1. Introduction

Fossil fuels (FFs) play a major role in powering the world’s current energy system, accounting for approximately 82% of the primary energy consumption according to the 2022 BP Statistical Review of World Energy [

1]. This reliance on coal, oil, and natural gas comes at a significant environmental cost as FFs are responsible for approximately 73% of global greenhouse gas (GHG) emissions [

2]. This dependence on FF is driving up greenhouse gas emissions, causing climate change and other environmental problems. Moving the global energy system towards sustainable energy sources is crucial to mitigate the impact of climate change and decrease greenhouse gas emissions.

Green hydrogen (GH) offers a zero-emission alternative to fossil fuels and could play a critical role in transitioning to a sustainable energy system. The Hydrogen Council defines it as the hydrogen produced from water electrolysis using renewable electricity [

3]. However, other renewable-based methods can also produce hydrogen, including biomass gasification and pyrolysis, thermochemical water splitting, photocatalysis, supercritical water gasification of biomass, as well as combined dark fermentation and anaerobic digestion techniques [

4].

As a zero-emission fuel, renewable hydrogen has the potential to replace fossil fuels in a range of applications in different sectors such as transportation, industry, building, and power. According to the Hydrogen for Net-Zero report from the Hydrogen Council, clean hydrogen production could reach approximately 660 million metric tons (Mt) in 2050, supplying 22% of the final energy demand and avoiding annual GHG emissions of 7 gigatons (Gt) of

[

3]. It is worth mentioning that in the Hydrogen’s Council report, clean hydrogen is defined as either renewable or low-carbon hydrogen; renewable/green hydrogen refers to hydrogen produced from water electrolysis with renewable electricity, while low-carbon hydrogen refers to hydrogen produced from fossil fuel reforming with carbon capture.

Hydrogen is a versatile energy carrier with numerous applications as a fuel or feedstock across different sectors. For instance, it can serve as a fuel for ground transportation, including both light vehicles and heavy-duty trucks, by using fuel cells that convert hydrogen into electricity with only water as a byproduct. Hydrogen can also be used to produce various fuels or liquid hydrogen for maritime or aviation applications, offering a cleaner and more sustainable alternative to traditional FF. In addition, hydrogen can be used directly in heating, including high-grade heat in industrial processes and building heat, providing a reliable and efficient energy source. Furthermore, hydrogen can help balance the grid as backup “generators” in power applications. Apart from its role as a fuel, hydrogen is also a valuable feedstock for different industries. For example, it can be used in ammonia synthesis for fertilizer production and iron reduction for steel.

According to the International Renewable Energy Agency (IRENA), the current global production of hydrogen is approximately 120 Mt, with two-thirds of it being pure hydrogen and the remaining one-third being in a mixture with other gases [

5]. Hydrogen production relies heavily on fossil fuels, with natural gas and coal serving as the primary energy sources. As of the end of 2021, it was estimated that approximately 47% of global hydrogen production came from natural gas, 27% from coal, 22% from oil as a by-product, around 3% was produced through electrolysis using the electrical grid, and only 1% of the global hydrogen output was produced directly using renewable energy [

6].

Currently, the production of GH is limited by the availability and cost of renewable energy sources and the technologies used to drive the electrolysis process, the electrolyzers. In the past, the major cost driver for GH production was the cost of renewable electricity. However, the continuously decreasing costs of solar photovoltaic and wind electricity have transformed the cost associated with the electrolyzers into the primary cost of the renewable hydrogen production system. There are still challenges that need to be addressed for electrolyzers to become a cost-competitive alternative. One of these challenges is the need for further technological advancements to improve the overall performance (i.e., its efficiency and lifetime) and the implementation of hydrogen policies to achieve economies of scale to bring costs down [

4,

7]. Addressing these challenges will be crucial for realizing the full potential of GH in the transition towards a more sustainable energy system.

Grey hydrogen and blue hydrogen are two prevalent methods of hydrogen production, each with distinct environmental and technical characteristics. Grey hydrogen is primarily produced through steam methane reforming (SMR), where natural gas (mainly methane) reacts with steam under high temperatures and pressures to yield hydrogen and carbon dioxide (CO

2) [

8]. This method is the most common due to its cost-effectiveness and established infrastructure, achieving efficiencies up to approximately 65–75% [

9]. However, it is highly carbon-intensive, emitting around 7.5–13 kg of CO

2 for every kilogram of hydrogen produced [

10]. This significant CO

2 output is a major contributor to greenhouse gas emissions, making grey hydrogen less favorable in terms of environmental sustainability.

In contrast, blue hydrogen also utilizes the SMR process but incorporates carbon capture, utilization, and storage (CCUS) technologies to address the environmental impact. CCUS systems capture up to 90–95% of the CO

2 emissions generated during hydrogen production, which is then either stored underground or utilized in other industrial processes [

8,

10]. This reduces the CO

2 emissions associated with blue hydrogen to approximately 0.8–3.9 kg per kilogram of hydrogen, significantly lowering its carbon intensity. The efficiency of blue hydrogen production is slightly lower than grey hydrogen due to the additional energy requirements for CCUS, typically around 55–65% [

9].

Both grey and blue hydrogen are extensively used in industrial applications such as oil refining, ammonia production, and several chemical manufacturing processes [

9]. However, blue hydrogen is increasingly perceived as a more sustainable option, aligning with global efforts to reduce carbon emissions and transition to a low-carbon economy. Blue hydrogen is becoming more and more prevalent as it provides an economically feasible method to benefit from the natural gas resources already in place while reducing the environmental impact through effective carbon management technology.

According to the International Energy Agency (IEA), producing hydrogen from fossil fuels is currently the lowest-cost option, while renewable options remain the most expensive pathway for hydrogen production. In 2020, grey hydrogen produced from steam reforming cost approximately EUR 0.47–1.50/kg, and it is projected to have a significant increase by 2050. Blue hydrogen produced from steam reforming with carbon capture was estimated in the range of EUR 0.94–1.88/kg and is projected to remain the same until 2050. A comparable cost trend could be observed for hydrogen production from coal, where hydrogen produced without carbon capture is anticipated to experience a considerable increase in cost, while that produced from coal with carbon capture is estimated to have a similar cost in 2050. The cost of using renewable energy for hydrogen production in 2020 was considerably higher, ranging from EUR 2.82 to 7.52/kg. Nonetheless, unlike conventional methods, the cost of renewable hydrogen production is anticipated to significantly decrease to the range of EUR 0.94–3.29/kg by 2050 [

11,

12,

13].

To achieve cost parity with natural gas-based production, the electricity required for the electrolysis process needs to cost around EUR 94/MWh [

14]. While this may seem high compared to long-term electricity prices, recent prices in European countries have regularly exceeded this level due to natural gas being the price-setting fuel in many electricity markets. This highlights the need to shift towards renewable energy sources such as solar PV and wind electricity generation, which have the potential to offer a cost-competitive alternative to natural gas with the necessary storage and flexibility measures. As technology continues to advance and economies of scale are achieved, the cost of renewable energy and electrolyzers is expected to decrease further, making them an increasingly attractive option for cost-effective and sustainable energy production.

The purpose of this paper is to provide a comprehensive analysis of the entire renewable hydrogen value chain, including the current technology available. The aim is to evaluate the hydrogen industry’s current status and future challenges and conduct an economic assessment of each system to determine the feasibility of integrating green hydrogen.

The following sections of the paper are structured as follows. In

Section 2, the state-of-the-art in the green hydrogen energy system value chain is presented. This section covers the electrolyzer systems for hydrogen production, configurations of the hydrogen production system for each renewable source, hydrogen storage methods for both large- and small-scale applications, and potential end-use applications of hydrogen.

Section 3 features an economic analysis of hydrogen production systems categorized by source and their primary cost components.

Section 4 provides a review of current and future expectations for the levelized cost of hydrogen (LCOH). Finally, the last section of the paper comprises a discussion and main conclusions drawn from the study.

2. Green Hydrogen Energy Systems: State of the Art

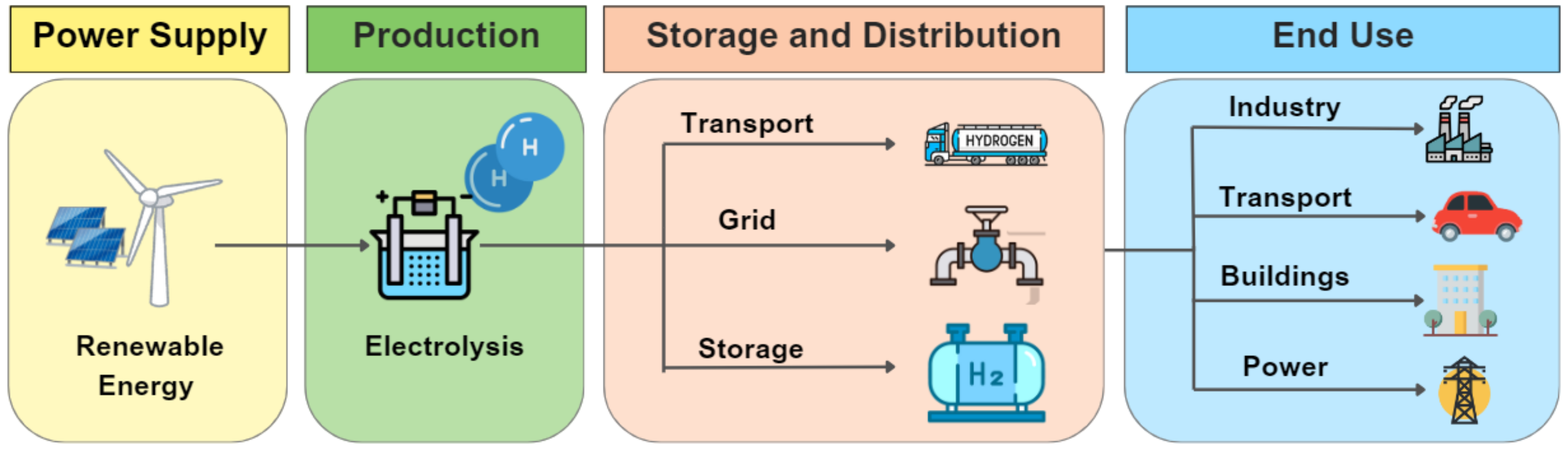

Meeting the rising demand for clean energy requires a reliable and efficient production and distribution system for hydrogen, especially green hydrogen generated from renewable energy sources. Such a system requires a well-configured and effective distribution network, which is referred to in this document as the green hydrogen supply chain (GHSC). As shown in

Figure 1, the GHSC comprises three stages. The first stage involves hydrogen production through water electrolysis using renewable energy sources such as solar, wind, or hydro. In the second stage, hydrogen is distributed via road/ship transportation as gaseous or liquid hydrogen, through pipeline systems in gaseous form, and it is stored in gaseous form. To ensure a constant supply of hydrogen, hydrogen storage systems are essential due to the intermittent availability of renewable sources and random demand along the distribution network. Finally, the third and final stage of the GHSC comprises the end-use applications of hydrogen, which include fuel for fuel cell electric vehicles (FCEVs), electricity generation, feedstocks in industrial processes such as steel, chemical, agriculture, and glass production, and heating and cooling for buildings and industry [

15,

16].

A reliable and efficient green hydrogen supply chain is essential for the wider use of hydrogen-based energy systems. It is critical to design an effective distribution network to ensure the continuous supply of green hydrogen. In this regard, advancements in technology and infrastructure development are crucial for creating a sustainable and scalable hydrogen economy. These advancements will not only enable the efficient production and distribution of green hydrogen but also reduce the cost of producing and delivering it to end users. While the ultimate goal of achieving net-zero emissions relies heavily on the use of hydrogen, this paper will specifically focus on the available technologies that enable the production of green hydrogen. A comprehensive research analysis of each technology will be presented, along with an examination of the challenges and prospects associated with them.

2.1. Green Hydrogen Production

Water electrolysis is a water-splitting method to produce GH using electricity from renewable sources. The chemical reaction that drives this process is shown in Equation (

1). This reaction requires a theoretical thermodynamic cell voltage of 1.23 V to split the water molecule (

) into hydrogen (

) and oxygen (

). However, due to the reaction kinetics and the ohmic resistances of the electrolyte and electrolyzer components, 1.48 V are needed [

17].

Based on the reaction stoichiometry, producing 1 kg of

via electrolysis requires 9 L of water and results in the creation of 8 kg of

as a by-product. One of the advantages of electrolysis is that it has a minimal water consumption relative to other sectors such as irrigated agriculture, which is responsible for 70% of the world’s total freshwater withdrawals [

18]. Electrolyzers are the most commonly employed technology for producing hydrogen through water electrolysis. Nevertheless, other technologies, such as photoelectrochemical and microbial electrolysis cells, have also been developed and researched for their potential to generate hydrogen from water.

2.1.1. Electrolyzer Technologies

Currently, there are two commercially available types of electrolyzer, alkaline water (AWE) and polymer electrolyte membrane (PEMEL). However, the promising advancements in the technology have led to the development of two other types of electrolyzer, anion exchange membranes (AEMs) and solid oxide electrolyzer cells (SOECs), which are currently being researched at the laboratory scale and have the potential to represent a significant step forward in the field.

According to the IEA, the global installed capacity of water electrolysis for hydrogen production reached around 300 MW by the end of 2020. The most widely used technology for this purpose was found to be AWE, accounting for 61% of the total installed capacity, while PEMEL accounted for 31% of the installed capacity. The remaining capacity was attributed to either unspecified electrolyzer technologies or SOECs [

13,

19].

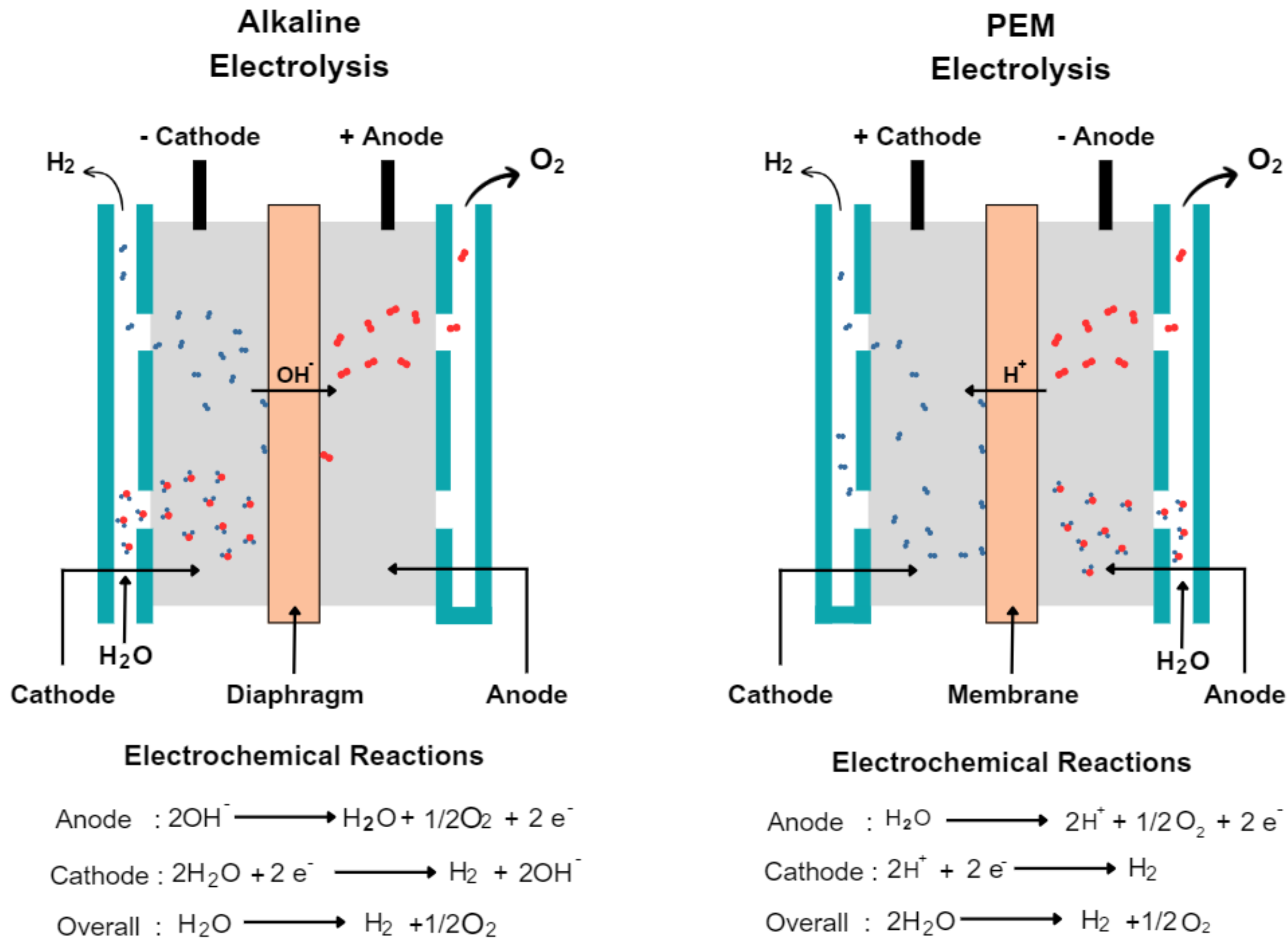

Figure 2 provides a simplified schematic representation of both an AWE and a PEMEL.

Figure 2.

Schematic representation of an (

left) AWE and (

right) PEMEL (adapted from [

20]).

Figure 2.

Schematic representation of an (

left) AWE and (

right) PEMEL (adapted from [

20]).

The installed capacity of electrolyzers for hydrogen production is expected to experience significant growth in the coming years. According to industry projections, the global installed electrolyzer capacity could reach up to 54 GW by 2030, taking into account the capacity under construction and planned. Moreover, if all projects at the early planning stages are included, the capacity could increase to as much as 91 GW by 2030 [

13].

This paper will focus on addressing AWE and PEMEL, which are the currently available commercial technologies.

Alkaline Water Electrolyzer (AWE)

Alkaline water electrolysis is an electrochemical water splitting technique that involves the use of two electrodes, an anode and a cathode, which are submerged in a liquid electrolyte consisting of 30–40 wt% potassium or sodium hydroxide (KOH or NaOH) [

21]. Two electrodes are separated by a diaphragm to allow the transport of hydroxide ions (

). When a direct current (DC) is applied across the electrodes, the water-splitting process begins. First, the reduction of alkaline water occurs at the cathode, which is where the hydrogen evolution reaction (HER) takes place. During this process, two moles of alkaline solution are initially reduced to produce one mole of

and two moles of

. The produced hydrogen gas can be eliminated from the cathodic surface, while the remaining

moves through the porous separator towards the anode side. At the anode, the

is discharged, resulting in the oxygen evolution reaction (OER), which produces half a molecule of

and one molecule of

[

15,

17].

Commercial AWE offers technical aspects such as efficiency in the range of 58–78%, operating temperature between 70 and 90 °C, current densities in the range of 0.2–0.8

, production capacities in the range of 500–30,000

, and low-purity hydrogen (99.9%) [

7,

21]. AWE faces a significant obstacle in achieving high current densities due to two primary challenges. Firstly, the moderate mobility of

and the usage of corrosive KOH electrolytes limit the current density. Secondly, the sensitivity of KOH to

can lead to the formation of salt, which reduces the concentration of

and conductivity. The presence of salt can also cause the anode gas diffusion layer’s pores to close, thereby limiting the transfer of ions and reducing the production of hydrogen [

17].

Polymer Electrolyte Membrane Electrolyzer (PEMEL)

PEMEL is made up of several components, including an electrolyte membrane, which selectively allows H

+ protons to flow and spatially separates the anode and the cathode compartments of the cell, electrodes, usually made of platinum or iridium-coated titanium substrate, bipolar plates, to separate individual cells and provide electrical connectivity between them [

17].

When a DC current is passed through the electrodes, the anode becomes positively charged and the cathode becomes negatively charged. At the anode, water is oxidized to form oxygen gas and protons (

). The protons produced at the anode migrate through the PEM to the cathode, where they combine with electrons (

) from the external circuit and hydrogen ions (

) from the cathode catalyst to form hydrogen gas. The hydrogen gas and oxygen gas produced at the electrodes are then collected and separated for use [

17].

Commercial PEMEL offers technical aspects such as efficiency in the range of 50–83%, operating temperature between 50 and 80 °C, higher current densities in the range of 1–2

, and production capacities in the range of 0.2–60

. The electricity consumption of a commercial PEMEL can reach 400 kW with a water consumption of approximately 25 L/h. Compared to the AWE, PEMEL produces high-purity (99.999%) hydrogen [

7,

21]. Overall, PEMEL has overcome some of the AWE drawbacks, such as the overall system efficiency, current density, and the purity of hydrogen produced. However, one of the key obstacles in the development of PEMEL is the significant cost associated with various components, such as electrode materials, current collectors, and bipolar plates [

15].

Emerging Technologies: Solid Oxide Electrolyzers (SOEC) and Anion Exchange Membrane (AEM)

While AWE and PEMEL stand as the most established technologies for hydrogen production through water electrolysis, recent advancements have facilitated the way for a variety of alternatives. Solid Oxide Electrolyzers Cells (SOECs) and Anion Exchange Membrane (AEM) Electrolysis have emerged as promising solutions.

The development of SOEC and AEM technologies has been driven by several key factors, including the need for enhanced efficiency, durability, and cost-effectiveness. Additionally, the advantages offered by these technologies, such as temperature flexibility, electrolyte versatility, and potential for non-precious metal catalyst utilization, have promoted research efforts towards their advancement.

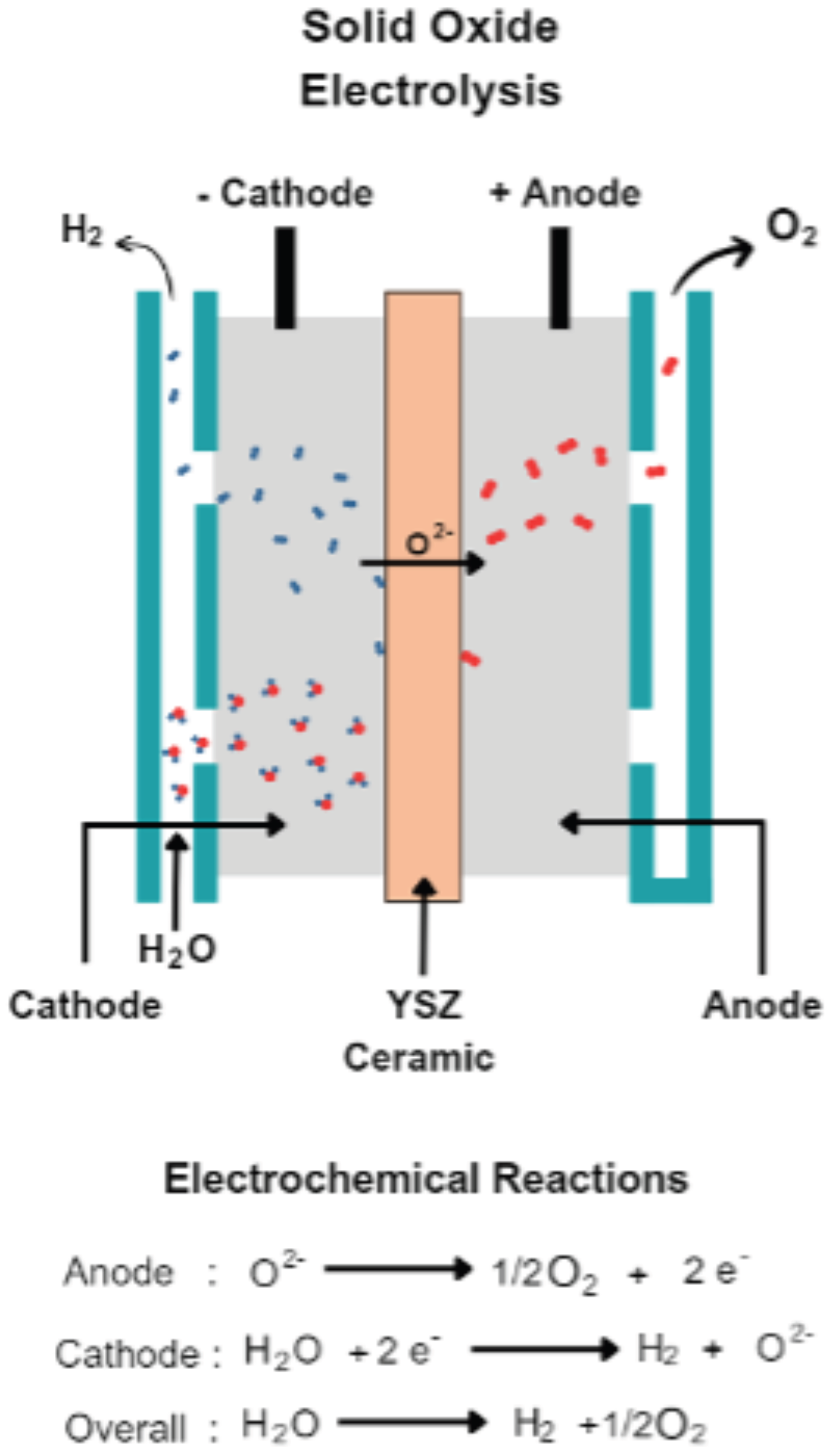

SOECs, like all electrochemical cells, consist of three primary components: a cathode (also referred to as a hydrogen electrode), an anode (referred to as the oxygen/air electrode), and an electrolyte. Typically, the anode comprises nickel and yttria-stabilized zirconia (YSZ), which acts as a porous electronic–ionic conductor. Conversely, the cathode is typically composed of lanthanum strontium manganite (LSM) due to its chemical and thermal stability. The electrolyte, usually made of YSZ, must possess high conductivity for

ions, be electrically insulated to prevent electronic conduction, and be dense enough to inhibit gas transport between electrodes [

22,

23].

Figure 3 shows a schematic representation of the operating principle of an SOEC.

On the cathode side, water molecules (steam) undergo electrochemical reduction to produce H

2 and

ions. Positioned between the anode and cathode, the electrolyte conducts oxygen ions to the anode, where they are oxidized to form oxygen molecules. Compared to AWE and PEMEL, this electrolysis process operates at high temperatures (800–1000 °C), this being the main advantage of this technology. This elevated operating temperature offers several advantages, including reduced ohmic losses, faster oxygen ion diffusion, and enhanced reaction kinetics, ultimately leading to improved overall efficiency [

24].

Regarding lifespan, numerous studies indicate that SOEC systems experience an average degradation rate of approximately 1% per 1000 h of operation, primarily attributable to the high operating temperatures. At an industry standard of replacing stacks when they reach 80% of their nameplate capacity, this degradation rate translates to a stack lifespan of approximately 2.5 years under full load. While this marks an improvement from just a decade ago when lifespans were less than half a year, it remains considerably shorter compared to PEM and alkaline technologies, which typically endure four to eight times longer [

25].

Despite their potential, SOECs face notable challenges, including limited stack power and the need for high operating temperatures. This requires the incorporation of supplementary equipment to support electrolyzer operation, leading to higher initial CAPEX. Currently, the largest SOEC systems deployed range from 100 kW to 1 MW in size. However, these installations predominantly serve as pilot or demonstration projects rather than being widely adopted for commercial use [

25].

AEM has emerged as a promising alternative to both PEMEL and AWE, offering potential solutions to some of their main challenges. Unlike PEMEL, which often struggles with catalyst stability and high cost due to the requirement of Platinum Group Metal (PGM) materials, AEM electrolysis employs non-precious metal catalysts, thereby significantly reducing costs while maintaining comparable efficiency. Additionally, AEM electrolysis offers improved durability and resistance to degradation compared to AWE, which typically suffers from electrode corrosion and requires highly pure water to prevent membrane fouling [

26,

27].

In AEM electrolysis, electrodes play a crucial role in facilitating the electrochemical reactions. Typically, these electrodes are composed of materials like nickel, nickel-based alloys, or other non-precious metals. These materials are chosen for their cost-effectiveness and durability in the harsh electrolysis environment. Unlike traditional PEMEL, which uses acidic electrolytes, AEM electrolyzers employ alkaline electrolytes. This choice offers several advantages, including increased conductivity and lower electrode corrosion rates. The backbone of this technology lies in the anion exchange membrane, which spatially separates the hydrogen and oxygen evolution reactions while allowing hydroxide ion (OH

−) migration. As a result, hydrogen ions (H

+) generated in the cathode recombine with electrons in the cathode to form hydrogen gas, while OH

− moves to the anode to produce oxygen gas [

28].

One of the key advantages of AEM electrolysis is its potential for cost reduction compared to other electrolysis technologies. By using non-precious metal catalysts and alkaline electrolytes, AEM electrolyzers can offer lower CAPEX and OPEX, making hydrogen production more economically viable. However, AEM electrolysis also has some drawbacks. The performance of AEM electrolyzers can be affected by membrane stability issues, such as chemical degradation and membrane fouling. Furthermore, the alkaline environment may limit the choice of electrode materials and catalysts, potentially impacting overall efficiency and durability [

29].

2.1.2. Electrolytic Hydrogen Production Equipment

Electrolyzers are the primary devices used for hydrogen production. However, in large-scale facilities, a more detailed subsystem is required to operate each technology successfully. These subsystems, also known as Balance of Plant (BoP), are essential for the optimal functioning of the main unit and involve a series of different equipment, depending on the technology used. BoP of hydrogen systems include subsystems such as water treatment, power supply, heat exchangers, cooling systems, piping, instrumentation, and control systems [

7].

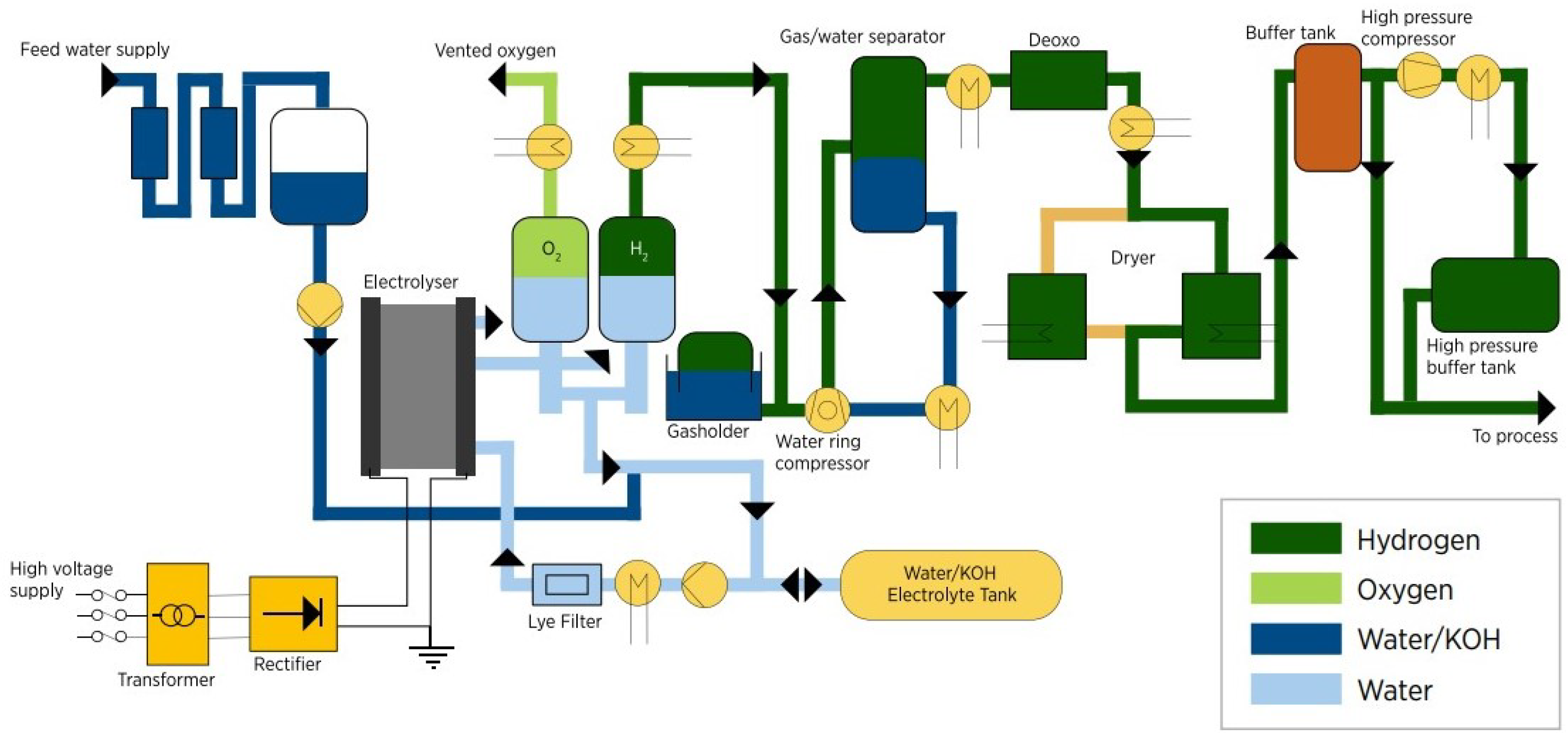

AWE Production Process Flow

The alkaline water hydrogen system comprises several components, including an alkaline electrolyzer stack, hydrogen and oxygen separators, a gas cooler, a lye circulating pump, a lye cooler, a water storage tank, an alkali tank, control valves, and other power electronics [

30].

Figure 4 presents a chart of the production process flow using an AWE.

The alkaline water electrolysis process begins by mixing the electrolyte in the alkali tank and pumping it into the electrolytic tank to initiate the hydrogen production process. The alkali solution is electrolyzed in the alkaline electrolyzer, resulting in a two-phase mixture of liquid electrolyte and product gases leaving the electrolysis stack. This mixture is then separated through the hydrogen and oxygen separators while the liquid is recirculated by centrifugal pumps. The hydrogen is then purified to reduce the oxygen concentration and water concentration by using a catalytic deoxo purification device and an adsorptive dryer to obtain high-purity products. The electrolyte flowing in the closed loop is kept at a controlled temperature (around 70 °C) through the use of a combination of shell-and-tube heat exchangers [

31,

32].

During electrolysis, water and alkali solution levels need to be periodically checked and replenished. The generator needs to be gradually pressurized to the set pressure by the regulating valve, which takes about 1 h [

30].

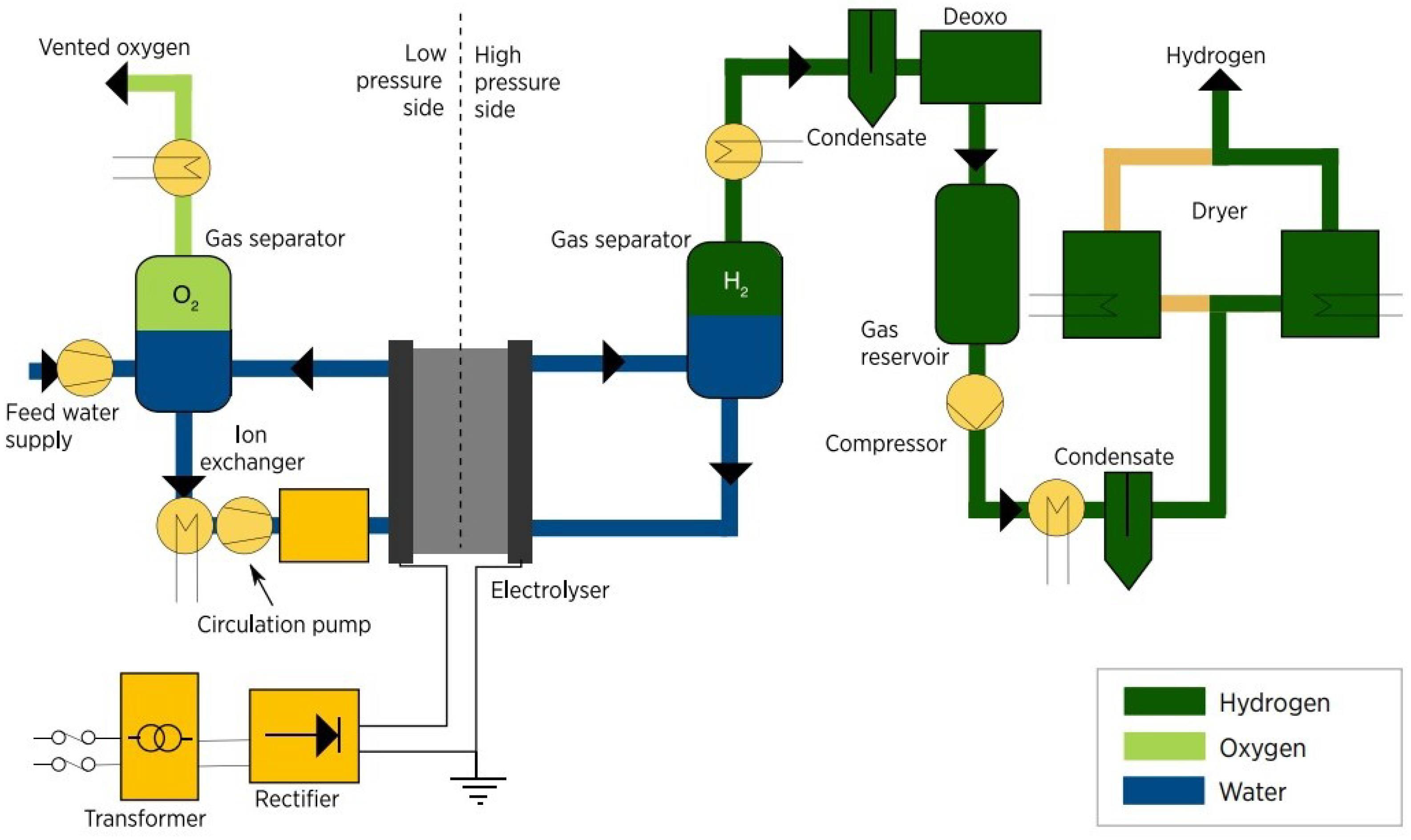

PEM Electrolysis Production Process Flow

The process begins by introducing de-ionized water into the oxygen separator. To ensure that the system remains unharmed, the water’s conductivity must be kept below 0.1 μS/cm [

33]. The water is then transported to the electrolyzer stack, which is considered the most critical part of the system. Before entering the electrolyzer stack, an ion exchange resin cartridge is employed to maintain low water conductivity. The water and oxygen produced are both emitted from the stack at the anode outlet and sent back to the oxygen separator. The temperature inside the system is regulated by a heat exchanger and is typically kept between 60 °C and 80 °C. Here, it is important to mention that if the produced oxygen is not required for another process, it is usually released into the atmosphere. Otherwise, it is subjected to drying and purification treatments. Only the anode side of the system is responsible for circulating water [

33].

Figure 5 presents a chart of the production process flow using a PEMEL.

On the other side, on the cathodic side, hydrogen and water are released as a gas mixture and then cooled to be separated at the hydrogen separator. Water is returned to the oxygen separator. The hydrogen is then purified to reduce both oxygen and water concentration below 5 ppm by using a catalytic deoxo purification device and an adsorptive dryer, respectively, before being stored. While the cathodic side maintains a pressure of up to 30 bar, the oxygen side is typically kept at ambient pressure to simplify system design and minimize cross-permeation [

33]. In addition, power and control electronics and safety equipment are also included in the system.

2.1.3. Sources for Renewable Electricity Production

Hydrogen is a versatile energy carrier that can be produced from a wide variety of resources. While most hydrogen is currently produced from fossil fuels, particularly natural gas, the use of electricity from the grid or renewable sources like wind, solar, geothermal, and biomass is also gaining momentum. In the longer term, direct generation of hydrogen from solar and wind energy is a viable option. Hybrid systems, such as those incorporating wind and solar energy, as well as hydropower plants, offer further alternatives for hydrogen production from green electricity. In recent years, there have been significant advances in electrolysis and renewable energy production, making the production of green hydrogen economically feasible [

34].

One of the primary obstacles in transitioning to renewable energy sources is their intermittent nature. Unlike fossil fuels, renewable energy sources such as wind and solar energy are vulnerable to fluctuations in weather conditions, making it difficult to regulate their output. However, hydrogen can act as a valuable energy storage solution, offering a means to overcome this challenge [

35]. The upcoming sections will present several promising technologies that can produce green hydrogen using renewable resources. We will explore the significant advantages and disadvantages of each method and offer an outlook on their potential.

Solar Energy

Solar energy is a natural resource that is both clean and renewable, making it an attractive alternative to traditional energy sources. In fact, the amount of sunlight that reaches the Earth’s surface in just one hour is enough to exceed the total global energy consumption for an entire year [

36]. Over the past few decades, there has been significant progress in the development of solar-driven

production technologies. These advances have been driven by the increasing demand for renewable energy, as well as improvements in the efficiency and cost-effectiveness of these technologies. Solar-driven hydrogen production technologies can be broadly classified into several methods, with photocatalytic (PC) water splitting, photoelectrochemical (PEC) water splitting, and photovoltaic (PV) water splitting being three of the most prominent technologies [

37].

PC water splitting involves the use of a semiconductor photocatalyst that is capable of absorbing light and generating pairs of charges. These charges can then interact with water molecules to produce both hydrogen and oxygen. PEC water splitting requires the use of specialized semiconductor materials immersed in an electrolyte solution. This process is similar to photovoltaic solar electricity generation, but instead of generating electricity, sunlight directly energizes the electrolysis process. Finally, the most promising method is PV water splitting, which involves using photovoltaic cells to generate electricity that drives the water splitting process. This process is being highly researched due to the current low cost of electricity production through PV panels [

37,

38].

Although all of these methods involve using direct sunlight to produce hydrogen, researchers have recently become interested in integrating electrolyzers with concentrated solar power (CSP) as a promising solution for green hydrogen production. By utilizing concentrated solar radiation, CSP plants can generate high temperatures to produce high-pressure steam to power a generator. The electricity produced is then used to drive the water-splitting process to produce green hydrogen [

37,

39].

Undoubtedly, photovoltaics applied to

, i.e., PV water splitting, is the most mature technology for solar-driven hydrogen production; therefore, we will provide some more details on this technology. The photovoltaic–electrochemical system is composed of two distinct components: the PV array and the electrolyzer. The PV array captures solar energy to generate electricity, which can be directly supplied to the electrolyzer for splitting water into hydrogen and oxygen at the cathode and anode [

37].

There are two possible configurations to connect the PV array with the electrolyzer: direct coupling and indirect connection. In the direct coupling method, the photovoltaic array and electrolyzer are optimally matched using a DC-DC controller and storage lithium battery. The inclusion of lithium-ion batteries in the system’s design is intended to address sudden increases in demand that the hydrogen system may be unable to manage. Maximum power point tracking (MPPT) is not included in this approach. On the other hand, the indirect connection method is more commonly used and involves the use of photovoltaic and control modules, batteries, and hydrogen storage systems. While this approach requires electronic equipment such as MPPT and DC-DC controllers, it can lead to some power transmission losses, reducing the overall efficiency and increasing costs [

40].

Therefore, the choice between the two methods depends on the specific application and system design. For instance, direct coupling may be preferred for small-scale applications where the system can be optimally matched, while indirect connection may be more suitable for large-scale systems where electronic equipment can be used to manage power fluctuations and optimize system performance. Although the PV array is directly connected to the electrolyzer, it is kept outside of the water–electrolyte solution to prevent corrosion.

Solar photovoltaics and water electrolysis are well-established technologies that have already been commercialized, making PV water splitting more advantageous than any other solar-driven H

2 production technology. Commercial PV cells and electrolyzers have high efficiencies, with PV cells surpassing 18% and electrolyzers ranging from 60% to 83%. As a result, a PV solar energy-to-hydrogen overall efficiency greater than 10% is easily achievable [

37].

Figure 6 provides a schematic representation of a PV-to-hydrogen system.

Figure 6.

Schematic representation of a PV to

system (adapted from [

41]).

Figure 6.

Schematic representation of a PV to

system (adapted from [

41]).

Wind Energy

Wind energy is also a renewable and clean source of electricity that can be harnessed to produce hydrogen through the process of water electrolysis. Wind turbines generate electricity in the form of alternating current (AC). However, DC is required for the water electrolysis process. To achieve this, the AC power generated by the wind turbine is first transmitted to an AC/DC converter. The converter transforms the AC power to DC power, which is then supplied to the water electrolysis system [

42]. There are different ways to configure a wind–electrolysis system H2Spectrum:

Direct configuration: The electricity generated by the wind turbine is used immediately for water electrolysis without being converted to another form of energy first. This configuration is particularly well suited for use in remote areas where wind farms are located.

Hybrid wind/grid electrolysis: Combines electricity from both wind turbines and the electrical grid to power the water electrolysis process. In this configuration, when there is insufficient or fluctuating wind power available, the electrolyzer can draw electricity from the grid to ensure a continuous supply of power for the electrolysis process. This can increase the overall efficiency of the system and ensure a reliable source of hydrogen production.

Surplus Wind Energy: Uses excess electricity generated by wind turbines to power the electrolysis process. When wind turbines generate more electricity than is needed by the grid or energy storage system, the surplus electricity is used to power the electrolyzer and split water into hydrogen and oxygen.

Each of these configurations can have a storage unit installed to store hydrogen. The storage of hydrogen is an essential aspect of wind–electrolysis systems, as the electricity generated from wind turbines can fluctuate depending on the weather conditions. Thus, storing the produced hydrogen during periods of excess wind power can enable the utilization of the stored hydrogen during times when the wind is not strong enough to generate enough electricity.

Figure 7 provides a schematic representation of a wind–electrolysis system.

Figure 7.

Schematic representation of a wind-to-

system (adapted from [

43]).

Figure 7.

Schematic representation of a wind-to-

system (adapted from [

43]).

Wind turbines can be installed either onshore or offshore, and both types of installations can be paired with an electrolyzer to produce hydrogen. While most wind turbines are located onshore, offshore installations have the potential to generate more energy per turbine. This is because offshore wind farms typically experience more consistent and stronger wind speeds than onshore wind farms, resulting in more efficient turbine operation and higher energy generation. In addition to more consistent and stronger winds, offshore wind turbines can typically generate more electricity than onshore turbines because they have higher capacity [

35,

42].

Although offshore wind power parks have the potential to be a valuable source of renewable hydrogen production, their electricity production costs are typically higher than other renewable resources. This is because of the significant expenses associated with logistics, larger tower structures, construction costs, and grid connectivity equipment. These factors require significantly larger capital investments compared to onshore wind farms, making offshore wind power a more expensive option for hydrogen production [

42].

Other Sources

Renewable energy sources, such as wind and solar, have already established themselves as crucial in green hydrogen production. These sources have been widely studied, and the production process using them has been well established. However, other renewable sources, such as hydropower, have also shown promise as potential sources for green hydrogen production. Hydropower is a mature technology with low GHG emissions that has been in use for decades. The advantages of hydropower for hydrogen production are several. Firstly, existing hydropower facilities can be used for hydrogen production without the need for additional infrastructure, which reduces the capital cost. Secondly, the cost of electricity generated by hydropower is low compared to other renewable energy sources, making it a cost-effective option for hydrogen production. Moreover, the utilization rates of hydropower plants are high, making them a reliable and efficient source of electricity for hydrogen production. However, there are some disadvantages to hydropower for hydrogen production, including the location of facilities and the potential for environmental impact.

Despite these challenges, new projects are emerging in locations benefiting from hydropower resources. In 2020, a 2 MW electrolysis plant was opened in Switzerland at the Gösgen hydropower plant under the ‘Hydrospider’ joint venture. Additionally, Southeast Asia’s first integrated H

2 production and vehicle refuelling station was commissioned in Sarawak, Malaysia, which includes a 500 kW electrolysis plant based on hydropower supply [

40,

44,

45].

2.2. Hydrogen Storage

Hydrogen is increasingly seen as a promising energy carrier considering its high energy content per unit mass of 120 MJ/kg. However, it presents challenges for efficient and cost-effective storage due to its low volumetric density of approximately 0.08238 kg/m

3 under normal temperature and pressure, resulting in a low energy content per unit volume of only 0.01 MJ/L [

46]. Addressing these challenges will be critical to realizing the full potential of hydrogen as a clean and renewable energy asset. There are several methods available to store hydrogen, each with its own advantages and limitations, making them suitable for different applications. The selection of an appropriate storage system depends on several factors, such as the type of application, the required energy density, the amount of hydrogen to be stored, the storage period, the capital and operating cost, and the local resources available [

47]. Hydrogen storage can be classified into two main categories: small-scale and large-scale storage.

2.2.1. Small-Scale Hydrogen Storage

For the hydrogen economy to thrive, it is necessary to have small-scale storage methods that enable the transportation and distribution of hydrogen for various applications. Small-scale storage is defined by its limited capacity and short-term storage period. Examples of potential applications for small-scale storage include residential, transportation, and power applications, such as heating, stationary fuel cells for FCEV, and emergency backup power units. Although other storage options can be employed for small-scale hydrogen applications, including chemical storage methods, this discussion will focus on the most established and commercially available options that are best suited for current hydrogen energy systems.

Compressed Storage

Under normal temperature and pressure, the density of the H

2 gas is very low, near about 0.08238 kg/m

3 (e.g., for storing 5 kg of hydrogen, a volume of around 60 m

3, with an energy content of 166.65 kWh, is required). For the same weight and energy content, the required gasoline volume is 0.019 m

3 [

46]. Thus, it is clear that to achieve cost-efficient storage, hydrogen density should be increased. Compressed storage is the most established storage technology for hydrogen; it involves the physical storage of hydrogen in high-pressure vessels capable of withstanding pressures of around 170–700 bar [

47]. Typically, steel tanks are used to store hydrogen, but for weight considerations, tanks made of carbon fiber lined with aluminum, steel, or specific polymers are also used. Compressing hydrogen is necessary to increase its storage density, but it is also an energy-intensive process that consumes about 13–18% of the lower heating value of hydrogen [

46]. At 35.0 MPa, the density of compressed hydrogen is around 23 kg/m

3, while at 70.0 MPa, it is around 38 kg/m

3 [

47].

Compressed hydrogen storage is primarily carried out aboveground, but it is also possible to store it underground, especially for fueling stations, as it reduces land use. This approach minimizes the risk of accidents, as the storage tanks are isolated from public areas. However, underground storage increases the difficulty associated with inspection and maintenance, which is crucial for ensuring the safe and reliable storage of hydrogen. Currently, the fuel cell vehicle industry requires hydrogen to be pressurized to 350–700 bar in vessels with storage capacities from 2 to 5 kg [

48], while stationary storage applications require capacities ranging from 100 to 1300 kg, with storage pressures ranging from 10 to 300 bar [

47]. These requirements must be met to ensure that hydrogen storage and distribution systems can efficiently support the growing demand for clean energy.

Liquid and Cryocompressed Storage

As previously mentioned, hydrogen is known for its lower energy density per unit volume compared to other fuels, making it necessary to have larger storage tanks to store the same amount of energy. To address this issue, the liquefaction of hydrogen is a potential solution. Compressed hydrogen at 200 and 700 bar and 288 K has a density of 15.0 and 40.2 kg/m

3, respectively, and heating values of 1.80 and 4.82 MJ/L. In comparison, hydrogen in liquid form at 1 and 3.5 bar and at its normal boiling point of 20 K (

°C) has a heating value of 8.50 and 7.68 MJ/L, respectively, and a density of 70.9 and 64.0 kg/m

3, respectively. Liquid hydrogen is approximately 1.8 times denser than high-pressure hydrogen at 700 bar and 288 K, highlighting its potential advantages in energy storage and transportation [

49]. However, the liquefaction process of hydrogen is energy-intensive, and it can consume up to 30% of the energy content of the stored hydrogen [

47].

Additionally, to minimize boil-off, it is necessary to maintain a constant pressure in the storage tank and ensure that it is well insulated. A cooling and venting system should also be in place to achieve this. Despite these challenges, liquid hydrogen presents a promising solution to overcome the energy density challenge of hydrogen storage and transportation [

47]. The need for thermal insulation in cryogenic hydrogen vessels highlights the technical challenges of storing and transporting liquid hydrogen. The use of vacuum insulation in double-walled vessels is a common solution to minimize heat loss and improve storage efficiency. However, boil-off losses remain a significant challenge that must be addressed to ensure the practicality and cost-effectiveness of using liquid hydrogen as a fuel.

On the other hand, to take advantage of the main characteristics of compressed and liquid hydrogen storage principles, cryo-compressed hydrogen storage has become an option. This method allows hydrogen to be stored at elevated pressures above ambient (1 bar) and at temperatures equivalent to or lower than its boiling point (

°C). By compressing hydrogen to 350 bar at

°C, its gravimetric and volumetric density can be increased from 70 g/L at 1 bar to 90 g/L, resulting in higher storage efficiency [

50,

51].

Cryo-compressed hydrogen storage technology offers the capability of filling the storage tank with compressed, cryo-compressed, or liquid hydrogen, presenting several advantages over other hydrogen storage methods, including a greater storage capacity and enhanced safety indicators. Despite these benefits, cryo-compressed tanks are not yet commercially feasible due to the availability of infrastructure and cost associated with this storage technique.

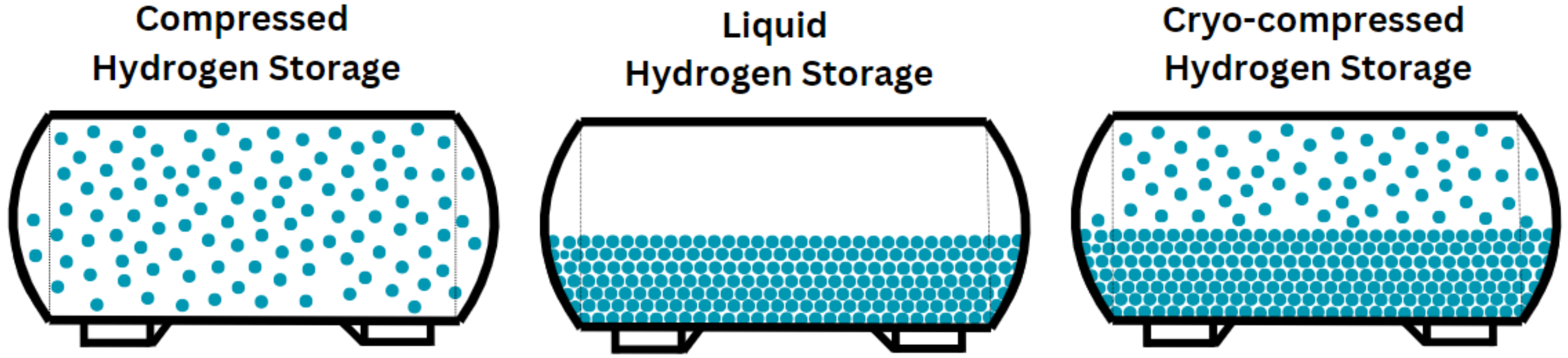

To visualize these storage methods, a schematic representation is introduced in

Figure 8 to illustrate the main differences of each storage type in terms of volumetric density. This figure clearly shows how compressed storage, liquid storage, and cryo-compressed storage compare in their ability to store hydrogen efficiently, highlighting the significantly higher volumetric density achieved through liquid and cryo-compressed storage compared to compressed and liquid storage.

2.2.2. Large-Scale Hydrogen Storage

A key challenge in realizing a viable hydrogen economy lies in establishing efficient and reliable storage systems that can bridge the gap between production facilities and smaller-scale storage units. In this context, the construction of large-scale storage facilities could be crucial in ensuring a consistent and ample reserve supply of hydrogen.

Cryogenic Storage

The initial capital investment for a new large-scale storage facility can be high due to the need for liquefaction equipment and storage. Additionally, the energy-intensive liquefaction process adds to the operating costs. However, investing in larger plants with higher liquefaction capacities can lead to cost savings in the long run. While the initial cost may be higher, the cost of hydrogen and the energy needed to liquefy hydrogen decrease per kilogram of hydrogen liquefied as the liquefaction capacity increases. Typical liquefaction capacities can range from 100 kg/h to 10,000 kg/h, allowing for a wide range of options depending on the specific needs of the facility. Onsite large-scale storage capacities can range from 115,000 kg to 900,000 kg, offering ample storage space to meet the demands of customers [

47].

Underground Storage

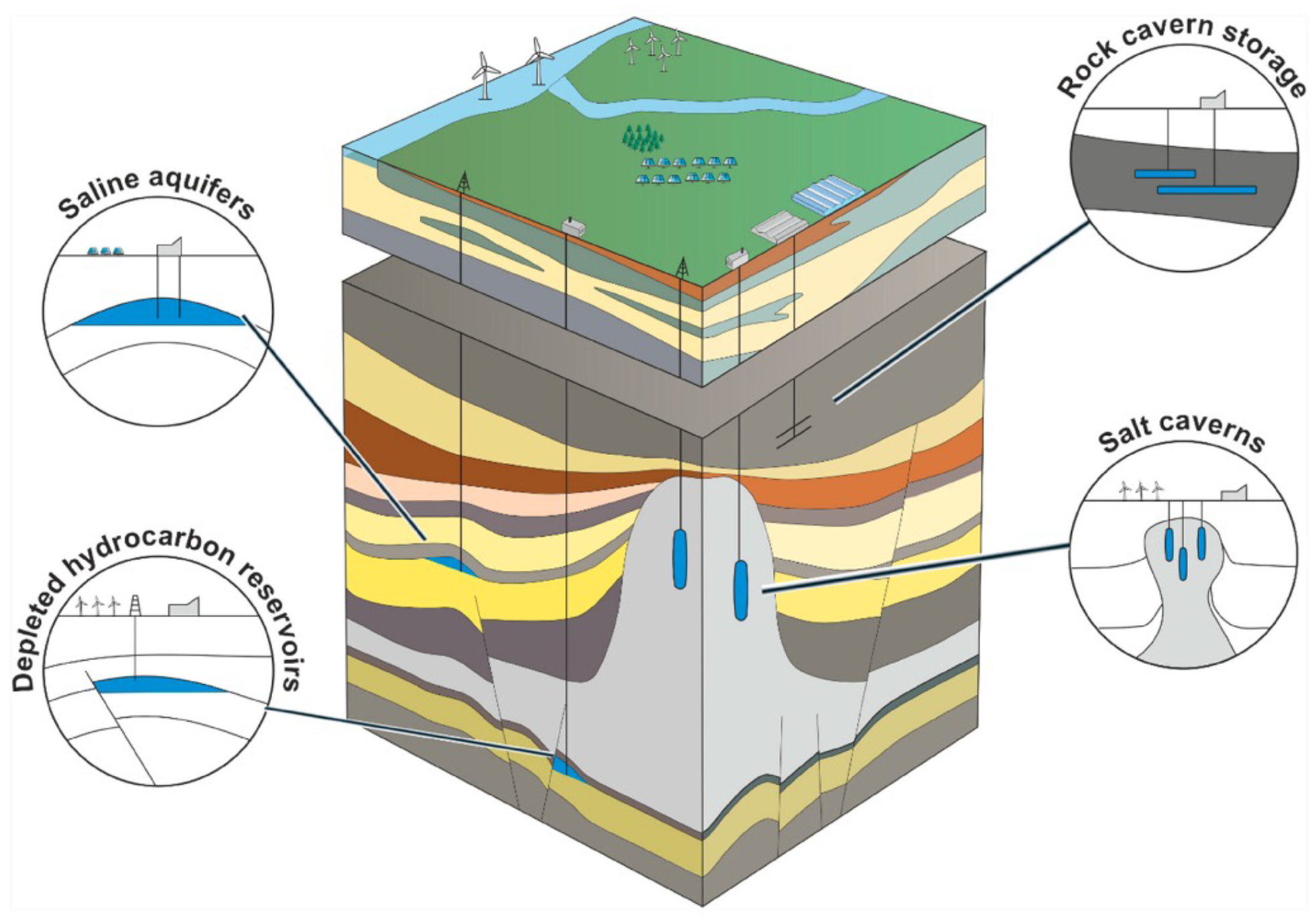

Natural underground formations, including aquifers, depleted natural gas fields, and manmade caverns such as salt caverns present a potential solution for hydrogen storage (

Figure 9). Aquifers are particularly attractive due to their water-bearing permeable rock or sand layers that can trap hydrogen injected at high pressure. In addition to aquifers, hydrogen can also be stored in the porous rock found in natural gas caverns [

52]. These hydrocarbon reservoirs, located deep beneath the subsurface, are known for their porous and permeable nature and because the vast majority of recoverable products have already been extracted from them. Depleted hydrocarbon reservoirs have a history of success as gas storage options, as they are known for storing hydrocarbons such as natural gas, and have well-established geological structures. Despite this, there is a potential risk to the purity of injected gas if the remaining gas in the reservoir is not properly managed, affecting the integrity of the stored hydrogen [

47,

53].

Figure 9.

Geological structures suitable for underground hydrogen storage (retrieved with permission from [

54]).

Figure 9.

Geological structures suitable for underground hydrogen storage (retrieved with permission from [

54]).

On the other hand, salt caverns offer secure and stable underground storage facilities for a range of materials, including oil, natural gas, and hydrogen. Formed by dissolving salt formations through the injection of fresh water under high pressure, salt caverns are typically found in underground salt domes. The pressure inside a salt cavern is critical and needs to be carefully monitored as it is affected by the amount of gas stored within it. With appropriate management, salt caverns provide a reliable and safe way to store hydrogen underground over extended periods [

47]. A typical salt cavern can be up to 2000 m deep, 1,000,000 m

3 in volume, 300 to 500 m in height, and 50 to 100 m in diameter, allowing for a huge storage capacity of hydrogen [

53].

2.2.3. Energy Carriers: Ammonia and Liquid Organic Carriers

Hydrogen faces considerable challenges in its storage and transportation due to its low volumetric energy density and demanding storage conditions. Addressing these limitations requires the transition to energy carriers with higher volumetric energy densities that can seamlessly integrate with existing infrastructure. Among these, ammonia emerges as a strong candidate. Ammonia (NH3) allows for the synthesis of a stable compound that has a large hydrogen storage capacity, providing an effective solution to hydrogen storage problems. The importance of this compound comes from its ability to be easily synthesized from two abundant elements—hydrogen and nitrogen—and its potential use as a vector for storing hydrogen.

One of the key advantages of using ammonia for hydrogen storage lies in its ability to store a significantly higher volume of hydrogen compared to liquid hydrogen itself. This stems from the fact that each molecule of ammonia contains three hydrogen atoms, making it a dense carrier of hydrogen. In its liquid form, ammonia holds approximately twice as much hydrogen by volume as liquid hydrogen, making it an efficient means of storing and transporting hydrogen. Moreover, ammonia has more common storage conditions than pure hydrogen, making it more feasible to store. Ammonia can exist as a liquid at far milder temperatures, about −33.3 °C at atmospheric pressure, whereas liquid hydrogen can only exist at extremely low temperatures, usually below −253 °C. Ammonia can be stored more conveniently because it stays liquid at room temperature when pressure is increased to about 10 bar [

55,

56].

However, it is essential to acknowledge the challenges associated with the dissociation process of ammonia back into hydrogen and nitrogen. This process typically involves catalysis at high temperatures, requiring a significant input of energy. Additionally, handling ammonia entails certain health and safety risks, necessitating careful consideration of safety protocols and regulations [

55]. Moreover, according to the World Economic Forum [

57], approximately 98% of ammonia value chain emissions stem from the hydrogen production stage, which is heavily reliant on fossil fuels.

Currently, the conventional method for producing ammonia, known as the Haber–Bosch process, is highly energy-intensive, relies heavily on grey hydrogen, and contributes to 73% of ammonia production, resulting in a high emission intensity of 2.4

per tonne [

57]. In this process, nitrogen (N

2) from the air reacts with grey hydrogen (H

2) under high pressures and temperatures in the presence of an iron catalyst to form ammonia (NH

3):

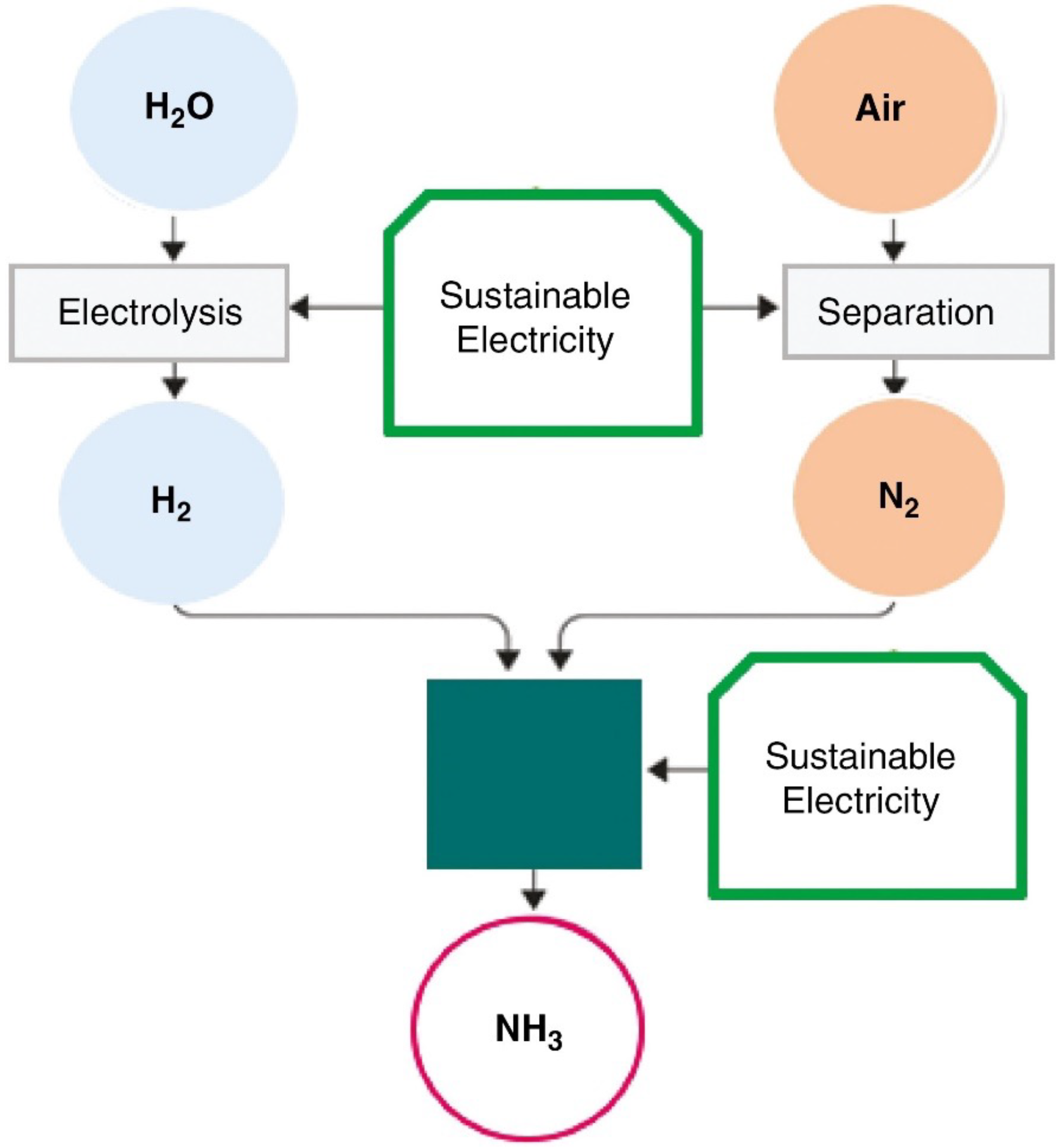

An alternative approach for green ammonia production involves using green hydrogen instead of hydrogen produced from fossil fuels. By integrating both the water splitting and the Haber–Bosch processes, the ammonia-related sectors can be decarbonized (

Figure 10). The production cost increase for low-emission production can vary from 40% to over 120% depending on the production route and region [

57].

Although this is the most promising alternative for large-scale production of green ammonia, it is important to acknowledge other innovative approaches, including direct electrochemical synthesis, electrocatalytic synthesis, photocatalytic synthesis, photoelectrocatalytic synthesis, and biocatalytic synthesis [

58].

Direct Electrochemical Synthesis: This method involves the direct conversion of nitrogen and water into ammonia using electricity, typically through an electrochemical cell. It aims to achieve high efficiency and selectivity under mild conditions.

Electrocatalytic Synthesis: Similar to the direct electrochemical approach, this method employs specialized catalysts to enhance the efficiency of nitrogen reduction reactions within an electrochemical cell, facilitating ammonia production at lower energy costs.

Photocatalytic Synthesis: This approach uses light-activated catalysts to drive the reduction of nitrogen to ammonia. Photocatalysis leverages solar energy, making it a potentially sustainable and environmentally friendly method.

Photoelectrocatalytic Synthesis: Combining aspects of both photocatalytic and electrocatalytic methods, this technique uses light and electrical energy together with catalysts to produce ammonia. It aims to maximize energy utilization from renewable sources.

Biocatalytic Synthesis: This method utilizes biological organisms or enzymes to catalyze the conversion of nitrogen into ammonia. It mimics natural nitrogen fixation processes and can operate under ambient conditions, offering a potentially low-energy alternative.

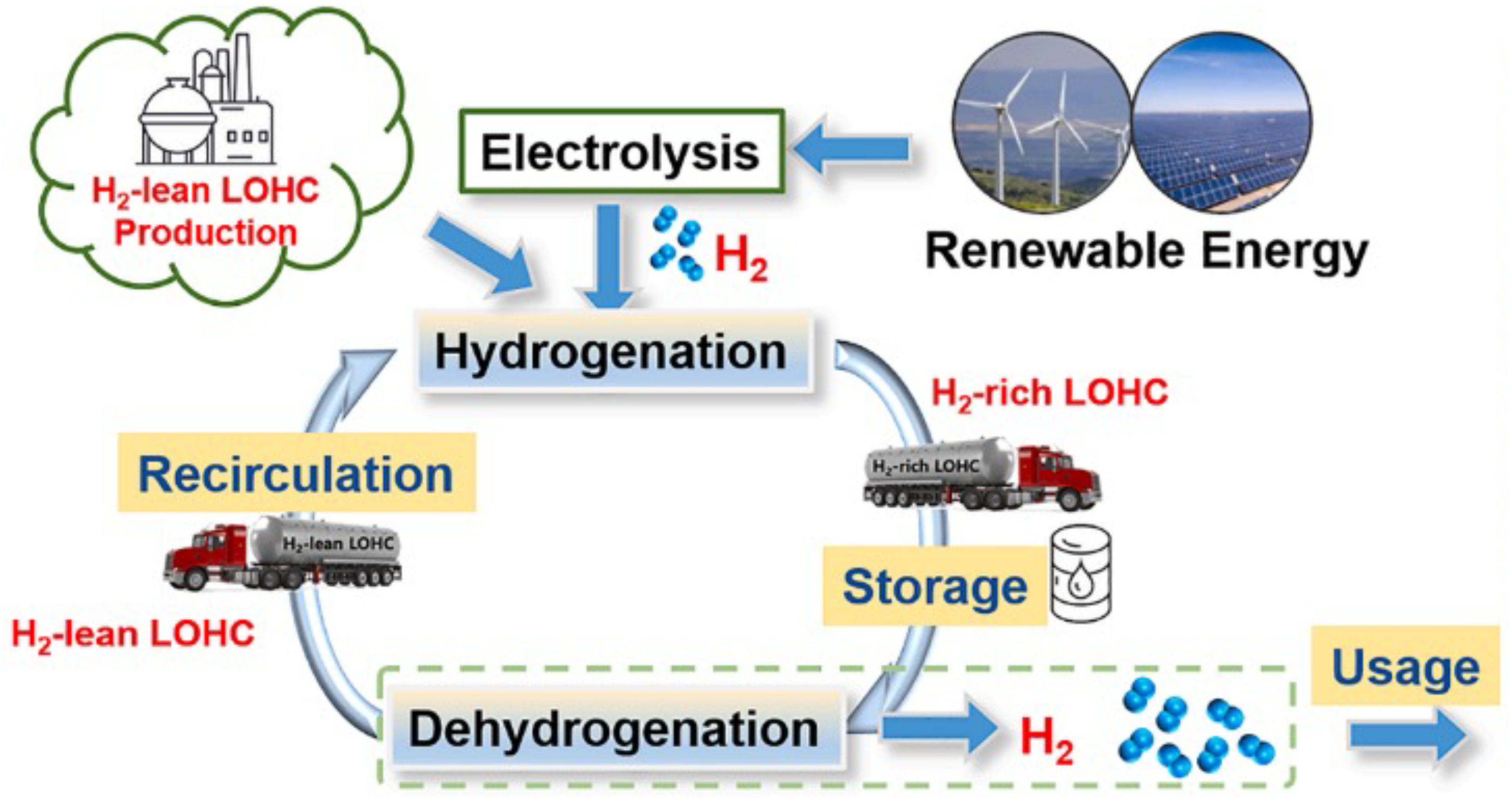

Large-scale hydrogen storage presents a critical challenge in realizing the potential of hydrogen as a clean energy carrier. One promising solution gaining traction is the use of Liquid Organic Hydrogen Carriers (LOHCs). LOHCs provide an attractive option for storing and transporting hydrogen in an efficient and safe manner, addressing key limitations of traditional methods.

LOHCs are characterized by their ability to undergo reversible hydrogenation and dehydrogenation reactions without significant degradation of their main carbon ring structure. These compounds exhibit specific chemical properties that enable them to efficiently absorb and release hydrogen while maintaining structural integrity. Compared to traditional hydrogen storage methods, LOHC technology offers a significantly higher storage capacity. The volumetric capacity can exceed a gravimetric capacity of 6 wt% (weight percent) [

59,

60].

Typically, these carriers are organic molecules such as N-ethycarbazole, dibenzyltoluene, naphtalene, and toluene/methylcyclohexane systems [

61]. During the hydrogenation process, hydrogen molecules are chemically bonded to the LOHC molecules under elevated pressure and moderate temperatures (100–200 °C). Conversely, during dehydrogenation, the LOHC releases hydrogen when exposed to higher temperatures (200–300 °C) and lower pressure [

62]. The reversible hydrogenation and dehydrogenation processes are facilitated by catalytic systems that enhance the reaction kinetics and efficiency. Commonly used catalysts include noble metals like palladium, platinum, and ruthenium, which provide the necessary activation energy for these reactions while maintaining high selectivity and stability [

63].

LOHCs represent a promising alternative for large-scale hydrogen storage, addressing key challenges associated with traditional storage methods. LOHC technology enables safe and efficient hydrogen storage and transportation using existing infrastructure, such as tankers, pipelines, and rail systems, thus integrating seamlessly into the current energy supply chain. Additionally, the recovery and reuse of LOHCs after hydrogen extraction highlight the sustainability and cost-effectiveness of this approach. This technology not only makes hydrogen a more viable clean energy source but also helps to build a strong and resilient hydrogen economy by ensuring a closed-loop system in which LOHCs can be cycled repeatedly (

Figure 11).

2.3. Hydrogen End-Use Applications

In 2021, the global demand for hydrogen surpassed 94 Mt. Refineries used about 40 Mt of this hydrogen as feedstock, reagents, or a source of energy. The remaining 50 Mt was consumed by various industries, with the chemical production sector accounting for 45 Mt and the steel and iron industry using the remaining 5 Mt. However, in this same year, there was also a slight increase in hydrogen demand for new applications in the heavy industry, transport, power generation, and building sectors, accounting for approximately 40 kt, around 0.04% of global hydrogen demand. The majority of this increasing demand came from road transportation, highlighting recent efforts to decarbonize the transport industry through advances in technology and policies for FCEVs [

13,

14].

Hydrogen is used by refineries in several processes, including removing sulfur and other impurities and upgrading heavy oil fractions into lighter products. It is estimated that in 2022, the refining sector will reach its maximum hydrogen demand, reaching 41 Mt, which is a 2.5% increase from 2021. This increase can be attributed to post-pandemic recovery in crude processing and regulations aimed at reducing sulfur emissions. The refining industry’s demand for hydrogen is largely met by a combination of by-product hydrogen and on-site production. Around half of the demand is met through by-product hydrogen, which is generated from other processes within the refinery such as catalytic naphtha reforming or from other petrochemical processes integrated into certain refineries such as steam crackers. The remaining demand is met through dedicated on-site hydrogen production. On-site hydrogen production is mainly achieved through natural gas reforming and coal gasification [

13].

In 2021, the United States was the largest consumer of hydrogen for refining applications, accounting for around 10 Mt. However, despite the current lead of the U.S., China has the largest installed refinery capacity and is expected to account for nearly 70% of the global net refinery additions during the 2019–2023 period [

14].

Currently, hydrogen is primarily used in industry for producing chemicals such as ammonia and methanol, and as a reducing agent in iron and steel manufacturing processes (DRI (direct reduced iron) is the product of direct reduction of iron ore in the solid state by carbon monoxide and hydrogen). Additionally, other industrial applications require smaller amounts of hydrogen, including various processes in electronics, glassmaking, and downstream chemical industries. As of 2021, the total demand for hydrogen for industrial applications was approximately 55 million metric tons. Ammonia production was the largest consumer, accounting for around 62% of the total share, followed by methanol production with almost 27%, and 9% for the steel and iron industry. The remaining 2% share was accounted for by the remaining applications mentioned before [

14].

As global demand for ammonia and methanol continues to rise, the overall industry sector is expected to see a corresponding increase in demand for hydrogen. By 2030, it is expected that this demand will rise by 30% and approach 50% by 2050 [

13]. Given that the majority of hydrogen is currently produced from fossil fuels, the transition to a more sustainable energy system for industry is required. Green hydrogen production is expected to play a critical role in this process, enabling a reduction in CO

2 emissions from industry while meeting the growing demand for ammonia, methanol, iron, and steel.

According to 2020 statistics [

64,

65], the transport sector has become the second largest contributor to the energy crisis, with a share of 29% of the total final energy consumption and 20.3% of GHG global emissions. It has the highest dependency index on fossil fuels compared to other industries, with 37% of global CO

2 emissions originating from transportation end-use. In the past decade, CO

2 emissions from the transportation sector have exhibited the fastest growth due to the increasing demand and the limited low-carbon emission technology options available for the industry [

66].

The four main contributors to global CO

2 emissions from transport are road, aviation, shipping, and rail transportation. Nearly 75% of these emissions stem from road vehicles, most of which come from cars and buses (45% of emissions), and the remaining 30% originate from trucks. Aviation, shipping, and rail transportation contribute approximately 12%, 11%, and 2% of the total CO

2 emissions, respectively [

67].

To address the increasing need for energy consumption and reduce GHG emissions in the transport sector, electric mobility has emerged as a strong option for clean transportation. FCEV has demonstrated high potential in storing and converting chemical energy into electricity, offering advantages such as high energy conversion rates, efficient drivetrain, and zero carbon dioxide emissions compared to conventional gasoline vehicles.

By 2021, hydrogen demand for the transportation sector has accounted for over 30 kt, showing more than 60% of increasing demand compared to 2020. In the transportation sector, road vehicles are the primary driver of demand for hydrogen fuel. Global FCEV deployment has been concentrated largely on passenger light-duty vehicles (PLDVs), constituting 74% of registered FCEVs in 2020, and heavy-duty vehicles such as trucks and buses, which have higher annual mileage and weight requirements than fuel cell electric cars. In 2021, demand for hydrogen from commercial vehicles surpassed that of buses for the first time, accounting for 45% of the total hydrogen demand in the transportation sector [

13,

14].

The building sector is a significant contributor to global carbon emissions, and hydrogen presents an opportunity to reduce the carbon footprint of buildings and improve energy efficiency. One of the primary applications of hydrogen in the building sector is for heating. Hydrogen boilers can replace traditional natural gas boilers, making them a zero-emission alternative for heating. However, the co-existence between natural gas equipment and hydrogen could also support decarbonization in a very specific context where gas infrastructure already exists. Several pilot projects are currently underway in various countries, testing the feasibility of hydrogen boilers for residential and commercial heating by using the natural gas pipeline. Natural gas currently meets 35% of global energy demand for heating, and blending hydrogen with natural gas can leverage existing infrastructure without requiring major modifications in some regions. At volumes of 5–20%, hydrogen blending can provide a low-carbon alternative to natural gas, reducing emissions and contributing to decarbonization efforts [

13,

14].

Another use of hydrogen in buildings is for co-generation, which involves producing both heat and electricity simultaneously. Co-generation systems can be powered by hydrogen, offering a more efficient and low-carbon way of producing energy. These systems can be used in various building types, including hospitals, data centers, and apartment buildings [

68].

Fuel cells, reciprocating engines, and gas turbines are some of the technologies that can utilize hydrogen as a primary or secondary fuel. Fuel cells are considered the best option for zero-emission electricity production since they directly convert the chemical energy of hydrogen into electrical energy through an electrochemical process. This results in relatively high efficiencies and zero greenhouse gas emissions, making fuel cells ideal for clean power generation applications. Fuel cells can also operate at lower temperatures, which simplifies their design and reduces maintenance requirements.

Reciprocating engines and gas turbines are also being developed to use hydrogen as a primary or secondary fuel. These technologies have been traditionally used with fossil fuels and can operate on a mixture of gases where hydrogen is the main component up to 70–95%. This enables them to provide clean power while still being compatible with the existing infrastructure [

13,

14].

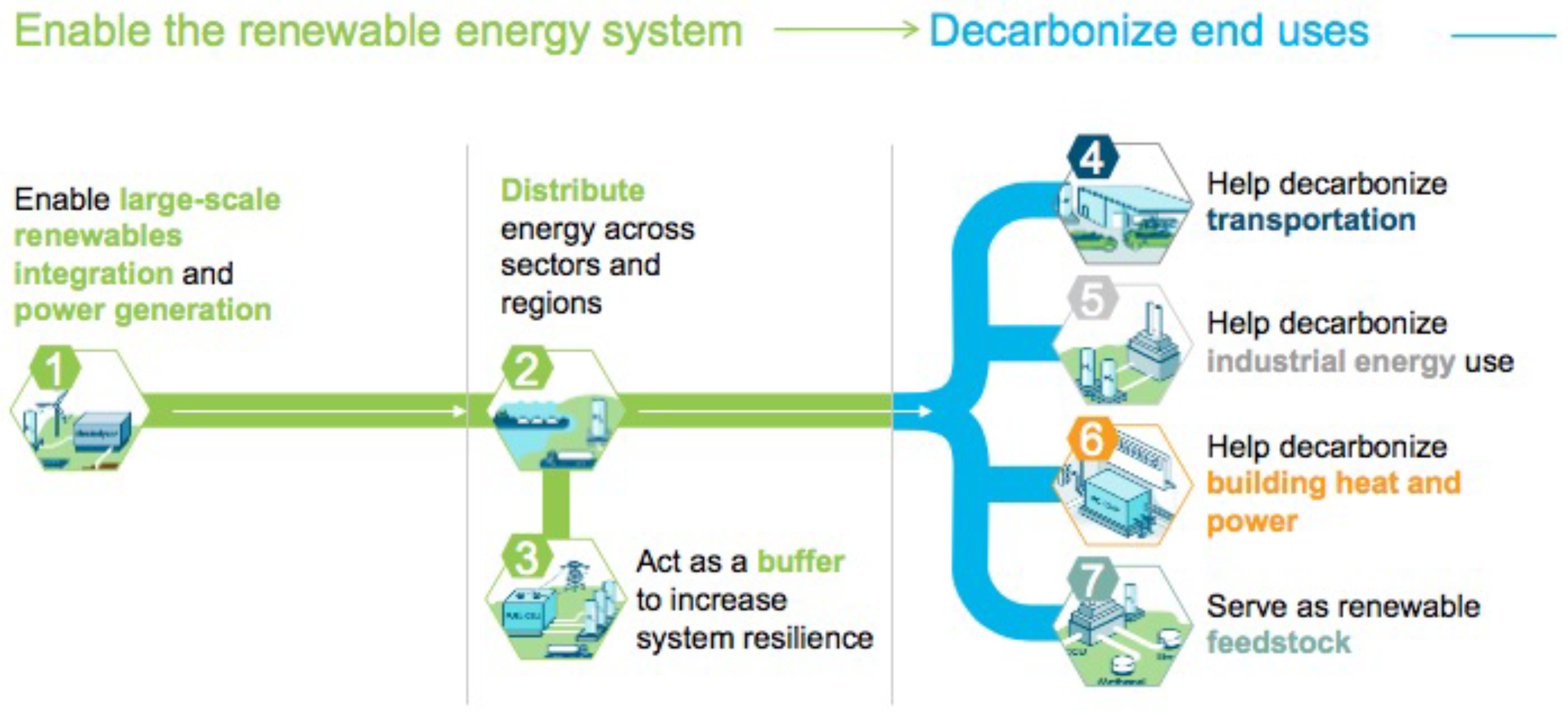

Figure 12 shows hydrogen’s role in decarbonizing major sectors of the economy.

Figure 12.

Hydrogen’s role in decarbonizing major sectors of the economy (retrieved with permission from [

69]).

Figure 12.

Hydrogen’s role in decarbonizing major sectors of the economy (retrieved with permission from [

69]).

3. Economic Analysis—Levelized Cost of Hydrogen (LCOH)

To assess the viability of hydrogen energy systems, a comprehensive evaluation of their technical and economic aspects is essential. This involves assessing the entire process, from the generation of the required electricity using PV panels and wind turbine generators (WTGs) to the production of hydrogen through an electrolyzer. To achieve a complete understanding of the system’s performance, it is crucial to determine each cost component in detail.

Similar to how the levelized cost of energy (LCOE) serves as an indicator for comparing the cost of electricity produced from renewable sources, the levelized cost of hydrogen (LCOH) is a commonly used metric for comparing the costs of producing hydrogen from various energy sources [

70]. LCOH offers a comprehensive view of the costs involved in producing one kilogram of hydrogen by considering the capital expenditures (CAPEX) and operational expenditures (OPEX) of the projects, production efficiency, system lifetime, performance degradation, and the cost of energy used [

71]. This metric proves to be particularly advantageous as it allows for a direct comparison of different energy sources and technologies.

The CAPEX are related to expenses to acquire or upgrade physical assets such as property, buildings, or equipment to produce hydrogen. This component is strongly affected by the renewable energy system adopted, the electrolyzer technology selected, either AWE or PEMEL, the necessary balance of the plant (BoP: drier, cooling, de-oxo and water de-ionization equipment), and the characteristics of the auxiliary services involved, such as water treatment, the compression and cooling system or hydrogen storage, among others. On the other hand, the OPEX costs are related to operating and maintaining the production facility. It is the expenditure incurred in the normal operation of the plant’s production. This estimate considers water consumption, the cost of renting the land, or the annual maintenance required for all the assets [

72].

The findings from the state-of-the-art chapter have enabled us to gain a macro-level understanding of the structure and functionality of hydrogen production systems as well as their main components. In this section, we are going to address the economic assessment of green hydrogen energy systems.

The LCOH can be calculated by considering the total capital and operational costs, as well as the cost of electricity consumed over the project’s lifetime. To accurately reflect the time value of money, it is crucial to account for the discount rate for each cost component. This indication is given by Equation (

3) given in EUR/kg of produced H

2.

where:

is the upfront investment cost.

is the annual O&M cost in year j.

is the annual electricity cost in year j.

is the end-life cost.

is the annual hydrogen production.

N is the total system lifetime.

a is the discount rate

As a result, the LCOH indicator provides valuable information about the average price at which hydrogen must be sold to ensure the project is financially viable [

71].

IRENA has identified three primary factors that are essential for ensuring the economic sustainability of hydrogen production from renewable sources. These factors include the capital expenditure associated with the electrolysis process, the LCOE required for powering the process with renewable energy, and the annual load factor (equivalent full load hours) of the system [

5]. Keeping a hydrogen production plant running for longer operating hours can result in lower production costs per unit of hydrogen. This is because the total cost of the project can be spread out over a larger quantity of hydrogen produced. Ideally, electrolyzer load factors should be above 50% to achieve low costs, but load factors above 35% can still be cost-effective. However, if the production plant runs for only a few hours, the LCOH will increase significantly [

5]. Therefore, it is important to assess the availability of renewable sources for each project to ensure a reliable and cost-effective supply of energy.

Currently, the dominant player in the hydrogen market is grey hydrogen, largely due to its low hydrogen production cost, which typically ranges from EUR 0.63–1.23/kg. However, there is a growing expectation that blue hydrogen will emerge as the primary pathway for hydrogen production. Blue hydrogen uses a carbon capture and storage (CCS) system to prevent emissions. Typically, the production cost of natural gas-based blue hydrogen is around EUR 0.93–1.72/kg. Despite its potential benefits, the CCS technology is still in the nascent stages and faces challenges in terms of its high cost and low

capture efficiencies. Green hydrogen is currently the most expensive option, costing around EUR 2.14–6.95/kg to produce [

40].

When considering renewable energy sources, wind power stands out as an attractive candidate for producing green hydrogen due to its cost-effective electricity generation. However, the production of hydrogen from wind power is vulnerable to fluctuations caused by changes in weather conditions. Solar energy, on the other hand, is a widely available and long-lasting source of energy, but its intermittency presents a challenge for hydrogen production. Moreover, additional equipment such as batteries or MPPT may be required to optimize solar electricity generation, which can increase the overall cost of producing hydrogen.

Although solar PV and wind are the primary focus of this economic analysis, given their promising performance–cost balance in green hydrogen production, it is essential to consider the LCOH for other renewable energy sources. A recent study [

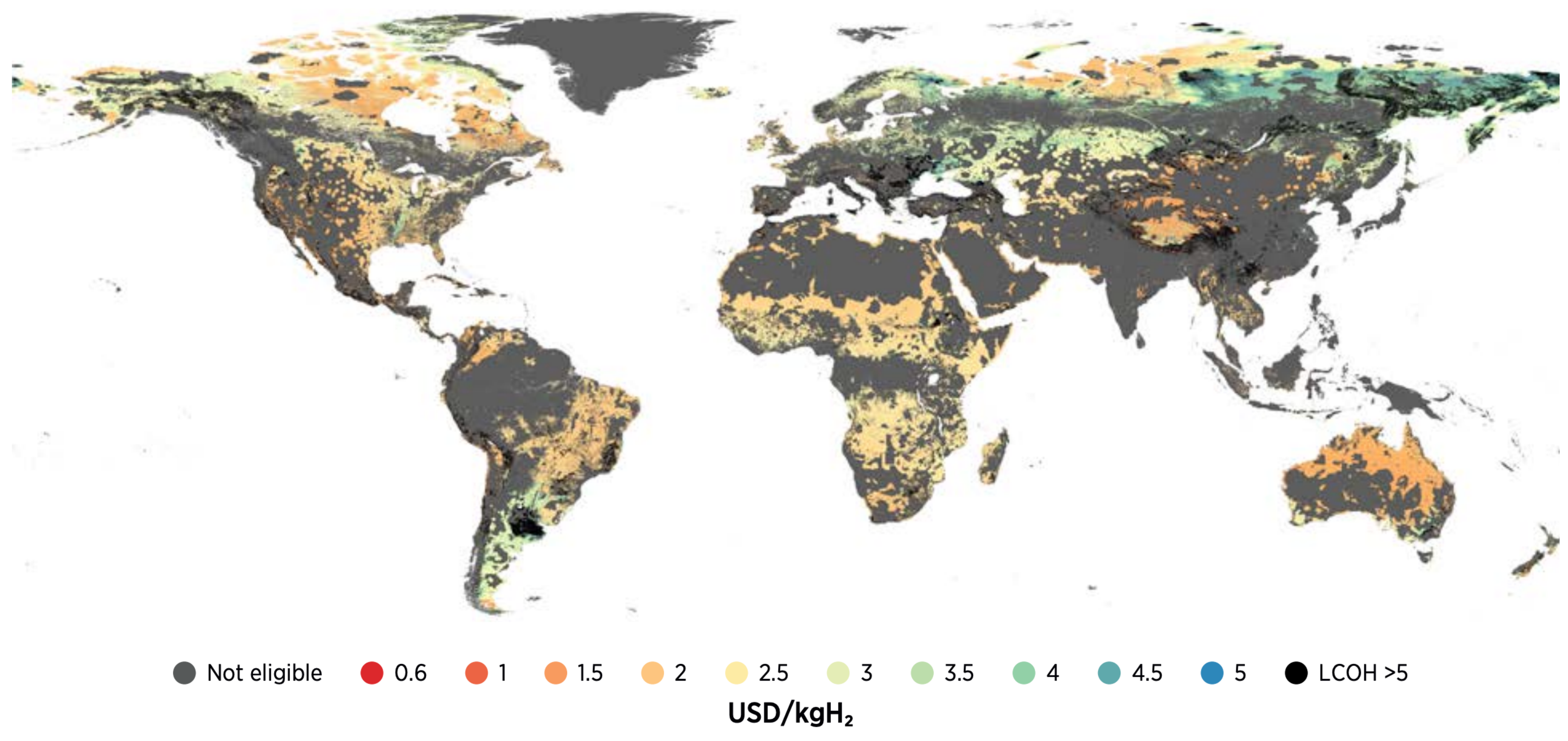

35] (see

Table 1) conducted in various locations worldwide, including Ontario, Chile, and Patagonia, indicates LCOH intervals for different energy sources and explanations for why some values are lower than others.

It can be concluded from

Table 1 that the most economical option for the electrolysis process is using grid electricity, followed by solar PV electricity and onshore wind. This is mainly due to the low cost of electricity production in these technologies, which contributes significantly to the overall hydrogen system. On the contrary, solar CSP and offshore wind technologies still face significant cost reduction challenges due to the high CAPEX and OPEX costs associated with electricity production. Another crucial factor that significantly impacts the LCOH is the capital cost associated with the electrolyzer stack. Currently, AWE remains the cheapest alternative due to several factors, including lower capital costs, higher stack lifetime, and lower operational costs.

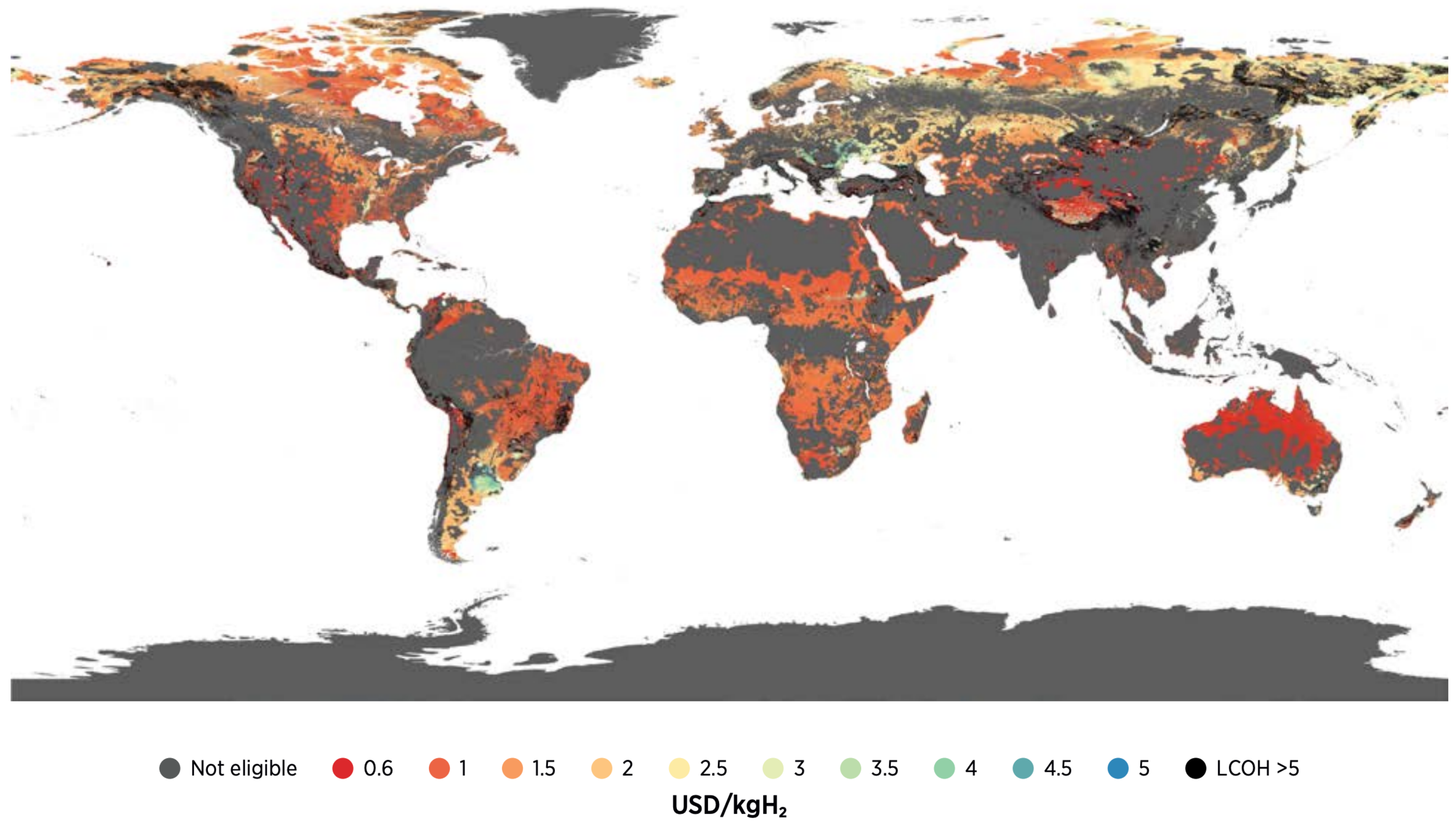

Given the ongoing global efforts towards decarbonization across several sectors, the IRENA’s Global Renewables Outlook for 2050 [

73] has identified a significant reduction in the cost of producing green hydrogen through the use of solar and wind energy sources. As a result, these two resources are projected to be the primary driver for the electrolysis process, taking into account the reduction in electrolyzer costs and

emissions. With an anticipated reduction in electrolyzer costs of 30% and 45% by 2030 and 2050, respectively, cost-competitive LCOH of around EUR 1.41/kg for wind-to-hydrogen systems and EUR 1.88/kg for solar-to-hydrogen systems is expected.

From another perspective, a report from 2020 on behalf of the International Council on Clean Transportation [

74] estimated the future cost (2050) of hydrogen production in the US and EU using three different electricity sources: (i) grid-connected; (ii) RES-connected; and (iii) using only otherwise curtailed energy. The main findings are reported in

Table 2.

3.1. Levelized Cost of Energy (LCOE)

The Oxford Institute for Energy Studies has established that for 2019, the cost of electricity accounted for around 70% of the share for green hydrogen production [

75]. However, some of the available renewable technologies already achieve competitive LCOE compared to conventional fossil fuel technologies for electricity generation [

76]. Onshore wind technology exhibited the lowest LCOE in 2021, at a rate of 0.03 EUR/kWh. On the other hand, hydropower and utility-scale solar PV closely follow with an LCOE of 0.05 EUR/kWh for both technologies. Furthermore, the data highlight that solar PV has experienced the most rapid reduction in cost per energy generated, with an impressive 88% decrease over the past decade.

To better comprehend these findings, it is vital to analyze the changes in the total installed cost and capacity factor over the past ten years. In [

77], the total installed cost, the capacity factor, and the LCOE for utility-scale solar PV and onshore and offshore wind are presented. Upon analyzing the case of onshore wind, it is evident that the capacity factor has increased from 27% to 39%. This improvement may be attributed to technological advancements, such as larger turbines, increased rotor diameters, and higher hub heights, which enhance the turbines’ efficiency. Additionally, the total installed cost has decreased due to economies of scale and projected new wind projects. The convergence of these two factors has led to a 68% decrease in LCOE between 2010 and 2021. Although this reduction is lower than that of solar PV, it still constitutes a significant decrease, indicating a positive outlook for the future.

In contrast to onshore wind, the case of solar PV differs significantly. Although the LCOE has dropped dramatically, the capacity factor has not seen much improvement, increasing only from 13.8% in 2010 to 17.2% in 2021. However, it is expected to increase in the upcoming years due to advances in trackers in utility-scale solar plants. The reduction in the cost of converting solar PV energy into electricity is due to the decrease in the total installed cost, combined with the slightly increasing capacity factor and declining operation and maintenance costs [

77]. It is noted that these data represent a global weighted average. However, it is known that solar and wind generation characteristics differ across regions, and this variability can have a significant impact on hydrogen production costs and output. Regions with high-capacity factors generally benefit from lower electricity generation costs, resulting in reduced expenses for hydrogen production [

71].

However, according to the consultant in assurance and risk management Det Norske Veritas (DNV) predictions, by 2050, both solar and wind energy will become significantly cheaper. Specifically, the average cost of solar PV energy is expected to drop by at least 40%. Solar PV is predicted to be the most cost-effective source of new electricity globally, despite its lower capacity factors compared to other renewable energy sources. Additionally, the increase in installed capacity along with cheaper and more efficient turbines will drive down the costs of onshore wind energy by 52% from 2020 to 2050, while fixed and floating offshore costs will decrease by 39% and 84%, respectively [

78]. The widespread deployment of wind and solar power generation is crucial in bringing down the expenses related to renewable electricity. This cost reduction will be essential for enabling the large-scale production of green hydrogen.

3.2. Electrolysis Systems

Currently, the second main cost driver for green hydrogen production is the electrolysis system, accounting for around 15% of the total share [

75]. Although PEM and AWE are commercially available and established, they are still considered highly expensive in terms of both CAPEX and OPEX. However, it is expected that both technologies will experience a significant decrease in overall cost as hydrogen production based on electrolysis continues to grow. Additionally, global policies aimed at decarbonizing various sectors with hydrogen as an energy source are directing efforts towards improving the performance of AWE and PEMEL technologies and achieving economies of scale.

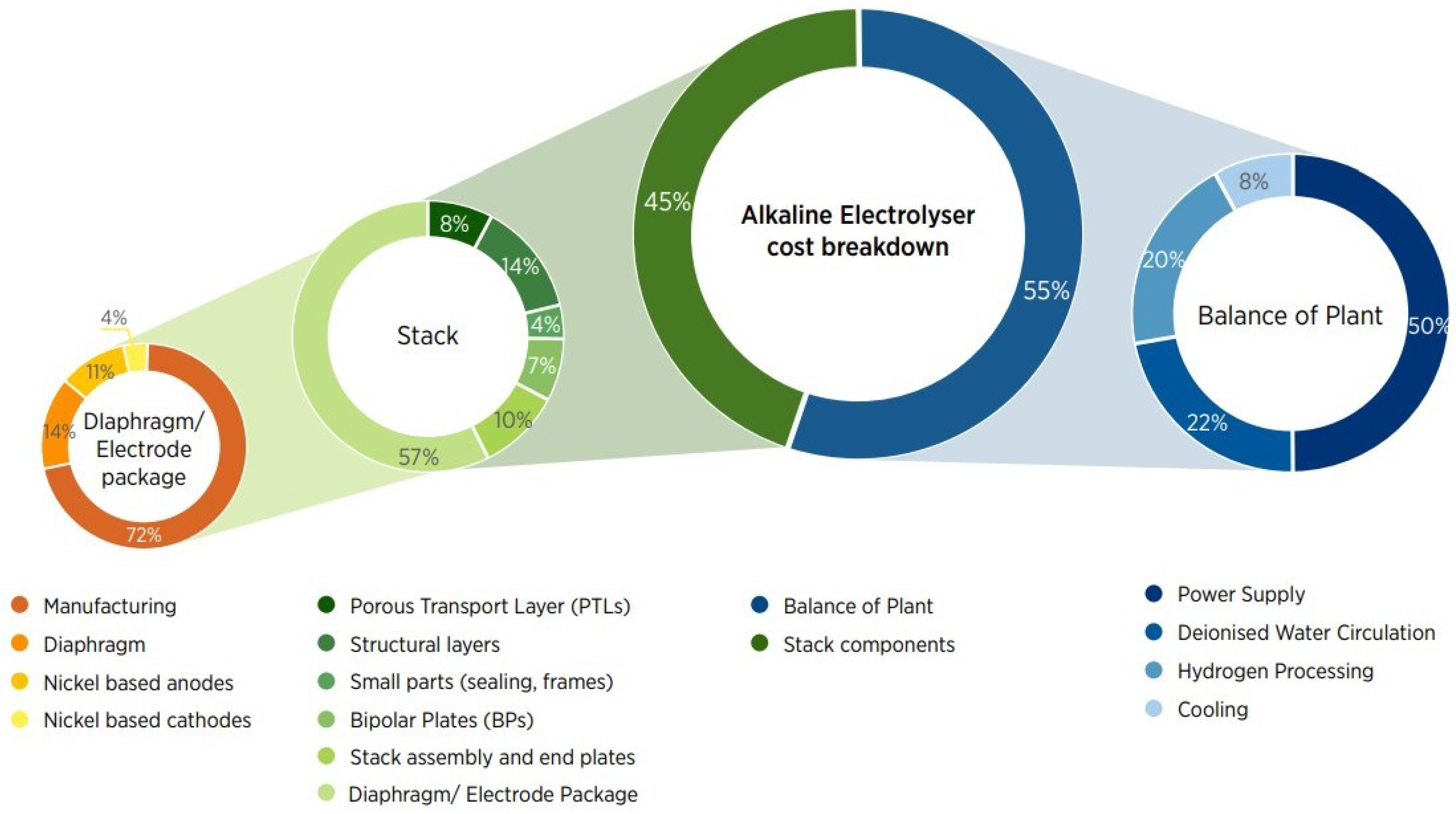

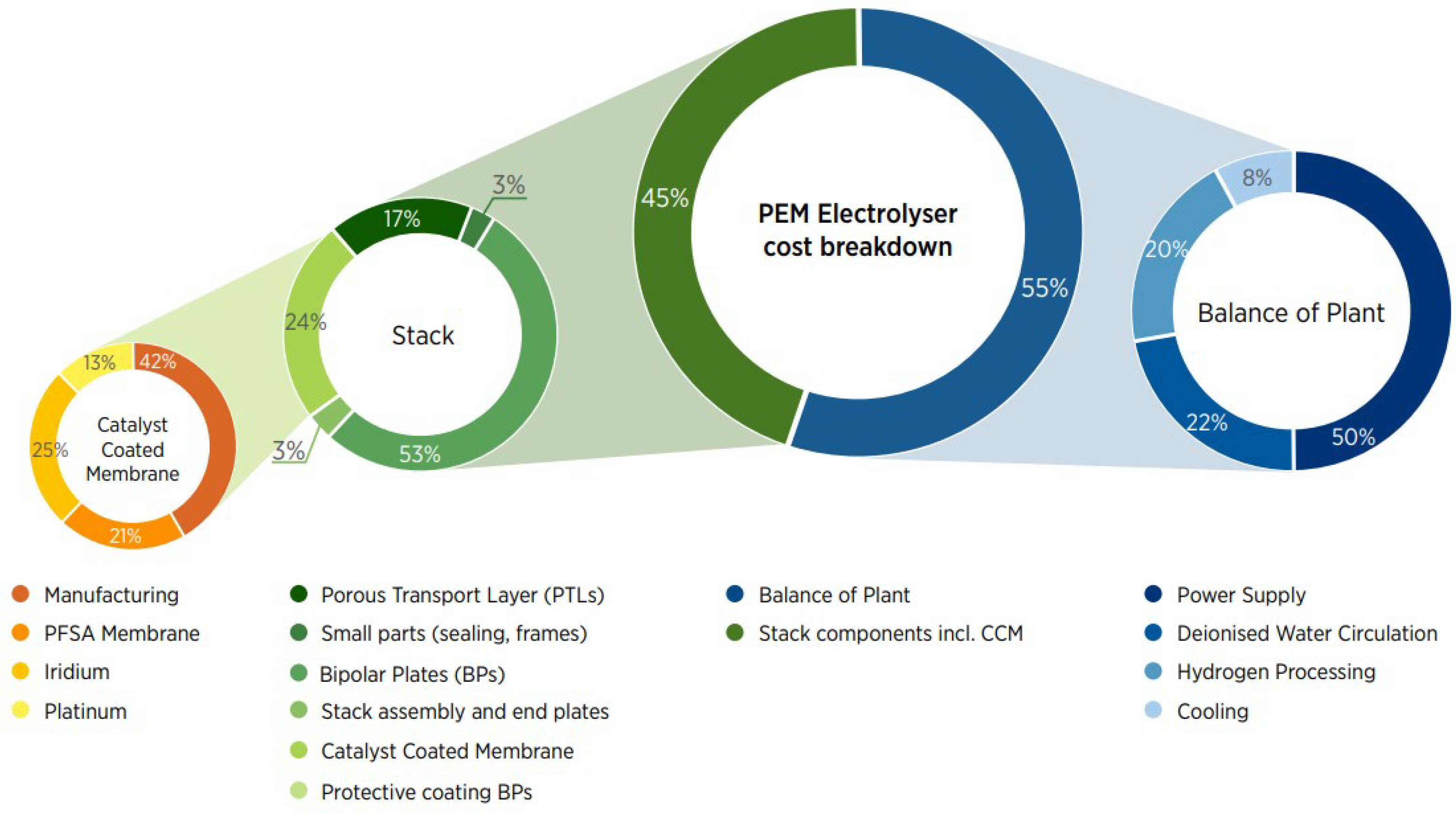

As stated before, an electrolysis system is mainly composed of an electrolyzer stack and the different components that allow the optimal functioning of the unit, namely the BoP. IRENA has determined that the electrolyzer stack accounts for approximately 45% of the total cost of the electrolysis system, while the BoP accounts for the remaining 55% for both PEMEL and AWE systems [

7]. However, it is important to state that this share is highly dependent on each manufacturing strategy, business case, design, and technical specifications.