5.3. Poverty Scorecard Analysis

The analysis of the poverty scorecard was performed on the cut-off band score and the category of poor, as shown in

Table 3. Based on those bands, the graduation level of respondents for each band was measured. The cut-off band and categories of poor were adopted from the assessment of measuring the impact of PPAF (Pakistan poverty alleviation fund) interventions using the Pakistan poverty scorecard (

PPAF 2012), where the categories are (1) extremely poor, who are the poor who are at less than or equals to 50% of the poverty line, (2) chronically poor, who are the poor who will remain poor due to their basic characteristics, has structural poverty and are at 50–75% of the poverty line, (3) transitory poor, who are the poor whose level of poverty transition changes due to income or expenditure shocks and are at 75–100% of the poverty line, (4) transitory vulnerable, who are the poor whose level of poverty is susceptible due to income or expenditure shocks and are at 100–125% of the poverty line, (5) transitory non-poor, who are the poor who are at 125–200% of the poverty line and (6) non-poor, who are the people who have a low chance of being poor and thus enjoy a high level of consumption and are at above 200% of the poverty line (

FD 2008;

Haq et al. 2008;

Sean O’Leary et al. 2011;

WB 2007).

The categories of poverty starting from extremely poor to non-poor were identified by PRSP-II (

FD 2008) for further analysis of the severity of poverty (

Sean O’Leary et al. 2011).

Haq et al. (

2008) and Sean

O’Leary et al. (

2011) have also used these six categories of poverty for the analysis and classifications of poor people. Although initially these categories were developed based on expenditure per adult,

PPAF (

2012) has modified and developed these categories based on poverty score with the help of the world bank’s guidelines.

Furthermore, interventions such as microcredit or social mobilizations in Pakistan use a poverty scorecard as a tool to assess the beneficiaries. That is why many reports on poverty or impacts of such types of interventions have performed their analysis with poverty scorecards, including BISP and SRSO. Likewise, in this study, the poverty scorecard has been used for the achievement of the second objective of the study, which was to measure the graduation of respondents on poverty score. As such, these bands and categories of poverty shown in

Table 3 adopted from (

PPAF 2012) were the perfect tools for the analysis and measurement of the poverty score and severity of the poverty. In this study, a total of 708 respondents were surveyed, among those 356 (50.3%) were beneficiaries (treatment group) of CIF and 352 (49.7%) respondents were non-beneficiaries (control group).

Figure 1 represents the comparison of the old and new poverty scorecard of the control group. It shows that in the old poverty scorecard only 16 households (respondents) were in the first category of the poverty band (0–11) named as extremely poor, whereas in the new poverty scorecard there are only 10 households (respondents) in this band. Likewise, it is also shown that 53 households (respondents) were in the second band (12–18) and were chronically poor in the old poverty scorecard, whereas only 27 households (respondents) are in this band in the new poverty scorecard. Furthermore, 8 households (respondents) in the third band (19–23), 15 households (respondents) in the fourth band (24–34) and 7 households (respondents) in the fifth band (35–50) and 2 households (respondents) in the sixth band (51–100) entitled as transitory poor, transitory vulnerable, transitory non-poor and non-poor respectively are available in the new poverty scorecard.

Table 4 presents the detailed figures for the graduation of the control group in each band. The results show that 69 new respondents’ poverty scorecard could be matched with the old poverty scorecard of the control group. Of those 69 respondents, only 41 (59%) respondents graduated on the poverty scorecard. Furthermore, as shown in the table, initially there were 16 households in the first band (0–11), but as per the new poverty scorecard only 2 (12.5%) households remained extremely poor, and 14 (87.5%) households graduated. Among those 14 graduated households, 9 (56.3%) moved to the second band (12–18), 2 (12.5%) moved to the fourth band (24–34), 3 (18.8%) moved to the fifth band (35–50) and were entitled as chronically poor, transitory vulnerable and transitory non-poor, respectively. Likewise, in the second band (12–18) initially, 53 households were there. Among them, 27 (50.9%) households have graduated to the next levels. From those 27 graduated households, 8 (15.1%) moved to the third band (19–23), 13 (24.5%) moved to the fourth band (24–34), 4 (7.5%) moved to the fifth band (35–50) and 2 (3.8%) moved to the sixth band and became transitory poor, transitory vulnerable, transitory non-poor and non-poor, respectively. The overall results show that out of 69 only 2 households have completely come out of poverty and moved to the non-poor category in the control group.

Figure 2 shows the comparison of the old and new poverty scorecard of the treatment group. As per the old poverty scorecards, 93 households (respondents) were there in the first band (0–11), currently, 21 households are found in the first band (0–11). However, in the second band (12–18) only 63 households were there in the old poverty scorecard and, currently, 51 households are there in the poverty scorecard. Furthermore, in the third band (19–23) only 10 households were found, and 31 households are found in the old and current poverty scorecard respectively. Whereas 44 households in the fourth band (24–34), 18 households in the fifth band (35–50) and 1 household in the sixth band (51–100) are found in the current poverty scorecard.

The further break-up of the figures for the graduation of the treatment group in each category is given in

Table 5. In the treatment group, 166 households’ old poverty scorecard was found and matched with the new one, among them 120 (72%) households (respondents) have graduated to the next levels and the remaining 46 households have either not changed their position or gone down.

Moreover, it indicates that in the first band (0–11), 93 households are there, and among them, 14 (15.1%) remained extremely poor, 27 (29%) moved to the second band (12–18), 18 (19.4%) moved to the third band (19–23), 25 (26.9%) moved to the fourth band (24–34) and 8 (8.6%) to the fifth band (35–50), and only 1 (1.1%) moved to the sixth band (51–100) and became chronically poor, transitory poor, transitory vulnerable, transitory non-poor and non-poor, respectively. Furthermore, in the band (12–18) only 5 (7.9%) households have moved downward and became extremely poor, 20 (31.7%) households remained in the same band as chronically poor, 12 (19%) households moved to the third band (19–23), 16 (25.4%) households moved to the fourth band (24–34) and 10 (15.9%) households moved to the fifth band (35–50). However, in the band (19–23), 2 (20%) households have moved down to the first band (0–11), 4 (40%) households have moved down to the second band (19–23), 1 (10%) household remained in the same band and only 3 (30%) households have been graduated to the fourth band (24–34). The overall results show that although 120 (72%) households have graduated in the treatment group, only 1 household has come out of poverty and moved to the non-poor category.

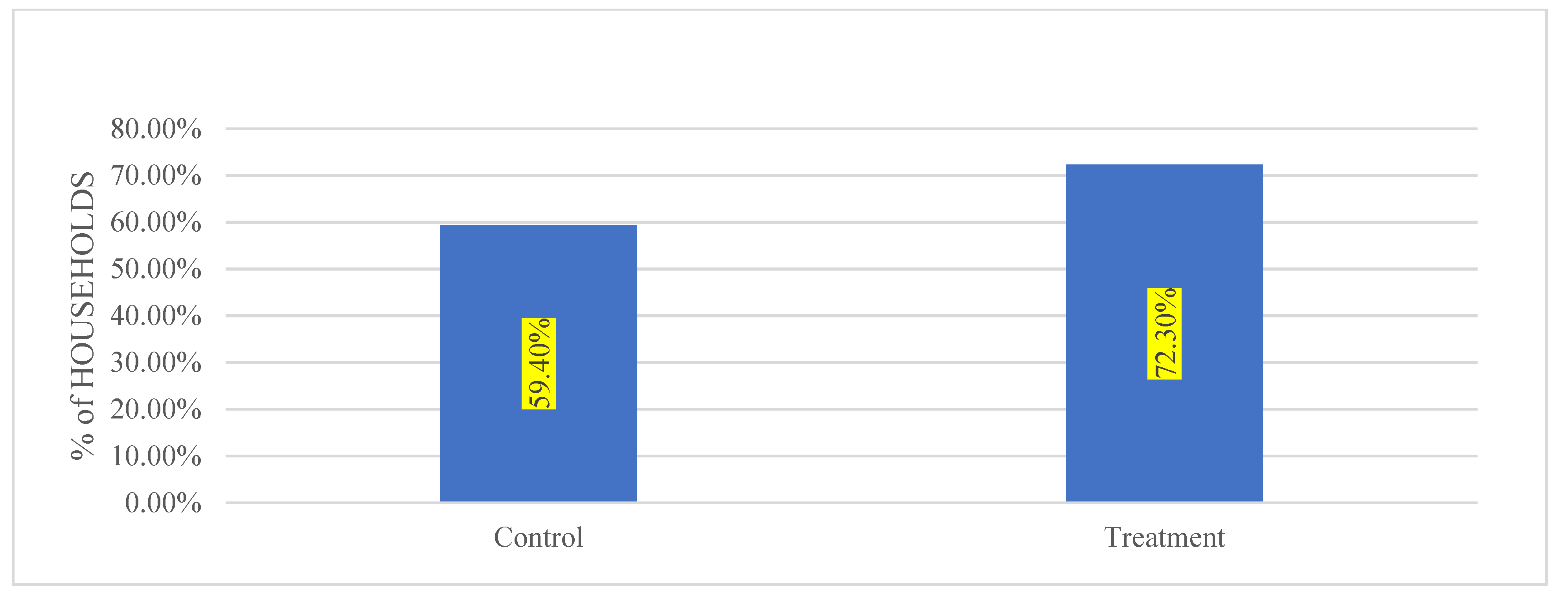

Figure 3 represents the comparison of the graduation of both groups. It shows that only 59.4% of households in the control group graduated as per the new poverty scorecard, whereas 72.3% of households from the treatment group graduated as per the new poverty scorecard.

The finding of the study confirms with the study of

Imai and Azam (

2012);

Shirazi (

2012);

Rashid and Makuwira (

2014);

Agbola et al. (

2017) that the microcredit intervention has a positive impact on the reduction of the poverty. Therefore, it can be inferred that respondents in the treatment group who have graduated to the next band have done so due to the CIF microcredit program intervention. Graduation in the control group has also been witnessed and this can be attributed to natural growth rates, other poverty alleviation tools such as BISP, and other microcredit programs, and families striving for income and food, education of their children, more income earners, and more opportunities for earning. Even so, it is indicated that microcredit has also played a vital role in the reduction of poverty and improving the poverty score of the beneficiaries to move from one category of poor to another upper category. Microcredit has a positive impact on income and consumption (

Imai and Azam 2012), along with income microcredit increases the savings and living standards of the beneficiaries (

Agbola et al. 2017). Microcredit programs have a significant impact on per capita income and per capita consumption expenditure (

Cuong 2008), enhanced livelihood in rural areas (

Rashid and Makuwira 2014) and increased assets, i.e., fans, bicycles and sewing machines (

Shirazi 2012). However, 17.7% of respondents have either not graduated or their status has worsened. The possible reason is that poor people borrow to fulfill their consumption (

Shirazi 2012). They may be tied up with the wrong type of farming activities and units (

Bateman 2012). However, from overall results, it can be suggested that after getting microcredit from CIF, a woman and her family’s poverty reduces, and her wellbeing increases.

The overall comparison of the graduation of both groups on all the levels is not sufficient to see the impact of microcredit on the graduation of women’s poverty score, because graduation to the next level does not confirm the wellbeing of respondents and they are still living under the poverty line. Therefore, the study conducted a detailed analysis and measured graduation on the last three bands of the poverty scorecard. The last three bands were selected for further analysis of graduation because respondents on these bands live above the poverty line and

Schreiner (

2016) also identified that the poverty score of respondents that ranges from 25 to 34 has a 47.1% to 39.5% likelihood of being below the poverty line on the national poverty line of Pakistan. Respondents having poverty score ranges of 35 to 49 have 29.8% to 16.9% likelihood and the poverty score range of 50 to 100 have a 10.7% to 0% likelihood of being below the poverty line on the national poverty line of Pakistan (

Schreiner 2016).

Table 6 shows the comparison of the graduation of both groups on the last three bands. It indicates that only 15 (62.5%) respondents in the control group and 44 (69.8%) respondents in the treatment group have graduated in the third band (24–34), whereas 7 (29.2%) respondents in the control group and 18 (28.6%) respondents in the treatment group have graduated in the fifth band (35–50). However, only 2 (8.3%) respondents and 1 (1.6%) respondent have graduated in the sixth band (51–100) in the control and treatment group, respectively. The overall results indicate that there is not a big difference in the graduation of the treatment and control group.

As shown in

Table 7, only 34.8% of respondents in the control group and 38% of respondents in the treatment group graduated to the last three bands of the poverty scorecard. The overall results suggest that the difference between graduation of treatment and control is 3.2% only, which is insignificant. Our findings confirm the study of

Sayvaya and Kyophilavong (

2015), which concluded that microcredit has a positive impact on poverty, but that impact is not significant. Therefore, we can infer that although microcredit is impacting woman poverty but not significantly and there are other factors as well, such as BISP and other social mobilizing support to rural women, which are reducing their poverty and increasing the graduation level.

5.4. Socio-Demographic Characteristics

Table 8 presents the socio-demographic characteristics of the treatment group who received microfinance loans and the control group who have not taken loans, and it further indicates that both groups based on their characteristics were divided into unmatched and matched samples by using the propensity score matching technique. It shows the t-statistics of comparing the mean of treatment and control groups, which differs significantly. According to unmatched samples, women in the treatment group are likely to be older and have significantly larger household size. In particular, with an average monthly income per family of approximately PKR 17,723.68, women’s family monthly income in the treatment group is significantly higher than the control group, which is having an average of approximately PKR 6692.92 per family, whereas, in matched samples, the average monthly income per family of women in the treatment group is approximately PKR 13,207.28, and is significantly higher than the control group, having an average of approximately PKR 11,722.61 per family. This indicates that the treatment group on average earns more income than the control group. Therefore, it suggests that microfinance has helped women to advance the level of their income. This finding is consistent with the study of

Al-Shami et al. (

2017a,

2017b) which states that microfinance has a positive impact on the monthly income of women. Similarly, with an average monthly consumption per family of approximately PKR 14,603.68, the treatment group in the matched sample is significantly higher than the control group, having an average of approximately PKR 12,571.57 per family. Similarly, with an average monthly consumption per family of approximately PKR 23,447.37, the treatment group in the unmatched sample is significantly higher than the control group, having an average of approximately PKR 8152.05 per family. In the unmatched sample, women who have a savings account are significantly more likely to join microfinance programs. In the matched sample, women who have a savings account have a significantly higher possibility to join microfinance programs earlier. This indicates that women in the treatment group have more savings accounts than the control group, as there is a requirement to open at least one bank account before applying for a microfinance loan from SRSO. Moreover, women also need a savings account to save their money earned from the business which was started from the loan amount. Similarly,

Agbola et al. (

2017) argue that microfinance has a moderately positive effect on poverty alleviation by the increased saving of its clients than non-clients. Women in the treatment group are less educated than the control group but there is no significant difference between them. According to the unmatched sample, women in the treatment group have significantly more total assets’ value and asset purchased value than non-borrowers, whereas, in the matched sample, total asset value and asset sold value of women in the treatment group are higher than the control group. Women participation in microfinance increases the value of their assets as they invest in different businesses and earn reasonable profit, which is also supported by the findings of

Hashemi et al. (

1996) that participation in microcredit increases women ownership of assets.

In the unmatched sample, women in the treatment group have significantly higher social empowerment with an average score of 32.89%, higher economic empowerment with an average score of 21.05% and relatively high political participation with an average score of 11.84%, than women in the control group with an average score of 8.22%, 2.74% and 1.37%. While social and economic empowerment and political participation are not significant in the matched sample.

Table 8 also shows a significant difference of the unmatched sample in women say in decision making with an average score of 42.11%, mobility with an average score of 80.26%, control over resources minor with an average score of 26.32% and control over major resources with an average score of 25% in the treatment group while 15.07%, 45.21%, 2.74% and 5.48% in the control group, whereas women in the treatment group have significantly more political awareness with more control over minor resources in the matched sample. These findings are consistent with a study of

Rehman et al. (

2015) which states that access to microcredit makes women more empowered in terms of health and education (the health and education of their children), social empowerment (social aspects of life), economic empowerment (decisions regarding purchases of households items), and political empowerment (aware of their rights). The composite empowerment in both unmatched and matched groups is significant but high in women of the treatment group in the unmatched sample. Moreover, children of age between 5 and 16 years of women in the treatment group have a significantly high enrollment rate in school with more children in the highest grade level. This finding is consistent with the study of

Mahmood (

2011) who finds that after getting microfinance, women are more empowered in household decisions such as the education of their children.

There is no significant difference between the two groups of women concerning both overall poverty scorecard including all loan cycles and poverty scorecard with loan cycle 3 and above in both matched and unmatched samples as their resultant t-statistics is not significant with an approximately same value of both treatment and control group. This indicates that the bias of treatment and control group was reduced and both groups are now comparable based on the selected pretreatment characteristics.

5.5. Logistic Regression Analysis

The analysis begins with the sample survey data. Logistic regression was performed to assess the impact of interest-free microfinance on the likelihood of women empowerment. The models contain eleven independent variables: four controlled variables (beneficiary, age, education, and occupation) and seven main independent variables (monthly income, monthly consumption, loan amount, BISP, saving amount, total assets values and asset purchased value). The independent variables are identified along the vertical axis of the logit model tables. The B values provided in the second column of logit model tables are coefficients for the constant that is used to identify the direction of the relationship between the independent variable and dependent variable. The

p-value is used to predict whether an independent variable would be significant in the model.

p-values are shown in the third column of logit model tables. The test that is used here is known as the Wald test. Wald is basically t

2 which is Chi-Square distributed with “df (degree of freedom)” equal to 1. This tests the null hypothesis that the constant equals 0. This hypothesis is rejected if the

p-value is smaller than the critical p-value. Wald test is labelled in column fourth of logit model tables. The “e

B” values are represented in the fifth column of logit model tables. “e

B” is the exponentiation of the B coefficient and represents odds ratios for each independent variable. The odds ratio is defined as the change in odds of being in one of the categories of the outcome when the value of a predictor increases by one unit (

Tabachnick et al. 2007). The Cox & Snell R Square and the Nagelkerke R Square values suggest the amount of variation in the dependent variable explained by the model, and it ranges between 0 and 1. The Cox & Snell R square is based on the log-likelihood for the model compared to the log-likelihood for a baseline model, whereas Nagelkerke R Square is an adjusted version of the Cox & Snell R-square. The models also adjust for the socio-demographic characteristics discussed above, but as we are not concerned here with the magnitude of their effects on women empowerment, their estimates are not shown.

Table 9 provides the last logistic regression model results of composite empowerment which is a combination of the previous ten models. At the 10% significance level, the likelihood of composite empowerment of women increases when total asset value increases. In this model, other variables reliably associated with composite empowerment of women are age, occupation type, i.e., farming, labour and SME owner and asset purchased value. The likelihood that composite empowerment of women declines as women’s age increases at a 10% significance level, shows that young women have more composite empowerment. The strongest predictor of reporting women composite empowerment is occupation type labour, recording an odd ratio of 4.896. This indicates that women working in labour are over 4.896 times more likely to report composite empowerment than other occupations, controlling all other factors in the model. The odds ratio of 2.404 and 3.987 for occupation type farming and SME owner is more than 1, indicating that for every additional increase in the number of women working in farming and SME owner are 2.404 and 3.987 times more likely to report having women composite empowerment, controlling for other factors in the model. The odds ratio of 0.979 for age is less than 1, indicating that for every additional year is 0.979 times less likely to report having women composite empowerment, controlling for other factors in the model. In other words, young women are 1.021 (1/0.979) times more likely to have composite empowerment, controlling for other factors in the model.

Furthermore, the odds ratio of 1 for total asset value and asset purchased value indicate that for every additional asset purchased value and asset sold value is 1 time less likely to report having women composite empowerment, controlling for other factors in the model. The two values 0.082 and 0.164 of R Square suggest that the variability in composite empowerment of women is between 8.2% and 16.4%. Overall, the model correctly predicted 89.1% of the cases.

The process of women’s empowerment is complex. This is confirmed by the results of the present analysis. The complexity of empowerment is apparent when comparing the relationships between independent and dependent variables. From the logistic regression results, we find that the various dimensions of empowerment (political empowerment, political awareness, political participation and ownership of household assets and income) are not necessarily related to the determinants (predictors) consistently. For example, the women having education have a negative relationship with ownership of household assets and income even though they are more likely to have ownership of household assets and income. Moreover, the composite score is lower for older women and higher for young women.

Concerning the exposure to the CIF microcredit program, the results suggest that occupation types have a positive impact on women empowerment as the number of women working as labour increases, the probability of social and economic empowerment in women increases. Women who work as labour are more likely to have greater freedom of mobility and are more likely to have control over minor and major resources. Women working as SME owners increases the probability of economic empowerment in women with more control over minor resources and ultimately leads to the probability of women overall empowerment as indicated by the composite score. Women as housewives show a negative relationship with the social empowerment of women due to several cultural norms and stereotypes, as in rural areas the mostly male-dominated society does not involve women to participate in different decision making. Women remain at home and perform household tasks. Further, results indicate that housewives do not have ownership of household assets and incomes because women are not allowed to work outside the house and earn some money to own any asset. Education is a very important indicator of women empowerment. There is considerable evidence for the claim that access to education can bring about changes in the cognitive ability of humans, especially women. The results of this study suggest that the increase in the education level of women increases the probability of political empowerment and political awareness in women whereas the probability of ownership of household assets and income decreases as the education level of women improves because while getting an education, women are unable to work and earn. This makes women more dependent on other family members for earnings.

Mostly, the CIF program helps women to increase their total asset value, and the results propose that if the total asset value increases the probability of economic and social empowerment in women increases. An increase in the total asset value also increases the women’s ownership of household assets and incomes as well as control over minor resources. Microcredit helps women to become independent in society by giving more control over resources. This results in increasing the probability of women overall empowerment as indicated by the composite score. For exposure to the CIF program, the results suggest that as the asset purchased value of family increases, the probability of political, social and economic empowerment of women, political participation and control over resources increases. For the control variables, the results suggest that if women’s age increases, the probability of women’s say in decision-making decreases while the mobility of women increases. In the other words, young women have more ease of mobility from outside the home. This study suggests that not only CIF programs empower women by strengthening their political, social and economic roles but also other indicators such as education level and occupation type have a strong impact on women empowerment.

{kind=link}

{kind=link}

{kind=link}