Dynamic Volatility Spillover Effects and Portfolio Strategies among Crude Oil, Gold, and Chinese Electricity Companies

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Dynamic Conditional Correlation

3.2. Volatility Spillover Effects

3.3. Hedge Ratios and Portfolio Weights

4. Data

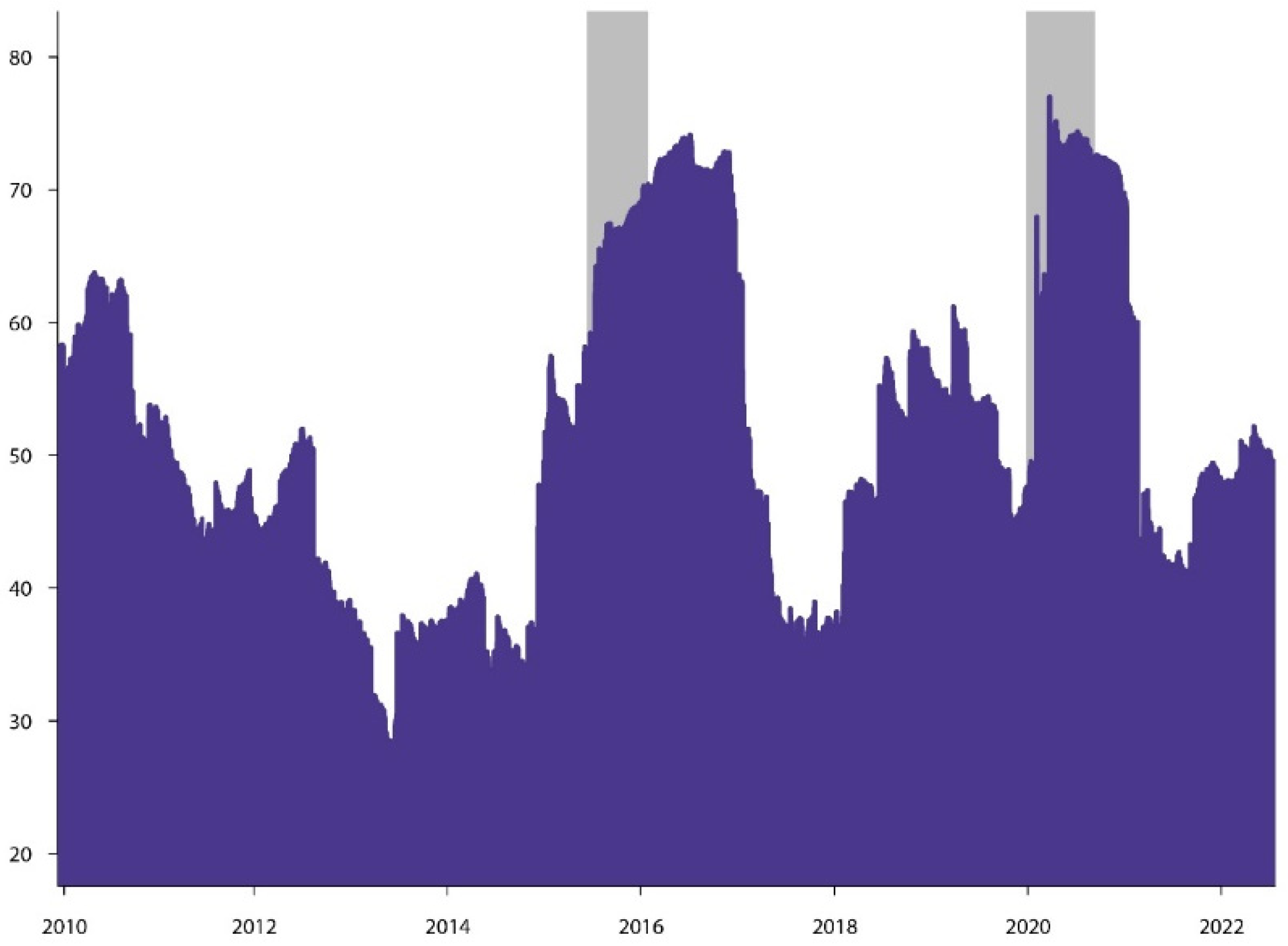

5. Empirical Results

5.1. Volatility Co-Movements

5.2. Portfolio Strategies

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Han, L.; Kordzakhia, N.; Trück, S. Volatility spillovers in Australian electricity markets. Energy Econ. 2020, 90, 104782. [Google Scholar] [CrossRef]

- Zhang, S.; Andrews-Speed, P.; Li, S. To what extent will China’s ongoing electricity market reforms assist the integration of renewable energy? Energy Policy 2018, 114, 165–172. [Google Scholar] [CrossRef]

- Li, Z.; Zou, F.; Mo, B. Does mandatory CSR disclosure affect enterprise total factor productivity? Ekon. Istraz. 2022, 35, 4902–4921. [Google Scholar] [CrossRef]

- Lin, J.; Kahrl, F.; Yuan, J.; Chen, Q.; Liu, X. Economic and carbon emission impacts of electricity market transition in China: A case study of Guangdong Province. Appl. Energy 2019, 238, 1093–1107. [Google Scholar] [CrossRef]

- Zheng, X.; Menezes, F.; Nepal, R. In between the state and the market: An empirical assessment of the early achievements of China’s 2015 electricity reform. Energy Econ. 2021, 93, 105003. [Google Scholar] [CrossRef]

- Mo, B.; Li, Z.; Meng, J. The dynamics of carbon on green energy equity investment: Quantile-on-quantile and quantile coherency approaches. Environ. Sci. Pollut. Res. 2022, 29, 5912–5922. [Google Scholar] [CrossRef]

- Liu, L. The Driving Force of CO2 Reduction in China’s Industries. Financ. Econ. Lett. 2022, 1, 33–39. [Google Scholar] [CrossRef]

- Zhao, X.; Zhong, Z.; Gan, C.; Yan, F.; Zhang, S. What is the appropriate pricing mechanism for China’s renewable energy in a new era? Comput. Ind. Eng. 2022, 163, 107830. [Google Scholar] [CrossRef]

- Gohli, H. High-voltage steering: China’s energy market reforms, industrial policy tools and the 2021 electricity crisis. Energy Res. Soc. Sci. 2022, 93, 102851. [Google Scholar] [CrossRef]

- Liu, H.; Zhang, Z.; Chen, Z.-M.; Dou, D. The impact of China’s electricity price deregulation on coal and power industries: Two-stage game modeling. Energy Policy 2019, 134, 110957. [Google Scholar] [CrossRef]

- Nardo, M.; Ossola, E.; Papanagiotou, E. Financial integration in the EU28 equity markets: Measures and drivers. J. Financ. Mark. 2022, 57, 100633. [Google Scholar] [CrossRef]

- Mensi, W.; Yousaf, I.; Vo, X.V.; Kang, S.H. Asymmetric spillover and network connectedness between gold, BRENT oil and EU subsector markets. J. Int. Financ. Mark. Inst. Money 2022, 76, 101487. [Google Scholar] [CrossRef]

- Jin, J.; Yu, J.; Hu, Y.; Shang, Y. Which one is more informative in determining price movements of hedging assets? Evidence from Bitcoin, gold and crude oil markets. Phys. A Stat. Mech. Its Appl. 2019, 527, 121121. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Oliyide, J.A.; Oduyemi, G.O. How COVID-19 upturns the hedging potentials of gold against oil and stock markets risks: Nonlinear evidences through threshold regression and markov-regime switching models. Resour. Policy 2021, 70, 101926. [Google Scholar] [CrossRef]

- Dutta, A.; Das, D.; Jana, R.; Vo, X.V. COVID-19 and oil market crash: Revisiting the safe haven property of gold and Bitcoin. Resour. Policy 2020, 69, 101816. [Google Scholar] [CrossRef]

- Basher, S.A.; Sadorsky, P. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Econ. 2016, 54, 235–247. [Google Scholar] [CrossRef]

- Xu, S.; Du, Z.; Zhang, H. Can Crude Oil Serve as a Hedging Asset for Underlying Securities?—Research on the Heterogenous Correlation between Crude Oil and Stock Index. Energies 2020, 13, 3139. [Google Scholar] [CrossRef]

- Kang, S.; Hernandez, J.A.; Sadorsky, P.; McIver, R. Frequency spillovers, connectedness, and the hedging effectiveness of oil and gold for US sector ETFs. Energy Econ. 2021, 99, 105278. [Google Scholar] [CrossRef]

- Naeem, M.A.; Hasan, M.; Arif, M.; Suleman, M.T.; Kang, S.H. Oil and gold as a hedge and safe-haven for metals and agricultural commodities with portfolio implications. Energy Econ. 2022, 105, 105758. [Google Scholar] [CrossRef]

- Engle, R. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Hassan, K.; Hoque, A.; Gasbarro, D. Separating BRIC using Islamic stocks and crude oil: Dynamic conditional correlation and volatility spillover analysis. Energy Econ. 2019, 80, 950–969. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef]

- Wen, F.; Cao, J.; Liu, Z.; Wang, X. Dynamic volatility spillovers and investment strategies between the Chinese stock market and commodity markets. Int. Rev. Financ. Anal. 2021, 76, 101772. [Google Scholar] [CrossRef]

- Antonakakis, N.; Cunado, J.; Filis, G.; Gabauer, D.; De Gracia, F.P. Oil volatility, oil and gas firms and portfolio diversification. Energy Econ. 2018, 70, 499–515. [Google Scholar] [CrossRef]

- Dai, Z.; Zhu, H. Time-varying spillover effects and investment strategies between WTI crude oil, natural gas and Chinese stock markets related to belt and road initiative. Energy Econ. 2022, 108, 105883. [Google Scholar] [CrossRef]

- Thanh, T.T.; Linh, V.M. An exploration of sources of volatility in the energy market: An application of a TVP-VAR extended joint connected approach. Sustain. Energy Technol. Assess. 2022, 53, 102448. [Google Scholar]

- Souhir, B.A.; Heni, B.; Lotfi, B. Price risk and hedging strategies in Nord Pool electricity market evidence with sector indexes. Energy Econ. 2019, 80, 635–655. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yılmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econ. 2014, 182, 119–134. [Google Scholar] [CrossRef]

- Ji, Q.; Zhang, D.; Geng, J.-B. Information linkage, dynamic spillovers in prices and volatility between the carbon and energy markets. J. Clean. Prod. 2018, 198, 972–978. [Google Scholar] [CrossRef]

- Ji, Q.; Xia, T.; Liu, F.; Xu, J.-H. The information spillover between carbon price and power sector returns: Evidence from the major European electricity companies. J. Clean. Prod. 2019, 208, 1178–1187. [Google Scholar] [CrossRef]

- Naeem, M.A.; Peng, Z.; Suleman, M.T.; Nepal, R.; Shahzad, S.J.H. Time and frequency connectedness among oil shocks, electricity and clean energy markets. Energy Econ. 2020, 91, 104914. [Google Scholar] [CrossRef]

- Liu, T.; He, X.; Nakajima, T.; Hamori, S. Influence of fluctuations in fossil fuel commodities on electricity markets: Evidence from spot and futures markets in Europe. Energies 2020, 13, 1900. [Google Scholar] [CrossRef]

- Zhang, W.; He, X.; Nakajima, T.; Hamori, S. How does the spillover among natural gas, crude oil, and electricity utility stocks change over time? Evidence from North America and Europe. Energies 2020, 13, 727. [Google Scholar] [CrossRef]

- Guo, H.; Davidson, M.R.; Chen, Q.; Zhang, D.; Jiang, N.; Xia, Q.; Kang, C.; Zhang, X. Power market reform in China: Motivations, progress, and recommendations. Energy Policy 2020, 145, 111717. [Google Scholar] [CrossRef]

- Xin-gang, Z.; Shu-ran, H. Does market-based electricity price affect China’s energy efficiency? Energy Econ. 2020, 91, 104909. [Google Scholar] [CrossRef]

- Wang, Z.; Gao, X.; An, H.; Tang, R.; Sun, Q. Identifying influential energy stocks based on spillover network. Int. Rev. Financ. Anal. 2020, 68, 101277. [Google Scholar] [CrossRef]

- Si, D.-K.; Li, X.-L.; Xu, X.; Fang, Y. The risk spillover effect of the COVID-19 pandemic on energy sector: Evidence from China. Energy Econ. 2021, 102, 105498. [Google Scholar] [CrossRef]

- Vardar, G.; Coşkun, Y.; Yelkenci, T. Shock transmission and volatility spillover in stock and commodity markets: Evidence from advanced and emerging markets. Eurasian Econ. Rev. 2018, 8, 231–288. [Google Scholar] [CrossRef]

- Ali, S.; Bouri, E.; Czudaj, R.L.; Shahzad, S.J.H. Revisiting the valuable roles of commodities for international stock markets. Resour. Policy 2020, 66, 101603. [Google Scholar] [CrossRef]

- Ahmed, A.D.; Huo, R. Volatility transmissions across international oil market, commodity futures and stock markets: Empirical evidence from China. Energy Econ. 2021, 93, 104741. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Ugolini, A.; Hernandez, J.A. Dynamic spillovers and network structure among commodity, currency, and stock markets. Resour. Policy 2021, 74, 102266. [Google Scholar] [CrossRef]

- Morema, K.; Bonga-Bonga, L. The impact of oil and gold price fluctuations on the South African equity market: Volatility spillovers and financial policy implications. Resour. Policy 2020, 68, 101740. [Google Scholar] [CrossRef]

- Maitra, D.; Chandra, S.; Dash, S.R. Liner shipping industry and oil price volatility: Dynamic connectedness and portfolio diversification. Transp. Res. Part E Logist. Transp. Rev. 2020, 138, 101962. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Naeem, M.A.; Peng, Z.; Bouri, E. Asymmetric volatility spillover among Chinese sectors during COVID-19. Int. Rev. Financ. Anal. 2021, 75, 101754. [Google Scholar] [CrossRef]

- Awan, T.M.; Khan, M.S.; Haq, I.U.; Kazmi, S. Oil and stock markets volatility during pandemic times: A review of G7 countries. Green Financ. 2021, 3, 15–27. [Google Scholar] [CrossRef]

- Wu, Y.; Ma, S. Impact of COVID-19 on energy prices and main macroeconomic indicators—evidence from China’s energy market. Green Financ. 2021, 3, 383–402. [Google Scholar] [CrossRef]

- Jareño, F.; González Pérez, M.d.l.O.; Belmonte, P. Asymmetric interdependencies between cryptocurrency and commodity markets: The COVID-19 pandemic impact. Quant. Financ. Econ. 2022, 6, 83–112. [Google Scholar] [CrossRef]

- Gates, B. Responding to COVID-19—A once-in-a-century pandemic? N. Engl. J. Med. 2020, 382, 1677–1679. [Google Scholar] [CrossRef]

- Norouzi, N.; de Rubens, G.Z.; Choupanpiesheh, S.; Enevoldsen, P. When pandemics impact economies and climate change: Exploring the impacts of COVID-19 on oil and electricity demand in China. Energy Res. Soc. Sci. 2020, 68, 101654. [Google Scholar] [CrossRef]

- Hosseini, S.E. An outlook on the global development of renewable and sustainable energy at the time of COVID-19. Energy Res. Soc. Sci. 2020, 68, 101633. [Google Scholar] [CrossRef]

- Zhang, H.; Chen, J.; Shao, L. Dynamic spillovers between energy and stock markets and their implications in the context of COVID-19. Int. Rev. Financ. Anal. 2021, 77, 101828. [Google Scholar] [CrossRef]

- Zhang, H.; Jin, C.; Bouri, E.; Gao, W.; Xu, Y. Realized higher-order moments spillovers between commodity and stock markets: Evidence from China. J. Commod. Mark. 2022, 100275. [Google Scholar] [CrossRef]

- Dai, Z.; Zhu, H.; Zhang, X. Dynamic spillover effects and portfolio strategies between crude oil, gold and Chinese stock markets related to new energy vehicle. Energy Econ. 2022, 109, 105959. [Google Scholar] [CrossRef]

- Zhu, J.; Song, Q.; Streimikiene, D. Multi-Time Scale Spillover Effect of International Oil Price Fluctuation on China’s Stock Markets. Energies 2020, 13, 4641. [Google Scholar] [CrossRef]

- Bouri, E.; Chen, Q.; Lien, D.; Lv, X. Causality between oil prices and the stock market in China: The relevance of the reformed oil product pricing mechanism. Int. Rev. Econ. Financ. 2017, 48, 34–48. [Google Scholar] [CrossRef]

- Mensi, W.; Vo, X.V.; Kang, S.H. Precious metals, oil, and ASEAN stock markets: From global financial crisis to global health crisis. Resour. Policy 2021, 73, 102221. [Google Scholar] [CrossRef]

- Wang, H.; Li, S. Asymmetric volatility spillovers between crude oil and China’s financial markets. Energy 2021, 233, 121168. [Google Scholar] [CrossRef]

- Peng, X. Do precious metals act as hedges or safe havens for China’s financial markets? Financ. Res. Lett. 2020, 37, 101353. [Google Scholar] [CrossRef]

- Zhang, Y.; Wang, M.; Xiong, X.; Zou, G. Volatility spillovers between stock, bond, oil, and gold with portfolio implications: Evidence from China. Financ. Res. Lett. 2021, 40, 101786. [Google Scholar] [CrossRef]

- Bouri, E.; Roubaud, D.; Jammazi, R.; Assaf, A. Uncovering frequency domain causality between gold and the stock markets of China and India: Evidence from implied volatility indices. Financ. Res. Lett. 2017, 23, 23–30. [Google Scholar] [CrossRef]

- Hsiao, C.Y.-L.; Lin, W.; Wei, X.; Yan, G.; Li, S.; Sheng, N. The impact of international oil prices on the stock price fluctuations of China’s renewable energy enterprises. Energies 2019, 12, 4630. [Google Scholar] [CrossRef]

- Qu, F.; Chen, Y.; Zheng, B. Is new energy driven by crude oil, high-tech sector or low-carbon notion? New evidence from high-frequency data. Energy 2021, 230, 120770. [Google Scholar] [CrossRef]

- Kroner, K.F.; Sultan, J. Time-varying distributions and dynamic hedging with foreign currency futures. J. Financ. Quant. Anal. 1993, 28, 535–551. [Google Scholar] [CrossRef]

- Kroner, K.F.; Ng, V.K. Modeling asymmetric comovements of asset returns. Rev. Financ. Stud. 1998, 11, 817–844. [Google Scholar] [CrossRef]

- Ku, Y.-H.H.; Chen, H.-C.; Chen, K.-H. On the application of the dynamic conditional correlation model in estimating optimal time-varying hedge ratios. Appl. Econ. Lett. 2007, 14, 503–509. [Google Scholar] [CrossRef]

- Chang, C.-L.; McAleer, M.; Tansuchat, R. Crude oil hedging strategies using dynamic multivariate GARCH. Energy Econ. 2011, 33, 912–923. [Google Scholar] [CrossRef]

- Li, Z.; Ao, Z.; Mo, B. Revisiting the valuable roles of global financial assets for international stock markets: Quantile coherence and causality-in-quantiles approaches. Mathematics 2021, 9, 1750. [Google Scholar] [CrossRef]

- Li, Z.; Mo, B.; Nie, H. Time and frequency dynamic connectedness between cryptocurrencies and financial assets in China. Int. Rev.Econ. Financ. 2023. [Google Scholar] [CrossRef]

- Assifuah-Nunoo, E.; Junior, P.O.; Adam, A.M.; Bossman, A. Assessing the safe haven properties of oil in African stock markets amid the COVID-19 pandemic: A quantile regression analysis. Quant. Financ. Econ. 2022, 6, 244–269. [Google Scholar] [CrossRef]

- Li, Z.; Chen, L.; Dong, H. What are bitcoin market reactions to its-related events? Int. Rev.Econ. Financ. 2021, 73, 1–10. [Google Scholar] [CrossRef]

- Li, Z.; Chen, H.; Mo, B. Can digital finance promote urban innovation? Evidence from China. Borsa Istanb. Rev. 2022. [Google Scholar] [CrossRef]

- Ming, Z.; Song, X.; Lingyun, L.; Yuejin, W.; Yang, W.; Ying, L. China’s large-scale power shortages of 2004 and 2011 after the electricity market reforms of 2002: Explanations and differences. Energy Policy 2013, 61, 610–618. [Google Scholar] [CrossRef]

- Zhao, S.; Chen, X.; Zhang, J. The systemic risk of China’s stock market during the crashes in 2008 and 2015. Phys. A Stat. Mech. Its Appl. 2019, 520, 161–177. [Google Scholar] [CrossRef]

- Li, J.; Liu, R.; Yao, Y.; Xie, Q. Time-frequency volatility spillovers across the international crude oil market and Chinese major energy futures markets: Evidence from COVID-19. Resour. Policy 2022, 77, 102646. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Choi, S.-Y. Analysis of stock market efficiency during crisis periods in the US stock market: Differences between the global financial crisis and COVID-19 pandemic. Phys. A Stat. Mech. Its Appl. 2021, 574, 125988. [Google Scholar] [CrossRef]

- Ferrer, R.; Shahzad, S.J.H.; López, R.; Jareño, F. Time and frequency dynamics of connectedness between renewable energy stocks and crude oil prices. Energy Econ. 2018, 76, 1–20. [Google Scholar] [CrossRef]

- Zhu, P.; Tang, Y.; Wei, Y.; Lu, T. Multidimensional risk spillovers among crude oil, the US and Chinese stock markets: Evidence during the COVID-19 epidemic. Energy 2021, 231, 120949. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Median | Max | Min | Std.Dev. | Skewness | Kurtosis | Jarque-Bera | ADF | ARCH-LM(10) | Obs. | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| WTI | 1.949 | 1.252 | 85.708 | 0.000 | 3.285 | 12.694 * | 258.704 * | 8,033,535.0 * | −8.108 * | 258.74 * | 2920 |

| HPI | 1.607 | 1.070 | 12.840 | 0.000 | 1.744 | 2.380 * | 10.352 * | 9333.2 * | −8.328 * | 337.1 * | 2920 |

| DTP | 1.520 | 1.006 | 11.244 | 0.000 | 1.691 | 2.498 * | 10.892 * | 10,614.3 * | −9.230 * | 320.17 * | 2920 |

| HDPI | 1.583 | 1.032 | 28.133 | 0.000 | 1.802 | 3.227 * | 24.992 * | 63,915.5 * | −8.901 * | 234.36 * | 2920 |

| SNGY | 1.310 | 0.819 | 10.592 | 0.000 | 1.520 | 2.660 * | 12.544 * | 14,524.2 * | −8.887 * | 491.94 * | 2920 |

| GDG | 1.618 | 1.025 | 33.201 | 0.000 | 1.958 | 3.722 * | 33.278 * | 118,279.3 * | −9.127 * | 240.6 * | 2920 |

| SCTE | 1.458 | 1.014 | 28.250 | 0.000 | 1.610 | 3.863 * | 39.088 * | 165,712.4 * | −9.916 * | 55.786 * | 2920 |

| CYDL | 2.044 | 1.337 | 20.618 | 0.000 | 2.161 | 2.062 * | 8.476 * | 5717.0 * | −8.794 * | 407.51 * | 2920 |

| GDEP | 2.050 | 1.332 | 20.651 | 0.000 | 2.207 | 2.340 * | 10.887 * | 10,234.5 * | −11.083 * | 227.64 * | 2920 |

| CQSXSL | 2.058 | 1.373 | 23.062 | 0.000 | 2.160 | 2.256 * | 10.540 * | 9393.2 * | −9.559 * | 230.69 * | 2920 |

| TFNY | 2.102 | 1.449 | 18.978 | 0.000 | 2.184 | 2.220 * | 9.653 * | 7784.4 * | −9.970 * | 285.41 * | 2920 |

| GZQYDL | 1.528 | 0.999 | 15.804 | 0.000 | 1.727 | 2.585 * | 12.384 * | 13,965.0 * | −8.193 * | 373.77 * | 2920 |

| CDGJ | 1.758 | 1.121 | 20.579 | 0.000 | 1.937 | 2.597 * | 13.750 * | 17,343.4 * | −8.450 * | 275.29 * | 2920 |

| GOLD | 0.683 | 0.485 | 9.443 | 0.000 | 0.729 | 3.225 * | 22.470 * | 51,181.9 * | −10.273 * | 129.78 * | 2920 |

| WTI | HPI | DTP | HDPI | SNGY | GDG | SCTE | CYDL | GDEP | CQSXSL | TFNY | GZQYDL | CDGJ | GOLD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| WTI | 0.107 | 0.097 | 0.138 | 0.085 | 0.124 | 0.105 | 0.069 | 0.094 | 0.143 | 0.129 | 0.125 | 0.097 | 0.209 | |

| HPI | 0.045 | 0.566 | 0.689 | 0.464 | 0.404 | 0.321 | 0.335 | 0.321 | 0.318 | 0.299 | 0.364 | 0.31 | 0.067 | |

| DTP | 0.068 | 0.402 | 0.576 | 0.572 | 0.469 | 0.426 | 0.432 | 0.403 | 0.365 | 0.395 | 0.43 | 0.387 | 0.072 | |

| HDPI | 0.087 | 0.537 | 0.418 | 1 | 0.523 | 0.494 | 0.376 | 0.408 | 0.381 | 0.35 | 0.34 | 0.436 | 0.366 | 0.091 |

| SNGY | 0.106 | 0.319 | 0.418 | 0.385 | 0.507 | 0.471 | 0.418 | 0.407 | 0.401 | 0.39 | 0.46 | 0.434 | 0.094 | |

| GDG | 0.098 | 0.318 | 0.382 | 0.301 | 0.407 | 0.372 | 0.417 | 0.416 | 0.411 | 0.415 | 0.472 | 0.439 | 0.082 | |

| SCTE | 0.052 | 0.252 | 0.329 | 0.321 | 0.344 | 0.315 | 0.339 | 0.314 | 0.318 | 0.314 | 0.442 | 0.37 | 0.119 | |

| CYDL | 0.06 | 0.265 | 0.361 | 0.329 | 0.358 | 0.334 | 0.309 | 0.357 | 0.328 | 0.434 | 0.358 | 0.376 | 0.082 | |

| GDEP | 0.077 | 0.219 | 0.293 | 0.291 | 0.311 | 0.327 | 0.24 | 0.305 | 0.328 | 0.362 | 0.341 | 0.399 | 0.039 | |

| CQSXSL | 0.064 | 0.207 | 0.263 | 0.233 | 0.288 | 0.31 | 0.241 | 0.257 | 0.276 | 0.362 | 0.364 | 0.361 | 0.115 | |

| TFNY | 0.072 | 0.247 | 0.344 | 0.274 | 0.318 | 0.32 | 0.243 | 0.37 | 0.278 | 0.279 | 0.32 | 0.421 | 0.101 | |

| GZQYDL | 0.1 | 0.265 | 0.321 | 0.313 | 0.37 | 0.345 | 0.356 | 0.31 | 0.297 | 0.279 | 0.256 | 0.438 | 0.116 | |

| CDGJ | 0.075 | 0.203 | 0.327 | 0.262 | 0.323 | 0.333 | 0.316 | 0.317 | 0.314 | 0.286 | 0.351 | 0.33 | 0.055 | |

| GOLD | 0.077 | 0.054 | 0.061 | 0.054 | 0.105 | 0.089 | 0.097 | 0.076 | 0.04 | 0.067 | 0.078 | 0.095 | 0.057 |

| WTI | HPI | DTP | HDPI | SNGY | GDG | SCTE | CYDL | GDEP | CQSXSL | TFNY | GZQYDL | CDGJ | GOLD | FROM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Panel(A): Whole period | |||||||||||||||

| WTI | 84.71 | 0.90 | 0.84 | 1.54 | 0.59 | 1.13 | 0.83 | 0.32 | 0.81 | 1.75 | 1.22 | 1.06 | 1.00 | 3.31 | 15.29 |

| HPI | 0.34 | 35.48 | 11.05 | 16.46 | 7.37 | 5.25 | 3.18 | 3.91 | 3.36 | 2.97 | 2.83 | 4.49 | 3.17 | 0.14 | 64.52 |

| DTP | 0.25 | 9.30 | 30.70 | 10.07 | 9.60 | 6.46 | 5.03 | 5.55 | 4.38 | 3.65 | 4.73 | 5.53 | 4.61 | 0.15 | 69.30 |

| HDPI | 0.51 | 14.34 | 9.73 | 30.76 | 8.54 | 6.88 | 4.05 | 4.90 | 4.25 | 3.19 | 3.21 | 5.49 | 3.93 | 0.21 | 69.24 |

| SNGY | 0.16 | 6.13 | 9.80 | 8.10 | 31.35 | 7.60 | 6.05 | 5.20 | 4.62 | 4.29 | 4.61 | 6.30 | 5.55 | 0.23 | 68.65 |

| GDG | 0.39 | 5.21 | 6.83 | 7.74 | 8.29 | 32.94 | 4.13 | 5.39 | 5.49 | 4.89 | 5.41 | 6.75 | 6.32 | 0.21 | 67.06 |

| SCTE | 0.38 | 4.11 | 7.42 | 5.24 | 8.83 | 5.13 | 40.59 | 4.36 | 3.57 | 3.54 | 3.62 | 7.47 | 5.15 | 0.57 | 59.41 |

| CYDL | 0.15 | 3.87 | 6.82 | 6.13 | 6.55 | 6.63 | 4.60 | 39.49 | 4.68 | 3.72 | 7.12 | 4.56 | 5.47 | 0.21 | 60.51 |

| GDEP | 0.37 | 3.90 | 6.36 | 5.68 | 6.44 | 7.01 | 3.58 | 5.07 | 41.41 | 4.05 | 5.24 | 4.46 | 6.38 | 0.05 | 58.59 |

| CQSXSL | 0.76 | 4.08 | 5.37 | 4.58 | 6.57 | 6.81 | 3.87 | 4.40 | 4.26 | 42.59 | 5.19 | 5.58 | 5.44 | 0.50 | 57.41 |

| TFNY | 0.61 | 3.47 | 6.07 | 4.25 | 5.95 | 6.41 | 3.78 | 7.37 | 4.99 | 4.74 | 41.14 | 3.73 | 7.11 | 0.38 | 58.86 |

| GZQYDL | 0.49 | 4.80 | 6.61 | 6.73 | 7.68 | 7.69 | 6.58 | 4.48 | 3.80 | 4.34 | 3.35 | 36.35 | 6.70 | 0.40 | 63.65 |

| CDGJ | 0.27 | 3.42 | 5.35 | 4.60 | 7.19 | 6.96 | 4.95 | 5.11 | 5.78 | 4.53 | 6.26 | 6.64 | 38.83 | 0.11 | 61.17 |

| GOLD | 3.86 | 0.35 | 0.37 | 0.61 | 0.81 | 0.46 | 1.11 | 0.55 | 0.08 | 1.09 | 0.85 | 1.15 | 0.24 | 88.47 | 11.53 |

| Contr. To others | 8.53 | 63.89 | 82.62 | 81.73 | 84.42 | 74.43 | 51.73 | 56.61 | 50.08 | 46.73 | 53.64 | 63.21 | 61.07 | 6.49 | 785.19 |

| Contr. incl. own | 93.25 | 99.37 | 113.33 | 112.49 | 115.77 | 107.37 | 92.32 | 96.10 | 91.49 | 89.32 | 94.77 | 99.56 | 99.90 | 94.96 | TS |

| Net spillovers | −6.75 | −0.63 | 13.33 | 12.49 | 15.77 | 7.37 | −7.68 | −3.90 | −8.51 | −10.68 | −5.23 | −0.44 | −0.10 | −5.04 | 56.08 |

| Panel(B): Chinese stock market crash | |||||||||||||||

| WTI | 74.98 | 0.45 | 0.32 | 3.78 | 0.38 | 5.44 | 0.12 | 2.52 | 1.50 | 2.43 | 3.20 | 0.88 | 1.09 | 2.92 | 25.02 |

| HPI | 0.07 | 15.18 | 10.96 | 9.36 | 8.07 | 4.51 | 9.19 | 7.95 | 6.89 | 5.66 | 6.86 | 7.62 | 7.46 | 0.22 | 84.82 |

| DTP | 0.11 | 11.02 | 15.04 | 7.65 | 10.11 | 4.28 | 8.03 | 8.86 | 7.33 | 5.46 | 7.74 | 7.25 | 6.96 | 0.15 | 84.96 |

| HDPI | 0.95 | 9.47 | 7.66 | 15.96 | 7.75 | 7.85 | 7.62 | 9.50 | 6.18 | 4.95 | 6.13 | 7.73 | 7.97 | 0.29 | 84.04 |

| SNGY | 0.17 | 8.69 | 10.76 | 6.65 | 15.59 | 4.46 | 9.02 | 7.68 | 5.88 | 6.45 | 8.63 | 7.36 | 8.67 | 0.00 | 84.41 |

| GDG | 1.30 | 5.79 | 4.92 | 9.81 | 6.33 | 17.87 | 4.09 | 9.27 | 8.09 | 6.15 | 9.04 | 7.32 | 9.48 | 0.53 | 82.13 |

| SCTE | 0.89 | 11.28 | 10.23 | 7.44 | 10.62 | 2.95 | 17.75 | 6.58 | 7.15 | 5.67 | 5.79 | 7.20 | 6.30 | 0.15 | 82.25 |

| CYDL | 0.51 | 7.93 | 8.30 | 9.40 | 7.41 | 7.73 | 5.82 | 14.04 | 7.00 | 6.65 | 8.66 | 7.91 | 8.55 | 0.11 | 85.96 |

| GDEP | 0.36 | 9.02 | 8.34 | 7.42 | 6.70 | 7.86 | 6.86 | 8.35 | 16.27 | 4.88 | 8.31 | 6.42 | 9.00 | 0.21 | 83.73 |

| CQSXSL | 0.49 | 8.36 | 7.59 | 5.70 | 9.03 | 5.80 | 6.52 | 8.12 | 5.06 | 17.95 | 7.85 | 8.08 | 9.25 | 0.20 | 82.05 |

| TFNY | 0.50 | 7.81 | 8.05 | 6.52 | 9.23 | 7.05 | 5.68 | 9.26 | 7.03 | 6.36 | 15.25 | 6.98 | 10.01 | 0.28 | 84.75 |

| GZQYDL | 0.45 | 8.27 | 7.99 | 8.14 | 7.97 | 6.47 | 6.82 | 8.95 | 5.72 | 6.78 | 7.12 | 16.63 | 8.47 | 0.21 | 83.37 |

| CDGJ | 0.19 | 8.08 | 6.90 | 7.96 | 8.75 | 7.20 | 6.04 | 7.90 | 7.50 | 7.10 | 8.87 | 7.97 | 15.43 | 0.12 | 84.57 |

| GOLD | 0.64 | 1.12 | 0.88 | 1.14 | 0.12 | 1.97 | 0.33 | 0.86 | 0.81 | 0.72 | 0.38 | 0.69 | 0.36 | 90.01 | 9.99 |

| Contr. To others | 6.63 | 97.29 | 92.90 | 90.96 | 92.48 | 73.55 | 76.13 | 95.81 | 76.12 | 69.26 | 88.58 | 83.41 | 93.57 | 5.38 | 1042.07 |

| Contr. incl. own | 81.60 | 112.47 | 107.94 | 106.92 | 108.06 | 91.42 | 93.87 | 109.85 | 92.39 | 87.21 | 103.83 | 100.04 | 109.00 | 95.39 | TS |

| Net spillovers | −18.40 | 12.47 | 7.94 | 6.92 | 8.06 | −8.58 | −6.13 | 9.85 | −7.61 | −12.79 | 3.83 | 0.04 | 9.00 | −4.61 | 74.43 |

| Panel(C): COVID−19 | |||||||||||||||

| WTI | 47.15 | 2.68 | 2.04 | 4.65 | 1.19 | 3.11 | 6.47 | 3.88 | 1.73 | 7.36 | 3.59 | 5.30 | 4.10 | 6.76 | 52.85 |

| HPI | 1.22 | 19.80 | 9.13 | 12.16 | 4.45 | 6.18 | 4.27 | 8.66 | 7.24 | 5.86 | 8.59 | 2.58 | 6.37 | 3.47 | 80.20 |

| DTP | 0.66 | 9.42 | 20.67 | 9.29 | 5.16 | 7.39 | 4.68 | 8.63 | 8.41 | 4.49 | 8.18 | 3.70 | 7.98 | 1.34 | 79.33 |

| HDPI | 1.92 | 12.21 | 8.97 | 19.73 | 4.53 | 5.32 | 4.82 | 8.66 | 6.60 | 6.78 | 7.81 | 4.56 | 5.98 | 2.13 | 80.27 |

| SNGY | 1.02 | 6.00 | 6.85 | 5.94 | 27.33 | 9.48 | 5.46 | 8.33 | 5.97 | 3.82 | 5.20 | 4.07 | 9.17 | 1.36 | 72.67 |

| GDG | 1.79 | 6.95 | 8.29 | 5.90 | 8.25 | 21.81 | 5.39 | 9.15 | 8.17 | 4.93 | 6.40 | 3.22 | 7.81 | 1.92 | 78.19 |

| SCTE | 3.35 | 5.46 | 6.51 | 6.14 | 5.27 | 6.78 | 23.57 | 8.70 | 3.40 | 5.67 | 5.65 | 6.29 | 9.84 | 3.36 | 76.43 |

| CYDL | 1.68 | 7.94 | 7.46 | 7.80 | 6.16 | 8.28 | 5.99 | 18.37 | 5.58 | 7.22 | 8.05 | 4.23 | 8.12 | 3.12 | 81.63 |

| GDEP | 1.73 | 9.79 | 10.67 | 9.22 | 4.77 | 7.68 | 2.87 | 7.69 | 22.06 | 6.00 | 8.06 | 2.03 | 5.88 | 1.56 | 77.94 |

| CQSXSL | 3.98 | 7.31 | 5.03 | 8.35 | 3.59 | 5.18 | 5.38 | 9.95 | 4.24 | 24.46 | 5.97 | 5.24 | 6.79 | 4.53 | 75.54 |

| TFNY | 1.76 | 9.42 | 8.71 | 8.70 | 4.15 | 6.21 | 4.74 | 9.30 | 6.81 | 5.09 | 21.45 | 3.55 | 7.41 | 2.71 | 78.55 |

| GZQYDL | 3.61 | 3.81 | 6.17 | 6.75 | 6.03 | 4.82 | 7.75 | 7.54 | 3.39 | 6.68 | 5.47 | 29.35 | 6.32 | 2.30 | 70.65 |

| CDGJ | 1.51 | 6.89 | 7.80 | 6.14 | 7.25 | 6.98 | 7.75 | 9.40 | 4.82 | 6.00 | 7.14 | 3.59 | 20.98 | 3.76 | 79.02 |

| GOLD | 5.86 | 7.12 | 2.90 | 4.22 | 2.04 | 2.87 | 5.61 | 6.40 | 0.89 | 7.66 | 5.25 | 3.19 | 5.58 | 40.41 | 59.59 |

| Contr. To others | 30.09 | 95.02 | 90.52 | 95.26 | 62.83 | 80.27 | 71.17 | 106.29 | 67.25 | 77.56 | 85.36 | 51.56 | 91.35 | 38.33 | 1042.87 |

| Contr. incl. own | 77.24 | 114.82 | 111.19 | 114.99 | 90.16 | 102.08 | 94.73 | 124.66 | 89.31 | 102.02 | 106.81 | 80.91 | 112.33 | 78.74 | TS |

| Net spillovers | −22.76 | 14.82 | 11.19 | 14.99 | −9.84 | 2.08 | −5.27 | 24.66 | −10.69 | 2.02 | 6.81 | −19.09 | 12.33 | −21.26 | 74.49 |

| Whole Period | HE(%) | Chinese Stock Market Crash | HE(%) | COVID-19 | HE(%) | |

|---|---|---|---|---|---|---|

| Panel A: WTI/stock (long/short) | ||||||

| WTI/HPI | 0.232 | 1.119 | 0.133 | −0.619 | 1.644 | 5.453 |

| WTI/DTP | 0.182 | 0.939 | 0.105 | −0.577 | 1.243 | 3.258 |

| WTI/HDPI | 0.267 | 1.902 | 0.17 | 5.166 | 1.677 | 8.741 |

| WTI/SNGY | 0.232 | 0.673 | 0.112 | −1.49 | 1.423 | 0.981 |

| WTI/GDG | 0.198 | 1.527 | 0.125 | 7.644 | 1.039 | 5.494 |

| WTI/SCTE | 0.21 | 1.094 | 0.099 | −2.29 | 1.634 | 8.599 |

| WTI/CYDL | 0.161 | 0.343 | 0.118 | 3.848 | 1.304 | 6.149 |

| WTI/GDEP | 0.099 | 0.811 | 0.098 | 1.105 | 0.52 | 3.051 |

| WTI/CQSXSL | 0.173 | 1.951 | 0.121 | 2.894 | 1.043 | 11.075 |

| WTI/TFNY | 0.166 | 1.633 | 0.113 | 3.489 | 0.925 | 6.086 |

| WTI/GZQYDL | 0.233 | 1.561 | 0.138 | 1.588 | 1.619 | 8.005 |

| WTI/CDGJ | 0.161 | 0.942 | 0.101 | 1.4 | 1.152 | 5.344 |

| Panel B: stock/WTI (long/short) | ||||||

| HPI/WTI | 0.135 | −1.021 | 0.197 | −0.715 | 0.153 | −38.665 |

| DTP/WTI | 0.104 | −0.163 | 0.147 | −0.376 | 0.116 | −33.215 |

| HDPI/WTI | 0.173 | −1.228 | 0.391 | 5.27 | 0.174 | −58.379 |

| SNGY/WTI | 0.095 | −0.724 | 0.177 | −1.552 | 0.114 | −86.986 |

| GDG/WTI | 0.158 | −0.468 | 0.486 | 7.787 | 0.124 | −61.461 |

| SCTE/WTI | 0.094 | 0.336 | 0.133 | −3.092 | 0.088 | −20.045 |

| CYDL/WTI | 0.146 | −1.854 | 0.282 | 3.915 | 0.152 | −70.722 |

| GDEP/WTI | 0.114 | 0.317 | 0.241 | 0.981 | 0.097 | −7.925 |

| CQSXSL/WTI | 0.18 | 0.314 | 0.3 | 2.77 | 0.201 | −17.646 |

| TFNY/WTI | 0.173 | −0.048 | 0.301 | 3.508 | 0.157 | −26.829 |

| GZQYDL/WTI | 0.134 | −0.125 | 0.309 | −0.067 | 0.109 | −44.203 |

| CDGJ/WTI | 0.123 | −0.299 | 0.294 | 0.798 | 0.128 | −43.394 |

| Whole Period | HE(%) | Chinese Stock Market Crash | HE(%) | COVID-19 | HE(%) | |

|---|---|---|---|---|---|---|

| Panel A: GOLD/stock (long/short) | ||||||

| GOLD/HPI | 0.041 | 0.349 | 0.023 | −0.359 | 0.126 | 13.549 |

| GOLD/DTP | 0.043 | 0.434 | 0.028 | −0.443 | 0.103 | 5.479 |

| GOLD/HDPI | 0.042 | 0.806 | 0.026 | 0.879 | 0.11 | 8.757 |

| GOLD/SNGY | 0.077 | 0.447 | 0.028 | −1.593 | 0.132 | 3.804 |

| GOLD/GDG | 0.055 | 0.233 | 0.028 | 1.406 | 0.117 | 5.525 |

| GOLD/SCTE | 0.065 | 1.366 | 0.031 | −0.321 | 0.149 | 9.226 |

| GOLD/CYDL | 0.044 | 0.428 | 0.025 | −0.03 | 0.106 | 10.161 |

| GOLD/GDEP | 0.019 | 0.123 | 0.015 | −0.277 | 0.039 | 1.056 |

| GOLD/CQSXSL | 0.044 | 1.295 | 0.025 | 0.163 | 0.083 | 12.363 |

| GOLD/TFNY | 0.04 | 0.978 | 0.021 | −0.553 | 0.087 | 8.619 |

| GOLD/GZQYDL | 0.057 | 1.297 | 0.023 | −0.11 | 0.136 | 6.208 |

| GOLD/CDGJ | 0.028 | 0.263 | 0.01 | −0.576 | 0.088 | 7.259 |

| Panel B: stock/GOLD (long/short) | ||||||

| HPI/GOLD | 0.186 | 0.434 | 0.312 | 0.034 | 0.36 | 11.824 |

| DTP/GOLD | 0.204 | 0.487 | 0.35 | 0.206 | 0.254 | 5.241 |

| HDPI/GOLD | 0.215 | 0.821 | 0.55 | 1.113 | 0.321 | 8.651 |

| SNGY/GOLD | 0.265 | 0.778 | 0.48 | −0.839 | 0.207 | 3.887 |

| GDG/GOLD | 0.348 | 0.438 | 0.916 | 1.848 | 0.295 | 7.035 |

| SCTE/GOLD | 0.278 | 1.42 | 0.408 | −0.013 | 0.226 | 11.357 |

| CYDL/GOLD | 0.362 | 0.501 | 0.611 | 0.319 | 0.339 | 13.296 |

| GDEP/GOLD | 0.169 | 0.129 | 0.322 | −0.008 | 0.18 | 1.166 |

| CQSXSL/GOLD | 0.374 | 1.306 | 0.59 | 0.493 | 0.514 | 12.525 |

| TFNY/GOLD | 0.346 | 0.993 | 0.534 | −0.186 | 0.431 | 9.414 |

| GZQYDL/GOLD | 0.274 | 1.335 | 0.526 | −0.259 | 0.225 | 7.095 |

| CDGJ/GOLD | 0.21 | 0.243 | 0.35 | −0.687 | 0.246 | 8.609 |

| Whole Period | HE(%) | Chinese Stock Market Crash | HE(%) | COVID-19 | HE(%) | |

|---|---|---|---|---|---|---|

| Panel A: WTI-stock pair | ||||||

| WTI/HPI | 0.44 | 68.995 | 0.61 | 37.461 | 0.294 | 88.256 |

| WTI/DTP | 0.431 | 70.391 | 0.589 | 36.588 | 0.291 | 89.331 |

| WTI/HDPI | 0.448 | 67.007 | 0.653 | 11.177 | 0.282 | 88.921 |

| WTI/SNGY | 0.345 | 77.132 | 0.625 | 38.142 | 0.22 | 94.033 |

| WTI/GDG | 0.483 | 63.494 | 0.778 | 3.652 | 0.272 | 90.682 |

| WTI/SCTE | 0.394 | 73.203 | 0.604 | 49.211 | 0.176 | 95.311 |

| WTI/CYDL | 0.574 | 56.971 | 0.688 | 19.65 | 0.313 | 87.865 |

| WTI/GDEP | 0.594 | 54.225 | 0.726 | 23.881 | 0.376 | 83.02 |

| WTI/CQSXSL | 0.579 | 54.243 | 0.74 | 21.346 | 0.384 | 79.652 |

| WTI/TFNY | 0.577 | 54.605 | 0.746 | 19.653 | 0.364 | 83.085 |

| WTI/GZQYDL | 0.429 | 69.362 | 0.707 | 31.796 | 0.21 | 93.833 |

| WTI/CDGJ | 0.495 | 63.763 | 0.747 | 24.095 | 0.279 | 89.932 |

| Panel B: GOLD-stock pair | ||||||

| GOLD/HPI | 0.829 | 10.02 | 0.948 | 2.698 | 0.803 | −2.247 |

| GOLD/DTP | 0.827 | 10.758 | 0.943 | 1.006 | 0.75 | 11.774 |

| GOLD/HDPI | 0.836 | 7.543 | 0.955 | −4.196 | 0.802 | 6.157 |

| GOLD/SNGY | 0.761 | 10.139 | 0.948 | 3.513 | 0.57 | 28.835 |

| GOLD/GDG | 0.859 | 6.575 | 0.983 | −1.474 | 0.71 | 24.083 |

| GOLD/SCTE | 0.805 | 8.393 | 0.956 | 3.751 | 0.614 | 27.127 |

| GOLD/CYDL | 0.898 | 5.796 | 0.967 | 0.587 | 0.801 | 8.33 |

| GOLD/GDEP | 0.894 | 7.529 | 0.969 | 1.965 | 0.823 | 15.272 |

| GOLD/CQSXSL | 0.904 | 4.296 | 0.979 | 1.011 | 0.898 | −5.216 |

| GOLD/TFNY | 0.903 | 4.739 | 0.978 | 1.87 | 0.872 | 1.79 |

| GOLD/GZQYDL | 0.828 | 7.059 | 0.973 | 2.712 | 0.657 | 27.406 |

| GOLD/CDGJ | 0.848 | 8.03 | 0.967 | 3.929 | 0.743 | 10.734 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, G.; Meng, J.; Mo, B. Dynamic Volatility Spillover Effects and Portfolio Strategies among Crude Oil, Gold, and Chinese Electricity Companies. Mathematics 2023, 11, 910. https://doi.org/10.3390/math11040910

Wang G, Meng J, Mo B. Dynamic Volatility Spillover Effects and Portfolio Strategies among Crude Oil, Gold, and Chinese Electricity Companies. Mathematics. 2023; 11(4):910. https://doi.org/10.3390/math11040910

Chicago/Turabian StyleWang, Guannan, Juan Meng, and Bin Mo. 2023. "Dynamic Volatility Spillover Effects and Portfolio Strategies among Crude Oil, Gold, and Chinese Electricity Companies" Mathematics 11, no. 4: 910. https://doi.org/10.3390/math11040910

APA StyleWang, G., Meng, J., & Mo, B. (2023). Dynamic Volatility Spillover Effects and Portfolio Strategies among Crude Oil, Gold, and Chinese Electricity Companies. Mathematics, 11(4), 910. https://doi.org/10.3390/math11040910