A Review on Battery Market Trends, Second-Life Reuse, and Recycling

,

,

,

,  and

and

Abstract

1. Introduction

2. Battery Type by Chemistry

2.1. Lead Acid Batteries

2.2. Nickel-Based Batteries

2.3. Lithium-Based Batteries

3. Battery Market Overview

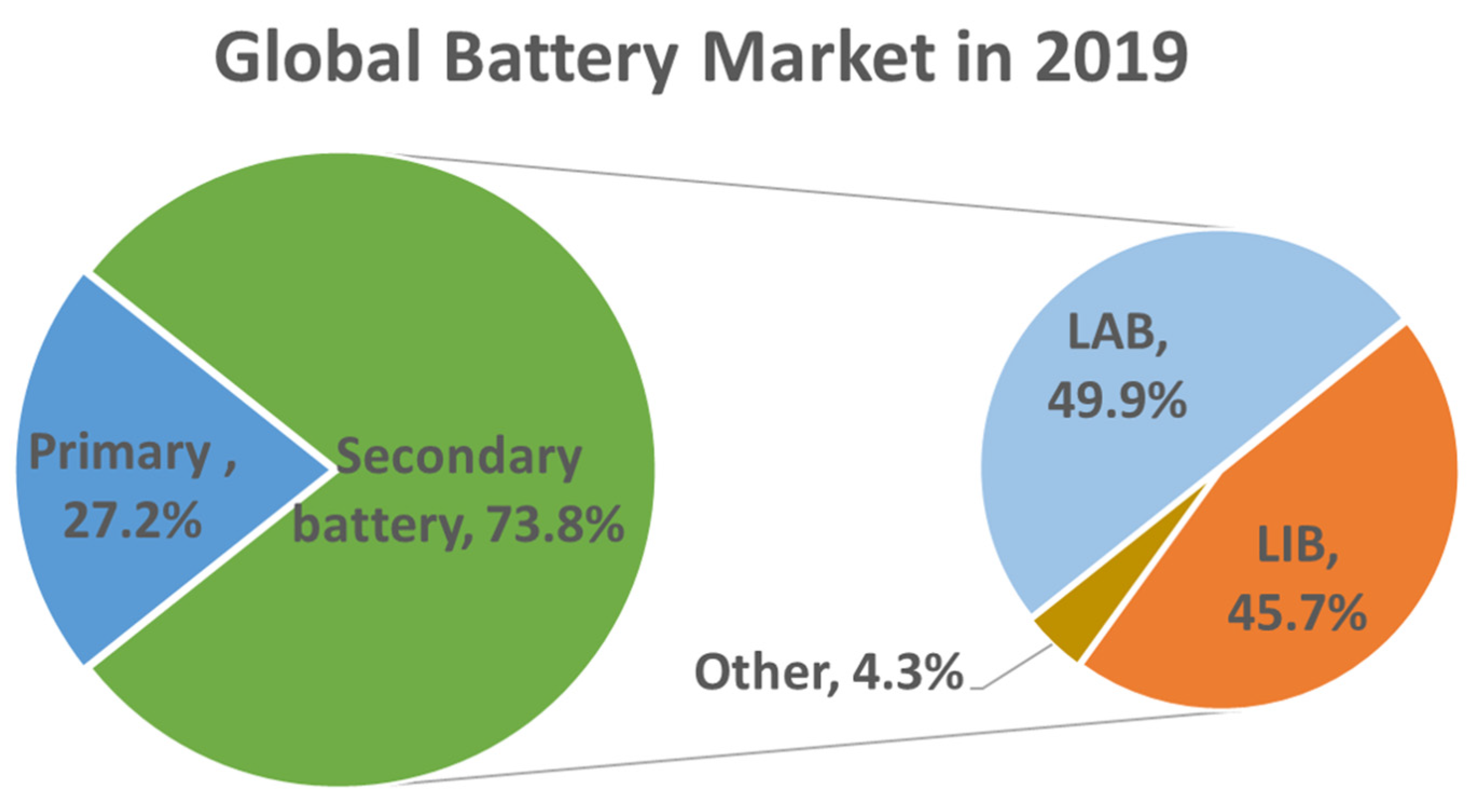

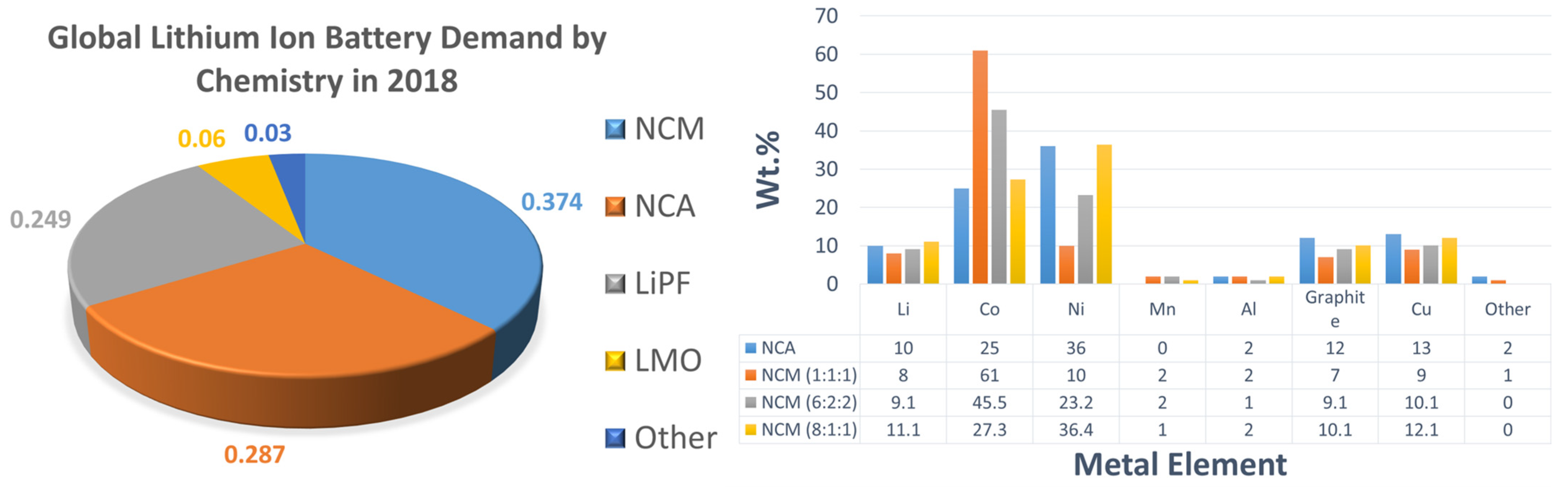

3.1. Market Share by Chemistry

3.2. The Global Battery Market Size

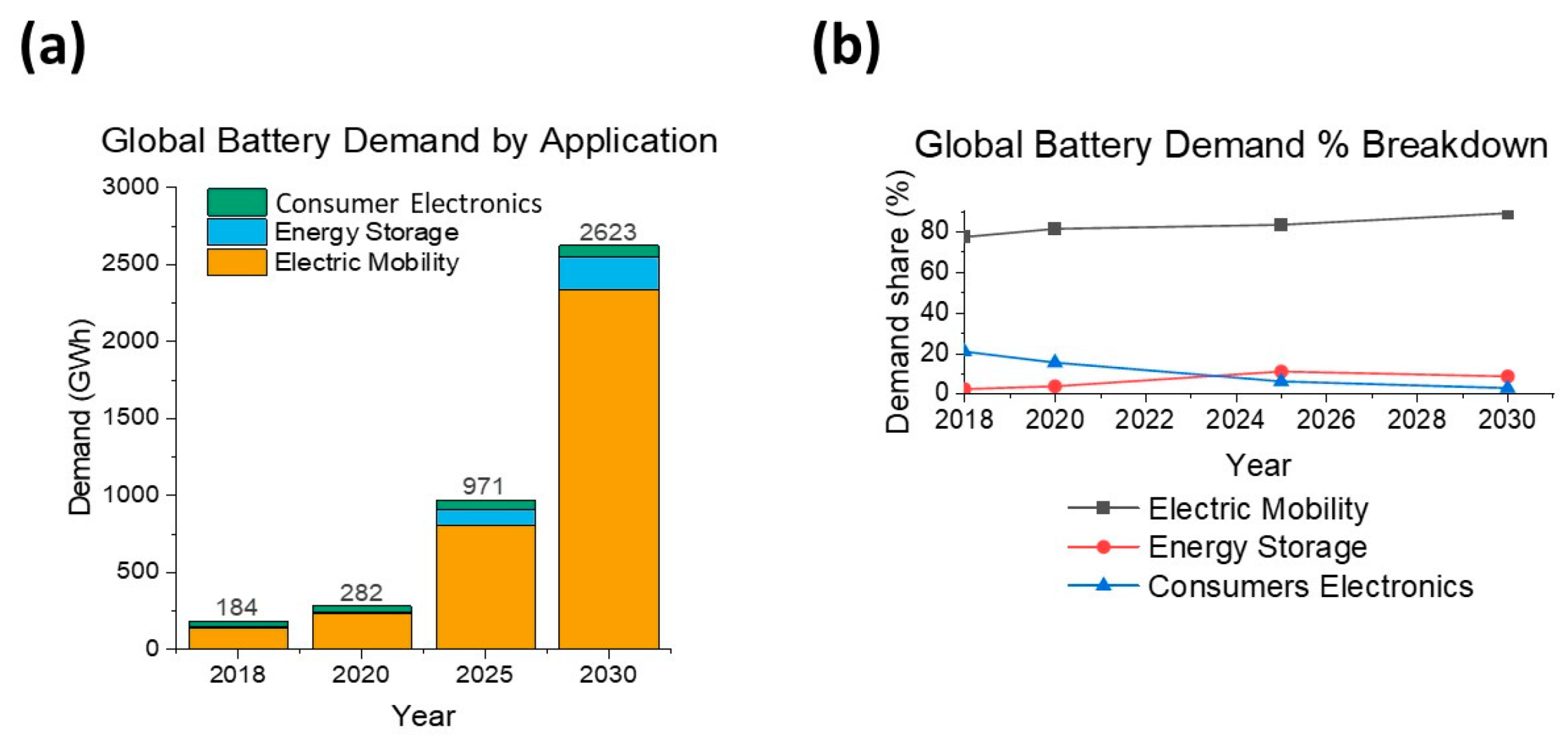

3.2.1. Global Battery Industry Growth by Application

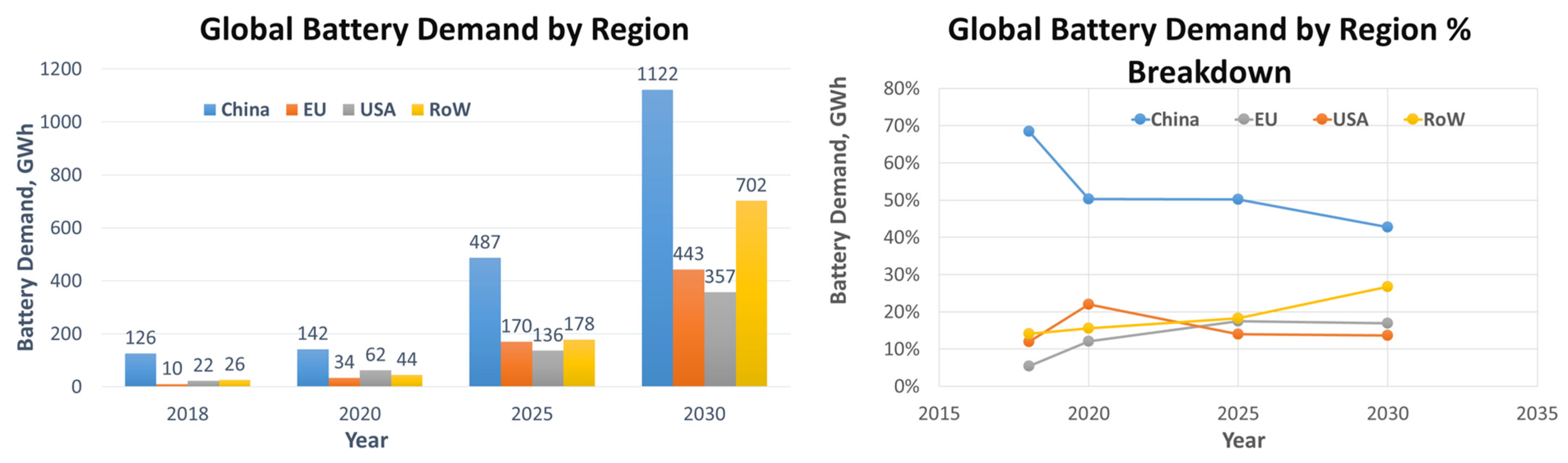

3.2.2. Global Battery Industry Growth by Region

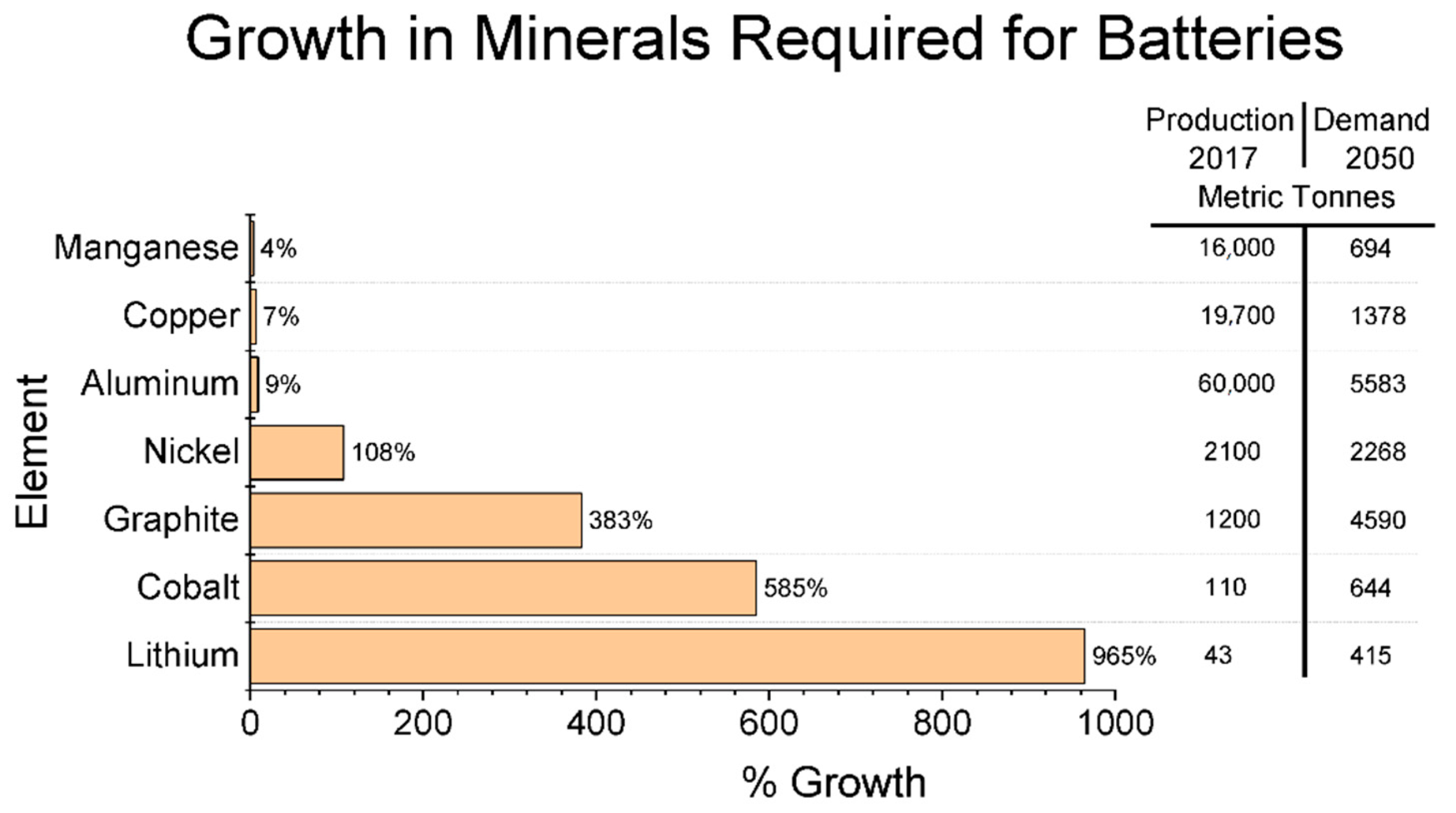

4. Impacts of Increased Battery Usage

4.1. Impact on Environment

4.1.1. Lead Acid Batteries

4.1.2. Lithium-Based Batteries

4.1.3. Nickel-Based Batteries

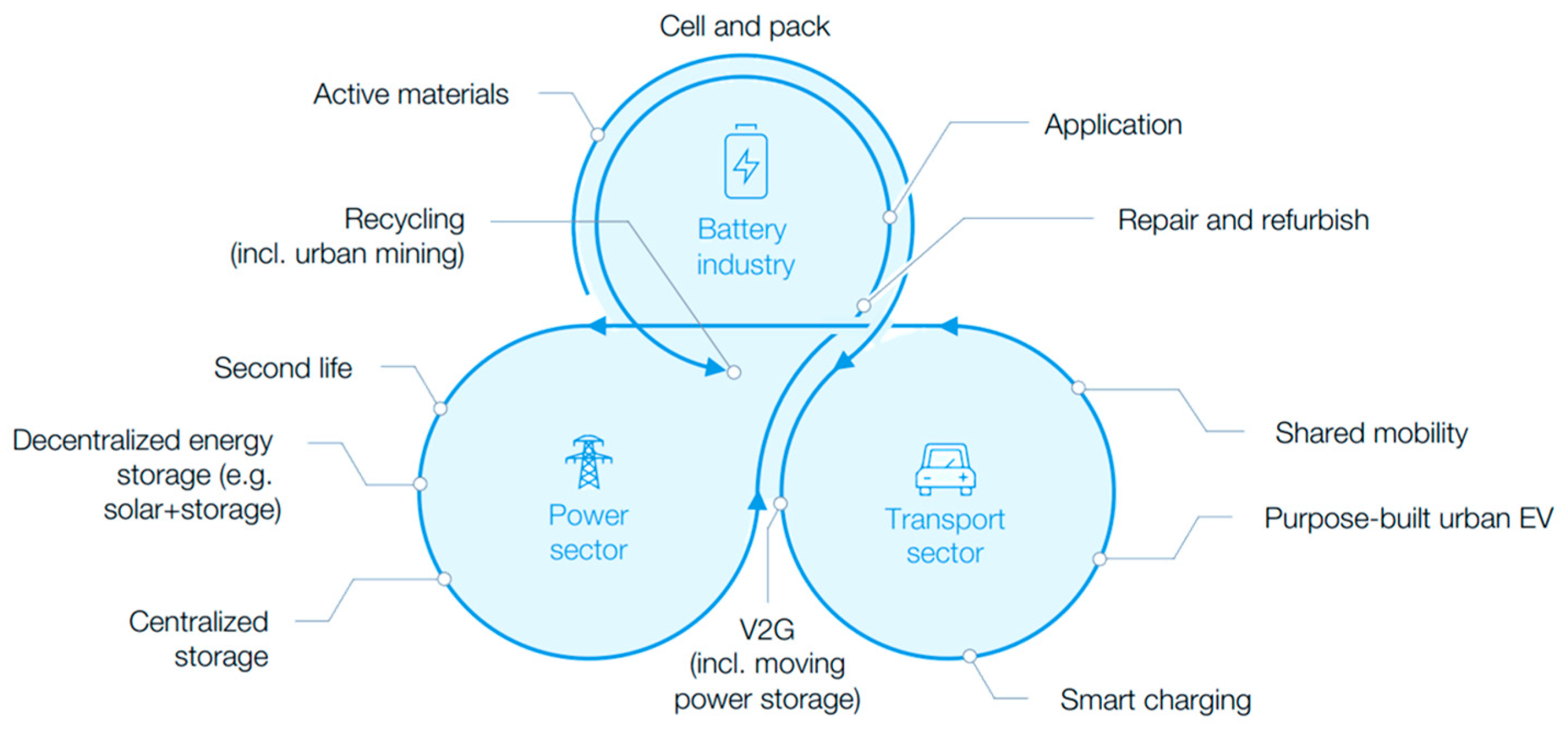

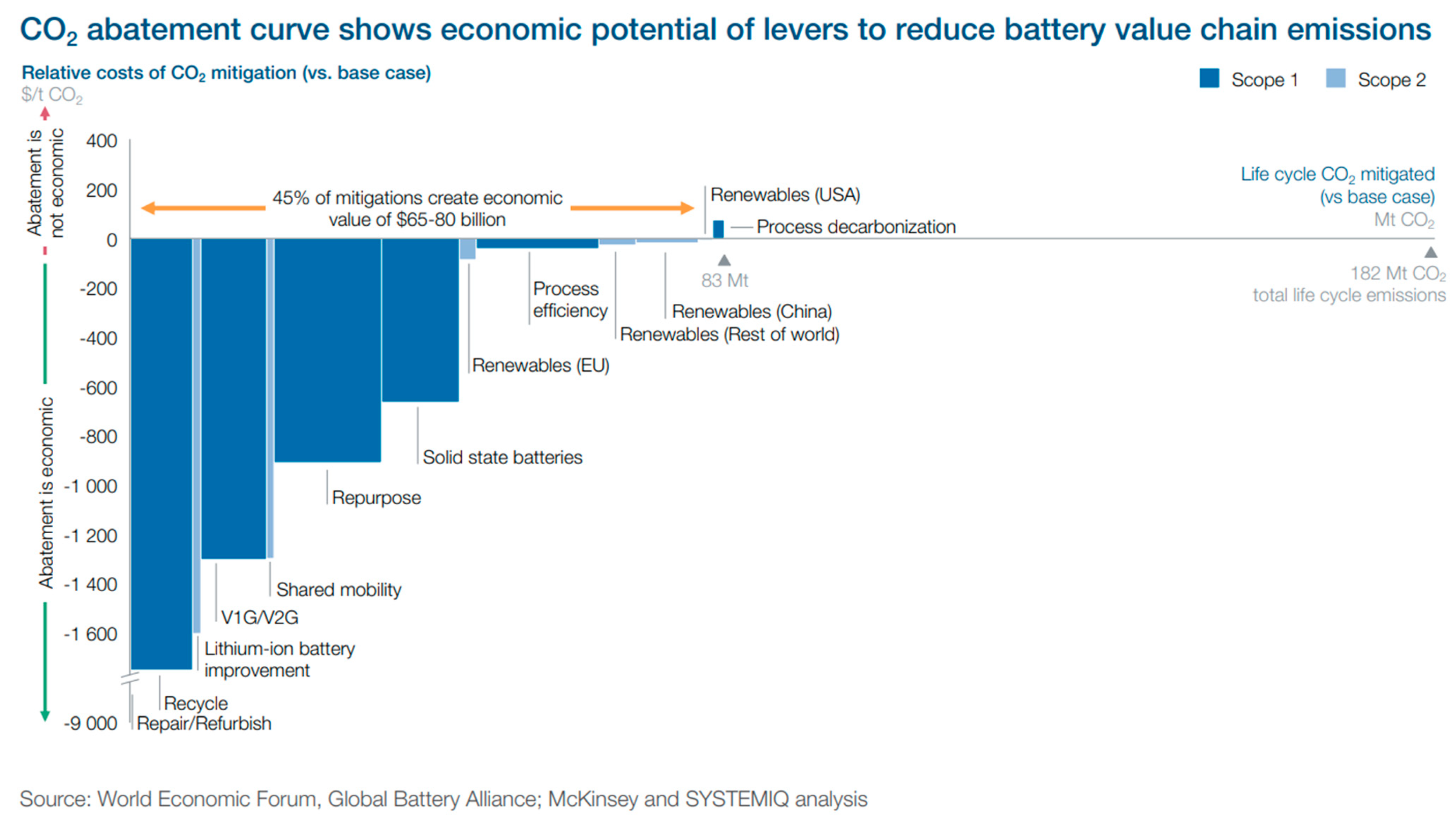

5. A Circular Economy Proposed for Battery Value Chain

6. Status of Battery Recycling

6.1. Battery Waste Recycling

6.2. Lead-Acid Battery Recycling

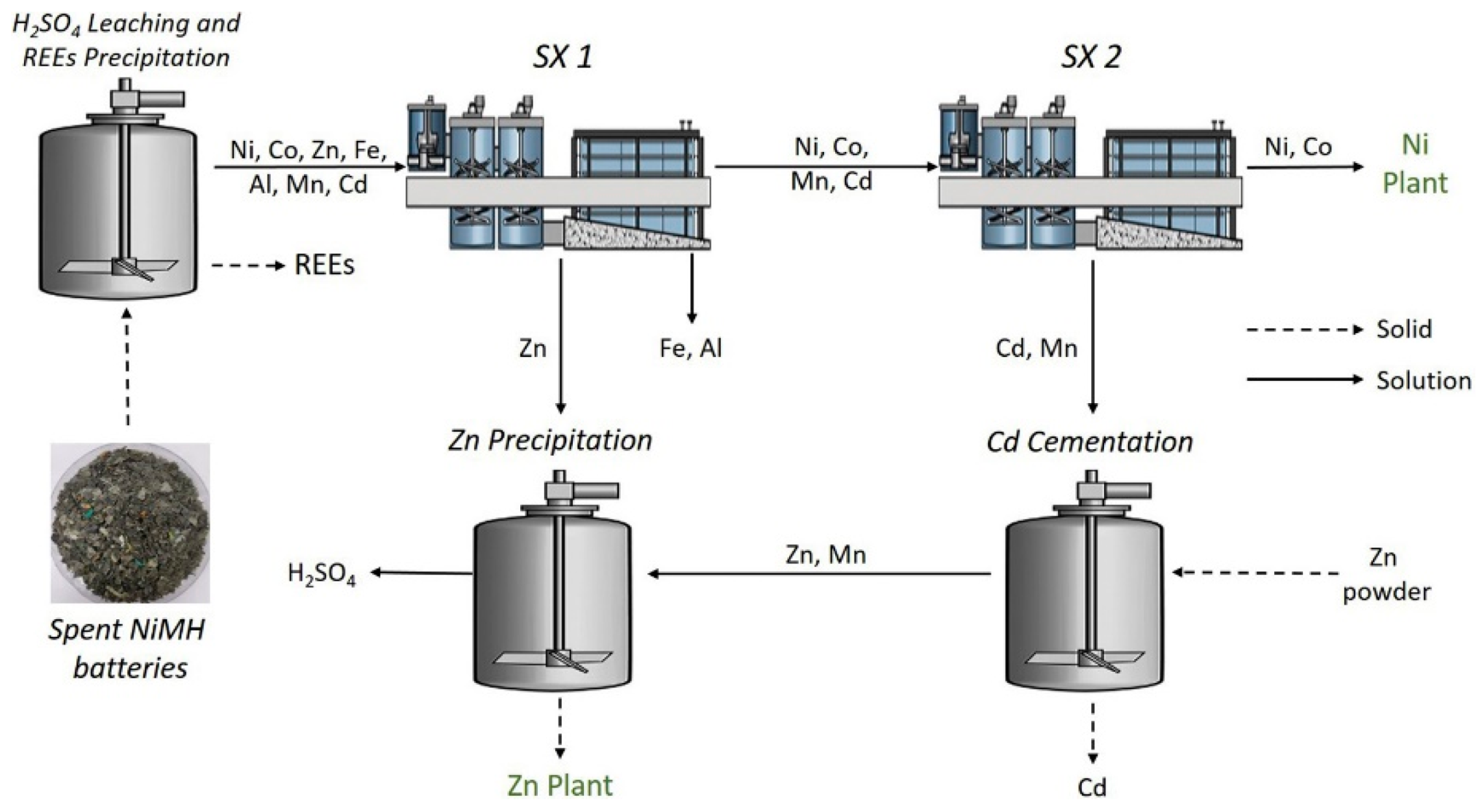

6.3. Nickel Metal Hydride Battery Recycling

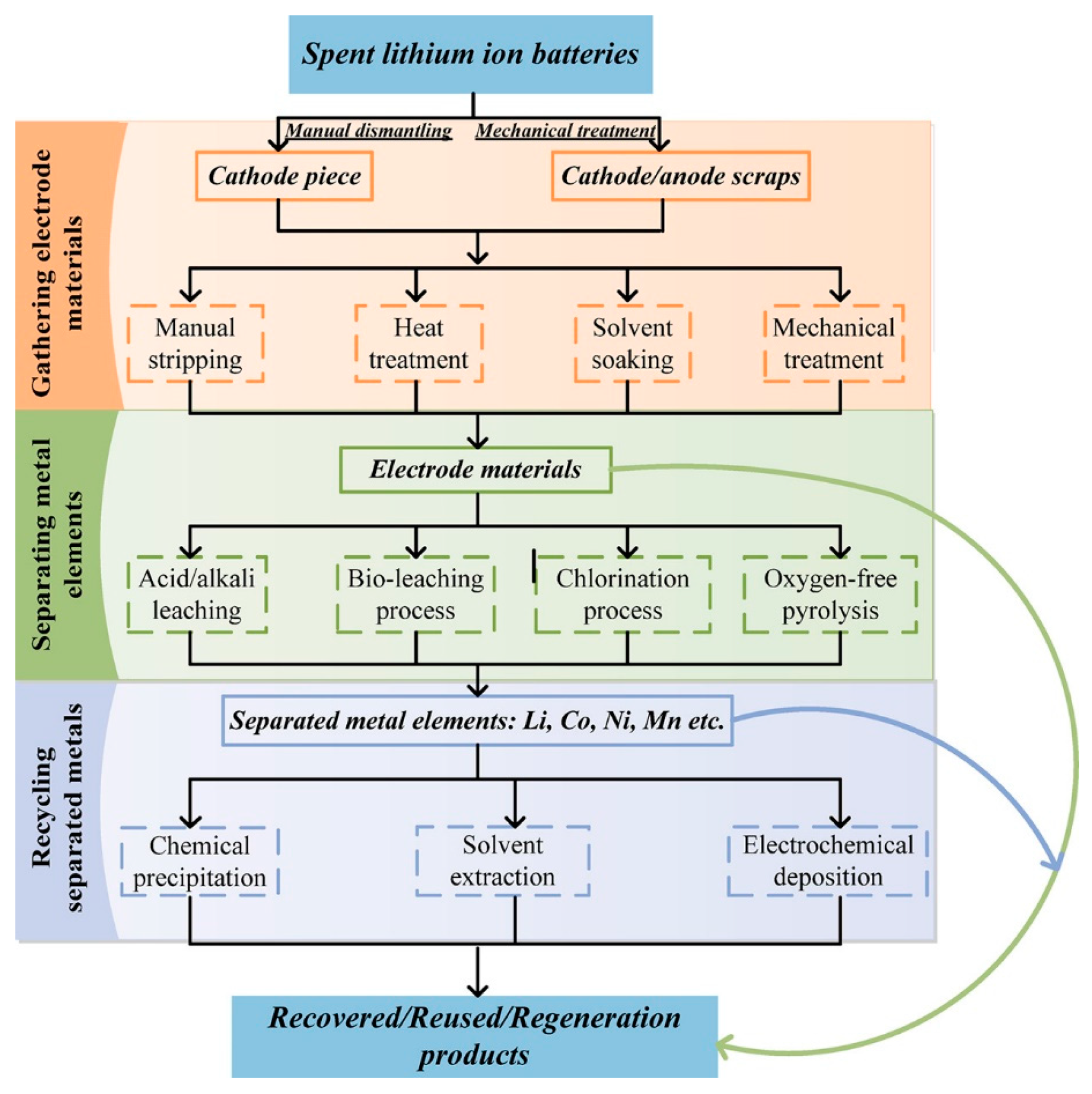

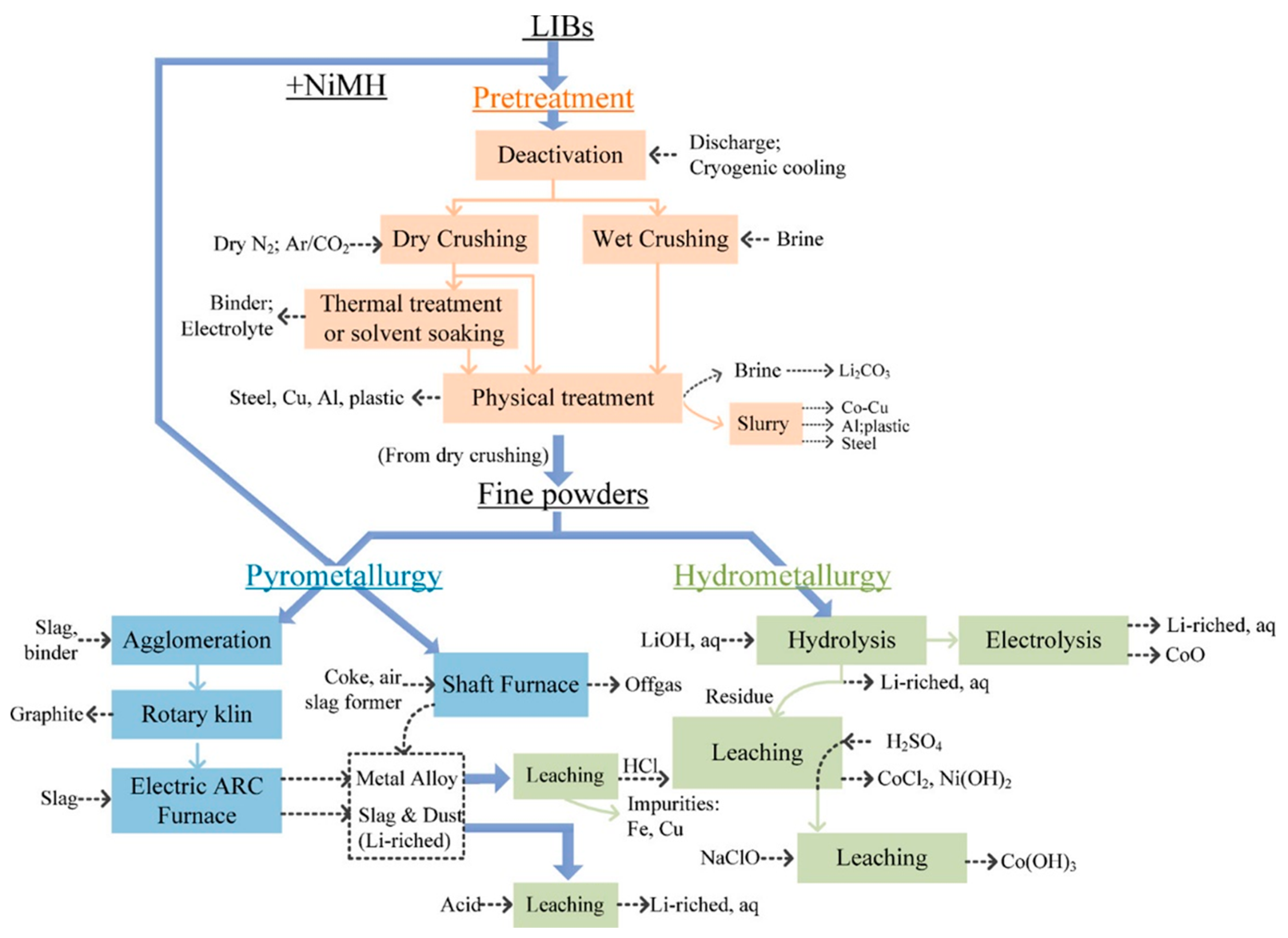

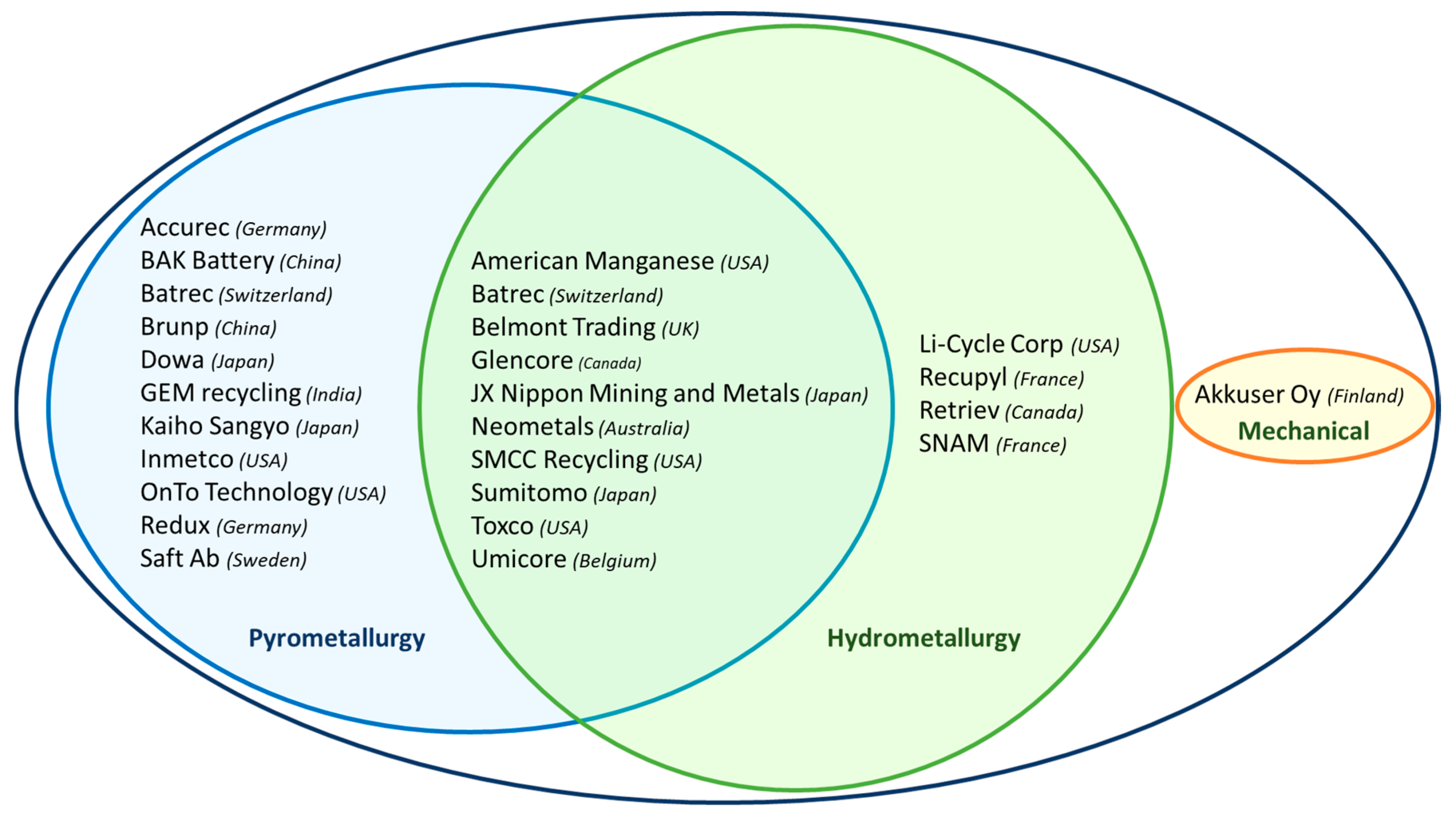

6.4. Lithium Ion Battery Recycling

6.4.1. Why LIB Recycling?

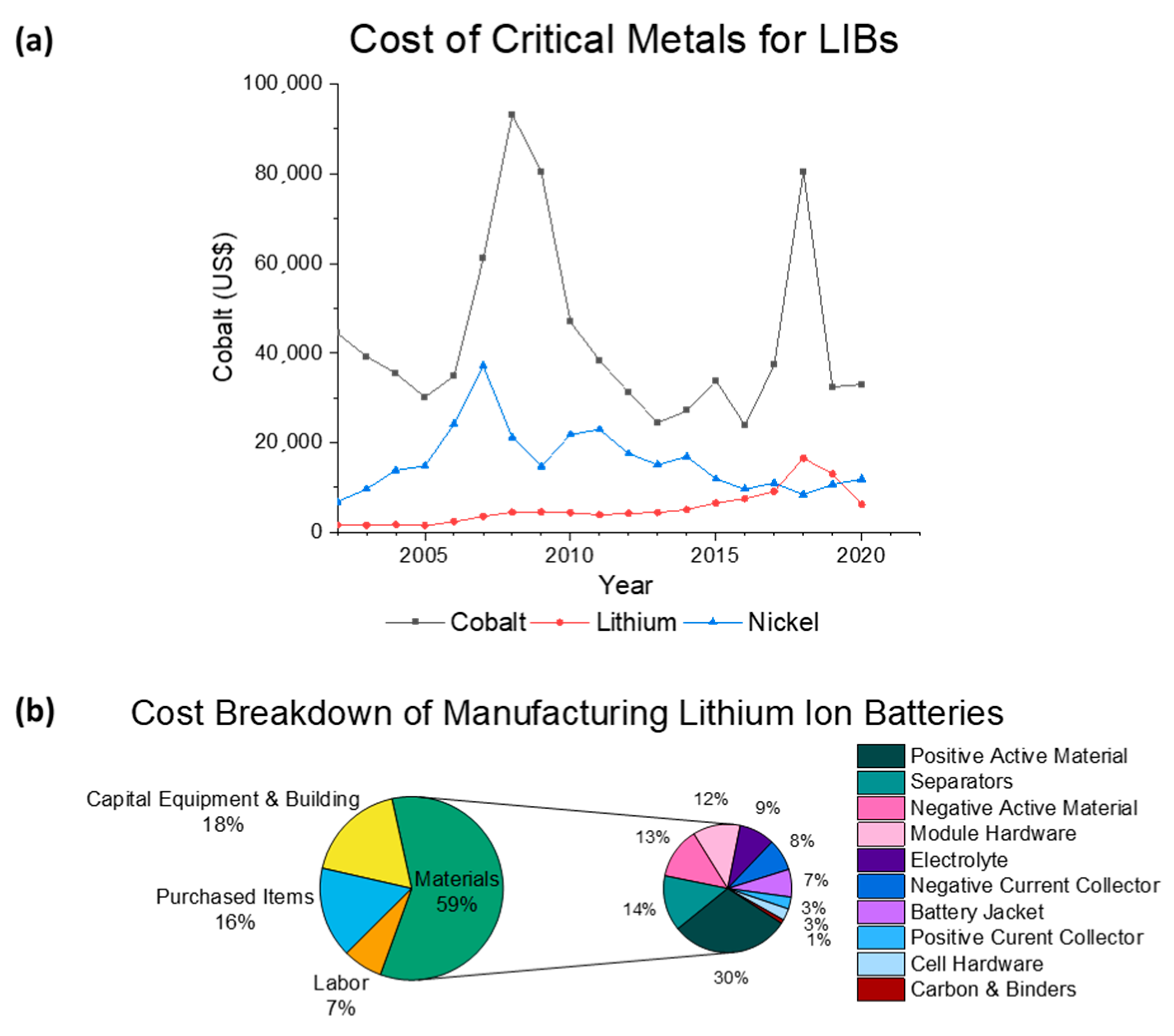

6.4.2. Economic Challenges of LIB Recycling

6.4.3. Battery Recycling Policy Status

- Europe

- The United States of America

- Asia Pacific region

6.4.4. Recycling Process Challenges

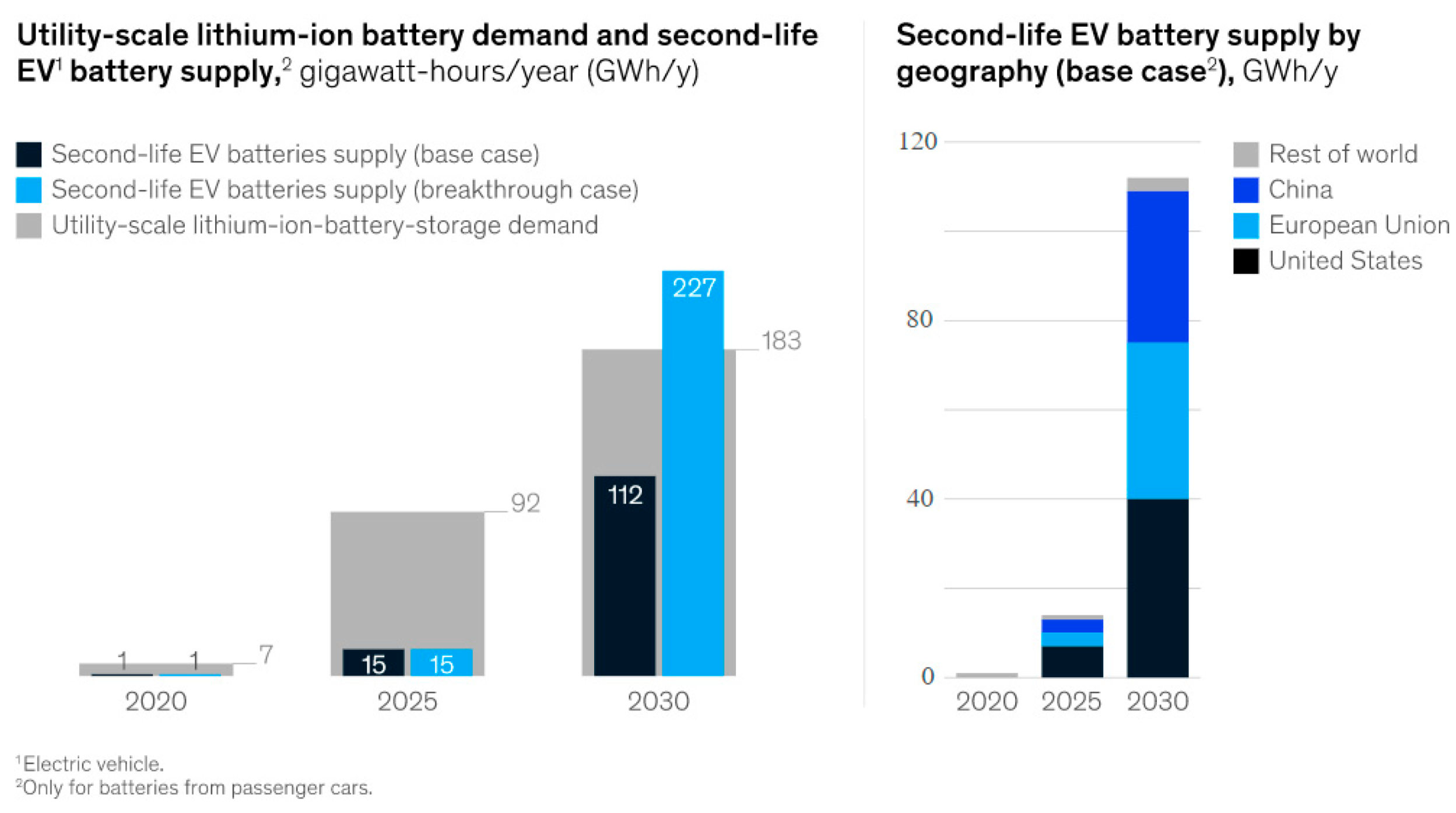

7. Status of Battery Reuse

- Government regulations supporting the reuse of EV batteries in China;

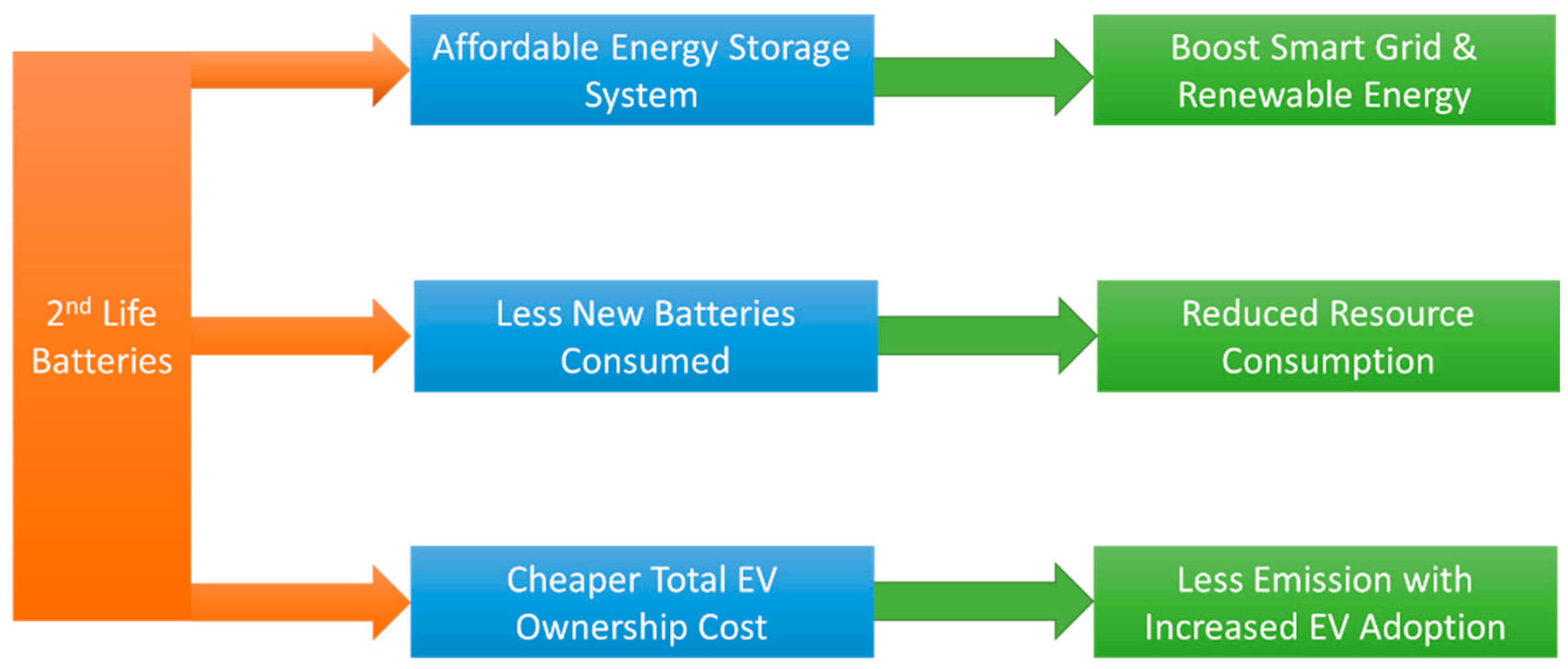

- The 80% residual energy left in the EoL EV batteries according to the EV battery design can be used for less energy demand applications, and

- The growing demand for electrical energy storage could be offset by using second-life batteries rather than newly manufactured products.

7.1. The Criteria for EoL EV Batteries’ First Life

7.2. Source of Second-Life Batteries (SLBs)

7.3. Impact of Ownership on Retired Batteries

- The EV manufacturer (OEM) is the battery owner and the EV owner leases the battery from the EV manufacturer,

- Third-party owns the battery and the EV owner leases the battery from the third party, and

- The EV owner is the battery owner.

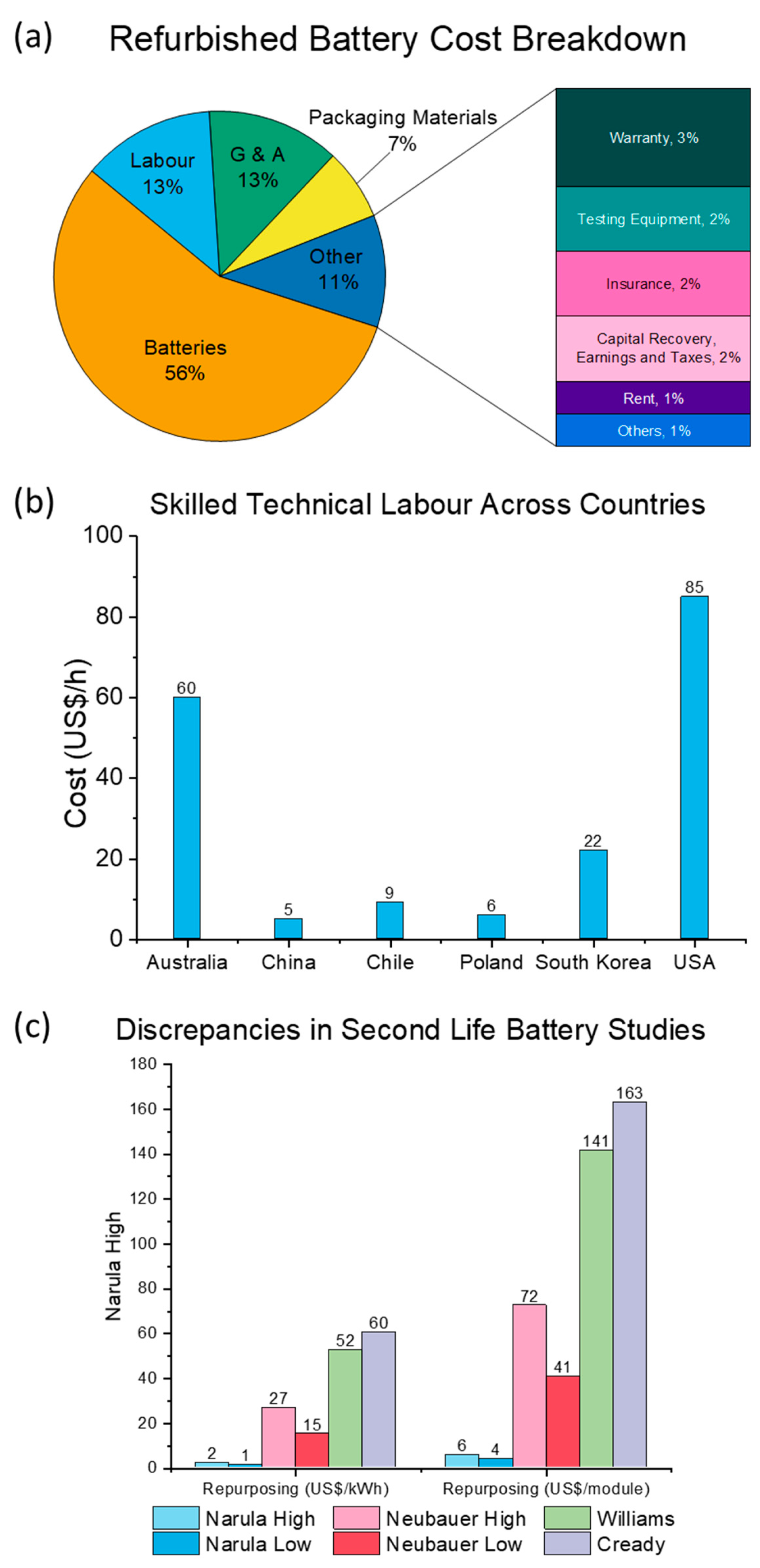

7.4. The Price Challenge of Second-Life Batteries

7.5. Technical Challenges of Using Second-Life Batteries

7.6. Second-Life Battery Applications and Their Economic Analysis

7.7. Activities of EV Battery Reuse

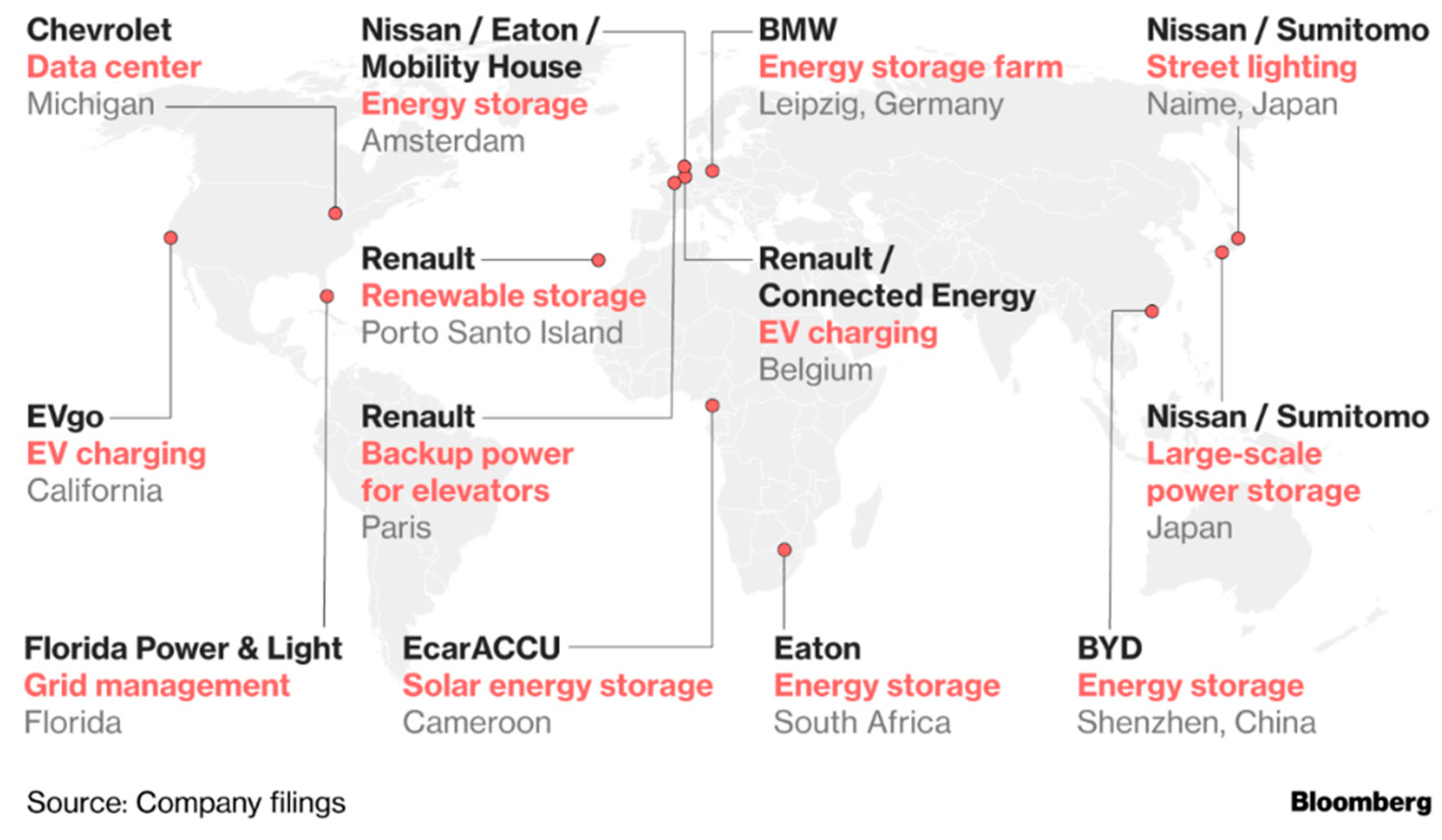

7.8. Recent Industrial Activities of Reusing Second-Life Batteries

8. Conclusions and Outlook

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Grand View Research. Battery Market Share, Size & Trend Analysis Report By Product (Lead Acid, Li-ion, Nickle Metal Hydride, Ni-Cd) By Application (Automotive, Industrial, Portable), By Region, and Segment Forecasts 2020–2027. Available online: https://www.grandviewresearch.com/industry-analysis/battery-market/segmentation (accessed on 30 April 2020).

- International Energy Agency. Global EV Outlook 2019; International Energy Agency: Paris, France, 2019; p. 231. [Google Scholar]

- Yun, Q.B.; He, Y.B.; Lv, W.; Zhao, Y.; Li, B.H.; Kang, F.Y.; Yang, Q.H. Chemical Dealloying Derived 3D Porous Current Collector for Li Metal Anodes. Adv. Mater. 2016, 28, 6932–6939. [Google Scholar] [CrossRef] [PubMed]

- Global Energy & Environment Research Team. Global Industrial Battery Market, Forecast to 2023: Growth in Renewable Energy and Distributed Generation to Drive the Global Industrial Battery Market; Frost & Sullivan: San Antonio, TX, USA, 2018; p. 196. [Google Scholar]

- The 2019 Lithium-ion Battery Market: Worldwide Industry Trends, Share, Size, Growth, Opportunity & Forecast to 2024. Available online: https://www.businesswire.com/news/home/20190703005177/en/2019-Lithium-ion-Battery-Market-Worldwide-Industry-Trends (accessed on 20 April 2020).

- Ballantyne, A.D.; Hallett, J.P.; Riley, D.J.; Shah, N.; Payne, D.J. Lead acid battery recycling for the twenty-first century. R. Soc. Open Sci. 2018, 5, 171368. [Google Scholar] [CrossRef]

- World Economic Forum and The Global Battery Alliance. A Vision for a Sustainable Battery Value Chain in 2030: Unlocking the Full Potential to Power Sustainable Development and Climate Change Mitigation; WeForum: Cologny, Switzerland, 2019; p. 52. [Google Scholar]

- Occupational Knowledge International. Health & Environmental Impacts from Lead Battery Manufacturing & Recycling in China; Occupational Knowledge International: San Francisco, CA, USA, 2012. [Google Scholar]

- O’Farrell, K.; Kinrade, P.; Jones, P.; Roser, L. Australian Battery Market Analysis. 2020, p. 149. Available online: https://www.sunwiz.com.au/battery-market-report-australia-2020/ (accessed on 11 December 2020).

- Zeng, X.; Li, J.; Ren, Y. Prediction of various discarded lithium batteries in China. In Proceedings of the 2012 IEEE International Symposium on Sustainable Systems and Technology (ISSST), Boston, MA, USA, 16–18 May 2012; pp. 1–4. [Google Scholar]

- Saxena, S.; Le Floch, C.; MacDonald, J.; Moura, S. Quantifying EV battery end-of-life through analysis of travel needs with vehicle powertrain models. J. Power Sources 2015, 282, 265–276. [Google Scholar] [CrossRef]

- Casals, L.C.; Amante García, B.; Canal, C. Second life batteries lifespan: Rest of useful life and environmental analysis. J. Environ. Manag. 2019, 232, 354–363. [Google Scholar] [CrossRef]

- Second-life Electric Vehicle Batteries 2020–2030 Key Players, Value Opportunities, Business Models and Market Forecast. Available online: https://www.idtechex.com/en/research-report/second-life-electric-vehicle-batteries-2020-2030/681 (accessed on 30 April 2020).

- Zheng, R.; Zhao, L.; Wang, W.; Liu, Y.; Ma, Q.; Mu, D.; Li, R.; Dai, C. Optimized Li and Fe recovery from spent lithium-ion batteries via a solution-precipitation method. Rsc Adv. 2016, 6, 43613–43625. [Google Scholar] [CrossRef]

- Richa, K. Sustainable management of lithium-ion batteries after use in electric vehicles. Ph.D. Thesis, Rochester Institute of Technology, Rochester, NY, USA, 2016. [Google Scholar]

- A Second Life for Used Batteries. Available online: https://www.bosch-presse.de/pressportal/de/en/a-second-life-for-used-batteries-64192.html (accessed on 30 April 2020).

- Reid, G.; Julve, J. Second Life-Batteries as Flexible Storage For Renewables Energies; Bundesverband Erneuerbare Energie: New Delhi, India, 2016. [Google Scholar]

- Audi Testing Second-Life EV Batteries in Factory Vehicles. Available online: https://www.greencarcongress.com/2019/03/20190307-audi2ndlife.html (accessed on 27 April 2020).

- Jiao, N. China Tower Can ‘Absorb’ 2 Million Retired Electric Vehicle Batteries. Available online: https://www.idtechex.com/de/research-article/china-tower-can-absorb-2-million-retired-electric-vehicle-batteries/15460 (accessed on 30 April 2020).

- Hutt, R. This Dutch Football Stadium Creates Its Own Energy and Stores It in Electric Car Batteries. Available online: https://www.weforum.org/agenda/2018/07/netherlands-football-johan-cruijff-stadium-electric-car-batteries/ (accessed on 30 April 2020).

- Lovell, J. Storage: Retirement Home for old EV Batteries? Available online: https://www.energycouncil.com.au/analysis/storage-retirement-home-for-old-ev-batteries/ (accessed on 1 May 2020).

- Engel, H.; Hertzke, P.; Siccardo, G. Second-life EV Batteries: The Bewest Value Pool in Energy Storage. Available online: https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/second-life-ev-batteries-the-newest-value-pool-in-energy-storage (accessed on 4 February 2021).

- Tobias Elwert, F.R.; Schneider, K.; Hua, Q.; Buchert, M. Behaviour of Lithium-Ion Batteries in Electric Vehicles; Springer: Berlin/Heidelberg, Germany, 2018; p. 316. [Google Scholar]

- The Goldman Sachs Group. China’s Battery Challenge: A New Solution to A Growth Problem; The Goldman Sachs Group: New York, NY, USA, 2017. [Google Scholar]

- Gaines, L. The future of automotive lithium-ion battery recycling: Charting a sustainable course. Sustain. Mater. Technol. 2014, 1–2, 2–7. [Google Scholar] [CrossRef]

- Gaines, L. Profitable Recycling of Low-Cobalt Lithium-Ion Batteries Will Depend on New Process Developments. One Earth 2019, 1, 413–415. [Google Scholar] [CrossRef]

- Jacoby, M. It’s Time to Get Serious about Recycling Lithium-Ion Batteries. Available online: https://cen.acs.org/materials/energy-storage/time-serious-recycling-lithium/97/i28 (accessed on 8 May 2020).

- King, S.; Boxall, N.J. Lithium battery recycling in Australia: defining the status and identifying opportunities for the development of a new industry. J. Clean. Prod. 2019, 215, 1279–1287. [Google Scholar] [CrossRef]

- Deign, J. How China Is Cornering the Lithium-Ion Cell Recycling Market. Available online: https://www.greentechmedia.com/articles/read/how-china-is-cornering-the-lithium-ion-cell-recycling-market (accessed on 6 May 2020).

- Maisch, M. Lithium-ion Recycling Rates Far Higher Than Some Statistics Suggest. Available online: https://www.pv-magazine.com/2019/07/12/lithium-ion-recycling-rates-far-higher-than-some-statistics-suggest/ (accessed on 15 May 2020).

- Rapier, R. The Lead-Acid Battery’s Demise Has Been Greatly Exaggerated. Available online: https://www.forbes.com/sites/rrapier/2019/10/27/the-lead-acid-batterys-demise-has-been-greatly-exaggerated/#565e8fc84016 (accessed on 24 April 2020).

- Wang, X.; Gaustad, G.; Babbitt, C.W.; Richa, K. Economies of scale for future lithium-ion battery recycling infrastructure. Resour. Conserv. Recycl. 2014, 83, 53–62. [Google Scholar] [CrossRef]

- Zeng, X.; Li, J.; Singh, N. Recycling of Spent Lithium-Ion Battery: A Critical Review. Crit. Rev. Environ. Sci. Technol. 2014, 44, 1129–1165. [Google Scholar] [CrossRef]

- Pagliaro, M.; Meneguzzo, F. Lithium battery reusing and recycling: A circular economy insight. Heliyon 2019, 5, e01866. [Google Scholar] [CrossRef] [PubMed]

- BU-705a: Battery Recycling as a Business. Available online: https://batteryuniversity.com/learn/article/battery_recycling_as_a_business (accessed on 5 May 2020).

- Aral, H.; Vecchio-Sadus, A. Toxicity of lithium to humans and the environment—A literature review. Ecotoxicol. Environ. Saf. 2008, 70, 349–356. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Ali, S.H.; Bazilian, M.; Radley, B.; Nemery, B.; Okatz, J.; Mulvaney, D. Sustainable minerals and metals for a low-carbon future. Science 2020, 367, 30. [Google Scholar] [CrossRef] [PubMed]

- Reinhardt, R.; Christodoulou, I.; Gasso-Domingo, S.; Garcia, B.A. Towards sustainable business models for electric vehicle battery second use: A critical review. J. Environ. Manag. 2019, 245, 432–446. [Google Scholar] [CrossRef] [PubMed]

- Zhang, W.X.; Xu, C.J.; He, W.Z.; Li, G.M.; Huang, J.W. A review on management of spent lithium ion batteries and strategy for resource recycling of all components from them. Waste Manag. Res. 2018, 36, 99–112. [Google Scholar] [CrossRef]

- Davidson, A.J.; Binks, S.P.; Gediga, J. Lead industry life cycle studies: environmental impact and life cycle assessment of lead battery and architectural sheet production. Int. J. Life Cycle Assess. 2016, 21, 1624–1636. [Google Scholar] [CrossRef]

- Larsson, F.; Bertilsson, S.; Furlani, M.; Albinsson, I.; Mellander, B.-E. Gas explosions and thermal runaways during external heating abuse of commercial lithium-ion graphite-LiCoO2 cells at different levels of ageing. J. Power Sources 2018, 373, 220–231. [Google Scholar] [CrossRef]

- Bok, J.-S.; Lee, J.-H.; Lee, B.-K.; Kim, D.-P.; Rho, J.-S.; Yang, H.-S.; Han, K.-S. Effects of synthetic conditions on electrochemical activity of LiCoO2 prepared from recycled cobalt compounds. Solid State Ion. 2004, 169, 139–144. [Google Scholar] [CrossRef]

- How do Lithium Batteries Work? Available online: https://batteryuniversity.com/learn/article/lithium_based_batteries (accessed on 23 April 2020).

- Linden, D.; Reddy, T.B. (Eds.) Handbook of Batteries, 3rd ed.; McGraw-Hill: New York, NY, USA, 2002. [Google Scholar]

- Bruno Scrosati, K.M.A.; van Schalkwijk, W.A. Lithium Batteries: Advanced Technologies and Applications; Hassoun, J., Ed.; John Wiley & Sons: Hoboken, NJ, USA, 2013; p. 44. [Google Scholar]

- Australian Trade and Investment Comission. The Lithium-Ion Battery Value Chain-New Economy Opportunities for Australia; Australian Trade and Investment Comission: Sydney, Austraila, 2018; p. 53. [Google Scholar]

- TechNavio. Global Secondary Battery Market 2020–2024; Technavio: London, UK, 2020. [Google Scholar]

- Chatterjee, P. Second Life Energy Storage Applications in Developing Countries. Available online: https://energyfutureslab.blog/2019/01/10/second-life-energy-storage-applications-in-developing-countries/ (accessed on 27 April 2020).

- Reddy, T.B.; Linden, D. Linden’s Handbook of Batteries, 4th ed.; Books24x: New York, NY, USA, 2011. [Google Scholar]

- Chakraborty, S. Recycling of Lead-Acid Batteries in Developing Countries. Available online: https://www.bioenergyconsult.com/lead-acid-batteries/ (accessed on 24 April 2020).

- Zeeshan, M.; Murugadas, A.; Ghaskadbi, S.; Ramaswamy, B.R.; Akbarsha, M.A. Ecotoxicological assessment of cobalt using Hydra model: ROS, oxidative stress, DNA damage, cell cycle arrest, and apoptosis as mechanisms of toxicity. Environ. Pollut. 2017, 224, 54–69. [Google Scholar] [CrossRef]

- Barghamadi, M.; Best, A.S.; Bhatt, A.I.; Hollenkamp, A.F.; Musameh, M.; Rees, R.J.; Rüther, T. Lithium–sulfur batteries—the solution is in the electrolyte, but is the electrolyte a solution? Energy Environ. Sci. 2014, 7, 3902–3920. [Google Scholar] [CrossRef]

- Grande, L.; Paillard, E.; Hassoun, J.; Park, J.B.; Lee, Y.J.; Sun, Y.K.; Passerini, S.; Scrosati, B. The Lithium/Air Battery: Still an Emerging System or a Practical Reality? Adv. Mater. 2015, 27, 784–800. [Google Scholar] [CrossRef]

- Battery Storage Systems: What Are Their Chemical Hazards? Available online: https://www.gses.com.au/wp-content/uploads/2016/09/GSES_Battery-Storage-Systems_what-are-their-chemical-hazards.pdf (accessed on 24 April 2020).

- Campion, C.L.; Li, W.T.; Lucht, B.L. Thermal decomposition of LiPF6-based electrolytes for lithium-ion batteries. J. Electrochem. Soc. 2005, 152, A2327–A2334. [Google Scholar] [CrossRef]

- Eshetu, G.G.; Bertrand, J.P.; Lecocq, A.; Grugeon, S.; Laruelle, S.; Armand, M.; Marlair, G. Fire behavior of carbonates-based electrolytes used in Li-ion rechargeable batteries with a focus on the role of the LiPF6 and LiFSI salts. J. Power Sources 2014, 269, 804–811. [Google Scholar] [CrossRef]

- Painting the Battery Green by Giving it a Second Life. Available online: https://batteryuniversity.com/learn/article/painting_the_battery_green_by_giving_it_a_second_life (accessed on 28 April 2020).

- BCC Research. Lithium Battery Recycling: North America Markets; FCB044A; Frost & Sullivan: San Antonio, TX, USA, 2018; p. 70. [Google Scholar]

- Palacín, M.R.; de Guibert, A. Why do batteries fail? Science 2016, 351, 1253292. [Google Scholar] [CrossRef]

- McManus, M.C. Environmental consequences of the use of batteries in low carbon systems: The impact of battery production. Appl. Energy 2012, 93, 288–295. [Google Scholar] [CrossRef]

- Mahmud, M.; Huda, N.; Farjana, S.; Lang, C. Comparative Life Cycle Environmental Impact Analysis of Lithium-Ion (LiIo) and Nickel-Metal Hydride (NiMH) Batteries. Batteries 2019, 5, 22. [Google Scholar] [CrossRef]

- Circular Economy and Waste Management. Available online: https://www.csiro.au/en/Research/Environment/Circular-Economy (accessed on 27 April 2020).

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: the expected transition to a balanced interplay of environmental and economic systems. J. Clean. Prod. 2016, 114, 11–32. [Google Scholar] [CrossRef]

- Kirchherr, J.; Reike, D.; Hekkert, M. Conceptualizing the circular economy: An analysis of 114 definitions. Resour. Conserv. Recycl. 2017, 127, 221–232. [Google Scholar] [CrossRef]

- Murray, A.; Skene, K.; Haynes, K. The Circular Economy: An Interdisciplinary Exploration of the Concept and Application in a Global Context. J. Bus. Ethics 2015, 140, 369–380. [Google Scholar] [CrossRef]

- Zeng, X.; Li, J.; Liu, L. Solving spent lithium-ion battery problems in China: Opportunities and challenges. Renew. Sustain. Energy Rev. 2015, 52, 1759–1767. [Google Scholar] [CrossRef]

- Technavio. Global Secondary Battery Recycling Market 2019–2023; Technavio: London, UK, 2019; p. 106. [Google Scholar]

- Battery Recycling Market by Chemistry, Source, Region—Global Forecast to 2025. Available online: https://www.reportlinker.com/p05099511/Battery-Recycling-Market-by-Chemistry-Source-End-Use-Material-And-Region-Global-Forecast-to.html?utm_source=PRN (accessed on 15 May 2020).

- Li, M.; Liu, J.; Han, W. Recycling and management of waste lead-acid batteries: A mini-review. Waste Manag. Res. 2016, 34, 298–306. [Google Scholar] [CrossRef] [PubMed]

- TechVision Group. Emerging Technologies in E-Waste and Battery Recycling; D80E-TV; Frost & Sullivan: San Antonio, TX, USA, 2018. [Google Scholar]

- Weng, C.H.; Feng, X.N.; Sun, J.; Peng, H. State-of-health monitoring of lithium-ion battery modules and packs via incremental capacity peak tracking. Appl. Energy 2016, 180, 360–368. [Google Scholar] [CrossRef]

- Els, F. Honda’s Starts Recycling Program to Extract 80% of Rare Earths from Used Hybrid Batteries. Available online: https://www.mining.com/hondas-starts-recycling-program-to-extract-80-of-rare-earths-from-used-hybrid-batteries-43719/ (accessed on 3 May 2020).

- Rodrigues, L.E.O.C.; Mansur, M.B. Hydrometallurgical separation of rare earth elements, cobalt and nickel from spent nickel–metal–hydride batteries. J. Power Sources 2010, 195, 3735–3741. [Google Scholar] [CrossRef]

- Agarwal, V.; Khalid, M.K.; Porvali, A.; Wilson, B.P.; Lundström, M. Recycling of spent NiMH batteries: Integration of battery leach solution into primary Ni production using solvent extraction. Sustain. Mater. Technol. 2019, 22, e00121. [Google Scholar] [CrossRef]

- Cui, Y. Carbonylation of Nickel and Iron from Reduced Oxides and Laterite Ore. Ph.D. Thesis, The University of New South Wales, Sydney, Australia, 2015. [Google Scholar]

- Why Lithium Has Turned from Gold to Dust for Investors. Available online: https://www.spglobal.com/en/research-insights/articles/why-lithium-has-turned-from-gold-to-dust-for-investors (accessed on 6 May 2020).

- Crompton, P. Closed Loop Lithium Battery Recycling Still Not Economical. Available online: https://www.bestmag.co.uk/content/closed-loop-lithium-battery-recycling-still-not-economical (accessed on 5 May 2020).

- Heelan, J.; Gratz, E.; Zheng, Z.; Wang, Q.; Chen, M.; Apelian, D.; Wang, Y. Current and Prospective Li-Ion Battery Recycling and Recovery Processes. JOM 2016, 68, 2632–2638. [Google Scholar] [CrossRef]

- Kim, H.; Jang, Y.-C.; Hwang, Y.; Ko, Y.; Yun, H. End-of-life batteries management and material flow analysis in South Korea. Front. Environ. Sci. Eng. 2018, 12, 3. [Google Scholar] [CrossRef]

- Second Life Batteries: A Sustainable Business Opportunity, Not A Conundrum. Available online: https://www.capgemini.com/2019/04/second-life-batteries-a-sustainable-business-opportunity-not-a-conundrum/ (accessed on 11 May 2020).

- Global Lithium-ion Battery Production and Capacity Expansion, Forecasts to 2025; K33F-18. May 2019. Available online: https://www.researchandmarkets.com/reports/4774506/global-lithium-ion-battery-production-and (accessed on 11 December 2020).

- Colthorpe, A. China to ‘Dominate Recycling and Second Life Battery Market Worth US$45bn by 2030′. Available online: https://www.energy-storage.news/news/china-to-dominate-recycling-and-a-second-life-battery-market-worth-us45bn-b (accessed on 8 May 2020).

- Kochhar, A.; Johnston, T.G. A process, apparatus, and system for recovering materials from batteries. International Patent Application WO2018218358A1, 6 December 2018. [Google Scholar]

- Lithium Prices to Continue Slide Despite Forecast Supply Disruptions and Strong Demand Growth. Available online: https://www.globenewswire.com/news-release/2019/07/17/1883820/0/en/Roskill-Lithium-prices-to-continue-slide-despite-forecast-supply-disruptions-and-strong-demand-growth.html (accessed on 6 May 2020).

- Cobalt Futures Historical Data. Available online: https://www.investing.com/commodities/cobalt-historical-data (accessed on 6 May 2020).

- Nickel Price. Available online: https://www.metalary.com/cobalt-price/ (accessed on 6 May 2020).

- Gallagher, K.G.; Nelson, P.A. 6—Manufacturing Costs of Batteries for Electric Vehicles. In Lithium-Ion Batteries, Pistoia, G., Ed.; Elsevier: Amsterdam, The Netherlands, 2014; pp. 97–126. [Google Scholar]

- Directive 2000/53/EC of the European Parliament and of the Council of 18 September 2000 on end-of life vehicles. Off. J. Eur. Union 2000, 269, 22.

- The European Parliament and the Council of the European Union. Directive 2006/66/EC on Batteries and Accumulators and Waste Batteries and Accumulators; The European Parliament and the Council of the European Union: Brussels, Belgium, 2006. [Google Scholar]

- The European Parliament and the Council of the European Union. Directive 2000/53/EC on End of Life Vehicles; The European Parliament and the Council of the European Union: Brussels, Belgium, 2000. [Google Scholar]

- The Waste Batteries and Accumulators (Amendment) Regulations. 2015. Available online: http://www.legislation.gov.uk/uksi/2015/1935 (accessed on 14 May 2020).

- PRBA. About PRBA. Available online: https://www.prba.org/about-prba/ (accessed on 7 May 2020).

- Winslow, K.M.; Laux, S.J.; Townsend, T.G. A review on the growing concern and potential management strategies of waste lithium-ion batteries. Resour. Conserv. Recycl. 2018, 129, 263–277. [Google Scholar] [CrossRef]

- Petzl, M.; Danzer, M.A. Nondestructive detection, characterization, and quantification of lithium plating in commercial lithium-ion batteries. J. Power Sources 2014, 254, 80–87. [Google Scholar] [CrossRef]

- New York State Rechargeable Battery Law. Available online: https://www.dec.ny.gov/docs/materials_minerals_pdf/batterylaw.pdf (accessed on 14 May 2020).

- Boyden, A.; Soo, V.K.; Doolan, M. The Environmental Impacts of Recycling Portable Lithium-Ion Batteries. Procedia Cirp 2016, 48, 188–193. [Google Scholar] [CrossRef]

- Department of Agriculture, Water and Environment. Product stewardship products and projects. Available online: https://www.environment.gov.au/protection/waste-resource-recovery/product-stewardship/projects (accessed on 7 May 2020).

- State of Victoria. Managing e-Waste in Victoria—Starting the Conversation. Available online: https://www.environment.vic.gov.au/__data/assets/pdf_file/0031/49729/E-waste-ban-discussion-paper_online_R.pdf (accessed on 7 May 2020).

- E-waste. Available online: https://www.epa.sa.gov.au/community/waste_and_recycling/e_waste (accessed on 7 May 2020).

- Why we need to ban e-waste from landfill now. Available online: https://www.totalgreenrecycling.com.au/why-we-need-to-ban-e-waste-from-landfill-now/ (accessed on 7 May 2020).

- O’Farrell, K.; Veit, R.; Vard, D. Study into Market Share and Stocks and Flows of Handheld Batteries in Australia, Melbourne; Sustainable Resource Use Pty Ltd.: Melbourne, Australia, 2014. [Google Scholar]

- Randell, P. Waste lithium-ion Battery Projections. Final Report. 2016. Available online: https://www.environment.gov.au/system/files/resources/dd827a0f-f9fa-4024-b1e0-5b11c2c43748/files/waste-lithium-battery-projections.pdf (accessed on 20 January 2021).

- Prior, T.; Wäger, P.A.; Stamp, A.; Widmer, R.; Giurco, D. Sustainable governance of scarce metals: The case of lithium. Sci. Total Environ. 2013, 461–462, 785–791. [Google Scholar] [CrossRef]

- Terazono, A.; Oguchi, M.; Iino, S.; Mogi, S. Battery collection in municipal waste management in Japan: Challenges for hazardous substance control and safety. Waste Manag. 2015, 39, 246–257. [Google Scholar] [CrossRef]

- Ministry of Ecology and Environment of the People’s Republic of China. Accelerating the Application of EV Guidance. Available online: http://www.mee.gov.cn/zcwj/gwywj/201811/t20181129_676570.shtml (accessed on 7 May 2020).

- Ministry of Ecology and Environment of the People’s Republic of China. “No Waste City” Trial Work Plan. Available online: http://www.mee.gov.cn/zcwj/gwywj/201901/t20190123_690456.shtml (accessed on 7 May 2020).

- Siqi, Z.; Guangming, L.; Wenzhi, H.; Juwen, H.; Haochen, Z. Recovery methods and regulation status of waste lithium-ion batteries in China: A mini review. Waste Manag. Res. 2019, 37, 1142–1152. [Google Scholar] [CrossRef]

- Song, J.; Yan, W.; Cao, H.; Song, Q.; Ding, H.; Lv, Z.; Zhang, Y.; Sun, Z. Material flow analysis on critical raw materials of lithium-ion batteries in China. J. Clean. Prod. 2019, 215, 570–581. [Google Scholar] [CrossRef]

- Li, J.; Yu, K.; Gao, P. Recycling and pollution control of the End of Life Vehicles in China. J. Mater. Cycles Waste Manag. 2014, 16, 31–38. [Google Scholar] [CrossRef]

- Harper, G.; Sommerville, R.; Kendrick, E.; Driscoll, L.; Slater, P.; Stolkin, R.; Walton, A.; Christensen, P.; Heidrich, O.; Lambert, S.; et al. Recycling lithium-ion batteries from electric vehicles. Nature 2019, 575, 75–86. [Google Scholar] [CrossRef]

- Zhang, T.; He, Y.; Wang, F.; Ge, L.; Zhu, X.; Li, H. Chemical and process mineralogical characterizations of spent lithium-ion batteries: An approach by multi-analytical techniques. Waste Manag. 2014, 34, 1051–1058. [Google Scholar] [CrossRef]

- Chen, H.; Shen, J. A degradation-based sorting method for lithium-ion battery reuse. PLoS ONE 2017, 12, e0185922. [Google Scholar] [CrossRef] [PubMed]

- Gaines, L. Lithium-ion battery recycling processes: Research towards a sustainable course. Sustain. Mater. Technol. 2018, 17. [Google Scholar] [CrossRef]

- Xiao, J.; Li, J.; Xu, Z. Challenges to Future Development of Spent Lithium Ion Batteries Recovery from Environmental and Technological Perspectives. Env. Sci Technol 2019. [Google Scholar] [CrossRef] [PubMed]

- Zhang, J.; Hu, J.; Liu, Y.; Jing, Q.; Yang, C.; Chen, Y.; Wang, C. Sustainable and Facile Method for the Selective Recovery of Lithium from Cathode Scrap of Spent LiFePO4 Batteries. ACS Sustain. Chem. Eng. 2019, 7, 5626–5631. [Google Scholar] [CrossRef]

- Velázquez-Martínez, O.V.J.; Santasalo-Aarnio, A.; Reuter, M.; Serna-Guerrero, R. A Critical Review of Lithium-Ion Battery Recycling Processes from a Circular Economy Perspective. Batteries 2019, 5, 68. [Google Scholar] [CrossRef]

- Cready, E.; Lippert, J.; Pihl, J.; Weinstock, I.; Symons, P. Technical and Economic Feasibility of Applying Used EV Batteries in Stationary Applications; Sandia National Labs.: Albuquerque, NM, USA, 2003.

- Hunt, G. Electric Vehicle Battery Test Procedures Manual Revision 2. Available online: https://avt.inl.gov/sites/default/files/pdf/battery/usabc_manual_rev2.pdf (accessed on 8 May 2020).

- Martinez-Laserna, E.; Gandiaga, I.; Sarasketa-Zabala, E.; Badeda, J.; Stroe, D.I.; Swierczynski, M.; Goikoetxea, A. Battery second life: Hype, hope or reality? A critical review of the state of the art. Renew. Sustain. Energy Rev. 2018, 93, 701–718. [Google Scholar] [CrossRef]

- Wood, E.; Alexander, M.; Bradley, T.H. Investigation of battery end-of-life conditions for plug-in hybrid electric vehicles. J. Power Sources 2011, 196, 5147–5154. [Google Scholar] [CrossRef]

- Hossain, E.; Murtaugh, D.; Mody, J.; Faruque, H.M.R.; Sunny, M.S.H.; Mohammad, N. A Comprehensive Review on Second-Life Batteries: Current State, Manufacturing Considerations, Applications, Impacts, Barriers & Potential Solutions, Business Strategies, and Policies. IEEE Access 2019, 7, 73215–73252. [Google Scholar] [CrossRef]

- Richa, K.; Babbitt, C.W.; Gaustad, G. Eco-Efficiency Analysis of a Lithium-Ion Battery Waste Hierarchy Inspired by Circular Economy. J. Ind. Ecol. 2017, 21, 715–730. [Google Scholar] [CrossRef]

- Martinez-Laserna, E.; Sarasketa-Zabala, E.; Sarria, I.V.; Stroe, D.; Swierczynski, M.; Warnecke, A.; Timmermans, J.; Goutam, S.; Omar, N.; Rodriguez, P. Technical Viability of Battery Second Life: A Study From the Ageing Perspective. IEEE Trans. Ind. Appl. 2018, 54, 2703–2713. [Google Scholar] [CrossRef]

- McLoughlin F., C.M. Secondary Re-use of Batteries from Electric Vehicles for Building Integrated Photo-Voltaic (BIPV) Applications; Technological University Dublin: Dublin, Ireland, 2015. [Google Scholar]

- Bowler, M. Battery Second Use: A Framework for Evaluating the Combination of Two Value Chains; Clemson University: Clemson, SC, USA, 2014. [Google Scholar]

- Neubauer, J.; Smith, K.; Wood, E.; Pesaran, A. Identifying and Overcoming Critical Barriers to Widespread Second Use of PEV Batteries; National Renewable Energy Lab. (NREL): Golden, CO, USA, 2015.

- Zu, C.X.; Li, H. Thermodynamic analysis on energy densities of batteries. Energy Environ. Sci. 2011, 4, 2614–2624. [Google Scholar] [CrossRef]

- Neubauer, J.; Pesaran, A. The ability of battery second use strategies to impact plug-in electric vehicle prices and serve utility energy storage applications. J. Power Sources 2011, 196, 10351–10358. [Google Scholar] [CrossRef]

- Neubauer, J.; Pesaran, A.; Williams, B.; Ferry, M.; Eyer, J. Techno-Economic Analysis of PEV Battery Second Use: Repurposed-Battery Selling Price and Commercial and Industrial End-User Value; No. 0148-7191; National Renewable Energy Lab.(NREL): Golden, CO, USA, 2012.

- Baumhöfer, T.; Brühl, M.; Rothgang, S.; Sauer, D.U. Production caused variation in capacity aging trend and correlation to initial cell performance. J. Power Sources 2014, 247, 332–338. [Google Scholar] [CrossRef]

- Heymans, C.; Walker, S.B.; Young, S.B.; Fowler, M. Economic analysis of second use electric vehicle batteries for residential energy storage and load-levelling. Energy Policy 2014, 71, 22–30. [Google Scholar] [CrossRef]

- Global Energy and Environment Research Team. Global Li-ion Batteries Market, Forecast to 2025; PAAC-27; Frost & Sullivan: San Antonio, TX, USA, 2019; p. 111. [Google Scholar]

- Stringer, D.; Ma, J. Where 3 Million Electric Vehicle Batteries Will Go When They Retire. Available online: https://www.bloomberg.com/news/features/2018-06-27/where-3-million-electric-vehicle-batteries-will-go-when-they-retire (accessed on 4 February 2021).

- Lamber, F. BMW and Bosch Open New 2.8 MWh Energy Storage Facility Built From Batteries from over 100 Electric Cars. Available online: https://electrek.co/2016/09/22/bmw-bosch-energy-storage-facility-built-from-batteries-from-over-100-electric-cars/ (accessed on 15 May 2020).

- Nissan Motor Corporation. Nissan LEAF first electric car to pass 400,000 sales; Nissan Motor Corporation: Yokohama, Japan, 2019. [Google Scholar]

- Proctor, D. EV Batteries Repurposed for Energy Storage. Available online: https://www.powermag.com/ev-batteries-repurposed-for-energy-storage/ (accessed on 15 May 2020).

- 4R Energy and Relectrify Collaborate in Second-Life Battery Storage Products. Available online: https://www.cefc.com.au/media/files/4r-energy-and-relectrify-collaborate-in-second-life-battery-storage-products/ (accessed on 15 May 2020).

- Connexx. 2018 News List. Available online: https://www.connexxsys.com/2018 (accessed on 15 May 2020).

- Field, K. Hyundai Partners With Wärtsilä On Stationary Storage Using Second-Life Batteries. Available online: https://cleantechnica.com/2018/07/10/hyundai-partners-with-wartsila-on-stationary-storage-using-second-life-batteries/ (accessed on 15 May 2020).

- Honda Expanding Partnership with SNAM on Second-Life Batteries and Battery Recycling in Europe. Available online: https://www.greencarcongress.com/2020/04/20200417-honda.html (accessed on 15 May 2020).

- Wenschinek, C. Unlocking the Value in Second-Life Electric Vehicle Batteries. Available online: https://www.idtechex.com/en/research-article/unlocking-the-value-in-second-life-electric-vehicle-batteries/15608 (accessed on 15 May 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Component | Composition a % | Commodity Value b US$/tonne |

|---|---|---|

| Cobalt | 5~20 | 33000 |

| Nickel | 5~15 | 11846 |

| Lithium | 1~7 | 6170 |

| Manganese | 10~15 | 47 |

| Iron | 5~25 | 87 |

| Aluminium | 4~24 | 1611 |

| Copper | 5~10 | 5183 |

| New Battery Price [US$/kWh] | Second Life DoD | Vehicle | Health Factor | Max Repurposed Battery Sell Price [US$/kWh] | Used Salvage value [US$/kWh] | Cost of Refurbishment [US$/kWh] |

|---|---|---|---|---|---|---|

| 250 | 60% | BEV75 | 0.33 | 83 | 51 | 32 |

| PHEV20 | 0.29 | 73 | 43 | 30 | ||

| 50% | BEV75 | 0.72 | 180 | 131 | 49 | |

| PHEV20 | 0.65 | 163 | 117 | 46 | ||

| 150 | 60% | BEV75 | 0.33 | 50 | 24 | 26 |

| PHEV20 | 0.29 | 44 | 19 | 25 | ||

| 50% | BEV75 | 0.72 | 108 | 72 | 36 | |

| PHEV20 | 0.65 | 98 | 64 | 34 |

| Market Application | Number of Repurposed Packs | Estimated Market Size (Ontario) | Cycle Frequency | Potential for Application | Limitations for Application a |

|---|---|---|---|---|---|

| Residential | 1–2 | >3 Millionc | Daily | Large market and small, easy-to-handle units | Regulated pricing minimizes savings for user |

| Market can be incrementally developed | Risk and maintenance must be addressed | ||||

| Telecommunication towers | 5–10 | 100,000 c | Daily and back-up | Motivated for onsite energy storage, and currently has many sites | High reliability demanded by application, and would be difficult to achieve |

| Light commercial | 10–15 | 10,000–100,000 c | Daily | Greater savings due to unregulated electrical pricing | Safety regulations for storing batteries on site must be determined |

| Have the expertise, location and personnel to support the technology | More packs are required | ||||

| Office building | 30–40 | 100,000 b | Daily | Greater savings due to unregulated electrical pricing | Larger application requires significant storage investment |

| Can complement generator use | Urban locations may create greater risks | ||||

| Fresh food distribution centers | 30–40 | 10,000–100,000 | Daily | Greater savings due to unregulated electrical pricing | Larger application requires significant storage investment |

| Large electrical demand with highly controllable equipment will work well with technology | Payback must be clearly demonstrated | ||||

| Often early adopters if business case can be demonstrated | |||||

| Have the expertise, location and personnel to support the technology | |||||

| Stranded power (renewables) | 900 | Uncertain (<10) d | 10–20/Month | Intermittent nature of renewable energy justifies energy storage | Size of application may use up supply or the supply will not be available |

| Have the expertise, location and personnel to support the technology | Complexity of controlling packs of varying states of health | ||||

| Motivated early adopters allow for greater market penetration of wind and solar | Increased risk of fire | ||||

| Transmission support | 1000 | Uncertain (<10) | 1/Month | Large energy needs create larger market for batteries | Size of application may use up supply or the supply will not be available |

| Currently users of auxiliary electricity services and thus have some comfort with the application | Benefits can still be achieved working with smaller market applications and customers. | ||||

| Motivated early adopters to help ease transmission congestion. | Complexity of controlling packs of varying states of health | ||||

| Increased risk of fire |

| Applications | Profitable (Yes/Maybe/No) | Comments |

|---|---|---|

| Accelerated calendar life testing | Yes | Profitable |

| Decentralised mini and microgrid (electricity access in rural areas in emerging markets). | Yes | Profitable |

| Distributed node telecom backup power | Yes | Profitable |

| Electric service power quality | Yes | Limited profits agreed by several studies |

| Light commercial load following | Yes | Profitable |

| Load-levelling | Yes | Only profitable under most favourable conditions (reduced auxiliary fees or wide price differences between on-peak and off-peak periods) |

| Power backup for generation asset outages | Yes | Profitable, 1.5 year payback period |

| Residential demand management (Energy time-shift + peak shaving) + PV | Yes | Profitable concluded by different studies. Savings surplus the costs of the batteries; best case with 6 years payback period |

| Residential load following | Yes | Profitable |

| Smart grid load dispatch | Yes | Profitable, Utilities obtain profits from second life use and EV owners perceive a reduction on the LCOE of the batteries of about 20% |

| T&D upgrade deferral | Yes | Limited profits |

| UPS | Yes | Profitable |

| Voltage support | Yes | Limited profits or profitable concluded by different studies |

| Wind generation grid integration, Short duration | Yes | Limited profits agreed by several studies |

| Area regulation | Maybe | Limited profits |

| Area regulation +Spinning reserve capacity | Maybe | Limited profits or not profitable from different studies |

| Demand charge management | Maybe | Limited profits or not profitable from different studies |

| Electric service reliability | Maybe | Limited profits or not profitable from different studies |

| Electric supply capacity | Maybe | Limited profits or not profitable from different studies |

| Electric supply reserve capacity | Maybe | Limited profits or not profitable from different studies |

| Energy time-shift | Maybe | Limited profits or not profitable from different studies |

| Load-following | Maybe | Limited profits or not profitable from different studies |

| Renewable capacity firming | Maybe | Limited profits or not profitable from different studies |

| Renewable energy time-shift | Maybe | Limited profits or not profitable from different studies |

| Substation on-site power | Maybe | Limited profits or not profitable from different studies |

| Time-of-use energy cost management | Maybe | Limited profits or not profitable from different studies |

| Transmission congestion relief | Maybe | Limited profits or not profitable from different studies |

| Transmission Support | Maybe | Limited profits or not profitable from different studies |

| Load Levelling/Energy Load Levelling/Energy | No | Not profitable |

| Power reliability +peak shaving | No | Not profitable |

| Wind generation grid integration, long duration | No | Not profitable |

| OEM | B2U Partner/Service Provider | EV Model | Capacity | B2U Application | Country |

|---|---|---|---|---|---|

| Daimler | GETEC, The Mobility House, Remondis | Smart | 13 MWh | Renewable energy | Germany |

| GM | ABB | Volt | 50 kWh/25 kW | Power supply | USA |

| GM | ABB | Volt | n/a | Renewable energy | USA |

| Renault | Eco2Charge | Kangoo ZE | 66 kWh | Renewable energy | France |

| Nissan | Eaton | Leaf | 4.2 kWh | Residential energy storage | UK |

| Nissan | Eaton & | Leaf | 4 MWh/4 MW | Peak shaving, Backup power | Netherlands |

| The Mobility House | |||||

| Nissan | Sumitomo | Leaf | 400 kWh/600 kW | Renewable energy | Japan |

| Mitsubishi & PSA | EDF & Forsee Power | Peugeot Ion, C-zero & iMiev | n/a | Renewable energy | France |

| BMW | UC San Diego | Mini-E | 160 kWh/100 kW | Renewable energy | USA |

| BMW | Vattenfall & Bosch | ActiveE & i3 | 2.8 MWh/2 MW | Renewable energy | Germany |

| BMW | Vattenfall | i3 | 12 kWh/50 kW | Fast charging | Germany |

| Renault | Connected Energy | Zoe | 50 kWh/50 kW | Fast charging | UK |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, Y.; Pohl, O.; Bhatt, A.I.; Collis, G.E.; Mahon, P.J.; Rüther, T.; Hollenkamp, A.F. A Review on Battery Market Trends, Second-Life Reuse, and Recycling. Sustain. Chem. 2021, 2, 167-205. https://doi.org/10.3390/suschem2010011

Zhao Y, Pohl O, Bhatt AI, Collis GE, Mahon PJ, Rüther T, Hollenkamp AF. A Review on Battery Market Trends, Second-Life Reuse, and Recycling. Sustainable Chemistry. 2021; 2(1):167-205. https://doi.org/10.3390/suschem2010011

Chicago/Turabian StyleZhao, Yanyan, Oliver Pohl, Anand I. Bhatt, Gavin E. Collis, Peter J. Mahon, Thomas Rüther, and Anthony F. Hollenkamp. 2021. "A Review on Battery Market Trends, Second-Life Reuse, and Recycling" Sustainable Chemistry 2, no. 1: 167-205. https://doi.org/10.3390/suschem2010011

APA StyleZhao, Y., Pohl, O., Bhatt, A. I., Collis, G. E., Mahon, P. J., Rüther, T., & Hollenkamp, A. F. (2021). A Review on Battery Market Trends, Second-Life Reuse, and Recycling. Sustainable Chemistry, 2(1), 167-205. https://doi.org/10.3390/suschem2010011