Time-Varying Granger Causality of COVID-19 News on Emerging Financial Markets: The Latin American Case

, , , and

, , , and

Abstract

1. Introduction

2. Data and Methods

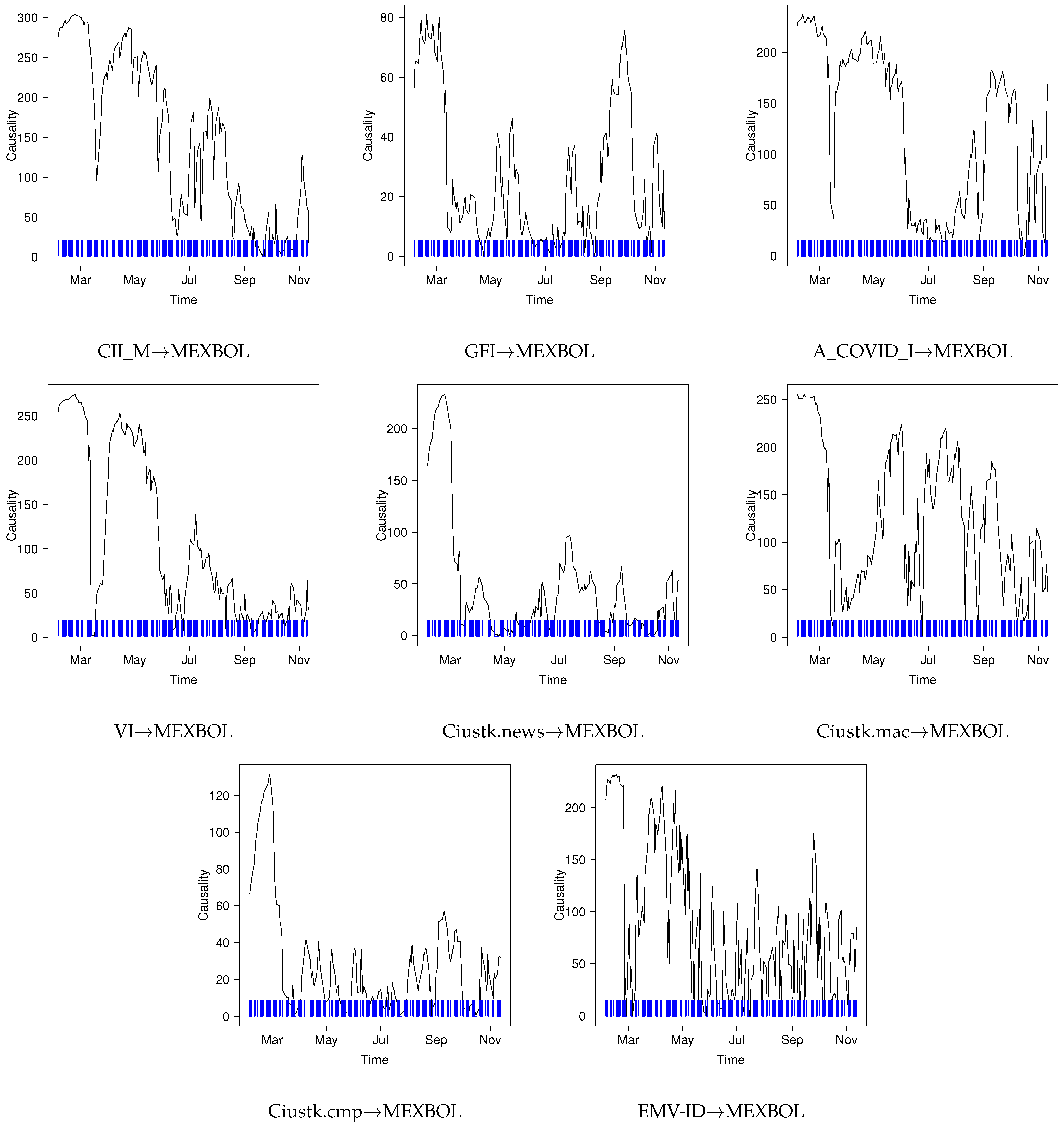

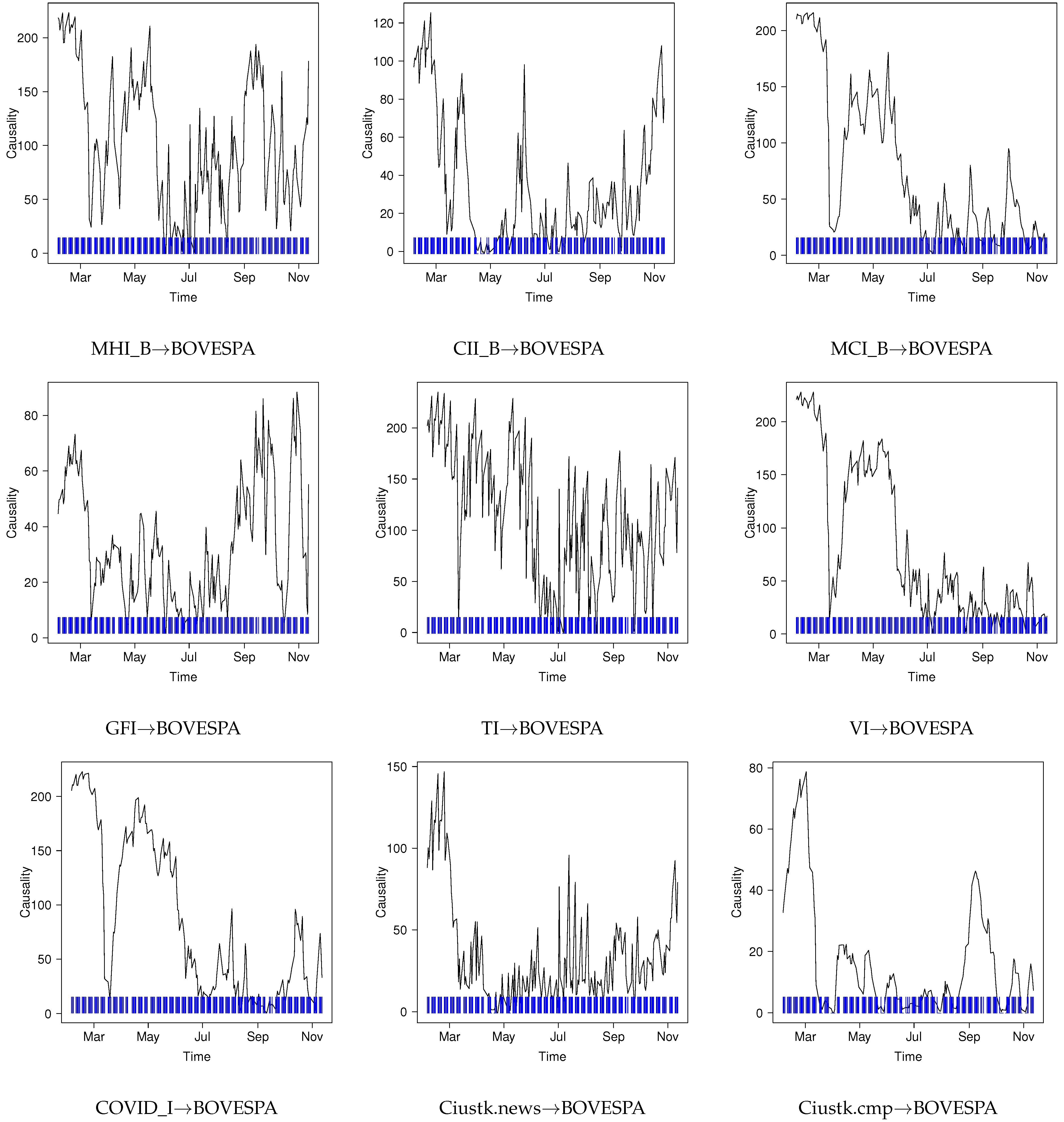

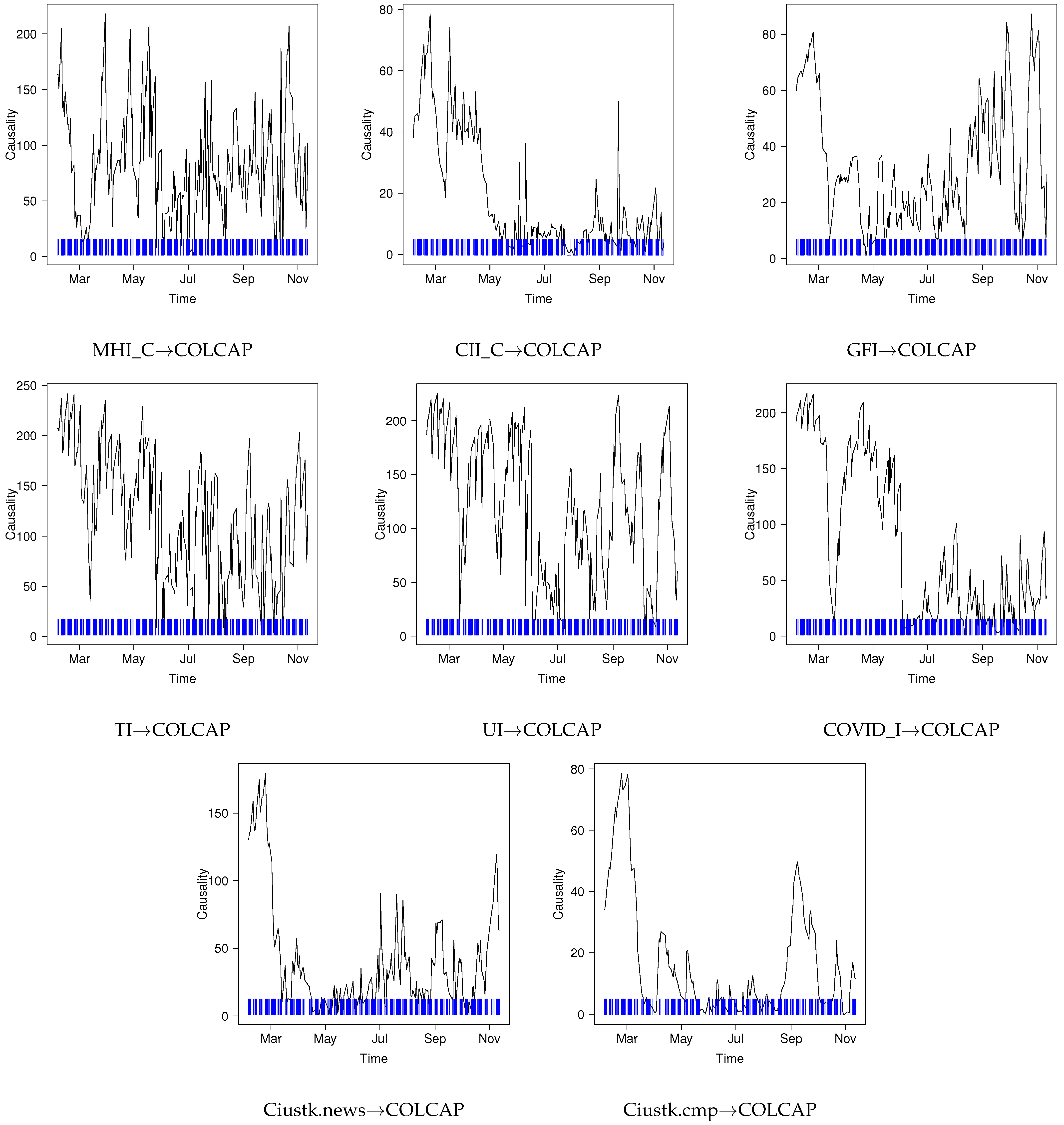

3. Results and Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

References

- World Health Organization. Rolling Updates on Coronavirus Disease (COVID-19). Available online: https://www.who.int/emergencies/diseases/novel-coronavirus-2019/events-as-they-happen (accessed on 20 November 2022).

- Economic Commission for Latin America and the Caribbean. Informe Sobre El Impacto Económico En América Latina y El Caribe de La Enfermedad Por Coronavirus (COVID-19); UNECLAC: Santiago, Chile, 2020; ISBN 9789210054140. [Google Scholar]

- Hasan, M.B.; Mahi, M.; Hassan, M.K.; Bhuiyan, A.B. Impact of COVID-19 Pandemic on Stock Markets: Conventional vs. Islamic Indices Using Wavelet-Based Multi-Timescales Analysis. N. Am. J. Econ. Financ. 2021, 58, 101504. [Google Scholar] [CrossRef]

- Yarovaya, L.; Elsayed, A.H.; Hammoudeh, S. Determinants of Spillovers between Islamic and Conventional Financial Markets: Exploring the Safe Haven Assets during the COVID-19 Pandemic. Financ. Res. Lett. 2021, 43, 101979. [Google Scholar] [CrossRef]

- Albulescu, C.T. COVID-19 and the United States Financial Markets’ Volatility. Financ. Res. Lett. 2021, 38, 101699. [Google Scholar] [CrossRef] [PubMed]

- Shehzad, K.; Xiaoxing, L.; Bilgili, F.; Koçak, E. COVID-19 and Spillover Effect of Global Economic Crisis on the United States’ Financial Stability. Front. Psychol. 2021, 12, 632175. [Google Scholar] [CrossRef] [PubMed]

- Nicola, M.; Alsafi, Z.; Sohrabi, C.; Kerwan, A.; Al-Jabir, A.; Iosifidis, C.; Agha, M.; Agha, R. The Socio-Economic Implications of the Coronavirus Pandemic (COVID-19): A Review. Int. J. Surg. 2020, 78, 185–193. [Google Scholar] [CrossRef]

- Wei, S.-J. Ten Keys to Beating Back COVID-19 and the Associated Economic Pandemic. In Mitigating the COVID Economic Crisis: Act Fast and Do Whatever It Takes; Baldwin, R., Weder di Mauro, B., Eds.; CEPR Press: London, UK, 2020; pp. 71–76. ISBN 978-1-912179-29-9. [Google Scholar]

- Sharma, S.S. A Note on the Asian Market Volatility During the COVID-19 Pandemic. Asian Econ. Lett. 2020, 1, 17661. [Google Scholar] [CrossRef]

- Hong, H.; Bian, Z.; Lee, C.C. COVID-19 and Instability of Stock Market Performance: Evidence from the U.S. Financ. Innov. 2021, 7, 12. [Google Scholar] [CrossRef]

- Topcu, M.; Gulal, O.S. The Impact of COVID-19 on Emerging Stock Markets. Financ. Res. Lett. 2020, 36, 101691. [Google Scholar] [CrossRef]

- Umar, Z.; Gubareva, M.; Teplova, T. The Impact of COVID-19 on Commodity Markets Volatility: Analyzing Time Frequency Relations between Commodity Prices and Coronavirus Panic Levels. Resour. Policy 2021, 73, 102164. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.; Hu, Y.; Lucey, B.; Oxley, L. Aye Corona! The Contagion Effects of Being Named Corona during the COVID-19 Pandemic. Financ. Res. Lett. 2021, 38, 101591. [Google Scholar] [CrossRef]

- Shaikh, I. On the Relation between the Crude Oil Market and Pandemic COVID-19. Eur. J. Manag. Bus. Econ. 2021, 30, 331–356. [Google Scholar] [CrossRef]

- Phan, D.H.B.; Narayan, P.K. Country Responses and the Reaction of the Stock Market to COVID-19 a Preliminary Exposition. Emerg. Mark. Financ. Trade 2021, 56, 2138–2150. [Google Scholar] [CrossRef]

- Javed, F.; Mantalos, P. Sensitivity of the Causality in Variance Test to the GARCH (1,1) Parameters. Chil. J. Stat. 2015, 6, 49–65. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Kost, K.; Sammon, M.; Viratyosin, T. The Unprecedented Stock Market Impact of COVID-19; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Bai, L.; Wei, Y.; Wei, G.; Li, X.; Zhang, S. Infectious Disease Pandemic and Permanent Volatility of International Stock Markets: A Long-Term Perspective. Financ. Res. Lett. 2020, 40, 101709. [Google Scholar] [CrossRef] [PubMed]

- Bouri, E.; Gkillas, K.; Gupta, R.; Pierdzioch, C. Forecasting Power of Infectious Diseases-Related Uncertainty for Gold Realized Variance. Financ. Res. Lett. 2021, 42, 101936. [Google Scholar] [CrossRef]

- Gupta, R.; Subramaniam, S.; Bouri, E.; Ji, Q. Infectious Disease-Related Uncertainty and the Safe-Haven Characteristic of US Treasury Securities. Int. Rev. Econ. Financ. 2021, 71, 289–298. [Google Scholar] [CrossRef]

- Li, Y.; Liang, C.; Ma, F.; Wang, J. The Role of the IDEMV in Predicting European Stock Market Volatility during the COVID-19 Pandemic. Financ. Res. Lett. 2020, 36, 101749. [Google Scholar] [CrossRef]

- RavenPack Coronavirus. Available online: https://coronavirus.ravenpack.com (accessed on 20 November 2022).

- Baig, A.S.; Butt, H.A.; Haroon, O.; Rizvi, S.A.R. Deaths, Panic, Lockdowns and US Equity Markets: The Case of COVID-19 Pandemic. Financ. Res. Lett. 2021, 38, 101701. [Google Scholar] [CrossRef]

- Ho, K.-Y.; Shi, Y.; Zhang, Z. News and Return Volatility of Chinese Bank Stocks. Int. Rev. Econ. Financ. 2020, 69, 1095–1105. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Boubaker, S.; Umar, Z. COVID-19 Media Coverage and ESG Leader Indices. Financ. Res. Lett. 2021, 45, 102170. [Google Scholar] [CrossRef]

- Cepoi, C.O. Asymmetric Dependence between Stock Market Returns and News during COVID-19 Financial Turmoil. Financ. Res. Lett. 2020, 36, 101658. [Google Scholar] [CrossRef]

- Tan, Ö. The Effect of Pandemic News on Stock Market Returns During the Covid-19 Crash: Evidence from International Markets. Connect. Istanb. Univ. J. Commun. Sci 2021, 60, 217–240. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Desroziers, A. The Stock Market Is Not the Economy? Insights from the COVID-19 Crisis. SSRN Electron. J. 2020, 1–40. [Google Scholar] [CrossRef]

- Niu, Z.; Liu, Y.; Gao, W.; Zhang, H. The Role of Coronavirus News in the Volatility Forecasting of Crude Oil Futures Markets: Evidence from China. Resour. Policy 2021, 73, 102173. [Google Scholar] [CrossRef]

- Naseem, S.; Mohsin, M.; Hui, W.; Liyan, G.; Penglai, K. The Investor Psychology and Stock Market Behavior During the Initial Era of COVID-19: A Study of China, Japan, and the United States. Front. Psychol. 2021, 12, 626934. [Google Scholar] [CrossRef]

- Xiang, Y.-T.; Yang, Y.; Li, W.; Zhang, L.; Zhang, Q.; Cheung, T.; Ng, C.H. Timely Mental Health Care for the 2019 Novel Coronavirus Outbreak Is Urgently Needed. Lancet Psychiatry 2020, 7, 228–229. [Google Scholar] [CrossRef] [PubMed]

- Jawadi, F.; Namouri, H.; Ftiti, Z. An Analysis of the Effect of Investor Sentiment in a Heterogeneous Switching Transition Model for G7 Stock Markets. J. Econ. Dyn. Control 2018, 91, 469–484. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Foglia, M.; Nasir, M.A.; Angelini, E. Feverish Sentiment and Global Equity Markets during the COVID-19 Pandemic. J. Econ. Behav. Organ. 2021, 188, 1088–1108. [Google Scholar] [CrossRef] [PubMed]

- Haroon, O.; Rizvi, S.A.R. COVID-19: Media Coverage and Financial Markets Behavior—A Sectoral Inquiry. J. Behav. Exp. Financ. 2020, 27, 100343. [Google Scholar] [CrossRef] [PubMed]

- Dong, H.; Gil-Bazo, J.; Ratiu, R.V. Information Demand during the COVID-19 Pandemic. J. Account. Public Policy 2021, 40, 106917. [Google Scholar] [CrossRef]

- Galai, D.; Sade, O. The “Ostrich Effect” and the Relationship between the Liquidity and the Yields of Financial Assets. J. Bus. 2006, 79, 2741–2759. [Google Scholar] [CrossRef]

- Devpura, N.; Narayan, P.K.; Sharma, S.S. Is Stock Return Predictability Time-Varying? J. Int. Financ. Mark. Institutions Money 2018, 52, 152–172. [Google Scholar] [CrossRef]

- Fernandez-Perez, A.; Gilbert, A.; Indriawan, I.; Nguyen, N.H. COVID-19 Pandemic and Stock Market Response: A Culture Effect. J. Behav. Exp. Financ. 2021, 29, 100454. [Google Scholar] [CrossRef] [PubMed]

- Namouri, H.; Jawadi, F.; Ftiti, Z.; Hachicha, N. Threshold Effect in the Relationship between Investor Sentiment and Stock Market Returns: A PSTR Specification. Appl. Econ. 2018, 50, 559–573. [Google Scholar] [CrossRef]

- Lu, F.; Hong, Y.; Wang, S.; Lai, K.; Liu, J. Time-Varying Granger Causality Tests for Applications in Global Crude Oil Markets. Energy Econ. 2014, 42, 289–298. [Google Scholar] [CrossRef]

- Blitz, D.; Huisman, R.; Swinkels, L.; van Vliet, P. Media Attention and the Volatility Effect. Financ. Res. Lett. 2020, 36, 101317. [Google Scholar] [CrossRef]

- Salisu, A.A.; Akanni, L.O. Constructing a Global Fear Index for the COVID-19 Pandemic. Emerg. Mark. Financ. Trade 2020, 56, 2310–2331. [Google Scholar] [CrossRef]

- Salisu, A.A.; Ogbonna, A.E.; Oloko, T.F.; Adediran, I.A. A New Index for Measuring Uncertainty Due to the COVID-19 Pandemic. Sustainability 2021, 13, 3212. [Google Scholar] [CrossRef]

- Narayan, P.K.; Iyke, B.N.; Sharma, S.S. New Measures of the COVID-19 Pandemic: A New Time-Series Dataset. Asian Econ. Lett. 2021, 2, 1–14. [Google Scholar] [CrossRef]

- Bera, A.K.; Jarque, C.M. Efficient Tests for Normality, Homoscedasticity and Serial Independence of Regression Residuals. Econ. Lett. 1981, 7, 313–318. [Google Scholar] [CrossRef]

- Meng, M.; Lee, J.; Payne, J.E. RALS-LM Unit Root Test with Trend Breaks and Non-Normal Errors: Application to the Prebisch-Singer Hypothesis. Stud. Nonlinear Dyn. Econom. 2017, 21, 31–45. [Google Scholar] [CrossRef]

- Engle, R. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Killick, R.; Fearnhead, P.; Eckley, I.A. Optimal Detection of Changepoints with a Linear Computational Cost. J. Am. Stat. Assoc. 2012, 107, 1590–1598. [Google Scholar] [CrossRef]

- Broock, W.A.; Scheinkman, J.A.; Dechert, W.D.; LeBaron, B. A Test for Independence Based on the Correlation Dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- Cevik, E.I.; Atukeren, E.; Korkmaz, T. Oil Prices and Global Stock Markets: A Time-Varying Causality-in-Mean and Causality-in-Variance Analysis. Energies 2018, 11, 2848. [Google Scholar] [CrossRef]

- Gupta, R.; Kanda, P.; Wohar, M.E. Predicting Stock Market Movements in the United States: The Role of Presidential Approval Ratings. Int. Rev. Financ. 2021, 21, 324–335. [Google Scholar] [CrossRef]

- Coronado, S.; Gupta, R.; Hkiri, B.; Rojas, O. Time-Varying Spillovers between Currency and Stock Markets in the USA: Historical Evidence from More than Two Centuries. Adv. Decis. Sci. 2020, 24, 1–32. [Google Scholar]

- Engle, R. Dynamic Conditional Correlation. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Kanda, P.; Burke, M.; Gupta, R. Time-Varying Causality between Equity and Currency Returns in the United Kingdom: Evidence from over Two Centuries of Data. Phys. A Stat. Mech. Appl. 2018, 506, 1060–1080. [Google Scholar] [CrossRef]

- Jammazi, R.; Ferrer, R.; Jareño, F.; Shahzad, S.J.H. Time-Varying Causality between Crude Oil and Stock Markets: What Can We Learn from a Multiscale Perspective? Int. Rev. Econ. Financ. 2017, 49, 453–483. [Google Scholar] [CrossRef]

- Gallotti, R.; Valle, F.; Castaldo, N.; Sacco, P.; De Domenico, M. Assessing the Risks of ‘Infodemics’ in Response to COVID-19 Epidemics. Nat. Hum. Behav. 2020, 4, 1285–1293. [Google Scholar] [CrossRef] [PubMed]

- Evans, K.P. Intraday Jumps and US Macroeconomic News Announcements. J. Bank Financ. 2011, 35, 2511–2527. [Google Scholar] [CrossRef]

- Jawadi, F.; Louhichi, W.; ben Ameur, H.; Ftiti, Z. Do Jumps and Co-Jumps Improve Volatility Forecasting of Oil and Currency Markets? Energy J. 2019, 40, 131–150. [Google Scholar] [CrossRef]

- Youssef, M.; Mokni, K.; Ajmi, A.N. Dynamic Connectedness between Stock Markets in the Presence of the COVID-19 Pandemic: Does Economic Policy Uncertainty Matter? Financ. Innov. 2021, 7, 13. [Google Scholar] [CrossRef] [PubMed]

- Azimli, A. The Impact of COVID-19 on the Degree of Dependence and Structure of Risk-Return Relationship: A Quantile Regression Approach. Financ. Res. Lett. 2020, 36, 101648. [Google Scholar] [CrossRef] [PubMed]

- Engelhardt, N.; Krause, M.; Neukirchen, D.; Posch, P.N. Trust and Stock Market Volatility during the COVID-19 Crisis. Financ. Res. Lett. 2021, 38, 101873. [Google Scholar] [CrossRef]

- Coronado, S.; Martinez, J.N.; Romero-Meza, R. Time-Varying Multivariate Causality among Infectious Disease Pandemic and Emerging Financial Markets: The Case of the Latin American Stock and Exchange Markets. Appl. Econ. 2021, 54, 3924–3932. [Google Scholar] [CrossRef]

- Romero-Meza, R.; Coronado, S.; Ibañez-Veizaga, F. COVID-19 y Causalidad En La Volatilidad Del Mercado Accionario Chileno. Estud. Gerenciales 2021, 37, 242–250. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mexico | Brazil | Colombia | ||||||

|---|---|---|---|---|---|---|---|---|

| MEXBOL | CII_M | BOVESPA | MHI_B | CII_B | MCI_B | COLCAP | MHI_C | CII_C |

| 02/25/20 | 03/10/20 | 06/02/20 | 03/12/20 | 03/09/20 | 03/06/20 | 08/21/20 | 09/01/20 | 06/08/20 |

| 04/28/20 | 07/31/20 | 07/03/20 | 05/15/20 | 06/12/20 | 08/21/20 | 09/01/20 | 06/08/20 | |

| 06/11/20 | 09/17/20 | 09/08/20 | 09/14/20 | 10/19/20 | ||||

| 07/08/20 | 10/12/20 | 10/19/20 | ||||||

| 07/21/20 | 10/26/20 | |||||||

| 08/28/20 | ||||||||

| 10/07/20 | ||||||||

| 10/27/20 | ||||||||

| Chile | Peru | Argentina | ||||||

| IPSA | PI_CH | MCI_CH | IGBVL | SI_P | CII_P | MARVEL | MCI_A | FNI_A |

| 04/02/20 | 05/27/20 | 03/04/20 | 06/03/20 | 07/08/20 | 04/13/20 | 02/12/20 | 02/26/20 | 03/23/20 |

| 07/16/20 | 06/03/20 | 07/07/20 | 08/04/20 | 08/13/20 | 08/13/20 | 03/06/20 | 06/02/20 | 03/26/20 |

| 09/08/20 | 07/16/20 | 08/25/20 | 05/08/20 | 04/24/20 | ||||

| 07/29/20 | 06/02/20 | |||||||

| 09/21/20 | 06/10/20 | |||||||

| 09/23/20 | 07/13/20 | |||||||

| 09/15/20 | ||||||||

| 09/30/20 | ||||||||

| U.S.A | ||||||||

| S&P | PI_US | FNI_US | CII_US | EMV-ID | ||||

| 03/06/20 | 05/11/20 | 05/04/20 | 03/09/20 | 04/07/20 | ||||

| 04/07/20 | 05/21/20 | 05/29/20 | ||||||

| 05/26/20 | 08/14/20 | |||||||

| 07/31/20 | ||||||||

| Indexes | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| GFI | A_COVID_I | MI | TI | UI | VI | COVID_I | Ciustk.news | Ciustk.mac | Ciustk.cmp |

| 04/03/20 | 05/22/20 | 05/22/20 | 03/05/20 | 06/01/20 | 04/03/20 | 05/15/20 | 04/13/20 | 04/01/20 | 04/13/20 |

| 10/23/20 | 06/05/20 | 10/20/20 | 03/27/20 | 10/22/20 | 11/06/20 | 06/05/20 | 05/29/20 | 07/07/20 | 05/28/20 |

| 08/13/20 | 05/21/20 | 08/14/20 | 07/30/20 | 10/06/20 | 07/08/20 | ||||

| 05/29/20 | 08/26/20 | ||||||||

| 09/23/20 | |||||||||

| New Index | Stock Market Index | ||||||

|---|---|---|---|---|---|---|---|

| MEXBOL | BOVESPA | COLCAP | IPSA | IGBVL | MARVEL | S&P | |

| CII_M | x | ||||||

| MHI_B | x | ||||||

| CII_B | x | ||||||

| MCI_B | x | ||||||

| MHI_C | x | ||||||

| CII_C | x | ||||||

| PI_CH | x | ||||||

| MCI_CH | x | ||||||

| SI_P | x | ||||||

| CII_P | x | ||||||

| FNI_A | x | ||||||

| MCI_A | x | ||||||

| PI_US | x | ||||||

| FNI_US | x | ||||||

| CII_US | x | ||||||

| GFI | x | x | x | x | x | x | x |

| A_COVID_I | x | x | x | ||||

| MI | x | x | |||||

| TI | x | x | x | x | |||

| UI | x | x | x | ||||

| VI | x | x | x | x | |||

| COVID_I | x | x | x | x | |||

| Ciustk.news | x | x | x | x | x | x | x |

| Ciustk.mac | x | x | x | x | x | ||

| Ciustk.cmp | x | x | x | x | x | x | x |

| EMV-ID | x | x | x | x | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Coronado, S.; Martinez, J.N.; Gualajara, V.; Romero-Meza, R.; Rojas, O. Time-Varying Granger Causality of COVID-19 News on Emerging Financial Markets: The Latin American Case. Mathematics 2023, 11, 394. https://doi.org/10.3390/math11020394

Coronado S, Martinez JN, Gualajara V, Romero-Meza R, Rojas O. Time-Varying Granger Causality of COVID-19 News on Emerging Financial Markets: The Latin American Case. Mathematics. 2023; 11(2):394. https://doi.org/10.3390/math11020394

Chicago/Turabian StyleCoronado, Semei, Jose N. Martinez, Victor Gualajara, Rafael Romero-Meza, and Omar Rojas. 2023. "Time-Varying Granger Causality of COVID-19 News on Emerging Financial Markets: The Latin American Case" Mathematics 11, no. 2: 394. https://doi.org/10.3390/math11020394

APA StyleCoronado, S., Martinez, J. N., Gualajara, V., Romero-Meza, R., & Rojas, O. (2023). Time-Varying Granger Causality of COVID-19 News on Emerging Financial Markets: The Latin American Case. Mathematics, 11(2), 394. https://doi.org/10.3390/math11020394