Real Options Volatility Surface for Valuing Renewable Energy Projects

Abstract

1. Introduction

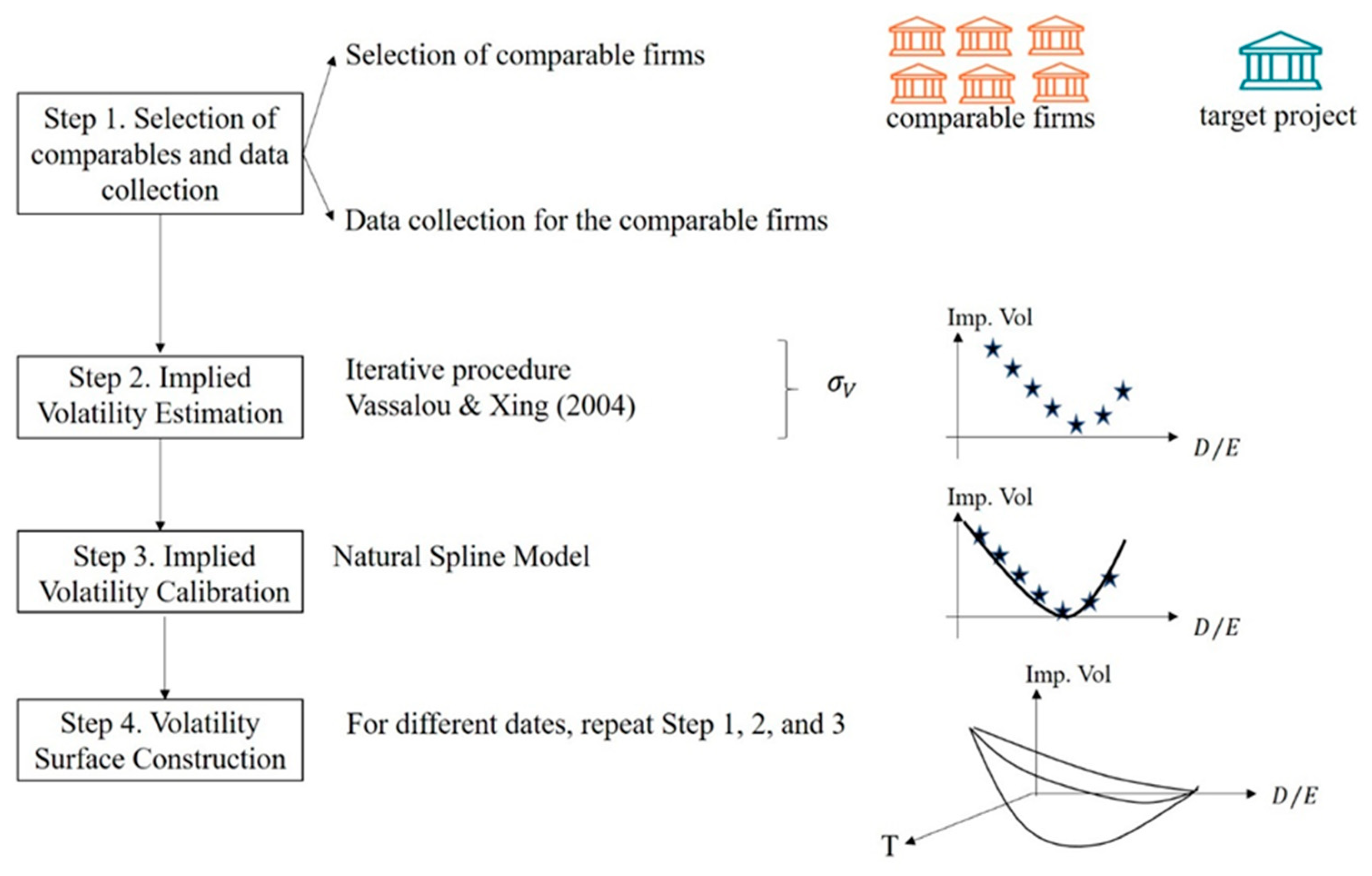

2. Materials and Methods

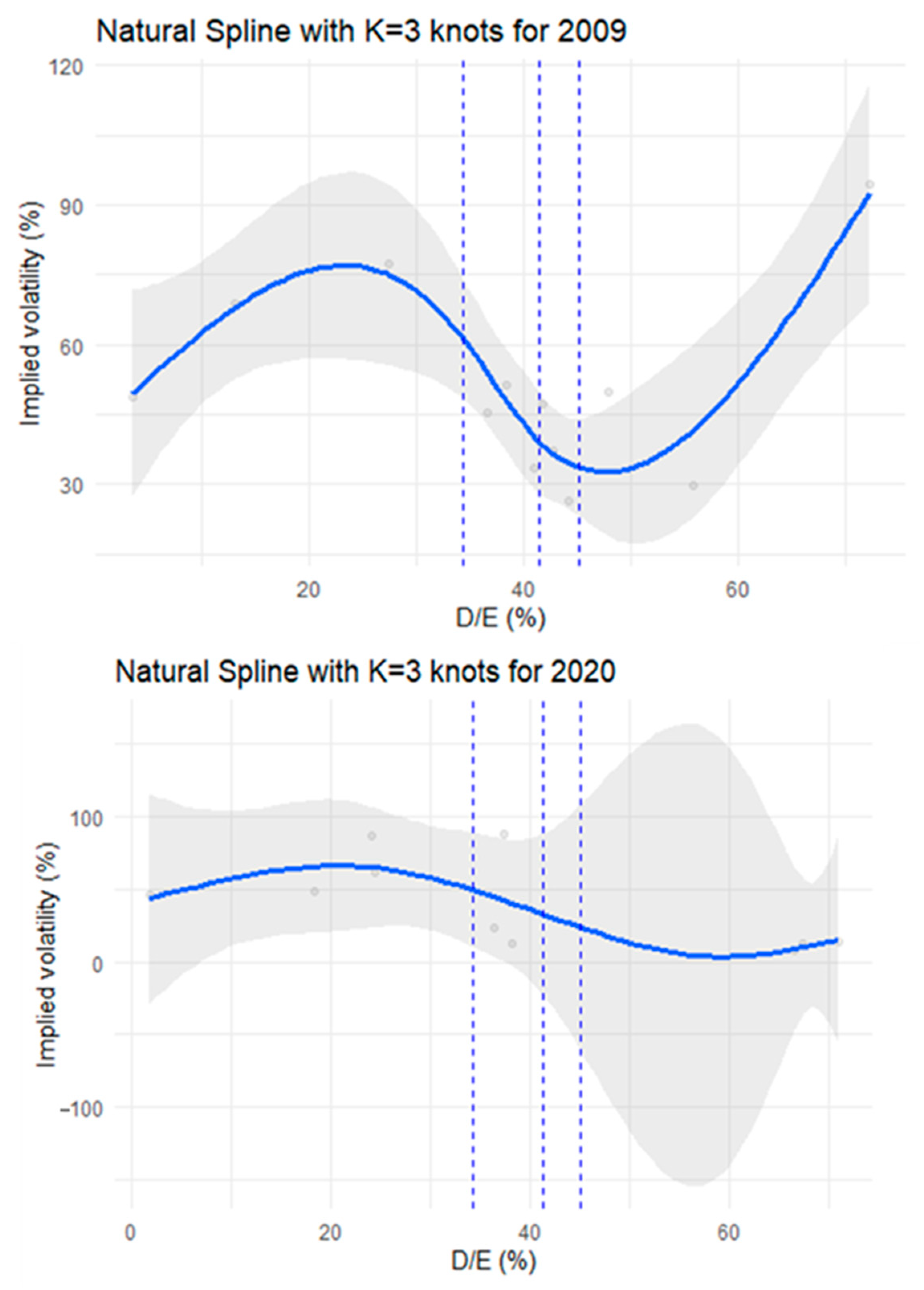

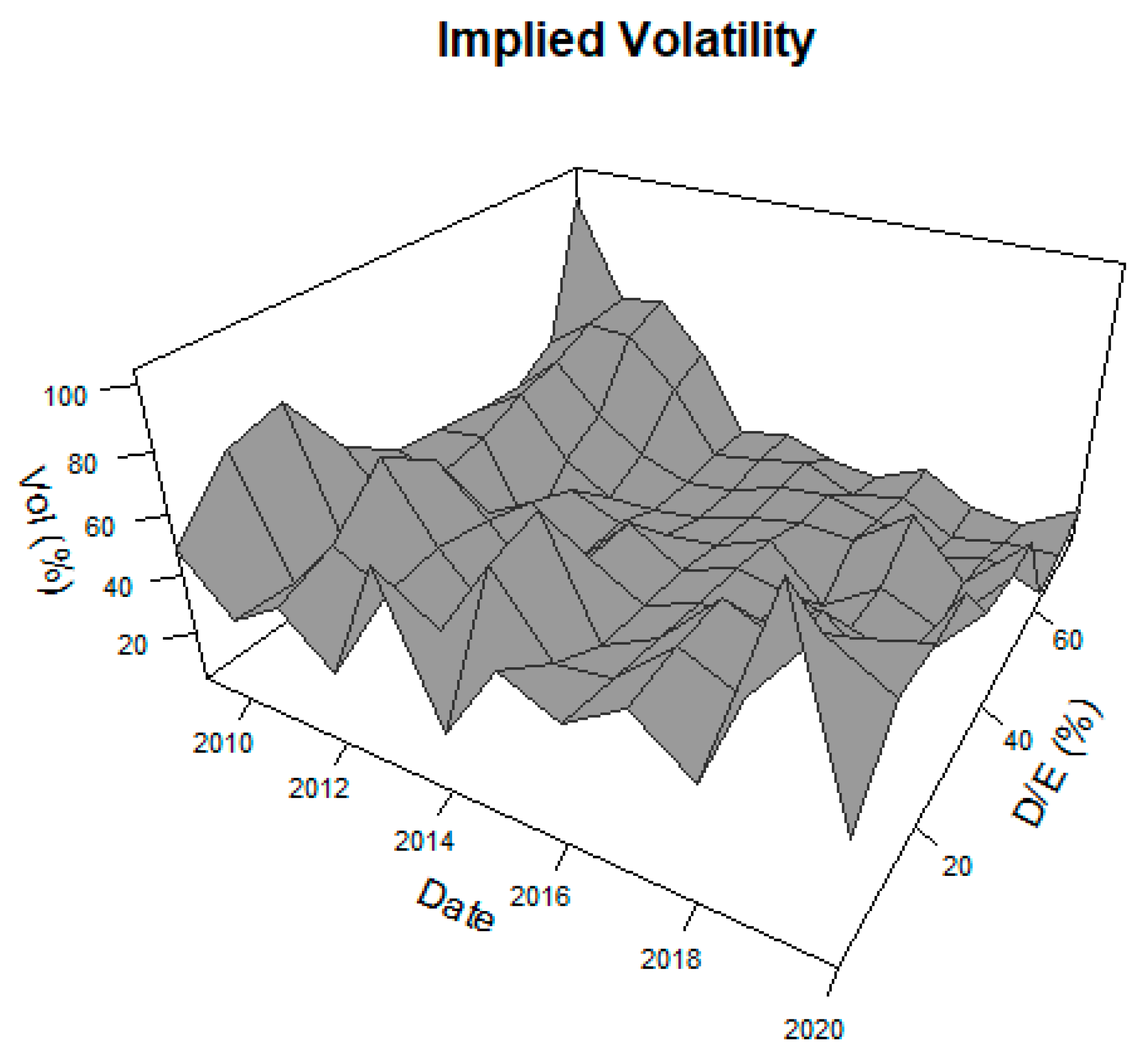

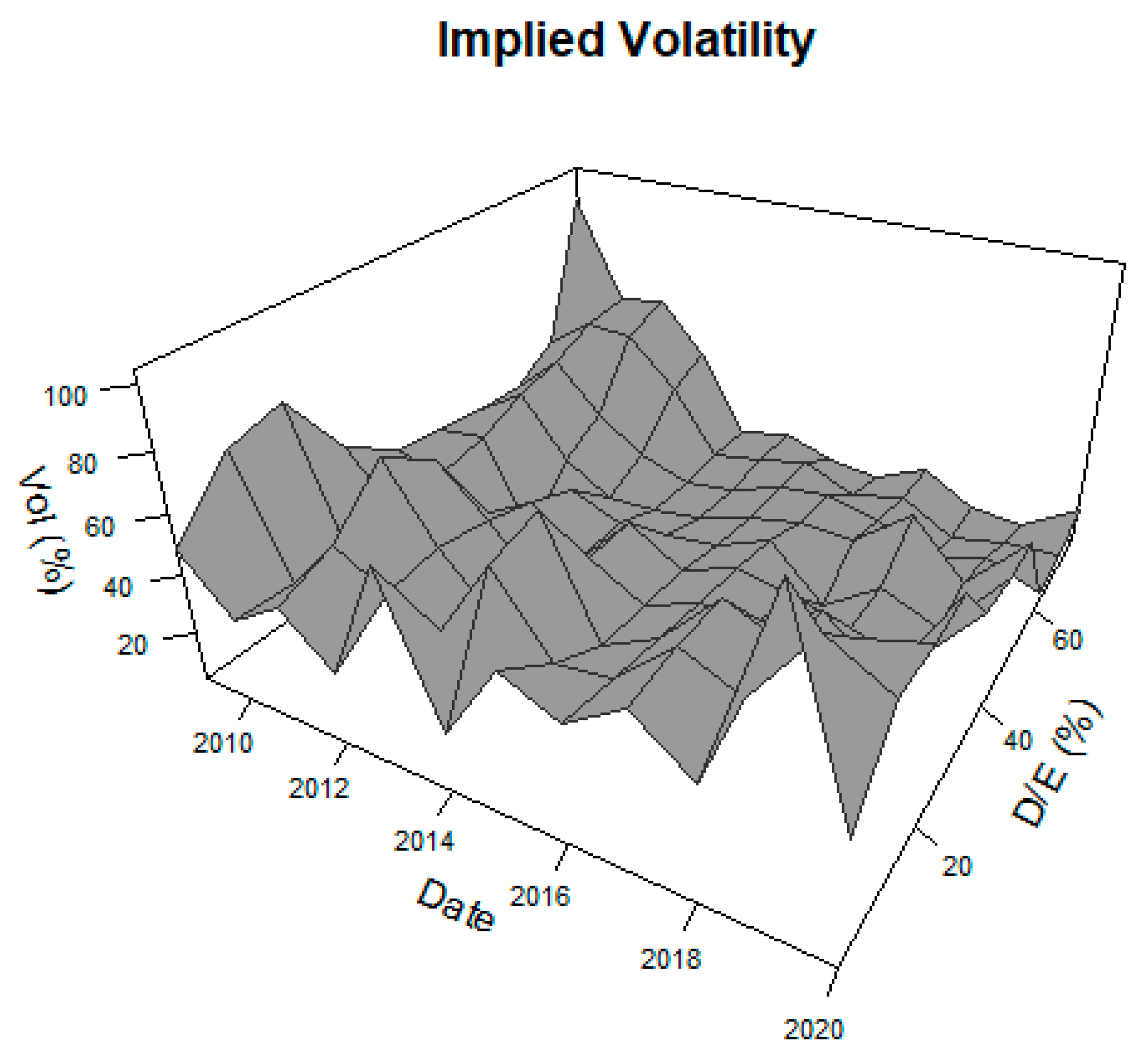

3. Results

- Case Study 1

- Case Study 2

- Case Study 3

4. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Liu, Y.; Zheng, R.; Chen, S.; Yuan, J. The economy of wind-integrated-energy-storage projects in China’s upcoming power market: A real options approach. Resour. Policy 2019, 63, 101434. [Google Scholar] [CrossRef]

- Aquila, G.; de Queiroz, A.R.; Balestrassi, P.P.; Junior, P.R.; Rocha, L.C.S.; Pamplona, E.O.; Nakamura, W.T. Wind energy investments facing uncertainties in the Brazilian electricity spot market: A real options approach. Sustain. Energy Technol. Assess 2020, 42, 100876. [Google Scholar] [CrossRef]

- Gupta, S.D. Using real options to value capacity additions and investment expenditures in renewable energies in India. Energy Policy 2021, 148, 111916. [Google Scholar] [CrossRef]

- Li, L.; Cao, X. Comprehensive effectiveness assessment of energy storage incentive mechanisms for PV-ESS projects based on compound real options. Energy 2020, 239, 121902. [Google Scholar] [CrossRef]

- Dixit, R.K.; Pindyck, R.S. Investment under Uncertainty; Princeton University Press: Princeton, NJ, USA, 1994. [Google Scholar]

- Cui, X.; Shibata, T. Investment strategies, reversibility, and asymmetric information. Eur. J. Oper. Res. 2017, 263, 1109–1122. [Google Scholar] [CrossRef]

- Li, Y.; Wu, M.; Li, Z. A real options analysis for RE investment decisions under China carbon trading market. Energies 2018, 11, 1817. [Google Scholar] [CrossRef]

- Smith, J.E. Alternative Approaches for Solving Real-Options Problems: (Comment on Brandão et al. 2005). Decis. Anal. 2005, 2, 89–102. [Google Scholar] [CrossRef]

- Godinho, P. Monte Carlo estimation of project volatility for real options analysis. J. Appl. Financ. 2006, 16, 15–30. [Google Scholar]

- Brandão, L.E.; Dyer, J.S.; Hahn, W.J. Volatility estimation for stochastic project value models. Eur. J. Oper. Res. 2012, 220, 642–648. [Google Scholar] [CrossRef]

- Ritzenhofen, I.; Spinler, S. Optimal design of feed-in-tariffs to stimulate RE investments under regulatory uncertainty—A real options analysis. Energy Econ. 2016, 53, 76–89. [Google Scholar] [CrossRef]

- Zhang, M.M.; Zhou, D.Q.; Zhou, P.; Chen, H.T. Optimal design of subsidy to stimulate RE investments: The case of China. Renew. Sust. Energ. Rev. 2017, 71, 873–883. [Google Scholar] [CrossRef]

- Lima, G.A.C.; Suslick, S.B. Estimating the volatility of mining projects considering price and operating cost uncertainties. Resour. Policy 2006, 31, 86–94. [Google Scholar] [CrossRef]

- Brach, M.A.; Paxson, D.A. A gene to drug venture: Poisson options analysis. R&D Manag. 2001, 31, 203–214. [Google Scholar]

- Mun, J. Real Options Analysis–Tools and Techniques for Valuing Strategic Investments and Decisions; John Wiley& Sons. Inc.: Hoboken, NJ, USA, 2002. [Google Scholar]

- Merton, R.C. On the pricing of corporate debt: The risk structure of interest rates. J. Financ. 1974, 29, 449–470. [Google Scholar]

- Lewis, N.A.; Eschenbach, T.G.; Hartman, J.C. Can we capture the value of option volatility? Eng. Econ. 2008, 53, 230–258. [Google Scholar] [CrossRef]

- Nicholls, G.M.; Lewis, N.A.; Zhang, L.; Jiang, Z. Breakeven volatility for real option valuation. Eng. Manag. J. 2014, 26, 49–61. [Google Scholar] [CrossRef]

- Godinho, P. Simulation-based estimation of state-dependent project volatility. Eng. Econ. 2018, 63, 188–216. [Google Scholar] [CrossRef]

- Myers, S.C.; Read, J.A. Real Options, Taxes and Financial Leverage (No. w18148); National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar] [CrossRef]

- Myers, S.C.; Read, J.A. Real Options and Hidden Leverage. J. Appl. Corp. Financ. 2022, 34, 67–80. [Google Scholar] [CrossRef]

- Byström, H. An alternative way of estimating asset values and asset value correlations. J. Fixed Income 2011, 21, 30–38. [Google Scholar] [CrossRef]

- Ronn, E.I.; Verma, A.K. Pricing risk-adjusted deposit insurance: An option-based model. J. Financ. 1986, 41, 871–895. [Google Scholar]

- Milidonis, A.; Stathopoulos, K. Do US insurance firms offer the “wrong” incentives to their executives? J. Risk Insur. 2011, 78, 643–672. [Google Scholar] [CrossRef]

- Duan, J.C. Maximum likelihood estimation using price data of the derivative contract. Math. Financ. 1994, 4, 155–167, Erratum in Math. Financ. 2000, 10, 461–462. [Google Scholar] [CrossRef]

- Ben-Abdellatif, M.; Ben-Ameur, H.; Chérif, R.; Fakhfakh, T. Quasi-maximum likelihood for estimating structural models. Les Cahiers GERAD ISSN 2021, 711, 2440. [Google Scholar]

- Vassalou, M.; Xing, Y. Default risk in equity returns. J. Financ. 2004, 59, 831–868. [Google Scholar] [CrossRef]

- Duan, J.C.; Gauthier, G.; Simonato, J.G. On the Equivalence of the KMV and Maximum Likelihood Methods for Structural Credit Risk Models; Groupe D’études et de Recherche en Analyse des Décisions: Montréal, QC, Canada, 2005. [Google Scholar]

- Christoffersen, B.; Lando, D.; Nielsen, S.F. Estimating volatility in the Merton model: The KMV estimate is not maximum likelihood. Math. Financ. 2022, 32, 1214–1230. [Google Scholar] [CrossRef]

- Lee, W.C. Redefinition of the KMV model’s optimal default point based on genetic-algorithms–Evidence from Taiwan. Expert Syst. Appl. 2011, 38, 10107–10113. [Google Scholar] [CrossRef]

- Charitou, A.; Dionysiou, D.; Lambertides, N.; Trigeorgis, L. Alternative bankruptcy rediction models using option-pricing theory. J. Bank Financ. 2013, 37, 2329–2341. [Google Scholar] [CrossRef]

- Doumpos, M.; Niklis, D.; Zopounidis, C.; Andriosopoulos, K. Combining accounting data and a structural model for predicting credit ratings: Empirical evidence from european listed firms. J. Bank Financ. 2015, 50, 599–607. [Google Scholar] [CrossRef]

- Afik, Z.; Arad, O.; Galil, K. Using Merton model for default prediction: An empirical assessment of selected alternatives. J. Empir. Financ. 2016, 35, 43–67. [Google Scholar] [CrossRef]

- Andreou, C.K.; Lambertides, N.; Panayides, P.M. Distress risk anomaly and misvaluation. Br. Account. Rev. 2021, 53, 100972. [Google Scholar] [CrossRef]

- Levine, O.; Wu, Y. Asset Volatility and Capital Structure: Evidence from Corporate Mergers. Manag. Sci. 2021, 67, 2773–2798. [Google Scholar] [CrossRef]

- Zhang, J.; He, L.; An, Y. Measuring banks’ liquidity risk: An option-pricing approach. J. Bank Financ. 2020, 111, 105703. [Google Scholar] [CrossRef]

- Lovreta, L.; Silaghi, F. The surface of implied firm’s asset volatility. J. Bank Financ. 2020, 112, 105253. [Google Scholar] [CrossRef]

- Forssbæck, J.; Vilhelmsson, A. Predicting Default–Merton vs. Leland. Leland. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2914545 (accessed on 9 February 2017).

- Christoffersen, B. Distance to Default Package. 2020. Available online: https://cran.r-project.org/web/packages/DtD/vignettes/Distance-to-default.pdf (accessed on 19 March 2023).

- Bharath, S.T.; Shumway, T. Forecasting default with the Merton distance to default model. Rev. Financ. Stud. 2008, 21, 1339–1369. [Google Scholar] [CrossRef]

- Amaya, D.; Boudreault, M.; McLeish, D.L. Maximum likelihood estimation of first-passage structural credit risk models correcting for the survivorship bias. J. Econ. Dyn. Control 2019, 100, 297–313. [Google Scholar] [CrossRef]

- Hastie, T.J. Generalized additive models. In Statistical Models in S; Chambers, J.M., Hastie, T.J., Eds.; Wadsworth & Brooks/Cole: Pacific Grove, CA, USA, 1992. [Google Scholar]

- Eissa, M.A.; Tian, B. Lobatto-Milstein Numerical Method in Application of Uncertainty Investment of Solar Power Projects. Energies 2017, 10, 43. [Google Scholar] [CrossRef]

- Abadie, L.M.; Chamorro, J.M. Valuation of real options in crude oil production. Energies 2017, 10, 1218. [Google Scholar] [CrossRef]

- Kroniger, D.; Madlener, R. Hydrogen storage for wind parks: A real options evaluation for an optimal investment in more flexibility. Appl. Energy 2014, 136, 931–946. [Google Scholar] [CrossRef]

- Binder, W.R.; Paredis, C.J.J.; Garcia, H.E. The Value of Flexibility in the Design of Hybrid Energy Systems: A Real Options Analysis. IEEE Power Energy Technol. Syst. J. 2017, 4, 74–83. [Google Scholar] [CrossRef]

- Martinez-Cesena, E.A.; Mutale, J. Wind Power Projects Planning Considering Real Options for the Wind Resource Assessment. IEEE Trans. Sustain. Energy 2012, 3, 158–166. [Google Scholar]

- McDonald, R.; Siegel, D. The value of waiting to invest. Quart. J. Econ. 1986, 101, 707–727. [Google Scholar] [CrossRef]

- Torani, K.; Rausser, G.; Zilberman, D. Innovation subsidies versus consumer subsidies: A real options analysis of solar energy. Energy Policy 2016, 92, 255–269. [Google Scholar] [CrossRef]

- Elder, J.; Serletis, A. Volatility in Oil Prices and Manufacturing Activity: An Investigation of Real Options. Macroecon Dyn. 2011, 15 (Suppl. 3), 379–395. [Google Scholar] [CrossRef]

- Passos, A.C.; Street, A.; Barroso, L.A. A Dynamic Real Option-Based Investment Model for Renewable Energy Portfolios. IEEE Trans. Power Syst. 2017, 32, 883–895. [Google Scholar] [CrossRef]

- Ghamkhari, M.; Wierman, A.; Mohsenian-Rad, H. Energy Portfolio Optimization of Data Centers. IEEE Trans. Smart Grid 2017, 8, 1898–1910. [Google Scholar] [CrossRef]

- Belz, A.; Giga, A. Of Mice or Men: Management of Federally Funded Innovation Portfolios with Real Options Analysis. IEEE Eng. Manag. Rev. 2018, 46, 1–35. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| 2009 | Mean | Median | ||||||||||||

| Lev (%) | 3.55 | 13.01 | 27.33 | 36.56 | 40.93 | 42.71 | 44.19 | 47.91 | 55.79 | 72.23 | 38.42 | 41.82 | Min | Max |

| Vol (%) | 48.79 | 68.75 | 77.45 | 45.41 | 33.48 | 37.27 | 26.37 | 49.85 | 29.88 | 94.58 | 51.18 | 47.10 | 26.37 | 94.58 |

| 2010 | Mean | Median | ||||||||||||

| Lev (%) | 3.48 | 10.59 | 23.08 | 29.36 | 36.00 | 40.15 | 46.25 | 49.44 | 58.98 | 63.15 | 36.05 | 38.07 | Min | Max |

| Vol (%) | 30.52 | 30.93 | 29.41 | 27.18 | 36.75 | 29.85 | 45.23 | 57.13 | 31.42 | 68.62 | 38.70 | 31.18 | 27.18 | 68.62 |

| 2011 | Mean | Median | ||||||||||||

| Lev (%) | 24.15 | 25.65 | 31.09 | 35.14 | 40.16 | 47.02 | 53.32 | 55.52 | 61.99 | 63.70 | 43.77 | 43.59 | Min | Max |

| Vol (%) | 52.77 | 32.01 | 87.41 | 36.75 | 28.06 | 5.65 | 8.42 | 47.38 | 28.02 | 75.73 | 40.22 | 34.38 | 5.65 | 87.41 |

| 2012 | Mean | Median | ||||||||||||

| Lev (%) | 16.47 | 26.76 | 36.15 | 38.52 | 42.10 | 44.89 | 51.33 | 57.06 | 60.86 | 61.78 | 43.59 | 43.49 | Min | Max |

| Vol (%) | 35.21 | 20.07 | 35.42 | 81.90 | 16.21 | 18.91 | 7.11 | 32.58 | 8.43 | 57.41 | 31.33 | 26.33 | 7.11 | 81.90 |

| 2013 | Mean | Median | ||||||||||||

| Lev (%) | 13.43 | 22.79 | 27.04 | 38.96 | 39.27 | 42.68 | 59.75 | 59.99 | 62.07 | 62.73 | 42.87 | 40.98 | Min | Max |

| Vol (%) | 69.63 | 33.49 | 21.17 | 6.20 | 40.15 | 9.92 | 13.02 | 10.15 | 19.81 | 3.37 | 22.69 | 16.42 | 3.37 | 69.63 |

| 2014 | Mean | Median | ||||||||||||

| Lev (%) | 12.96 | 22.84 | 24.75 | 38.47 | 38.68 | 44.70 | 57.41 | 58.79 | 63.50 | 71.50 | 43.36 | 41.69 | Min | Max |

| Vol (%) | 21.75 | 76.05 | 51.65 | 43.06 | 37.36 | 15.77 | 12.48 | 18.63 | 12.61 | 15.10 | 30.45 | 20.19 | 12.48 | 76.05 |

| 2015 | Mean | Median | ||||||||||||

| Lev (%) | 19.13 | 29.22 | 37.57 | 37.62 | 39.60 | 46.28 | 63.64 | 63.83 | 65.35 | 73.81 | 47.61 | 42.94 | Min | Max |

| Vol (%) | 47.76 | 49.74 | 17.70 | 9.08 | 45.73 | 21.74 | 21.07 | 24.81 | 12.24 | 9.66 | 25.95 | 21.41 | 9.08 | 49.74 |

| 2016 | Mean | Median | ||||||||||||

| Lev (%) | 19.85 | 30.35 | 33.59 | 36.71 | 38.30 | 41.80 | 59.80 | 61.99 | 71.70 | 74.95 | 46.91 | 40.05 | Min | Max |

| Vol (%) | 40.35 | 54.42 | 27.01 | 13.00 | 56.96 | 27.11 | 27.88 | 20.46 | 9.02 | 8.67 | 28.49 | 27.06 | 8.67 | 56.96 |

| 2017 | Mean | Median | ||||||||||||

| Lev (%) | 20.02 | 23.42 | 27.14 | 36.39 | 38.07 | 47.05 | 61.38 | 70.78 | 71.90 | 77.55 | 47.37 | 42.56 | Min | Max |

| Vol (%) | 32.07 | 85.44 | 68.98 | 23.88 | 7.14 | 34.39 | 22.16 | 17.93 | 6.72 | 5.33 | 30.40 | 23.02 | 5.33 | 85.44 |

| 2018 | Mean | Median | ||||||||||||

| Lev (%) | 20.56 | 26.76 | 28.25 | 31.43 | 38.24 | 56.78 | 63.71 | 71.60 | 72.27 | 72.32 | 48.19 | 47.51 | Min | Max |

| Vol (%) | 26.70 | 83.30 | 63.35 | 12.89 | 20.60 | 40.66 | 26.00 | 4.61 | 10.06 | 7.85 | 29.60 | 23.30 | 4.61 | 83.30 |

| 2019 | Mean | Median | ||||||||||||

| Lev (%) | 20.75 | 26.68 | 30.24 | 37.45 | 40.83 | 59.21 | 61.36 | 68.85 | 71.87 | 73.69 | 49.09 | 50.02 | Min | Max |

| Vol (%) | 113.38 | 35.74 | 101.68 | 20.18 | 15.00 | 33.00 | 10.69 | 9.66 | 5.43 | 9.11 | 35.39 | 17.59 | 5.43 | 113.38 |

| 2020 | Mean | Median | ||||||||||||

| Lev (%) | 1.83 | 18.28 | 24.12 | 24.47 | 36.37 | 37.37 | 38.12 | 66.57 | 67.37 | 70.98 | 38.55 | 36.87 | Min | Max |

| Vol (%) | 46.03 | 48.71 | 86.33 | 61.27 | 22.81 | 87.23 | 13.05 | 8.23 | 13.13 | 13.67 | 40.05 | 34.42 | 8.23 | 87.23 |

| Parameter | Symbol | Value | Unit |

|---|---|---|---|

| Current cash flow from investment | S | 302.8878 | $US million |

| Fixed investment cost | I | 340 | $US million |

| Time to invest | T | 25 | Years |

| Volatility | 0.1045 | ||

| Risk-free discount rate | r | 0.0875 |

| Kroniger and Madlener [45] | Lowest Vol (January 2014) | Highest Vol (January 2014) | |

|---|---|---|---|

| 0.2100 | 0.1248 | 0.7605 | |

| 1.9367 | 2.8209 | 1.1232 | |

| 0.2615 | 0.1598 | 0.6782 | |

| 2.0676 | 1.5492 | 9.1199 | |

| 1.0676 | 0.5492 | 8.1199 |

| Calculations Based on Torani et al. [49] | Mean Vol in 2013 (Our Study) | Median Vol in 2013 (Our Study) | |

|---|---|---|---|

| 0.2007 | 0.2269 | 0.1642 | |

| 0.0289 | 0.0289 | 0.0289 | |

| −0.0441 | −0.0441 | −0.0441 | |

| 1.0118 | 1.0111 | 1.0127 | |

| 0.0102 | 0.0102 | 0.0102 | |

| 0.8760 | 0.9285 | 0.8137 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

González-Muñoz, R.-I.; Molina-Muñoz, J.; Mora-Valencia, A.; Perote, J. Real Options Volatility Surface for Valuing Renewable Energy Projects. Energies 2024, 17, 1225. https://doi.org/10.3390/en17051225

González-Muñoz R-I, Molina-Muñoz J, Mora-Valencia A, Perote J. Real Options Volatility Surface for Valuing Renewable Energy Projects. Energies. 2024; 17(5):1225. https://doi.org/10.3390/en17051225

Chicago/Turabian StyleGonzález-Muñoz, Rosa-Isabel, Jesús Molina-Muñoz, Andrés Mora-Valencia, and Javier Perote. 2024. "Real Options Volatility Surface for Valuing Renewable Energy Projects" Energies 17, no. 5: 1225. https://doi.org/10.3390/en17051225

APA StyleGonzález-Muñoz, R.-I., Molina-Muñoz, J., Mora-Valencia, A., & Perote, J. (2024). Real Options Volatility Surface for Valuing Renewable Energy Projects. Energies, 17(5), 1225. https://doi.org/10.3390/en17051225