Separation and Recycling Potential of Rare Earth Elements from Energy Systems: Feed and Economic Viability Review

Abstract

:1. Introduction

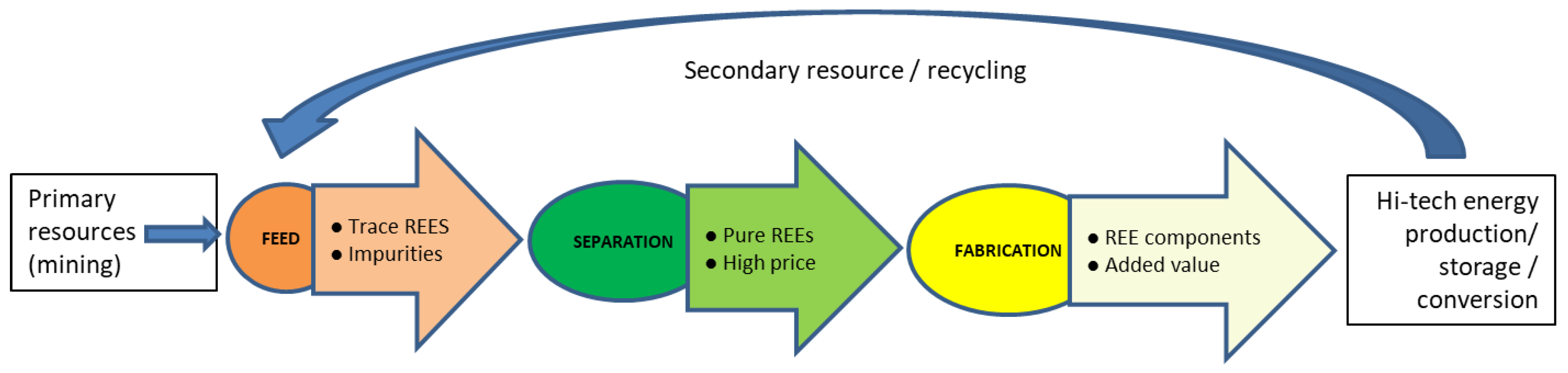

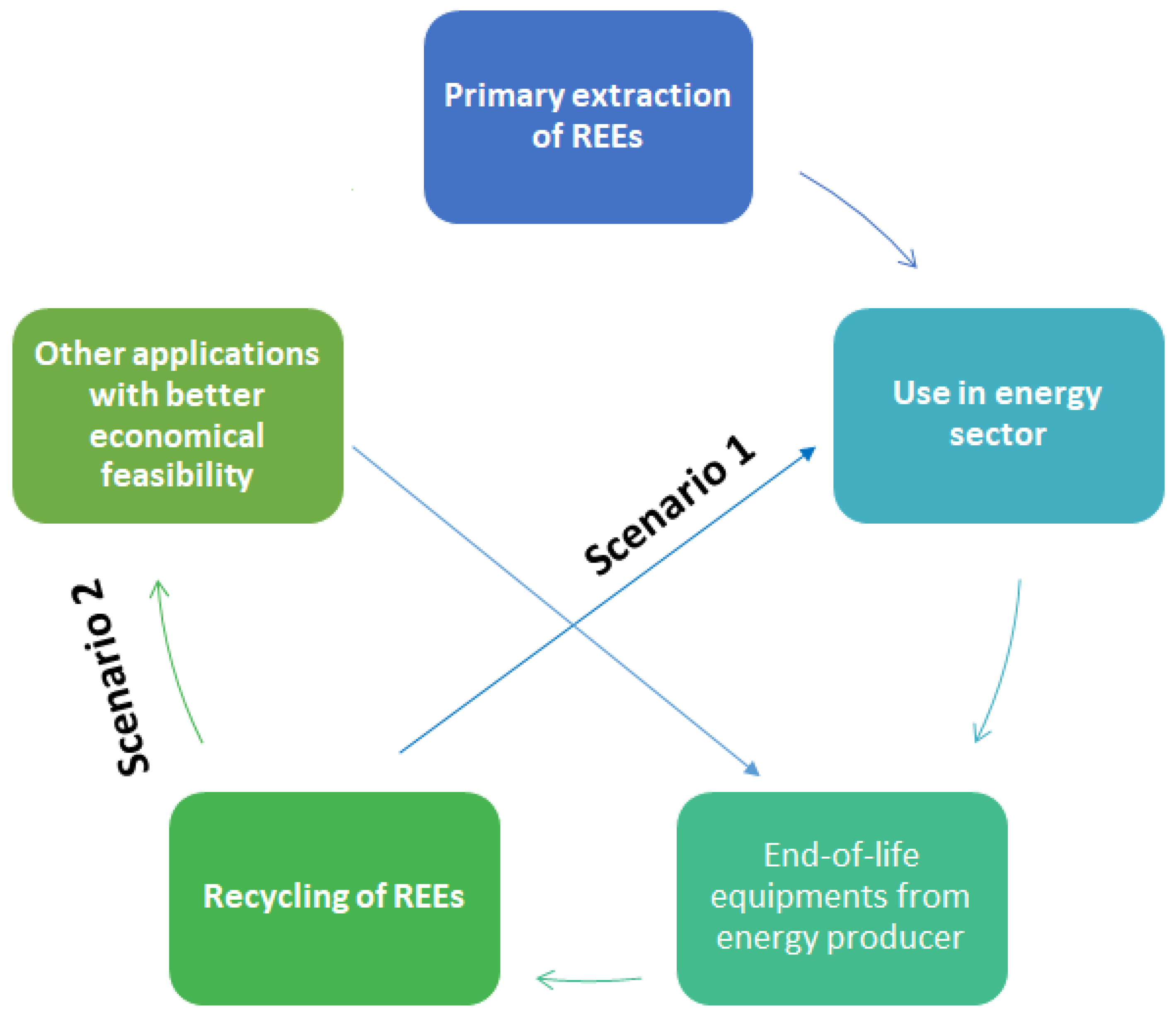

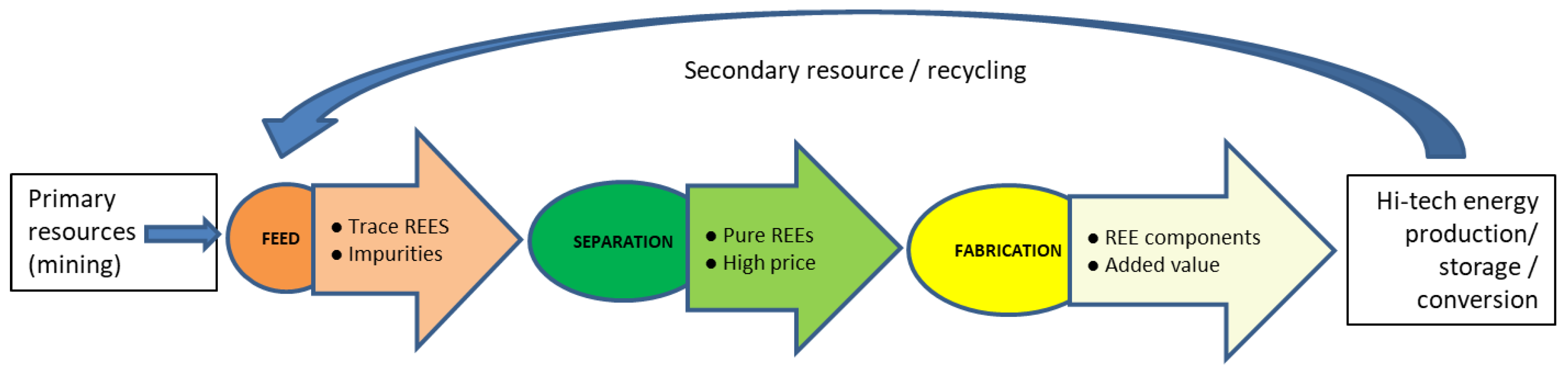

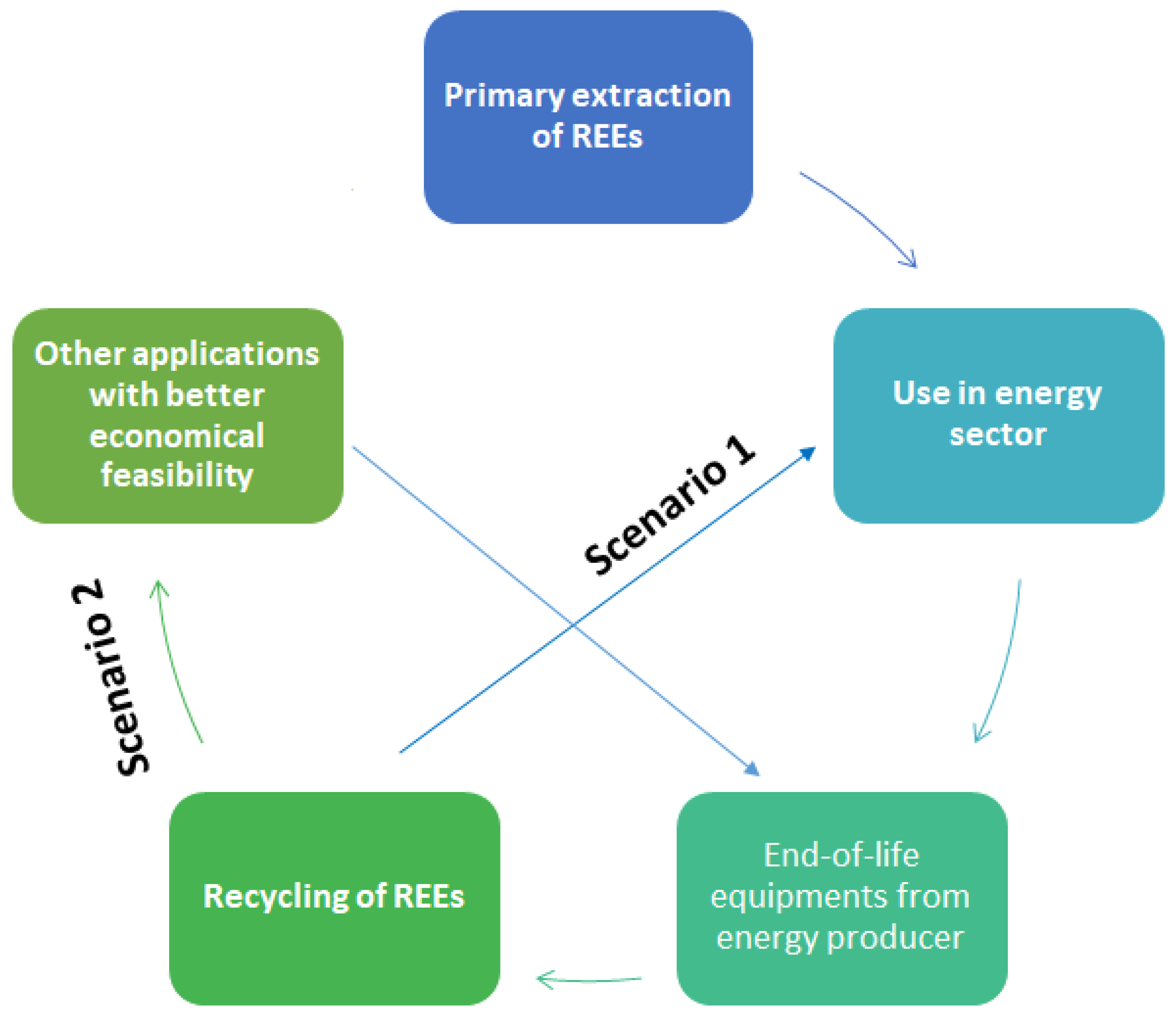

2. Background and Methodology of Review

- -

- What quantity of the REEs can be recovered from the recycling process?

- -

- What quality in terms of purity of the element can be obtained?

- -

- In what chemical form could be the output element?

- -

- What market prospects do such elements have against mining supply?

- -

- Wind power generation (magnets);

- -

- Energy storage (NiMH batteries);

- -

- Energy-saving and conversion (lighting).

3. Results

3.1. Nickel Metal Hydride (NiMH) Batteries

3.2. Permanent Magnets

- -

- Difficulty to decompose the chemical compounds (technological difficulties);

- -

- Low concentrations of REEs in the goods and location deep within consumer products;

- -

- Lack of financial incentives;

- -

- Inefficient collection of end-of-use objects.

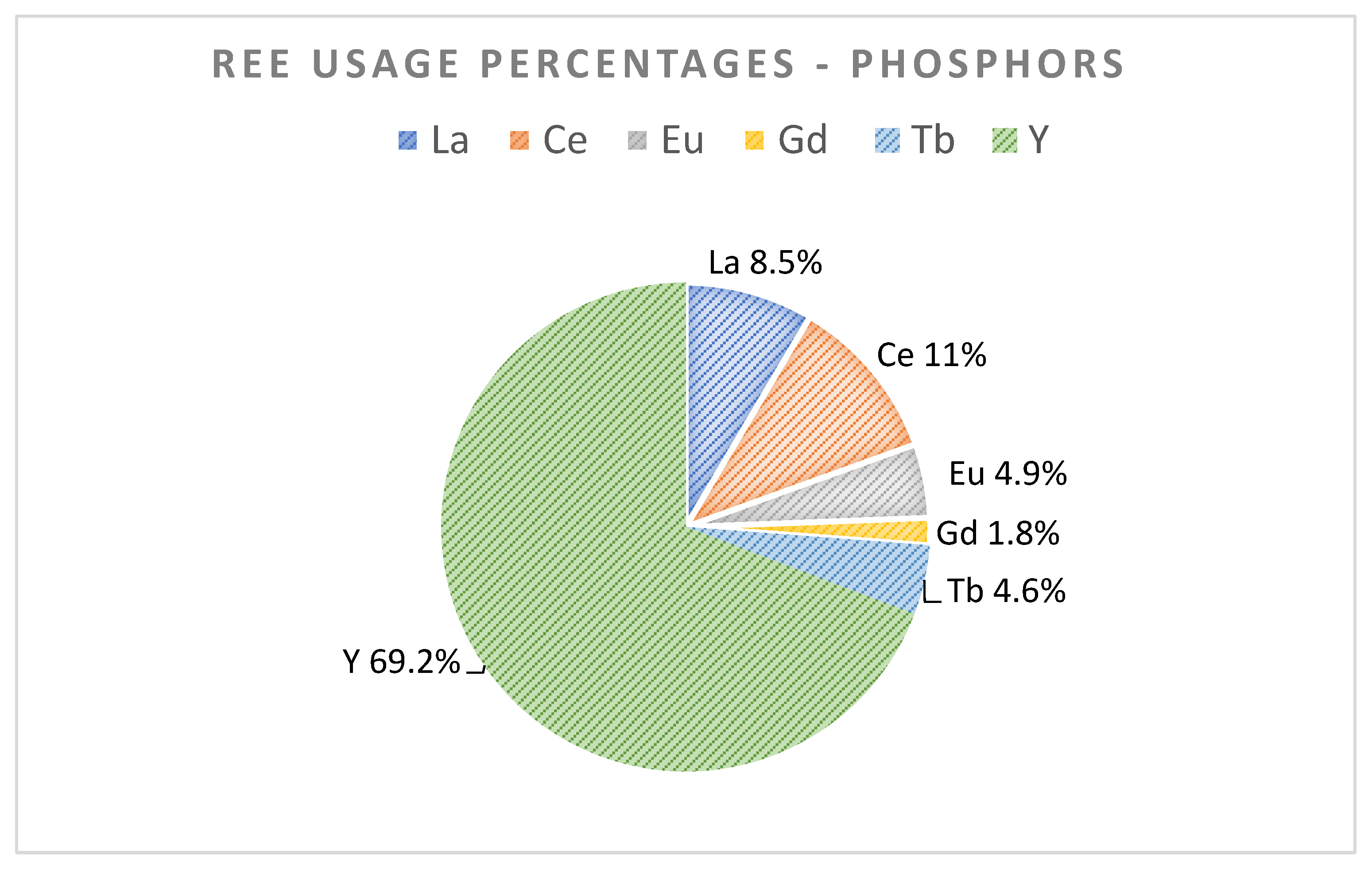

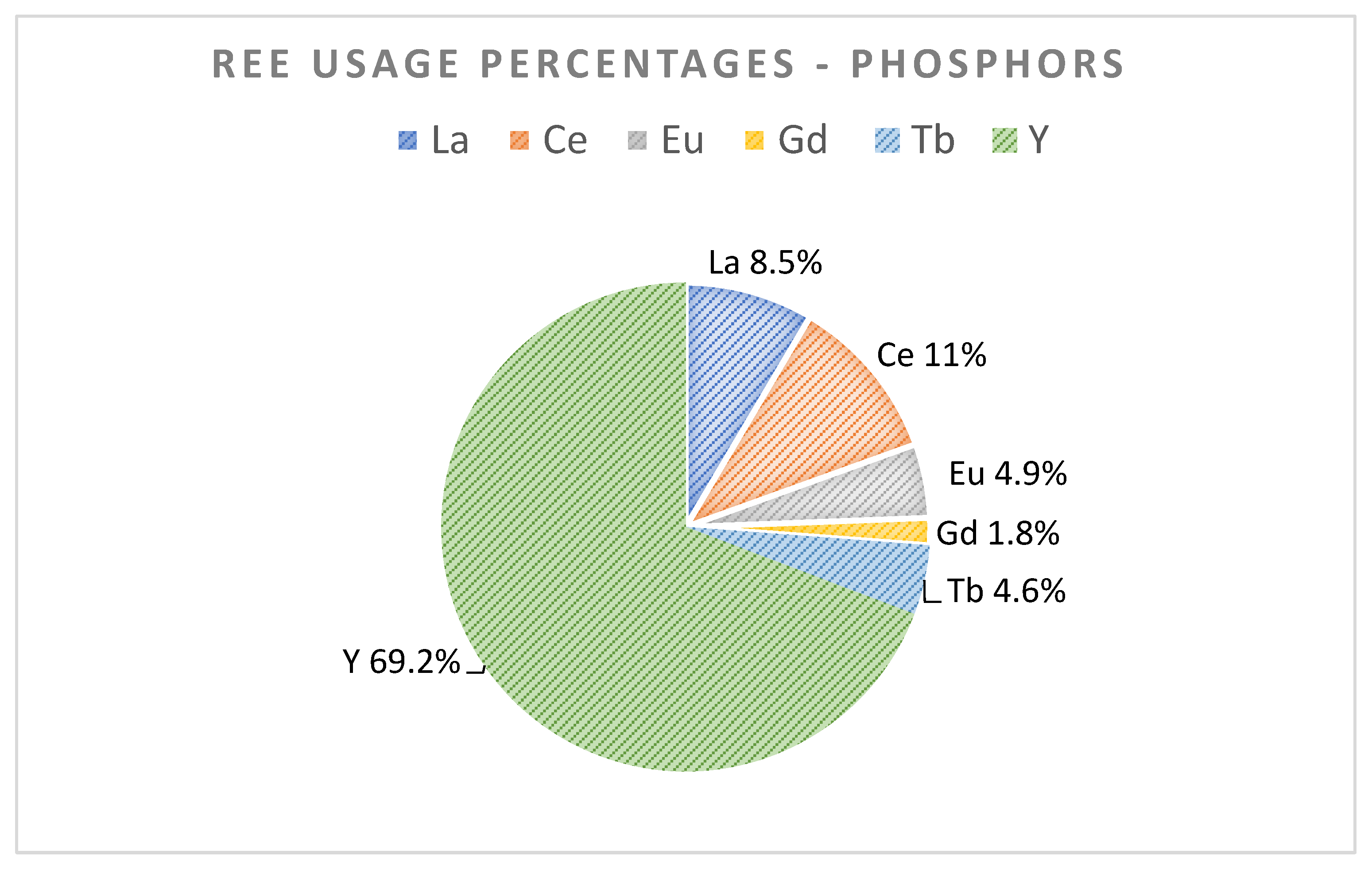

3.3. Lamp Phosphors

- Direct re-use of lamps (out phased due to technological change to LEDs);

- Separation of phosphor components or mixtures and reuse in lamp (or other) industry;

- Recovery of REE content on an individually high purity level.

4. Discussion

4.1. Criticality Assessment of Rare Earth Elements

4.2. Challenges of Recycling

4.3. Recycling Potentials

4.4. Existing Recycling Projects and Processes

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Patil, A.B.; Tarik, M.; Struis, R.P.; Ludwig, C. Exploiting end-of-life lamps fluorescent powder e-waste as a secondary resource for critical rare earth metals. Resour. Conserv. Recycl. 2021, 164, 105153. [Google Scholar] [CrossRef]

- Rare Earth Element Metals Recycling: Is There Hope After All? (Part 1). (13 September 2016) and Rare Earth Element Metals Recycling: Is There Hope After All? (Part 2) (20 September 2016). Available online: https://www.thermofisher.com/blog/metals/rare-earth-element-metals-recycling-is-there-hope-after-all-part-1/; https://www.thermofisher.com/blog/metals/rare-earth-element-metals-recycling-is-there-hope-after-all-part-2/ (accessed on 16 October 2018).

- Binnemans, K.; Jones, P.T.; Blanpain, B.; Van Gerven, T.; Yang, Y.; Walton, A.; Buchert, M. Recycling of rare earths: A critical review. J. Clean. Prod. 2013, 51, 1–22. [Google Scholar] [CrossRef]

- Binnemans, K.; McGuiness, P.; Jones, P.T. Rare-earth recycling needs market intervention. Nat. Rev. Mater. 2021, 6, 459–461. [Google Scholar] [CrossRef]

- Zepf, V.; Reller, A.; Rennie, C.; Ashfiled, M.; Simmons, B.P. Materials Critical to the Energy Industry. An Introduction. 2nd Edition. 2014. Available online: https://dokumen.tips/documents/materials-critical-to-the-energy-industry-an-introduction-a-materials-critical.html (accessed on 17 February 2022).

- FOEN, Federal Office for the Environment. Electrical and Electronic Equipment. Available online: https://www.bafu.admin.ch/bafu/en/home/themen/thema-abfall/abfallwegweiser--stichworte-a--z/elektrische-und-elektronische-geraete.html (accessed on 23 December 2021).

- Goodenough, K.; Schilling, J.; Jonsson, E.; Kalvig, P.; Charles, N.; Tuduri, J.; Deady, E.; Sadeghi, M.; Schiellerup, H.; Müller, A.; et al. Europe’s rare earth element resource potential: An overview of REE metallogenetic provinces and their geodynamic setting. Ore Geol. Rev. 2016, 72, 838–856. [Google Scholar] [CrossRef]

- Guyonnet, D.; Planchon, M.; Rollat, A.; Escalon, V.; Tuduri, J.; Charles, N.; Vaxelaire, S.; Dubois, D.; Fargier, H. Material flow analysis applied to rare earth elements in Europe. J. Clean. Prod. 2015, 107, 215–228. [Google Scholar] [CrossRef] [Green Version]

- European Commission. Critical Materials for Strategic Technologies and Sectors in the EU—A Foresight Study. 2020. Available online: https://ec.europa.eu/docsroom/documents/42881 (accessed on 17 February 2022).

- Gauß, R.; Burkhardt, C.; Carencotte, F.; Gasparon, M.; Gutfleisch, O.; Higgins, I.; Karajić, M.; Klossek, A.; Mäkinen, M.; Schäfer, B.; et al. Rare Earth Magnets and Motors: A European Call for Action. In Rare Earth Magnets and Motors Cluster of the European Raw Materials Alliance; Berlin, Germany, 2021; Available online: https://eit.europa.eu/sites/default/files/2021_09-24_ree_cluster_report2.pdf (accessed on 17 February 2022).

- European Commission, Critical Raw Materials Resilience: Charting a Path towards Greater Security and Sustainability, Fourth Critical Raw Materials List. 2020. Available online: https://ec.europa.eu/docsroom/documents/42849 (accessed on 17 February 2022).

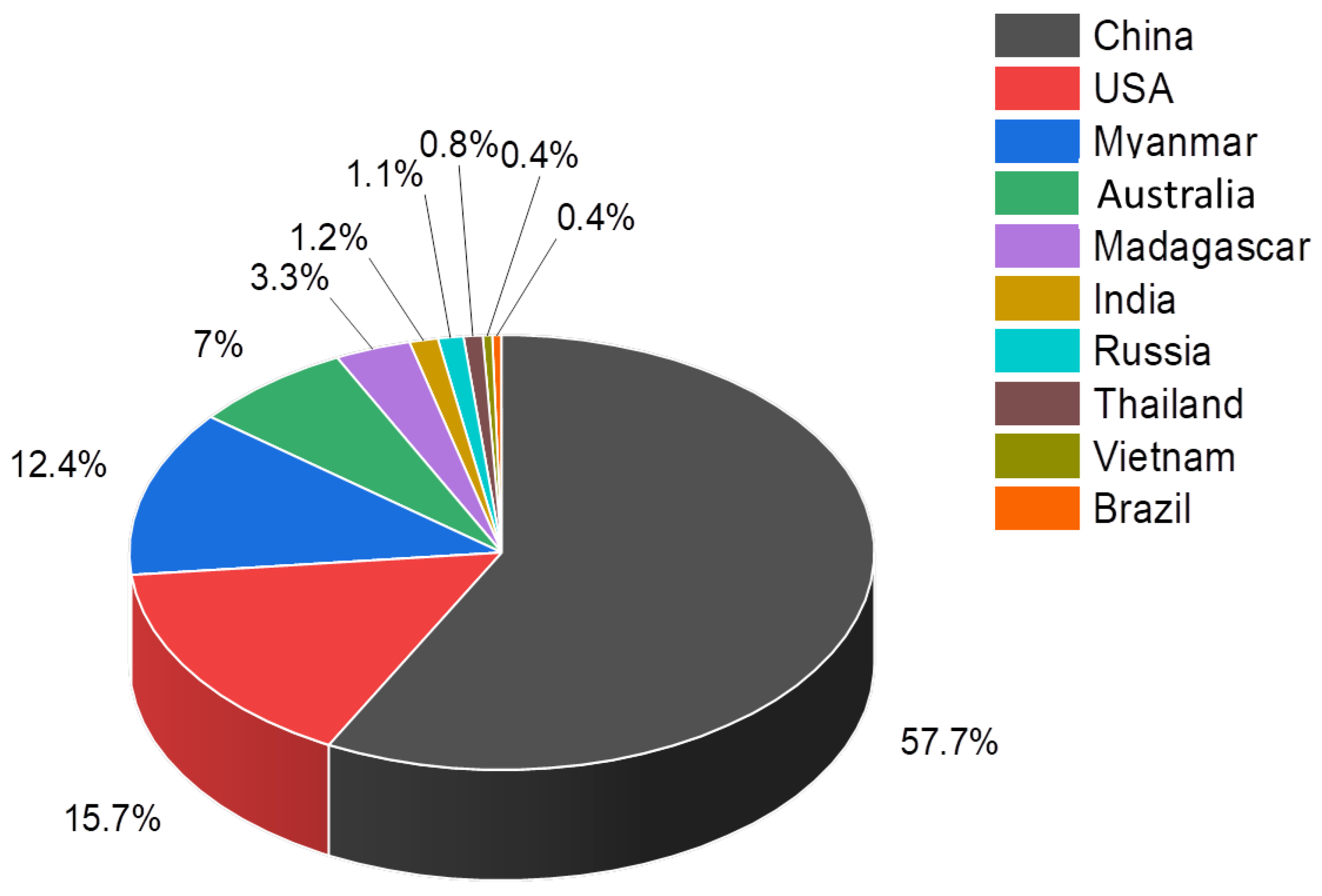

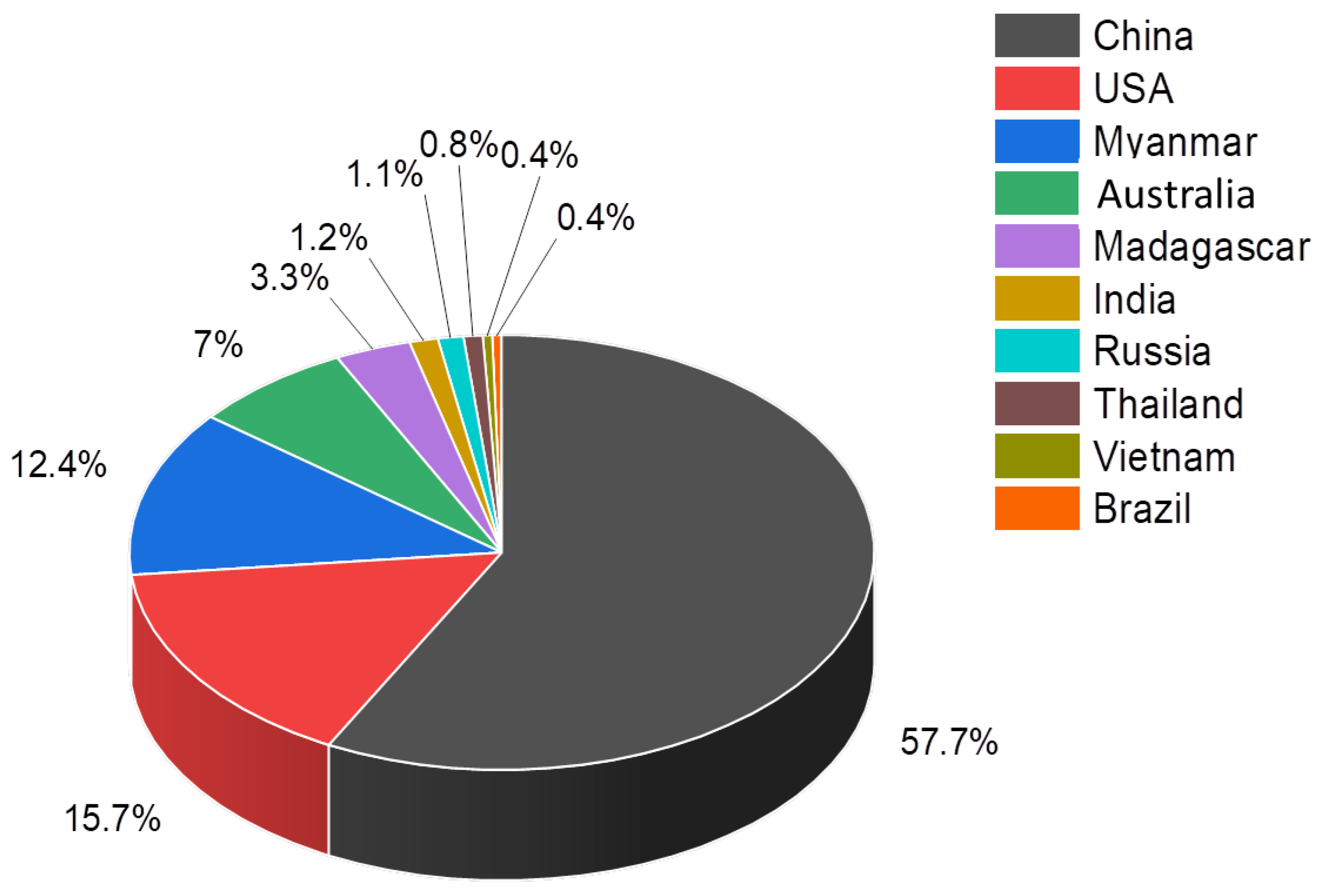

- Top 10 Countries for Rare Earths Production. 2021. Available online: https://investingnews.com/daily/resource-investing/critical-metals-investing/rare-earth-investing/rare-earth-producing-countries/ (accessed on 15 December 2021).

- Royen, H.; Fortkamp, U. Rare Earth Elements-Purification, Separation and Recycling, Pubished by the IVL Swedish Environmental Research Institute. Report Number C 211. 2016. Available online: https://www.ivl.se/download/18.76c6e08e1573302315f3b85/1480415049402/C211.pdf (accessed on 17 February 2022).

- Lucas, J.; Lucas, P.; Mercier, T.L.; Rollat, A.; Davenport, W.G. Rare Earths Production, use and Price. In Rare Earths: Science, Technology, Production and Use; Elsevier: Amsterdam, The Netherlands, 2015; Chapters 1–19; ISBN 978-0-444-62735-3. [Google Scholar]

- Zhang, P.; Yokoyama, T.; Itabashi, O.; Wakui, Y.; Suzuki, T.M.; Inoue, K. Hydrometallurgical process for recovery of metal values from spent nickel-metal hydride secondary batteries. Hydrometallurgy 1998, 50, 61–75. [Google Scholar] [CrossRef]

- Li, L.; Xu, S.; Ju, Z.; Wu, F. Recovery of Ni, Co and rare earths from spent Ni–metal hydride batteries and preparation of spherical Ni(OH)2. Hydrometallurgy 2009, 100, 41–46. [Google Scholar] [CrossRef]

- Curtis, N. Rare Earths, We Can Touch Them Everyday. In Lynas Presentation at the JP Morgan Australia Corporate Access Days; New York, NY, USA, 2010; Retrieved on 14 January 2022; Available online: https://www.asx.com.au/asxpdf/20100927/pdf/31sqqzmv0ng1tb.pdf (accessed on 17 February 2022).

- Rademaker, J.H.; Kleijn, R.; Yang, Y. Recycling as a Strategy against Rare Earth Element Criticality: A Systemic Evaluation of the Potential Yield of NdFeB Magnet Recycling. Environ. Sci. Technol. 2013, 47, 10129–10136. [Google Scholar] [CrossRef] [PubMed]

- Mueller, S.R.; Wäger, P.A.; Turner, D.A.; Shaw, P.J.; Williams, I.D. A framework for evaluating the accessibility of raw materials from end-of-life products and the Earth’s crust. Waste Manag. 2017, 68, 534–546. [Google Scholar] [CrossRef] [PubMed]

- Net Zero by 2050: A Roadmap for the Global Energy Sector IEA (2021); OECD Publishing: Paris, France, 2021. [CrossRef]

- Zakotnik, M.; Devlin, E.; Harris, I.; Williams, A. Hydrogen Decrepitation and Recycling of NdFeB-type Sintered Magnets. J. Iron Steel Res. Int. 2006, 13, 289–295. [Google Scholar] [CrossRef]

- Solvay (2015) SOLVAY Latest Developments in Rare Earth Recovery from Urban Mines. 2015. Available online: https://ec.europa.eu/docsroom/documents/14043/attachments/1/translations/en/renditions/native (accessed on 17 February 2022).

- Ku, A.Y.; Setlur, A.A.; Loudis, J. Impact of Light Emitting Diode Adoption on Rare Earth Element Use in Lighting: Implications for Yttrium, Europium, and Terbium Demand. Electrochem. Soc. Interface 2015, 24, 45–49. [Google Scholar] [CrossRef]

- Gambogi, J. 2015 Minerals Year Book. USGS. 2015. Available online: https://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/myb1-2015-raree.pdf (accessed on 17 February 2022).

- Du, X.; Graedel, T. Uncovering the end uses of the rare earth elements. Sci. Total Environ. 2013, 461–462, 781–784. [Google Scholar] [CrossRef] [PubMed]

- Wäger, P.; Widmer, R.; Stamp, A. Scarce Technology Metals—Applications, Criticalities and Intervention Options; Federal Office for the Environment: Bern, Switzerland, 2011. [Google Scholar]

- Atwater, H.; Fromer, N.; Otten, V. Critical Materials for Sustainable Energy Applications; The Resnick Institute, 2011; Available online: https:/Authors.library.caltech.edu/32727/1/ri_criticalmaterials_report.pdf (accessed on 17 February 2022).

- Patil, A.B.; Struis, R.P.W.J.; Testino, A.; Ludwig, C. Extraction of Rare Earth Metals: The New Thermodynamic Considerations Toward Process Hydrometallurgy. In Shape Casting; Springer International Publishing: Cham, Switzerland, 2021; pp. 187–194. [Google Scholar]

- De Lima, I.B. Rare Earths Industry and Eco-management. Rare Earths Ind. 2016, 8, 293–304. [Google Scholar] [CrossRef]

- Reimer, M.V.; Schenk-Mathes, H.Y.; Hoffmann, M.F.; Elwert, T. Recycling Decisions in 2020, 2030, and 2040—When Can Substantial NdFeB Extraction be Expected in the EU? Metals 2018, 8, 867. [Google Scholar] [CrossRef] [Green Version]

- Baldé, C.P.; Forti, V.; Gray, V.; Kuehr, R.; Stegmann, P. The Global E-waste Monitor; United Nations University (UNU): Bonn, Germany; International Telecommunication Union (ITU): Geneva, Switzerland; International Solid Waste Association (ISWA): Vienna, Austria, 2017. [Google Scholar]

- Wei, Y.; Salih, K.A.; Rabie, K.; Elwakeel, K.Z.; Zayed, Y.E.; Hamza, M.F.; Guibal, E. Development of phosphoryl-functionalized algal-PEI beads for the sorption of Nd(III) and Mo(VI) from aqueous solutions—Application for rare earth recovery from acid leachates. Chem. Eng. J. 2021, 412, 127399. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

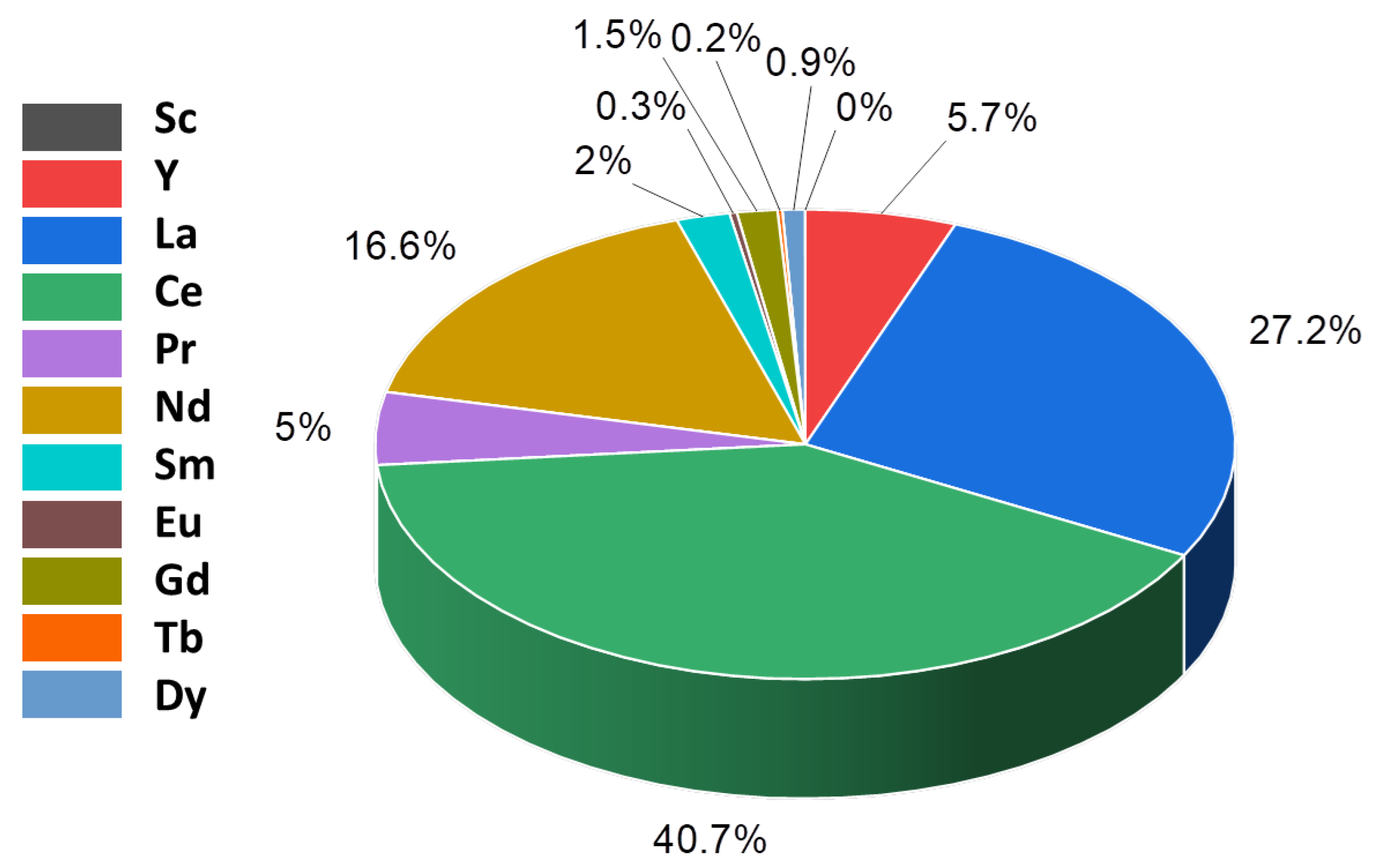

| Applications | Batteries or Fuel Cells | Lighting Phosphors | Turbine | Permanent Magnets and e-Mobility |

|---|---|---|---|---|

| REEs in use | Sc, La, Ce, Nd, and Pr | Y, La, Ce, Eu, Gd, and Tb | Y, Nd, Pr, and Dy | Nd, Pr, Dy, Gd, and Tb |

| La | Ce | Pr | Nd | Sm | |

|---|---|---|---|---|---|

| Flow into use in Europe (the year 2010) in ton metal | 600 | 400 | 40/50 | 120 | 40 |

| Rare earths usage (%) by battery alloys from Curtis (2010) [17] | 50 | 33.4 | 3.3 | 10 | 3.3 |

| Nd | Pr | Dy | Gd | Tb | |

|---|---|---|---|---|---|

| Flow into use (ton metal) in Europe (year 2010) | 1230 | 310 | 230 | 35 | 3.5 |

| REE content with magnet (wt%) | 70 | 18 | 13 | 2 | 0.2 |

| 2011 | 2015 | 2020 | 2025 | 2030 | |

|---|---|---|---|---|---|

| Recycling potential for Nd | 15% | 11% | 5% | 4% | 9% |

| Recycling potential for Dy | 0% | 0% | 0% | 2% | 7% |

| Y | Eu | Tb | La | Ce | Gd | |

|---|---|---|---|---|---|---|

| In-use stock for year 2010 in tons metal | 2300 | 200 | 140 | 283 | 366 | 60 |

| Application | Estimated Average Lifetime (Years) | Potential Recycling (%) |

|---|---|---|

| Magnets | 15 | 6.67% |

| Phosphors | 6 | 16.67% |

| NiMH batteries | 10 | 10.00% |

| Total | 7.78% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Patil, A.B.; Paetzel, V.; Struis, R.P.W.J.; Ludwig, C. Separation and Recycling Potential of Rare Earth Elements from Energy Systems: Feed and Economic Viability Review. Separations 2022, 9, 56. https://doi.org/10.3390/separations9030056

Patil AB, Paetzel V, Struis RPWJ, Ludwig C. Separation and Recycling Potential of Rare Earth Elements from Energy Systems: Feed and Economic Viability Review. Separations. 2022; 9(3):56. https://doi.org/10.3390/separations9030056

Chicago/Turabian StylePatil, Ajay B., Viktoria Paetzel, Rudolf P. W. J. Struis, and Christian Ludwig. 2022. "Separation and Recycling Potential of Rare Earth Elements from Energy Systems: Feed and Economic Viability Review" Separations 9, no. 3: 56. https://doi.org/10.3390/separations9030056

APA StylePatil, A. B., Paetzel, V., Struis, R. P. W. J., & Ludwig, C. (2022). Separation and Recycling Potential of Rare Earth Elements from Energy Systems: Feed and Economic Viability Review. Separations, 9(3), 56. https://doi.org/10.3390/separations9030056