Measurement of Systemic Risk in the Colombian Banking Sector

Abstract

:1. Introduction

2. Literature Review

3. Proposed Methodology

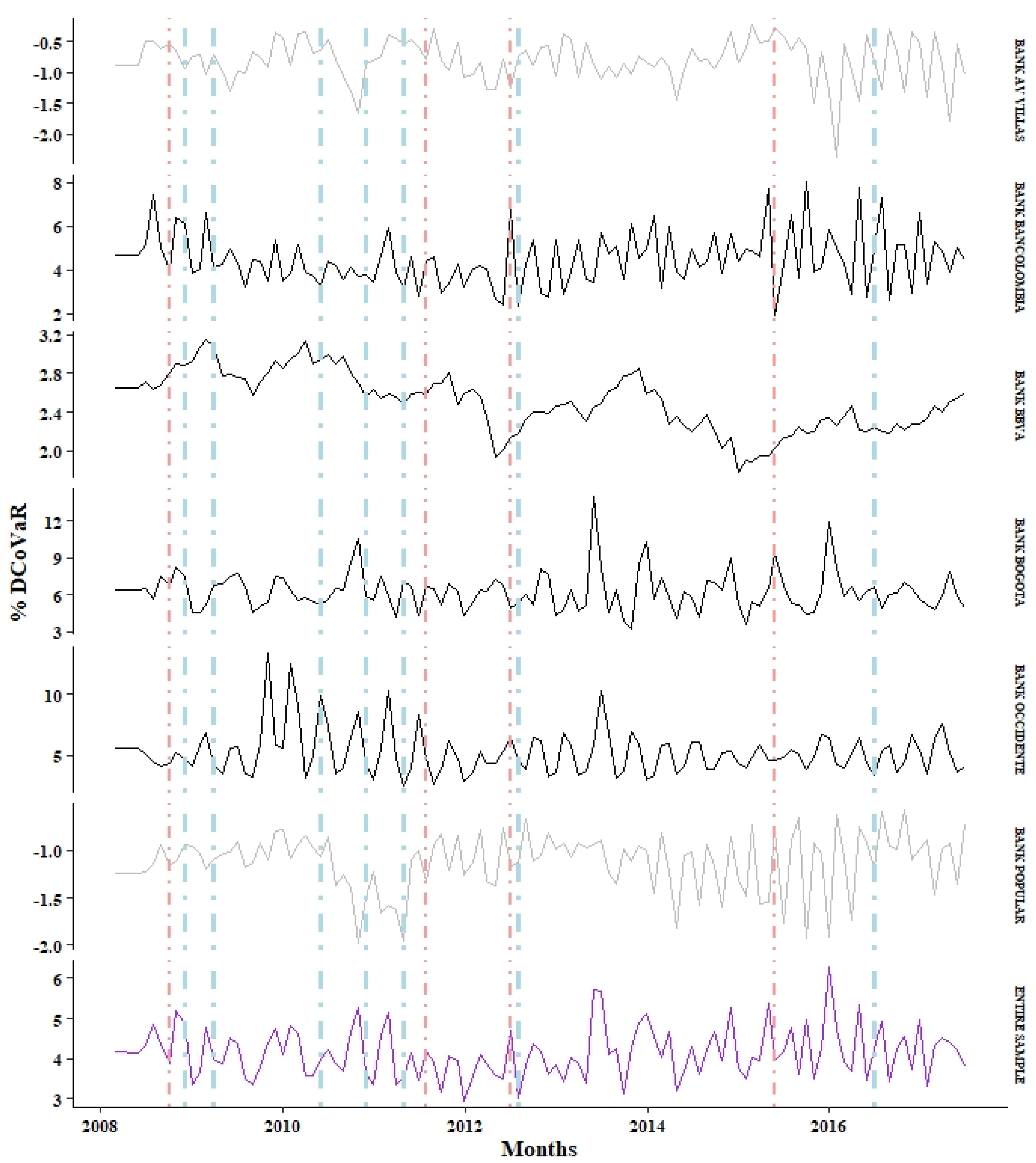

3.1. CoVaR

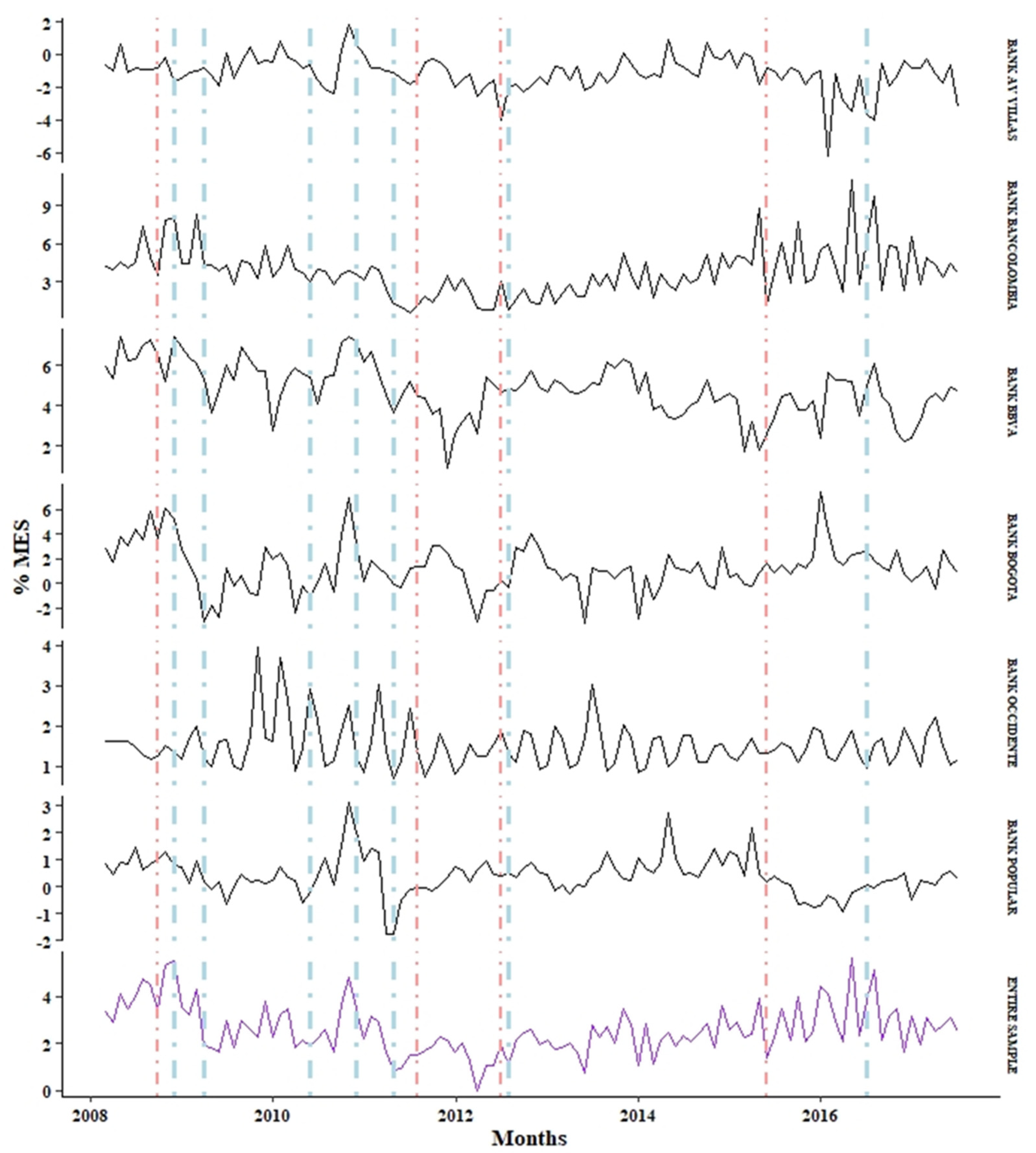

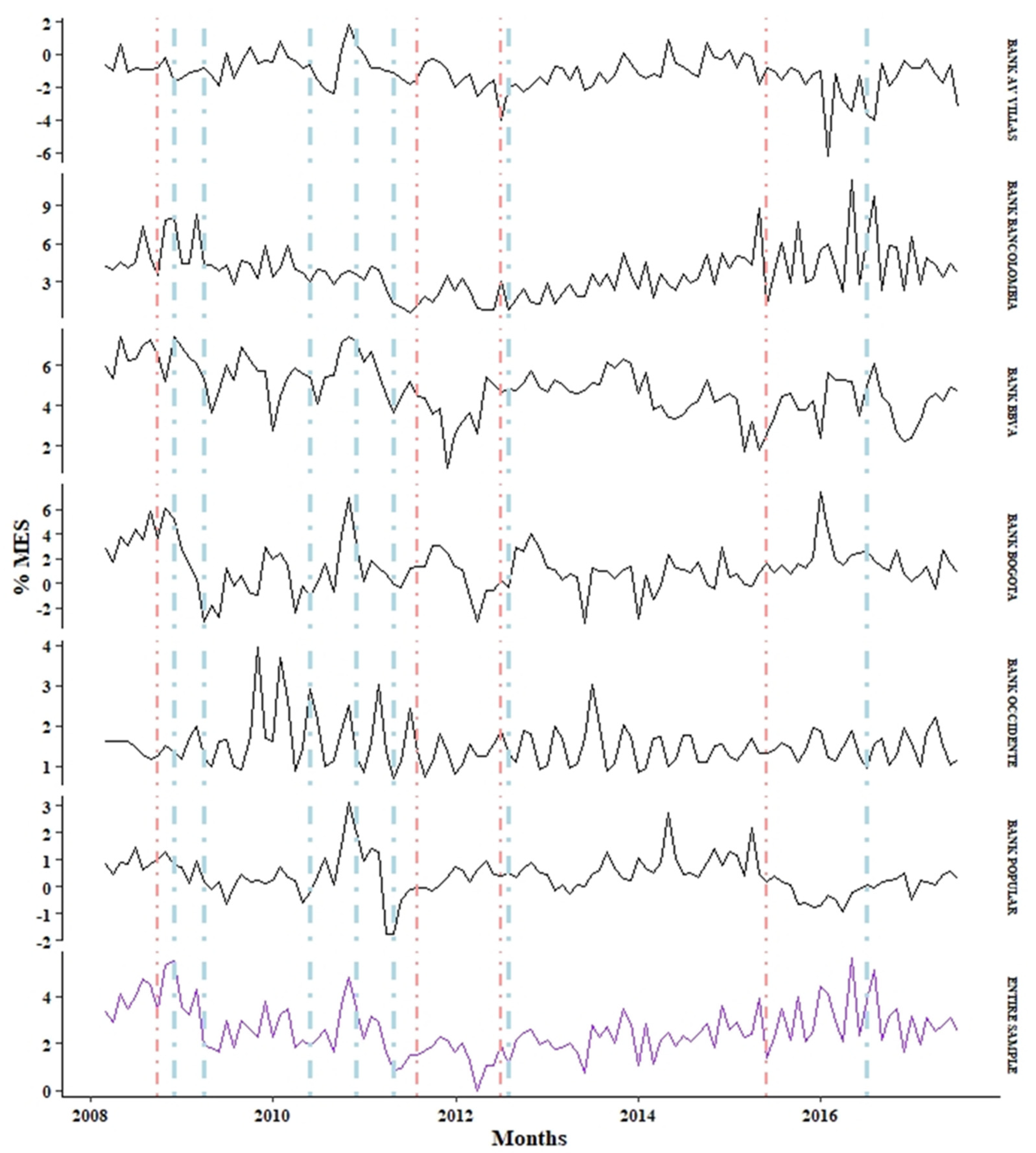

3.2. MES

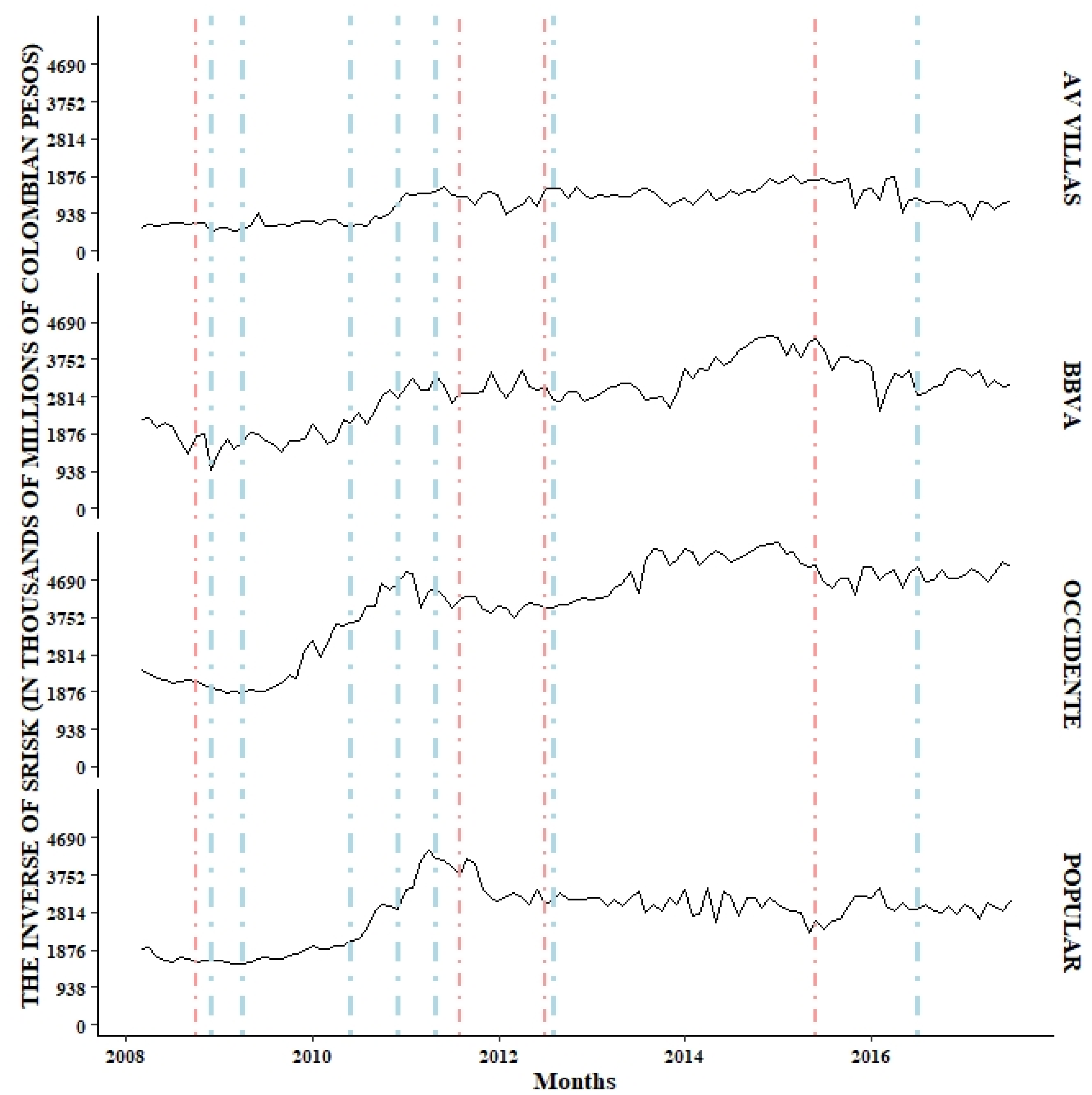

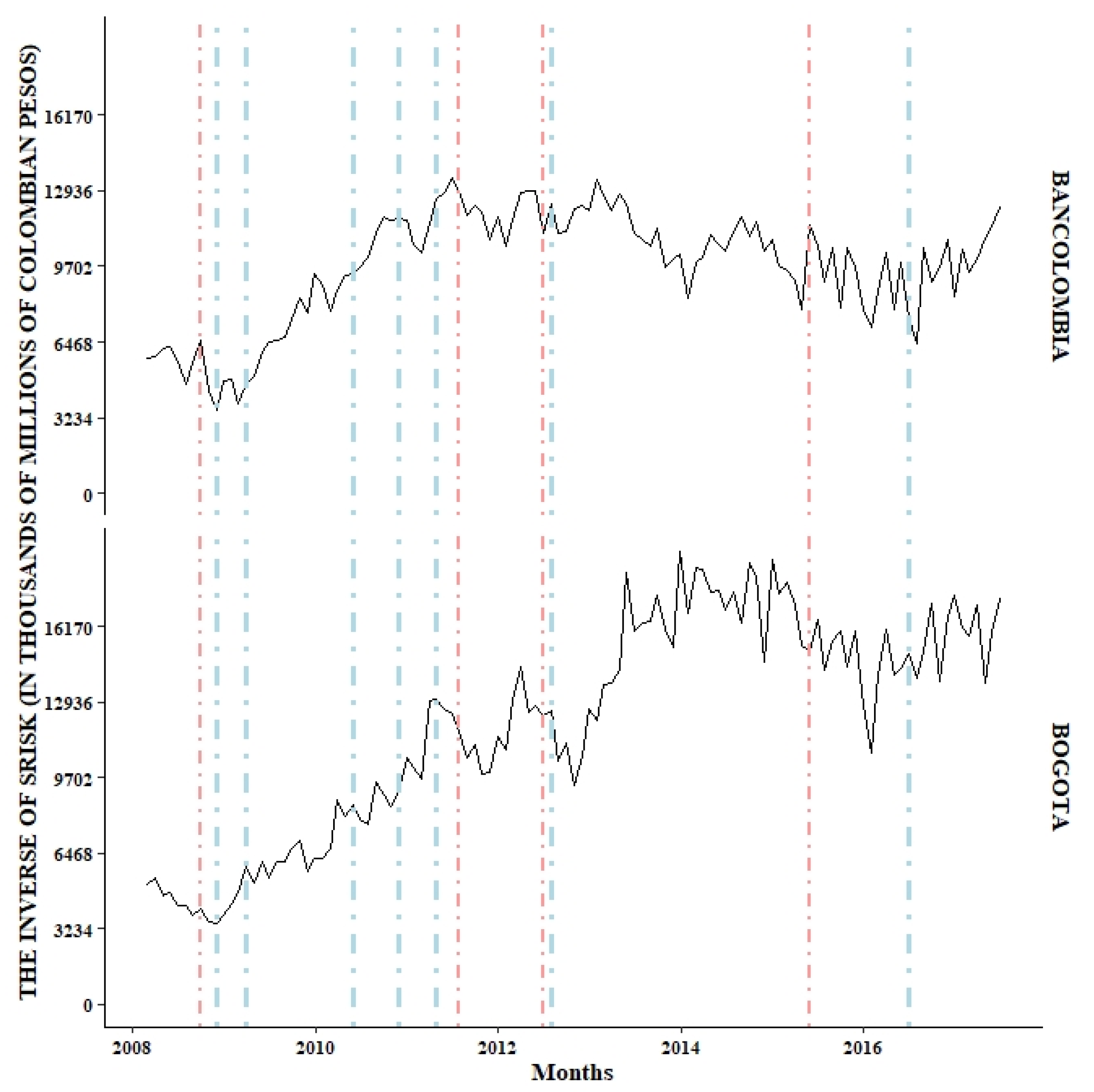

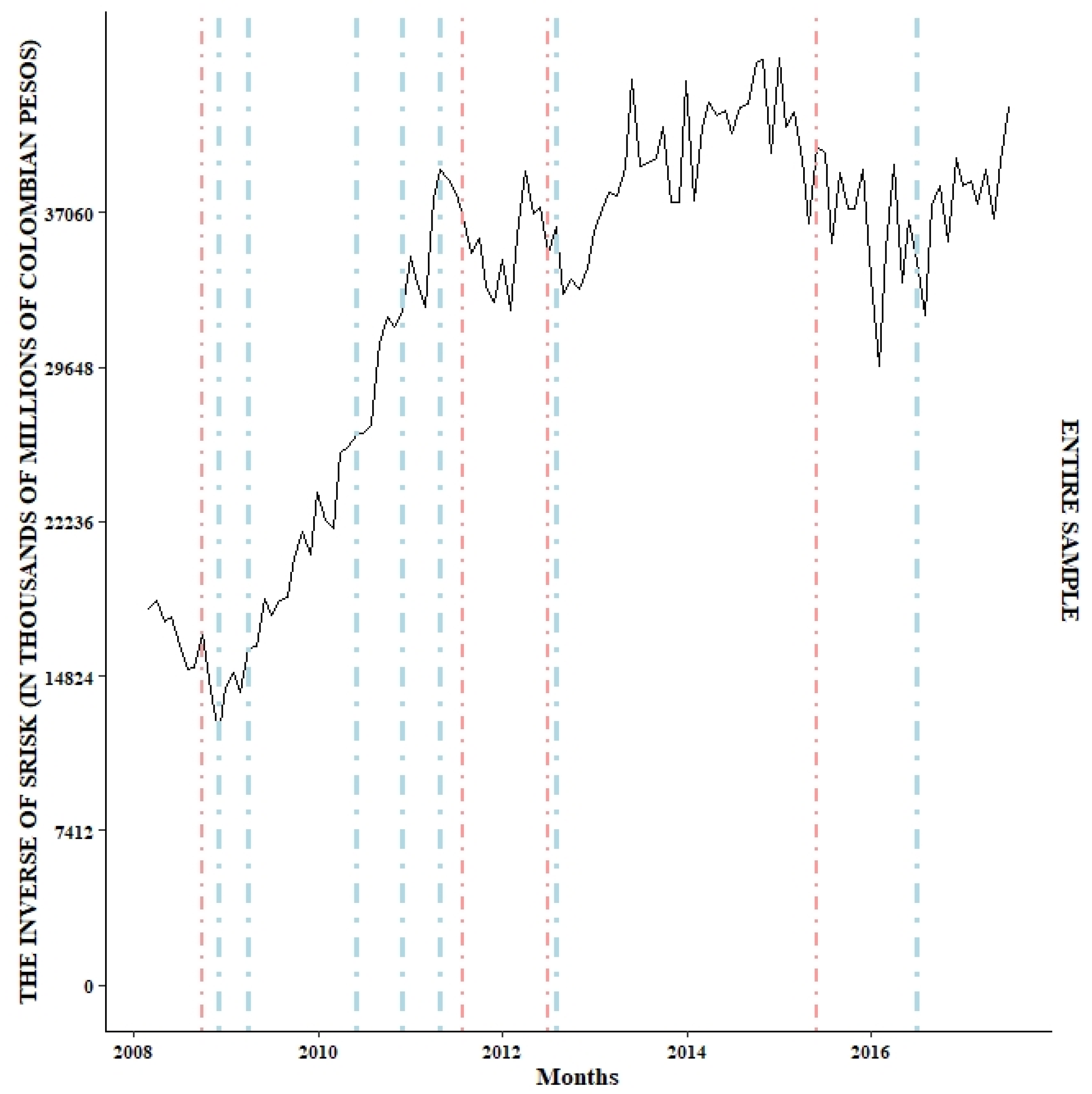

3.3. SRISK

4. Computational Results

4.1. Characteristics That Contribute to Systemic Risk

- Size of the Institution: Evidence indicates that size is correlated with the complexity of the institution and the interconnection with the rest of the system (Bostandzic and Weiß 2018). Large institutions are generally less substitutable, a circumstance that tends to present a greater risk to the system’s integrity. The natural logarithm of an institution’s total assets is taken as a proxy for the above characteristics.

- Fund Structure: For the structure of banks’ funds, the leverage behavior of the institution and the fragility and composition of the funds are used. To capture the leverage behavior of an institution, the leverage variable proposed by Acharya et al. (2017), defined as the quasi-value in the market of the assets divided by the market capitalization of the institution under consideration, is used. The long-term financing indicator developed by the Financial Superintendence of Colombia and the ratio between deposits and total obligations are used to capture the structure and fragility of the funds.

- Business Model: Three variables are used that can adequately characterize this characteristic in banks to determine the structure of the business model: income other than interest, the portfolio as a percentage of assets and the portfolio provision’s natural logarithm.

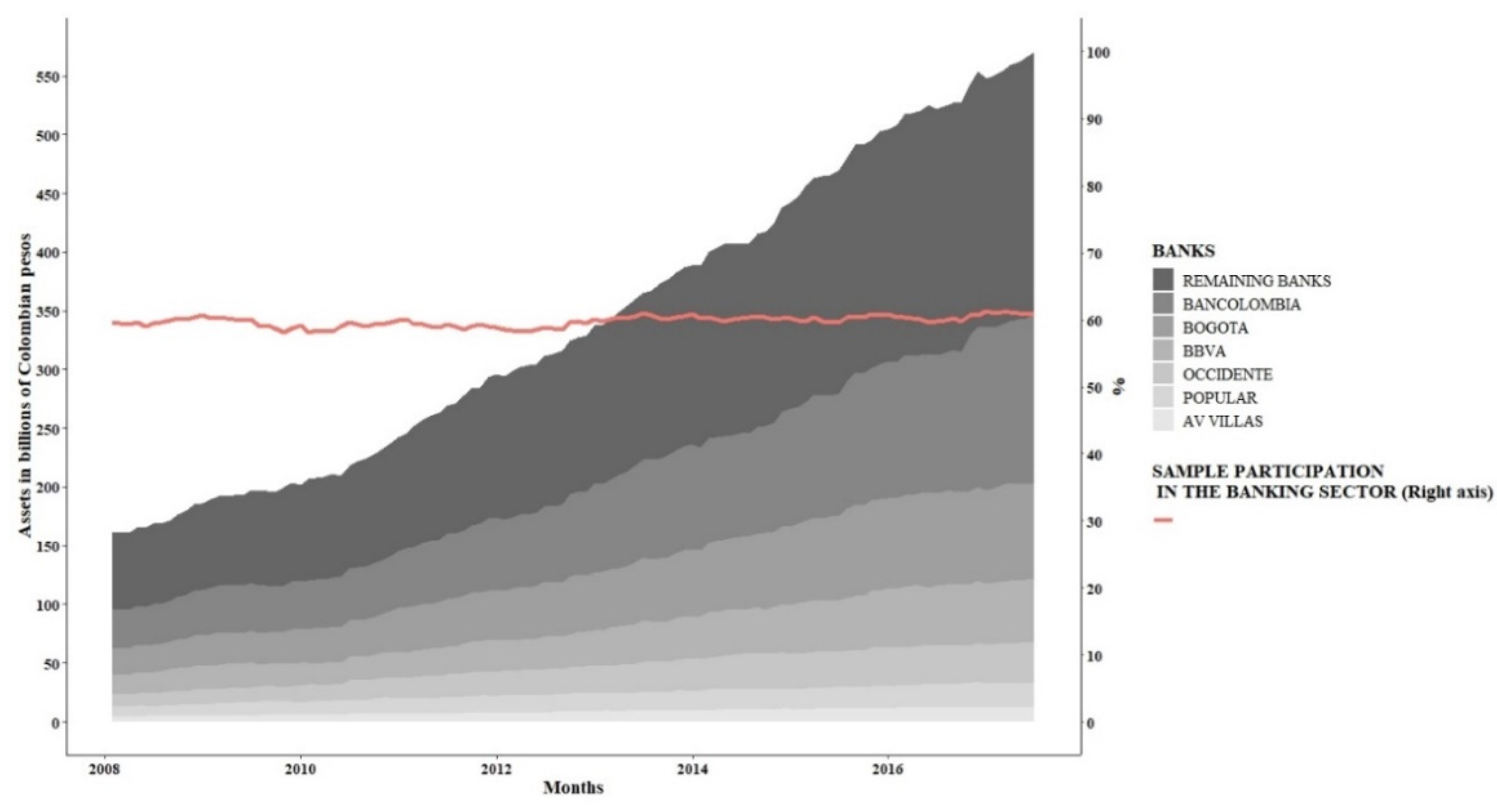

4.2. Market Value of Total Assets

- Corresponds to the book value of the total assets of bank at time .

- Corresponds to the book value of the total shares of bank at time .

- Corresponds to the market value of the total shares of bank at time . This variable considers both ordinary and preferred shares issued by the institution under consideration.

- Corresponds to the ratio between total assets and the book value of the shares of bank at time

- Corresponds to the market value of the total financial assets of the bank at time .

5. Discussion and Managerial Insights

6. Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

Appendix A

| Variable Name | Definition | Data Source |

| VIX | VIX measures market expectation of near-term volatility conveyed by stock index option prices | Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org (accessed on 27 January 2020) |

| LIQSPR | Short-term liquidity margin. Difference between three-month repo rate and three-month treasury bill rate. | Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org (accessed on 27 January 2020) |

| TBR3M | Change in the three-month treasury bill rate. | Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org (accessed on 27 January 2020) |

| YIESPR | Change in the slope of the returns curve. Spread between ten-year and three-month treasury bill rate. | Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org (accessed on 27 January 2020) |

| CRESPR | Change in the credit spread between BAA-rated bonds and treasury bill rate (both with a maturity of ten years). | Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org (accessed on 27 January 2020) |

| VOLTRM | Conditional volatility of the representative foreign exchange rate returns of the Colombian foreign exchange market. Obtained from an ARMA-EGARCH (3.4–7.2) model. | Own calculations with data obtained from the Banco de la república de Colombia. |

| VOLCOLG | Conditional volatility of the Colombia’s stock market index returns. Obtained from an ARMA-EGARCH (5.3–7.1) model. | Own calculations with data obtained from the Banco de la república de Colombia. |

| VOLTES | Conditional volatility of the returns of Colombia’s treasury bills index (IDXTES). Obtained from an ARMA-EGARCH (3.4–6.3) model. | Own calculations with data obtained from the Banco de la república de Colombia. |

| Banks’ characteristics | ||

| Total Assets | Natural logarithm of the asset’s book value. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Leverage | It corresponds to the quasi-market value of assets divided by the market value of equity, where the quasi-market value of assets is the book value of assets minus book value of equity + market value of equity (Acharya et al. 2017). | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Operating income different from interests | Operating income different from interest divided by total interest income. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Portfolio | Participation of gross portfolio in total assets. This variable is calculated as the division of the gross portfolio by total assets. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Portfolio provision | Natural logarithm of the portfolio provision. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Long-term financing index | Indicator that captures the need to finance short-term debts with long-term resources (assets). It is obtained by dividing the subtraction of the obligations and short-term assets by the long-term assets. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Deposits | Corresponds to the division of total deposits by total liabilities. | Own calculations with data obtained from the managerial indicators published by the Superintendencia Financiera de Colombia. |

| Source: Owner. | ||

Appendix B

Appendix C

References

- Acharya, Viral V. 2009. A theory of systemic risk and design of prudential bank regulation. Journal of Financial Stability 5: 224–55. [Google Scholar] [CrossRef]

- Acharya, Viral V., Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson. 2017. Measuring systemic risk. The Review of Financial Studies 30: 2–47. [Google Scholar] [CrossRef]

- Aparicio, Mónica, Alexandra Heredia, Camilo José Hernández, Juan Carlos Quintero, and Olga Esperanza Serna. 2012. Crisis Financieras Sistémicas en Colombia y Contraste con el Escenario Actual. Documento de Investigación. Colombia: Fogafin. [Google Scholar]

- Arias, Mauricio, Juan Carlos Mendoza-Gutiérrez, and David Pérez-Reyna. 2010. Applying covar to measure systemic market risk: The colombian case. Temas de Estabilidad Financiera 47: 1–16. [Google Scholar]

- Berger, Allen N., Jin Cai, Raluca A. Roman, and John Sedunov. 2021. Supervisory enforcement actions against banks and systemic risk. Journal of Banking & Finance. [Google Scholar] [CrossRef]

- Bostandzic, Denefa, and Gregor N. F. Weiß. 2018. Why do some banks contribute more to global systemic risk? Journal of Financial Intermediation 35: 17–40. [Google Scholar] [CrossRef]

- Boucher, Christophe M., Patrick S. Kouontchou, Bertrand B. Maillet, and O. Scaillet. 2013. The Co-CoVaR and Some Other Fair Systemic Risk Measures with Model Risk Corrections. Available online: www.systemic-riskhub.org/papers/selectedworks/BoucherKouontchouMailletScaillet_2013_fullpaper.pdf (accessed on 27 January 2020).

- Brownlees, Christian, and Robert F. Engle. 2016. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies 30: 48–79. [Google Scholar] [CrossRef]

- Cabrera-Rodríguez, Wilmar Alexander, Jorge Luis Hurtado-Guarín, Miguel Morales, and Juan Sebastián Rojas-Bohórquez. 2014. A Composite Indicator of Systemic Stress (CISS) for Colombia. Borradores de Economía; No. 826. Colombia: Banco de República. [Google Scholar]

- Cáceres, José Antonio. 2009. Colombia ante la crísis financiera global. Revista Escuela de Administración de Negocios 65: 5–30. [Google Scholar] [CrossRef]

- Castelao, Silvina, Sofía Palmigiani, and Patricia Lampes. 2013. Riesgo Sistémico: Una Aproximación Para el Sistema Bancario Uruguayo. No. 2013003. Montevideo: BCU. [Google Scholar]

- Coleman, Thomas F., Alex LaPlante, and Alexey Rubtsov. 2018. Analysis of the SRISK measure and its application to the Canadian banking and insurance industries. Annals of Finance 14: 547–70. [Google Scholar] [CrossRef]

- Davydov, Denis, Sami Vähämaa, and Sara Yasar. 2021. Bank liquidity creation and systemic risk. Journal of Banking & Finance 123: 106031. [Google Scholar]

- Drakos, Anastassios A., and Georgios P. Kouretas. 2015. Bank ownership, financial segments and the measurement of systemic risk: An application of CoVaR. International Review of Economics & Finance 40: 127–40. [Google Scholar]

- Duan, Yuejiao, Sadok El Ghoul, Omrane Guedhami, Haoran Li, and Xinming Li. 2021. Bank systemic risk around COVID-19: A cross-country analysis. Journal of Banking & Finance 133: 106299. [Google Scholar]

- Engle, Robert. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics 20: 339–50. [Google Scholar]

- Estrada, Dairo Ayiber, and Daniel Esteban Osorio-Rodríguez. 2006. A market risk approach to liquidity risk and financial contagion. Revista Ensayos Sobre Política Económica 24: 242–71. [Google Scholar] [CrossRef]

- Foggitt, Gregory M., Andre Heymans, Gary W. van Vuuren, and Anmar Pretorius. 2017. Measuring the systemic risk in the South African banking sector. South African Journal of Economic and Management Sciences 20: 1–9. [Google Scholar] [CrossRef] [Green Version]

- Furfine, Craig H. 2003. Interbank exposures: Quantifying the risk of contagion. Journal of Money, Credit and Banking 35: 111–28. [Google Scholar] [CrossRef]

- Grilli, Ruggero, Gabriele Tedeschi, and Mauro Gallegati. 2015. Markets connectivity and financial contagion. Journal of Economic Interaction and Coordination 10: 287–304. [Google Scholar] [CrossRef]

- Group of Ten. 2001. Report on Consolidation in the Financial Sector. Available online: https://www.imf.org/external/np/g10/2001/01/Eng/index.htm (accessed on 27 January 2020).

- Guerra, Solange Maria, Thiago Christiano Silva, Benjamin Miranda Tabak, Rodrigo Andrés de Souza Penaloza, and Rodrigo César de Castro Miranda. 2016. Systemic risk measures. Physica A: Statistical Mechanics and its Applications 442: 329–42. [Google Scholar] [CrossRef]

- International Monetary Fund. 2010. Annual Report 2010 Supporting a Balanced Global Recovery. Available online: https://www.imf.org/~/media/Websites/IMF/imported-flagship-issues/external/pubs/ft/ar/2010/eng/pdf/_ar10engpdf.ashx (accessed on 1 September 2021).

- Kleinow, Jacob, Fernando Moreira, Sascha Strobl, and Sami Vähämaa. 2017. Measuring systemic risk: A comparison of alternative market-based approaches. Finance Research Letters 21: 40–46. [Google Scholar] [CrossRef] [Green Version]

- Koenker, Roger, and Gilbert Bassett Jr. 1978. Regression quantiles. Econometrica: Journal of the Econometric Society 1: 33–50. [Google Scholar] [CrossRef]

- Laeven, Luc, Lev Ratnovski, and Hui Tong. 2016. Bank size, capital, and systemic risk: Some international evidence. Journal of Banking & Finance 69: S25–S34. [Google Scholar]

- Laverde, Mariana, and Javier Gutiérrez-Rueda. 2012. ¿Cómo Caracterizar Entidades Sistémicas? Medidas de Impacto Sistémico Para Colombia. Temas de Estabilidad Financiera, No. 65. Colombia: Banco de República. [Google Scholar]

- León, Carlos, and Clara Machado. 2011. Designing an Expert Knowledge-Based Systemic Importance Index for Financial Institutions. Borradores de Economía, No. 669. Colombia: Banco de República. [Google Scholar]

- León, Carlos, Clara Machado, Miguel Sarmiento, Freddy Cepeda, Orlando Chipatecua, and Jorge Cely. 2011. Riesgo sistémico y estabilidad del sistema de pagos de alto valor en Colombia: Análisis bajo topología de redes y simulación de pagos. Revista Ensayos Sobre Política Económica (ESPE) 29: 109–75. [Google Scholar] [CrossRef]

- Lin, Edward MH, Edward W. Sun, and Min-Teh Yu. 2018. Systemic risk, financial markets, and performance of financial institutions. Annals of Operations Research 262: 579–603. [Google Scholar] [CrossRef]

- López-Espinosa, Germán, Antonio Moreno, Antonio Rubia, and Laura Valderrama. 2012. Short-term wholesale funding and systemic risk: A global CoVaR approach. Journal of Banking & Finance 36: 3150–62. [Google Scholar]

- Luciano, Elisa, and Clas Wihlborg. 2018. Financial synergies and systemic risk in the organization of bank affiliates. Journal of Banking & Finance 88: 208–24. [Google Scholar]

- Meuleman, Elien, and Rudi Vander Vennet. 2020. Macroprudential policy and bank systemic risk. Journal of Financial Stability 47: 100724. [Google Scholar] [CrossRef] [Green Version]

- Nelson, Daniel B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society 59: 347–70. [Google Scholar] [CrossRef]

- Reig, Paula. 2017. Diez Años de Crisis en 24 Acontecimientos Clave. Available online: https://www.bbva.com/es/diez-anos-crisis-24-acontecimientos-clave/ (accessed on 23 March 2020).

- Silva, Walmir, Herbert Kimura, and Vinicius Amorim Sobreiro. 2017. An analysis of the literature on systemic financial risk: A survey. Journal of Financial Stability 28: 91–114. [Google Scholar] [CrossRef]

- Silva-Buston, Consuelo. 2019. Systemic risk and competition revisited. Journal of Banking & Finance 101: 188–205. [Google Scholar]

- Tobias, Adrian, and Markus K. Brunnermeier. 2011. CoVaR. No 17454, NBER Working Papers. Cambridge: National Bureau of Economic Research, Inc., Available online: https://econpapers.repec.org/repec:nbr:nberwo:17454 (accessed on 23 April 2020).

- Tobias, Adrian, and Markus K. Brunnermeier. 2016. CoVaR. The American Economic Review 106: 1705. [Google Scholar]

- V-Lab. n.d. Dynamic MES. Available online: https://vlab.stern.nyu.edu/docs/srisk/MES (accessed on 24 April 2020).

- Vogl, Christian. 2015. Systemic Risk Measurement in the Eurozone—A Multivariate GARCH Estimation of CoVaR. Lund: Lund University. [Google Scholar]

- Zedda, Stefano, and Giuseppina Cannas. 2020. Analysis of banks’ systemic risk contribution and contagion determinants through the leave-one-out approach. Journal of Banking & Finance 112: 105160. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Descriptive Statistics | N | Banks | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AV VILLAS | BANCOLOMBIA | BBVA | BOGOTÁ | OCCIDENTE | POPULAR | ||||||||

| Bank | System | Bank | System | Bank | System | Bank | System | Bank | System | Bank | System | ||

| Mín | 113 | −0.428 | −0.336 | −0.514 | −0.178 | −0.302 | −0.236 | −0.142 | −0.212 | −0.095 | −0.314 | −0.197 | −0.267 |

| 1st Qu. | 113 | −0.049 | −0.038 | −0.056 | −0.031 | −0.059 | −0.023 | −0.02 | −0.023 | −0.016 | −0.029 | −0.027 | −0.033 |

| Median | 113 | 0.01 | 0.028 | 0.051 | 0.01 | −0.01 | 0.017 | 0.006 | 0.022 | 0.002 | 0.026 | 0.003 | 0.024 |

| Average | 113 | 0.029 | 0.027 | 0.03 | 0.017 | 0.014 | 0.021 | 0.01 | 0.021 | 0.009 | 0.024 | 0.004 | 0.022 |

| 3rd Qu. | 113 | 0.073 | 0.104 | 0.117 | 0.069 | 0.056 | 0.073 | 0.038 | 0.075 | 0.023 | 0.087 | 0.039 | 0.07 |

| Max | 113 | 1776 | 0.362 | 0.594 | 0.284 | 0.341 | 0.24 | 0.157 | 0.298 | 0.199 | 0.326 | 0.252 | 0.258 |

| Specification | AV VILLAS | BANCOLOMBIA | BBVA | BOGOTÁ | OCCIDENTE | POPULAR | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| System | Bank | System | Bank | System | Bank | System | Bank | System | Bank | System | Bank | ||

| ARMA | AR1 | −0.034479 *** (0.000002) | −0.246957 *** (0.000079) | −0.049502 *** (0.000090 | −0.214773 *** (0.000130) | 0.302472 *** (0.000307) | −1.07579 *** (0.000134) | −1.026864 *** (0.001008) | −0.404966 *** (0.000017) | −0.103862 *** (0.000009) | |||

| AR2 | 0.842407 *** (0.000113) | 0.151093 *** (0.000241) | −0.195470 *** (0.000173) | 0.824432 *** (0.000828) | −0.726260 *** (0.002171) | −0.94786 *** (0.000556) | −1.095858 *** (0.001594) | −0.731353 *** (0.000040) | |||||

| AR3 | 0.041250 *** (0.000139) | −0.144043 *** (0.000095) | |||||||||||

| MA1 | 0.275944 *** (0.000001) | 0.224597 *** (0.000269) | 0.470256 *** (0.000408) | −0.133322 *** (0.000054) | 1.05083 *** (0.003667) | −0.25046 *** (0.000009) | 1.125084 *** (0.000669) | 0.533917 *** (0.000044) | −0.046343 *** (0.000009) | ||||

| MA2 | −1.095661 *** (0.000231) | −0.991695 *** (0.000063) | 0.538468 *** (0.000342) | 0.86165 *** (0.001624) | 1.234945 *** (0.000874) | 0.686710 *** (0.000009) | −0.076016 *** (0.000005) | ||||||

| MA3 | −0.240641 *** (0.000104) | −0.188052 *** (0.000150) | 0.278034 *** (0.000166) | 0.292615 *** (0.000109) | 0.229717 *** (0.000012) | −0.073302 *** (0.000001) | |||||||

| MA4 | 0.355981 *** (0.000014) | 0.264615 *** (0.000076) | −0.447289 *** (0.001104) | −0.184071 *** (0.000318) | 0.051772 *** (0.000028) | ||||||||

| EGARCH | ARCH1 | 0.799366 *** (0.000303) | 0.012710 *** (0.000031) | 0.246493 *** (0.000754) | −0.576275 *** (0.000133) | 0.605561 *** (0.000035) | −0.069722 *** (0.000166) | 0.33965 *** (0.001264) | 0.44333 *** (0.000105) | 0.537437 *** (0.000114) | 0.422964 *** (0.001229) | 0.011183 *** (0.000047) | 0.149429 *** (0.000013) |

| ARCH2 | −0.579092 *** (0.000059) | 0.323211 *** (0.000908) | −0.384483 *** (0.001015) | 0.140552 *** (0.000034) | −0.789385 *** (0.000009) | 0.132865 *** (0.000190) | 0.154661 *** (0.000050) | 0.157589 *** (0.000014) | |||||

| ARCH3 | −0.451457 *** (0.000105) | −0.853260 *** (0.000486) | 0.702936 *** (0.000578) | 0.219627 *** (0.000737) | −0.104234 *** (0.000032) | ||||||||

| ARCH4 | 0.471059 *** (0.000138) | −0.376674 *** (0.000009) | |||||||||||

| GARCH1 | 0.644798 *** (0.000292) | 0.726499 *** (0.000853) | 0.997655 *** (0.009199) | 0.036037 *** (0.000044) | 0.540945 *** (0.000161) | 0.961643 *** (0.003489) | 0.35768 *** (0.001203) | 0.41782 *** (0.000115) | −0.042545 *** (0.000041) | 0.815780 *** (0.000302) | −0.125789 *** (0.000047) | −0.227812 *** (0.000061) | |

| GARCH2 | −0.107191 *** (0.000058) | −0.022221 *** (0.000009) | 0.534309 *** (0.000690) | −0.490466 *** (0.000137) | −0.21096 *** (0.000147) | −0.77307 *** (0.000482) | −0.328719 *** (0.000051) | −1.000000 *** (0.000075) | 0.973641 *** (0.001867) | −0.009186 *** (0.000001) | |||

| GARCH3 | 0.787467 *** (0.001844) | 0.296964 *** (0.000203) | 0.688145 *** (0.000609) | 0.70607 *** (0.000028) | 0.53256 *** (0.000298) | 0.493064 *** (0.000072) | 0.712506 *** (0.000023) | 0.036081 *** (0.000036) | 0.734146 *** (0.000337) | ||||

| GARCH4 | −0.748643 *** (0.001662) | −0.62262 *** (0.001066) | −0.86264 *** (0.000495) | 0.037023 *** (0.000091) | −0.066404 *** (0.000157) | −0.682825 *** (0.000912) | −0.129795 *** (0.000016) | ||||||

| GAMMA1 | −0.885067 *** (0.000101) | 0.996195 *** (0.000574) | 0.115575 *** (0.000175) | 0.632487 *** (0.000820) | −0.420413 *** (0.000873) | −0.246882 *** (0.001143) | 1.15198 *** (0.032347) | 1.21458 *** (0.000511) | 0.721123 *** (0.000233) | 0.930880 *** (0.000041) | 1.589955 *** (0.001813) | 0.459014 *** (0.000084) | |

| GAMMA2 | 0.029432 *** (0.000030) | −0.943253 *** (0.000887) | −0.331180 *** (0.001007) | −1.079320 *** (0.000993) | −0.417899 *** (0.000043) | 1.408392 *** (0.000516) | 0.076924 *** (0.000026) | 1.140554 *** (0.000129) | |||||

| GAMMA3 | 1.135463 *** (0.000306) | −0.448216 *** (0.000036) | −1.413676 *** (0.000585) | −0.140913 *** (0.000193) | −0.888913 *** (0.001216) | ||||||||

| GAMMA4 | −1.427526 *** (0.0000499 | 1.201497 *** (0.002484) | |||||||||||

| Specifications | Banks | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AV VILLAS | BANCOLOMBIA | BBVA | BOGOTÁ | OCCIDENTE | POPULAR | ||||||||

| System | Bank | System | Bank | System | Bank | System | Bank | System | Bank | System | Bank | ||

| Statistic of Weighted ARCH LM Tests | LAG | 3.562 * (8) | 3.006 * (6) | 2.149 (5) | 0.2935 (8) | 0.3971 (7) | 0.8164 (3) | 0.1252 (6) | 0.006104 (6) | 2.378 (7) | 0.05129 (6) | 0.01764 (8) | 0.004192 (7) |

| LAG | 5.027 (10) | 4.306 (8) | 2.688 (7) | 1.3683 (10) | 1.5182 (9) | 0.9351 (5) | 0.4744 (8) | 0.108698 (8) | 2.679 (9) | 0.34029 (8) | 1.50173 (10) | 0.008476 (9) | |

| LAG | 6.327 (12) | 4.751 (10) | 3.553 (9) | 1.8888 (12) | 2.8858 (11) | 1.656 (7) | 1.0434 (10) | 0.211909 (10) | 4.512 (11) | 3.94416 (10) | 1.72761 (12) | 0.013002 (11) | |

| Statistic of Weighted Ljung-Box Test on Standardized Residuals | LAG(1) | 0.345 | 0.225 | 0.5031 | 0.01174 | 0.4766 | 0.3104 | 0.9113 | 0.6687 | 0.003 | 0.1306 | 0.7995 | 0.07855 |

| LAG [2 x (p + q) + (p + q) − 1] | 9.145 | 1.497 | 1.1633 | 1.43577 | 9.1705 | 5.7734 | 5.6035 | 2.1882 | 7.931 | 6.9093 | 1.3296 | 3.1782 | |

| LAG [4 x (p + q) + (p + q) − 1] | 15.927 | 2.522 | 2.2855 | 3.18303 | 18.0695 | 15.5513 | 8.8423 | 3.8606 | 13.376 | 11.9768 | 2.4611 | 6.2216 | |

| t-value of Sign Bias Test | Sign Bias | 0.2625 | 1.92338 * | 0.474 | 1.0172 | 1.1945 | 0.1973 | 1.0692 | 0.6155 | 0.4014 | 0.5628 | 0.7137 | 0.9539 |

| −Sign Bias | 0.3557 | 0.31216 | 0.01592 | 0.21837 | 0.1144 | 0.4438 | 0.4976 | 0.061 | 0.6078 | 0.152 | 0.783 | 0.2512 | |

| +Sign Bias | 1.289 | 0.05067 | 0.24486 | 0.02748 | 1.1768 | 0.1897 | 1.6055 | 0.2599 | 0.6237 | 1.532 | 1.476 | 1.2071 | |

| Joint Effect | 2.043 | 6.30388 * | 0.33806 | 3.16204 | 2.0518 | 0.2438 | 3.2451 | 1.4817 | 1.0996 | 2.3709 | 3.0869 | 7.3373 * | |

| Statistic of Adjusted Pearson Goodness-of-Fit Test | Group 20 | 25.23 | 24.52 | 24.52 | 23.11 | 16.73 | 10.01 | 13.9 | 14.61 | 18.86 | 13.55 | 17.44 | 19.92 |

| Group 30 | 32.75 | 30.1 | 29.57 | 26.38 | 36.47 | 20.01 | 22.66 | 29.04 | 27.97 | 22.13 | 27.44 | 20.54 | |

| Group 40 | 42.4 | 48.77 | 40.27 | 31.78 | 36.73 | 27.53 | 28.95 | 30.37 | 45.23 | 33.19 | 37.44 | 36.73 | |

| Group 50 | 47.62 | 58.24 | 37.88 | 48.5 | 42.7 | 37 | 44.08 | 31.2 | 47.62 | 39.65 | 47.62 | 37.88 | |

| Dynamic Conditional Correlation (DCC) | p1 | 0.051755 ** (0.025315) | 0.039008 ** (0.015635) | 0.086556 *** (0.004175) | 0.25804 *** (0.059624) | 0.000000 ** (0.000000) | 0.063595 *** (0.021299) | ||||||

| q1 | 0.486054 *** (0.185008) | 0.860154** (0.380315) | 0.461762 ** (0.214375) | 0.37346 *** (0.131889) | 0.902351 *** (0.115806) | 0.553310 *** (0.165288) | |||||||

| Normal distribution | Yes | Yes | Yes | Yes | Yes | Yes | |||||||

| Quantile Regression (τ = 0.05) | Intercept | −0.13094 *** (0.01403) | −0.103357 *** (0.009594) | −0.10624 *** (0.01127) | −0.10761 *** (0.01062) | −0.13298 *** (0.01459) | −0.10531 *** (0.01152) | ||||||

| Beta | −0.03467 (0.22383) | 0.189388 *** (0.055078) | 0.20543 ** (0.07904) | 0.73401 *** (0.17231) | 0.73588 *** (0.18341) | −0.11914 (0.16436) | |||||||

| Banks | Descriptive Statistics | N | SRISK | %DCoVaR | %MES |

|---|---|---|---|---|---|

| AV VILLAS | Mín | 113 | 454.30 | –2.38 | –6.26 |

| 1st Qu. | 113 | 787.00 | –0.96 | –1.58 | |

| Median | 113 | 1263.00 | –0.79 | –1.02 | |

| Average | 113 | 1191.00 | –0.81 | –1.13 | |

| 3rd Qu. | 113 | 1496.00 | –0.55 | –0.55 | |

| Max | 113 | 1891.00 | –0.24 | 1.80 | |

| BANCOLOMBIA | Mín | 113 | 3593.00 | 1.93 | 0.60 |

| 1st Qu. | 113 | 7959.00 | 3.66 | 2.44 | |

| Median | 113 | 10,307.00 | 4.34 | 3.64 | |

| Average | 113 | 9675.00 | 4.47 | 3.76 | |

| 3rd Qu. | 113 | 11,528.00 | 5.11 | 4.48 | |

| Max | 113 | 13,455.00 | 0.80 | 10.98 | |

| BBVA | Mín | 113 | 966.00 | 1.78 | 0.94 |

| 1st Qu. | 113 | 2298.00 | 2.27 | 4.03 | |

| Median | 113 | 2981.90 | 2.54 | 4.77 | |

| Average | 113 | 2888.20 | 2.51 | 4.81 | |

| 3rd Qu. | 113 | 3460.10 | 2.71 | 5.68 | |

| Max | 113 | 4348.40 | 3.15 | 7.45 | |

| BOGOTA | Mín | 113 | 3480.00 | 3.25 | –3.26 |

| 1st Qu. | 113 | 8466.00 | 5.23 | 0.17 | |

| Median | 113 | 12,759.00 | 6.27 | 1.20 | |

| Average | 113 | 12,024.00 | 6.29 | 1.27 | |

| 3rd Qu. | 113 | 15,956.00 | 6.96 | 2.39 | |

| Max | 113 | 19,400.00 | 14.01 | 7.44 | |

| OCCIDENTE | Mín | 113 | 1835.00 | 2.46 | 0.69 |

| 1st Qu. | 113 | 3680.00 | 3.92 | 1.13 | |

| Median | 113 | 4393.00 | 4.97 | 1.44 | |

| Average | 113 | 4110.00 | 5.22 | 1.52 | |

| 3rd Qu. | 113 | 4988.00 | 5.89 | 1.72 | |

| Max | 113 | 5624.00 | 13.36 | 3.95 | |

| POPULAR | Mín | 113 | 1530.00 | –1.98 | –1.78 |

| 1st Qu. | 113 | 2160.00 | –1.25 | 0.05 | |

| Median | 113 | 2973.00 | –1.07 | 0.38 | |

| Average | 113 | 2766.00 | –1.13 | 0.41 | |

| 3rd Qu. | 113 | 3182.00 | –0.93 | 0.82 | |

| Max | 113 | 4395.00 | –0.58 | 3.11 | |

| SAMPLE | Mín | 113 | 12,044.00 | 2.96 | 0.00 |

| 1st Qu. | 113 | 26,491.00 | 3.66 | 1.89 | |

| Median | 113 | 35,914.00 | 4.09 | 2.39 | |

| Average | 113 | 32,653.00 | 4.15 | 2.60 | |

| 3rd Qu. | 113 | 39,109.00 | 4.56 | 3.21 | |

| Max | 113 | 44,470.00 | 6.26 | 5.62 |

| Dependent Variables | |||

|---|---|---|---|

| Independent Variables | Inverse of SRISK | DCoVaR | MES |

| Log-natural assets | −0.00123 | 0.00625 | |

| (0.00440) | (0.00630) | ||

| Leverage | −0.00170 | −0.00023 | |

| (0.00153) | (0.00110) | ||

| Long-term financing index | −0.00140 | −0.00250 *** | −0.00060 |

| (0.00390) | (0.00088) | (0.00210) | |

| Deposits | −0.00986 | −0.00054 | −0.00250 |

| (0.00626) | (0.00081) | (0.00270) | |

| Other incomes different from the interest | −0.00080 | −0.00045 | −0.00100 |

| (0.00340) | (0.00036) | (0.00100) | |

| Portfolio | −0.00170 | 0.00011 | −0.00080 |

| (0.00620) | (0.00071) | (0.00100) | |

| Provisions Portfolio | −0.00490 | −0.00057 | 0.00630 |

| (0.02000) | (0.00470) | (0.00850) | |

| Fixed effects—banks | Yes | Yes | Yes |

| Fixed effects—time | Yes | Yes | Yes |

| Observations | 672 | 452 | 565 |

| R2 | 0.0006 | 0.0170 | 0.0420 |

| Adjusted R2 | −0.2190 | −0.3500 | −0.2252 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rivera-Escobar, O.; Escobar, J.W.; Manotas, D.F. Measurement of Systemic Risk in the Colombian Banking Sector. Risks 2022, 10, 22. https://doi.org/10.3390/risks10010022

Rivera-Escobar O, Escobar JW, Manotas DF. Measurement of Systemic Risk in the Colombian Banking Sector. Risks. 2022; 10(1):22. https://doi.org/10.3390/risks10010022

Chicago/Turabian StyleRivera-Escobar, Orlando, John Willmer Escobar, and Diego Fernando Manotas. 2022. "Measurement of Systemic Risk in the Colombian Banking Sector" Risks 10, no. 1: 22. https://doi.org/10.3390/risks10010022

APA StyleRivera-Escobar, O., Escobar, J. W., & Manotas, D. F. (2022). Measurement of Systemic Risk in the Colombian Banking Sector. Risks, 10(1), 22. https://doi.org/10.3390/risks10010022