Abstract

Sustainable economic development plans have been shattered by the devastating COVID-19 crisis, which brought about an economic recession. The companies are suffering from financial losses, leading to financial distress and disengagement from sustainable economic goals. Many companies fail to achieve considerable financial performances, which may lead to unachieved organizational goal and a loss of direction in decision-making and investment. According to the past studies, there has been no comprehensive study done on the financial performance of the companies based on liquidity, solvency, efficiency, and profitability ratios by integrating the entropy method and fuzzy technique for order reference based on similarity to the ideal solution (TOPSIS) model in portfolio investment. Therefore, this paper aims to propose a multi-criteria decision-making (MCDM) model, namely the entropy-fuzzy TOPSIS model, to evaluate the financial performances of companies based on these important financial ratios for portfolio investment. The fuzzy concept helps reduce vagueness and strengthen the meaningful information extracted from the financial ratios. The proposed model is illustrated using the financial ratios of companies in the Dow Jones Industrial Average (DJIA). The results show that return on equity and debt-to-equity ratios are the most influential financial ratios for the performance evaluation of the companies. The companies with good financial performance, such as the best HD company, have been determined based on the proposed model for portfolio selection. A mean-variance (MV) model is used to validate the proposed model in the portfolio investment. At a minimum level of risk, the proposed model is able to generate a higher mean return than the benchmark DJIA index. This paper is significant as it helps to evaluate the financial performance of the companies and select the well-performing companies with the proposed model for portfolio investment.

MSC:

90B50

1. Introduction

The present needs must be attained without adversely affecting our future or the Earth, our home. This notion has moved into the center of discussion since the late 1980s and has since been put into writing as the Sustainable Development Goals (SDGs) in 2015 to be achieved in the next 15 years [1]. The call for the understanding, implementation, and management of SDGs is urgent, with the ultimate goal of generating long-term values for businesses, societies, and the environment. Several insightful companies have taken this initiative to apply various indicators under the SDGs to scan for business opportunities and global risks to enhance their financial performances through sustainable economic developments [2]. The companies pay notable attention to their financial performances because financial results reflect the quantifiable aspects of organizational goal achievements and, hence, allow companies to gauge their successes on a timely basis. In addition, based on recent financial performances, the management team is able to make prudent budgets and decisions to position the company strategically in the local and international markets. Investors also look at financial performances to establish their intentions for initial or continuous support of a company after weighing the risks and returns.

However, COVID-19 has impeded some progress toward sustainable economic developments in many parts of the world, which has then affected their financial performances. Safitri et al. [3] studied the impacts of COVID-19 on these efforts in Indonesia and found that social and economic sectors had been hit hard since 2020. Many industrial activities were also disrupted due to strict protocols to control this infectious disease. A study by Suriyankietkaew and Nimsai [4] also proved that economic activities have been stagnant as COVID-19 cases soared. In addition, the International Monetary Fund (IMF) pointed out that fiscal stimulus during this time could help improve resiliency and reduce the divergence from sustainable economic development goal attainment. As a result, countries in America, Asia, and Europe are standing together in solidarity and have responded by providing assistance to individuals and businesses [5]. However, despite governmental aid, high financial impacts are still felt by businesses, with many facing closure due to financial instability [6].

Over the years, sustainable economic development has helped countries develop economies and assisted companies in strengthening their financial statuses. However, as a result of the outbreak, commercial activities face labor, occupational health and safety, sales, and cash flow challenges that blur the future of businesses. In addition, individuals, families, and corporations tend to be conservative and save their capital, which then results in slower economic growth [7]. Furthermore, amid Omicron-variant concerns in the United States, with many flights halted for the 2021 year-end holidays, the Dow Jones Industrial Average (DJIA) plummeted more than 400 points, leading to growing anxieties among the listed companies [8]. This has reversed many companies’ plans to perform expansions deemed risky, as there is a clear sign of a sluggish recovery from the recession and businesses could continue to suffer from weak balance sheets [9]. As much as they focus on strengthening their bottom lines, companies also realize the necessity of improving liquidity and leverage levels in a financial crisis [10]. In fact, financial strategies should be in place to be activated instantly during a crisis to reduce its daunting consequences [11].

Achim et al. [12] found that the large listed companies in Romania still faced a notable drop in quick ratio (QR), return on equity (ROE), and return on assets (ROA) in 2020. The results from Karim et al. [13] also indicated drops in liquidity, solvency, and operating efficiency of companies in Bangladesh during this health crisis. As a large economic zone, companies in the European Union began suffering from revenue shocks and deteriorating solvency levels since the start of the pandemic, with no definite timetable for recovery, as proven in research by Mirza et al. [14]. In China, listed companies also saw reductions in ROE and asset turnover (AT) [15]. Vito and Gómez [16] explained that companies tend to experience lower sales, which led to a cash crunch, causing the companies to resort to borrowing to reduce short-term liquidity concerns. Rababah et al. [17] revealed that some industries had worrying declines in financial performances as they were worst hit by the outbreak. In addition, financial distress could lead to operational issues such as debts, lower employee morale, and reduced productivity [18]. Given that the financial positions of a large number of companies are highly volatile, there is a pressing need for companies to continuously assess their financial health.

The financial performance of a company can be assessed using a multi-criteria decision-making (MCDM) model. The MCDM is popular due to its success in allowing simultaneous assessment of both optimistic and pessimistic decision criteria, where some criteria generate values while others incur expenses for a decision alternative [19]. Generally, the MCDM model involves the ranking of decision alternatives with regards to various criteria in order to obtain the best solution. Shaverdi et al. [20] studied the financial performance of petrochemical companies in Iran using a combination of the fuzzy analytic hierarchy process (AHP) and the fuzzy Technique for Order Performance by Similarity to an Ideal Solution (TOPSIS). In this study, the decision criteria were made up of liquidity, leverage, activity, and profitability ratios such as the current ratio (CR), the quick ratio (QR), the debt-to-equity ratio (DER), the debt-to-assets ratio (DAR), the AT, the ROA, and the ROE. Shaverdi et al. [20] also noted that uncertainties in real-life situations could be mitigated using fuzzy logic to overcome the limitations of the traditional MCDM model. A fuzzy AHP with CR, QR, DER, DAR, ROA, and ROE was also used in a separate study in Iran [21]. Further, researchers in India also categorized financial ratios into liquidity, leverage, and profitability ratios and adopted CR, QR, DAR, and ROE to evaluate the performances of companies in India with AHP [22]. In Turkey, commercial banks were investigated based on their financial performances with various financial indicators using AHP [23]. The financial aspects of the service and banking industries were examined with financial indicators using fuzzy AHP in Taiwan [24]. CR, QR, DER, DAR, AT, ROA, and ROE were also applied to assess technology companies in Turkey using TOPSIS to increase the power of assessment [25]. In measuring the efficiency of ports in India, Gayathri et al. [26] found that debt ratios had the greatest significance and that integrated MCDM models offered better evaluation.

According to Shannon [27], in decision-making analysis, the quantity and quality of data greatly influence the precision and reliability of the results. Shannon’s entropy reflects the amount of useful information within a set of data to determine criteria weights in MCDM models such as TOPSIS. In addition, Shannon theorized that as an entropy value gets smaller, the criterion weight shall be greater with additional information carried by the criterion and greater effects on the research objective [28]. Shannon’s entropy’s application to determining the objective weights of decision criteria before the alternatives are ranked using the TOPSIS model can be found in a study on the selection of industrial robots in India, and the results of entropy TOPSIS were found to be useful [29]. Furthermore, Shannon’s entropy was proven to be prominent when this method was integrated with TOPSIS to assess the risks present in heritage sites in China, which then assisted the local government in risk mitigation in culturally preserved areas [30]. Moreover, flood vulnerability assessments and rail system performance research were also done with Shannon’s entropy and TOPSIS [31,32].

The introduction of fuzzy set theory by Zadeh [33] has had extensive use for the quantification of linguistic aspects of data. The fuzzy set theory offers higher flexibility in decision boundaries and can therefore, reflect particularities more precisely [34]. In addition, when crisp data is less suitable to model an event due to vagueness, interval judgment with linguistic terms can be used for initial evaluation. All linguistic terms can be transformed into triangular fuzzy numbers (TFNs) for quantitative computations [35]. The TOPSIS model is applicable to rank decision alternatives by calculating Euclidean intervals. This means obtaining distances from positive (PIS) and negative ideal solutions (NIS). The most feasible alternative shall have the shortest Euclidean interval from PIS and the furthest interval from NIS simultaneously. After identifying the decision criteria and alternatives in TOPSIS, the next step is to assign significance levels to the decision criteria by assigning weights to each criterion. The literature does not provide a definite computational method to find criteria weights [36]. Therefore, in this research, entropy is proposed to quantify the weights of the criteria before fuzzy TOPSIS is applied. The fuzzy integration with TOPSIS has been applied for project selection [37,38], dry bulk carrier selection [39], and website evaluation [40].

According to the past studies, there has been no comprehensive study done on the financial performance of the companies based on liquidity, solvency, efficiency, and profitability ratios by integrating the entropy method and fuzzy TOPSIS model in portfolio investment. The novelty of this research lies in the integrated entropy-fuzzy TOPSIS model used to evaluate the financial performance of companies and determine the best performing companies for portfolio investment. Secondly, this paper employs TFNs to reduce the vagueness of data obtained from financial ratios. Therefore, this research adopts a comprehensive set of financial ratios that involve liquidity, solvency, efficiency, and profitability ratios for their financial performance evaluation of companies based on the financial statements. This paper intends to contribute by identifying the influential financial ratios that contribute to the financial performance of the companies so that the companies can work on enhancing critical ratios to increase the companies’ values. This study can also serve as a reference for investors making portfolio investments. The investors can determine an optimal portfolio from the well-performing companies in terms of financial performance for portfolio investment based on the proposed model. Section 2 demonstrates the methodology of the proposed entropy-fuzzy TOPSIS model. Section 3 presents the empirical results of this study. Section 4 summarizes the findings of this research and its conclusion.

2. Materials and Methods

This research aims to propose an MCDM model, namely the entropy-fuzzy TOPSIS model, to assess and compare the financial performance of all components of the DJIA with a total of 30 companies from 2015 to 2021 for portfolio investment. Throughout the years, TOPSIS has emerged as one of the most powerful and reliable methods to provide resolutions to managerial policy implementations and complications [41]. In real life, financial information incorporated into the coefficients of objective functions and constraints contains vagueness, which could be eliminated with fuzzy set theory.

In fact, there has been no proper judgment on the exact value of a financial ratio that reflects the best performance of a company. Moreover, a considerably fair ratio value in an industry in a region may not reflect the same information in other sectors and nations due to the adoption of different strategies and external factors such as legalities and level of competition. However, a rise or decline in a ratio value over consecutive years may not necessarily signal a success or hazard in a company’s business structure and operation [42]. Therefore, due to subjectivity, the entropy-fuzzy TOPSIS model is proposed in this research. Figure 1 shows the flowchart for this research.

Figure 1.

Process flowchart.

The proposed model consists of two stages, as shown below:

Stage-1: Compute the weights of decision criteria (financial ratios) using Shannon’s entropy method.

Stage-2: Assess and rank the decision alternatives (companies) with a fuzzy TOPSIS model.

Table 1 presents the research framework proposal to assess the financial performances of 30 companies under the DJIA using the entropy-fuzzy TOPSIS model.

Table 1.

Research framework proposal.

Table 1 highlights the framework proposal of this research, including the objective, decision criteria, and decision alternatives to assess and rank the financial performance of companies under the DJIA. The DJIA is a prominent US equity index, which consists of the 30 listed companies in the United States [43,44]. In addition, the DJIA measures the entire direction of the stock market. As the index goes up, the market is usually doing well. If the index falls, the stocks are underperforming [45,46]. Seven sets of prominent financial ratios, including CR, QR, DER, DAR, AT, ROA, and ROE, are fixed as the decision criteria. According to González et al. [47], financial ratios are categorized into four types: liquidity, solvency, efficiency, and profitability. The liquidity-type ratios reflect information on the ability to meet short-term obligations. However, solvency ratios consider the potential to meet long-term debts and are most likely linked to the financial health of a company. The efficiency ratios are highly operational measures that analyze the effective deployment of resources for sales generation and are commonly related to cash flows. In fact, investors and shareholders postulate on profitability ratios, which indicate the value creation of a company [48,49]. Furthermore, these four categories of financial ratios have also been supported in a study by Horta [50] and reported by S&P, a giant credit rating company [51]. As a result, this research incorporates all four categories of financial ratios, in which CR and QR are used to study liquidity, DER and DAR for solvency, AT for efficiency, and ROA and ROE are adopted to observe the profitability of a company [52,53,54]. The 30 companies under DJIA then serve as the decision alternatives in this research. The proposed model is presented in Section 2.1.

2.1. Proposed Entropy-Fuzzy TOPSIS Model

Upon the collection of financial ratio data from the financial statements of the 30 companies, Shannon’s entropy method is applied in Stage-1 to compute the objective weights of the decision criteria due to the vagueness and ambiguity of the financial ratios [55,56]. The implicit information existing among various criteria can be captured to obtain the value dispersion for analysis, which is the strength of Shannon’s entropy method [57]. However, as the entropy value gets larger, the entropy weight will become smaller, reflecting less information and the lesser importance of the criteria in a research study, and vice versa. In addition, Shannon’s entropy has also received great interest in TOPSIS studies [58]. The details of Shannon’s entropy method in Stage-1 are presented in the following steps:

Step-1: Determine the weights of the decision criteria with Shannon’s entropy method [59]. When there are alternatives and criteria, the initial decision matrix, , is:

shows the value of th criterion from the th alternative.

Step-2: Normalize the initial decision matrix, .

Step-3: Obtain the information entropy, , of criterion .

Step-4: Compute the entropy weight, of criterion .

where and .

Stage-2 of this research incorporates a fuzzy TOPSIS model to assess and rank the decision alternatives. Due to the limitation of providing unconcise information in TOPSIS, a fuzzy TOPSIS was then proposed by Chen [60]. The fuzzy TOPSIS is based from cardinal data on the criteria. The most critical concept of fuzzy TOPSIS is the interval or extent between fuzzy positive ideal solutions (PIS) and fuzzy negative ideal solutions (NIS) for the alternatives, respectively. In order to improve the suitability and reputability of this research, the assessment and ranking of the alternatives engage the use of linguistic variables with triangular fuzzy numbers (TFNs), which could exist in vector forms . The membership of a TFN can be found below:

where .

Due to this, the chances of capturing imprecise data will be reduced with the adoption of mathematical means [61]. The steps for the entropy-fuzzy TOPSIS model are explained below.

Step-5: Construct a fuzzy decision matrix, from the ratings of alternatives and criteria [58]. Rating is given to each alternative using linguistic variables of TFNs as shown in Table 2 [61,62,63,64].

where where is the lower bound, is the median, and is the upper bound, with .

Table 2.

Linguistic variables corresponding to TFNs.

According to Table 2, the rating from the fuzzy decision matrix is converted into TFNs. This conversion is based on where the rating will fall between the intervals of minimum value and maximum value for each financial ratio. For instance, the ratings with lower values will be rated as having very low linguistic terms. On the other hand, the ratings with higher values will be classified as very high linguistic terms. The ratings with intermediate values will be categorized as low, medium, or high in linguistic terms based on the interval between the minimum value and maximum value of the financial ratios.

Step-6: Compute the normalized fuzzy decision matrix, .

In this step, the optimistic and pessimistic criteria are classified. In this research, CR, QR, AT, ROA, and ROE are the optimistic criteria expecting maximum values, whereas DER and DAR are the pessimistic criteria with a minimum value to be obtained [59,62].

For the optimistic criteria, normalization can be computed as follows.

For the pessimistic criterion, normalization can be performed as follows.

where = optimistic criterion and = pessimistic criterion.

Step-7: Calculate the weighted normalized fuzzy decision matrix, by multiplying the normalized fuzzy decision matrix, , with the entropy weight of criteria, .

Step-8: Determine the fuzzy PIS, and fuzzy NIS, .

Step-9: Calculate the extent of every alternative with and .

Extent of alternative to :

Extent of alternative to :

Step-10: Determine the overall extent of an alternative to , , and , .

Step-11: Calculate the closeness coefficient ( for every alternative [63].

The alternative with the greatest value is the best alternative, while the remaining alternatives can be ranked based on the descending order of values [64].

2.2. Validation of the Proposed Model in Portfolio Investment

In this paper, the proposed model is validated in portfolio investment with a real-life case study on the DJIA. The portfolio optimization is determined by the mean-variance (MV) model. The MV model is developed by Markowitz [65] to construct an optimal portfolio to achieve the expected return at a minimum level of risk [66,67,68,69,70]. Furthermore, the investor is assumed to be rational in maximizing returns and minimizing risks. In this study, the top 15 companies, which are determined by the ranking of the proposed model, are selected for portfolio investment. Further, the MV portfolio optimization model is adopted to determine an optimal portfolio [71]. According to the previous studies, the researchers used the MV model to construct the optimal portfolio [72,73,74,75,76,77,78].

The MV portfolio optimization model’s formulation is demonstrated as follows:

Subject to

where

- denotes a parameter representing the target rate of return required by an investor,

- denotes the weight invested in asset j,

- denotes covariance between assets i and j,

- denotes the expected return of asset j per period,

- n denotes the number of assets,

- denotes weight invested in asset i.

The objective function of the MV portfolio optimization model is to minimize portfolio risk, which is indicated in Equation (17). The purpose of Equation (18) is to make sure that the total of all the weights of assets is equal to one. In addition, Equation (19) is utilized to get the returns at the desired level of return. Moreover, the weights of the assets must be positive. This constraint is presented in Equation (20). The Equation (20) shows that short sales are also not allowed for the MV portfolio optimization model since they require positive weights for assets. Therefore, it is a limitation of the proposed entropy-fuzzy TOPSIS model integrated into a portfolio optimization model for portfolio investment.

Equation (21) shows the portfolio mean return [79].

where

- denotes the expected return of asset j per period,

- denotes the weight invested in asset j,

- denotes the portfolio’s mean return.

The portfolio performance ratio is determined based on the equation below [75].

The performance of the optimal portfolio is compared with the benchmark DJIA in terms of mean return.

3. Empirical Results

The results of this study consist of three sections. Section 3.1 presents the priorities of financial ratios using the entropy weight method as described in Stage 1 of the proposed model. In addition, Section 3.2 presents the financial performance evaluation and ranking of the companies using fuzzy TOPSIS as presented in Stage 2 of the proposed model. Finally, Section 3.3 presents the validation of the proposed entropy-fuzzy TOPSIS model in portfolio investment.

3.1. Priorities of Financial Ratios with Entropy Weight Method

The weights of the financial ratios are determined using the entropy weight method. Table 3 displays the initial decision matrix for the companies with respect to all financial ratios.

Table 3.

The initial decision matrix for the companies with respect to all financial ratios.

Next, the initial decision matrix is normalized to form the normalized decision matrix as presented in Table 4.

Table 4.

The normalized decision matrix for the companies with respect to all financial ratios.

After that, the information entropy () and the entropy weight () of the financial ratios are determined as shown in Table 5.

Table 5.

The information entropy () and the entropy weight () of the financial ratios.

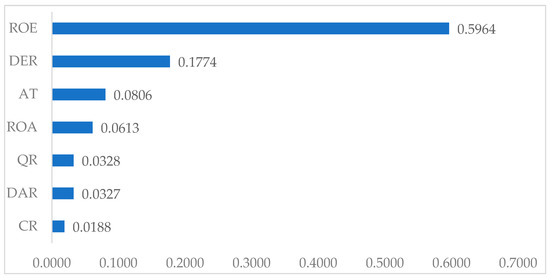

Based on Table 5, the information entropy () for CR, QR, DER, DAR, AT, ROA, and ROE are 0.9816, 0.9681, 0.8271, 0.9681, 0.9215, 0.9403, and 0.4190, respectively. Next, the entropy weight () of the financial ratios can be determined. Figure 2 displays the entropy weights of the financial ratios.

Figure 2.

Entropy weights of financial ratios.

According to Figure 2, the weights of financial ratios are determined using the entropy weight method. Based on the results, ROE is identified as the most influential financial ratio in determining the companies’ financial performance. The ROE has the highest weight of 0.5964. In addition, the DER achieves the second highest weight of 0.1774. The AT obtained a weight of 0.0806, followed by ROA (0.0613), QR (0.0328), DAR (0.0327), and finally CR (0.0188).

3.2. Financial Performance Evaluation and Ranking of Companies with the Proposed Entropy-Fuzzy TOPSIS Model

The financial performance of the companies is assessed by the proposed entropy-fuzzy TOPSIS model. The initial decision matrix from Table 3 is used to assess the financial performance and determine the ranking of the companies. Initially, the ratings from Table 3 are converted into TFNs, and then the fuzzy decision matrix is formed. This conversion is based on where the rating will fall between the intervals of minimum value and maximum value for each financial ratio. The fuzzy decision matrix for the companies with respect to all financial ratios is shown in Table 6.

Table 6.

The fuzzy decision matrix for the companies with respect to all financial ratios.

For the fuzzy decision matrix, all the financial ratios for each company are translated into TFNs due to the presence of uncertainty and ambiguity in the data. Next, the normalized fuzzy decision matrix is created by normalizing the fuzzy decision matrix. The weighted normalized fuzzy decision matrix is formed by multiplying the normalized fuzzy decision matrix with the entropy weights of the financial ratios. The weighted normalized fuzzy decision matrix for the companies with respect to their financial ratios is presented in Table 7.

Table 7.

The weighted normalized fuzzy decision matrix for the companies with respect to all financial ratios.

The fuzzy PIS () and the fuzzy NIS () for each financial ratio are determined and shown in Table 8.

Table 8.

The fuzzy PIS () and the fuzzy NIS ().

The fuzzy PIS () and the fuzzy NIS () for each financial ratio in the weighted normalized fuzzy decision matrix are established. In this study, the fuzzy PIS () for CR, QR, DER, DAR, AT, ROA, and ROE are (0.015, 0.019, 0.019), (0.025, 0.033, 0.033), (0.059, 0.177, 0.177), (0.011, 0.033, 0.033), (0.063, 0.081, 0.081), (0.048, 0.061, 0.061), and (0.464, 0.596, 0.596) respectively. On the other hand, the fuzzy NIS () for CR, QR, DER, DAR, AT, ROA, and ROE are (0.002, 0.002, 0.006), (0.004, 0.004, 0.011), (0.020, 0.020, 0.025), (0.004, 0.004, 0.005), (0.009, 0.009, 0.027), (0.007, 0.007, 0.020), and (0.066, 0.066, 0.199), respectively.

For the next step, the extent of each company from the fuzzy PIS and the fuzzy NIS is computed and presented in Table 9.

Table 9.

Extent of all companies with fuzzy PIS and fuzzy NIS.

After that, the closeness coefficients of the companies are determined. The companies’ rankings are determined based on the closeness coefficients achieved. Table 10 presents the entropy-fuzzy TOPSIS closeness coefficients as well as the ranking of companies.

Table 10.

The entropy-fuzzy TOPSIS closeness coefficients and ranking of companies.

3.3. Validation of the Proposed Entropy-Fuzzy TOPSIS Model in Portfolio Investment

Finally, the validation of the proposed entropy-fuzzy TOPSIS model in portfolio investment is performed with a real-world case study on DJIA. Based on the proposed model, the optimal MV portfolio is determined by the selected companies with good financial performance. Table 11 presents the summary statistics and performance of the optimal MV portfolio.

Table 11.

Summary statistics and performance of the optimal MV portfolio.

According to Table 10, the values of the closeness coefficients are determined based on the proposed entropy-fuzzy TOPSIS model. A larger value of the closeness coefficients implies the most performing companies. Based on the results, the closeness coefficients of the companies range from 0.0418 to 0.7534. Among the companies, HD is identified as the best company in terms of financial performance, with the largest closeness coefficient of 0.7534. This implies that HD has the closest proximity to the ideal solution, considering the presence of uncertainty and fuzziness in the data. As a result, HD outperforms other companies and thus achieves the first ranking based on the proposed entropy-fuzzy TOPSIS model. The second ranking is obtained by NKE, followed by UNH, MSFT, WMT, INTC, AAPL, JNJ, WBA, CSCO, V, AMGN, MMM, HON, DOW, DIS, CVX, PG, CAT, TRV, MRK, IBM, JPM, CRM, MCD, AXP, VZ, KO, GS, and finally BA. In this study, BA scored the lowest value of 0.0418. Additionally, this study has indicated that there are ample opportunities for the companies with low performances to make continuous improvements by considering the good companies for future benchmarking.

The entropy-fuzzy TOPSIS model is proposed in this paper because the fuzzy analysis takes the vagueness and uncertainty of the data into account. The results of this study are converted into TFNs, and then the fuzzy decision matrix is formed. The fuzzy method is taken into consideration in this study since uncertainty and vagueness of data are involved. In this paper, the companies’ financial performances are assessed by seven important financial ratios, which are CR, QR, DER, DAR, AT, ROA, and ROE. After analyzing the financial ratios with the entropy weight method, the weights and priorities of the financial ratios are determined. The financial ratio with the highest weight is ROE, followed by DER, AT, ROA, QR, DAR, and CR. In this research, an entropy-fuzzy TOPSIS model is proposed to evaluate the financial performances of companies based on liquidity, solvency, efficiency, and profitability ratios to determine the companies with good financial performance for portfolio investment.

According to Table 11, the proposed model generates a portfolio mean return of 0.0225 at a portfolio risk of 0.0445. The proposed model gives a portfolio performance ratio of 0.5056. The results of this study show that the optimal MV portfolio of the proposed model is able to generate a higher mean return (0.0225) than the benchmark DJIA index return (0.0095). Therefore, it shows the effectiveness of the proposed model, which outperforms the benchmark DJIA index with a higher mean return. The proposed model provides insights to the investors in identifying and selecting the good performing companies in terms of financial performance for portfolio investment.

4. Conclusions

In this paper, an entropy-fuzzy TOPSIS model is proposed to evaluate the financial performance of companies based on liquidity, solvency, efficiency, and profitability ratios to determine the companies with good financial performance for portfolio investment. The proposed entropy-fuzzy TOPSIS model consists of two stages. The first stage involves Shannon’s entropy weight method to determine the objective weights of the financial ratios, which are CR, QR, AT, DER, DAR, ROA, and ROE. In this study, ROE and DER are identified as the influential financial ratios for the financial performance evaluation of companies which are the components of the DJIA. The second stage includes the fuzzy TOPSIS model to assess and rank the companies based on their financial performance. Regarding the ranking of the companies, HD is determined to be the best company, followed by NKE, UNH, MSFT, WMT, INTC, and AAPL. The companies with good financial performance have been determined based on the proposed model for portfolio selection.

The validation of the proposed entropy-fuzzy TOPSIS model in portfolio investment is performed using the MV model. Based on the proposed model, the optimal MV portfolio is determined by the selected companies with good financial performance. The results indicate that the proposed model is able to generate an optimal MV portfolio with higher mean return than the benchmark DJIA index. This implies that the proposed model outperforms the benchmark DJIA index with a higher portfolio mean return based on the selection of well-performing companies. This study provides insights to investors in portfolio investment. The investors can determine an optimal portfolio from the well-performing companies in terms of financial performance for portfolio investment based on the proposed model. The limitation of the proposed model is that it does not allow short selling in portfolio investment.

The companies could embark on making decisions and taking initiatives to enhance the top financial ratios to improve their financial performance. The financial ratios used in this research include liquidity, solvency, efficiency, and profitability ratios. Based on the integration of fuzzy in the proposed model, uncertainties in financial data can be reduced, which is important for decision making in financing, expansion, and growth. Future studies could consider the application of the proposed entropy-fuzzy TOPSIS model for portfolio investment in other stock markets, such as developed, emerging, or developing markets.

Author Contributions

Conceptualization, W.H.L. and W.S.L.; methodology, W.H.L., W.S.L. and K.F.L.; software, W.H.L., W.S.L. and K.F.L.; validation, W.H.L., W.S.L. and P.F.L.; formal analysis, W.H.L., W.S.L., K.F.L. and P.F.L.; investigation, W.H.L., W.S.L., K.F.L. and P.F.L.; resources, W.H.L. and W.S.L.; data curation, W.H.L., W.S.L., K.F.L. and P.F.L.; writing—original draft preparation, W.H.L., W.S.L., K.F.L. and P.F.L.; writing—review and editing, W.H.L., W.S.L., K.F.L. and P.F.L.; supervision, W.H.L. and W.S.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

This research is supported by the Universiti Tunku Abdul Rahman, Malaysia.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Barcellos-Paula, L.; la Vega, I.D.; Gil-Lafuente, A.M. The quintuple helix of innovation model and the SDGs: Latin-American countries’ case and its forgotten effects. Mathematics 2021, 9, 416. [Google Scholar] [CrossRef]

- Lafuente-Lechuga, M.; Cifuentes-Faura, J.; Faura-Martínez, U. Sustainability, Big Data and Mathematical Techniques: A Bibliometric Review. Mathematics 2021, 9, 2557. [Google Scholar] [CrossRef]

- Safitri, Y.; Ningsih, R.D.; Agustianingsih, D.P.; Sukhwani, V.; Kato, A.; Shaw, R. COVID-19 Impact on SDGs and the Fiscal Measures: Case of Indonesia. Int. J. Environ. Res. Public Health 2021, 18, 2911. [Google Scholar] [CrossRef] [PubMed]

- Suriyankietkaew, S.; Nimsai, S. COVID-19 impacts and sustainability strategies for regional recovery in Southeast Asia: Challenges and opportunities. Sustainability 2021, 13, 8907. [Google Scholar] [CrossRef]

- International Monetary Fund. Fiscal Monitor: Policy for the Recovery. Washington, WA, USA, 2020. Available online: https://www.imf.org/en/Publications/FM/Issues/2020/09/30/october-2020-fiscal-monitor (accessed on 25 December 2021).

- Sachs, J.; Schmidt-Traub, G.; Kroll, C.; Lafortune, G.; Fuller, G.; Woelm, F. The Sustainable Development Goals and COVID-19. In Sustainable Development Report 2020; Cambridge University Press: Cambridge, UK, 2020; Available online: https://s3.amazonaws.com/sustainabledevelopment.report/2020/2020_sustainable_development_report.pdf (accessed on 25 December 2021).

- Donthu, N.; Gustafsson, A. Effects of COVID-19 on business and research. J. Bus. Res. 2020, 117, 284–289. [Google Scholar] [CrossRef]

- Nikkei Asia. Dow Closes Down 430 Points on Omicron Fears. 2021. Available online: https://asia.nikkei.com/Business/Markets/Dow-closes-down-430-points-on-omicron-fears (accessed on 25 December 2021).

- Bachman, D. United States Economic Forecast. 2021. Available online: https://www2.deloitte.com/us/en/insights/economy/us-economic-forecast/united-states-outlook-analysis.html (accessed on 25 December 2021).

- Batrancea, L.M. An Econometric Approach on Performance, Assets, and Liabilities in a Sample of Banks from Europe, Israel, United States of America, and Canada. Mathematics 2021, 9, 3178. [Google Scholar] [CrossRef]

- Batrancea, L. The Nexus between Financial Performance and Equilibrium: Empirical Evidence on Publicly Traded Companies from the Global Financial Crisis Up to the COVID-19 Pandemic. J. Risk. Finance. 2021, 14, 218. [Google Scholar] [CrossRef]

- Achim, M.V.; Safta, I.L.; Văidean, V.L.; Mureșan, G.M.; Borlea, N.S. The impact of covid-19 on financial management: Evidence from Romania. Econ. Res.-Ekon. Istraz. 2022, 35, 1807–1832. [Google Scholar] [CrossRef]

- Karim, M.R.; Shetu, S.A.; Razia, S. COVID-19, liquidity and financial health: Empirical evidence from South Asian economy. Asian J. Econ. Bank. 2021, 5, 307–323. [Google Scholar] [CrossRef]

- Mirza, N.; Rahat, B.; Naqvi, B.; Rizvi, S.K.A. Impact of COVID-19 on corporate solvency and possible policy responses in the EU. Q. Rev. Econ. Finance. 2020. [Google Scholar] [CrossRef]

- Zheng, F.; Zhao, Z.; Sun, Y.; Khan, Y.A. Financial performance of China’s listed firms in presence of coronavirus: Evidence from corporate culture and corporate social responsibility. Curr. Psychol. 2021. [Google Scholar] [CrossRef] [PubMed]

- Vito, A.D.; Gómez, J. Estimating the COVID-19 cash crunch: Global evidence and policy. J. Account. Public Policy 2020, 39, 106741. [Google Scholar] [CrossRef]

- Rababah, A.; Al-Haddad, L.; Sial, M.S.; Chunmei, Z.; Cherian, J. Analyzing the effects of COVID-19 pandemic on the financial performance of Chinese listed companies. J. Public Affairs 2020, 20, e2440. [Google Scholar]

- Ali, S.; Talha, N. During COVID-19, impact of subjective and objective financialknowledge and economic insecurity on financial managementbehavior: Mediating role of financial wellbeing. J. Public Affairs 2021, 22, e2789. [Google Scholar]

- Stojić, G.; Stević, Z.; Antuchevićienė, J.; Pamučar, D.; Vasiljević, M. A novel rough WASPAS approach for supplier selection in a company manufacturing PVC carpentry products. Information 2018, 9, 121. [Google Scholar] [CrossRef]

- Shaverdi, M.; Ramezani, I.; Tahmasebi, R.; Rostamy, A.A.A. Combining fuzzy AHP and fuzzy TOPSIS with financial ratios to design a novel performance evaluation model. Int. J. Fuzzy Syst. 2016, 18, 248–262. [Google Scholar] [CrossRef]

- Shaverdi, M.; Heshmati, M.R.; Ramezani, I. Application of fuzzy AHP approach for financial performance evaluation of Iranian petrochemical sector. Procedia Comput. Sci. 2014, 31, 995–1004. [Google Scholar] [CrossRef]

- Monga, R.; Aggrawal, D.; Singh, J. Application of AHP in evaluating the financial performance of industries. In Advances in Mathematics for Industry 4.0, 1st ed.; Ram, M., Ed.; Academic Press: London, UK, 2020; pp. 319–333. [Google Scholar]

- İç, Y.T.; Yurdakul, M.; Pehlivan, E. Development of a hybrid financial performance measurement model using AHP and DOE methods for Turkish commercial banks. Soft Comput. 2021, 26, 2959–2979. [Google Scholar] [CrossRef]

- Chiang, J.; Chiou, C.; Doong, S.; Chang, I. Research on construction of performance indicators for the marketing alliance of catering industry and credit card issuing banks by using the Balanced Scorecard and fuzzy AHP. Sustainability 2020, 12, 9005. [Google Scholar] [CrossRef]

- Bulgurcu, B.K. Application of TOPSIS technique for financial performance evaluation of technology firms in Istanbul Stock Exchange Market. Procedia Soc. Behav. Sci. 2012, 62, 1033–1040. [Google Scholar] [CrossRef]

- Gayathri, C.; Kamala, V.; Gajanand, M.S.; Yamini, S. Analysis of operational and financial performance of ports: An integrated fuzzy DEMATEL-TOPSIS approach. Benchmarking Int. J. 2021, 29, 1046–1066. [Google Scholar] [CrossRef]

- Shannon, C.E. A mathematical theory of communication. Bell Syst. Tech. 1948, 27, 379–423. [Google Scholar] [CrossRef]

- Saraswat, S.K.; Digalwar, A.K. Evaluation of energy alternatives for sustainable development of energy sector in India: An integrated Shannon’s entropy fuzzy multicriteria decision approach. Renew. Energy 2021, 171, 58–74. [Google Scholar] [CrossRef]

- Chodha, V.; Dubey, R.; Kumar, R.; Singh, S.; Kaur, S. Selection of industrial arc welding robot with TOPSIS and Entropy MCDM techniques. Mater. Today Proc. 2022, 50, 709–715. [Google Scholar] [CrossRef]

- Li, J.; Chen, Y.; Yao, X.; Chen, A. Risk management priority assessment of heritage sites in China based on entropy weight and TOPSIS. J. Cult. Herit. 2021, 49, 10–18. [Google Scholar] [CrossRef]

- Yang, W.; Xu, K.; Lian, J.; Ma, C.; Bin, L. Integrated flood vulnerability assessment approach based on TOPSIS and Shannon entropy methods. Ecol. Indic. 2018, 89, 269–280. [Google Scholar] [CrossRef]

- Huang, W.; Shuai, B.; Sun, Y.; Wang, Y.; Antwi, E. Using entropy-TOPSIS method to evaluate urban rail transit system operation performance: The China case. Transp. Res. A 2018, 111, 292–303. [Google Scholar] [CrossRef]

- Zadeh, L.A. Fuzzy sets. Inf. Control. 1965, 8, 338–353. [Google Scholar] [CrossRef]

- Hwang, B. Chapter 3—Methodology. In Performance and Improvement of Green Construction Projects: Management Strategies and Innovations; Butterworth-Heinemann: Oxford, UK, 2018; pp. 15–22. [Google Scholar]

- Nădăban, S.; Dzitac, S.; Dzitac, I. Fuzzy TOPSIS: A general view. Procedia Comput. Sci. 2016, 91, 823–831. [Google Scholar] [CrossRef]

- Sokolović, J.; Stanujkić, D.; Śtirbanović, Z. Selection of process for aluminium separation from waste cables by TOPSIS and WASPAS methods. Miner. Eng. 2021, 173, 107186. [Google Scholar] [CrossRef]

- Shamsuzzoha, A.; Piya, S.; Shamsuzzaman, M. Application of fuzzy TOPSIS framework for selecting complex project in a case company. J. Glob. Oper. Strateg. Sourc. 2021, 14, 528–566. [Google Scholar] [CrossRef]

- Palczewski, K.; Sałabun, W. The fuzzy TOPSIS applications in the last decade. Procedia Comput. Sci. 2019, 159, 2294–2303. [Google Scholar] [CrossRef]

- Sahin, B.; Yip, T.L.; Tseng, P.; Kabak, M.; Soylu, A. An application of a fuzzy TOPSIS multi-criteria decision analysis algorithm for dry bulk carrier selection. Information 2020, 11, 251. [Google Scholar] [CrossRef]

- Kabassi, K.; Botonis, A.; Karydis, C. Evaluating websites of specialized cultural content using fuzzy multi-criteria decision making theories. Informatica 2020, 44, 45–54. [Google Scholar] [CrossRef]

- Sharma, N.K.; Kumar, V.; Verma, P.; Luthra, S. Sustainable reverse logistics practices and performance evaluation with fuzzy TOPSIS: A study on Indian retailers. Clean. Logist. Supply Chain 2021, 1, 100007. [Google Scholar] [CrossRef]

- Korol, T. The implementation of fuzzy logic in forecasting financial ratios. Contemp. Econ. 2017, 12, 165–188. [Google Scholar]

- Leal, M.; Ponce, D.; Puerto, J. Portfolio problems with two levels decision-makers: Optimal portfolio selection with pricing decisions on transaction costs. Eur. J. Oper. Res. 2020, 284, 712–727. [Google Scholar] [CrossRef]

- Lahmiri, S.; Bekiros, S. Nonlinear analysis of Casablanca Stock Exchange, Dow Jones and S&P500 industrial sectors with a comparison. Physica A 2020, 539, 122923. [Google Scholar]

- Kamaludin, K.; Sundarasen, S.; Ibrahim, I. Covid-19, Dow Jones and equity market movement in ASEAN-5 countries: Evidence from wavelet analyses. Heliyon 2021, 7, e05851. [Google Scholar] [CrossRef] [PubMed]

- Plastun, A.; Sibande, X.; Gupta, R.; Wohar, M.E. Evolution of price effects after one-day abnormal returns in the US stock market. N. Am. J. Econ. Finance 2021, 57, 101405. [Google Scholar] [CrossRef]

- González, F.F.; Webb, J.; Sharmina, M.; Hannon, M.; Braunholtz-Speight, T.; Pappas, D. Local energy businesses in the United Kingdom: Clusters and localism determinants based on financial ratios. Energy 2022, 239, 122119. [Google Scholar] [CrossRef]

- Messer, R. Common financial ratios. In Financial Modeling for Decision Making: Using MS-Excel in Accounting and Finance; Emerald Publishing Limited: Bingley, UK, 2020; p. 325. [Google Scholar]

- Batrancea, L. The influence of liquidity and solvency on performance within the healthcare industry: Evidence from publicly listed companies. Mathematics 2021, 9, 2231. [Google Scholar] [CrossRef]

- Horta, I.M.; Camanho, A.S.; da Costa, J.M. Performance assessment of construction companies: A study of factors promoting financial soundness and innovation in the industry. Int. J. Prod. Econ. 2012, 137, 84–93. [Google Scholar] [CrossRef]

- Huang, J.; Wang, H. A data analytics framework for key financial factors. J. Model. Manag. 2016, 12, 178–189. [Google Scholar] [CrossRef]

- Nguyen, L.T.M.; Dinh, P.H. Ex-ante risk management and financial stability during the COVID-19 pandemic: A study of Vietnamese firms. China Finance Rev. Int. 2021, 11, 349–371. [Google Scholar] [CrossRef]

- Wieprow, J.; Gawlik, A. The Use of Discriminant Analysis to Assess the Risk of Bankruptcy of Enterprises in Crisis Conditions Using the Example of the Tourism Sector in Poland. Risks 2021, 9, 78. [Google Scholar] [CrossRef]

- Zorn, A.; Esteves, M.; Baur, I.; Lips, M. Financial Ratios as Indicators of Economic Sustainability: A Quantitative Analysis for Swiss Dairy Farms. Sustainability 2018, 10, 2942. [Google Scholar] [CrossRef]

- Lee, P.T.; Lin, C.; Shin, S. Financial performance evaluation of shipping companies using entropy and grey relation analysis. In Multi-Criteria Decision Making in Maritime Studies and Logistics; Lee, P., Yang, Z., Eds.; Springer International Publishing: New York, NY, USA, 2018; pp. 219–247. [Google Scholar]

- Yadav, S.K.; Dharani, M. Prioritizing of banking firms in India using entropy-TOPSIS method. Int. J. Bus. Innov. Res. 2019, 20, 554–570. [Google Scholar] [CrossRef]

- Li, Z.; Luo, Z.; Wang, Y.; Fan, G.; Zhang, J. Suitability evaluation system for the shallow geothermal energy implementation in region by Entropy Weight Method and TOPSIS method. Renew. Energy 2022, 184, 564–576. [Google Scholar] [CrossRef]

- Chen, P. Effects of the entropy weight on TOPSIS. Expert Syst. Appl. 2021, 168, 114186. [Google Scholar] [CrossRef]

- Mavi, R.K.; Goh, M.; Mavi, N.K. Supplier selection with Shannon entropy and fuzzy TOPSIS in the context of supply chain risk management. Procedia Soc. Behav. Sci. 2016, 235, 216–225. [Google Scholar] [CrossRef]

- Chen, C.T. Extensions of the TOPSIS for group decision-making under fuzzy environment. Fuzzy Sets Syst. 2000, 114, 1–9. [Google Scholar] [CrossRef]

- Solangi, Y.A.; Cheng, L.; Shah, S.A.A. Assessing and overcoming the renewable energy barriers for sustainable development in Pakistan: An integrated AHP and fuzzy TOPSIS approach. Renew. Energy 2021, 173, 209–222. [Google Scholar] [CrossRef]

- Emovon, I.; Aibuedefe, W.O. Fuzzy TOPSIS application in materials analysis for economic production of cashew juice extractor. Fuzzy Inf. Eng. 2020, 12, 1–18. [Google Scholar] [CrossRef]

- Mathangi, S.; Maran, J.P. Sensory evaluation of apple ber using fuzzy TOPSIS. Mater. Today Proc. 2021, 45, 2982–2986. [Google Scholar] [CrossRef]

- Liu, P. An extended TOPSIS method for multiple attribute group decision making based on generalized interval-valued trapezoidal fuzzy numbers. Informatica 2011, 35, 185–196. [Google Scholar]

- Markowitz, H. Mean–variance approximations to expected utility. Eur. J. Oper. Res. 2014, 234, 346–355. [Google Scholar] [CrossRef]

- Tayali, H.A.; Tolun, S. Dimension reduction in mean-variance portfolio optimization. Expert Syst. Appl. 2018, 92, 161–169. [Google Scholar] [CrossRef]

- Huang, X. Mean–variance models for portfolio selection subject to experts’ estimations. Expert Syst. Appl. 2012, 39, 5887–5893. [Google Scholar] [CrossRef]

- Pinasthika, N.; Surya, B.A. Optimal portfolio analysis with risk-free assets using index-tracking and Markowitz mean-variance portfolio optimization model. J. Bus. Manag. 2014, 3, 737–751. [Google Scholar]

- Spaseski, N. Portfolio management: Mean-variance analysis in the US asset market. Eur. J. Bus. Soc. Sci. 2014, 3, 242–248. [Google Scholar]

- Markowitz, H.M. Foundations of portfolio theory. J. Financ. 1991, 46, 469–477. [Google Scholar] [CrossRef]

- Markowitz, H. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Xiao, H.; Ren, T.; Zhou, Z. Time-consistent strategies for the generalized multiperiod mean-variance portfolio optimization considering benchmark orientation. Mathematics 2019, 7, 723. [Google Scholar] [CrossRef]

- Lefebvre, W.; Loeper, G.; Pham, H. Mean-variance portfolio selection with tracking error penalization. Mathematics 2020, 8, 1915–1937. [Google Scholar] [CrossRef]

- Aljinović, Z.; Marasović, B.; Šestanović, T. Cryptocurrency portfolio selection—A multicriteria approach. Mathematics 2021, 9, 1677–1697. [Google Scholar] [CrossRef]

- Fernandez-Navarro, F.; Martinez-Nieto, L.; Carbonero-Ruz, M.; Montero-Romero, T. Mean squared variance portfolio: A mixed-integer linear programming formulation. Mathematics 2021, 9, 223. [Google Scholar] [CrossRef]

- Park, H. Modified mean-variance risk measures for long-term portfolios. Mathematics 2021, 9, 111. [Google Scholar] [CrossRef]

- Corsaro, S.; De Simone, V.; Marino, Z.; Scognamiglio, S. l1-Regularization in portfolio selection with machine learning. Mathematics 2022, 10, 540. [Google Scholar] [CrossRef]

- Novais, R.G.; Wanke, P.; Antunes, J.; Tan, Y. Portfolio optimization with a mean-entropy-mutual information model. Entropy 2022, 24, 369. [Google Scholar] [CrossRef]

- Bodie, Z.; Kane, A.; Marcus, A. Investments, 12th ed.; McGraw-Hill: New York, NY, USA, 2021. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).