Power System Portfolio Selection and CO2 Emission Management Under Uncertainty Driven by a DNN-Based Stochastic Model

Abstract

1. Introduction

2. Stochastic Electricity Economic Cost (EEC) of Systemic Portfolios: A Review

2.1. The Stochastic Electricity Economic Cost (EEC)

2.2. Systemic Portfolios

2.3. Optimal Systemic Portfolios

3. The Dynamics of Stochastic Factors: A DNN-Based Model

3.1. Modeling the Joint Dynamics of Gas and Coal

DNN Validation and Performance Evaluation

3.2. Modeling the Dynamics of Carbon Prices

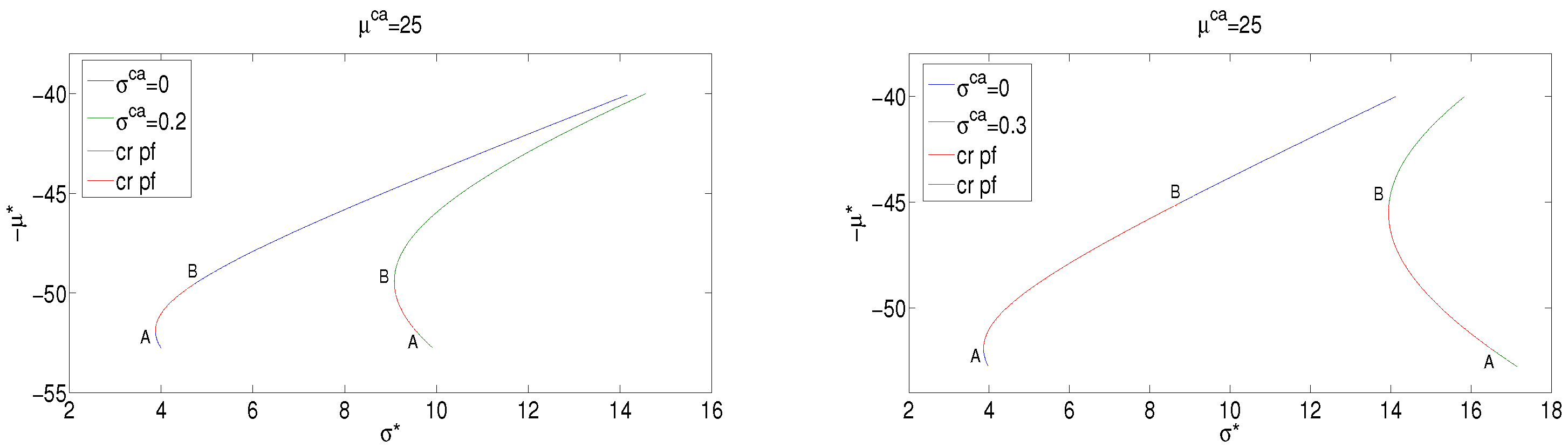

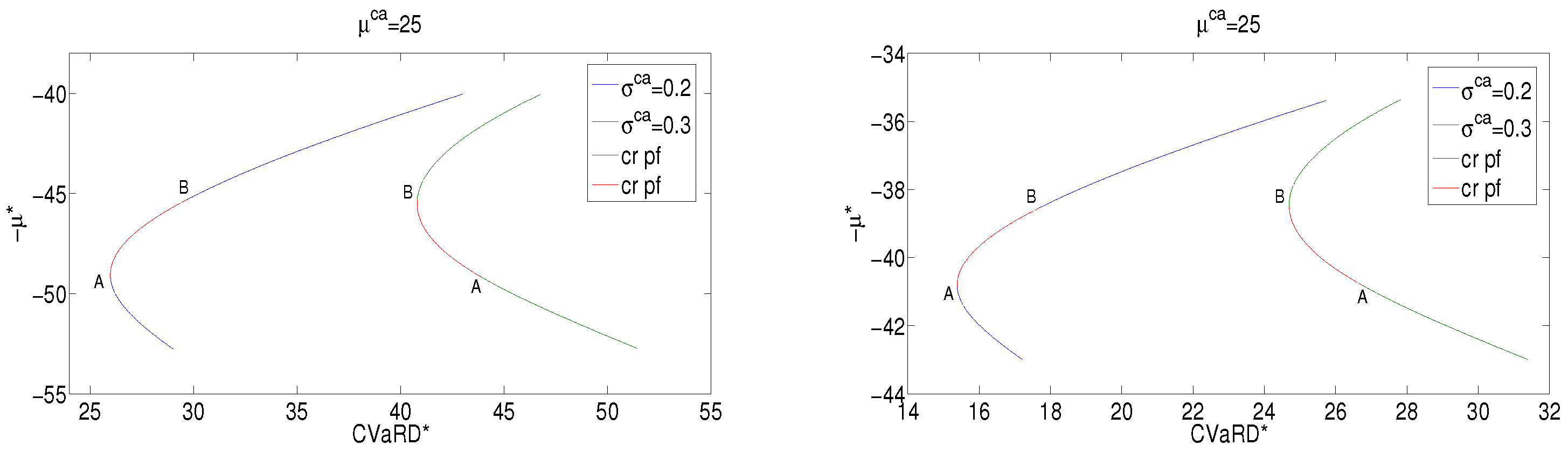

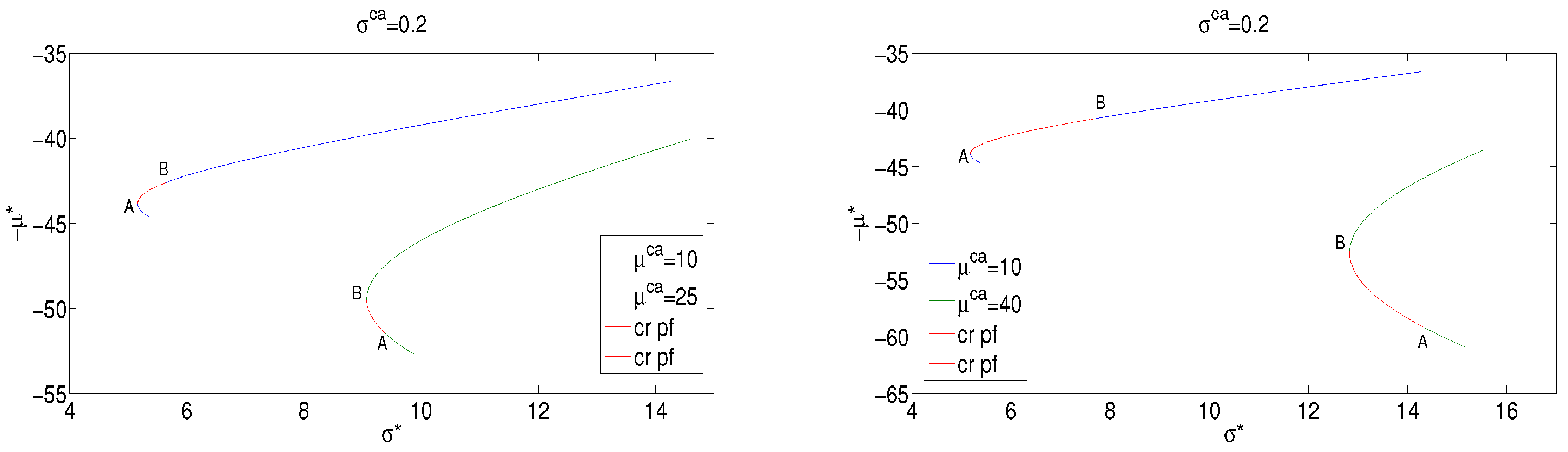

4. CO2 Price Volatility and Emission Management

Economic and Policy Implications

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Data and Sources

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Units | Gas | Coal | Wind | |

|---|---|---|---|---|

| Technology symbol | ga | co | wi | |

| Nominal capacity factor | 87% | 85% | 42% | |

| Heat rate | Btu/kWh | 6600 | 8800 | 0 |

| Overnight cost | $/kW | 956 | 3558 | 1644 |

| Fixed O&M costs | $/kW/year | 10.76 | 41.19 | 45.98 |

| Variable O&M costs | mills/kWh | 3.42 | 4.50 | 0 |

| CO2 intensity | Kg-C/mmBtu | 14.5 | 25.8 | 0 |

| Fuel real escalation rate | 2.0% | 0.3% | 0 | |

| Construction period | # of years | 3 | 4 | 3 |

| Plant life | # of years | 30 | 30 | 30 |

References

- Markowitz, H. Porfolio Selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Awerbuch, S.; Berger, M. Applying Portfolio Theory to EU Electricity Planning and Policy-Making; IEA/EET Working Paper EET/2003/03; International Energy Agency: Paris, France, 2003. [Google Scholar]

- DeLlano-Paz, F.; Calvo-Silvosa, A.; Iglesias, S.; Soares, I. Energy planning and modern portfolio theory: A review. Renew. Sustain. Energy Rev. 2017, 77, 636–651. [Google Scholar] [CrossRef]

- Joskow, P.L. Comparing the costs of intermittent and dispatchable electricity generating technologies. Am. Econ. Rev. 2011, 101, 238–241. [Google Scholar] [CrossRef]

- Reichelstein, S.; Sahoo, A. Time of day pricing and the levelized cost of intermittent power generation. Energy Econ. 2015, 48, 97–108. [Google Scholar] [CrossRef]

- Gómez Sánchez, M.; Macia, Y.M.; Fernández Gil, A.; Castro, C.; Nuñez González, S.M.; Pedrera Yanes, J. A Mathematical Model for the Optimization of Renewable Energy Systems. Mathematics 2021, 9, 39. [Google Scholar] [CrossRef]

- Hittinger, E.; Whitacre, J.F.; Apt, J. Compensating for wind variability using co-located natural gas generation and energy storage. Energy Syst. 2010, 1, 417–439. [Google Scholar] [CrossRef]

- Roy, S. Uncertainty of optimal generation cost due to integration of renewable energy sources. Energy Syst. 2016, 7, 365–389. [Google Scholar] [CrossRef]

- Jin, S.; Ryan, S.M.; Watson, J.P.; Woodruff, D.L. Modeling and solving a large-scale generation expansion planning problem under uncertainty. Energy Syst. 2011, 2, 209–242. [Google Scholar] [CrossRef]

- Camargo, L.A.S.; Leonel, L.D.; Ramos, D.S.; Deri Stucchi, A.G. A Risk Averse Stochastic Optimization Model for Wind Power Plants Portfolio Selection. In Proceedings of the International Conference on Smart Energy Systems and Technologies (SEST), Istanbul, Turkey, 7–9 September 2020; pp. 1–6. [Google Scholar] [CrossRef]

- Tao, Y.; Luo, X.; Wu, Y.; Zhang, L.; Liu, Y.; Xu, C. Portfolio selection of power generation projects considering the synergy of project and uncertainty of decision information. Comput. Ind. Eng. 2023, 175, 108896. [Google Scholar] [CrossRef]

- Glensk, B.; Madlener, R. Multi-period portfolio optimization of power generation assets. Oper. Res. Decis. 2013, 23, 31–38. [Google Scholar]

- Roques, F.A.; Newbery, D.M.; Nuttall, W.J.; William, J. Fuel mix diversification incentives in liberalized electricity markets: A meanâ-variance portfolio theory approach. Energy Econ. 2008, 30, 1831–1849. [Google Scholar] [CrossRef]

- Mari, C. Stochastic NPV Based vs Stochastic LCOE Based Power Portfolio Selection Under Uncertainty. Energies 2020, 13, 3677. [Google Scholar] [CrossRef]

- Mari, C. Hedging electricity price volatility using nuclear power. Appl. Energy 2014, 113, 615–621. [Google Scholar] [CrossRef]

- Liu, M.; Wu, F.F. Portfolio optimization in electricity markets. Electr. Power Syst. Res. 2007, 77, 1000–1009. [Google Scholar] [CrossRef]

- Rocha, P.; Khun, D. Multistage stochastic portfolio optimisation in deregulated electricity markets using linear decision rules. Eur. J. Oper. Res. 2012, 216, 397–408. [Google Scholar] [CrossRef]

- Sen, S.; Yu, L.; Genc, T. A stochastic programming approach to power portfolio optimization. Oper. Res. 2006, 54, 55–72. [Google Scholar] [CrossRef]

- Glensk, B.; Madlener, R. Fuzzy Portfolio Optimization of Power Generation Assets. Energies 2018, 11, 3043. [Google Scholar] [CrossRef]

- Sarykalin, S.; Serraino, G.; Uryasev, S. Value-At-Risk vs. Conditional Value-At-Risk in risk management and optimization. INFORMS TutORials Oper. Res. 2014, 270–294. [Google Scholar] [CrossRef]

- Rockafellar, R.T.; Uryasev, S. The fundamental risk quadrangle in risk management, optimization and statistical estimation. Surv. Oper. Res. Manag. Sci. 2013, 18, 33–53. [Google Scholar] [CrossRef]

- Hatami, A.R.; Seifi, H.; Sheikh-El-Eslami, M. Optimal selling price and energy procurement strategies for a retailer in an electricity market. Electr. Power Syst. Res. 2009, 79, 246–254. [Google Scholar] [CrossRef]

- Lucheroni, C.; Mari, C. CO2 Volatility impact on energy portfolio choice: A fully stochastic LCOE theory analysis. Appl. Energy 2017, 190, 278–290. [Google Scholar] [CrossRef]

- Delarue, E.; Van den Bergh, K. Carbon mitigation in the electric power sector under cap-and-trade and renewables policies. Energy Policy 2016, 92, 34–44. [Google Scholar] [CrossRef]

- Delarue, E.; Van den Bergh, K. Quantifying CO2 abatement cost in the power sector. Energy Policy 2015, 80, 88–97. [Google Scholar]

- Zhang, F.; Zhang, Z. The tail dependence of the carbon markets: The implication of portfolio management. PLoS ONE 2020, 15, 0238033. [Google Scholar] [CrossRef]

- Alabugin, A.; Osintsev, K.; Aliukov, S.; Almetova, Z.; Bolkov, Y. Mathematical Foundations for Modeling a Zero-Carbon Electric Power System in Terms of Sustainability. Mathematics 2023, 11, 2180. [Google Scholar] [CrossRef]

- Hanson, D.; Schmalzer, D.; Nichols, C.; Balash, P. The impacts of meeting a tight CO2 performance standard on the electric power sector. Energy Econ. 2016, 60, 476–485. [Google Scholar] [CrossRef]

- Lv, X.; Li, X.; Jia, D.; Shen, Z. Collaborative optimization for multipath coal-fired power project transition and renewable energy power project portfolio selection considering capacity payment and CCER. Appl. Energy 2025, 381, 125147. [Google Scholar] [CrossRef]

- Feng, Z.H.; Zou, L.L.; Wei, Y.M. Carbon price volatility: Evidence from EU ETS. Appl. Energy 2011, 88, 590–598. [Google Scholar] [CrossRef]

- Balietti, A.C. Trader types and volatility of emission allowance prices. Evidence from EU ETS Phase I. Energy Policy 2016, 98, 607–620. [Google Scholar] [CrossRef]

- Gargallo, P.; Lample, L.; Miguel, J.A.; Salvador, M. Co-Movements between Eu Ets and the Energy Markets: A Var-Dcc-Garch Approach. Mathematics 2021, 9, 1787. [Google Scholar] [CrossRef]

- Nanduri, V.; Kazemzadeh, N. A survey of carbon market mechanisms and models. In Handbook of CO2 in Power Systems; Springer: Berlin/Heidelberg, Germany, 2012; pp. 89–106. [Google Scholar]

- Yang, M.; Blyth, W.; Bradley, R.; Bunn, D.; Clarke, C.; Wilson, T. Evaluating the power investment options with uncertainty in climate policy. Energy Econ. 2008, 30, 1933–1950. [Google Scholar] [CrossRef]

- Kiriyama, E.; Suzuki, A. Use of real options in nuclear power plant valuation in the presence of uncertainty with CO2 emission credit. J. Nucl. Sci. Technol. 2004, 41, 756–764. [Google Scholar] [CrossRef]

- Reedman, L.; Graham, P.; Coombes, P. Using a Real Options Approach to Model Technology Adoption Under Carbon Price Uncertainty: An Application to the Australian Electricity Generation Sector. Econ. Rec. 2006, 82, 64–73. [Google Scholar] [CrossRef]

- García-Martos, C.; Rodríguez, J.; Sánchez, M.J. Modelling and forecasting fossil fuels, CO2 and electricity prices and their volatilities. Appl. Energy 2013, 101, 363–375. [Google Scholar] [CrossRef]

- Rundo, F.; Trenta, F.; Di Stallo, A.L.; Battiato, S. Machine Learning for quantitative finance applications: A survey. Appl. Sci. 2019, 9, 5574–5593. [Google Scholar] [CrossRef]

- Yu, P.; Yan, X. Stock price prediction based on deep neural networks. Neural Comput. Appl. 2020, 32, 1609–1628. [Google Scholar] [CrossRef]

- Sezer, O.B.; Gudelek, M.U.; Ozbayoglu, A.M. Financial time series forecasting with deep learning: A systematic literature review: 2005–2019. Appl. Soft Comput. 2020, 90, 106181. [Google Scholar] [CrossRef]

- Torres, J.F.; Hadjout, D.; Sebaa, A.; Martínez-Álvarez, F.; Troncoso, A. Deep Learning for Time Series Forecasting: A Survey. Big Data 2021, 9, 3–21. [Google Scholar] [CrossRef]

- Wong, W.K.; Xia, M.; Chu, W.C. Adaptive neural networks models for time-series forecasting. Eur. J. Oper. Res. 2010, 207, 807–816. [Google Scholar] [CrossRef]

- Che, Z.; Purushotham, S.; Cho, K.; Sontag, D.; Liu, Y. Recurrent Neural Networks for Multivariate Time Series with Missing Values. Sci. Rep. 2018, 8, 6085. [Google Scholar] [CrossRef]

- Mari, C.; Mari, E. Stochastic DNN-based models meet hidden Markov models: A challenge on natural gas prices at the Henry Hub. Neural Comput. Appl. 2025. [Google Scholar]

- EC. Guide to Cost-Benefit Analysis of Investment Projects; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Mari, C. Power system portfolio selection under uncertainty. Energy Syst. 2019, 10, 321–353. [Google Scholar] [CrossRef]

- EIA. Annual Energy Outlook 2016; U.S. Energy Information Administration, Department of Energy: Washington, DC, USA, 2016. [Google Scholar]

- EIA. Capital Cost Estimates for Utility Scale Electricity Generating Plants; U.S. Energy Information Administration, Department of Energy: Washington, DC, USA, 2016.

- EIA. Levelized Cost and Levelized Avoided Cost of New Generation Resources in the Annual Energy Outlook 2016; U.S. Energy Information Administration, Department of Energy: Washington, DC, USA, 2016. [Google Scholar]

- Mari, C. CO2 price volatility effects on optimal power system portfolios. Energies 2018, 11, 1903. [Google Scholar] [CrossRef]

- Stacy, T.F.; Taylor, G. The Levelized Cost of Electricity From Existing Generation Resources; Institute for Energy Research: Washington, DC, USA, 2015. [Google Scholar]

- Taylor, G.; Tanton, T. The Hidden Costs of Wind Electricity; American Tradition Institute: Washington, DC, USA, 2012. [Google Scholar]

- Angrist, J.D.; Pischke, J.-S. Quantile Regression. In Mostly Harmless Econometrics: An Empiricist’s Companion; Princeton University: Princeton, NJ, USA, 2009. [Google Scholar]

- Mari, C.; Mari, E. Gaussian clustering and jump-diffusion models of electricity prices: A deep learning analysis. Decis. Econ. Financ. 2021, 44, 1039–1062. [Google Scholar] [CrossRef]

- Gu, J.; Wang, Z.; Kuen, J.; Ma, L.; Shahroudy, A.; Shuai, B.; Liu, T.; Wang, X.; Wang, G.; Cai, J.; et al. Recent advances in convolutional neural networks. Pattern Recognit. 2018, 77, 354–377. [Google Scholar] [CrossRef]

- Ren, H.; Cromwell, E.; Kravitz, B.; Chen, X. Technical note: Using long short-term memory models to fill data gaps in hydrological monitoring networks. Hydrol. Earth. Syst. Sci. Discuss. 2022, 26, 1727–1743. [Google Scholar] [CrossRef]

- NREL. Renewable Electricity Futures Study; National Renewable Energy Laboratory: Washington, DC, USA, 2012.

- IEA. IEA Wind—2023 Annual Report; International Energy Agency: Paris, France, 2023. [Google Scholar]

- IEA-NEA. Projected Costs of Generating Electricity—2020 Edition; International Energy Agency—Nuclear Energy Agency: Paris, France, 2020. [Google Scholar]

- Steinbach, J.; Staniaszek, D. Discounting Rates in Energy System Analysis; Fraunhofer ISI, BPIE: Brussels, Belgium, 2015. [Google Scholar]

| Layer | Parameters |

|---|---|

| Input | shape = |

| Embedding | input_dim = 40,000, output_dim = 100, input_length = |

| Convolutional | filters = 128, kernel_size = 5, activation = ReLU |

| MaxPooling | pool_size = 2 |

| Convolutional | filters = 64, kernel_size = 5, activation = ReLU |

| MaxPooling | pool_size = 2 |

| LSTM | units = 256, dropout = 0.2 |

| LSTM | units = 128, dropout = 0.1 |

| Dense | units = , activation = Softmax |

| Technology | ||||

|---|---|---|---|---|

| 0 | wi | 40% | 40% | 40% |

| ga | 6% | 6% | 6% | |

| co | 54% | 54% | 54% | |

| 0.470 | 0.470 | 0.470 | ||

| 0.20 | wi | 40% | 40% | 40% |

| ga | 8% | 18% | 31% | |

| co | 52% | 42% | 29% | |

| 0.461 | 0.413 | 0.350 | ||

| 0.30 | wi | 40% | 40% | 40% |

| ga | 13% | 39% | 59% | |

| co | 47% | 21% | 1% | |

| 0.437 | 0.312 | 0.215 |

| Technology | ||||

|---|---|---|---|---|

| 0 | wi | 40% | 40% | 40% |

| ga | 6% | 6% | 6% | |

| co | 54% | 54% | 54% | |

| 0.470 | 0.470 | 0.470 | ||

| 0.20 | wi | 40% | 40% | 40% |

| ga | 9% | 19% | 32% | |

| co | 51% | 41% | 28% | |

| 0.456 | 0.408 | 0.345 | ||

| 0.30 | wi | 40% | 40% | 40% |

| ga | 14% | 37% | 58% | |

| co | 46% | 23% | 2% | |

| 0.432 | 0.321 | 0.220 |

| Technology | |||||

|---|---|---|---|---|---|

| wi | 40% | 40% | 40% | 40% | 40% |

| ga | 10% | 21% | 31% | 41% | 52% |

| co | 50% | 39% | 29% | 19% | 8% |

| 0 | 10 | 35.9 | 4.2 |

| 25 | 39.4 | 4.2 | |

| 40 | 42.9 | 4.2 | |

| 0.2 | 10 | 35.9 | 4.6 |

| 25 | 39.4 | 5.8 | |

| 40 | 42.9 | 7.7 | |

| 0.3 | 10 | 35.9 | 5.2 |

| 25 | 39.4 | 8.8 | |

| 40 | 42.9 | 12.4 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mari, C.; Lucheroni, C.; Sinha, N.; Mari, E. Power System Portfolio Selection and CO2 Emission Management Under Uncertainty Driven by a DNN-Based Stochastic Model. Mathematics 2025, 13, 1477. https://doi.org/10.3390/math13091477

Mari C, Lucheroni C, Sinha N, Mari E. Power System Portfolio Selection and CO2 Emission Management Under Uncertainty Driven by a DNN-Based Stochastic Model. Mathematics. 2025; 13(9):1477. https://doi.org/10.3390/math13091477

Chicago/Turabian StyleMari, Carlo, Carlo Lucheroni, Nabangshu Sinha, and Emiliano Mari. 2025. "Power System Portfolio Selection and CO2 Emission Management Under Uncertainty Driven by a DNN-Based Stochastic Model" Mathematics 13, no. 9: 1477. https://doi.org/10.3390/math13091477

APA StyleMari, C., Lucheroni, C., Sinha, N., & Mari, E. (2025). Power System Portfolio Selection and CO2 Emission Management Under Uncertainty Driven by a DNN-Based Stochastic Model. Mathematics, 13(9), 1477. https://doi.org/10.3390/math13091477