Sustainable Banking: New Forms of Investing under the Umbrella of the 2030 Agenda

Abstract

1. Introduction

2. New Forms of Investment in the Context of SDGs

3. SIBs Barriers and Opportunities for Investors

4. Social Impact Bonds Valuation

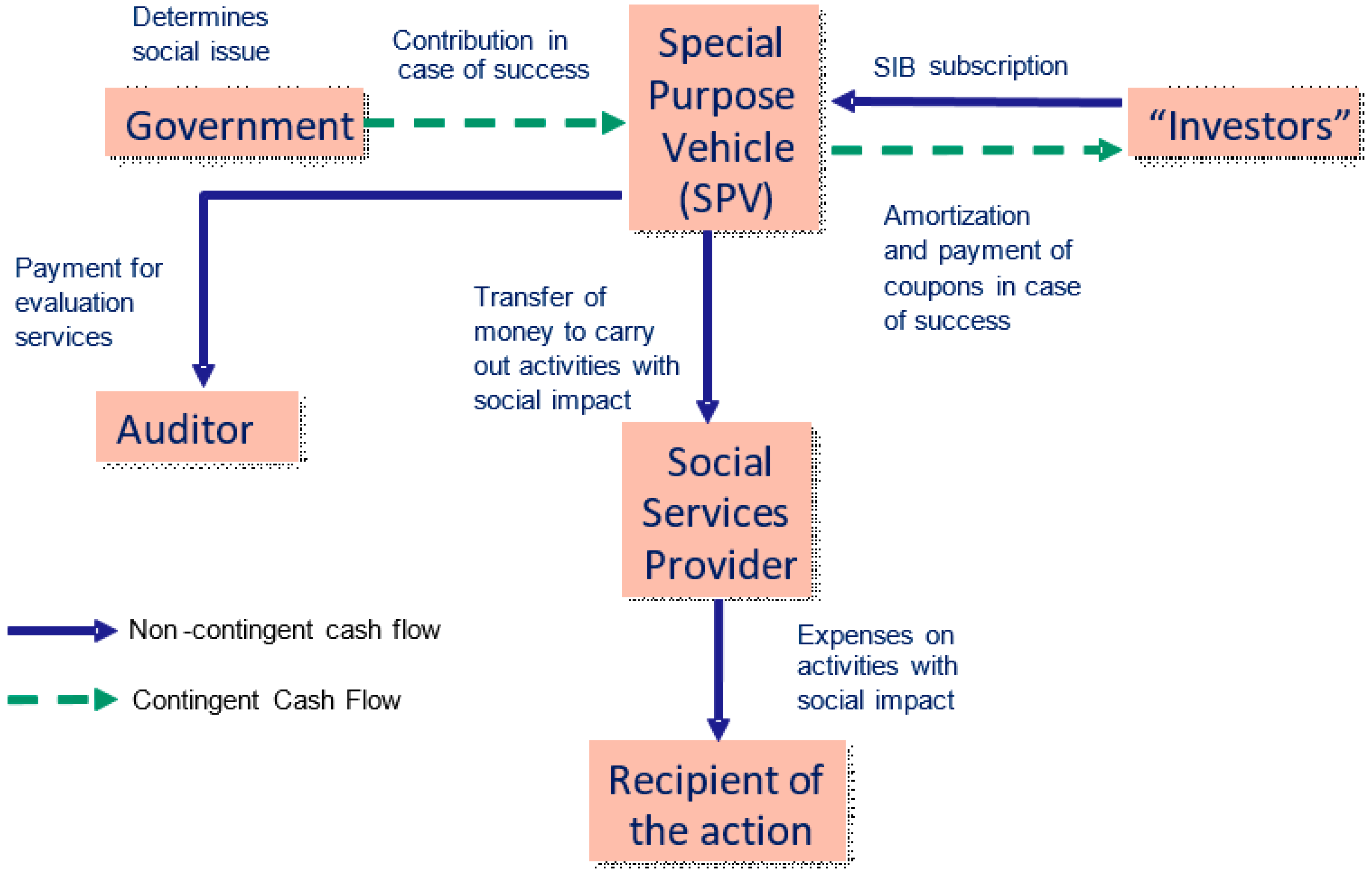

4.1. SIBs: Features and Risks

- Investors. This particular type of investor provides the financial resources necessary to carry out the activity required for the fulfillment of the social goal throughout the life of the SIB.

- Public administration. A public administration, be it a town hall, regional administration, or central administration, acquires the commitment to reimburse the cost of the activity carried out plus an additional amount if the initial goals are achieved.

- Recipients of the action. This is the group of people who receive assistance and benefits from the intervention so that their social or economic situation is improved. This group could be, for example, the homeless, children with basic needs that are not covered, the long-term unemployed, or those who have just left prison. In short, it refers to people who should be protected under the auspices of SDGs 1 and 10.

- Social Services Provider. Throughout the life of the SIB, social service providers are responsible for implementing the necessary actions to achieve the goals set for the recipient group. These are entities specialized in the provision of social services, either companies or NGOs.

- Auditor. At the end of the life of the SIB, an independent entity must proceed to verify whether the stated goals have been achieved. The achievement of the goals originates in the obligation of the public administration to return capital and interest to investors. The role of auditor is performed by an independent company or by an independent institution such as, for example, a university.

- SPV. The SPV is an entity created and managed by a bank to perform tasks related to the issuance, management, and amortization of the SIB. Through the SPV, the bank is in charge of the creation of the product, the design of its structure, the management of the activities, and the liquidation of the cash flows that derive from its operation. The SIB is issued by the SPV and subscribed to by investors. In case of success, the committed public administration transfers the funds to the SPV and the latter proceeds to amortize the SIB and to pay coupons (if any). The SPV is also responsible for hiring and managing the services that must be provided by legal and financial management professionals. In short, the SPV is responsible for the management of the product and maintains agency relations with the participants in the process.

4.2. SIB: Financial Definition and Valuation Methodology

4.3. Valuation of the Peterborough SIB

- If the recidivism rate decreases by more than 13%, a coupon of 13% is paid.

- If the recidivism rate decreases by more than 10% but less than 13%, the rate of decrease is paid.

- If the rate of recidivism decreases by less than 10%, nothing is paid.

- In the year 2017, if there has not been a decrease of recidivism of more than 10% in any year, but the average decrease along the three years has been more than 7.5%, that average is paid. If the average rate drops below 7.5%, nothing is paid.

- If in any of the evaluation periods the decrease in recidivism has been greater than 10%, the principal is collected.

- If in any of the assessment periods the decrease in recidivism has been less than 10%, but on average the decrease has been greater than 7.5%, the principal is collected.

- If in all the evaluation periods the decrease has been less than 10% and on average the decrease has been less than 7.5%, the investor does not receive the principal.

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Fink, L. A sense of purpose. Available online: https://www.blackrock.com/corporate/investor-relations/2018-larry-fink-ceo-letter (accessed on 8 March 2020).

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- US SIF. Sustainable and Impact Investing—Overview. Available online: https://www.ussif.org/files/2018 Infographic overview (1)(1).pdf (accessed on 8 March 2020).

- SpainSIF. 2018 Sustainable and Responsible Investment in Spain. Available online: https://www.spainsif.es/wp-content/uploads/dlm_uploads/2018/12/AF_Spainsif_Study_2018web_pxp.pdf (accessed on 8 March 2020).

- Rosati, F.; Faria, L.G.D. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Scheyvens, R.; Banks, G.; Hughes, E. The private sector and the SDGs: The need to move beyond ‘business as usual’. Sustain. Dev. 2016, 24, 371–382. [Google Scholar] [CrossRef]

- Miralles-Quirós, J.L.; Miralles-Quirós, M.M.; Nogueira, J.M. Diversification benefits of using exchange-traded funds in compliance to the sustainable development goals. Bus. Strateg. Environ. 2019, 28, 244–255. [Google Scholar] [CrossRef]

- Kolk, A.; Kourula, A.; Pisani, N. Multinational enterprises and the Sustainable Development Goals: What do we know and how to proceed? Transnatl. Corp. 2017, 24, 9–32. [Google Scholar] [CrossRef]

- Witte, C.; Dilyard, J. Guest editors’ introduction to the special issue: The contribution of multinational enterprises to the Sustainable Development Goals. Transnatl. Corp. 2017, 24, 1–8. [Google Scholar] [CrossRef]

- Impact Bond Global Database. Available online: https://sibdatabase.socialfinance.org.uk/ (accessed on 2 February 2020).

- Forcadell, F.J.; Aracil, E. Sustainable banking in Latin American developing countries: Leading to (mutual) prosperity. Bus. Ethics 2017, 26, 382–395. [Google Scholar] [CrossRef]

- Forcadell, F.J.; Aracil, E.; Úbeda, F. The influence of innovation on corporate sustainability in the international banking industry. Sustainability 2019, 11, 3210. [Google Scholar] [CrossRef]

- Schinckus, C. Financial innovation as a potential force for a positive social change: The challenging future of social impact bonds. Res. Int. Bus. Financ. 2017, 39, 727–736. [Google Scholar] [CrossRef]

- Disley, E.; Rubin, J.; Scraggs, E.; Burrowes, N.; Culley, D. Lessons Learned from the Planning and Early Implementation of the Social Impact Bond at HMP Peterborough; Research Series 5/11; Ministry of Justice (UK): London, UK, 2011.

- Neyland, D. On the transformation of children at-risk into an investment proposition: A study of Social Impact Bonds as an anti-market device. Sociol. Rev. 2017, 66, 492–510. [Google Scholar] [CrossRef]

- Schinckus, C. The valuation of social impact bonds: An introductory perspective with the Peterborough SIB. Res. Int. Bus. Financ. 2015, 35, 104–110. [Google Scholar] [CrossRef]

- Hasan, M. Valuation of the Peterborough Prison Social Impact. Master’s Thesis, University of Western Ontario, London, ON, Canada, 2013. [Google Scholar]

- Ciufo, G.; Jagelewski, A. Social Impact Bonds in Canada: Investor insights. Available online: https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/financial-services/ca-en-financial-services-social-impact-bonds-in-canada-investor-insights.pdf (accessed on 8 March 2020).

- Scognamiglio, E.; Di Lorenzo, E.; Sibillo, M.; Trotta, A. Social uncertainty evaluation in Social Impact Bonds: Review and framework. Res. Int. Bus. Financ. 2019, 47, 40–56. [Google Scholar] [CrossRef]

- Bergfeld, N.; Klausner, D.; Samel, M. (Survey) Improving Social Impact Bonds: Assessing Alternative Financial Models to Scale Pay-for-Success. Available online: www.hks.harvard.edu/mrcbg (accessed on 2 March 2020).

- Saltuk, Y.; Bouri, A.; Leung, G. Insight into the impact investment market. Available online: https://thegiin.org/assets/documents/Insight into Impact Investment Market2.pdf (accessed on 8 March 2020).

- Disley, E.; Rubin, J. Phase 2 report from the payment by results social impact bond pilot at HMP Peterborough; Ministry of Justice (UK): London, UK, 2014.

- Galitopoulou, S.; Noya, A.N. Understanding Social Impact Bonds; OECD: Paris, France, 2016. [Google Scholar]

- Forcadell, F.J.; Aracil, E. European Banks’ Reputation for Corporate Social Responsibility. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 1–14. [Google Scholar] [CrossRef]

- La Torre, M.; Trotta, A.; Chiappini, H.; Rizzello, A. Business Models for Sustainable Finance: The Case Study of Social Impact Bonds. Sustainability 2019, 11, 1887. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Paramati, S.R.; Alam, M.S.; Apergis, N. The role of stock markets on environmental degradation: A comparative study of developed and emerging market economies across the globe. Emerg. Mark. Rev. 2018, 35, 19–30. [Google Scholar] [CrossRef]

- Waddock, S.A. A Typology of Social Partnership Organizations. Adm. Soc. 1991, 22, 480–515. [Google Scholar] [CrossRef]

- Salamon, L.M. Of Market Failure, Voluntary Failure, and Third-Party Government: Toward a Theory of Government-Nonprofit Relations in the Modern Welfare State. J. Volunt. Action Res. 1987, 16, 29–49. [Google Scholar] [CrossRef]

- Young, D.R. Alternative Models of Government-Nonprofit Sector Relations: Theoretical and International Perspectives. Nonprofit Volunt. Sect. Q. 2000, 29, 149–172. [Google Scholar] [CrossRef]

- Blowfield, M. Business and development: Making sense of business as a development agent. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 414–426. [Google Scholar] [CrossRef]

- Tseng, M.-L.; Tan, P.; Jeng, S.-Y.; Lin, C.-W.; Negash, Y.; Darsono, S. Sustainable Investment: Interrelated among Corporate Governance, Economic Performance and Market Risks Using Investor Preference Approach. Sustainability 2019, 11, 2108. [Google Scholar] [CrossRef]

- United Nations General Assembly. Transforming our world: The 2030 Agenda for Sustainable Development. Available online: https://documents-dds-ny.un.org/doc/UNDOC/GEN/N15/291/89/PDF/N1529189.pdf?OpenElement (accessed on 8 March 2020).

- Ritvala, T.; Salmi, A.; Andersson, P. MNCs and local cross-sector partnerships: The case of a smarter Baltic Sea. Int. Bus. Rev. 2014, 23, 942–951. [Google Scholar] [CrossRef]

- de Lange, D.E. Legitimation Strategies for Clean Technology Entrepreneurs Facing Institutional Voids in Emerging Economies. J. Int. Manag. 2016, 22, 403–415. [Google Scholar] [CrossRef]

- UN Global Compact. Scaling Finance for the Sustainable. Available online: https://www.unglobalcompact.org/library/5721 (accessed on 8 March 2020).

- Gustafsson-Wright, E.; Gardiner, S.; Putcha, V. The Potential and Limitations of Impact Bonds: Lessons from the first five years of experience worldwide; Global Economy and Development at Brookings at Brookings: Washington, DC, USA, 2015. [Google Scholar]

- Fraser, A.; Tan, S.; Lagarde, M.; Mays, N. Narratives of Promise, Narratives of Caution: A Review of the Literature on Social Impact Bonds. Soc. Policy Adm. 2018, 52, 4–28. [Google Scholar] [CrossRef]

- Strickland, B. Survey of Trends in Private Sector Partnerships for International Development and Modalities for Engagement. Available online: https://extranet.creativeworldwide.com/caiistaff/dashboard_giroadmincaiistaff/dashboard_caiiadmindatabase/publications/Survey_Of_Trends.pdf (accessed on 8 March 2020).

- Noya, A.; Galitopoulou, S. Understanding Social Impact Bonds. Available online: http://www.oecd.org/cfe/leed/UnderstandingSIBsLux-WorkingPaper.pdf (accessed on 8 March 2020).

- Instiglio & Thomson Reuters Foundation A Legal Roadmap for Social Impact Bonds in Developing Countries. Available online: https://www.instiglio.org/wp-content/uploads/2015/02/Legal-Road-Map-for-SIBs-in-Developing-Countries.pdf (accessed on 8 March 2020).

- Cooper, C.; Graham, C.; Himick, D. Social impact bonds: The securitization of the homeless. Account. Organ. Soc. 2016, 55, 63–82. [Google Scholar] [CrossRef]

- Warner, M.E. Private finance for public goods: Social impact bonds. J. Econ. Policy Reform 2013, 16, 303–319. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Polit. Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Merton, R. Theory of Rational Option. Bell J. Econ. 1973, 4, 141–183. [Google Scholar] [CrossRef]

- Rubinstein, M.; Reiner, E. Breaking Down the Barriers. Risk 1991, 4, 28–35. [Google Scholar]

- Lamothe Fernandez, P.; Perez Somalo, M. Opciones financieras y productos estructurados; McGraw Hill: Madrid, Spain, 2006. [Google Scholar]

- Rubin, J. Evaluation of the Social Impact Bond. Lessons from planning and early implementation at HMP Peterborough; RAND Europe: Cambridge, UK, 2011. [Google Scholar]

- Fischer, R.L.; Richter, F.G.C. SROI in the pay for success context: Are they at odds? Eval. Program Plann. 2017, 64, 105–109. [Google Scholar] [CrossRef]

- Emerson, J.; Wachowicz, J.; Chun, S. Social Return on Investment: Exploring Aspects of Value Creation in the Nonprofit Sector. Soc. Purp. Enterp. Ventur. Philanthr. New Millenn. 2000, 132–173. [Google Scholar]

{kind=link}

| Barriers | Approach | Opportunities |

|---|---|---|

| The absence of a clear financial formulation [13,18,19], which implies a financial sacrifice without a clear measurement system [18,19,20,21] and difficulty to monetize the results [20] | Financial | Try innovative financial models to solve social problems and combine social and financial returns [18,37] |

| Small market size and product portfolio, and limited experience with results [18,19], which limit quality investments [21] | The confidence that the government will pay if the results are satisfactory [23] | |

| Need to create a mechanism for joint investments or risk-sharing for the development of new products or services [39] | That a large group of investors participate and therefore the risk is divided [23] | |

| Scarce opportunities to exit [21] | Opportunity to reinvest the return on investment in another program if the SIB has been implemented well [23,37] | |

| Scarce innovation in SIB fund structures to link them to the needs of the companies’ investment portfolios [21] | Learning about social investment [14] | |

| Poor regulation [18,20] and a need to regulate the capacity to finance the SIB structure without intermediaries, social investment, the capacity to contract directly with the government, limitations, and procedures in foreign investment and the repatriation of profits [40,41] | ||

| Not having a common understanding with other stakeholders on impact investment [20,21], and difficulty for investors to understand the value contribution [21] | Management & Reputation | Engaging with service providers (NGOs) [14] |

| Difficulty in recruiting professionals with the right skills to understand the model [21] | Link it to the CSR policy and increase visibility and brand image [13,23] | |

| Poor control over service providers (NGOs) [19] and financial cost of the agreement with all stakeholders [20] | Be the first to invest in a field as a mechanism to generate positioning or image [23] | |

| Social/environmental risks [42] and reputational risk [20] | Desire to invest ethically and in line with the corporate mission [14] | |

| It is a perverse incentive for corporate philanthropy and the non-profit sector to seek commercial interests over the social mission; it represents the worst of both sectors (financial and social) [19,38] | Business Ethics | Willingness to support a new type of product that benefits society [14], doing good and allowing for moderate returns [23] |

| It is a product with preventive objectives and not solutions to existing problems [18] | Improving collaboration between the public, private, and third sectors [18,19,37,38] |

| Reinsertion Rate | 2013 | 2015 | 2017 |

|---|---|---|---|

| Reinsertion greater than 13% | 37.1% | 36.5% | 37.1% |

| Reinsertion between 10% and 13% | 11.4% | 11.5% | 11.2% |

| Reinsertion of less than 10% | 51.5% | 52.0% | 51.8% |

| Reinsertion Rate | 2013 | 2015 | 2017 |

|---|---|---|---|

| Reinsertion greater than 10% | 48.5% | 48.0% | 48.2% |

| Year | 2013 | 2015 | 2017 |

|---|---|---|---|

| Risk free rate | 3.50% | 3.50% | 3.50% |

| PV of the expected coupon is 13% | 4.34% | 4.00% | 3.79% |

| PV of the expected coupon is between 10% and 13% | 1.19% | 1.13% | 1.03% |

| PV of the expected coupon is more than 7.5% on average | - | - | 0.03% |

| PV of the principal if any coupon is more than 10% | - | - | 67.70% |

| PV of the principal with an average coupon of more than 7.5% | - | - | 0.31% |

| SIB Valuation | % | GBP |

|---|---|---|

| Value of the SIB | 83.52% | 4,175,945 |

| Value of the principal | 68.02% | 3,400,825 |

| Value of the coupons | 15.50% | 775,120 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Méndez-Suárez, M.; Monfort, A.; Gallardo, F. Sustainable Banking: New Forms of Investing under the Umbrella of the 2030 Agenda. Sustainability 2020, 12, 2096. https://doi.org/10.3390/su12052096

Méndez-Suárez M, Monfort A, Gallardo F. Sustainable Banking: New Forms of Investing under the Umbrella of the 2030 Agenda. Sustainability. 2020; 12(5):2096. https://doi.org/10.3390/su12052096

Chicago/Turabian StyleMéndez-Suárez, Mariano, Abel Monfort, and Fernando Gallardo. 2020. "Sustainable Banking: New Forms of Investing under the Umbrella of the 2030 Agenda" Sustainability 12, no. 5: 2096. https://doi.org/10.3390/su12052096

APA StyleMéndez-Suárez, M., Monfort, A., & Gallardo, F. (2020). Sustainable Banking: New Forms of Investing under the Umbrella of the 2030 Agenda. Sustainability, 12(5), 2096. https://doi.org/10.3390/su12052096