1. Introduction

A Bitcoin halving event is defined as an event that decreases a Bitcoin miner’s reward by half, which occurs roughly every four years [

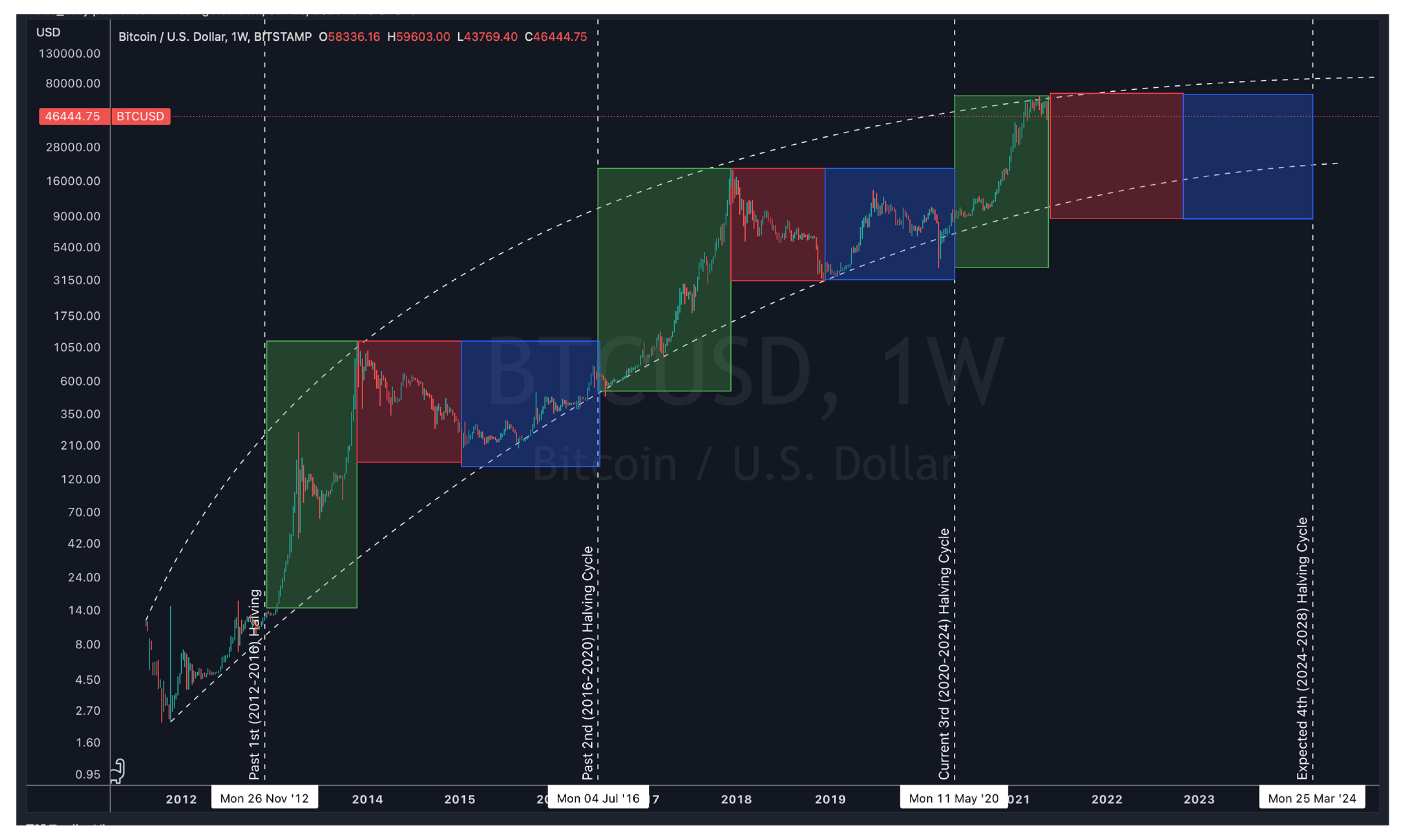

1]. Bitcoin price chart and past studies showed that the halving event impacted Bitcoin price in specific manners that formed the Bitcoin halving cycle.

In

Figure 1, each cycle is segregated by vertical dash lines. Each of the three boxes within a cycle represents the Bitcoin bull market, bear market, and stagnation, respectively. By examining the Bitcoin price chart illustrated in

Figure 1, it can be seen that a Bitcoin halving cycle typically consists of three stages: a one-year bull market, followed by a one-year bear market, followed by a two-year stagnation. During the one-year bull market, Bitcoin surpasses its previous high to achieve a new all-time high, per Meynkhard’s [

1] findings and has stood the test of time as of the time of this writing. It can also be seen in

Figure 1 that Bitcoin is in its third halving cycle and has completed its one-year bull market. Therefore, Bitcoin is expected to be in the one-year bear market stage as of the time of this writing.

There are specific sequences of events during each of the three stages of a Bitcoin halving cycle.

Figure 2,

Figure 3,

Figure 4 and

Figure 5 illustrate the five sequences of events consistently taking place during a bear market in Bitcoin’s past two halving cycles. Below are the five sequences of events:

Occurrence of reversal pattern at an all-time high;

Followed by a 50% crash from the all-time high;

Followed by a recovery back to 20% away from the all-time high;

Followed by a 70% crash from the all-time high;

Eventually bottoming out at 85% from the all-time high.

The Bitcoin halving cycle suggests that Bitcoin price movement follows specific sequences, and is independent of other assets. This has significant implications for Bitcoin properties, encompassing its risk profile, volatility dynamics, safe haven properties, and hedge properties. For instance, Bitcoin should be negatively correlated to the stock market to exhibit safe haven and hedge properties according to the framework proposed by Baur and McDermott [

2]. However, Bitcoin halving cycle implies independence (no correlation) of stock market movements. Given the predictability of the Bitcoin price movement, Bitcoin could exhibit time-varying properties that might not be inherent. Furthermore, given the distinctiveness of the three stages within a cycle, there could be certain volatility dynamics that are specific to each stage. While the Bitcoin halving cycle may impact Bitcoin safe haven, hedge properties, and volatility dynamics, these findings may not hold significance without significant industrial and institutional exposures and interests.

Bitcoin is rapidly gaining recognition as an investment vehicle at the retail, institutional, and federal levels. The deputy governor of the People’s Bank of China (PBOC), Li Bo, acknowledged Bitcoin as an investment alternative [

3]. The first two Bitcoin Exchange Traded Funds (ETF), were approved in Canada and launched in February 2021. In an interview with CNBC in 2021, Rick Rieder, BlackRock’s chief investment officer of global income, revealed that BlackRock, one of the world’s largest asset managers, has entered the Bitcoin space [

4].

Many significant events also occurred in early 2021, suggesting the beginning of the increasing industrial adoption of Bitcoin. These events include big corporations accepting or facilitating payments via Bitcoin, S&P500 companies buying billions of dollars worth in Bitcoin, approval of the first-ever Bitcoin Exchange Traded Funds (ETF), and the world’s largest asset management company entering the Bitcoin space [

4]. Additionally, Apple Pay officially announced support of payments via Bitcoin in February 2021, while Google Pay and Samsung Pay have plans to support payments via Bitcoin in Q1 2021. According to SEC Filings, in January 2021, Tesla Inc., an S&P500 company, purchased USD 1.5 billion worth of Bitcoin for diversification and returned maximization of cash not required to maintain operating liquidity. Tesla Inc. also added that it expects to accept Bitcoin for payments soon.

An aspect of industrial adoption is reflected by the rapid expansion in the Bitcoin supply chain. One component of the supply chain is the Bitcoin mining operation. Several well-known Bitcoin mining companies are Bitfarms, Riot Blockchain, and Marathon Digital Holdings. In May 2020, Bitfarms announced the acquisition of 6600 miners, costing an estimated ~USD 43 million. A company’s Bitcoin mining capacity is measured in hast rate per second (H/s), and Bitfarm’s acquisition of 6600 miners will increase its mining capacity to 2.5 EH/s. Bitfarms stated that the company aims to achieve 8 EH/s by the end of 2022, implying that the company would be required to invest an estimated ~USD 80 mil before 2022 to achieve that milestone. Riot Blockchain, Marathon Digital Holdings, and other mining companies are also aggressively expanding their operations.

Another aspect of industrial adoption is the emergence of crypto-asset exchanges and institutional trading volume. For example, Coinbase went public on 14 April 2021, at a valuation of ~USD 65 billion. It is the second world’s largest crypto exchange after Binance. In addition, Coinbase reported that institutional trading volume was double that of retail trading volume in Q1 2021, citing that institutional interest has surpassed retail traders’ [

5]. With other major crypto exchanges, such as Gemini, also planning to go public, more capital will be invested into Bitcoin and its supply chain.

1.1. Implications of Bitcoin Rapid Adoption and the Halving Cycle

Firstly, the extensive industrial and institutional adoption suggests that the importance of Bitcoin risk assessment is becoming apparent as more capital is being risked into Bitcoin and its supply chain. According to Ark Invest [

6], Bitcoin would be lifted to ~USD 400,000 per coin if institutions allocate 5% of their funds to Bitcoin. Bitcoin’s drastic increase in adoption suggests that its role may go beyond that of the medium of payment or store of value to a hedge against the stock market.

Bitcoin is referred to as digital gold [

7], and this comparison is apt as gold can be used as a hedge against many stock markets [

8]. The notion of Bitcoin as digital gold is echoed by prolific portfolio manager Cathie Wood of ARK Invest. Two common properties of gold are being a safe haven and a hedge against the stock market and economic turmoil [

2,

9,

10]. However, Bitcoin’s role in this context is highly disputed. Some previous studies regarded Bitcoin as a speculative asset based on transaction data [

11,

12], while others believe that Bitcoin exhibits safe haven properties and diversification benefits [

13,

14], implying that the safe haven property of both Bitcoin is dependent on markets, market conditions, time horizon, and other factors such as government intervention and market participant reactions to market events [

15,

16,

17,

18]. Moreover, the properties of Bitcoin and gold could begin to interrelate. There may be signs that funds are flowing out of gold to the Bitcoin [

19]. A recent contrasting finding suggests that gold did not exhibit safe haven properties against one of the US stock indices (S&P500) during the COVID-19 pandemic [

17]. As a result, there might be a possibility that Bitcoin is displacing gold as a safe haven asset amidst the rising momentum of its adoption.

Secondly, the stages and sequences of events in the Bitcoin halving cycle suggest that there may be the existence of regimes in Bitcoin volatility dynamics during each stage or sequence of events. A deeper open problem suggested by past studies [

20] is the lack of a fundamental approach to assessing the value and risk of Bitcoin. The potential existence of regimes that are associated with different stages in the Bitcoin halving cycle will only add to the challenges of Bitcoin risk assessment. For instance, Value-at-risk (VaR) is one of the statistical measurements that assess Bitcoin volatility over a specific time frame by determining Bitcoin probability and severity of losses. Since VaR is sensitive toward volatility, regime changes can cause the VaR computed throughout low volatility to understate the actual risk level. Aside from the potential existence of regimes associated with the Bitcoin cycle, black-swan events, such as the COVID-19 pandemic, can also result in the same effect.

The lack of a fundamental approach to Bitcoin risk assessment also has another set of significant implications for Altcoins such as Ethereum (ETH). Agosto and Cafferata [

20] examined the co-explosivity in the crypto market and the interdependencies of crypto prices. The authors found high interdependence in the crypto market and that the Bitcoin explosive periods also coincide with the Altcoins’. This finding also aligns with other recent notable studies [

21,

22,

23]. For instance, Bitcoin is found to be negatively related to Ripple (XRP), and this negative relationship is amplified during bubble periods. The interdependence between cryptocurrency prices, such as the Bitcoin–Ripple relationship, is found to be related to the function of the cryptocurrencies.

In short, due to the extent of Bitcoin’s impact on the wider crypto market, it is even more essential to access the Bitcoin risk assessment (VaR) under specific contexts (or regimes). Limited past studies considered the Bitcoin risk assessment (VaR) in the context of the recent COVID-19 pandemic, a spike in the USA’s money supply, and a drastic increase in industrial and institutional participation in Bitcoin and Bitcoin supply chain. Furthermore, Bitcoin completed its second halving cycle in May 2020 and entered its third cycle.

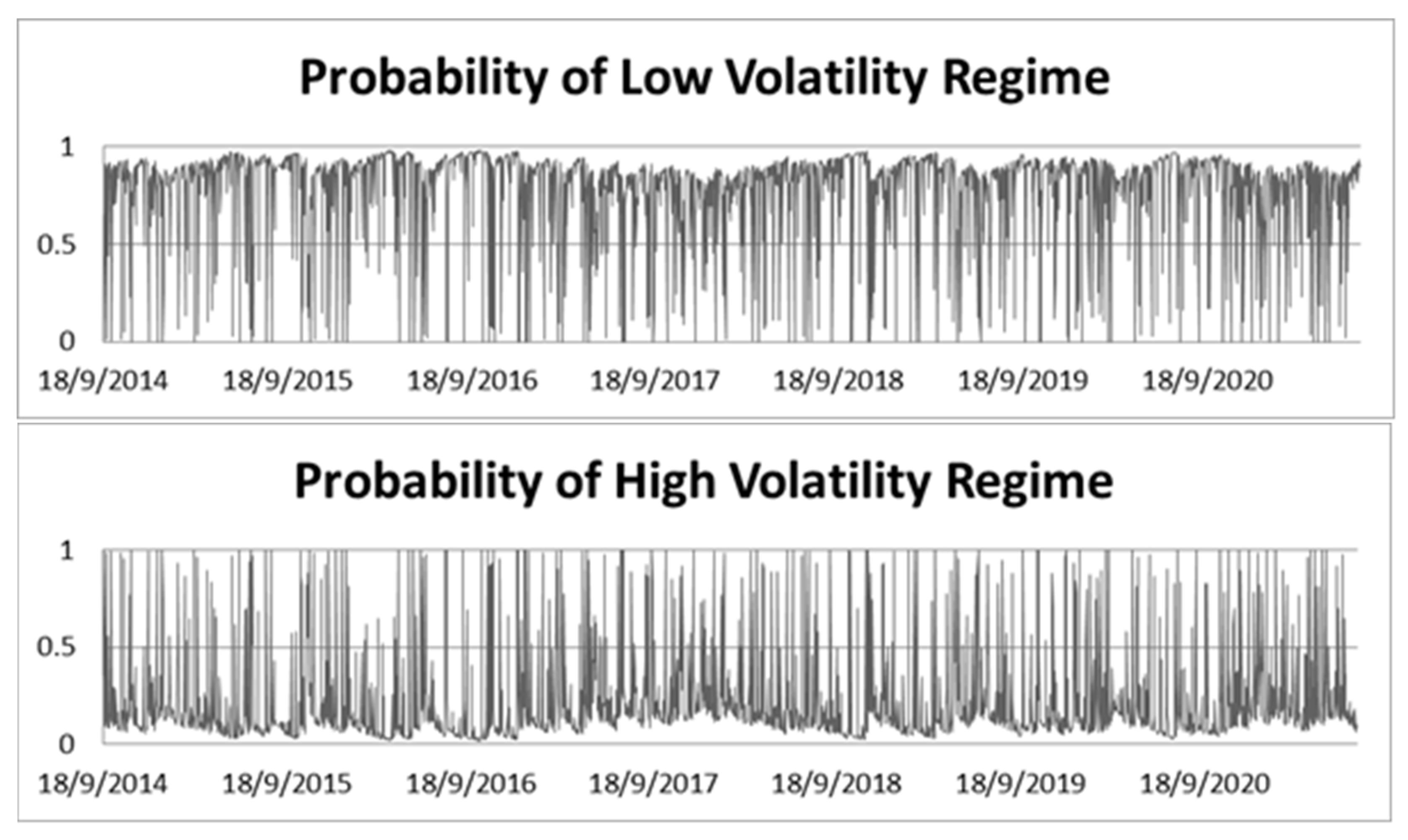

Ardia, Bluteau, and Rüede [

24] found that regime changes existed in the Bitcoin GARCH volatility dynamics between 19 August 2011, and 2 March 2018. The authors accounted for regime changes in Bitcoin volatility using regime-switching GARCH models, such as the Markov Switching GARCH (MSGARCH) model. The authors found that regime-switching GARCH models suited Bitcoin volatility better than a single-regime GARCH based on Deviance Information Criterion (DIC) and VaR forecasting. Maciel [

25] also reported similar findings during this period and showed that regime-switching GARCH forecasted VaR more accurately than its single-regime counterparts. There is also a similar recent study that analyzed how prices transit between different regimes (“bull”, “stable, and “bear”), but this study examines the Bitcoin price dynamics at a more granular level based on the unique and well-defined decade-old four-year cycle consisting of three phases with distinctive sequences of events illustrated in

Figure 1,

Figure 2 and

Figure 3.

1.2. Objective

Therefore, the goal of this study is twofold: (1) to examine the safe haven and hedge properties of gold and Bitcoin specifically against the US stock indices before and after the market crash in March 2020; (2) to examine Bitcoin volatility dynamics via Markov-Switching (MS) GARCH models under the above-mentioned context. This work primarily extends the two past studies where one study, [

26], examined the safe haven and hedge properties of Bitcoin and gold against the G7 stock market indices between 2010–2018, while the other, [

24], studied the regime changes existed in Bitcoin GARCH volatility dynamics between 2011–2018. This study extends these two past studies by investigating periods after 2018 (from 2017 to 2021) where the COVID-19 black-swan event and major developments in Bitcoin adoption occurred that could displace gold.

5. Conclusions

This study introduces a unique perspective on the Bitcoin safe haven and hedge properties through Bitcoin’s decade-old halving cycle. This study showed that Bitcoin halving cycle might be able to explain the time-varying safe haven and hedge properties reported by previous studies [

15,

16,

17,

18], where time periods with safe haven and hedge properties might coincide with periods of negative correlation (as required by Baur and McDermott’s framework [

2]). This might also be the reason Bitcoin failed to exhibit safe haven and hedge properties despite major industrial and institutional Bitcoin adoption and the fund outflow from gold into Bitcoin. Practically, this finding suggests that investors should not invest in Bitcoin for Bitcoin safe haven and hedge properties because time periods with safe haven and hedge properties might coincide with periods of negative correlation. On the other hand, this study provided additional evidence showing that gold also failed to exhibit safe haven and hedge properties after the pandemic; this aligns with the findings of past studies. One possible explanation for gold’s loss of safe haven and hedge properties is the funds’ outflow from gold-related ETFs during the pandemic. Since Bitcoin also failed to exhibit safe haven and hedge properties, Bitcoin has yet to displace gold as the new safe haven commodity.

As shown in this study, Bitcoin halving cycle is well-defined in terms of price volatility and timing and is also independent (not correlated) to the stock market. This violates one of the conditions required, proposed by Baur and McDermott [

2], to exhibit safe haven and hedge properties, which are a negative correlation to the stock market. Therefore, in this respect, findings related to the safe haven and hedge properties of Bitcoin and gold may not extrapolate beyond the COVID-19 black-swan event and should be reinvestigated in the future.

Findings related to regime changes in Bitcoin’s GARCH volatility dynamics could be extrapolated well beyond the COVID-19 black-swan event, as this study is consistent with the findings from past studies before the COVID-19 pandemic. This study found that regimes do exist in Bitcoin’s GARCH volatility dynamics through the pandemic. Therefore, the Markov-switching model remains recommended over its single-regime counterparts with low and high volatility periods rather than the distinct stages of a Bitcoin halving cycle. Moreover, the relationship between low and high volatility regimes are asymmetric. Future studies could consider using more recent techniques to improve the robustness of the safe haven and hedge properties framework [

2] and regime change models [

24] to better address Bitcoin’s time-varying properties. We also recommend future studies revisit Bitcoin safe haven and hedge properties in the future as continued industrial and institutional adoption may break Bitcoin’s decade-old halving cycle.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}