De-Risking the Energy Efficient Renovation of Commercial Office Buildings through Technical-Financial Risk Assessment

,

,

Abstract

1. Introduction

2. Background on De-Risking Energy Efficiency in the Building Renovation Sector

3. EEnvest Evaluation Methodology for Energy Efficient Renovation Projects

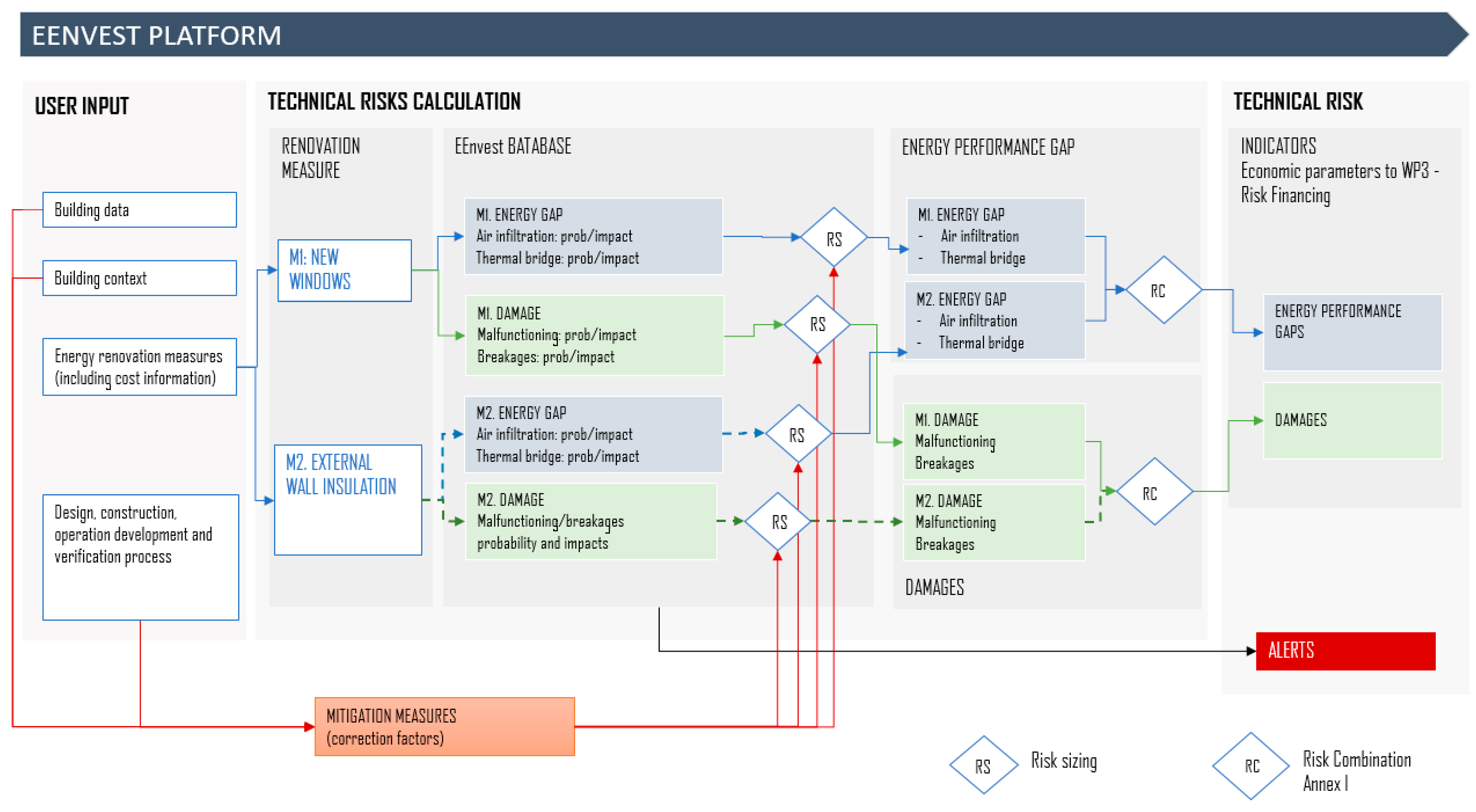

3.1. Definition of Technical Risk

Technical Risk Calculation Methodology

3.2. Definition of Financial Risk Associated with Technical Risk

- i.

- Technical performance: if the renovation measures do not perform as expected, then the financial performance of the investment will also be directly affected. In the case of energy performance gap, lower energy savings means lower economic and financial savings, while in the case of damage, an additional investment is required in order to achieve the expected results;

- ii.

- Climate: warm winters and cold summers affect the overall economic convenience of an energy efficiency investment, as they imply lower energy requirement for the building. This means, compared with the baseline of historical energy consumption, that the real amount of energy saved will be lower than expected, implying a lower return on the investment;

- iii.

- Energy price: the variation of the cost of energy also affects the economic convenience of an investment, as the same amount of energy saved in terms of kWh will correspond to a different Euro amount.

- The event of damage causes an additional investment for extraordinary maintenance/repair. As a consequence, in order to estimate its impact on the financial performance, the probability distribution of the damage random variable, expressed as a percentage, is applied to the investment cost, and considered as a negative economic component for the calculation of financial indicators.

- The event of underperformance causes a reduction of energy savings compared to expectations. As a consequence, in order to estimate its impact on the financial performance, the probability distribution of the energy gap random variable is applied to the expected value of energy savings and considered as a negative economic component for the calculation of financial indicators.

- EES = Expected Energy Saving, expressed in kWh, provided by the user as input;

- EP = Energy Price, expressed in €/kWh, provided by the user as input (based on actual prices observed for the energy audit) and linked to a probability distribution based on the analysis of historical series;

- EnergyGap = Risk of technical underperformance as explained above, expressed as a probability distribution in terms of % of EES;

- HDD = Heating Degree Days, representing the climate risk in terms of a probability distribution calculated on the basis of the historical series;

- Investment = Investment cost

- Damage = Risk of technical damage as explained above, expressed as a probability distribution in terms of % of the investment cost.

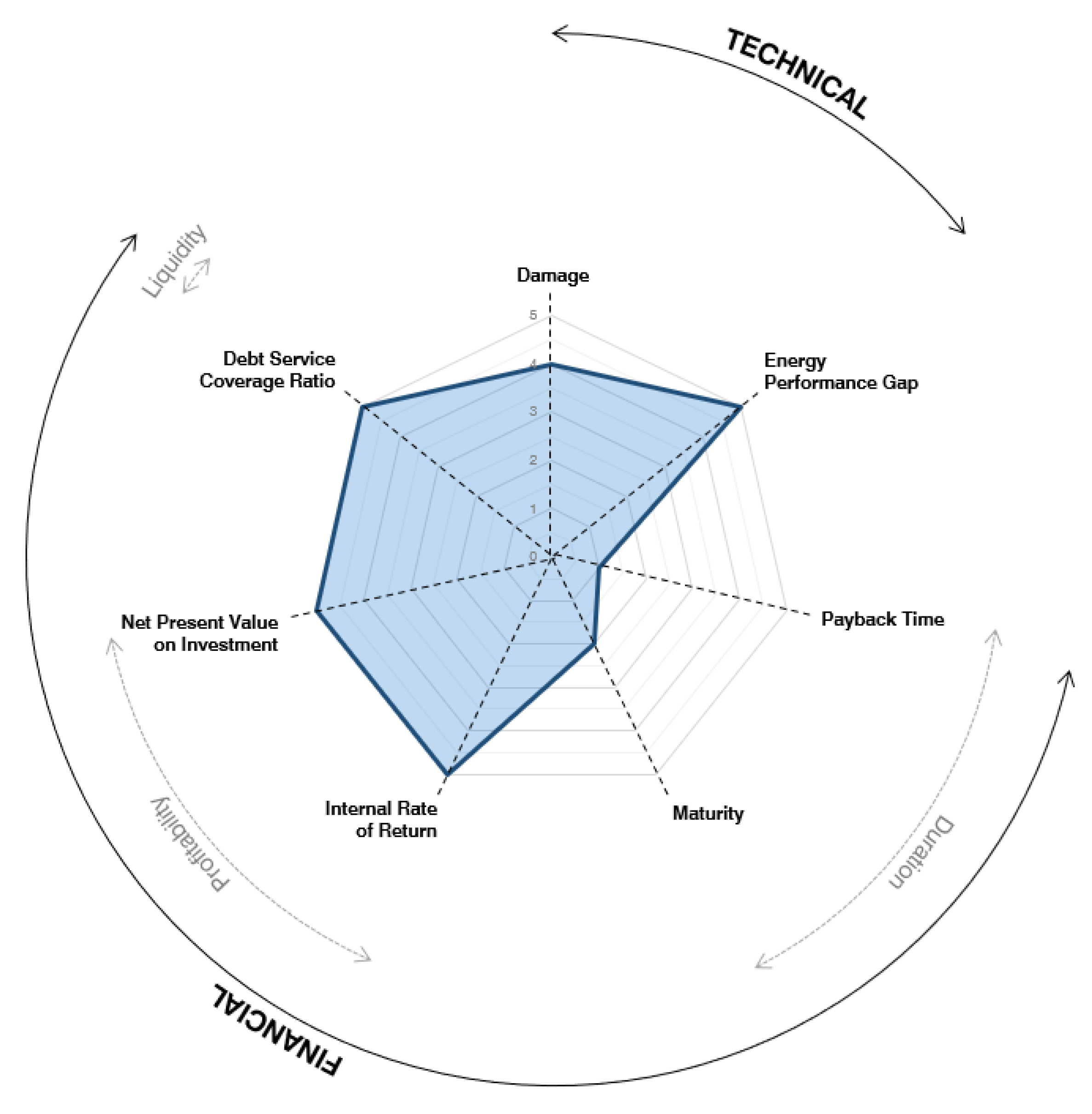

3.3. Financial Evaluation of Energy Efficient Building Renovation Based on the Occurrence of Technical Risk: The EEnvest Evaluation Methodology

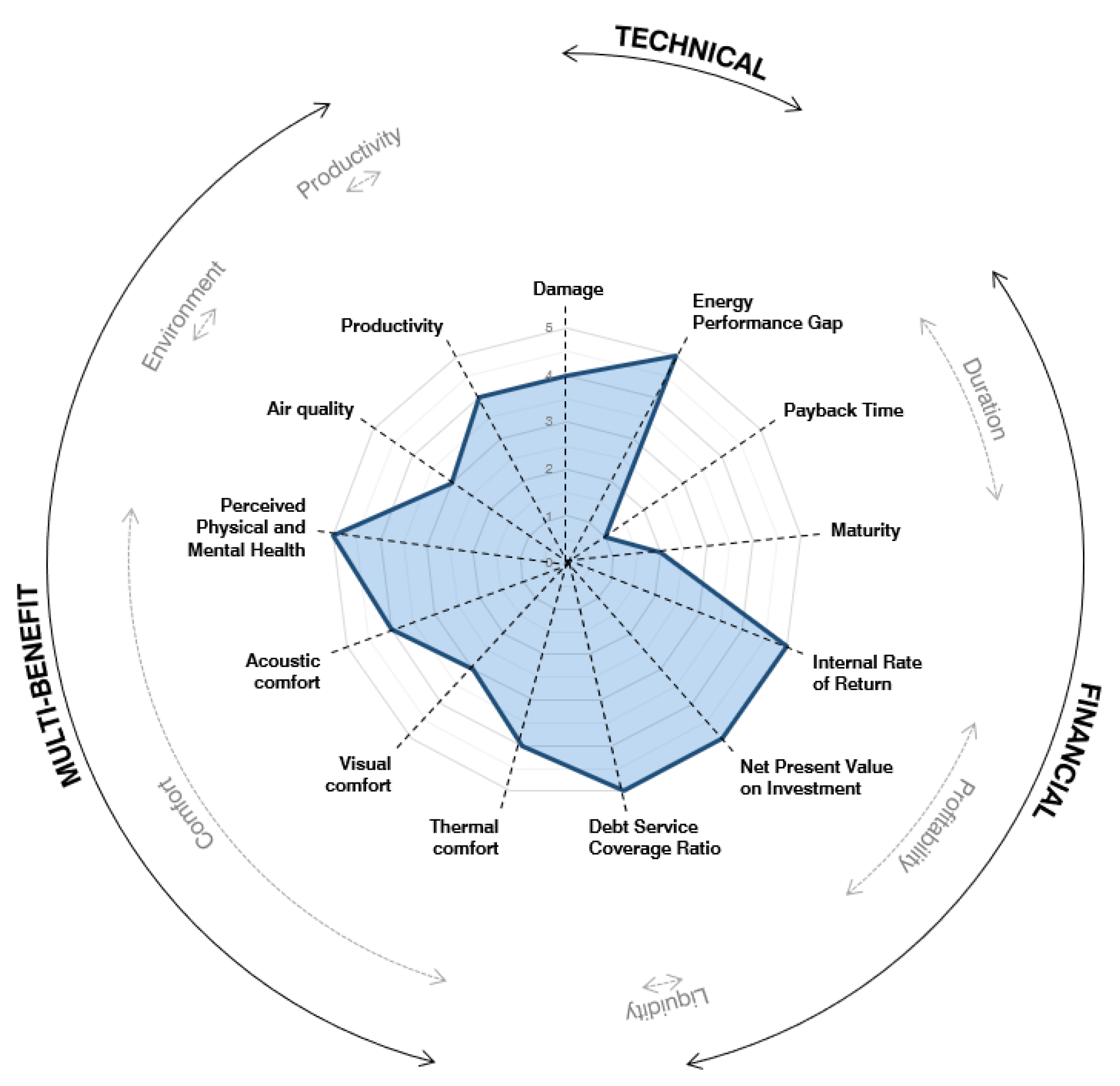

- Similarity between observations.

- Comparison between observations.

- Presence of outlier variables.

- Using multiple polygons in the same radar chart makes it hard to read.

- Representing too many variables creates too many axes and can also make the chart more complicated and harder to read.

- The variables on the different axes are usually nominally independent, therefore it can be hard to compare values across each variable.

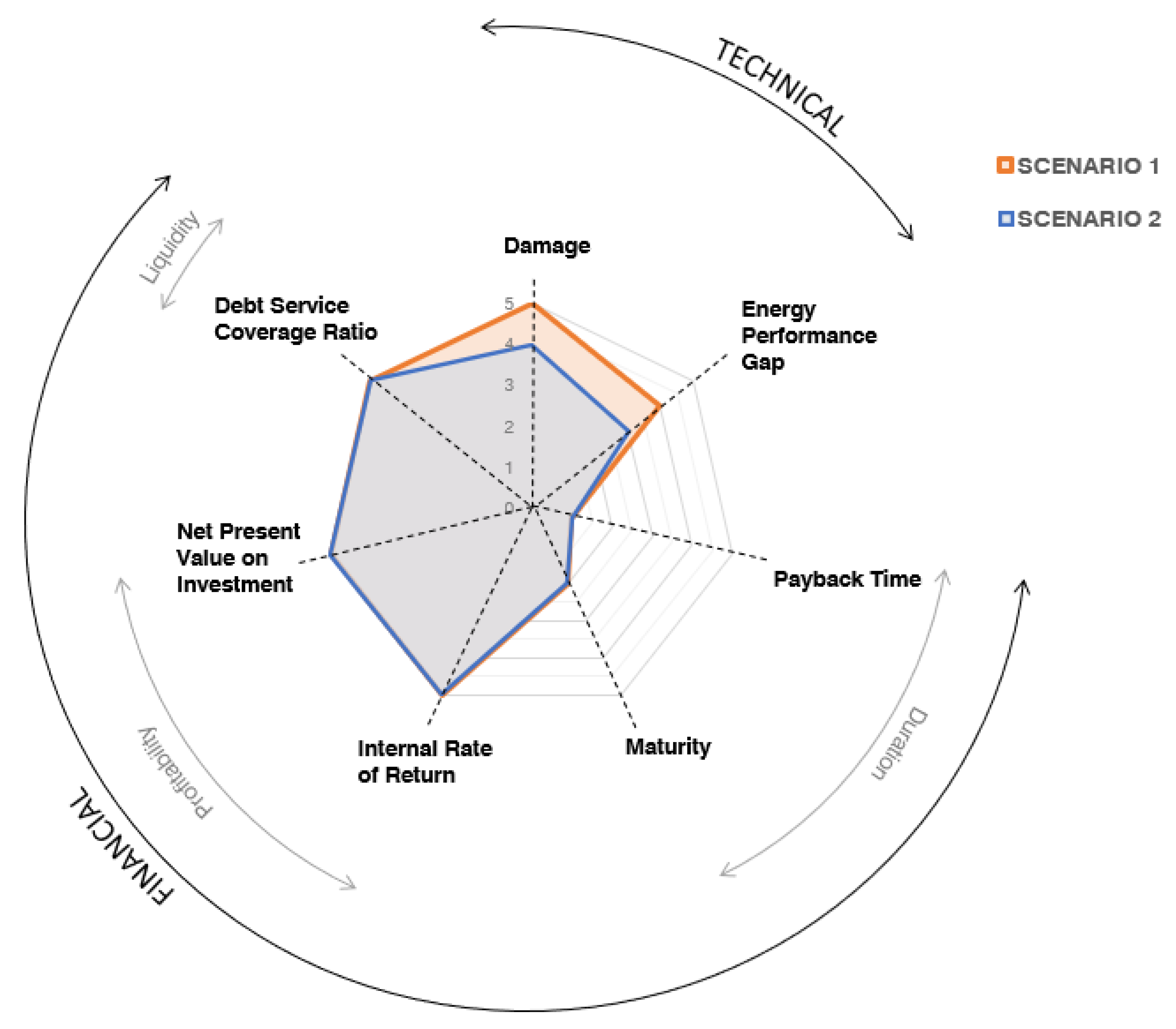

- The main pros of the radar visualization are:

- Overlaying multiple “webs” on a radar graph allows a very easy visual comparison against reference data sets.

- A reference polygon can be used as a benchmark for easy comparison.

- Deficiencies or strengths in performance are easy to visualize.

4. Case Study: Renovation of an Office Building

- -

- Natural gas consumption for thermal energy equal to approximately 1.5 M kWh/year, with an associated cost up to about 50,000 € (with a price of natural gas of 0.03 €/kWh).

- -

- Electric consumption about 3.2 M kWh/year, with associated costs up to 420,000 € (considering the electric price of 0.13 €/kWh).

- -

- Operation and maintenance (O&M) cost of the whole building, close to 316,000 € (this data includes the costs of maintenance contracts of the building construction, thermal and electric systems, operation and replacement and substitution of the materials or components).

- -

- Scenario 1 includes the mitigation measures, such as the LEED certification and the energy performance monitoring; according to this, the investment is slightly higher, with a payback time of 7.46 years.

- -

- Scenario 2 does not include any mitigation measure; the investment is lower, and the payback time is reduced to 7.26 years.

4.1. Technical Risk Evaluation

- -

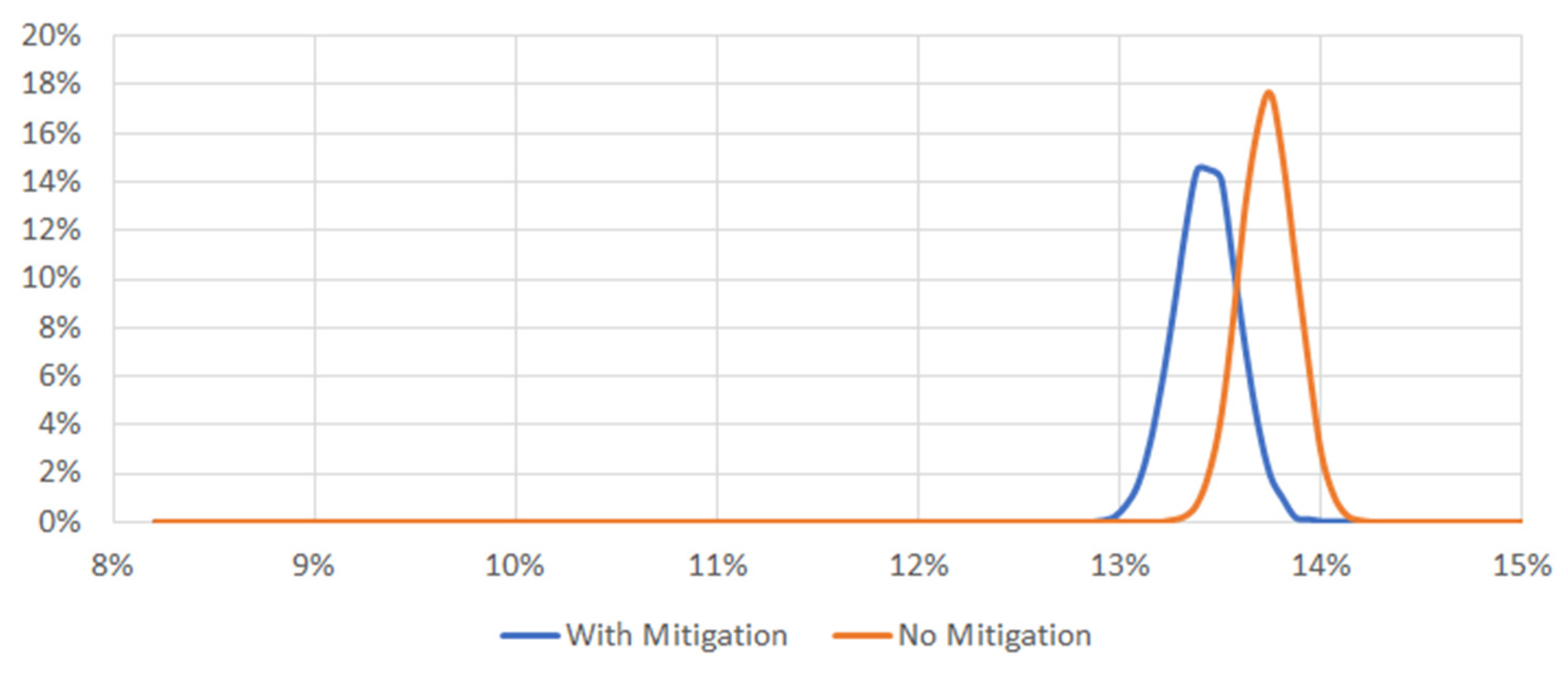

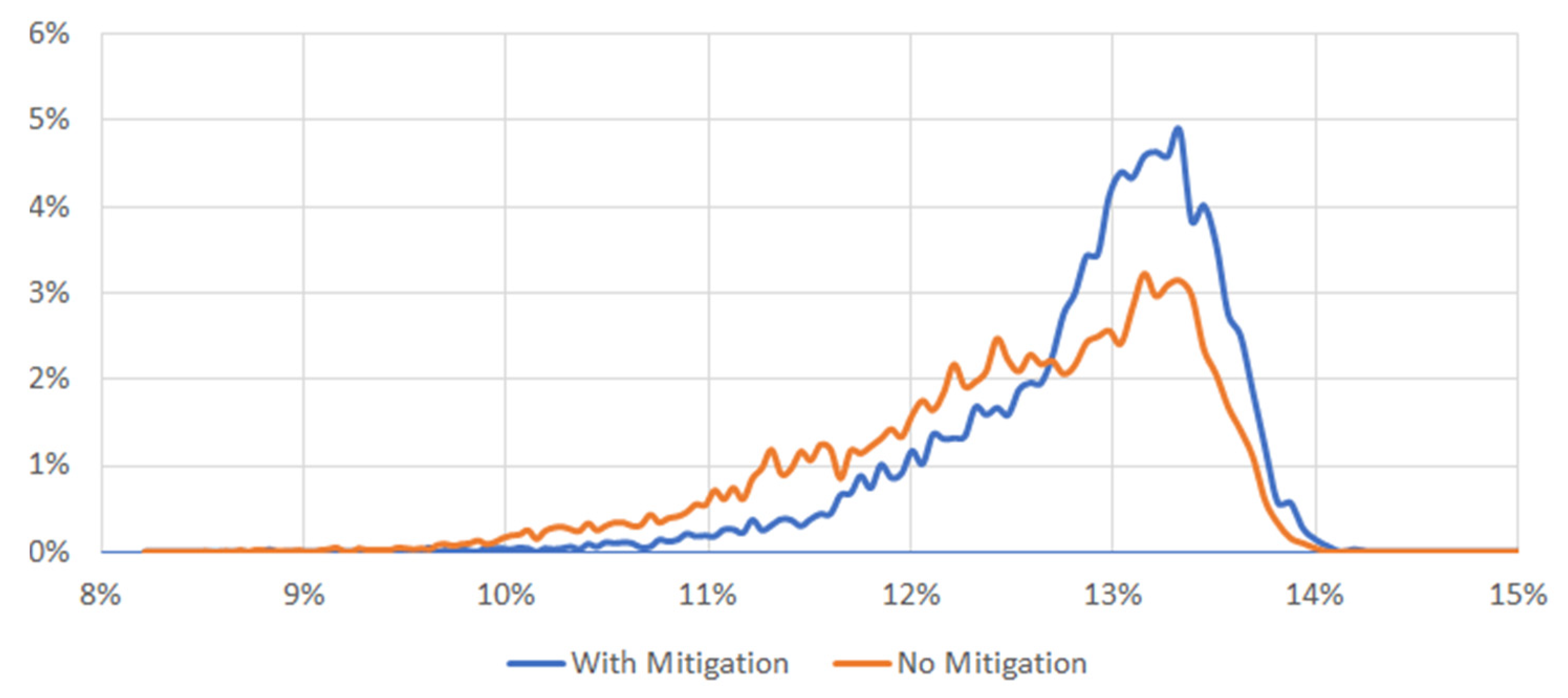

- damage indicators double the investment deviation from scenario 1;

- -

- energy gap indicator doubles the (annual) energy costs of scenario 1;

- -

- payback time indicator with technical risk is higher than scenario 1.

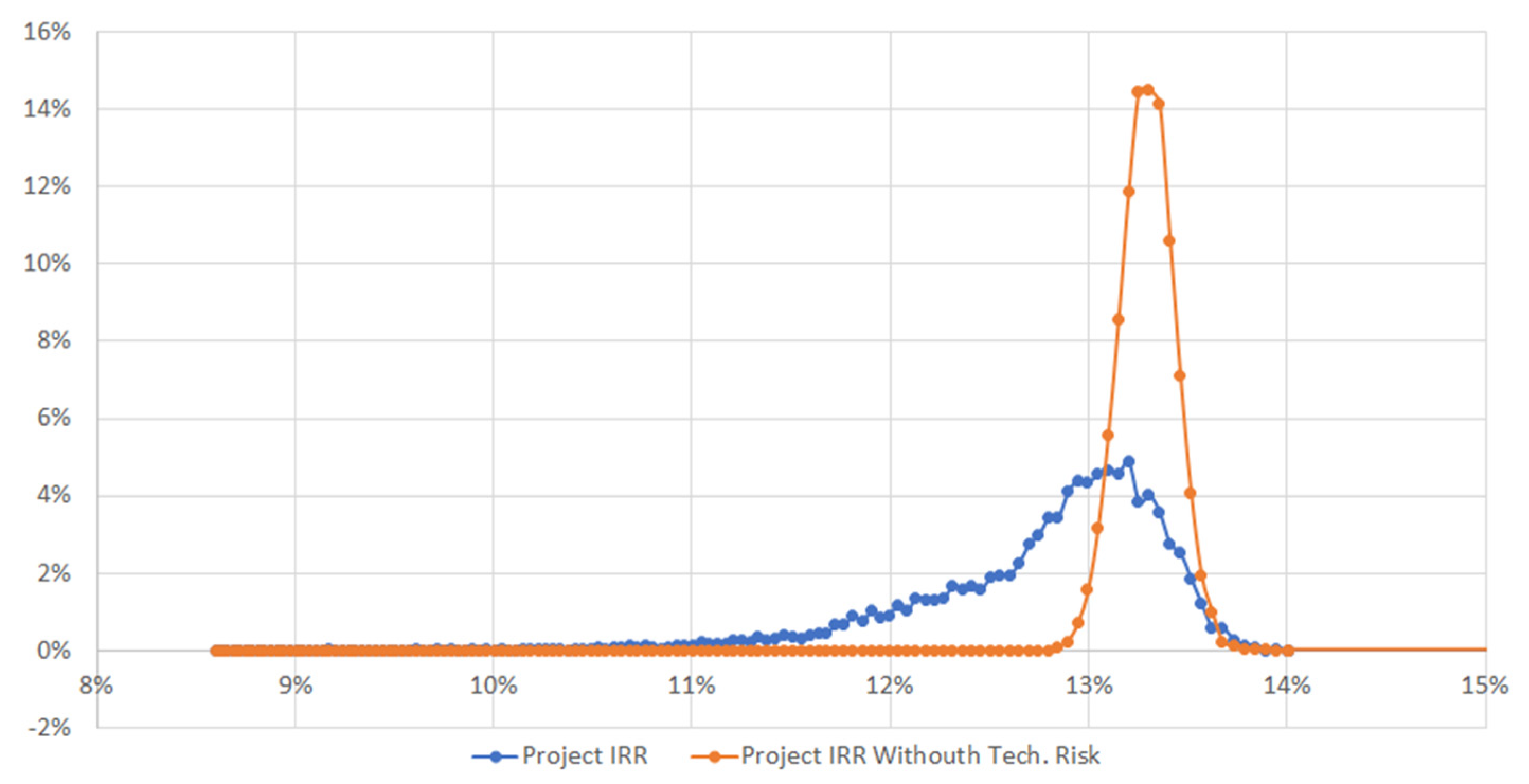

4.2. Financial Risk Associated to the Occurrence of Technical Risks in Window Substitution

5. Discussion

5.1. Technical Risk

5.2. Financial Risk

5.3. EEnvest Combined Evaluation and Progress against the State of the Art

6. Conclusions and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| KPI | Key Performance Indicators |

| EC | European Commission |

| EU | European Union |

| ISO | International Standard Organization |

| EPC | Energy Performance Certificates or Contracts |

| IFAD | International Fund for Agricultural Development |

| UN | United Nations |

| LEED EB:O&M | Leadership in Energy and Environmental Design certification for Existing Buildings: Operations and Maintenance |

| LEED | Leadership in Energy and Environmental Design |

| USGBC | United States Green Building Council |

| HDD | Heating Degree Days |

| IRR | Internal Rate of Return |

| FMEA | Failure Mode and Effect Analysis |

| SPV | Special Purpose Vehicle |

| NPV | Net Present Value |

References

- European Parliament. Directive (EU) 2018/2002 of the European Parliament and of the Council of 11 December 2018 Amending Directive 2012/27/EU on Energy Efficiency, Official Journal of the European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32018L2002&from=EN (accessed on 28 December 2021).

- European Parliament. Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources, Official Journal of the European Union. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32018L2001&from=EN (accessed on 28 December 2021).

- BPIE—Building Performance Institute Europe Renovating the EU Building Stock. Available online: http://bpie.eu/focus-areas/renovating-the-eu-building-stock (accessed on 28 December 2021).

- EURIMA Deep Renovation. Available online: https://www.eurima.org/energy-efficiency-in-buildings/deep-renovation.html (accessed on 28 December 2021).

- BPIE—Building Performance Institute Europe. 97% of Buildings in the EU Need to Be Upgraded. 2019. Available online: http://bpie.eu/wp-content/uploads/2017/12/State-of-the-building-stock-briefing_Dic6.pdf (accessed on 28 December 2021).

- Billio, M.; Costola, M.; Hristova, I.; Pelizzon, L. Final Report on Correlation Analysis between Energy Efficiency and Risk (D5.7); Energy efficiency Data Protocol and Portal: Bruseel, Belgium, 2020. [Google Scholar]

- Loureiro, T.; Gil, M.; Desmaris, R.; Andaloro, A.; Karakosta, C.; Plesser, S. De-Risking Energy Efficiency Investments through Innovation. Proceedings 2020, 65, 3. [Google Scholar] [CrossRef]

- Wiguna, I.P.A.; Scott, S. Nature of the critical risk factors affecting project performance in Indonesian building contracts, Association of Researchers in Construction Management. In Proceedings of the 21st Annual ARCOM Conference, London, UK, 7–9 September 2005. [Google Scholar]

- ISO—The International Organization for Standardization. ISO 31000:2009-Risk Management-Principles and Guidelines; ISO 310002009; ISO—The International Organization for Standardization: Geneva, Switzerland, 2009. [Google Scholar]

- Turner, C.; Analyst, S.; Frankel, M. Energy Performance of LEED® for New Construction Buildings; New Buildings Institute: White Salmon, WA, USA, 2008. [Google Scholar]

- Carbon Trust. Closing the Gap: Lessons Learned on Realizing the Potential of Low Carbon Building Design Sharing; Carbon Trust: London, UK, 2011. [Google Scholar]

- Zero Carbon Hub. A Review of the Modelling Tools and Assumptions: Topic 4, Closing the Gap between Designed and Built Performance; Zero Carbon Hub: London, UK, 2010. [Google Scholar]

- Menezes, A.C.; Cripps, A.; Bouchlaghem, D.; Buswell, R. Predicted vs. actual energy performance of non-domestic buildings: Using post-occupancy evaluation data to reduce the performance. Gap. Appl. Energy 2012, 97, 355–364. [Google Scholar] [CrossRef]

- Douglas, J.; Ransom, B. Understanding Building Failures, 3rd ed.; Taylor & Francis Group: Oxfordshire, UK, 2007. [Google Scholar]

- European Commission. Financing for Energy Efficiency Investments—Smart Finance for Smart Buildings. 2020. Available online: https://ec.europa.eu/info/funding-tenders/opportunities/portal/screen/opportunities/topic-details/lc-sc3-b4e-11-2020 (accessed on 28 December 2021).

- Ankamah-Yeboah, I.; Rehdanz, K. Explaining the Variation in the Value of Building Energy Efficiency Certificates: A Quantitative Meta-Analysis; Kiel Institute for the World Economy (IfW): Kiel, Germany, 2014. [Google Scholar]

- Ayikoe Tettey, U.Y.; Gustavsson, L. Energy savings and overheating risk of deep energy renovation of a multi-storey residential building in a cold climate under climate change. Energy 2020, 202, 117578. [Google Scholar] [CrossRef]

- Semprini, G.; Gulli, R.; Ferrante, A. Deep regeneration vs. shallow renovation to achieve nearly Zero Energy in existing buildings: Energy saving and economic impact of design solutions in the housing stock of Bologna. Energy Build. 2017, 156, 327–342. [Google Scholar] [CrossRef]

- Krizmane, M.; Borodinecs, A.; Dzelzitis, E. Enabling the Landscape for Deep Green Renovations. Energy Procedia 2016, 96, 404–412. [Google Scholar] [CrossRef][Green Version]

- Energy Efficient Mortgages Initiative. Energy Efficient Mortgages Initiative (EEMI): EeDaPP Confirms Negative Correlation Between Energy Efficiency and Risk (Press Release), Brussel, 31 August 2020. Available online: https://www.energy-efficient-mortgage-label.org/open-file/3/Energy-Efficient-Mortgages-Initiative-EEMI-EeDaPP-confirms-negative-correlation-between-energy-efficiency-and-risk (accessed on 28 December 2021).

- International Partnership for Energy Efficiency Cooperation (IPEEC). Building Energy Performance Gap Issues. An International Review. 2019. Available online: https://www.energy.gov.au/sites/default/files/the_building_energy_performance_gap-an_international_review-december_2019.pdf (accessed on 28 December 2021).

- Van Dronkelaar, C.; Dowson, M.; Burman, E.; Spataru, C.; Mumovic, D. A Review of the Regulatory Energy Performance Gap and Its Underlying Causes in Non-domestic Buildings. Front. Mech. Eng. 2016, 1, 17. [Google Scholar] [CrossRef]

- Qi, Y.; Qian, Q.K.; Meijer, F.M.; Visscher, H.J. Identification of Quality Failures in Building Energy Renovation Projects in Northern China. Sustainability 2019, 11, 4203. [Google Scholar] [CrossRef]

- Grillone, B.; Mor, G.; Danov, S.; Cipriano, J.; Lazzari, F.; Sumper, A. Baseline Energy Use Modeling and Characterization in Tertiary Buildings Using an Interpretable Bayesian Linear Regression. Methodol. Energ. 2021, 14, 5556. [Google Scholar] [CrossRef]

- Cuerda, E.; Guerra-Santin, O.; Sendra, J.J.; Neila, F.J. Understanding the performance gap in energy retrofitting: Measured input data for adjusting building simulation models. Energy Build 2020, 209, 109688. [Google Scholar] [CrossRef]

- Jackson, J. Energy Budgets at Risk (EBaR): A Risk Management Approach to Energy Purchase and Efficiency Choices; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2008. [Google Scholar]

- Mahdavinejad, M.; Silvayeh, S.; Nourian, Y. Review on Shifting to Energy Efficiency in Recent Architectural Studies in Iran. Arman Archit. Urban Dev. 2017, 10, 69–77. [Google Scholar]

- Cristino, T.M.; Lotufo, F.A.; Delinchant, B.; Wurtz, F.; Faria Neto, A. A comprehensive review of obstacles and drivers to building energy-saving technologies and their association with research themes, types of buildings, and geographic regions. Renew. Sustain. Energy Rev. 2021, 135, 110191. [Google Scholar] [CrossRef]

- Mecca, S.; Masera, M. Technical risk analysis in construction by means of FMEA methodology. Liverp. John Moores Univ. Assoc. Res. Constr. Manag. 1999, 2, 425–434. [Google Scholar]

- Saaty, R.W. The analytic hierarchy process-what it is and how it is used. Math. Model. 1987, 9, 3–5. [Google Scholar] [CrossRef]

- Roberti, F.; Oberegger, U.F.; Lucchi, E.; Troi, A. Energy retrofit and conservation of a historic building using multi-objective optimization and an analytic hierarchy process. Energy Build 2017, 138, 1–10. [Google Scholar] [CrossRef]

- Andaloro, A.; Paoletti, G.; Garzia, F.; Gubert, M.; Oberegger, U.F. Report on Technical Risks in Renovation (D2.1). 2020. Available online: http://www.EEnvest.eu/wp-content/uploads/2021/09/EEnvest_D2.1_FINAL.pdf (accessed on 28 December 2021).

- De Groot, H.L.F.; Verhoef, E.T.; Nijkamp, P. Energy saving by firms: Decision-making, barriers and policies. Energy Econ. 2001, 23, 717–740. [Google Scholar] [CrossRef]

- Rasmussen, J. Energy-efficiency investments and the concepts of non-energy benefits and investment behaviour. ECEEE Ind. Summer Study Proc. 2014, 2, 733–744. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicators | Code | Scale 1 | |

|---|---|---|---|

| Damage | Damage indicator quantifies the investment deviation due to possible malfunctioning or failures of the energy renovation measures adopted in the renovation project. | T.1 | 1. D > 3% 2. 2% < D < 3% 3. 1% < D < 2% 4. 0.5% < D < 1% 5. D < 0.5% |

| Energy performance gap | Energy gap indicator quantifies the energy performance deviation | T.2 | 1. EPG > 10% 2. 5% < EPG < 10% 3. 2% < EPG < 5% 4. 1% < EPG < 2% 5. EPG < 1% |

| Indicators | Code | Scale | |

|---|---|---|---|

| Payback time | Payback time is the amount of time that the investment will take to recover the initial cost, when the length of the investment time reaches a breakeven point. | F.1 | 1. PT > 12 y 2. 10 y < PT < 12 y 3. 7 y < PT < 10 y 4. 5 y < PT < 7 y 5. PT < 5 y |

| Maturity | Maturity is defined as the total duration of the project needed to achieve a zero NPV (IRR equal to cost of capital). | F.2 | 1. M > 25 y 2. 20 y < M < 25 y 3. 15 y < M < 20 y 4. 10 y < M < 15 y 5. M < 10 y |

| Internal Rate of Return | Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a specific project equal to zero. | F.3 | 1. IRR < 2% 2. 2% < IRR < 4% 3. 4% < IRR < 6% 4. 6% < IRR < 10% 5. IRR > 10% |

| Net Present Value on Investment | Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present. The NPV/investment ratio gives a measure of profitability of the project. | F.4 | 1. NPV < 10% 2. 10% < NPV < 20% 3. 20% < NPV < 30% 4. 30% < NPV < 40% 5. NPV > 40% |

| Debt–Service Coverage Ratio | Debt–Service Coverage Ratio (DSCR) is an indicator of the project’s ability to repay a debt. It is calculated as the ratio between the operative cash flows generated by the project and the cash flows for debt, lease or other obligations (debt service, both for interests and principal payment) due in one year. | F.5 | 1. DSCR < 1.1 2. 1.1 < DSCR < 1.2 3. 1.2 < DSCR < 1.3 4. 1.3 < DSCR < 1.4 5. DSCR > 1.4 |

| General Project Data | |

|---|---|

| Building Use/Typology | Office |

| Building construction year | 2001 |

| Building renovation year | 2019 |

| Net Floor Area NFA | 24,470 m2 |

| Net Volume NV | 97,000 m3 |

| Heating Degree Days (20 °C) | 1415 |

| Baseline | Energy Consumption * | Costs |

|---|---|---|

| Natural gas | 1,468,243 kWh/a | 49,920 € |

| Electricity | 3,286,000 kWh/a | 420,608 € |

| Energy consumption total. annual | 470,528 € | |

| O&M cost ** | 316,162 € | |

| Total. Annual (Energy consumption + O&M) | 786,690 € |

| Building Services | Costs | |

|---|---|---|

| Heating System | Heat Pump (water) | 190,000 € |

| Distribution system | Completed for pipes, fittings/valves/circulators/expansion vessel | 37,000 € |

| Mechanical ventilation system (VMC) | VMC (Air handler/Ventilation duct/Built-in components/Outlets/diffuser) | 112,500 € |

| Lights type | Low power consumption lights, LED | 403,787 € |

| Building Energy Management System (BEMS) | BEMS project by an expert certified UNI-EN 15232 | 190,000 € |

| Building automation system of: Lighting Thermal system (heating and cooling) Monitoring system of energy consumption | ||

| Photovoltaic system | Production: 43,200 kWh/year PV Installed: 38 kWp | 156,731 € |

| Other costs for the projects, management, experts, administrative procedures, mitigation measures, etc. | 215,991 € | |

| Total investment (VAT excluded) | 1,306,009 € | |

| Renovation Scenario | Energy Consumption * | Costs |

|---|---|---|

| Natural gas | 1,890,243 kWh/a | 64,268 € |

| Electricity | 1,806,000 kWh/a | 231,168 € |

| Energy consumption total. annual | 295,436 € | |

| O&M costs ** | 316,162 € | |

| Total. Annual (Energy consumption + O&M) | 611,598 € |

| Renovation Project | Renovation Measures | Mitigation Measures | Costs of Energy Savings | Investment | Payback Time | |

|---|---|---|---|---|---|---|

| (€) | (%) | (€) | (Year) | |||

| SCENARIO 1 | Heating, cooling, ventilation, lighting system | LEED, Energy performance monitoring | 175,092 € | 37% | 1,306,009 € | 7.46 |

| SCENARIO 2 | Heating, cooling, ventilation, lighting system | - | 175,092 € | 37% | 1,270,862 € | 7.26 |

| Damage | Energy Performance Gap | Payback timewith Technical Risks | |||

|---|---|---|---|---|---|

| Increased Investment | Increase of Energy Cost | ||||

| € | % | € | % | (Year) | |

| SCENARIO 1 | 3982 € | 0.30% | 3073 € | 1.04% | 7.57 |

| SCENARIO 2 | 7762 € | 0.61% | 7422 € | 2.51% | 7.74 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Andaloro, A.; Salvalai, G.; Fregonese, G.; Tso, L.; Paoletti, G. De-Risking the Energy Efficient Renovation of Commercial Office Buildings through Technical-Financial Risk Assessment. Sustainability 2022, 14, 1011. https://doi.org/10.3390/su14021011

Andaloro A, Salvalai G, Fregonese G, Tso L, Paoletti G. De-Risking the Energy Efficient Renovation of Commercial Office Buildings through Technical-Financial Risk Assessment. Sustainability. 2022; 14(2):1011. https://doi.org/10.3390/su14021011

Chicago/Turabian StyleAndaloro, Annalisa, Graziano Salvalai, Gabriele Fregonese, Linda Tso, and Giulia Paoletti. 2022. "De-Risking the Energy Efficient Renovation of Commercial Office Buildings through Technical-Financial Risk Assessment" Sustainability 14, no. 2: 1011. https://doi.org/10.3390/su14021011

APA StyleAndaloro, A., Salvalai, G., Fregonese, G., Tso, L., & Paoletti, G. (2022). De-Risking the Energy Efficient Renovation of Commercial Office Buildings through Technical-Financial Risk Assessment. Sustainability, 14(2), 1011. https://doi.org/10.3390/su14021011