Local Gaussian Cross-Spectrum Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Definitions

2.1. The Local Gaussian Correlations

2.2. The Local Gaussian Cross-Spectrum

- 1.

- With and as the univariate marginal cumulative distributions of, respectively, and , and Φ as the cumulative distribution of the univariate standard normal distribution, define normalized versions and by

- 2.

- For a given point and for each bivariate lag h pair , a local Gaussian cross-correlation can be computed based on a five-parameter local Gaussian approximation of the bivariate density of at .

- 3.

- When , the local Gaussian cross-spectrum at the point is defined as

- 1.

- coincides with for all when is a multivariate Gaussian time series.

- 2.

- The following holds when is the diagonal reflection of :

2.3. Related Local Gaussian Entities

| Algorithm 1 For a sample of size n from a multivariate time series, an m-truncated estimate of is constructed by means of the following procedure. |

|

2.4. Estimation

The Input Parameters and Some Other Technical Details

2.5. Asymptotic Theory for

2.5.1. A Brief Sketch of the Requirements for

2.5.2. Convergence Theorems for , , and

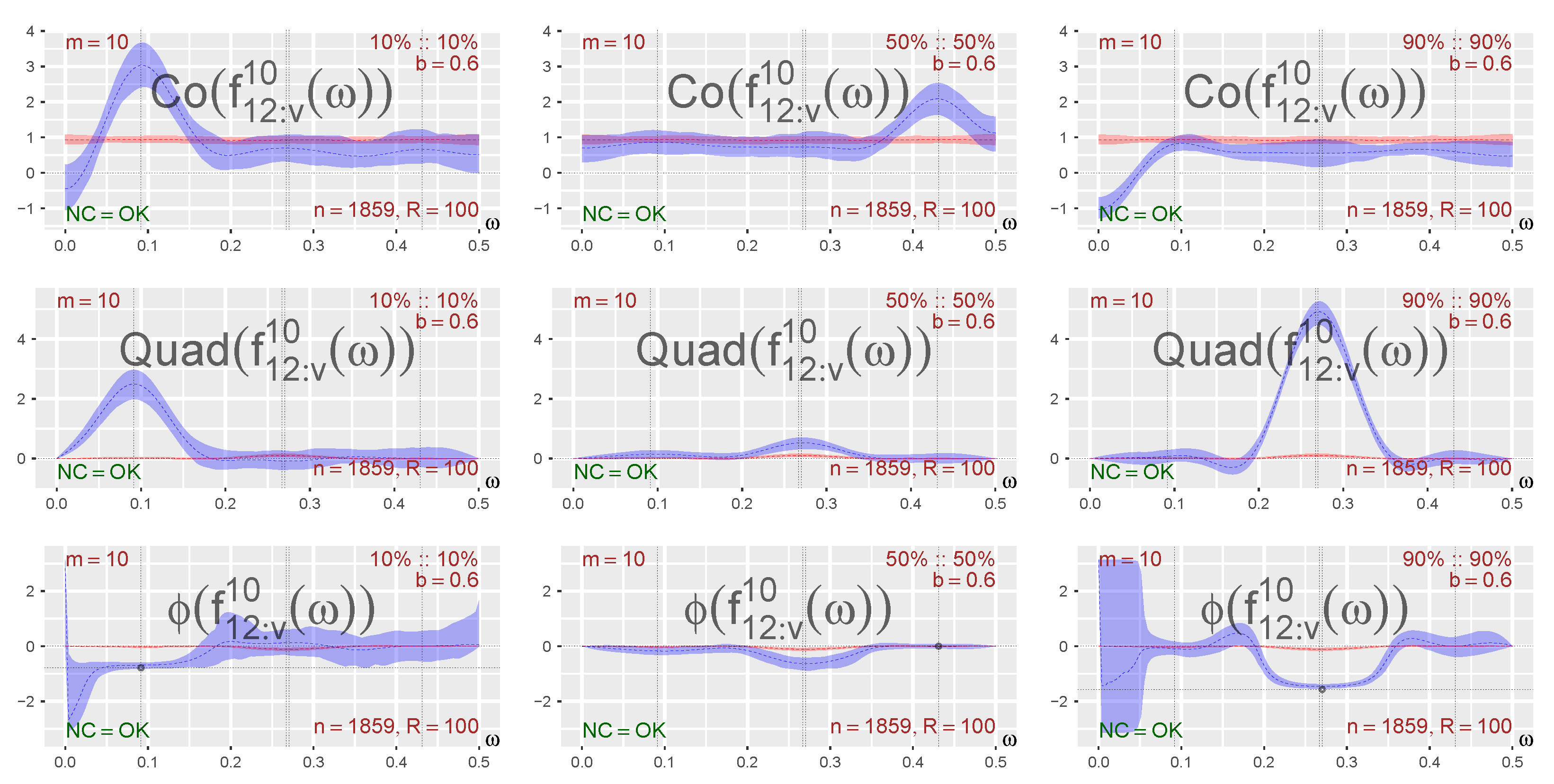

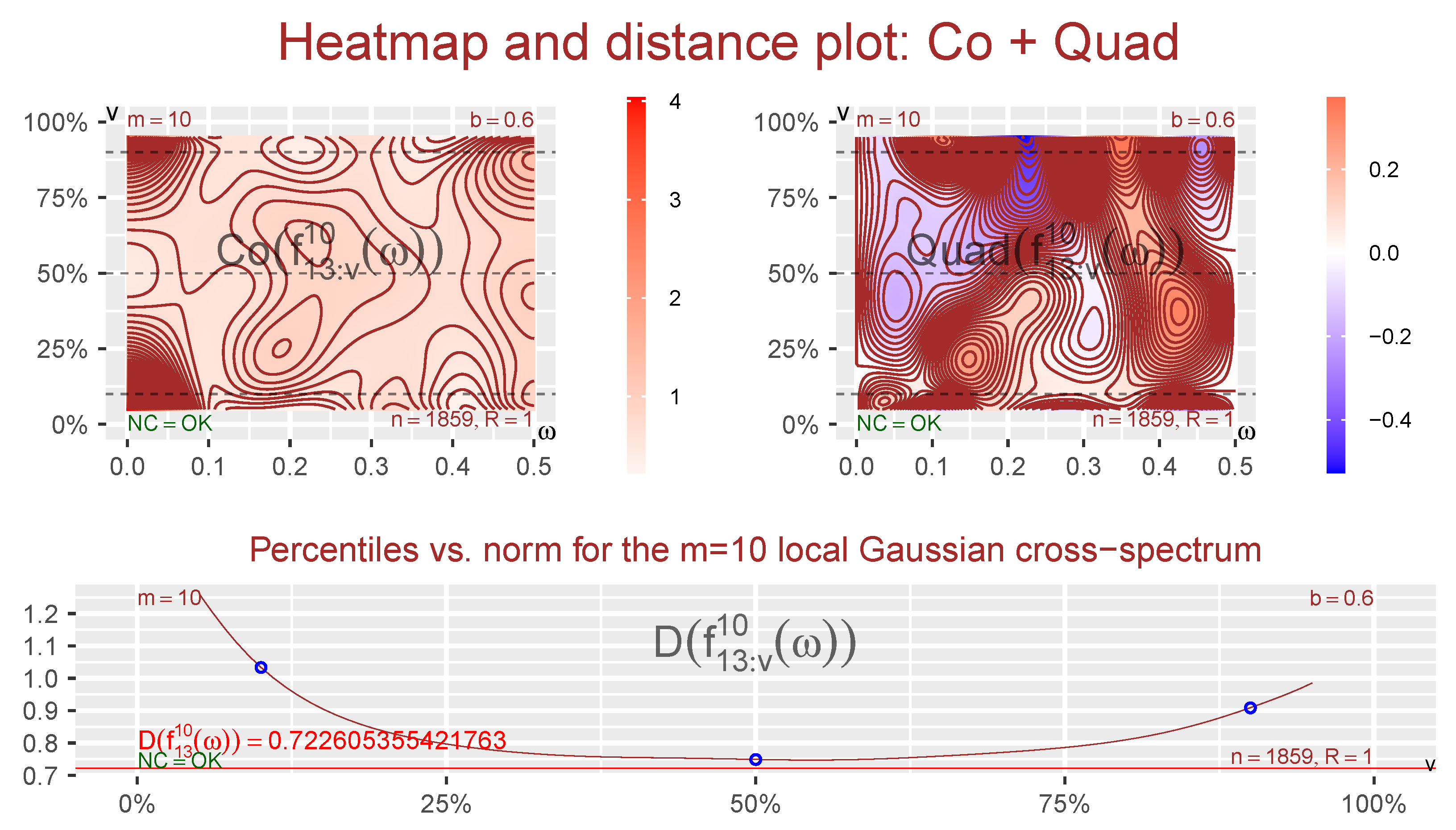

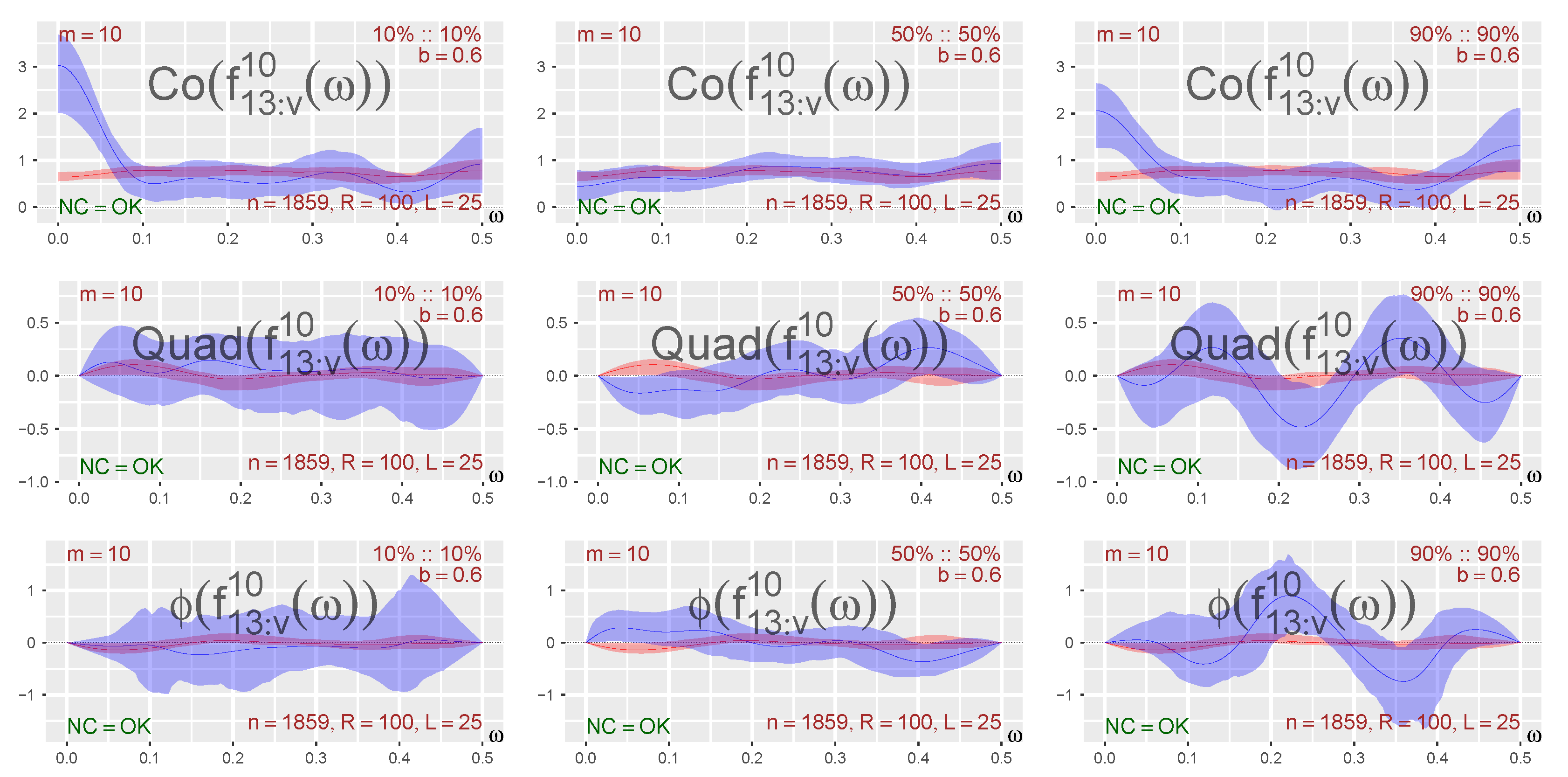

3. Visualizations and Interpretations

3.1. Sanity Testing the Implemented Estimation Algorithm

3.1.1. Bivariate Gaussian White Noise

3.1.2. Bivariate Local Trigonometric Examples

- Select bivariate time series .

- Select a random variable I with values in the set , and use this to sample a collection of indices (that is, for each t, an independent realization of I is taken). Let denote the probabilities for the different outcomes.

- Define by means of the equationThe indicator function 𝟙{·} ensures that only one of the bivariate -components contributes for a given value t, that is, it is also possible to write .

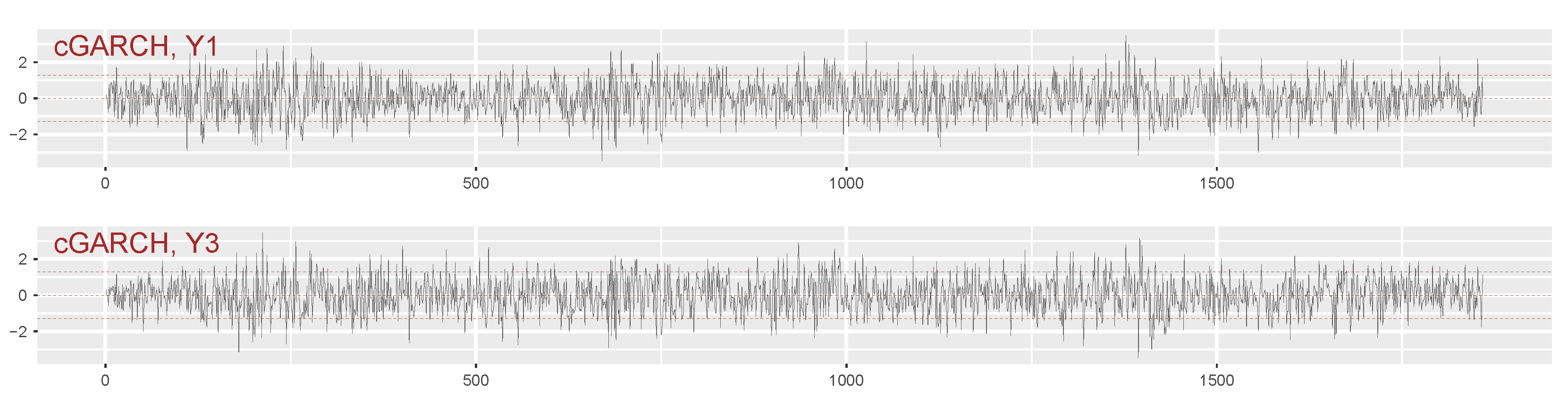

3.2. A Real Multivariate Time Series and a Poorly Fitted GARCH-Type Model

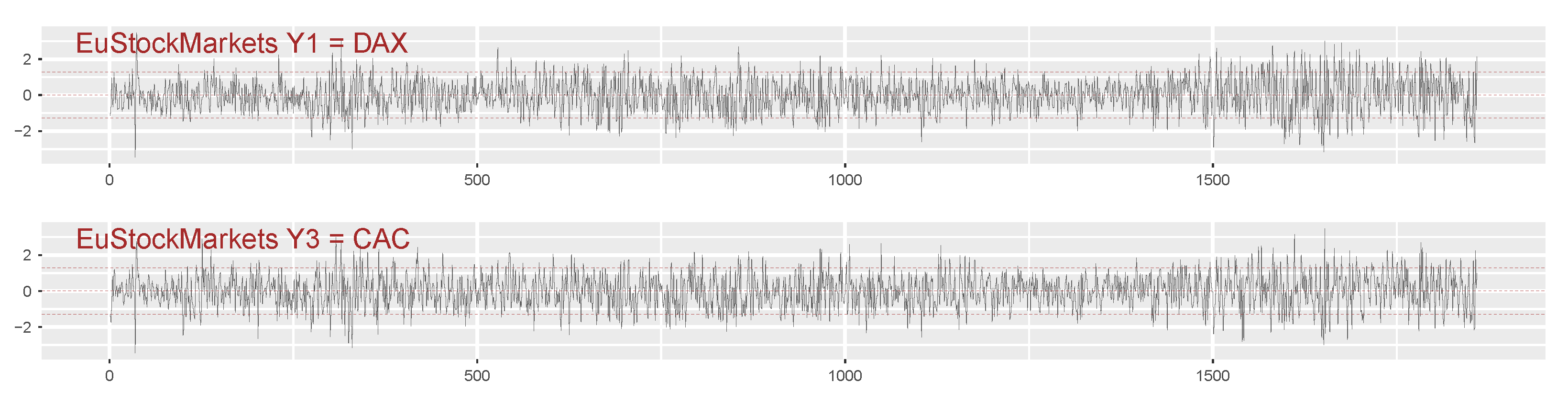

3.2.1. The DAX–CAC Subset of the EuStockMarkets-Log-Returns

3.2.2. A Simple Copula-GARCH-Model Fitted to the EuStockMarkets Log-Returns

- Fit the selected model to the data.

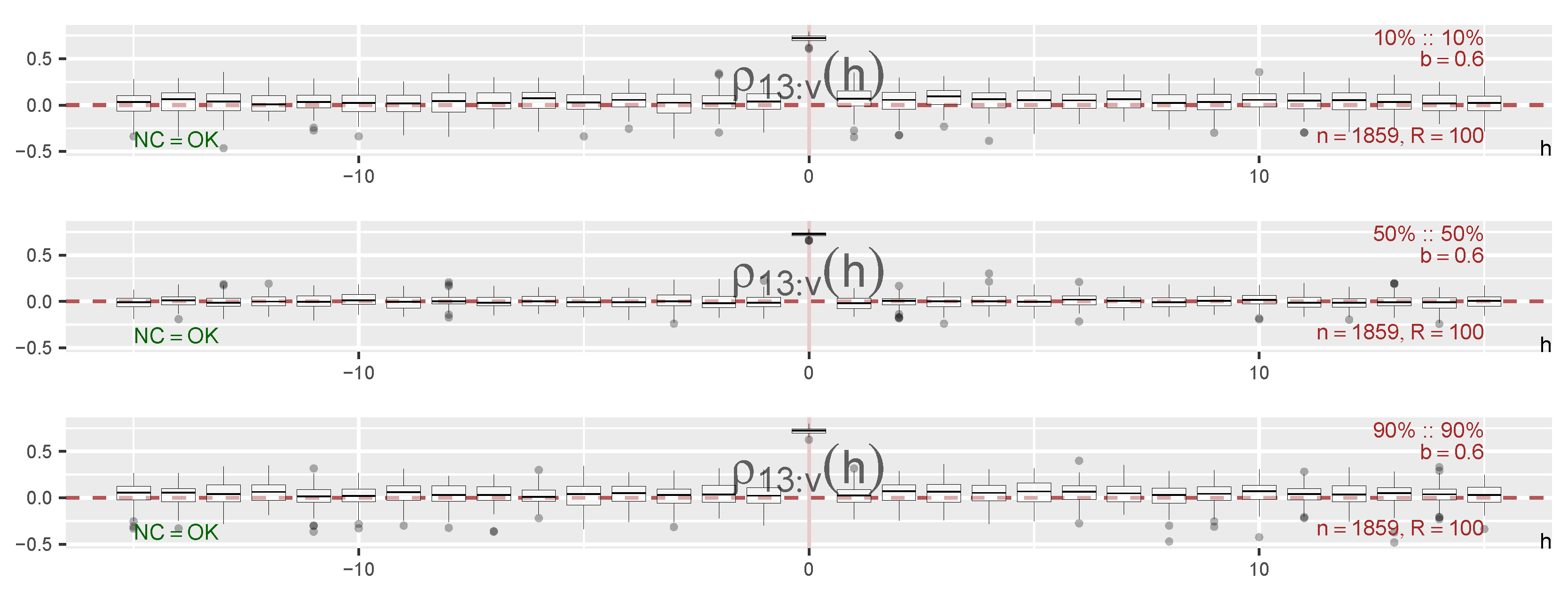

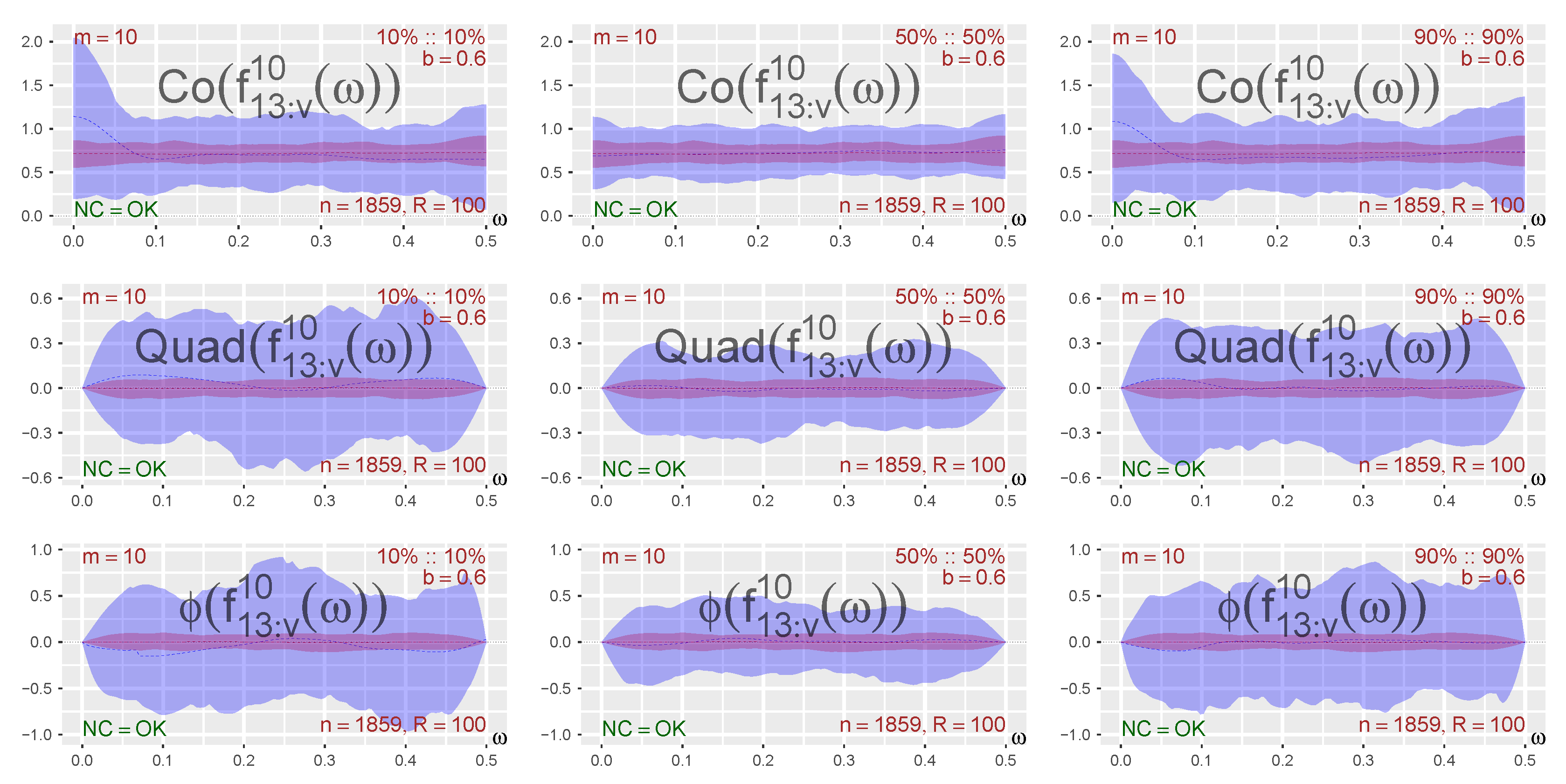

- Perform a local Gaussian spectrum investigation based on simulated samples from the fitted model. The parameters should match those used in the investigation of the original data.

- Compare the plots based on the original data with corresponding plots based on the simulated data from the model. It can be of interest to not only compare the Co-, Quad-, and Phase-plots, but also include plots that show the traces and the estimated local Gaussian auto- and cross-spectra.

4. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | This multivariate approach was initiated in the first author’s Ph.D. thesis, available at https://bora.uib.no/handle/1956/16950. The version in this paper has been extended with new methods and visualizations that were developed due to review comments related to the univariate theory published in JT22. |

| 2 | This is due to the way the local Gaussian correlation is defined; see Tjøstheim and Hufthammer (2013) for details. |

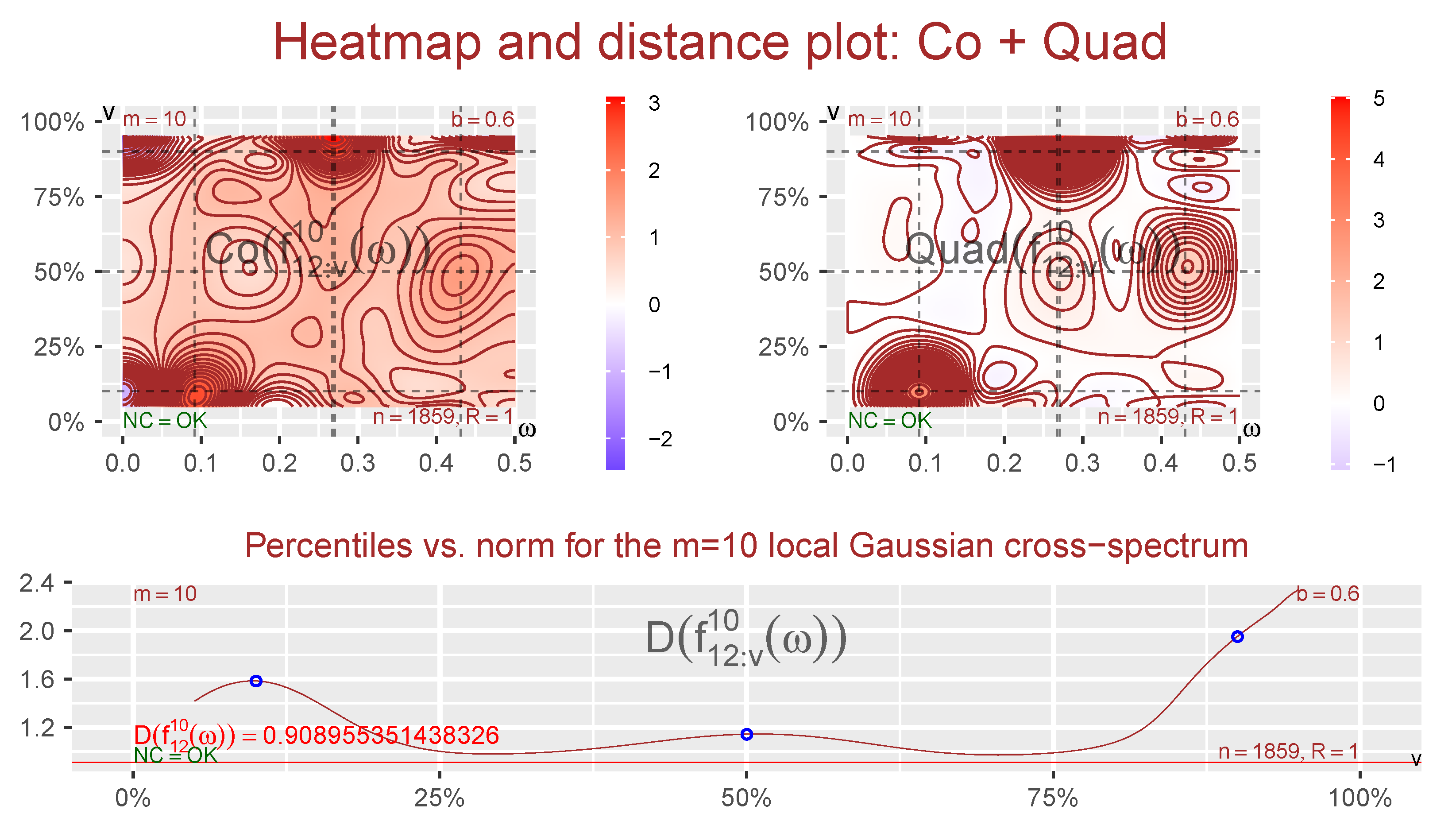

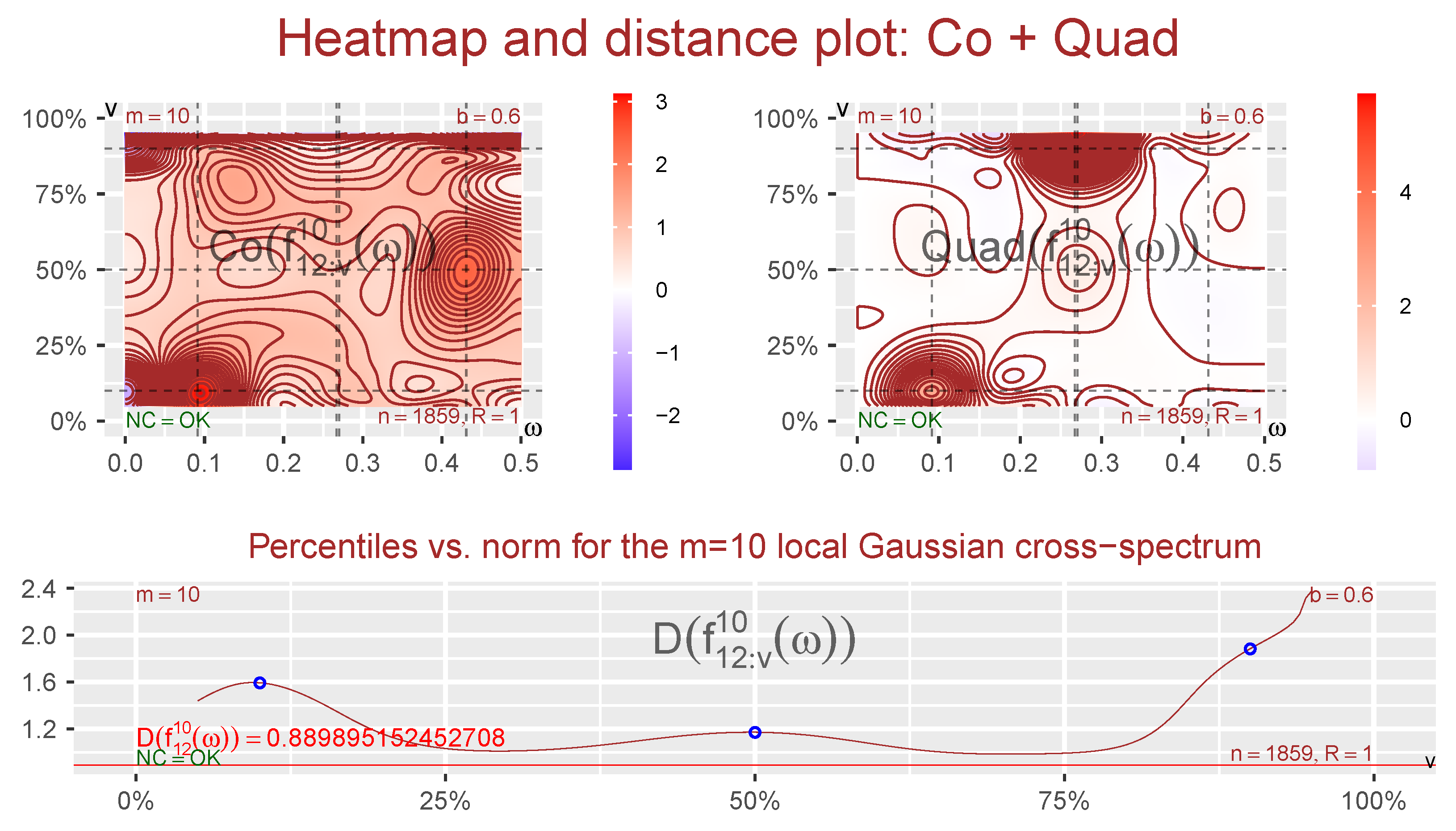

| 3 | The corresponding coordinates are , , and . |

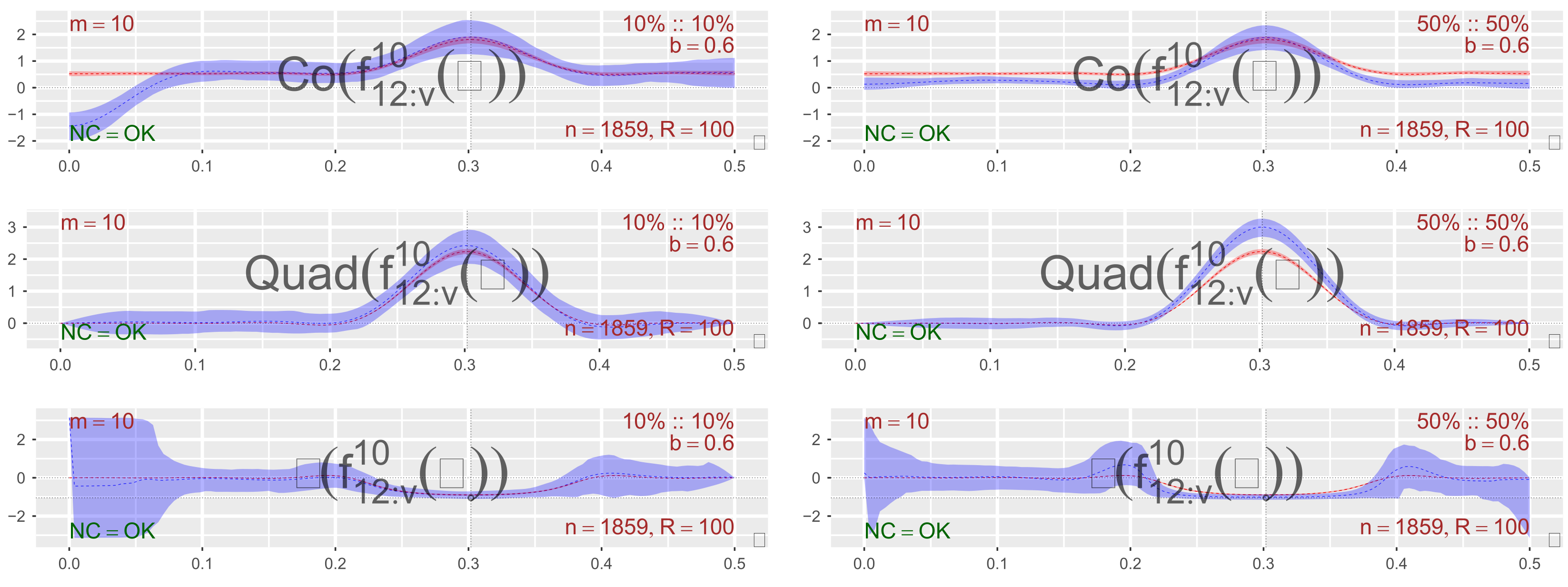

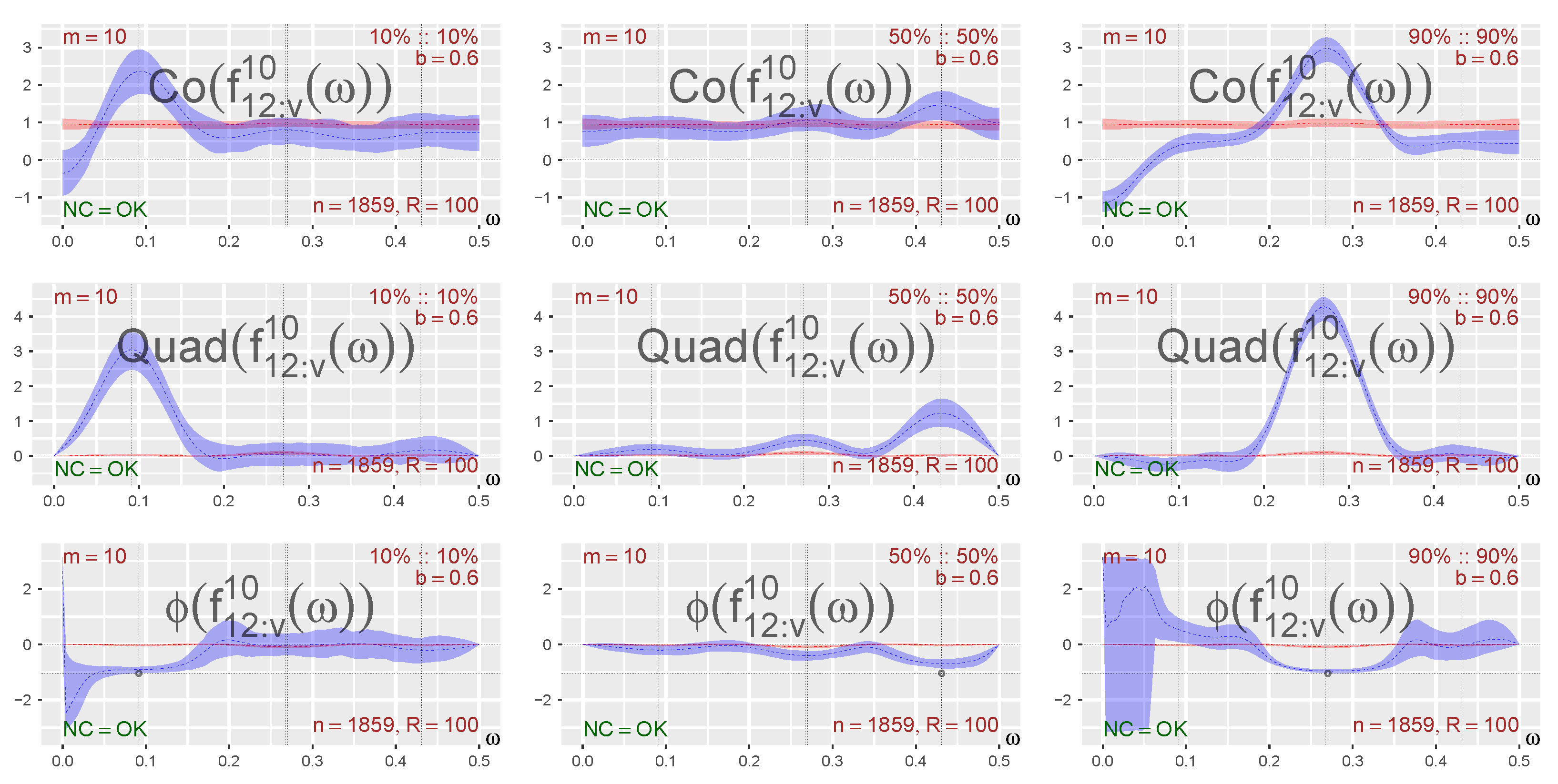

| 4 | The Amplitude-plots are not included here since the interesting details (in most cases) would already have been detected by the other plots. |

| 5 | If you have a black and white copy of this paper, then read “blue” as “light” and “red” as “dark”. |

| 6 | The dotted lines represent the means of the estimated values, whereas the 90% pointwise confidence intervals are based on the 5% and 95% quantiles of these samples. |

| 7 | In this respect, the situation is similar to the detection of a pure sinusoidal for the global spectrum. |

| 8 | The corresponding script in the R-package localgaussSpec enables an investigation of all the combinations between DAX, SMI, CAC, and FTSE, but only the DAX–CAC subset will be discussed here. |

| 9 | |

| 10 | Use remotes::install_github("LAJordanger/localgaussSpec") to install the package. See Section S6.1 in the online Supplementary Material for further details. |

References

- Aït-Sahalia, Yacine, Julio Cacho-Diaz, and Roger J. A. Laeven. 2015. Modeling financial contagion using mutually exciting jump processes. Journal of Financial Economics 117: 585–606. [Google Scholar] [CrossRef]

- Baruník, Jozef, and Tobias Kley. 2019. Quantile coherency: A general measure for dependence between cyclical economic variables. The Econometrics Journal 22: 131–52. [Google Scholar] [CrossRef]

- Berentsen, Geir Drage, Tore Selland Kleppe, and Dag Bjarne Tjøstheim. 2014. Introducing localgauss, an R Package for Estimating and Visualizing Local Gaussian Correlation. j-J-STAT-SOFT 56: 1–18. [Google Scholar] [CrossRef]

- Birr, Stefan, Tobias Kley, and Stanislav Volgushev. 2019. Model assessment for time series dynamics using copula spectral densities: A graphical tool. Journal of Multivariate Analysis 172: 122–46, Dependence Models. [Google Scholar] [CrossRef]

- Bollerslev, Tim, and Eric Ghysels. 1996. Periodic Autoregressive Conditional Heteroscedasticity. Journal of Business & Economic Statistics 14: 139–51. [Google Scholar] [CrossRef]

- Brillinger, David R. 1965. An Introduction to Polyspectra. The Annals of Mathematical Statistics 36: 1351–74. [Google Scholar] [CrossRef]

- Brillinger, David R. 1991. Some history of the study of higher-order moments and spectra. Statistica Sinica 1: 24J. [Google Scholar]

- Brillinger, David R., ed. 1984. The Collected Works of John W. Tukey. Volume I. Time Series: 1949–1964. Introductory Material by William S. Cleveland and Frederick Mosteller. Wadsworth Statistics/Probability Series; Pacific Grove: Wadsworth. [Google Scholar]

- Brockwell, Peter J., and Richard A. Davis. 1986. Time Series: Theory and Methods. New York: Springer, Inc. [Google Scholar]

- Chen, Tianbo, Ying Sun, and Ta-Hsin Li. 2021. A semi-parametric estimation method for the quantile spectrum with an application to earthquake classification using convolutional neural network. Computational Statistics & Data Analysis 154: 107069. [Google Scholar] [CrossRef]

- Chung, Jaehun, and Yongmiao Hong. 2007. Model-free evaluation of directional predictability in foreign exchange markets. Journal of Applied Econometrics 22: 855–89. [Google Scholar] [CrossRef]

- Ciaburro, Giuseppe, and Gino Iannace. 2021. Machine Learning-Based Algorithms to Knowledge Extraction from Time Series Data: A Review. Data 6: 55. [Google Scholar] [CrossRef]

- Eyjolfsson, Heidar, and Dag Tjøstheim. 2023. Multivariate self-exciting jump processes with applications to financial data. Bernoulli, in press. [Google Scholar]

- Ghalanos, Alexios. 2022a. rmgarch: Multivariate GARCH Models. R Package Version 1.3-9. Available online: https://cran.r-project.org/package=rmgarch (accessed on 10 December 2022).

- Ghalanos, Alexios. 2022b. rugarch: Univariate GARCH Models. R Package Version 1.4-9. Available online: https://cran.r-project.org/package=rugarch (accessed on 10 December 2022).

- Hjort, Nils Lied, and M. C. Jones. 1996. Locally parametric nonparametric density estimation. Annals of Statistics 24: 1619–47. [Google Scholar] [CrossRef]

- Hong, Yongmiao. 1999. Hypothesis Testing in Time Series via the Empirical Characteristic Function: A Generalized Spectral Density Approach. Journal of the American Statistical Association 94: 1201–20. [Google Scholar] [CrossRef]

- Hong, Yongmiao, Jun Tu, and Guofu Zhou. 2007. Asymmetries in Stock Returns: Statistical Tests and Economic Evaluation. The Review of Financial Studies 20: 1547–81. [Google Scholar] [CrossRef]

- Jordanger, Lars Arne, and Dag Tjøstheim. 2022. Nonlinear Spectral Analysis: A Local Gaussian Approach. Journal of the American Statistical Association 117: 1010–27. [Google Scholar] [CrossRef]

- Klimko, Lawrence A., and Paul I. Nelson. 1978. On Conditional Least Squares Estimation for Stochastic Processes. Annals of Statistics 6: 629–42. [Google Scholar] [CrossRef]

- Künsch, Hans R. 1989. The Jackknife and the Bootstrap for General Stationary Observations. The Annals of Statistics 17: 1217–41. [Google Scholar] [CrossRef]

- Li, Ta-Hsin. 2020. From zero crossings to quantile-frequency analysis of time series with an application to nondestructive evaluation. Applied Stochastic Models in Business and Industry 36: 1111–30. [Google Scholar] [CrossRef]

- Li, Ta-Hsin. 2021. Quantile-frequency analysis and spectral measures for diagnostic checks of time series with nonlinear dynamics. Journal of the Royal Statistical Society: Series C (Applied Statistics) 2: 270–90. [Google Scholar] [CrossRef]

- Li, Ta-Hsin. 2022a. Quantile Fourier Transform, Quantile Series, and Nonparametric Estimation of Quantile Spectra. Preprint. [Google Scholar] [CrossRef]

- Li, Ta-Hsin. 2022b. Quantile-Frequency Analysis and Deep Learning for Signal Classification. Preprint. [Google Scholar] [CrossRef]

- Li, Zeda. 2023. Robust conditional spectral analysis of replicated time series. Statistics and Its Interface 16: 81–96. [Google Scholar] [CrossRef]

- Otneim, Håkon, and Dag Tjøstheim. 2017. The locally Gaussian density estimator for multivariate data. Statistics and Computing 27: 1595–616. [Google Scholar] [CrossRef]

- Politis, Dimitris N., and Joseph P. Romano. 1992. A General Resampling Scheme for Triangular Arrays of α-Mixing Random Variables with Application to the Problem of Spectral Density Estimation. The Annals of Statistics 20: 1985–2007. [Google Scholar] [CrossRef]

- R Core Team. 2020. R: A Language and Environment for Statistical Computing. Vienna: R Foundation for Statistical Computing. [Google Scholar]

- Teräsvirta, Timo, Dag Tjøstheim, and Clive William John Granger. 2010. Modelling Nonlinear Economic Time Series. Oxford: Oxford University Press. [Google Scholar]

- Tjøstheim, Dag, and Karl Ove Hufthammer. 2013. Local Gaussian correlation: A new measure of dependence. Journal of Econometrics 172: 33–48. [Google Scholar] [CrossRef]

- Tjøstheim, Dag, Håkon Otneim, and Bård Støve. 2021. Statistical Modeling Using Local Gaussian Approximation. Cambridge: Academic Press. [Google Scholar]

- Tukey, John W. 1959. An introduction to the measurement of spectra. In Probability and Statistics, The Harald Cramér Volume. Edited by Ulf Grenander. Stockholm: Almqvist and Wiksell, pp. 300–30. [Google Scholar]

- Zhao, Zifeng, Peng Shi, and Zhengjun Zhang. 2022. Modeling multivariate time series with copula-linked univariate d-vines. Journal of Business & Economic Statistics 40: 690–704. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jordanger, L.A.; Tjøstheim, D. Local Gaussian Cross-Spectrum Analysis. Econometrics 2023, 11, 12. https://doi.org/10.3390/econometrics11020012

Jordanger LA, Tjøstheim D. Local Gaussian Cross-Spectrum Analysis. Econometrics. 2023; 11(2):12. https://doi.org/10.3390/econometrics11020012

Chicago/Turabian StyleJordanger, Lars Arne, and Dag Tjøstheim. 2023. "Local Gaussian Cross-Spectrum Analysis" Econometrics 11, no. 2: 12. https://doi.org/10.3390/econometrics11020012

APA StyleJordanger, L. A., & Tjøstheim, D. (2023). Local Gaussian Cross-Spectrum Analysis. Econometrics, 11(2), 12. https://doi.org/10.3390/econometrics11020012