Pricing the Volatility Risk Premium with a Discrete Stochastic Volatility Model

Abstract

:1. Introduction

2. Literature Review

3. Stochastic Volatility and the Market Price of Risk

3.1. Volatility Risk Premium

3.2. NGARCH Stochastic Volatility Model

- (i)

- is lognormally distributed (under ),

- (ii)

- , almost surely with respect to ,

4. Model Estimation and Numerical Results

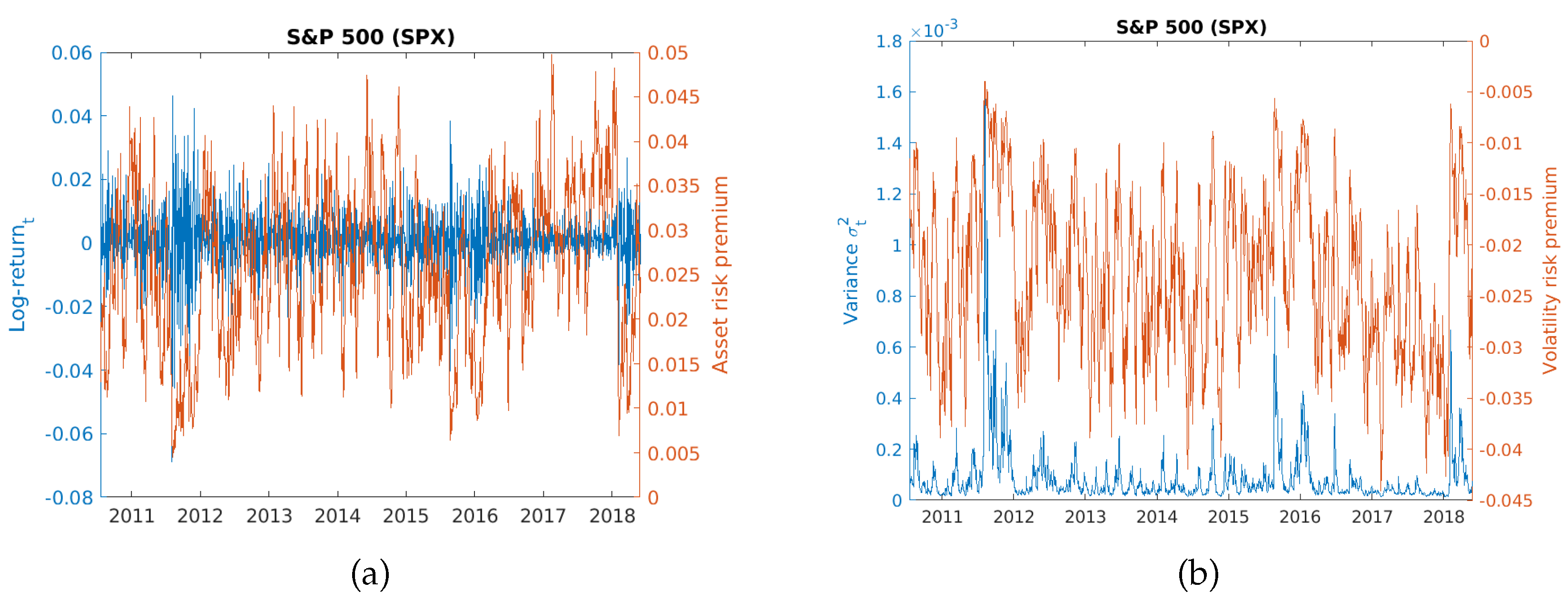

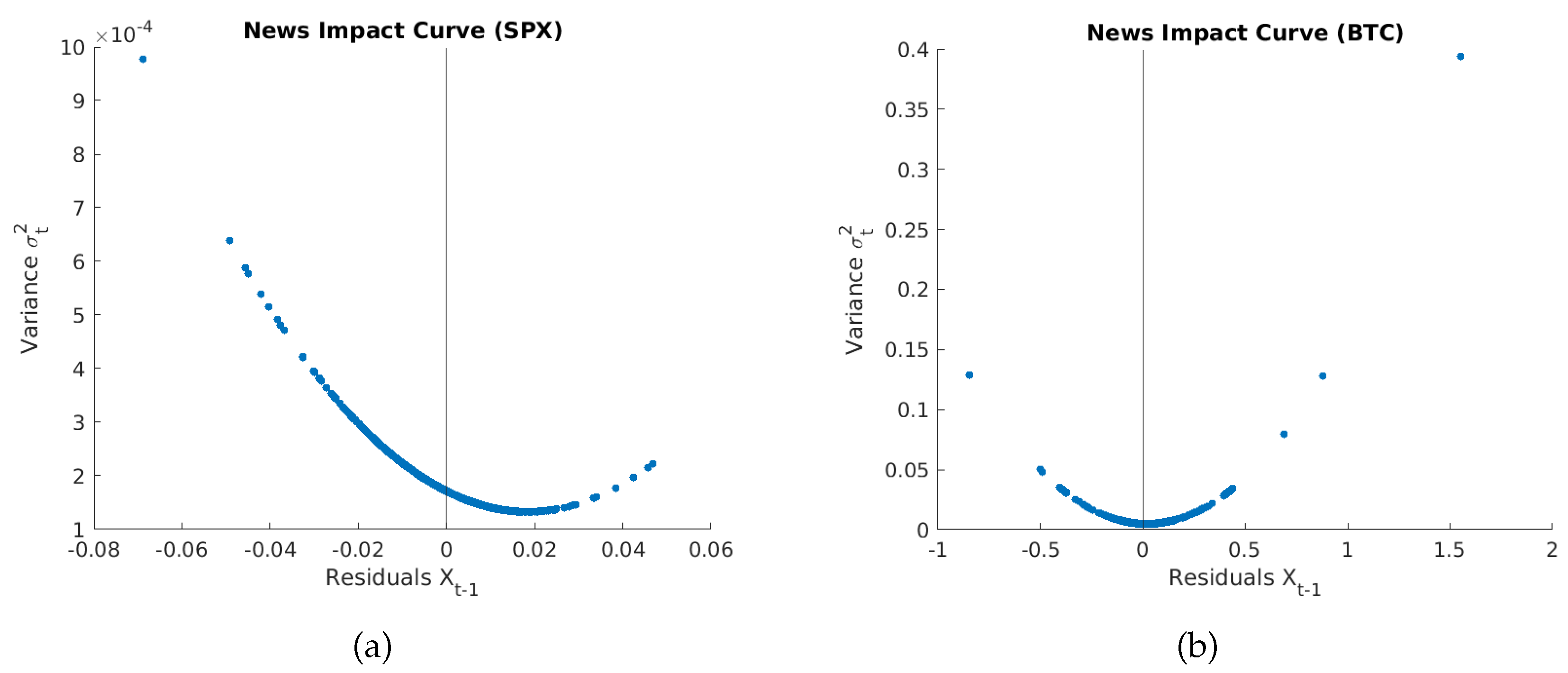

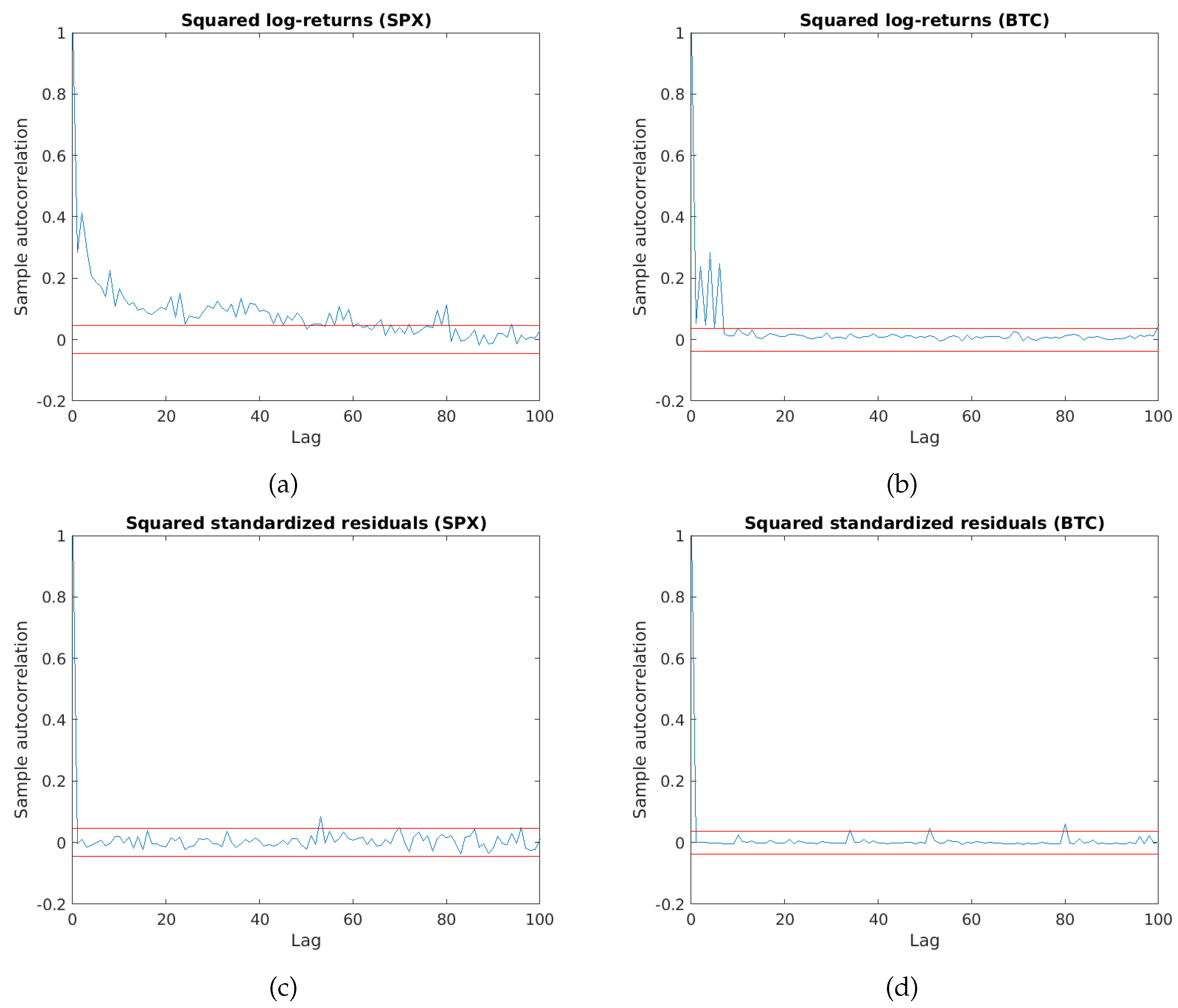

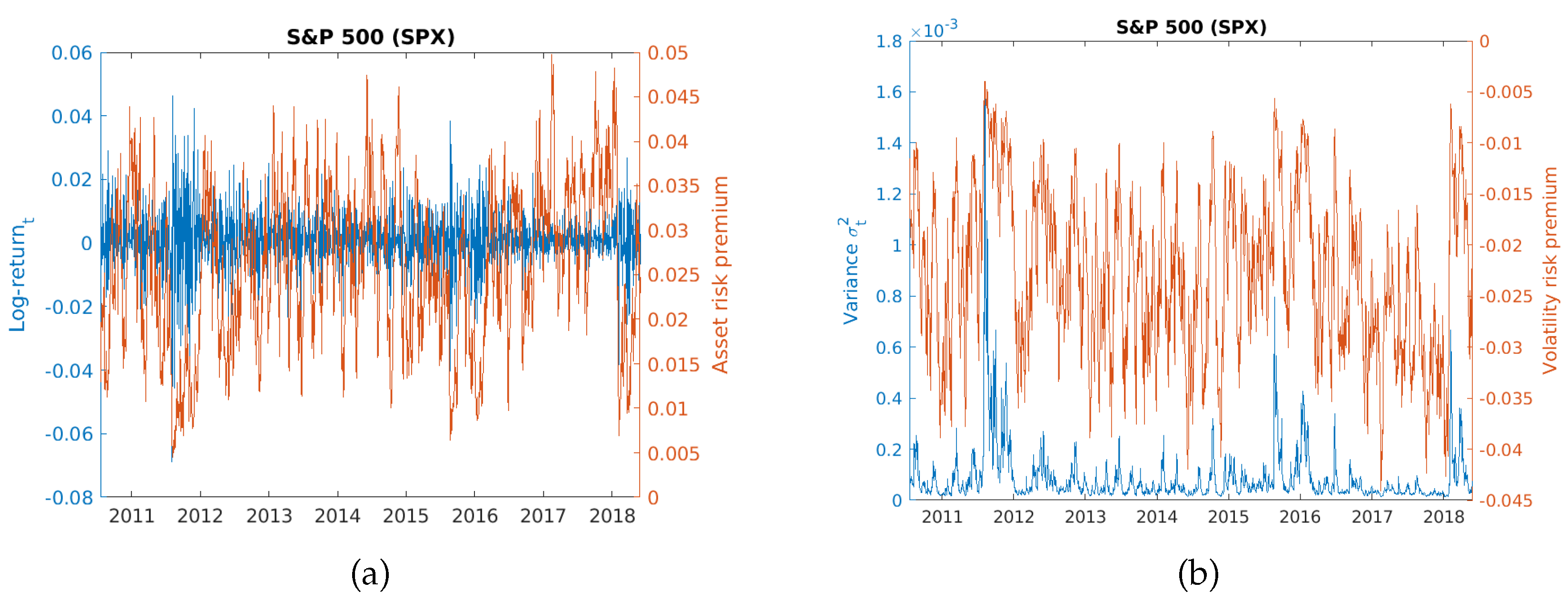

4.1. Parameter Estimates and Interpretation

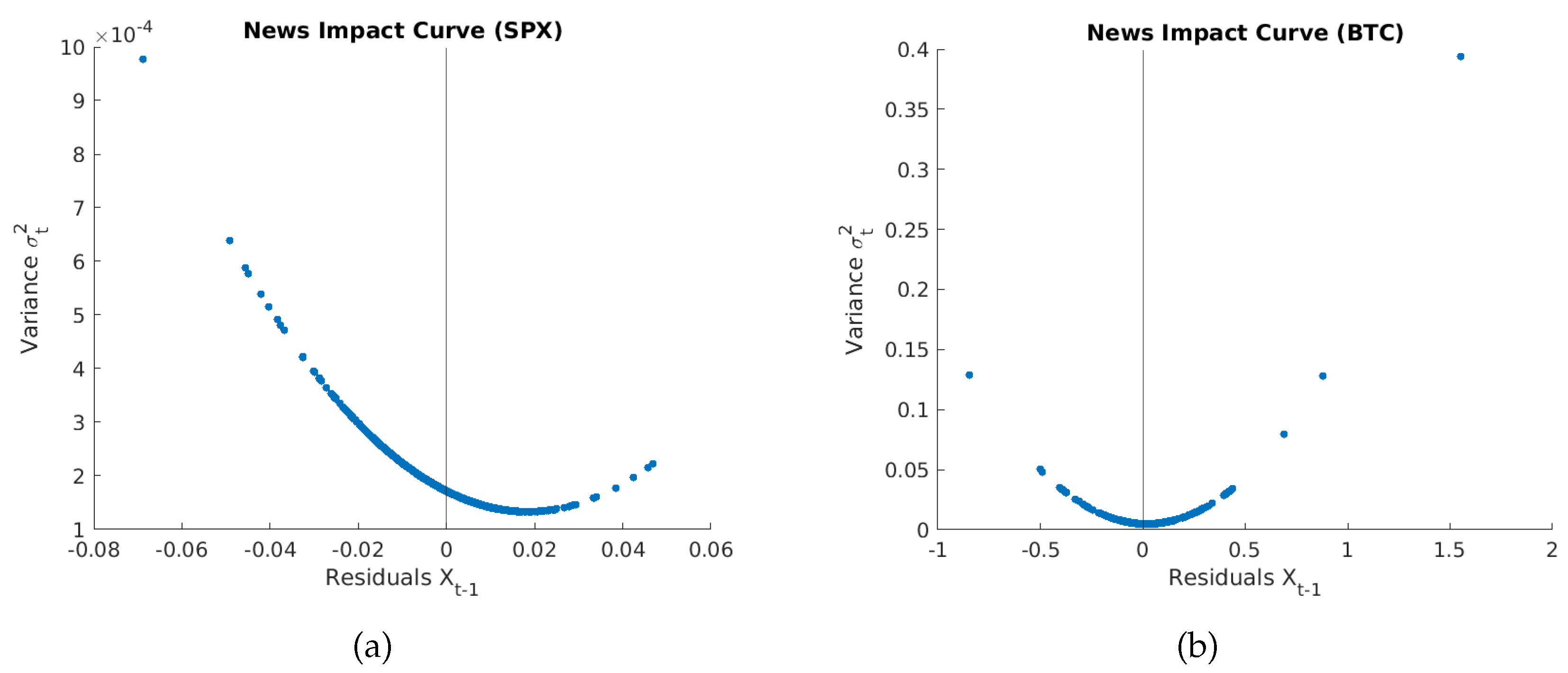

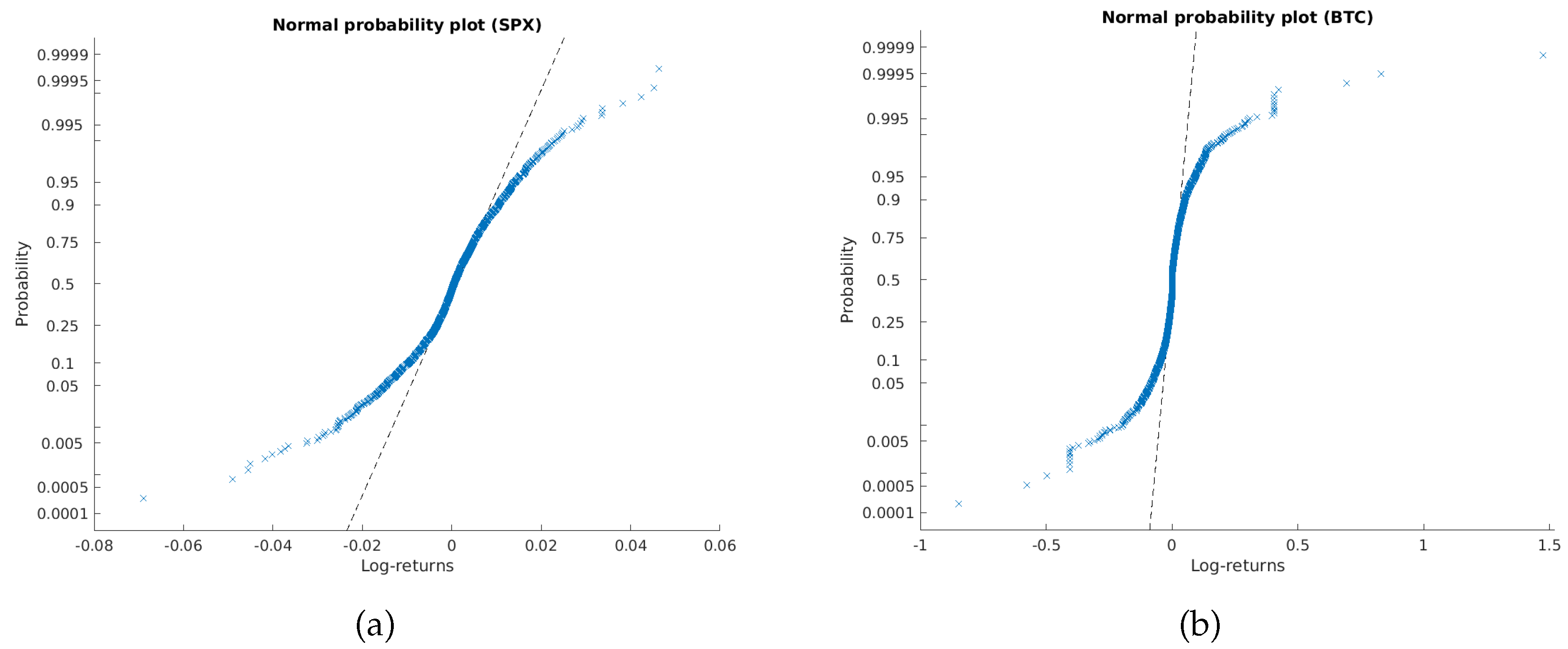

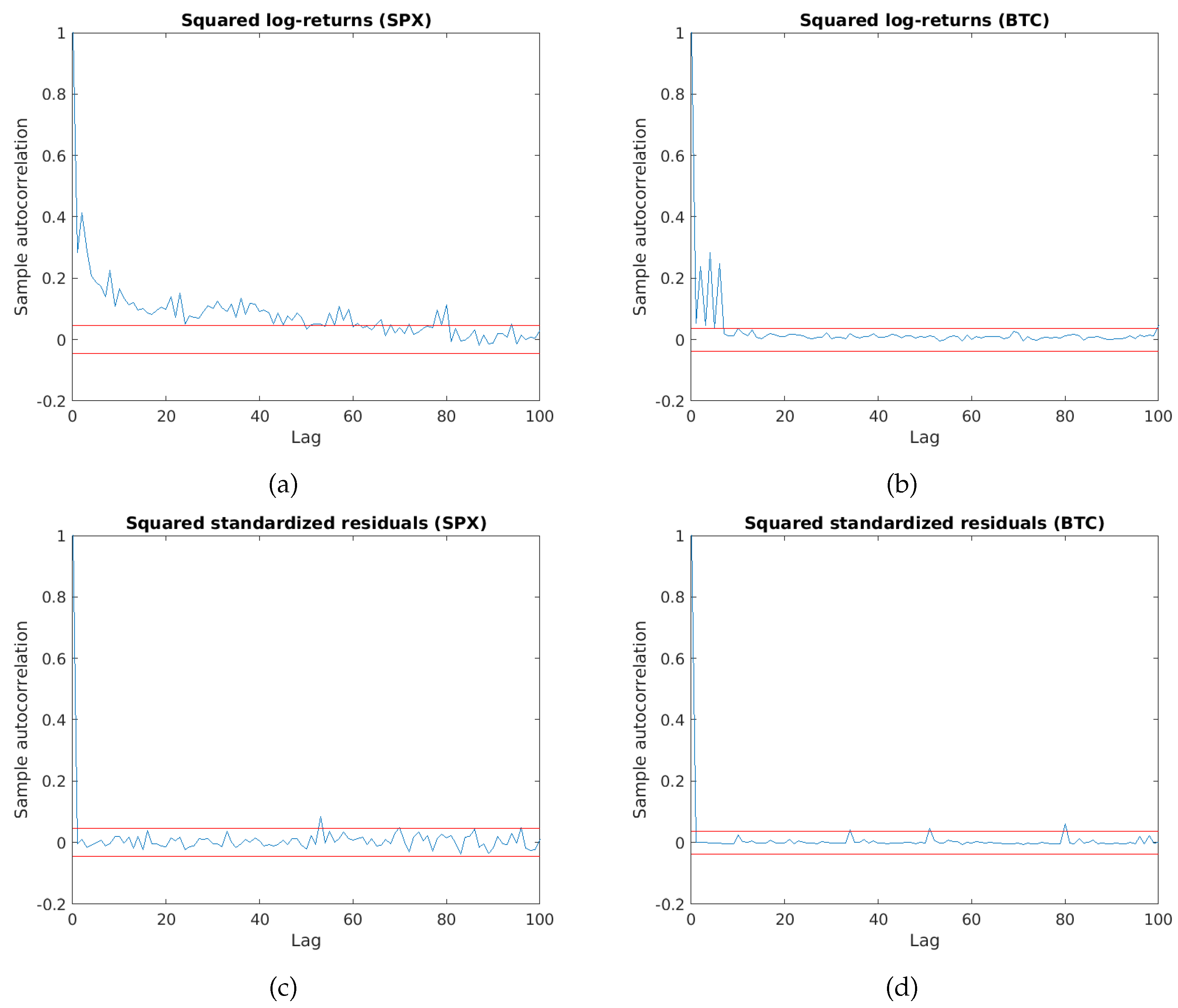

4.2. Model Fit

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef] [Green Version]

- Merton, R.C. Theory of Rational Option Pricing. Bell J. Econ. Manag. Sci. 1973, 4, 141–183. [Google Scholar] [CrossRef] [Green Version]

- Barndorff-Nielsen, O.E.; Shephard, N. Non-Gaussian Ornstein-Uhlenbeck-Based Models and Some of Their Uses in Financial Economics. J. R. Stat. Soc. Ser. (Stat. Methodol.) 2001, 63, 167–241. [Google Scholar] [CrossRef]

- Hubalek, F.; Posedel, P. Joint analysis and estimation of stock prices and trading volume in Barndorff-Nielsen and Shephard stochastic volatility models. Quant. Financ. 2011, 11, 917–932. [Google Scholar] [CrossRef] [Green Version]

- Pindyck, R. Risk, Inflation, and the Stock Market. Am. Econ. Rev. 1984, 74, 335–351. [Google Scholar]

- Brunnermeier, M.K.; Sannikov, Y. A Macroeconomic Model with a Financial Sector. Am. Econ. Rev. 2014, 104, 379–421. [Google Scholar] [CrossRef] [Green Version]

- Miyajima, K.; Shim, I. Asset managers in emerging market economies. BIS Q. Rev. 2014, 19–34. Available online: https://www.bis.org/publ/qtrpdf/r_qt1409e.htm (accessed on 1 June 2021).

- Engle, R.F.; NG, V.K. Measuring and Testing the Impact of News on Volatility. J. Financ. 1993, 48, 1749–1778. [Google Scholar] [CrossRef]

- Duan, J.C. The GARCH option pricing model. Math. Financ. 1995, 5, 13–32. [Google Scholar] [CrossRef]

- Bollerslev, T.; Gibson, M.; Zhou, H. Dynamic estimation of volatility risk premia and investor risk aversion from option-implied and realized volatilities. J. Econom. 2011, 160, 235–245. [Google Scholar] [CrossRef] [Green Version]

- Corradi, V.; Distaso, W.; Mele, A. Macroeconomic determinants of stock volatility and volatility premiums. J. Monet. Econ. 2013, 60, 203–220. [Google Scholar] [CrossRef]

- Negrea, B. The Volatility Premium Risk: Valuation and Forecasting. J. Appl. Quant. Methods 2009, 4, 154–165. [Google Scholar]

- Christoffersen, P.; Heston, S.; Jacobs, K. Capturing option anomalies with a variance-dependent pricing kernel. Rev. Financ. Stud. 2013, 26, 1963–2006. [Google Scholar] [CrossRef]

- Zhang, W.; Zhang, J.E. GARCH Option Pricing Models and the Variance Risk Premium. J. Risk Financ. Manag. 2020, 13, 51. [Google Scholar] [CrossRef] [Green Version]

- Duan, J.C. Cracking the smile. Risk 1996, 9, 55–59. [Google Scholar]

- Christoffersen, P.; Jacobs, K. Which GARCH Model for Option Valuation? Manag. Sci. 2004, 50, 1204–1221. [Google Scholar] [CrossRef] [Green Version]

- Fouque, J.P.; Papanicolaou, G.; Sircar, K.R. Derivatives in Financial Markets with Stochastic Volatility; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Hobson, D.G. Stochastic Volatility; School of Mathematical Sciences, University of Bath: Bath, UK, 1996. [Google Scholar]

- Javaheri, A. Inside Volatility Arbitrage: The Secrets of Skewness; John Wiley & Sons: Hoboken, NJ, USA, 2011; Volume 317. [Google Scholar]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Posedel, P. Analysis of the exchange rate and pricing foreign currency options on the croatian market: The ngarch model as an alternative to the black-scholes model. Financ. Theory Pract. 2006, 30, 347–368. [Google Scholar]

- Duan, J.C. Augmented GARCH (p, q) process and its diffusion limit. J. Econom. 1997, 79, 97–127. [Google Scholar] [CrossRef]

- Peetz, D.; Mall, G. Why Bitcoin is Not a Currency But a Speculative Real Asset. 2017. Available online: https://ssrn.com/abstract=3098765 (accessed on 1 June 2021). [CrossRef]

- MATLAB; Version 2021a; The MathWorks Inc.: Natick, MA, USA, 2021.

- Siu, T.K.; Elliott, R.J. Bitcoin option pricing with a SETAR-GARCH model. Eur. J. Financ. 2020, 27, 564–595. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis, 4th ed.; International, Ed.; Prentice Hall: Hoboken, NJ, USA, 2000; pp. 201–215. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SPX | BTC | |||||

|---|---|---|---|---|---|---|

| Par. | Est. Value | Std. Error | Z-Stat. | Est. Value | Std. Error | Z-Stat. |

| 3.131 | 9.1783 | 35.2208 | ||||

| 0.1106 | 0.0122 | 9.0585 | 0.1657 | 0.0057 | 29.3083 | |

| 0.6768 | 0.0199 | 34.0946 | 0.7962 | 0.0037 | 217.9210 | |

| 1.3328 | 0.1243 | 10.7268 | 0.2504 | 0.0272 | 9.1968 | |

| 1.5521 | 0.0039 | 0.0011 | 3.6623 | |||

| Persistence | 0.9838 | 0.9723 | ||||

| Log-likelihood | −8697.73 | −7145.99 | ||||

| Min () | Max () | Med. () | Mean () | St.dev. () | Skew. () | Kurt. () | |

|---|---|---|---|---|---|---|---|

| SPX | −0.0441 | −0.0039 | −0.0230 | −0.0227 | 0.0079 | 0.0173 | 2.2497 |

| BTC | −0.0428 | −0.0019 | −0.0294 | −0.0279 | 0.0100 | 0.4793 | 2.2233 |

| Mean () | St.dev. () | Skewness () | Kurtosis () | |

|---|---|---|---|---|

| SPX | 0.0145 | 0.9994 | −0.5663 | 5.0493 |

| BTC | 0.0121 | 1.0008 | 3.6860 | 93.2303 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Posedel Šimović, P.; Tafro, A. Pricing the Volatility Risk Premium with a Discrete Stochastic Volatility Model. Mathematics 2021, 9, 2038. https://doi.org/10.3390/math9172038

Posedel Šimović P, Tafro A. Pricing the Volatility Risk Premium with a Discrete Stochastic Volatility Model. Mathematics. 2021; 9(17):2038. https://doi.org/10.3390/math9172038

Chicago/Turabian StylePosedel Šimović, Petra, and Azra Tafro. 2021. "Pricing the Volatility Risk Premium with a Discrete Stochastic Volatility Model" Mathematics 9, no. 17: 2038. https://doi.org/10.3390/math9172038

APA StylePosedel Šimović, P., & Tafro, A. (2021). Pricing the Volatility Risk Premium with a Discrete Stochastic Volatility Model. Mathematics, 9(17), 2038. https://doi.org/10.3390/math9172038