Abstract

In many West African river basins, households regularly experience floods and the associated impacts. In the absence of widely accessible formal risk transfer mechanisms (e.g., insurance), households often have to cope with financial impacts. Only a few studies have explored the financial effects of floods on agriculture-dependent households in the region and the role formal and informal risk transfer plays in their mitigation. This study addresses this gap, explores flood impacts with financial implications for households, and researches the existing strategies to mitigate them. Moreover, it aims to better understand how different measures influence the recovery process. The study draws on primary data from a household survey (n = 744) in the Lower Mono River basin, combined with stakeholder workshops and semi-structured interviews, and applies a generalized linear model to the survey data. The results reveal four flood impact types with financial implications: agricultural, material, health, and trade. Moreover, a shortened recovery time is significantly associated with assistance from savings groups and cooperatives—groups originally not formed to help during floods. In light of the severe and frequent flood impacts, effective and publicly accepted adaptation measures are needed to enable favorable conditions for creating sustainable and accessible risk transfer mechanisms.

Keywords:

financial; flood impacts; households; risk transfer; coping; insurance; recovery; Togo; Benin 1. Introduction

In the past decades, flood events in West Africa have become increasingly devastating [1]. Numerous river basins in West Africa, such as the Niger, Volta, Oti, or Mono basins, are at high risk of flooding [2,3,4,5]. The population in these areas commonly experiences fatalities caused by flooding and is affected by widespread material damage, displacement, and interruption of livelihood activities [6,7,8,9]. Moreover, the Sixth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC) observed a trend of more frequent occurrences of river floods in West Africa since the 1980s and projected increased monsoon precipitation coupled with a delayed onset and retreat for the future [10]. Other trends that exacerbate the problem of floods in the region are settlement expansion into flood risk zones [11,12], deforestation through mangrove loss [13], and land-use change of large areas of forest and other naturalized areas into cropland or settlements [14]. Given the perennial reoccurrence of flood events in the area, new and more intensified flood risk management efforts are required [15].

Flood impacts in the region span across various categories, including damage to buildings, health impacts, loss of livelihoods and income, environmental degradation, displacement, lack of food and drinking water, interruption of social activities, and constrained mobility [16,17]. Generally, in various tropical countries, there is a lack of baseline/reference information with regard to impact and risk assessments, requiring many to resort to using existing (and low-cost) data [18,19,20]. Similarly, information on financial damages of flood events in West Africa is relatively sparse, and publicly accessible regional or national disaster inventories are lacking. In addition, other existing databases, such as EM-DAT, only register direct damage to property, crops, and livestock [21]. Addressing these practical gaps, a number of recent studies have started to explore the financial implications of flood impacts in the region and how they unfold at the household level. For example, Ajibade et al. [22] qualitatively assessed how flood impacts intersect with gender and socio-economic status at the household level. Afriyie et al. [23] explored the vulnerability of natural, physical, social, financial, and human assets to shocks such as floods and adaptation strategies in the broader sense from a livelihood perspective by carrying out focus group discussions. In addition, Kheradmand et al. [24] estimated the economic damages to households in terms of residential house damage in different dike height scenarios by combining flood hazard and asset maps. However, existing research has not yet determined how much the various dimensions of flood impacts (e.g., agricultural, health, business interruption, etc.) actually cost households.

One way to mitigate the financial impacts of flooding is through risk transfer, such as insurance [25,26]. Though case studies of flood risk management in West Africa recommend such risk transfer, it does not play a significant role yet in the region [16]. Currently, academic literature addressing risk transfer for floods generally focuses on formal mechanisms, such as insurance and public risk pools [26,27,28,29,30,31,32,33]; it pays limited attention to other forms of risk transfer. The academic literature addressing informal risk transfer arrangements in the context of floods is an exception to this. One example worth mentioning are experimentally formed risk-sharing groups in Bangladesh that showed that disaster-affected members were less likely to drop out of risk-sharing groups than non-affected members [34]. Moreover, a study found that households with at least one member being part of a savings group in Dar es Salaam, Tanzania, recovered faster financially than households without a member in such groups [35]. In reference to climate-related disasters in general, Hallegatte et al. [36] stated that poorer households often have access only to social protection mechanisms, such as government assistance and support from Non-Governmental Organizations (NGOs), in times of a disaster with larger severity, while richer households can access insurance or accumulate savings. Still, a relative sparseness of research that focuses on the context of floods can be observed. A reason for this could be the perceived inability of such arrangements to address large-scale events such as floods, which are likely to affect a major share of or even the entire risk-sharing community [37]. Nevertheless, existing flood risk-related research suggests the importance of mutual support activities in the response process after flood events in the West African region [16]. However, whether such support activities also go beyond reconstruction aid remains unclear. In addition, it is not clear whether these activities take place in the financial domain and can be classified as risk transfer mechanisms [16]. It is relevant to assess whether the existing ways of dealing with financial implications from flood impacts can significantly contribute to the financial recovery process. This analysis will indicate the current state of the risk transfer landscape and the necessity for and the feasibility of creating a potential flood insurance mechanism to complement the existing measures. As a consequence, this research will contribute to finding more sustainable ways of financial risk management in the research area.

To address to previously outlined research gaps, this study addresses which types of flood impacts cause financial consequences for households. Moreover, this study explores the measures through which financial consequences from flood impacts are mitigated as well as their contribution to the financial recovery process. Within those measures, the role of risk transfer is examined with a specific focus. We aimed to shed light on the need for a potential flood insurance product in the research area that considers flood impacts with financial implications and complements the established practices of addressing such impacts. The following research questions were addressed:

- (1)

- What are the flood impacts with financial implications for households?

- (2)

- What measures are available to households to address these impacts, and can they be classified as risk transfer?

- (3)

- How long do affected households take, on average, to recover financially from various types of flood impacts with financial implications?

- (4)

- What are the associations of existing measures with financial recovery, and what are the limitations of such measures?

We first provide background information about the current state-of-the-art on floods and risk transfer in the research area. Subsequently, we describe the methodological approach for data collection and analysis. Then, the results are presented in the order of the previously outlined research questions and discussed in relation to other academic literature. Finally we provide a concise take-home message derived from the discussion of the results.

2. Background

2.1. Risk Transfer

Risk transfer describes “shifting the financial consequences of particular risks from one party to another, whereby a household, community, enterprise or State authority will obtain resources from the other party after a disaster occurs, in exchange for ongoing or compensatory social or financial benefits provided to that other party” [38]. It can be distinguished from risk retention, external financing, and emergency assistance, and as an ex-ante instrument, it involves an agreement between parties before a disastrous event [39]. Risk transfer mechanisms are central to managing the financial implications of flood impacts [40] and can be either formal or informal [38]. While formal risk transfer mechanisms mostly come in the form of insurance contracts, catastrophe bonds, contingent credit facilities, or reserve funds, informal risk transfer occurs within networks of families or communities and involves sharing of gifts or credits between its members [38]. Such arrangements, sometimes referred to as risk sharing, are seen to be more context-specific, to entail fewer transaction costs, to be more flexible and affordable, to be based on trust, and to be adaptable to local conditions [35,37]. Table 1 shows an overview of the common aspects of risk transfer based on UNDRR and Cissé [38,39].

Table 1.

Aspects of risk transfer (based on UNDRR and Cissé [38,39]).

In the field of Disaster Risk Reduction, it is well known that despite extensive efforts in risk reduction, a certain level of residual risk will most likely exist as a baseline [41]. In some cases, this risk is chosen not to be addressed, due to, for example, the residual risk level being socially accepted or the costs of risk reduction being higher than the cost of the expected damage [42]. In flood-related research from developed economies, such debates mostly revolve around the implementation of structural control measures, their protection gaps and potential failure [43,44,45], as well as the coverage of such risks by insurance [46,47,48]. However, especially in the context of developing economies, efforts in flood risk reduction are not well developed, and the population is often exposed to a high level of risk, affecting their financial achievements, among other impacts [16]. Still, informal risk transfer mechanisms allow the exposed population in such areas to alleviate the financial impacts of disaster events at least to a certain extent [35,37]. In light of the projected climatic changes and subsequent extreme events, in particular, floods the West African region [10], the question remains whether such mechanisms can be sustainable in the long run.

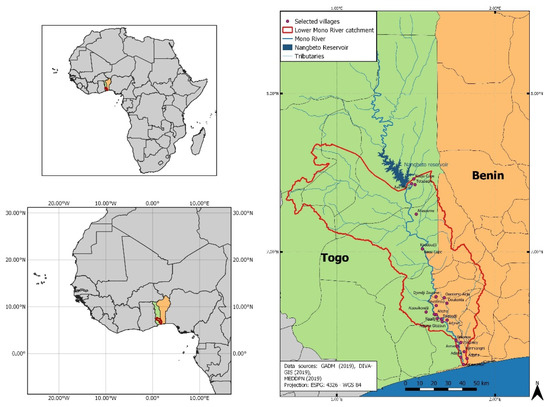

2.2. Case Study Area: Lower Mono River Basin

The Lower Mono River basin (LMRB), a transboundary river basin shared between Togo and Benin (Figure 1, has experienced flood events in both countries in the past decade, including in 2007 [49,50], 2010 [51,52], 2019 [53,54], 2021 [55,56]. Currently, floods in the basin have become such a problem that they occur almost on a yearly basis in varying intensities [57]. The hydrology of the LMRB was modified by the construction of the Nangbeto Dam in 1987 [57] for hydropower generation and as a water reservoir to be used for fishing and irrigation [58]. While the Dam was found to have a low influence on the regulation of floods, especially during times of peak flow [59], the periodic opening of the reservoir seems to have played an essential role in the generation of downstream floods, especially in the view of the affected population [54,60,61,62,63,64]. The precipitation maxima within the area are characterized by two peaks in May and October in the South of the basin and from May to September around the area of the Nangbeto reservoir [65]. Moreover, in the light of climate change, the annual maxima of daily precipitation in the area are expected to increase further, leading to a more substantial impact of heavy rainfall events on discharge within the river basin and thus to flood events of higher severity [5]. Apart from climatic changes, there are also other anthropogenic factors contributing to the flooding problem in the area, such as deforestation as well as the expansion of settlements, farmland, and infrastructure into exposed areas [57,66,67].

Figure 1.

Research area with villages selected for household survey.

The floods in the largely rural LMRB usually cause extensive damage, for example, to houses, infrastructure, public buildings, and human health, due to the flood water remaining in the living environment for some time [6,55,56]. Additionally, they affect the livelihoods and the productive assets of the population, who largely depend on agriculture as their primary livelihood source, followed by fishing, trading, palm oil production, and keeping livestock [66,68,69]. These impacts put an additional strain on the affected population’s finances, and they are often left to figure out ways of dealing with the flood impacts in the long term with limited resources [70], aside from disaster assistance and relief activities by the government and NGOs. In particular, financial damages that can be addressed with risk transfer mechanisms have gained increasing attention through the political momentum of the G7 InsuResilience Initiative and the subsequent InsuResilience Global Partnership [71]. The latter aims at raising the number of persons insured against climate and disaster shocks globally to 500 million by 2025 in the light of loss and damage experienced by climate change [72]. Despite the devastating impacts arising from floods in the region, the application of formal risk transfer mechanisms, such as insurance, for these impacts are not yet widely prevalent in West Africa in general [16], Togo [3], and Benin [73,74].

In the absence of widespread access to such formal risk transfer mechanisms, informal or partly informal mechanisms are more likely to fill the void. For example, support from social networks, in the form of providing emotional, financial, or material support, as well as access to money, food, shelter, and labor, for affected family members or friends have been found to play a crucial role in coping with and recovering from flood impacts in the West African region [16]. Similarly, for the Togolese part of the LMRB, Clubs des Mères (CM) were identified to have high importance in evacuating flood victims as well as in supporting their recovery process [57]. The CMs are organized by the Red Cross and are a well-known example of a women’s group, which, aside from their other support activities, possesses a solidarity fund that covers unforeseen health expenses on a loan basis [75]. Nevertheless, such arrangements could be unable to address large-scale events such as floods, which are likely to affect a large share of or even the entire risk-sharing community [37]. In this context, it is crucial to investigate the existing mechanisms, both formal and informal, to cope with financial flood impacts and showcase if they portray some form of risk transfer.

2.3. Data Collection and Analysis

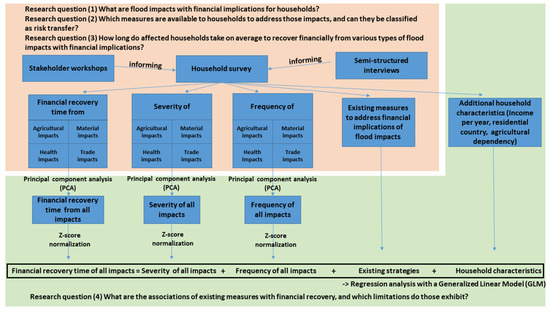

This study applied a mixed-methods approach to shape the quantitative data collection based on previously collected qualitative insights in the domain of financial coping strategies on the local level (Figure 2). Therefore, the study started out qualitatively, with stakeholder workshops and semi-structured interviews. Based on these, a household survey was carried out to further analyze the findings quantitatively.

Figure 2.

Overview of the selection of methods and their relation to the research questions.

2.3.1. Workshop/Semi-Structured Interviews

The process of data collection began with two virtual stakeholder workshops, inquiring about flood impacts with financial implications and the existing measures to address them. The workshops were held separately in Togo (11 participants) and Benin (14 participants) with participants from ministries, disaster management authorities, volunteer-based organizations, NGOs, Nangbeto Dam/Mono Basin authorities, community mayors, research institutions, and development cooperation institutions. Information was collected on the financial flood impacts prevalent in the research area and the existing mechanisms to deal with them. This information was collected using the online collaboration tools Mentimeter and Miro. In addition, 16 semi-structured interviews were conducted in the research area to complement this data and to prepare the survey data collection. Therefore, residents of flood-affected households were purposively selected to obtain their views on financial flood impacts and the existing ways of transferring these financial risks. We aimed to keep a balanced mixture of female and male interviewees in the semi-structured interviews with village residents.

2.3.2. Household Survey

Following these consultations, a household survey was conducted in the LMRB between March 2021 and April 2021. It provided data on the prevalence of flood impacts with financial implications and the existing mechanisms to recover from them across the LMRB in a quantitative manner. The LMRB was surveyed by dividing the research area into flood risk zones of low, medium, and high risk based on elevation data and proximity to the river. Then, 24 villages were selected across these flood-risk zones by considering reports on their flood affectedness (Figure 1).

Within the villages, respondent households were selected by taking a censored proportional sample based on the number of households in each village (11.2%). The random selection of households in the villages was made by instructing the interviewers to start at a central landmark and use a random interval and walking direction, until the end of the village was reached [76]. A household was interviewed if they were to some extent dependent on agriculture for their livelihood. The required sample size was determined to be 636 by applying a censored proportional sampling approach; this was exceeded, with 744 interviewees. The data collection through the questionnaire was administered on KoboToolBox and carried out together with a team of ten simultaneously deployed field assistants on mobile devices (tablets and mobile phones).

2.3.3. Principal Component Analysis

The advantage of a principal component analysis (PCA) is that it is able to reduce dimensionality and still preserve most of the variation in data [77]. Thus, the PCA is applied to the household survey dataset to consolidate the different dimensions of flood impacts with financial implications into one score. This is done to use the PCA score later in regression analysis and avoid the risk of overfitting the regression model [78]. The PCA yields the Eigenvector, the direction of maximum variance in the complete data, and is therefore a suitable way to objectively summarize the data into one parameter [79,80]. The PCA is performed separately for the respective indicators, collected in a household survey of flood impact severity, flood impact frequency, and the financial recovery time. As also shown in Figure 2, the PCA was applied on three different sets of variables, yielding three scores that summarized (1) the severity of flood impacts for all types of flood impacts, (2) the frequency of flood impacts for all types of flood impacts, and (3) the financial recovery time of households from all types of flood impacts (S1 and S2 in Supplementary Material). The PCA scores were then transformed into z-scores to make them comparable to each other and to enable using them in the same regression model.

2.3.4. Generalized Linear Regression Model

Subsequently, a generalized linear regression model (GLM) was applied to the household survey data to research the associations of existing measures with reducing or prolonging the financial recovery time of interviewed households in the LMRB. A GLM was selected over a structured equation model (SEM) because a sample must contain 10–15 events per predictor to avoid overfitting the regression model [81]. Thus, the obtained sample size would not have allowed this criterion in the case of an SEM or by considering further interactions between predictors. The model was built as a combination of predictive and causal modeling [78]. The considered aspect of causal modeling is the selection of variables for the model based on factual logic (Table 2, “reason for inclusion”). The considered aspect of predictive modeling was the attention to the significance of the results: the p-value.

Table 2.

Model inputs for the GLM.

In the GLM (Table 2), the financial recovery time of households was taken as a dependent variable. The following variables were selected as independent variables for the GLM: frequency of all impact types, severity of all impact types, existing strategies to deal with financial flood impacts, household income per year, level of agricultural dependency, and the residence country of the interviewed household (descriptive statistics for main variables in S1 in Supplementary Material). The model aimed to elaborate on which of the existing strategies already play an important role in the financial recovery of a household. The results of the GLM were visualized in a graph format, since it enabled the graphical depiction of the dimension and direction of the results [82]. An adjustment to the sampling design was applied in the GLM to make the results proportional to the number of households in the respective villages.

3. Results

3.1. Characteristics and Prevalence of Flood Impacts with Financial Implications on the Household Level in the LMRB

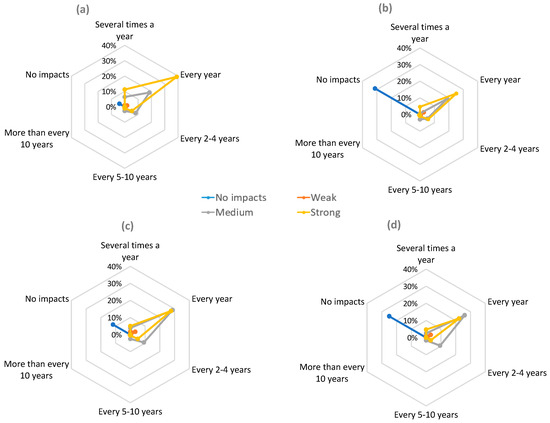

The results of the workshops and semi-structured interviews showed that flood impacts that financially affect households in the LMRB can be categorized into four broader categories (agricultural, material, health, and trade impacts). In the household survey, the interviewed households were also asked to self-report the frequency and severity of the financial impacts from these respective impact categories.

The first category comprised agricultural damages, particularly the loss and destruction of crops and plantations. With the occurrence of a damaging flood, the investment in agricultural work has been in vain. The households must therefore spend money to obtain food for themselves. It was also mentioned that most households primarily cultivate for self-consumption and secondarily for selling on the market. Therefore, as soon as the flood affects the fields, the households face problems covering their own food consumption properly, which affects their health and necessitates the purchase of food. In addition, they lose out on their invested money in the case they grow crops for the market. The loss of animals (such as poultry, sheep, or pigs) also translates into a loss of financial investment for the household. Agricultural impacts were the most prevalent in the study area, with 96.0% of households having experienced at least some form of such impacts over the last 20 years. In this period, agricultural impacts also happened every year for the majority (59.4%), and for some, even several times a year (18.7%) on average. Regarding the intensity of the impacts, the majority were of severe (56.6%) or medium (35.7%) intensity, while only a few households experienced weak (3.7%) or no agricultural impacts (4.0%). Figure 3a illustrates how the severity and frequency of agricultural impacts are interrelated.

Figure 3.

Frequency and severity of flood impacts with financial implications as reported in the household surveys (n = 744): (a) agricultural, (b) material, (c) health, and (d) trade impacts.

The second category comprised the material damages, particularly the damage or destruction of houses, as a result of flooding. In the case of a damaging flood event, the reconstruction or reinforcement of the foundation of the house may be necessary, which translates into incurred repair costs for the household by buying cement. Similarly, replacing lost (non-agricultural) personal material belongings and valuables after an impactful flood event is associated with costs. In the past 20 years, 68.8% of the interviewed households experienced some form of material impact within the study area. In this period, material impacts happened every year for a large share of households (46.7%) and every two to four years for some (11.4%) on average. The average severity of the material impacts over the last 20 years was severe (37.3%) or medium (27.4%) for most households. However, around a third of interviewed households did not experience material impacts (31.2%), while a minority experienced weak impacts (4.1%) on average. Figure 3b illustrates how the severity and frequency of material impacts are interrelated.

Thirdly, floods were mentioned to affect the health of household members by raising the likelihood of falling ill with malaria, diarrhea, or sore feet by walking through the flood waters, particularly for children. The subsequent payments for medical care or medication translate into a cost for the household. Health impacts were a widely prevalent category of flood impacts with financial implications, with 88.3% of interviewed households experiencing at least some form of such impacts over the past 20 years. A large share experienced these impacts every year (59.5%), some even several times a year (10.7%), while another share experienced them every two to four years (14.6%). The average severity of the health impacts was strong (38.1%) and medium (44.5%) for the interviewed households, while 5.7% experienced weak impacts. Figure 3c illustrates how the severity and frequency of health impacts are interrelated.

Finally, floods affect the trade activity of a household due to the damaging of stored agricultural or other manufactured products. Households also encounter difficulties of transporting the goods to the market due to inundated or damaged roads or even affected marketplaces. Thus, these types of impacts lead to lost income that would be generated otherwise. Impacts on trade were experienced by 75.1% of interviewed households over the last 20 years. A major share (51.6%) of interviewed households experienced impacts on trade activities once a year, on average, to at least some degree. Another share (13.4%) experienced them every two to four years, while only 1.7% experienced them every five to ten years. Regarding the severity of the events, the largest share of households experienced these impacts with strong (30.2%) and medium (39.7%) severity. In comparison, only 5.2% experienced them in weak severity. Figure 3d illustrates how the severity and frequency of trade impacts are interrelated.

3.2. Financial Coping Strategies

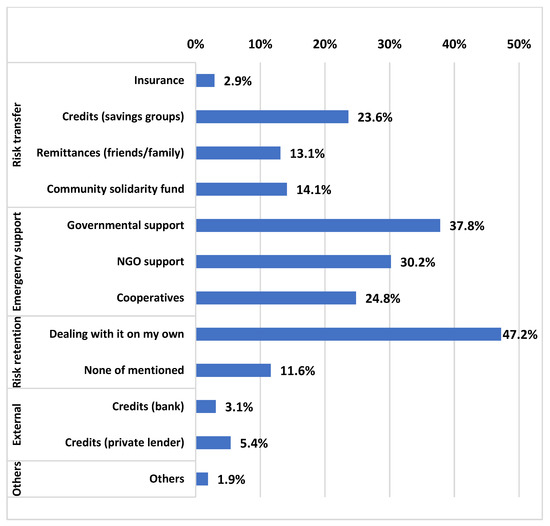

This study yielded categories of options among the population at risk to deal with the previously outlined flood impacts with financial implications (Figure 4). Respondents were able to select multiple responses regarding the options usually available to them. The existing practices are divided into risk transfer, emergency response, risk retention, and external sources of financing.

Figure 4.

Existing options at the household level to deal with flood impacts containing financial implications as reported in the household survey (multiple responses possible; n = 744).

Firstly, based on Table 1, some existing measures were identified as risk transfer, both formal and informal. As a formal example of risk transfer, insurance (2.9%) can be mentioned, since it has a legal framework that explicitly regulates its business. The low prevalence of insurance illustrates the currently minor role of formal risk transfer mechanisms in addressing the financial impacts of floods in the LMRB. Concerning informal risk transfer mechanisms, credits from savings groups (roundtable savings groups/tontines/clubs de mères) frequently were mentioned (23.6%). However, these groups are usually not formed with the objective to provide assistance in times of flooding. Instead, their aim is to save for investments of their members in the private domain (e.g., education, construction, purchases). In some emergency cases, it is possible for households to obtain credits from such groups, though they usually have to be paid back within a few months. This aspect is underscored by 58.4% of interviewed households being members of savings groups in general; however, only 23.6% were able to receive some form of financial assistance after experiencing a harmful flood event, leading to incurring expenses. Still, due to the aspects of pooling financial resources, mutual exchanges, and leniency in times of being flood-affected, it is perceived as a form of risk transfer in this study. Likewise, community solidarity funds (14.1%) were reported to exist in some villages to support cultural activities or funerals of community members. In some cases of having disproportionally highly affected community members, a few of them were able to receive some form of financial assistance from the fund. Thus, these funds can be seen as risk transfer in this study because they act as a form of risk pool on the village level based on mutual exchanges that financially support flood-affected village members under certain circumstances, despite not being formed for that purpose. Moreover, remittances from family or friends (13.1%) appeared as another form of informal risk transfer, though at a lower frequency. This is categorized as risk transfer in this study because these transactions are mostly informal expectations between family members or friends of assistance in times of need, with the aspiration of being reciprocal.

Furthermore, another group of existing measures that could be observed as mitigating the financial implications of flood impact in the LMRB was classified as emergency assistance. Prevalent measures from that category were the support from governmental actors (37.8%) and NGOs (30.2%). These two measures were not classified as risk transfer due to the fact that they do not contain the aspect of beneficiaries exchanging benefits to the party that provides coverage. In some cases, the support came in the form of cash transfer, while in others, it did not but entailed the provision of food, shelter, or medication as emergency response. In any case, this assistance was taken into account in this study since it avoided, or compensated for, potential financial expenses of households. Moreover, a further prevalent type of emergency assistance came in cooperatives (24.8%). In the study area, cooperatives were understood as groups of farmers who organize themselves for mutual help to work in the field or in fishing. Generally, cooperatives are not formed to provide assistance in times of flooding. However, in some cases, members assist each other in rescuing material goods in anticipation of a flood and in the restoration process of the agricultural activities after a flood, which is usually associated with financial expenses. As a consequence, cooperatives were not classified as risk transfer because they do not directly involve the provision of financial support and are not formed with the intent of providing support in times of flooding, yet they do so due to the absence of other measures.

A very prevalent category of measures to address the financial implications of flood impacts can be seen as risk retention. In the household survey, the most frequent response of interviewed households was to deal with the financial implications of flood impacts using their own means (47.2%). This option comprised using one’s own savings, selling material belongings, or resorting to generate alternative forms of income. It is also worth noting that 11.6% indicated not having any means, not even their own, to deal with the financial implications of flood impacts. Other external and less prevalent sources of credit that go beyond the networks of family or community were credits from a private lender (5.4%) and credits from formal providers such as banks (finance institutions) (3.1%).

3.3. Financial Recovery Times of Households from Flood Impacts

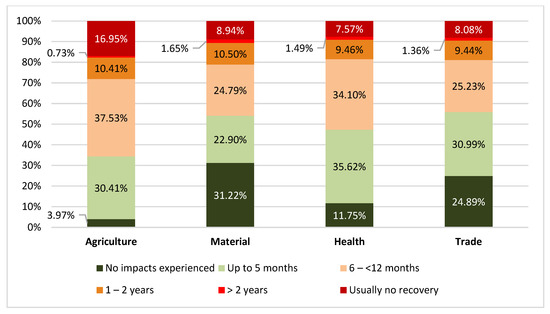

Another aspect researched in the household survey was the time that households needed on average to recover financially from the four types of impacts identified as having financial implications (agricultural, material, health, trade; Figure 5). Recovery was defined as the moment at which households perceived themselves as having recovered the financial expenses that they incurred through the impacts of the flood. Regarding agricultural impacts, around 70% recovered within one year or less or did not experience such impacts. In contrast, around 80% of the households recovered within one year for the other three types of impacts. Moreover, shares of households take on average longer than one year to recover (11.14% for agricultural; 12.15% for material; 10.95% for health; and 10.8% for trade impacts). In addition, it is important to mention that some households indicated that they usually do not recover from the financial implications of flood events that they experience (16.95% for agricultural; 8.94% for material; 7.57% for health; and 8.08% for trade impacts).

Figure 5.

Average financial recovery time of households from flood impacts with financial implications by impact category as reported in the household surveys (n = 744).

3.4. Limitations of Existing Financial Coping Strategies

In order to address the associations of existing measures with financial recovery, and the limitations they exhibit, a regression analysis with a generalized linear model (GLM) was performed (Table 3). The R-squared value of the GLM amounted to 0.2700, portraying a strong value of explanatory power for the variance in financial recovery time.

Table 3.

GLM results.

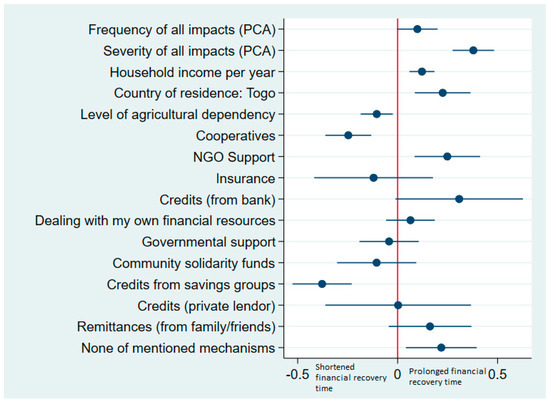

The results of the regression analysis (Figure 6) illustrated the influence of the frequency and severity of (Section 3.1) and the existing strategies to deal with (Section 3.2) flood impacts with financial implications on shortening or prolonging the financial recovery time. Additionally, the influence of factors such as the level of household income, residence country, and the level of agricultural dependency was tested. If the coefficient is a positive value, the presence of the variable is associated with a household taking longer to recover financially. If the coefficient is a negative value, the presence of the variable is associated with a household taking less time to recover financially. The findings are statistically significant for all variables whose p-values are below 0.05 (if the blue and red lines in Figure 6 do not intersect). The detailed GLM results can also be found in Table 3.

Figure 6.

Association of factors with financial recovery time from flood impacts (GLM results).

The analysis revealed significant influences of the following variables. Firstly, the aggregated severity of all four types of flood impacts with financial implications had a strong and highly significant association with a prolongation of the financial recovery time, which is an intuitive finding. However, this could not be found for the aggregated frequency of all four types of flood impacts with financial implications. Secondly, it was shown that the household income per year is slightly yet significantly associated with a prolongation of the financial recovery time. Thirdly, it was found that residing in Togo is significantly associated with a prolongation of the financial recovery time of households. Moreover, it was shown that the level of agricultural dependency is slightly yet significantly associated with a decrease in households’ financial recovery time. Regarding the influence of the existing strategies (outlined in Section 3.2), it became apparent that both cooperatives and credits from savings groups have a strong and highly significant association with a shortened financial recovery time of households. Interestingly, NGO support was associated with a strong and highly significant prolongation of financial recovery time. However, this observation could be explained by NGOs mostly focusing their work on highly flood-affected people. Finally, cases where no means were available to a household were significantly associated with a longer financial recovery time, which is an intuitive finding.

No statistically significant results could be produced for insurance, using one’s own resources, governmental support, community solidarity funds, credits from a private lender, credits from banks, and remittances from family or friends. However, it is also possible that the observed associations of existing measures with a shortened or prolonged financial recovery time are due to predominantly being drawn upon in times of high or low flood severity, respectively (e.g., credits from savings groups/cooperatives in times of low frequency/severity or NGO support in times of high frequency/severity; see S3 in Supplementary Material for separate GLMs assessing the individual relationship between flood impact frequency and severity with the remaining independent variables).

4. Discussion

The reported frequency and severity of flood impacts with financial implications that the study found in the LMRB can be seen as too high to be suitable for creating a flood insurance mechanism without further efforts in flood risk reduction. Consequently, a large share of the population at risk in the LMRB would not be able to afford an insurance mechanism. This is due to the fact that this area experiences flood impacts every year or, in some cases, several times a year; thus, residents would potentially be charged high premiums [40]. Under such conditions, flood insurance would not be economically attractive for insurance companies either. Consequently, concerted adaptation efforts are needed to substantially reduce the recurrence period of flood impacts for the majority of the basin population to better fulfill the conditions of insurability [40]. This is also envisaged in risk layering approaches that recommend applying adaptation measures in the case of damages frequently appearing [39,83]. Risk transfer approaches are well suited for low-frequency, high-impact events but not for events that occur in high frequency [84].

Furthermore, the study found that the existing options to deal with the financial implications of flood impacts rather seldomly take the shape of risk transfer. The most common strategies in LMRB are private risk retention and emergency relief from governmental actors or NGOs. This finding is in agreement with Hallegatte et al. [36], who stated that poorer households often only have access to social protection mechanisms, such as government assistance and NGO support, in times of a disaster with larger severity. In comparison, richer households can better access formal mechanisms such as insurance [36]. In essence, the results show that, currently, there are no mechanisms in place that are explicitly designed to alleviate the financial implications of flood impacts in the LMRB. It appears as if locally led development initiatives (cooperatives, savings groups, solidarity funds and, in particular, private financial resources) have to serve as means of financial coping in times of experiencing flood impacts, which they were not originally designated for. It can also be assumed that the high percentage of households using their own financial resources can be explained by a lack of other options rather than choosing this route. As a consequence, at the household and community level in the LMRB, many are constrained in their financial achievements in the event of a harmful flood event because they must use resources that were not intended for such a purpose. This point is further illustrated by those interviewed households indicating that they took longer than one year to recover or never recovered from the financial implications of flood impacts. In a context in which floods have become a yearly occurrence, this situation is not sustainable. Such flood impacts are bound to repeatedly erode their ability to cope with the impacts over time.

In addition, the study found that if a household was able to access support from a cooperative or receive a credit from a savings group, it was also strongly associated with a shorter financial recovery time. The latter finding corroborates the result of Panman et al. [35], who showed that flood-affected households in Dar es Salaam that had at least one member in a savings group recovered faster than non-members. Moreover, access to credits from savings groups increased only marginally across income groups in this study. The finding is interesting with regard to Hallegatte et al. [36], who stated that savings or credit is often not an option for poorer households. Nevertheless, the local structure of the mechanism seems to enable broader access and flexibility, albeit entailing smaller amounts than from conventional credit providers. More qualitative research is needed to explore the ways and criteria under which such support takes place in cooperatives and savings groups, since only a third of the households that were members in savings groups could access some kind of financial assistance in times of flooding. It should be pointed out that savings groups and cooperatives were not set up to provide assistance to their members in times of flooding in the research area. However, they should be of high interest in the case of designing a formal risk transfer mechanism to act as potential components of a scheme and even be engaged in prevention and awareness-raising activities, as also suggested by Panman et al. [35]. In addition, even in established flood insurance systems such as the National Flood Insurance Programme (NFIP; USA), the role of continuous awareness-raising for risk is seen as crucial to keep people engaged in actively subscribing to the program over time [85]. It could be worth exploring how a potential formal insurance product would act as a replacement or complementary mechanism to existing informal practices of risk sharing [86,87]. The role of mobile payment technology in informal risk sharing [88] could be of importance in this context as well. In addition, it could be of relevance to conduct such a study in a comparative manner between urban and rural contexts, regarding potential differences in disaster vulnerability [89].

This study presents some limitations. Firstly, the four identified categories of flood impacts with financial implications might be the most prevalent ones that were found in the LMRB. However, it cannot be ruled out that there are further ways in which flood impacts cause a financial need in a household (such as the cost of ecosystem-related losses/environmental degradation), given the diversity of flood impacts in the West African region [16]. Furthermore, this study bears the limitation of working with self-reported data from flood-affected households on flood frequency and severity as well as the respective impacts. Therefore, care has to be taken when interpreting the data, as the data might slightly differ from data from more objective sources due to potential perception bias. However, this approach was necessary to be able to explore the topic in the area due to the absence of other hydrological databases or disaster impact inventories. In addition, this study bears the limitation of potentially overlooking unknown confounders in the GLM as well as only showing plausible but not causal relationships due to being an observational study. Another useful angle of approaching the topic would have been to perform a panel study in which the same households were interviewed at several points in time. In that way, the long-term effect of certain coping strategies on financial well-being could have been better assessed.

Future research in the LMRB also needs to generate reliable recommendations for adaptation measures while keeping in mind the level of acceptance of those measures among the population at risk. If effective adaptation measures are implemented and insurance is pursued subsequently at some point, it will be essential to explore the understanding, trust, and willingness to buy a potential product among the population regarding such schemes due to the low level of previous exposure to insurance. In addition, several methods to increase coverage could be drawn upon from the NFIP context, such as opt-out designs, mandatory offers, community policies, and low-income voucher programs [90]. Furthermore, another aspect to be considered and drawn upon from the NFIP is to consider the ways in which a potential insurance mechanism has redistributional effects in making lower-income households receive a larger share of the payouts [91]. However, it will also be crucial to learn from factors of success and failure from other microinsurance schemes targeting low-income earners and to carefully balance the components of a potential scheme in terms of humanitarian intervention and business venture [92]. Moreover, the findings of this study could impact disaster databases such as EM-Dat in terms of collecting impact data in a more encompassing way that goes beyond direct damages [21]. The financial burdens on a household level arising from a disaster could be considered. However, a consensus for a standardized methodology for post-disaster needs assessments would be required to generate the required data. Thus, further research will be needed to provide additional empirical insights to enrich the perspective gained from this study.

5. Conclusions

This study shows that flood impacts have diverse financial implications, and innovative risk transfer approaches are required to address them. However, as current levels of impact frequency and severity show, effective adaptation measures are necessary for the LMRB to fulfill insurability criteria. In addition, there are currently no formal risk transfer mechanisms in place in the LMRB that were set up to help in times of flooding. In the absence of other mechanisms, locally led development initiatives (cooperatives, savings groups, community solidarity funds) have to step in even though they were not formed for that purpose. This situation erodes the financial achievements of the affected population and prevents them from recovering financially from flood impacts. While the current recurrence period of flood damages does not favor the direct implementation of an insurance mechanism, the setting up of an appropriate risk transfer instrument, adapted to the local context and involving established local actors, is necessary for the long term. Therefore, the role of cooperatives and savings groups in the financial recovery process should be explored further. These groups appear to be relevant actors closely aligned to the local population, and they can be potentially integrated into an innovative insurance/risk transfer scheme. Such approaches could address the residual risk that remains after the implementation of effective adaptation measures that manage to reduce the reoccurrence period of flood impacts. To achieve progress in this area, this study finishes with a strong recommendation for further research in the areas of generating reliable recommendations for adaptation measures and exploring the level of interest of the population regarding potential insurance schemes and the trust of and experience with such products. Research on the latter aspects will shed more light on the suitability of insurance in a “smart mix” of adaptation measures from a different perspective.

Supplementary Materials

The following supporting information can be downloaded at: https://www.mdpi.com/article/10.3390/su14148433/s1, Supplementary file S1: descriptive statistics for the main input variables of the GLM; Supplementary file S2: principal component analyses; Supplementary file S3: separate GLM for the relationship between the frequency/severity of impacts and the remaining independent variables.

Author Contributions

Conceptualization, S.W., J.R. and M.S.; methodology, S.W., S.T. and N.I.P.D.; formal analysis, S.W.; investigation, S.W., S.T. and N.I.P.D.; resources, S.W., S.T. and N.I.P.D.; data curation, S.W., S.T. and N.I.P.D.; writing—original draft preparation, S.W.; writing—review and editing, S.W., S.T., N.I.P.D., M.H., M.S. and J.R.; visualization, S.W. and M.H.; supervision, J.R. and M.S.; project administration, S.W., S.T. and N.I.P.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the German Federal Ministry for Education and Research (BMBF) through the CLIMAFRI project (grant number 01LZ1710A-E). The APC was funded by the Open Access Fund of the University of Bonn.

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki, and approved by the Institutional Review Board of the Center for Development Research (ZEF) (protocol code 1a_21 11/02/2021).

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Acknowledgments

The authors would like to acknowledge the participants of the stakeholder workshops and the interviewees of the semi-structured interviews and the household survey in the Lower Mono River catchment. In addition, the authors would like to thank the team of field assistants that helped in carrying out the household survey data collection.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

References

- Badou, F.D.; Hounkpè, J.; Yira, Y.; Ibrahim, M.; Bossa, A.Y. Increasing devastating flood events in West Africa: Who is to blame? In Regional Climate Change Series: Floods; Adegoke, J., Sylla, M.B., Bossa, A.Y., Ogunjobi, K., Adounkpe, J., Eds.; WASCAL Publishing: Accra, Ghana, 2019; pp. 84–90. [Google Scholar]

- Aich, V.; Koné, B.; Hattermann, F.; Paton, E. Time Series Analysis of Floods across the Niger River Basin. Water 2016, 8, 165. [Google Scholar] [CrossRef]

- Komi, K.; Amisigo, B.; Diekkrüger, B. Integrated Flood Risk Assessment of Rural Communities in the Oti River Basin, West Africa. Hydrology 2016, 3, 42. [Google Scholar] [CrossRef]

- Komi, K.; Amisigo, B.; Diekkrüger, B.; Hountondji, F. Regional Flood Frequency Analysis in the Volta River Basin, West Africa. Hydrology 2016, 3, 5. [Google Scholar] [CrossRef]

- Amoussou, E.; Awoye, H.; Totin Vodounon, H.S.; Obahoundje, S.; Camberlin, P.; Diedhiou, A.; Kouadio, K.; Mahé, G.; Houndénou, C.; Boko, M. Climate and Extreme Rainfall Events in the Mono River Basin (West Africa): Investigating Future Changes with Regional Climate Models. Water 2020, 12, 833. [Google Scholar] [CrossRef]

- Floodlist. Togo and Benin—Mono River Flooding Affects 50,000. Available online: https://floodlist.com/africa/togo-benin-mono-river-floods-october-november-2019 (accessed on 30 September 2021).

- Floodlist. Togo—Thousands Affected by Oti River Floods in North. Available online: https://floodlist.com/africa/togo-oti-river-floods-october-2020 (accessed on 30 September 2021).

- Floodlist. West Africa—Floods Hit Burkina Faso and Northern Ghana. Available online: https://floodlist.com/africa/west-africa-burkinafaso-ghana-september-2020 (accessed on 30 September 2021).

- Floodlist. West Africa—More Floods in Niger, Death Toll Rises in Burkina Faso. Available online: https://floodlist.com/africa/floods-niger-burkinafaso-september-2020 (accessed on 30 September 2021).

- Masson-Delmotte, V.; Zhai, P.; Pirani, A.; Connors, S.L.; Péan, C.; Berger, S.; Caud, N.; Chen, Y.; Goldfarb, L.; Gomis, M.I.; et al. Summary for Policymakers. In Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; IPCC, Ed.; Cambridge University Press: Cambridge, UK, 2021. [Google Scholar]

- Tiepolo, M.; Galligari, A. Urban expansion-flood damage nexus: Evidence from the Dosso Region, Niger. Land Use Policy 2021, 108, 105547. [Google Scholar] [CrossRef]

- Güneralp, B.; Güneralp, İ.; Liu, Y. Changing global patterns of urban exposure to flood and drought hazards. Glob. Environ. Chang. 2015, 31, 217–225. [Google Scholar] [CrossRef]

- Padonou, E.A.; Gbaï, N.I.; Kolawolé, M.A.; Idohou, R.; Toyi, M. How far are mangrove ecosystems in Benin (West Africa) conserved by the Ramsar Convention? Land Use Policy 2021, 108, 105583. [Google Scholar] [CrossRef]

- Asenso Barnieh, B.; Jia, L.; Menenti, M.; Zhou, J.; Zeng, Y. Mapping Land Use Land Cover Transitions at Different Spatiotemporal Scales in West Africa. Sustainability 2020, 12, 8565. [Google Scholar] [CrossRef]

- Okoye, C. Risk Management Options for Flood Mitigation in West Africa. Available online: https://futureafricaforum.org/2020/06/11/risk-management-options-for-flood-mitigation-in-west-africa/ (accessed on 28 September 2021).

- Wagner, S.; Souvignet, M.; Walz, Y.; Balogun, K.; Komi, K.; Kreft, S.; Rhyner, J. When does risk become residual? A systematic review of research on flood risk management in West Africa. Reg. Environ. Chang. 2021, 21, 84. [Google Scholar] [CrossRef]

- Yazdani, M.; Mojtahedi, M.; Loosemore, M.; Sanderson, D. A modelling framework to design an evacuation support system for healthcare infrastructures in response to major flood events. Prog. Disaster Sci. 2022, 13, 100218. [Google Scholar] [CrossRef]

- Quesada-Román, A. Flood risk index development at the municipal level in Costa Rica: A methodological framework. Environ. Sci. Policy 2022, 133, 98–106. [Google Scholar] [CrossRef]

- Granados-Bolaños, S.; Quesada-Román, A.; Alvarado, G.E. Low-cost UAV applications in dynamic tropical volcanic landforms. J. Volcanol. Geotherm. Res. 2021, 410, 107143. [Google Scholar] [CrossRef]

- Pinos, J.; Quesada-Román, A. Flood Risk-Related Research Trends in Latin America and the Caribbean. Water 2022, 14, 10. [Google Scholar] [CrossRef]

- EM-Dat. The Emergency Events Database—Universite Catholique de Louvain (UCL). Available online: https://public.emdat.be/ (accessed on 28 September 2021).

- Ajibade, I.; McBean, G.; Bezner-Kerr, R. Urban flooding in Lagos, Nigeria: Patterns of vulnerability and resilience among women. Glob. Environ. Chang. 2013, 23, 1714–1725. [Google Scholar] [CrossRef]

- Afriyie, K.; Ganle, J.K.; Santos, E. ‘The floods came and we lost everything’: Weather extremes and households’ asset vulnerability and adaptation in rural Ghana. Clim. Dev. 2018, 10, 259–274. [Google Scholar] [CrossRef]

- Kheradmand, S.; Seidou, O.; Konte, D.; Barmou Batoure, M.B. Evaluation of adaptation options to flood risk in a probabilistic framework. J. Hydrol. Reg. Stud. 2018, 19, 1–16. [Google Scholar] [CrossRef]

- Haer, T.; Botzen, W.J.W.; Aerts, J.C.J.H. Advancing disaster policies by integrating dynamic adaptive behaviour in risk assessments using an agent-based modelling approach. Environ. Res. Lett. 2019, 14, 44022. [Google Scholar] [CrossRef]

- Mai, T.; Mushtaq, S.; Reardon-Smith, K.; Webb, P.; Stone, R.; Kath, J.; An-Vo, D.-A. Defining flood risk management strategies: A systems approach. Int. J. Disaster Risk Reduct. 2020, 47, 101550. [Google Scholar] [CrossRef]

- Treby, E.J.; Clark, M.J.; Priest, S.J. Confronting flood risk: Implications for insurance and risk transfer. J. Environ. Manag. 2006, 81, 351–359. [Google Scholar] [CrossRef]

- Surminski, S.; Oramas-Dorta, D. Flood insurance schemes and climate adaptation in developing countries. Int. J. Disaster Risk Reduct. 2014, 7, 154–164. [Google Scholar] [CrossRef]

- Jongman, B.; Hochrainer-Stigler, S.; Feyen, L.; Aerts, J.C.J.H.; Mechler, R.; Botzen, W.J.W.; Bouwer, L.M.; Pflug, G.; Rojas, R.; Ward, P.J. Increasing stress on disaster-risk finance due to large floods. Nat. Clim. Chang. 2014, 4, 264–268. [Google Scholar] [CrossRef]

- Thieken, A.H.; Kienzler, S.; Kreibich, H.; Kuhlicke, C.; Kunz, M.; Mühr, B.; Müller, M.; Otto, A.; Petrow, T.; Pisi, S.; et al. Review of the flood risk management system in Germany after the major flood in 2013. Ecol. Soc. 2016, 21, 51. [Google Scholar] [CrossRef]

- Hochrainer-Stigler, S.; Linnerooth-Bayer, J.; Lorant, A. The European Union Solidarity Fund: An assessment of its recent reforms. Mitig. Adapt. Strateg. Glob. Chang. 2017, 22, 547–563. [Google Scholar] [CrossRef]

- Prettenthaler, F.; Albrecher, H.; Asadi, P.; Köberl, J. On flood risk pooling in Europe. Nat. Hazards 2017, 88, 1–20. [Google Scholar] [CrossRef]

- Kron, W.; Eichner, J.; Kundzewicz, Z.W. Reduction of flood risk in Europe—Reflections from a reinsurance perspective. J. Hydrol. 2019, 576, 197–209. [Google Scholar] [CrossRef]

- Islam, A.; Leister, C.M.; Mahmud, M.; Raschky, P.A. Natural disaster and risk-sharing behavior: Evidence from rural Bangladesh. J. Risk Uncertain 2020, 61, 67–99. [Google Scholar] [CrossRef]

- Panman, A.; Madison, I.; Kimacha, N.N.; Falisse, J.-B. Saving Up for a Rainy Day? Savings Groups and Resilience to Flooding in Dar es Salaam, Tanzania. Urban Forum 2021, 33, 13–33. [Google Scholar] [CrossRef]

- Hallegatte, S.; Bangalore, M.; Bonzanigo, L.; Fay, M.; Kane, T.; Narloch, U.; Rozenberg, J.; Treguer, D.; Vogt-Schilb, A. Shock Waves: Managing the Impacts of Climate Change on Poverty; World Bank Publications: Washington, DC, USA, 2016; Available online: https://documents1.worldbank.org/curated/en/260011486755946625/pdf/ShockWaves-FullReport.pdf (accessed on 24 January 2022).

- Germanwatch & MCII. Climate Risk Insurance and Informal Risk-Sharing: A Critical Literature Appraisal. Available online: https://climate-insurance.org/wp-content/uploads/2020/05/Climate_risk_insurance_and_ISRA_Discussion_Paper_No_4_FINAL-2.pdf (accessed on 30 September 2021).

- UNDRR. Risk Transfer: Terminology. Available online: https://www.undrr.org/terminology/risk-transfer (accessed on 30 September 2021).

- Cissé, J.D. Climate and Disaster Risk Financing Instruments: An Overview; United Nations University Institute for Environment and Human Security: Bonn, Germany, 2021; Available online: https://climate-insurance.org/wp-content/uploads/2021/05/Climate-and-Disaster-Risk-Financing-Instruments.pdf (accessed on 30 January 2022).

- Radermacher, R.; Dror, I.; Noble, G. Challenges and strategies to extend health insurance to the poor. In Protecting the Poor: A Microinsurance Compendium; Churchill, C., Ed.; Munich Re Foundation: Munich, Germany, 2006; pp. 66–93. [Google Scholar]

- Schinko, T.; Mechler, R.; Hochrainer-Stigler, S. The Risk and Policy Space for Loss and Damage: Integrating Notions of Distributive and Compensatory Justice with Comprehensive Climate Risk Management. In Loss and Damage from Climate Change: Concepts, Methods and Policy Options, Climate Risk Management, Policy and Governance; Mechler, R., Bouwer, L.M., Schinko, T., Surminski, S., Linnerooth-Bayer, J., Eds.; Springer: Cham, Switzerland, 2019; pp. 83–110. [Google Scholar]

- Bouwer, L.M. Observed and Projected Impacts from Extreme Weather Events: Implications for Loss and Damage. In Loss and Damage from Climate Change: Concepts, Methods and Policy Options, Climate Risk Management, Policy and Governance; Mechler, R., Bouwer, L.M., Schinko, T., Surminski, S., Linnerooth-Bayer, J., Eds.; Springer: Cham, Switzerland, 2019; pp. 63–82. [Google Scholar]

- Ridolfi, E.; Di Francesco, S.; Pandolfo, C.; Berni, N.; Biscarini, C.; Manciola, P. Coping with Extreme Events: Effect of Different Reservoir Operation Strategies on Flood Inundation Maps. Water 2019, 11, 982. [Google Scholar] [CrossRef]

- Tourment, R.; Beullac, B.; Poulain, D. Management and Safety of Flood Defense Systems. In Floods; Vinet, F., Ed.; Elsevier: Amsterdam, The Netherlands, 2017; pp. 31–44. ISBN 9781785482694. [Google Scholar]

- Pinter, N.; Huthoff, F.; Dierauer, J.; Remo, J.W.; Damptz, A. Modeling residual flood risk behind levees, Upper Mississippi River, USA. Environ. Sci. Policy 2016, 58, 131–140. [Google Scholar] [CrossRef]

- Christophers, B. The allusive market: Insurance of flood risk in neoliberal Britain. Econ. Soc. 2019, 48, 1–29. [Google Scholar] [CrossRef]

- Surminski, S.; Eldridge, J. Flood insurance in England—An assessment of the current and newly proposed insurance scheme in the context of rising flood risk. J. Flood Risk Manag. 2017, 10, 415–435. [Google Scholar] [CrossRef]

- Thomas, A.; Leichenko, R. Adaptation through insurance: Lessons from the NFIP. Int. J. Clim. Chang. Strateg. Manag. 2011, 3, 250–263. [Google Scholar] [CrossRef]

- UN OCHA. OCHA Natural Disaster Bulletin: N° 8/Octobre 2007. Available online: https://reliefweb.int/sites/reliefweb.int/files/resources/0CDEFF8F9C8A732185257392005B3B60-Full_Report.pdf (accessed on 10 July 2021).

- UN OCHA. West Africa—Floods: As of 27 September 07. Available online: https://reliefweb.int/sites/reliefweb.int/files/resources/2A3EBB3602FF36418525736400536822-ocha_FL_wa070927.pdf (accessed on 10 July 2021).

- United Nations. Bénin: Les Inondations Continuent, L’aide Parvient Aux Sinistrés. Available online: https://news.un.org/fr/story/2010/11/200062-benin-les-inondations-continuent-laide-parvient-aux-sinistres (accessed on 10 May 2021).

- United Nations Economic Commission for Africa. Rapport D’evaluation Sur L’intégration et la Mise en Oeuvre des Mesures de Réduction des Risques de Catastrophe au Togo. Available online: https://archive.uneca.org/sites/default/files/uploaded-documents/Natural_Resource_Management/drr/drr-in-togo_french_final.pdf (accessed on 10 May 2021).

- Vert Togo. Togo/Inondations: Le Débordement du Fleuve du Mono Fait un Mort à Klikamé. Available online: https://vert-togo.com/togo-inondations-le-debordement-du-fleuve-du-mono/ (accessed on 10 May 2021).

- Hounkpêvi, A.F. URGENT—Débordement du Fleuve Mono: 15 Villages Sous L’eau à Athiémé. Available online: http://lautrefigaro.over-blog.com/2019/10/urgent-debordement-du-fleuve-mono-15-villages-sous-l-eau-a-athieme.html (accessed on 10 May 2021).

- Vigan, D.C. Débordement du Fleuve Mono: Au Moins Trois Communes en Proie Aux Inondations. Available online: https://lanation.bj/debordement-du-fleuve-mono-au-moins-trois-communes-en-proie-aux-inondations/ (accessed on 10 July 2021).

- Agence Bénin Presse. Environnement/Près de 70,000 Populations Affectées Par L’inondation du Fleuve Mono Dans les Communes D’ATHIÉMÉ et de Grand-Popo Selon la PDRRC-ACC. Available online: https://www.agencebeninpresse.info/web/depeche/63/pres-de-70-000-populations-affectees-par-l-inondation-du-fleuve-mono-dans-les-communes-d-athieme-et-de-grand-popo-selon-la-pdrrc (accessed on 10 July 2021).

- Ntajal, J.; Lamptey, B.L.; Mahamadou, I.B.; Nyarko, B.K. Flood disaster risk mapping in the Lower Mono River Basin in Togo, West Africa. Int. J. Disaster Risk Reduct. 2017, 23, 93–103. [Google Scholar] [CrossRef]

- African Development Bank. Benin/Togo Nangbeto Hydroelectric Dam Project Performance Evaluation Report (PPER). Available online: https://www.afdb.org/en/documents/document/multinational-nangbeto-hydroelectric-dam-benin-togo-9679 (accessed on 10 June 2021).

- Amoussou, E.; Tramblay, Y.; Totin, H.S.; Mahé, G.; Camberlin, P. Dynamique et modélisation des crues dans le bassin du Mono à Nangbéto (Togo/Bénin). Hydrol. Sci. J. 2014, 59, 2060–2071. [Google Scholar] [CrossRef]

- Ntajal, J.; Lamptey, B.L.; Mianikpo Sogbedjic, J.; Kpotivid, W.-B.K. Rainfall trends ad flood frequency analyses in the Lower Mono River Basin in Togo, West Africa. Int. J. Adv. Res. 2016, 4, 2320–9186. [Google Scholar]

- Nato, G. Risques de Catastrophe Liés aux Inondations dans le Mono: L’Anpc Alerte et Sensibilise la Plateforme de Lokossa. Available online: https://actubenin.com/risques-de-catastrophe-lies-aux-inondations-dans-le-monolanpc-alerte-et-sensibilise-la-plateforme-de-lokossa (accessed on 10 July 2021).

- Toussounon, A. Nangbéto: Quand la Source D’énergie Devient Source de Malheurs. Available online: https://www.podcastjournal.net/Nangbeto-Quand-la-source-d-energie-devient-source-de-malheurs_a5882.html (accessed on 10 July 2021).

- Mike, M. Crue du Fleuve Mono: Probables Lâchées D’eau Depuis Nangbéto. Available online: https://matinlibre.com/2021/08/31/crue-du-fleuve-mono-probables-lachees-deau-depuis-nangbeto/ (accessed on 10 July 2021).

- Parkoo, E.N.; Thiam, S.; Adjanou, K.; Kokou, K.; Verleysdonk, S.; Adounkpe, J.G.; Villamor, G.B. Comparing Expert and Local Community Perspectives on Flood Management in the Lower Mono River Catchment, Togo and Benin. Water 2022, 14, 1536. [Google Scholar] [CrossRef]

- Hounguè, N.R.; Ogbu, K.N.; Almoradie, A.D.S.; Evers, M. Evaluation of the performance of remotely sensed rainfall datasets for flood simulation in the transboundary Mono River catchment, Togo and Benin. J. Hydrol. Reg. Stud. 2021, 36, 100875. [Google Scholar] [CrossRef]

- Wetzel, M.; Schudel, L.; Almoradie, A.; Komi, K.; Adounkpè, J.; Walz, Y.; Hagenlocher, M. Assessing flood risk dynamics in data-scarce environments—Experiences from combining participatory Impact Chains with Bayesian Network Analysis in the Lower Mono River Basin, Benin. Front. Water 2022, 4, 837688. [Google Scholar] [CrossRef]

- Thiam, S.; Salas, E.A.L.; Hounguè, N.R.; Almoradie, A.D.S.; Verleysdonk, S.; Adounkpe, J.G.; Komi, K. Modelling Land Use and Land Cover in the Transboundary Mono River Catchment of Togo and Benin Using Markov Chain and Stakeholder’s Perspectives. Sustainability 2022, 14, 4160. [Google Scholar] [CrossRef]

- Kissi, A.E.; Abbey, G.A.; Agboka, K.; Egbendewe, A. Quantitative Assessment of Vulnerability to Flood Hazards in Downstream Area of Mono Basin, South-Eastern Togo: Yoto District. J. Geogr. Inf. Syst. 2015, 7, 607–619. [Google Scholar] [CrossRef]

- The World Bank. Small but Smart: Benin and Togo Cooperate to Ensure Water Security. Available online: https://www.worldbank.org/en/news/feature/2018/01/25/small-but-smart-benin-and-togo-cooperate-to-ensure-water-security (accessed on 10 June 2021).

- Agbédoufio, P. Risques des Catastrophes dans le Mono: Lokossa en État D’alerte. Available online: https://matinlibre.com/2020/09/04/risques-des-catastrophes-dans-le-mono-lokossa-en-etat-dalerte/ (accessed on 10 June 2021).

- Deutsche Klimafinanzierung. Die InsuResilience Initiative und Global Partnership. Available online: https://www.deutscheklimafinanzierung.de/instrument/insuresilience/ (accessed on 15 November 2021).

- InsuResilience Global Partnership. InsuResilience Global Partnership Vision 2025. Available online: https://www.insuresilience.org/wp-content/uploads/2021/11/vision2025_211022.pdf (accessed on 15 November 2021).

- Lokonon, B.O.K. Urban households’ attitude towards flood risk, and waste disposal: Evidence from Cotonou. Int. J. Disaster Risk Reduct. 2016, 19, 29–35. [Google Scholar] [CrossRef]

- Meton, A. Gestion des Risques et Catastrophes: L’assurance Comme une Priorité, Selon le Professeur Théodore Adjakpa. Available online: https://lanation.bj/gestion-des-risques-et-catastrophes-lassurance-comme-une-priorite-selon-le-professeur-theodore-adjakpa/ (accessed on 10 June 2021).

- Livelihoods Centre. Brochure de L’approche des «Clubs des Mères». Available online: https://www.livelihoodscentre.org/documents/114097690/114438848/LRC.+Brochure+approche+Club+de+Me%CC%80res.pdf/823cdbe8-0649-3c0d-4947-7267693c5673?t=1580204839368 (accessed on 10 July 2021).

- Levy, P.S.; Lemeshow, S. Sampling of Populations: Methods and Applications, 4th ed.; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2008; ISBN 0470374594. [Google Scholar]

- Sabharwal, C.L.; Anjum, B. Data Reduction and Regression Using Principal Component Analysis in Qualitative Spatial Reasoning and Health Informatics. Polibits 2016, 53, 31–42. [Google Scholar] [CrossRef][Green Version]

- Rothmann, K.J. Epidemiology: An Introduction, 2nd ed.; Oxford University Press: Oxford, UK, 2012; ISBN 978-0-19-975455-7. [Google Scholar]

- Jolliffe, I.T.; Cadima, J. Principal component analysis: A review and recent developments. Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 2016, 374, 20150202. [Google Scholar] [CrossRef] [PubMed]

- Vidal, R.; Ma, Y.; Sastry, S.S. Generalized Principal Component Analysis; Springer: New York, NY, USA, 2016; ISBN 978-0-387-87810-2. [Google Scholar]

- Babyak, M.A. What You See May Not Be What You Get: A Brief, Nontechnical Introduction to Overfitting in Regression-Type Models. Psychosom. Med. 2004, 66, 411–421. [Google Scholar] [PubMed]

- Kastellec, J.P.; Leoni, E.L. Using Graphs Instead of Tables in Political Science. Perspect. Politics 2007, 5, 755–771. [Google Scholar] [CrossRef]

- Cissé, J.D.; Kreft, S.; Toepper, J.; Stadtmueller, D. From Innovation to Learning: A Strategic Evidence Roadmap for Climate and Disaster Risk Finance and Insurance; Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH: Bonn/Eschborn, Germany, 2021; Available online: https://climate-insurance.org/wp-content/uploads/2021/10/Strategic-CDRFI-Evidence-Roadmap.pdf (accessed on 17 March 2022).

- Schäfer, L.; Waters, E.; Kreft, S.; Zissener, M. Making Climate Risk Insurance Work for the Most Vulnerable: Seven Guiding Principles; UNU-EHS Publication Series Policy Report No. 1; Munich Climate Insurance Initiative: Bonn, Germany, 2016; Available online: http://collections.unu.edu/eserv/UNU:5830/MCII_ProPoor_161031_Online_meta.pdf (accessed on 2 March 2022).

- Kousky, C.; Shabman, L.; Linder-Baptie, Z.; St. Peter, E. Perspectives on Flood Insurance Demand Outside the 100-Year Floodplain; Issue Brief; Wharton University of Pennsylvania: Philadelphia, PA, USA, 2020; Available online: https://riskcenter.wharton.upenn.edu/wp-content/uploads/2020/05/Perspectives-on-Flood-Insurance-Demand-Outside-the-100-Year-Floodplain.pdf (accessed on 21 June 2022).

- Berg, E.; Blake, M.; Morsink, K. Risk sharing and the demand for insurance: Theory and experimental evidence from Ethiopia. J. Econ. Behav. Organ. 2022, 195, 236–256. [Google Scholar] [CrossRef]

- Will, M.; Groeneveld, J.; Frank, K.; Müller, B. Informal risk-sharing between smallholders may be threatened by formal insurance: Lessons from a stylized agent-based model. PLoS ONE 2021, 16, e0248757. [Google Scholar] [CrossRef]

- Riley, E. Mobile money and risk sharing against village shocks. J. Dev. Econ. 2018, 135, 43–58. [Google Scholar] [CrossRef]

- Quesada-Román, A.; Ballesteros-Cánovas, J.A.; Granados-Bolaños, S.; Birkel, C.; Stoffel, M. Improving regional flood risk assessment using flood frequency and dendrogeomorphic analyses in mountain catchments impacted by tropical cyclones. Geomorphology 2022, 396, 108000. [Google Scholar] [CrossRef]

- Kousky, C.; Lingle, B.; Kunreuther, H.; Shabman, L. Moving the Needle on Closing the Flood Insurance Gap; Wharton University of Pennsylvania: Philadelphia, PA, USA, 2019; Available online: https://riskcenter.wharton.upenn.edu/wp-content/uploads/2019/02/Moving-the-Needle-on-Closing-the-Flood-Insurance-Gap.pdf (accessed on 21 June 2022).

- Bin, O.; Bishop, J.; Kousky, C. Does the National Flood Insurance Program Have Redistributional Effects? B.E. J. Econ. Anal. Policy 2017, 17, 20160321. [Google Scholar] [CrossRef]

- Yore, R.; Walker, J.F. Microinsurance for disaster recovery: Business venture or humanitarian intervention? An analysis of potential success and failure factors of microinsurance case studies. Int. J. Disaster Risk Reduct. 2019, 33, 16–32. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).