Exploring How Corporate Maturity Moderates the Value Relevance of ESG Disclosures in Sustainable Reporting: Evidence from Bangladesh’s Developing Market

Abstract

1. Introduction

2. Literature Review

2.1. ESG Disclosures and Firm Value in Emerging Markets

2.2. Corporate Maturity and ESG Disclosure Behavior

2.3. Theoretical Foundations

- Signaling Theory [23]: ESG disclosures act as observable signals that help bridge information asymmetry, particularly for younger firms with limited performance histories. This aligns with [31], who argue that firms in early lifecycle stages must actively signal credibility through non-financial disclosures to attract external resources. This signaling function becomes particularly pronounced in the presence of ESG-focused investors who are more responsive to non-financial performance metrics—a finding echoed by [32], who demonstrate that ESG-oriented investors strengthen the relationship between ESG disclosure and firm performance.

- Corporate Lifecycle Theory [25]: ESG disclosure intensity and purpose vary across firm lifecycle stages.

2.4. Synthesis and Hypothesis Development

3. Research Methodology

3.1. Research Design and Approach

3.2. Sample Selection and Data Sources

3.3. Development of the ESG Disclosure Index

- Environmental: e.g., emissions, climate strategy, water and waste management.

- Social: e.g., labor rights, DEI, community engagement, product responsibility.

- Governance: e.g., board composition, risk management, anti-corruption policies.

3.4. Variables and Measures

3.4.1. Dependent Variable

3.4.2. Independent Variable

3.4.3. Moderating Variable: Corporate Maturity

- Firm Age: Measured as years since incorporation. This variable was used both as a continuous measure and as a categorical moderator. For initial regression models, firms were classified as “young” or “mature” based on a median split (median = 28 years). Firms below the median were labeled “young,” and those at or above were labeled “mature”.However, the limitations of using a median split, which may reduce explanatory power and introduce arbitrary thresholds, are acknowledged. To address this, supplemental analyses were conducted using tercile splits and alternative age cutoffs to ensure robustness of the findings. Furthermore, firm age and lifecycle stage were modeled independently in interaction terms to capture potentially distinct moderating effects.

- Firm Lifecycle Stage: Classified as growth, maturity, or decline using [25] cash flow pattern-based model, considering operating, investing, and financing cash flow signs. This classification was used to verify the consistency of findings when firm age and lifecycle are applied as separate or alternative proxies for corporate maturity.

3.4.4. Control Variables

3.5. Model Specification

- = Firm value (Tobin’s Q or MTB) for firm i at time t

- = ESG disclosure score

- = Corporate maturity (firm age or lifecycle dummy)

- = Interaction term for moderation analysis

- = Control variables

- = Industry fixed effects

- = Year fixed effects

- = Error term

3.6. Estimation Techniques

4. Empirical Findings

4.1. Correlation Analysis

4.2. Panel Regression Results

4.3. Robustness Checks

- Supplementary Regressions: Tercile-based age groups and alternate cutoffs yielded consistent results in terms of sign and significance, confirming that the moderation effect of corporate maturity is not driven by arbitrary dichotomization. Detailed outputs of these robustness tests are presented in Appendix C, which confirms the consistency of the moderation effect across specification models.

- Alternative ESG Metrics: A weighted ESG disclosure index was applied; results remained consistent in both sign and significance.

- Endogeneity Controls: Two-stage least squares 2SLS regression using lagged ESG scores as instruments confirmed the causal effect of ESG disclosures on firm value.

- Propensity Score Matching (PSM): Firms with high ESG disclosure were matched with low-disclosure firms. The positive effect of ESG–value association persisted in the matched sample.

- Subsample Analysis: Post-2020 observations (following BSEC’s ESG guidance) revealed a stronger ESG–value relationship, underscoring the influence of evolving regulatory frameworks.

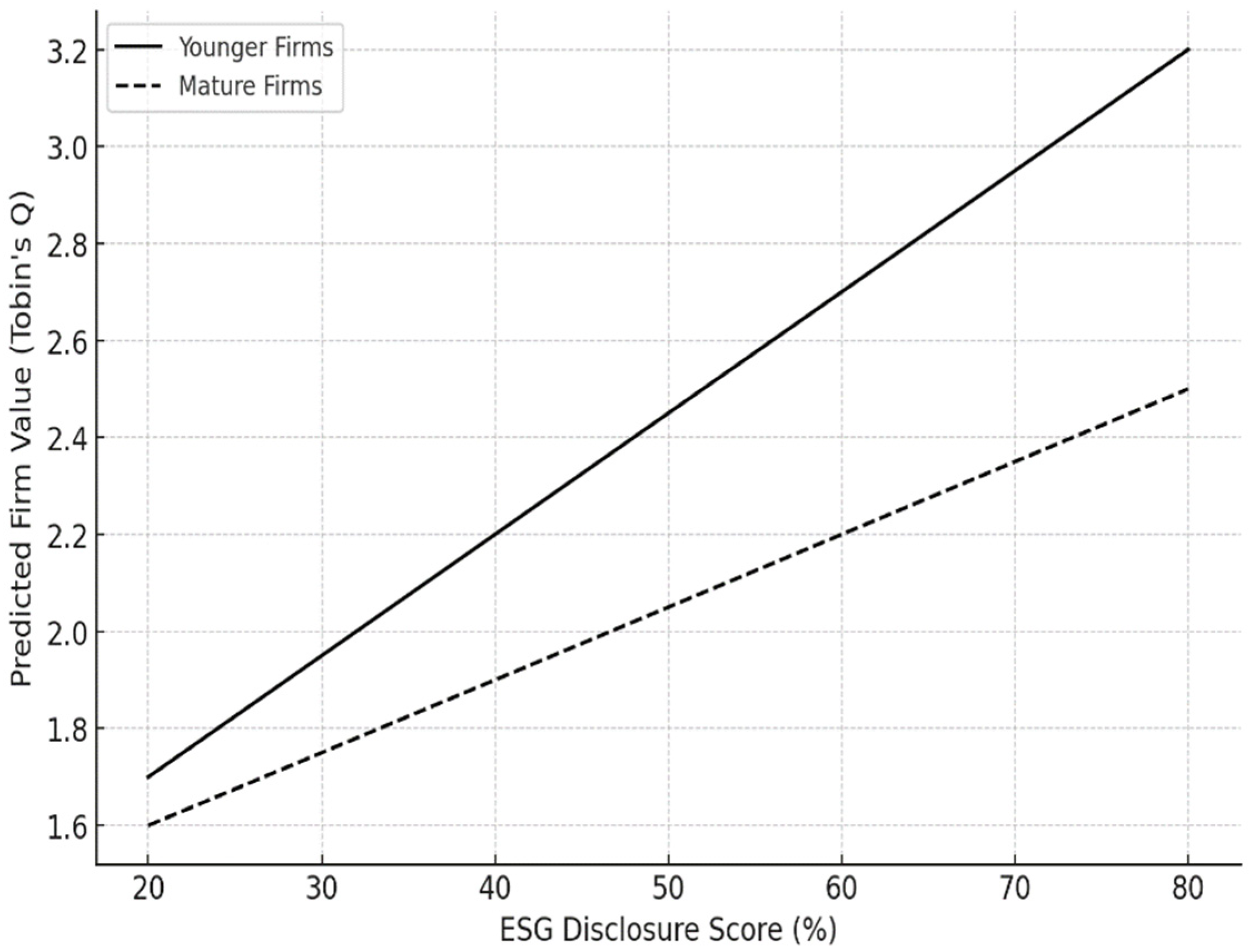

4.4. Discussion of Findings

5. Conclusion and Implications

5.1. Summary of Findings

5.2. Theoretical Contributions

- It introduces corporate maturity as a novel moderating variable in the ESG–firm value relationship, offering a lifecycle-based lens to assess disclosure outcomes.

- By integrating signaling, legitimacy, and lifecycle theories, the study presents a context-sensitive framework for interpreting ESG dynamics in emerging markets. While these theories are not new, their combined application to the ESG–value relationship in the context of corporate maturity represents a novel analytical contribution. By integrating lifecycle awareness into ESG analysis, this framing captures both the multidimensional nature of ESG determinants and the shifting expectations placed on firms at different stages of development.

- It fills a regional research gap by providing context-specific evidence from Bangladesh, an under-researched developing economy experiencing rapid ESG evolution.

5.3. Practical Implications

5.4. Limitations and Directions for Future Research

- ESG disclosure scores were based on publicly available documents, which may not fully capture informal or internal sustainability efforts.

- Although this study employed 2SLS and Propensity Score Matching to address endogeneity concerns, both techniques entail methodological limitations. Specifically, the use of lagged ESG scores as instruments in 2SLS may introduce serial correlation, reducing instrument validity. Similarly, PSM’s binary grouping of ESG scores can result in a loss of data richness and weaken explanatory accuracy. Future research should apply advanced estimation techniques, such as system GMM or panel smooth transition regression, to better capture dynamic relationships and non-linear moderation effects in ESG–value studies.

- The study is limited to Bangladesh, which may affect generalizability. Comparative studies across other developing economies would provide broader insights.

- While this study included standard financial controls, it did not account for governance-specific variables such as board size or independence, which could influence ESG disclosure quality and firm valuation. Future studies should consider including such variables to capture board-level strategic influences.

5.5. Concluding Remarks

5.6. Recommendations

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. ESG Disclosure Index (Used in the Study)

- Environmental Disclosures

- Environmental Policy and Strategy

- Clear policy statements on environmental protection and sustainability.

- Alignment of environmental strategy with national and international standards.

- Climate Change and Energy Use

- 3.

- Carbon emissions (Scope 1, 2, and 3).

- 4.

- Measures for energy efficiency and renewable energy use.

- 5.

- Impact of climate change on business operations.

- Waste and Water Management

- 6.

- Waste reduction, recycling, and disposal strategies.

- 7.

- Water usage and conservation initiatives.

- Biodiversity and Land Use

- 8.

- Efforts to preserve biodiversity in operational areas.

- 9.

- Sustainable land use and reforestation programs.

- Environmental Compliance

- 10.

- Compliance with environmental regulations.

- 11.

- Information on penalties, fines, or litigations related to environmental breaches.

- Social disclosures

- Human Rights and Labor Practices

- 12.

- Policies on human rights and labor rights adherence.

- 13.

- Measures to prevent forced and child labor in operations and supply chain.

- Diversity, Equity, and Inclusion (DEI)

- 14.

- Workforce diversity metrics (gender, age, ethnicity).

- 15.

- Inclusion programs for underrepresented groups.

- Employee Health, Safety, and Well-being

- 16.

- Occupational health and safety initiatives.

- 17.

- Mental health and wellness programs for employees.

- Community Engagement and Development

- 18.

- Corporate contributions to community development (education, healthcare).

- 19.

- Partnerships with local communities.

- Customer Relations and Product Responsibility

- 20.

- Product quality, safety, and innovation disclosures.

- 21.

- Customer satisfaction and feedback mechanisms.

- Governance Disclosures

- Board Structure and Independence

- 22.

- Composition of the board, including independent directors.

- 23.

- Diversity in board composition.

- Executive and Board Compensation

- 24.

- Remuneration policies for board members and executives.

- 25.

- Disclosure of compensation structures and bonuses.

- Shareholder Rights and Transparency

- 26.

- Voting rights and shareholder engagement practices.

- 27.

- Mechanisms for transparency in shareholder communication.

- Audit Committee and Risk Management

- 28.

- Role of audit committee in overseeing ESG matters.

- 29.

- Disclosure of risk management strategies related to ESG.

- Ethical Conduct and Anti-corruption

- 30.

- Corporate code of conduct.

- 31.

- Anti-bribery and anti-corruption policies and practices.

- Data Privacy and Cybersecurity

- 32.

- Measures taken to ensure data protection and privacy.

- 33.

- Cybersecurity initiatives and response plans.

Appendix B. Weighted ESG Disclosure Index

- Overview

- Weighting Methodology

- Materiality by sector (e.g., environmental issues in manufacturing vs. governance in services)

- Stakeholder relevance (e.g., importance to investors, regulators, consumers)

- Disclosure frequency and impact in the pilot assessment (based on 10 firms)

- Alignment with international ESG reporting frameworks (GRI, SASB, TCFD)

{kind=link}

{kind=link}

| ESG Category | Number of Indicators | Category Weight (%) | Notes |

|---|---|---|---|

| Environmental | 10 | 35% | Emphasis on emissions, energy, water in high-impact sectors |

| Social | 12 | 30% | Focus on DEI, labor, community engagement |

| Governance | 11 | 35% | Includes board structure, risk management, ethics |

- Example Weighted Score Calculation

- Discloses 8 of 10 Environmental indicators (Environmental weight = 40%)

- Discloses 6 of 12 Social indicators (Social weight = 25%)

- Discloses 9 of 11 Governance indicators (Governance weight = 35%)

- Validation and Robustness

- Feedback from two academic ESG experts and one practitioner

- Comparison with unweighted results

- Sensitivity analyses using alternate weight configurations

Appendix C. Robustness Tests Using Alternative Corporate Maturity Specifications

| Model Specification | ESG Coefficient (β) | ESG × Maturity Coefficient (β) | Adj. R2 | Notes |

|---|---|---|---|---|

| Model 1 (Median Split, Baseline) | 0.024 ** | −0.000 | 0.209 | Maturity defined as firm age ≥ 28 |

| Model 2 (Tercile Split: Young vs. Old) | 0.025 ** | −0.002 * | 0.211 | Lowest third = “Young”; highest third = “Old”; middle excluded |

| Model 3 (Cutoff at 25 years) | 0.023 ** | −0.001 * | 0.208 | Based on industry lifecycle norms |

| Model 4 (Age as Continuous Interaction) | 0.022 ** | −0.0001 * | 0.210 | ESG × Age (continuous) used instead of dummy |

References

- KPMG. The Time Has Come: KPMG Survey of Sustainability Reporting. SustainCase—Sustainability Magazine. 2020. Available online: https://sustaincase.com/the-time-has-come-kpmg-survey-of-sustainability-reporting-2020/ (accessed on 23 June 2025).

- UNCTAD. Guidance on Core Indicators for Entity Reporting on Contribution Towards Implementation of the Sustainable Development Goals; United Nations Conference on Trade and Development: Geneva, Switzerland, 2020; Available online: https://unctad.org/publication/guidance-core-indicators-entity-reporting-contribution-towards-implementation (accessed on 23 June 2025).

- Friede, G.; Busch, T.; Bassen, A. ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.-Y.; Koh, L. The Impact of Environmental, Social, and Governance Disclosure on Firm Value: The Role of CEO Power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef]

- Ed-Dafali, S.; Adardour, Z.; Derj, A.; Bami, A.; Hussainey, K. A PRISMA-Based Systematic Review on Economic, Social, and Governance Practices: Insights and Research Agenda. Bus Strategy Environ. 2025, 34, 1896–1916. [Google Scholar] [CrossRef]

- Fatemi, A.; Glaum, M.; Kaiser, S. ESG Performance and Firm Value: The Moderating Role of Disclosure. Glob. Financ. J. 2018, 38, 45–64. [Google Scholar] [CrossRef]

- Răpan, C.M.; Banța, V.-C.; Manea, A.; Aridah, M.W. Value Relevance of ESG Scores: Evidence from European Stock Exchange Markets. Oblìk ì Fìnansi 2022, 2, 68–75. [Google Scholar] [CrossRef]

- Cort, T.; Esty, D. ESG Standards: Looming Challenges and Pathways Forward. Organ. Environ. 2020, 33, 491–510. [Google Scholar] [CrossRef]

- Chung, R.; Bayne, L.; Birt, J. The Impact of Environmental, Social and Governance (ESG) Disclosure on Firm Financial Performance: Evidence from Hong Kong. Asian Rev. Account. 2024, 32, 136–165. [Google Scholar] [CrossRef]

- Adardour, Z.; Ed-Dafali, S.; Mohiuddin, M.; El Mortagi, O.; Sbai, H.; Bouzahir, B. Exploring the Drivers of Environmental, Social, and Governance (ESG) Disclosure in an Emerging Market Context Using a Mixed Methods Approach. Future Bus. J. 2025, 11, 107. [Google Scholar] [CrossRef]

- Sultana, S.; Zulkifli, N.; Zainal, D. Environmental, Social and Governance (ESG) and Investment Decision in Bangladesh. Sustainability 2018, 10, 1831. [Google Scholar] [CrossRef]

- Setiawati, A.; Hidayat, T. The Influence of Environmental, Social, Governance (ESG) Disclosures on Financial Performance. J. Econ. Manag. Bank. 2023, 9, 225–240. [Google Scholar] [CrossRef]

- Angir, P.; Weli, W. The Influence of Environmental, Social, and Governance (ESG) Disclosure on Firm Value: An Asymmetric Information Perspective in Indonesian Listed Companies. Binus Bus. Rev. 2024, 15, 29–40. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.; Miralles-Quirós, J.; Valente Gonçalves, L. The Value Relevance of Environmental, Social, and Governance Performance: The Brazilian Case. Sustainability 2018, 10, 574. [Google Scholar] [CrossRef]

- Wahyuni, P.D.; Utami, S.W.; Tanjung, J. The Impact of ESG Disclosure on Firm Value Relevance: Moderating Effect of Competitive Advantage. Eur. J. Account. Audit. Financ. Res. 2024, 12, 19–33. [Google Scholar] [CrossRef]

- Shaikh, I. Environmental, Social, and Governance (ESG) Practice and Firm Performance: An International Evidence. J. Bus. Econ. Manag. 2022, 23, 218–237. [Google Scholar] [CrossRef]

- Faccia, A.; Manni, F.; Capitanio, F. Mandatory ESG Reporting and XBRL Taxonomies Combination: ESG Ratings and Income Statement, a Sustainable Value-Added Disclosure. Sustainability 2021, 13, 8876. [Google Scholar] [CrossRef]

- Broniewicz, E.; Jastrzębska, E.; Lulewicz-Sas, A. Environmental Disclosures According to ESRS in ESG Reporting of Selected Banks in Poland. Econ. Environ. 2024, 88, 719. [Google Scholar] [CrossRef]

- Dziadkowiec, A.; Daszynska-Zygadlo, K. Disclosures of ESG Misconducts and Market Valuations: Evidence from DAX Companies. Eng. Econ. 2021, 32, 95–103. [Google Scholar] [CrossRef]

- Zuraida, Z.; Houqe, N.; van Zijl, T. Value Relevance of Environmental, Social and Governance Disclosure. In Handbook of Finance and Sustainability; Edward Elgar: Cheltenham, UK, 2016. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. The Economic Relevance of Environmental Disclosure and Its Impact on Corporate Legitimacy: An Empirical Investigation. Bus Strategy Environ. 2015, 24, 431–450. [Google Scholar] [CrossRef]

- Spence, M. Job Market Signaling. Q. J. Econ. 1973, 87, 355. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2011, 37, 39–67. [Google Scholar] [CrossRef]

- Dickinson, V. Cash Flow Patterns as a Proxy for Firm Life Cycle. Account. Rev. 2011, 86, 1969–1994. [Google Scholar] [CrossRef]

- Hasan, R.; Miah, M.D.; Hassan, M.K. The Nexus between Environmental and Financial Performance: Evidence from Gulf Cooperative Council Banks. Bus Strategy Environ. 2022, 31, 2882–2907. [Google Scholar] [CrossRef]

- Shin, E. How Would Mandatory ESG Disclosure Impact Small and Mid-Sized Companies?: Analysis on Relationship between ESG Performance and Financials by Corporate Size. SSRN Electron. J. 2021. Available online: https://www.researchgate.net/publication/356380633_How_would_mandatory_ESG_disclosure_impact_small_and_mid-sized_companies_Analysis_on_relationship_between_ESG_performance_and_financials_by_corporate_size_ESG_uimu_gongsi_jungsojung-gyeon_gieob-ege_wig (accessed on 23 June 2025).

- Abdi, Y.; Li, X.; Càmara-Turull, X. Exploring the Impact of Sustainability (ESG) Disclosure on Firm Value and Financial Performance (FP) in Airline Industry: The Moderating Role of Size and Age. Environ. Dev. Sustain. 2022, 24, 5052–5079. [Google Scholar] [CrossRef]

- Wan Ismail, W.A.; Mohd Saad, S.; Lode, N.A.; Kustiningsih, N. Corporate Sustainability Reporting and Firm’s Financial Performance in Emerging Markets. Int. J. Acad. Res. Bus. Soc. Sci. 2022, 12, 396–407. [Google Scholar] [CrossRef]

- Balogh, I.; Srivastava, M.; Tyll, L. Towards Comprehensive Corporate Sustainability Reporting: An Empirical Study of Factors Influencing ESG Disclosures of Large Czech Companies. Soc. Bus. Rev. 2022, 17, 541–573. [Google Scholar] [CrossRef]

- Diebecker, J.; Rose, C.; Sommer, F. Corporate Sustainability Performance Over the Firm Life Cycle: Levels, Determinants, and the Impact on Accounting Performance. SSRN Electron. J. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3084601 (accessed on 23 June 2025). [CrossRef]

- Chen, Z.; Xie, G. ESG Disclosure and Financial Performance: Moderating Role of ESG Investors. Int. Rev. Financ. Anal. 2022, 83, 102291. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571. [Google Scholar] [CrossRef]

- Deegan, C. Introduction: The Legitimising Effect of Social and Environmental Disclosures—A Theoretical Foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Kumar, P.; Firoz, M. Does Accounting-Based Financial Performance Value Environmental, Social and Governance (ESG) Disclosures? A Detailed Note on a Corporate Sustainability Perspective. Australas. Bus. Account. Financ. J. 2022, 16, 41–72. [Google Scholar] [CrossRef]

- GRI. GRI Standards: The Global Standards for Sustainability Impacts; GRI: Amsterdam, The Netherlands, 2021. [Google Scholar]

- SASB. SASB Standards Overview; SASB: San Francisco, CA, USA, 2023. [Google Scholar]

- TCFD. Task Force on Climate-Related Financial Disclosures; TCFD: Basel, Switzerland, 2023. [Google Scholar]

- UN SDGs. The Sustainable Development Goals Report; UN SDGs: New York, NY, USA, 2024. [Google Scholar]

- Ohlson, J.A. Earnings, Book Values, and Dividends in Equity Valuation. Contemp. Account. Res. 1995, 11, 661–687. [Google Scholar] [CrossRef]

- Murata, R.; Hamori, S. ESG Disclosures and Stock Price Crash Risk. J. Risk Financ. Manag. 2021, 14, 70. [Google Scholar] [CrossRef]

- Shmelev, S.E.; Gilardi, E. Sustainable Business as a Force for Good in the Context of Climate Change: An Econometric Modelling Approach. Sustainability 2025, 17, 1530. [Google Scholar] [CrossRef]

- Polma, P.; Winston, A. Net Positive: How Courageous Companies Thrive by Giving More Than They Take by Paul Polman|Goodreads; Harvard Business Review Press: New York, NY, USA, 2021. [Google Scholar]

- Elkington, J. Green Swans: The Coming Boom in Regenerative Capitalism; Fast Company Press: New York, NY, USA, 2020; ISBN 1732439125. [Google Scholar]

| Variable | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| ESG Disclosure Score (%) | 46.47 | 10.13 | 16.52 | 75.84 |

| Market-to-Book Ratio (MTB) | 1.87 | 0.45 | 0.54 | 3.37 |

| Tobin’s Q | 1.84 | 0.38 | 0.48 | 3.09 |

| Firm Age (Years) | 28.28 | 9.91 | 5.00 | 51.00 |

| Lifecycle Stage | Growth | Maturity | Decline | |

| Distribution (%) | 8 | 52 | 40 | |

| Variable | ESG Disclosure | MTB | Tobin’s Q | Firm Age |

|---|---|---|---|---|

| ESG Disclosure | 1.00 | 0.46 ** | 0.36 ** | −0.15 * |

| Firm Value (MTB) | 0.46 ** | 1.00 | 0.10 ** | −0.05 |

| Tobin’s Q | 0.36 ** | 0.10 ** | 1.00 | −0.03 |

| Firm Age | −0.15 * | −0.15 | −0.03 | 1.00 |

| Model | Adj. R2 | ESG β | ESG × Age β |

|---|---|---|---|

| Model 1 | 0.005 | — | — |

| Model 2 | 0.210 | 0.020 ** | — |

| Model 3 | 0.209 | 0.024 ** | −0.000 |

| Model 4 | 0.207 | 0.024 ** | −0.000 |

| Model Group | ESG β (p-Value) | ESG × Age β (p-Value) | Adj. R2 |

|---|---|---|---|

| High Sustainability Exposure | 0.026 (p < 0.01) | −0.003 (p < 0.05) | 0.238 |

| Low Sustainability Exposure | 0.022 (p < 0.05) | −0.001 (p > 0.10) | 0.205 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Islam, S.M.M. Exploring How Corporate Maturity Moderates the Value Relevance of ESG Disclosures in Sustainable Reporting: Evidence from Bangladesh’s Developing Market. Sustainability 2025, 17, 5936. https://doi.org/10.3390/su17135936

Islam SMM. Exploring How Corporate Maturity Moderates the Value Relevance of ESG Disclosures in Sustainable Reporting: Evidence from Bangladesh’s Developing Market. Sustainability. 2025; 17(13):5936. https://doi.org/10.3390/su17135936

Chicago/Turabian StyleIslam, Saleh Mohammed Mashehdul. 2025. "Exploring How Corporate Maturity Moderates the Value Relevance of ESG Disclosures in Sustainable Reporting: Evidence from Bangladesh’s Developing Market" Sustainability 17, no. 13: 5936. https://doi.org/10.3390/su17135936

APA StyleIslam, S. M. M. (2025). Exploring How Corporate Maturity Moderates the Value Relevance of ESG Disclosures in Sustainable Reporting: Evidence from Bangladesh’s Developing Market. Sustainability, 17(13), 5936. https://doi.org/10.3390/su17135936