Corporate Social Responsibility in Finance

Share This Topical Collection

Editor

Topical Collection Information

Dear Colleagues,

The growing significance of CSR as a phenomenon within financial economics has raised a fundamental question: does CSR enhance shareholder value or is it an agency cost enjoyed by a firm’s top executives at the expense of stockholders? While a number of studies have examined this question from different perspectives, the evidence continues to be conflicting in nature. In this Topical Collection of the International Journal of Financial Studies, we investigate the agency cost and the value-enhancing perspectives of CSR. In particular, we invite papers that focus on the implications of different corporate governance mechanisms on corporate social responsibility. These mechanisms include, but are not limited to:

- Board monitoring

- Executive compensation and incentive

- Financial analyst

- Institutional ownership

- Accounting and auditing

- Cultural environment

- Media

- Law and regulations

Prof. Dr. Frank Li

Collection Editor

Manuscript Submission Information

Manuscripts should be submitted online at www.mdpi.com by registering and logging in to this website. Once you are registered, click here to go to the submission form. All submissions that pass pre-check are peer-reviewed. Accepted papers will be published continuously in the journal (as soon as accepted) and will be listed together on the collection website. Research articles, review articles as well as short communications are invited. For planned papers, a title and short abstract (about 250 words) can be sent to the Editorial Office for assessment.

Submitted manuscripts should not have been published previously, nor be under consideration for publication elsewhere (except conference proceedings papers). All manuscripts are thoroughly refereed through a single-blind peer-review process. A guide for authors and other relevant information for submission of manuscripts is available on the Instructions for Authors page. International Journal of Financial Studies is an international peer-reviewed open access monthly journal published by MDPI.

Please visit the Instructions for Authors page before submitting a manuscript.

The Article Processing Charge (APC) for publication in this open access journal is 1800 CHF (Swiss Francs).

Submitted papers should be well formatted and use good English. Authors may use MDPI's

English editing service prior to publication or during author revisions.

Keywords

- corporate social responsibility

- sustainability

- corporate governance

- executive compensation

- corporate finance

- agency problem

Published Papers (15 papers)

Open AccessArticle

Corporate Social Responsibility in Canadian Family Businesses: A Socioemotional Wealth Perspective

by

Imen Latrous, Jihene Kchaou, Myriam Ertz and Yosra Mnif

Cited by 5 | Viewed by 5114

Abstract

After having gained prominence in the late 20th century, corporate social responsibility (CSR) has emerged as a critical business aspect, adopted widely across the corporate landscape. Although family firms play a significant global role, research on their relationship with CSR performance remains sparse

[...] Read more.

After having gained prominence in the late 20th century, corporate social responsibility (CSR) has emerged as a critical business aspect, adopted widely across the corporate landscape. Although family firms play a significant global role, research on their relationship with CSR performance remains sparse and inconclusive. This paper seeks to bridge this gap by employing the primary classification of family firms, the socioemotional wealth perspective, and its FIBER model to examine their influence on CSR performance. The focus is on Canadian public companies listed on the S&P/TSX Composite Index from 2014 to 2022. Utilizing the NBC Canadian Family Index, the findings suggest that family firms exhibit superior CSR performance compared to their non-family counterparts. Further analyses indicate that family firms with greater control and influence by family members, those named after the family, those with strong emotional ties, and first-generation family firms tend to have enhanced CSR performance. By developing a socioemotional wealth score through FIBER dimensions to classify family firms, this study underscores the association of family firms with higher CSR performance, validating the robustness of the results.

Full article

Open AccessArticle

Sustainability Initiatives, Knowledge-Intensive Innovators, and Firms’ Performance: An Empirical Examination

by

Rajesh Kumar Bhaskaran

Cited by 8 | Viewed by 5260

Abstract

This paper examines the role of sustainability as a major driver of innovation, and assesses its affect on firms’ performance. This study was based on companies listed in the Forbes list of 100 most innovative companies and BCG’s 50 most innovative companies. The

[...] Read more.

This paper examines the role of sustainability as a major driver of innovation, and assesses its affect on firms’ performance. This study was based on companies listed in the Forbes list of 100 most innovative companies and BCG’s 50 most innovative companies. The innovative sample firms had higher ESG and component scores than the matched control firms, with statistical significance. In terms of distinctiveness of governance, the innovative firms had larger boards, independent board members, higher diversity, and longer board tenure. Innovative firms had superior financial performance in comparison with the matched control firms. A logit regression model was employed to predict whether firms that adopt sustainability initiatives tend also to be innovative companies. Firms with high intensity of investment in social and governance initiatives tended to be innovative. Innovative firms had greater focus on social initiatives related to employee satisfaction, promotion of a healthy and safe workplace, and diversity. However, innovative firms tended to score lower in terms of human rights initiatives. Innovative firms provided superior governance practices for shareholders and effective usage of antitakeover defense mechanisms. Debt-intensive firms tended to be innovative.

Full article

Open AccessArticle

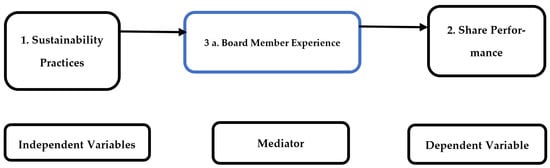

The Impact of Sustainability Practices on Share Performance with Mediation of Board Members Experience: A Study on Malaysian Listed Companies

by

Uzair Bhatti and Noralfishah Sulaiman

Cited by 4 | Viewed by 5606

Abstract

The purpose of this paper is to explore the impact of ESG sustainability practices (i.e., Environmental, Social, Governance/economic) on share performance. Moreover, the objective of the study is to investigate the sustainability practices with mediation of board member experience, which might contribute in

[...] Read more.

The purpose of this paper is to explore the impact of ESG sustainability practices (i.e., Environmental, Social, Governance/economic) on share performance. Moreover, the objective of the study is to investigate the sustainability practices with mediation of board member experience, which might contribute in maintaining the share performance. The study is unique in such a way that instead of analysing the stated relationship with internal financial performance measures such as return on asset (ROA) or return on equity (ROE), this study will investigate the relationship using external performance measures such as firm share performance. In this research, data were collected from 100 Bursa Malaysia listed companies using purposive sampling during the sampling period from 2017 to 2020. The data were analysed using the Autoregressive Distributed Lag (ARDL) bound testing model instead of a traditional regression model to examine the causal relationship. The results of the study showed the long-run steady relationships through the error correction term (ECT) at the optimum lag. Further, the findings also revealed that there is no short run association between the sustainability practices and the stock performance with mediation of the board experience. The findings also showed that sustainability practices have a significant impact on share performance with mediation of board experience. It is found that sustainability practices, especially environmental and social, are essential to attract investors. The results have also demonstrated that a board of directors of different ages has different knowledge, competencies, and expertise which could prove beneficial in terms of board diversity that decides to adapt the best sustainability practices. These findings provide some inference for future research on the relationship of sustainability practices and share performance with other mediating factors of board attributes.

Full article

►▼

Show Figures

Open AccessArticle

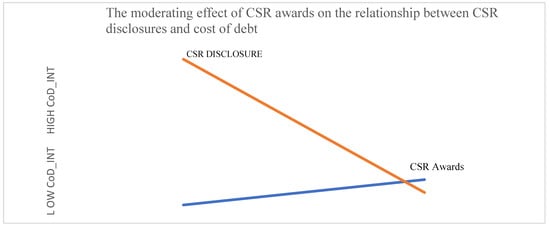

CSR Disclosures, CSR Awards and Corporate Governance as Determinants of the Cost of Debt: Evidence from Malaysia

by

Shyamala Dhoraisingam Samuel, Sakthi Mahenthiran and Ravindran Ramasamy

Cited by 13 | Viewed by 9307

Abstract

The current study examines the relationship between corporate social responsibility (CSR) disclosures, media announcements of CSR awards and a firm’s cost of debt in Malaysia. The sample consists of 104 Malaysian publicly listed companies belonging to the Edge Billion Ringgit Club between 2009

[...] Read more.

The current study examines the relationship between corporate social responsibility (CSR) disclosures, media announcements of CSR awards and a firm’s cost of debt in Malaysia. The sample consists of 104 Malaysian publicly listed companies belonging to the Edge Billion Ringgit Club between 2009 to 2015. The study uses panel data regression analysis and the ordinary least squares estimation method. The results find that the interaction between CSR disclosures and winning awards for a company’s CSR initiatives and practices lowers the cost of debt. Our study concludes that, when a company discloses more information on its CSR initiatives and practices, it reduces the cost of debt. Thus, we argue that CSR disclosures and awards can act as proxies for branding listed firms, making them more marketable and allowing them to negotiate better debt contracts. However, the study shows that politically connected companies have a higher debt cost than non-politically connected firms. Furthermore, our results indicate that smaller boards are effective, but audit committees are not effective in monitoring the board of directors in Malaysian listed firms.

Full article

►▼

Show Figures

Open AccessArticle

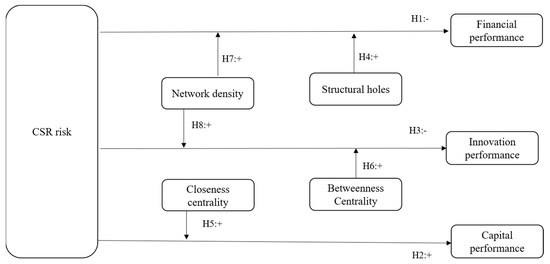

Corporate Social Responsibility Risk and Firm Performance: A Network Perspective

by

Jiaqi Luo, Mingxiao Bi and Dandan Jia

Cited by 6 | Viewed by 5640

Abstract

This study explored how corporate social responsibility (CSR) risk, social networks, and firm performance interacted in light of resource dependence theory and information asymmetry theory to bridge the literature gap between CSR risk and firm performance under the conditions of China’s network. We

[...] Read more.

This study explored how corporate social responsibility (CSR) risk, social networks, and firm performance interacted in light of resource dependence theory and information asymmetry theory to bridge the literature gap between CSR risk and firm performance under the conditions of China’s network. We used data from Shanghai and Shenzhen A-share listed firms in China from 2010 to 2019 to conduct a social network analysis and random-effects GLS regression analysis. The study revealed the following: (1) CSR risk hurts financial performance, while structural holes and network density attenuate this effect; (2) CSR risk positively impacts capital performance, which is amplified by closeness centrality; (3) CSR risk harms innovation performance, while betweenness centrality and network density mitigate this effect. Despite CSR risk bringing short-term benefits, this effect is not sustained. Generally, CSR risks are more detrimental to firms than beneficial. In this study, we strengthen the basis of the research on CSR risk and firm performance, along with research on social networks, advising firms to avoid CSR risks and utilize their networks to mitigate such risks and achieve a better performance.

Full article

►▼

Show Figures

Open AccessFeature PaperArticle

What Do the Consequences of Environmental, Social and Governance Failures Tell Us about the Motivations for Corporate Social Responsibility?

by

Richard Walton

Cited by 4 | Viewed by 6244

Abstract

This paper investigates the motivations behind corporate social responsibility (CSR) by considering the consequences of environmental, social and governance (ESG) failures that CSR is intended to avoid. Using data from 2581 public U.S. firms over 2007–2018, this paper finds that such failures are

[...] Read more.

This paper investigates the motivations behind corporate social responsibility (CSR) by considering the consequences of environmental, social and governance (ESG) failures that CSR is intended to avoid. Using data from 2581 public U.S. firms over 2007–2018, this paper finds that such failures are associated with increased CEO turnover. This relationship is driven primarily by CEOs with longer tenures and by environmental issues. These negative events are also found to be associated with declines in the firm’s sales growth, employment growth and equity returns. CSR activities that reduce the incidence of such events therefore benefit both the CEO and the shareholder. Interestingly, replacing the CEO does not mitigate the negative impacts of such events on the firm, nor does it reduce the incidence of such events in subsequent years. The decision to remove the CEO following such failures appears costly to both the CEO and the firm’s shareholders.

Full article

Open AccessArticle

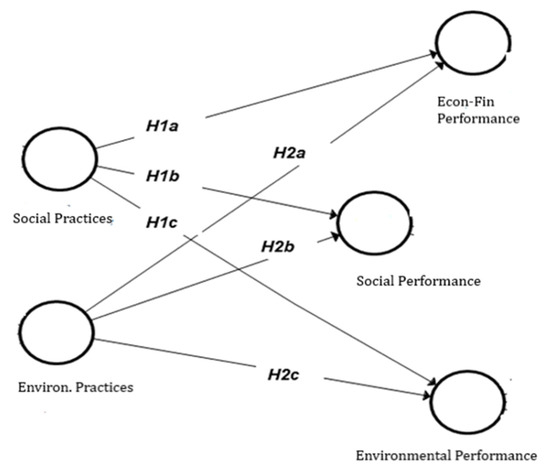

Consequences of Social and Environmental Corporate Responsibility Practices: Managers’ Perception in Mozambique

by

Eulália Madime and Tiago Cruz Gonçalves

Cited by 13 | Viewed by 5361

Abstract

The objective of this paper is to analyze the relationship between the social and environmental practices of Corporate Social Responsibility (CSR), and the economic–financial, social, and environmental performance in Mozambican companies, from the managers’ perspectives. The data were collected from a sample of

[...] Read more.

The objective of this paper is to analyze the relationship between the social and environmental practices of Corporate Social Responsibility (CSR), and the economic–financial, social, and environmental performance in Mozambican companies, from the managers’ perspectives. The data were collected from a sample of 227 companies through a survey questionnaire. We used structural equation modelling to analyze how the managers correlate the different social and environmental practices with performance at the financial, social, and environmental levels. The results showed that the relationship between all major components of the social and environmental practices, and the economic–financial, social, and environmental performance is positive but insignificant with the exception of the social practices of community support, which has a weak relationship with the economic–financial performance, environmental performance, and social performance, as well as the environmental practices. The data indicate that there is a need for strengthening the appropriate economic–financial incentive policies and strategies for the agents who promote good CSR practices in the country, in order to obtain satisfactory, measurable, and comparable economic–financial, social, and environmental performance.

Full article

►▼

Show Figures

Open AccessReview

The Effect of Corporate Social Responsibility on Earnings Management: Bibliometric Review

by

José Manuel Santos-Jaén, Ana León-Gómez and José Serrano-Madrid

Cited by 34 | Viewed by 9528

Abstract

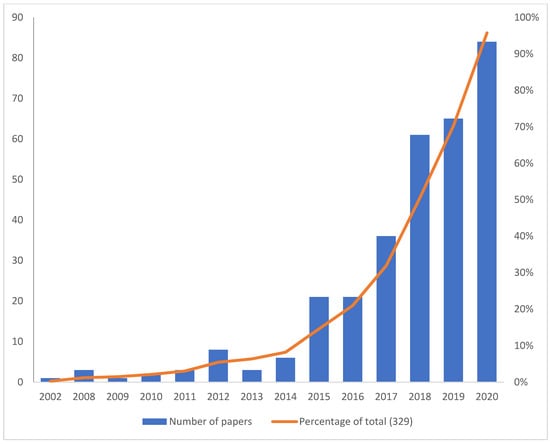

This review aims to study the knowledge development and research dissemination on the influence of Corporate Social Responsibility (CSR) on earnings management through a social network approach using a bibliometric review. A systematic bibliometric review was carried out on 329 papers obtained from

[...] Read more.

This review aims to study the knowledge development and research dissemination on the influence of Corporate Social Responsibility (CSR) on earnings management through a social network approach using a bibliometric review. A systematic bibliometric review was carried out on 329 papers obtained from the Clarivate Analytics Web of Science (WoS) Core Collection database. The data were analyzed by year, journal, author, institution, country, affiliation, subject area and term analysis. The results reveal the growing interest of researchers in studying the impact of CSR. Although the USA and China dominate publication production, there are a large number of authors from more than 50 countries around the world. The results also show that being prolific does not imply being influential in this area. The keyword patterns showed some interesting potential areas of study on this topic. The findings of this paper provide insight to the research on the analysis of the influence of CSR on earnings management. The most important findings consist of a number of gaps in the literature, such as gender diversity, voluntary disclosure of information and existence of an audit committee, among others, that allow for future fields of research to improve the analysis of the influence of CSR in EM. This research should also prove helpful to managers, owners and auditors. This is the first bibliometric review developed on this topic and it can be extrapolated to any place in the world.

Full article

►▼

Show Figures

Open AccessArticle

Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France

by

Sonia Boukattaya and Abdelwahed Omri

Cited by 12 | Viewed by 7094

Abstract

The present work aimed to examine the association between Corporate Social performance (CSP) and corporate financial performance (CFP) taking into account corporate social irresponsibility. Here, we used a sample of French non-financial firms listed on SBF 120 between 2011 and 2016. Our findings

[...] Read more.

The present work aimed to examine the association between Corporate Social performance (CSP) and corporate financial performance (CFP) taking into account corporate social irresponsibility. Here, we used a sample of French non-financial firms listed on SBF 120 between 2011 and 2016. Our findings provided evidence that corporate social responsibility (CSR) and corporate social irresponsibility (CSI) exert opposite effects on the CFP. Using an estimation of the vector autoregressive (VAR) model for panel data, we showed that the CSI has a greater and more lasting impact on CFP than CSR.

Full article

►▼

Show Figures

Open AccessArticle

Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance

by

Wenzhen Mai and Nik Intan Norhan binti Abdul Hamid

Cited by 5 | Viewed by 6168

Abstract

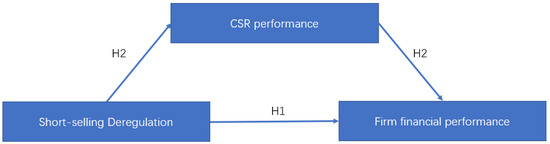

The aim of this study is to examine the effect of short-selling deregulation on the financial performance of SMEs in China. The external governance role of short-selling is also tested by adopting corporate social responsibility (CSR) performance as the mediating effect. This study

[...] Read more.

The aim of this study is to examine the effect of short-selling deregulation on the financial performance of SMEs in China. The external governance role of short-selling is also tested by adopting corporate social responsibility (CSR) performance as the mediating effect. This study investigates a panel data analysis with a sample of 5038 firm-years of SMEs listed in Shenzhen Stock Exchange from 2010 to 2019. The PSM-DID method is adopted in this study to alleviate self-selection and endogenous problems to observe the comparable pure effect of short-selling deregulation, while the mediation test is conducted based on Baron and Kenny’s model. The finding of this study showed that the existence of short-selling could enhance firm financial performance and the mediating effect of CSR performance position in their relationship. In addition, the further analysis revealed that the mediating effect of CSR is more pronounced for family businesses and firms with high real short-selling threats. The robust test of alternative measurements is conducted and valid. This study provides insights for policymakers to consider further short-selling ban lifting and corporate executives to practice more CSR activities to improve the financial performance. Limitations and further implications of this study are also discussed.

Full article

►▼

Show Figures

Open AccessArticle

The Impact of Environmental Sustainability Disclosure on Stock Return of Saudi Listed Firms: The Moderating Role of Financial Constraints

by

Abdulaziz Mohammed Alsahlawi, Kaouther Chebbi and Mohammed Abdullah Ammer

Cited by 37 | Viewed by 9055

Abstract

Environmental sustainability represents nowadays a significant factor for business sector. Firms carry out many initiatives to develop environmental practices. Investors increasingly consider environmental discloser by firms and integrate this disclosure into the investment decision-making process. Using a database of Saudi listed firms, this

[...] Read more.

Environmental sustainability represents nowadays a significant factor for business sector. Firms carry out many initiatives to develop environmental practices. Investors increasingly consider environmental discloser by firms and integrate this disclosure into the investment decision-making process. Using a database of Saudi listed firms, this study adds to the literature by examining the relationship between the environmental sustainability disclosure and stock return and whether this relationship is moderated by the financial constraints. We find that the environmental sustainability disclosure has significant and negative impact on stock return, indicating that investors do not consider environmental disclosure when valuing the stocks. Furthermore, our results propose that the negative impact of environmental disclosure on stock return is more evident in firms with financial constraints. This study provides managerial implications for regulatory authorities, firms and investors. The environmental practices can be value relevant. However, these practices need to be efficiently integrated into stock valuation.

Full article

Open AccessArticle

Corporate Social Responsibility: Motives and Financial Performance

by

Muhannad Atmeh, Mohammad Shaban and Malek Alsharairi

Cited by 10 | Viewed by 7242

Abstract

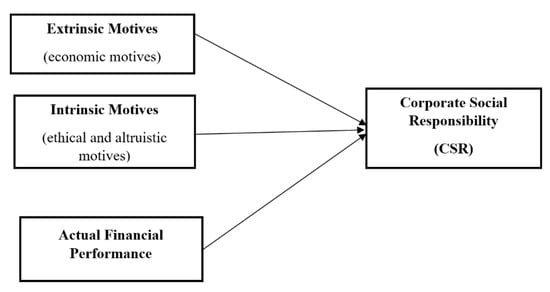

The relationship between companies and society has been questioned for a long time. However, the effect of the motives behind CSR regarding the companies’ actual engagement with CSR has received little attention, especially in emerging markets. This paper tackles this issue for the

[...] Read more.

The relationship between companies and society has been questioned for a long time. However, the effect of the motives behind CSR regarding the companies’ actual engagement with CSR has received little attention, especially in emerging markets. This paper tackles this issue for the first time using a sample of Jordanian companies. We explore the effect of two types of motives on the level of engagement in CSR: extrinsic motive (financial) and intrinsic motives (ethical and altruistic). The relationship between the company’s actual financial performance and CSR is also investigated. Primary data were collected using a questionnaire, distributed to Jordanian company’s managers in five sectors: pharmaceutical, technology and telecommunication, construction, farming, and financial services. Multiple regression analysis was conducted to depict the relationships. Results show that the intrinsic motives have a significant effect on CSR, while the extrinsic motive has none. When intrinsic motives were tested separately, results showed that the ethical motive had a significant effect, while the altruistic had no effect. In both cases, CSR was shown to be more significantly driven by the company’s financial performance. Different stakeholders such as policymakers, entrepreneurs, researchers, and investors may use the results of this study to increase companies’ involvement in CSR.

Full article

►▼

Show Figures

Open AccessArticle

Correlation between the DJSI Chile and the Financial Indices of Chilean Companies

by

Karime Chahuán-Jiménez

Cited by 3 | Viewed by 4116

Abstract

The Dow Jones Sustainability Index Chile (DJSI Chile) is made up of leading sustainability companies that are investing great effort into sustainable management. This study correlates the DJSI Chile with the financial indices (return on equity (ROE), return on assets (ROA), market value,

[...] Read more.

The Dow Jones Sustainability Index Chile (DJSI Chile) is made up of leading sustainability companies that are investing great effort into sustainable management. This study correlates the DJSI Chile with the financial indices (return on equity (ROE), return on assets (ROA), market value, earnings, and leverage) of companies that belong to the General Stock Price Index (IGPA) in Chile. The methodology used was quantitative, considering Chilean companies in the IGPA, including companies belonging to the DJSI Chile, applying a normality and correlation test based on the results. In conclusion, the study shows that in the results for the ROE, ROA, and leverage variables, there is no positive correlation with the DJSI Chile. However, the DJSI Chile is correlated with market value (for approximately 80% of the companies), and with earnings, there is a slightly higher correlation for the companies that belong to the DJSI Chile than for the remaining companies in the IGPA, thus if there exists a correlation between the DJSI Chile index and the variables market value and earnings, the index enables the prediction of those financial variables or predicts the finance indices (value market and earnings) of the companies that make up the DJSI Chile basing in the DJSI Chile index.

Full article

Open AccessArticle

Corporate Social Responsibility and Firm Value Protection

by

Daniel Ogachi and Zeman Zoltan

Cited by 19 | Viewed by 11083

Abstract

The conception of Corporate Social Responsibility has continued to gain a lengthy discussion in all aspects of corporate finance with a particular focus on its contributing to financial performance. Despite its prominence globally, many companies have not embraced the concept, as most of

[...] Read more.

The conception of Corporate Social Responsibility has continued to gain a lengthy discussion in all aspects of corporate finance with a particular focus on its contributing to financial performance. Despite its prominence globally, many companies have not embraced the concept, as most of them have remained doubtful about its contribution to corporate financial performance. Several companies have digressed the idea to merely an aspect of charity and cost instead of cost reduction and market creation. The fixed-effect model of panel data analysis was applied for the study period from 2010 to 2019 to measure relationships on CSR’s effect on the financial performance of listed companies in Kenya. The study used panel data for the years 2010–2019. The research used trend analysis for ten years to analyse data using canonical correlations, Logistic Regression analysis and ARIMA models to establish relationships among the variables of the study. Our results offer new evidence on the linearity effect of CSR on financial performance suggest that Corporate Social Responsibilities activities are very vital influencers of firm value, as they have a positive influence on the financial performance of companies.

Full article

►▼

Show Figures

Open AccessArticle

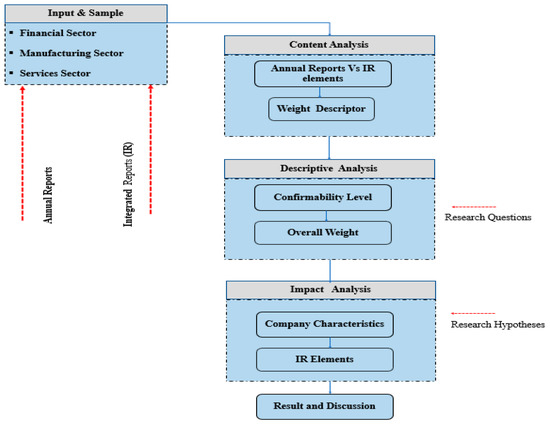

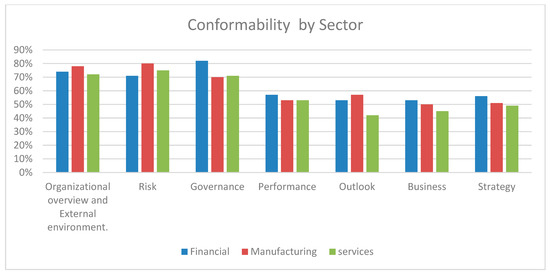

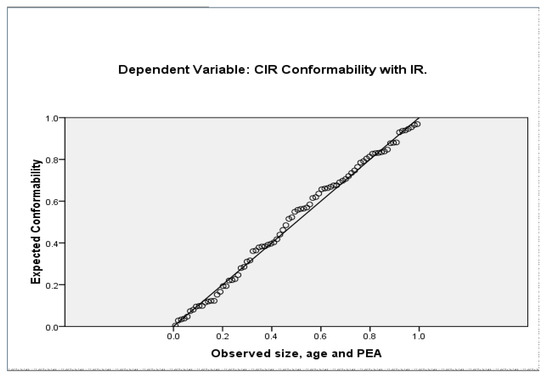

Conformity of Annual Reports to an Integrated Reporting Framework: ASE Listed Companies

by

Ghada A. Altarawneh and Asma’a Omar Al-Halalmeh

Cited by 7 | Viewed by 6686

Abstract

The objectives of this study are to determine the level of conformity between Current Issued Reports (CIRs) and Integrated Report (IR) elements of the Amman Stocks Exchange (ASE) listed companies, as well as to determine whether the investigated corporate characteristics (size, age, quality

[...] Read more.

The objectives of this study are to determine the level of conformity between Current Issued Reports (CIRs) and Integrated Report (IR) elements of the Amman Stocks Exchange (ASE) listed companies, as well as to determine whether the investigated corporate characteristics (size, age, quality assurance (QA), earning per share (EPS), industry type, foreign ownership (FO)) of these companies have any impact on the conformability of CIRs. It is worth mentioning that (QA), and (EPS), have never been examined by looking at its association with corporate disclosures, and IR in particular. Based on adoption of the IR framework and using the method of content analysis, corporate annual reports and other stand-alone reports of 82 companies in 2017 and 2018 within the financial, industrial, and services sectors, were chosen for this study. The findings of the study provide an answer to the research question and show that sectors vary in their levels of conformity. It reveals that the service sector shows the lowest conformability compared to other sectors, whereas the financial firms conform 65%, followed by the industrial sector. It also finds a positive association between CIRs conformability and variables of size, age of company and quality assurance. However, EPS, FO and type of industry were found to have no impact on the conformability of CIRs to the IR framework. This study has contributed to IR research, which, as a field, has previously received very little recognition among scholars in Jordan. Moreover, IR still does not exist in Jordan’s business practices.

Full article

►▼

Show Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}