Modeling Electricity Price Dynamics Using Flexible Distributions

Abstract

:1. Introduction

2. Literature Review

3. Methodology

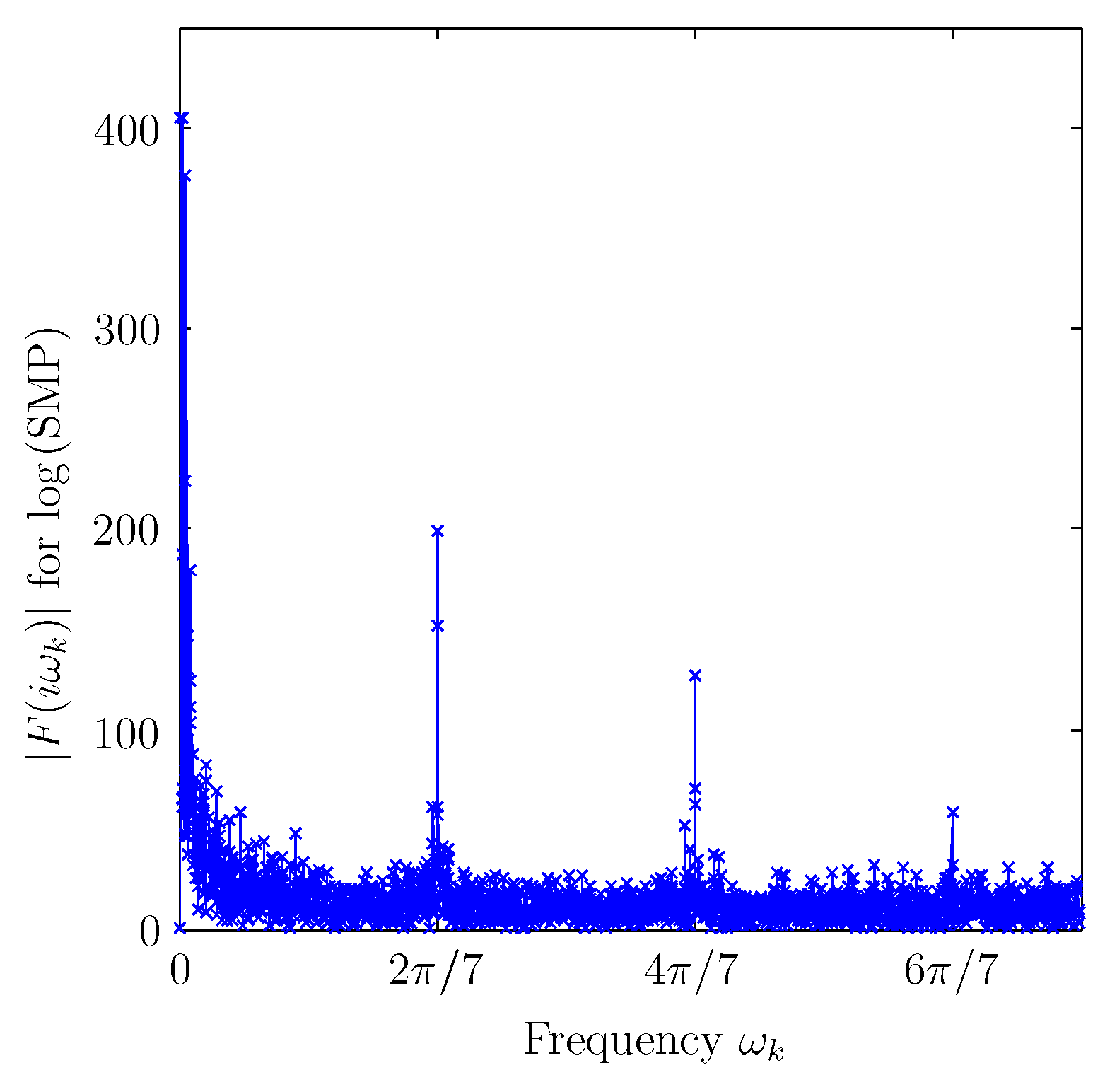

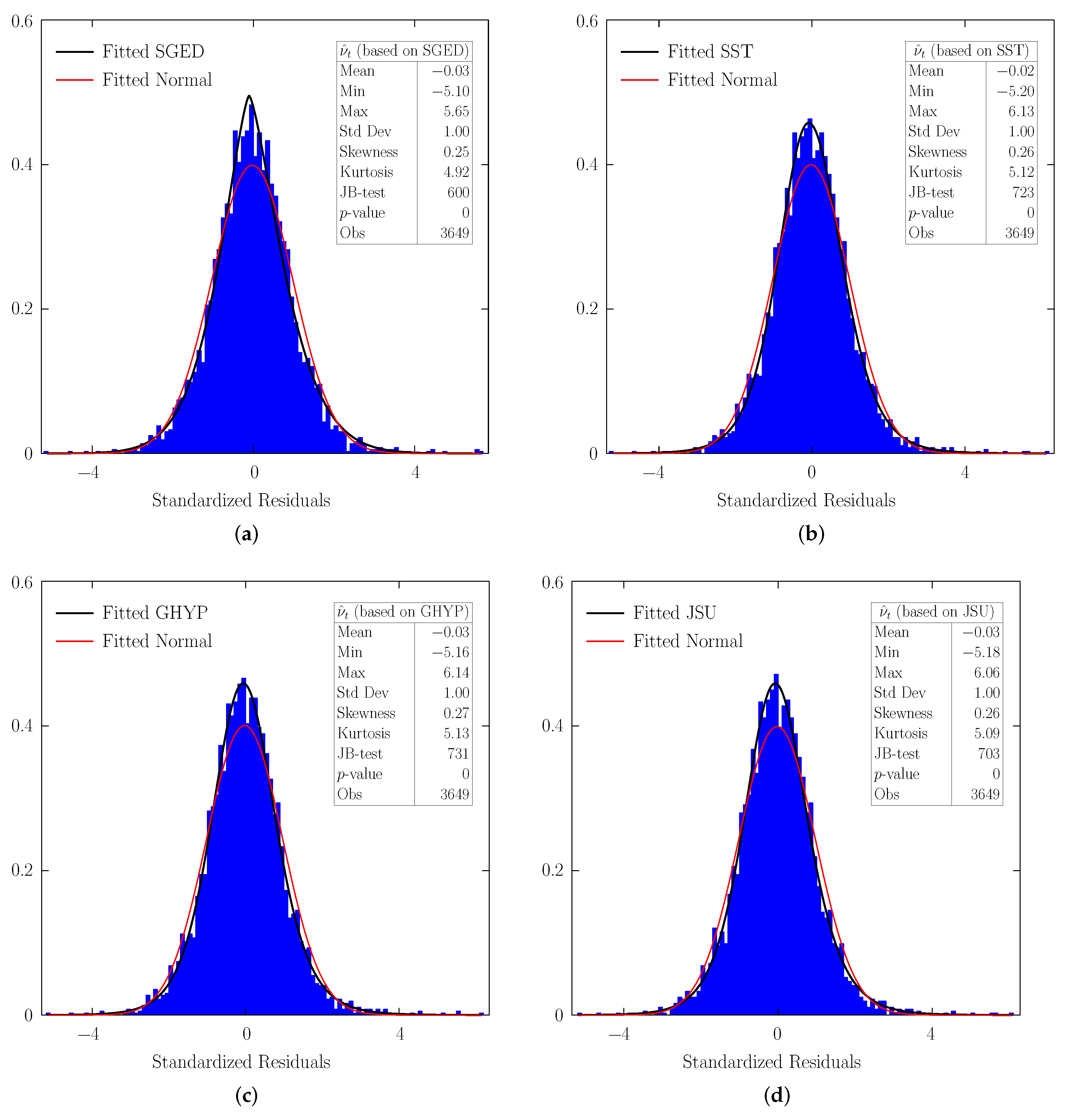

4. Estimation Results

5. Discussion

6. Conclusions and Policy Implications

Funding

Acknowledgments

Conflicts of Interest

Nomenclature

| Mean parameter | |

| Standard deviation parameter | |

| Shape parameter | |

| Skewness parameter | |

| Peakedness parameter | |

| Gamma function defined as | |

| Set of real numbers | |

| -test | Goodness of fit test |

| p-value | Probability value of a test statistic |

| (if p-value is less than 0.10, then the null hypothesis is rejected) | |

| Natural logarithm of SMP from the peak-demand period of day t | |

| Residuals from the mean equation (not standardized) | |

| Conditional variance or volatility (based on notation in [23]) | |

| Normal distribution with zero mean and conditional variance | |

| Information set at time (based on notation in [23]) | |

| The indicator function equal to 1 if and 0 otherwise | |

| Standardized residuals |

Abbreviations

| AIC | Akaike Information Criterion |

| AR | Autoregressive |

| ARCH | Autoregressive Conditional Heteroscedasticity |

| BDS-test | Brock–Dechert–Scheinkman test of i.i.d. |

| Coef of Var | Coefficient of Variation |

| COVID-19 | Corona Virus Disease 2019 |

| GARCH | Generalized Autoregressive Conditional Heteroscedasticity |

| GED | Generalized Error Distribution |

| GHYP | Generalized Hyperbolic Distribution |

| i.i.d. | independent and identically distributed |

| JB-test | Jarque–Bera normality test [31] |

| JSU | Johnson’s distribution |

| Obs | Number of Observations |

| Regime 1 | April 1990–March 1993 (Coal contracts), Reference period |

| Regime 2 | April 1993–March 1994 |

| Regime 3 | April 1994–March 1996 (Price-cap regulation) |

| Pre-Regime 4 | April 1996–July 1996 |

| Regime 4 | July 1996–July 1999 (Divestment 1 introduced on 1 July 1996) |

| Regime 5 | July 1999–March 2001 (Divestment 2 introduced on 20 July 1999) |

| SGED | Skew Generalized Error Distribution |

| SMP | System Marginal Price |

| SST | Skew Student’s t distribution |

| St Dev | Standard Deviation |

References

- Hadsell, L.; Marathe, A.; Shawky, H.A. Estimating the volatility of wholesale electricity spot prices in the US. Energy J. 2004, 25, 23–40. [Google Scholar] [CrossRef] [Green Version]

- Bessembinder, H.; Lemmon, M.L. Equilibrium pricing and optimal hedging in electricity forward markets. J. Financ. 2002, 57, 1347–1382. [Google Scholar] [CrossRef]

- Herrera, A.M.; Hu, L.; Pastor, D. Food price volatility and macroeconomic factors: Evidence from GARCH and GARCH-X estimates. Int. J. Forecast. 2018, 34, 622–635. [Google Scholar] [CrossRef]

- Ziel, F.; Weron, R. Day-ahead electricity price forecasting with high-dimensional structures: Univariate vs. multivariate modeling frameworks. Energy Econ. 2018, 70, 396–420. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Y.J.; Yao, T.; Ripple, R. Volatility forecasting of crude oil market: Can the regime switching GARCH model beat the single-regime GARCH models? Int. Rev. Econ. Financ. 2019, 59, 302–317. [Google Scholar] [CrossRef]

- Hasanov, A.S.; Shaiban, M.S.; Al-Freedi, A. Forecasting volatility in the petroleum futures markets: A re-examination and extension. Energy Econ. 2020, 86, 104626. [Google Scholar] [CrossRef]

- Nonejad, N. Crude oil price volatility and equity return predictability: A comparative out-of-sample study. Int. Rev. Financ. Anal. 2020, 71, 101521. [Google Scholar] [CrossRef]

- Dutta, A.; Bouri, E.; Roubaud, D. Modelling the volatility of crude oil returns: Jumps and volatility forecasts. Int. J. Financ. Econ. 2021, 26, 889–897. [Google Scholar] [CrossRef]

- Kocaarslan, B.; Soytas, U. Reserve currency and the volatility of clean energy stocks: The role of uncertainty. Energy Econ. 2021, 104, 105645. [Google Scholar] [CrossRef]

- Luo, J.; Demirer, R.; Gupta, R.; Ji, Q. Forecasting oil and gold volatilities with sentiment indicators under structural breaks. Energy Econ. 2022, 105, 105751. [Google Scholar] [CrossRef]

- Xu, Y.; Lien, D. Forecasting volatilities of oil and gas assets: A comparison of GAS, GARCH, and EGARCH models. J. Forecast. 2022, 41, 259–278. [Google Scholar] [CrossRef]

- Bowden, N.; Payne, J.E. Short term forecasting of electricity prices for MISO hubs: Evidence from ARIMA-EGARCH models. Energy Econ. 2008, 30, 3186–3197. [Google Scholar] [CrossRef]

- Escribano, A.; Peña, J.I.; Villaplana, P. Modelling electricity prices: International evidence. Oxf. Bull. Econ. Stat. 2011, 73, 622–650. [Google Scholar] [CrossRef] [Green Version]

- Geman, H.; Roncoroni, A. Understanding the fine structure of electricity prices. J. Bus. 2006, 79, 1225–1261. [Google Scholar] [CrossRef] [Green Version]

- Zhou, F.; Huang, Z.; Zhang, C. Carbon price forecasting based on CEEMDAN and LSTM. Appl. Energy 2022, 311, 118601. [Google Scholar] [CrossRef]

- Evans, J.E.; Green, R.J. Why Did British Electricity Prices Fall after 1998? MIT Center for Energy and Environmental Policy Research Working Paper Series No. 03-007; MIT Center: Cambridge, MA, USA, 2003. [Google Scholar]

- Koopman, S.J.; Ooms, M.; Carnero, M.A. Periodic seasonal Reg-ARFIMA-GARCH models for daily electricity spot prices. J. Am. Stat. Assoc. 2007, 102, 16–27. [Google Scholar] [CrossRef] [Green Version]

- Abramova, E.; Bunn, D. Forecasting the intra-day spread densities of electricity prices. Energies 2020, 13, 687. [Google Scholar] [CrossRef] [Green Version]

- Joskow, P.L. Foreword: US vs. EU Electricity Reforms Achievement. In Electricity Reform in Europe; Glachant, J.M., Lévêque, F., Eds.; Edward Elgar Publishing Limited: Cheltenham, UK, 2009. [Google Scholar]

- Robinson, T.; Baniak, A. The volatility of prices in the English and Welsh electricity pool. Appl. Econ. 2002, 34, 1487–1495. [Google Scholar] [CrossRef]

- Tashpulatov, S.N. Estimating the volatility of electricity prices: The case of the England and Wales wholesale electricity market. Energy Policy 2013, 60, 81–90. [Google Scholar] [CrossRef] [Green Version]

- Tashpulatov, S.N. The impact of behavioral and structural remedies on electricity prices: The case of the England and Wales electricity market. Energies 2018, 11, 3420. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroscedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Nelson, D.B. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the relation between the expected value and the volatility of the nominal excess returns on stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Hansen, P.R.; Lunde, A. A forecast comparison of volatility models: Does anything beat a GARCH(1,1)? J. Appl. Econom. 2005, 20, 873–889. [Google Scholar] [CrossRef] [Green Version]

- Charles, A.; Darné, O. Forecasting crude-oil market volatility: Further evidence with jumps. Energy Econ. 2017, 67, 508–519. [Google Scholar] [CrossRef]

- Ergen, I.; Rizvanoghlu, I. Asymmetric impacts of fundamentals on the natural gas futures volatility: An augmented GARCH approach. Energy Econ. 2016, 56, 64–74. [Google Scholar] [CrossRef]

- Klein, T.; Walther, T. Oil price volatility forecast with mixture memory GARCH. Energy Econ. 2016, 58, 46–58. [Google Scholar] [CrossRef] [Green Version]

- Jarque, C.M.; Bera, A.K. A test for normality of observations and regression residuals. Int. Stat. Rev. 1987, 55, 163–172. [Google Scholar] [CrossRef]

- Ewing, B.; Malik, F. Modelling asymmetric volatility in oil prices under structural breaks. Energy Econ. 2017, 63, 227–233. [Google Scholar] [CrossRef]

- Shalini, V.; Prasanna, K. Impact of the financial crisis on Indian commodity markets: Structural breaks and volatility dynamics. Energy Econ. 2016, 53, 40–57. [Google Scholar] [CrossRef]

- Wangsness, P.B.; Halse, A.H. The impact of electric vehicle density on local grid costs: Empirical evidence from Norway. Energy J. 2021, 42, 149–167. [Google Scholar] [CrossRef]

- Koopman, S.J.; Lukas, A.; Scharth, M. Predicting time-varying parameters with parameter-driven and observation-driven models. Rev. Econ. Stat. 2016, 98, 97–110. [Google Scholar] [CrossRef] [Green Version]

- Gosset, W.S. The probable error of a mean. Biometrika 1908, 6, 1–24. [Google Scholar]

- Subbotin, M.T.H. On the law of frequency of error. Mat. Sb. 1923, 31, 296–301. [Google Scholar]

- Box, G.E.P.; Tiao, G.C. Bayesian Inference in Statistical Analysis; Addison-Wesley Publishing Co.: Reading, MA, USA, 1973. [Google Scholar]

- Bosco, B.P.; Parisio, L.P.; Pelagatti, M.M. Deregulated wholesale electricity prices in Italy: An empirical analysis. Int. Adv. Econ. Res. 2007, 13, 415–432. [Google Scholar] [CrossRef]

- Fernández, C.; Steel, M. On Bayesian modeling of fat tails and skewness. J. Am. Stat. Assoc. 1998, 93, 359–371. [Google Scholar]

- Hansen, B.E. Autoregressive conditional density estimation. Int. Econ. Rev. 1994, 35, 705–730. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E. Exponentially decreasing distributions for the logarithm of particle size. Proc. R. Soc. Lond. A Math. Phys. Eng. Sci. 1977, 353, 401–419. [Google Scholar]

- Johnson, N.L. Systems of frequency curves derived from the first law of Laplace. Trab. Estad. 1954, 5, 283–291. [Google Scholar] [CrossRef]

- Lee, Y.H.; Pai, T.Y. REIT volatility prediction for skew-GED distribution of the GARCH model. Expert Syst. Appl. 2010, 37, 4737–4741. [Google Scholar] [CrossRef]

- Su, J.B. How to mitigate the impact of inappropriate distributional settings when the parametric value-at-risk approach is used. Quant. Financ. 2014, 14, 305–325. [Google Scholar] [CrossRef]

- Theodossiou, P. Skewed generalized error distribution of financial assets and option pricing. Multinatl. Financ. J. 2015, 19, 223–266. [Google Scholar] [CrossRef] [Green Version]

- Ioannidis, F.; Kosmidou, K.; Savva, C.; Theodossiou, P. Electricity pricing using a periodic GARCH model with conditional skewness and kurtosis components. Energy Econ. 2021, 95, 105110. [Google Scholar] [CrossRef]

- Fu, Y.; Zheng, Z. Volatility modeling and the asymmetric effect for China’s carbon trading pilot market. Phys. A Stat. Mech. Its Appl. 2020, 542, 123401. [Google Scholar] [CrossRef]

- Frömmel, M.; Han, X.; Kratochvil, S. Modeling the daily electricity price volatility with realized measures. Energy Econ. 2014, 44, 492–502. [Google Scholar] [CrossRef]

- Eberlein, E.; Keller, U. Hyperbolic distributions in finance. Bernoulli 1995, 1, 281–299. [Google Scholar] [CrossRef]

- Küchler, U.; Neumann, K.; Sørensen, M.; Streller, A. Stock returns and hyperbolic distributions. Math. Comput. Model. 1999, 29, 1–15. [Google Scholar] [CrossRef]

- Frestad, D.; Benth, F.E.; Koekebakker, S. Modeling term structure dynamics in the Nordic electricity swap market. Energy J. 2010, 31, 53–86. [Google Scholar] [CrossRef] [Green Version]

- Simonato, J.G. American option pricing under GARCH with non-normal innovations. Optim. Eng. 2019, 20, 853–880. [Google Scholar] [CrossRef]

- Lízal, L.M.; Tashpulatov, S.N. Do producers apply a capacity cutting strategy to increase prices? The case of the England and Wales electricity market. Energy Econ. 2014, 43, 114–124. [Google Scholar] [CrossRef]

- Tashpulatov, S.N. Analysis of electricity industry liberalization in Great Britain: How did the bidding behavior of electricity producers change? Util. Policy 2015, 36, 24–34. [Google Scholar] [CrossRef] [Green Version]

- National Grid Company. Seven Year Statement; National Grid Company: Coventry, UK, 1994–2001. [Google Scholar]

- Kullback, S.; Leibler, R.A. On information and sufficiency. Ann. Math. Stat. 1951, 22, 16–27. [Google Scholar] [CrossRef]

- Brock, W.A.; Dechert, W.D.; Scheinkman, J.A.; LeBaron, B. A test for independence based on the correlation dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- White, H. Maximum likelihood estimation of misspecified models. Econometrica 1982, 50, 1–25. [Google Scholar] [CrossRef]

- Erdogdu, E. Asymmetric volatility in European day-ahead power markets: A comparative microeconomic analysis. Energy Econ. 2016, 56, 398–409. [Google Scholar] [CrossRef] [Green Version]

- Lin, Y.; Xiao, Y.; Li, F. Forecasting crude oil price volatility via a HM-EGARCH model. Energy Econ. 2020, 87, 104693. [Google Scholar] [CrossRef]

- Tashpulatov, S.N. The impact of regulatory reforms on demand weighted average prices. Mathematics 2021, 9, 1112. [Google Scholar] [CrossRef]

- European Commission. Summary of Commission Decision of 26 November 2008 relating to a proceeding under Article 82 of the EC Treaty and Article 54 of the EEA Agreement (Cases COMP/39.388—German Electricity Wholesale Market and COMP/39.389—German Electricity Balancing Market). Off. J. Eur. Union 2009, 52, 8. [Google Scholar]

- Poddar, D.; Kalic, N.; Hersey, E.; van Werkum, R. Divestment Powers for the Australian Electricity Market—Is Its Bark Worse Than Its Bite? Clifford Chance: London, UK, 2019; pp. 1–5. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Price | Regime 1 | Regime 2 | Regime 3 | Pre-Regime 4 | Regime 4 | Regime 5 |

|---|---|---|---|---|---|---|

| Apr 90–Mar 93 | Apr 93–Mar 94 | Apr 94–Mar 96 | Apr 96–July 96 | July 96–July 99 | July 99–Mar 01 | |

| Coal Contracts | Price-Cap Reg | Divestment 1 | Divestment 2 | |||

| Mean | 25.66 | 32.90 | 37.22 | 35.25 | 41.99 | 35.91 |

| Min | 14.78 | 14.94 | 7.88 | 17.17 | 14.54 | 12.15 |

| Max | 62.97 | 55.95 | 211.24 | 76.74 | 105.09 | 77.89 |

| St Dev | 4.69 | 6.52 | 17.64 | 11.39 | 19.29 | 11.95 |

| Coef of Var (%) | 18.26 | 19.81 | 47.40 | 32.30 | 45.95 | 33.28 |

| Obs | 1096 | 365 | 731 | 91 | 1114 | 616 |

| Assumed Distribution Intercepts and Variables | SGED | SST | GHYP | JSU | |||||

|---|---|---|---|---|---|---|---|---|---|

| Coef | Std Err | Coef | Std Err | Coef | Std Err | Coef | Std Err | ||

| Mean Equation | −0.3728 *** | 0.0147 | −0.4892 *** | 0.0872 | −0.4976 *** | 0.0936 | −0.4792 *** | 0.0803 | |

| 0.3110 *** | 0.0091 | 0.3066 *** | 0.0069 | 0.3061 *** | 0.0107 | 0.3069 *** | 0.0019 | ||

| 0.1388 *** | 0.0060 | 0.1422 *** | 0.0195 | 0.1417 * | 0.0730 | 0.1413 *** | 0.0306 | ||

| 0.0362 *** | 0.0022 | 0.0381 | 0.0258 | 0.0380 | 0.0278 | 0.0382 ** | 0.0186 | ||

| 0.0577 *** | 0.0119 | 0.0569 *** | 0.0214 | 0.0573 *** | 0.0165 | 0.0572 *** | 0.0165 | ||

| 0.1306 *** | 0.0051 | 0.1304 *** | 0.0192 | 0.1303 *** | 0.0258 | 0.1303 *** | 0.0270 | ||

| 0.1759 *** | 0.0061 | 0.1705 *** | 0.0308 | 0.1708 *** | 0.0082 | 0.1713 *** | 0.0192 | ||

| −0.0486 *** | 0.0096 | −0.0468 | 0.0310 | −0.0468 * | 0.0282 | −0.0472 ** | 0.0193 | ||

| −0.0484 *** | 0.0065 | −0.0445 ** | 0.0217 | −0.0441 ** | 0.0175 | −0.0446 *** | 0.0172 | ||

| 0.1320 *** | 0.0052 | 0.1275 *** | 0.0179 | 0.1276 *** | 0.0204 | 0.1281 *** | 0.0206 | ||

| −0.0421 *** | 0.0076 | −0.0422 * | 0.0248 | −0.0421 ** | 0.0198 | −0.0421 ** | 0.0165 | ||

| 0.0988 *** | 0.0043 | 0.1020 *** | 0.0168 | 0.1022 *** | 0.0185 | 0.1017 *** | 0.0186 | ||

| −0.0534 *** | 0.0063 | −0.0546 *** | 0.0191 | −0.0550 *** | 0.0162 | −0.0551 *** | 0.0163 | ||

| −0.0449 *** | 0.0090 | −0.0435 *** | 0.0151 | −0.0438 *** | 0.0131 | −0.0437 *** | 0.0127 | ||

| 0.0372 *** | 0.0040 | 0.0386 ** | 0.0151 | 0.0390 *** | 0.0129 | 0.0388 *** | 0.0121 | ||

| −0.0286 *** | 0.0048 | −0.0264 ** | 0.0123 | −0.0265 | 0.0177 | −0.0267 *** | 0.0065 | ||

| 0.0669 *** | 0.0107 | 0.0655 *** | 0.0111 | 0.0655 *** | 0.0112 | 0.0654 *** | 0.0102 | ||

| 0.0616 *** | 0.0015 | 0.0723 *** | 0.0028 | 0.0731 *** | 0.0051 | 0.0714 *** | 0.0006 | ||

| Regime 2 | 0.0206 *** | 0.0055 | 0.0201 ** | 0.0082 | 0.0203 | 0.0144 | 0.0202 *** | 0.0056 | |

| Regime 3 | 0.0353 *** | 0.0097 | 0.0344 *** | 0.0114 | 0.0354 * | 0.0196 | 0.0352 *** | 0.0087 | |

| Pre-Regime 4 | 0.0246 | 0.0325 | 0.0273 | 0.0334 | 0.0287 | 0.0377 | 0.0277 | 0.0321 | |

| Regime 4 | 0.0315 *** | 0.0087 | 0.0286 ** | 0.0127 | 0.0294 | 0.0237 | 0.0295 *** | 0.0060 | |

| Regime 5 | −0.0037 | 0.0097 | −0.0023 | 0.0121 | −0.0019 | 0.0187 | −0.0020 | 0.0084 | |

| 0.0080 ** | 0.0033 | 0.0079 ** | 0.0039 | 0.0079 * | 0.0043 | 0.0079 ** | 0.0040 | ||

| −0.0136 *** | 0.0021 | −0.0141 *** | 0.0040 | −0.0138 *** | 0.0040 | −0.0139 *** | 0.0040 | ||

| −0.0111 *** | 0.0029 | −0.0117 *** | 0.0037 | −0.0115 *** | 0.0036 | −0.0114 *** | 0.0036 | ||

| −0.0117 *** | 0.0033 | −0.0115 *** | 0.0035 | −0.0114 *** | 0.0036 | −0.0115 *** | 0.0036 | ||

| 0.0105 *** | 0.0033 | 0.0105 *** | 0.0035 | 0.0106 *** | 0.0034 | 0.0104 *** | 0.0034 | ||

| Volatility Equation | 0.0037 *** | 0.0005 | 0.0037 *** | 0.0006 | 0.0037 *** | 0.0005 | 0.0036 *** | 0.0005 | |

| 0.1571 *** | 0.0367 | 0.1653 *** | 0.0386 | 0.1674 *** | 0.0395 | 0.1646 *** | 0.0383 | ||

| 0.0810 *** | 0.0205 | 0.0903 *** | 0.0219 | 0.0900 *** | 0.0216 | 0.0888 *** | 0.0215 | ||

| 0.0314 ** | 0.0156 | 0.0229 | 0.0166 | 0.0218 | 0.0164 | 0.0242 | 0.0162 | ||

| 0.0412 ** | 0.0194 | 0.0378 * | 0.0195 | 0.0388 * | 0.0208 | 0.0385 ** | 0.0193 | ||

| 0.0761 *** | 0.0244 | 0.0776 *** | 0.0245 | 0.0785 *** | 0.0246 | 0.0780 *** | 0.0246 | ||

| 0.0903 *** | 0.0247 | 0.1091 *** | 0.0271 | 0.1101 *** | 0.0280 | 0.1066 *** | 0.0261 | ||

| 0.0961 *** | 0.0224 | 0.0941 *** | 0.0226 | 0.0922 *** | 0.0225 | 0.0933 *** | 0.0223 | ||

| 0.0802 | 0.0522 | 0.0882 | 0.0539 | 0.0829 | 0.0540 | 0.0845 | 0.0534 | ||

| Regime 2 | 0.0038 *** | 0.0011 | 0.0041 *** | 0.0012 | 0.0041 *** | 0.0012 | 0.0040 *** | 0.0012 | |

| Regime 3 | 0.0287 *** | 0.0038 | 0.0277 *** | 0.0040 | 0.0283 *** | 0.0040 | 0.0280 *** | 0.0040 | |

| Pre-Regime 4 | 0.0547 *** | 0.0179 | 0.0559 *** | 0.0183 | 0.0570 *** | 0.0184 | 0.0559 *** | 0.0182 | |

| Regime 4 | 0.0336 *** | 0.0042 | 0.0324 *** | 0.0043 | 0.0326 *** | 0.0044 | 0.0325 *** | 0.0043 | |

| Regime 5 | 0.0280 *** | 0.0043 | 0.0275 *** | 0.0045 | 0.0279 *** | 0.0045 | 0.0275 *** | 0.0044 | |

| 0.0031 *** | 0.0006 | 0.0034 *** | 0.0006 | 0.0033 *** | 0.0007 | 0.0033 *** | 0.0006 | ||

| 1.4254 *** | 0.0459 | 6.8967 *** | 0.7803 | 0.0290 ** | 0.0130 | 1.9448 *** | 0.1241 | ||

| 1.0539 *** | 0.0225 | 1.0431 *** | 0.0253 | 0.9946 *** | 0.0007 | 0.1625 ** | 0.0759 | ||

| −3.4734 *** | 0.3959 | ||||||||

| SGED | SST | GHYP | JSU | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dimension | 2 | 0.46 | 0.13 | 0.15 | 0.23 | 0.30 | 0.09 | 0.09 | 0.11 | 0.31 | 0.09 | 0.09 | 0.15 | 0.32 | 0.10 | 0.10 | 0.15 |

| 3 | 0.30 | 0.15 | 0.12 | 0.17 | 0.13 | 0.08 | 0.06 | 0.07 | 0.15 | 0.08 | 0.06 | 0.11 | 0.15 | 0.09 | 0.06 | 0.10 | |

| 4 | 0.12 | 0.18 | 0.12 | 0.20 | 0.04 | 0.08 | 0.06 | 0.10 | 0.04 | 0.09 | 0.06 | 0.13 | 0.05 | 0.10 | 0.07 | 0.13 | |

| 5 | 0.07 | 0.32 | 0.17 | 0.32 | 0.03 | 0.18 | 0.10 | 0.19 | 0.03 | 0.21 | 0.10 | 0.24 | 0.03 | 0.22 | 0.11 | 0.23 | |

| 6 | 0.10 | 0.68 | 0.40 | 0.71 | 0.05 | 0.46 | 0.30 | 0.52 | 0.06 | 0.51 | 0.30 | 0.57 | 0.05 | 0.52 | 0.32 | 0.55 | |

| Assumed Theoretical Distribution | ||||

|---|---|---|---|---|

| SGED | SST | GHYP | JSU | |

| Sign Bias | 0.45 | 0.12 | 0.13 | 0.14 |

| Negative Sign Bias | 1.28 | 1.35 | 1.33 | 1.33 |

| Positive Sign Bias | 1.55 | 1.91 * | 1.90 * | 1.88 * |

| Joint Effect | 4.68 | 5.75 | 5.70 | 5.62 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tashpulatov, S.N. Modeling Electricity Price Dynamics Using Flexible Distributions. Mathematics 2022, 10, 1757. https://doi.org/10.3390/math10101757

Tashpulatov SN. Modeling Electricity Price Dynamics Using Flexible Distributions. Mathematics. 2022; 10(10):1757. https://doi.org/10.3390/math10101757

Chicago/Turabian StyleTashpulatov, Sherzod N. 2022. "Modeling Electricity Price Dynamics Using Flexible Distributions" Mathematics 10, no. 10: 1757. https://doi.org/10.3390/math10101757

APA StyleTashpulatov, S. N. (2022). Modeling Electricity Price Dynamics Using Flexible Distributions. Mathematics, 10(10), 1757. https://doi.org/10.3390/math10101757