Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Corporate Social Performance and Firm Financial Performance

2.2. CSR, CSI, and Firm Performance

3. Empirical Design

3.1. Data and Sample

3.2. Variables

3.3. Emirical Model

4. Results

4.1. Preliminary Analysis

4.2. Estimation Results

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Abrigo, Michael RM, and Inessa Love. 2016. Estimation of panel vector autoregression in Stata. Stata Journal 16: 778–804. [Google Scholar] [CrossRef] [Green Version]

- Ahmadi, Ali, Nejia Nakaa, and Abdelfettah Bouri. 2018. Chief Executive Officer attributes, board structures, gender diversity and firm performance among French CAC 40 listed firms. Research in International Business and Finance 44: 218–26. [Google Scholar] [CrossRef]

- Akaike, Hirotugu. 1969. Fitting autoregressive models for prediction. Annals of the Institute of Statistical Mathematics 21: 243–47. [Google Scholar] [CrossRef]

- Akaike, Hirotugu. 1977. An objective use of Bayesian models. Annals of the Institute of Statistical Mathematics 29: 9–20. [Google Scholar] [CrossRef]

- Akaike, Hirotugu. 1981. Likelihood of a model and information criteria. Journal of Econometrics 16: 3–14. [Google Scholar] [CrossRef]

- Al-Hadi, Ahmed, Bikram Chatterjee, Ali Yaftian, Grantley Taylor, and Mostafa Monzur Hasan. 2019. Corporate social responsibility performance, financial distress and firm life cycle: Evidence from Australia. Accounting & Finance 59: 961–89. [Google Scholar] [CrossRef]

- Andrews, Donald WK, and Biao Lu. 2001. Consistent model and moment selection procedures for GMM estimation with application to dynamic panel data models. Journal of Econometrics 101: 123–64. [Google Scholar] [CrossRef]

- Armstrong, J. Scott. 1977. Social Irresponsibility in Management. Journal of Business Research 5: 185–213. [Google Scholar] [CrossRef] [Green Version]

- Ayadi, Mohamed, Martin. I. Kusy, Minyoung Pyo, and Samir Trabelsi. 2015. Corporate social responsibility, corporate governance, and managerial risk-taking. Journal of Theoretical Accounting Research 11: 50–113. [Google Scholar] [CrossRef]

- Barnea, Amir, and Amir Rubin. 2010. Corporate social responsibility as a conflict between shareholders. Journal of Business Ethics 97: 71–86. [Google Scholar] [CrossRef]

- Baron, David P., Maretno Agus Harjoto, and Hoje Jo. 2011. The economics and politics of corporate social performance. Business and Politics 13: 1–46. [Google Scholar] [CrossRef] [Green Version]

- Blasi, Silvia, Massimiliano Caporin, and Fulvio Fontini. 2018. A Multidimensional Analysis of the Relationship Between Corporate Social Responsibility and Firms’ Economic Performance. Ecological Economics 147: 218–29. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, Sabri, Alexis Cellier, Riadh Manita, and Asif Saeed. 2020. Does corporate social responsibility reduce financial distress risk? Economic Modelling 91: 835–51. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Rey Dang, and Duc Khuong Nguyen. 2014. Does board gender diversity improve the performance of French listed firms? Gestion 2000 31: 259–69. [Google Scholar] [CrossRef]

- Boukattaya, Sonia, and Abdelwahed Omri. 2021. Impact of Board Gender Diversity on Corporate Social Responsibility and Irresponsibility: Empirical Evidence from France. Sustainability 13: 4712. [Google Scholar] [CrossRef]

- Boulouta, Ioanna. 2013. Hidden connections: The link between board gender diversity and corporate social performance. Journal of Business Ethics 113: 185–97. [Google Scholar] [CrossRef]

- Brammer, Stephen, Chris Brooks, and Stephen Pavelin. 2006. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financial Management 35: 97–116. [Google Scholar] [CrossRef] [Green Version]

- Cheng, Beiting, Ioannis Ioannou, and George Serafeim. 2014. Corporate social responsibility and access to finance. Strategic Management Journal 35: 1–23. [Google Scholar] [CrossRef]

- Činčalová, Simona, and Veronika Hedija. 2020. Firm Characteristics and Corporate Social Responsibility: The Case of Czech Transportation and Storage Industry. Sustainability 12: 1992. [Google Scholar] [CrossRef] [Green Version]

- Clarkson, Max E. 1995. A stakeholder framework for analyzing and evaluating corporate social performance. Academy of Management Review 20: 92–117. [Google Scholar] [CrossRef]

- Cooper, Michael J., Huseyin Gulen, and Michael J. Schill. 2008. Asset growth and the cross-section of stock returns. Journal of Finance 63: 1609–51. [Google Scholar] [CrossRef]

- Cui, Jinhua, Hoje Jo, and Haejung Na. 2018. Does corporate social responsibility affect information asymmetry? Journal of Business Ethics 148: 549–72. [Google Scholar] [CrossRef]

- Dang, Chongyu, Zhichuan Frank Li, and Chen Yang. 2018. Measuring firm size in empirical corporate finance. Journal of Banking & Finance 86: 159–76. [Google Scholar] [CrossRef]

- Dhaliwal, Dan S., Suresh Radhakrishnan, Albert Tsang, and Yong George Yang. 2012. Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. The Accounting Review 87: 723–59. [Google Scholar] [CrossRef]

- Eccles, Robert G., and George Serafeim. 2013. A tale of two stories: Sustainability and the quarterly earnings call. Journal of Applied Corporate Finance 25: 8–19. [Google Scholar] [CrossRef]

- El Ghoul, Sadok, Omrane Guedhami, and Yongtae Kim. 2017. Country-level institutions, firm value, and the role of corporate social responsibility initiatives. Journal of International Business Studies 48: 360–85. [Google Scholar] [CrossRef] [Green Version]

- El Ghoul, Sadok, Omrane Guedhami, Chuck C. Kwok, and Dev R. Mishra. 2011. Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance 35: 2388–406. [Google Scholar] [CrossRef]

- Fatemi, Ali, Iraj Fooladi, and Hassan Tehranian. 2015. Valuation effects of corporate social responsibility. Journal of Banking & Finance 59: 182–92. [Google Scholar] [CrossRef]

- Fatemi, Ali, Martin Glaum, and Stefanie Kaiser. 2018. ESG performance and firm value: The moderating role of disclosure. Global Finance Journal 38: 45–64. [Google Scholar] [CrossRef]

- Freeman, R. Edward. 1984. Strategic Management: A Stakeholder Approach. Pitman Series in Business and Public Policy. Boston: Pitman, p. 276. [Google Scholar]

- Friedman, Milton. 1970. The social responsibility of business is to increase profit. The New York Times Magazine, September 13, 32–33. [Google Scholar]

- Frooman, Jeff. 1997. Socially irresponsible and illegal behavior and shareholder wealth a meta-analysis of event studies. Business & Society 36: 221–49. [Google Scholar] [CrossRef]

- Frooman, Jeff. 1999. Stakeholder influence strategies. Academy of Management Review 24: 191–205. [Google Scholar] [CrossRef]

- Galant, Adriana, and Simon Cadez. 2017. Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istraživanja 30: 676–93. [Google Scholar] [CrossRef]

- Goel, Puneeta, and Rupali Misra. 2017. Sustainability Reporting in India: Exploring Sectoral Differences and Linkages with Financial Performance. Vision-The Journal of Business Perspective 21: 214–24. [Google Scholar] [CrossRef]

- Goss, Allen, and Gordon S. Roberts. 2011. The impact of corporate social responsibility on the cost of bank loans. Journal of Banking & Finance 35: 1794–810. [Google Scholar] [CrossRef]

- Gregory-Smith, Ian, Brian GM Main, and Charles A. O’Reilly III. 2014. Appointments, pay and performance in UK boardrooms by gender. The Economic Journal 124: F109–F28. [Google Scholar] [CrossRef] [Green Version]

- Hannan, Edward J., and Barry G. Quinn. 1979. The determination of the order of an autoregression. Journal of the Royal Statistical Society. Series B (Methodological) 41: 190–95. [Google Scholar] [CrossRef]

- Harjoto, Maretno, and Indrarini Laksmana. 2018. The impact of corporate social responsibility on risk taking and firm value. Journal of Business Ethics 151: 353–73. [Google Scholar] [CrossRef]

- Hill, Charles WL, and Thomas M. Jones. 1992. Stakeholder-agency theory. Journal of Management Studies 29: 131–54. [Google Scholar] [CrossRef]

- Hong, Harrison, and Marcin Kacperczyk. 2009. The price of sin: The effects of social norms on markets. Journal of Financial Economics 93: 15–36. [Google Scholar] [CrossRef]

- Hunjra, Ahmed Imran, Sabri Boubaker, Murugesh Arunachalam, and Asad Mehmood. 2021. How does CSR mediate the relationship between culture, religiosity and firm performance? Finance Research Letters 39: 101587. [Google Scholar] [CrossRef]

- Ioannou, Ioannis, and George Serafeim. 2015. The impact of corporate social responsibility on investment recommendations: Analysts’ perceptions and shifting institutional logics. Strategic Management Journal 36: 1053–81. [Google Scholar] [CrossRef] [Green Version]

- Jahmane, Abderrahmane, and Brahim Gaies. 2020. Corporate social responsibility, financial instability and corporate financial performance: Linear, non-linear and spillover effects—The case of the CAC 40 companies. Finance Research Letters 34: 101483. [Google Scholar] [CrossRef]

- Jensen, Michael. 2001. Value maximisation, stakeholder theory, and the corporate objective function. European Financial Management 7: 297–317. [Google Scholar] [CrossRef] [Green Version]

- Jo, Hoje, and Haejung Na. 2012. Does CSR reduce firm risk? Evidence from controversial industry sectors. Journal of Business Ethics 110: 441–56. [Google Scholar] [CrossRef]

- Jo, Hoje, and Maretno A. Harjoto. 2012. The causal effect of corporate governance on corporate social responsibility. Journal of Business Ethics 106: 53–72. [Google Scholar] [CrossRef]

- Jones, Thomas M. 1995. Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review 20: 404–37. [Google Scholar] [CrossRef]

- Kanouse, David E., and L. Reid Hanson Jr. 1972. Negativity in evaluations. In Attribution: Perceiving the Causes of Behavior. Edited by Edward E. Jones, David E. Kanouse, Harold H. Kelley, Richard E. Nisbett, Stuart Valins and Bernard Weiner. Morristown: General Learning Press, pp. 47–62. [Google Scholar] [CrossRef]

- Li, Zhichuan, Dylan B. Minor, Jun Wang, and Chong Yu. 2019. A learning curve of the market: Chasing alpha of socially responsible firms. Journal of Economic Dynamics and Control 109: 103772. [Google Scholar] [CrossRef]

- Lin-Hi, Nick, and Karsten Müller. 2013. The CSR bottom line: Preventing corporate social irresponsibility. Journal of Business Research 66: 1928–36. [Google Scholar] [CrossRef]

- Lu, Weisheng, K. W. Chau, Hongdi Wang, and Wei Pan. 2014. A decade’s debate on the nexus between corporate social and corporate financial performance: A critical review of empirical studies 2002–2011. Journal of Cleaner Production 79: 195–206. [Google Scholar] [CrossRef] [Green Version]

- Luo, Xueming, Christian Homburg, and Jan Wieseke. 2010. Customer satisfaction, analyst stock recommendations, and firm value. Journal of Marketing Research 47: 1041–58. [Google Scholar] [CrossRef]

- Lyon, Thomas, Yao Lu, Xinzheng Shi, and Qie Yin. 2013. How do investors respond to Green Company Awards in China? Ecological Economics 94: 1–8. [Google Scholar] [CrossRef]

- Maqbool, Shafat, and M. Nasir Zameer. 2018. Corporate social responsibility and financial performance: An empirical analysis of Indian banks. Future Business Journal 4: 84–93. [Google Scholar] [CrossRef]

- Mason, Chris, and John Simmons. 2014. Embedding corporate social responsibility in corporate governance: A stakeholder systems approach. Journal of Business Ethics 119: 77–86. [Google Scholar] [CrossRef]

- McWilliams, Abagail, and Donald Siegel. 2001. Corporate social responsibility: A theory of the firm perspective. Academy of Management Review 26: 117–27. [Google Scholar] [CrossRef]

- Mishra, Saurabh, and Sachin B. Modi. 2013. Positive and negative corporate social responsibility, financial leverage, and idiosyncratic risk. Journal of Business Ethics 117: 431–48. [Google Scholar] [CrossRef]

- Nekhili, Mehdi, Haithem Nagati, Tawhid Chtioui, and Claudia Rebolledo. 2017. Corporate social responsibility disclosure and market value: Family versus nonfamily firms. Journal of Business Research 77: 41–52. [Google Scholar] [CrossRef]

- Nguyen, Pascal, and Anna Nguyen. 2015. The effect of corporate social responsibility on firm risk. Social Responsibility Journal 11: 324–39. [Google Scholar] [CrossRef]

- Nollet, Joscha, George Filis, and Evangelos Mitrokostas. 2016. Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Economic Modelling 52: 400–7. [Google Scholar] [CrossRef] [Green Version]

- Oikonomou, Ioannis, Chris Brooks, and Stephen Pavelin. 2012. The impact of corporate social performance on financial risk and utility: A longitudinal analysis. Financial Management 41: 483–515. [Google Scholar] [CrossRef] [Green Version]

- Oikonomou, Ioannis, Chris Brooks, and Stephen Pavelin. 2014. The financial effects of uniform and mixed corporate social performance. Journal of Management Studies 51: 898–925. [Google Scholar] [CrossRef]

- Okafor, Anthony, Michael Adusei, and Bosede Ngozi Adeleye. 2021. Corporate social responsibility and financial performance: Evidence from US tech firms. Journal of Cleaner Production 292: 126078. [Google Scholar] [CrossRef]

- Pekovic, Sanja, and Sebastian Vogt. 2021. The fit between corporate social responsibility and corporate governance: The impact on a firm’s financial performance. Review of Managerial Science 15: 1095–125. [Google Scholar] [CrossRef]

- Price, Joseph M., and Wenbin Sun. 2017. Doing good and doing bad: The impact of corporate social responsibility and irresponsibility on firm performance. Journal of Business Research 80: 82–97. [Google Scholar] [CrossRef]

- Ramzan, Muhammad, Muhammad Amin, and Muhammad Abbas. 2021. How does corporate social responsibility affect financial performance, financial stability, and financial inclusion in the banking sector? Evidence from Pakistan. Research in International Business and Finance 55: 101314. [Google Scholar] [CrossRef]

- Reverte, Carmelo, Eduardo Gomez-Melero, and Juan Gabriel Cegarra-Navarro. 2016. The influence of corporate social responsibility practices on organizational performance: Evidence from Eco-Responsible Spanish firms. Journal of Cleaner Production 112: 2870–84. [Google Scholar] [CrossRef]

- Roodman, David. 2009. How to do xtabond2: An introduction to difference and system. gmm in stata. The Stata Journal 9: 86–136. [Google Scholar] [CrossRef] [Green Version]

- Rossi, Matteo, Jamel Chouaibi, Salim Chouaibi, Wafa Jilani, and Yamina Chouaibi. 2021. Does a Board Characteristic Moderate the Relationship between CSR Practices and Financial Performance? Evidence from European ESG Firms. Journal of Risk and Financial Management 14: 354. [Google Scholar] [CrossRef]

- Schwarz, Gideon. 1978. Estimating the dimension of a model. The Annals of Statistics 6: 461–64. [Google Scholar] [CrossRef]

- Sroufe, Robert, and Venugopal Gopalakrishna-Remani. 2019. Management, social sustainability, reputation, and financial performance relationships: An empirical examination of US firms. Organization & Environment 32: 331–62. [Google Scholar] [CrossRef] [Green Version]

- St-Pierre, Josée, Pierre-André Julien, and Martin Morin. 2010. L’effet de l’âge et de la taille sur la performance financière et économique des PME. Journal of Small Business & Entrepreneurship 23: 287–306. [Google Scholar] [CrossRef]

- Sun, Wenbin, and Kexiu Cui. 2014. Linking corporate social responsibility to firm default risk. European Management Journal 32: 275–87. [Google Scholar] [CrossRef]

- Sun, Wenbin, and Zhihua Ding. 2021. Is doing bad always punished? A moderated longitudinal analysis on corporate social irresponsibility and firm value. Business & Society 60: 1811–48. [Google Scholar] [CrossRef]

- Sweetin, Vernon H., Lynette L. Knowles, John H. Summey, and Kand S. McQueen. 2013. Willingness-topunish the corporate brand for corporate social irresponsibility. Journal of Business Research 66: 1822–30. [Google Scholar] [CrossRef]

- Taylor, Joseph, Joseph Vithayathil, and Dobin Yim. 2018. Are corporate social responsibility (CSR) initiatives such as sustainable development and environmental policies value enhancing or window dressing? Corporate Social Responsibility and Environmental Management 25: 971–80. [Google Scholar] [CrossRef]

- Van Marrewijk, Marcel. 2003. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. Journal of Business Ethics 44: 95–105. [Google Scholar] [CrossRef]

- Veitch, Russell, and William Griffitt. 1976. Good news-bad news: Affective and interpersonal effects. Journal of Applied Social Psychology 6: 69–75. [Google Scholar] [CrossRef]

- Velte, Patrick. 2017. Does ESG performance have an impact on financial performance? Evidence from Germany. Journal of Global Responsibility 8: 169–78. [Google Scholar] [CrossRef]

- Wang, Zhihong, and Joseph Sarkis. 2017. Corporate social responsibility governance, outcomes, and financial performance. Journal of Cleaner Production 162: 1607–16. [Google Scholar] [CrossRef]

- Weber, Olaf. 2017. Corporate sustainability and financial performance of Chinese banks. Sustainability Accounting, Management and Policy Journal 8: 358–85. [Google Scholar] [CrossRef] [Green Version]

- Yang, Shou-Lin. 2016. Corporate social responsibility and an enterprise’s operational efficiency: Considering competitor’s strategies and the perspectives of long-term engagement. Quality & Quantity 50: 2553–69. [Google Scholar] [CrossRef]

{kind=link}

| Variables | N | Mean | Standard Deviation | First Quartile | Median | Third Quartile | Minimum | Maximum |

|---|---|---|---|---|---|---|---|---|

| Tobin’s Q | 486 | 1.1224 | 0.8884 | 0636 | 0.89 | 1.338 | 0.254 | 7.86 |

| CSP | 486 | 0.5609 | 0.1498 | 0.44 | 0.56 | 0.68 | 0.22 | 0.92 |

| CSR | 486 | 0.6468 | 0.1324 | 0.57 | 0.65 | 0.75 | 0.25 | 0.92 |

| CSI | 486 | 0.5241 | 0.2274 | 0.37 | 0.41 | 0.79 | 0.08 | 1 |

| B-SIZE | 486 | 13.265 | 3.52 | 11 | 13 | 16 | 5 | 26 |

| INDEP | 486 | 0.5147 | 0.1928 | 0.39 | 0.47 | 0.64 | 0.07 | 1 |

| DUAL | 486 | 0.5844 | 0.4933 | 0 | 1 | 1 | 0 | 1 |

| BIG4 | 486 | 0.5185 | 0.5002 | 0 | 1 | 1 | 0 | 1 |

| F-SIZE | 486 | 9.297 | 1.316 | 8.34 | 9.08 | 10.28 | 6.53 | 12.54 |

| AGE | 486 | 3.871 | 0.8553 | 3.3 | 3.81 | 4.5 | 0 | 5.24 |

| LEV | 486 | 0.8736 | 1.2036 | 0.331 | 0.6355 | 1.129 | −5.061 | 11 |

| GROWTH | 486 | 0.0587 | 0.1276 | 0 | 0.04 | 0.1 | −0.59 | 0.74 |

| ICB Code | Industry | Firms Number | Percentage of Firms | Tobin’s Q | CSP | CSR | CSI |

|---|---|---|---|---|---|---|---|

| 0001 | Oil & Gas | 4 | 4.9% | 0.8108 | 51.17% | 60.42% | 51.75% |

| 1000 | Basic Materials | 4 | 4.9% | 1.0423 | 55.83% | 63.33% | 53.5% |

| 2000 | Industrials | 22 | 27.2% | 0.9614 | 57.24% | 63.47% | 49.30% |

| 3000 | Consumer Goods | 16 | 19.8% | 1.5862 | 54.75% | 65.70% | 56.41% |

| 4000 | Health Care | 5 | 6.2% | 1.6117 | 52.03% | 59.63% | 48% |

| 5000 | Consumer services | 17 | 21% | 0.8829 | 59.86% | 68.82% | 52.52% |

| 6000 | Telecommunications | 1 | 1.2% | 0.7933 | 42.67% | 72.67% | 87% |

| 7000 | Utilities | 5 | 6.2% | 0.6399 | 49.77% | 66.33% | 69.5% |

| 9000 | Technology | 7 | 8.6% | 1.41581 | 58.64% | 60.62% | 43.79% |

| Total | 81 | 100% | 1.1224 | 56.09% | 64.58% | 52.41% | |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Tobin’s Q | 1 | |||||||||||

| 2. CSP | 0.0337 | 1 | ||||||||||

| 3. CSR | −0.1013 ** | 0.5325 *** | 1 | |||||||||

| 4. CSI | −0.1978 *** | −0.2950 *** | 0.2709 *** | 1 | ||||||||

| 5. B-SIZE | −0.2056 *** | −0.1273 *** | 0.2304 *** | 0.3012 *** | 1 | |||||||

| 6. INDEP | −0.0851 * | 0.1916 *** | 0.2796 *** | 0.0393 | −0.2751 *** | 1 | ||||||

| 7. DUAL | −0.2062 *** | −0.1273 *** | −0.0325 | −0.0506 | 0.2899 *** | −0.1840 *** | 1 | |||||

| 8. BIG4 | −0.1392 *** | 0.1224 *** | 0.4190 *** | 0.2165 *** | 0.2047 *** | 0.0249 | 0.1315 *** | 1 | ||||

| 9. F-SIZE | −0.2858 *** | −0.0620 | 0.4665 *** | 0.4243 *** | 0.6225 *** | −0.0016 | 0.1621 *** | 0.3135 *** | 1 | |||

| 10. AGE | 0.1658 *** | 0.0704 | 0.1215 *** | −0.0653 | 0.0894 ** | −0.0529 | 0.0203 | −0.0251 | 0.1883 *** | 1 | ||

| 11. LEV | −0.1938 *** | 0.0104 | 0.0751 * | 0.0458 | 0.0628 | 0.0173 | −0.0063 | 0.0339 | 0.1898 *** | 0.0302 | 1 | |

| 12. GROWTH | 0.2012 *** | −0.0455 | −0.1920 *** | −0.1096 ** | −0.0996 ** | −0.0082 | 0.0108 | −0.1154 ** | −0.1056 ** | 0.0495 | 0.0035 | 1 |

| Variables | Equation (1) | Equation (2) | ||

|---|---|---|---|---|

| Coefficient | P > ∣z∣ | Coefficient | P > ∣z∣ | |

| Tobin’s Qt−1 | 0.3856 *** | 0.000 | 0.3887 | 0.000 |

| CSP | 0.0477 | 0.447 | - | - |

| CSR | - | - | 0.0158 | 0.931 |

| CSI | - | - | −0.2823 *** | 0.000 |

| B-SIZE | −0.0040 | 0.648 | −0.0045 | 0.593 |

| INDEP | 0.0509 | 0.599 | 0.0324 | 0.722 |

| DUAL | 0.0237 | 0.469 | 0.0056 | 0.855 |

| BIG4 | −0.1612 *** | 0.001 | −0.1508 *** | 0.004 |

| SIZE | −0.3112 *** | 0.002 | −0.2231 ** | 0.036 |

| AGE | −0.0891 | 0.426 | −0.0618 | 0.555 |

| LEV | 0.0076 * | 0.059 | 0.0042 | 0.205 |

| GROWTH | 0.0886 | 0.417 | 0.0866 | 0.374 |

| Year-industry fixed effects | Yes | Yes | ||

| Wald chi square | 143.14 *** | 191.11 *** | ||

| Arellano-Bond test AR(1) (z, p-value) | −2.9353 (0.0033) | −3.0345 (0.0024) | ||

| Arellano-Bond test AR(2) (z, p-value) | −0.3810 (0.7032) | −0.48049 (0.6309) | ||

| Sargan Test (Chi2, p-value) | 14.2936 (0.1123) | 14.6089 (0.1023) | ||

| Variables | Coefficient | Z-Statistic | P > ∣z∣ |

|---|---|---|---|

| Tobin’s Qt−1 | 0.1444 | 1.32 | 0.186 |

| CSRt−1 | 0.8331 * | 1.69 | 0.091 |

| CSIt−1 | −0.2685 ** | −2.59 | 0.010 |

| B-SIZE | 0.0252 | 1.06 | 0.287 |

| INDEP | 1.0580 ** | 2.01 | 0.044 |

| DUAL | 0.0692 | 0.38 | 0.707 |

| BIG4 | −0.2786 | −1.50 | 0.134 |

| F-SIZE | −0.5116 *** | −2.62 | 0.009 |

| AGE | 0.4100 | 1.17 | 0.242 |

| LEV | 0.0370 * | 1.86 | 0.063 |

| GROWTH | −0.0551 | −0.26 | 0.794 |

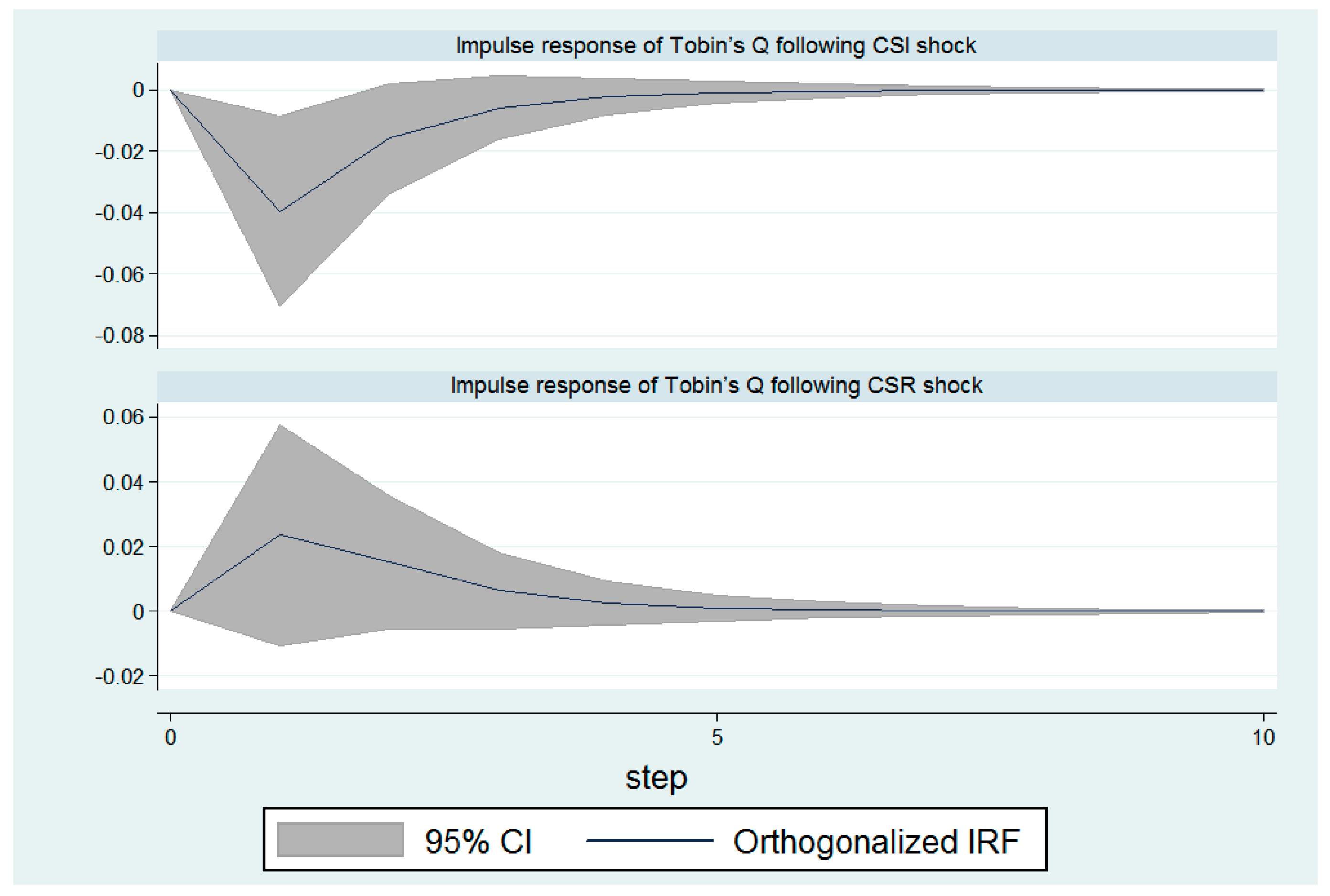

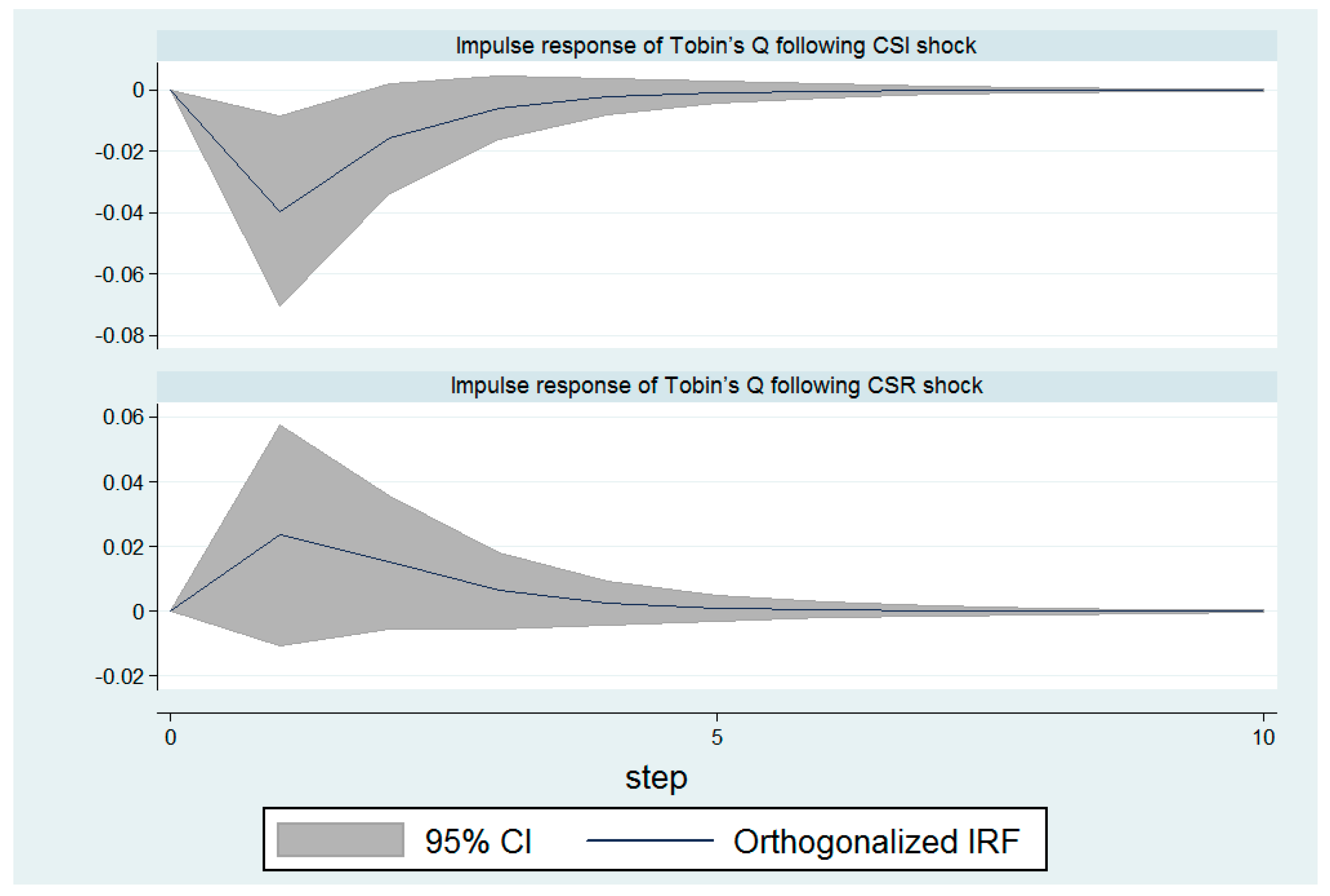

| Response Variable: Tobin’s Q | Impulse Variables | |

|---|---|---|

| CSR | CSI | |

| Periods | ||

| 1 | 0 | 0 |

| 2 | 0.0161 | 0.0456 |

| 3 | 0.0225 | 0.0521 |

| 4 | 0.0236 | 0.0529 |

| 5 | 0.0238 | 0.0530 |

| 6 | 0.0238 | 0.0531 |

| 7 | 0.0238 | 0.0531 |

| 8 | 0.0238 | 0.0531 |

| 9 | 0.0238 | 0.0531 |

| 10 | 0.0238 | 0.0531 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Boukattaya, S.; Omri, A. Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France. Int. J. Financial Stud. 2021, 9, 54. https://doi.org/10.3390/ijfs9040054

Boukattaya S, Omri A. Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France. International Journal of Financial Studies. 2021; 9(4):54. https://doi.org/10.3390/ijfs9040054

Chicago/Turabian StyleBoukattaya, Sonia, and Abdelwahed Omri. 2021. "Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France" International Journal of Financial Studies 9, no. 4: 54. https://doi.org/10.3390/ijfs9040054

APA StyleBoukattaya, S., & Omri, A. (2021). Corporate Social Practices and Firm Financial Performance: Empirical Evidence from France. International Journal of Financial Studies, 9(4), 54. https://doi.org/10.3390/ijfs9040054