Regulation of Small Modular Reactors (SMRs): Innovative Strategies and Economic Insights

, , , , and

, , , , and

Abstract

1. Introduction

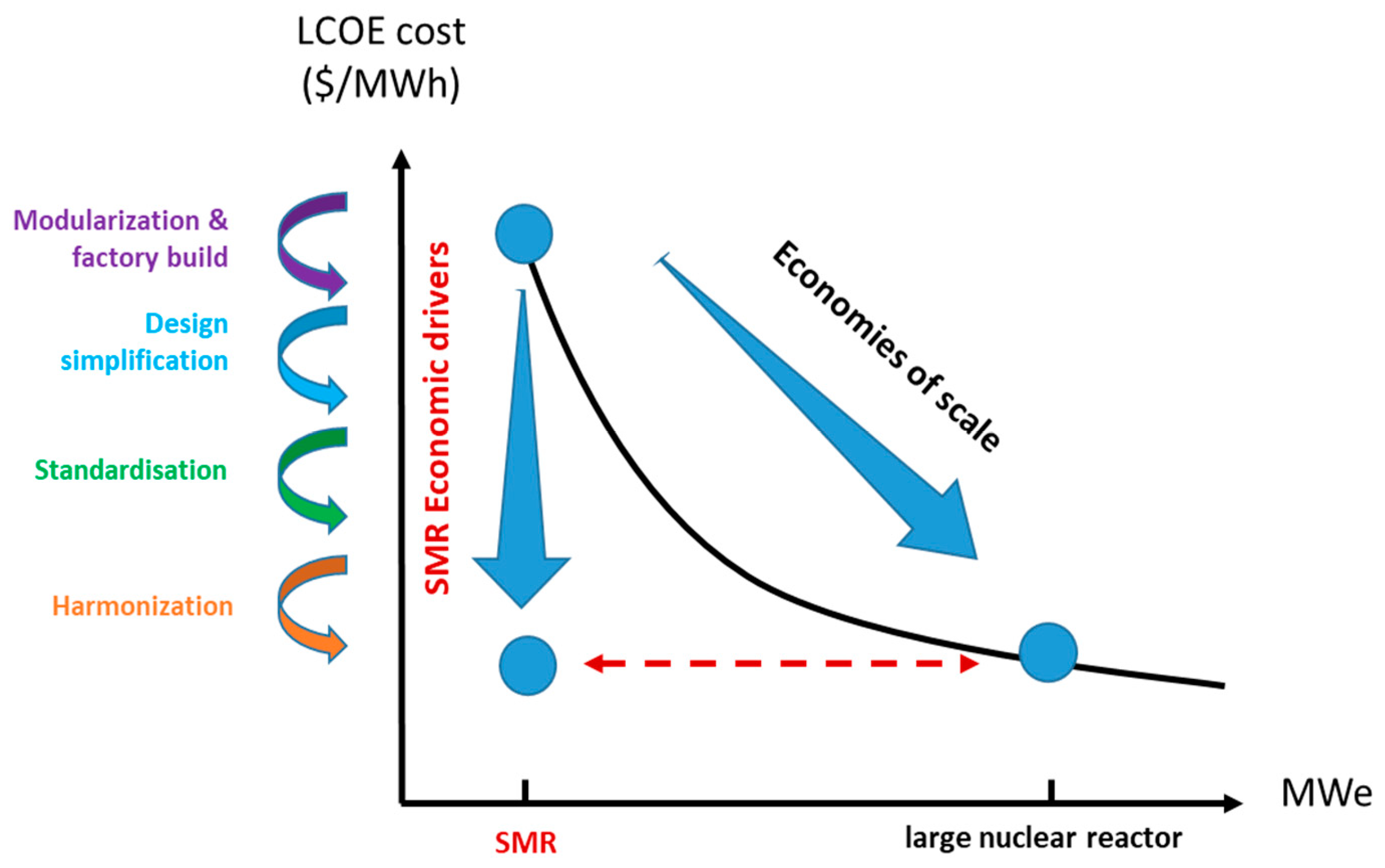

Comparative Analysis: SMRs Versus Large Nuclear Reactors

2. Literature Review

2.1. SMR Development and Grid Integration

2.2. Economic Imperatives

2.3. Licensing, Regulatory Challenges, and Opportunities

2.4. Environmental Considerations and Waste Management

2.4.1. Life Cycle Assessment (LCA)

2.4.2. Advanced Fuel Cycles: Implications for Waste Management

2.4.3. Decommissioning in the Age of Modularity: New Approaches and Challenges

2.5. Security and Non-Proliferation

2.5.1. Cybersecurity for Digital SMRs: A Critical Challenge

- Increased attack surface: Digital systems expand potential entry points for cyberattacks [42].

- Supply chain security: Ensuring the integrity of complex supplier networks is crucial, as compromised components could introduce [43].

- Remote monitoring and control: Features for remote operation may be exploited by malicious actors if not properly secured [44].

- Evolving threat landscape: The nuclear sector requires adaptive cybersecurity strategies to address constantly evolving threats [45].

2.5.2. Physical Protection Strategies for Distributed SMR Deployment

- Perimeter security: Adapting physical barriers and surveillance systems for varied deployment scenarios [47].

- Insider threats: Implementing personnel reliability programs and access controls to mitigate insider risks [48].

- Transportation security: Securing the transport of fuel, components, and reactor modules [49].

- Emergency response: Coordinating with local law enforcement and emergency services for effective response [50].

2.5.3. Safeguards by Design: Integrating Non-Proliferation into SMR Development

- Material accountancy: Designing systems for easy monitoring and verification of nuclear material [53].

- Containment and surveillance: Simplifying the application of containment and surveillance by inspectors [54].

- Remote monitoring: Developing secure systems for remote transmission of safeguarding data [55].

- Proliferation resistance: Incorporating features like long-life cores or low-enriched fuel to enhance proliferation resistance [56].

2.6. Global SMR Initiatives: Lessons and Insights

2.6.1. United States

Case Study: NuScale Power US600

- Best Practices for Future SMR Applications:

- Early Pre-Application Engagement: Early interaction allowed NRC to familiarize itself with the design and resolve issues pre-emptively.

- Focus on Highly Challenging Issues (HCIs): Early identification and resolution of HCIs led to efficient processing.

- Streamlined Safety Evaluation Report: A focused approach on critical safety issues provided a clearer regulatory basis.

2.6.2. Canada

2.6.3. United Kingdom (UK)

- Streamlined Process: The Office for Nuclear Regulation (ONR) and Environment Agency now use a flexible, stepwise approach for earlier regulatory feedback [74].

- Increased Efficiency: The adapted GDA reduces assessment time and resources while maintaining safety standards [75].

- International Alignment: Bilateral agreements, such as with the Canadian Nuclear Safety Commission, harmonize SMR regulatory approaches [76].

- Advanced Nuclear Fund: A GBP 385 million fund supports SMRs and Advanced Modular Reactors, underscoring the commitment to nuclear innovation [78].

- UK SMR Consortium: Led by Rolls-Royce, this consortium includes industry, academia, and government to develop a UK SMR design [79].

- Regulatory Engagement: Early developer–regulator interactions address potential challenges proactively [80].

- Design Philosophy: The design uses UK nuclear supply chain capabilities and modularity to cut costs and construction times [82].

- Government Support: The project received GBP 210 million in government funding, matched by private investment [80].

- Regulatory Progress: Rolls-Royce SMR entered the GDA process in 2021, testing the new regulatory framework [83].

- Market Potential: The design has domestic and export opportunities, with potential UK sites under consideration [84].

- Job Creation: The project could create up to 40,000 jobs, highlighting economic benefits [77].

2.6.4. China

2.6.5. Russia

2.6.6. Korea

3. Materials and Methods

3.1. Data Sources and Collection

3.2. Data Processing and Validation

3.3. Economic Analysis

Assumptions

- The SMR operating parameters, timelines, and FOAK values for capital and operating costs were obtained from the report [14], which presents an optimistic outlook and is representative of estimated costs and expected performance.

- We assume that the primary use of the SMRs will be electricity generation and, as such, a wholesale electricity price of USD 50/MWh is selected.

- The assumed electricity price is based on data provided by the [91], which reports that the average wholesale electricity price across the major trading hubs in the U.S. in 2020 ranged from USD 22/MWh to USD 77/MWh. The chosen price of USD 50/MWh is approximately the midpoint of this range, making it a reasonable estimate.

- We also assume the insurance cost to be 0.05% of the OCC.

- In our analysis, we do not factor in additional regulatory costs, taxes, or government support mechanisms and incentives, such as production tax credits, investment tax credits, or other similar financial support mechanisms.

3.4. Sensitivity Analysis—Technology Adoption Rate

- Scenario Development: We developed optimistic, base case, and pessimistic scenarios to provide a range of potential outcomes. These scenarios incorporate different assumptions about technological progress, regulatory environments, and market conditions.

- Monte Carlo Simulation: We conducted 10,000 simulations using Latin Hypercube sampling to account for uncertainties in key parameters and factors affecting SMR adoption.

- Sensitivity Analysis: We calculated correlation coefficients to determine the sensitivity of the adoption rate to each factor. This helps identify which factors have the most significant impact on SMR adoption rates.

- Distribution Analysis: We analyzed the probability distribution of adoption rates in I 2050 to understand the range and likelihood of various outcomes. This provides insights into the most probable adoption rates and the spread of possible results.

4. Recommendations for Advancing SMR Deployment

4.1. Innovative Regulatory, Licensing, and Economic Strategies

4.1.1. Risk-Informed Licensing

4.1.2. Adaptive Regulatory Framework

4.1.3. Economic Viability Assessments

4.1.4. Public–Private Partnerships

4.2. Next Generation Security and Non-Proliferation Strategies

4.2.1. Advanced Security Integration

4.2.2. International Collaboration and Non-Proliferation Compliance

4.2.3. Quantum-Resistant Cybersecurity Protocols

4.3. Public Engagement and Communication Strategies

4.3.1. Utilizing Virtual Reality (VR) for Enhanced Public Understanding

4.3.2. Collaborative Educational Initiatives

4.3.3. Transparent and Continuous Public Engagement

4.4. Implementation Roadmap

- Deploying SmallModular Reactors (SMRs) requires a phased strategy that integrates regulatory innovations, security measures, public engagement, and economic planning. The Plan-Do-Study-Act (PDSA) method provides a structured approach that ensures these strategies are systematically tested, refined, and scaled for full deployment. Each phase aligns with the strategies discussed in previous sections:

- Regulatory and economic strategies (Section 4.1) are incorporated into the foundational phase. (Year 0–2)

- Security frameworks (Section 4.2) are tested in pilot projects before full-scale implementation. (Year 2–5)

- Public engagement efforts (Section 4.3) ensure community participation throughout the deployment process. (Year 5–10)The following roadmap details how these strategies are applied over a 10-year period.

4.4.1. The PDSA Cycle

- Plan (Years 0–2): Establish the regulatory foundation.

- Form an innovation task force.

- Develop training programs on AI, blockchain, and quantum technologies.

- Partner with tech companies and research institutions.

- Define success criteria and KPIs.

- Evaluation: Collect baseline data, set timelines, and gather feedback from training.

- Do (Years 2–5): Test and refine strategies.

- Launch pilots for AI-assisted regulation, digital twins, and quantum-resistant cybersecurity.

- Implement blockchain in licensing.

- Execution: Run pilots, collect performance data, and engage stakeholders.

- Evaluation: Measure pilot effectiveness and feasibility for scaling.

- Study (Years 2–5): Analyze pilot results.

- Compare results with KPIs.

- Identify successes and areas for improvement.

- Review training, partnerships, and technology use.

- Evaluation: Analyze data, review findings, and document lessons learned.

- Act (Years 5–10): Full deployment and improvement.

- ○

- Scale successful pilots.

- ○

- Integrate AI, blockchain, and quantum-resistant technologies.

- ○

- Implement continuous improvement.

- ●

- Evaluation: Monitor performance, update PDSA based on new data, and adjust strategies.

4.4.2. Key Performance Indicators (KPIs)

- Speeding Up the Licensing Process: Monitor the time for licensing completion. A reduction indicates increased efficiency and faster SMR deployment.

- Catching Safety Issues Early: Track early detections of safety issues. An increase suggests effective early identification by AI and monitoring technologies.

- Obtaining Correct Economic Predictions: Compare predicted vs. actual economic outcomes of SMR projects. Greater accuracy indicates effective economic modeling.

- Staying One Step Ahead of Security Threats: Monitor the detection and neutralization of security threats by AI systems. Higher detection rates show effective security measures.

- Building Public Trust and Engagement: Use surveys and feedback to gauge public trust and participation. Increased trust indicates successful communication strategies.

5. Results

5.1. Economic Analysis

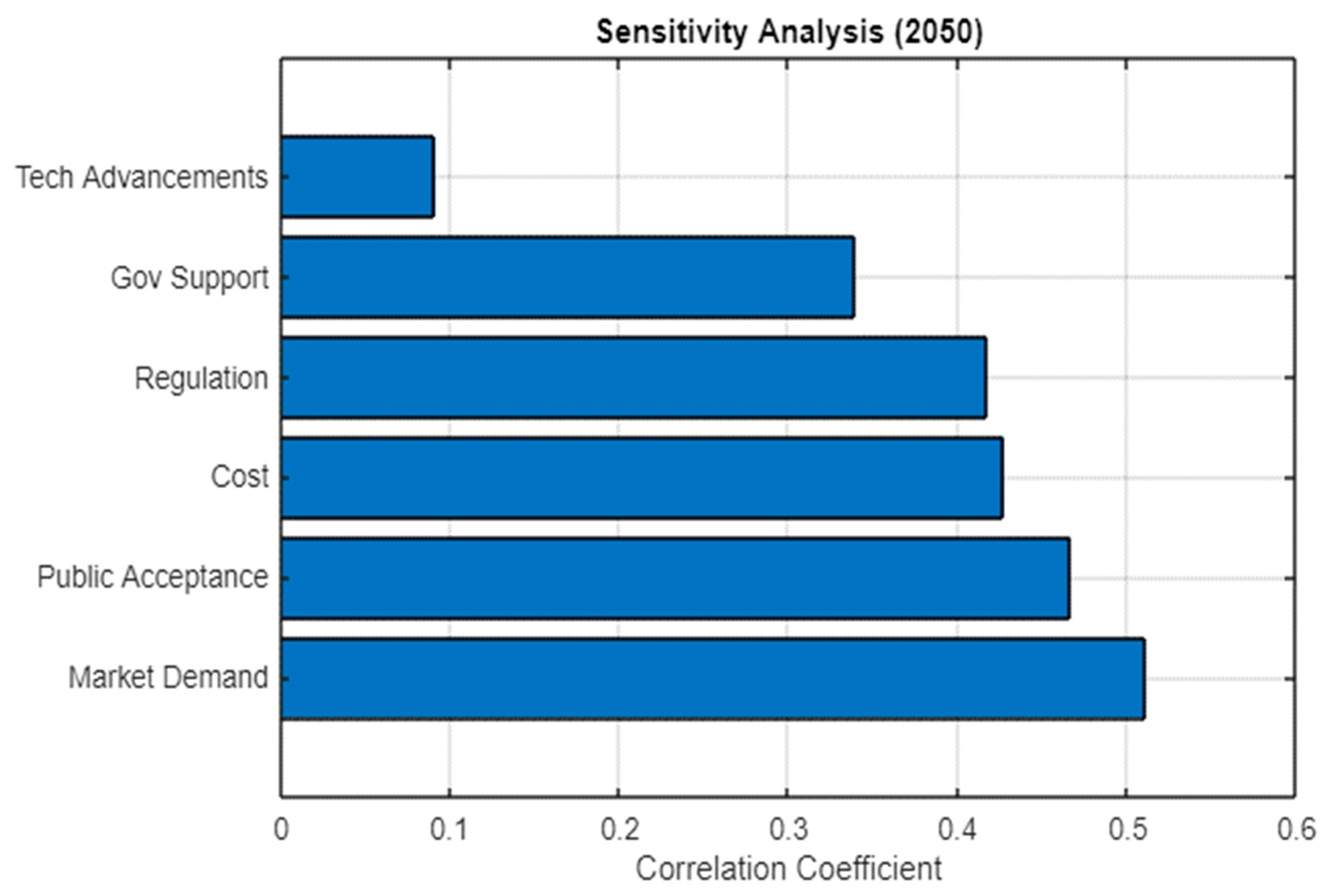

5.2. Sensitivity Analysis—Technology Adoption Rate

- Market Demand (correlation coefficient ≈ 0.58)

- ○

- Highest impact;

- ○

- Reflects the need and appetite for SMR technology in various energy markets;

- ○

- Suggests that identifying and developing suitable markets is crucial for SMR adoption.

- Public Acceptance (correlation coefficient ≈ 0.55)

- ○

- High impact;

- ○

- Reflects public perception, community support, and societal attitudes toward nuclear energy;

- ○

- Highlights the importance of public engagement and education in SMR deployment.

- Regulation (correlation coefficient ≈ 0.52)

- ○

- High impact;

- ○

- Encompasses licensing processes, safety standards, and policy frameworks;

- ○

- Suggests that streamlining regulatory processes could significantly accelerate SMR adoption.

- Cost (correlation coefficient ≈ 0.50)

- ○

- Moderate to high impact;

- ○

- Covers capital costs, operational expenses, and competitiveness with other energy sources;

- ○

- Indicates that economic factors play a significant role in adoption decisions.

- Government Support (correlation coefficient ≈ 0.48)

- ○

- Moderate impact;

- ○

- Includes financial incentives, research funding, and policy backing;

- ○

- Underscores the role of consistent government support in fostering SMR development.

- Technological Advancements (correlation coefficient ≈ 0.20)

- ○

- Lower impact;

- ○

- Encompasses improvements in design, efficiency, safety features, and manufacturing processes;

- ○

- This indicates that current SMR designs are seen as technologically viable.

5.2.1. Scenario Analysis

- Optimistic Scenario: Shows strong growth, reaching about 9% adoption by 2050.

- ○

- Assumes strong market demand, favorable regulatory environment, high levels of public acceptance, and significant government support;

- ○

- Represents the potential for accelerated SMR deployment under ideal conditions.

- Base Case Scenario: Projects moderate growth, reaching about 4.5% by 2050.

- ○

- Reflects current trends and moderate assumptions;

- ○

- Suggests steady growth in SMR adoption with acceleration in later years.

- Pessimistic Scenario: Indicates slower growth, ending at about 3% by 2050.

- ○

- Assumes challenges in market development, regulatory approval, public acceptance, or government support;

- ○

- Highlights potential barriers to SMR adoption that could hinder growth.

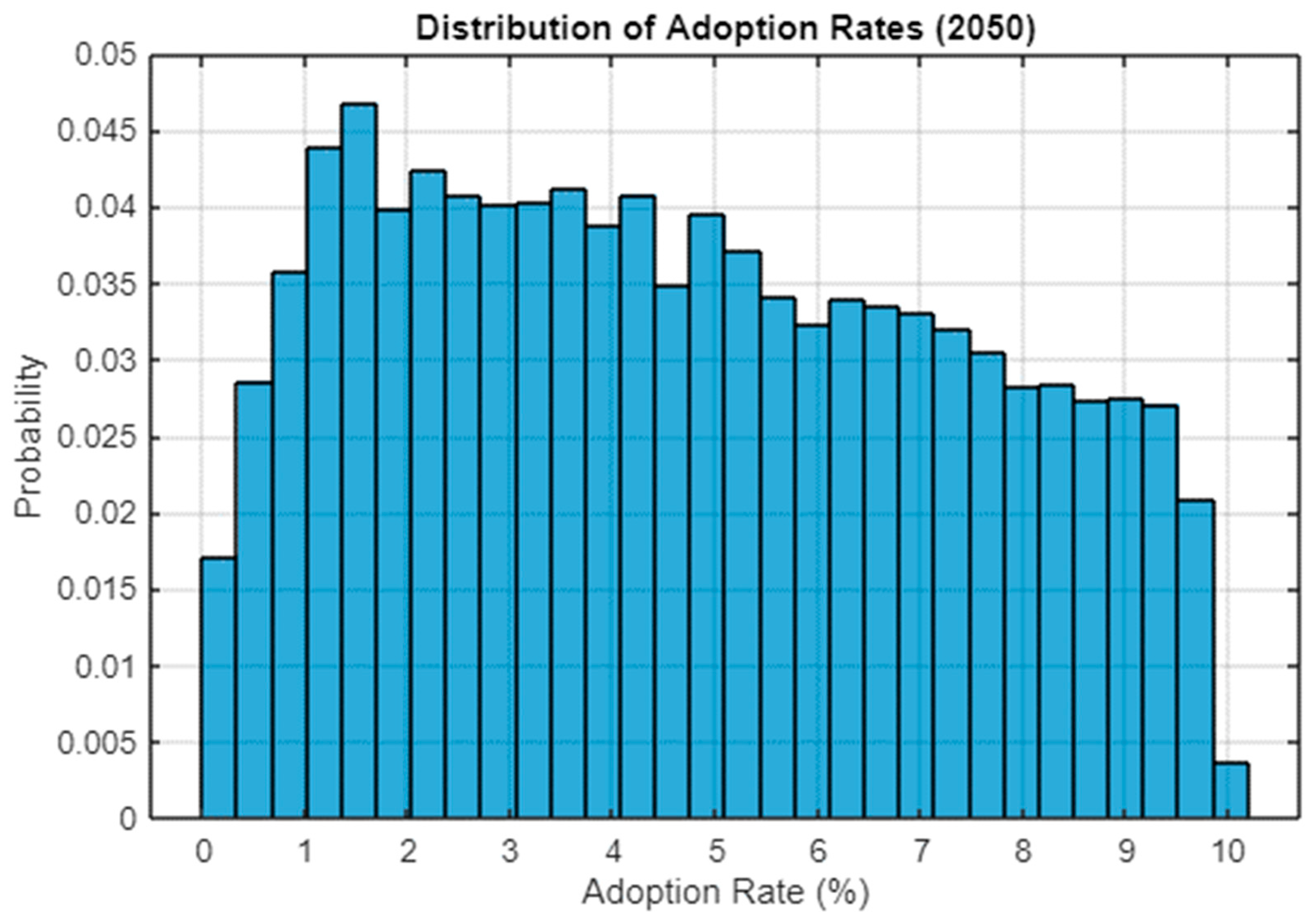

5.2.2. Distribution of Adoption Rates (2050)

- A right-skewed distribution;

- Peak probability between a 2 and 4% adoption rate;

- Low probability of very low (<1%) or very high (>10%) adoption rates;

- A long right tail, suggesting potential for higher-than-expected adoption rates.

5.2.3. Projected Installed SMR Capacity

- By 2040, the projected installed capacities are as follows:

- ○

- Base case: approximately 633 MW;

- ○

- Optimistic scenario: approximately 1.2 GW;

- ○

- Pessimistic scenario: approximately 512 MW.

- By 2050, these capacities are expected to increase to the following:

- ○

- Base case: approximately 983 MW;

- ○

- Optimistic scenario: approximately 2.9 GW;

- ○

- Pessimistic scenario: approximately 650 MW.

6. Discussion

6.1. Assessment Summary

- The results now appear much more realistic and in line with typical expectations for SMR projects.

- The NPV distribution suggests a generally positive economic outlook, but with acknowledged risks.

- The IRR, while positive, is modest, which is appropriate for a large infrastructure project with significant public benefit.

- The payback period now reflects the long-term nature of nuclear power investments.

- The LCOE distribution indicates that the project could be cost-competitive with other energy sources.

6.2. Payback Period and Cost Considerations

- Economic variability is more pronounced than previously understood;

- Cost reductions between FOAK and NOAK are more incremental;

- Robust risk management is crucial for successful SMR investments;

- Multiple factors contribute to project economic uncertainty.

6.3. LCOE and Market Competitiveness

- Limited cost advantages between FOAK and NOAK implementations;

- Significant economic uncertainty across project lifecycles;

- The need for robust risk management strategies;

- The importance of flexible investment approaches.

6.4. Technology Adoption Projections

6.5. Policy and Regulatory Implications

6.6. Regional and Market-Specific Considerations

7. Conclusions

Limitations and Future Work

- The development of more sophisticated financial models incorporating project-specific risk factors;

- Analyses of potential cost reductions through advanced manufacturing and construction techniques;

- Investigations of non-electric applications and their impact on project economics;

- Assessments of regulatory frameworks’ evolution and their impact on deployment timelines;

- Evaluations of workforce development needs and their influence on deployment capabilities.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Glossary of SMR Technologies and Regulatory Concepts

Appendix A.1. SMR Technologies

Appendix A.2. Regulatory Concepts

Appendix B. Regulatory Framework Comparison Matrix for Small Modular Reactors (SMRs)

| Aspect | United States (NRC) | Canada (CNSC) | United Kingdom (ONR) | IAEA Guidelines |

| Licensing Process | Part 52 process; design certification; combined license | Vendor Design Review (VDR) process; graded approach | Generic Design Assessment (GDA) process | Provides general safety standards and guidelines |

| Safety Requirements | 10 CFR Part 50 and Part 52; design-specific review standards | REGDOC-2.5.2 “Design of Reactor Facilities” | Safety Assessment Principles (SAPs) | IAEA Safety Standards Series |

| Emergency Planning Zones | Considering SMR-specific zones; potential for reduced EPZ | Graded approach based on reactor characteristics | Site-specific assessment; flexible approach | Recommends graded approach based on potential hazards |

| Staffing Requirements | Exploring changes to minimum staffing for SMRs | Performance-based approach | Goal-setting approach; demonstrate adequate staffing | Provides general guidance on staffing |

| Security Requirements | 10 CFR Part 73; considering SMR-specific approach | Graded approach based on threat and risk assessments | Nuclear Industries Security Regulations 2003 | Nuclear Security Series; recommends graded approach |

| Fuel Cycle Considerations | Similar to large reactors; exploring SMR-specific approaches | Facility-specific licensing | Similar to large reactors; case-by-case assessment | Provides general guidance on fuel cycle safety |

| Decommissioning | Similar to large reactors; considering SMR-specific guidance | Graded approach based on facility risk | Similar to large reactors; case-by-case assessment | Provides general guidance on decommissioning |

| Multi-Module Considerations | Developing guidance for multi-module facilities | Consideration in regulatory framework | Addressed in GDA process | Provides general guidance for multi-unit sites |

| Advanced Manufacturing Methods | Developing guidance for additive manufacturing, etc. | Consideration in regulatory framework | Addressed in manufacturing and construction assessment | Provides general guidance on quality assurance |

| Public Engagement | Public hearings and comment periods | Public involvement throughout licensing process | Public consultations during GDA and site licensing | Recommends stakeholder involvement |

References

- OCED. Small Modular Reactors: Challenges and Opportunities. Nuclear Energy Agency (NEA). 2021. Available online: https://smrroadmap.ca/wp-content/uploads/2018/12/Economics-Finance-WG.pdf (accessed on 21 July 2024).

- Song, D. 16—Small modular reactors (SMRs): The case of China. In Handbook of Small Modular Nuclear Reactors, 2nd ed.; Ingersoll, D.T., Carelli, M.D., Eds.; Woodhead Publishing: Cambridge, UK, 2021; pp. 395–408. [Google Scholar] [CrossRef]

- Bartak, J.; Bruna, G.; Cognet, G. Economics of Small Modular Reactors: Will They Make Nuclear Power More Competitive? J. Energy Power Eng. 2021, 15, 193–201. [Google Scholar] [CrossRef]

- Locatelli, G.; Bingham, C.; Mancini, M. Small modular reactors: A comprehensive overview of their economics and strategic aspects. Prog. Nucl. Energy 2014, 73, 75–85. [Google Scholar] [CrossRef]

- GE Hitachi. BWRX-300 Small Modular Reactor. GE Vernova. 2024. Available online: https://www.gevernova.com/nuclear/carbon-free-power/bwrx-300-small-modular-reactor (accessed on 21 July 2024).

- Nuclear Regulatory Commission (NRC). Westinghouse AP300. 2024. Available online: https://www.nrc.gov/reactors/new-reactors/advanced/who-were-working-with/pre-application-activities/westinghouse.html (accessed on 21 July 2024).

- Mignacca, B.; Locatelli, G. Economics and finance of Small Modular Reactors: A systematic review and research agenda. Renew. Sustain. Energy Rev. 2020, 118, 109519. [Google Scholar] [CrossRef]

- Boarin, S.; Mancini, M.; Ricotti, M.; Locatelli, G. Economics and financing of small modular reactors (SMRs). In Handbook of Small Modular Nuclear Reactors, 2nd ed.; Ingersoll, D.T., Carelli, M.D., Eds.; Woodhead Publishing: Cambridge, UK, 2021; pp. 241–278. [Google Scholar] [CrossRef]

- Hussein, E.M.A. Emerging small modular nuclear power reactors: A critical review. Phys. Open 2020, 5, 100038. [Google Scholar] [CrossRef]

- Black, R.L. Licensing of small modular reactors (SMRs). In Handbook of Small Modular Nuclear Reactors; Elsevier: Amsterdam, The Netherlands, 2021; pp. 279–298. [Google Scholar] [CrossRef]

- Nuclear Energy Agency (NEA). Projected Costs of Generating Electricity (p. 49). International Energy Agency (IEA). 2020. Available online: https://iea.blob.core.windows.net/assets/ae17da3d-e8a5-4163-a3ec-2e6fb0b5677d/Projected-Costs-of-Generating-Electricity-2020.pdf (accessed on 21 July 2024).

- American Public Power Association. Small Modular Reactor Technology Delivers Reliability, Resiliency, Safety and Affordability. American Public Power Association. 2022. Available online: https://www.publicpower.org/periodical/article/small-modular-reactor-technology-delivers-reliability-resiliency-safety-and-affordability (accessed on 21 July 2024).

- Boarin, S.; Locatelli, G.; Mancini, M.; Ricotti, M.E. Financial case studies on small- and medium-size modular reactors. Nucl. Technol. 2012, 178, 218–232. [Google Scholar] [CrossRef]

- SMR Start. The Economics of Small Modular Reactors. 2021. Available online: https://www.nei.org/CorporateSite/media/filefolder/advanced/SMR-Start-Economic-Analysis-2021-(APPROVED-2021-03-22).pdf (accessed on 21 July 2024).

- Energy.gov. Sector Spotlight: Advanced Nuclear. Energy.Gov. 2024. Available online: https://www.energy.gov/lpo/articles/sector-spotlight-advanced-nuclear (accessed on 21 July 2024).

- Sam, R.; Sainati, T.; Hanson, B.; Kay, R. Licensing small modular reactors: A state-of-the-art review of the challenges and barriers. Prog. Nucl. Energy 2023, 164, 104859. [Google Scholar] [CrossRef]

- Nuclear Energy Agency (NEA). Small Modular Reactors: Challenges and Opportunities (No. 7560). 2021. Available online: https://inis.iaea.org/collection/NCLCollectionStore/_Public/52/041/52041043.pdf?r=1 (accessed on 21 July 2024).

- IAEA SMR Regulators’ Forum. Pilot Project Report: Considering the Application of a Graded Approach, Defence-in-Depth and Emergency Planning Zone Size for Small Modular Reactors. 2018. Available online: https://www.iaea.org/sites/default/files/18/01/smr-rf-report-no-appendixes-150118.pdf (accessed on 21 July 2024).

- US Nuclear Regulatory Commission. Emergency Preparedness Rulemaking. NRC Web. 2024. Available online: https://www.nrc.gov/reactors/new-reactors/advanced/modernizing/rulemaking/emergency-preparedness.html (accessed on 21 July 2024).

- Lee, J.; Yoon, Y.T.; Lee, G.-J. Renewable Energy Sources: From Non-Dispatchable to Dispatchable, and Their Application for Power System Carbon Neutrality Considering System Reliability. J. Electr. Eng. Technol. 2024, 19, 2015–2028. [Google Scholar] [CrossRef]

- Kuznetsov, V. Options for small and medium sized reactors (SMRs) to overcome loss of economies of scale and incorporate increased proliferation resistance and energy security. Prog. Nucl. Energy 2008, 50, 242–250. [Google Scholar]

- Davidson, J.A. The Role of Nuclear Energy in the Global Energy Transition; Oxford Institute for Energy Studies: Oxford, UK, 2022. [Google Scholar]

- Carless, T.S.; Griffin, W.M.; Fischbeck, P.S. The environmental competitiveness of small modular reactors: A life cycle study. Energy 2016, 114, 84–99. [Google Scholar] [CrossRef]

- Zhang, X.; Bauer, C.; Mutel, C.L.; Volkart, K. Life Cycle Assessment of Small Modular Reactors: A comparative study based on IPCC scenarios for 2050. Energy 2019, 186, 115820. [Google Scholar]

- Boldon, L.M.; Sabharwall, P. Small Modular Reactor: First-of-a-Kind (FOAK) and Nth-of-a-Kind (NOAK) Economic Analysis (INL/EXT-14-32616, 1167545); Idaho National Laboratory: Idaho Falls, ID, USA, 2014. [Google Scholar] [CrossRef]

- Stevanka, K.; Chvala, O. Lessons from the US approach to licensing of Small Modular Reactors. In Proceedings of the 2023 23rd International Scientific Conference on Electric Power Engineering (EPE), Brno, Czech Republic, 24–26 May 2023; pp. 1–6. [Google Scholar] [CrossRef]

- Ramana, M.V.; Blaise, K. Regulation vs Promotion: Small Modular Nuclear Reactors in Canada. Energy Policy 2024, 192, 114228. [Google Scholar] [CrossRef]

- Schlegel, J.P.; Bhowmik, P.K. Small modular reactors. In Nuclear Power Reactor Designs; Elsevier: Amsterdam, The Netherlands, 2024; pp. 283–308. [Google Scholar] [CrossRef]

- World Nuclear Association. Small Nuclear Power Reactors. 16 February 2024. Available online: https://world-nuclear.org/information-library/nuclear-fuel-cycle/nuclear-power-reactors/small-nuclear-power-reactors (accessed on 4 August 2024).

- US Department of Energy. DOE Announces $900 Million to Accelerate Deployment of Next-Generation Light Water Small Modular Reactors. 5 March 2024. Available online: https://www.energy.gov/oced/funding-notice-generation-iii-small-modular-reactor-program (accessed on 4 August 2024).

- International Atomic Energy Agency. (n.d.). International Conference on Small Modular Reactors and their Applications 2024. Available online: https://www.iaea.org/events/smr2024 (accessed on 4 August 2024).

- Rosner, R.; Goldberg, S. Small Modular Reactors—Key to Future Nuclear Power Generation in the US Energy Policy Institute at Chicago; The Harris School of Public Policy Studies; University of Chicago: Chicago, IL, USA, 2011. [Google Scholar]

- Ingersoll, D.T.; Houghton, Z.J.; Bromm, R.; Desportes, C. Integration of security into the design of Generation IV reactors. Prog. Nucl. Energy 2015, 85, 297–318. [Google Scholar]

- US Department of Energy. (n.d.). Benefits of Small Modular Reactors (SMRs). Available online: https://www.energy.gov/ne/benefits-small-modular-reactors-smrs (accessed on 4 August 2024).

- Zohuri, B. Geopolitical and Economic Impact of Near-Term Fissionable Small Modular Reactors (SMRs) of Generation-IV (Gen-IV) and The Transition to Mid-Term. Sci. Set J. Econ. Res. 2023, 2, 1–6. [Google Scholar]

- US Department of Energy. Pathways to Commercial Liftoff: Advanced Nuclear. September 2024. Available online: https://liftoff.energy.gov/wp-content/uploads/2024/10/LIFTOFF_DOE_Advanced-Nuclear_Updated-2.5.25.pdf (accessed on 2 February 2025).

- SMR Start. Opportunities for Small Modular Reactors in Electric Utility Resource Planning. 2020. Available online: https://www.nei.org/CorporateSite/media/filefolder/advanced/SMR-Start-Public-SMRs-in-IRPs-(APPROVED-2020-02-28)-24.pdf (accessed on 21 July 2024).

- Godsey, K.M. A comparative life cycle assessment of small modular reactors and conventional nuclear power plants. Energy Policy 2019, 131, 230–242. [Google Scholar]

- Locatelli, G.; Mancini, M.; Todeschini, N. Generation IV nuclear reactors: Current status and future prospects. Energy Policy 2015, 61, 1503–1520. [Google Scholar]

- Wigeland, R.; Taiwo, T.; Ludewig, H.; Todosow, M.; Halsey, W.; Gehin, J.; Jubin, R.; Buelt, J.; Stockinger, S.; Jenni, K.; et al. Nuclear Fuel Cycle Evaluation and Screening—Final Report; INL/EXT-14-31465; Idaho National Laboratory: Idaho Falls, ID, USA, 2014. [Google Scholar]

- Byman, D.; Pomper, M.A. Vulnerability in the Grid: Lessons from the Russian Cyber Attack on Ukraine; Nuclear Threat Initiative: Washington, DC, USA, 2018. [Google Scholar]

- Kargl, F.; van der Heijden, R.W.; König, H.; Valdes, A.; Dacier, M.C. Insights on the security and dependability of industrial control systems. IEEE Secur. Priv. 2020, 12, 75–78. [Google Scholar]

- NEI. Cyber Security for Nuclear Power Plants; Nuclear Energy Institute: Washington, DC, USA, 2019. [Google Scholar]

- Glukhov, A.; Dats’ko, O.; Pivovarov, A. Cyber security of digital control systems at nuclear power plants. Nucl. Radiat. Saf. 2019, 1, 51–58. [Google Scholar]

- Baylon, C.; Brunt, R.; Livingstone, D. Cyber Security at Civil Nuclear Facilities: Understanding the Risks; Chatham House Report; Chatham House for the Royal Institute of International Affairs: London, UK, 2015. [Google Scholar]

- IAEA. Computer Security for Nuclear Security; IAEA Nuclear Security Series No. 42-G; IAEA: Vienna, Austria, 2021. [Google Scholar]

- Garcia, M.L. Vulnerability Assessment of Physical Protection Systems; Butterworth-Heinemann: Oxford, UK, 2018. [Google Scholar]

- Bunn, M.; Sagan, S.D. (Eds.) Insider Threats; Cornell University Press: Ithaca, NY, USA, 2016. [Google Scholar]

- World Nuclear Transport Institute. Security of the Transport of Radioactive Materials. WNTI Review Series No. 3. 2018. Available online: https://www.wnti.co.uk/industry/security/ (accessed on 21 July 2024).

- Harrington, C. Emergency Preparedness for Nuclear and Radiological Incidents; CRC Press: Boca Raton, FL, USA, 2020. [Google Scholar]

- NEA. The Safety of Long-Term Interim Storage Facilities for Spent Nuclear Fuel and Radioactive Waste; NEA No. 7406; NEA: Singapore, 2020. [Google Scholar]

- IAEA. International Safeguards in Nuclear Facility Design and Construction; IAEA Nuclear Energy Series No. NP-T-2.8; IAEA: Vienna, Austria, 2013. [Google Scholar]

- Bjornard, T.; Bean, R.; Durst, P.; Hockert, J. Safeguards-by-design: Early integration of physical protection and safeguardability into the design of nuclear facilities. In Nuclear Power Plant Design and Analysis Codes; Elsevier: Amsterdam, The Netherlands, 2015. [Google Scholar]

- IAEA. Design Measures to Facilitate Implementation of Safeguards at Future Water-Cooled Nuclear Power Plants; IAEA Nuclear Energy Series No. NP-T-2.8; IAEA: Vienna, Austria, 2019. [Google Scholar]

- Stein, G.; Risley, A.; Dewji, S. Blockchain technology and its applicability to the practice of nuclear safeguards. ESARDA Bull. 2017, 55, 30–37. [Google Scholar]

- Whitlock, J.J.; Sprinkle, J.K.; Henzl, V.; Trellue, H.R. Evaluation of proliferation resistance for advanced nuclear fuel cycles. Nucl. Technol. 2016, 194, 152–170. [Google Scholar]

- IAEA. Preventive and Protective Measures against Insider Threats; IAEA Nuclear Security Series No. 8-G (Rev. 1); IAEA: Vienna, Austria, 2018. [Google Scholar]

- Hund, G.; Kuykendall, T. Integrating safeguards and security into the design of small modular reactors. In Small Modular Reactors; Woodhead Publishing: Cambridge, UK, 2020; pp. 189–209. [Google Scholar]

- US Nuclear Regulatory Commission. International Organizations. NRC Web. 2021. Available online: https://www.nrc.gov/about-nrc/ip/intl-organizations.html (accessed on 21 July 2024).

- US Nuclear Regulatory Commission. Design Certification—NuScale US600. NRC Web. 2024. Available online: https://www.nrc.gov/reactors/new-reactors/advanced/who-were-working-with/past-license-activities/nuscale.html (accessed on 21 July 2024).

- US Nuclear Regulatory Commission. Part 53—Risk Informed, Technology-Inclusive Regulatory Framework for Advanced Reactors. NRC Web. 2024. Available online: https://www.nrc.gov/reactors/new-reactors/advanced/modernizing/rulemaking/part-53.html (accessed on 21 July 2024).

- US Nuclear Regulatory Commission. Pre-Application Information for the NuScale US600 Design. NRC Web. 2023. Available online: https://www.nrc.gov/reactors/new-reactors/advanced/who-were-working-with/past-license-activities/nuscale/documents.html (accessed on 21 July 2024).

- McDermott, J.; Daly, M. First-of-a-Kind Nuclear Project Is Terminated in a Blow to Biden’s Clean Energy Agenda. AP News. 9 November 2023. Available online: https://apnews.com/article/nuclear-power-nuscale-clean-energy-wind-biden-7f3a7fe754b77d8d6cbad8662b87a9c3 (accessed on 21 July 2024).

- Sovacool, B.K. What are we doing here? Analyzing fifteen years of energy scholarship and proposing a social science research agenda. Energy Res. Soc. Sci. 2014, 1, 1–29. [Google Scholar] [CrossRef]

- Natural Resources Canada. Canada’s Small Modular Reactor Action Plan. 2020. Available online: https://www.nrcan.gc.ca/our-natural-resources/energy-sources-distribution/nuclear-energy-uranium/canadas-small-nuclear-reactor-action-plan/21183 (accessed on 21 July 2024).

- Górzyński, M. The Pan-Canadian SMR Action Plan: A collaborative approach to nuclear innovation. Energy Strategy Rev. 2021, 35, 100651. [Google Scholar]

- Walton, R. Canada’s SMR Action Plan: Collaborative Innovation in Nuclear Energy. Energy Policy 2021, 152, 112216. [Google Scholar]

- Canadian Nuclear Association. 2021 Canadian Nuclear Factbook. 2021. Available online: https://cna.ca/welcome-2/the-canadian-nuclear-factbook-2021-en/ (accessed on 21 July 2024).

- Canadian Nuclear Safety Commission (CNSC). Pre-Licensing Vendor Design Review; Canadian Nuclear Safety Commission: Ottawa, ON, Canada, 2021. Available online: http://nuclearsafety.gc.ca/eng/reactors/power-plants/pre-licensing-vendor-design-review/index.cfm (accessed on 21 July 2024).

- Ontario Power Generation (OPG). OPG Advances Clean Energy Generation Project. 2021. Available online: https://www.opg.com/releases/opg-advances-clean-energy-generation-project/ (accessed on 21 July 2024).

- World Nuclear News. OPG Submits Application to Construct Canada’s First Commercial SMR. 2022. Available online: https://www.world-nuclear-news.org/Articles/OPG-applies-for-construction-licence-for-Darlingto (accessed on 21 July 2024).

- World Nuclear Association. (n.d.). Thorium. 2 May 2024. Available online: https://world-nuclear.org/information-library/current-and-future-generation/thorium (accessed on 4 August 2024).

- Department for Business, Energy & Industrial Strategy (BEIS). Energy White Paper: Powering Our Net Zero Future. UK Government. 2020. Available online: https://www.gov.uk/government/publications/energy-white-paper-powering-our-net-zero-future (accessed on 21 July 2024).

- Office for Nuclear Regulation (ONR). New Nuclear Power Plants: Generic Design Assessment. 2021. Available online: http://www.onr.org.uk/new-reactors/index.htm (accessed on 21 July 2024).

- World Nuclear Association. Nuclear Power in the United Kingdom. 2021. Available online: https://www.world-nuclear.org/information-library/country-profiles/countries-t-z/united-kingdom.aspx (accessed on 21 July 2024).

- Office for Nuclear Regulation (ONR) & Canadian Nuclear Safety Commission (CNSC). Memorandum of Understanding between the Office for Nuclear Regulation of Great Britain and the Canadian Nuclear Safety Commission; Office for Nuclear Regulation (ONR) & Canadian Nuclear Safety Commission (CNSC): Ottawa, ON, Canada, 2019.

- Nuclear Industry Association (NIA). Nuclear Power in the UK. 2021. Available online: https://www.niauk.org?industry-issues/nuclear-power-in-the-uk/ (accessed on 21 July 2024).

- HM Government. The Ten Point Plan for a Green Industrial Revolution. 2020. Available online: https://www.gov.uk/government/publications/the-ten-point-plan-for-a-green-industrial-revolution (accessed on 21 July 2024).

- Rolls-Royce. UK SMR: A National Endeavour. 2020. Available online: https://nuclear.foe.org.au/wp-content/uploads/Rolls-Royce-2017-SMR-national-endeavour-see-p22.pdf (accessed on 21 July 2024).

- Department for Business, Energy & Industrial Strategy (BEIS). £210 Million Government Investment for UK Small Modular Reactor; UK Government: London, UK, 2021.

- Energy Technologies Institute. The Role for Nuclear in UK’s Transition to a Low Carbon Economy; Energy Technologies Institute: Birmingham, UK, 2018. [Google Scholar]

- Rolls-Royce. Small Modular Reactors. 2021. Available online: https://www.rolls-royce.com/innovation/small-modular-reactors.aspx (accessed on 21 July 2024).

- Office for Nuclear Regulation (ONR). Generic Design Assessment of Rolls-Royce SMR; Office for Nuclear Regulation (ONR): Bootle, UK, 2022.

- Rolls-Royce. Rolls-Royce SMR: The UK SMR. 2021. Available online: https://www.rolls-royce-smr.com/ (accessed on 21 July 2024).

- Song, D. Small modular reactors (SMRs): The case of China. In Handbook of Small Modular Nuclear Reactors; Woodhead Publishing: Cambridge, UK, 2021; pp. 395–408. [Google Scholar]

- Murakami, T.; Anbumozhi, V. Small Modular Reactor (SMR) Deployment: Advantages and Opportunities for ASEAN; Economic Research Institute for ASEAN and East Asia: Senayan, Indonesia, 2022. [Google Scholar]

- Nian, V.; Zhong, S. Economic feasibility of flexible energy productions by small modular reactors from the perspective of integrated planning. Prog. Nucl. Energy 2020, 118, 103106. [Google Scholar] [CrossRef]

- Kuznetsov, V. 19—Small modular reactors (SMRs): The case of Russia. In Handbook of Small Modular Nuclear Reactors, 2nd ed.; Ingersoll, D.T., Carelli, M.D., Eds.; Woodhead Publishing: Cambridge, UK, 2021; pp. 467–501. [Google Scholar] [CrossRef]

- Vopilovskiy, S.S. Strategic Trends in Energy Development of the Northern Territories of Russia. Arct. North 2022, 49, 20–32. [Google Scholar] [CrossRef]

- Nuclear Energy Agency (NEA). Accelerating SMRs for Net Zero: NEA International Workshop on the Economics of SMRs. 2024. Available online: https://www.oecd-nea.org/jcms/pl_89581/accelerating-smrs-for-net-zero-nea-international-workshop-on-the-economics-of-smrs (accessed on 21 July 2024).

- U.S. Energy Information Administration. Wholesale U.S. Electricity Prices Were Generally Lower and Less Volatile in 2020 than 2019. 8 January 2021. Available online: https://www.eia.gov/todayinenergy/detail.php?id=46396&utm_source=chatgpt.com (accessed on 15 February 2025).

- Martins, A.C.R.; Martins, A.C.R. A Sandbox for the US Financial System|The Regulatory Review. The Regulatory Review. 18 August 2021. Available online: https://www.theregreview.org/2021/08/19/rossi-martins-sandbox-for-us-financial-system/ (accessed on 21 July 2024).

- Baluk, H.; Androshchuk, I.; Havadzyn, N.; Zhyvko, Z.; Hura, V. Marketing and sustainable economic development of the energy complex: A case study of the administrative and legal planning of a public-private partnership. Int. J. Relig. 2024, 5, 908–918. [Google Scholar] [CrossRef]

- Andrianov, A.; Kuptsov, I.; Andrianov, A.; Andrianova, O. Comparative analysis of the investment attractiveness of nuclear power plant concepts based on small and medium sized reactor modules and a large nuclear reactor. Nucl. Energy Technol. 2020, 6(3), 167–173. [Google Scholar] [CrossRef]

- Norton Rose Fulbright. (n.d.). Applying Blockchain to the Nuclear Sector. Norton Rose Fulbright. Available online: https://www.nortonrosefulbright.com/en/knowledge/publications/5f320cc5/applying-blockchain-to-the-nuclear-sector (accessed on 21 July 2024).

- Verhoest, K.; Petersen, O.; Scherrer, W.; Soecipto, R. How do governments support the development of public private partnerships? measuring and comparing ppp governmental support in 20 european countries. Transp. Rev. 2015, 35, 118–139. [Google Scholar] [CrossRef]

- Enerdata. Small Modular Reactors: Advancing Nuclear Power Generation for a Sustainable Future. Enerdata. 2024. Available online: https://www.enerdata.net/publications/executive-briefing/smr-world-trends.html (accessed on 21 July 2024).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Features | Advantages | Disadvantages |

|---|---|---|

| Factory fabrication |

|

|

| Standardization |

|

|

| Scalability |

|

|

| Degree of modularization |

|

|

| Design simplification |

|

|

| Harmonization |

|

|

| Flexibility |

|

|

| Category | Parameter | FOAK Values | NOAK Values |

|---|---|---|---|

| Capital Costs | Overnight Capital Cost (OCC) | USD 3800/kWe | USD 1198/kWe |

| Licensing Cost | USD 40 M | USD 28 M | |

| Decommissioning Costs (At the end of Year 60) | USD 50 M | USD 50 M | |

| Operating Costs | Fixed and Variable O & M Cost | USD 22/MWh | USD 18/MWh |

| Fuel Cost | USD 8/MWh | USD 7/MWh | |

| Insurance | 0.5% of CAPEX | 0.5% of CAPEX | |

| Timelines | Construction Period (No revenue generation) | 3 years | 2.5 years |

| Operational Life | 60 years | 60 years | |

| Operational Parameters | Capacity | 300 MWe | 300 MWe |

| Capacity Factor | 90% | 92% | |

| Revenue Assumptions | Electricity Price | USD 50/MWh | USD 50/MWh |

| Annual Electricity Generation | 2,365,200 MWh/year | 2,416,320 MWh/year | |

| Nominal Discount Rate (r) | 5.5% | 5.5% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Josephs, R.E.; Yap, T.; Alamooti, M.; Omojiba, T.; Benarbia, A.; Tomomewo, O.; Ouadi, H. Regulation of Small Modular Reactors (SMRs): Innovative Strategies and Economic Insights. Eng 2025, 6, 61. https://doi.org/10.3390/eng6040061

Josephs RE, Yap T, Alamooti M, Omojiba T, Benarbia A, Tomomewo O, Ouadi H. Regulation of Small Modular Reactors (SMRs): Innovative Strategies and Economic Insights. Eng. 2025; 6(4):61. https://doi.org/10.3390/eng6040061

Chicago/Turabian StyleJosephs, Rachael E., Thomas Yap, Moones Alamooti, Toluwase Omojiba, Achouak Benarbia, Olusegun Tomomewo, and Habib Ouadi. 2025. "Regulation of Small Modular Reactors (SMRs): Innovative Strategies and Economic Insights" Eng 6, no. 4: 61. https://doi.org/10.3390/eng6040061

APA StyleJosephs, R. E., Yap, T., Alamooti, M., Omojiba, T., Benarbia, A., Tomomewo, O., & Ouadi, H. (2025). Regulation of Small Modular Reactors (SMRs): Innovative Strategies and Economic Insights. Eng, 6(4), 61. https://doi.org/10.3390/eng6040061