1. Introduction

At the current stage, the Sustainable Development Goals have been firmly established in public consciousness. One of the manifestations of ecologically responsible behavior is the desire to minimize waste, particularly regarding the packaging of finished products [

1]. At the same time, the circular economy is gaining special importance, the specificity of which consists of the minimization of waste using the most complex production cycle. This allows not only achieving the goals of sustainable development, but also has a significant contribution to the global competitiveness of a country [

2,

3]. Thus, researchers have proven that the indicators that are a priority for the implementation of the circular economy also ensure significant progress in achieving the Sustainable Development Goals [

4,

5]. It is important that the role and scope of circular economy implementation are becoming more and more significant in the conditions of Industry 4.0 [

6,

7]. Ensuring maximum efficiency, comprehensive implementation of innovations and convenience for users becomes the task not only of individual companies, but also of entire cities and regions. It is manifested in the implementation of smart concept cities [

8], as well as in the development of the sharing economy [

9]. It is important that the development of the circular economy is formed under the influence of a significantly larger number of factors than other economic trends [

10]. In general, progress in achieving sustainable development goals related to clean energy has become increasingly noticeable recently [

11]. This is evidenced by the fact that the increase in the volume of energy production in countries does not lead to a proportional increase in greenhouse gas emissions [

12]. At the same time, renewable energy production is becoming increasingly large-scale and diversified [

13].

One of the main incentives for the development of alternative energy sources is ensuring the country’s energy security. For example, researchers prove that the level of energy security is higher precisely in those countries that have significant volumes of energy production from renewable sources or at least have their own energy production resources from non-renewable sources [

14]. It is quite interesting that modern empirical studies indicate that the dependence of GDP volumes on crude oil prices is observed only for oil-producing countries [

15]. This indicates a decrease in the energy dependence of the economy on fossil energy sources. On the other hand, one of the target criteria for the long-term development of the energy industry is to increase the efficiency of energy production. The relevance of energy efficiency is important not only in the context of energy, but also from the point of view of economic security [

16]. In addition, the significant role of energy efficiency for the formation of a carbon-neutral economy has been confirmed [

17]. At the same time, there is a rather close connection between the three directions of national security—economic, environmental and energy—which determines the complex nature of the impact of the energy efficiency growth and renewable energy on both national and global development [

18].

All this proves that at the current stage, the transition to environmentally safe energy production technologies requires the use of additional incentives. At the same time, it is necessary to study the effectiveness of individual regulatory instruments. This made it possible to form the purpose of the research as an assessment of the impact of environmental taxation on the processes of biofuel production and consumption.

2. Literature Review

It is important to correctly define the stimulating influence measures for the development of green energy. Environmental taxation has significant effectiveness in ensuring various aspects of national security. Thus, individual environmental taxes can simultaneously ensure the growth of environmental, energy and economic security [

19]. At the same time, in order to achieve the maximum effect, not only is the general level of environmental taxation important, but so is the combination of environmental taxes [

20]. For example, the existence of a significant impact of environmental taxes on emissions of harmful substances in agriculture has been proven, which, among other things, depends on the features of environmental tax reforms [

21]. In addition, the general conditions of the socio-economic development of a country are also important, which can strengthen or weaken the effectiveness of regulatory instruments [

22,

23,

24,

25]. Such factors include the general level of tax culture of the population [

26]. Globalization trends have led to significant convergence in the general conditions of environmental taxation, which is especially relevant for countries geographically close and in terms of economic development [

27]. On the other hand, it has been proven that the environmental effectiveness of environmental taxes depends on the quality of the tax system construction, as well as on the availability of non-tax instruments aimed at minimizing harmful effects, such as regulatory documents and directives [

28]. At the same time, retrospective studies show that in countries rich in natural resources, tax regulation has a less restrictive nature than in other countries [

29]. This creates long-term threats of depletion of resource potential and the state of the natural environment of such countries. It also discourages the transformational processes of transition to a green economy, which in the future threatens the country’s competitiveness.

At the current stage, green energy is becoming a factor affecting a significant number of economic processes. Thus, its significant role in transformations in international trade has been proven [

30]. At the same time, green energy can provide significant transformations of the carbon economy while maintaining the scale of functioning of all its branches [

31]. The global character of green energy is confirmed not only by ecological and economic effects, but also by its indirect impact on the health of the population [

32,

33]. It should be noted that the level of development of green energy still differs significantly between countries. However, the existence of both private and public activity regarding its development is important [

34].

Modern trends in the development of environmentally safe energy testify to the growing role of bioenergy. It not only has a smaller ecological footprint, but also increases the efficiency of the functioning of other industries from the point of view of maximizing the use of resources and ensuring recycling. It has been proven that the growth of the production of a type of biofuel such as ethanol implies an expansion in the cultivation of agricultural crops, which are raw materials for its production [

35]. At the same time, innovative projects and investment solutions that ensure the progress of sustainable development in agriculture are important today [

36]. Achieving the goals of sustainable development is often associated with the integration of various industries [

37]. The production of biofuel from food waste is an excellent example of the integration of the food and energy industries. Such integration will have a positive impact on both industries—on the one hand, increasing energy efficiency and the development of the green economy, and on the other hand, increasing the rationality of agriculture and improving food security [

38].

Reducing the level of emissions of harmful substances into the natural environment currently occupies an important place in the context of ensuring sustainable development. It is related to the preservation of the state of our planet and the leveling of the threats of climate change [

39,

40]. The idea of producing biofuel from food industry waste has a double positive effect on the state of the environment, as it allows minimizing unproductive environmental pollution. In this context, the sources of environmental pollution are both the processes of energy production and consumption, and the functioning of agriculture [

41]. At the same time, it has been empirically proven that the consumption of ethanol significantly reduces the total emissions of carbon dioxide. This reflects the positive environmental impact of replacing traditional energy sources with biofuel [

42]. On the other hand, it is determined that the observance of short supply chains in agriculture is not only a guarantee of its ecological development, but also a determinant of food security for the population [

43].

Modern empirical studies have also proven that financial incentives have always been more effective in ensuring the transition to more energy-efficient technologies than reputational factors and awareness of the importance of global goals. For example, the existence of a close connection between the scale of the shadow economy and the intensity of production and consumption of renewable energy has been proven [

44]. Moreover, the shadow economy is connected not only with economic manifestations, but also with environmental manifestations [

45].

Studies of economic and environmental competitiveness in the field of agriculture proved the existence of a weak dependence between them [

46]. Traditionally, the goal of any business is always about maximizing profit, which neglects resources and influences outside the company. However, recently, the resource crisis has become more and more noticeable, which shifts the emphasis to conducting green business, which, despite additional costs, has unconditional reputational benefits in the context of the spread of the concept of sustainable development [

47]. In the process of transformation of the ecological outlook of enterprises, ecological innovations play a significant role. They ultimately have a positive effect on both the ecological footprint of the functioning of enterprises and the economic growth of the country as a whole [

48,

49]. It has been proven that despite the lack of financial profits at the stages of development and implementation of ecological innovations, they can not only compensate for the economic result in the future, but also create additional value for the company, for example, in the form of its green brand [

50]. That is why, at the current stage, environmental projects should be considered not only as a response to regulatory influence, but also as investments in the development of companies [

51,

52]. At the same time, the determining factor in the growth of environmental responsibility of companies is precisely the position of its main stakeholders [

53,

54].

It has been proven that despite the unconditional importance of the transition of organizations to environmentally responsible practices, to ensure the transformation of organizational behavior in the direction of green changes, it is important to apply a comprehensive policy of change management. It will allow the most effective implementation of environmentally friendly technologies and products [

55,

56]. In particular, researchers note that the publicity of information about the level of compliance of the company’s activities with the goals of sustainable development ensures appropriate progress in achieving them [

57].

Recently, the concept of waste minimization and the factors that ensure it are gaining popularity. In this context, understanding the factors that determine such behavior is important. Researchers empirically confirm the influence of both external and internal factors on the environmentally responsible behavior of households [

58]. It has been proven that the reduction in household food waste is largely determined by the level of financial literacy of the population [

59]. This proves the fact that at the current stage, it is important to strengthen the educational component regarding the need for comprehensive support of initiatives to promote the goals of sustainable development [

60]. At the same time, it is interesting that the behavior of households is more ecologically responsible in relation to private objects than at work or in public places [

61]. In this regard, green training sessions organized by employers, which increase the level of environmental awareness of the population, are gaining popularity [

62]. Efforts to create a green brand of companies and green marketing in general also provide a significant effect of stimulating the population’s inclination to environmentally responsible behavior [

63]. Scientists have also proven that the inclination to green consumption is determined not only by the level of environmental knowledge, but also by the country’s cultural features [

64]. At the same time, energy efficiency remains a significant problem, not only in terms of optimizing energy consumption, but also in the context of minimizing the environmental pollution that occurs in the process of its consumption [

65]. Existing research proves that the development of the system of alternative energy production and consumption depends on a wide range of factors. On the other hand, research in the field of bioenergy production and consumption is quite poor. At the same time, this direction is promising from both a scientific and a practical perspective. Currently, there are only a few studies on determining the regulatory tools for the development of biofuels. Thus, existing research is limited by the general characteristics of the regulatory environment for bioenergy production (current taxes or existing tax incentives). At the same time, it is important to assess the impact of existing conditions of traditional energy taxation on the intensity of transformation of the structure of its production and consumption. In this regard, it was suggested that a significant level of taxation of producers and consumers of energy obtained from traditional sources stimulates their transition to the use of alternative energy. The proposed study has no analogues in modern scientific literature.

The purpose of the study is to identify meaningful and cause-and-effect relationships between environmental taxation and biofuel production and consumption. For this purpose, we combined bibliometric and panel regression modeling methods. The indicators of environmental taxation were chosen as revenue from energy taxes (which are handled to a greater extent by energy producers and provide for a higher level of taxation for traditional energy, as well as reduced or no taxation of alternative energy production), as well as revenue from transport taxes (which are paid by fuel consumers (car owners), and quite often the level of transport taxes depends on the type of fuel used by the car). The absolute volumes of biofuel production and consumption in several European countries were chosen as the parameters of biofuel development. Another task of the research was to determine the duration of achieving a significant effect of environmental taxes in stimulating the production and consumption of biofuels (by the introduction of different time lags into the model), as well as to define the specifics of the environmental taxes’ impact on the production and consumption of different types of biofuels (implemented by building separate evaluation models for biodiesel and ethanol production and consumption).

The proposed study has significant scientific and practical value. On the one hand, the expected results allow us to substantiate the potential of the state regulatory influence on the development of the bioenergy industry. On the other hand, the identified impacts make a significant contribution to increasing the effectiveness of forecasting the scale of biofuel production and consumption growth as a result of the application of regulatory tools. It might be useful also in the stage of planning the regulatory strategy for biofuel development.

3. Materials and Methods

This research consisted of the two stages (

Figure 1). In the first stage, contextual links between biofuels (bioenergy) and environmental taxation were investigated by the method of bibliometric analysis. In the second stage, the number of hypotheses about the impact of environmental taxes on biofuel production and consumption were substantiated and tested.

The first stage of the research involves the analysis of meaningful connections that arise in the process of scientific study of bioenergy and biofuel, as well as the connection of environmental taxation with them. To carry out this stage of the research, the VOSviewer version 1.6.17 bibliometric analysis toolkit was used. Publications indexed by the scientometric database Scopus were chosen as the basis for the bibliometric analysis. The first block of analysis is dedicated to identifying the most relevant directions of scientific research in the field of bioenergy and biofuel. For its implementation, 7973 articles with the categories “biofuel” and “bioenergy” found in the titles, list of keywords or abstracts were selected. The study made it possible to outline the areas of grouping of interests of scientists in the study of biofuel and bioenergy issues. Within the first block of this stage of the analysis, the evolution of the appearance of key words in scientific research was investigated, which made it possible to ascertain the achieved level of scientific thought in the study of biofuels and bioenergy. The second block of the first stage of research is related to the identification of key links between environmental taxation and the production and consumption of bioenergy and biofuel. For this, 314 articles indexed by the Scopus scientometric database were selected, which simultaneously refer to keywords such as “environmental tax” and “bioenergy” or “biofuel”. The result of the implementation of this block of research was the identification of the main tasks, methods and directions of the impact of environmental taxation on the production and consumption of biofuels. It allowed us to substantiate both the target orientation of environmental taxes and the main objects that can be taxed to ensure the stimulation of biofuel production.

The conducted theoretical research formed the basis for conducting an empirical analysis of the relationship between the parameters of environmental taxation and the production and consumption of biofuel. Its results made it possible to substantiate the working hypotheses of the study.

Hypothesis 1: Environmental taxes have a direct impact on both production and consumption of biofuels.

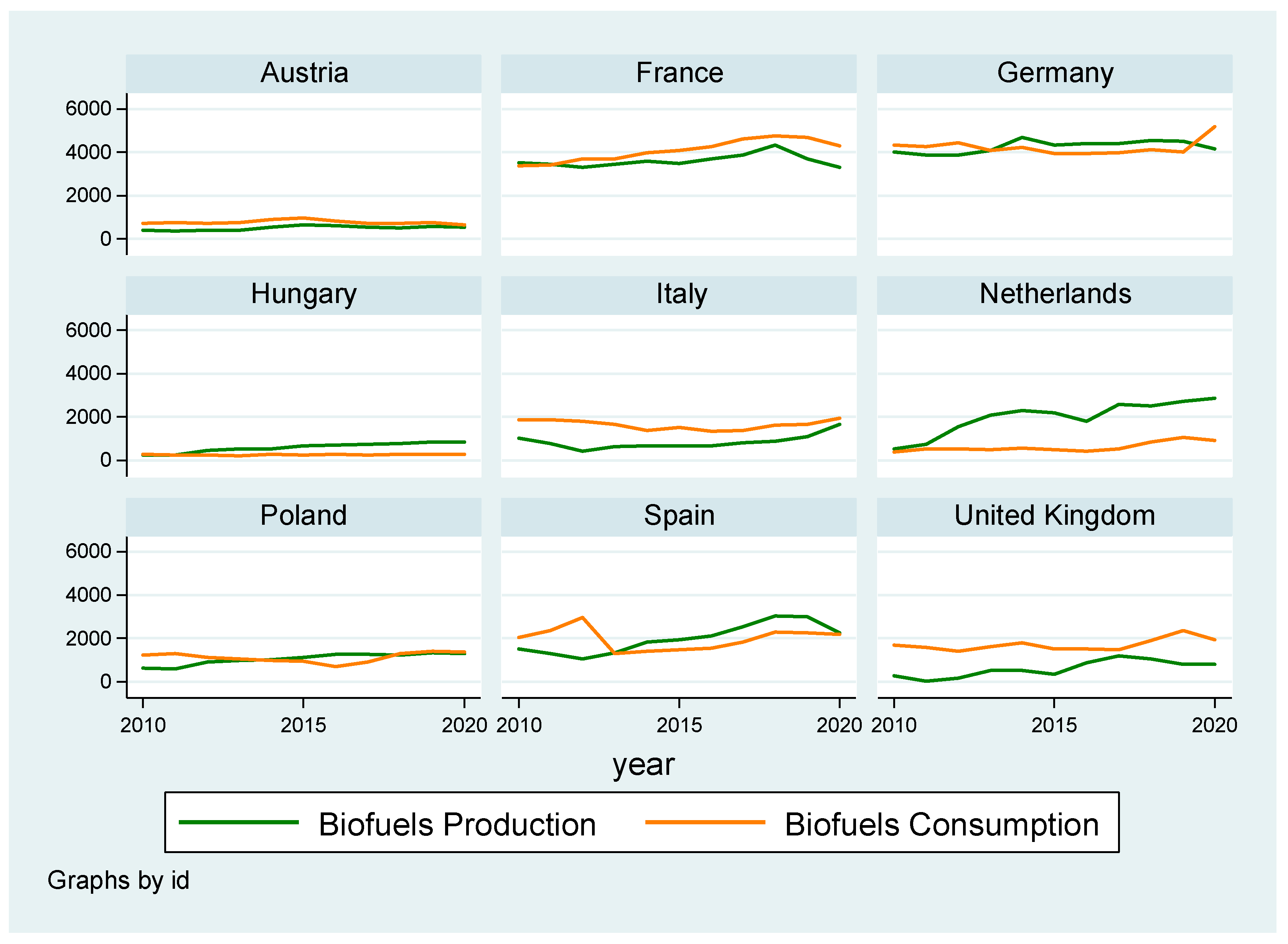

The main idea illustrated by this hypothesis is that with the growth of tax revenues from environmental taxes, economic entities have a desire to eliminate the additional tax burden, which leads to the transformation of the objects of taxation. A statistical sample of 9 European countries (Austria, France, Germany, Hungary, Italy, The Netherlands, Poland, Spain, U.K.) was formed for calculations. It is for these countries that data on biofuel production and consumption are available, and their environmental taxation systems are quite diverse for research. The research period is 2010–2020.

Figure 2 shows data on the dynamics of biofuel production and consumption in the specified countries.

The conducted research shows that the countries of the sample show different degrees of progress in the production and consumption of biofuels. Thus, Italy and The Netherlands turned out to be the leaders, while Austria and Hungary show the lowest indicators among those studied. It is important that during the studied period, the volumes of consumption and production of bioenergy gradually increased. At the same time, the fact that the studied countries can be conditionally divided into three groups attracts attention—those that independently provide their own biofuel needs (Poland, Austria, Germany); those that produce enough biofuel not only for own consumption, but also for export (The Netherlands, Spain, Hungary); and those that consume more biofuel than they produce, forcing it to be imported (U.K., Italy, France). This allows us to draw a general conclusion about the heterogeneity of the development of biofuel production in European countries and the need to study the causes of such heterogeneity. Accordingly, the indicators of biofuel production and consumption volumes were selected as the resulting variables in the construction of econometric models for evaluation.

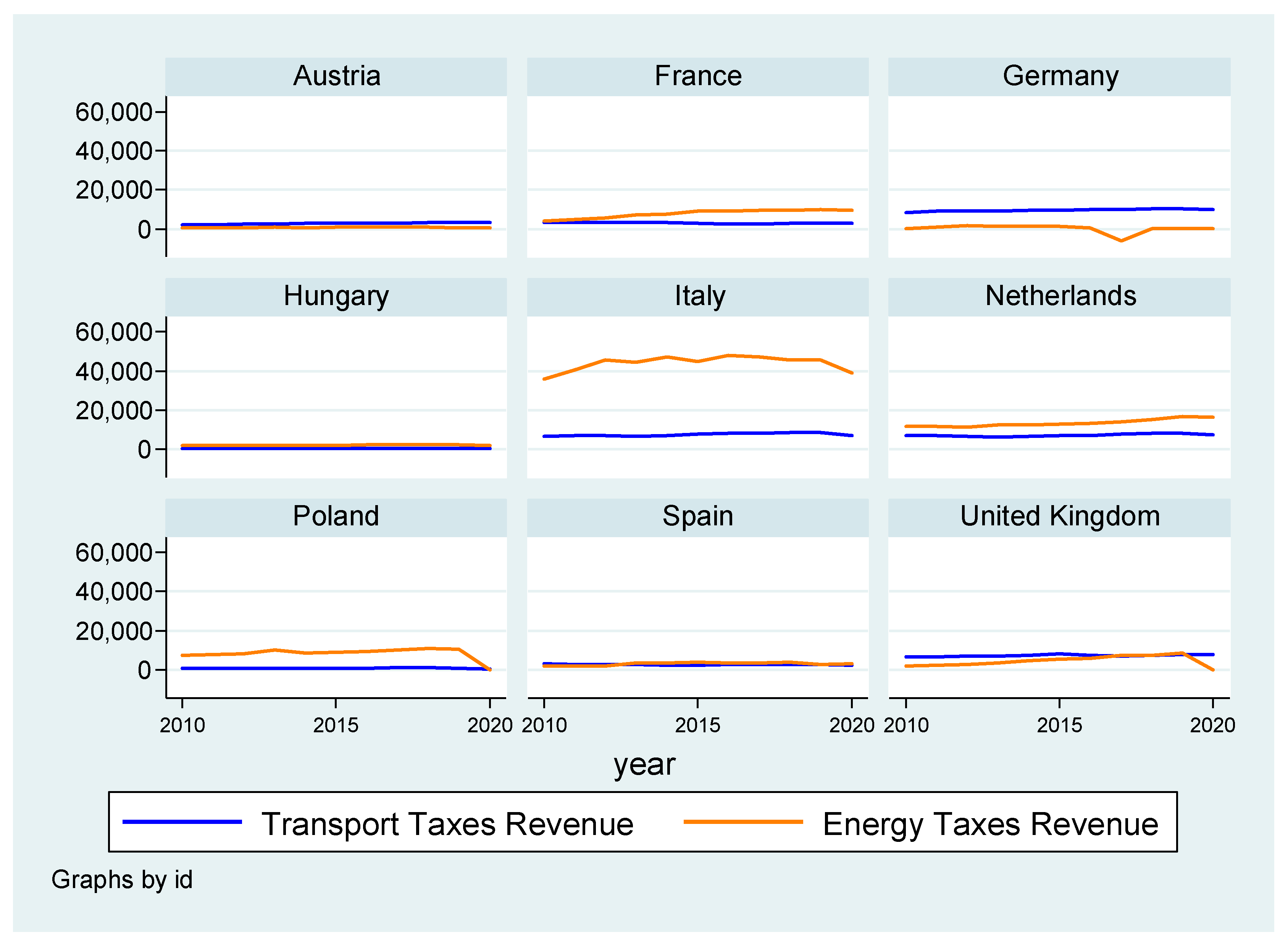

When choosing factor variables for assessing the impact of environmental taxes on trends in biofuel production and consumption, the current state of environmental taxation systems should be investigated. The conducted analysis proved that despite the wide variability of environmental taxation, there are two types of environmental taxes in all selected European countries—energy taxes and transport taxes. The analysis of the features of environmental taxation proved that these types of taxes have the potential of regulatory impact on the production and consumption of biofuels. So, energy taxes levied on energy producers tend to have some incentives for renewable and bioenergy production. At the same time, the type of fuel and the volume of emissions generated by the car are quite often used as criteria for taxation by transport taxes. This creates additional incentives for vehicle owners to use environmentally friendly fuels. The data presented in

Table 1 demonstrate that different amounts of energy and transport taxes operate in the studied countries.

For example, in Great Britain, there is one transport tax, in Germany—2, and in Austria and France—5. In France, there is only one energy tax, and in Hungary, Poland and Spain, there are 6 different taxes on energy and energy resources. In order to unify the data for calculation, the impact of environmental taxes is estimated by two factor variables: TransportTax—total revenue from transport taxes, mln US dollars; EnergyTax—total revenues from energy taxes, mln US dollars.

Figure 3 shows the dynamics of revenues from the specified environmental taxes in the studied European countries.

It should be noted that Italy is the leader in terms of the amount of revenues, in which revenues from energy taxes are significantly higher than in other countries. At the same time, the dynamics of income indicators are quite uniform in all the studied countries; only minor fluctuations are observed. However, a more in-depth analysis proved that during the studied period in various countries, changes in environmental taxation systems were constantly taking place, existing tax instruments were canceled, and new ones were established and changes were made to the conditions of taxation with current taxes. In this regard, it can be expected that such changes will also have a certain regulatory effect.

At the same time, it is important that the impact of indirect instruments is not instantaneous. Thus, the processes of structural changes in energy production and consumption, replacement of energy-intensive equipment, etc., take a long time, even if management decisions are made quickly. All this made it possible to substantiate the following research hypothesis.

Hypothesis 2: The impact of environmental taxes on the production and consumption of biofuels is delayed in time.

To test this hypothesis, when building econometric models, the time lag of the influence of the variables TransportTax and EnergyTax on indicators of production and consumption of biofuel is from 1 to 4 years.

The literature review and bibliometric analysis proved that the processes of biofuel production and consumption are quite complex and are characterized by a close connection with several social, economic and environmental processes. This made it possible to propose the third research hypothesis.

Hypothesis 3: Parameters of biofuel production and consumption are determined by a complex of economic and social prerequisites that complement the impact of environmental taxes.

To test this hypothesis, several control variables are considered when building econometric models:

- -

EnvTax—Total revenues from environmental taxes in relation to WFP, %. This indicator illustrates the general degree of development of the environmental taxation system in the country, as well as the level of fiscal efficiency of environmental taxes.

- -

CO2—Indicator of CO2 emissions into the environment per dollar of GDP produced in the country, kg. This parameter simultaneously characterizes the production structure of the national economy. Thus, it is expected that countries with a high level of the indicator have a higher level of energy intensity of the economy and a significant share of extractive and heavy processing industry.

- -

R&D—Research and development expenditure, % of GDP. This indicator is a characteristic of the country’s general degree of focus on the development of technological innovations and their commercial application.

- -

FIm—Fuel imports, % of merchandise imports. An indicator that reflects the degree of energy dependence of the country on external sources of supply and is also a characteristic of the shortage of energy produced on the national market.

Today, the most common types of biofuels are biodiesel, ethanol, renewable diesel and biojet. Available statistics show that their production and consumption are characterized by quite different levels of activity. This may be related both to the peculiarities of production technologies and to economic factors. That is why the fourth hypothesis was also formulated for the research.

Hypothesis 4: Environmental taxation has a specific effect on the production and consumption of various types of biofuels.

Analysis of the availability of information on the production and consumption of different types of biofuels allowed us to select two types of biofuels for further calculations—biodiesel and ethanol. It is these types of biofuels that are produced in all the studied countries, which allows us to expect statistically significant results of the calculations.

To test all the mentioned hypotheses, the method of panel regression modeling was chosen, namely the panel-corrected standard errors model. A general view of the econometric model is as follows:

where

is an indicator of

n parameter of biofuel production or consumption in the country

i in the period

t;

is an indicator of

m group of environmental tax revenue in the country

i in the period

t (transport taxes or energy taxes);

EnvTax it is a parameter of general environmental tax revenues to GDP ratio in the country

i in the period

t;

CO2 it is an indicator of CO2 emissions ratio to GDP unit in the country

i in the period

t;

R&D it is an indicator of research and development expenditures as a GDP % in the country

i in the period

t;

FIm it is an indicator of fuel import in the total import structure in the country

i in the period

t; β

1, β

2, β

3, β

4 and β

5 are the regression coefficients indicating an impact of the independent variables; β

0 is a constant of the regression equation;

ε is a standard error of the model.

4. Results

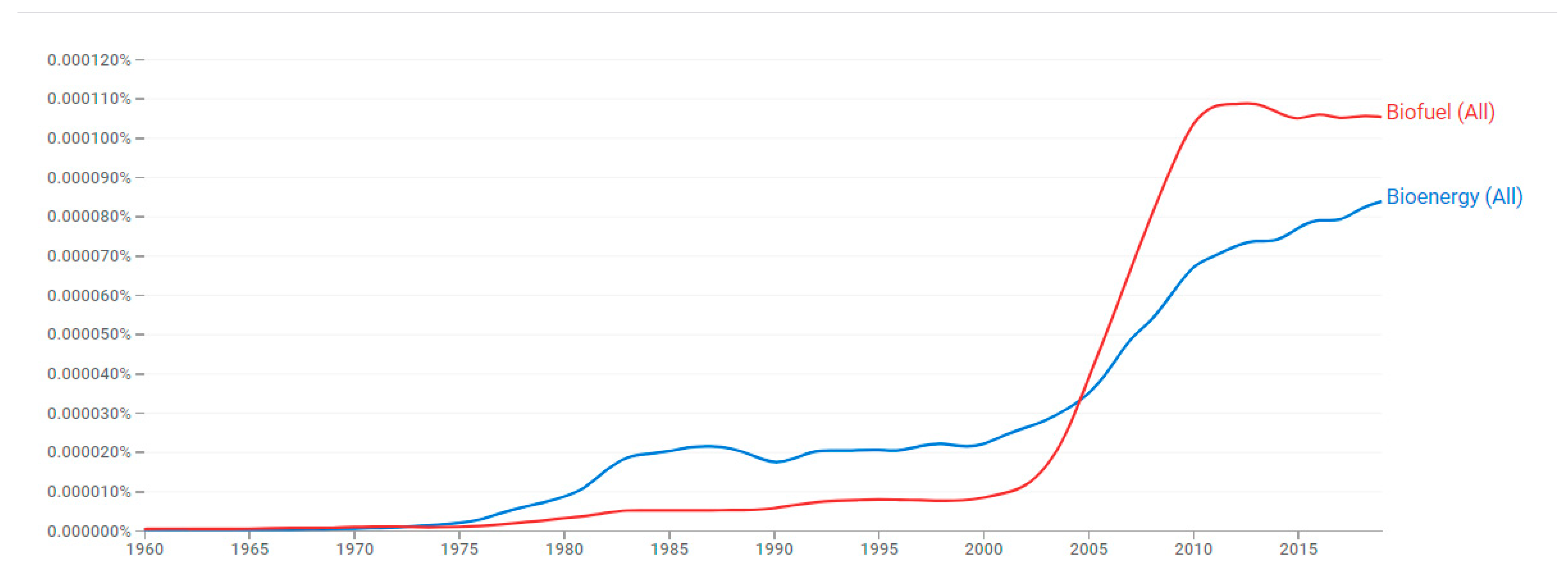

The first stage of research concerns the evolution of the idea of biofuel production and consumption. As evidenced by the results of the analysis obtained using Google Books Ngram Viewer (

Figure 4), the first references to bioenergy and biofuels date back to the 1970s. In the period up to the 2000s, there is a trend of gradually increasing interest in bioenergy and biofuel production processes. The sharpest jump in attention to the issue of bioenergy was recorded in the period 2000–2015. At the same time, we note that in recent years, publication activity devoted to the problems of bioenergy and biofuel has slowed down somewhat. It is also worth paying attention to the fact that in the period of 1970–2000, mentions of bioenergy are much more frequent, while the issue of biofuels receives less attention. Since 2005, there has been a real information boom in biofuel research issues, while there remains a strong general interest in the field of bioenergy. This indicates that the topic of bioenergy is already moving from the stage of general study to the search for the most promising areas of implementation of technologies for energy production from biosources.

The next block of research is devoted to the identification of meaningful interrelationships related to the processes of transition to the production and consumption of bioenergy. The bibliometric analysis of keywords, titles and abstracts of scientific articles devoted to the issues of bioenergy and biofuel made it possible to identify five clusters of keywords that mediate their study (

Figure 5).

The first cluster (red) contains 350 keywords, with the most widespread being “biomass”, “biofuels”, “bioenergy”, “renewable energy”, “ethanol”, “energy crops”, “greenhouse gases”, “fossil fuels”, “land use”, “forestry”, “agriculture”, “ecology”, “feedstocks”, “carbon sequestration”, “oils and fats”, “energy efficiency” and “sustainability”. This cluster characterizes the general reasons for biofuel development in terms of minimizing environmental footprint and increasing energy efficiency. The second cluster (green) is created by 186 items such as “electricity”, “hydrogen”, “methane”, “biogas”, “anaerobic digestion”, “bioreactor”, “food”, “microbial fuel cells”, “wastewater treatment” and “biorefineries”, which describe the main directions of bioenergy production. The third cluster (blue) contains 149 keywords concerning the different technologies of biofuel production (“biodiesel”, “microorganisms”, “temperature”, “combustion”, “heating”, “vegetable oil”, “pyrolysis”, etc.). The yellow cluster is formed by 149 keywords that characterize different substances used in biofuel production (“cellulose”, “lignin”, “metabolism”, “alcohol”, “bio-ethanol production”, “photosynthesis”, “biosynthesis”, etc.). The last cluster (violet) is composed of 126 keywords concerning to chemical processes of bioenergy production (“bioelectric energy sources”, “chemistry”, “electrodes”, “biosensic techniques”, “glucose”, “catalysis”, etc.).

The conducted research proved that the most widely researched direction in the field of bioenergy production is the technological component. At the same time, the analysis of the chronology of scientific research is also of significant scientific interest (

Figure 6).

The obtained results indicate that the development of bioenergy has already completed the stage of formation of basic production technologies and processes and is moving to the stage of mass production and maximization of economic and social benefits. This is evidenced by the fact that scientific research in recent years is characterized by key words such as “carbon capture”, “life cycle”, “human”, “food waste “, “agricultural waste”, “pollutant removal “, “wastewater treatment”, “refining” and “circular economy”.

Thus, we can state the fact that the commercialization of bioenergy and biofuel production is currently being scaled up. This actualizes the need to study the economic efficiency of mass production, the prospects for the transformation of the energy sector, and justify the feasibility of investment decisions. In this direction, it becomes more important to ensure long-term benefits for humanity from the transition to the production and consumption of bioenergy. At the same time, such processes are not instantaneous and require quite significant costs. That is why it is important not only to declare the role of bioenergy in the context of sustainable development, but also to create additional economic incentives for the main producers and consumers of energy. In this context, it is also important to evaluate the main relationships that arise when applying tax levers to increase the production and consumption of bioenergy. To this end, we conducted a bibliometric analysis of keywords in scientific publications corresponding to the query “environmental taxes” and “bioenergy” or “biofuel” (

Figure 7).

The first cluster (red colored) contains 53 items related with the different goals of environmental taxes establishment (“environmental impact”, “environmental protection”, “sustainable development”, “energy conservation”, “food security”, “energy resource”, “human”, “economic development”, etc.). This cluster characterizes the most general strategic effects that must be achieved as a result of the functioning of the environmental tax system. The green cluster is formed by 49 keywords with the most meaningful including “emission control”, “environmental policy”, “carbon dioxide”, “forestry”, “global warming”, “carbon sequestration”, “pollution tax”, “climate policy”, etc. This cluster describes the ecological impact of environmental tax and some specific instruments used to achieve such impact. The third (blue) cluster is created by 42 keywords concerning the goals of environmental tax in the scope of energy policy (“energy policy”, “greenhouse gases”, “economic and social effects”, “energy security”, “renewable fuels”, “commerce”, “ethanol”, “biodiesel” and others). The next cluster is yellow. It contains 29 keywords related to the economic aspects of bioenergy production such as “environmental economics”, “costs”, “optimization”, “cost-benefit analysis”, “competitiveness”, “economic conditions”, etc. The fifth (violet) cluster consists of 24 keywords concerning the different types and technologies of bioenergy production (“bioconversion”, “renewable energy”, “solar energy”, “bioethanol”, “cultivation”, “crops”, “wind power”, etc.). The last cluster has a turquoise color and contains 20 keywords such as “life cycle”, “public policy”, “economic analysis”, “incentive”, etc. This cluster generalizes the meaning of bioenergy for society and the role of environmental tax in the common strategy of long-term economic and social development.

The conducted research proved that environmental taxes are widely used in the context of achieving various goals of sustainable development. At the same time, the introduction of tax incentives for renewable energy or increased taxation of objects related to the use of traditional energy sources allow the transmission mechanism of the influence of environmental taxes to stimulate the production and consumption of bioenergy in general and biofuel.

The next stage of the research is the assessment of the impact of certain groups of environmental taxes on the production and consumption of biofuel.

Table 2 shows the results of the assessment of the impact of transport tax revenues on the total production volumes of different types of biofuels.

The conducted calculations proved that, in general, transport taxes have a stimulating effect on biofuel production processes. Thus, with an increase in tax revenues from transport taxes by 1 million dollars, the average annual growth of biofuel production amounts to 113,000 L. At the same time, the evaluation of the results obtained with the application of different durations of the time lag proved that when a time lag of 1 to 2 years is introduced into the model, the value of the coefficient of influence of transport taxes on the production of biofuel increases, which gradually decreases with a further increase in the time lag. This indicates that the greatest stimulating effect of the existence of transport taxes for biofuel production is observed in the short term.

The revealed influence of the control variables of the model is quite interesting. Thus, the indicator of the total burden of environmental taxation turned out to be a disincentive factor for biofuel production. This indicates that the habit of economic subjects to pay a significant amount of taxes minimizes their efforts to optimize energy security and reduce the tax burden. Attention should also be paid to the fact that in countries with a traditionally high level of carbon dioxide emissions per unit of GDP, a significantly lower level of biofuel production is observed. The revealed inverse relationship indicates the complexity of the transformation of national economies for which there is a high dependence on energy from fossil sources. The calculations confirmed the expected direct relationship between the growth of research and development funding in the country and the increase in biofuel production. In addition, the influence of the fuel import parameter on biofuel production was statistically insignificant, which indicates the insufficient level of attention to the development of alternative energy precisely in the context of solving the problem of energy dependence and energy security of countries.

Within the framework of the next block of analysis, we evaluate the influence of the group of energy taxes on the production of biofuel. The results of the evaluation are shown in

Table 3.

The obtained results prove that the application of energy taxes has a statistically significant and direct effect on the provision of biofuel production. At the same time, it is important that the introduction of a time lag into the model was not accompanied by an increase in the regression coefficients for the variable of income from energy taxes. This indicates that there is no delayed impact of energy taxes on biofuel production processes, which makes it possible to use them as a short-term impact tool. The overall impact of environmental taxes on biofuel production, as in the previous model, turned out to be reversed. Attention should also be paid to the fact that statistically insignificant results were obtained in this group of models regarding the impact of CO2 emissions on biofuel production. This indicates that the application of energy taxes to a greater extent concerns the producers of energy, and not the production companies that are its consumers. Similarly to the previous stage of the study, a statistically significant direct relationship between R&D funding and biofuel production was found, and the impact of energy imports on bioenergy production was not confirmed.

The next block of research was to identify the role of environmental taxes in changing the behavior of energy consumers.

Table 4 summarizes the results of assessing the impact of transport taxes on biofuel consumption. The direct impact of transport taxes on biofuel consumption has been confirmed. Moreover, it can be stated that this influence is delayed—with the increase in the time lag in the model, the value of the coefficient of influence of environmental taxes on the volume of biofuel consumption by economic subjects increases. Importantly, the impact of energy taxes on biofuel consumption was direct, but not time-lagged, as evidenced by the results in

Table 5.

The next block of analysis is devoted to assessing the impact of transport and energy taxes on the production and consumption of certain types of biofuels. Econometric models were built for evaluation, considering the influence of factor and control variables. At the same time, only the values of the regression coefficients for the main factor variables were summarized for further analysis. Thus, the results presented in

Table 6 indicate that transport taxes have a statistically significant effect on biodiesel production, as well as on biodiesel and bioethanol consumption. At the same time, it is important that this influence can be considered delayed in time, since the coefficients of the influence of transport taxes on the volumes of biofuel consumption increase with the increase in the time lag introduced into the model.

The results of assessing the impact of energy taxes on the production and consumption of different types of biofuels are presented in

Table 7.

The obtained results show that energy taxes have a statistically significant effect on the production and consumption of biodiesel and are also an incentive for ethanol consumption. At the same time, energy taxes do not have a delayed effect, since the regression coefficients are reduced when time lags are introduced into the model.

5. Discussion

The conducted research made it possible to substantiate the theoretical interrelationships of environmental taxes with the production and consumption of biofuel, as well as to empirically confirm several existing dependencies. Thus, the first hypothesis regarding the direct impact of environmental taxes on biofuel production and consumption was fully confirmed. The conducted study proved that both transport and energy taxes have a direct impact on the production and consumption of biofuels. This allows them to be used in the future not only as an economic policy tool, but also as an incentive to ensure transformations in the energy industry. In this context, it is promising for further research to study the influence of other groups of environmental taxes on the production and consumption of biofuels, as well as an in-depth analysis of the search for the most effective tax instruments that stimulate the production and consumption of biofuels to the greatest extent.

The construction of econometric models considering time lags from 1 to 4 years made it possible to partially confirm the hypothesis regarding the delayed impact of environmental taxes on the consumption and production of biofuel. Thus, the scale of the impact of transport taxes on the production and consumption of biofuels notably increases with the increase in the time lag of the study, while no such effect was found for energy taxes. At the same time, the existence of a close connection between transport and energy taxes and the volumes of consumption and production of biofuels indicates that their application has a rather rapid effect, which should be considered in the process of developing the state policy of regulating the energy sector.

During the research, the hypothesis about the influence of economic conditions on the production and consumption of biofuel was also partially confirmed. So, it was determined that the growth of research and development costs is an incentive for the growth of biofuel production and consumption in all analyzed directions, and the growth of the share of environmental taxes in GDP discourages the development of the bioenergy industry. In most of the studied cases, the disincentive effect of the CO2 emission indicator was also revealed, while the dependence of the development of bioenergy on energy imports was not confirmed. This indicates that the development of bioenergy in each country has different prospects depending on its historical features, as well as on the current state of the economy. This allows countries to build their own systems for stimulating the development of bioenergy. At the same time, there are broad prospects for further research in this direction. The influence of social factors, the role of the development of the system of state regulation of the economy, the quality of management, the general technological development of the country, etc., should be studied.

The results of testing the hypothesis regarding the specificity of the impact of environmental taxes on the production and consumption of certain types of biofuels turned out to be quite interesting. It was found that the studied transport and energy taxes are significant incentives for the growth of consumption of all studied types of biofuels, while in the context of biofuel production, only the impact of environmental taxes on biodiesel production was found to be significant. This indicates the possibility of developing the design of environmental taxes in such a way as to stimulate the growth of production of specific types of biofuels; however, most existing transport and energy taxes do not yet provide such an opportunity.

Research on identifying the impact of environmental taxes on biofuel production and consumption was conducted for the first time. The obtained results made it possible not only to theoretically substantiate the connection of environmental taxation with the growth of the share of bioenergy, but also to empirically confirm the presence of a significant impact of environmental taxes on the growth of biofuel circulation. Also new are the results regarding the detected time lags of influence. They prove that the expected effects from the use of regulatory tools for the production and consumption of biofuels are quite quickly achievable. The analyzed influence of the control variables proved that the technological development of the country and the current environmental conditions are additional incentives for the development of bioenergy.

The conducted research has certain limitations. In particular, the studied effects were confirmed only for a sample of European countries, so it can be expected that when the research base is expanded, the impact results may change slightly. This proves the need for additional calculations for countries with different regional specifics and different levels of technological and economic development. On the other hand, in the research process, we used generalized data regarding the indicators of environmental taxation (total revenues by groups of environmental taxes) and regarding the volumes of biofuel produced and consumed. This somewhat simplifies the existing cause and effect relationships. Therefore, it is advisable to conduct a more detailed analysis of the effectiveness of specific tax instruments, aimed at the creation of incentives specifically for bioenergy.

The conducted research also creates a basis for further analysis of economic tools for ensuring the development of bioenergy. Thus, studies of the effectiveness of investment programs in the field of bioenergy, analysis of economic losses and gains as a result of the transformation of the energy industry, forecasting the duration of such transformations and the payback of investments in the development of bioenergy, evaluating the effectiveness of various instruments of state regulatory influence on the development of bioenergy, etc., are of considerable scientific interest.

6. Conclusions

The conducted research proved that the factors of reducing harmful environmental impacts have a significant role among the prerequisites for the development of bioenergy. In this regard, the impact of environmental taxes on the production and consumption of biofuel was assessed. The obtained results proved that transport and energy taxes have a rather strong direct influence on the growth of biofuel production and consumption. At the same time, it is important that the effectiveness of transport taxes increases in the medium term, and the greatest impact of energy taxes is formed in the short term. It was also found that the economic conditions that have developed in the countries also have a significant impact on the production and consumption of biofuels. The influence of transport and energy taxes on the production and consumption of various types of biofuels is characterized by insignificant specificity, which indicates the greater effectiveness of the development of universal rather than narrowly focused tax instruments. All this creates a scientific basis for improving the state energy policy and developing the system of environmental taxation.

The proposed methodology and obtained results have the potential for further use in scientific research. Thus, the direction of studying the influence of environmental taxes on the production and consumption of various types of alternative energy is promising. On the other hand, in further studies, it will be possible to expand the sample of countries to identify the impact of national specifics on the effectiveness of regulatory instruments for the development of alternative energy. Another promising direction is the study of the complex impact of tax instruments and state support (investments, budget expenditures) on the development of bioenergy production.

The obtained results also have practical value. Thus, the revealed effects regarding the specifics of the influence of transport and energy taxes on the production and consumption of biofuel can be used in the development of regulatory strategies for the transformation of the energy sector. Identified time lags of the impact of environmental taxes on the intensity of biofuel production and consumption can increase the effectiveness of forecasting the results of the application of regulatory instruments. This has potential practical implications for countries implementing the concept of energy sector transformation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}