Features and Scope of Regulatory Technologies: Challenges and Opportunities with Industrial Internet of Things

Abstract

1. Introduction

2. Current Supervisory or Regulatory Technologies

2.1. Definition of Several Concepts: Fintech, RegTech, SupTech

2.1.1. FinTech

- Fintech needs a practical and systematic framework.

- A stable and efficient public infrastructure and trust in the payment system are required for public policies.

- Absolute regulation may not be suitable or effective enough for Fintech.

- Significant data protection issues are caused by the use of big data and new technologies.

- knowledge of the success factors of equity crowdfunding open to non-accredited investors.

- Issues in secure data storage and processing.

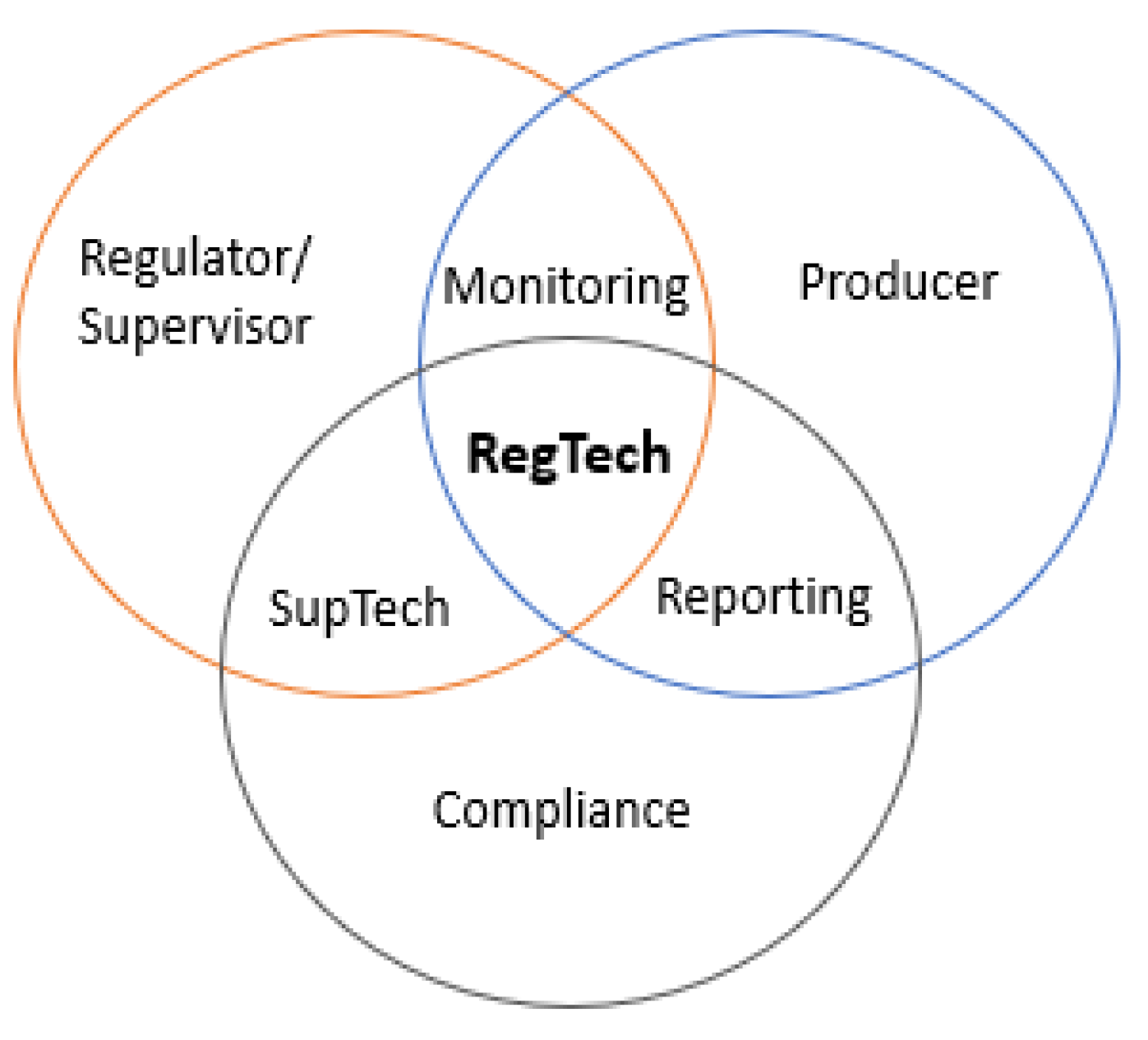

2.1.2. RegTech

2.1.3. SupTech (RegTech for Supervisors)

2.2. Three Stages of RegTech Development

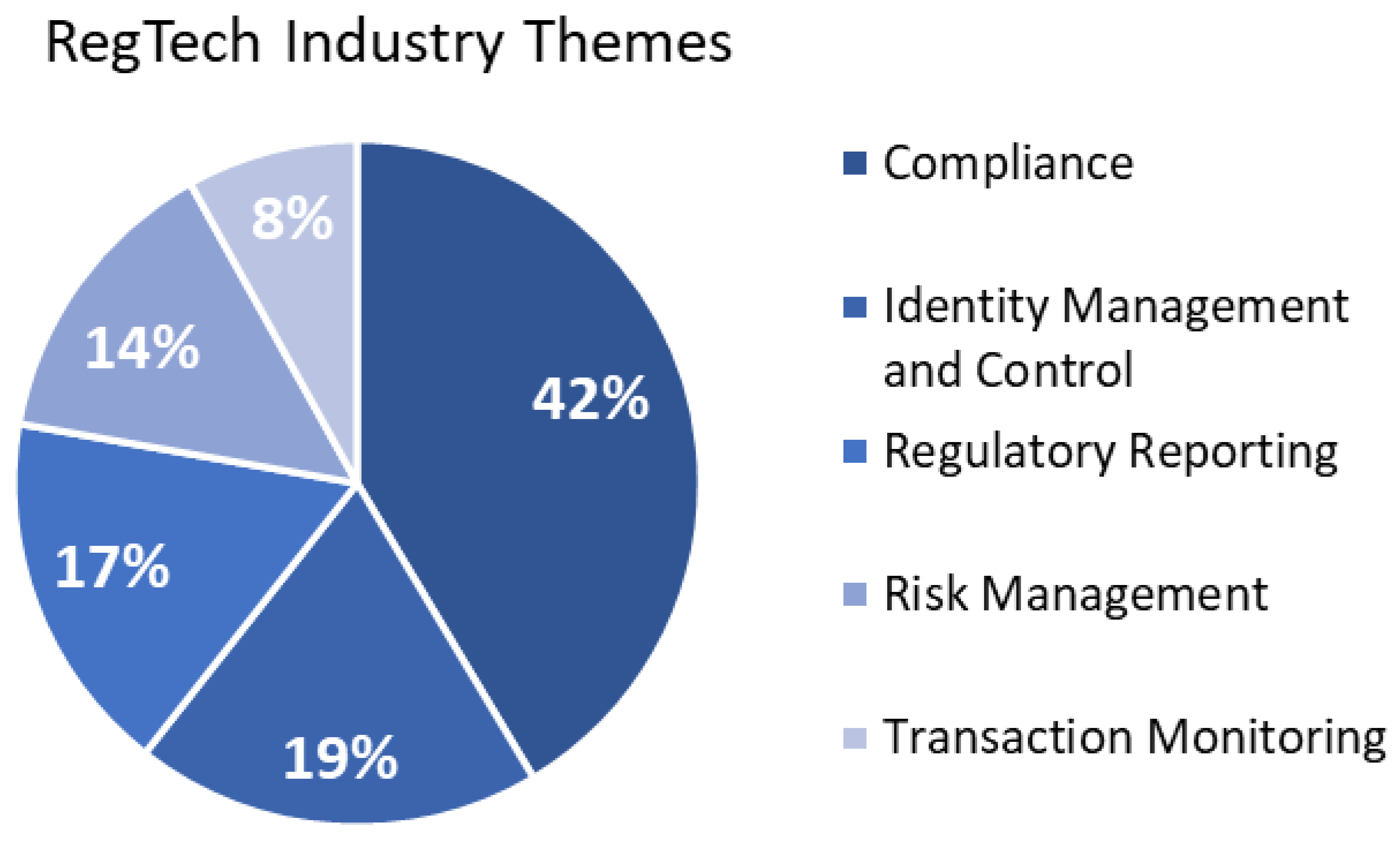

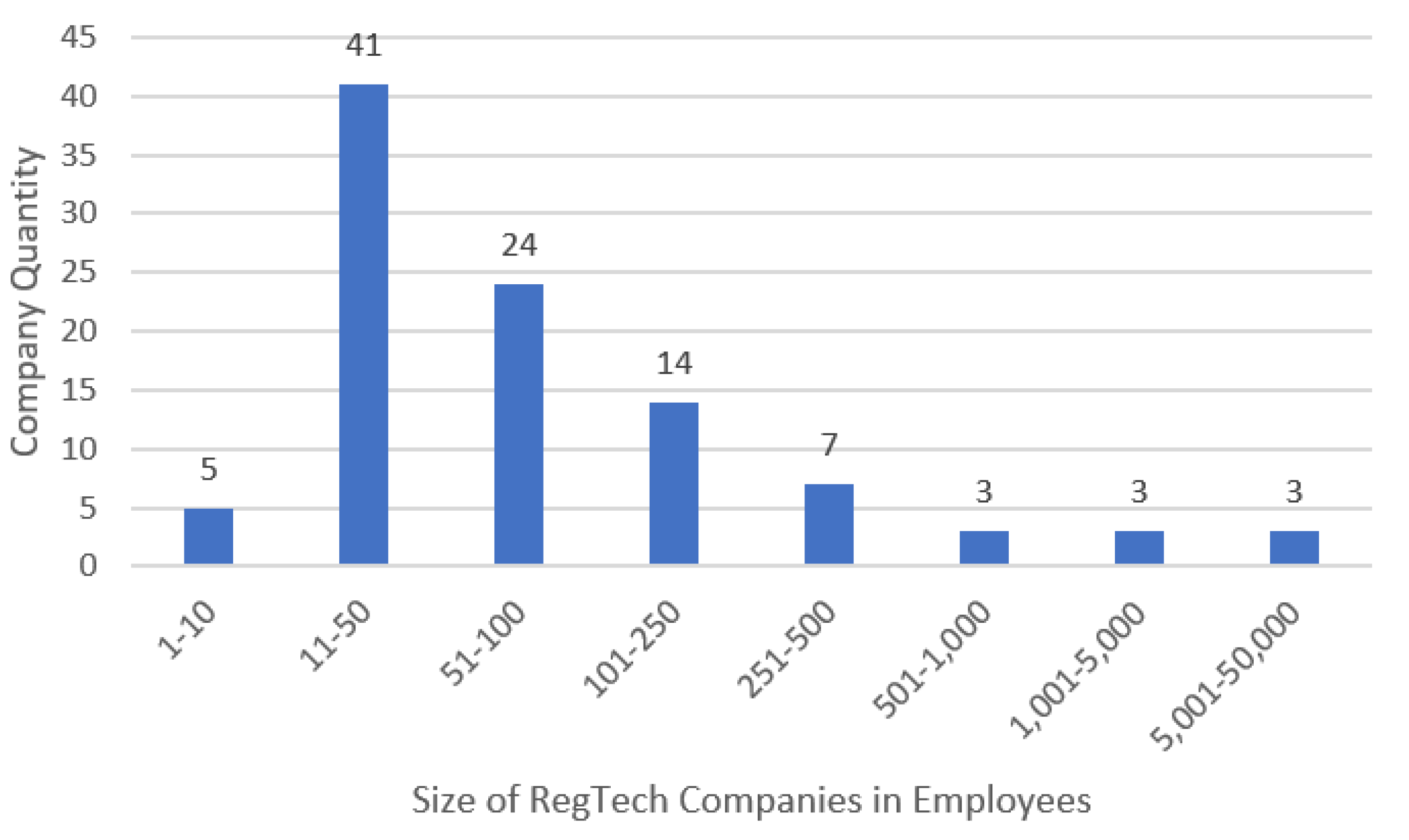

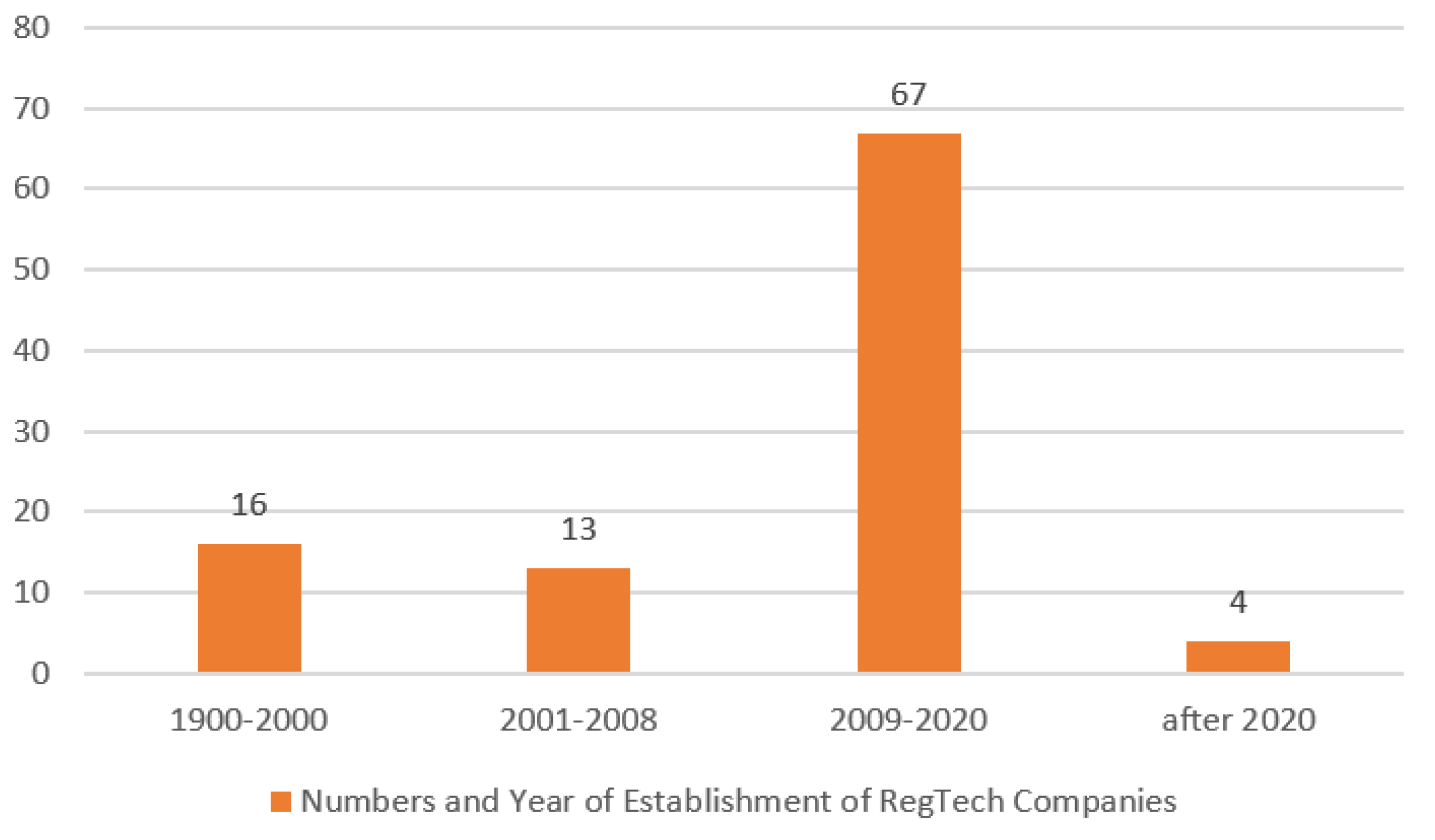

2.3. Current Development of RegTech and Existing Applications

2.4. Existing RegTech Applications

- Digital Transformation and Automation (by “Profinch”)

- Market surveillance (by “Solidus Labs”)

- Web3 scam prevention (by “Solidus Labs”)

- Web3 Intelligence and Forensics (by “Merkle Science”)

- Blockchain Analytics and Investigations (by “Coinfirm”)

- Data Privacy (by “Enveil”)

- Taxation Reporting (by “MAP FinTech”)

- Trade Surveillance (by “MAP FinTech”)

- Staff Compliance (by “U-Reg”)

- Data Exchange (by “U-Reg”)

- Contract Lifecycle Management (by “SignDesk”)

- eSignature (by “SignDesk”)

3. Fundamental Technologies for RegTech

3.1. Features

- Collaboration: RegTech solutions often require collaboration between different stakeholders, such as regulators, industry associations, and technology providers. This can help promote innovation and best practices in regulatory compliance [34].

3.2. Tools

- AI and Machine Learning: AI is an advanced technology that can perform tasks in areas that require human intelligence with the implementation and development of computer systems, including a broad range of techniques, algorithms, and methodologies that enable computers to mimic or simulate human intelligence. It involves creating intelligent machines that can perceive, reason, learn, and problem-solve in ways similar to or surpassing human capabilities [35]. For example, the AI-based scoring system is more objective in making credit decisions more precise and reasonable without bias and with brilliant fraud detection, no matter how sophisticated or complex the regulations are [36]. In addition, AI plays an incredible role in complying with the General Data Protection Regulation (GDPR) [37,38], the European Data Protection Law that aims to protect personal information. For instance, Aigine offers a tool based on AI to detect personal data from various sources, including structured or unstructured files such as emails or notes, to handle the challenge of unstructured personal data through four stages: filtering, highlighting, assessing, and documenting [16]. Machine learning is a subset of AI that focuses on algorithms and models that enable computers to learn from and make predictions or decisions based on data. It involves training computer systems to automatically improve performance on a specific task through experience and without explicit programming.

- Blockchain: Blockchain technology can improve transparency and traceability in compliance processes. For example, it can be used to create tamper-proof records of transactions and improve the audit trail [39,40,41]. Blockchain technology has several potential applications in RegTech, primarily due to its ability to provide an immutable and transparent record of transactions.

- Natural Language Processing: NLP can analyze unstructured data, such as text documents, to identify and flag potential compliance issues [42].

3.3. Policies and Standard Operating Procedures

- Know Your Customer: Blockchain can be used to create a decentralized and secure identity verification system that allows customers to prove their identity without the need for intermediaries. This can streamline the KYC process for financial institutions while maintaining data privacy and security [53,54].

- Regulatory Reporting: Blockchain can be used to create a secure and transparent audit trail of regulatory reports, making it easier for regulators to monitor compliance and identify potential issues. This can potentially reduce the burden of regulatory reporting for financial institutions and improve the overall quality of the data [54].

- Supply chain compliance: Blockchain can be used to create a secure and transparent record of transactions in supply chains, enabling companies to track the movement of goods and ensure compliance with regulations. This can aid in reducing the risk of fraud and improving the overall efficiency of supply-chain management [55].

- Smart contracts: Blockchain can be used to automate compliance processes through the use of smart contracts, which are self-executing contracts that automatically enforce the terms of an agreement. This lowers the impact of errors and improves the overall efficiency of compliance processes [56].

3.4. Applications

- Supply chain management: IoT devices can be used to collect data from physical assets and locations, such as factories or supply-chain nodes. These data can be stored on a blockchain, creating a secure and transparent record of transactions [57]. This can help to ensure compliance with regulations, such as food safety regulations, by providing an auditable trail of the movement of goods and the conditions under which they were transported.

- Anti-Money Laundering (AML): Blockchain can be used to create a secure and tamper-proof record of transactions, making it easier to detect and prevent money laundering and other financial crimes. This reduces the risk of fraud and increases transparency in the financial system [53].

- Asset tracking and management: IoT devices can be used to track and monitor the condition of assets, such as machinery or vehicles [58,59,60]. Similar to the supply chain. These data can be stored on a distributed database, creating a reliable and quickly accessible record of the asset’s history. This can help to ensure compliance with regulations, such as maintenance schedules or environmental standards, by providing an auditable trail of the asset’s use and maintenance.

- Identity verification: Blockchain can be used to create a decentralized and secure identity verification system. IoT devices can be used to collect biometric data, such as fingerprints [61] or facial recognition, to verify the identity of individuals. This can help streamline financial institutions’ KYC processes and reduce the risk of identity theft or fraud.

- Product tracking and monitoring: IoT devices can be used to monitor the quality of products in real-time, such as temperature, humidity [62,63], or vibration. These data can also be stored on a blockchain, creating a record of the product’s history. This can help identify quality issues and ensure that products meet the required quality standards.

- Quality control and testing: IoT devices can collect data for quality control [64] and testing processes, such as test results or inspection data, to monitor compliance with these requirements. Based on this, it can trigger automatic actions if required. This can help identify quality issues and improve the overall quality of products.

3.5. RegTech and TRL

4. RegTech in Financial Sector

4.1. Benefits of the Current Compliance Application in Financial Sectors

- Compliance Efficiency: With the help of RegTech applications, the compliance processes can be automated, greatly reducing manual effort and time to save costs and improve productivity in compliance operations [69]. In addition, useful tools enable financial entities to keep good auditable records of compliance activities by maintaining a robust audit trail [25] and capturing all relevant actions during the compliance process, which provides clear evidence for future investigations. Moreover, financial regulations keep changing [16], which not only costs entities time to keep pace with them but may also cause potential non-compliance risks without good regulatory change management. RegTech solutions can automatically monitor and interpret regulatory changes and provide timely updates and alerts so that organizations can stay informed and adapt their compliance processes and policies accordingly. For example, the NLP can help users interpret the regulatory rules and identify any changes or updates; Robotic Process Automation can produce the regulatory reports automatically; distributed ledger technology can verify and check the authentication of the report; and the programming interface will enable the report to be submitted directly to regulators or supervisors [70]. The combination of various digital technologies can have a greater effect on the compliance process.

- Transparency and Regulatory Collaboration: RegTech can handle real-time monitoring [70] and internal and external reporting. On the one hand, by analyzing real-time data such as transactions, market activities, and regulatory changes, financial institutions can identify potential compliance issues or suspicious transactions and take appropriate action immediately against any potential risks. In addition, entities can identify and assess risks via real-time monitoring, detect patterns, and generate insights that support risk mitigation strategies by analyzing large volumes of data. On the other hand, RegTech also facilitates automated, accurate, and timely reporting to regulators or supervisors, contributing to transparency and accountability [32] and building trust between entities and supervisors. As a result, better collaboration and communication between two parties can be facilitated by providing a standardized platform with automated reporting, which can streamline the exchange of information, reduce duplication of efforts, and foster a more efficient and transparent relationship.

- Customer Due Diligence: Client background checks are crucial in the financial industry to avoid causing financial crimes such as money laundering. As criminals become more technologically advanced, it presents unprecedented challenges for financial service providers. Hence, customer due diligence processes such as Know Your Customer (KYC) and Anti-Money Laundering (AML) checks are inevitable [71]. By automating data collection, verification, and risk assessment, the applied RegTech can make more accurate analyses and judgments in due diligence procedures as well as streamline customer onboarding with reduced manual errors [71], establishing a good reputation in customer service.

- Data Integrity and Security: RegTech solutions often incorporate robust data management and security features, including encryption, access controls, audit trails, and other security measures to protect sensitive information and prevent data breaches [72], which helps financial companies ensure the integrity, confidentiality, and accuracy of data used in regulatory compliance.

4.2. Shortcomings of the Current Compliance Application in Financial Sectors

- establishing a collaborative relationship among financial institutions, technology providers, and regulatory bodies to identify the specific challenges faced by compliance applications.

- creating regulatory sandboxes or innovation hubs that allow for better understanding of the limitations and challenges while providing an opportunity to refine and improve them based on real-world feedback.

- issuing clear guidance on compliance requirements and expectations, taking technological advancements into account.

- initiating pilot programs or demonstrations to showcase the effectiveness of compliance applications.

- regularly monitoring the evolution of compliance applications and providing timely updates to regulations and compliance requirements.

5. RegTech Applications in Non-Financial Sectors

5.1. Agriculture Sector

- Limited data availability: RegTech solutions rely on data to provide insights and automate compliance processes. However, data can be limited or fragmented in agriculture, making it difficult to develop effective RegTech solutions. For example, data on weather patterns, soil conditions, and crop yields may be available from different sources, making it challenging to integrate and analyze the data [76,77]. Weather pattern data may be obtained from local weather stations, while soil condition data is collected from soil testing laboratories, and remote sensing techniques capture information about soil composition. Additionally, crop yield data are sourced from agricultural surveys, farm management systems, and market reports. These diverse sources lead to data fragmentation, where information is scattered across multiple platforms, formats, and sources.

- High implementation costs: Implementing RegTech solutions can be expensive and may be prohibitive for smaller farms. To gather the required data, the farm would need to invest in various sensors, which can be quite costly considering the scale of deployment across different fields or crops. In addition, acquiring and maintaining the necessary hardware, software, and connectivity infrastructure can add to the expenses. Moreover, collecting and analyzing the data may involve utilizing cloud-based storage, advanced analytics platforms, and data integration tools. These technologies often come with subscription fees or licensing costs, which can be prohibitive for smaller farms with limited budgets. Furthermore, farmers or farm managers may need training to operate the sensors, interpret the data, and make informed decisions based on the insights obtained, which requires additional expenses for professional training or hiring consultants. Lastly, sensors may require software updates and potential system repairs that incur additional costs. This can limit the adoption of RegTech solutions, particularly in developing countries or regions where agriculture is a significant source of income [78].

- Lack of standardization: Agriculture is a complex industry, with different crops, farming practices, and regulations varying by region and country. Different crops have unique growth requirements, susceptibility to pests and diseases, and market demands. For example, if there are two regions and region A specializes in wheat production and follows conventional farming practices, the local regulatory authority requires farmers to adhere to specific guidelines for pesticide usage, irrigation methods, and soil conservation. In contrast, if region B focuses on vineyard cultivation and practices organic farming methods, the regulatory framework in this region places strong emphasis on organic certification, water conservation, and biodiversity protection. Farms in Region B need to keep detailed records of crop inputs, such as organic fertilizers, compost, and pest control products, to secure organic certification. This can make it challenging to develop RegTech solutions that are widely applicable and can be scaled across different contexts [77,79].

- Limited understanding and awareness: Many farmers and agricultural stakeholders may not be aware of the potential benefits of RegTech solutions [76,78] or may lack the technical expertise to implement and use them effectively [78,80]. A small family-owned farm in a rural area with tight budgets may be reluctant to allocate resources towards technology adoption if farmers are not aware of the potential return on investment or long-term benefits. The farmers have been using traditional farming practices for generations and are not familiar with modern technologies or digital solutions. They may also lack the necessary skills and knowledge to set up and operate the required hardware, software, and connectivity infrastructure and struggle with data collection, analysis, and interpretation. This can limit the adoption and impact of RegTech solutions in agriculture [81].

- Regulatory barriers: In some cases, regulations may not allow the use of certain technologies or may require manual processes that cannot be automated with RegTech solutions. For example, drones equipped with advanced imaging sensors and artificial intelligence algorithms can efficiently identify pest infestations, monitor crop health, and optimize irrigation practices. However, due to concerns related to airspace regulations, privacy, or safety, the regulatory framework in a particular region may prohibit or limit the use of drones in agriculture. In addition, some agricultural regulations may require manual processes or paper-based record-keeping for compliance purposes. For instance, a regulation might require farmers to manually record the use of certain pesticides or the application of specific fertilizers, which poses challenges when integrating RegTech solutions that automate data collection, analysis, and reporting. This can limit the potential impact of RegTech in agriculture.

5.2. Manufacturing

5.3. Healthcare

5.4. Logistics

5.5. International Trade and Business

- Trade Compliance Automation: The complex international political environment brings significant regulatory challenges to cross-border trades [87] that need to comply with regulations imposed by governments and international bodies. Providing real-time monitoring and screening of parties involved in trade transactions against sanctioned lists or restricted entities can ensure compliance with export control requirements, mitigate reputational risks, and help businesses avoid penalties. The trade compliance processes can be automated by digitizing documentation, automating data collection, and providing real-time updates on regulatory changes to achieve a simplified compliance process and smoother cross-border transactions with reduced error.

- Cross-Border Payments: The settlement of payments for international trade carries a high risk. In international trade, the consignee often refuses to pay the final payment for various reasons. This problem can be avoided to a certain extent by using smart contracts [88].

- Efficient Documentation Management: International trade involves extensive documentation, including contracts, invoices, bills of lading, and certificates of origin. Proper digitalization reduces reliance on physical paperwork [89], improves accessibility, and facilitates efficient sharing of documents with trading partners and regulatory authorities. It also ensures proper record-keeping, easy retrieval, and compliance with document retention requirements. For instance, RegTech can assist in classifying products more accurately in terms of their harmonized system (HS) codes and automatically calculating customs duties to minimize errors, improve efficiency, and ensure compliance with tariff regulations.

5.6. Challenges in Non-Financial Sectors

- Lack of Customization: Existing RegTech applications, derived from the financial industry, may not be readily applicable to the wide range of non-financial regulations to cater for the specific compliance needs of different sectors, which will create gaps in compliance coverage and hinder effective regulatory compliance in specific industries.

- Complex and Evolving Regulatory Landscape: Keeping pace with the evolving regulatory landscape is challenging as regulations of various industries can be complex and rapidly changing, which leads to difficulties in staying up to date with regulatory changes, gaps in compliance coverage, and potential non-compliance risks.

- Limited Adoption and Awareness: RegTech adoption in non-financial sectors is relatively low, and the limited awareness of available RegTech solutions may result in a lack of understanding about these technologies’ potential benefits and limitations.

- Integration Challenges: Many non-financial organizations have legacy systems that were not designed to accommodate modern RegTech solutions. Integrating new RegTech applications with existing infrastructure can be challenging. It requires additional investments in technology and staff training and may also cause disruptions during implementation. In addition, disparate systems with different data sources collected from non-financial entities are not easily integrated, which presents great challenges to the existing applications in effectively aggregating, normalizing, and analyzing data.

- Standardization: The implementation of RegTech in the financial sector is comparatively advanced and well-established, with hundreds of applications providing relatively complete functional modules and practical technical applications. However, it is still in the initial application stage in other sectors, such as agriculture, the food industry, supply-chain management, etc. No matter how developed they are, on-shelf applications lack uniformity and standardization.

6. Comparing FinTech and Different RegTech

6.1. Different Business Focuses

6.2. Different Compliance Focus

6.3. Different Audit Sequences

6.4. Value Chain

- Industrial Equipment: Industrial equipment is unnecessary in the financial industry, but it is indispensable in most physical industries.

- Physical Safety of Humans: Compliance in the financial sector is less concerned with people’s physical health and safety, which is considered as important as product quality in non-financial fields due to its huge impact.

- Field Data: There is no field data in finance. However, it is a critical source of information for non-financial entities. Collecting field data is more challenging because of extreme weather and human interference.

- Logistics: Logistics is only available in non-financial industries to contribute to the value-adding process. Thus, logistics-relevant activities are also within the scope of compliance, such as the truck driver’s behavior, the internal environment of containers in transportation, etc.

6.5. Virtual vs. Physical World

6.6. Human Roles

7. RegTech and Industrial Internet of Things

7.1. The Core of RegTech

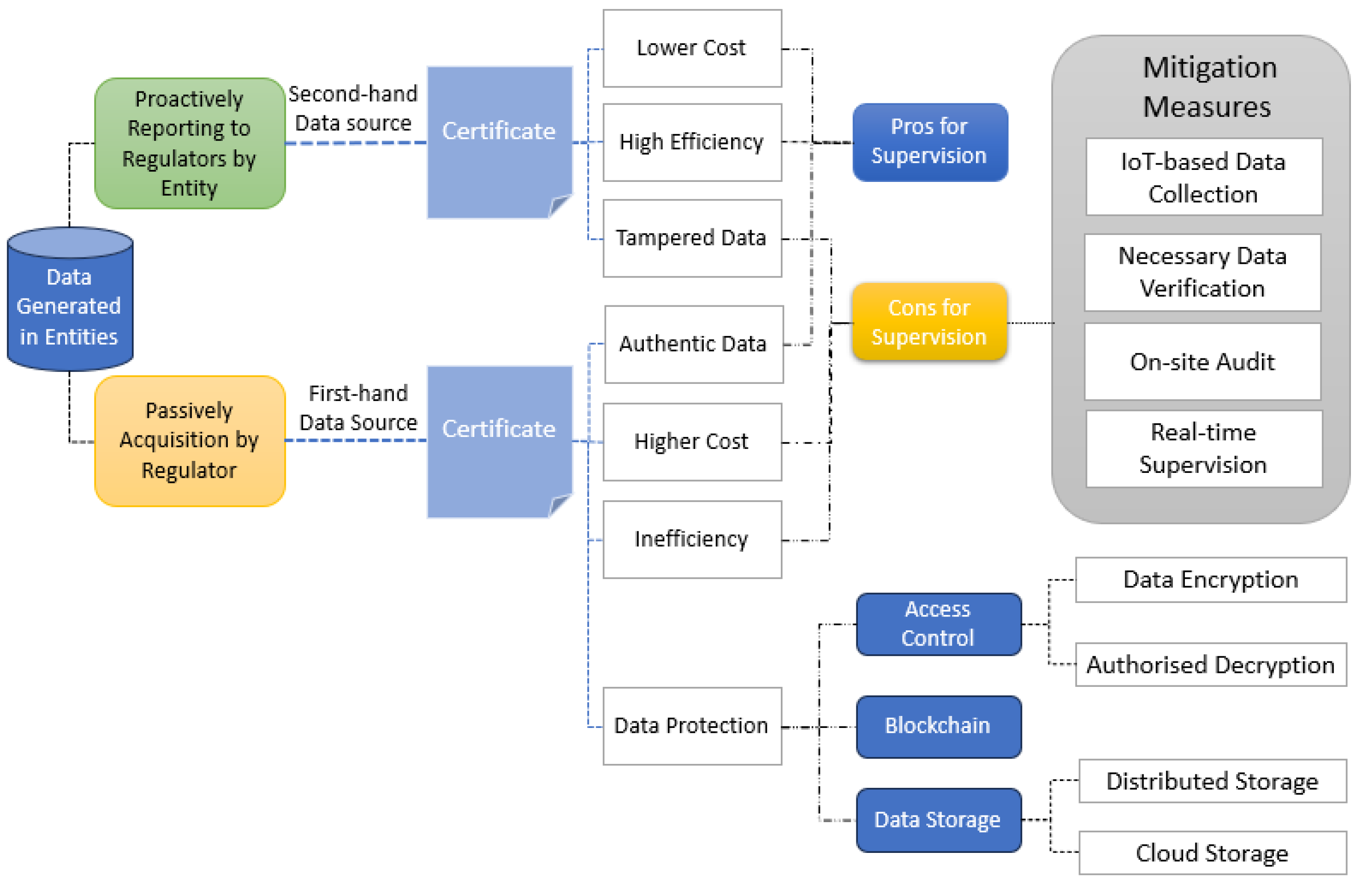

- Data collection is a continuous, repeating process that involves quality management internally and regulatory compliance externally. Considering the privacy of data and the protection of organizations’ interests, a screener is necessary to be designed in the data collection process to make sure that only the compliance-related required data are retrieved. In the traditional regulation audit process, regulation-related data are prepared in advance by the organizations on paper or digital devices. Collecting authentic data is a significant challenge for supervisors, as these documents can be easily forged or tampered with.

- Data processing is the step where the authentication of data should be verified and the fake, invalid, and irrelevant data should be cleared.

- Data analysis is the process where the generated data are matched with the standard of regulatory rules, and a positive or negative decision is made along with it.

- Data visualization is the proper presentation of data, showing the result of data analysis in a readable and easy-to-comprehend format. Data storage, or data archiving, is the definitive treatment of data. In this step, all the data should have clear identification, and they deserve various destinations as per their categories. In terms of complexity, the most time-consuming procedure is data processing.

- Unstructured Data: Data is collected from various sources within organizations without a unified format, so it is time-consuming for regulators to aggregate information and identify risks.

- The complexity of Received Data: The increasing regulations, which are increasingly complex, challenge the expertise of professionals to make timely and correct judgments or recommendations.

- New Risks Caused by the Dynamic Development of Entities: Migrating financial companies to virtual companies may bring new potential risks to the industry in terms of regulation and management.

7.2. The Need for IIoT in RegTech

7.3. Data Security and Access Control

7.4. Data Storage and Archiving

7.5. Potential IIoT-Based Regulatory Supervision Framework

- IoT-based Data Collection: this not only saves labor costs for producers for data collection by replacing traditional manual work but also increases the transparency of the process.

- Necessary Data Verification: this measure prevents data fraud risks such as IoT devices being damaged or tampered with by humans. It can be achieved by introducing AI and ML technologies to assist decision-making after certain algorithms are trained [111].

- On-site Audit: Activities in the non-financial sectors involve fieldwork. A proper on-site audit is necessary, as supervisors can only partially rely on online supervision. For example, pesticide spraying is important for the cultivation of crops because it is effective against pests and diseases. However, excessive pesticide use is a serious threat to human health, and therefore precise control of pesticide doses is very important. It is therefore important to check records of pesticide purchases and actual use.

- Real-Time Supervision: Real-time monitoring in some critical procedures with automatic reporting to regulators can help manufacturers comply with regulations with less labor cost in data collection as well as establish a good reputation. Machine learning can help companies eliminate potential risks by using daily data to predict their occurrence in advance. On-premises real-time monitoring is difficult, as companies would be reluctant to set up such infrastructure without any benefit. However, manufacturers can also benefit if the IIoT is deployed for both their own production and compliance monitoring.

8. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Grassi, L.; Lanfranchi, D. RegTech in public and private sectors: The nexus between data, technology and regulation. J. Ind. Bus. Econ. 2022, 49, 441–479. [Google Scholar] [CrossRef]

- Firmansyah, B.; Arman, A.A. A Systematic Literature Review of RegTech: Technologies, Characteristics, and Architectures. In Proceedings of the 2022 International Conference on Information Technology Systems and Innovation (ICITSI), Bandung, Indonesia, 8–9 November 2022; pp. 310–315. [Google Scholar]

- Butler, T. Towards a standards-based technology architecture for RegTech. J. Financ. Transform. 2017, 45, 49–59. [Google Scholar]

- Gasparri, G. Risks and Opportunities of RegTech and SupTech Developments. Front. Artif. Intell. 2019, 2, 14. (In English) [Google Scholar] [CrossRef] [PubMed]

- Dziawgo, T. Supervisory Technology As a New Tool for Banking Sector Supervision. J. Bank. Financ. Econ. 2021, 15, 5–13. [Google Scholar] [CrossRef]

- Schueffel, P. Taming the beast: A scientific definition of fintech. J. Innov. Manag. 2016, 4, 32–54. [Google Scholar] [CrossRef]

- Wilkins, C. Financial Stability Implications from Fintech: Supervisory and Regulatory Issues that Merit Authorities’ Attention; Financial Stability Board: Basel, Switzerland, 2017. [Google Scholar]

- SafariCom. SafariCom. Available online: https://www.safaricom.co.ke/personal/m-pesa/getting-started (accessed on 15 July 2023).

- Puschmann, T. Fintech. Bus. Inf. Syst. Eng. 2017, 59, 69–76. [Google Scholar] [CrossRef]

- Suryono, R.R.; Budi, I.; Purwandari, B. Challenges and Trends of Financial Technology (Fintech): A Systematic Literature Review. Information 2020, 11, 590. [Google Scholar] [CrossRef]

- Call for Input: Supporting the Development and Adoption of RegTech. Available online: https://www.fca.org.uk/news/news-stories/call-input-supporting-development-and-adoption-regtech (accessed on 8 June 2023).

- FinTech, R. SupTech: What They Mean for Financial Supervision. 2017, 20, 20. Available online: https://www.torontocentre.org/videos/FinTech_RegTech_and_SupTech_What_They_Mean_for_Financial_Supervision.pdf (accessed on 29 July 2023).

- Billington, C.; Lee, H.L.; Tang, C.S. Successful strategies for product rollovers. MIT Sloan Manag. Rev. 1998, 39, 3. [Google Scholar]

- Teichmann, F.; Boticiu, S.; Sergi, B.S. RegTech–Potential benefits and challenges for businesses. Technol. Soc. 2023, 72, 102150. [Google Scholar] [CrossRef]

- Narang, S. Accelerating Financial Innovation Through RegTech: A New Wave of FinTech. In Fostering Innovation and Competitiveness with FinTech, RegTech, and SupTech; IGI Global: Hershey, PA, USA, 2021; pp. 61–79. [Google Scholar]

- Johansson, E.; Sutinen, K.; Lassila, J.; Lang, V.; Martikainen, M.; Lehner, O.M. Regtech-a necessary tool to keep up with compliance and regulatory changes. ACRN J. Financ. Risk Perspect. Spec. Issue Digit. Account. 2019, 8, 71–85. [Google Scholar]

- Yang, D.; Li, M. Evolutionary approaches and the construction of technology-driven regulations. Emerg. Mark. Financ. Trade 2018, 54, 3256–3271. [Google Scholar] [CrossRef]

- Umalkar, M. RegTech: An untapped opportunity. J. Digit. Bank. 2021, 6, 72–82. [Google Scholar]

- Turki, M.; Hamdan, A.; Cummings, R.T.; Sarea, A.; Karolak, M.; Anasweh, M. The regulatory technology “RegTech” and money laundering prevention in Islamic and conventional banking industry. Heliyon 2020, 6, e04949. [Google Scholar] [CrossRef]

- Buckley, R.; Arner, D.; Barberis, J. The Emergence of Regtech 2.0: From Know Your Customer to Know Your Data. J. Financ. Transform. 2016, 44, 79–86. [Google Scholar] [CrossRef]

- RegTech Companies. Available online: https://www2.deloitte.com/lu/en/pages/technology/articles/regtech-companies-compliance.html (accessed on 17 April 2023).

- “REGTECH100-2023”, in “REGTECH100”, 2023. Available online: https://fintech.global/regtech100/wp-content/uploads/2022/12/RegTech100-Report-2023.pdf (accessed on 16 July 2023).

- Butler, T.; O’Brien, L. Understanding RegTech for digital regulatory compliance. Disrupting Financ. FinTech Strategy 21st Century 2019, 85–102. [Google Scholar]

- Yan, P.; Crane, M.; Brennan, R. GDPR Compliance tools: Best practice from RegTech. In Proceedings of the Enterprise Information Systems: 22nd International Conference, ICEIS 2020, Virtual Event, 5–7 May 2020; Revised Selected Papers. Springer: Berlin/Heidelberg, Germany, 2021; pp. 905–929. [Google Scholar]

- Papantoniou, A.A. Regtech: Steering the regulatory spaceship in the right direction? J. Bank. Financ. Technol. 2022, 6, 1–16. [Google Scholar] [CrossRef]

- Ivanoski, J.; Bailey, D.; Walters, M.; Vazirani, J. The transformative power of regtech. Front. Financ. Decis.-Mak. Financ. Serv. 2017, 57, 14–17. [Google Scholar]

- Colaert, V. RegTech as a response to regulatory expansion in the financial sector. Available at SSRN 2677116 2018. [Google Scholar]

- Walshe, J.; Cropper, T. Should you be banking on RegTech? J. Secur. Oper. Custody 2018, 10, 167–175. [Google Scholar]

- Kurum, E. RegTech solutions and AML compliance: What future for financial crime? J. Financ. Crime 2023, 30, 776–794. [Google Scholar] [CrossRef]

- Arner, D.W.; Zetzsche, D.A.; Buckley, R.P.; Weber, R.H. The future of data-driven finance and RegTech: Lessons from EU big bang II. Stan. JL Bus. Fin. 2020, 25, 245. [Google Scholar]

- Armstrong, P. Developments in RegTech and SupTech; Paris Dauphine University: Paris, France, 2018; Available online: https://www.esma.europa.eu/sites/default/files/library/esma71-99-1070_speech_on_regtech.pdf (accessed on 22 July 2018).

- McCarthy, J. The regulation of RegTech and SupTech in finance: Ensuring consistency in principle and in practice. J. Financ. Regul. Compliance 2023, 31, 186–199. [Google Scholar] [CrossRef]

- Packin, N.G. RegTech, compliance and technology judgment rule. Chi.-Kent L. Rev. 2018, 93, 193. [Google Scholar]

- Ryan, P.; Crane, M.; Brennan, R. Design challenges for GDPR RegTech. arXiv 2020, arXiv:2005.12138. [Google Scholar]

- Bolton, M.; Mintrom, M. RegTech and creating public value: Opportunities and challenges. Policy Des. Pract. 2023, 1–17. [Google Scholar] [CrossRef]

- Khanzode, K.C.A.; Sarode, R.D. Advantages and disadvantages of artificial intelligence and machine learning: A literature review. Int. J. Libr. Inf. Sci. (IJLIS) 2020, 9, 3. [Google Scholar]

- Mahalakshmi, V.; Kulkarni, N.; Kumar, K.P.; Kumar, K.S.; Sree, D.N.; Durga, S. The Role of implementing Artificial Intelligence and Machine Learning Technologies in the financial services Industry for creating Competitive Intelligence. Mater. Today Proc. 2022, 56, 2252–2255. [Google Scholar] [CrossRef]

- Regulation, G.D.P. General data protection regulation (GDPR). Intersoft Consult. Accessed Oct. 2018, 24. Available online: https://gdpr-info.eu/art-24-gdpr/ (accessed on 17 April 2023).

- Voigt, P.; Von dem Bussche, A. The eu general data protection regulation (gdpr). In A Practical Guide, 1st ed.; Springer International Publishing: Cham, Switzerland, 2017; Volume 10, p. 10-5555. [Google Scholar]

- Neovius, M.; Karlsson, J.; Westerlund, M.; Pulkkis, G. Providing tamper-resistant audit trails for cloud forensics with distributed ledger based solutions. Cloud Comput. 2018, 2018, 29. [Google Scholar]

- Ahmad, A.; Saad, M.; Njilla, L.; Kamhoua, C.; Bassiouni, M.; Mohaisen, A. Blocktrail: A scalable multichain solution for blockchain-based audit trails. In Proceedings of the ICC 2019–2019 IEEE International Conference on Communications (ICC), Shanghai, China, 20–24 May 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 1–6. [Google Scholar]

- Ahmad, A.; Saad, M.; Bassiouni, M.; Mohaisen, A. Towards blockchain-driven, secure and transparent audit logs. In Proceedings of the 15th EAI International Conference on Mobile and Ubiquitous Systems: Computing, Networking and Services, New York, NY, USA, 5–7 November 2018; pp. 443–448. [Google Scholar]

- Carrell, D.S.; Cronkite, D.; Palmer, R.E.; Saunders, K.; Gross, D.E.; Masters, E.T.; Hylan, T.R.; Von Korff, M. Using natural language processing to identify problem usage of prescription opioids. Int. J. Med. Inform. 2015, 84, 1057–1064. [Google Scholar] [CrossRef]

- Zetsche, D.A.; Buckley, R.P.; Arner, D.W.; Barberis, J.N. From FinTech to TechFin: The regulatory challenges of data-driven finance. NYUJL Bus. 2017, 14, 393. [Google Scholar]

- Aziz, H.; Guled, A. Cloud computing and healthcare services. J. Biosens. Bioelectron. 2016, 7, 220. [Google Scholar] [CrossRef]

- Youssef, A.E. Exploring cloud computing services and applications. J. Emerg. Trends Comput. Inf. Sci. 2012, 3, 838–847. [Google Scholar]

- Atlam, H.F.; Alenezi, A.; Alharthi, A.; Walters, R.J.; Wills, G.B. Integration of cloud computing with internet of things: Challenges and open issues. In Proceedings of the 2017 IEEE International Conference on Internet of Things (iThings) and IEEE Green Computing and Communications (GreenCom) and IEEE Cyber, Physical and Social Computing (CPSCom) and IEEE Smart Data (SmartData), Exeter, UK, 21–23 June 2017; IEEE: Piscataway, NJ, USA, 2017; pp. 670–675. [Google Scholar]

- Syed, R.; Suriadi, S.; Adams, M.; Bandara, W.; Leemans, S.J.; Ouyang, C.; ter Hofstede, A.H.; van de Weerd, I.; Wynn, M.T.; Reijers, H.A. Robotic process automation: Contemporary themes and challenges. Comput. Ind. 2020, 115, 103162. [Google Scholar] [CrossRef]

- Kumar, K.N.; Balaramachandran, P.R. Robotic process automation-a study of the impact on customer experience in retail banking industry. J. Internet Bank. Commer. 2018, 23, 1–27. [Google Scholar]

- Devarajan, Y. A study of robotic process automation use cases today for tomorrow’s business. Int. J. Comput. Tech. 2018, 5, 12–18. [Google Scholar]

- Nagy, J.; Oláh, J.; Erdei, E.; Máté, D.; Popp, J. The role and impact of Industry 4.0 and the internet of things on the business strategy of the value chain—The case of Hungary. Sustainability 2018, 10, 3491. [Google Scholar] [CrossRef]

- Zhang, Q.; Huang, T.; Zhu, Y.; Qiu, M. A case study of sensor data collection and analysis in smart city: Provenance in smart food supply chain. Int. J. Distrib. Sens. Netw. 2013, 9, 382132. [Google Scholar] [CrossRef]

- Pal, K. Internet of things and blockchain technology in apparel manufacturing supply chain data management. Procedia Comput. Sci. 2020, 170, 450–457. [Google Scholar] [CrossRef]

- Malhotra, D.; Saini, P.; Singh, A.K. How blockchain can automate KYC: Systematic review. Wirel. Pers. Commun. 2022, 122, 1987–2021. [Google Scholar] [CrossRef]

- Parra-Moyano, J.; Thoroddsen, T.; Ross, O. Optimised and dynamic KYC system based on blockchain technology. Int. J. Blockchains Cryptocurrencies 2019, 1, 85–106. [Google Scholar] [CrossRef]

- Wang, B.; Lin, Z.; Wang, M.; Wang, F.; Xiangli, P.; Li, Z. Applying blockchain technology to ensure compliance with sustainability standards in the PPE multi-tier supply chain. Int. J. Prod. Res. 2022, 61, 4934–4950. [Google Scholar] [CrossRef]

- Shojaei, A.; Flood, I.; Moud, H.I.; Hatami, M.; Zhang, X. An implementation of smart contracts by integrating BIM and blockchain. In Proceedings of the Future Technologies Conference (FTC) 2019, San Francisco, CA, USA, 14–15 November 2019; Volume 2, pp. 519–527. [Google Scholar]

- Park, A.; Li, H. The effect of blockchain technology on supply chain sustainability performances. Sustainability 2021, 13, 1726. [Google Scholar] [CrossRef]

- Bernal, E.; Spiryagin, M.; Cole, C. Onboard condition monitoring sensors, systems and techniques for freight railway vehicles: A review. IEEE Sens. J. 2018, 19, 4–24. [Google Scholar] [CrossRef]

- Munirathinam, S. Industry 4.0: Industrial internet of things (IIOT). In Advances in computers; Elsevier: Amsterdam, The Netherlands, 2020; Volume 117, pp. 129–164. [Google Scholar]

- Zhou, C.; Damiano, N.; Whisner, B.; Reyes, M. Industrial Internet of Things:(IIoT) applications in underground coal mines. Min. Eng. 2017, 69, 50. [Google Scholar] [CrossRef]

- Reising, D.; Cancelleri, J.; Loveless, T.D.; Kandah, F.; Skjellum, A. Radio identity verification-based IoT security using RF-DNA fingerprints and SVM. IEEE Internet Things J. 2020, 8, 8356–8371. [Google Scholar] [CrossRef]

- Sinha, N.; Pujitha, K.E.; Alex, J.S.R. Xively based sensing and monitoring system for IoT. In Proceedings of the 2015 International Conference on Computer Communication and Informatics (ICCCI), Coimbatore, India, 8–10 January 2015; pp. 1–6. [Google Scholar]

- Venkatesan, R.; Tamilvanan, A. A sustainable agricultural system using IoT. In Proceedings of the 2017 International Conference on Communication and Signal Processing (ICCSP), Chennai, India, 6–8 April 2017; pp. 0763–0767. [Google Scholar]

- Shahbazi, Z.; Byun, Y.-C. Integration of blockchain, IoT and machine learning for multistage quality control and enhancing security in smart manufacturing. Sensors 2021, 21, 1467. [Google Scholar] [CrossRef]

- Tomaschek, K.; Olechowski, A.; Eppinger, S.; Joglekar, N. A survey of technology readiness level users. In Proceedings of the INCOSE International Symposium, 18 July 2016; Wiley Online Library: Hoboken, NJ, USA, 2016; Volume 26, pp. 2101–2117. [Google Scholar]

- What the RegTech Industry Means for the Booming Mortgages Industry Right Now. Available online: https://www.planetcompliance.com/what-the-regtech-industry-means-for-the-booming-mortgages-industry-right-now/ (accessed on 10 June 2023).

- Waldron, B.R.a.D. Fighting Back against Synthetic Identity Fraud. Available online: https://www.mckinsey.com/capabilities/risk-and-resilience/our-insights/fighting-back-against-synthetic-identity-fraud (accessed on 6 June 2023).

- MORTGAGE QC INDUSTRY TRENDS—Q3 2020. Available online: https://www.acesquality.com/resources/reports/q3-2020-aces-mortgage-qc-industry-trends (accessed on 10 June 2023).

- Arner, D.W.; Barberis, J.; Buckey, R.P. FinTech, RegTech, and the reconceptualization of financial regulation. Nw. J. Int’l L. Bus. 2016, 37, 371. [Google Scholar]

- Von Solms, J. Integrating Regulatory Technology (RegTech) into the digital transformation of a bank Treasury. J. Bank. Regul. 2021, 22, 152–168. [Google Scholar] [CrossRef]

- Singh, C.; Lin, W. Can artificial intelligence, RegTech and CharityTech provide effective solutions for anti-money laundering and counter-terror financing initiatives in charitable fundraising. J. Money Laund. Control 2021, 24, 464–482. [Google Scholar] [CrossRef]

- Elimelech, O.C.; Ferrante, S.; Josman, N.; Meyer, S.; Lunardini, F.; Gómez-Raja, J.; Galán, C.; Cáceres, P.; Sciama, P.; Gros, M. Technology use characteristics among older adults during the COVID-19 pandemic: A cross-cultural survey. Technol. Soc. 2022, 71, 102080. [Google Scholar] [CrossRef]

- Cowburn, N.; Barnet, P. RegTech Opportunities in a Post-4MLD/5MLD World. RegTech Book 2019. [Google Scholar] [CrossRef]

- Kampan, K.; Tsusaka, T.W.; Anal, A.K. Adoption of Blockchain Technology for Enhanced Traceability of Livestock-Based Products. Sustainability 2022, 14, 13148. [Google Scholar] [CrossRef]

- Akhter, R.; Sofi, S.A. Precision agriculture using IoT data analytics and machine learning. J. King Saud Univ.-Comput. Inf. Sci. 2022, 34, 5602–5618. [Google Scholar] [CrossRef]

- Anidu, A.; Dara, R. A review of data governance challenges in smart farming and potential solutions. In Proceedings of the 2021 IEEE International Symposium on Technology and Society (ISTAS), Waterloo, ON, Canada, 28–31 October 2021; IEEE: Piscataway, NJ, USA, 2021; pp. 1–8. [Google Scholar]

- Virk, A.L.; Noor, M.A.; Fiaz, S.; Hussain, S.; Hussain, H.A.; Rehman, M.; Ahsan, M.; Ma, W. Smart farming: An overview. Smart Village Technol. Concepts Dev. 2020, 17, 191–201. [Google Scholar]

- Amiri-Zarandi, M.; Hazrati Fard, M.; Yousefinaghani, S.; Kaviani, M.; Dara, R. A platform approach to smart farm information processing. Agriculture 2022, 12, 838. [Google Scholar] [CrossRef]

- Pivoto, D.; Waquil, P.D.; Talamini, E.; Finocchio, C.P.S.; Dalla Corte, V.F.; de Vargas Mores, G. Scientific development of smart farming technologies and their application in Brazil. Inf. Process. Agric. 2018, 5, 21–32. [Google Scholar] [CrossRef]

- Ada, E.; Sagnak, M.; Uzel, R.A.; Balcıoğlu, İ. Analysis of barriers to circularity for agricultural cooperatives in the digitalization era. Int. J. Product. Perform. Manag. 2022, 71, 932–951. [Google Scholar] [CrossRef]

- How Regtech Will Help Drive the Manufacturing Industry Forward. Available online: https://www.planetcompliance.com/how-regtech-will-help-drive-the-manufacturing-industry-forward/ (accessed on 12 June 2023).

- Timmons, J. The Cost of Federal Regulation. Available online: https://www.nam.org/the-cost-of-federal-regulation/ (accessed on 20 May 2023).

- Hickey, A. Compliance May Cost Companies Millions, but Non-Compliance Costs Even More. Available online: https://www.ciodive.com/news/compliance-may-cost-companies-millions-but-non-compliance-costs-even-more/513280/ (accessed on 12 June 2023).

- RegTech Transforming the Healthcare Industry. Available online: https://www.planetcompliance.com/regtech-transforming-the-healthcare-industry/ (accessed on 12 June 2023).

- Treasury, D.o.t., (Ed.) National Money Laundering Risk Assessment; 2022; p. 71. Available online: https://home.treasury.gov/system/files/136/2022-National-Money-Laundering-Risk-Assessment.pdf (accessed on 12 June 2023).

- Fadahunsi, A.; Rosa, P. Entrepreneurship and illegality: Insights from the Nigerian cross-border trade. J. Bus. Ventur. 2002, 17, 397–429. [Google Scholar] [CrossRef]

- Li, X.H. Blockchain-based cross-border E-business payment model. In Proceedings of the 2021 2nd International Conference on E-Commerce and Internet Technology (ECIT), Hangzhou, China, 5–7 March 2021; IEEE: Piscataway, NJ, USA, 2021; pp. 67–73. [Google Scholar]

- Amankwah-Amoah, J.; Khan, Z.; Wood, G.; Knight, G. COVID-19 and digitalization: The great acceleration. J. Bus. Res. 2021, 136, 602–611. [Google Scholar] [CrossRef] [PubMed]

- Gao, S.; Ling, S.; Liu, W. The role of social media in promoting information disclosure on environmental incidents: An evolutionary game theory perspective. Sustainability 2018, 10, 4372. [Google Scholar] [CrossRef]

- Li, K.; Cheng, L.; Teng, C.-I. Voluntary sharing and mandatory provision: Private information disclosure on social networking sites. Inf. Process. Manag. 2020, 57, 102128. [Google Scholar] [CrossRef]

- Tweneboah-Koduah, S.; Skouby, K.E.; Tadayoni, R. Cyber security threats to IoT applications and service domains. Wirel. Pers. Commun. 2017, 95, 169–185. [Google Scholar] [CrossRef]

- Al Nafea, R.; Almaiah, M.A. Cyber security threats in cloud: Literature review. In Proceedings of the 2021 International Conference on Information Technology (ICIT), Amman, Jordan, 14–15 July 2021; IEEE: Piscataway, NJ, USA, 2021; pp. 779–786. [Google Scholar]

- Humayun, M.; Niazi, M.; Jhanjhi, N.; Alshayeb, M.; Mahmood, S. Cyber security threats and vulnerabilities: A systematic mapping study. Arab. J. Sci. Eng. 2020, 45, 3171–3189. [Google Scholar] [CrossRef]

- Ullah, F.; Naeem, H.; Jabbar, S.; Khalid, S.; Latif, M.A.; Al-Turjman, F.; Mostarda, L. Cyber security threats detection in internet of things using deep learning approach. IEEE Access 2019, 7, 124379–124389. [Google Scholar] [CrossRef]

- Bahga, A.; Madisetti, V.K. Blockchain platform for industrial internet of things. J. Softw. Eng. Appl. 2016, 9, 533–546. [Google Scholar] [CrossRef]

- Golosova, J.; Romanovs, A. The advantages and disadvantages of the blockchain technology. In Proceedings of the 2018 IEEE 6th Workshop on Advances in Information, Electronic and Electrical Engineering (AIEEE), Vilnius, Lithuania, 8–10 November 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 1–6. [Google Scholar]

- Niranjanamurthy, M.; Nithya, B.; Jagannatha, S. Analysis of Blockchain technology: Pros, cons and SWOT. Clust. Comput. 2019, 22, 14743–14757. [Google Scholar] [CrossRef]

- Ali, O.; Jaradat, A.; Kulakli, A.; Abuhalimeh, A. A comparative study: Blockchain technology utilization benefits, challenges and functionalities. IEEE Access 2021, 9, 12730–12749. [Google Scholar]

- Wu, B.; Duan, T. The advantages of blockchain technology in commercial bank operation and management. In Proceedings of the 2019 4th International Conference on Machine Learning Technologies, Nanchang China, 21–23 June 2019; pp. 83–87. [Google Scholar]

- Ramu, G.; Eswara Reddy, B. Secure architecture to manage EHR’s in cloud using SSE and ABE. Health Technol. 2015, 5, 195–205. [Google Scholar] [CrossRef]

- Mhatre, S.; Nimkar, A.V. Secure cloud-based federation for EHR using multi-authority ABE. In Proceedings of the Advanced Computing and Intelligent Engineering: Proceedings of ICACIE 2017, Central University of Rajasthan, Ajmer, India, 23–25 November 2017; Springer: Berlin/Heidelberg, Germany; Volume 2, pp. 3–15. [Google Scholar]

- Reedy, B.E.; Ramu, G. A Secure Framework for Ensuring EHR’s Integrity Using Fine-Grained Auditing and CP-ABE. In Proceedings of the 2016 IEEE 2nd International Conference on Big Data Security on Cloud (BigDataSecurity), IEEE International Conference on High Performance and Smart Computing (HPSC), and IEEE International Conference on Intelligent Data and Security (IDS), New York, NY, USA, 9–10 April 2016; IEEE: Piscataway, NJ, USA, 2016; pp. 85–89. [Google Scholar]

- Wang, S.; Zhang, Y.; Zhang, Y. A blockchain-based framework for data sharing with fine-grained access control in decentralized storage systems. IEEE Access 2018, 6, 38437–38450. [Google Scholar] [CrossRef]

- Yang, X.; Maiti, A.; Jiang, J.; Kist, A. Forecasting and Monitoring Smart Buildings with the Internet of Things, Digital Twins and Blockchain. In Online Engineering and Society 4.0, Cham; Auer, M.E., Bhimavaram, K.R., Yue, X.-G., Eds.; Springer International Publishing: Cham, Switzerland, 2022; pp. 213–224. [Google Scholar]

- Gao, W.; Hatcher, W.G.; Yu, W. A survey of blockchain: Techniques, applications, and challenges. In Proceedings of the 2018 27th International Conference on Computer Communication and Networks (ICCCN), Hangzhou, China, 30 July–2 August 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 1–11. [Google Scholar]

- Steichen, M.; Fiz, B.; Norvill, R.; Shbair, W.; State, R. Blockchain-based, decentralized access control for IPFS. In Proceedings of the 2018 IEEE International Conference on Internet of Things (iThings) and IEEE Green Computing and Communications (GreenCom) and IEEE Cyber, Physical and Social Computing (CPSCom) and IEEE Smart Data (SmartData), Halifax, NS, Canada, 30 July–3August 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 1499–1506. [Google Scholar]

- Huang, H.-S.; Chang, T.-S.; Wu, J.-Y. A secure file sharing system based on IPFS and blockchain. In Proceedings of the 2nd International Electronics Communication Conference, Singapore, 8–10 July 2020; pp. 96–100. [Google Scholar]

- Sun, J.; Yao, X.; Wang, S.; Wu, Y. Blockchain-based secure storage and access scheme for electronic medical records in IPFS. IEEE Access 2020, 8, 59389–59401. [Google Scholar] [CrossRef]

- Jones, D.; Snider, C.; Nassehi, A.; Yon, J.; Hicks, B. Characterising the Digital Twin: A systematic literature review. CIRP J. Manuf. Sci. Technol. 2020, 29, 36–52. [Google Scholar] [CrossRef]

- Maiti, A.; Raza, A.; Kang, B.H.; Hardy, L. Estimating service quality in industrial internet-of-things monitoring applications with blockchain. IEEE Access 2019, 7, 155489–155503. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| FinTech | RegTech | |

|---|---|---|

| Time Period | 1993–Now | 2015–Now |

| Focus | Deliver innovative financial products, services, and solutions | Address regulatory compliance challenges faced by organizations |

| Aim | Enhance and automate various financial processes, increase accessibility, improve efficiency, and provide new business models. | Help organizations meet their compliance obligations more efficiently, accurately, and cost-effectively. |

| Sector Scope | Finance only, negligible tangible products involved | Varied and often involve tangible products that generate unique data |

| Key Technologies | Well-developed e.g., application program interface, artificial intelligence, machine learning, internet of things, big data analytics, distributed ledger technology, smart contracts, cloud computing, cryptography, biometrics | Everything in Fintech, but it is still evolving |

| Subsector | Times Covered in the Report | Percentage |

|---|---|---|

| Risk Management | 65 | 19% |

| Compliance Management | 64 | 19% |

| Onboarding Verification | 57 | 17% |

| Regulatory Reporting | 49 | 14% |

| Transaction Monitoring | 39 | 12% |

| Identification/Background checks | 22 | 6% |

| Cybersecurity/Information Security | 16 | 5% |

| Communications Monitoring | 13 | 4% |

| 3rd Party Vendor Management | 5 | 1% |

| Capital Planning/Stress Testing | 4 | 1% |

| Investigations | 3 | 1% |

| Regulatory Change Management | 2 | 1% |

| Aspects\Sectors | Finance | Agriculture | Manufacturing | Food Services | International Trade |

| Aim of Compliance | Financial crime | Product Safety | Product Safety | Food Safety | Product Safety |

| Physical Safety of Humans | N/A | YES | YES | YES | YES |

| Business Focus | Transaction | Farming/ Planting | Processing; SCM | Processing; SCM | Processing; SCM; Logistics; Transaction |

| Value Chain | Simple | Simple | Complex | Complex | Complex |

| Business Procedures Complexity | Low | Medium | High | Medium | High |

| Industrial Equipment | N/A | Medium | High | Medium | High |

| Logistics | No | YES | YES | YES | YES |

| Physical Environment | Not necessary | Necessary | Necessary | Necessary | Necessary |

| Field Data | No | YES | YES | YES | YES |

| Network Dependency | High | Low | Low | Low | Medium |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, J.; Maiti, A.; Fei, J. Features and Scope of Regulatory Technologies: Challenges and Opportunities with Industrial Internet of Things. Future Internet 2023, 15, 256. https://doi.org/10.3390/fi15080256

Li J, Maiti A, Fei J. Features and Scope of Regulatory Technologies: Challenges and Opportunities with Industrial Internet of Things. Future Internet. 2023; 15(8):256. https://doi.org/10.3390/fi15080256

Chicago/Turabian StyleLi, Jinying, Ananda Maiti, and Jiangang Fei. 2023. "Features and Scope of Regulatory Technologies: Challenges and Opportunities with Industrial Internet of Things" Future Internet 15, no. 8: 256. https://doi.org/10.3390/fi15080256

APA StyleLi, J., Maiti, A., & Fei, J. (2023). Features and Scope of Regulatory Technologies: Challenges and Opportunities with Industrial Internet of Things. Future Internet, 15(8), 256. https://doi.org/10.3390/fi15080256