The Impact of Green Finance and Technological Innovation on Corporate Environmental Performance: Driving Sustainable Energy Transitions

Abstract

1. Introduction

2. Literature Review and Theoretical Analysis

2.1. Literature Review

2.1.1. Definition of Green Finance in Global Literature

2.1.2. Impact of Green Finance on Environmental Outcomes

2.1.3. Role of Technological Advances in Enhancing Environmental Performance:

2.1.4. Comparative Analysis on American, European, and Asian Markets

2.2. Theoretical Analysis

2.2.1. Green Finance Policy and Corporate Environmental Performance

2.2.2. Green Finance Policy, Innovation Input, and Corporate Environmental Performance

2.2.3. Green Finance Policy, Green Technology Innovation, and Corporate Environmental Performance

3. Research Design

3.1. Data Source and Justification

3.2. Model Construction

3.3. Variable Definition

4. Empirical Results and Analysis

4.1. Descriptive Statistics

4.2. Benchmark Regression

4.3. Mechanism Analysis

4.4. Heterogeneity Analysis

4.4.1. Firm Size Heterogeneity

4.4.2. Firm Nature Heterogeneity

4.4.3. Regional Heterogeneity

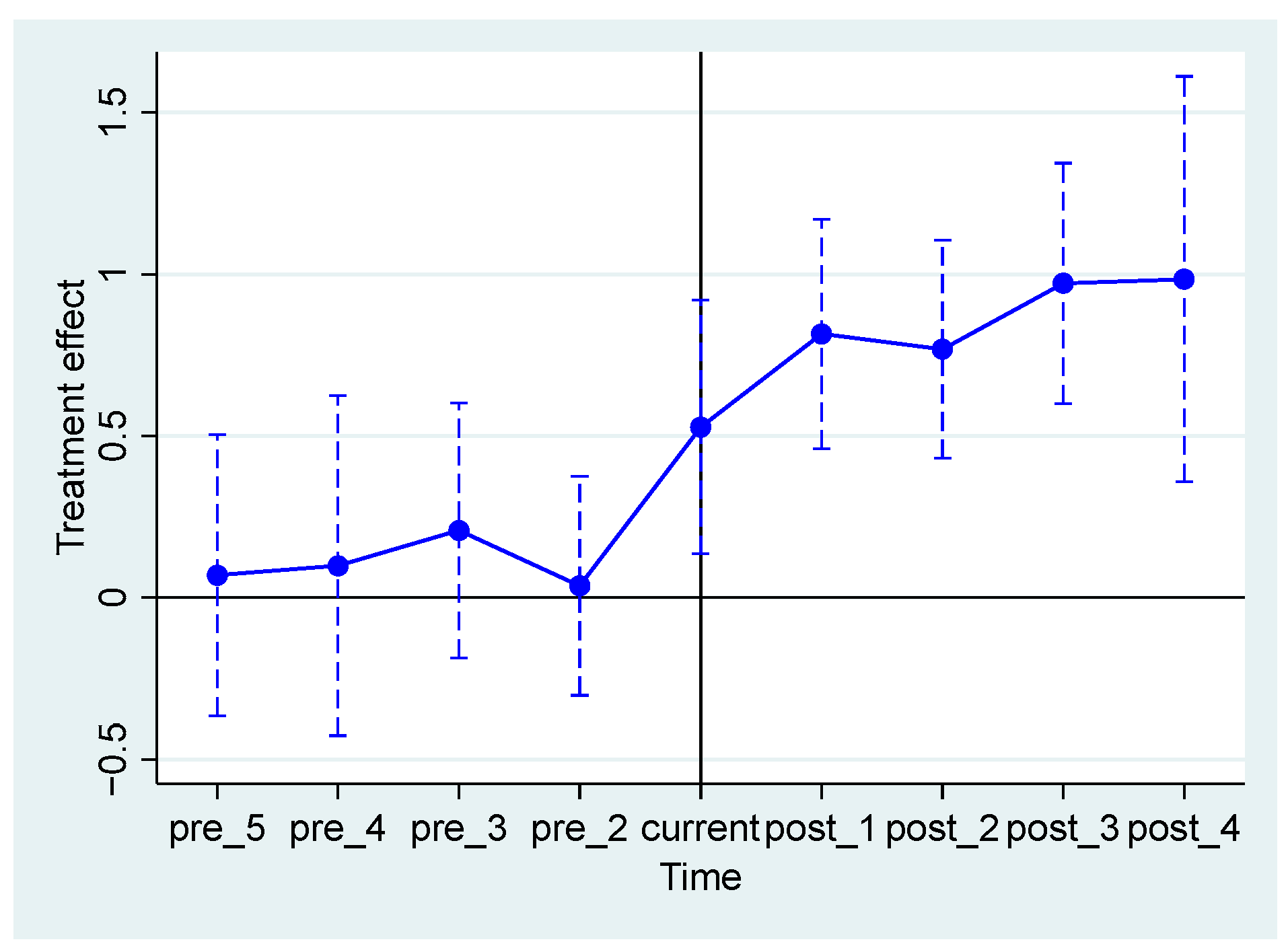

4.4.4. Parallel Trend Test

4.4.5. Placebo Test

4.4.6. PSM-DID

5. Discussion and Implications

5.1. Discussion

5.2. Implication

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Kandpal, V.; Jaswal, A.; Santibanez Gonzalez, E.D.; Agarwal, N. Challenges and Opportunities for Sustainable Energy Transition and Circular Economy. In Sustainable Energy Transition: Circular Economy and Sustainable Financing for Environmental, Social and Governance (ESG) Practices; Springer: Cham, Switzerland, 2024; pp. 307–324. [Google Scholar]

- Sovacool, B.K.; Griffiths, S.; Kim, J.; Bazilian, M. Climate change and energy security: A novel and adaptive policy framework. Energy Policy 2021, 158, 112544. [Google Scholar] [CrossRef]

- Zhou, M.; Li, X. Influence of green finance and renewable energy resources over the sustainable development goal of clean energy in China. Resour. Policy 2022, 78, 102816. [Google Scholar] [CrossRef]

- Alharbi, S.S.; Al Mamun, M.; Boubaker, S.; Rizvi, S.K.A. Green finance and renewable energy: A worldwide evidence. Energy Econ. 2023, 118, 106499. [Google Scholar] [CrossRef]

- Bhattacharyya, R. Green finance for energy transition, climate action and sustainable development: Overview of concepts, applications, implementation and challenges. Green Financ. 2022, 4, 1–35. [Google Scholar] [CrossRef]

- Mavlutova, I.; Spilbergs, A.; Verdenhofs, A.; Kuzmina, J.; Arefjevs, I.; Natrins, A. The Role of Green Finance in Fostering the Sustainability of the Economy and Renewable Energy Supply: Recent Issues and Challenges. Energies 2023, 16, 7712. [Google Scholar] [CrossRef]

- Bhatia, M.S.; Jakhar, S.K. Green finance and sustainable development: Empirical evidence from emerging economies. J. Clean. Prod. 2023, 384, 135369. [Google Scholar] [CrossRef]

- Zhang, D.; Mohsin, M.; Rasheed, A.K.; Chang, Y.; Taghizadeh-Hesary, F. The critical contribution of green finance towards sustainable development: Evaluating the model of technological innovation and sustainability in developing economies. Environ. Sci. Pollut. Res. 2022, 29, 8290–8303. [Google Scholar]

- Wang, Y.; Chen, Y.; Zhang, L.; Zhao, D. The impact of green finance on corporate environmental performance: Evidence from a systematic review and future research agenda. J. Clean. Prod. 2021, 311, 127637. [Google Scholar] [CrossRef]

- Calza, F.; Parmentola, A.; Tutore, I. Green technological innovation and environmental performance: The moderating role of stakeholder engagement. Bus. Strategy Environ. 2021, 30, 4001–4015. [Google Scholar] [CrossRef]

- Zhang, S.; Yu, X.; Zhao, L. Exploring the integration of green finance and innovation within corporate strategies: A case of China’s manufacturing sector. J. Environ. Manag. 2021, 302, 113979. [Google Scholar] [CrossRef]

- Cai, R.; Guo, J. Finance for the Environment: A Scientometrics Analysis of Green Finance. Mathematics 2021, 9, 1537. [Google Scholar] [CrossRef]

- Hesary-Taghizadeh, F.; Yoshino, N. Analyzing the Characteristics of Green Bond Markets to Facilitate Green Finance in the Post-COVID-19 World. Sustainability 2021, 13, 5719. [Google Scholar] [CrossRef]

- Musciano, C.B. Is Your Socially Responsible Investment Fund Green or Greedy? How a Standard ESG Disclosure Framework Can Inform Investors and Prevent Greenwashin. Ga. L. Rev. 2022, 57, 427. [Google Scholar]

- Zhang, L. The Role of Regulatory Oversight in Ensuring the Efficacy of Green Finance Investments. J. Environ. Res. 2022, 35, 145–160. [Google Scholar]

- Zhang, D.; Rong, Z.; Ji, Q. Green innovation and firm performance: Evidence from listed companies in China. Resour. Conserv. Recycl. 2019, 144, 48–55. [Google Scholar] [CrossRef]

- Shih, Y.-C.; Chiu, Y.-H. Green finance and climate change adaptation: Empirical evidence from Asia. J. Clean. Prod. 2021, 326, 129313. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Yoshino, N. Sustainable solutions for green finance and the challenges faced by the renewable energy sector. Int. J. Financ. Econ. 2021, 27, 412–430. [Google Scholar] [CrossRef]

- Babic, M. Green finance in the global energy transition: Actors, instruments, and politics. Energy Res. Soc. Sci. 2024, 111, 103482. [Google Scholar] [CrossRef]

- Flammer, C. Corporate green bonds. J. Financ. Econ. 2021, 142, 499–516. [Google Scholar] [CrossRef]

- Sharma, G.D.; Verma, M.; Shahbaz, M.; Gupta, M.; Chopra, R. Transitioning green finance from theory to practice for renewable energy development. Renew. Energy 2022, 195, 554–565. [Google Scholar] [CrossRef]

- Dikau, S.; Volz, U. Central Bank mandates, sustainability objectives and the promotion of green finance. Ecol. Econ. 2021, 184, 107022. [Google Scholar] [CrossRef]

- Bei, J.; Wang, C. Renewable energy resources and sustainable development goals: Evidence based on green finance, clean energy and environmentally friendly investment. Resour. Policy 2023, 80, 103194. [Google Scholar] [CrossRef]

- Zheng, C.; Deng, F.; Zhuo, C.; Sun, W. Green credit policy, institution supply and enterprise green innovation. Econ. Anal. 2022, 1, 20–34. [Google Scholar] [CrossRef]

- Wu, K.; Bai, E.; Zhu, H.; Lu, Z.; Zhu, H. Can green credit policy promote the high-quality development of China’s heavily-polluting enterprises? Sustainability 2023, 15, 8470. [Google Scholar] [CrossRef]

- Chien, F.S.; Ngo, Q.T.; Hsu, C.C.; Chau, K.Y.; Iram, R. Assessing the mechanism of barriers towards green finance and public spending in small and medium enterprises from developed countries. Environ. Sci. Pollut. Res. Int. 2021, 28, 60495–60510. [Google Scholar] [CrossRef]

- Chai, S.; Zhang, K.; Wei, W.; Ma, W.; Abedin, M.Z. The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. J. Clean. Prod. 2022, 363, 132458. [Google Scholar] [CrossRef]

- Fan, H.; Peng, Y.; Wang, H.; Xu, Z. Greening through finance? J. Dev. Econ. 2021, 152, 102683. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Wang, Z.; Huang, Z. Green loan and subsidy for promoting clean production innovation. J. Clean. Prod. 2018, 187, 421–431. [Google Scholar] [CrossRef]

- Li, S.; Zhang, W.; Zhao, J. Does green credit policy promote the green innovation efficiency of heavy polluting industries?—Empirical evidence from China’s industries. Environ. Sci. Pollut. Res. Int. 2022, 29, 46721–46736. [Google Scholar] [CrossRef]

- Guo, J. Impact of environmental regulation on green technological innovation: Chinese evidence of the Porter effect. China Fin. Econ. Rev. 2019, 8, 96–115. [Google Scholar]

- Luo, S.; He, G. Research on the influence of emission trading system on enterprises’ green technology innovation. Discret. Dyn. Nat. Soc. 2022, 2022, 1694001. [Google Scholar] [CrossRef]

- Zhu, J.; Fan, C.; Shi, H.; Shi, L. Efforts for a circular economy in China: A comprehensive review of policies. J. Ind. Ecol. 2019, 23, 110–118. [Google Scholar] [CrossRef]

- Chen, Q.; Ning, B.; Pan, Y.; Xiao, J. Green finance and outward foreign direct investment: Evidence from a quasi-natural experiment of green insurance in China. Asia Pac. J. Manag. 2021, 39, 899–924. [Google Scholar] [CrossRef]

- Chen, H.; Yao, M.; Chong, D. Research on institutional innovation of China’s green insurance investment. J. Ind. Integr. Mgmt. 2019, 04, 1950003. [Google Scholar] [CrossRef]

- Hu, Y.; Du, S.; Wang, Y.; Yang, X. How does green insurance affect green innovation? Evidence from China. Sustainability 2023, 15, 12194. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, H. The relationship between corporate environmental performance and environmental disclosure in China. Bus. Strategy Environ. 2019, 28, 471–482. [Google Scholar]

- Wang, Z.; Xu, L.; Du, J. How does green finance impact environmental performance? Evidence from China. J. Clean. Prod. 2020, 258, 120711. [Google Scholar]

- Liu, R.; He, F.; Ren, J. Promoting or inhibiting? The impact of enterprise environmental performance on economic performance: Evidence from China’s large iron and steel enterprises. Sustainability 2021, 13, 6465. [Google Scholar] [CrossRef]

- Tao, H.; Zhuang, S.; Xue, R.; Cao, W.; Tian, J.; Shan, Y. Environmental finance: An interdisciplinary review. Technol. Forecast. Soc. Change 2022, 179, 121639. [Google Scholar] [CrossRef]

- Sharma, G.D.; Verma, M.; Shahbaz, M.; Gupta, M.; Chopra, R. Green technological innovation, green finance, and financial development and their role in green total factor productivity: Empirical insights from China. J. Clean. Prod. 2023, 382, 135131. [Google Scholar]

- Xu, B.; Li, S.; Afzal, A.; Mirza, N.; Zhang, M. The impact of financial development on environmental sustainability: A European perspective. Resour. Policy 2022, 78, 102814. [Google Scholar] [CrossRef]

- Wang, L.; Long, Y.; Li, C. Research on the impact mechanism of heterogeneous environmental regulation on enterprise green technology innovation. J. Environ. Manag. 2022, 322, 116127. [Google Scholar] [CrossRef] [PubMed]

- Samour, A.; Baskaya, M.M.; Tursoy, T. The impact of financial development and FDI on renewable energy in the UAE: A path towards sustainable development. Sustainability 2022, 14, 1208. [Google Scholar] [CrossRef]

- Usman, O.; Alola, A.A.; Akadiri, S. Saint Effects of Domestic Material Consumption, Renewable Energy, and Financial Development on Environmental Sustainability in the EU-28: Evidence from a GMM Panel-VAR. Renew. Energy 2022, 184, 239–251. [Google Scholar] [CrossRef]

- Musa, M.S.; Jelilov, G.; Iorember, P.T.; Usman, O. Effects of Tourism, Financial Development, and Renewable Energy on Environmental Performance in EU-28: Does Institutional Quality Matter? Environ. Sci. Pollut. Res. 2021, 28, 53328–53339. [Google Scholar] [CrossRef]

- Shahbaz, M.; Topcu, B.A.; Sarıgül, S.S.; Vo, X.V. The Effect of Financial Development on Renewable Energy Demand: The Case of Developing Countries. Renew. Energy 2021, 178, 1370–1380. [Google Scholar] [CrossRef]

- Zioło, M.; Bąk, I.; Spoz, A. Sustainable Energy Sources and Financial Development Nexus—Perspective of European Union Countries in 2013–2021. Energies 2024, 17, 3332. [Google Scholar] [CrossRef]

- Yan, Q.; Wan, K. Energy-Consuming Right Trading Policy and Corporate ESG Performance: Quasi-Natural Experimental Evidence from China. Energies 2024, 17, 3257. [Google Scholar] [CrossRef]

- Yang, D.; Xie, Y. Corporate Social Responsibility, Green Innovation Capability, and Corporate Environmental Performance. Financ. Account. Mon. 2019, 6, 100–104. [Google Scholar] [CrossRef]

- de Freitas Netto, S.V.; Sobral, M.F.F.; Ribeiro, A.R.B.; da Luz Soares, G.R. Concepts and forms of greenwashing: A systematic review. Environ. Sci. Eur. 2020, 32, 19. [Google Scholar] [CrossRef]

- Santos, C.; Coelho, A.; Marques, A. A systematic literature review on greenwashing and its relationship to stakeholders: State of art and future research agenda. Manag. Rev. Q. 2024, 74, 1397–1421. [Google Scholar] [CrossRef]

- Chen, S.C.-I.; Xu, X.; Lu, S.; Jiang, W. Leveraging Information Technology and Data Analytics for Sustainable Corporate Practices: A Case Study on the Impact of Green Finance Policies. In Proceedings of the 2023 13th International Conference on Information Technology in Medicine and Education (ITME), Wuyishan, China, 24–26 November 2023; pp. 730–733. [Google Scholar] [CrossRef]

- Madaleno, M.; Nogueira, M.C. How Renewable Energy and CO2 Emissions Contribute to Economic Growth, and Sustainability—An Extensive Analysis. Sustainability 2023, 15, 4089. [Google Scholar] [CrossRef]

- Madaleno, M.; Dogan, E.; Taskin, D. A step forward on sustainability: The nexus of environmental responsibility, green technology, clean energy and green finance. Energy Econ. 2022, 109, 105945. [Google Scholar] [CrossRef]

- Zhang, G.; Chen, S.C.-I.; Yue, X. Blockchain Technology in Carbon Trading Markets: Impacts, Benefits, and Challenges—A Case Study of the Shanghai Environment and Energy Exchange. Energies 2024, 17, 3296. [Google Scholar] [CrossRef]

- Fu, C.; Lu, L.; Pirabi, M. Advancing green finance: A review of climate change and decarbonization. Digit. Econ. Sustain. Dev. 2024, 2, 1. [Google Scholar] [CrossRef]

- Hou, H.; Wang, Y.; Zhang, M. Green finance drives renewable energy development: Empirical evidence from 53 countries worldwide. Environ. Sci. Pollut. Res. 2023, 30, 80573–80590. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Symbol | Variable Definition |

|---|---|---|---|

| Explained variable | Corporate environmental performance | lnEP | The natural logarithm of the amount invested in environmental protection |

| Explanatory variable | Group dummy | Treat | The experimental group takes 1, and the control group takes 0 |

| Time dummy | Post | 2017 and later take 1; otherwise, take 0 | |

| Green finance policy | Treat × Post | The experimental group of enterprises in 2017 and later take 1; otherwise, take 0 | |

| Control variable | Enterprise scale | Size | The natural log of total assets |

| Asset–liability ratio | Lev | Ratio of total liabilities to total assets | |

| Return on assets | ROA | Ratio of net profit to total assets | |

| Asset operation capability | ATO | Operating income divided by total assets | |

| Enterprise growth | Growth | Increase in operating income divided by previous period operating income |

| Variables | Observations | Mean Value | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| lnEP | 1193 | 17.02 | 2.331 | 8.294 | 27.95 |

| did | 1193 | 0.342 | 0.475 | 0 | 1 |

| treat | 1193 | 0.647 | 0.478 | 0 | 1 |

| post | 1193 | 0.495 | 0.500 | 0 | 1 |

| size | 1193 | 22.93 | 1.505 | 19.20 | 28.55 |

| lev | 1193 | 0.446 | 0.199 | 0.037 | 1.345 |

| ROA | 1193 | 0.053 | 0.223 | −0.683 | 7.445 |

| ATO | 1193 | 0.716 | 0.489 | 0.036 | 8.601 |

| Growth | 1193 | 0.083 | 0.143 | −1.315 | 0.837 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | lnEP | lnEP | lnEP | lnEP |

| did | 1.174 *** | 1.014 *** | 1.345 *** | 1.422 *** |

| (8.50) | (4.80) | (12.24) | (8.58) | |

| size | 0.793 *** | 0.818 *** | ||

| (18.57) | (17.87) | |||

| lev | 0.741 ** | 0.579 | ||

| (2.08) | (1.60) | |||

| ROA | −0.005 | 0.033 | ||

| (−0.03) | (0.21) | |||

| ATO | 0.417 *** | 0.403 *** | ||

| (2.78) | (2.73) | |||

| Growth | 0.208 | 0.172 | ||

| (0.47) | (0.37) | |||

| Constant | 16.619 *** | 16.226 *** | −2.264 ** | −2.243 ** |

| (205.64) | (33.16) | (−2.52) | (−2.32) | |

| Year | NO | YES | NO | YES |

| Observations | 1193 | 1193 | 1193 | 1193 |

| adj.R2 | 0.0563 | 0.0619 | 0.367 | 0.369 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | R&D Investment | R&D Personnel | Apply for a Patent Independently | Joint Patent Application |

| did | 1.278 *** | 1.378 *** | 1.424 *** | 1.623 *** |

| (0.167) | (0.167) | (0.220) | (0.211) | |

| RD × did | 13.494 *** | |||

| (3.789) | ||||

| RP × did | 0.098 *** | |||

| (0.017) | ||||

| Gredl × did | 0.117 * | |||

| (0.064) | ||||

| Grelh × did | 0.514 *** | |||

| (0.115) | ||||

| size | 0.777 *** | 0.784 *** | 0.933 *** | 0.917 *** |

| (0.049) | (0.054) | (0.060) | (0.061) | |

| lev | 0.304 | 0.736 * | 0.386 | 0.431 |

| (0.387) | (0.418) | (0.478) | (0.482) | |

| ROA | 1.165 | 1.632 | 0.391 | 0.556 |

| (1.867) | (1.970) | (2.130) | (2.135) | |

| ATO | 0.354 ** | 0.532 *** | 0.234 | 0.197 |

| (0.176) | (0.206) | (0.150) | (0.148) | |

| Growth | −0.016 | 0.307 | −0.666 | −0.672 |

| (0.689) | (0.742) | (0.910) | (0.908) | |

| Constant | −0.942 | −1.283 | −4.484 *** | −4.231 *** |

| (1.004) | (1.194) | (1.281) | (1.290) | |

| Year | YES | YES | YES | YES |

| Observations | 1089 | 909 | 733 | 733 |

| adj.R2 | 0.404 | 0.428 | 0.399 | 0.398 |

| (1) | (2) | |

|---|---|---|

| Variables | Large Enterprises | Small and Medium Enterprises |

| did | 1.453 *** | 1.375 *** |

| (0.212) | (0.269) | |

| size | 0.694 *** | 0.699 *** |

| (0.082) | (0.128) | |

| lev | 0.342 | 0.560 |

| (0.534) | (0.502) | |

| ROA | −0.384 | −0.298 |

| (1.744) | (0.388) | |

| ATO | 0.266 ** | 0.640 * |

| (0.129) | (0.359) | |

| Growth | 0.531 | −0.105 |

| (0.821) | (0.651) | |

| Constant | 1.004 | 0.012 |

| (1.905) | (2.704) | |

| Year | YES | YES |

| Observations | 598 | 595 |

| adj.R2 | 0.270 | 0.132 |

| (1) | (2) | |

|---|---|---|

| Variables | State-Owned Enterprises | Non-State-Owned Enterprises |

| did | 2.050 *** | 1.051 *** |

| (0.280) | (0.216) | |

| size | 0.747 *** | 0.875 *** |

| (0.060) | (0.082) | |

| lev | 0.432 | 0.548 |

| (0.507) | (0.592) | |

| ROA | −2.361 | 1.969 |

| (2.149) | (3.534) | |

| ATO | 0.376 ** | 0.373 |

| (0.159) | (0.305) | |

| Growth | 0.017 | 0.780 |

| (0.811) | (1.364) | |

| Constant | −0.359 | −4.025 ** |

| (1.324) | (1.694) | |

| Year | YES | YES |

| Observations | 552 | 615 |

| adj.R2 | 0.391 | 0.292 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variables | Eastern Region | Central Region | Western Region |

| did | 1.446 *** | 1.413 ** | 0.600 |

| (0.194) | (0.547) | (0.603) | |

| size | 0.808 *** | 0.690 *** | 0.865 *** |

| (0.054) | (0.132) | (0.137) | |

| lev | 0.172 | 1.657 | 0.251 |

| (0.510) | (1.103) | (0.817) | |

| ROA | 3.277 | −1.946 | −10.314 ** |

| (2.587) | (3.952) | (4.085) | |

| ATO | 0.592 ** | 0.411 | 0.386 ** |

| (0.249) | (0.282) | (0.193) | |

| Growth | −0.302 | 0.716 | 3.389 ** |

| (1.225) | (1.479) | (1.546) | |

| Constant | −2.575 ** | 1.120 | −3.862 |

| (1.078) | (2.740) | (2.801) | |

| Year | YES | YES | YES |

| Observations | 728 | 205 | 198 |

| adj.R2 | 0.382 | 0.297 | 0.432 |

| (1) | |

|---|---|

| Variables | lnEP |

| pre_5 | 0.070 |

| (0.32) | |

| pre_4 | 0.099 |

| (0.37) | |

| pre_3 | 0.208 |

| (1.04) | |

| pre_2 | 0.037 |

| (0.22) | |

| current | 0.528 *** |

| (2.64) | |

| post_1 | 0.816 *** |

| (4.51) | |

| post_2 | 0.769 *** |

| (4.48) | |

| post_3 | 0.972 *** |

| (5.15) | |

| post_4 | 0.985 *** |

| (3.09) | |

| Constant | 16.755 *** |

| (273.49) | |

| Firm | YES |

| Observations | 1193 |

| adj.R2 | 0.0534 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | Full Sample | Nearest Neighbor Matching 1:1 | Nuclear Matching | Radius Matching |

| did | 1.422 *** | 1.483 *** | 1.422 *** | 1.422 *** |

| (8.58) | (8.19) | (8.59) | (8.58) | |

| size | 0.818 *** | 0.890 *** | 0.817 *** | 0.818 *** |

| (17.87) | (14.71) | (17.96) | (17.87) | |

| lev | 0.579 | 0.850 * | 0.590 | 0.579 |

| (1.60) | (1.78) | (1.65) | (1.60) | |

| ROA | 0.033 | 0.418 ** | 0.257 | 0.033 |

| (0.21) | (2.45) | (0.18) | (0.21) | |

| ATO | 0.403 *** | 0.200 | 0.396 *** | 0.403 *** |

| (2.73) | (1.29) | (2.70) | (2.73) | |

| Growth | 0.172 | 0.969 | 0.098 | 0.172 |

| (0.37) | (1.50) | (0.15) | (0.37) | |

| Constant | −2.243 ** | −4.329 *** | −2.245 ** | −2.243 ** |

| (−2.32) | (−3.36) | (−2.32) | (−2.32) | |

| Year | YES | YES | YES | YES |

| Observations | 1193 | 829 | 1192 | 1193 |

| adj.R2 | 0.369 | 0.429 | 0.369 | 0.369 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, S.C.-i.; Xu, X.; Own, C.-M. The Impact of Green Finance and Technological Innovation on Corporate Environmental Performance: Driving Sustainable Energy Transitions. Energies 2024, 17, 5959. https://doi.org/10.3390/en17235959

Chen SC-i, Xu X, Own C-M. The Impact of Green Finance and Technological Innovation on Corporate Environmental Performance: Driving Sustainable Energy Transitions. Energies. 2024; 17(23):5959. https://doi.org/10.3390/en17235959

Chicago/Turabian StyleChen, Sonia Chien-i, Xinlei Xu, and Chung-Ming Own. 2024. "The Impact of Green Finance and Technological Innovation on Corporate Environmental Performance: Driving Sustainable Energy Transitions" Energies 17, no. 23: 5959. https://doi.org/10.3390/en17235959

APA StyleChen, S. C.-i., Xu, X., & Own, C.-M. (2024). The Impact of Green Finance and Technological Innovation on Corporate Environmental Performance: Driving Sustainable Energy Transitions. Energies, 17(23), 5959. https://doi.org/10.3390/en17235959