Abstract

The Norwegian charging infrastructure ecosystem was investigated from a user perspective by (1) developing knowledge of end-user experiences with public charging, (2) mapping BEV owners and future owner’s user-friendliness needs and the extent to which these needs are met, (3) pointing at potential user-friendliness improvements, (4) mapping the charging infrastructure ecosystem and business models, and (5) developing scenarios for the future system development and the impact on charging infrastructure user-friendliness. The article draws on the literature, a BEV (battery electric vehicle) and ICEV (internal combustion engine vehicle) owner survey, 15 BEV owner interviews, 21 charging infrastructure actor interviews, and open information sources on the charger actors. The unregulated charging system evolved into a complex web of actors that developed their own charging networks following their individually sensible business models, which in sum led to serious user-friendliness issues. To gain access to all chargers, users need to interact with up to 20–30 apps and 13 payment systems, which comes on top of different plug types, power levels, and charger interfaces. Some actors support roaming, while others oppose it. OEMs want users to interface with chargers through the navigation system. In the future, the system will become even more complex and less user friendly as more actors join unless, e.g., consolidation, regulation, or independent network orchestrators reduce the complexity.

1. Introduction

This article regarding battery electric vehicle (BEV) charging infrastructure in Norway builds on two papers the authors presented at the World Electric Vehicle Symposium in Oslo 13–15 June 2022 titled: “Demand for standardization of public fast charger stations—user perspectives” [1] and “The Norwegian Charging Infrastructure Ecosystem” [2], as well as a report with an overview of the Norwegian charging infrastructure ecosystem [3]. These documents were developed as part of a research and innovation action that focused on finding ways to improve the user-friendliness of the overall Norwegian charging infrastructure ecosystem. The articles cover user needs for and experiences with public charging infrastructure and the business perspectives of the charging infrastructure through 2021. The hypothesis is that the way the market was developed and has become organized has led to unsatisfactory user experiences. The focus of the study is on user-friendliness issues related to the access to and use of charging infrastructure, not on the number of chargers deployed. The study does not cover the Tesla Supercharger network.

The aim of the study was to (1) develop knowledge concerning end-user experiences of using public charging services in Norway, (2) map BEV owners and future owner’s charging needs in terms of the user-friendliness of charging services, (3) map the charging infrastructure ecosystem and the various applied business models, (4) identify to what extent user needs are met within the current charging infrastructure ecosystem, (5) to point out potential user-friendliness improvements, and (6) establish scenarios for the future system development and their impact on the user-friendliness of the charging infrastructure and the actors’ business models to provide guidance on how the system can be made to function better.

The article contributes to the global research on charging infrastructure by shedding light on the gap between BEV user needs and what an unregulated charging infrastructure ecosystem actually provides in the world’s largest per capita BEV market. Other countries with rapidly growing BEV fleets will need guidance for developing charging infrastructure, as do actors developing charging infrastructure for heavy trucks. Both groups can learn from the Norwegian experience.

The article starts off in Section 2 with a presentation of the BEV and charging infrastructure status in Norway and an overview of the current knowledge of BEV owners need for and interaction with charging infrastructure. Section 3 presents an overview of the research on business models for charging. The materials and methods used is the present study are presented in Section 4, followed by the results in Section 5 and the discussion and the conclusion in Section 6.

2. BEV Ownership and Charging Infrastructure Use in Norway

2.1. BEV Ownership in Norway

The Norwegian charging infrastructure ecosystem case is particularly interesting as Norway is the world leader in BEV adoption per capita [4]. Over 460,000 BEVs were on the road at the end of 2021, which constituted 16% of the total passenger car fleet [5]. The BEV market share reached 54% in 2020, 65% in 2021 [6], and 79% in the first half of 2022 [7]. All other countries are far behind these fleet and market shares. This leading role is the result of three decades of active BEV policies with large incentives [4,8,9], market activities, industrial innovation [10], and charging infrastructure deployment. The parliament’s ambitious goal since 2017 has been that all new passenger cars sold in Norway shall be zero-emission from 2025 [11]. This target was a back-casting of the required transport sector contribution to reduce the national greenhouse gas emissions (GHG) by 40% by 2030, which Norway committed to in the 2016 Paris Agreement NDC [12]. These developments put pressure on the build out of fast chargers and other public and private charging infrastructure so that the charging barrier to BEV adoption could be reduced.

2.2. BEV Charging in Norway

In 2000, there were about 3000 BEV owners in Norway [10]. They charged their BEVs mainly at home using domestic outdoor sockets and occasionally at existing publicly available outdoor sockets outside offices, hotels, or cafés [10]. Fast charging was not possible until after 2010. An unregulated fast-growing charging infrastructure ecosystem has since 2010 emerged as a BEV enabler. However, this ecosystem built out by actors following their individual strategies and business models is not providing the expected user experience to many BEV users, which may somewhat deter future BEV growth. Charging infrastructure needs to work more effortlessly as BEV buyers progress from being mainly technology-interested multi-vehicle households to being more like vehicle owners in general [13,14].

BEV owners’ preferred charging locations are still primarily at home, then at work and in other public locations [13], a pattern also found in other countries according to a review of the global literature on BEV charging by Hardman et al. [15]. Over 90% of Norwegian BEV owners charge at home [13]. Most households can install a wall box charging solution [13] as they have access to a private parking spot. Flat owners must rely on installation of shared charging systems in the buildings’ common parking facilities. Such installations are supported economically by several counties and municipalities [16]. Many of the early adaptors changed to BEVs from internal combustion engine vehicles (ICEVs) due to environmental/technological interest and economic incentives [13,17,18]. When “everyone” is driving BEVs, they will demand more or less the same “seamlessness” at the public charging stations as at petrol stations. This will require an increased standardization, both regarding charging and payment, as well as a better handling of queues. This will be even more important in the future when more car owners without access to private charging facilities make the transition to BEVs.

Fast chargers along major roads and in cities enable longer trips and solve everyday range issues [16]. About 75% of BEV owners in three Norwegian counties reported having used fast chargers when driving long distances [19]. Another Norwegian survey found that the average non-Tesla BEV driver used public fast chargers about 19 times per year and obtained about 5% of the energy used by their BEV from fast chargers [13,20]. Yet, 40% used public fast chargers as rarely as 1–3 times per year. Long distance driving remains one of the final barriers to BEV adoption [13,16] in single-car households. Most BEVs are, however, used by multi-vehicle households that can use an ICEV for long distance driving. BEV models with a longer range can enable long distance trips, but many BEV owners dread taking their BEV for long trips [13,19]. The fast charge network expansion has helped, but there are still several user-friendliness issues that need to be addressed. Users want easy access to public chargers, but user surveys show that charging queues can be an issue on peak travel days/times [13], chargers can be out of order, payment could be easier, and users do not want to use a myriad of apps [13,19] to access chargers.

There were in early 2022 about 4000 public fast charging points in Norway, within a steadily expanding network [21]. There are around 10 major operators in the market with more than 280 charging stations (including Tesla), as well as 20–25 operators with fewer stations and charging points [21]. Unlike petrol stations, where pumps and user interfaces are rather standardized, fast charging in Norway is characterized by different charging systems, power levels, user interfaces, plugs, access and payment solutions, and (up to 2022) also a variety of pricing schemes. Consequently, BEV users must navigate in a complex charging landscape where they interact with a variety of systems and solutions that makes charging less streamlined and more time consuming than filling petrol, especially for those who seldom use public fast chargers. Very few public fast chargers have bank terminals, so users must pay via apps, operator-specific payment cards, SMS messaging, or other means. To avoid extra costs associated with SMS messaging, customers must register their credit card information in each charging operator’s system. When registered, the customer identification can operate the charger via an app or an RFID (radio-frequency identification) card. Few actors have opened for roaming, which would have made it easier for users to use the same authentication and payment solution across operators, making the BEV user experience more streamlined. The networks of slow chargers have similar payment systems, access, roaming, and user interface issues.

3. Business Models for Charging Stations

The functioning of the Norwegian charging infrastructure ecosystem and how it is influenced by the business models of its actors has not been investigated previously. There is substantial research on business models for charging infrastructure that focuses on the ability to develop sustainable income. Yet, it seems that research on how charging infrastructure business models can deliver the charging services that users need and prefer has been neglected in Norway and elsewhere. The gap between the services delivered and the needs and wants of users can become a threat to the sustainability of the charging infrastructure ecosystem in the long run and a barrier to increasing the adoption rate of BEVs.

International studies point out that for the BEV charging market to be economically sustainable in the long run, there is a need for businesses that generate value for the end customer, but also a sufficient return on the huge investments made in the charging infrastructure hardware and software. Well-suited business models are needed to achieve this. There is a large amount of public discussion about how the economics of public charging infrastructure depends on the applied business models, but not so much in the scientific literature, according to Zhang et al. [22]. Greene et al. [23] points out that as the charging market appears now, there is uncertainty about what are well-suited business models for public charging, partly because the utilization rate is still generally low, and that the roles of the public and private sectors are not well defined. This conclusion is also supported by de Rubens et al. [24] and Van der Kam et al. [25], who also point out that the difficulties in finding profitable business models are one of the biggest challenges for the roll-out of public charging infrastructure. Studies such as those by the Boston Consulting Group [26], Deloitte [27], Helmus and Van den Hoed [28], and Schroeder and Traber [29] point out that it is common for businesses to struggle to find profitability in investments and operations in public charging infrastructure, especially fast-charging infrastructure. This situation is related to the fundamental fact that the costs of investment and operation are high relative to the size of the initial customer base, i.e., BEV users, and their willingness to pay. A Norwegian charging deployment strategy developed in 2012 [30,31] therefore found that fast chargers should be deployed at locations where other revenue streams could be pursued, e.g., kiosks, restaurants, or shopping centers. BCG [32] found that lack of government guidelines and requirements have resulted in a chaotic ecosystem for charging in several countries.

The ecosystem for EV charging covers many different sectors. Within each sector, there is a myriad of products and services to deliver to different customer segments. Different companies can provide products and services both within a segment of a sector and across segments and sectors. In other words, there are thousands of possible business models based on combinations of these aspects. A classical illustration of the enormous range of possible business models can be found in the morphological boxes in Kley et al. [33] that are used to show the potential for new business models in the expanded ecosystem for electric cars, batteries, charging infrastructure, and the energy system.

4. Materials and Methods

The analysis in this article is mainly qualitative, building on different types of data sources in order to obtain a broad overview, as well as to go in-depth on certain aspects of the current charging infrastructure user needs and to understand the functioning of the current ecosystem. How well the charging infrastructure ecosystem accommodates these user needs and the reasons for any discrepancies are then investigated for the current situation and in future scenarios.

4.1. Methods Used to Investigate User Needs

4.1.1. Literature Review

The literature on user needs and interaction with charging infrastructure in Norway were analyzed to provide the background for the analysis. The literature has consisted mainly of peer-reviewed scientific articles, but also research and consultancy reports and government documents. The literature review focused on studies of the situation in Norway. Norway is so far ahead of other countries in terms of BEV adoption that results obtained elsewhere have limited relevance to the current Norwegian conditions.

4.1.2. Vehicle User Survey

An online survey was carried out in June 2021. The participants were recruited from the NAF (Norwegian Automobile Federation) member base through a special invitation sent out to 10,000 NAF members, of which 1237 responded. A total of 76% of these were BEV owners, 18% were ICEV owners, 5% were PHEV owners, and 1% used car sharing services. ICEV owners represent here the potential future BEV owners that have not yet made the transition. The mean age of the respondents was 54 years, and the majority were men. The survey contained questions about car ownership and driving behavior. BEV owners were asked about charging behavior and views on public charging infrastructure in Norway, and more specifically about payment methods, pricing, experiences pertaining to charging queues, user-friendliness, and preferred charging station facilities. ICEV owners were asked about their views on BEVs and asked to state their imagined preferences regarding number of charging stops and acceptable charging time if they were to become BEV owners.

4.1.3. BEV Owner Interviews

A total of 15 semi-structured anonymous interviews were conducted with BEV owners in 2021. In order to gain insight into different user groups experiences and views regarding their use of charging infrastructure, a strategic sampling strategy was utilized. The target was to reflect variations in BEV user groups and be representative of different types of BEV users with different housing situations, car usage patterns, and charging behavior. Participants were recruited from the NAF member base, from members of the car sharing service “Bilkollektivet”, and from contacts within our existing professional network. Nine of the participants were male, and six were female. The respondents’ ages ranged from 20 to 70 years. Interviews were carried out virtually via Microsoft Teams or over telephone. The interviews lasted between 30 and 80 min. Upon completion, each interview was transcribed, and a thematic analysis was performed to identify salient themes in the data reflecting BEV users experiences.

4.2. Methods Used to Investigate the Functioning of the Charging Infrastructure Ecosystem

4.2.1. Literature Review

The international literature on business models for charging was analyzed as background for understanding the motives of the charging infrastructure actors and the potentials and preconditions for developing sustainable businesses for the different types of actors. Peer-reviewed studies, consultancy reports, and government documents were applied. No literature covering this topic was available specifically for Norway.

4.2.2. Open Data Collection

Open data on the Norwegian charging infrastructure ecosystem and its actors were systematically collected to be able to understand how the overall charging ecosystem functions, i.e., who are the actors, what do they do, and who interacts with whom and how do they interact? These open data include data and information from the web pages of the actors and their partners, as well as news articles and other open documents.

4.2.3. Charging Infrastructure Ecosystem Value Chain Analysis

The BEV charging ecosystem actors were systemized as a value chain for the purpose of the analysis in this article, which is consistent with the approach in reports by ADL [34], the Boston Consulting Group [26], Capgemini [35], Deloitte [27], and PwC [36]. Inspiration was drawn from these when illustrating the value chain in this article. Supporting functions from government and membership organizations were included alongside the value chain, as illustrated in Figure 1.

Figure 1.

Illustration of the value chain for electric car charging.

4.2.4. Charging Ecosystem Actor Interaction Mapping

The ecosystem was also systemized as a functional map that shows the monetary and co-operative interactions between the different actors and actor types, e.g., CPOs, EMSPs, land and facility owners, MaaS actors, RFID card issuers, software suppliers, and owners of common parking facilities (public facilities as well as private parking facilities for flat owners). The map provides a holistic view of the Norwegian charging infrastructure ecosystem. It was built up by analyzing data from reports, press articles, and open sources.

4.2.5. Semi-Structured Interviews with Charging Infrastructure Actors

A total of 21 semi-structured anonymous interviews were carried out via Microsoft Teams. To cover the entire ecosystem as defined in Figure 1, the following actors were interviewed: charge point operators (CPOs), electromobility service providers (EMSPs), mobility as a service (MaaS) companies, hardware and software (HW/SW) suppliers, landowners, BEV producers (OEMs) represented by their importers, energy companies, and government agencies. Some of the actors had activities in several parts of the ecosystem. The interviews were carried out during the period of June–October 2021 and were transcribed afterwards.

4.3. Charging Infrastructure Scenarios

On the basis of the outcome of an internal workshop, 10 potential scenarios for the future charging infrastructure landscape were developed and discussed. To span out the potential future of the ecosystem in a manageable setting, the authors used their best judgment to reduce the number of scenarios to the five most likely scenarios. These final five scenarios were then further discussed in terms of their ability to meet future user needs and their business model implications.

5. Results

5.1. User Needs

5.1.1. User-Friendliness

Respondents from the survey and participants in the interviews reported experiencing several user-friendliness issues when using public fast chargers. Many of the issues BEV users experience can be traced back to the diversity of service providers in the market for fast charging. Each of these have developed their own charging offering on the basis of their own business model. The charging stations vary greatly in terms of layout, user interfaces, payment solutions, and charger activation, which comes on top of the different types of plugs, the cables with different lengths and locations, and different charging power levels associated with the BEV technology and chargers in general. Consequently, several of the respondents were dissatisfied with public fast charging services and emphasized the need for standardization of all public charging stations. Quotes from interview participants:

“There are many different systems in terms of physical plugs. What kind of plug is this? What power can I get out of this one? What is most up to date? Is it the same standard on a Tesla? After a while, you start to understand”.Informant 6

“Often I see people that are not accustomed to driving an electric vehicle, trying to use the charger that I’m already using, thinking they can use the other cable (there are two options, one that I can’t remember the name of and CSS). Visible information on the charger should have been available where it says that you can only use one cable at a time”.Informant 8

A quote from a survey participant is as follows: “Charging of a BEV should be just as simple as filling petrol. Drive to the station, insert the cable, and pay with a bank/credit card. I have never experienced that this succession differs between different petrol stations. It should be equal to use all public charging stations; it should be simple.”.

To avoid having to learn the operation and payment system of other operators, 55% of the respondents in our survey stated that they deliberately used the same charger operator each time they use public chargers, a fact that could be mistaken for customer loyalty. Almost half of the respondent stated that they had bought a BEV with large batteries to avoid having to use public chargers. This development could threaten the long-term profitability of fast charging. It can also lead to larger than necessary batteries in Norwegian BEVs, which would have a negative ecological impact.

5.1.2. Pricing and Payment Method

The operators of the fast-charging stations in Norway had different prices and pricing models up to 2022. During 2022, all major actors changed to pricing per kWh. The survey and interviews were carried out in 2021, and pricing was then a major user concern. The survey and interview results on this topic are presented here, as this experience will be important to other countries to learn from. Up to the end of 2021, some CPOs and EMSPs charged for kWh, some per minute to avoid users charging slowly past 80% battery state-of-charge, and some used a combination of these solutions.

Many found paying by the minute unfair because the important part is how much kWh you receive. Most of the respondents found it difficult to understand in advance how much the charging would cost. This was evident in the survey as well as in the interviews. About 70% of the BEV owners in the survey either partly or fully agreed to the statement “it is difficult to understand what the price of using public fast chargers will be”. A majority within both the group using public fast chargers 1–3 times a year and the group using public chargers more than 20 times each year agreed on the difficulty of understanding the price. Price information was often lacking or difficult to understand. In the interviews, several of the participants drew parallels to fueling on petrol stations, where pricing information tends to be clear and easy to understand. In the case of public fast chargers, BEV users were often not provided with price information until the charging had finished.

Quotes from interview participants:

“What annoys me is the price. The taximeter starts before the charging has begun and it ends a couple of seconds after the charging is finished. The Norwegian Metrology Service should conduct controls on fast charger stations, like they do on gas stations, so we are not taken advantage of. It boils down to seconds”.Informant 4

“The problem is lacking information about how fast I’m charging; how much I’m charging and how much it costs. These three things tend to be hidden at most charging stations. It’s normally when you have finished charging that you know how much you’ve spent, unless you’ve brought a calculator and do the math yourself”.Informant 9

“It’s like going to a petrol station where they’ve covered all the prices with white tags. You can’t see the price before after you’ve charged. That really sucks”.Informant 5

The following are quotes from survey participants:

“It is hopeless that precise pricing is not available, like at petrol stations. I would prefer information about actual costs and received kWh during the charging session. Ideally, I could indicate the wanted charging percentage at the beginning, and the charging session would automatically stop when this percentage is achieved”.

“I want to be able to pay by credit/debit card, get information on the price before I start the charging, and receive information about the actual costs after the charging session is ended”.

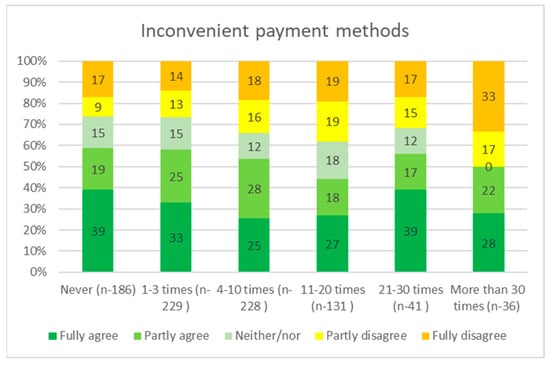

More than 50% of the BEV owners found the payment method at public fast charging stations inconvenient (Figure 2) according to the survey. Figure 2 shows the level of dissatisfaction/inconvenience with the payment systems, depending on how often they used public fast chargers during a year. Many state that they wished paying with credit/bank card was an option (this is currently only tested out at a small percentage of the fast charger stations in Norway). BEV owners who seldom use public fast chargers find the payment method slightly more inconvenient than the ones that use public chargers more often. Even among BEV owners who use the chargers more than 20 times a year, the level of dissatisfaction is relatively high.

Figure 2.

Distribution showing BEV owners’ level of agreement to the statement “I find payment solutions at fast-charging stations inconvenient”, according to the number of times the respondents have used public fast chargers the last 12 months (n-851).

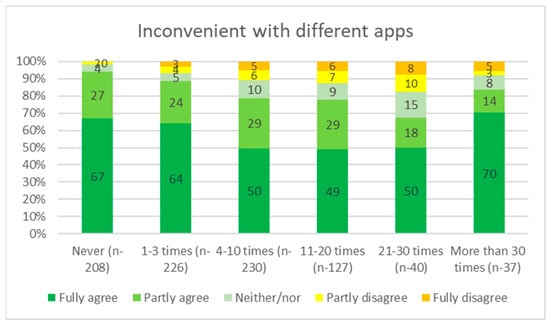

The average BEV driver in the user survey had downloaded three different charger operator apps. About 75% agree to the statement “It is inconvenient when charging operators operate with different apps”. The perceived inconvenience was fairly independent of the number of times the respondent used public fast chargers (Figure 3). There were some variations between age groups, but this could be sample related. It was a tendency that those who seldom (three times or less per year) or often (30 times or more) used public chargers were somewhat more annoyed.

Figure 3.

Distribution showing BEV owners’ level of agreement to the statement “It is inconvenient when charging operators operate with different apps”, on the basis of the number of times the respondents used public fast chargers the last 12 months (n-868).

The following are quotes from interview participants:

“Having all these apps is confusing, because if I’m planning a trip, I can’t just use Google Maps and find all the different charger services there. My experience is that I’m unable to get a full overview, and that I’m forced to use each app individually to locate charging stations, and get information about the terms and so forth, and then I’m not even sure if I have the right app”.Informant 10

“An opportunity for simpler payment would be nice. To be able to pay with credit card (…). An elderly person who uses fast chargers on rare occasions would want to do it as simple as possible. If this was better, I think the development in terms of the number of electric vehicles would go much faster”.Informant 5

The following is a quote from a survey participant:

“It should have been a common method for payment at all public charging stations, without having to download an app to the phone. Should be possible to pay with debit or credit card. Not everybody is comfortable with apps, especially the elderly”.

5.1.3. Information and On-Site Services

Findings from the survey and the interviews suggest that BEV owners desire better information about the availability and operational status of chargers, i.e., information about out-of-order charging points and available charging points at the different charging stations. Moreover, several informants wished for road signs indicating the location of charging stations along main roads. For long-distance drivers (driving 100 km+), access to the same amenities at fast charging stations as they are used to from petrol stations are highly valued when using public chargers. Amenities mentioned include basic facilities such as toilets or benches, but also service options and the possibility to buy food and beverages. Lighting conditions on site were also frequently mentioned. Enough lighting is important to be able to read the information on the charger and to be able to locate and insert the correct cable. The fact that most charging stations are built without roofing or other means of shelter is a topic of great frustration for many BEV owners. Being under a roof when using public chargers, especially during the winter, is appreciated when it is raining/snowing. Many BEV owners pointed out the need for a system for handling charging queues, which has become an increasing problem, especially during the seasonal vacation times, public holidays, and on weekends.

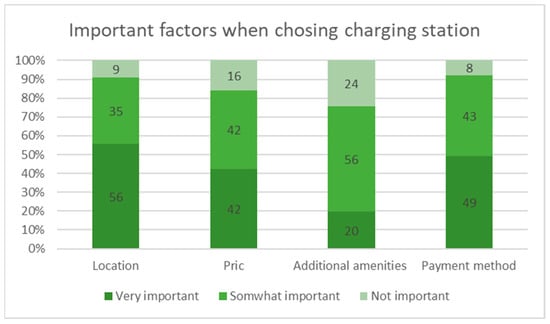

Figure 4 shows how BEV owners consider the importance of different factors when choosing a charging station. Location and payment methods were considered the most important factors, but price and amenities were also important. About 75% agree that amenities at fast charger stations are important (the question did not differ between the charging stations located in the cities or along main roads connecting cities). The availability of amenities was more important at stations typically used by long distance travelers.

Figure 4.

Important factors when choosing public charging station. BEV owners; n-675.

The following are quotes from interview participants:

“I normally charge where I can use toilets, buy ice-cream, coffee etc. That is much more OK than (charging stations) where there are just two chargers in the middle of nowhere. It’s nice to be able to do something other than just sit in the car. I would not let it determine my path, but along the route I am going, I would choose charging stations with extra service options. This is more important than if I save 15 kroner (NOK, NOK 1 = EUR 0.1) on charging”.Informant 7

“I’m not very fond of chargers that are in the middle of nowhere. It must be facilities that allows you to do something there while charging. Gas station, toilet, etc.”.Informant 8

“I have experienced that the there are no available charging points when arriving at a charging station. It’s difficult to know how long others plan to charge and where to park in the meantime. How does the queuing system work? Are you supposed to drive to the next charging point? (…) I get that all charging points are busy sometimes, but the fact that you’re not provided with any information regarding when it will be available, creates a sense of uncertainty. There should be a function on the charger where you could plot in ‘I need to have 50 km left so I get home, how long does it take?’”.Informant 5

The following are quotes from survey participants:

“When it comes to amenities, the type of amenities is not so important, if it is a grocery store, a kiosk or a café. The important thing is that there is something. The best option would be if the chargers were placed at petrol station because they are usually open 24/7 and have toilet facilities”.

“A form of booking/queue handling system should be available, to avoid arguments and “pointed elbows” on popular weekends”.

These user opinions about location and amenities points at a need to involve facility owners, fuel and energy stations, and roadside cafés and shops in the development of a nation’s charging infrastructure, as pointed out already in 2012 in a proposed strategy for charging infrastructure deployment [30,31]. Such actors have indeed been important in developing the Norwegian charging infrastructure ecosystem, as seen in the next section.

5.2. The Norwegian Charging Infrastructure Ecosystem Actor Landscape

Turning to the supply side, the charging infrastructure market consists of a number of actors from the public sector and many different parts of the private sector that have built up a vivid charging market since 2010. These actors play different roles in the value chain, as well as in making the charging market work. The most important roles in the charging infrastructure ecosystem are outlined in Table 1.

Table 1.

Actor types and roles in the Norwegian charging infrastructure ecosystem.

The core actors in the charging infrastructure ecosystem are the CPOs (Mer, Recharge, BKK/Eviny, Lyse, Ionity, Kople, CircleK, Tesla, and others), some of which have an integrated EMSP service, such as Mer, Eviny, CircleK, Kople, and Tesla (non-Tesla BEV charging), or offer such services via a broader roaming service (Fortum Charge and Drive). The roaming EMSPs Elton, Kople, and Elbilforeningen/Ladeklubben (EV Association) connect BEV drivers with CPOs via an app or an RFID card and handle payment at connected CPO networks so that their user gets one bill. RFID cards work as identification, but payment information must be linked to the RFID card number within each CPO/EMSP system/app when they do not support roaming. International roaming actors (Hubject, Digital Charging Solutions, Plugsurfing, Shell NewMotion) aggregate CPO networks into international charging networks, facilitate payment between actors, and are accessible for EMSPs. They have a limited foothold in Norway.

Landowners, i.e., municipalities (Oslo, Bergen, Trondheim, Stavanger, etc.) and other public property owners (Avinor, BaneNor) rent out land to put chargers on. Fast-food chains (McDonalds, Burger King), shopping centers (Steen and Strøm, Olav Thon Gruppen), grocery chains (Norges-gruppen, Coop, Rema 1000) and other store chains (Ikea), hotel chains (Olav Thon Gruppen), and fuel stations (CircleK, and others) install chargers at their facilities, often in cooperation with CPOs, in order to attract customers to their facilities.

OEMs provide BEV owners access to chargers through their proprietary charging ecosystems (VW We charge, Mercedes Me Charge, Kia Charge, etc.) and enable interaction with charging infrastructure via the vehicle navigation system. They are aided by international software and roaming actors such as Digital Charging Solutions GMBH and enter into bilateral agreements with Norwegian CPOs to obtain access to their charger networks. These OEMs’ strategy is to offer as many chargers as possible through their EMSPs, a strategy opposing that of the integrated CPO/EMSPs that wants to own the customer. For the future, OEMs such as VW, Audi, and BMW will pursue plug and charge in co-operation with Ionity (OEM owned ultra-fast charger CPO).

EV fleet operators (imove, Bilkollektivet, Bildeleringen, MoveAbout, Vy, Hyre, Leaseplan, Easly, Hertz, Avis, and others) rent out BEVs over longer or shorter periods but often leave it to the user to find out how and where to charge. Peer-to-peer charging is explored by some actors (Plugshare, Cloudcharge, ChargeBnB).

Map services such as A Better Route Planner, Google Maps, Ladestasjoner.no, Elbil.no, Opplysningen1881, and others display charger maps and offer route planners. They use the Nobil database of public charging infrastructure. Norwegian and international companies such as Driivz, Current, Virta, and others provide back-office and white label charging infrastructure management software.

The energy retail sector (Fjordkraft, Hafslund Eco, BKK, and others) sells the electricity used for charging. Some also provide charging solutions that allow users to shift charging to off-peak hours (Tibber). Some electricity grid operators install normal and fast chargers locally, often in co-operation with larger CPOs. Finally, there are a number of actors that develop (Zaptec), sell (Fjordkraft), and install chargers (Smartly/lyse, BKK, Kople, etc.) in public parking facilities (Apcoa, Easypark), at workplaces, in apartment buildings (Ohmia charging, Hafslund, Mer), and in private houses (CircleK). Many of these actors are also involved elsewhere in the charging infrastructure ecosystem, for instance, as CPOs and energy retailers.

As the actors within these actor types pursued their individually sound, and in some cases, opposing business models, a complex web of charging infrastructure actors and solutions emerged. While it may make sense for an individual actor to oppose roaming and “own the customer”, the result is a form of “tragedy of the commons” [37] in which the overall system does not take sufficient care of user needs for easy access to and use of the total public charging infrastructure. This is illustrated by the fact that BEV owners in 2022 needed more than 20 apps, e.g., Mer, Bilkraft (Eviny), Fortum Charge and Drive, Circle K charge, Ionity, Kople, E.on drive, Ishavsveien, Vattenfall InCharge, Cloudcharge, Shell Recharge, Elton, Ladeklubben, Apcoa Flow, EasyPark, Bergen parkering, Avinor, Smart charge, Charge365, Plugsurfing, Tesla (from 31 January 2022), and Ladeklubben (from February 2022) to obtain access to all chargers in Norway. The average user has about three apps installed, and 50–70% of surveyed BEV users thought that it is inconvenient to have so many apps (see Section 4.1). Users may also encounter 13 different payment methods [3], including apps, RFID cards, SMS payment, web page payments accessed manually or via QR code scanning, plug and charge, tap to charge, instant payment solution apps (the Norwegian payment solution Vipps) or QR codes, variants of subscription services, payment integration with vehicle navigation systems, and OEMs’ EMSPs. The first CPO that offered bank card payment opened their first station in 2021, but only a few stations have this option, which is highly desired by the users. A large share of the surveyed BEV owners found that the multitude of different payment methods at the different public fast charging stations are inconvenient. BCG [32] found similar issues with apps and payment system complexity in other countries.

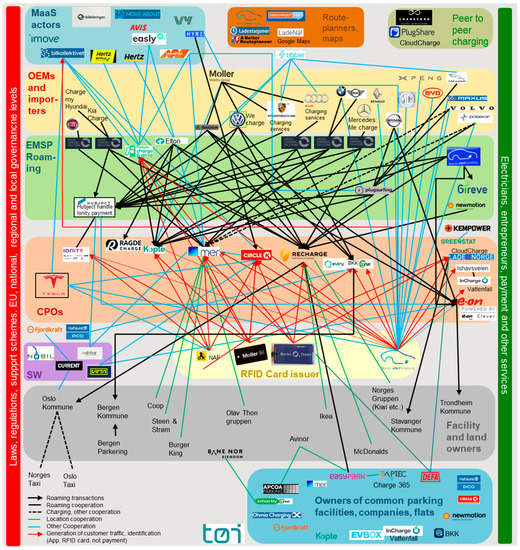

The main actors in the ecosystem are positioned in Figure 5 in relation to each other, and lines show with whom and how they interact through, e.g., roaming transactions, generation of traffic, location cooperation, or other forms of cooperation. The figure shows where the cooperation between actors in different sectors of the ecosystem is most and least extensive, and it provides a good illustration of how something as seemingly simple as charging BEVs involves a very complex business landscape. One of the reasons for the added complexity is that some actors allow roaming while others do not. In fact, several of the largest actors have an opposing strategy to roaming. They want to “own the customer”, as they expect such a strategy to be most profitable. If all CPOs had allowed for roaming, the relationship could be depicted by one line going from each CPO to the roaming hubs, with lines going out to all EMSPs. Instead, there is large variation in the number of lines going from a CPO to the various EMSPs and roaming hubs. Those that do not allow roaming have entered into a number of bi-lateral contracts that provide some users external access to these otherwise closed networks. From the end users’ point of view, the lack of roaming means less interoperability between CPOs, which causes friction if they want to switch between different CPOs and makes the user experience less streamlined.

Figure 5.

The Norwegian charging infrastructure ecosystem. Roaming transactions: thick black line with arrow; roaming co-operation: thick black line; other charging co-operation: stippled thick black line; location co-operation: green line; other co-operation: blue line; generation of customer traffic by co-operation on customer identification (RFID card issuers, etc.): red line with arrow. Source: the authors.

5.3. Promising Business Models in the Norwegian Charging Infrastructure Ecosystem

Wangsness and Figenbaum [3] found that more than 40 business models within the seven parts of the EV charging value chain shown in Figure 1 are currently practiced in Norway. They provided a qualitative evaluation of these business models according to their profitability, scalability, and contribution to the public charging infrastructure, which were the parameters also used by Spöttle et al. [38]. Seven business models were highlighted as particularly interesting, with typical actor examples in parentheses:

- Integrated location owner + CPO + EMSP + charging system supplier for housing cooperatives/condominiums, private households and companies, semi-closed but cooperates with other CPOs (Circle K).

- Integrated CPO + EMSP + charging system supplier for apartment buildings, companies + pop-up charging, open for roaming and also a provider of CPO services under contract for a number of municipalities/counties (Kople).

- Roaming EMSP with map services (Elton).

- Provider of platform solutions for CPOs, EMSPs, installers, electricity producers, and grid companies, which enable operation and management, smart charging, and eventually V2G (current).

- Electricity supplier EMSP (without roaming) + supplier of hardware and software solutions for charging at homes, housing cooperatives/condominiums, workplaces, and destinations (Fortum Charge and Drive).

- Integrated CPO + EMSP + charging system supplier for apartment buildings and companies, semi-closed. Can also be an asset owner, and in some cases a site owner (Mer and BKK).

- Manufacturer of hardware and software—all segments (up to 22 kW AC) (Easee and Zaptec). These actors mainly produce chargers for home and parking facilities.

The first six business models are discussed further below as they are most relevant for the user experience associated with charging away from home.

It is highlighted in several places in the reviewed literature, e.g., Pagani et al. [39], PwC [36], Schroeder and Traber [29], and Zhang et al. [22], that much of the profit potential in the charging market will come from being able to combine several revenue streams. Circle K is doing just that. Their energy stations make money from BEVs charging there, where they act as both CPO and EMSP for several of the charging stations. With larger volumes to their energy stations, they draw greater revenue from the retail part of the business (food etc.). In addition, they sell hardware, software, and support solutions to homes, for apartment buildings, property developers, and workplaces.

Kople also has a business model that stands out. They act as a “turnkey provider” for apartment buildings, workplaces, and destinations (hotels, shops, etc.) and an “end-to-end integrator” as owner, CPO, and EMSP for its charging network with normal, fast, and ultra-fast chargers. Their charging network is also open for roaming, which means that they contribute to a larger charging network for their customers and other networks’ customers.

Although the reviewed literature does not often refer to aggregators/roaming hubs, they are sometimes highlighted as a promising business model, for instance by the Boston Consulting Group [26] and Capgemini [35]. Elton’s business model is interesting in this respect. After a few months of developing the solution, it became possible to use their platform and app to roam between major players such as Ionity, Recharge, and Kople in both Norway and Sweden, with the possibility to search for the fastest and cheapest charging option in the app.

Vehicle-to-grid (V2G) services are considered to have a very high revenue potential according to ADL [34] and Bland et al. [40]. In the Norwegian ecosystem, Current stands out. In addition to providing platform solutions to CPOs, EMSPs, installers, power producers, and grid companies, as well as enabling operation and management of charging services, the Current platform also supports smart charging and V2G functionality. Current provides software solutions to several stages of the value chain and several charging segments that support roaming through open standards (where they also offer certification), smart charging, and V2G.

Fortum Charge and Drive is also an interesting business model as a large EMSP that is also an electricity retailer that sells home charging equipment. Fortum is thus close to having an “end-to-end energy” business model with multiple revenue streams, but without having to take the risk with the investment and operation of hardware, which a CPO must do. Fortum Charge and Drive was an integrated CPO/EMSP until the CPO part was spun off as “Recharge” in 2020.

It will be interesting to follow the business model of more closed CPOs that do not offer roaming in general but cooperate with some OEMs and see if they manage to grow while retaining a firm grip on their customers. In the Norwegian ecosystem, Mer and Eviny (previously BKK) stand out. If they manage to deliver a large enough stand-alone network to their customers and ensure loyalty and bring in new customers through their large presence, it is possible that they will be more profitable than if they had chosen a more open strategy with roaming. Their current strategy also enables bilateral agreements that open the network to specific groups.

The position of these actors in the value chain is shown in Table 2, together with a selection of other Norwegian actors.

Table 2.

Selected actors positioning in the charging infrastructure value chain (see Figure 1).

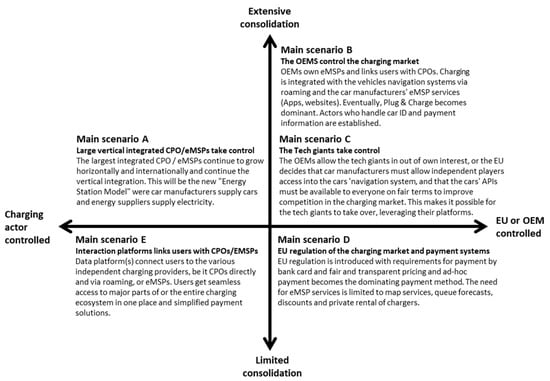

5.4. Scenarios for the Future

Time will tell which business models will deliver on long-term profitability and scalability while meeting user needs. The ecosystem for BEV charging is developing rapidly and there is great uncertainty about what this ecosystem will look like in, e.g., 5–10 years. Differences in the relative strength of different economic drivers (e.g., technological developments, regulation, or customer loyalty to incumbents) will lead to different futures for this ecosystem and different results for the end-user experience. In such instances, it is useful to construct a set of scenarios for the different directions the ecosystem can take. A total of 10 different scenarios were identified during and following an internal project workshop. All these scenarios are described and discussed in more detail in a report by Wangsness and Figenbaum [3]. For the purpose of this article, the 10 scenarios are summarized briefly below:

- Business-as-usual (BAU) with many and probably increasing number of players. Voluntary roaming is limited, and none of the CPO networks are large enough by themselves so that BEV drivers can get by with only one user interface on a long trip to a new destination. New actors joining will lead to increased user complexity by adding more apps and payment solutions to the overall system. The user needs for simple and efficient charging analyzed in Section 5.1 will thus not be met.

- Consolidation into large, vertically integrated semi-closed CPOs. The least profitable CPOs have dropped out of the market or merged with the large remaining ones that grow alongside the BEV market. They tend to have a large horizontal (multiple charging customer segments) and vertical coverage (e.g., energy retail and energy stations with convenience products). This scenario will function better for users than the BAU. The number of actors will be reduced, and each actor will have a larger network. Given their size, some users may only need to use one network.

- Interaction and roaming platforms connect charging infrastructure players with charging customers. Interaction and roaming platforms gain enough volume so that it becomes hard for the “stubborn” CPOs and EMSPs to “lock in” their customers by refusing roaming. This scenario will allow users to virtually interact with only one app to gain access to multiple CPOs networks, as Elton is today on a small scale. This development would improve the user-friendliness of charging but can be more costly for the user as the platform will add a small cost to the transaction.

- “The people want to roam freely!” Roaming becomes the industry standard. Preferences of both charging customers for maximal roaming possibilities and site owners for maximal volumes will favor CPOs that agree to roaming and put pressure on the CPOs that follow a more closed strategy. Charging will be more easily accessible for users but may be slightly more costly due to the roaming charges.

- Car manufacturer (OEM)-controlled future with charging integrated into the car’s navigation system. OEMs will directly or indirectly provide EMSP services through the cars’ navigation system, as a part of their expanded service portfolio. Such services will increase in relative importance, as revenue from vehicle maintenance services will decline. OEMs will have leverage to obtain seamless access to CPO networks and even be a force pressuring for expanded roaming possibilities. This scenario will significantly improve the user-friendliness of charging.

- Plug and charge—the cars identify themselves automatically and payment is seamless. Some OEMs and CPOs will lead the way towards increased use of plug and charge in order to compete with the customer experience of Tesla, which already offers this service. Plug and charge will make it much easier to charge where it is enabled, but may not work on all chargers, at least in a long switchover period. The potential for improved user-friendliness is very large, but in an early transition period it may add complexity by becoming yet another solution for identification and payment.

- Regulation requires a splitting into separate CPOs and eMSPs. In order to ensure more competition and less “lock-in” of customers, regulators require in this scenario that CPOs and EMSPs are separate companies and require CPOs to provide fair access to all EMSPs. This scenario will be similar for users, like scenario 4. The difference is how it comes about.

- BEVs obtain a longer range that allows charging mainly at home and at destinations. Fast charging will in this scenario be of less relative importance compared to home and destination charging, which is much cheaper. There will be a strong growth in destination charging, “become-your-own-CPO-solutions”, and peer-to-peer charging solutions. For users, this will be a simplification as charging issues will be encountered less frequently and long-distance driving will be easier.

- The EU sets the standard for ensuring seamless charging across national borders in Europe (including Norway). The regulation will make ad hoc payment simpler, likely with bank/credit cards, as well as more transparent, and it will allow BEV users to be anonymous. It will reduce the need for EMSPs. It also reduces CPOs’ ability to “lock in” customers, but other user-friendliness issues such as different plugs, power levels, and charging interfaces will remain.

- The technology giants take over. Tech giants (e.g., Google and Apple) have become the dominant EMSPs as they provide services through products the charging customer already uses, i.e., the smart phone. These tech giants have payment solutions and ample amounts of data for prediction of real-time traffic conditions to fine tune their services already. OEMs will have strong incentives to give the tech giants’ platforms access to their navigation systems. This scenario can provide BEV owners with services not available to ICEV owners, such as real-time info about the likelihood of queues when needing to charge on the basis of data they already use for travel time prediction.

The five most likely scenarios (the authors’ assessment) were analyzed further, as shown in Figure 6, and differentiated across the degree of consolidation in the market and whether the market development is steered from charging actors or external actors. The customer experience compared to BAU will improve to a variable degree in these scenarios. It can be useful to have a mix of main scenarios A and B in mind when making a strategy in the BEV charging infrastructure ecosystem, as these scenarios exemplify outcomes of the battle between the large integrated CPOs/EMSPs and OEMs regarding the control of the charging market. Both of these types of actors need to be aware of the snowball effect of an increasing number of players and platforms offering e-roaming connected together by network orchestrators and interaction platforms as in scenario E. Tech giants can also be in the lead if they gain access to the navigation systems/vehicle displays as in scenario C. Better customer experiences can also be achieved through regulation of the market as in scenario D. EMSPs can in scenario D become less needed if fair pricing is required for drop-in customers and if unified payment systems that do not require user registration become mandatory. Authorities may need to pursue such regulations if the market actors themselves cannot establish an overall acceptable customer experience, through voluntary roaming, co-operation, or consolidation.

Figure 6.

Main scenarios for the future of the Norwegian charging market. Source: the authors.

6. Discussion and Conclusions

The user needs for and experiences with charging infrastructure, the motivations and strategies of the business actors that delivers these services to users, and the ability of the overall charging infrastructure ecosystem to meet the user needs were investigated. Combined, the analyses enable an understanding of how the Norwegian charging infrastructure system evolved, how it now works, and how it is likely to evolve in the future with and without interventions and how this will or will not meet user needs.

6.1. Considering Developments up to 2021

The Norwegian BEV market has been built up organically over 30 years with incentives for purchase and use of BEVs [4,8,9], which created a large and competitive market. The same applies to the deployment of public charging infrastructure, which started from 2009. Enova, Transnova, and counties and municipalities have provided economic support for charging infrastructure deployment, requiring only a minimum of technical standards and that at least one common payment system was available, without specifying which. Within the terms of these public support schemes and tenders, actors pursued their business models, competed with other actors, and developed their own payment and user interface solutions from scratch. This development started when BEVs had small batteries and each charging session had a low value. Low transaction cost and basic user interface systems were therefore prioritized over user-friendliness. Many different payment solutions were pursued, and each actor developed their own app for access and payment. While this approach likely enabled installation of more chargers early on, the large number of individual actors with a variety of incompatible strategies, solutions, payment systems, and apps has become a major challenge for BEV users [21,41,42], as also seen in other countries [32]. The total charging infrastructure network has expanded significantly, i.e., as the sum of all the CPO networks, but the overall system has not become intuitive or simple to use for BEV owners. Major reasons for the lack of user-friendliness are that roaming is only offered by a few actors and that credit/debit card payment is not available apart from at some test stations. To try to make charging easier, various patches have been introduced such as the use of RFID cards for identification at charging stations and various map services providing an overview of the total offering. Large actors have refused to open their charging networks for roaming as they want to keep their customers exclusively in their networks, believing that this will generate more profit for them. The way the market functions is thus a result of how individual actors have followed their individually sensible business models and used their market power for their own benefit. This is an example of the classic “tragedy of the commons” dilemma.

Survey and interview results shows that many BEV users as a result of these developments experience several issues when using public fast chargers. The lack of user-friendliness and the lack of standardized payment systems across operators are important disadvantages that may become a barrier to future BEV adoption. According to a survey by the Norwegian EV Association, 88% of current BEV owners want a simpler universal system that is independent of which company that operates the charging station [41]. More than 70% of BEV owners want to pay for charging with a credit/debit card [41]. Findings from the present study are consistent with these results.

Recent years have shown consistent improvements to the fast charger network, particularly in terms of availability [13,16]. However, findings from the present study suggest that there is still a long way to go in terms of user-friendliness. As BEV market shares increase and BEV buyers are becoming the majority car buyers [4], the need for a more user-friendly experience will become pressing. Standardization can increase the overall user-friendliness by

- Standardizing the payment method. The same type(s) of payment methods should be available at all stations. Preferably, it is one common app for all charging stations, as well as easy options for drop-in clients (debit/credit card option).

- Standardizing the pricing system. The price should be clearly marked, and the pricing system should be easily comparable between different charging stations (without having to download an app).

- Standardizing the charging operation (user-friendliness). Available user information, placing of charging cables to fit all vehicle models, method for starting the charging, etc. Universal design at fast charging stations (easy use independent of nationality, technological skills, or disabilities).

- Standardizing the level of amenities at fast charging stations along the major highway network, such as, for instance, toilets, light, garbage bins, road signs, roof, etc.

There has been no progress on the standardization of payment systems, which could solve many of the issues that BEV users are experiencing today. Access to a universal app for use of and payment for chargers would for instance have solved the issue of having to install many apps and interface with a multitude of payment systems. It would particularly simplify identification and payment for those using public chargers occasionally. Moreover, a universal app could also provide users with accurate and simpler price information, regardless of service provider. Large actors have refused to provide external actors access to their networks, which so far has made a universal user-friendly solution impossible. Elton and the EV Association’s “Ladeklubben” have developed such solutions on a small scale with a handful of CPOs that support roaming. Another improvement would be to make payment with credit/debit card standard. This payment option is only tested out in a handful locations, but findings from the current and other studies [21,41,42] imply that most BEV users would like to have this option. The EU [43] is considering standardizing this payment method at public charging stations. For charging at 50 kW and more, the EU’s preliminary plan is to require payment card readers at all charging stations by 2027 (or a contactless solution). Other methods to simplify the existing authentication and payment methods discussed in Norway [21] are to use the toll road AutoPass chip or a type of ANPR (automatic number plate recognition) system.

It was up until 2022 difficult for BEV owners to obtain an overview of the price of charging. Different operators used different pricing systems, i.e., paying for minutes, paying for kWh, or a combination of both. The price of charging also varied depending if you were a drop-in customer or a registered customer of the operator. Drop-in customers typically paid two times more with SMS messaging than those registered as customers and using an app or RFID card [21]. The pricing system became more standardized during 2022. All actors now price charging in NOK per kWh charged, which is what the users have wanted, and the added cost of charging for unregistered customers has been reduced.

Standardization of the charging access, which is important for the user-friendliness of charging, has not progressed much apart from better and more accessible user information [21]. There are also issues regarding universal access [21]. The chargers must according to Norwegian law be accessible for people with disabilities, which requires more space around the vehicle and charger for wheelchair users. Such requirements can be difficult to meet as the chargers were often installed in narrow parking spaces and because of the need to install barriers to protect cables and chargers from being hit by vehicles [44]. The operators have focused on expanding the number of chargers, at the expense of universal access [44,45], but a standard for universal charging access is being developed [21]. In Norway, many of the BEV owners only use public chargers 1-3 times a year [13,19,20], which makes it important that the user information at the charging stations is available (in both Norwegian and English) and is easy to understand for inexperienced users. The EU [43] is planning to include regulation for accessible user information, traffic signs, and information on prices in the updated version of Directive 2014/94/EU.

Customers generally want the same amenities at charging stations as at petrol stations. For long-distance travelers, the following amenities are especially important [19,21,30]: toilets, cover/roof protecting for rain/snow, access to a food vendor or a café, resting areas, garbage bins, 24/7 service, and access to water for window washing. Most fast chargers have therefore been installed in existing parking spots [44,45] at fuel stations, cafés, restaurants, food stores, and shopping centers. Having such amenities available is not just a question of providing a better user experience, it also enables more revenue streams related to the vehicle charging that could add positively to the overall return on investment in charging infrastructure. These locations also have electricity available already, which can reduce the cost of installing chargers.

6.2. Future Developments and Furter Research

The direction the charging infrastructure ecosystem will evolve in if no regulation is put in place is not clear. Business as usual will likely increase the overall complexity as new actors will join with different degrees of cooperation and interoperability with existing providers of charging solutions. It would likely lead to even more apps and varieties of access and payment systems and be less desirable for users wishing to obtain simpler access to chargers. Business as usual is unlikely to continue long into the future. Consolidation of CPOs and EMSPs into larger and fewer actors is a scenario that can reduce the user complexity, but users may still need to establish customer relations with several operators to obtain full access everywhere. OEMs have a key role by controlling the vehicle navigation system and may thus be able to force the charging infrastructure actors to realign. In other scenarios, integrated CPO and EMSPs may need to be split into separate entities through regulation to make it possible for OEM EMSPs and independent EMSPs to offer a large share of the chargers through their service. This has advantages in terms of transparency and simplicity under normal operation. Furthermore, tech giants such as Google or Apple may disrupt the charging infrastructure market by linking their map services that have real-time traffic flow data, to charger status data and access control, and integrate that with their existing payment systems (e.g., Google pay, Apple pay), in order to offer an advanced EMSP service with real-time queue predictions and routing options to less used chargers.

Charging infrastructure for heavy-duty trucks will also be an important development for the EV charging ecosystem. Developers of such infrastructure and government support agencies should learn from the Norwegian experiences with BEV charging infrastructure. They should, for instance, agree on one common standard, and roaming should be a requirement from the outset. The charging transactions will be much larger than for BEVs due to the larger batteries (currently about 2-6 times larger than the largest BEVs). The added cost of roaming charges will be small compared to the transaction value, so there is little reason not to plan for and demand roaming. Moreover, the value of time for a trucking operation is a great amount higher than for an average passenger car driver, implying high demand for smooth charging operations with low time use. Truck charging infrastructure will also need to be utilized fully, due to the large surface areas and high-power levels required for truck charging. The truck infrastructure should be separate from that of passenger cars and light commercial vehicles so that trucks do not block several chargers when charging at the infrastructure put in place for BEVs. This is already an issue with trucks with CCS charge inlets [46]. CharIn is working on the MegaWatt charging system (MCS) for trucks, and a prototype of the connector design allowing for up to 3.7 MW charging was demonstrated at the 35th World Electric Vehicle Symposium in Oslo in June 2022 [47].

There are many ways to extend the research on the charging infrastructure users, actors, and ecosystem. Further research can, for instance, expand the analysis of the user needs with real charger transaction data, and of the ecosystem with financial data from the businesses operating in the ecosystem. Even if financial data at the desired level of detail are not available, official (more aggregated) financial data may over time say something about the magnitudes and development of importance within the ecosystem. Since this ecosystem is a rapidly evolving, it is of great interest to follow, document, and analyze the changes taking place. This will enable a better understanding of the ecosystem dynamics and make it possible to learn from the success factors and pitfalls in the transition to a fully electrified transport sector.

6.3. Caveats

The ecosystem for EV charging is complex. The qualitative assessments in this article have provided a holistic overview of charging of BEVs in Norway but are subject to uncertainty. The data for this article were collected until the end of 2021, so the article does not consider developments in 2022. Some important developments in Norway during 2022 were that

- Tesla opened on 31 January a total of 15 locations and 315 charge points for non-Tesla owners, which was expanded to 58 locations and 812 charge points on 3 May. Non-Tesla owners must, however, use yet another app to gain access, and not all BEVs can use Tesla chargers due to the positioning of the charge inlet and the length of the cables.

- The EV Association launched their roaming EMSP service “Ladeklubben” (Charging club) on 17 February. A blue RFID card provides access to charging at Recharge, Kople, Ionity, E.on, and Powered by E.on, providing access to 275,000 chargers across Europe.

- The popular Norwegian instant payment service “Vipps” became more common as Mer and Eviny also took it into use during 2022.

- Pricing became standardized during 2022. All the large CPOs and EMSPs now charge in NOK per kWh.

Author Contributions

Conceptualization, E.F., P.B.W., A.H.A. and V.M.; methodology, E.F., P.B.W., A.H.A. and V.M.; survey software, QuenchTec; validation, E.F., P.B.W., A.H.A. and V.M.; formal analysis, E.F., P.B.W., A.H.A. and V.M.; investigation, E.F., P.B.W., A.H.A. and V.M.; resources, E.F.; survey data curation, A.H.A.; writing—original draft preparation, E.F., P.B.W., A.H.A. and V.M.; writing—review and editing, E.F., P.B.W., A.H.A. and V.M.; visualization, E.F., P.B.W., A.H.A. and V.M.; supervision, E.F.; project administration, E.F.; funding acquisition, E.F. All authors have read and agreed to the published version of the manuscript.

Funding

The research was funded by the Research Council of Norway, through the Spot-on project (grant no. 321090), with a small contribution from the MoZEES FME (grant no. 257653).

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki, and approved by the Ethics Committee of the Norwegian Agency for Shared Services in Education and Research (protocol code NSD 976704, 4 May 2021).

Informed Consent Statement

Informed consent was obtained from all the anonymous subjects involved in the study.

Data Availability Statement

Not applicable.

Acknowledgments

The authors wish to thank the partners of the Spot-on research and innovation project, e.g., Powerzeek, Bouvet, NAF, Q-Free, Know-it, Kluge, and ITS-Norway, for their constructive comments and co-operation on interviews with the charging infrastructure actors and BEV owners.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Amundsen, A.H.; Milch, V. Demand for standardization of public fast charger stations—User perspectives. In Proceedings of the 35th International Electric Vehicle Symposium and Exhibition (EVS35), Oslo, Norway, 11–15 June 2022. [Google Scholar]

- Figenbaum, E.; Wangsness, P.B. The Norwegian Charging Infrastructure Ecosystem. In Proceedings of the 35th International Electric Vehicle Symposium and Exhibition (EVS35), Oslo, Norway, 11–15 June 2022. [Google Scholar]

- Wangsness, P.B.; Figenbaum, E. The Charging Market—Complex and Dysfunctional or Future-Oriented? TOI Report (in Norwegian) 1867/2022. Institute of Transport Economics, September 2022. Available online: https://www.toi.no/publications/the-charging-market-complex-and-dysfunctional-or-future-oriented-article37371-29.html (accessed on 27 September 2022).

- Figenbaum, E. Norway—The World Leader in BEV Adoption. In Who’s Driving Electric Cars. Lecture Notes in Mobility; Contestabile, M., Tal, G., Turrentine, T., Eds.; Springer: Cham, Switzerland, 2020. [Google Scholar] [CrossRef]

- IEA. Norway (Electromobility Status 2022). In The Electric Drive Charges Ahead. IEA HEVTCP Annual Report 2022. 2022. Available online: https://ieahev.org/wp-content/uploads/2022/05/DIGITAL-HEVTCP_2022_Annual_Report_Final-with-Cover.pdf (accessed on 1 August 2022).

- Statistics Norway, to Av Tre Nye Personbiler er Elbiler. Available online: https://www.ssb.no/transport-og-reiseliv/landtransport/statistikk/bilparken/artikler/to-av-tre-nye-personbiler-er-elbiler (accessed on 25 April 2022).

- OFVAS. Car Sales Statistics. Bilsalget i JUNI 2022 (og Første Halvår 2022). OFV AS. 2022. Available online: https://ofv.no/bilsalget/bilsalget-i-juni-2021-2-2 (accessed on 1 August 2022).

- Figenbaum, E. Retrospective Total Cost of Ownership analysis of Battery Electric Vehicles in Norway. Transp. Res. Part D 2022, 105, 105103246. [Google Scholar] [CrossRef]

- Figenbaum, E. Perspectives on Norway’s supercharged electric vehicle policy. Environ. Innov. Soc. Transit. 2017, 25, 14–34. Available online: http://www.sciencedirect.com/science/article/pii/S2210422416301162 (accessed on 22 March 2022). [CrossRef]

- Figenbaum, E. The 1990 to 2020 Technology Innovation System supporting Norway’s BEV revolution. Working Paper. 19 March 2022. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4061401 (accessed on 10 August 2022).

- Ministry of Transport. National Transport Plan 2022–2033. Oslo. 2021. Available online: https://www.regjeringen.no/en/topics/transport-and-communications/content-2021/national-transport-plan-20222033/id2866098/ (accessed on 10 January 2022).

- Government. UNFCCC Paris Agreement. Norway’s First NDC 2016. Norway’s Nationally Determined Contribution to the Paris Agreement. 20 June 2016. Available online: https://unfccc.int/sites/default/files/NorwayINDC.pdf (accessed on 27 September 2022).

- Figenbaum, E.; Nordbakke, S. Battery Electric Vehicle User Experiences in Norway’s Maturing Market. TØI Report 1719/2019. Available online: https://www.toi.no/publications/battery-electric-vehicle-user-experiences-in-norway-s-maturing-market-article35709-29.html?deviceAdjustmentDone=1 (accessed on 10 May 2022).

- Fevang, E.; Figenbaum, E.L.; Halse, A.H.; Hauge, K.E.; Johansen, B.J.; Raaum, O. 2021. Who goes electric? The anatomy of electric car ownership in Norway. Transp. Res. Part D 2021, 92, 102727. [Google Scholar] [CrossRef]

- Hardman, S.; Jenn, A.; Tal, G.; Axsen, J.; Beard, G.; Daina, N.; Figenbaum, E.; Jakobsson, N.; Jochem, P.; Kinnear, N.; et al. A review of consumer preferences of and interactions with electric vehicle recharging infrastructure. Transp. Res. Part D 2018, 62, 508–523. Available online: https://www.sciencedirect.com/science/article/pii/S1361920918301330 (accessed on 27 September 2022). [CrossRef]

- Figenbaum, E. Electromobility status in Norway: Mastering Long Distances—The Last Hurdle to Mass Adoption. TØI Report 1627/2018. Institute of Transport Economics. 2018. Available online: https://www.toi.no/publications/electromobility-status-in-norway-mastering-long-distances-the-last-hurdle-to-mass-adoption-article34903-29.html (accessed on 27 September 2022).

- Bjerkan, K.Y.; Nørbech, T.E.; Nordtømme, M.E. Incentives for Promoting Battery Electric Vehicle (BEV) Adoption in Norway. Transp. Res. Part D 2016, 43, 169–180. [Google Scholar] [CrossRef]

- Figenbaum, E.; Kolbenstvedt, M. Learning from Norwegian Battery Electric and Plug-In Hybrid Vehicle Users. Results from a Survey of Vehicle Owners. TØI Report 1492/2016. Institute of Transport Economics. Available online: https://www.toi.no/publications/learning-from-norwegian-battery-electric-and-plug-in-hybrid-vehicle-users-results-from-a-survey-of-vehicle-owners-article33869-29.html (accessed on 27 September 2022).

- Ydersbond, I.M.; Amundsen, A.H. Fast Charging and Long-Distance Driving by Electric Cars in Inland Norway, ISBN 978-82-480-2148-3, TOI Report 1775, Oslo, Institute of Transport Economics. 2020. Available online: https://www.toi.no/publications/fast-charging-and-long-distance-driving-by-electric-cars-in-inland-norway-article36311-29.html (accessed on 27 September 2022).

- Figenbaum, E. Battery electric fast charging—Evidence from Norwegian market. World Electr. Veh. J. 2020, 11, 38. [Google Scholar] [CrossRef]

- Norwegian Environment Agency & Norwegian Public Road Association. Kunnskapsgrunnlag om Hurtigladeinfrastruktur for Veitransport. Oslo. 2022. Available online: https://www.regjeringen.no/contentassets/a07ef2d3142344989dfddc75f5a92365/kunnskapsgrunnlag_1mars.pdf (accessed on 27 September 2022).

- Zhang, Q.; Li, H.; Zhu, L.; Campana, P.E.; Lu, H.; Wallin, F.; Sun, Q. Factors influencing the economics of public charging infrastructures for EV—A review. Renew. Sustain. Energy Rev. 2018, 94, 500–509. Available online: https://www.sciencedirect.com/science/article/abs/pii/S136403211830460X (accessed on 27 September 2022). [CrossRef]

- Greene, D.L.; Kontou, E.; Borlaug, B.; Brooker, A.; Muratori, M. Public charging infrastructure for plug-in electric vehicles: What is it worth? Transp. Res. Part D Transp. Environ. 2020, 78, 102182. Available online: https://www.sciencedirect.com/science/article/abs/pii/S1361920919305309 (accessed on 27 September 2022). [CrossRef]

- de Rubens, G.Z.; Noel, L.; Kester, J.; Sovacool, B.K. The market case for electric mobility: Investigating electric vehicle business models for mass adoption. Energy 2020, 194, 116841. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0360544219325368 (accessed on 27 September 2022). [CrossRef]

- van der Kam, M.; van Sark, W.; Alkemade, F. Multiple roads ahead: How charging behavior can guide charging infrastructure roll-out policy. Transp. Res. Part D Transp. Environ. 2020, 85, 102452. Available online: https://www.sciencedirect.com/science/article/pii/S1361920920306398 (accessed on 10 August 2022). [CrossRef]

- Boston Consulting Group. Winning the Battle in the EV Charging Ecosystem. BCG. 2021. Available online: https://www.bcg.com/publications/2021/the-evolution-of-charging-infrastructures-for-electric-vehicles (accessed on 9 June 2021).

- Deloitte. Hurry up and… Wait: The Opportunities Around Electric Vehicle Charge Points in the UK. 2019. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/energy-resources/deloitte-uk-Electric-Vehicles-uk.pdf (accessed on 21 January 2021).

- Helmus, J.; Van den Hoed, R. Key performance indicators of charging infrastructure. World Electr. Veh. J. 2016, 8, 733–741. Available online: https://www.mdpi.com/2032-6653/8/4/733 (accessed on 10 August 2022). [CrossRef]

- Schroeder, A.; Traber, T. The economics of fast charging infrastructure for electric vehicles. Energy Policy 2012, 43, 136–144. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0301421511010470 (accessed on 10 August 2022). [CrossRef]

- Pöyry 2012a. Strategi og Kriteriesett for Utplassering av Hurtigladere (del 1). Utarbeidet for Transnova og Statens Vegvesen. Pöyry Rapport R-2012-007. Available online: https://docplayer.me/1090511-Strategi-og-kriteriesett-for-utplassering-av-hurtigladere-del-1-utarbeidet-for-transnova-og-statens-vegvesen-r-2012-007.html (accessed on 10 August 2022).

- Pöyry 2012b. Alternative Forretningsmodeller for Etablering av Hurtigladestasjoner—Del 2. Available online: https://www.osti.gov/etdeweb/servlets/purl/22000205 (accessed on 10 August 2022).