Corporate Social Responsibility: Motives and Financial Performance

Abstract

1. Introduction

2. CSR: The Underlying Motives and the Actual Financial Performance

2.1. Extrinsic Motives

2.2. Intrinsic Motives

2.3. The Actual Financial Performance and the Jordanian Context

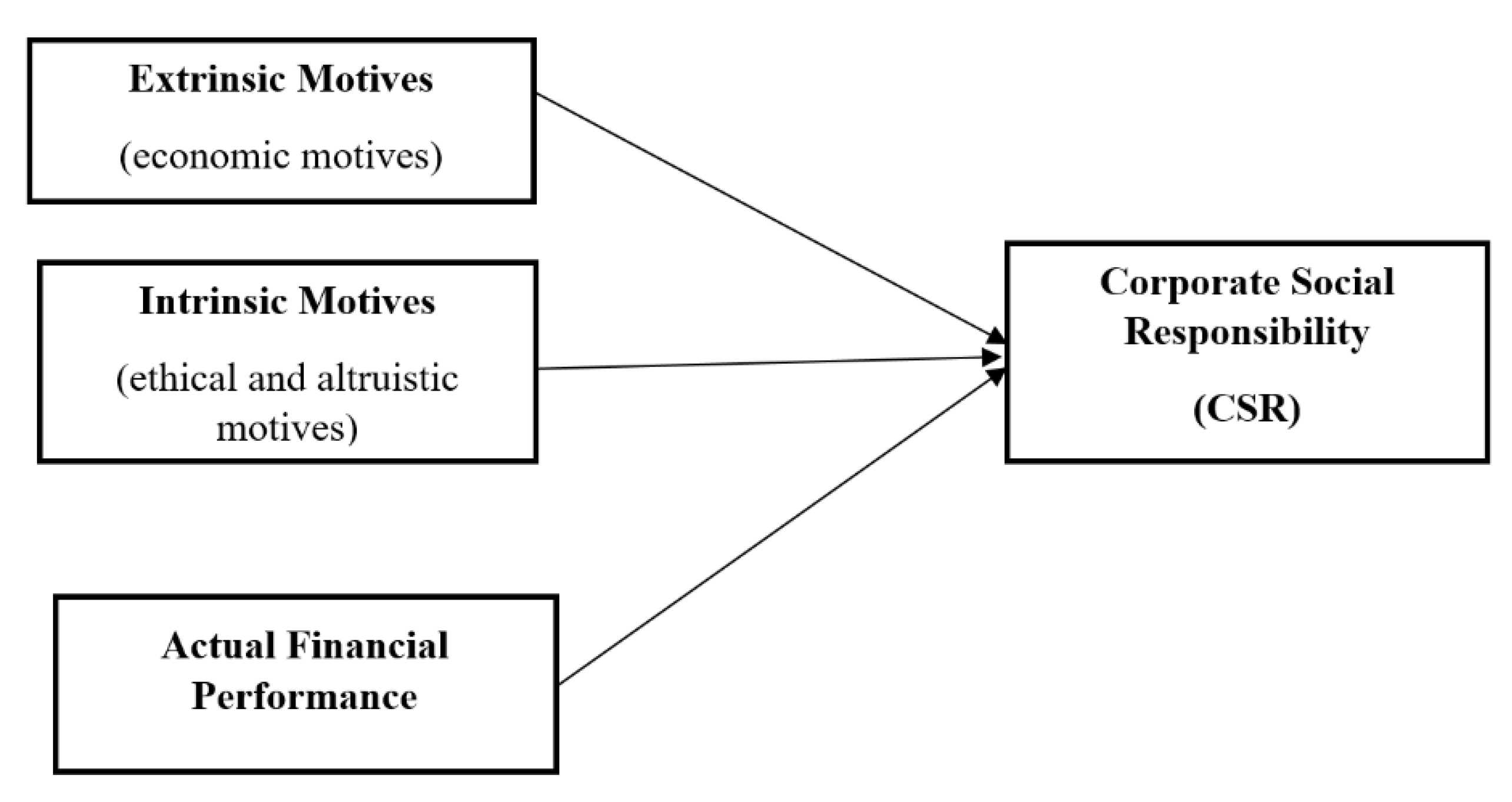

3. Theoretical Framework

- a competitive advantage among peers;

- a provider of a good corporate reputation;

- a promoter of the firm’s products;

- a quality that attracts qualified employees and improves personnel productivity; and

- a value-added activity that is comparable to R&D and advertising.

- an ethical obligation, i.e., managers feel obliged to do it because it is right, not because it is enjoyable; and

- altruism, whereby managers enjoy contributing to the common good and the well-being of others.

- the actual return on assets is better compared to peers; and

- the actual net profit margins are better compared to peers in the same industry sector.

4. Methodology

4.1. Measurements of Variables

4.1.1. Measurement of CSR

4.1.2. Measurement of the Motives behind CSR

- : extrinsic motive;

- : the perceived impact of CSR on financial performance;

- : the relative importance of financial performance;

- : ethical motive;

- : the perception that CSR is an ethical duty;

- : the relative importance of meeting ethical duty.

4.1.3. The Actual Financial Performance

4.1.4. Control Variables

4.2. The Population and the Study Sample

5. Empirical Findings and Discussion

5.1. Descriptive Statistics

5.2. Empirical Results

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Abu Farha, Enas, and Mahmoud Alkhalaileh. 2016. The relationship between corporate social responsibility’s disclosure and financial performance: An empirical study of Jordanian companies listed on Amman Stock Exchange. Jordan Journal of Business Administration 12: 401–15. [Google Scholar] [CrossRef]

- Abuzanoona, W. T. 2012. The Effect of Corporate Social Responsibility and Organizational Culture on Innovation Climate: Analytical Study on the Banking Sector in Jordan. Available online: https://theses.ju.edu.jo/Original_Abstract/JUF0725297.pdf (accessed on 15 February 2018).

- Albdour, Ali Abbaas, and Ikhlas I. Altarawneh. 2012. Corporate Social Responsibility and Employee Engagement in Jordan. Available online: https://www.researchgate.net/publication/271316888_Corporate_Social_Responsibility_and_Employee_Engagement_in_Jordan (accessed on 6 July 2018).

- Ali, A., Ellisha Nasruddin, and Soh Keng Lin. 2010. The relationship between internal corporate social responsibility and organizational commitment within the banking sector in Jordan. World Academy of Science, Engineering and Technology 67: 262–81. [Google Scholar]

- Barnett, Michael L., and Robert M. Salomon. 2012. Does it Pay to be Really Good? Addressing the Shape of the Relationship Between Social and Financial Performance. Strategic Managment Journal 33: 1304–20. [Google Scholar] [CrossRef]

- Berenson, Mark, David Levine, Kathryn A. Szabat, and Timothy C. 2015. Basic Business Statistics Concepts and Applications. Essex: Pearson. [Google Scholar]

- Berman, Shawn L., Andrew C. Wicks, Suresh Kotha, and Thomas M. Jones. 1999. Does stakeholder orientation matter?: The relationship between stakeholder management models and firm financial performance. Academy of Management Journal 42: 488–506. [Google Scholar]

- Boli, John, and D. Hartsuiker. 2001. World culture and transnational corporations: Sketch of a project. Paper presented at International Conference on Effects of and Responses to Globalization, Istanbul, Turkey, May 21–22. [Google Scholar]

- Bowen, Howard. 1953. Social Responsibilities of the Businessman. New York: Harper & Row. [Google Scholar]

- Caiado, Rodrigo Goyannes Gusmão, Osvaldo Luiz Gonçalves Quelhas, Janice Helena de Oliveira Dias, Maria de Lurdes Costa Domingos, Sergio Luiz Braga França, and Marcelo Jasmim Meiriño. 2018. Adherence of social responsibility management in Brazilian organizations. Social Responsibility Journal 14: 194–212. [Google Scholar] [CrossRef]

- Carroll, Archie B. 1979. A three-dimensional conceptual model of corporate performance. Academy Management Review 4: 497–505. [Google Scholar] [CrossRef]

- Clarkson, Max. 1995. A Stakeholder Framework for Analyzing and Evaluating Corporate Social Performance. The Academy of Management Review 20: 92–117. [Google Scholar] [CrossRef]

- Dare, Julia. 2016. Will the Truth Set Us Free? An Exploration of CSR Motive and Commitment. Journal of the Center for Business Ethics 121: 85–122. [Google Scholar] [CrossRef]

- Dess, Gregory G., and Richard B. Robinson, Jr. 1984. Measuring organizational performance in the absence of objective measures: The case of the privately-held firm and conglomerate business unit. Strategic Management Journal 5: 265–75. [Google Scholar] [CrossRef]

- Etzioni, Amitai. 1988. The Moral Dimension: Towards a New Economics. New York: The Free Press. [Google Scholar]

- European Commission. 2001. A Sustainable Europe for a Better World: A European Strategy for Sustainable Development. Brussels: European Commission. [Google Scholar]

- Evan, William M., and R. Edward Freeman. 1988. A Stakeholder Theory of the Modern Corporation: Kantian Capitalism. Ethical Theory and Business, 75–84. [Google Scholar]

- Famiyeh, Samuel. 2017. Corporate Social Responsibility and Firm’s Performance: Empirical Evidence. Social Responsibility Journal 13: 390–406. [Google Scholar] [CrossRef]

- Freeman, R. 1984. Strategic Management: A Stakeholder Approach. Boston: Pitman. [Google Scholar]

- Freeman, Ina, and Amir Hasnaoui. 2010. The Meaning of Corporate Social Responsibility: The Vision of Four Nations. Journal of Business Ethics 100: 419–43. [Google Scholar] [CrossRef]

- Friedman, Milton. 1970. The Social Responsibility of Business is to Increase its Profits. New York Times Magazine, Sepetmber 13, 122–26. [Google Scholar]

- Galaskiewicz, Joseph, and Michelle Sinclair Colman. 2006. collaboration between corporations and nonprofit organizations. In The Non-Profit Sector: A Research Handbook. Edited by Walter W. Powell and Richard Steinberg. New Haven: Yale University Press, pp. 180–200. [Google Scholar]

- Gardberg, Naomi A., and Charles J. Fombrun. 2006. Corporation Citizenship: Creating Intangible Assets Across institutional Environments. Academy of Management Review 31: 329–46. [Google Scholar] [CrossRef]

- Goergen, Marc. 2012. International Corporate Governance. Harlow: Pearson Education Limited. [Google Scholar]

- Golden rule in Islam. 2017. Qur’an Today. Available online: http://quraan-today.blogspot.com/2014/01/golden-rule-in-Islam-treat-others-as.html (accessed on 21 May 2018).

- Graafland, Johan, and Bert Van de Ven. 2006. Strategic and Moral Motivation for Corporate Social Responsibility. Journal of Corporate Citizenship 22: 111–23. [Google Scholar] [CrossRef]

- Graafland, Johan, and Corrie Mazereeuw-Van der Duijn Schouten. 2012. Motives for Corporate Social Responsibility. De Economist 160: 377–96. [Google Scholar] [CrossRef]

- Graafland, Johan J., Sylvester C. W. Eijffinger, and H. SmidJohan. 2004. Benchmarking of Corporate Social Responsibility: Methodological Problems and Robustness. Journal of Business Ethics 53: 137–52. [Google Scholar] [CrossRef]

- Hair, Joseph F., Ralph E. Anderson, Ronald L. Tatham, and William C. Black. 1998. Multivariate Data Analysis. New Jersey: Prentice Hall. [Google Scholar]

- Hemingway, Christine A., and Patrick W. Maclagan. 2004. Managers’ personal values as drivers of corporate social responsibility. Journal of Business Ethics 50: 33–44. [Google Scholar] [CrossRef]

- Hillman, Amy J., and Gerald D. Keim. 2001. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strategic Managment Journal 22: 125–39. [Google Scholar] [CrossRef]

- Hofstede Insights. 2020. Available online: https://www.hofstede-Insights.com/country-comparison/jordan/ (accessed on 12 May 2020).

- Homburg, Christian, Harley Krohmer, and John P. Workman. 1999. Strategic consensus and performance: The role of strategy type and market-related dynamism. Strategic Management Journal 20: 339–57. [Google Scholar] [CrossRef]

- Ikram, Atif, Zhichuan Frank Li, and Travis MacDonald. 2020. CEO Pay Sensitivity (Delta and Vega) and Corporate Social Responsibility. Sustainability 12: 7941. [Google Scholar] [CrossRef]

- Jamali, Dima, Asem M. Safieddine, and Myriam Rabbath. 2008. Corporate Governance and Corporate Social Responsibility Synergies and Interrelationships. Corporate Governance: An International Review 16: 443–59. [Google Scholar] [CrossRef]

- Janamrung, Benjamas, and Panya Issarawornrawanich. 2015. The association between corporate social responsibility index and performance of firms in industrial products and resources industries: Empirical evidence from Thailand. Social Responsibility Journal 11: 893–903. [Google Scholar] [CrossRef]

- Jones, Thomas M. 1995. Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review 20: 404–37. [Google Scholar] [CrossRef]

- Lee, Min-Dong Paul. 2008. A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead. International Journal of Management Reviews 10: 53–73. [Google Scholar] [CrossRef]

- Matten, Dirk, and Jeremy Moon. 2008. “Implicit” and “explicit” CSR: A conceptual framework for a comparative understanding of corporate social responsibility. The Academy of Management Review 33: 404–24. [Google Scholar] [CrossRef]

- Matthew 7:12. n.d. Bible Gateway. Available online: https://www.biblegateway.com/passage/?search=Matthew+7:12 (accessed on 3 February 2017).

- McWilliams, Abagail, and Donald Siegel. 2001. Corporate social responsibility: A theory of the firm perspective. Academy ofManagement Review 26: 117–27. [Google Scholar]

- Miles, Morgan P., and Jeffrey G. Covin. 2000. Environmental marketing: A source of reputational, competitive. Journal of Business Ethics 23: 299–311. [Google Scholar] [CrossRef]

- Montgomery, Douglas C., Elizabeth A. Peck, and G. Geoffrey Vining. 2007. Introduction to Linear Regression Analysis, 4th ed. Hoboken: John Wiley & Sons Inc. [Google Scholar]

- Omar, Bilal Fayiz, and Nidal Omar Zallom. 2016. Corporate social responsibility and market value: Evidence from Jordan. Journal of Financial Reporting and Accounting 14: 2–29. [Google Scholar] [CrossRef]

- Renneboog, Luc, Jenke Ter Horst, and Chendi Zhang. 2008. The price of ethics: Evidence from socially responsible mutual funds around the world. Journal of Corporate Finance 14: 302–22. [Google Scholar] [CrossRef]

- Rowley, Timothy J. 1997. Moving Beyond Dyadic Ties: A Network Theory of Stakeholder Influences. Academy of Management Review 22: 887–910. [Google Scholar] [CrossRef]

- Schopenhauer, Arthur. 1840. On the Basis of Morality. Translated by E. F. Payne. Ann Arbor: The University of Michigan. New York: Berghahn Books. [Google Scholar]

- Sen, Sankar, and Chitra Bhanu Bhattacharya. 2001. Does Doing Good Always Lead to Doing Better? Consumer Reactions to Corporate Social Responsibility. Journal of Marketing Research 38: 43–62. [Google Scholar] [CrossRef]

- Stovall, O. Scott, John D. Neill, and David Perkins. 2004. Corporate Governance, Internal Decision Making, and the Invisible Hand. Journal of Business Ethics 51: 221–27. [Google Scholar] [CrossRef]

- Torugsa, Nuttaneeya Ann, Wayne O’Donohue, and Rob Hecker. 2012. Capabilities, Proactive CSR and Financial Performance in SMEs: Empirical Evidence from an Australian Manufacturing Industry sector. Journal of Business Ethics 109: 483–500. [Google Scholar] [CrossRef]

- Turban, Daniel B., and Daniel W. Greening. 1996. Corporate social performance and organizational attractiveness. Academy of Management Journal 40: 658–72. [Google Scholar]

- Turker, Duygu. 2009. Measuring Corporate Social Responsibility: A Scale Development Study. Journal of Business Ethics 85: 411–27. [Google Scholar] [CrossRef]

- Waddock, Sandra A., and Samuel B. Graves. 1997. The Corporate Social Performance-Financial Performance Link. Strategic Managment Journal 18: 303–19. [Google Scholar] [CrossRef]

- Wallich, H. C., and J. J. Mcgowan. 1970. A New Rationale for Corporate Social Policy. New York: Committee for Economic Development. [Google Scholar]

{kind=link}

| No. | Item | Category |

|---|---|---|

| 1. | Our company supports employees who want to acquire additional education. | Employees |

| 2. | Our company offers equal opportunities for minorities. | |

| 3. | Our company offers equal opportunities for women. | |

| 4. | Our company offers equal opportunities to all its employees. | |

| 5. | Our company prevents abuse in the workplace. | |

| 6. | There is an influence of the works council on company policy. | |

| 7. | The management of our company is primarily concerned with employees’ needs and wants. | |

| 8. | Our company contributes to employee safety more than is required by law. | |

| 9. | Our company policies encourage employees to develop their skills and careers and offer an individual training program. | |

| 10. | Our company has complaint procedures for customers. | Customers |

| 11. | Our company respects consumer rights beyond the legal requirements. | |

| 12. | Development of a sustainable alternative for customers. | |

| 13. | Our company works on increasing employee attention to the environment. | Environment |

| 14. | Our company works on reducing pollution more than is required by law. | |

| 15. | Our company prevents inside trading of stocks. | Shareholders |

| 16. | Our company adopts a long-term perspective in decision-making in order to guarantee sufficient cash flow and produce a persistent superior return to shareholders/owners. | |

| 17. | Our company competes with its rivals in an ethical framework and respect their intellectual property. | Competitors |

| 18. | Our company makes investments to create a better life for future generations. | Society |

| 19. | Our company does charity donations, financial support for people, and activities for the well-being of society. | |

| 20. | Our company strives to create employment opportunities. | |

| 21. | Our company tries to help the government/NGO in solving social problems. | |

| 22. | Our company contributes to the reintegration of the disabled more than is required by law. | |

| 23. | Our company complies with the Jordanian corporate governance code. | |

| 24. | Our company has control over the labor standards of suppliers for compliance with legal requirements, i.e., safety, environmental standards. | Suppliers |

| 25. | Our company has a complaints procedure for suppliers. | |

| 26. | Our company performs quality control of supplier products. | |

| 27. | Code of ethics Yes/No | Use of instruments |

| 28. | Ethics committee Yes/No | |

| 29. | Ethical training Yes/No | |

| 30. | Use of external audits Yes/No | |

| 31. | Code of conduct Yes/No | |

| 32. | ISO certification Yes/No | |

| 33. | Social manual Yes/No | |

| 34. | Social reporting Yes/No |

| We allocated up to, but not more than, 10 points to each of the set of statements (0 represents the least degree of importance). |

| Panel (1) Our company performs in a manner consistent with: |

|

|

|

|

| Panel (2) Our company monitors new opportunities that can enhance the organization’s: |

|

|

|

|

| Panel (3) Our company is committed to: |

|

|

|

|

| Sector | % | Company Age | % | Size | % | Public | % |

|---|---|---|---|---|---|---|---|

| Pharmaceutical | 17.2 | <3 years | 15.6 | Very small | 10.9 | Public | 17.2 |

| Financial Services | 18.8 | from 3 to <10 years | 37.5 | Small | 43.8 | Non-public | 82.8 |

| Construction | 28.1 | from 10 to <20 years | 18.8 | Medium | 18.8 | ||

| Technology & Telecom | 29.7 | >20 years | 28.1 | Large | 26.5 | ||

| Farming | 6.2 | ||||||

| Total | 100 | Total | 100 | Total | 100 | Total | 100 |

| Mean | SD | Min | Median | Max | |

|---|---|---|---|---|---|

| CSR | 3.22 | 0.46 | 1.93 | 3.25 | 4.00 |

| Extrinsic Motives | 10.66 | 5.06 | 0 | 11.00 | 21.33 |

| Altruistic Motive | 1.76 | 0.87 | 0.33 | 1.66 | 4 |

| Ethical Motive | 7.50 | 3.00 | 2.66 | 7.5 | 16 |

| Intrinsic Motives | 9.26 | 3.32 | 4 | 9.16 | 17.66 |

| Actual Financial Performance | 3.14 | 0.84 | 1 | 3 | 5 |

| Publicly Listed | 0.17 | 0.38 | 0 | 0 | 1 |

| Pharmaceuticals | 0.17 | 0.38 | 0 | 0 | 1 |

| Construction | 0.28 | 0.45 | 0 | 0 | 1 |

| Farming | 0.06 | 0.24 | 0 | 0 | 1 |

| Tech. & Comm. | 0.29 | 0.46 | 0 | 0 | 1 |

| Fin. Service | 0.18 | 0.39 | 0 | 0 | 1 |

| Very Small | 0.10 | 0.31 | 0 | 0 | 1 |

| Small | 0.43 | 0.50 | 0 | 0 | 1 |

| Medium | 0.18 | 0.39 | 0 | 0 | 1 |

| Large | 0.26 | 0.44 | 0 | 0 | 1 |

| 0–3y | 0.15 | 0.36 | 0 | 0 | 1 |

| 3–10y | 0.37 | 0.48 | 0 | 0 | 1 |

| 10–20y | 0.18 | 0.39 | 0 | 0 | 1 |

| >20y | 0.28 | 0.45 | 0 | 0 | 1 |

| Extrinsic Motives | Intrinsic Motives | Act. Fin. Perform. | Publicly Listed | Pharma | Construction | Farming | Fin. Serv. | Tech & Comm. | Very Small | Small | Medium | Large | 0–3y | 3–10y | 10–20y | >20y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Extrinsic Motives | 1.000 | ||||||||||||||||

| Intrinsic Motives | −0.472 | 1.000 | |||||||||||||||

| Act. Fin Perform. | 0.078 | −0.014 | 1.000 | ||||||||||||||

| Publicly Listed | −0.006 | −0.237 | 0.096 | 1.000 | |||||||||||||

| Pharma | 0.166 | −0.057 | 0.047 | 0.012 | 1.000 | ||||||||||||

| Construction | −0.143 | 0.199 | −0.249 | −0.193 | −0.285 | 1.000 | |||||||||||

| Farming | −0.077 | −0.175 | 0.034 | 0.053 | −0.118 | −0.162 | 1.000 | ||||||||||

| Fin. Serv. | 0.089 | −0.043 | 0.229 | 0.312 | −0.219 | −0.301 | −0.124 | 1.000 | |||||||||

| Tech & Comm. | −0.032 | −0.020 | −0.007 | −0.115 | −0.296 | −0.406 | −0.168 | −0.312 | 1.000 | ||||||||

| Very Small | −0.008 | −0.082 | −0.343 | −0.195 | −0.025 | 0.069 | −0.074 | 0.026 | −0.030 | 1.000 | |||||||

| Small | 0.197 | −0.199 | −0.125 | −0.208 | 0.012 | 0.083 | 0.053 | −0.113 | −0.024 | −0.365 | 1.000 | ||||||

| Medium | −0.119 | 0.175 | 0.246 | 0.078 | 0.078 | −0.131 | 0.098 | 0.061 | −0.039 | −0.303 | −0.172 | 1.000 | |||||

| Large | −0.221 | 0.155 | 0.290 | 0.406 | −0.072 | 0.040 | 0.000 | 0.092 | −0.059 | −0.462 | −0.263 | −0.218 | 1.000 | ||||

| 0–3 y | 0.022 | −0.118 | −0.181 | −0.147 | 0.138 | 0.037 | 0.138 | −0.017 | −0.209 | 0.292 | −0.147 | 0.041 | −0.186 | 1.000 | |||

| 3–10y | 0.116 | −0.144 | −0.280 | −0.255 | 0.004 | 0.038 | −0.193 | −0.110 | 0.155 | 0.335 | 0.177 | −0.185 | −0.357 | −0.241 | 1.000 | ||

| 10–20y | −0.104 | 0.207 | 0.239 | −0.024 | −0.024 | −0.143 | 0.030 | 0.056 | 0.097 | −0.086 | −0.024 | 0.161 | −0.022 | −0.162 | −0.378 | 1.000 | |

| >20y | 0.029 | 0.016 | 0.267 | 0.452 | −0.009 | −0.005 | −0.018 | 0.145 | −0.102 | −0.358 | −0.193 | −0.026 | 0.522 | −0.201 | −0.469 | −0.316 | 1.000 |

| Unstandardized Coefficients | Standardized Coefficients * | p-Value | |

|---|---|---|---|

| Extrinsic Motives (H1) | 0.01 | 0.02 | 0.76 |

| Intrinsic Motives (H2) | 0.05 | 0.17 | 0.01 |

| Actual Financial Performance (H3) | 0.30 | 0.26 | 0.00 |

| Publicly Listed | 0.40 | 0.40 | 0.06 |

| Pharma. | 0.22 | 0.22 | 0.21 |

| Construction | 0.03 | 0.03 | 0.81 |

| Farming | 0.22 | 0.22 | 0.38 |

| Fin. Services | 0.06 | 0.06 | 0.72 |

| Very Small | 0.01 | 0.01 | 0.96 |

| Small | 0.15 | 0.15 | 0.42 |

| Medium | −0.12 | −0.12 | 0.50 |

| 0–3y | 0.35 | 0.35 | 0.09 |

| 3–10y | 0.28 | 0.28 | 0.11 |

| 10–20y | 0.06 | 0.06 | 0.70 |

| Unstandardized Coefficients | Standardized Coefficients | p-Value | |

|---|---|---|---|

| Extrinsic Motives (H1) | 0.02 | 0.11 | 0.23 |

| Ethical Motive (H2a) | 0.04 | 0.13 | 0.03 |

| Altruistic Motive (H2b) | 0.20 | 0.17 | 0.07 |

| Actual Financial Performance (H3) | 0.28 | 0.24 | 0.00 |

| Publicly Listed | 0.40 | 0.40 | 0.06 |

| Pharma | 0.21 | 0.21 | 0.22 |

| Construction | 0.03 | 0.03 | 0.81 |

| Farming | 0.26 | 0.26 | 0.31 |

| Fin. Service | 0.10 | 0.10 | 0.59 |

| Very Small | 0.03 | 0.03 | 0.86 |

| Small | 0.18 | 0.18 | 0.34 |

| Medium | −0.14 | −0.14 | 0.45 |

| 0–3y | 0.29 | 0.29 | 0.17 |

| 3–10y | 0.21 | 0.21 | 0.24 |

| 10–20y | 0.01 | 0.01 | 0.94 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Atmeh, M.; Shaban, M.; Alsharairi, M. Corporate Social Responsibility: Motives and Financial Performance. Int. J. Financial Stud. 2020, 8, 76. https://doi.org/10.3390/ijfs8040076

Atmeh M, Shaban M, Alsharairi M. Corporate Social Responsibility: Motives and Financial Performance. International Journal of Financial Studies. 2020; 8(4):76. https://doi.org/10.3390/ijfs8040076

Chicago/Turabian StyleAtmeh, Muhannad, Mohammad Shaban, and Malek Alsharairi. 2020. "Corporate Social Responsibility: Motives and Financial Performance" International Journal of Financial Studies 8, no. 4: 76. https://doi.org/10.3390/ijfs8040076

APA StyleAtmeh, M., Shaban, M., & Alsharairi, M. (2020). Corporate Social Responsibility: Motives and Financial Performance. International Journal of Financial Studies, 8(4), 76. https://doi.org/10.3390/ijfs8040076