1. Introduction

In modern manufacturing, the production of precision dies and molds is a critical operation that directly influences cost efficiency, part accuracy, and lead time. Dies are foundational components used in processes such as casting, forging, stamping, and plastic molding. Their fabrication must balance geometric complexity, material performance, and production volume. Traditionally, die manufacturing has relied on machining, a subtractive process involving CNC milling, wire EDM, and grinding. Machining offers high precision and tight tolerances but often suffers from high tool wear, material waste, and extended cycle times—especially when complex geometries or deep cavities are involved [

1,

2].

To address the limitations of machining in small-batch or intricate component production, conventional investment casting (CIC) has long been utilized. CIC involves creating wax or polymer patterns, coating them with ceramic slurry, and then evacuating the material to form a mold cavity. The method allows for near-net-shape production of highly detailed features with minimal machining post-processing. However, the CIC process is both labor- and logistics-intensive, requiring specialized handling for pattern fabrication, mold building, dewaxing, and metal pouring stages. This leads to high upfront tooling costs, long lead times, and inefficiencies when producing customized or limited-run parts [

3].

To overcome these challenges, rapid prototyping (RP) technologies such as stereo lithography (SLA), selective laser sintering (SLS), and fused deposition modeling (FDM) have been integrated into the casting workflow, an approach known as rapid investment casting (RIC). RP enables the direct fabrication of pattern geometries without metal tooling, reducing setup time and enabling mass customization. Studies show that RP-based casting can significantly reduce design iterations and improve the agility of product development cycles [

1,

4]. However, RP introduces its own limitations, including equipment cost, a limited material range for pattern creation, and relatively higher energy usage per unit part [

5,

6].

While all three methods—machining, CIC, and RP have unique advantages, there is a notable absence of unified cost modeling frameworks that quantitatively compare them under consistent economic assumptions. Previous studies have largely focused on performance metrics such as dimensional accuracy, tensile strength, or process throughput [

1,

2] without holistically evaluating the economic burden across design, logistics, production, and environmental costs. Moreover, studies that address cost modeling often focus on a single process and do not enable side-by-side decision-making for industrial users.

Therefore, the purpose of this study is to bridge this methodological gap by developing a comprehensive activity-based costing (ABC) model that evaluates the total cost structure of MP, CIC, and RP specifically for tooling and die production. This unified framework allows for a direct comparison of economic performance, identifies major cost drivers, and supports a more informed, sustainable, and flexible process selection for modern manufacturing environments.

2. Problem Statement

Despite the technical maturity of the machining process (MP), conventional investment casting (CIC), and rapid prototyping (RP), manufacturers often lack a reliable method to compare their total economic impact under consistent conditions. The existing literature tends to evaluate these processes in isolation, focusing on individual metrics such as dimensional accuracy or material behavior without integrating the full cost structure including design, logistics, production, and environmental cost. Moreover, the few studies that do explore cost often rely on simplified or generalized models that do not reflect process-specific cost drivers in practical industrial scenarios. This gap creates uncertainty for manufacturers, particularly when selecting the most cost-effective method for low-volume, high-precision tooling and die applications. Therefore, there is a need for a unified, data-driven cost modeling framework that enables a transparent quantitative comparison of MP, CIC, and RP and supports economically optimized decision-making.

3. Materials and Methods

3.1. Methodology and Data Collection

This study adopts the activity-based costing (ABC) methodology to construct a comprehensive cost model for three distinct die manufacturing approaches, namely the machining process (MP), conventional investment casting (CIC), and rapid prototyping (RP). ABC is particularly suited for manufacturing environments, as it enables detailed tracking and assignment of costs based on actual resource usage across all major stages, including design, logistics, production, and environmental impacts. By capturing cost drivers specific to each process, this approach allows for a granular and realistic evaluation of economic performance.

To ensure accuracy and relevance, all input data were derived from real-world experimental trials conducted under controlled conditions within a workshop setting. Each manufacturing method was applied to fabricate comparable low-volume dies. During these trials, critical cost-related parameters, such as labor time, machine utilization hours, energy consumption, material usage, and tool wear, were recorded systematically using digital energy meters, manual time tracking, and material flow documentation. In addition, equipment specifications and lifespan details were referenced from OEM datasheets and technical manuals.

Transportation costs were estimated using geographic data obtained via Google Maps, which provided accurate distances between material suppliers, foundry locations, and waste disposal sites. These distances were then used to calculate fuel consumption and carbon emissions based on standard truck parameters and emission factors published by environmental authorities. Waste generation data was collected during shell building and post-processing stages, with disposal charges determined using current rates from local municipal waste management services.

To test the stability and reliability of the developed cost model, a sensitivity analysis was conducted. This analysis examined how variations in key cost components, specifically labor cost, material cost, and environmental cost, affect the overall total cost in each manufacturing route. The objective was to identify the most cost-sensitive parameters and assess the model’s robustness under fluctuating economic and operational scenarios.

This rigorous combination of empirical data collection, geographic logistics mapping, and sensitivity analysis ensures that the resulting cost model not only reflects real industrial conditions but also provides actionable insights for manufacturers seeking to optimize process selection in terms of cost-effectiveness and sustainability.

3.2. Cost Modeling Equations

The total cost (C

total) for each manufacturing route was computed by summing three major components, namely design cost, logistics cost, and production cost, as shown in Equation (1).

Design Cost:

Design cost was estimated using the total number of designer hours multiplied by hourly rates, as defined below:

where

nd = number of designers;

Cd = design labor cost per hour;

td = time required for design in hours.

Logistics Cost:

Logistics cost included transportation, transport-related environmental costs, and waste disposal:

where

TCi = transportation cost per km;

Di = distance in km (obtained via Google Maps);

Ei = fuel energy per km;

ntruck = number of trucks used;

Cw = waste disposal cost per kg;

Qw = waste quantity in kg.

Production Cost:

Production cost was the most comprehensive component, composed of labor, material, equipment, energy, and environmental costs:

where

n = number of workers;

C = labor cost per hour;

t = total labor time;

Mc = cost per unit of material;

Q = quantity of material used;

EeqCi = equipment cost per hour;

tieq = equipment operating time;

ELi = equipment lifespan;

ECu = unit energy cost;

Pieq = equipment power rating (kW);

Eieq = emission intensity per kWh;

CECO2 = carbon cost per kg of CO2 emitted.

These equations, when applied to the collected data, enabled the generation of a complete cost profile for each process. The resulting values were then used for cross-comparison, performance evaluation, and strategic recommendation.

4. Results and Discussions

This section presents results for the comparative cost analysis of the three manufacturing processes, namely the machining process (MP), conventional investment casting (CIC), and rapid prototyping (RP), using the activity-based costing (ABC) framework. The model not only provides total cost estimations but also disaggregates expenses into design, logistics, production, and environmental components. To ensure the model’s robustness, sensitivity analysis was also conducted by varying key cost drivers, such as environmental cost and logistics parameters.

4.1. Total Cost Comparision

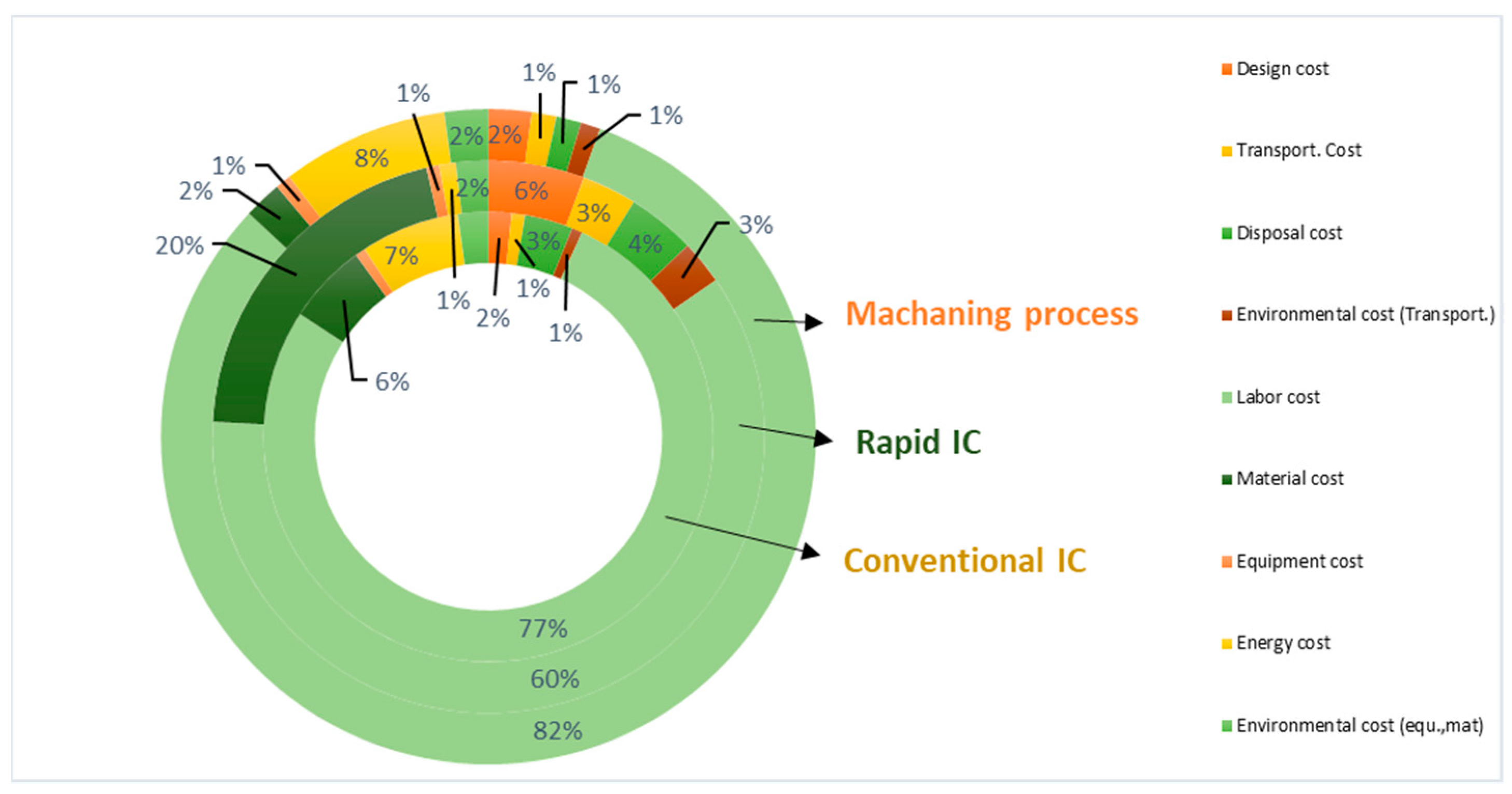

As shown in

Table 1, the rapid prototyping (RP) process demonstrates the lowest total cost (INR 124,685.50), which is significantly lower than the machining process (INR 330,252.70) and conventional investment casting (INR 422,600.35). While the MP has the highest production cost (94.45%), its logistics cost remains minimal (3.43%). CIC, on the other hand, incurs the highest total and logistics cost, reflecting inefficiencies in handling and transportation. The donut chart in

Figure 1 highlights these differences in proportional cost distribution across the three processes.

4.2. Cost Driver Analysis

Design costs were constant across all three processes, as the same digital model and design time were assumed.

Logistics cost plays a critical role in CIC, where material transport, disposal, and environmental costs increase due to the bulky and delicate wax pattern handling.

Production cost is heavily influenced by labor and energy consumption. CIC has the highest labor cost, whereas RIC benefits from significant reductions in manpower due to digital pattern fabrication.

In RP, although logistics cost is slightly higher than MP, it compensates through a drastic reduction in labor (INR 75,400 vs. INR 268,800 in MP) and energy costs, supporting its efficiency in small-batch production.

4.3. Senstivity Analysis

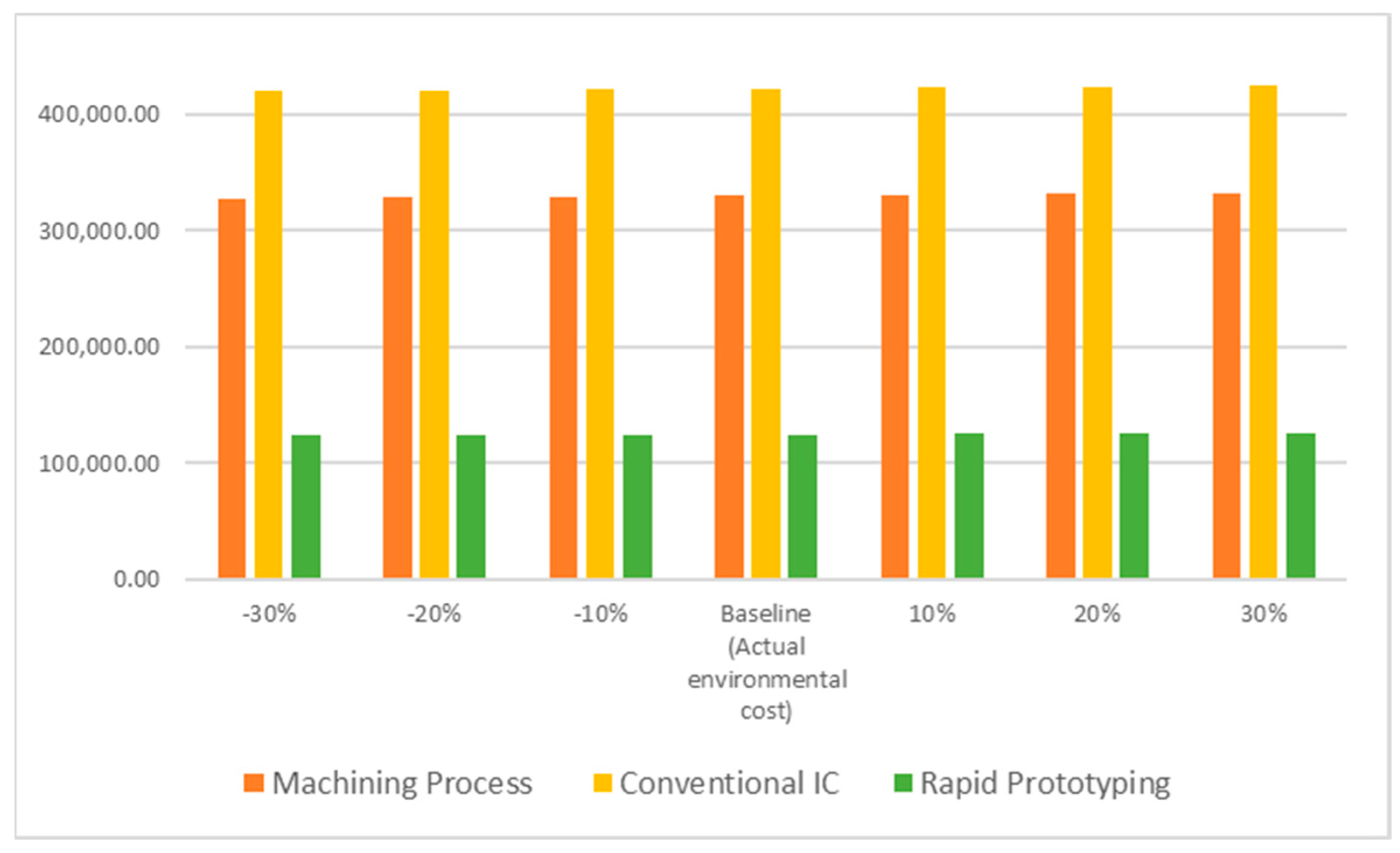

Sensitivity analysis was carried out to evaluate the influence of variations in key cost parameters on the overall outcome of the comparative assessment between the machining process (MP), conventional investment casting (CIC), and rapid prototyping (RP). The parameters considered for this analysis include environmental cost, labor cost, and logistic cost. These were selected based on their significant contribution to the total cost of the manufacturing processes under study.

A sensitivity analysis was conducted on environmental cost by varying it in a range of ±30% from the baseline, with intervals of 10%. The resulting trends are illustrated in

Figure 2.

Across all variations, conventional investment casting (CIC) consistently incurred the highest environmental cost, followed by the machining process (MP), while rapid prototyping (RP) exhibited the lowest cost. This pattern remained stable even under significant fluctuations in environmental cost, indicating that RP is comparatively more environmentally sustainable and less sensitive to environmental cost variations. The results clearly demonstrate that RP contributes to lower environmental burdens, thereby making it a more suitable option from a sustainability perspective.

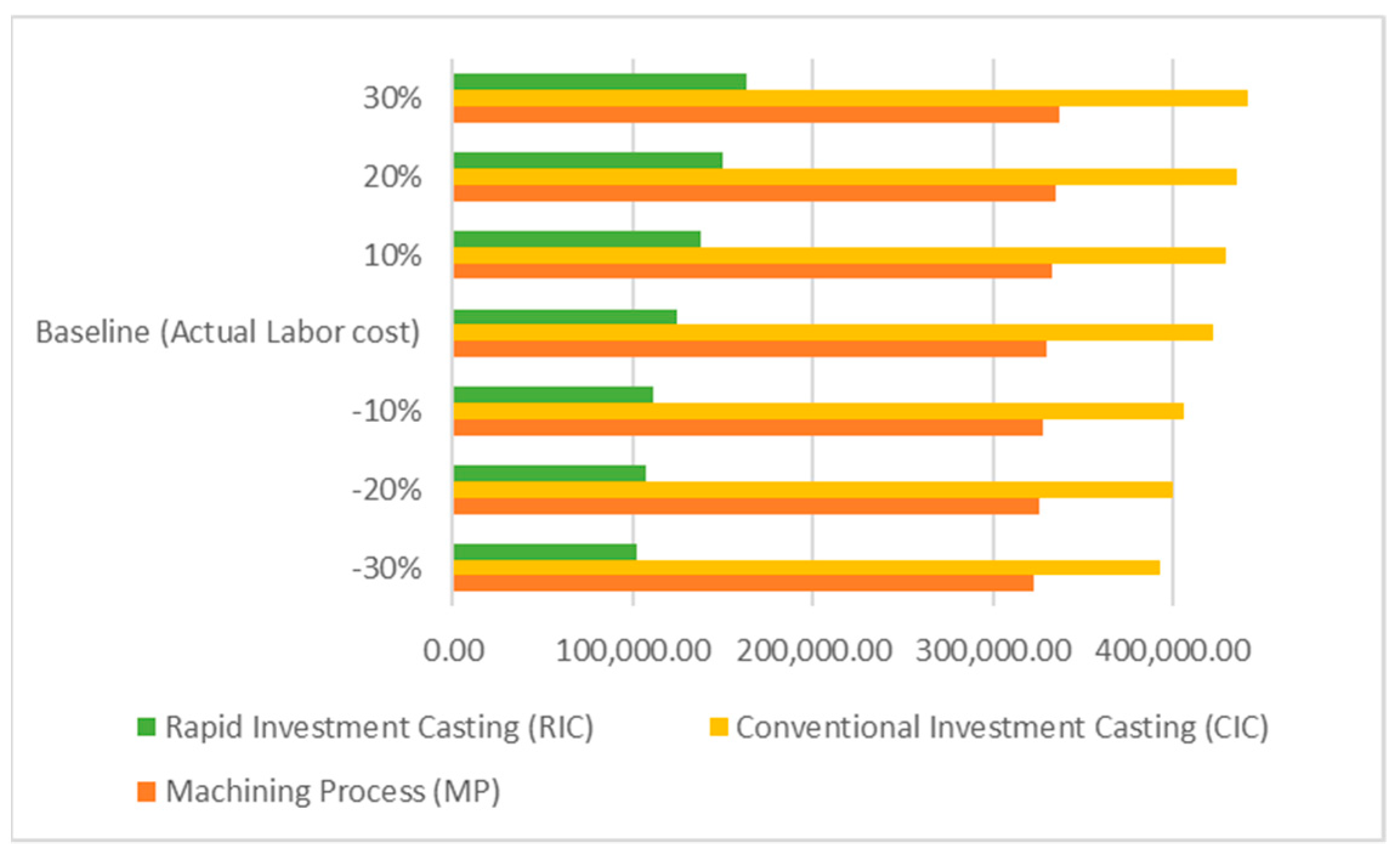

The labor cost sensitivity analysis was performed by altering the actual labor cost by ±30% in 10% increments. The impact of these changes is presented in

Figure 3.

It was observed that CIC incurred the highest labor cost in all scenarios, owing to its labor-intensive nature and longer process cycle. MP showed moderate sensitivity, while RP maintained the lowest labor cost throughout the analysis. The lower labor dependency in RP, due to automation and shorter process time, contributes to its economic advantage. The results indicate that RP is more resilient to fluctuations in labor cost and is therefore a cost-effective alternative, especially in regions with high labor expenses.

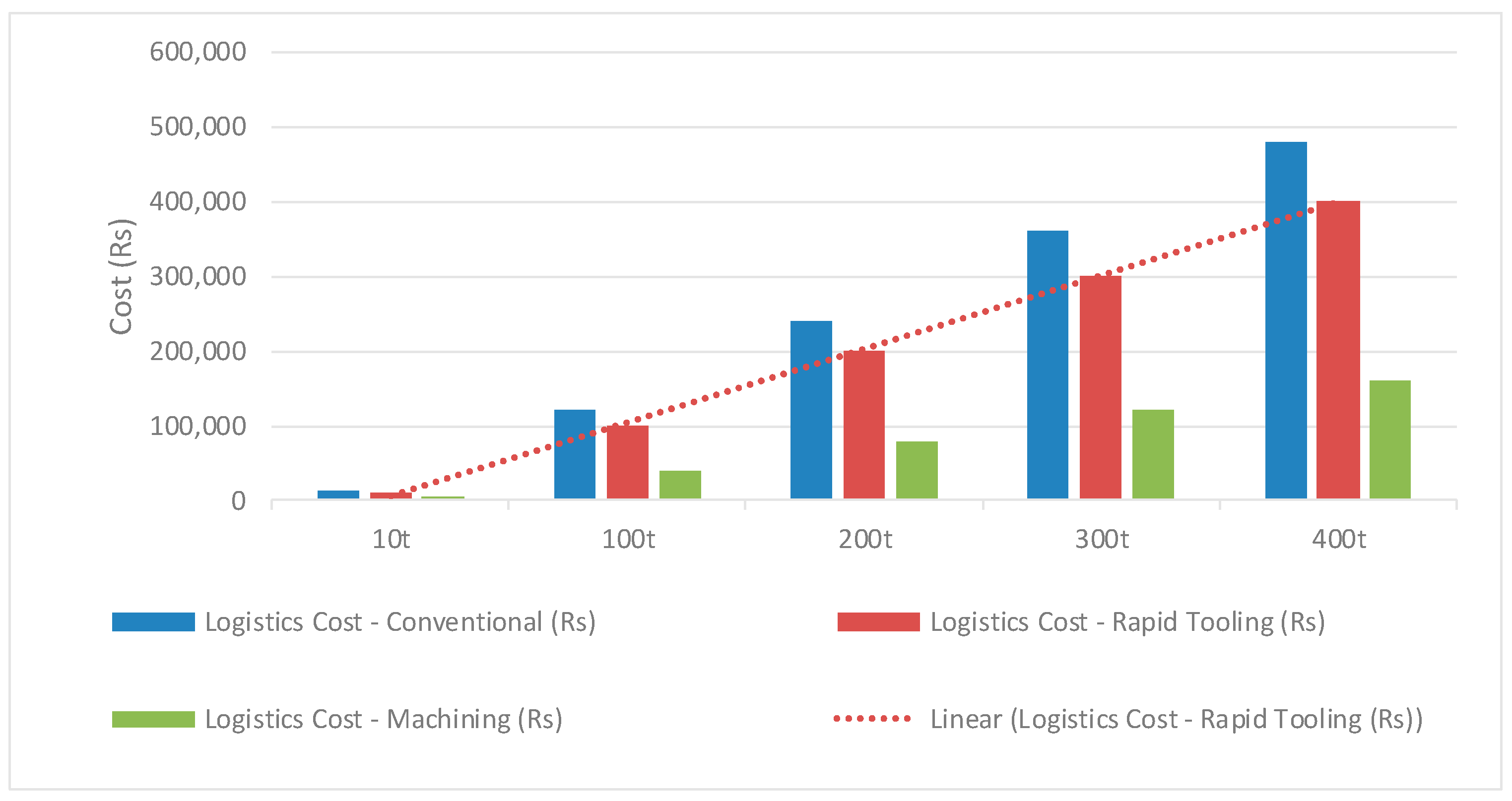

The final sensitivity analysis examined how material cost varies with the quantity of material processed, measured in tons (t). Material costs were analyzed for production quantities of 100 t, 200 t, 300 t, and 400 t, as shown in

Figure 4.

The analysis revealed that CIC incurred the highest material cost at all quantity levels, followed closely by the machining process. In contrast, rapid prototyping (RP) demonstrated the lowest material cost across the range. Furthermore, the trend in RP’s material cost increase was more gradual, as highlighted by the linear trendline included in the graph. This indicates better scalability and cost control in RP, especially in bulk production. The results confirm that RP is more material-efficient and less sensitive to increases in production quantity compared to conventional methods.

5. Conclusions

This study conducted a detailed comparative analysis of three manufacturing methods, namely the machining process (MP), conventional investment casting (CIC), and rapid prototyping (RP) based on their cost structure and sensitivity to environmental, labor, and material cost variations. The total cost analysis revealed that RP is significantly more economical, with a total cost of INR 124,685.50, compared to INR 330,252.70 for MP and INR 422,600.35 for CIC. This indicates that RP is approximately 62.23% more cost-effective than CIC and 62.23% more economical than MP. Furthermore, RP achieved a 77% reduction in labor cost compared to CIC and a 72% reduction compared to MP. Energy costs in RP were also reduced by over 95%, demonstrating its operational efficiency. The sensitivity analysis supported these findings, showing that RP remained the most stable and least impacted under variations in environmental cost, labor cost, and material cost across different production scales. Overall, RP stands out as the most cost-efficient and environmentally sustainable manufacturing approach, making it a highly suitable choice for modern, scalable, and resource-conscious production systems.

Author Contributions

Conceptualization, M.S.; methodology, S.B. under the guidance of M.S.; software, S.B.; validation, S.B. and M.S.; formal analysis, S.B.; investigation, S.B.; resources, M.S.; data curation, S.B.; writing—original draft preparation, S.B.; writing—review and editing, S.B. and M.S.; visualization, S.B.; supervision, M.S.; project administration, M.S.; funding acquisition, M.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Higher Education Commission (HEC) of Pakistan under the National Research Program for Universities (NRPU), grant number NRPU-17013.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author. The data are not publicly available due to institutional restrictions.

Conflicts of Interest

The authors declare no conflict of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| MP | Machining Process |

| CIC | Conventional Investment Casting |

| RP | Rapid Prototyping |

| CNC | Computer Numerical Control |

| EDM | Electric Discharge Machine |

| SLA | Stereo lithography |

| SLS | Selective Laser Sintering |

| FDM | Fused Deposition Modeling |

References

- Urbanic, R.J.; Saqib, S.M. A manufacturing cost analysis framework to evaluate machining and fused filament fabrication additive manufacturing approaches. Int. J. Adv. Manuf. Technol. 2019, 102, 3091–3108. [Google Scholar] [CrossRef]

- Zhou, Y.; Xing, T.; Song, Y.; Li, Y.; Zhu, X.; Li, G.; Ding, S. Digital-twin-driven geometric optimization of centrifugal impeller with free-form blades for five-axis flank milling. J. Manuf. Syst. 2021, 58, 22–35. [Google Scholar] [CrossRef]

- Silva, F.J.; Sousa, V.F.; Pinto, A.G.; Ferreira, L.P.; Pereira, T. Build-Up an Economical Tool for Machining Operations Cost Estimation. Metals 2022, 12, 1205. [Google Scholar] [CrossRef]

- Lu, J.; Chen, Z.; Liao, X.; Chen, C.; Ouyang, H.; Li, S. Multi-objective optimization for improving machining benefit based on WOA-BBPN and a Deep Double Q-Network. Appl. Soft Comput. 2023, 142, 110330. [Google Scholar] [CrossRef]

- Cai, W.; Liu, C.; Jia, S.; Chan, F.T.; Ma, M.; Ma, X. An emergy-based sustainability evaluation method for outsourcing machining resources. J. Clean. Prod. 2020, 245, 118849. [Google Scholar] [CrossRef]

- Pan, J.; Li, C.; Tang, Y.; Li, W.; Li, X. Energy Consumption Prediction of a CNC Machining Process with Incomplete Data. IEEE/CAA J. Autom. Sin. 2021, 8, 987–1000. [Google Scholar] [CrossRef]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}