Modeling Bitcoin plus Ethereum as an Open System of Systems of Public Blockchains to Improve Their Resilience against Intentional Risk

, , , , and

, , , , and

Abstract

1. Introduction

1.1. Epigraph

1.2. Blockchain

1.3. Bitcoin

1.4. Ethereum

1.5. Complex Networks

1.6. System of Systems Engineering

1.7. Intentional Risk Management

1.8. Structure of the Paper

2. Related Works

2.1. Blockchain: When Technology Changes Society

2.2. BTC and ETH: Public Blockchains as Complex Networks

2.3. Approaching Systems Engineering: Open vs. Closed Systems

2.4. Open Systems Principles

2.5. Network-Centricity in Systems of Systems

2.6. Paradoxes in SoS Management

2.7. Blockchain as a System of Systems

2.8. Intentional Risk

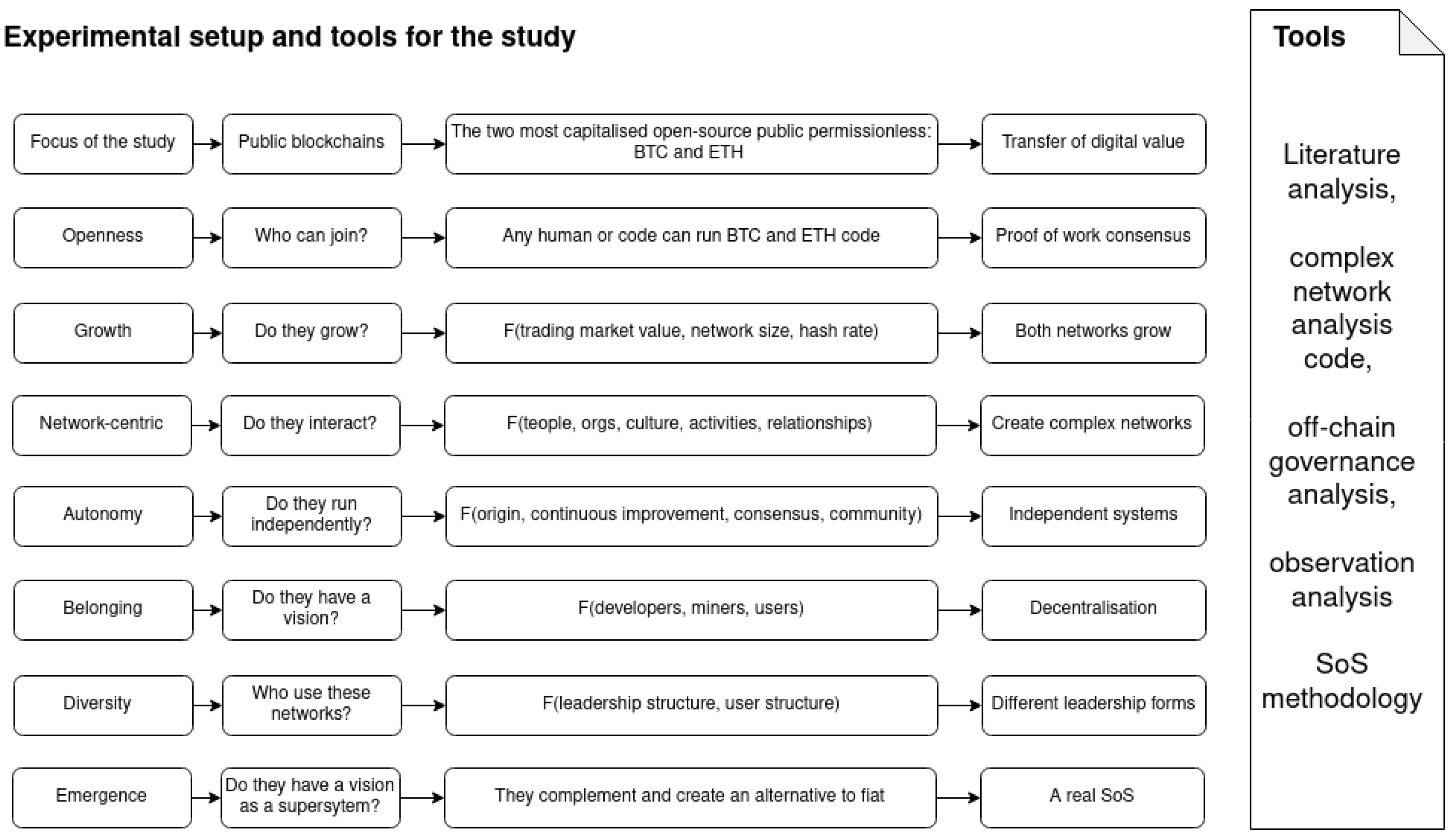

3. Methodology and Implementation

3.1. Research Methodology

3.2. Methodological Implementation

- Step 1: Identification of a SoS.A System of Systems (SoS) exists when its components are independent complex systems that interact with each other to accomplish a common goal [13]. We postulate that BTC and ETH are the two most prominent components of the SoS of public blockchains. They are two different systems, both with the goal of offering a digital distributed network of value;

- Step 2: Open systems with growing complexity.Once we identify a SoS of public blockchains, our second step is to determine whether BTC and ETH are open systems. As we have seen in Section 2.4, openness facilitates the inclusion of new components into a SoS. Under these premises, Section 4.2 analyses BTC and ETH as open systems with growing complexity;

- Step 3: Network centricity.The rapid development of information networks such as the Internet has facilitated interactions among SoS via network services up to the point that we talk about net-centric SoS. The existence of a service-oriented arquitecture (SOA) on top of a data network is a key characteristic for net-centric or network-centric SoS, also named net-centric enterprise systems [53]. Section 4.3 explores a service-oriented architecture (SOA) in BTC and ETH. More holistically, elements such as people, organisations, cultures, activities and interrelationships enable both systems to interact [13];

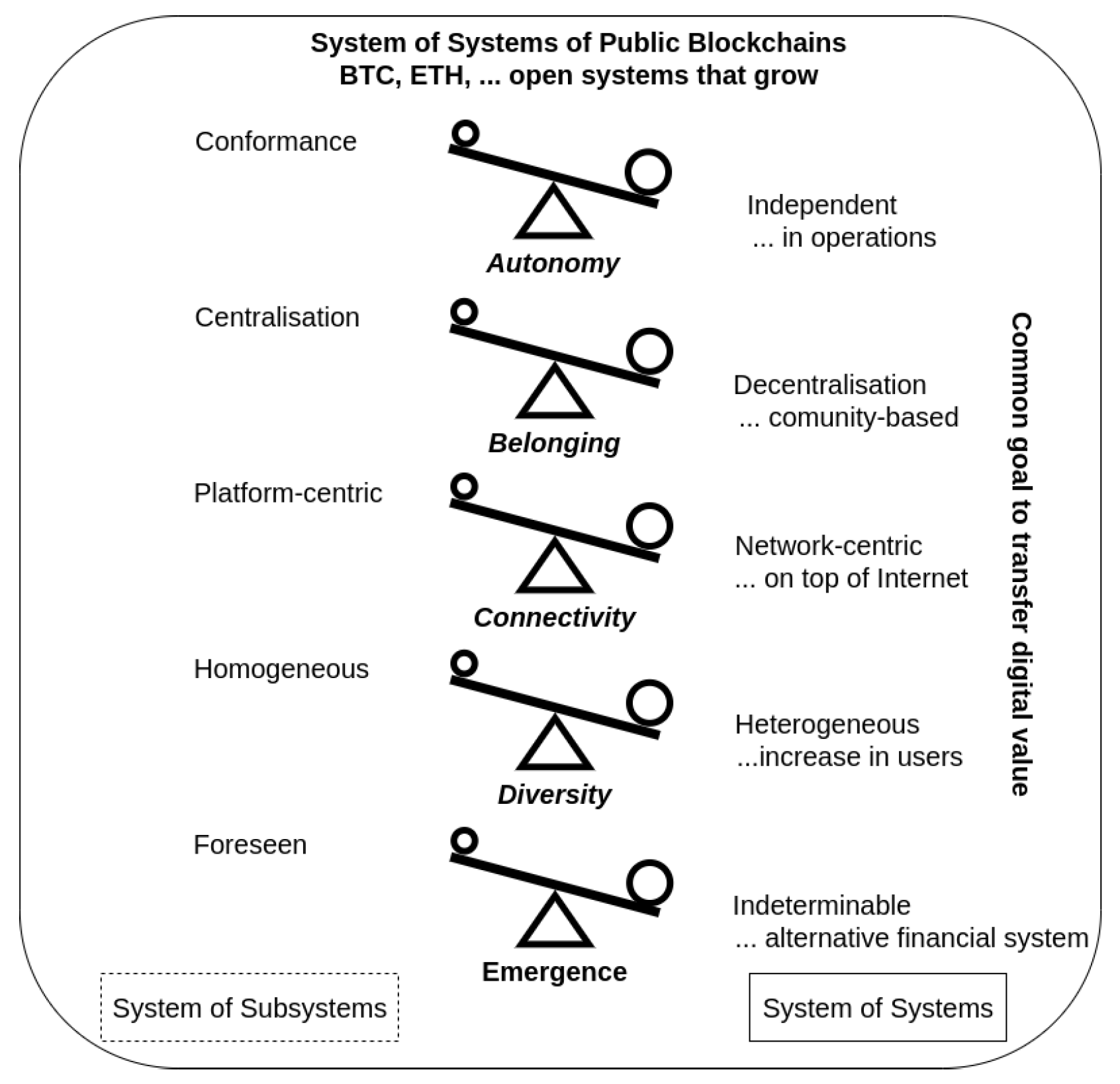

- Step 4: SoS characteristics.We characterise a SoS based on its properties as a more optimal way to comprehend its complexity instead of just framing it with a definition [52]. Chapter eight in [13] presents the SoS context based on five characteristics: autonomy, belonging, connectivity, diversity and evolutive emergence. In Section 4, we analyse these five characteristics for both BTC and ETH, and use the balance panel for each of them:

- (a)

- Autonomy.Autonomous systems operate independently [13]. We analyse BTC and ETH governance models, based on informal consensus. They are both independent. We describe key stakeholders such as their development and support communities and how they reach design decisions and try to avoid software forks while maintaining project legitimacy;

- (b)

- Belonging.The property of belonging to a system relates to its vision [13]. We explore BTC and ETH visions and identify opt in and opt out possibilities within the system and the balance that they strike between centralisation and decentralisation in mining power, community support, number of users and contributing developers;

- (c)

- Connectivity.We study how BTC and ETH interact between one another [13], especially in a scripted manner, and determine their common underlying technical foundation. We also determine whether the identified network-centricity is growing and examine the price correlation that both currencies show. From the platform viewpoint, we focus on their mining reward and supply models;

- (d)

- Diversity.A SoS achieves diversity if its holons are different to each other. We refer to leadership structure, range of business cases to answer, appetite for change and potential reasons to join these networks as proxies to understand the diversity present in this SoS;

- (e)

- Emergence.A pivotal feature of any SoS is the appearance of both intended and unintended properties that are not detectable in the specific component systems, i.e., holons. Emergence concentrates the added value of using SoSE. We compare the initial vision of the SoS of public blockchains [4,8] with its current use in two different levels, i.e., SoS-wide and holon-specific, and we identify properties that emerge from considering BTC and ETH as part of a more comprehensive system. We analyse the geopolitical consequences of this new financial SoS;

- Step 5: Vulnerabilities and threats. Resilience against intentional risk.We complete this analysis with the vulnerabilities we identify in the SoS and the threats it is exposed to. We use one of the identified threats, related to intentional risk, to come up with a series of security measures that would increase resilience against intentional risk. For this, we use the parameters proposed by Chapela et al. [16], i.e., value, accessibility and anonymity.

4. Analysis and Results

4.1. The System of Systems of Public Blockchains

4.2. Openness and Growth

- (a)

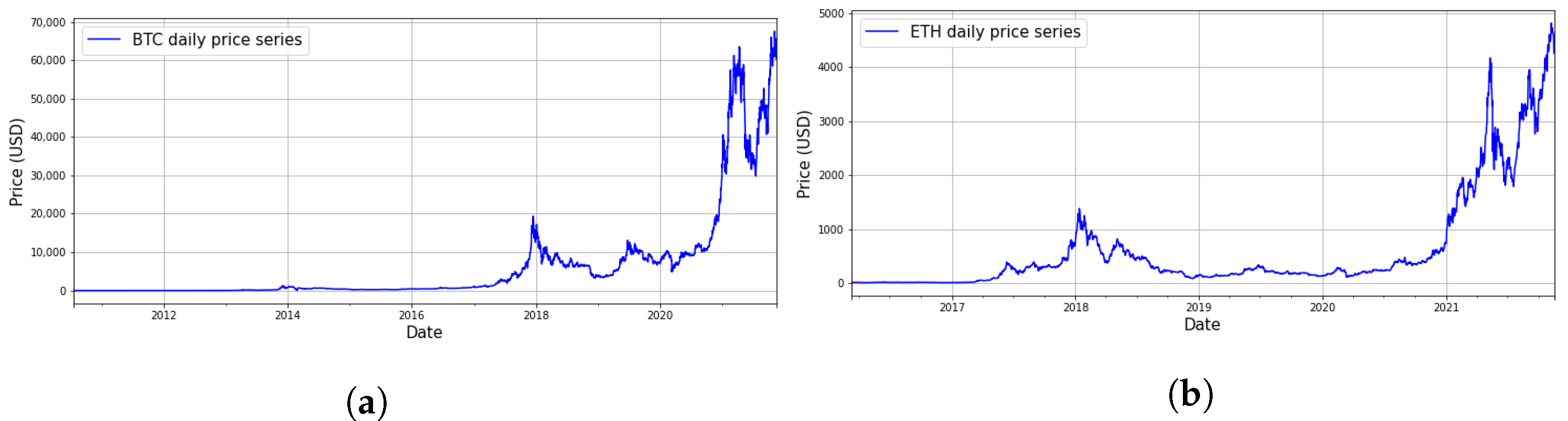

- Trading market: It is possible to buy and sell BTC and ETH coins. Both BTC and ETH are two public blockchain implementations that have attracted growing attention in the financial markets. Although their daily market price and their hash rate fluctuate considerably, both dimensions, price and total hash rate, have grown relentlessly for the last five years.Figure 3a depicts the daily BTC market price since its start. The upward trend is patent. BTC market capitalisation as a cryptoasset is growing. Equally, Figure 3b depicts the daily ETH market price since its start. An upward trend is patent as well. These steep climbing prices attract new users, both retail and institutional, generating more transactions. In July 2020, BTC market capitalisation reached USD 170 B; less than a year later, in April 2021, the figure topped USD 1099 B, going up to USD 1142 B in November 2021 [3], paving the way for an incessant growth during this decade. The Ethereum cryptoasset had a market capitalisation of USD 26 B in July 2020. In April 2021, this figure was of USD 222 B. In November 2021, the market value of ETH led to a capitalisation of USD 505 B [3];

- (b)

- Network size: As price and network size are positively correlated in both BTC [59] and ETH [48], their networks grow. According to bitnodes [60], there were around 10,540 full active BTC nodes in July 2020 while, surprisingly, there were around 9610 nodes in April 2021. A node is a BTC server that keeps a copy of the entire blockchain and validates transactions. A miner node is a node that validates blocks. In November 2021, the number of active BTC nodes reached 13,898. The trend in ETH is the opposite: according to ethernodes [61], there were close to 7900 active ETH nodes in July 2020 and over 4250 in April 2021. In November 2021, ref. [62] counted 3238 nodes. Table 4 summarises the BTC and ETH figures mentioned.Network growth is visible in the address space. A node in each of these networks is an address (see Section 2.2). By design, based on the recommendation not to re-use addresses in transactions, address spaces continue growing in BTC and ETH since their inception. This continuous growth contributes to their distributed nature and to their complexity as addresses do not expire. Equally, block validation, i.e., mining, generates new coins as well, bitcoins and ether, respectively, increasing the number of coins circulating in the systems;

- (c)

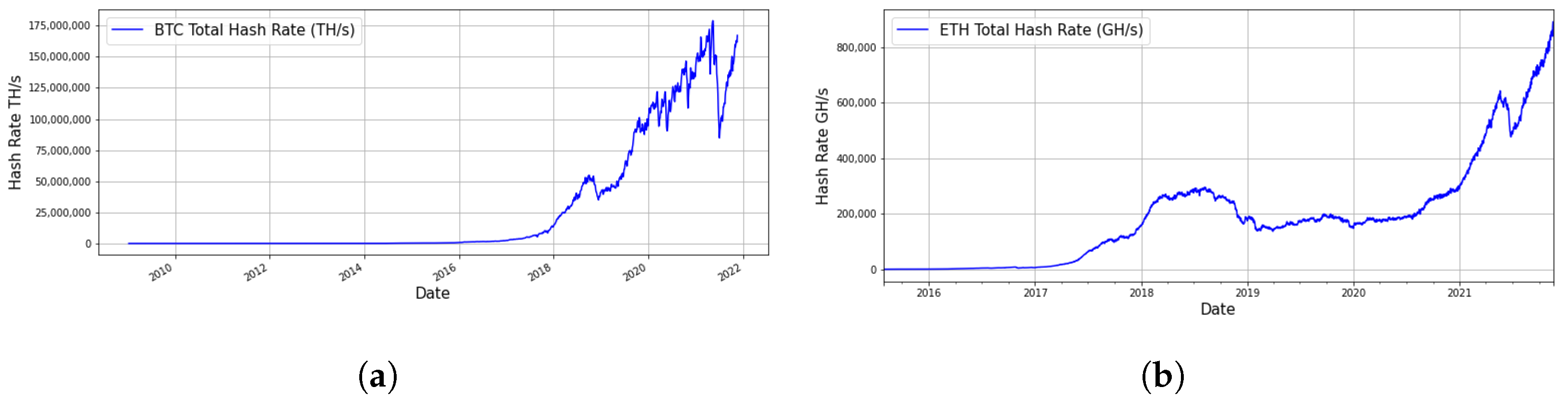

- Hash rate: Third, hash rate measures the computing power, i.e., calculation complexity, required to mine BTC and ETH blocks. Figure 4a,b shows how, especially since 2020, hash rates also increase. Both dimensions, market price and hash rate, indicate that the complexity of these systems, consequently, grow with time. They find themselves in a causality dilemma, and this is an inherent signal of complexity [63].

4.3. Network Centricity

4.4. Autonomy

4.5. Belonging

4.6. Connectivity

4.7. Diversity

4.8. Emergence

4.8.1. Intended Emergent Properties

4.8.2. High-Level Unintended Emergent Property

4.8.3. Holon-Specific Unintended Emergent Properties

4.8.4. Vulnerabilities and Threats of the SoS of Public Blockchains

- Adoption requires understanding.The knowledge-based barrier to entry is considerable. Participants in this public blockchain-based SoS require understanding of the underlying mathematical, cryptographic and economic concepts upon which both BTC and ETH are built. There is hardly any abstraction layer between users and the internal complex functioning of these blockchains;

- Adoption requires hiding complexity. The user-friendliness of the software tools that interface with this SoS is still very low;

- Early stage of evolution. Even with high rates of adoption and rising market capitalisation, public blockchains are still at a very early development phase. The industry is flourishing and growing fast; however, it has not yet reached any consolidation phase;

- Signs of centralisation. Complex network theory-based literature identifies linear and super-linear preferential attachment in BTC and ETH in their transaction networks [36,37,48,59]. This reveals the higher degree of dependence on specific super-hub nodes in these networks. An additional sign of initial centralisation is the decrease in the number of active ETH nodes [76].

- Governance exclusively dependent on code. The smart exploitation of any programming error in the code that implements elements such as mining rewards, smart contracts and distributed autonomous organisations (DAO, a distributed governance engine) can siphon out funds and make any public blockchain project fail. A real example of this already happened in Ethereum in 2016 [94].

- Regulation. The overall impact that financial regulation will have on the future of this SoS is still unknown. Taxation, legal jurisdiction, cross-border implications and know your customer requirements are just some examples of key regulatory aspects that are still not fully defined for the distributed SoS of public blockchains;

- Privacy vs. Traceability Trade off. One of the first business cases for the use of BTC was the online black market “Silk Road” [95]. Identities behind BTC addresses were not known. However, anonymity is not a design feature in BTC but, rather, pseudo-anonymity [5]. Ethereum does not offer transaction anonymity either. The lack of auditable and regulated know your customer procedures could hamper the mass growth of public blockchains;

- Future developments in encryption. Bitcoin uses SHA-256 as its hashing algorithm [96] and the Elliptic Curve Digital Signature Algorithm (ECDSA) with the elliptic curve secp256k1 to sign transactions [97]. The taproot BTC upgrade introduces Schnorr signatures [83]. Ethereum uses Keccak-256 [98] to hash transactions and ECDSA to sign them [99]. Future developments in quantum computing [100] could render current cryptographic algorithms used in public blockchains insecure. Should this happen, then the core development communities mentioned in Section 4.4 should react quickly with the corresponding cryptographic upgrade by proposing new key lengths or, alternatively, new algorithms;

- Missing co-operation. The permanent interaction between the SoS of traditional finance with the SoS of public blockchains is not yet defined. The governance frameworks in both systems need to find a common ground to allow for future-proof interactions between both financial proposals;

- Intentional risk. The economic value locked in the SoS of public blockchains is growing. Consequently, the interest of ill-intentioned actors to extract value out of it is also increasing [101]. The future of this SoS will depend on its resilience against intentional risk.

4.9. Resilience against Intentional Risk

- : the value as the quantity of cryptocurrency or fungible tokens held by the address . By design, this is public information. As an example, in the case of NFTs, this attribute simply refers to the value assigned by the market to it;

- : the accessibility of . This is a function of the accessibility to its private cryptographic key. Having access to the private key gives the possibility to claim ownership of . A high implies poor protection measures to keep the private key secure;

- : the anonymity of . This measures the degree of uncertainty to link with a screened identity in the physical world. A high implies that cannot be associated to a confirmed physical identity. Attackers of a public blockchain implementation use a collection of with a high as consecutive destinations of their fraudulent transactions to make tracking unfeasible.

5. Conclusions

- (a)

- Our proposed methodology, based on SoSE, is a valid and replicable tool to understand and to manage complex “supersystems” or “networks of networks”.We apply this methodology to the complexity present in public blockchains: we model BTC and ETH, two public open and permissionless blockchain implementations, as holons that complement each other within a SoS of public blockchains. Public blockchains enable the transfer of digital private property with a link, or not, to physical private property. Thanks to the use of SoSE, we identify that BTC aspires to become “sound money”, i.e., stable non-inflationary money, a digital global reserve asset. ETH, the “distributed world computer”, aims to become the “alternative financial conduit” system to run decentralised finance;

- (b)

- The unintended emergent property of the SoS of public blockchains is to stand as an alternative to the traditional centralised financial system based on fiat currencies.This emergent property only appears when we focus on BTC and ETH, and, more generally, on public blockchain implementations, as a unique “supersystem”. This SoS transfers digital value and competes with the traditional financial system as a potentially future-proof and disruptive alternative to the way the world conducts finance, especially since the Nixon shock in 1971 [102] with the cancellation of the direct convertibility of the USD into gold;

- (c)

- One of the threats to the future of the SoS of public blockchains is its exposure to intentional risk. The materialisation of this risk could impact its mass adoption;

- (d)

- The parameters proposed by Chapela et al. [16] in their intentional risk equation, i.e., value, accessibility and anonymity, are useful to suggest a series of security measures that would increase the resilience against intentional risk of the SoS of public blockchains.These measures apply to the governance, design, development, operation and communication phases present in the implementation of this SoS;

- (e)

- The optimisation of these intentional risk parameters, i.e., value, accessibility and anonymity, in the SoS of public blockchains, will impact positively on the evolution of the emergent property of this SoS.

6. Future Work

- (a)

- To analyse how the SoS of public blockchains links with the SoS of traditional centralised fiat currency-based finance;

- (b)

- To explore whether the modeling of the Decentralised Finance (DeFi) ecosystem is a SoS in itself;

- (c)

- To build a complete application programming interface (API) that would facilitate the implementation of security measures in public blockchains with the objective of increasing their resilience against intentional risk;

- (d)

- To explore the potential applications of machine learning and artificial intelligence (ML/AI) techniques, as described by Xu et al. [103], in the prevention, detection and mitigation of intentional risks against public blockchains.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Yli-Huumo, J.; Ko, D.; Choi, S.; Park, S.; Smolander, K. Where Is Current Research on Blockchain Technology? A Systematic Review. PLoS ONE 2016, 11, e0163477. [Google Scholar] [CrossRef]

- Walport, M. Distributed Ledger Technology: Beyond Block Chain. UK Government Chief Scientific Adviser. 2015. Available online: https://bit.ly/3yzbq34 (accessed on 16 November 2021).

- Coinmarketcap. Cryptocurrencies Market Capitalisation in Real Time. Available online: https://coinmarketcap.com/all/views/all/ (accessed on 25 November 2021).

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. Nakamotoinstitute.org, October 2008. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 16 November 2021).

- Reid, F.; Harrigan, M. An Analysis of Anonymity in the Bitcoin System. In Proceedings of the IEEE Third International Conference on Privacy, Security, Risk and Trust, Boston, MA, USA, 9–11 October 2011; pp. 1318–1326. [Google Scholar] [CrossRef]

- Weber, W.E. A Bitcoin Standard: Lessons from the Gold Standard. No. 2016-14; Bank of Canada Staff Working Paper. 2016. Available online: http://hdl.handle.net/10419/148121 (accessed on 1 December 2021).

- Ethereum. ETH Corporate Site. Available online: https://www.ethereum.org/ (accessed on 16 November 2021).

- Ethereum.org. Ethereum Whitepaper. Available online: https://ethereum.org/en/whitepaper/ (accessed on 16 November 2021).

- Partida, A.; Criado, R.; Romance, M. Identity and Access Management Resilience against Intentional Risk for Blockchain-Based IOT Platforms. Electronics 2021, 10, 378. [Google Scholar] [CrossRef]

- Partida, A.; Criado, R.; Romance, M. Visibility Graph Analysis of IOTA and IoTeX Price Series: An Intentional Risk-Based Strategy to Use 5G for IoT. Electronics 2021, 10, 2282. [Google Scholar] [CrossRef]

- Boccaletti, S.; Latora, V.; Moreno, Y.; Chavez, M.; Hwang, D.-U. Complex networks: Structure and dynamics. Phys. Rep. 2006, 424, 175–308. [Google Scholar] [CrossRef]

- Newman, M.E.J. The structure and function of complex networks. SIAM Rev. 2003, 45, 167–256. [Google Scholar] [CrossRef]

- Jamshidi, M. System of Systems Engineering: Innovations for the 21st Century; First Published: 21 April 2008; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2009; ISBN 9780470195901/9780470403501. [Google Scholar] [CrossRef]

- Liu, X.; Peng, H.; Gao, J. Vulnerability and controllability of networks of networks. Chaos Solitons Fractals 2015, 80, 125–138. [Google Scholar] [CrossRef]

- Partida, A. Secure IT Up! Cyber Insurance Due Diligence; CreateSpace Independent Publishing Platform: Scotts Valley, CA, USA, 2012; ISBN 9781478314752. [Google Scholar]

- Chapela, V.; Criado, R.; Moral, S.; Romance, M. Intentional Risk Management through Complex Networks Analysis; Springer Briefs in Optimization; Springer: Berlin/Heidelberg, Germany, 2015. [Google Scholar]

- Marella, V.; Kokabha, M.R.; Merikivi, J.; Tuunainen, V. Rebuilding Trust in Cryptocurrency Exchanges after Cyber-attacks. In Proceedings of the 54th Hawaii International Conference on System Sciences, Maui, HI, USA, 5–8 January 2021; pp. 5636–5646. [Google Scholar]

- Suciu, G.; Nădrag, C.; Istrate, C.; Vulpe, A.; Ditu, M.; Subea, O. Comparative analysis of distributed ledger technologies. In Proceedings of the 2018 Global Wireless Summit (GWS), Chiang Rai, Thailand, 25–28 November 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 370–373. [Google Scholar] [CrossRef]

- Thomas, S.; Schwartz, E. A Protocol for Interledger Payments. Hyperledger Working Group. Interledger.org. 2016. Available online: https://interledger.org/interledger.pdf (accessed on 16 November 2021).

- Frankenfield, J. Interledger Protocol. investopedia.com. Available online: https://www.investopedia.com/terms/i/interledger-protocol.asp (accessed on 19 November 2021).

- Reijers, W.; O’Brolcháin, F.; Haynes, P. Governance in Blockchain Technologies & Social Contract Theories. Ledger J. 2016, 1, 134–151. [Google Scholar] [CrossRef]

- Catalini, C.; Gans, J.S. Some Simple Economics of the Blockchain; Working Paper 22952; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar] [CrossRef]

- ECB. Distributed Ledger Technology. In Focus, Issue 1, European Central Bank. 2016. Available online: https://bit.ly/3fHcOYS (accessed on 16 November 2021).

- ESMA. The Distributed Ledger Technology Applied to Securities Markets; Report ESMA50-1121423017-285, Discussion Paper; European Securities and Markets Authority: Paris, France, 2017. Available online: https://bit.ly/344omjI (accessed on 16 November 2021).

- Pinna, A.; Ruttenberg, W. Distributed Ledger Technologies in Securities Post Trading: Revolution or Evolution. Available online: https://bit.ly/3oHEMaY (accessed on 16 November 2021).

- Longo, F.; Nicoletti, L.; Padovano, A.; d’Atri, G.; Forte, M. Blockchain-enabled supply chain: An experimental study. Comput. Ind. Eng. 2019, 136, 57–69. [Google Scholar] [CrossRef]

- Filippi, P.D.; Hassan, S. Blockchain technology as a regulatory technology: From code is law to law is code. arXiv 2018, arXiv:1801.02507. [Google Scholar] [CrossRef]

- Hölbl, M.; Kompara, M.; Kamišalić, A.; Zlatolas, L.N. A Systematic Review of the Use of Blockchain in Healthcare. Symmetry 2018, 10, 470. [Google Scholar] [CrossRef]

- Peiró, N.N.; García, E.J.M. Blockchain and land registration systems. Eur. Prop. Law J. 2017, 6, 296–320. [Google Scholar] [CrossRef]

- Vasiliy, E.; Spirkina, A.; Buinevich, M.; Vladyko, A. Technological Aspects of Blockchain Application for Vehicle-to-Network. Information 2020, 11, 465. [Google Scholar] [CrossRef]

- Stroukal, D.; Nedvedova, B. Bitcoin and other cryptocurrencies as an instrument of crime in cyberspace. In Proceedings of the 4th Business & Management Conference, Istanbul (IISES), Istanbul, Turkey, 12–14 October 2016; Available online: https://bit.ly/3fgyNap (accessed on 16 November 2021).

- Malone, J.A. Bitcoin and Other Virtual Currencies for the 21st Century; CreateSpace Independent Publishing Platform: Scotts Valley, CA, USA, 1861; Available online: https://amzn.to/3oFn73I (accessed on 16 November 2021).

- Srivastava, G.; Dhar, S.; Dwivedi, A.D.; Crichigno, J. Blockchain education. In Proceedings of the 2019 IEEE Canadian Conference of Electrical and Computer Engineering (CCECE), Edmonton, AB, Canada, 5 May 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 1–5. [Google Scholar] [CrossRef]

- Tasca, P.; Tessone, C.J. A Taxonomy of Blockchain Technologies: Principles of Identification and Classification. Ledger J. 2019, 4. [Google Scholar] [CrossRef]

- Dinh, T.T.A.; Liu, R.; Zhang, M.; Chen, G.; Ooi, B.C.; Wang, J. Untangling Blockchain: A Data Processing View of Blockchain Systems. IEEE Trans. Knowl. Data Eng. 2018, 30, 1366–1385. [Google Scholar] [CrossRef]

- Kondor, D.; Pósfai, M.; Csabai, I.; Vattay, G. Do the Rich Get Richer? An Empirical Analysis of the Bitcoin Transaction Network. PLoS ONE 2014, 9, e86197. [Google Scholar] [CrossRef]

- Maesa, D.D.F.; Marino, A.; Ricci, L. Data-driven analysis of Bitcoin properties: Exploiting the users graph. Int. J. Data Sci. Anal. Nat. Res. 2018, 6, 63–80. [Google Scholar] [CrossRef]

- Sommer, D. Processing Bitcoin Blockchain Data Using a Big Data-Specific Framework. Available online: https://files.ifi.uzh.ch/CSG/staff/scheid/extern/theses/BA-D-Sommer.pdf (accessed on 16 November 2021).

- Wheatley, S.; Sornette, D.; Huber, T.; Reppen, M.; Gantner, R.N. Are Bitcoin bubbles predictable? Combining a generalized Metcalfe’s Law and the Log-Periodic Power Law Singularity model. R. Soc. Open Sci. 2019, 6, 180538. Available online: https://royalsocietypublishing.org/doi/abs/10.1098/rsos.180538 (accessed on 1 December 2021). [CrossRef]

- Bovet, A.; Campajola, C.; Mottes, F.; Restocchi, V.; Vallarano, N.; Squartini, T.; Tessone, C.J. The evolving liaisons between the transaction networks of Bitcoin and its price dynamics. arXiv 2019, arXiv:1907.03577. [Google Scholar]

- Garcia, D.; Tessone, C.J.; Mavrodiev, P.; Perony, N. The digital traces of bubbles: Feedback cycles between socio-economic signals in the Bitcoin economy. J. R. Soc. Interface 2014, 11, 20140623. Available online: https://royalsocietypublishing.org/doi/abs/10.1098/rsif.2014.0623 (accessed on 1 December 2021). [CrossRef] [PubMed]

- Liang, J.; Li, L.; Zeng, D. Evolutionary dynamics of cryptocurrency transaction networks: An empirical study. PLoS ONE 2018, 13, e0202202. [Google Scholar] [CrossRef]

- Somin, S.; Gordon, G.; Altshule, Y. Social Signals in the Ethereum Trading Network. arXiv 2018, arXiv:1805.12097. [Google Scholar]

- Guo, D.; Dong, J.; Wang, K. Graph structure and statistical properties of Ethereum transaction relationships. Inf. Sci. 2019, 492, 58–71. [Google Scholar] [CrossRef]

- Lin, D.; Wu, J.; Yuan, Q.; Zheng, Z. Modeling and Understanding Ethereum Transaction Records via a Complex Network Approach. IEEE Trans. Circuits Syst. II Express Briefs 2020, 67, 2737–2741. [Google Scholar] [CrossRef]

- Ferretti, S.; D’Angelo, G. On the Ethereum blockchain structure: A complex networks theory perspective. Concurr. Comput. Pract. Exp. 2020, 32, e5493. [Google Scholar] [CrossRef]

- Somin, S.; Gordon, G.; Pentland, A.; Shmueli, E.; Altshuler, Y. ERC20 Transactions over Ethereum Blockchain: Network Analysis and Predictions. arXiv 2020, arXiv:2004.08201. [Google Scholar]

- Collibus, F.M.D.; Partida, A.; Piškorec, M.; Tessone, C.J. Heterogeneous Preferential Attachment in Key Ethereum-Based Cryptoassets. Front. Phys. 2021, 568. [Google Scholar] [CrossRef]

- Github. Public Python Repository to Plot BTC and ETH Transactions Degree Distributions in Block Slices. Available online: https://github.com/acoxonante/sos (accessed on 26 December 2021).

- Schlager, K.J. Systems engineering-key to modern development. IRE Trans. Eng. Manag. 1956, 3, 64–66. [Google Scholar] [CrossRef]

- Azani, C.H. System of systems architecting via natural development principles. In Proceedings of the 2008 IEEE International Conference on System of Systems Engineering, Monterey, CA, USA, 2–4 June 2008; pp. 1–6. [Google Scholar] [CrossRef]

- Gorod, A.; Sauser, B.; Boardman, J. System-of-Systems Engineering Management: A Review of Modern History and a Path Forward. IEEE Syst. J. 2008, 2, 484–499. [Google Scholar] [CrossRef]

- Dahmann, J.; Baldwin, K.; Rebovich, G. Systems of Systems and Net-Centric Enterprise Systems. In Proceedings of the 7th Annual Conference on Systems Engineering Research (CSER 2009), Loughborough, UK, 20–23 April 2009; Available online: https://www.researchgate.net/publication/228990763_Systems_of_Systems_and_Net-Centric_Enterprise_Systems (accessed on 1 December 2021).

- Handy, C. Balancing Corporate Power: A New Federalist Paper. Harvard Business Reviw, November–December 2009 Issue, Leadership. Available online: https://hbr.org/1992/11/balancing-corporate-power-a-new-federalist-paper (accessed on 1 December 2021).

- Roth, N. An Architectural Assessment of Bitcoin: Using the Systems Modeling Language. Procedia Comput. Sci. 2015, 44, 527–536. [Google Scholar] [CrossRef][Green Version]

- Mylrea, M. Distributed Autonomous Energy Organizations: Next-Generation Blockchain Applications for Energy Infrastructure. In Artificial Intelligence for the Internet of Everything; Lawless, W., Mittu, R., Sofge, D., Moskowitz, I.S., Russell, S., Eds.; Chapter 12; Academic Press: Cambridge, MA, USA, 2019; pp. 217–239. ISBN 9780128176368. [Google Scholar] [CrossRef]

- Andina, D.; Partida, A. IT Security Management: IT Securiteers—Setting up an IT Security Function; Lecture Notes in Electrical Engineering, Book 61; Springer: Berlin/Heidelberg, Germany, 2010; ISBN 9789048188819. [Google Scholar]

- Li, X.; Jiang, P.; Chen, T.; Luo, X.; Wen, Q. A survey on the security of blockchain systems. Future Gener. Comput. Syst. 2020, 107, 841–853. [Google Scholar] [CrossRef]

- Vallarano, N.; Tessone, C.J.; Squartini, T. Bitcoin Transaction Networks: An overview of recent results. Front. Phys. 2020, 8, 286. [Google Scholar] [CrossRef]

- Bitcoin. BTC Reachable Nodes. Available online: https://bitnodes.earn.com/ (accessed on 16 December 2021).

- Ethernodes Dashboard. Available online: https://www.ethernodes.org/network/1 (accessed on 21 November 2021).

- Ethernodes Dashboard. Available online: https://etherscan.io/nodetracker (accessed on 16 November 2021).

- Bitcoin Network Hashrate VS Price Explained. Available online: https://stats.buybitcoinworldwide.com/hashrate-vs-price/ (accessed on 3 December 2021).

- Bitcoin Developer. Bitcoin API. RPC API Reference. Available online: https://developer.bitcoin.org/reference/rpc/index.html (accessed on 21 November 2021).

- Ethereum API. Ethers.js Library. Available online: https://docs.ethers.io/v5/api/ (accessed on 21 November 2021).

- Gansler, J.S.; Lucyshyn, W.; Spiers, A. The Role of Lead System Integrator. Available online: https://dair.nps.edu/handle/123456789/2424 (accessed on 1 December 2021).

- Github. Bitcoin Core Contributors. Available online: https://github.com/bitcoin/bitcoin/blob/master/CONTRIBUTING.md (accessed on 16 November 2021).

- Nabilou, H. Bitcoin Governance as a Decentralized Financial Market Infrastructure. SSRN . 16 March 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3555042 (accessed on 1 December 2021).

- Github. Bitcoin Improvement Proposal (BIP). Submission Workflow. Available online: https://github.com/bitcoin/bips#readme (accessed on 16 November 2021).

- Github. Ethereum Project Management Repository. Available online: https://github.com/ethereum/pm (accessed on 16 November 2021).

- Github. Ethereum Improvement Proposals. Available online: https://github.com/ethereum/eips/issues (accessed on 16 November 2021).

- Github. Ethereum Code Repository. Available online: https://github.com/ethereum (accessed on 16 November 2021).

- Buterin, V. The Most Important Scarce Resource is Legitimacy. March 2021. Available online: https://vitalik.ca/general/2021/03/23/legitimacy.html (accessed on 16 November 2021).

- Singh, R.; Dwivedi, A.D.; Srivastava, G.; Wiszniewska-Matyszkiel, A.; Cheng, X. A game theoretic analysis of resource mining in blockchain. Clust. Comput. 2020, 23, 2035–2046. [Google Scholar] [CrossRef]

- Cambridge Center for Alternative Finance. Bitcoin Mining Map. Evolution of Country Share. November 2021. Available online: https://ccaf.io/cbeci/mining_map (accessed on 23 November 2021).

- Conway, L. Thestreet.com. Ethereum Has Lost over 6500 Nodes in the Last Two Weeks. 2021. Available online: https://www.thestreet.com/crypto/ethereum/ethereum-is-still-missing-huge-amount-of-nodes-after-unintentional-hard-fork (accessed on 3 December 2021).

- Crypto.com. Measuring Global Crypto Users. February 2021. Available online: https://bit.ly/2OujUq9 (accessed on 16 November 2021).

- Electric Capital. Blockchain Developer Analysis Report. August 2019. Available online: https://bit.ly/328lcdT (accessed on 16 November 2021).

- Coinmarketcap. Wrapped BTC Market Capitalisation in Real Time. Available online: https://coinmarketcap.com/currencies/wrapped-bitcoin/ (accessed on 16 November 2021).

- Bitcoin.com. Side-Chaining $3 Billion in Value: There’s More Than 141,000 Tokenized Bitcoins Issued on Ethereum. 2020. Available online: https://bit.ly/3rZ1iwe (accessed on 16 November 2021).

- Binance.com. Tokenized Bitcoin on Ethereum Explained. April 2021. Available online: https://academy.binance.com/en/articles/tokenized-bitcoin-on-ethereum-explained (accessed on 16 November 2021).

- Coinmetrics.com. BTC ETH Price Correlation. November 2021. Available online: https://charts.coinmetrics.io/correlations (accessed on 4 August 2021).

- Investopedia.com. Bitcoin’s Taproot Upgrade: What You Should Know. Available online: https://www.investopedia.com/bitcoin-taproot-upgrade-5210039 (accessed on 4 December 2021).

- Bitcoin Lightning Network. Available online: https://lightning.network/ (accessed on 3 December 2021).

- Ethereum 2.0. Available online: https://ethereum.org/en/eth2/ (accessed on 3 December 2021).

- Blockchain.com. An Estimation of Hashrate Distribution amongst the Largest Mining Pools. April 2021. Available online: https://www.blockchain.com/charts/pools (accessed on 16 November 2021).

- Blockchain.com. Top 25 Miners by Block. Available online: https://etherscan.io/stat/miner?range=7&blocktype=blocks (accessed on 16 November 2021).

- Ethereum.org. Ethereum Improvement Proposals. Available online: https://eips.ethereum.org/all (accessed on 16 November 2021).

- Oliver Wyman. Crypto-Assets: Their Future and Regulation. Available online: https://owy.mn/2OC6jgE (accessed on 16 November 2021).

- Miyamae, T.; Honda, T.; Tamura, M.; Kawaba, M. Performance improvement of the consortium blockchain for financial business applications. J. Digit. Bank. 2018, 2, 369–378. [Google Scholar]

- Coincodex.com. Stablecoins by Market Cap and Volume. Available online: https://coincodex.com/cryptocurrencies/sector/stablecoins/ (accessed on 16 November 2021).

- Greenwald, M.B. The Future of the United States Dollar: Weaponizing the US Financial System. Available online: https://bit.ly/3fZwglF (accessed on 4 December 2021).

- Finder.com. The Top 50 NFT Collections You Should Know about. Available online: https://www.finder.com/cryptocurrency/nft-collections (accessed on 4 December 2021).

- Cryptopedia. Gemini.com. What Was the DAO? 2021. Available online: https://www.investopedia.com/tech/what-dao/ (accessed on 3 December 2021).

- Christin, N. Traveling the Silk Road: A measurement analysis of a large anonymous online marketplace. In Proceedings of the 22nd International Conference on World Wide Web, Rio de Janeiro, Brazil, 13–17 May 2013; pp. 213–224. [Google Scholar] [CrossRef]

- Bitcoin.it. Hash. Available online: https://en.bitcoinwiki.org/wiki/Hash (accessed on 4 December 2021).

- Bitcoin.it. Elliptic Curve Digital Signature Algorithm. Available online: https://en.bitcoin.it/wiki/Elliptic_Curve_Digital_Signature_Algorithm (accessed on 4 December 2021).

- Ethereum Wiki. Ethash. Available online: https://eth.wiki/en/concepts/ethash/ethash (accessed on 4 December 2021).

- Github.com. Ethereum Cryptography. Available online: https://github.com/ethereum/js-ethereum-cryptography (accessed on 4 December 2021).

- Gisin, N.; Ribordy, G.; Tittel, W.; Zbinden, H. Quantum cryptography. Rev. Mod. Phys. 2002, 74, 145. [Google Scholar] [CrossRef]

- Damianou, A.; Khan, M.A.; Angelopoulos, C.M.; Katos, V. Threat Modelling of IoT Systems Using Distributed Ledger Technologies and IOTA. In Proceedings of the 2021 17th International Conference on Distributed Computing in Sensor Systems (DCOSS), Pafos, Cyprus, 14 July 2021; IEEE: Piscataway, NJ, USA, 2021; pp. 404–413. [Google Scholar] [CrossRef]

- Irwin, D.A. The Nixon shock after forty years: The import surcharge revisited. World Trade Rev. 2013, 12, 29–56. [Google Scholar] [CrossRef][Green Version]

- Xu, Y.; Liu, X.; Cao, X.; Huang, C.; Liu, E.; Qian, S.; Liu, X.; Wu, Y.; Dong, F.; Qiu, C.-W.; et al. Artificial intelligence: A powerful paradigm for scientific research. Innovation 2021, 2, 100179. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Blockchain Name | Window Duration | Date | Number of Blocks | Average Number of Transactions per Block |

|---|---|---|---|---|

| BTC | 48 h | 21 December 2020 | 278 | 2000 |

| ETH | 2 min | 26 December 2020 | 10 | 144 |

| Topic | Study | Main Takeaway | References |

|---|---|---|---|

| Blockchain technology | Many use cases | A driver for change | [18,19,20,21] |

| Impacting many sectors | [21,22,23,24,25,28,29,30,31,32,33] | ||

| Key implementations: BTC & ETH | As complex networks | Power law degrees | [5,34,35,36,37,38,39,40,41] |

| “Rich get richer” | [9,42,43,44,45,46,47,48] | ||

| Systems Engineering | Complexity | Open vs. close systems | [51] |

| SoSE | Supersystems | 5 SoS properties | [13,52] |

| Network-centricity | Info exchange | [9,13,53] | |

| Blockchain as SoS | Only focus on BTC | No complementary roles | [13,55,56] |

| Intentional risk | Attacks | Static vs. dynamic risk | [16,57,58] |

| Parameters | Value, accessibility and anonymity | [16,57] | |

| Our contribution | |||

| Public blockchains | Modelled as a SoS | To improve resilience | [55,56] |

| against intentional risk |

| Step | Label | Description | Why? |

|---|---|---|---|

| 1 | Common goal | Component systems share an ultimate goal | Definition of SoS |

| 2 | Open & Complex | Open systems with growing complexity? | Continuous evolution |

| 3 | Network-centric | Components use networks to communicate | Information exchange |

| Autonomy, Belonging | |||

| 4 | Characteristics | Connectivity, Diversity | SoS Balance panel |

| Evolutive emergence | |||

| 5 | Risk analysis | Vulnerabilities and threats | Future evolution |

| Resilience against intentional risk |

| Blockchain | Start | Active Nodes | Market Cap (USD B) | ||||

|---|---|---|---|---|---|---|---|

| Name | Date | 7/2020 | 4/2021 | 11/2021 | 7/2020 | 4/2021 | 11/2021 |

| BTC | 2009 | 10,540 | 9610 | 13,898 | 170 | 1099 | 1142 |

| ETH | 2014 | 7900 | 4250 | 3238 | 26 | 222 | 505 |

| Interaction via | Description | Relevance |

|---|---|---|

| People | Holders of crypto keep BTC and ETH in their portfolio | Increasing |

| Organisations | Crypto exchanges offer swaps between BTC and ETH and other coins | Increasing |

| Culture | BTC and ETH share decentralised principles | Stable |

| Activities | Coin wrapping, e.g., WBTC: an ERC20 token in ETH | Increasing |

| Relationships | Both subject to additional financial regulation | Increasing |

| Blockchain | Users | Contrib. | Core Developers | Active Node Location (%) | ||

|---|---|---|---|---|---|---|

| Name | (M) | Devs. | 4/2021 | 11/2021 | 4/2021 | 11/2021 |

| BTC | 71 | 500 | 37 | 39 | CN (65) | US (35), KZ (14), RU (12) |

| ETH | 14 | 1000 | 69 | 81 | US (34), DE (22) | US (35), DE (15) |

| Realm | Emergent Property | Intended |

|---|---|---|

| SoS | Decentralised network of digital value | Yes |

| SoS | Alternative to fiat-based financial system | No |

| BTC | Peer to peer electronic cash system | Yes |

| BTC | Digital global reserve asset (“digital gold”) | No |

| ETH | The world distributed computer | Yes |

| ETH | Main DeFi platform (“alternative financial conduit”) | No |

| ETH | Platform to transfer “unique” digital value | No |

| Project | Origin | Business Case | Market Cap | Consensus |

|---|---|---|---|---|

| (B USD) | ||||

| Binance Coin (BNB) | 2017 | Biggest crypto exchange’s blockchain | 111 | Proof of authority |

| Solana (SOL) | 2020 | DeFi solution with short processing times | 61 | Proof of history |

| Cardano (ADA) | 2017 | Decentralised app engine | 54 | Proof of stake |

| Polkadot (DOT) | 2017 | Multi-chain focused on cross-chain transfers | 37 | Nominated proof of stake |

| Action | Principle | Phase |

|---|---|---|

| Reduce asset value | Distribute value across many addresses | Design/Operations |

| Avoid very rich hubs | Operations | |

| Decrease accessibility | Maintain the use of strong crypto | Design |

| Improve code security | Development | |

| Simplify interfaces | Development | |

| Improve private key security | Design/Dev/Operations | |

| Extend use of cold storage | Operations | |

| Enhance security awareness in users | Communications | |

| Decrease anonymity | Improve identity management | Operations |

| Link with physical identities | Governance | |

| Achieve global legal coverage | Governance | |

| Extend blockchain monitoring | Operations | |

| Increase legal measures | Extend know your customer processes | Operations |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Partida, A.; Gerassis, S.; Criado, R.; Romance, M.; Giráldez, E.; Taboada, J. Modeling Bitcoin plus Ethereum as an Open System of Systems of Public Blockchains to Improve Their Resilience against Intentional Risk. Electronics 2022, 11, 241. https://doi.org/10.3390/electronics11020241

Partida A, Gerassis S, Criado R, Romance M, Giráldez E, Taboada J. Modeling Bitcoin plus Ethereum as an Open System of Systems of Public Blockchains to Improve Their Resilience against Intentional Risk. Electronics. 2022; 11(2):241. https://doi.org/10.3390/electronics11020241

Chicago/Turabian StylePartida, Alberto, Saki Gerassis, Regino Criado, Miguel Romance, Eduardo Giráldez, and Javier Taboada. 2022. "Modeling Bitcoin plus Ethereum as an Open System of Systems of Public Blockchains to Improve Their Resilience against Intentional Risk" Electronics 11, no. 2: 241. https://doi.org/10.3390/electronics11020241

APA StylePartida, A., Gerassis, S., Criado, R., Romance, M., Giráldez, E., & Taboada, J. (2022). Modeling Bitcoin plus Ethereum as an Open System of Systems of Public Blockchains to Improve Their Resilience against Intentional Risk. Electronics, 11(2), 241. https://doi.org/10.3390/electronics11020241