1. Introduction

District heating systems often rely on fossil fuels for heat generation, resulting in significant greenhouse gas emissions [

1]. Decarbonizing district heating systems is crucial to mitigating climate change and achieving sustainable energy goals [

2].

Energy-intensive industries (such as the cement, steel, pulp and paper, or chemical industries) use large amounts of energy in their production processes and inevitably generate waste heat. Some of this waste heat can be avoided by internal recovery and used, for example, to preheat a secondary process. Once these internal heat recovery options have been exhausted, there is an opportunity to reuse the often high-quality waste heat beyond the system boundaries by feeding it into district heating networks [

3,

4].

By utilizing climate-neutral heat sources, such as waste heat from energy-intensive industries, district heating systems can significantly reduce their greenhouse gas emissions, reliance on fossil fuel-based heat sources, and improve system resilience and reliability [

4,

5]. Furthermore, higher energy prices make the recovery of industrial excess heat in district heating systems more favorable to other alternative energy sources, such as biomass, in the long term [

4]. On the industrial side, the efficiency of the industrial process can be increased through operational optimization and process adaptations when feeding excess heat into district heating networks. On the other side, the heat network operator can achieve an increase in capacity, leading to additional profits, and significantly reduce heat losses [

6].

Siddique et al. [

7] show that a decarbonized district heating supply will rely heavily on industrial waste heat, in addition to bioenergy and electrification. In some cases, industrial waste heat can contribute to a high proportion of a city’s heat demand [

8].

Feeding industrial waste heat into the network of a district heating operator requires the cooperation of both parties. Such an energy cooperation has to overcome manifold barriers associated with different disciplines. While the specific technical aspects (profiles, storage systems, etc.) and economic feasibility (surplus of avoided energy input compared to investment) are prerequisites for final implementation, a large number of interdisciplinary hurdles have to be overcome beforehand [

9,

10,

11,

12]. These hurdles are often due to a lack of information and communication [

13,

14]. In addition, compared to long-term investments made by the energy sector or public institutions [

15,

16], investments made by industrial companies are often subject to short payback periods and an aversion to guarantees or responsibilities (focus on core business). At the same time, the payback periods may be extended if the waste heat is only used in winter [

17]. Risks are another barrier that needs to be considered in the design of business models and contracts [

17,

18].

This paper builds on the previous work of Moser and Lassacher [

16], who conducted an internet and literature research and showed that there are already a large number of implementations of company-external use of industrial waste heat in district heating networks. They identified 45 implemented cases in Austria, which have a capacity of 600 MW and supply 1.75 TWh/a to external users. Out of the 45 cases, 42 provide excess heat for district heating networks, while three supply independent external companies. In approximately half of the cases, the heat comes from heat recovery, while in the other half, it comes from industrial combustion (e.g., production residues). Moser and Lassacher calculated that about 2% of the Austrian industrial end-use energy demand is reused in district heating networks, covering about 7% of the national annual district heating supply. They also showed that two-thirds of the projects were implemented after 2010.

Moser and Lassacher focused on summarizing all Austrian cases and aimed for a short technical description of these. Due to their approach, they were not able to investigate the non-technical aspects such as economics, organization, or social and legal aspects in detail. Thus, it remained unclear how the projects were initiated and how the stakeholders agreed on a common business model.

The aim of this paper is, therefore, to reinvestigate the existing Austrian practical examples and examine how these projects were initiated and implemented. The paper aims to show—and this is the innovative content and contribution to the body of knowledge—how the first contacts came about, how the implementation process proceeded (i.e., the steps that were taken until the agreement was reached), and what business model or contractual agreement was achieved at the end of the negotiation process. The basic characteristics of the individual processes will be generalized so that the development processes can be replicated, thus contributing to the implementation of further practical examples. The results should also provide policymakers with insights on how to standardize third-party facilitation.

A review of the related literature up to 2020 on the framework conditions, such as the general waste heat potential, as well as on the specific literature on the feeding of industrial waste heat into district heating networks, can be found in Moser and Lassacher [

16]. An important paper published since then is that of Fritz et al. [

19]. They build upon the results of Moser and Lassacher [

16] and complement them with examples from Germany and France. As part of a parallel survey to the one conducted in this study, they also examine the business models and profitability, but their analysis focuses on projects that have not yet been implemented. Similar to Södergren and Palm [

20] and Moser and Rodin [

13], they highlight the role of public or institutional intermediaries.

In the methods section, this paper recaps and updates the database of Moser and Lassacher [

16], as well as the method and content of the conducted survey. All results of the survey are presented in the results section, followed by a final section that discusses and summarizes the findings.

2. Materials and Methods

The following section describes how a questionnaire based on the database of Moser and Lassacher [

16] was created, sent out, and how the responses were collected and analyzed.

2.1. List of Implementations

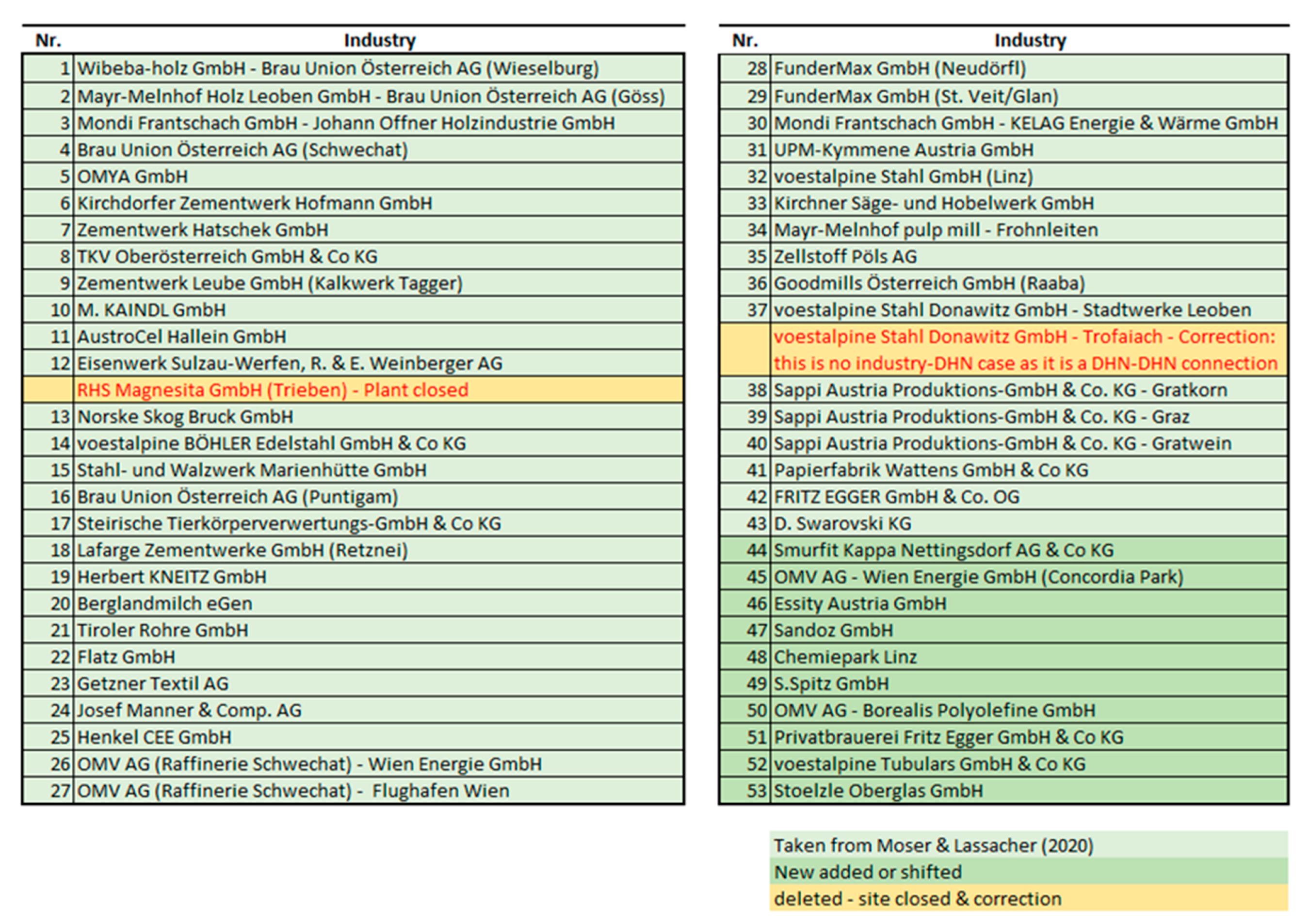

Moser and Lassacher [

16] carried out an extensive literature and internet search based on industries, regions, and types of use in order to compile a comprehensive list of existing inter-company waste heat utilization in Austria. The aim was to provide an overview of the projects implemented in Austria so far, derive previously unknown key data for energy statistics, and determine the amount of waste heat used externally and its share in certain energy balance categories. Furthermore, the study investigated whether the waste heat originated from industrial combustion or industrial heat recovery and whether district heating networks were the preferred destination for external use of industrial waste heat. Additionally, the hypothesis that only highly profitable projects were realized was examined but remained unanswered.

In total, 45 implementations were identified. It should be noted that only implementations involving cooperation between an industrial company and a heat customer were recognized. Other types of waste heat sources, such as power plants, waste incineration plants, sewage treatment plants, or server centers, were not included as their underlying processes and services are designed for longer periods and involve less long-term risk than industrial processes. Since risk and the associated short-term nature form a central barrier to cooperation between industry and district heating, only such projects were included by Moser and Lassacher [

16]. Consequently, waste incineration plants or wastewater treatment plants were excluded. Implementations were also excluded if the actors were not independent at the time of implementation, e.g., if they belonged to the same group or were a company that was later split up. (This led to the exclusion of, for example, the cooperation between OMV AG and Borealis Polyolefine GmbH in Schwechat, the joint supply infrastructure of the companies in the Chemiepark in Linz, Fritz Egger GmbH & Co OG and Privatbrauerei Egger GmbH & Co KG in Lower Austria, or S.Spitz GmbH in Attnang-Puchheim). After the publication of the paper, two additional existing implementations were discovered, and they have since been added to the list: Essity Austria GmbH and Bioenergie Ortmann GmbH in Pernitz [

21] and Sandoz GmbH in Kundl [

22]. Furthermore, the list incorrectly included one cooperation. (The cooperation between voestalpine Donawitz and Kelag in Trofaiach turned out to be a transfer of heat from Stadtwerke Leoben to Kelag; it is therefore not an organizational connection between the industry and the Kelag district heating network). Since the list was compiled in 2018, the RHI Magnesita plant in Trieben has been closed, so that the provision of waste heat has also ended [

23]. Furthermore, the list now also includes the above-mentioned cooperations that were excluded due to equal ownership, as their contractual and business agreements may be similar and therefore of interest. Additionally, the list now includes newly planned and already implemented projects, such as Smurfit Kappa Nettingsdorf AG & Co KG in Nettingsdorf [

24] and OMV AG around its location in Schwechat [

25].

The result is a list of 51 waste heat cooperations. This list was used as a basis for contact.

In order to provide a complete list of currently known implementations in

Figure 1, it is necessary to mention two more implementations that were newly identified or newly agreed upon after the list was completed and the questionnaire was sent out. One is the district heating feed-in of Stoelzle Oberglas GmbH into the district heating network of Energie Steiermark in Köflach. The heat recovery cooperation was already implemented in 2015 using exhaust gas heat exchangers to recover waste heat from the glass production furnaces. The homepage states that compensated 4300 tCO

2 were offset, but there is no conversion into supplied energy quantities [

26]. In addition, the future waste heat cooperation between voestalpine Tubulars GmbH & Co KG and the Bioenergie Group became known after the questionnaire was sent out. This cooperation involves waste heat from the production of steel tubes, which are formed at a temperature of 1300 °C, resulting in a waste heat capacity of around 4 MW. The heat will be delivered directly to the city through a 9 km long district heating pipeline. Construction work will start in 2022, and the plant is scheduled to be commissioned in 2023 [

27].

2.2. Questionnaire

The questionnaire is included in

Appendix A of this report. It is a semi-structured questionnaire, which was considered to be an optimal design with regard to the expected number of responses. Individual answers can be elaborated by the respondent and compared by the authors, while a stricter structuring is irrelevant as a high enough number for statistical significance is not expected.

The search for contact partners resulted in the identification of around 100 contacts. These contacts were mostly identified through a time-intensive search for each company, while in some cases the contact person was quickly identified through personal relations and/or previous collaboration with the authors. For budgetary reasons, it was decided to send the questionnaire only to the industrial waste heat providers. One exception is a brewery company that is both a customer and a supplier in various cases of cooperation and therefore answered questions about the disposal of waste heat. The questionnaire, in the form of a text-file, was sent to all companies in mid-December 2021. Participants had the option of returning the survey as an attachment via email or discussing the questionnaire via a telephone call or web conference (referred to as an “interview” in this paper). Both options were used equally. In the case of a telephone call or web conference, the survey was filled out by the authors. This allowed the authors to clarify information and ask detailed questions. The survey closed on 31 January 2022.

Respondents were assured that their participation would be anonymous and untraceable, with only the name of the company appearing in any publications as a participant in the survey. The survey results are not published in aggregated or anonymized form, as most questions are not answered numerically but contain detailed textual explanations. Conclusions about the actual company would therefore be possible even with anonymous answers. Respondents were assured that only the company name would appear in any publication as a participant in the survey. All other information will not be attributed to individual companies in any publications, and the dataset will not be made available externally.

Questionnaire responses were received from 16 companies, with 4 companies responding for more than one case. In total, questionnaires were received for 24 out of the 51 cooperations. The respondents included companies from various industries, including the food and beverage industry (in particular a large Austrian brewery), the pulp and paper industry, the cement industry, the steel industry, and the chemical and petrochemical industry. The responding companies are Brau Union AG, Mondi Frantschach GmbH, OMYA GmbH, Kirchdorfer Zementwerk Hofmann GmbH, Zementwerk Hatschek GmbH, Zementwerk Leube GmbH, Stahl- und Walzwerk Marienhütte GmbH, Lafarge Zementwerke GmbH, Josef Manner & Comp. AG, OMV AG, Zellstoff Pöls AG, voestalpine Stahl Donawitz GmbH, Sappi Austria Produktions-GmbH & Co. KG, Papierfabrik Wattens GmbH & Co KG, Smurfit Kappa Nettingsdorf AG & Co KG, and Essity Austria GmbH.

3. Results

Out of the 24 responses received, 3 of them pertain to an implementation between two industrial companies. These types of cooperation represent a special case, as they involve different risks, uncertainties, and strategies (cf. Moser and Lassacher [

16]). Therefore, they are not included in the evaluation performed in this paper. The following results are based on the remaining 21 responses.

Out of the 21 responses, 17 companies answered the question regarding the maximum capacity, while 20 answered the question regarding the typical annual quantity. Full-load hours were not queried but they were calculated as a case-specific multiplier of the maximum capacity to the annual quantity provided (

Table 1).

The average capacity of the waste/excess heat supply is 29 MW, excluding the upper and lower outliers, it is 20 MW. Four out of the 17 cases have a maximum capacity of 2 MW or less. Industrial waste heat recovery and external supply have no lower bound; the answers suggest that there is no minimum size for (economic) feasibility. Probably, with the capacity, the costs of recovery and integration also decrease. If the investment costs for heat recovery, (short-distance) pipelines, and feed-in facilities, as well as the running costs, are low enough, even low capacities and low quantities justify feed-in. It is also possible that smaller district heating networks cooperate with smaller waste heat sources. Since there is no definition for the size of district heating networks (in fact, one supplier and one customer are sufficient), the recovered heat source can be of any size (e.g., from a carpentry or supermarket). Moreover, perhaps small capacities are easier to integrate into district heating networks. Although not statistically significant, it can be noted that the five smallest implementations by MW have, on average, about the same full load hours as the average; so, obviously, small capacity is case-specific, and it cannot be generalized that small capacities are easier to integrate.

The cases deliver an average of 78.8 GWh/a, without the upper and lower outliers, it is 51 GWh/a. This results in an average of about 3160 full load hours. Four out of the 17 implementations have more than 4500 full load hours, while two out of the 17 have less than 2000 full load hours. As expected, the use of waste heat/surplus heat shows, on average, a high number of full load hours, which is clearly above the typical average values (volume divided by capacity) of Austrian district heating networks of about 2000. This reflects the low variable costs of waste heat, which secures an early position in the heat merit order (cf [

17].).

All 21 respondents provided information on the characterization of the source of the source of waste/surplus heat; therefore,

n = 21 (

Table 2). The question was multiple-choice, so more than one answer was possible. The choices were “excess heat from industrial combustion”, “waste heat from process, directly feedable via heat exchanger” and “waste heat from process, prepared via heat pump”. Ten out of 21 answers indicated the use of recovered heat from the process, which is directly usable via heat exchangers, six times, both excess heat from industrial combustion and waste heat from process, direct use via heat exchangers, were ticked in combination. Once, excess heat from the process direct use via heat exchangers and prepared via heat pump was ticked in combination. Two times excess heat from industrial combustion, and two times waste heat excess heat from process, prepared via heat pump were ticked by the respondents. Based on the questionnaire responses and accompanying interviews, it can be assumed that the other implementations do not have multiple sources of the same category but usually only one source of waste/excess heat is actually used. The implementations reporting multiple sources are significantly larger on average (60 MW and 185 GWh/year, or 32 MW and 92 GWh/year excluding high and low outliers) than the average of the other responding implementations (13 MW and 33 GWh/year).

Of the 21 responses received, all respondents provided information on the characterization of the use of the fed-in waste/excess heat (

Table 3). The question also allowed for several possible answers. The choices were “base load coverage”, “feed-in only during the heating season”, and “other”, the latter of which could be specified. The “base load coverage” response option was intended to indicate that waste/excess heat is the preferred heat source to meet customer demand (hot water and heating). Responses that were noted under “other” but were consistent with this were moved. This includes those implementations that can provide a full supply (even year-round) but are only available during industrial operation. All implementations remaining in the “other” category take responsibility for the full supply of the district heating network with their waste/excess heat, including the available backups/alternatives. Summarizing the answers to this question, they support the assumption that waste heat is used to cover the base load, which is consistent with the above-mentioned results on full load hours. The base load was selected 15 out of 21 times, five respondents stated full supply of the district heating network with supply responsibility, one answer could not be clearly assigned, and feed-in only in the heating season did not apply to any of the respondents.

3.1. Motivation & Initiation

This section analyzes the drivers for the first contact and the subsequent implementation, focusing firstly on a personal level, i.e., the people involved and how they intervene with the cooperation partners, and secondly on a corporate level, i.e., the operational circumstances. Finally, a cross-comparison will be made to highlight the relevance of both circumstances and people.

3.1.1. Acting People

Out of the 21 responses, 18 provided information on who initiated the collaboration (

Table 4). The question was multiple-choice, i.e., several options could be selected. This was deliberately chosen in order to account for equal initiators. Three choices were selected three times, ten times two choices were selected, and six times a single choice was selected.

The option “legal requirements” was not selected at all, i.e., requirements in the course of plant approval or similar did not lead to implementation in any case.

The management or employees of the industrial companies were selected as initiators in 14 out of the 30 selections, while the management or employees of their cooperation partners were chosen only eight times. It remains uncertain whether the responses would be different or reversed if district heating companies, rather than industrial companies, had participated in the survey. Within the industrial companies, it appears that ambitious employees seem to play a more decisive role than management. From the outside, i.e., from the perspective of the cooperation partner, it is possible that the respondents would have chosen the management of the cooperation partner, since they were the ones who approached the industry.

Third parties were selected eight times, but their role is particularly worth mentioning in five individual cases (with a total of six selections). The written statements mention the mayor, the head of the municipal office, or the municipal council. The positive role of local policy makers is thus made clear. Supra-regional policy makers are not mentioned in their role as initiators. (The role of supra-regional policy makers is mentioned in another question, i.e., in the granting of subsidies).

3.1.2. Relationships

The idea of collaboration and how it came about was explored through an open-ended question, and the responses were categorized based on the primary motivation described by the respondents. The following categories represent the most specific statements:

“Known people/good contact”: includes all implementations where the description of the initiation indicates a good understanding, a regular exchange, and a certain trust (also by third parties like mayors).

“Current interest”: includes all implementations where there was an obvious advantage/need due to a particular situation such as new buildings, ongoing site changes, etc., and contact was established as a result.

“Long sought, finally realized”: includes all implementations where the description of the initiation indicates a long-lasting awareness of the potential, but a lack of economic viability or need; the realization came about due to new actors or changes in the situation of one of the cooperation partners.

Two of the 18 cases could not be clearly assigned: in one case, the initiation was based on the search for best practice examples found in another plant in the industry that served as a model; the other case arose more by chance during a conversation about other topics (the conversation, in turn, cannot be reliably assigned to the category “people I know/good contact”) (

Table 5).

According to the explanations provided by the respondents:

About one-third of the implementations resulted from exchanges in a good discussion climate, followed by fundamental decisions, open handling of data, and tough but fair negotiations.

Two-thirds of the implementations were more likely to result from technical and economic factors. These include situations where new investments are made in industrial operations, the district heating network, or the surrounding area, leading to the identification of new potential. The consideration for collaboration may be spontaneous or the result of long-term attention. It can be assumed that this process is also characterized by openness and fairness.

3.1.3. Circumstances

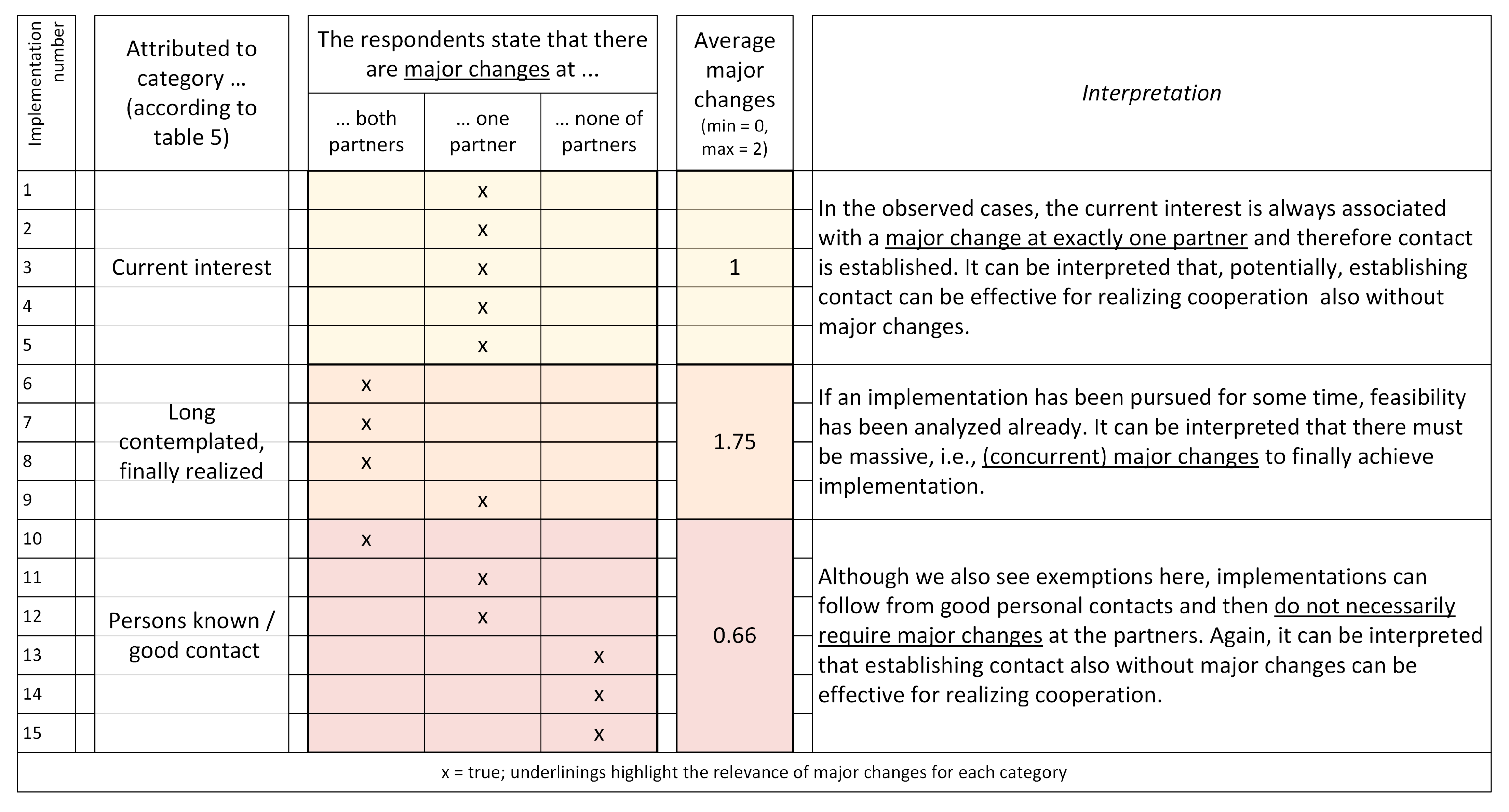

Another question asked about the timing of the cooperation. This was to test the hypothesis that significant changes in one of the partners (e.g., new construction or major modification of the facility) could be interpreted as a commitment and contribute to higher trust. Significant changes could occur in the industry, in the district heating network, in both, or in neither. Selecting none of these options could mean that neither is true, but also that no answer is given to this question. Through the accompanying interviews, the non-selection could be clearly interpreted as “none” in six out of nine cases; the other three cases that remained unclear were eliminated (thus

n = 18) (

Table 6).

3.1.4. Correlation of People and Circumstances

To determine the relationship between good contacts and the need for big changes in implementing collaborations, the correlation between the two previously analyzed questions was examined. After eliminating cases where clear answers were not available, there were 15 responses remaining (

Figure 2).

It seems obvious that a “current interest” comes from (only) one actor who is highly interested, and that implementation is an issue-focused situation/development. Projects that have been pursued for a long time require massive changes before they can finally be realized. If there are good contacts (the interviewees mentioned fellow students, former employees, frequent meetings at regional events, etc.), projects can be realized even without significant changes in the partner companies.

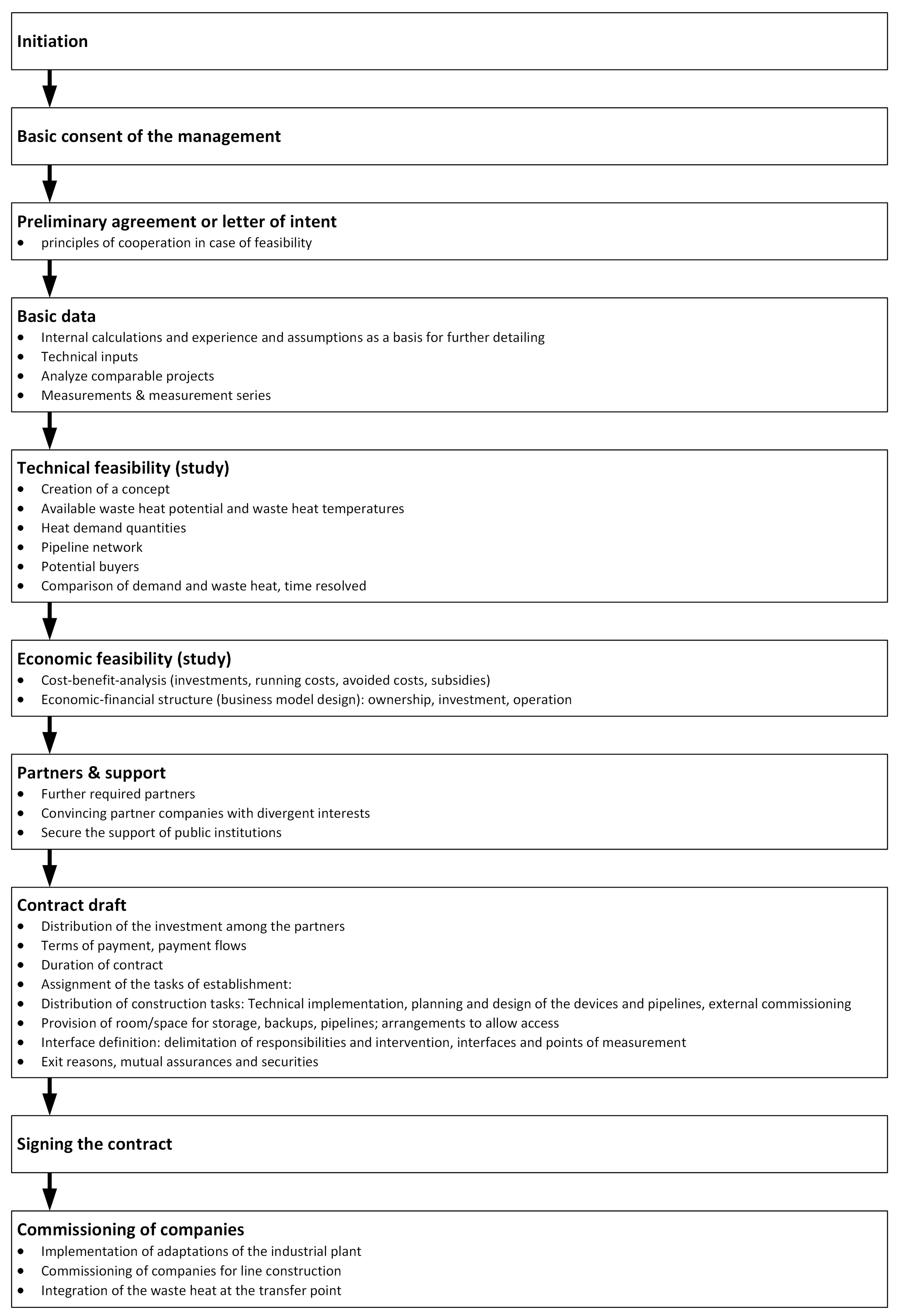

3.2. Implementation Process

Compared to the other questions, the survey included a very open question about the implementation process. Respondents were asked about the necessary steps, such as measurements, meetings, assurances, contract negotiations, external information gathering, internal persuasion, and the involvement of different levels. They were also asked how trust was built through the information provided, and how long the process took.

Eight (n = 8) respondents indicated the duration of the process from initial initiation to the start of construction. The author’s impression from the interviews was that the respondents did not know exactly and that most of them estimated the duration. They stated that the process took between “0.5–0.75” years as the shortest duration and “1–2” years as the longest duration. It only took longer in cases where the district heating network had to be established together with the cooperation and customers had to be integrated.

The question about necessary steps was answered for 16 out of the 21 cases. Possibly due to the open-ended nature of the question, the answers vary greatly in their focus and level of detail. They do not allow for categorization. Instead, when put together like a puzzle, they provide an overall picture of the process and indicate that the implementation is working well (

Figure 3).

3.3. Contract Negotiations

Out of the 21 the responding industrial companies, 19 provided information on how the cooperation with the district heating network is organized. Regarding the organization of the cooperation, 18 of the 19 implementations are organized by contracts between two clearly separated companies and with clear interfaces. Only one implementation is organized through a joint subsidiary, which likely requires a set of contracts between the industrial company and the subsidiary, along with greater transparency and co-determination rights resulting from the participation.

In four out of 11 responses, a sample/template contract was available from the district heating network operator. In one of these cases, the model contract was already specified for the purchase of industrial waste heat. In the other seven cases, the contract was jointly developed (apparently from scratch). Some cases involved the group’s legal department, while others required external lawyers. In one case, the contract was drafted on the basis of the initial letter of intent, and in another case, the starting point was the technical design of the cooperation.

Especially when no sample/template contracts were used, the agreements prove to be complex in the following topics:

Long duration, ranging up to 15 or even 20 years.

Pricing: although the link to price indices is mentioned as a simplification, it is clearly reported that, while technical discussions are easy, price negotiations are complex as “no one wants to pay more than necessary” and yet everyone must feel treated fairly; in a bilateral cooperation, partners are equally important and thus all partners must not feel “cheated” to finally sign the contract.

Responsibility for the interfaces between parties.

Ownership rights in extreme cases (e.g., bankruptcies, closure).

In addition to the core contents of the heat supply contract, easement agreements must also be concluded.

In some cases, the drafting of contracts was a long and arduous process (“preparation by internal legal department, further preparation by them, longer term work by external lawyers”), but others report very short processes (“three to four efficient rounds of negotiations, not more than one day in total”, “openly designed with few obligations”). The complexity of the cases and the different technical aspects involved likely contributed to these variations. Family-owned industrial companies (again) seem to reach a positive conclusion easier/faster than international corporations. However, as explicitly and implicitly stated in the interviews, the creation of the contract is generally characterized by the trust established at the beginning.

3.4. Business Model

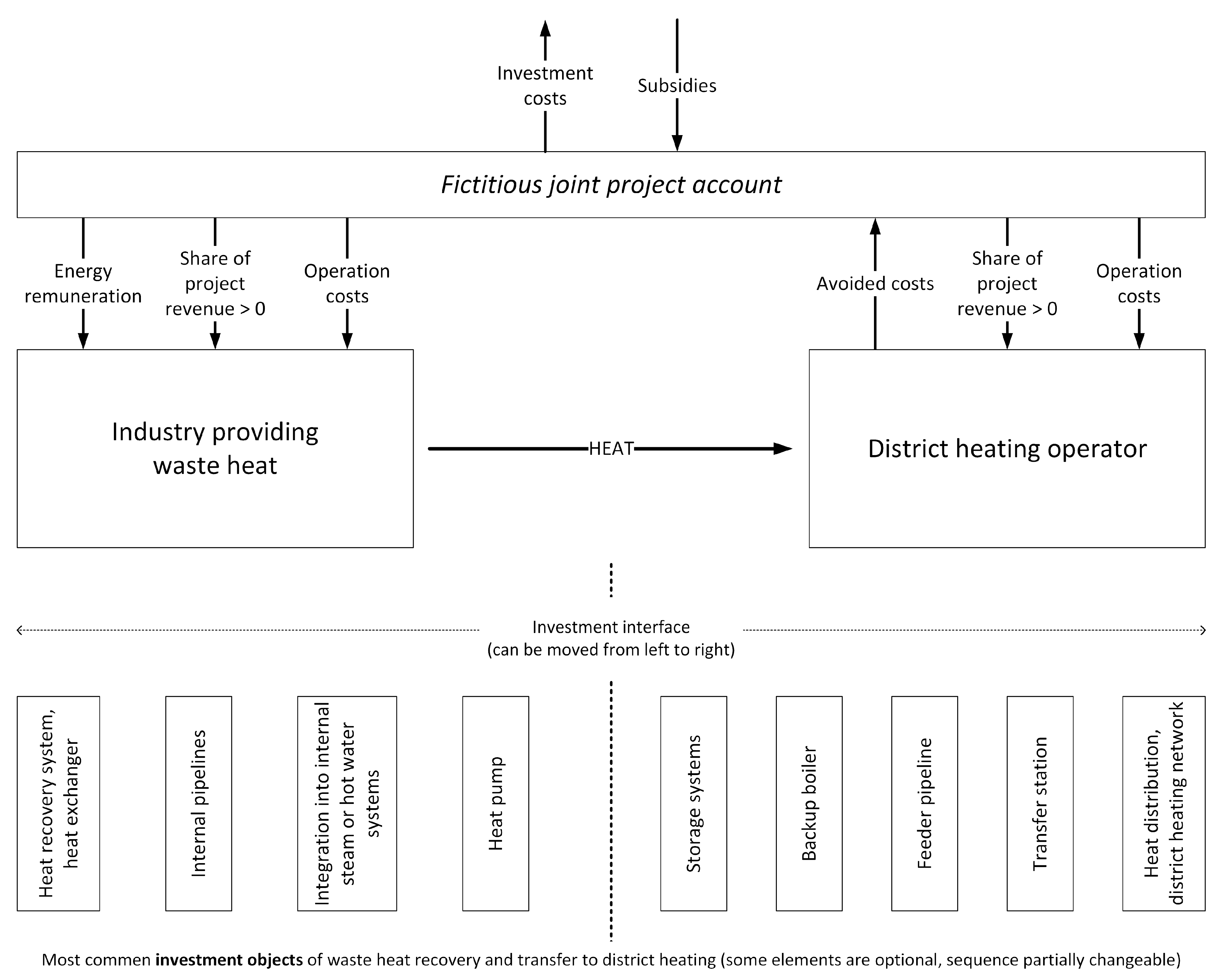

Cash flows occur in two main situations: during the investment phase of the project implementation, mainly through expenditures on both sides of the cooperation to technology providers/plant constructors and during the operation phase, mainly through payments from the district heating network operator, using the waste heat to the supplying industry.

3.4.1. Investment

In the case of financing or investment, either a predefined interface (transfer station/heat meter), which is later relevant for billing, also separates the investments, or one partner bears a larger share of the investment costs. After eliminating vague explanations and repetitions, the responses (

n = 14) were categorized. The results are shown in

Table 7.

The four categories do not correspond to the four business scenarios identified by Fritz et al. [

19]. However, the distribution of cases confirms their hypothesis that “industrial excess heat producers are more likely to engage with [waste heat provision] for district heating if this does not induce costs or require investments on their part”.

In their statements, the respondents provided information on the investment components used in their project. At the same time, as explained above, they provided information on their allocation to the actors. Similarly, the cash flows can be summarized based on the information provided (based on the cost comparison of Moser et al. [

17]). The resulting cost components and cash flows are summarized in

Figure 4.

Moser et al. [

17] derive that a project must first be profitable from a mutual perspective, and then the profits must be redistributed to benefit each partner. To represent this, a fictitious joint project account is created where all revenues (and avoided expenses) are deposited, and all expenses are withdrawn. The income comes almost exclusively from the heating company, which primarily saves on fuel costs. In addition, there may be investment subsidies from the government. Expenses include (i) initial investment, (ii) operating and maintenance costs, and (iii) compensation for the alternative use of heat (if applicable, e.g., lost income from electricity generation). After all income and expenses have been considered, there must be a profit in the sense of an economic surplus, which is divided between the two partners. Avoided cooling costs were not mentioned as a motivation in the interviews and are therefore not shown in the

Figure 4.

3.4.2. Billing

The responses regarding billing show very clearly that almost exclusively kWh-based billing is used in ongoing operations.

The prices in Euro/kWh are in most cases contractually indexed, with the choice of the price indices depending on the design of the system or the available back-ups or alternatives. Examples mentioned are the consumer price index and indices for electricity, gas, fuel oil, and energy wood. Another response mentions the use of the regulated retail price. In two cases, the kWh price is lower until the project is paid off, after which the price is based on predetermined indices and the profit is shared.

A total of three specific price quotes provided in the responses, which are context-specific and refer to particular situations or system configurations at specific points in time, sometimes several years in the past. These are twice 10 Euro/MWh and once 20 Euro/MWh. These are quoted here as collected values, although it must be clearly stated that they lack any generalizability and any necessary context.

The price of heat is also linked to the distribution of investments—if they are allocated more to one partner, the price changes in favor of that partner. For example, an industrial company that invests in the entire system, provides higher temperature heat, also generates peak loads, provides back-up, and manages heat transport, will obtain a higher price than an industrial company that invests nothing, has no responsibility, and occasionally provides lower temperature heat. While the former acts similarly to a typical district heating operator and can expect similar prices, the remuneration for the latter will be low. Based on the interviews, we expect a 10:1 ratio in the Euro/MWh remuneration for these polar supply qualities. We cannot make any statement as to how the individual parameters correlate with the overall remuneration.

Six out of the 21 implementations have indicated to what extent there is a supply obligation of the industrial plant to the district heating network. Four out of the 6 state that there is no obligation to supply, but do not specify whether there are further rules. In another case, waste heat must be delivered when it is available; other uses are excluded. In the other case there is a guaranteed minimum output, which is only not obligatory if the district heating network does not require it.

Other theoretically possible price components such as fixed cost compensation or standby compensation, etc., are not mentioned in the interviews or are denied when asked. In some cases, rental fees are charged for the use of space and/or premises on the plant site where transfer stations, back-up boilers or storage facilities are located. In some cases, specific amounts are also charged for necessary repairs/maintenance.

3.5. Payback Period

The survey asked the question “Payback period of the project for your company [years]”, which was clearly marked as optional. There are 8 responses to this question (

Table 8). The average payback period (expected at the time of the decision) is 9 years (mean value); and the almost identical median is 8.5 years. Only one project stands out with a low payback period—within the three years often mentioned for industrial energy projects (cf. Moser et al. [

17]). This result allows to reject the hypothesis that only highly-profitable projects are realized, which was raised by Moser and Lassacher but remained unanswered due to a lack of data in their study. Potential explanations can be found below.

In this context, the additional information from the accompanying interviews is very revealing. In one interview, the interviewee mentioned that (third-party) experienced implementers consider a payback period of 6–7 years to be feasible. At the same time, factors such as the image of the company, its positioning as sustainable, or its commitment to the region play an important role, which means that even longer payback periods are accepted (cf. “strengthening local ties” as described as a motivating factor in Fritz et al. [

19]). This is often accompanied by low investments in relation to total sales or total location costs, and some even consider a failure of the cooperation to be bearable.

3.6. Handling Risks

The fourth block of the questionnaire dealt with risks and uncertainties, which are a source of a variety of barriers to the waste heat cooperation between an industrial company and a district heating network, as identified in the literature (Rodin and Moser [

9]).

In two-thirds of the cases, external risks and uncertainties, such as market changes are hedged through the price index defined in the contract. In addition, the following perspectives on risks and mitigation measures can be translated into recommendations: Risks and uncertainties lead to contractual clauses according to respondents.

New construction (industrial plant or district heating network side) is a commitment. Larger investments and the availability of raw materials for specialized industrial plants confirm that it will stay in place—this can be seen as risk mitigation.

Cooling plants must remain at the industrial site, and backup systems must be available for district heating (network, either at the industry site or the heating plant. This ensures protection against unplanned outages, planned shutdowns, and production stoppages.

Options to acquire or utilize assets serve as a hedge in the event of a longer-term production stoppage.

Take-or-pay and deliver-or-pay arrangements or residual-value-clauses help avoid sunk costs.

Insurance as a measure to mitigate risks and uncertainties are mentioned only once in all the questionnaires.

4. Discussion

In this section, we focus on the limitations of the results and then summarize the main findings into three blocks.

4.1. Restrictions on Validity

The validity of scientific results consists of internal and external validity. The external validity results from a high number of cases and is usually referred to as “statistical significance”. Even if all Austrian cases answered in full detail, this statistical significance could not be achieved. Moreover, due to the large number of parameters that make up the development and design of a cooperation, it would not be assumed that the correlations of individual parameters achieve significance, even if all European cooperations were recorded. Another problem for the statistical significance is that the many qualitative answers can hardly be quantified and are therefore difficult to put in relation. Consequently, here, validity can only be achieved through internal validity, which results from the causality of the qualitatively described arguments. Through the design of the questionnaire and the corresponding questions in the interviews, the authors were careful to explore the arguments and presented them in detail in the individual question sections. Arguments or potential reasons were presented, for example, for the arguments for longer payback periods; limitations were clearly highlighted, as can be clearly seen in the example of the waste heat price.

4.2. Replicability Outside Austria

The results come exclusively from cooperations in Austria. The district heating market in Austria is not regulated on the supply side, which is also the case in most European countries [

10]. Like Austria, almost all EU countries are market economies, i.e., the same principles apply, such as the need for profitability, the assessment of risks, etc. The industries and large-scale industrial technologies are widely the same, and the district heating networks also function similarly, which means that there is technical comparability. The following subsections of the discussion also show that many results are supported by results from other countries.

Differences can exist in certain framework conditions, such as the heating degree days or heating load curves. Technically, differences in the district heating systems could be decisive, for example, if lower flow temperatures allow easier feed-in. Other energy prices or subsidy systems can also be relevant from an economic perspective. Furthermore, many of the results also relate to social aspects such as relationships and trust, which can also differ in other cultures.

In conclusion, it can be stated that the Austrian results can generally offer good indications for the support of a successful implementation of a cooperation, although many details would likely have to be adapted country-specifically.

4.3. Third Parties as Facilitators

The waste heat cooperation was most often initiated by the management or employees of the waste heat supplier. In fewer cases, from the point of view of the waste heat suppliers, the implementation of external waste heat utilization was initiated by the management or employees of the cooperation partner.

However, the positive role and impact of local policymakers are highlighted. In addition, applied researchers and consultants/auditors can play a similar role. Third parties such as local policymakers appear as a point of concentration of information, allowing them to identify potentials and mediate between partners. These results are in line with those found in the literature, e.g., in Södergren and Palm [

20] or Fritz et al. [

19]. We also find that third parties or policymakers from a higher level than the local level are not mentioned as being initiators. However, they could play an important role by institutionalizing support for cooperation (e.g., GreenLab Skive in Denmark or Center IUS in Sweden) or by raising awareness of the issue on the part of mayors or municipal officials.

4.4. Trust, Transparency and Clarity

In many cases, the idea of cooperation arose from good contacts on both sides of the cooperation partners, i.e., the idea of a waste heat cooperation was promoted, especially by good understanding, regular exchange, and a certain level trust. Subsequently, the project could be realized without significant changes in the partner companies. This is a clear implication that the good contact ensures a direct and uncomplicated basis for discussion and that there is also trust in the statements of the future cooperation partner. Again, this is in line with the results obtained from the literature, e.g., Fritz et al. [

19]. Unfortunately, some of the mentioned forms of good contacts (e.g., fellow students) are not a prerequisite for employees and management. However, the question is not how and whether these prerequisites are present, but how they can be created through external facilitation. One of the interviewees mentioned that the partners often meet at regional events, and this form of good contact gives an indication of the possibility of initiation. Institutionalizing support for cooperation could be an option. Establishing the initial contact is the key step towards implementation, as evident in the category of projects implemented after a “current interest” arose.

Once the initial contact is established, the technical parameters have to match. This is a laborious task and also requires trust in the reliability of the information provided by the cooperation partner, which often implies the need to share measurement data and energy purchase prices. It often involves additional tests or measurements. Component design may have had to be modified for technical applicability, which in turn had an impact on investment costs. Nevertheless, respondents considered this work to be normal, while many pointed to price negotiations as a second key step due to their complexity.

First, all the partners’ costs must be covered. However, there are no rules for the distribution of the surplus. The share of the investment, possible alternatives, etc. play an important role in the negotiation. Nevertheless, it is essential for this bilateral cooperation that both partners sign the contract; all partners must, therefore, feel that they are being treated fairly. The survey shows that the creation of a contract is generally characterized by the trust established at the beginning. However, trust and transparency also play a central role in price negotiations, as they determine the individual feeling of whether a contractual (price) clause is perceived as fair. Some respondents report full mutual inspection possibilities, and in several cases, it is known that a joint subsidiary ensures this transparency.

In contrast to other areas where large parts are standardized (e.g., the frequency or the grid levels in the electricity sector), technical and economic parameters interact in a heat cooperation (Moser et al. [

17]), which increases the complexity of negotiations. Regarding the organization of the cooperation, 18 out of the 19 implementations are organized by contracts between two clearly separated companies and with clear interfaces. These interfaces, directly or implicitly mentioned, are used as boundaries for investments, responsibilities, and billing. They increase clarity and reduce complexity.

4.5. Business Models and Economics

Experienced implementers consider a payback period of 6–7 years as feasible, which seems to be in line with the risks associated with short-term industrial production and market interest rates for such projects (at least for the 2010s until the beginning of 2022). Presumably, based on the answers of the respondents, the image of the company, the commitment to its regional ties and the low investments compared to the industrial plant as a whole (i.e., negligible risks) allow the implementers to accept longer payback periods as well. We find an average payback period (estimated at the time of the decision) of 9 years, with significant variations from 3 to 15 years.

From the perspective of the district heating operator, new construction or major modification of the industrial plant is a commitment to the site and thus reduces the risks associated with redeployment or eventual closure. In line with the notion that projects are associated with major changes, awareness of major changes can be a signal for external intermediaries to get involved. This may be the case for many companies at the local level, as the practical examples show that there is no minimum size for (economic) feasibility.

In order to ensure equal interests, one case reports that the investments were distributed in such a way that the payback periods for the industry and the district heating operator were the same. A common amortization point also makes sense because different procedures can be chosen before and after, e.g., no dividend is paid before amortization. Of course, this model is primarily applicable to the most common business model with a clear cut-off point. In the other models, the risk is distributed differently with the investments. The business models range from full investment by district heating to full service by industry. However, the risks usually lead directly to contract components, which means that the partner is also involved.

The value of waste heat is highly case-specific, but at least qualitatively, we can generalize that it is clearly related to the temperature supplied (direct feed vs. preparation, e.g., with a heat pump), the continuity of supply (24/7/365 vs. weekday daytime only), any guarantees regarding the quantity supplied, the assignment of responsibilities (operation of storage and back-up systems), the flexibility of supply (e.g., coverage of peaks) and the share of investment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}