task delegation, the necessity of new (independent data handling) institutions, etc.; however, again, there is very little information about the exact roles of the stakeholders inside smart grids pilot projects, nor as facilitators of the renewable energy transition.

DSOs in the Netherlands play a major role in improving the reliability and robustness of the local grids in response to the supply of distributed renewable energy and expected peaks in demand for charging EVs. To support this statement, Dutch DSOs participated in 28 out of 31 projects with at least 15 households in each. In 12 of these pilots, they were part of the project consortium [43]. Regarding TSOs, their role is closely related to that of the DSOs, with the duties of developing and maintaining the transmission of electricity, and balancing supply and demand across different districts. They usually have a particular interest in new DER technologies as vehicle-to-grid (V2G) in order to provide local balance and supply to decrease transmission and avoid congestion. In the Netherlands, the TSO also pilots some of the smart grids with aggregators.

3.2. Market Layer

From the existing literature, it can be concluded that several incentives for smart grid environments are present at the market level. Namely, aggregators can operate on the spot markets, i.e., by energy arbitrage, and on the balancing markets [8], however, some market barriers are present. For example, in many European countries, it is impossible for renewable electricity generation to operate on balancing markets, while this generation is very suitable to use for downward regulation [46]. Another current market inefficiency is the risk that current renewables generation incentive schemes (especially feed-in tariffs) decrease the value of newly installed renewables generation over time. Smart grids can address this by more efficiently matching supply and demand.

From a market perspective, one could argue that, when the shares of renewables in the grid increase to high levels, their inherent fluctuations would cause more volatile spot market prices and higher imbalance prices, thus providing higher incentives, and possibly business models, for smart solutions. On the other hand, one could also argue that, before that was the case, stakeholders would need to (and will) gain experience in these smart solutions because of the pivotal role that the electricity system plays in our society. Whether the current market model is already suitable for deploying smart grids thus remains therefore a matter for discussion in forthcoming years.

3.2.1. Pricing of Electricity and the EU Electricity Market

Concerning the pricing of electricity, in nodal pricing (or locational marginal pricing), which is incorporated in the electricity system of the USA, prices are set at different nodes in the system (places where supply and demand meet). In zonal pricing, as used in the EU electricity markets, prices are the same across the entire zone, not taking transmission limits into account. Therefore, the criticism of zonal pricing is that it does not stimulate the optimal placement of variable renewable electricity production [47,48]. For example, in Germany, much wind electricity production is located in the north, but the transmission line does not have the capacity to transfer this electricity to the south, resulting in congestion losses [47,49]. In 2015, 566 TWh was traded on the European Power Exchange (EPEX, including Germany, Austria, Luxembourg, France, the UK, the Netherlands, Belgium, Switzerland), while 59 TWh was traded on the intraday market, although the intraday market grew faster (26% versus 20%) [50].

There may be concerns about price and power fluctuations, regarding the market and technologies layers; however, flexible market scenarios, which control unwanted fluctuations, have recently been reported [51,52]. In addition, moderate fluctuations may potentially accelerate DER deployment, the design of various smart energy products and services, widen the international electricity networks’ power transfer capacities and agreements as part of EPEX, meaning that one aspect viewed as unbeneficial for one layer, may come to be potentially beneficial for the future of smart grids. For such perspectives, the three-layer approach facilitates the identification of interactions between layers, and therefore permits more global and multidisciplinary approaches on smart grids and energy transitions.

3.2.2. Flexibility of the Market

In terms of the dynamics in the electricity supply system, and due to system stability reasons, demand and supply need to match at any instant in time; otherwise, the system is in imbalance. In liberalized electricity systems, market mechanisms implemented to maintain the balance are increasing. In short-term markets and balancing especially, flexibilities aggregated from end-users (customers or prosumers) provide an increasing potential for smart grids. Such flexibility can be used for several use cases, such as balancing, optimizing trading costs and minimizing costs from the imbalance settlement (e.g., caused by forecast errors in renewable electricity generation) or for the customer to increase their own consumption, whereby these use cases can be associated with different roles/actors.

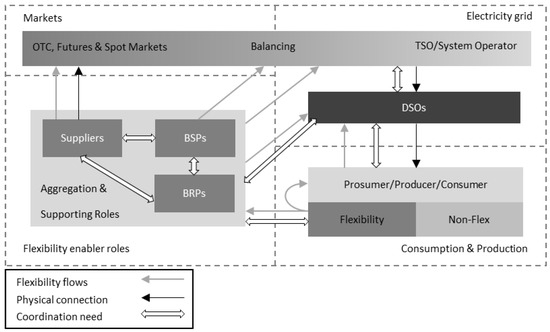

When using the flexibility for one use case, however, several other actors may be influenced by this activation, either positively or negatively. Future markets in smart grid environments indicate an increased coordination need between several actors in regard to the integration of flexibility, and different flexibility use cases are depicted based on different roles, as shown in Figure 3.

Figure 3.

Stakeholder overview showing the flow of flexibility.

3.3. Technologies Layer

The technologies layer covers systems, technologies, and energy products and services that physically create a smart grid environment. In this section, the physical systems of smart grid will be analyzed from three perspectives; DER, demand side flexibility and resource side flexibility. These perspectives were to highlight smart grid flexibility, which is considered to be the key component for its integration into the electricity network [44].

3.3.1. Distributed Energy Resources

From the perspective of residential smart grids the following technologies can be distinguished: DER systems in the form of micro-generators and energy storage, smart appliances, smart meters, energy monitoring, and home automation (Table 2).

Table 2.

Technologies layers in a smart energy system (adapted from [9,36]).

With reference to the technologies layer, mainly capabilities regarding the flexibility of specific technologies or residential applications are of interest. In addition to the above, hydrogen as a storage medium has received much attention in the last few years because of the flexibility it can provide [53,54]. Electrolyzers can provide wind/solar peak shaving by splitting water with renewable energy sources electricity and producing hydrogen. This bulk energy storage process is known as power-to-gas. At peak demand, fuel cells can use hydrogen to quickly respond to the load demand. Hydrogen energy technologies are complementary to batteries, which can supply day-to-day electricity, whilst hydrogen can be used for long-term energy storage, particularly seasonal storage (summer-to-winter).

3.3.2. Demand Side Flexibility

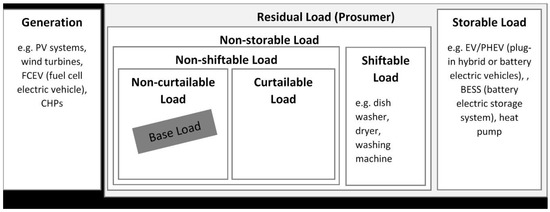

Technical flexibility stresses two main aspects: controllability (e.g., on/off modes, shiftability, modulation, and so on) and characteristics (e.g., minimum and maximum power, reaction time, etc.). Apart from these general characterizations of resources, metrics can be introduced to specify a certain resource with respect to its capability, or ’characteristics’. In [55], different approaches for defining flexibility in terms of characteristics are discussed, in which the three main aspects identified are ramp magnitude, ramp frequency, and response time. Figure 4 shows a classification of the residual load for the stakeholders group ’prosumer’, in terms of controllability. The base load represents the consumption in the prosumer premises, without any degree of freedom for flexibility or controllability. Loads providing controllability can be distinguished along with their ability to curtail, shift or store energy. As a concrete example, we can mention smart washing machines or dishwashers, which can provide a controllability, albeit within limits [56], to the smart grid for it to activate before the latest run time defined by the user [17]. In the case where a user programs the schedule of the appliance for economic reasons, the smart grid will optimize this according to the three layers: stakeholder (objective), market layer (price), technology (demand shifting).

Figure 4.

Prosumer residual load in terms of controllability (adapted from [57]).

3.3.3. Resource-Side Flexibility

While generators and large resources can be described in terms of three main technical aspects, such as ramp magnitude, ramp frequency, and response time, smaller demand resources might need to be characterized using more details.

Based on individual technical parameters, the eligibility of the system types can be evaluated for smart energy product and service applications. The energy resources described in this section can be assigned following the categories of controllability, shown in Figure 4 at the beginning of this section. Regarding the characteristics of resources, Table 3 provides an overview of some these for individual systems.

Table 3.

Characteristics of resources in terms of flexibility

The availability and activation duration of all the investigated systems is somehow limited either by technical parameters or by the needs or influence of customers. In terms of power supply or demand, most systems range within typical power connection values of households in Europe (~17 kW). Depending on system configurations, EVs or PV systems may exceed this value significantly, which may lead to increasing needs for grid investments (e.g., transformers, power lines, etc.). It was shown that the investigated systems at the residential level provide a different potential for flexibility applications. Whilst existing systems—such as PV systems, heat pumps, or appliances—provide limited controllability (except for downward regulation), the introduction of stationary battery energy storage systems in particular can enable full flexibility for local optimization or ancillary services.

4. Discussion and Perspectives

Although smart grids are still in an early stage of development, in recent years, societal implementation has gained momentum through the deployment of smart meters and small and medium scale smart grid pilots [44,58,59,60]. The transition to smart grids would create electricity systems that would enable consumers to make informed and empowered energy-related choices, promoting personal behavioral changes [39,61]. In this regard, evaluative studies and reports, such as [62,63,64,65] have highlighted the relevance of end-users in smart grid deployment. Nowadays, statistically significant data concerning social factors in stakeholder issues are few compared to the number of papers on technologies and market layers analyses [1]. Social-acceptance, in regard to product adaptation, appears to be a slow process, nevertheless, it is one of the key factors in the fast deployment of smart grids into the actual grid [39]. The continuous interactions and co-evolution of the three layers will define the smart grid environment, and the more interaction there is, the more rapid the transition will be to a fully smart grid. Our study aimed to highlight this multi-layer interaction to enable a wider point of view and practical solutions.

The first crucial point for social implementation is the selection bias in monitoring surveys caused by the so-called Hawthorne effect (see [66]). For instance, one of the world’s largest datasets of appliances, Pecan Street [67], is sharing the circuit-level residential electricity data in the USA intended for research purposes. The data has shown that the monitored residences are consuming far less electricity (33–60%) compared than the means of that specific region’s other network users, probably due to being a volunteer or being conscious that they are participating in a pilot experiment. Active participation of the individuals is crucial for efficient integration and energy resilience, therefore the design of smart products and services is crucial to maintaining their motivation to be energy efficient. In the stakeholders layer, detailed consumer profiles analyses are needed in order to point out such important facts, which will guide the technologies and market layers on structural issues in the electricity network. Treating raw data according to only the market and technologies layers, without considering end-users and stakeholders, is already inducing unneglectable simulation uncertainties on an hourly basis, and the high prediction errors may induce significant organizational and structural errors. The data purged of bias will help us to focus on specific smart energy products and services, their research and development [68].

Pecan Street’s recent data analyses from 12,083 monitored residences showed that 50% of the electricity used was related to air conditioning units, water heaters, and refrigerators [69]. Such applications could be shiftable loads if thermal isolation was feasible and sufficient, which again underlines the importance of load flexibility management. The main barrier would be the initial costs of these zero energy households, additionally equipping them with devices such as heat pumps, which in the EU are now supported by policy. Creating facilities and smart energy products, depending on end-users’ surveys about these devices and comfort expectancies, would be a cost-effective solution. Moreover, users’ knowledge with regard to smart grids (such as an abundance of feedback information) has been shown to both enhance acceptance and to create confusion, and in contexts, people prefer demand load control (the ability of energy suppliers to control user consumption) while they reject it in others.

For EU countries, the risk of residential peak demand is high and similar for countries such as Italy, Norway, and Germany, for average households, while on the other hand, Bulgaria and the UK differ completely [70]. Global warming also plays a role in the trend of peak demand. In 2014, France had the lowest peak demand on record since 2004 [71]. Other EU countries’ consumption profiles and peak demand characteristics remain to be validated for the smart grids from ongoing EU pilot projects [1]. At the regional level, zone policies and network characteristics vary. For instance, for the Netherlands, the barriers to fast deployment of smart grids are mostly uncertainty of the benefits, with only about 11.1% of the network contains renewable energy generation in 2015 [72], while a target of 14% renewables by 2020 in the Netherlands has been stated [73]. Meanwhile, Austria has a target of 34% renewable energy by 2020, and 100% self-sufficiency in energy by 2050 [74]. The main reason for this is the use of hydroelectricity as a huge energy reservoir to flatten the demand curve, which improves the renewable energy cost effectiveness by erasing the need for residential batteries. Austria is actually marketing itself as the ‘battery of Europe’. Transnational collaborations and knowledge sharing initiatives between these types of countries are in progress, in order to learn from favorable conditions and to consider weak points, so as provide more solid initiatives [1]. For instance, in the Netherlands, there are some investment plans in operation until 2025, as the green hydrogen economy in north, which might be a solution for the electricity grid capacity and flexibility problems in a cost effective way, through combining with other renewable/sustainable energy sources [75]. The renewable energy seasonal surplus could be converted and stored as hydrogen, transferred across the country by the existing gas network (after minor conversion), and could be stored in salt caverns to provide seasonal flexibility, and to balance regional pros and cons, salt caverns and the dramatic decrease in renewable energy production during winter.

Regarding energy efficiency and sustainable energy usage by EU citizens, the three-layer model usage will keep their motivations in pace, as feeling part of the energy transition. Smart products and services would give them the possibility to become greener or accomplish their economic objectives giving them a certain degree of freedom, meanwhile also providing the ability to the smart grid to optimize the shiftable load whenever available. Techno-economical approaches, or fully automated demand load control, or massive deployment of smart grids, would certainly bring resilience and efficiency from a technical and organizational perspective, which is of course a necessity [24,25]. However, in the residential sector, if not combined with the stakeholders layer, these approaches might fail to make citizens become more energy resilient or sustainable. Furthermore, because they might not feel part of the energy transition, the usage performance of new technology devices might drop. Or even worse, it paradoxically increase citizens’ consumption, as they may tend to consume more due to disempowerment resulting from the automated processes. Automated demand load would certainly reduce the peak demand, by risking this to be perceived as a real constraint for the residential sector. Even used to a moderate extent, if end-user perspectives are not taken into account, they will greatly reduce the acceptance of smart grids. Our three-layer model aims to highlight such interactions and the possible consequences, where the solution should come from all layers, not only from a top-down approach. The main barrier to smart grid deployments is the lack of multidisciplinary considerations for the residential sector where uncertainties are vast and objectives, consumption and production patterns, geographic attributes, local authority aims and policies are not identical.

5. Conclusions

Our study aimed to present a three-layer model (stakeholders, markets, technologies) for the assessment of residential smart grids. In this way, knowledge about the actual performance of residential smart grids can be collected and evaluated within its framework. The use of the three-layer approach increases awareness of the multidisciplinary aspects of the problem, which most of the recent and extensive technical literature reviews point out [11].

We defined and discussed each layer in terms of recent issues from different perspectives. Uncertainties still exist with regard to market structures, task delegation, the necessity for new (data-handling) institutions, etc. Issues resulting from human factors and the stakeholders layers, comfort expectancies, the aims and requirements of smart grid users are still unknown parameters, however they are deemed to be crucial in order to fit the market and demand energy management systems in smart grids. If the goal of some consumers is to be more sustainable, and for others to relinquish any comforts, but only to sell some of their local energy production, then the conflict of interest has to be analyzed well considering the entire grid. Consuming only renewable energies and storing them may not be the greenest way, as batteries also have notable ecological impacts. Bottom-up end user and stakeholder capacities and demands must be analyzed in conjunction with statistical consumption graphs. Also, a portfolio of users identified for minimizing bias, should be considered in order to discern structural and pricing issues in smart grids. Modellers admit the necessity of including many parameters, especially stakeholder behavioral or characterization parameters [54]. Social acceptance and practices also have to be considered closely and more data is needed to be more statistically significant, in order to define to what extent flexibility may play a role [28].

Funding

This research has received funding from the European Union’s Horizon 2020 research and innovation programme under the ERA-Net Smart Grids plus, grant number 646039, from the Netherlands Organisation for Scientific Research (NWO) and from BMVIT/BMWFW under the Energy der Zukunft programme.

Acknowledgments

Our project has received funding in the framework of the joint programming initiative ERA-Net Smart Grids Plus, with support from the European Union’s Horizon 2020 research and innovation programme. We would like to thank Esin Gültekin for her contributions on literature studies. Furthermore, we would like to acknowledge all participants in the smart grid pilots (in the Netherlands) involved in this study for their willingness to share their data, experiences, and knowledge with the researchers.

Conflicts of Interest

The authors declare no conflict of interest.

Disclaimer

The content and views expressed in this material are those of the authors and do not necessarily reflect the views or opinion of the ERA-Net SG+ initiative. Any reference given does not necessarily imply the endorsement by ERA-Net SG+.

References

- Reinders, A.; de Respinis, M.; van Loon, J.; Stekelenburg, A.; Bliek, F.; Schram, W.; van Sark, W.; Esteri, T.; Uebermasser, S.; Lehfuss, F.; et al. Co-evolution of smart energy products and services: A novel approach towards smart grids. In Proceedings of the 2016 Asian Conference on Energy, Power and Transportation Electrification, Singapore, 25–27 October 2016; pp. 1–6. [Google Scholar]

- ERA-Net Smart Grids Plus. European Research Area Network – Smart Grids Plus; ERA NET: Amsterdam, The Netherlands, 2017; pp. 5–8. [Google Scholar]

- International Energy Agency. World Energy Outlook; Organization for Economic Co-Operation and Development (OECD): Paris, France, 2011; ISBN 978-92-64-12413-4. [Google Scholar]

- Geelen, D.; Vos-Vlamings, M.; Filippidou, F.; van den Noort, A.; van Grootel, M.; Moll, H.; Reinders, A.; Keyson, D. An end-user perspective on smart home energy systems in the PowerMatching City demonstration project. In Proceedings of the IEEE Innovative Smart Grid Technologies Europe (PES ISGT) Europe 2013, Copenhagen, Denmark, 6–9 October 2013; pp. 1–5. [Google Scholar]

- Verhoef, L.; Graamans, L.; Gioutsos, D.; van Wijk, A.; Geraedts, J.; Hellinga, C. ShowHow: A Flexible, Structured Approach to Commit University Stakeholders to Sustainable Development. In Handbook of Theory and Practice of Sustainable Development in Higher Education; Leal Filho, W., Azeiteiro, U.M., Alves, F., Molthan-Hill, P., Eds.; Springer: Cham, Switzerland, 2017; pp. 491–508. ISBN 978-3-319-47876-0. [Google Scholar]

- Griffiths, J.; Maggs, H.; George, E. Stakeholder Involvement; World Health Organization (WHO): Geneva, Switzerland, 2007. [Google Scholar]

- Metz, D. Economic Evaluation of Energy Storage Systems and Their Impact on Electricity Markets in a Smart-grid Context. Ph.D. Thesis, University of Porto, Porto, Portugal, 2017. [Google Scholar]

- Universal Smart Energy Framework. USEF: The Framework Explained; USEF Foundation: Arnhem, The Netherlands, 2018. [Google Scholar]

- Van Wijk, A.; Verhoef, L. Our Car as Power Plant; IOS Press: Amsterdam, The Netherlands, 2014; ISBN 978-1-61499-377-3. [Google Scholar]

- van Wijk, A.; van der Roest, E.; Boere, J. Solar Power to the People; IOS Press BV: Amsterdam, The Netherlands, 2017; ISBN 978-1-61499-832-7. [Google Scholar]

- Nosratabadi, S.M.; Hooshmand, R.-A.; Gholipour, E. A comprehensive review on microgrid and virtual power plant concepts employed for distributed energy resources scheduling in power systems. Renew. Sustain. Energy Rev. 2017, 67, 341–363. [Google Scholar] [CrossRef]

- Oldenbroek, V.; Verhoef, L.A.; van Wijk, A.J.M. Fuel cell electric vehicle as a power plant: Fully renewable integrated transport and energy system design and analysis for smart city areas. Int. J. Hydrogen Energy 2017, 42, 8166–8196. [Google Scholar] [CrossRef]

- Gercek, C. Evaluation of heat pumps for balancing grids in combination with solar energy production: A Dutch Case Study. In Proceedings of the Solar Integration Workshop 2018, Stockholm, Sweden, 15–19 October 2018. [Google Scholar]

- Gercek, C.; Reinders, A. Photovoltaic Energy Integration: A Case Study on Residential Smart Grids Pilots in The Netherlands. In Proceedings of the 35th European Photovoltaic Solar Energy Conference and Exhibition (EU PVSEC), Brussels, Belgium, 24–28 September 2018. [Google Scholar]

- Schram, W.L.; Lampropoulos, I.; van Sark, W.G.J.H.M. Photovoltaic systems coupled with batteries that are optimally sized for household self-consumption: Assessment of peak shaving potential. Appl. Energy 2018, 223, 69–81. [Google Scholar] [CrossRef]

- Weck, M.H.J.; van Hooff, J.; van Sark, W.G.J.H.M. Review of barriers to the introduction of residential demand response: A case study in the Netherlands: Barriers to residential demand response in smart grids. Int. J. Energy Res. 2017, 41, 790–816. [Google Scholar] [CrossRef]

- Gercek, C.; Reinders, A. Balancing Renewable Energy Sources in Electricity Grids the Netherlands—How Residential Smart Grids can Contribute to Flexibility of Grids. In Proceedings of the DIT-ESEIA Conference on Smart Energy Systems in Cities and Regions, Dublin, Ireland, 10–12 April 2018. [Google Scholar]

- Robledo, C.B.; Oldenbroek, V.; Abbruzzese, F.; van Wijk, A.J.M. Integrating a hydrogen fuel cell electric vehicle with vehicle-to-grid technology, photovoltaic power and a residential building. Appl. Energy 2018, 215, 615–629. [Google Scholar] [CrossRef]

- CEN-CENELEC-ETSI Smart Grid Coordination Group. Smart Grid Reference Architecture. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/xpert_group1_reference_architecture.pdf (accessed on 1 November 2018).

- Lannoye, E.; Flynn, D.; O’Malley, M. Evaluation of Power System Flexibility. IEEE Trans. Power Syst. 2012, 27, 922–931. [Google Scholar] [CrossRef]

- Chen, S.; Liu, C.-C. From demand response to transactive energy: State of the art. J. Mod. Power Syst. Clean Energy 2017, 5, 10–19. [Google Scholar] [CrossRef]

- Universal Smart Energy Framework. USEF: The Framework Specifications; USEF Foundation: Arnhem, The Netherlands, 2018. [Google Scholar]

- Flexiblepower Alliance Network (FAN). Energy Flexibility Platform & Interface; FAN: Delft, The Netherlands, 2018. [Google Scholar]

- Marzband, M.; Fouladfar, M.H.; Akorede, M.F.; Lightbody, G.; Pouresmaeil, E. Framework for smart transactive energy in home-microgrids considering coalition formation and demand side management. Sustain. Cities Soc. 2018, 40, 136–154. [Google Scholar] [CrossRef]

- Marzband, M.; Azarinejadian, F.; Savaghebi, M.; Pouresmaeil, E.; Guerrero, J.M.; Lightbody, G. Smart transactive energy framework in grid-connected multiple home microgrids under independent and coalition operations. Renew. Energy 2018, 126, 95–106. [Google Scholar] [CrossRef]

- Darlington, S.; Felsen, L.B.; Siegel, K.M.; Deschamps, G.; Hansen, R.C.; Ishimaru, A.; Keller, J.B.; King, R.W.P.; Marcuvitz, N.; Senior, T.B.A.; et al. U.S.A. National Assembly, Committee Report, Fifteenth URSI General Munich, September 1966: Commission 6, Radio Waves and Transmission of Information; Progress. in Radio Waves and Transmission of. Radio Sci. 1966, 1, 1371–1379. [Google Scholar] [CrossRef]

- US Government. Energy Independence and Security Act; 110th United States Congress, Public law 110-140; U.S. Government Printing Office: Washington, DC, USA, 2007.

- Gangale, F.; Vasiljevska, J.; Mengolini, A.; Fulli, G. Smart Grid Projects Outlook 2017: Facts, Figures and Trends in Europe; Joint Research Centre: Brussels, Belgium, 2017. [Google Scholar]

- Office of Electric Delivery and Energy Reliability for the SGIG. Recovery Act Smart Grid Document Collection; Key Documents from DOE’s Recovery Act Smart Grid Investment Grant and Demonstrations Programs; US Department of Energy: Washington, DC, USA, 2016.

- JUCCE. Smart Grid in China. Available online: https://www.juccce.org/smartgrid (accessed on 16 November 2018).

- Michaels, L.; Parag, Y. Motivations and barriers to integrating ‘prosuming’ services into the future decentralized electricity grid: Findings from Israel. Energy Res. Soc. Sci. 2016, 21, 70–83. [Google Scholar] [CrossRef]

- Fell, M.J.; Shipworth, D.; Huebner, G.M.; Elwell, C.A. Public acceptability of domestic demand-side response in Great Britain: The role of automation and direct load control. Energy Res. Soc. Sci. 2015, 9, 72–84. [Google Scholar] [CrossRef]

- Horne, C.; Darras, B.; Bean, E.; Srivastava, A.; Frickel, S. Privacy, technology, and norms: The case of smart meters. Soc. Sci. Res. 2015, 51, 64–76. [Google Scholar] [CrossRef] [PubMed]

- Van Vliet, B.; Chappells, H.; Shove, E. Infrastructures of Consumption: Environmental Innovation in the Utility Industries; Earthscan: London, UK; Sterling, VA, USA, 2005; ISBN 978-1-85383-996-2. [Google Scholar]

- Goulden, M.; Bedwell, B.; Rennick-Egglestone, S.; Rodden, T.; Spence, A. Smart grids, smart users? The role of the user in demand side management. Energy Res. Soc. Sci. 2014, 2, 21–29. [Google Scholar] [CrossRef]

- Geelen, D.V. Empowering End-Users in the Energy Transition: An Exploration of Products and Services to Support Changes in Household Energy Management; TU Delft: Delft, The Netherlands, 2014. [Google Scholar]

- Naus, J.; Spaargaren, G.; van Vliet, B.J.M.; van der Horst, H.M. Smart grids, information flows and emerging domestic energy practices. Energy Policy 2014, 68, 436–446. [Google Scholar] [CrossRef]

- Geelen, D.; Scheepens, A.; Kobus, C.; Obinna, U.; Mugge, R.; Schoormans, J.; Reinders, A. Smart energy households’ pilot projects in The Netherlands with a design-driven approach. In Proceedings of the 2013 4th IEEE/PES Innovative Smart Grid Technologies Europe, ISGT Europe 2013, Lyngby, Denmark, 6–9 October 2013; pp. 1–5. [Google Scholar]

- Smale, R.; van Vliet, B.; Spaargaren, G. When social practices meet smart grids: Flexibility, grid management, and domestic consumption in The Netherlands. Energy Res. Soc. Sci. 2017, 34, 132–140. [Google Scholar] [CrossRef]

- Raimi, K.T.; Carrico, A.R. Understanding and beliefs about smart energy technology. Energy Res. Soc. Sci. 2016, 12, 68–74. [Google Scholar] [CrossRef]

- Buchanan, K.; Banks, N.; Preston, I.; Russo, R. The British public’s perception of the UK smart metering initiative: Threats and opportunities. Energy Policy 2016, 91, 87–97. [Google Scholar] [CrossRef]

- Döbelt, S.; Jung, M.; Busch, M.; Tscheligi, M. Consumers’ privacy concerns and implications for a privacy preserving Smart Grid architecture—Results of an Austrian study. Energy Res. Soc. Sci. 2015, 9, 137–145. [Google Scholar] [CrossRef]

- Reinders, A.; Hassewend, B.; Obinnna, U.; Markocic, E.; de Respinis, M.; Schram, W.; van Sark, W.; Gultekin, E.; van Mierlo, B.; van Wijk, A.; et al. Literature Study on Existing Smart Grids Experiences; University of Twente: Enschede, The Netherlands, 2018; pp. 27–42. [Google Scholar]

- Verbong, G.P.; Beemsterboer, S.; Sengers, F. Smart grids or smart users? Involving users in developing a low carbon electricity economy. Energy Policy 2013, 52, 117–125. [Google Scholar] [CrossRef]

- Lopes, M.A.; Antunes, C.H.; Janda, K.B.; Peixoto, P.; Martins, N. The potential of energy behaviours in a smart (er) grid: Policy implications from a Portuguese exploratory study. Energy Policy 2016, 90, 233–245. [Google Scholar] [CrossRef]

- Hu, J.; Harmsen, R.; Crijns-Graus, W.; Worrell, E.; van den Broek, M. Identifying barriers to large-scale integration of variable renewable electricity into the electricity market: A literature review of market design. Renew. Sustain. Energy Rev. 2018, 81, 2181–2195. [Google Scholar] [CrossRef]

- Neuhoff, K.; Barquin, J.; Bialek, J.W.; Boyd, R.; Dent, C.J.; Echavarren, F.; Grau, T.; von Hirschhausen, C.; Hobbs, B.F.; Kunz, F. Renewable electric energy integration: Quantifying the value of design of markets for international transmission capacity. Energy Econ. 2013, 40, 760–772. [Google Scholar] [CrossRef]

- Wang, Q.; Zhang, C.; Ding, Y.; Xydis, G.; Wang, J.; Østergaard, J. Review of real-time electricity markets for integrating distributed energy resources and demand response. Appl. Energy 2015, 138, 695–706. [Google Scholar] [CrossRef]

- Scharff, R. Design of Electricity Markets for Efficient Balancing of Wind Power Generation; KTH Royal Institute of Technology: Stockholm, Sweden, 2015. [Google Scholar]

- European Power Exchange. EPEX SPOT Reaches in 2015 the Highest Spot Power Exchange Volume Ever; European Power Exchange: Paris, France, 2016. [Google Scholar]

- Qin, J.; Ma, Q.; Shi, Y.; Wang, L. Recent Advances in Consensus of Multi-Agent Systems: A Brief Survey. IEEE Trans. Ind. Electron. 2017, 64, 4972–4983. [Google Scholar] [CrossRef]

- Jain, R.K.; Qin, J.; Rajagopal, R. Data-driven planning of distributed energy resources amidst socio-technical complexities. Nat. Energy 2017, 2, 17112. [Google Scholar] [CrossRef]

- Valverde, L.; Rosa, F.; Bordons, C.; Guerra, J. Energy Management Strategies in hydrogen Smart-Grids: A laboratory experience. Int. J. Hydrogen Energy 2016, 41, 13715–13725. [Google Scholar] [CrossRef]

- Patel, P.; Jahnke, F.; Lipp, L.; Abdallah, T.; Josefik, N.; Williams, M.; Garland, N. Fuel Cells and Hydrogen for Smart Grid. In Proceedings of the 2010 Fuel Cell Seminar & Exposition, San Antonio, TX, USA, 18–21 October 2011; pp. 305–313. [Google Scholar]

- Lund, P.D.; Lindgren, J.; Mikkola, J.; Salpakari, J. Review of energy system flexibility measures to enable high levels of variable renewable electricity. Renew. Sustain. Energy Rev. 2015, 45, 785–807. [Google Scholar] [CrossRef]

- Staats, M.R.; de Boer-Meulman, P.D.M.; van Sark, W.G.J.H.M. Experimental determination of demand side management potential of wet appliances in the Netherlands. Sustain. Energy Grids Netw. 2017, 9, 80–94. [Google Scholar] [CrossRef]

- He, X.; Hancher, L.; Azevedo, I.; Keyaerts, N.; Meeus, L.; Glachant, J.-M. Shift, Not Drift: Towards Active Demand Response and Beyond; European University Institute (EUI): Florence, Italy, 2013. [Google Scholar]

- Stephens, J.C.; Wilson, E.J.; Peterson, T.R.; Meadowcroft, J. Getting smart? climate change and the electric grid. Challenges 2013, 4, 201–216. [Google Scholar] [CrossRef]

- Naus, J.; van Vliet, B.J.; Hendriksen, A. Households as change agents in a Dutch smart energy transition: On power, privacy and participation. Energy Res. Soc. Sci. 2015, 9, 125–136. [Google Scholar] [CrossRef]

- Wolsink, M. The research agenda on social acceptance of distributed generation in smart grids: Renewable as common pool resources. Renew. Sustain. Energy Rev. 2012, 16, 822–835. [Google Scholar] [CrossRef]

- DeWaters, J.E.; Powers, S.E. Energy literacy of secondary students in New York State (USA): A measure of knowledge, affect, and behavior. Energy Policy 2011, 39, 1699–1710. [Google Scholar] [CrossRef]

- European Consumer Markets Evaluation Consortium. The Functioning of Retail Electricity Markets for Consumers in the European Union; European Commission: Brussel, Belgium, 2010. [Google Scholar]

- EU-Commission Energy 2020: A Strategy for Competitive, Sustainable and Secure Energy; No. 639; Publications Office of the European Union: Luxembourg, 2010.

- European Technology Platform. SmartGrids Strategic Deployment Document for Europe’s Electricity Networks of the Future; European Technology Platform SmartGrids: Brussels, Belgium, 2008. [Google Scholar]

- International Energy Agency. World Energy Outlook; Organization for Economic Co-operation and Development (OECD): Paris, France, 2017; ISBN 978-92-64-28205-6. [Google Scholar]

- Schwartz, D.; Fischhoff, B.; Krishnamurti, T.; Sowell, F. The Hawthorne effect and energy awareness. Proc. Natl. Acad. Sci. USA 2013, 110, 15242–15246. [Google Scholar] [CrossRef] [PubMed]

- Pecan Street. Pecan Street Online Database; Pecan Street: Austin, TX, USA, 2016. [Google Scholar]

- Glasgo, B.; Hendrickson, C.; Azevedo, I.L. Assessing the value of information in residential building simulation: Comparing simulated and actual building loads at the circuit level. Appl. Energy 2017, 203, 348–363. [Google Scholar] [CrossRef]

- Glasgo, B.; Hendrickson, C.; Azevedo, I.M.L. Using advanced metering infrastructure to characterize residential energy use. Electr. J. 2017, 30, 64–70. [Google Scholar] [CrossRef]

- Torriti, J. The Risk of Residential Peak Electricity Demand: A Comparison of Five European Countries. Energies 2017, 10, 385. [Google Scholar] [CrossRef]

- Réseau de Transport d’Electricité. 2014 Annual Electricity Report; Réseau de Transport d’Electricité: Paris, France, 2015. [Google Scholar]

- Eurostat. Your Key to European Statistics; Eurostat: Luxembourg, 2015. [Google Scholar]

- Ministry of Economic Affairs and Climate Policy. Dutch Goals with EU; Ministry of Economic Affairs and Climate Policy: The Hague, The Netherlands, 2017.

- Federal Ministry of Economy, Family and Youth, Energy Strategy Austria. Energy Strategy Austria; Federal Ministry of Economy, Family and Youth, Energy Strategy Austria: Vienna, Austria, 2017. [Google Scholar]

- Northern Innovation Board. The Green Hydrogen Economy in the Northern Netherlands; Northern Innovation Board: Groningen, The Netherlands, 2017. [Google Scholar]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).