2. Literature Review

As [

8] state, decision-making can be described as a cognitive and intuitive process of human behavior when individuals create options or an action is chosen from the various alternatives which are based on certain criteria (

Figure 1).

Many studies have tried to understand managerial decision-making and its relation to risk. There are many studies with tested hypotheses derived from research in sustainable, strategy, finance and behavioral decision theory in order to assess the influence of both organizational and cognitive factors on the risk assessment errors [

9,

10,

11,

12,

13,

14,

15,

16]. It was found that both organizational and cognitive factors have an impact on the risk of decision-making.

Other theories have explored the influence of economic and psychological factors on risky behavior within the management of an enterprise. But only few studies and little research has been devoted to the investigation of the influence of complex, content, emotional, behavioral and also hormonal factors on preferences and risk evaluation in decision-making process in any level of an enterprise management [

17,

18,

19,

20,

21,

22,

23].

Financial decisions and behavior, such as investment, are supposed to meet normative expectations by performing utility trade-offs between the calculated outputs, such as expected values, and certain financial alternatives [

24]. As the decision-maker is rational, he/she must choose the alternative with the highest utility which is independent of the decision-making context. According to normative theory, information that cannot be calculated on the expected values of the options should not influence the choices made. Experiments have presented that the behavioral effects of decision-making content are independent of contexts like summary and description. The results of a survey on retirement planning behavior revealed that emotions could be important predictors of long-term care insurance purchase intentions [

25].

Mainstream economists tend to employ axiomatic normative assumptions about decision agency, and research evidence from psychology and neuroscience provide strong empirical support for the effects of human emotions on risky behavior. Understanding the role of emotions in decision-making and their neural underpinnings plays an important role in economic and psychological studies [

26]. They specify emotions as immediate or anticipated. Anticipated emotions refer to the emotions which people expect to feel as a consequence of choosing one decision alternative over another. Immediate emotions include all affective states that the decision-maker uses at the time of decision-making.

In recent decades, economists have been studying anticipated emotions, such as regret and disappointment, while psychologists have focused on immediate emotions. The authors of [

27] focused directly at financial decision-making, and there are several studies that present the complex between emotions and risky decisions. Reference [

28] observed that the timing of the resolution of risk and anticipatory emotions predicted investment and financial behavior. Similarly, reference [

29] argued that trait of anxiety predicts low-risk investment and financial decision, whereas the trait of anger is associated with higher financial risk-taking. Some experimental findings revealed that happier people spend less, and they are also less likely to have debts. They are more worried about the future, and thus they save more money. A study made by [

30] showed that people tend to spend more money when they are in a sad and depressed mood.

Focus is also placed upon the question of how these emotions can be effectively controlled in order to reach the best utility through the decision-making. Although much has been written about neurotransmitters [

31] in relation to risk and decision-making, a critical area that has been relatively neglected by psychologists and economists is the hormonal underpinning of risk [

32].

Financial and investment decisions can be seen as the most important life-shaping decisions that people make. Because of sustainable, many household decisions violate sound financial principles. They have under-diversified stock holdings and low retirement saving rates. Top corporate managers make decisions that are affected by overconfidence and personal history. Many of these behaviors can be explained by well-known principles from cognitive science [

33].

Behavioral finance is an area or sub-discipline of behavioral economics that examines real behavior and decision-making of people and investors in the field of finance, including the knowledge of psychology and sociology [

34,

35,

36,

37,

38]. According to [

39,

40], behavioral finance explains our actions and behaviors, but modern finance is related to the explanation of actions of an economic man. According to [

41], traditional finance is related to decisions in which full information is available for making investment decision.

Usually, investors are not aware of their behavioral biases. If investors become conscious of biases they can face, they can act more rationally [

42,

43]. According to [

44,

45], behavioral biases include both cognitive biases (such as anchoring, representativeness, mental accounting and availability) and emotional biases (such as risk aversion, overconfidence and regret aversion). Reference [

46] described in their article “Judgment under Uncertainty: Heuristics and Biases” the systematic errors in the thinking of ordinary people, while analyzing the origin of such errors in the cognitive mechanism. They found out that emotional and psychological factors were the source of a change in the behavior of the subjects, but only when these were borderline situations of decision-making and getting to know something unknown. In that case, this could also be applied to the targeted subject of decision-making, i.e., shareholders of woodworking (WW) and furniture manufacturing and trading (FMT) enterprises.

According to [

47], standard economic theory is designed to offer mathematically structured solutions and to perceive the human being as an economically rational subject. They are based on idealized financial behavior. Behavioral finance, in turn, tries to emulate the phenomenon of the human psyche and is based on observed behavior. References [

48,

49] state that behavioral finance has originated as a new trend in economics and focuses on the economic aspects of deviations from the rational behavior of subjects, especially the impact of cognitive distortions, psychological and emotional condition of the subject. Factors of human behavior influence decision-making and disable to receive rationally new information through emotional action.

The most significant psychological, emotional and cognitive factors are [

50]:

Love, hatred, sadness, happiness, powerlessness, panic, depression, desperation, anxiety (emotional);

Knowledge, expertise, concentration, recognition ability, logical thinking, human character, short-term and long-term memory process (cognitive);

Power, security, certainty, personality, shame, self-esteem, freedom, self-realization, friendship, health, attractiveness (psychological).

The Slovak Republic is relatively independent of importing the natural resources inputs, being built on a domestic national resource base of sustainable character, and therefore it is possible to permanently show an active balance of foreign trade. Related to domestic natural resources, suitable geographic location, and acceptable energy demands, the wood-processing industry represents an important field of industry for the Slovak national economy, while thus enabling further development of small and medium enterprises [

51]. The wood-processing industry is composed of the wood, furniture and cellulose-paper industries based on domestic and ecological resources [

52,

53].

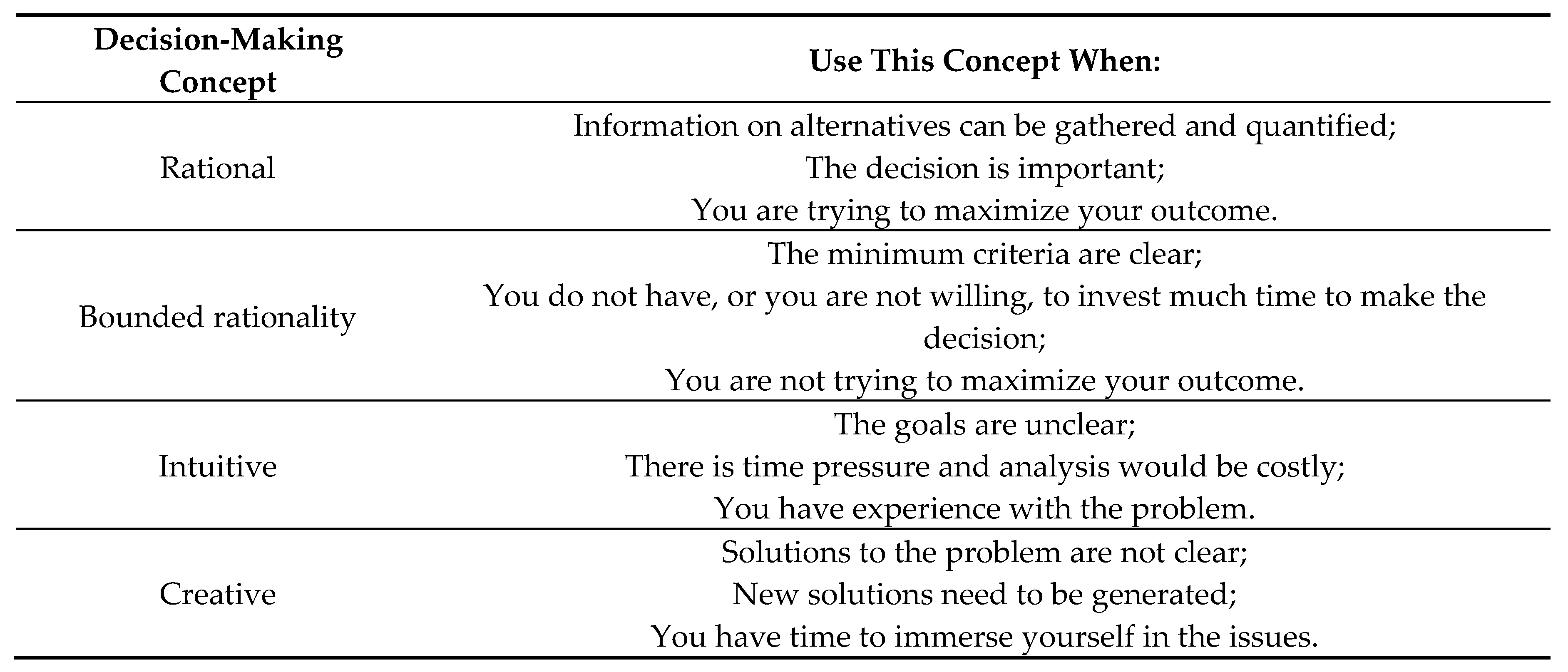

The result and contribution of our paper lie in the design of a decision-making concept. As it is presented by [

33,

39,

54], the decision-making process lies in choosing among alternative courses of action, including inaction. Structured decision-making processes include rational, bounded rationality, and creative decision-making. Each of these can be useful, depending on the circumstances and on particular solved problem. The four different decision-making concepts (

Figure 2) vary in terms of how experienced or motivated decision-makers are to make a relevant choice. Choosing the right approach can make an organization more effective and it could also improve the ability to carry out all basic managerial functions like planning, organizing, leading and control.

The objective of the paper is to identify and investigate the impact of significant cognitive, psychological and emotional factors affecting the financial decision-making of the shareholders of WW and FMT enterprises. This could lead to the design of a decision-making concept which takes into account not only cognitive but also psychological and emotional factors and their influences on the decision-making process.

3. Methodology

This research was focused on the analysis of the current situation of the issues concerning behavioral aspects that influence the financial decision-making of shareholders of WW and FMT enterprises. The data collection was carried out by means of a questionnaire survey focused on the WW and FMT enterprises operating in Slovakia. The first part of the questionnaire included demographic data, the aim of which was to differentiate the respondents according to the size of the enterprise (micro, small, medium and large), type of enterprise (production and non-production sector), length of time on the market (less than 1 year, less than 5 years, less than 15 years and more than 15 years) and the job position in the enterprise (employee, shareholder, manager). The second part of the questionnaire contained questions aimed at respondents expressing agreement or disagreement with statements in the field of cognitive, psychological and emotional factors. Respondents expressed their opinion using a five-step rating scale (−2, very negative; −1, negative; 0, don’t know; 1, positive; 2, very positive) for each cognitive, psychological and emotional factor. The aim was to find out which behavioral factors have a significant impact on shareholders’ financial decision-making.

The whole sample consisted of all organizations and enterprises operating in the Slovak Republic, i.e., 559,841 active economic subjects [

55]. The random and purposive sampling was used for the selection of respondents into the selected sample. The purposive sampling was used for the selection of WW and FMT enterprises. Respondents were addressed through electronic forms (questionnaires) sent directly to their addresses. Subsequently, the sample size was defined using a mathematical relationship to calculate the minimum number of respondents to be involved in the survey [

56]:

where

n is the minimum number of respondents;

z is the coefficient of reliability (

z = 1.96 ≥ the reliability of the research reaches 95.0%);

p and

q are the percentage of questioned respondents (the extent of knowledge of respondents with regard to the problem is unknown, the whole sample is divided in half, i.e.,

p and

q = 50%); and ∆ is the maximum acceptable error (the value of maximum acceptable error was determined at 5%).

Out of the total number of 2.549 respondents, 453 respondents participated in the questionnaire survey. In order to keep the contextual framework of the paper, the evaluation of the survey results focused on the 412 shareholders of WW and FMT enterprises.

Figure 3 presents the percentage of respondents according to their job position in the enterprise. Out of the total number of respondents, 91% were shareholders, 5% managers and 4% employees. On this basis, it was necessary to exclude 41 respondents from the sample, i.e., 23 managers and 18 employees.

Two research questions (RQ) were formulated within the research area:

RQ1: What emotional factors are the source of cases when people change their behavior and deviate from economic rationality?

RQ2: Which key cognitive, psychological and emotional factors influence the rational decision-making behavior of shareholders of WW and FMT enterprises?

Based on the research questions and the available literary sources [

46,

47,

48,

49,

50], four hypotheses were formulated as follows:

Hypothesis 1 (H1). It is assumed that people are rational, and their behavior corresponds to that. Emotions such as fear, love and hatred are the source of cases when people change their behavior and deviate from economic rationality.

Hypothesis 2 (H2). It is assumed that the key factor that most influences the rational decision-making behavior of shareholders of WW and FMT enterprises is expertise as a cognitive factor.

Hypothesis 3 (H3). It is assumed that the key factor that most influences the rational decision-making behavior of shareholders of WW and FMT enterprises is certainty as a psychological factor.

Hypothesis 4 (H4). It is assumed that the key factor that most influences the rational decision-making behavior of shareholders of WW and FMT enterprises is happiness as an emotional factor.

The results of the survey were processed and evaluated with statistical software STATISTICA 10. Testing was performed at the significance level α = 0.05. Graphical and descriptive methods were applied in order to evaluate the Hypothesis H1. Pearson’s Chi-square test and contingency coefficients (Cramer’s V and Pearson´s contingency coefficient C) were used to evaluate the Hypotheses H2, H3 and H4.

4. Results

It terms of the enterprise size, the structure of the research sample consisted mainly of small enterprises (41%), medium enterprises (28%) and micro enterprises (25.1%). Large enterprises represented the lowest proportion (5.90%). Enterprises operating in the production sector constituted 65% and the rest were represented by the non-production sector (woodworking and furniture trading enterprises). With regard to the time on the market, the enterprises operating for less than 15 years (42%) and more than 15 years (34%) presented the largest proportion. Enterprises operating on the market for less than 5 years constituted 17% and the remaining 7% was represented by enterprises with less than 1 year on the market.

Figure 4 presents the findings concerning the change in behavior of shareholders of WW and FMT enterprises in borderline (unknown) situations by expressing their attitudes to the statement using five-step rating scale: “Emotions such as fear, love and hatred are the source of cases when people change their behavior during borderline (unknown) situations.” A very positive attitude with this statement was expressed by 18.3% of respondents and half (51.0%) respondents indicated a positive attitude. A total of 22.9% of the respondents were not able to express themselves clearly and a total of 7.90% of respondents expressed negative or very negative attitudes. It follows that these shareholders do not consider specific emotions to be the cause of changes in their behavior. The hypothesis H1 has been confirmed by the graphical evaluation, i.e., the assumption that people are rational, and their behavior corresponds to that. Emotions such as fear, love and hatred are the source of cases when people change their behavior and deviate from rationality.

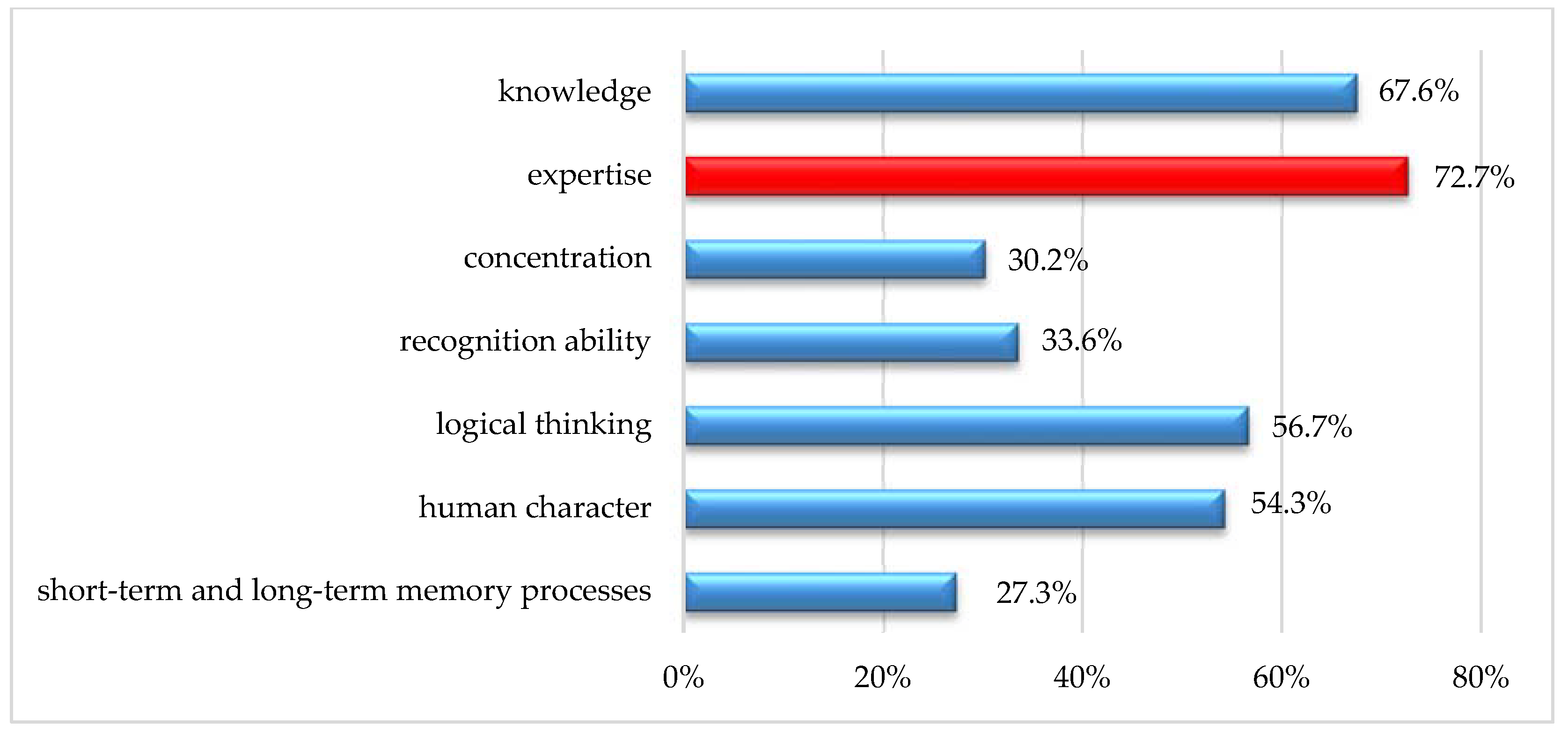

Another part of the results was focused on investigating the impact of cognitive, psychological and emotional factors on the behavior of shareholders in decision-making situations. Respondents could select several aspects belonging to groups of cognitive, psychological and emotional factors.

Figure 5 presents the impact of cognitive factors on the rational behavior of shareholders. Out of cognitive factors, expertise has the largest impact on rational behavior in the decision-making process of shareholders (72.7%). Other significant cognitive factors are knowledge (67.6%), logical thinking (56.7%) and the character of the shareholders (54.3%).

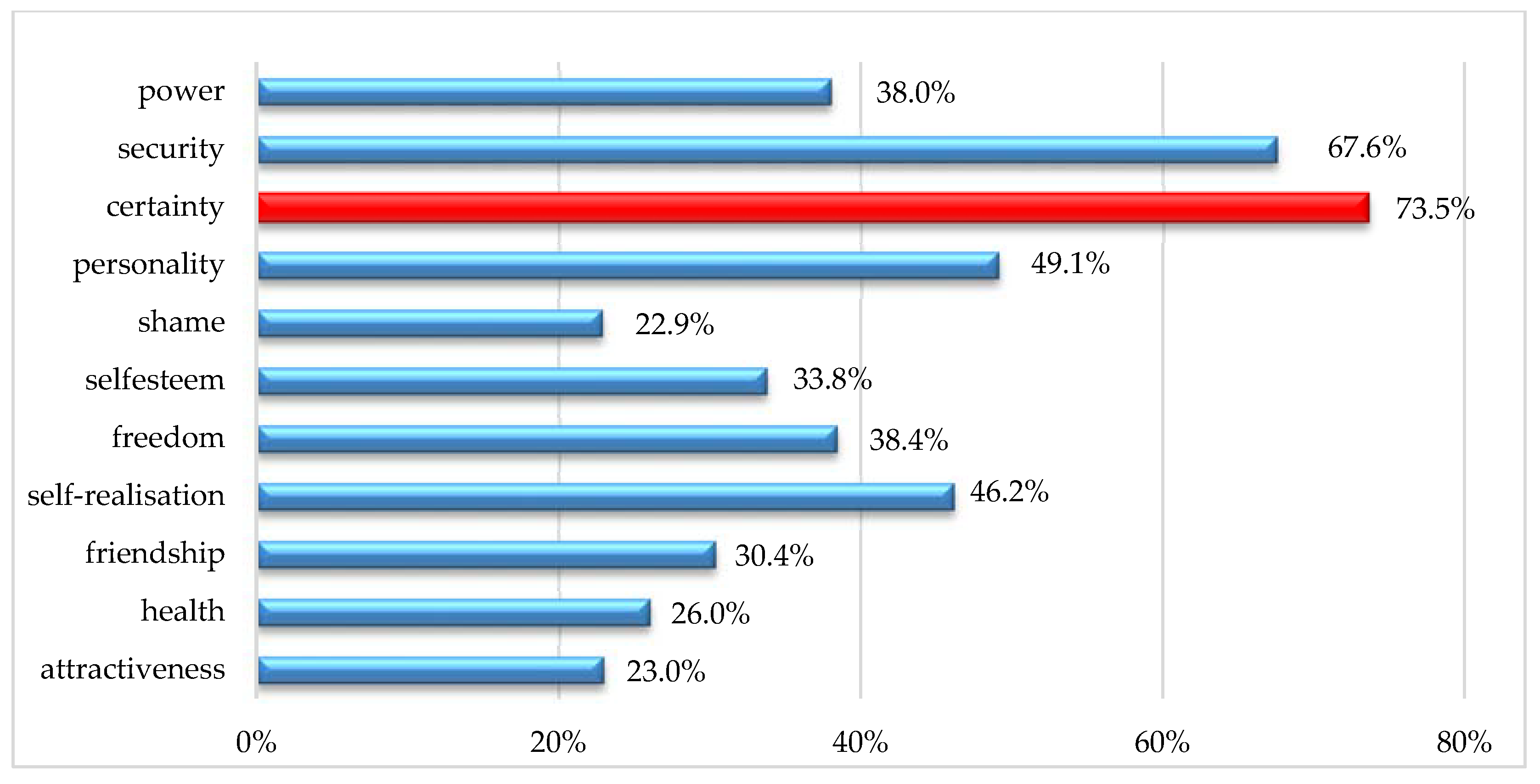

Out of the psychological factors, it is certainty (73.5%) that has the most significant impact on rational behavior of the shareholders. Security (67.6%), personality (49.1%) and self-realization (46.2%) have also reached a considerable impact.

Figure 6 presents the significance of individual psychological factors.

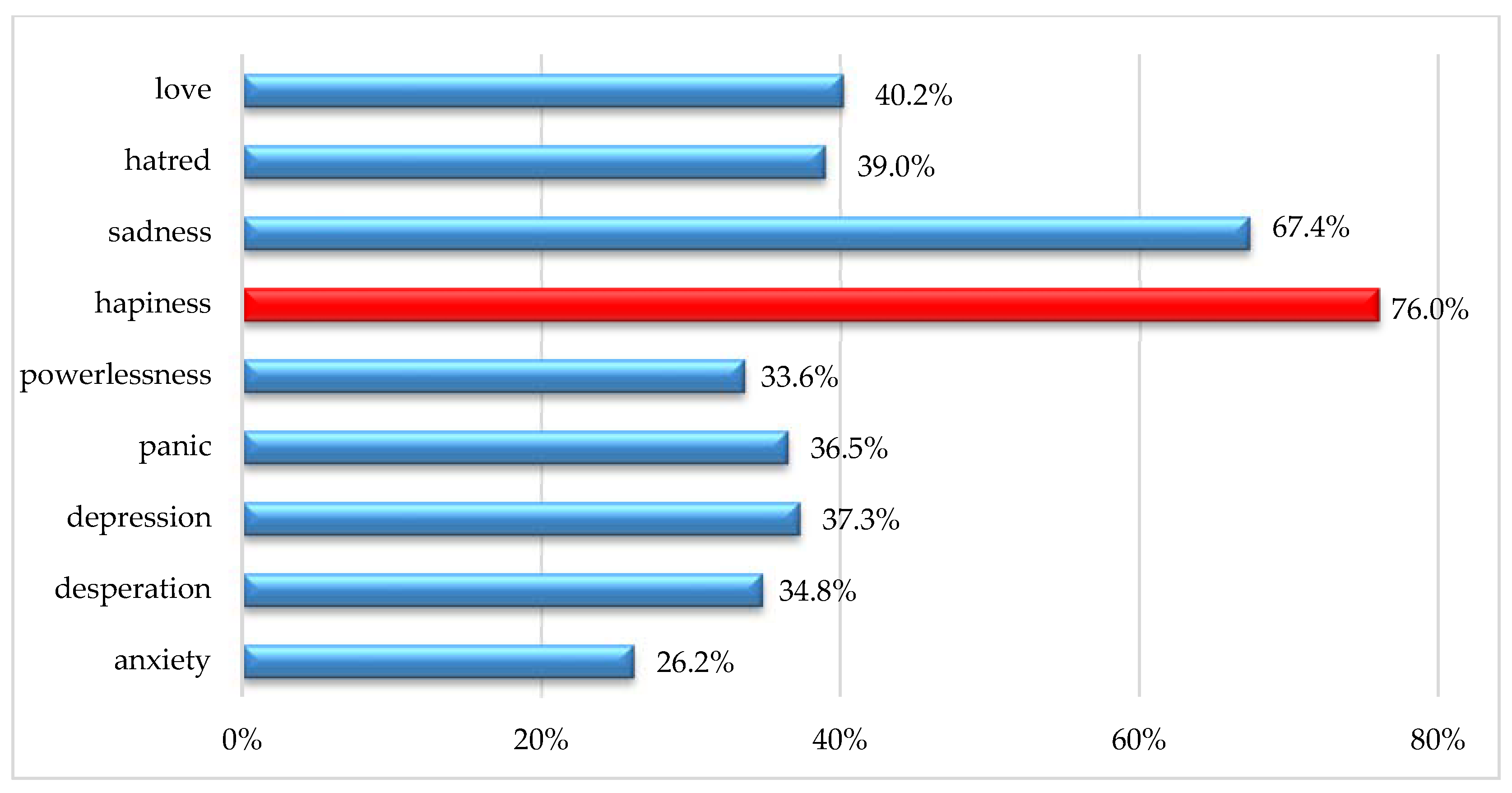

Happiness (76%) is the most important factor influencing the rational behavior of the shareholders in terms of emotional factors. Sadness (67.4%) as a counterpart of happiness is the second significant emotional factor. Love and hatred ranked among the third most important factors. The significance of individual emotional factors for the rational behavior of shareholders is presented in

Figure 7.

In relation to the second research question, the graphical evaluation of the impact of behavioral (cognitive, psychological and emotional) factors has revealed that the key factors that most influence the rational decision-making behavior of shareholders of WW and FMT enterprises are the expertise as a cognitive factor, certainty as psychological and happiness as an emotional factor.

In the next part of the paper, the impact of cognitive, psychological and emotional factors on the financial decision-making process were pointed out through mathematical-statistical analysis.

Based on the

p level (0.00824), the null hypothesis in favor of the alternative hypothesis was rejected, implying a dependence between the influence of expertise as a cognitive factor and shareholders of WW and FMT enterprises (

Table 1). Less than 20% of the theoretical frequencies were less than the value 5, and thus the condition of good approximation was fulfilled. The value of the Cramer’s V reached the level 0.1526185, which pointed out the existence of a weak dependence between the respondents’ job position and the impact of behavioral aspects on the sustainable financial decision-making process.

Based on the statistical data evaluation of the impact of certainty on internal interest groups, it was possible to confirm the interdependence between individual variables (

Table 2). Due to the value of the

p level (0.00000), the null hypothesis was rejected in favor of the alternative hypothesis with confirmation of the existence of dependence between the shareholders of WW and FMT enterprises and certainty as a psychological factor. Also, in this case, the condition of good approximation was fulfilled (less than 20% of theoretical frequencies were less than 5). The contingency coefficient with the value of 0.2383203 and the Cramer’s V 0.453908 pointed out the existence of weak dependence between the job position of the respondents and behavioral aspects on sustainable financial decision-making process.

By comparing the

p level (0.01817) with the selected significance level (α = 0.05), the null hypothesis was rejected (

Table 3). The rejection of the null hypothesis in favor of the alternative hypothesis confirmed the existence of dependence between happiness as an emotional factor and shareholders of WW and FMT enterprises. The condition of good approximation was fulfilled also in this case. The contingency coefficient with the value of 0.381510 and the Cramer’s V 0.1394885 showed a weak dependence between the variables.

Based on statistical observation, the

p level was lower than the significance level (0.00000 < 0.5), which has led to the rejection of the null hypothesis in favor of the alternative hypothesis, i.e., the existence of dependence between the sadness as an emotional factor and shareholders of WW and FMT enterprises (

Table 4). Out of the statistical results, less than 20% of the theoretical frequencies were less than 5, thus satisfying the condition of good approximation. The contingency coefficient with the value of 0.3087603 and the Cramer’s V 0.3246214 pointed out the existence of medium strong dependence between the variables.

Mathematical-statistical analysis of the impact of behavioral (cognitive, psychological and emotional) factors has confirmed the Hypotheses H2, H3, and H4. These include expertise (cognitive factor), certainty (psychological factor), happiness and sadness (emotional factor). The key behavioral aspects have contributed to the formulation of conclusions and recommendations aimed at the elimination of systematic errors in the sustainable financial decision-making of shareholders of WW and FMT enterprises.

Expertise is the most valuable factor for the shareholders. It is considered as the ability to use expertise effectively to reach profit and sustainable growth. By the applying, training and trying of expertise, it is possible to gain experience gradually and so increases the level of knowledge [

57,

58]. The lack of knowledge leads to subsequent errors in the first phase of decision-making—the lack of necessary information. Reference [

59] confirms in his study that intelligence, cognitive style, age, experience and level of knowledge play an important role in the decision-making process.

Certainty is an everyday part of our lives. The shareholders of enterprises regularly make decisions based on subjective and objective factors to feel safe and that nothing would jeopardize the security of the enterprise. In the context of business activities, we encounter various security threats that negatively affect the sustainable functioning of the enterprise. As a result, fear and uncertainty prevail among most shareholders and entrepreneurs. With regard to fear and uncertainty, it is extremely important to set the objectives correctly at every decision-making stage and determine the likelihood of threats based on a lack of knowledge. Relevant information and sufficient knowledge and experience of the decision-makers applied to solve the decision-making problem helps to specify the likelihood of the occurrence of certain phenomenon and also to identify the potential consequences of different decisions. The assessment of likelihood is extremely important since its task is to determine the extent, i.e., quantify the considered uncertainty. Under the conditions of uncertainty, the shareholders of enterprises can use a large amount of historical data to determine likelihood of individual variants. In case they have no relevant information, the solution variants would not contribute to solving the occurred problem in the decision-making process. Reference [

54] confirms that our contemporary world is significantly influenced by various kinds of uncertainty. Some decisions are made intuitively and only with partially available information. There is no optimal decision-making concept because the majority of decisions are made under the conditions of uncertainty.

Happiness and decision-making are inseparable parts of a human being. The shareholders (entrepreneurs) become often responsible for many other people who they manage and work with as well as for sustainability. Despite the fact that most shareholders (entrepreneurs) have a supportive network of people they can consult when making difficult and important decisions, the final decision is in the hands of enterprise shareholders. The meaning lies in the accepting responsibility for the decisions. Reference [

60] point out in their study that happiness has an impact on making decisions, and this has not been so far sufficiently described as an emotional variable.

Sadness as an emotional factor has an important impact on the behavior of shareholders of WW and FMT enterprises and in many cases it hinders rational thinking. Where it invokes negative emotions in people, it absorbs the thinking. It this case, it is possible to assume that the shareholders will make incorrect decisions in the first phase and the feedback can reveal that the choice of the variant was not correct. Reference [

61] confirms the impact of sadness on the rational behavior in their study so that sadness makes people (managers, shareholders) risk averse, less patient and more sensitive to negative experiences.

Many scholars [

62,

63,

64,

65] confirmed that the impact of cognitive, psychological and emotional factors on an individual’s decisions is substantial and fundamental.

Shareholders of WW and FMT enterprises should accept individual behavioral aspects that have a significant impact on their decision-making. It is, therefore, necessary to understand the meaning of the impact of individual factors on their decision-making process in the enterprise, and thus in time prevent the negative effect on their rational thinking. For each enterprise shareholder, victory means not just defeating and dominating the market, but above all winning over themselves in terms of controlling their emotions, seeking independent thinking and resilience to the sustainable environment. According to [

66,

67], important activities that can prevent systematic errors in financial decision-making may include understanding and avoiding psychological deviations, acquiring sufficient experience and knowledge, not overlapping private and the professional lives, understanding one’s own deficiencies and avoiding disturbances, the early identification of potential risks and threats, a retrospective look at strategy and reorganization, sufficient time for making important decisions, not making hasty decisions, and listening and being open to the opinions of others.

Mapping the behavioral aspects that have an impact on the financial decision-making of an enterprise’s shareholders seems to be a starting point for the specification of critical factors and further for the design of a decision-making concept. Key factors that impact rational behavior and financial decision-making of shareholders were determined from the results of empirical research. By the concept, systematic errors in practical decision-making within the management of an enterprise could be eliminated or at least minimized. The last hypothesis was assessed according to the design of decision-making concept.

Hypothesis 5 (H5). It is assumed that the concept, with identified key psychological, cognitive and emotional factors, will be a tool for the relevant decision-making of an enterprise’s shareholders.

On the base of the key factors, a relevant decision-making concept for systematic decision-making errors will be designed.

It can be said that doing business is a long-term, difficult and challenging process which contains daily and necessary decisions within various managerial levels in an enterprise. This is necessary for sustainability of business. The performance of an enterprise’s shareholder is affected mainly on his/her experiences and knowledge. It is important to make not only qualitative but also flexible and relevant decisions. It means that shareholders should have sense of responsibility for the whole enterprise and its indicators. It requires some competencies: communication competence; empathy; and the competencies of listening to others, being tolerant of others and self-control.

There are some decision-making errors of enterprises’ shareholders which can be mentioned [

8,

27,

42]:

A lack of knowledge, experience and communication skills;

Poor organizational structure;

The incompetence of decision-making under the conditions of uncertainty;

Preference of one’s own alternatives;

Incorrect risk analysis;

Lost market opportunities;

No development of a business plan:

A lack of strategy;

Uncertain goals and priorities;

The lack of effective monitoring of an enterprise.

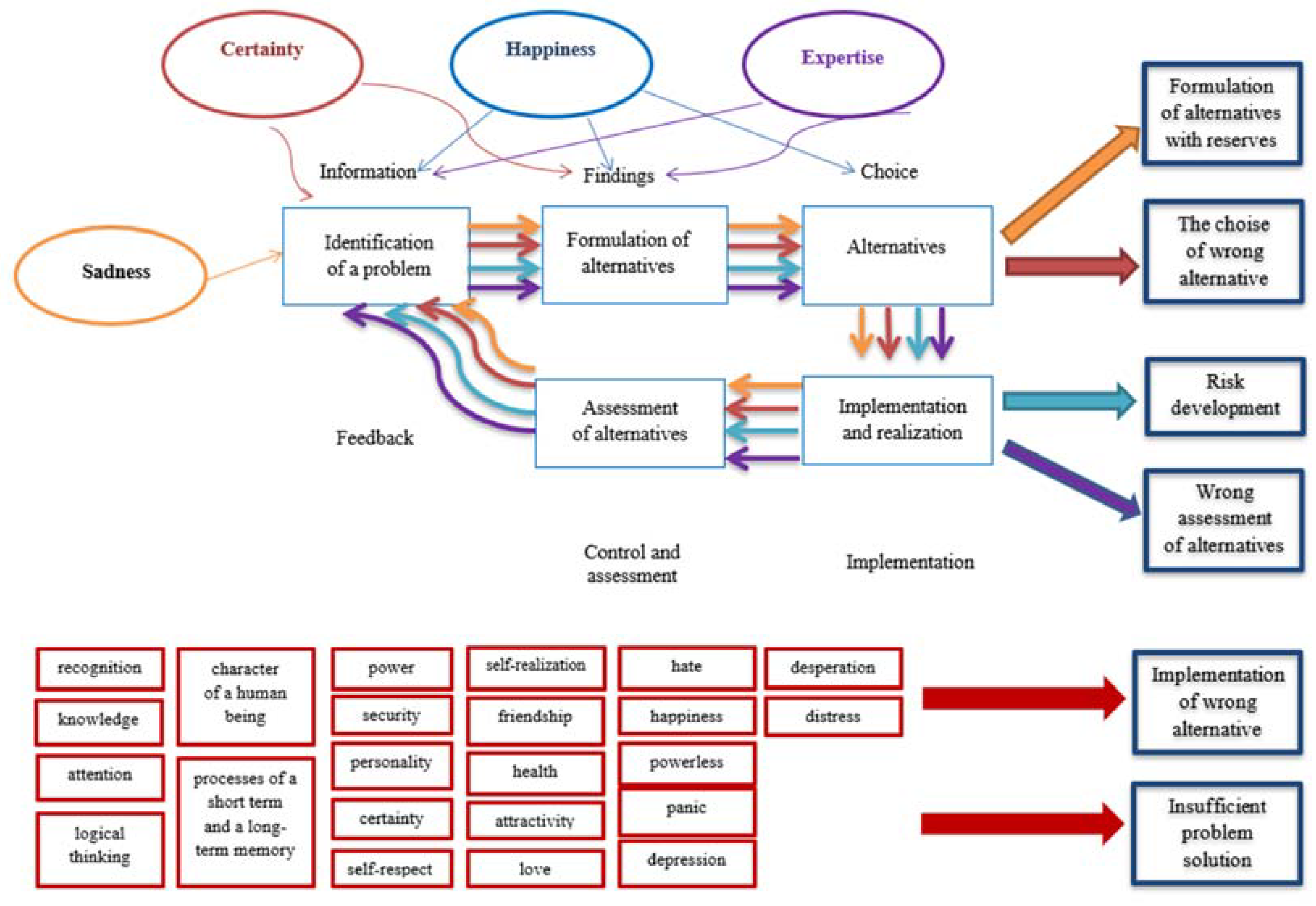

According to the above-mentioned errors it the following discrepancies in the financial process can be assumed: insufficient identification of a problem, formulation of alternatives with reserves, the choice of incorrect alternatives, risk development, incorrect assessment of alternatives, the implementation of the incorrect alternative, insufficient problem-solving.

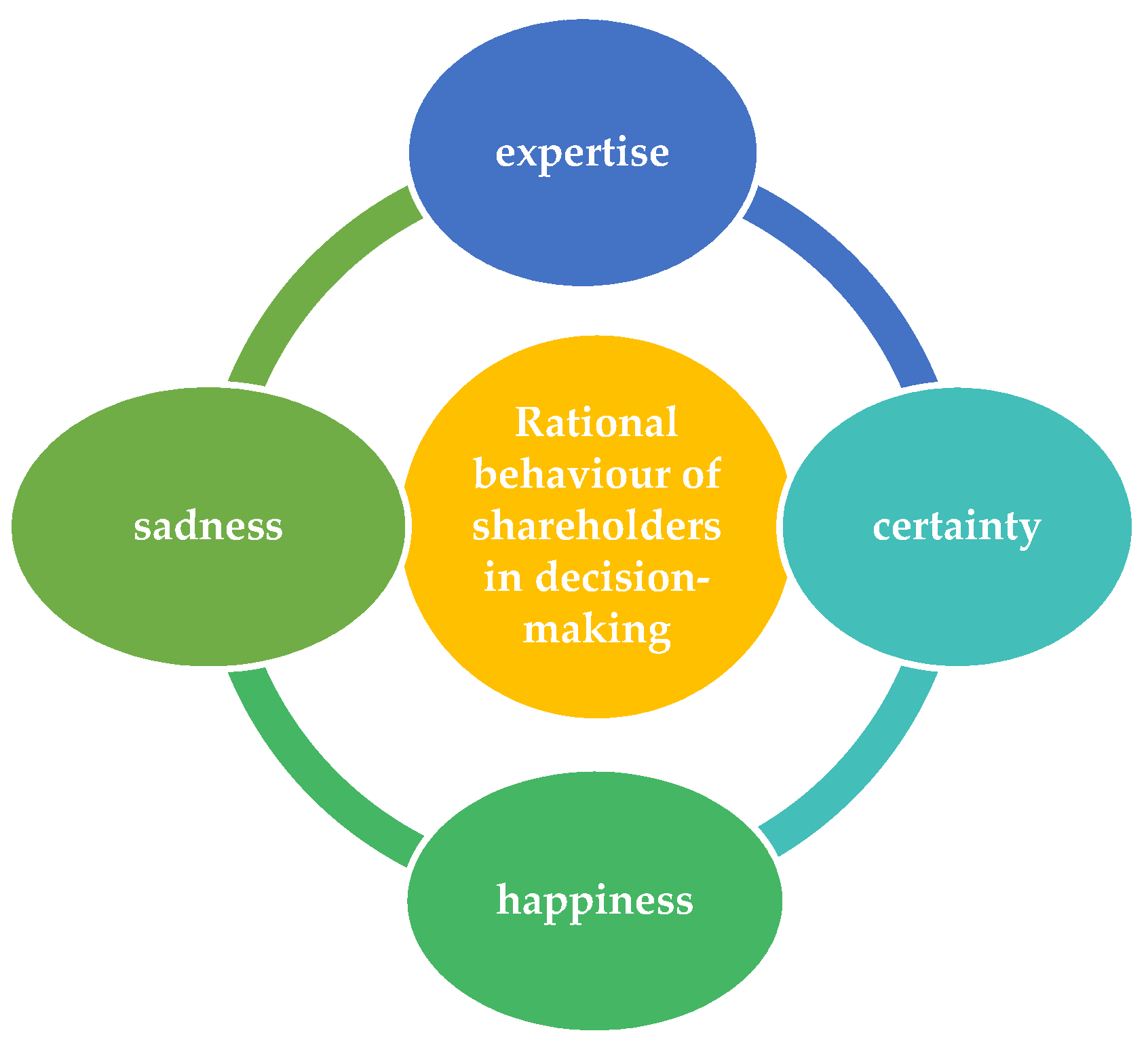

By the design of a decision-making concept, discrepancies and the incorrect decisions of an enterprise’s shareholders can be eliminated. Due to the four key behavioral factors (expertise, certainty, happiness and sadness) which were identified by statistical testing, the dependency between given factors and the chosen internal group of shareholders, a concept of systematic decision-making errors can be designed, as it is presented in

Figure 8.

Figure 9 presents a complex decision-making concept by the application of four key behavioral factors.

An outcome of our paper it was a relevant decision-making concept containing the application of behavioral factors. We can say that such a concept is a new approach (which was also declared by the managers participated in our experiment) to the understanding of managerial behavior and the factors which have significant effect on this behavior. Input data were gathered by empirical research and in the following they were evaluated by mathematical and statistical analysis. Our results show that factors like expertise, certainty, happiness and sadness have a great impact on managerial behavior related to financial decision-making. Out of the cognitive factors, expertise has the largest impact on rational behavior in the decision-making process of shareholders; the second most important cognitive factor is knowledge, which together with expertise can be considered as the most important drivers for the company’s sustainable growth.

Certainty is an everyday part of our lives. The shareholders and managers regularly make decisions which can jeopardize the security of the enterprise. In the context of business activities, we encounter various security threats that could negatively affect the ideal functioning of the enterprise. With regard to fear and uncertainty, it is important to set the objectives correctly at every decision-making stage and to determine the probability of threats based on knowledge. The assessment of probability is extremely important since its goal is to determine the extent and quantification of uncertainty. The shareholders of enterprises can use a large amount of historical and relevant data, or apply their experience and skills, in order to determine the likelihood of individual variants and the possible implications of their decisions.

Happiness and decision-making are inseparable parts of a human being. Happiness has an impact on making a decision, and this factor has not been so far sufficiently described and investigating as an emotional variable. There are various situations where most shareholders and managers have a supportive network of people they can consult when making difficult and important decisions, the final decision should be made by enterprise shareholders. The meaning lies in the accepting responsibility for the decisions.

Sadness as an emotional factor has an important impact on the behavior of shareholders of enterprises mentioned in our research, and in many cases it hinders rational thinking. Where it invokes negative emotions in people, it absorbs the thinking. It this case in is possible to assume that the shareholders will make incorrect decisions in the first phase and the feedback can reveal that the choice of the variant was not correct.

Shareholders of WW and FMT enterprises should accept individual behavioral aspects that have a significant impact on their decision-making. It is, therefore, necessary to understand the meaning of the impact of individual factors on their decision-making process in the enterprise and thus in time prevent the negative effect on their rational thinking.

5. Discussion

The paper dealt with the correlation and relationship among specified behavioral factors of a human being and decision-making: the financial decision-making of enterprise shareholders and managers. It is also necessary to compare our results with similar research topics, as is presented below.

Reference [

68] founded that simplicity became the magic word in the area of financial engineering. It is necessary to make financial information relevant, simple and accessible for managers and investors in order that they assume more responsibility. But this does not seem to work satisfactorily, because the problem is not the input of financial decision-making but the output. The impediment for making financial and investment decisions is not cognitive but emotional. At the center of this emotional obstacles lies regret and the fear of regret. Many research papers in psychology and behavioral economics documents this phenomenon. People are often reluctant to take decisions if they expect that they might regret them.

Reference [

69] explored in 2019 that most economic concepts assume a situation in which humans make logical, rational decisions by weighing all the factors and evidence out the most sensible choice. Behavioral economics, which explores how psychological, cognitive and emotional factors influence individual financial or investment decision-making processes, has gained importance and respect in recent times. Bad investment and financial decisions are often associated with emotions. According to [

69], the more complex the choice and more uncertain the subject is, the more emotions may influence the decision and these emotions are often irrational, especially in investment.

Reference [

70] examined the irrational financial decisions of investors and shareholders in the behavioral finance. He found that emotional and cognitive factors have a strong impact on investors’ decision-making process. Some of the factors that affect investors’ decision-making processes are loss aversion, overconfidence, over- and under-reaction, and herd behavior. Reference [

71] examined the impact of investors’ psychological and behavioral elements on investors’ decision-making process. They make their investment decisions rather on behavioral factors including mental accounting, cognitive dissonance, greed, fear and heuristics. In this context, studies have examined the effect of cognitive and arbitrage limits on investment decisions with varied results. Behavioral finance offers alternatives for making investment decisions. During the financial crises of 2008, most investors suffered due to their behavioral attitudes. Also reference [

72] came to similar results like our research. They developed theoretical concepts which suggests that investors generally have behavioral features like self-attribution and overconfidence. Thus, due to the lack of skills and overconfidence, these investors generally make inaccurate investment decisions. Past studies have found that some investors due to their behavior, including the disposition effect, over-confidence and misguided beliefs, bear heavy losses in their stock investment.

Another research study presented by [

21] dealing with emotional behavioral factors on the decision-making of managers confirmed our findings. The study has presented some important recommendations for companies that want to know more about how managers respond in certain emotionally charged situations. First, evidence from brain activity confirmed that emotions are important driver of decisions. Emotional responses are hardwired into every person’s brain, so there may be ramifications to companies whose workplace environments heighten employees’ emotional reactions or that pit colleagues against one another. Companies must acknowledge these responses and focus on developing ways to reduce their negative impact.

Second, while using performance-based pay is costly to companies, it leads managers to make more economically optimal choices. Performance-based pay may be effective in any company in which employees need to “slow-down” their decision-making to consider more carefully the importance of a variety of information (including emotion-based cues). When a manager has a strong tendency to rely on his/her instincts during decision-making, or if emotional factors affect his/her decisions, performance-based pay can help prompt more-deliberative decision-making, align economic interests, and lead to more profitable alternatives. Performance-based awards may benefit companies that rely on employee expertise based on their extensive knowledge and past experience. This finding was assumed in hypothesis H2.

Third, this new understanding of the effects of something that the company has control over, the design of pay and awards plans, raise the possibility that other factors the company can control, such as monitoring, decision prompts, task instructions, written or verbal commitments to conduct business in a certain way, can prompt similar processing changes and thus lead to greater and sustainable economic benefits.

Our research found that the hypothesis H1 has been confirmed by the graphical evaluation, i.e., the assumption that people are rational, and their behavior corresponds to that. Emotions such as fear, love and hatred are the source of cases when people change their behavior and deviate from rationality.

Another part of the results was focused on investigating the impact of cognitive, psychological and emotional factors on the behavior of shareholders in decision-making situations. Respondents could select several aspects belonging to groups of cognitive, psychological and emotional factors.

The second research question about the impact evaluation of behavioral (cognitive, psychological and emotional) factors has revealed that the key factors that most influence the rational decision-making behavior of shareholders of WW and FMT enterprises are the expertise as a cognitive factor, certainty as psychological and happiness with sadness as an emotional factor. Based on the

p-level (0.00824), the null hypothesis in favor of the alternative hypothesis was rejected, implying a dependence between the influence of expertise as a cognitive factor and shareholders of WW and FMT enterprises (

Table 1).

Based on the statistical data evaluation of the impact of security on internal interest groups, it was possible to confirm the interdependence between individual variables (

Table 2). Due to the value of the

p level (0.00000), the null hypothesis was rejected in favor of the alternative hypothesis, with confirmation of the existence of dependence between the shareholders of WW and FMT enterprises and certainty as a psychological factor.

By comparing the

p level (0.01817) with the selected significance level (α = 0.05), the null hypothesis was rejected (

Table 3). The rejection of the null hypothesis in favor of the alternative hypothesis confirmed the existence of dependence between happiness as an emotional factor and shareholders of WW and FMT enterprises.

Based on statistical observation, the

p level was lower than the significance level (0.00000 < 0.5), which has led to the rejection of the null hypothesis in favor of the alternative hypothesis, i.e., the existence of dependence between the sadness as an emotional factor and shareholders of WW and FMT enterprises (

Table 4).

Hypotheses H2, H3 and H4 have been confirmed by the mathematical-statistical analysis of the impact of behavioral (cognitive, psychological and emotional) factors. These include expertise (cognitive factor), certainty (psychological factor), happiness and sadness (emotional factors). The key behavioral aspects have contributed to the formulation of conclusions and recommendations aimed at the elimination of systematic errors in the financial decision-making of shareholders of WW and FMT enterprises.

6. Conclusions

Entrepreneurship is a long-term, demanding process that requires the high level of involvement of enterprise shareholders. Shareholders are more important for the sustainability of a business. The performance of enterprise shareholders depends principally on their knowledge and experience. It is important to make the right decision and to have a sense of responsibility. It is essential to be able to communicate, feel empathetically, listen, be tolerant to others, and have the ability of self-control in coping with stressful situations. Behavioral factors such as expertise, certainty, happiness and sadness inherently affect the behavior of shareholders in financial decisions in the enterprise.

A goal of this research was to identify and investigate the impact of significant cognitive, psychological and emotional factors affecting the financial decision-making of shareholders of woodworking and furniture making enterprises. The results confirmed that individuals are rational which is correspondent to their behavior. Emotions like fear, love and hatred are the reasons behind humans’ change of behavior and decline from rationality.

A very positive or positive agreement with this statement was expressed by 69.3% of respondents and only 7.90% of respondents expressed negative attitudes. Further research focused on investigating the impact of cognitive, psychological and emotional factors on the behavior of shareholders in decision-making situations. From the file of cognitive factors, expertise has the highest impact on rational behavior in the decision-making process of WW and FMT shareholders, which was confirmed by p-level (0.00824). Other significant cognitive factors are knowledge (67.6%) and logical thinking (56.7%). Insufficient experience and knowledge of business can lead to incorrect financial decisions that could jeopardize the sustainable existence of the business itself. Among the psychological factors, certainty (73.5%) is the most significant factor affecting the rational behavior of the shareholders, which was also confirmed by mathematical and statistical methods. Security (67.6%), personality (49.1%) and self-realization (46.2%) have also a considerable impact.

The last part of our research investigated impact of emotional factors. Happiness (declared by 76% of respondents) is the most important factor influencing the rational behavior of the shareholders in terms of emotional factors. The H4 hypothesis was confirmed by the presented results. Sadness (67.4%) as a counterpart of happiness is the second most significant emotional factor. Sadness has a significant impact on shareholder’s behavior change, and this effect can manifest itself in a positive way (positive thinking, avoiding negative and risk factors, talks) or in a negative way (failure to meet business objectives, worsening reputation, jeopardizing business existence). Love (40.2%) and hatred (39%) ranked among the following important factors.

According to the results, the authors designed the relevant decision-making concept which takes into account not only cognitive but also psychological and emotional factors and their influence on the decision-making process which could positively affect sustainable development of the above-mentioned type of enterprises. By the design of a relevant decision-making concept with the application of behavioral factors errors in shareholders’ financial decision-making can be eliminated, taking into account the sustainable development of WW and FMT enterprises. The proposed concept was designed based on the four identified key behavioral factors, expertise, certainty, happiness and sadness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}