A Systematic Multi-Criteria Quantitative Model for Evaluating the Change Order Impact on Contractors’ Cash Flow

Abstract

1. Introduction and Literature Review

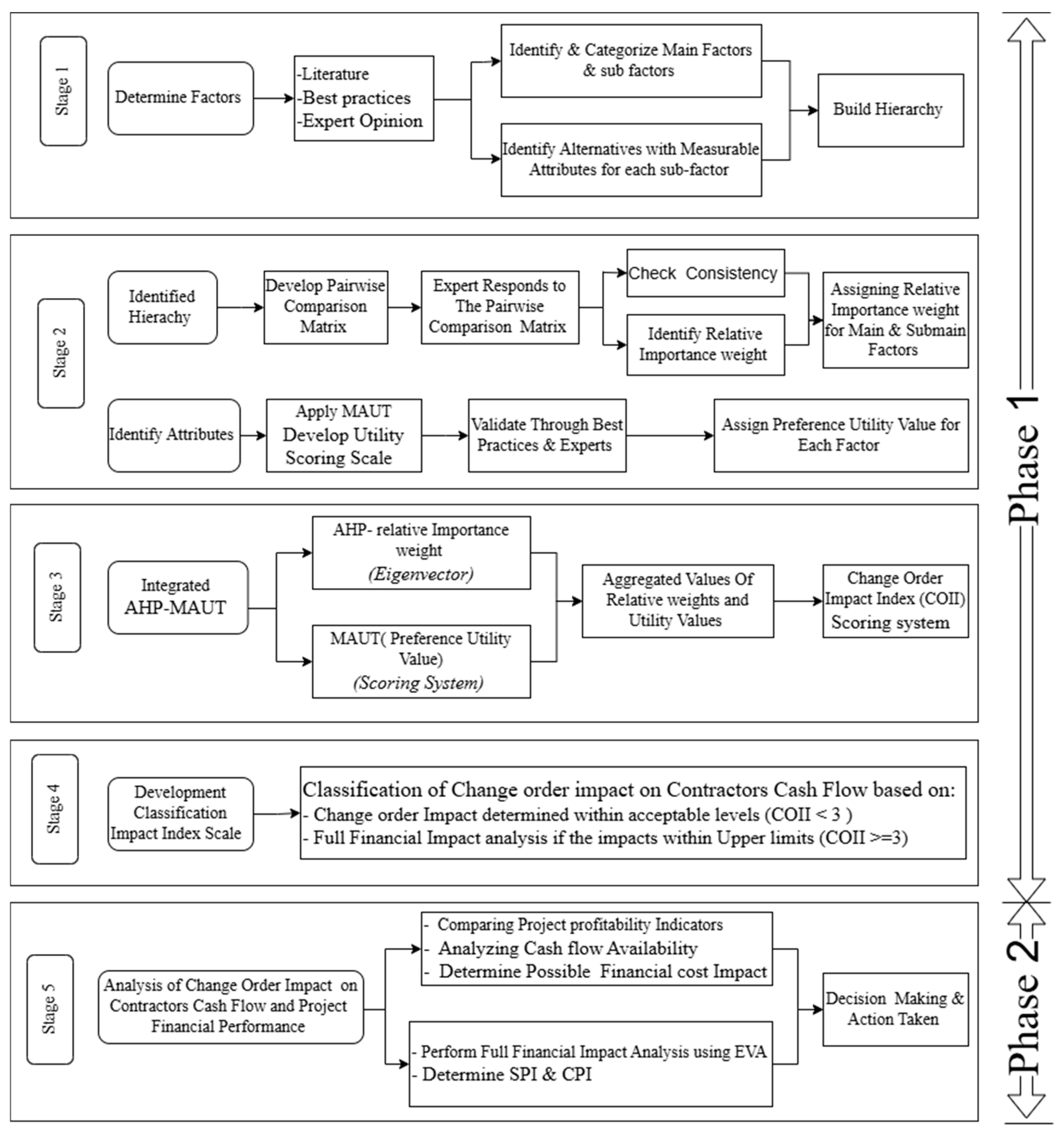

2. Research Methodology Phases

2.1. Stages of Phase One

2.1.1. First Stage: Identification and Categorization of Factors

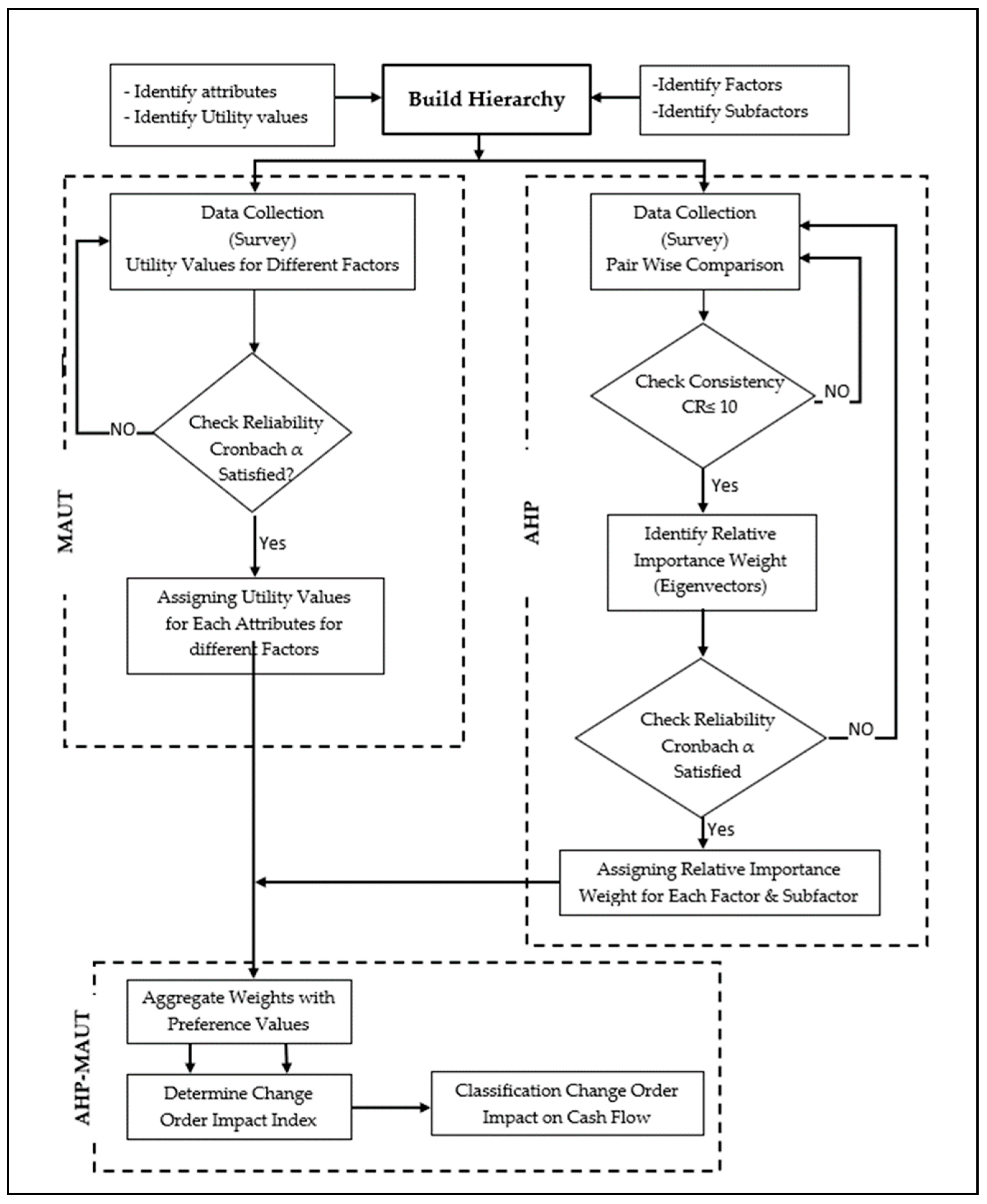

2.1.2. Second Stage: Determining Relative Importance Using AHP

2.1.3. Third Stage: Integration of AHP and MAUT for COII Development

2.1.4. Fourth Stage: Classification of the COII Scale

2.2. Stage Five of Phase Two

3. Data Collection and Analysis

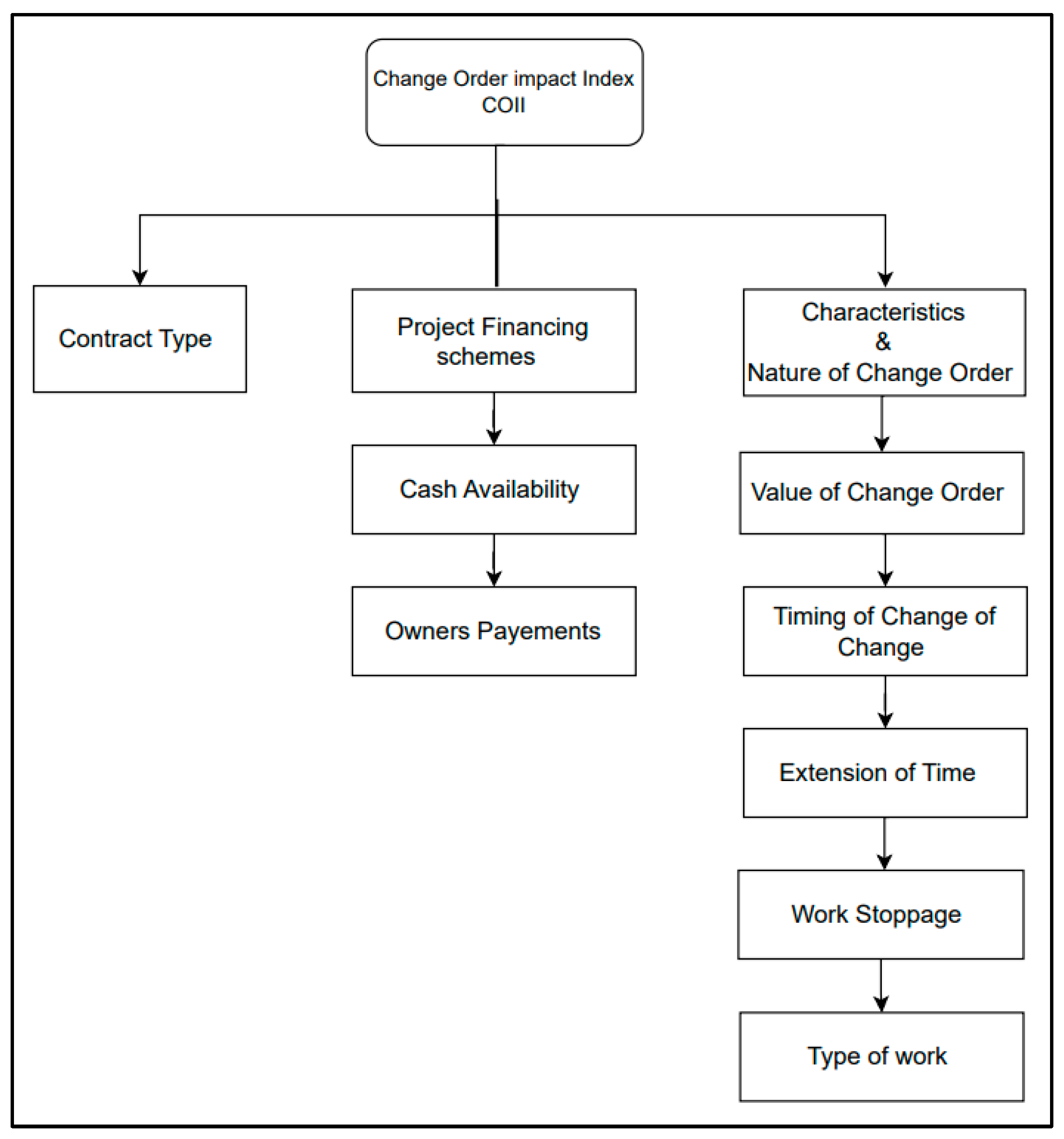

3.1. Factors Affecting Contractors’ Cash Flow and Project Financial Performance

3.2. Factors Utility Values

4. Data Analysis and Model Development

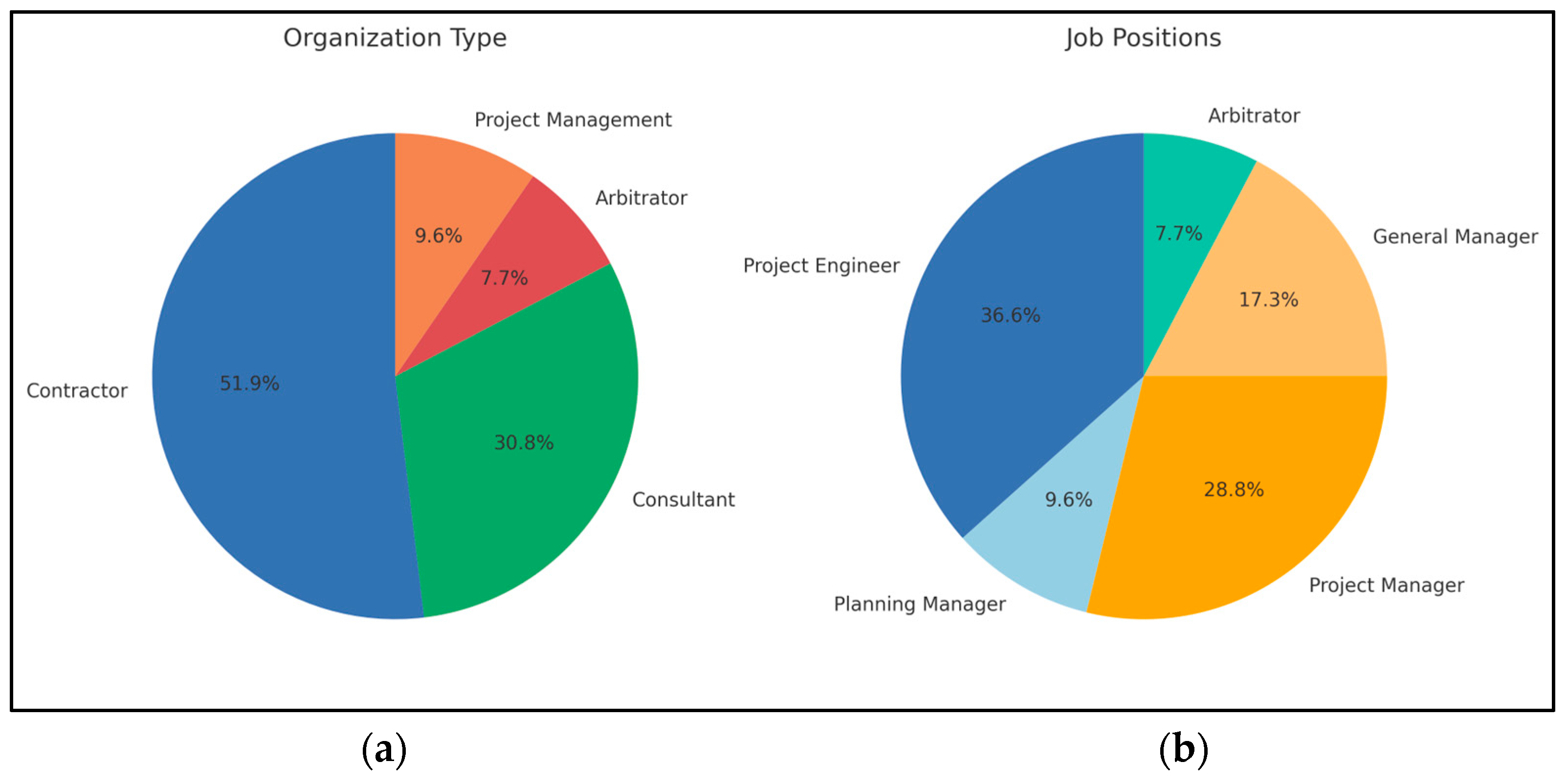

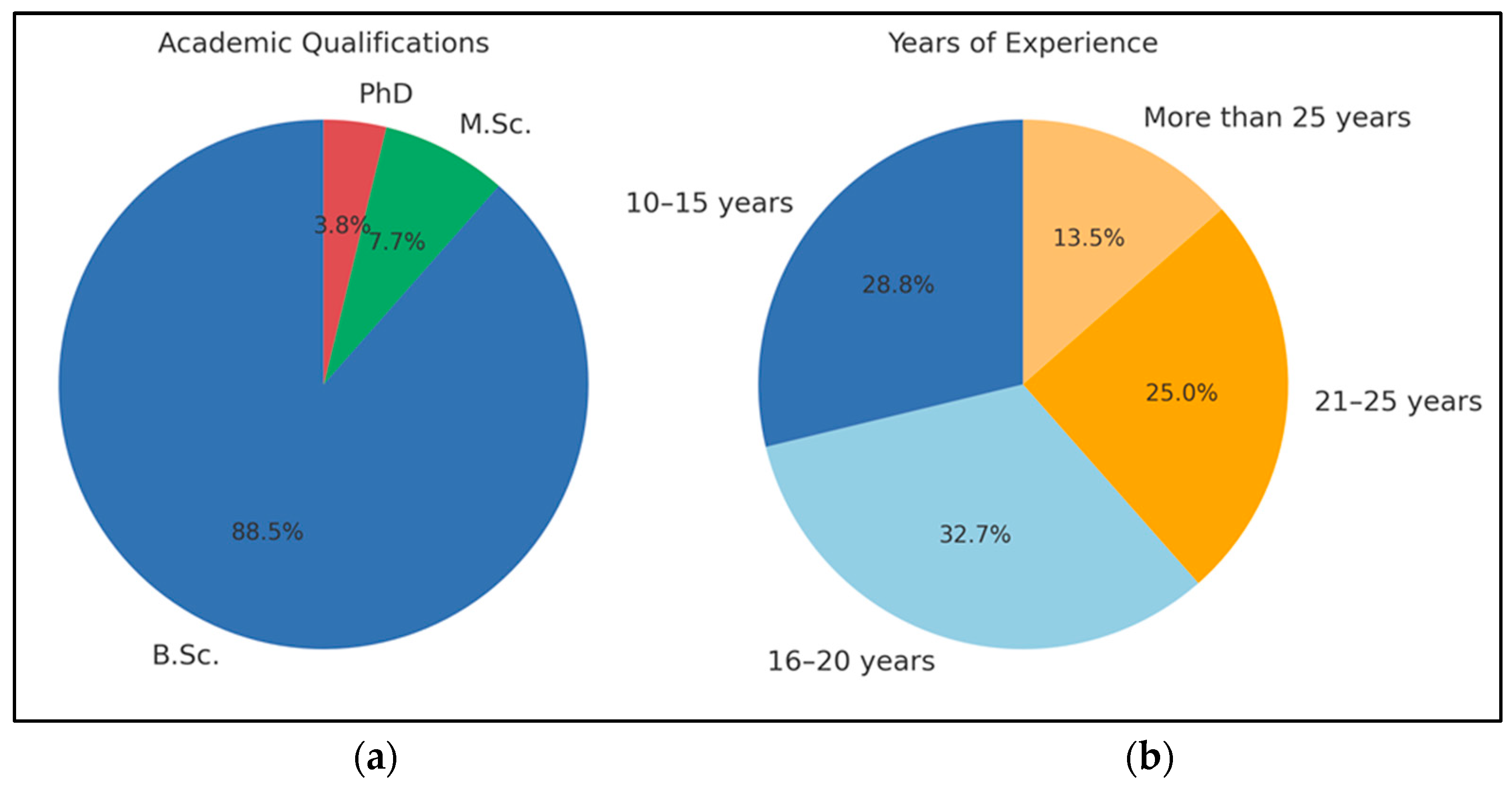

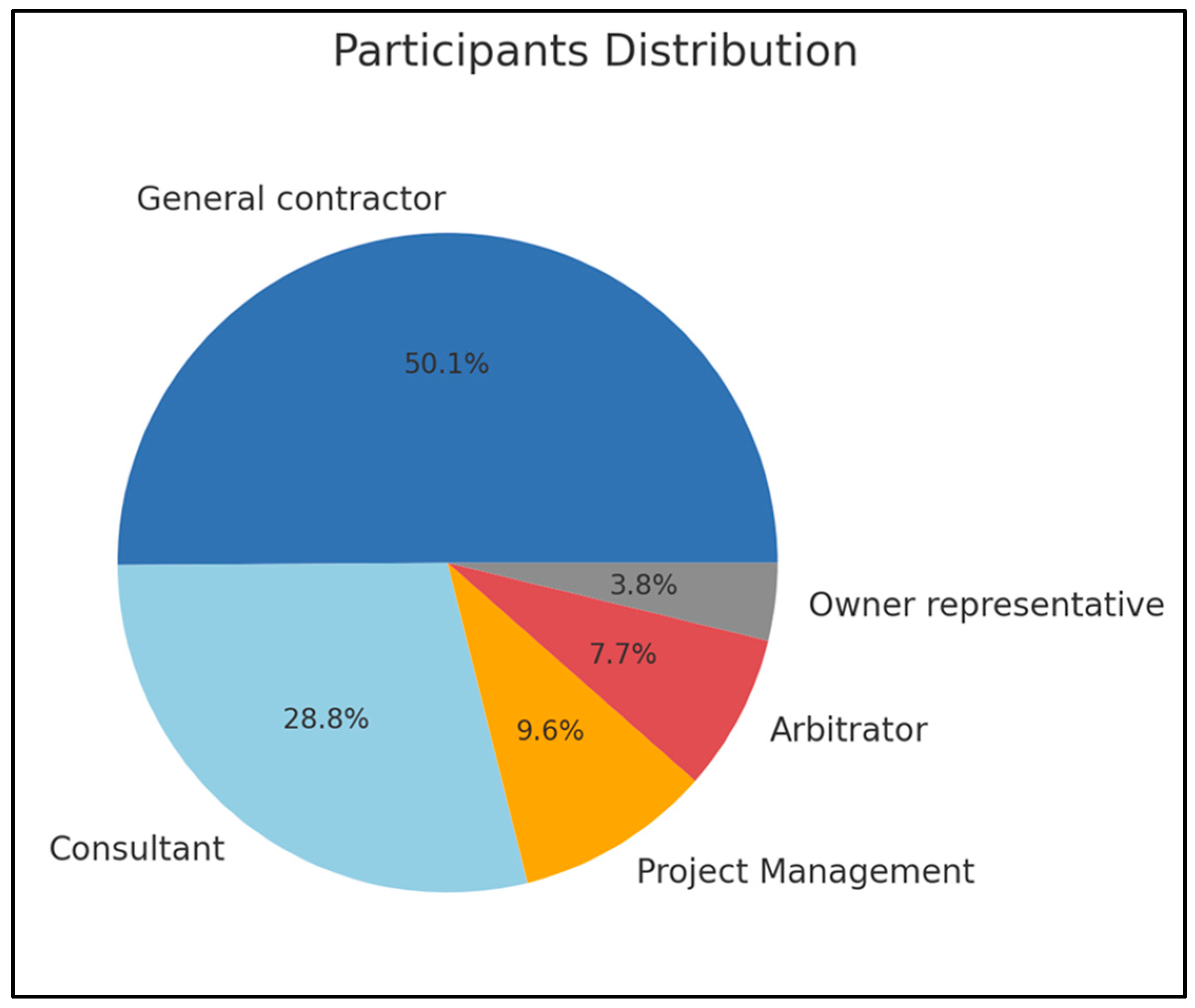

4.1. The Sample Characteristics

4.2. Determining Relative Weights

4.3. Data Reliability

Main Factors Relative Weight Data Reliability

4.4. Determining Utility Values

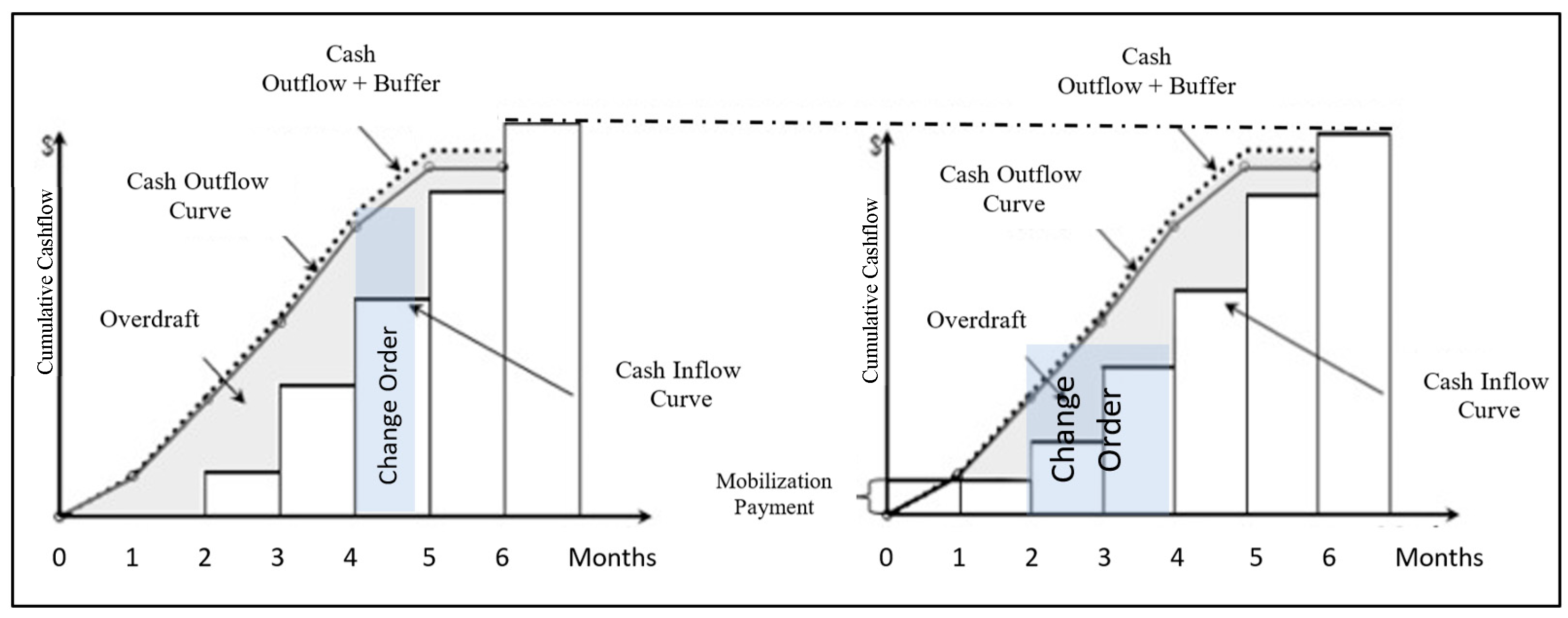

4.4.1. Cash Availability

4.4.2. Owners’ Payments

4.4.3. Contract Types

4.4.4. Change Order Values

4.4.5. Timing of Change Orders

4.4.6. Time Extension

4.4.7. Addition, Omission, and Rework

4.4.8. Work Stoppage

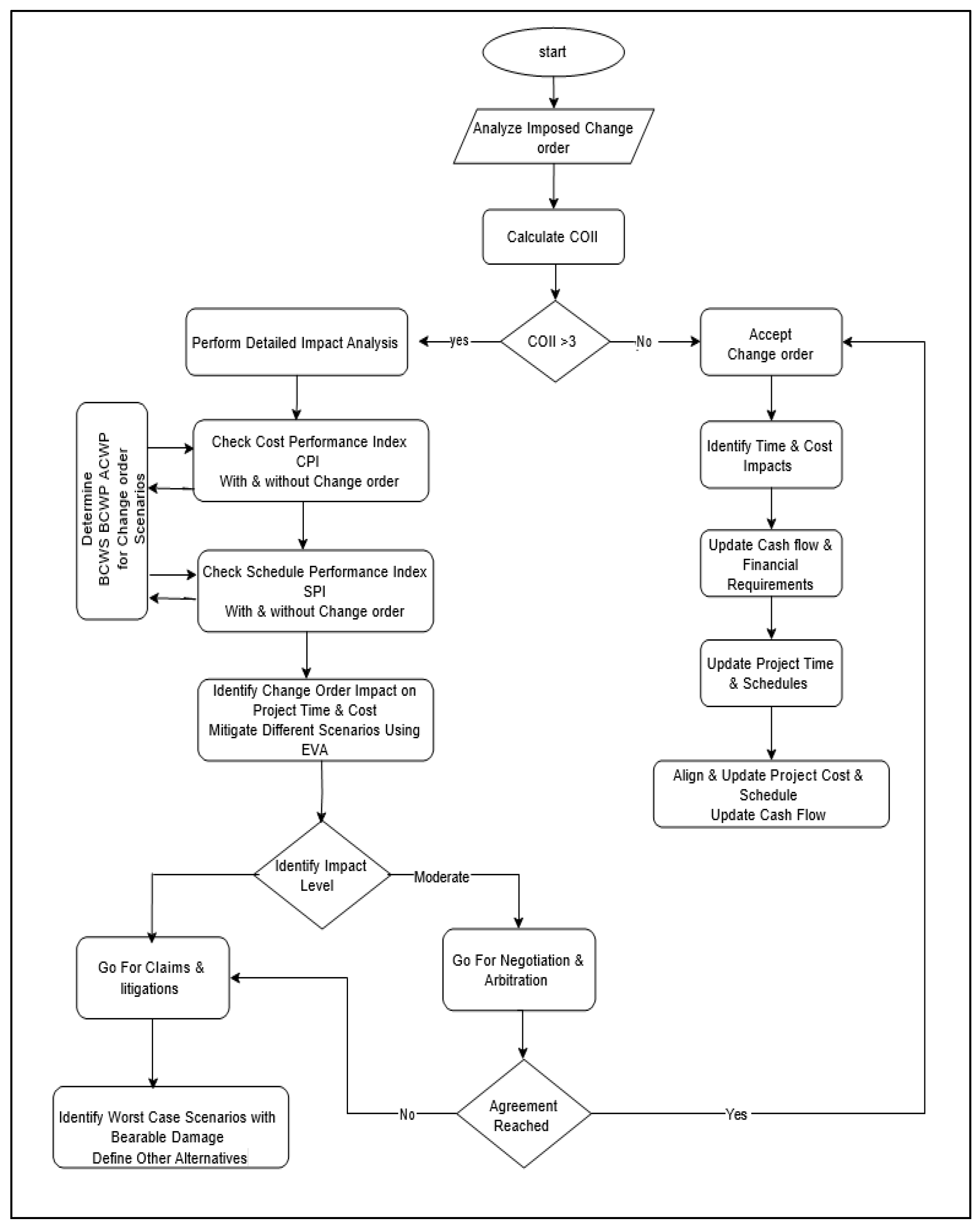

4.5. Change Order Impact Index Calculation

4.5.1. Change Order Impact Index Interpretation

4.5.2. Change Order Impact Index Analysis

4.6. Model Validation

5. Discussion and Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Naji, K.K.; Gunduz, M.; Naser, A.F. The Effect of Change-Order Management Factors on Construction Project Success: A Structural Equation Modeling Approach. J. Constr. Eng. Manag. 2022, 148, 04022085. [Google Scholar] [CrossRef]

- Demiss, B.A.; Elsaigh, W.A. Application of novel hybrid deep learning architectures combining Convolutional Neural Networks (CNN) and Recurrent Neural Networks (RNN): Construction duration estimates prediction considering preconstruction uncertainties. Eng. Res. Express 2024, 6, 032102. [Google Scholar] [CrossRef]

- Heravi, G.; Charkhakan, M.H. Predicting Change by Evaluating the Change Implementation Process in Construction Projects Using Event Tree Analysis. J. Manag. Eng. 2015, 31, 04014081. [Google Scholar] [CrossRef]

- Alkhalifah, S.J.; Tuffaha, F.M.; Al Hadidi, L.A.; Ghaithan, A. Factors influencing change orders in oil and gas construction projects in Saudi Arabia. Built Environ. Proj. Asset Manag. 2023, 13, 430–452. [Google Scholar] [CrossRef]

- Zangana, H.M.; Bazeed, S.M.S.; Ali, N.Y.; Abdullah, D.T. Navigating Project Change: A Comprehensive Review of Change Management Strategies and Practices. Indones. J. Educ. Soc. Sci. 2024, 3, 166–179. [Google Scholar] [CrossRef]

- Tarawneh, S.; Almahmoud, A.F.; Hajjeh, H. Impact of cash flow variation on project performance: Contractors’ perspective. Eng. Manag. Prod. Serv. 2023, 15, 73–85. [Google Scholar] [CrossRef]

- Koopman, K.; Cumberlege, R. Cash flow management by contractors. IOP Conf. Ser. Earth Environ. Sci. 2021, 654, 012028. [Google Scholar] [CrossRef]

- Purnus, A.; Bodea, C.-N. Financial Management of the Construction Projects: A Proposed Cash Flow Analysis Model at Project Portfolio Level. Organ. Technol. Manag. Constr. Int. J. 2015, 7, 1217–1227. [Google Scholar] [CrossRef]

- Mahmoud, H.; Ahmed, V.; Beheiry, S. Construction Cash Flow Risk Index. J. Risk Financ. Manag. 2021, 14, 269. [Google Scholar] [CrossRef]

- Alashwal, A.M.; Chew, M.Y. Simulation techniques for cost management and performance in construction projects in Malaysia. Built Environ. Proj. Asset Manag. 2017, 7, 534–545. [Google Scholar] [CrossRef]

- Chadee, A.; Ali, H.; Gallage, S.; Rathnayake, U. Modelling the Implications of Delayed Payments on Contractors’ Cashflows on Infrastructure Projects. Civ. Eng. J. 2023, 9, 52–71. [Google Scholar] [CrossRef]

- Sahu, P.; Bera, D.K.; Parhi, P.K. Analyzing the impact of construction delays on disputes in india: A statistical and machine learning approach. J. Mech. Contin. Math. Sci. 2024, 19, 24–34. [Google Scholar] [CrossRef]

- Kyrychenko, S.O.; Katsevych, M.M. Risk Management of Financial Activities in the Construction Industry. Bus. Inf. 2024, 10, 175–181. [Google Scholar] [CrossRef]

- Alzara, M. Exploring the Impacts of Change Orders on Performance of Construction Projects in Saudi Arabia. Adv. Civ. Eng. 2022, 2022, 5775926. [Google Scholar] [CrossRef]

- Alajmi, A.M.; Ahmed Memon, Z. A Review on Significant Factors Causing Delays in Saudi Arabia Construction Projects. Smart Cities 2022, 5, 1465–1487. [Google Scholar] [CrossRef]

- Martanti, A.Y.; Kasih, T.P.; Tanojo, F.H. Study of Work Order Variation and Its Influence On Project Performance in Terms of Cost and Implementation Time in the Tenjoresmi Area Arrangement Project. Asian J. Eng. Soc. Health 2024, 3, 362–373. [Google Scholar] [CrossRef]

- Sanjaya, A.; Isvara, W. Risk Factor Assessment Causing Contract Change Orders in the Double-Double Track Project. J. Res. Soc. Sci. Econ. Manag. 2024, 4, 485–496. [Google Scholar] [CrossRef]

- Waty, M. Road construction change order analysis (technical causes and initiators). Int. J. Appl. Sci. Technol. Eng. 2023, 1, 866–881. [Google Scholar] [CrossRef]

- Muhammad, Q.S.A.; Shuaibu, Q.K.U.; Hassan, I.A. Assessing the Factors Influencing Cashflow Management in Project Delivery in Kaduna Metropolis, Nigeria. Int. J. Sci. Adv. 2023, 4, 719–725. [Google Scholar] [CrossRef]

- Buertey, J.I.T.B.; Adjei-Kumi, T.A.K. Cashflow forecasting in the construction industry: The case of Ghana. Pentvars Bus. J. 2012, 6, 65–81. [Google Scholar] [CrossRef]

- Kazar, G. A data-driven approach for predicting cash flow performance of public owners in building projects: Insights from Turkish cases. Eng. Constr. Archit. Manag. 2024, 31, 2541–2564. [Google Scholar] [CrossRef]

- Firmansyah, A.A.; Sahab, M.T.Z.; Wisudanto, W. The influence of investment decisions, free cash flow, and debt policy on the financial performance of construction companies. J. Ilm. Manaj. Ekon. Akunt. (MEA) 2023, 7, 1719–1734. [Google Scholar] [CrossRef]

- Maulanisa, N.F.; Chumaidiyah, E.; Sriwana, I.K. A system dynamics modeling approach for improving engineering, procurement, and construction project performance: A case study. J. Infrastruct. Policy Dev. 2024, 8, 8730. [Google Scholar] [CrossRef]

- Jahangoshai Rezaee, M.; Yousefi, S.; Chakrabortty, R.K. Analysing causal relationships between delay factors in construction projects. Int. J. Manag. Proj. Bus. 2021, 14, 412–444. [Google Scholar] [CrossRef]

- Kotb, M.; Ibrahim, M.A.R.; Al-Olayan, Y.S. A Study of the Cash Flow Forecasting Impact on the Owners Financial Management of Construction Projects in the State of Kuwait. Asian Bus. Res. 2018, 3, 69. [Google Scholar] [CrossRef]

- Jagannathan, M.; Delhi, V.S.K. Decoding a construction organisation’s tendency to litigate: An understanding through financial statements. Built Environ. Proj. Asset Manag. 2023, 13, 453–470. [Google Scholar] [CrossRef]

- Voigt, A.; Khalaf, M.; Mattar, S.G. Impact of Cash Shortages on Project Performance. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2023, 15. [Google Scholar] [CrossRef]

- FMajaham, R.F.; Mustapa, M.; Darmansah, N.F. A Critical Review of Internal Factors Impacting the Growth of Construction Firms. Int. J. Res. Innov. Soc. Sci. 2025, VIII, 1501–1513. [Google Scholar] [CrossRef]

- Dorrah, D.H.; McCabe, B. Integrated Agent-Based Simulation and Game Theory Decision Support Framework for Cash Flow and Payment Management in Construction Projects. Sustainability 2023, 16, 244. [Google Scholar] [CrossRef]

- Al-Shihabi, S.; Elazouni, A. Modified Finance-Based Scheduling with Activity Splitting. Mathematics 2025, 13, 139. [Google Scholar] [CrossRef]

- Kim, Y.J.; Skibniewski, M.J. Cash and Claim: Data-Based Inverse Relationships between Liquidity and Claims in the Construction Industry. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2020, 12. [Google Scholar] [CrossRef]

- Safitri, A.A.; Wiryasuta, I.K.H.; Sandi, E.A. Variasi Sistem Pembayaran Terhadap Cash Flow (Studi Kasus: Pembangunan Laboratorium Terpadu AKN Blitar). J. Tek. Sipil Giratory UPGRIS 2024, 1, 10–19. [Google Scholar] [CrossRef]

- Jiang, C.; Li, X.; Lin, J.-R.; Liu, M.; Ma, Z. Adaptive control of resource flow to optimize construction work and cash flow via online deep reinforcement learning. Autom. Constr. 2023, 150, 104817. [Google Scholar] [CrossRef]

- Zayed, T.; Liu, Y. Cash flow modeling for Construction projects. Eng. Constr. Archit. Manag. 2014, 21, 170–189. [Google Scholar] [CrossRef]

- Söylen, Z.; Mammadova, F.; Fasounaki, M.; Özmen, A.İ.; İnce, G. Cash Flow Forecasting Based on Wavelet Transform and Neural Networks. In Proceedings of the 2023 8th International Conference on Computer Science and Engineering (UBMK), Burdur, Turkey, 13–15 September 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 306–311. [Google Scholar] [CrossRef]

- Zheng, Y.; Tu, K. A Robust Forecasting Framework for Multi-Series Cash Flow Prediction. In Proceedings of the 2023 6th International Conference on Information Communication and Signal Processing (ICICSP), Xi’an, China, 23–25 September 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 898–902. [Google Scholar] [CrossRef]

- Kim, H.; Grobler, F. Preparing a Construction Cash Flow Analysis Using Building Information Modeling (BIM) Technology. J. Constr. Eng. Proj. Manag. 2013, 3, 1–9. [Google Scholar] [CrossRef]

- Zhu, L.; Yan, M.; Bai, L. Prediction of Enterprise Free Cash Flow Based on a Backpropagation Neural Network Model of the Improved Genetic Algorithm. Information 2022, 13, 172. [Google Scholar] [CrossRef]

- Alkhattabi, L.; Alkhard, A.; Gouda, A. Effects of change orders on the budget of the public sector construction projects in the kingdom of Saudi Arabia. Results Eng. 2023, 20, 101628. [Google Scholar] [CrossRef]

- Xiao, H.; Proverbs, D. Factors influencing contractor performance: An international investigation. Eng. Constr. Archit. Manag. 2003, 10, 322–332. [Google Scholar] [CrossRef]

- Adejoh, A.A.; Asebiomo, M.M.; Ogunbode, E.B.; Oyewobi, L.O.; Sani, M.A.; Isa, R.B.; Jimoh, R.A. Influence of Contractor Selection Criteria on Critical Success Factors of Public Project Delivery in Abuja. Environ. Technol. Sci. J. 2023, 13, 86–98. [Google Scholar] [CrossRef]

- Zamim, S.K. Identification of crucial performance measurement factors affecting construction projects in Iraq during the implementation phase. Cogent Eng. 2021, 8, 1882098. [Google Scholar] [CrossRef]

- Gunduz, M.; Mohammad, K.O. Assessment of change order impact factors on construction project performance using Analytic Hierarchy Process (AHP). Technol. Econ. Dev. Econ. 2019, 26, 71–85. [Google Scholar] [CrossRef]

- Omopariola, E.D.; Windapo, A.O.; Edwards, D.J.; Aigbavboa, C.O.; Yakubu, S.U.-N.; Obari, O. Modelling the domino effect of advance payment system on project cash flow and organisational performance. Eng. Constr. Archit. Manag. 2023, 31, 59–78. [Google Scholar] [CrossRef]

- Bissoon, S.; Outridge, D. Delayed payments impacts on planned cash flow of small and medium contractors for a special purpose company. In Proceedings of the International Conference on Emerging Trends in Engineering & Technology (IConETech-2020), Vellore, India, 24–25 February 2020; pp. 313–324. [Google Scholar] [CrossRef]

- Cui, Q.; Hastak, M.; Halpin, D. Systems analysis of project cash flow management strategies. Constr. Manag. Econ. 2010, 28, 361–376. [Google Scholar] [CrossRef]

- Chiang, Y.; Cheng, E.W.L. Construction loans and industry development: The case of Hong Kong. Constr. Manag. Econ. 2010, 28, 959–969. [Google Scholar] [CrossRef]

- Lee, J.I.; Lee, H.-S.; Park, M. Contractor Liquidity Evaluation Model for Successful Public Housing Projects. J. Constr. Eng. Manag. 2018, 144, 04018109. [Google Scholar] [CrossRef]

- El-adaway, I.; Fawzy, S.; Burrell, H.; Akroush, N. Studying Payment Provisions under National and International Standard Forms of Contracts. J. Leg. Aff. Disput. Resolut. Eng. Constr. 2017, 9, 04516011. [Google Scholar] [CrossRef]

- Hesham, H.K. Payment procedures under FIDIC construction contract. Proc. Int. Struct. Eng. Constr. 2022, 9(LDR-05-1–LDR-05-6). [Google Scholar] [CrossRef]

- Roja, Z.; Kalkis, H.; Roja, I.; Zalkalns, J.; Sloka, B. Work strain predictors in construction work. Agron. Res. 2017, 15, 2090–2099. [Google Scholar] [CrossRef]

- Marulanda, A.; Neuenschwander, M. Contractual time for completion adjustment in the FIDIC Emerald Book. In Tunnels and Underground Cities: Engineering and Innovation Meet Archaeology, Architecture and Art; CRC Press: Boca Raton, FL, USA, 2019; pp. 4494–4500. [Google Scholar] [CrossRef]

- Moselhi, O.; Assem, I.; El-Rayes, K. Change Orders Impact on Labor Productivity. J. Constr. Eng. Manag. 2005, 131, 354–359. [Google Scholar] [CrossRef]

- Choi, K.; Lee, H.W.; Bae, J.; Bilbo, D. Time-Cost Performance Effect of Change Orders from Accelerated Contract Provisions. J. Constr. Eng. Manag. 2016, 142, 04015085. [Google Scholar] [CrossRef]

- Khuder, S.S.; Ibrahim, A.; Eedan, O. Adopting a Method for Calculating the Impact of Change Orders on the Time it Takes to Complete Bridge Projects. Iraqi J. Civ. Eng. 2022, 15, 52–58. [Google Scholar] [CrossRef]

- Omopariola, E.D.; Windapo, A.O.; Edwards, D.J.; Chileshe, N. Attributes and impact of advance payment system on cash flow, project and organisational performance. J. Financ. Manag. Prop. Constr. 2022, 27, 306–322. [Google Scholar] [CrossRef]

- Dabirian, S.; Ahmadi, M.; Abbaspour, S. Analyzing the impact of financial policies on construction projects performance using system dynamics. Eng. Constr. Archit. Manag. 2023, 30, 1201–1221. [Google Scholar] [CrossRef]

- Liu, Y. Risk Analysis and Research for Construction Projects. Adv. Econ. Manag. Political Sci. 2023, 19, 181–187. [Google Scholar] [CrossRef]

- Ismaeil, E.M.H.; Sobaih, A.E.E. A Proposed Model for Variation Order Management in Construction Projects. Buildings 2024, 14, 726. [Google Scholar] [CrossRef]

- Mofleh Alshehhi, H.S. The impact of risk management on the performance of construction projects. In Proceedings of the MBP 2024 Tokyo International Conference on Management & Business Practices, 18–19 January Proceedings of Social Science and Humanities Research Association (SSHRA), Tokyo, Japan, 18–19 January 2024; pp. 114–115. [Google Scholar] [CrossRef]

- Oladapo, A.A. A quantitative assessment of the cost and time impact of variation orders on construction projects. J. Eng. Des. Technol. 2007, 5, 35–48. [Google Scholar] [CrossRef]

- Al Maamari, A.; Khan, F. Evaluating the Causes and Impact of Change Orders on Construction Projects Performance in Oman. Int. J. Res. Entrep. Bus. Stud. 2021, 2, 41–50. [Google Scholar] [CrossRef]

- Wang, J.; Yuan, H. Factors affecting contractors’ risk attitudes in construction projects: Case study from China. Int. J. Proj. Manag. 2011, 29, 209–219. [Google Scholar] [CrossRef]

- Taylan, O.; Bafail, A.O.; Abdulaal, R.M.S.; Kabli, M.R. Construction projects selection and risk assessment by fuzzy AHP and fuzzy TOPSIS methodologies. Appl. Soft Comput. 2014, 17, 105–116. [Google Scholar] [CrossRef]

- Cheng, M.-Y.; Hoang, N.-D.; Wu, Y.-W. Cash flow prediction for construction project using a novel adaptive time-dependent least squares support vector machine inference model. J. Civ. Eng. Manag. 2015, 21, 679–688. [Google Scholar] [CrossRef]

- Peleskeica, C.A.; Dorcav, V.; Munteanura, R.A.; Munteanur, R. Risk Consideration and Cost Estimation in Construction Projects Using Monte Carlo Simulation. Management 2015, 10, 18544223. [Google Scholar]

- Barbosa, P.S.F.; Pimentel, P.R. A linear programming model for cash flow management in the Brazilian construction industry. Constr. Manag. Econ. 2001, 19, 469–479. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Main Factors | Subfactors | Attributes |

|---|---|---|

| Project Financing Schemes | Cash Availability | Cash is available |

| % Cash Available and % Bank Loans | ||

| Bank Loans | ||

| Loan Limit Achieved | ||

| Owner’s Payments | Extremely Delays | |

| Moderately Delays | ||

| No Delays | ||

| Contract Type | Unit Price | |

| Lump Sum | ||

| Cost Plus a Fixed Fee | ||

| Cost Plus Percentage of Cost | ||

| Guaranteed Maximum Price | ||

| Target Price Plus a Fee | ||

| Characteristics and Nature of Change Orders | Value Of Change Orders | >0% ≤5% |

| >5% ≤10% | ||

| >10% ≤15% | ||

| >15% ≤20% | ||

| >20% | ||

| Timing of Change Orders | <0% (Before construction) | |

| >0% ≤25% | ||

| >25% ≤50% | ||

| >50% ≤75% | ||

| >75% ≤100% | ||

| Extension of Time | Extremely Sufficient | |

| Sufficient | ||

| Moderately Sufficient | ||

| Not Sufficient | ||

| Work Stoppage | Stoppage | |

| No Stoppage | ||

| Type of Work | Addition | |

| Omission | ||

| Rework | ||

| Type of Participants | No. of Forms Send | No. of Forms Responded to | % of Responding | % Out of 52 Returned Forms of Response |

|---|---|---|---|---|

| Arbitrators | 8 | 4 | 50 | 8 |

| Consultants | 40 | 16 | 40 | 31 |

| Contractors | 60 | 27 | 45 | 52 |

| Project Managers | 12 | 5 | 42 | 9 |

| Total | 120 | 52 | 43 | 100 |

| Main Factors | Subfactors | Level 1 (W1) | Level 2 (W2) | Final Weight (W1 × W2) |

|---|---|---|---|---|

| Project Financing Schemes | Cash Availability | 0.44 | 0.56 | 0.246 |

| Owner’s Payments | 0.44 | 0.194 | ||

| Contract Type | --------- | 0.30 | 1 | 0.3 |

| Characteristics and Nature of Change Orders | Value of Change Orders | 0.26 | 0.30 | 0.078 |

| Timing of Change Orders | 0.22 | 0.057 | ||

| Extension of Time | 0.15 | 0.039 | ||

| Work Stoppage | 0.28 | 0.073 | ||

| Type of Work | 0.05 | 0.013 |

| Cronbach’s Alpha | Interpretation |

|---|---|

| 0.9. and greater | High Reliability |

| 0.8–0.89 | Good Reliability |

| 0.7–0.79 | Acceptable Reliability |

| 0.65–0.69 | Marginal Reliability |

| 0.5–0.64 | Minimal Reliability |

| Main and Subfactors | Reliability |

|---|---|

| Project Financing Schemes | 0.91 |

| Contract Type | 0.82 |

| Characteristics and Nature of Change Orders | 0.88 |

| Subfactor Attributes | Reliability |

|---|---|

| Cash Availability Attributes | 0.89 |

| Owner’s Payment Attributes | 0.87 |

| Contract Type Attributes | 0.81 |

| Value of Change Order Attributes | 0.85 |

| Timing of Change Order Attributes | 0.91 |

| Extension of Time Attributes | 0.86 |

| Work Stoppage Attributes | 0.75 |

| Type of Work Attributes | 0.79 |

| Utility | Score | Score Interpretation |

|---|---|---|

| Cash is Available | 1 | High cash availability positively impacts cash flow, allowing easy financial management and investment in new projects. |

| % Cash Available | 2 | The impact depends on the total cash pool; higher percentages are generally positive but less beneficial if the total is small. |

| Bank Loans | 3 | Bank loans are a common business practice but imply future cash outflows for repayments, potentially affecting cash flow. |

| % Bank Loans | 4 | High reliance on bank loans indicates potential cash flow stress and adds interest costs, negatively impacting cash flow. |

| Loan Limit Achieved | 5 | Reaching the loan limit suggests a critical cash flow situation, severely limiting financial flexibility and response capability. |

| Payment Status | Score | Interpretation of Impact on Contractor’s Cash Flow |

|---|---|---|

| No Delays | 1 | Minimal impact with on-time payments, ensuring steady cash flow. |

| Minor Delays | 2 | Low impact due to slight delays within permissible FIDIC limits. |

| Moderate Delays | 3 | Moderate impact, necessitating short-term financial adjustments. |

| Significant Delays | 4 | High impact with considerable delays, causing substantial strain. |

| Extreme Delays | 5 | Critical impact with severe delays, leading to legal disputes and financial distress. |

| Contract Type | Score | Impact Interpretation on Contractors’ Cash Flow |

|---|---|---|

| Cost Plus a Fixed Fee | 1 | Offers financial stability by covering all costs plus a fixed fee, minimizing unexpected financial risks. |

| Unit Price | 2 | Provides flexibility and incentives for cost efficiency but carries some risk with inaccurate cost estimations. |

| Target Price Plus a Fee | 2 | Incentivizes meeting or under-running target costs, with financial risks if targets are not met. |

| Lump Sum | 3 | Ensures payment certainty but includes the risk of bearing cost overruns within certain limits. |

| Guaranteed Maximum Price | 3 | Limits cost exposure, but the contractor bears the risk of overruns up to the maximum price. |

| Cost Plus Percentage of Cost | 4 | Covers all costs but may lead to inefficiencies and lower profit margins due to a lack of strong cost-control incentives. |

| (Hypothetical High-Risk Contract) | 5 | Represents a high-risk scenario where the contractor bears major unforeseen costs or substantial penalties. |

| Change Order Value | Score | Interpretation Impact on Contractors’ Cash Flow |

|---|---|---|

| >0% to ≤5% | 1 | Minimal impact, likely manageable within the initial budget as per Clause 13.1. |

| >5% to ≤10% | 2 | Moderate impact, with transparency and negotiation options as outlined in Clauses 13.3 and 13.4. |

| >10% to ≤15% | 3 | Noticeable impact, involving negotiation and potential delays, as per Clauses 52.3 and 14.1. |

| >15% to ≤20% | 4 | Substantial disruption, with complex compensation claims and potential for contract termination, as per Clauses 14.2 and 20.1. |

| >20% | 5 | Severely impactful, indicating drastic changes that may require contract renegotiation or legal recourse. |

| Change Order Timing | Score | Detailed Impact Interpretation |

|---|---|---|

| Before construction (Completion <0%) | 1 | Minimal Impact: Changes can be integrated with minimal adjustments to planning and budgeting, resulting in negligible financial disruption. |

| Completion between 0% and 25% | 2 | Low Impact: Early-stage changes generally require minor modifications to the project plan and budget, causing low financial strain. |

| Completion between 25% and 50% | 3 | Moderate Impact: Mid-project changes necessitate notable adjustments in resource allocation and may lead to moderate financial and scheduling challenges. |

| Completion between 50% and 75% | 4 | High Impact: Changes in this advanced stage can cause significant project disruptions, leading to considerable cost overruns and potential delays, heavily impacting cash flow. |

| Completion between 75% and 100% | 5 | Maximum Impact: Late-stage changes typically result in substantial disruptions, severe cost overruns, and extensive delays, severely affecting the contractor’s cash flow and possibly the project’s viability. |

| Time Extension | Score | Interpretation of Impact on Contractor’s Cash Flow |

| Extremely Sufficient | 1 | Least Impact: Minimal or no negative impact on cash flow, efficient resource management, and potential cost savings. |

| Sufficient | 2 | Low Impact: Adequate additional time for comfortable resource adjustment and manageable impacts on financial health. |

| Moderately Sufficient | 3 | Moderate Impact: Some relief with a noticeable impact through the partial offset of financial challenges. |

| Not Sufficient | 4 | High Impact: Inadequate extra time for significant mitigation, leading to considerable financial strain. |

| Critically Insufficient | 5 | Greatest Impact: Severely insufficient time extensions, causing substantial financial difficulties and potentially jeopardizing project viability. |

| Action | Score | Interpretation of Impact on Contractor’s Cash Flow |

|---|---|---|

| Addition | ||

| 1 | Full coverage by budget or client funds, with no financial strain. | |

| 2 | Slight increase in scope, with minimal financial strain. | |

| 3 | Noticeable extension in scope, with moderate budget adjustments and cash flow challenges. | |

| 4 | Significant scope extension, with major budget overruns and cash flow issues. | |

| 5 | Drastic scope change, with severe budget and cash flow crises. | |

| Omission | ||

| 1 | No financial loss, with a possible reduction in project costs without affecting profitability. | |

| 2 | Minor reduction in project scope, with a slightly positive or neutral effect on cash flow. | |

| 3 | Moderate reduction in scope, impacting profitability but not critically. | |

| 4 | Large-scale scope reduction, negatively impacting profitability and cash flow. | |

| 5 | Substantial scope reduction, severely affecting financial viability. | |

| Rework | ||

| 1 | Minor rework with negligible cost implications, with no disruption to timeline. | |

| 2 | Small amount of extra work, slightly impacting the budget and schedule. | |

| 3 | Significant rework, with additional time and resources needed, affecting schedule and budget. | |

| 4 | Extensive rework leading to major delays and cost overruns, significantly affecting financial health. | |

| 5 | Critical rework necessitating extensive additional work, causing major project delays and budget crises. |

| Stoppage Level | Score | Impact on the Contractor’s Cash Flow |

|---|---|---|

| No Stoppage | 1 | Minimal impact; cash flow remains stable due to uninterrupted progress. |

| Minor Stoppage | 2 | Slight disruption but generally manageable within the project’s financial structure. |

| Moderate Stoppage | 3 | Noticeable impact, necessitating financial adjustments and careful project management. |

| Significant Stoppage | 4 | Major disruptions leading to substantial financial strain and requiring strategic handling. |

| Severe Stoppage | 5 | Critical impact, potentially leading to serious financial challenges and project instability. |

| COII Numerical Value | COII Linguistic | Interpretations |

|---|---|---|

| ≥1 COII <2 | Minor Impact | The change order will have a positive or no impact on the project’s cash flow. |

| ≥2 COII <3 | Moderate Impact | The change order might negatively affect the project’s cash flow. However, before claiming, an impact analysis should be performed. |

| ≥3 COII <4 | Significant Impact | The change order will significantly affect the project’s cash flow. However, its impact should be analyzed. |

| ≥4 COII ≤5 | Severe Impact | The change order would severely affect the project’s cash flow. However, it needs to be determined through a thorough impact analysis. |

| Index | <2.5 | 2.5–3.49 | 3.5–5 |

|---|---|---|---|

| Classification | Weak | Moderate | High |

| Level of Agreement | Strongly Disagree | Disagree | Moderately Agree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| Rating Scale | 1 | 2 | 3 | 4 | 5 |

| No. | Questions | Strongly Disagree 1 | Disagree 2 | Moderately Agree 3 | Agree 4 | Strongly Agree 5 | Mean | Percentage % | Classification |

|---|---|---|---|---|---|---|---|---|---|

| 1 | The developed model and the impact analysis are applicable in construction projects. | 0 | 0 | 4 | 9 | 7 | 4.15 | 8.3 | High |

| 2 | The developed model and the impact analysis are easy to use and valid to be used in construction projects. | 0 | 0 | 3 | 12 | 5 | 4.1 | 82 | High |

| 3 | The developed model and the impact analysis are considered as a powerful controlling tool. | 0 | 0 | 3 | 6 | 11 | 4.4 | 88 | High |

| 4 | The developed model and the impact analysis are considered as a proactive forecasting tool. | 0 | 0 | 4 | 7 | 9 | 4.25 | 85 | High |

| 5 | The developed model and the impact analysis could be considered and applied as a base to determine the change orders impact on contractor’s cash flow in construction projects. | 0 | 0 | 3 | 4 | 13 | 4.5 | 90 | High |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qasem, A.M.J. A Systematic Multi-Criteria Quantitative Model for Evaluating the Change Order Impact on Contractors’ Cash Flow. Buildings 2025, 15, 1246. https://doi.org/10.3390/buildings15081246

Qasem AMJ. A Systematic Multi-Criteria Quantitative Model for Evaluating the Change Order Impact on Contractors’ Cash Flow. Buildings. 2025; 15(8):1246. https://doi.org/10.3390/buildings15081246

Chicago/Turabian StyleQasem, Altayeb Mohd Jamil. 2025. "A Systematic Multi-Criteria Quantitative Model for Evaluating the Change Order Impact on Contractors’ Cash Flow" Buildings 15, no. 8: 1246. https://doi.org/10.3390/buildings15081246

APA StyleQasem, A. M. J. (2025). A Systematic Multi-Criteria Quantitative Model for Evaluating the Change Order Impact on Contractors’ Cash Flow. Buildings, 15(8), 1246. https://doi.org/10.3390/buildings15081246