1. Introduction

Banks, credit unions, and insurance companies bear the responsibility of protecting vast amounts of sensitive information and critical infrastructure. While perimeter-based security measures are still necessary and should be built upon, they still need to be improved to sufficiently safeguard these assets against increasingly complex and robust cyber threats. Financial institutions’ challenges in securing their networks have been further intensified by the increasing interconnectedness of systems, the popularity of cloud computing, and the widespread use of mobile and Internet-of-Things (IoT) devices.

The financial impact of cyberattacks on financial institutions can be substantial, leading to significant financial losses and reputational damage. For instance, a study by [

1] revealed that a cyberattack can increase cash holdings from a base level of 23% of assets to 26.87%. This increase in cash holdings is a sign that businesses are taking precautions to lessen the financial impact of potential cyberattacks.

Additionally, decreased firm value, weaker stock market performance, lower operating performance, decreased merger and acquisition activity, customer loss, and an increased cost of capital are some of the effects of reputational damage that a study by [

2] has documented. This highlights the substantial financial and reputational consequences that financial institutions may face following a cyberattack.

Traditional perimeter-based defences and the Defence-in-Depth approach, while providing layered security, have shown limitations in addressing sophisticated internal and external threats. These models often struggle to adapt dynamically to changing threat environments and may not effectively handle threats that have penetrated network perimeters.

The Zero Trust model has become a possible security framework that could help solve these problems by shifting the focus from traditional perimeter-based security to a more all-encompassing and granular approach [

3]. The Zero Trust model is based on the principle “never trust, always verify,” and it calls for the continuous verification of users, devices, and applications before providing them access to confidential data and resources [

4]. Financial institutions are moving towards this model due to its potential to prevent advanced persistent threat (APT) attacks or significantly mitigate them. APT attacks are particularly concerning for financial institutions due to the potential for substantial financial losses and reputational damage. Incorporating the Zero Trust model can help reduce the risk of such attacks, thereby safeguarding the financial institution’s assets and maintaining customer trust. The ever-changing nature of today’s threats makes this model’s more dynamic and adaptable security stance crucial.

Blockchain is one such technology that can provide a secure and transparent platform for information sharing in a Zero Trust context [

5]. It can prevent unauthenticated participants from sharing information and filter out forged information through smart contracts and consensus mechanisms [

6]. It guarantees anonymity yet entity authentication, data privacy yet data trustworthiness, and participant stimulation yet fairness [

5]. Additionally, blockchain can ensure access management, user authentication, and transaction security in a Zero Trust architecture [

7].

Blockchain technology has been increasingly applied in the financial industry, particularly in startup financing, supply chain finance, and banking services. It has been shown to streamline institutional functions, reduce operational risks, and improve business income [

8,

9,

10]. In recent years, several financial firms like Goldman Sachs, J.P. Morgan, and other banking giants have established their blockchain laboratories, collaborating closely with blockchain platforms [

10]. Additionally, blockchain technology has been applied in areas such as sustainable supply chain finance, central bank digital currencies, and transaction systems using smart contracts [

11]. The technology’s impact on the financial industry is significant, with its characteristics, performance, and advantages dramatically influencing various aspects of the industry.

Recent studies, such as those by [

12], proposed a framework based on the Zero Trust concept and blockchain technology with the focus of making the banking sector safe from cyber attacks and data breaches. In addition to the framework, an algorithm for blockchain-based online transactions was designed to make use of practical implementation in the future. The use of blockchain technology in the finance industry has been shown to decrease banks’ stock market volatility and facilitate price stabilisation [

13]. Additionally, the application of blockchain in finance can accelerate the system to a stable state, ensuring compliance with contracts and enhancing automatic monitoring capabilities [

14].

However, current implementations of Zero Trust in the banking sector, as discussed by [

12], reveal limitations in scalability and adaptability. Responding to these challenges, this paper introduces a novel framework that integrates blockchain technology within the Zero Trust model, inspired by advancements in other sectors, such as e-health, where [

7] have effectively employed a similar integration for secure medical image sharing. The proposed framework in our study is designed to enhance identity and access management, device and network security, and data protection in financial institutions, addressing the limitations of traditional models like Defence in Depth and the existing Zero Trust models and elevating their scalability and adaptability.

The primary objective of this research is to propose a comprehensive, Zero Trust model-based framework enhanced with blockchain technology and tailored for the finance industry. This framework aims to address the limitations of traditional cybersecurity models by offering significant improvements in defences against cyber attacks. Additionally, the research examines the framework’s influence on the operational efficacy of banking applications, specifically regarding its impact on transaction processing efficiency, system throughput, scalability, and resilience to cyber threats. By doing so, this study aims to address the following research questions:

How does the integration of blockchain technology within a Zero Trust model framework improve cybersecurity measures in financial institutions?

What cyber threats and vulnerabilities are effectively mitigated by the proposed blockchain-enhanced Zero Trust framework, and through what mechanisms?

How does the proposed framework balance enhanced security measures with operational efficiency, particularly in terms of transaction latency, system throughput, and scalability?

How does the proposed framework compare with established cybersecurity frameworks in the financial industry, particularly in terms of adherence to Zero Trust principles, regulatory compliance (including AML and KYC), data protection, and operational efficiency?

The framework incorporates strong authentication and authorisation processes, robust device and network security mechanisms, and advanced data protection techniques to mitigate cyber threats effectively and maintain the confidentiality, integrity, and availability of critical financial data, ultimately increasing consumer confidence in the institution’s services. This study demonstrates the framework’s effectiveness through practical examples and insights gained from implementing a prototype bank app. A comprehensive evaluation of the framework’s performance against existing cybersecurity frameworks was conducted, including compliance and regulatory adherence, implementation complexity, performance efficiency, and adaptability to evolving cyber threats. Additionally, this paper provides a detailed summary of Zero Trust, its evolution, and how it is reshaping the future of the finance industry. At the time of writing this paper, no study had proposed a Zero Trust model-based framework for financial institutions.

The remaining part of this paper is organised as follows:

Section 2 discusses the Zero Trust framework, cybersecurity frameworks for the finance industry, cybersecurity challenges in the finance industry, real-world Zero Trust approaches, and security models in the finance industry.

Section 3 details the proposed framework and its components with and without Zero Trust implementation.

Section 4 provides implementation details and evaluation methodology.

Section 5 analyses the results and discusses the benefits. Finally,

Section 6 concludes this paper and provides future research directions.

2. Background and Related Work

This section examines and summarises current research relevant to applying the Zero Trust model in financial organisations. The aim is to offer a detailed look at the Zero Trust approach, existing cybersecurity challenges in the finance industry, existing cybersecurity frameworks and solutions in the financial sector, real-world Zero Trust approaches, and the current security models used in the finance industry. Given the growing complexity and sophistication of cyber threats targeting financial institutions and the legal requirements that these organisations face, the review emphasises the necessity for a comprehensive and adaptive security architecture for the finance sector.

2.1. Zero Trust

Zero Trust is a strategic initiative for cybersecurity that can keep an organisation safe [

15]. It does this by getting rid of blind trust and continuously validating each step of digital interaction. Zero Trust is based on the principle “never trust, always verify”. Its goal is to protect today’s technological environment while making digital transformation easier. It uses multi-factor authentication, network segmentation, elimination of lateral movement, layer 7 threat prevention, and streamlining granular “least access” policies.

The concept of “Zero Trust” arose from the realisation that conventional security models are based on the out-of-date idea that everything within an organisation’s network can be trusted without further investigation [

4]. Because there are not enough fine-grained security controls, users (including threat actors and malicious insiders) can freely move around the network, access sensitive data, and send it out because the network trusts them.

Principles of Zero Trust

Zero Trust is based on three core principles, as outlined in the NIST Special Publication 800-207.

2.2. Zero Trust Architecture

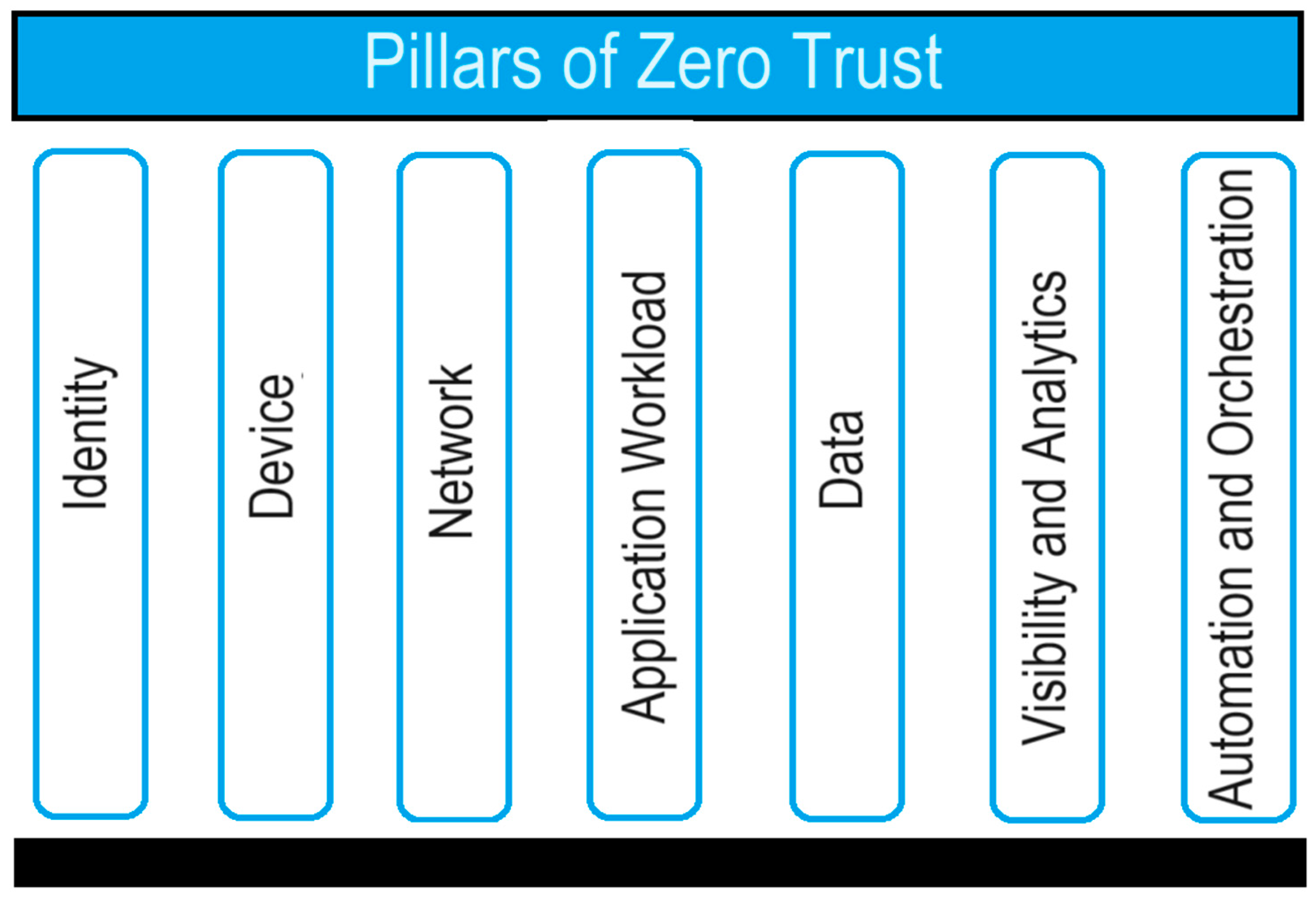

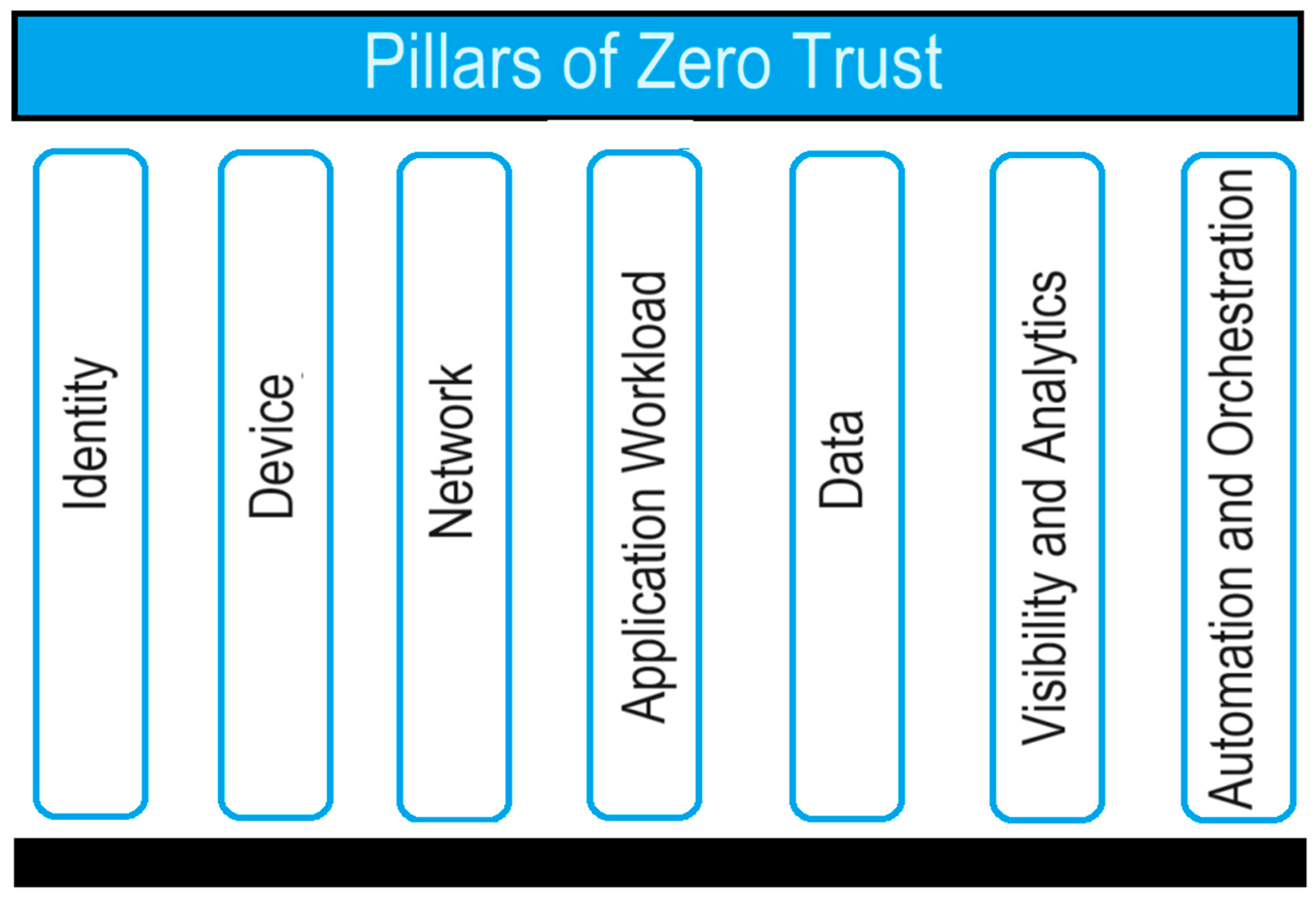

The Zero Trust model encompasses several pillars that form the foundation of its implementation, as shown in

Figure 1. These pillars include Zero Trust data, networks, workloads, people, devices, applications, visibility and analytics, and automated orchestration. Zero Trust data focuses on protecting data as the primary objective and implementing controls to detect and prevent unauthorised access [

17]. Zero Trust networks involve separating, isolating, and limiting network access, making it difficult for attackers to move laterally within the network. Zero Trust workloads encompass securing all applications and back-end software to prevent unauthorised access and interference. Zero Trust people emphasise the need to limit and monitor user access to resources and to trust but verify all user actions.

Zero Trust devices involve securing and controlling every device connected to the network to prevent potential access points for attackers. Zero Trust applications focus on securing access at the application layer by connecting user, device, and data components. Visibility and analytics enable organisations to have complete visibility into their IT environment and use analytics to detect and respond to suspicious activities in real time. Automated orchestration involves continuously enforcing Zero Trust rules and automating security systems to keep up with the increasing number of monitoring events.

In the last decade, businesses have begun to spread their DAAS (data, assets, applications, and services) across different servers and cloud storage options. Due to this decentralisation, it is no longer possible to secure a network by isolating it within a single location, group of devices, or group of users. The Zero Trust framework was made in this distributed, cloud-native environment to help businesses protect their most valuable assets.

Based on the idea that there is no secure network perimeter, Zero Trust requires designing a system in which every user and service is treated as a possible security risk, no matter how deeply they are embedded in the network. Access requests must be constantly checked to ensure that the system can connect to the applications and services [

19]. Users and devices would undergo continuous authentication of their identities and privileges, and logins, connections, and API tokens would have a finite lifespan. User DAAS access can be closely monitored with this “never trust, always verify” strategy. Access control, constant evaluation, and maximum observability are essential in the cloud-native world, where consumers may be geographically dispersed, using various devices, and actively trying to access DAAS via secure and unsecured networks [

20].

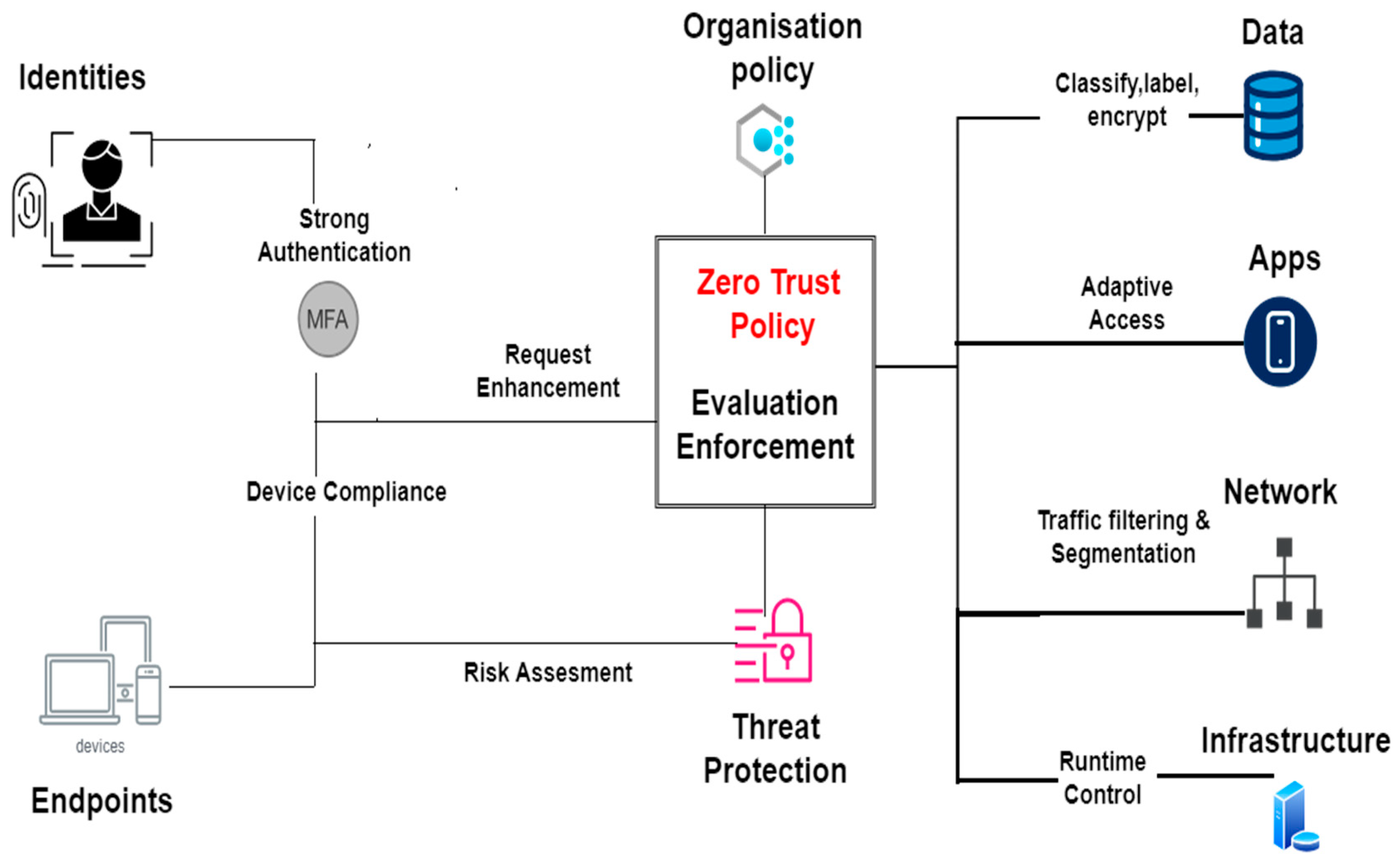

The Zero Trust model treats every request as if it came from the public Internet rather than trusting that anything behind the company firewall is secure. Zero Trust teaches us to “never trust, always verify,” regardless of the source or target of a request [

21]. Each request is checked for authentication, authorisation, and encryption before access is given, as shown in

Figure 2. The principles of micro-segmentation and least-privileged access are used to restrict communication between nodes. Anomalies are identified and dealt with instantly by employing sophisticated intelligence and analytics.

2.3. Existing Cybersecurity Challenges in the Finance Industry

The finance industry, particularly banks, faces a diverse range of security challenges due to the dynamic digital landscape and the sensitive nature of its operations [

23]. These challenges are multifaceted, interconnected, and continually evolving, necessitating robust and adaptive security measures.

The prevalence of cyber threats, including sophisticated malware, ransomware attacks, phishing, and social engineering campaigns, has escalated in recent years, demanding advanced cybersecurity strategies to combat the complexity and variety of these attacks [

24]. Data breaches in the finance sector not only led to financial losses but also undermined customer trust, emphasising the critical need for effective data protection measures. The growing concern for privacy, compounded by regulations such as the General Data Protection Regulation (GDPR), places additional pressure on financial institutions to safeguard customer data and ensure compliance with data privacy laws.

The banking industry faces increased risks from cyber threats, primarily through mobile applications, web portals, and other communication channels [

25]. Furthermore, the efficient management of cyber risk in IT-based banking systems is stressed by managers, regulators, and international organisations, as cyber risk can adversely affect banks and financial institutions [

26]. One of the critical challenges faced by banks is the behaviour of their employees, which can lead to cybersecurity threats. It has been noted that cybersecurity threats originating from employees’ incorrect behaviour remain a significant challenge in the banking sector [

27]. A recent example that highlights the persistent threat of phishing and social engineering in the financial sector is the 2021 phishing attack on Banco de España. This attack involved a sophisticated phishing campaign that targeted the bank’s customers, employing fraudulent emails and websites that closely mimicked the bank’s official communications. This incident not only resulted in financial losses but also raised serious concerns about the security of customer information, demonstrating the ongoing challenge that financial institutions face in protecting against these types of cyber threats.

Additionally, until banking staff are appropriately trained to operate and behave in a cyber-resilient manner, banks will continue to be exposed to a wide variety of cyber threats. Weak security controls in the banking sector have led to difficulties in detecting and preventing fraud. The recent credit crisis has exposed considerable weaknesses in risk management across the financial services industry, necessitating a critical review of governance mechanisms.

The banking sector is also exposed to various types of cybercrimes, including underground attack technologies, which have been examined in the context of the Nigerian banking sector [

28]. Furthermore, the paper “Cyber Security Challenges through the Lens of the Financial Industry” draws attention to the increased concern among European and international authorities regarding cybersecurity risks faced by the financial industry, emphasising the need for proper prevention, identification, assessment, and management of these risks [

29].

Moreover, the economic cost of publicly announced information security breaches has been studied, with limited evidence of an overall negative stock market reaction to such breaches. However, the financial costs associated with data breaches are growing, and data breach disclosure laws have been found to impact the cash policies of corporations in the United States [

30]. This underscores the financial implications of cybersecurity challenges for banks and financial institutions.

In addressing these challenges, financial institutions must adopt a holistic and layered approach to security. The Zero Trust model, with its principle of “never trust, always verify,” offers a promising framework to counter these threats by fundamentally rethinking how security is implemented.

2.4. Existing Cybersecurity Frameworks for the Finance Industry

Financial institutions prioritise robust cybersecurity measures to protect against cyberattacks and secure sensitive financial data. Existing cybersecurity frameworks guide them in implementing best practices and ensuring the confidentiality, integrity, and availability of critical data and information. This section delves into some of the popular existing cybersecurity frameworks used in the finance industry.

2.4.1. NIST Cybersecurity Framework

One widely accepted cybersecurity framework in the banking sector is the National Institute of Standards and Technology (NIST) Cybersecurity Framework. Organisations widely recognise and utilise the NIST Cybersecurity Framework to facilitate cybersecurity risk management [

31]. This framework provides a comprehensive approach to identifying, protecting, detecting, responding to, and recovering from cybersecurity incidents. It emphasises the importance of risk assessment, continuous monitoring, and incident response planning [

32]. The NIST Cybersecurity Framework also promotes collaboration and information sharing among stakeholders to enhance cybersecurity resilience [

33].

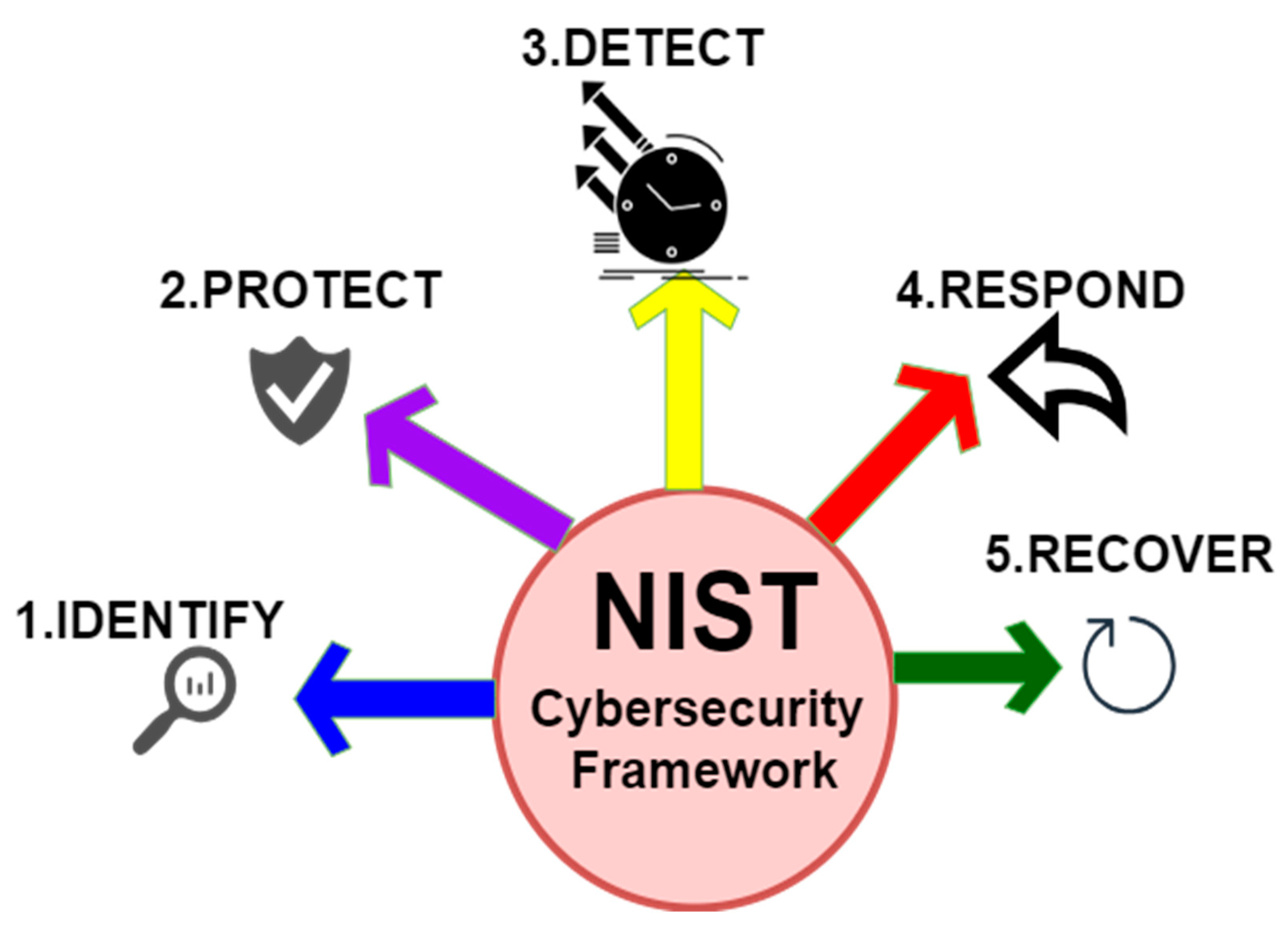

As illustrated in

Figure 3, the NIST Cybersecurity Framework consists of five core functions: Identify, Protect, Detect, Respond, and Recover.

Identify function: This involves understanding the organisation’s cybersecurity risks, establishing governance, and managing assets and access controls;

Protect function: It focuses on implementing safeguards against potential threats and vulnerabilities. This includes activities such as access control, awareness training, and data protection measures;

Detect function: This involves continuous monitoring and timely detection of cybersecurity events. This includes activities such as anomaly detection, security event monitoring, and incident detection;

Respond function: It focuses on taking appropriate actions to mitigate the impact of a cybersecurity incident. This includes activities such as incident response planning, communication, and coordination;

Recover function: This involves restoring normal operations and services after a cybersecurity incident. This includes activities such as recovery planning, improvements, and lessons learned [

34].

Figure 3.

NIST Cybersecurity Framework [

35].

Figure 3.

NIST Cybersecurity Framework [

35].

The NIST Cybersecurity Framework provides the finance industry with a flexible and customisable approach to managing cybersecurity risks. It can be tailored to an organisation’s specific needs and risk profile. The framework encourages organisations to assess their current cybersecurity posture, set goals, and prioritise actions based on their risk assessment. It also emphasises the importance of continuous improvement and adaptation to evolving cyber threats [

36]. However, it is important to note that the NIST Cybersecurity Framework has some limitations: the framework does not provide specific technical implementation details or prescribe specific security controls. It provides high-level guidance and principles, leaving the implementation details to the organisation’s discretion [

37].

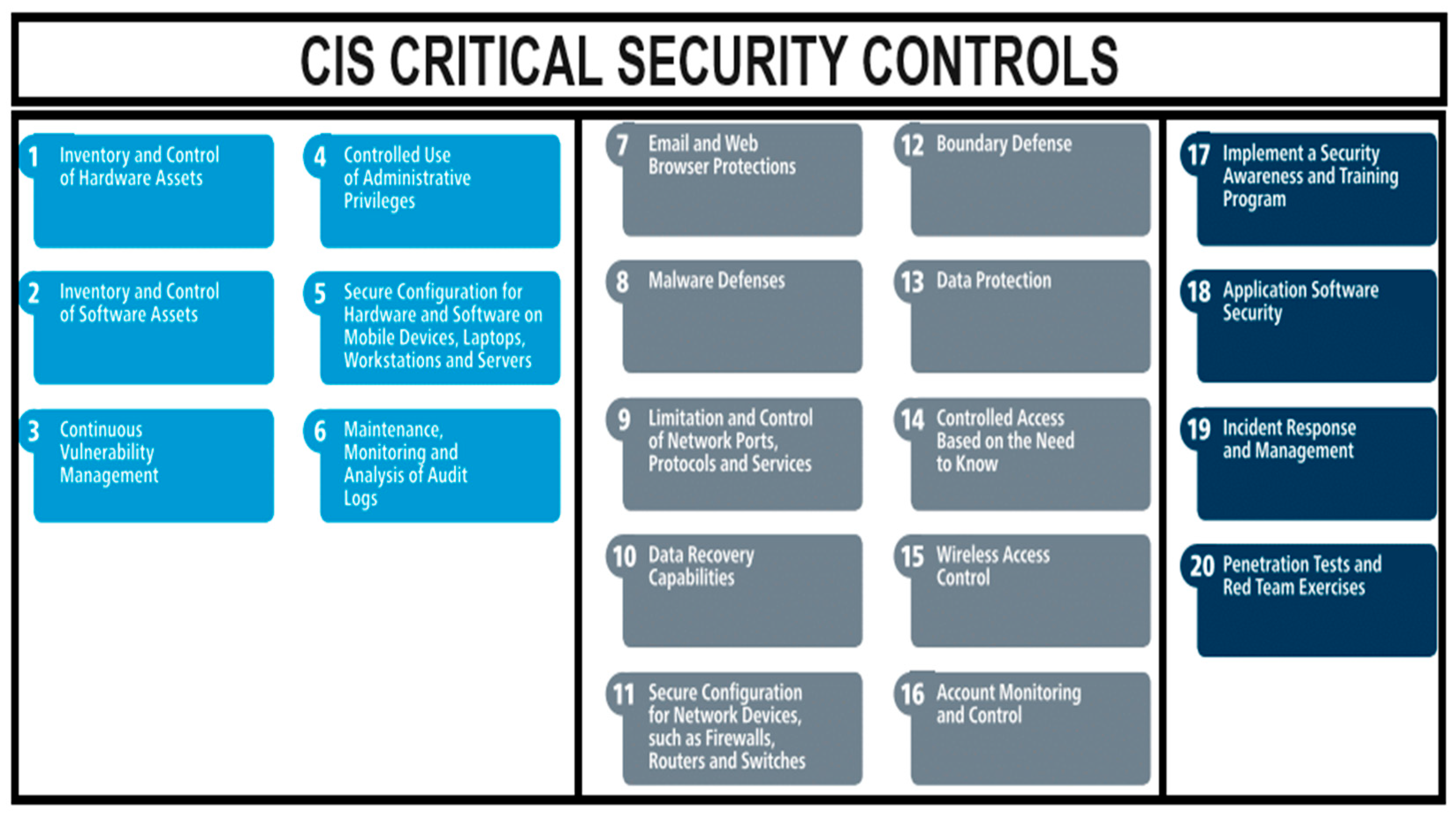

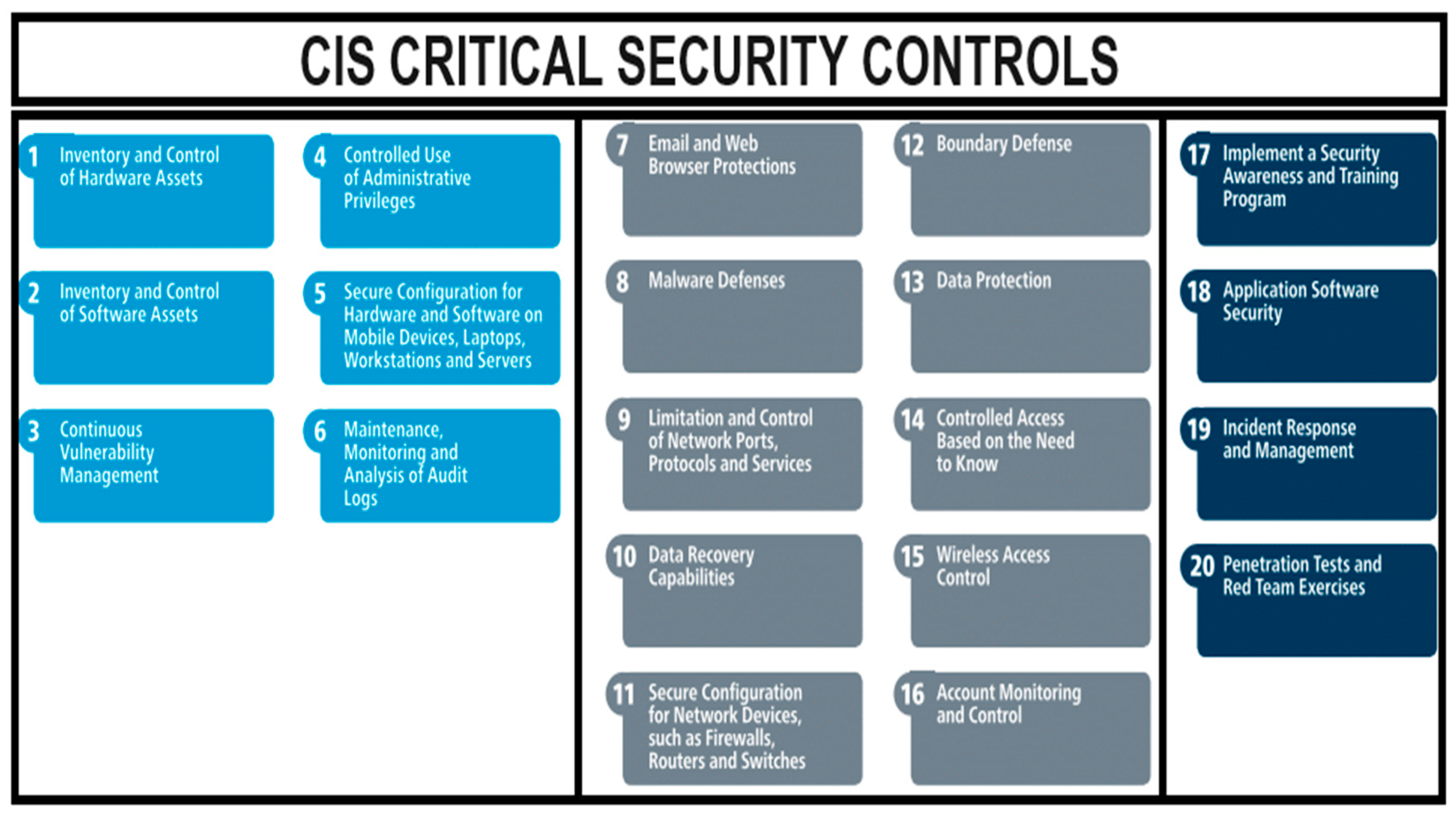

2.4.2. Centre for Internet (CIS) Critical Security Controls

Another significant cybersecurity framework widely used in the finance industry is the CIS Critical Security Controls [

38]. These controls offer a prioritised set of actions organisations can implement to enhance their cybersecurity posture. The controls encompass various areas, including inventory and control of hardware and software assets, continuous vulnerability management, secure configuration for hardware and software, and controlled use of administrative privileges, as shown in

Figure 4.

The CIS Critical Security Controls are specifically designed to address common cybersecurity risks and provide organisations with a roadmap for implementing effective security measures. By adhering to these controls, organisations can improve their ability to detect and respond to cyber threats, reduce vulnerabilities, and safeguard sensitive financial information.

Inventory and Control of Hardware and Software Assets: This control focuses on maintaining an up-to-date inventory of all hardware and software assets within the organisation. It aids in identifying and managing potential vulnerabilities and ensuring that only authorised devices and software are utilised;

Continuous Vulnerability Management: This control emphasises the importance of regularly scanning and assessing systems for vulnerabilities. By implementing vulnerability management processes, organisations can promptly identify and remediate vulnerabilities, thereby reducing the risk of exploitation by attackers;

Secure Configuration for Hardware and Software: It is a critical control that emphasises the implementation of secure configurations for all hardware and software assets. This control ensures that systems are configured securely, following industry best practices and minimising potential security breaches;

Controlled Use of Administrative Privileges: It is another important control that aims to limit and monitor the use of administrative privileges within the organisation.

These controls, along with others included in the CIS Critical Security Controls framework, provide stakeholders with a comprehensive approach to managing cybersecurity risks in the finance industry. By addressing areas such as inventory and control of assets, vulnerability management, secure configuration, and controlled use of administrative privileges, organisations can enhance their ability to detect, respond to, and mitigate cyber threats in the finance industry. However, one limitation of the CIS Critical Security Controls is that they are not updated as frequently as other frameworks. Cyber threats and attack techniques constantly evolve, and new vulnerabilities and risks emerge regularly [

39].

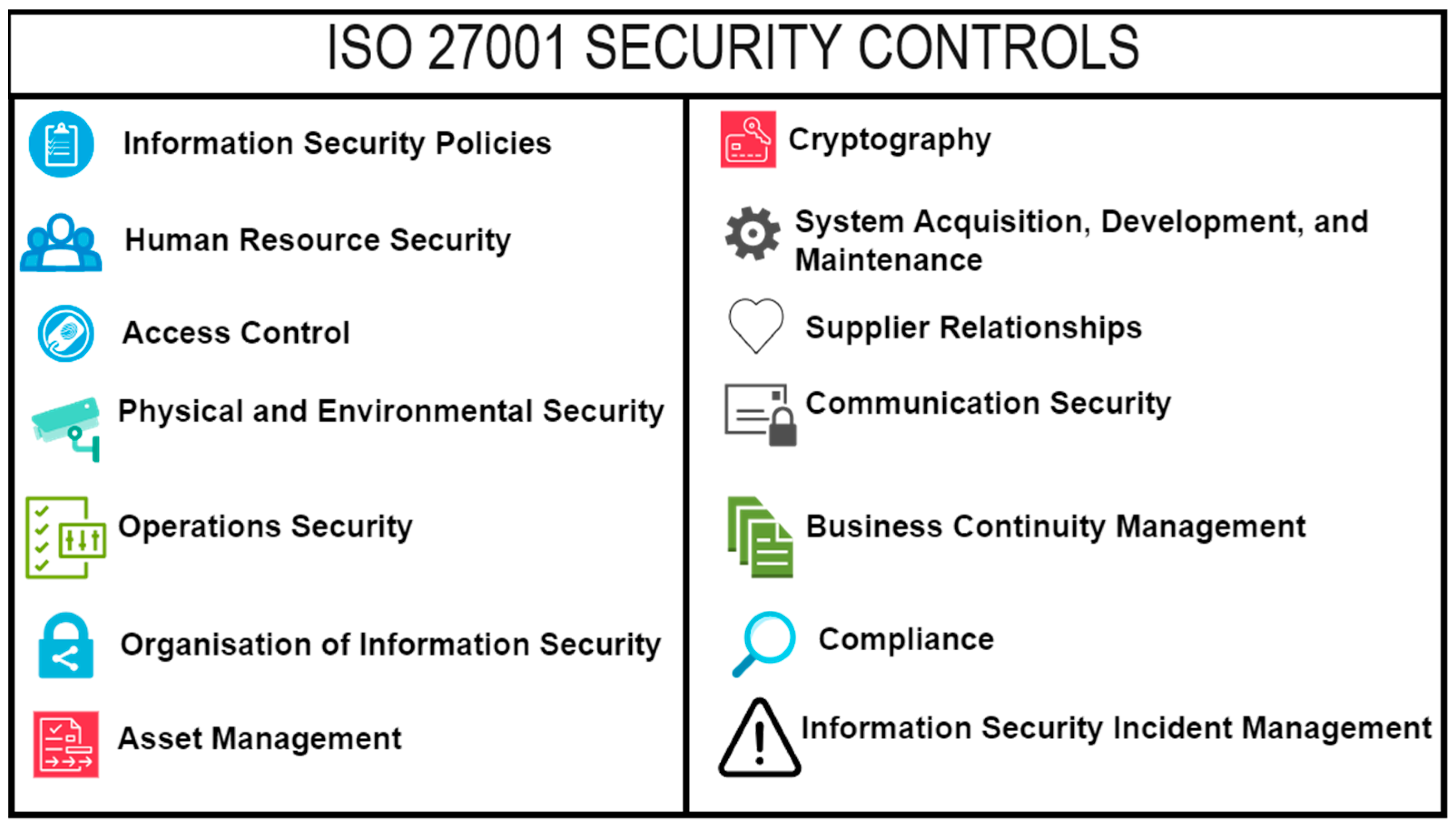

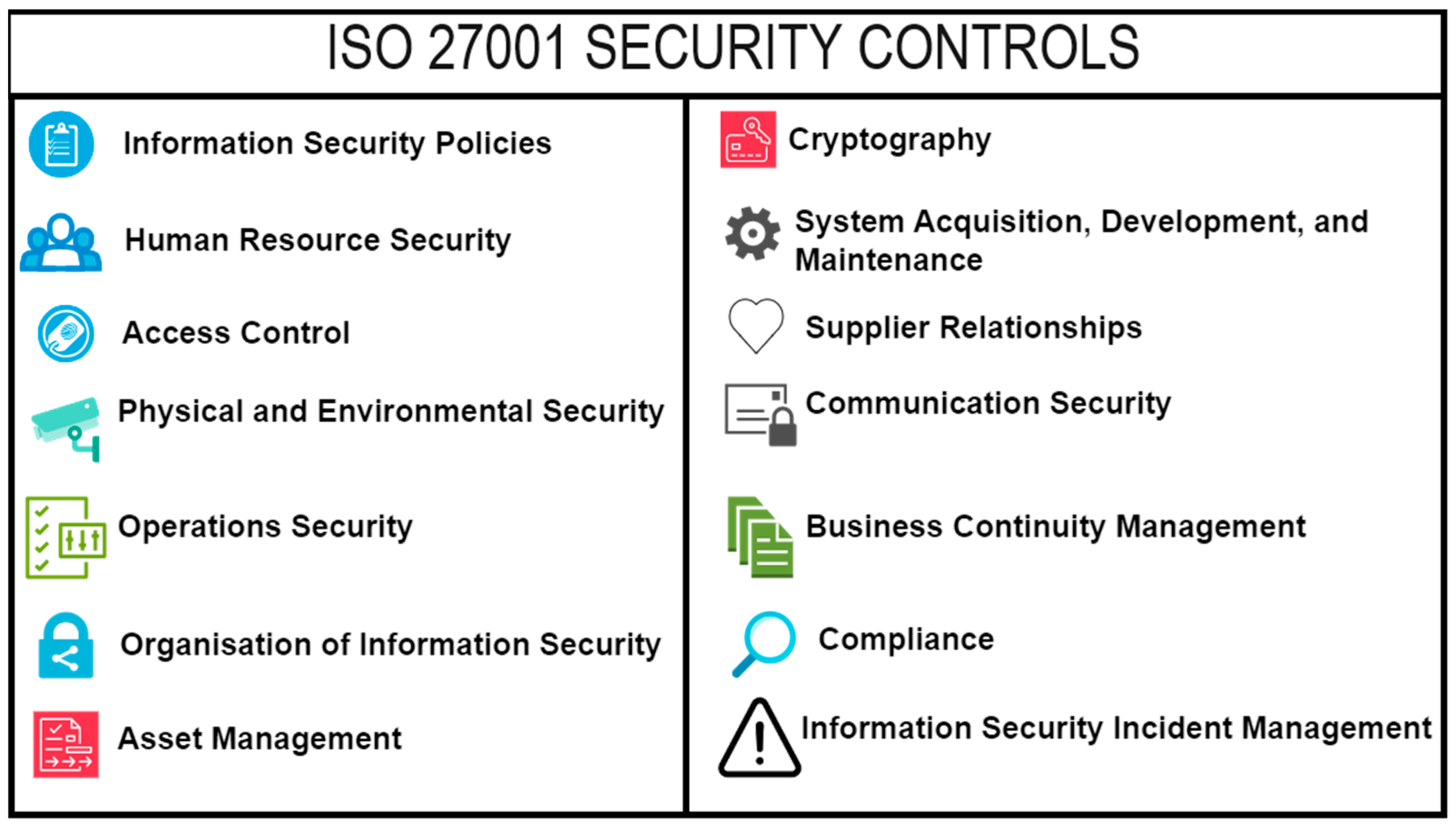

2.4.3. ISO 27001/27002

ISO 27001/27002 [

40] is an international standard for information security management systems (ISMS) that banks and financial institutions widely adopt to ensure the confidentiality, integrity, and availability of their information. This standard provides a systematic approach to managing sensitive company information, including financial data. It outlines a risk management process and provides a set of controls that organisations can implement to protect their information assets [

41].

The ISO 27001 standard focuses on establishing, implementing, maintaining, and continually improving an ISMS within the organisation. It provides a framework for organisations to identify and assess information security risks, define security objectives and controls, and monitor and review the effectiveness of the implemented controls as shown in

Figure 5 [

42]. The standard emphasises the importance of a risk-based approach to information security management, ensuring that controls are implemented based on the identified risks and the organisation’s risk appetite [

43].

ISO 27002, on the other hand, provides a code of practice for information security controls. It offers a comprehensive set of security controls that organisations can select and implement based on their specific needs and risk profiles. These controls cover various areas, such as access control, cryptography, physical and environmental security, and incident management [

44]. By implementing the controls outlined in ISO 27001/27002, banks and financial institutions can establish a robust information security management system.

This helps them protect sensitive financial data, prevent unauthorised access, and mitigate the risk of security breaches. The standard provides a structured and systematic approach to managing information security risks, ensuring appropriate controls are in place to safeguard critical information assets [

45]. However, it is important to note that implementing ISO 27001/27002 requires significant effort and resources. Organisations need to conduct a thorough risk assessment, develop and implement security policies and procedures, and regularly monitor and review the effectiveness of the implemented controls. This can be a complex and time-consuming process, requiring the involvement and commitment of various stakeholders within the organisation [

46].

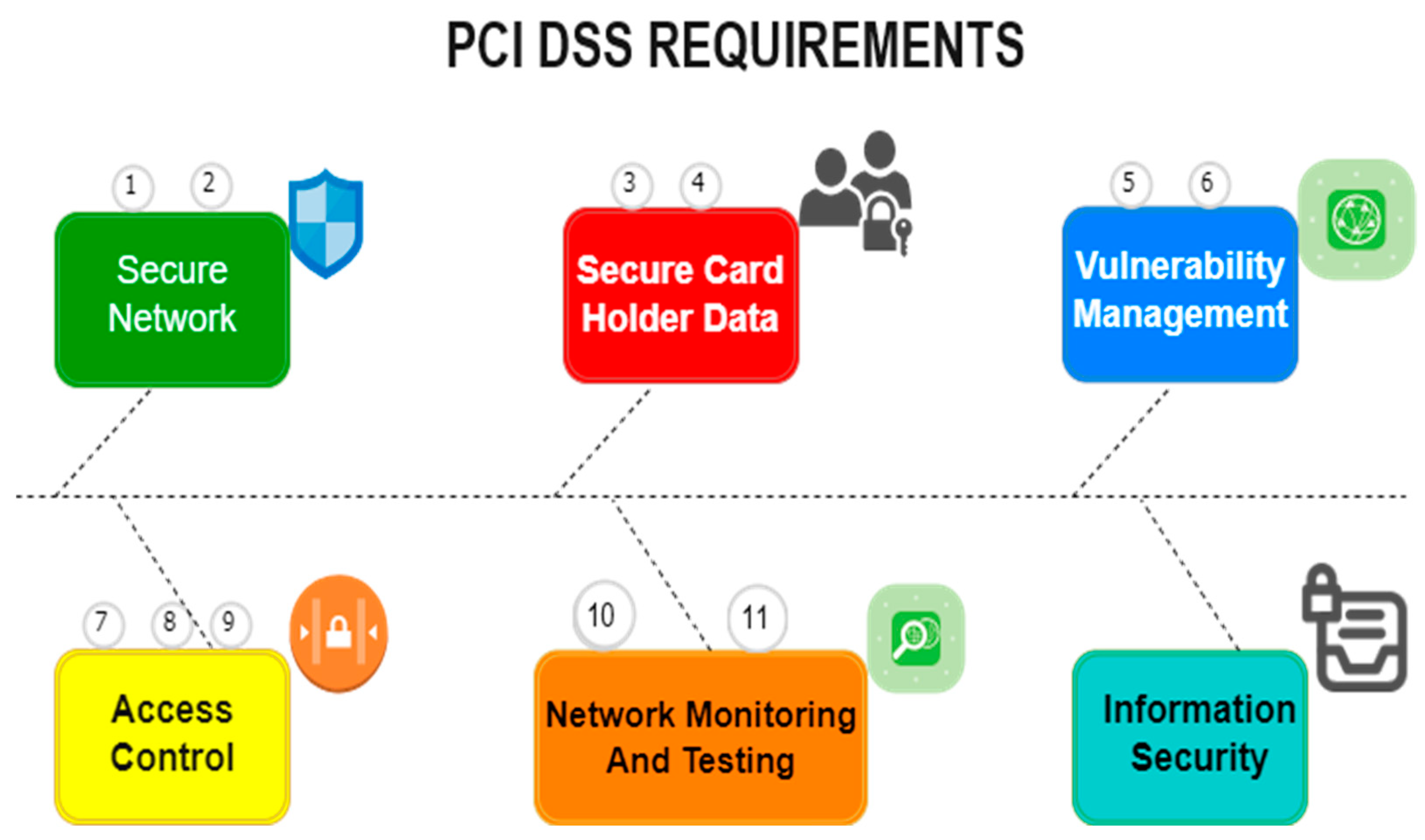

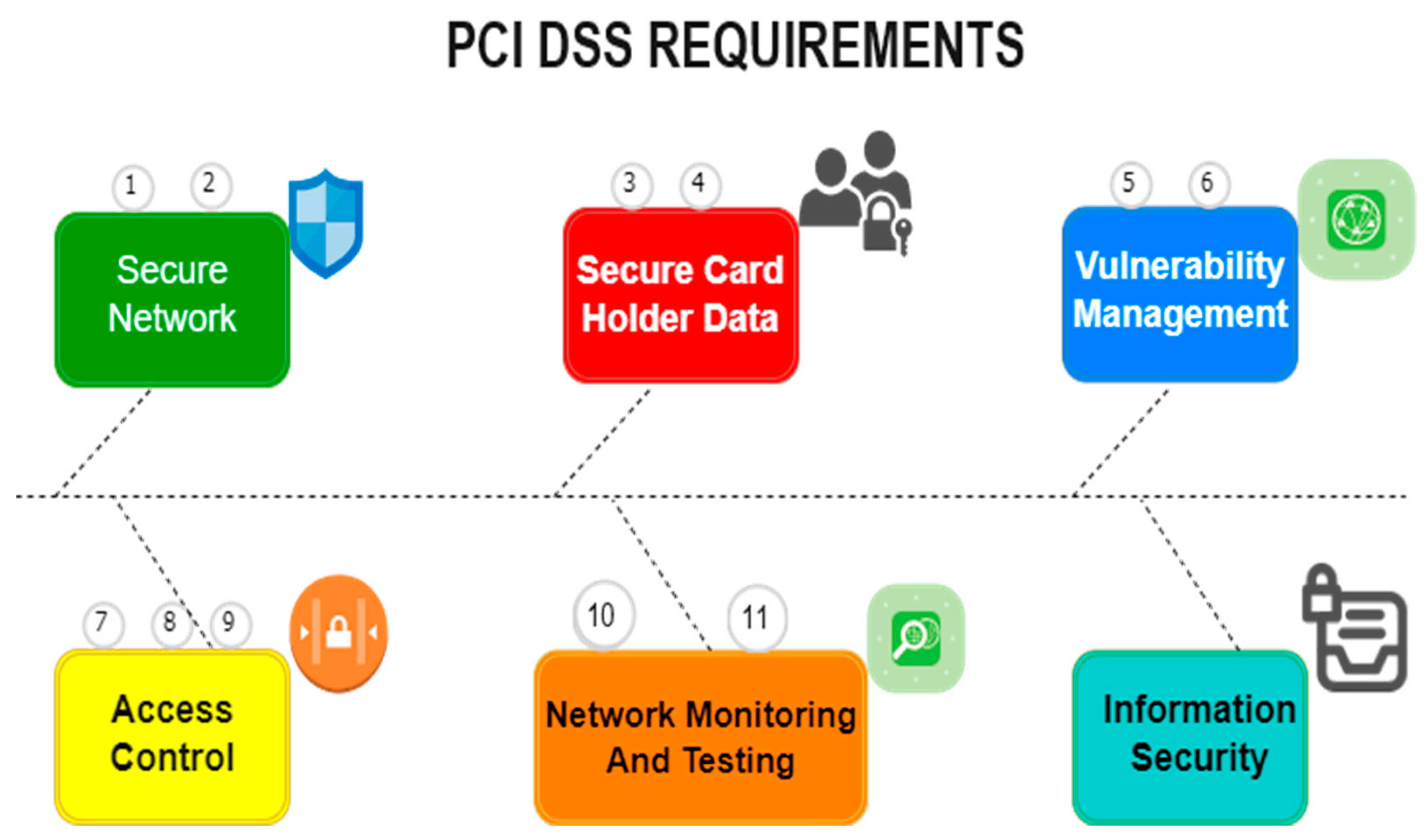

2.4.4. PCI DSS

The Payment Card Industry Data Security Standard (PCI DSS) is a global standard specifically designed to secure cardholder data in credit card transactions. It is essential for financial institutions involved in payment card transactions and aims to protect sensitive financial information. The PCI DSS standard outlines a set of requirements that organisations must comply with to ensure cardholder data security. These requirements cover various aspects of information security, including network security, access control, encryption, and vulnerability management, as shown in

Figure 6. By adhering to these requirements, organisations can mitigate the risk of data breaches and unauthorised access to cardholder information [

47]. One of the key aspects of PCI DSS is the requirement for organisations to maintain a secure network infrastructure. This includes implementing firewalls, regularly updating security patches, and restricting access to cardholder data. By maintaining a secure network, organisations can prevent unauthorised access and protect cardholder information from potential threats [

48].

Another important requirement of PCI DSS is the implementation of strong access control measures. This involves assigning unique user IDs, implementing strong authentication mechanisms, and regularly reviewing user access privileges. By enforcing strict access controls, organisations can ensure that only authorised individuals have access to cardholder data [

50]. Encryption is also a crucial component of PCI DSS. The standard requires organisations to encrypt cardholder data during transmission and storage. Encryption helps protect sensitive information from being intercepted or accessed by unauthorised parties, thereby reducing the risk of data breaches [

51].

Furthermore, PCI DSS emphasises the importance of regular vulnerability scanning and penetration testing. Organisations are required to conduct regular scans to identify and address vulnerabilities in their systems. By proactively identifying and addressing vulnerabilities, organisations can reduce the risk of exploitation by attackers [

52]. However, it is important to note that PCI DSS has a limited scope and may require supplementary security measures to ensure comprehensive protection of cardholder information [

53].

The finance industry, including the banking sector, has recognised the critical importance of cybersecurity. The above-mentioned cybersecurity frameworks have been developed to guide the finance industry in managing cybersecurity risks and protecting sensitive financial information. These frameworks provide a structured approach to identify, protect, detect, respond to, and recover from cyber threats. However, it is crucial for the finance industry to continuously monitor and improve their cybersecurity measures to stay resilient against evolving cyber threats.

2.5. Real-World Zero Trust Approaches

The rising number of cyber threats targeting financial institutions necessitates shifting from traditional perimeter-based security models to more robust and adaptive frameworks. The Zero Trust model has emerged as a feasible paradigm, with several real-world implementations manifesting its principles in practical settings. This section delves into some of the prominent real-world implementations of the Zero Trust model, including Google’s BeyondCorp, Forrester NGFW/ZTX, the Software-Defined Perimeter (SDP), and VMWare NSX, exploring their architectures, functionalities, and the context of their applicability.

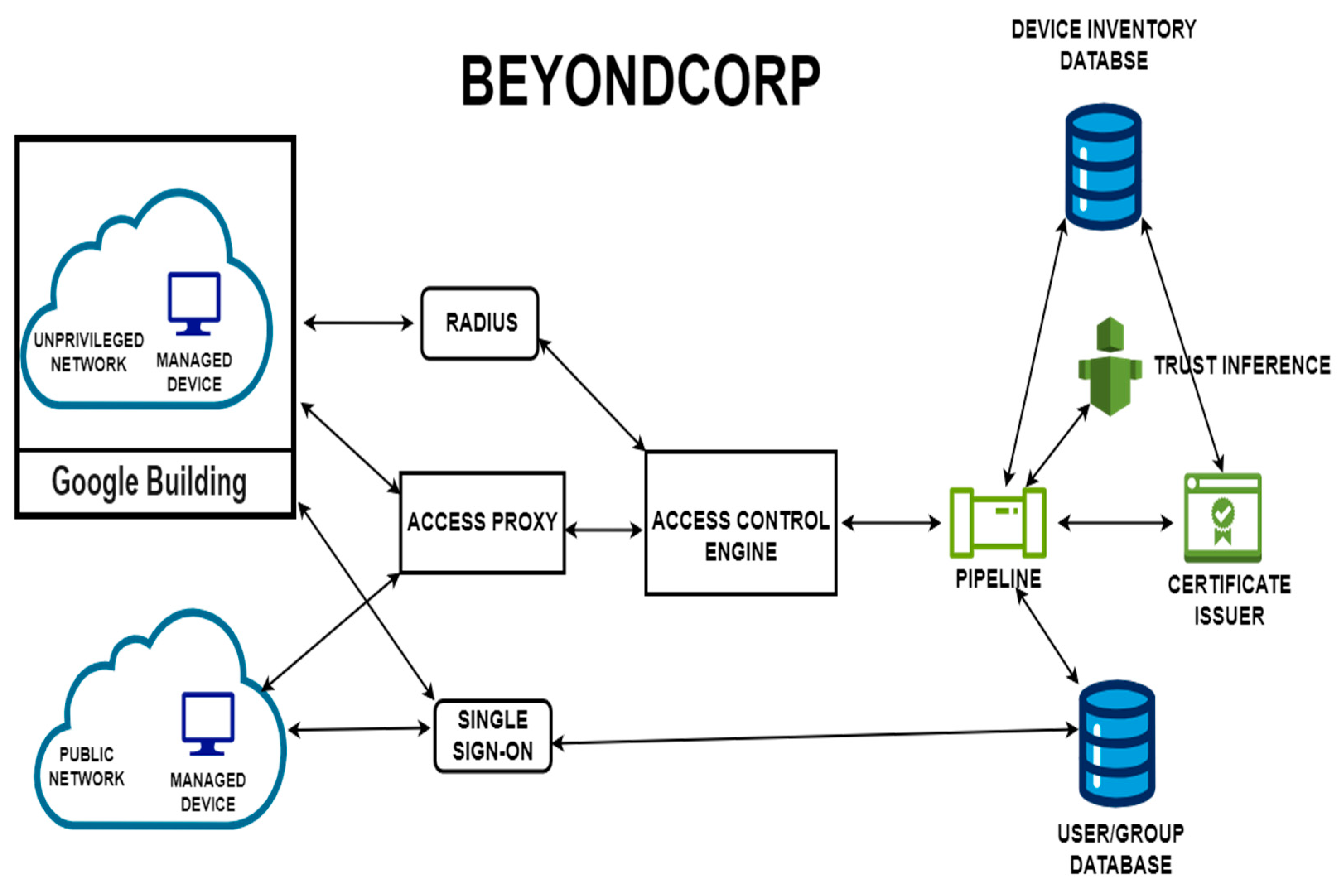

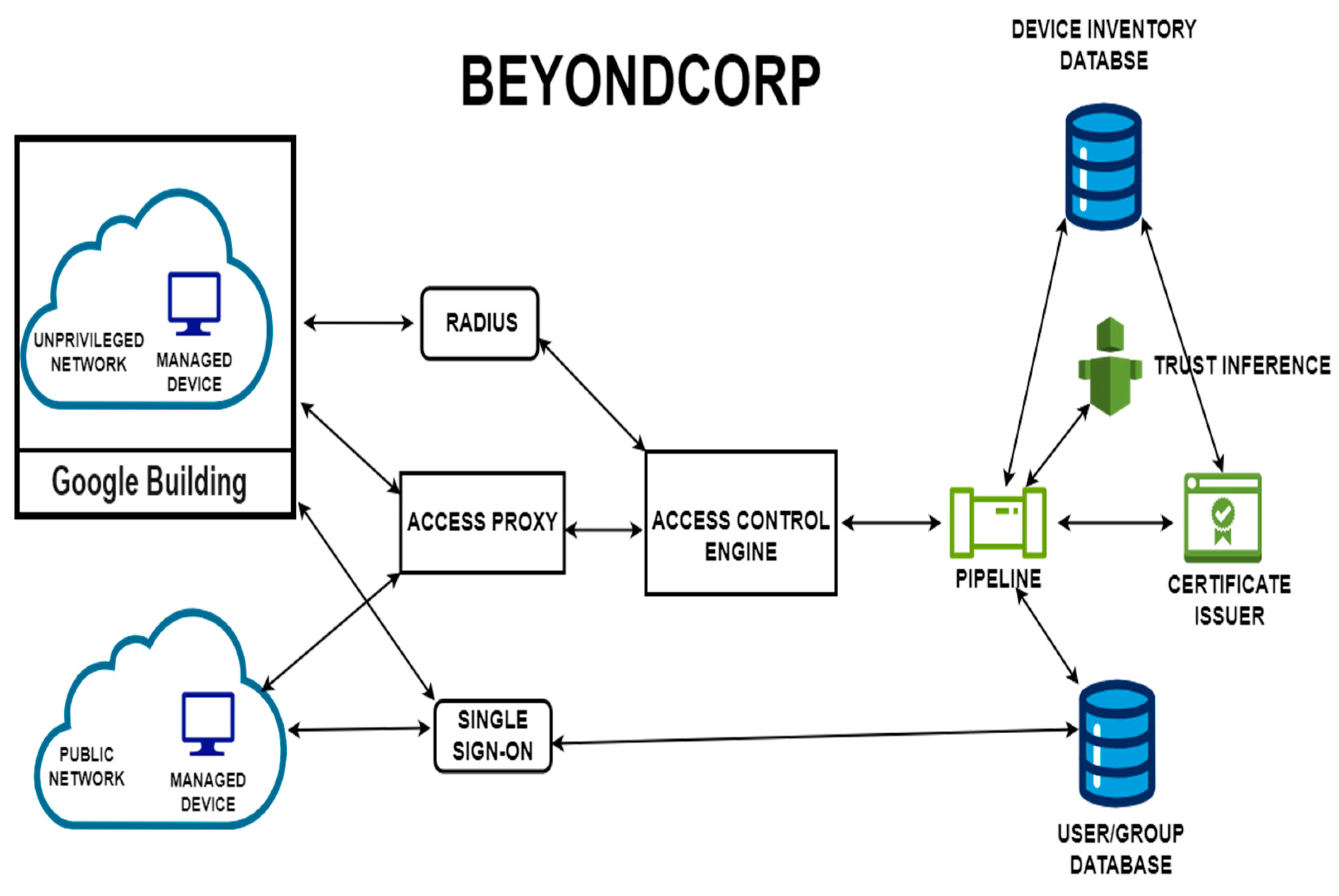

2.5.1. BeyondCorp

BeyondCorp, developed by Google, represents an updated version of the Zero Trust model, using both their extensive expertise and community feedback. By shifting access rules away from network boundaries and focusing on individual users, BeyondCorp eliminates the need for VPNs. This approach aligns with the NIST Zero Trust guidelines for device agent/gateway-based deployment [

54]. The complete structure of BeyondCorp includes key components such as Single Sign-On (SSO), access proxy, control engine, lists of users and devices, security rules, and a trusted database. This creates a strong system for protecting modern applications and services [

55].

BeyondCorp questions the idea that separating network areas is sufficient for protecting sensitive data. Instead, it introduces a user- and device-focused process for authentication and permission when accessing applications. Although promising, this paradigm shift presents challenges in transitioning without disrupting user experiences. The advent of BeyondProd as a cloud-native security service exemplifies the continuous evolution to accommodate varying organisational needs [

7]. BeyondCorp represents an updated version of the Zero Trust model that focuses on individual users and devices rather than network boundaries, as shown in

Figure 7. It eliminates the need for VPNs and introduces a user- and device-focused process for authentication and permission. While promising, the transition to BeyondCorp may present challenges in terms of the user experience. Nonetheless, the continuous evolution of BeyondCorp, such as the introduction of BeyondProd, demonstrates its adaptability to meet the evolving needs of organisations.

2.5.2. Forrester NGFW/ZTX

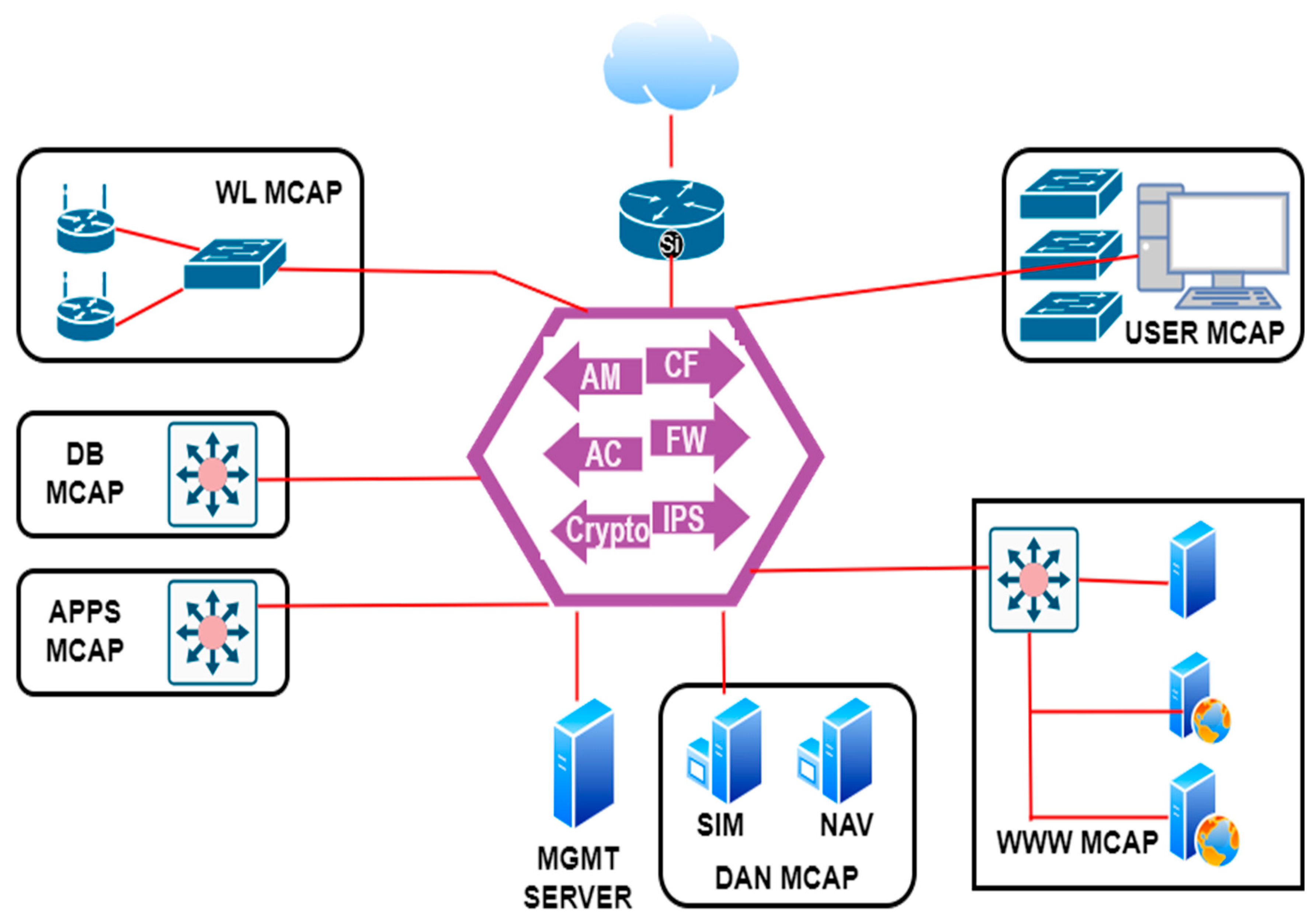

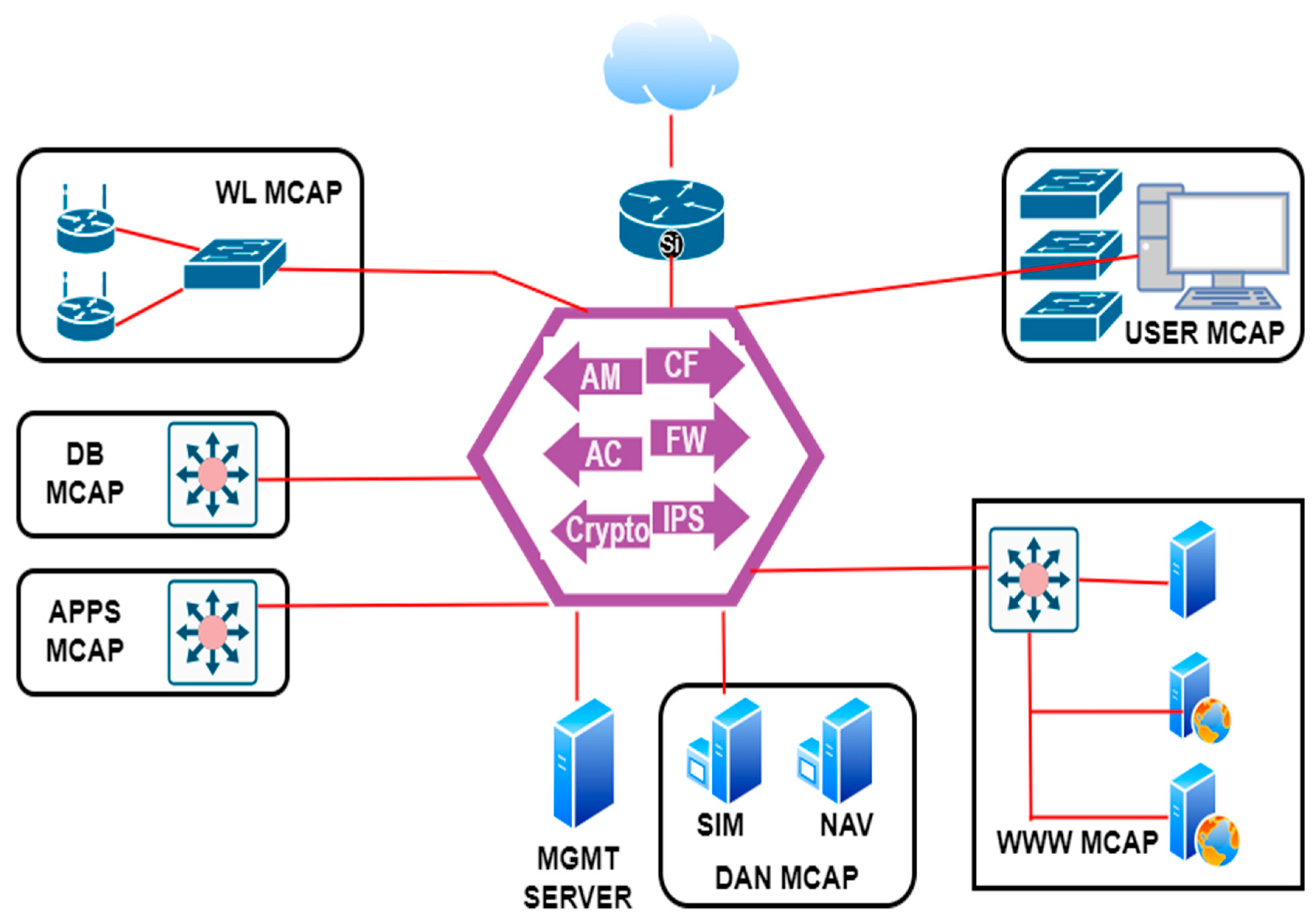

The Forrester NGFW/ZTX model, proposed by Kindervag in 2010, advocates for a centralised engine to segregate the corporate network into micro-core and perimeter (MCAP) segments, as shown in

Figure 8. This model aligns with NIST’s resource portal-Based deployment model and provides a simplistic yet effective framework, particularly suitable for organisations with a large number of IoT devices.

The Forrester Zero Trust eXtended (ZTX) framework expands beyond network segmentation and encompasses seven crucial dimensions where Zero Trust principles apply: networks, data, people, workloads, devices, visibility and analytics, automation, and orchestration. This comprehensive framework enables security personnel to understand how different technologies contribute to network isolation, segmentation, security, data categorisation, encryption, and control principles. It also facilitates the implementation of policies to secure human users, network infrastructure resources, and application workloads in both public and private cloud environments. However, a notable drawback of the Forrester NGFW/ZTX model is the firewall’s inability to authenticate users due to limitations in the segmentation engine [

58]. The model’s limitations in user authentication highlight the need for additional technologies like IAM and VPNs to address this challenge.

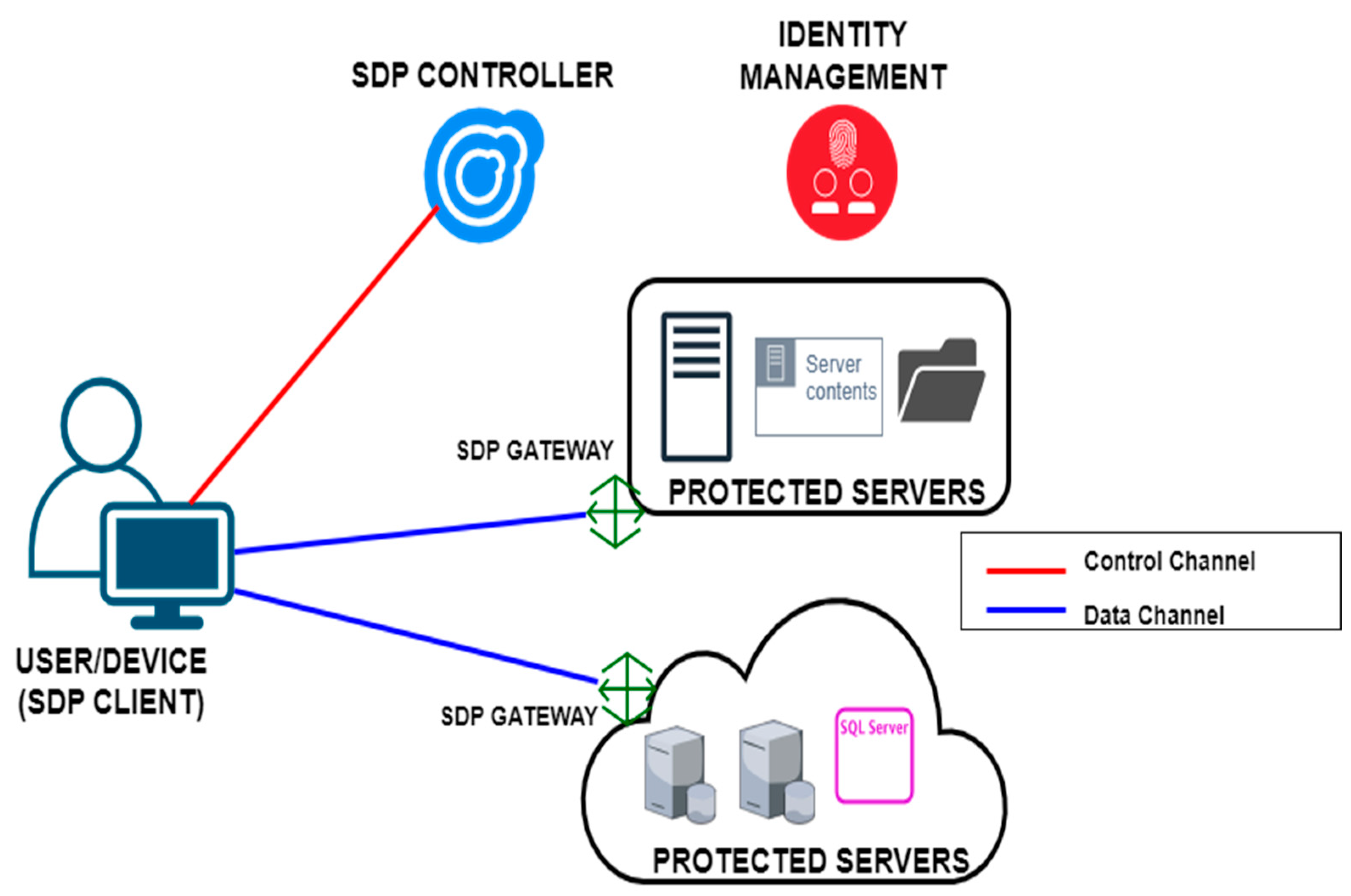

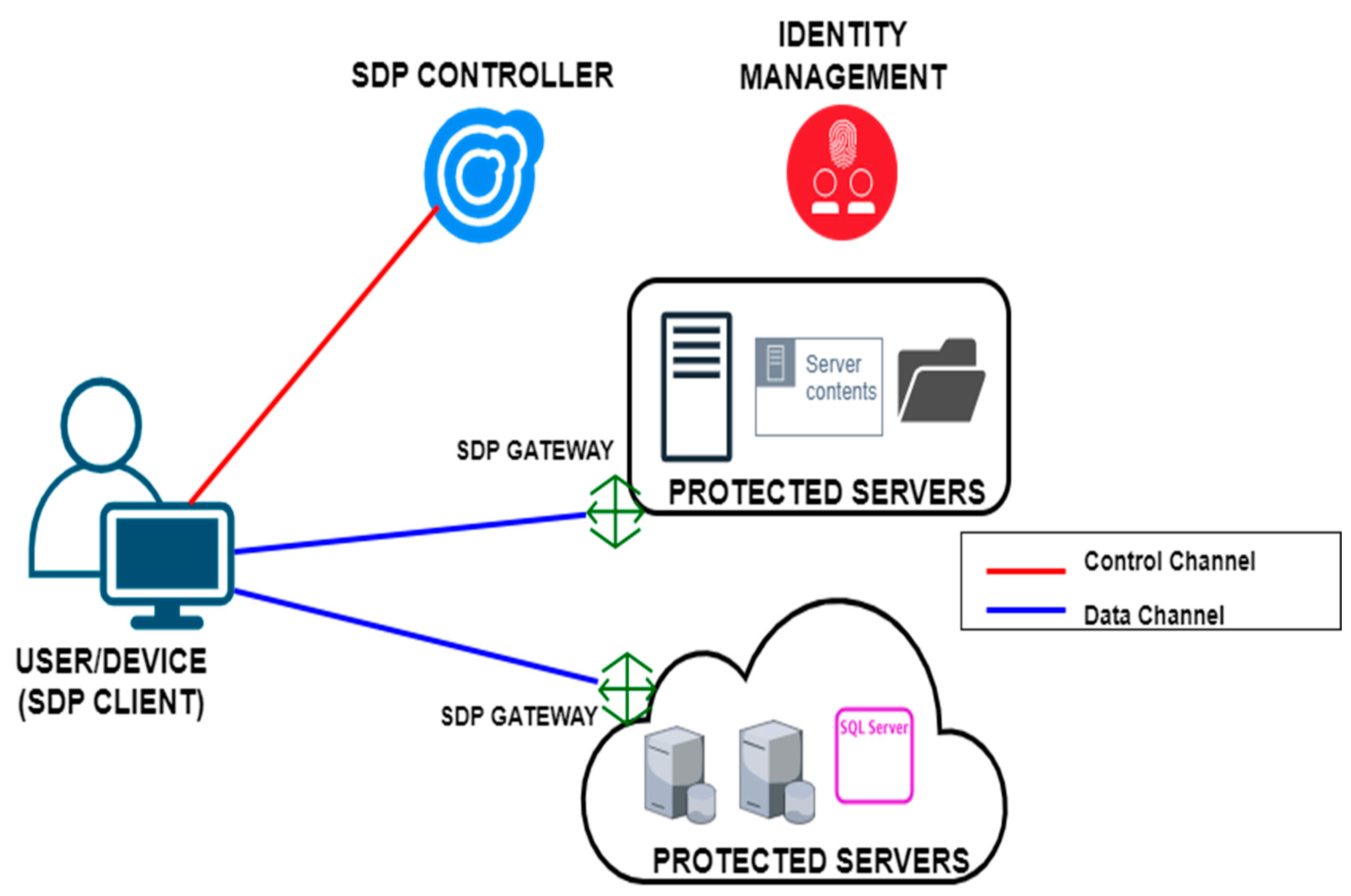

2.5.3. Cloud Security Alliance’s (CSA) Software-Defined Perimeter

The Software-Defined Perimeter (SDP) model, originating from the U.S. Department of Defence, emphasises network access micro-segmentation and creates on-the-fly one-to-one connections between users and the required resources. Unlike traditional models, SDP focuses on protecting both the user and the application, employing a unique session initiation protocol to enable precise access control [

59].

The SDP framework consists of two essential components: the SDP controller and the SDP host or gateway, as shown in

Figure 9. These components work together to establish a secure communication channel between authorised entities. This framework offers a more granular and dynamic approach to network security. The SDP model aligns with the principles of Zero Trust, as it emphasises the need for strict access control and verification of both users and devices. By implementing SDP, organisations can achieve a higher level of security by reducing the attack surface and ensuring that only authorised entities can access specific resources. However, the implementation process may pose challenges, requiring careful consideration and setup on both the resource and endpoint.

2.5.4. VMware NSX

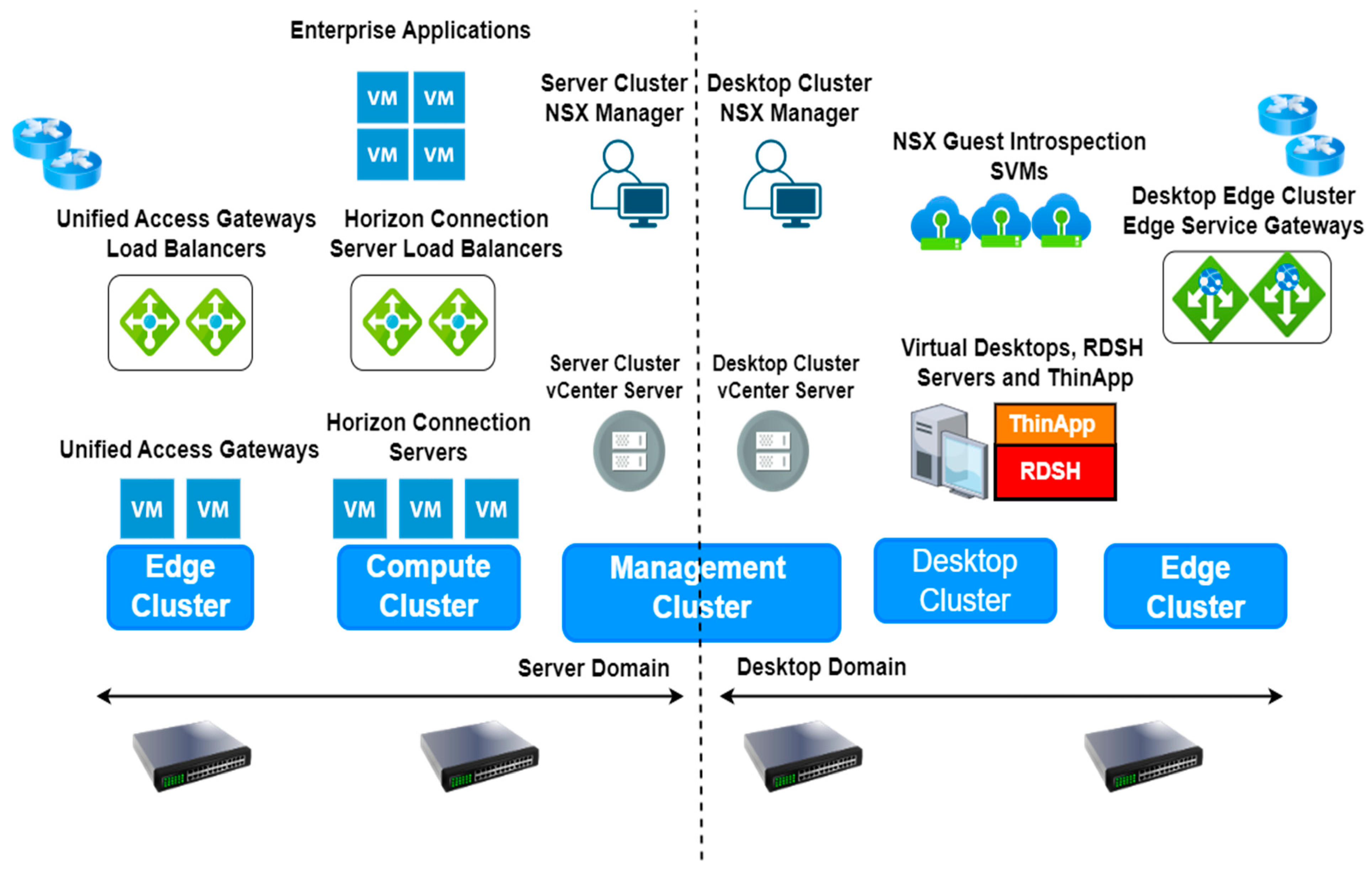

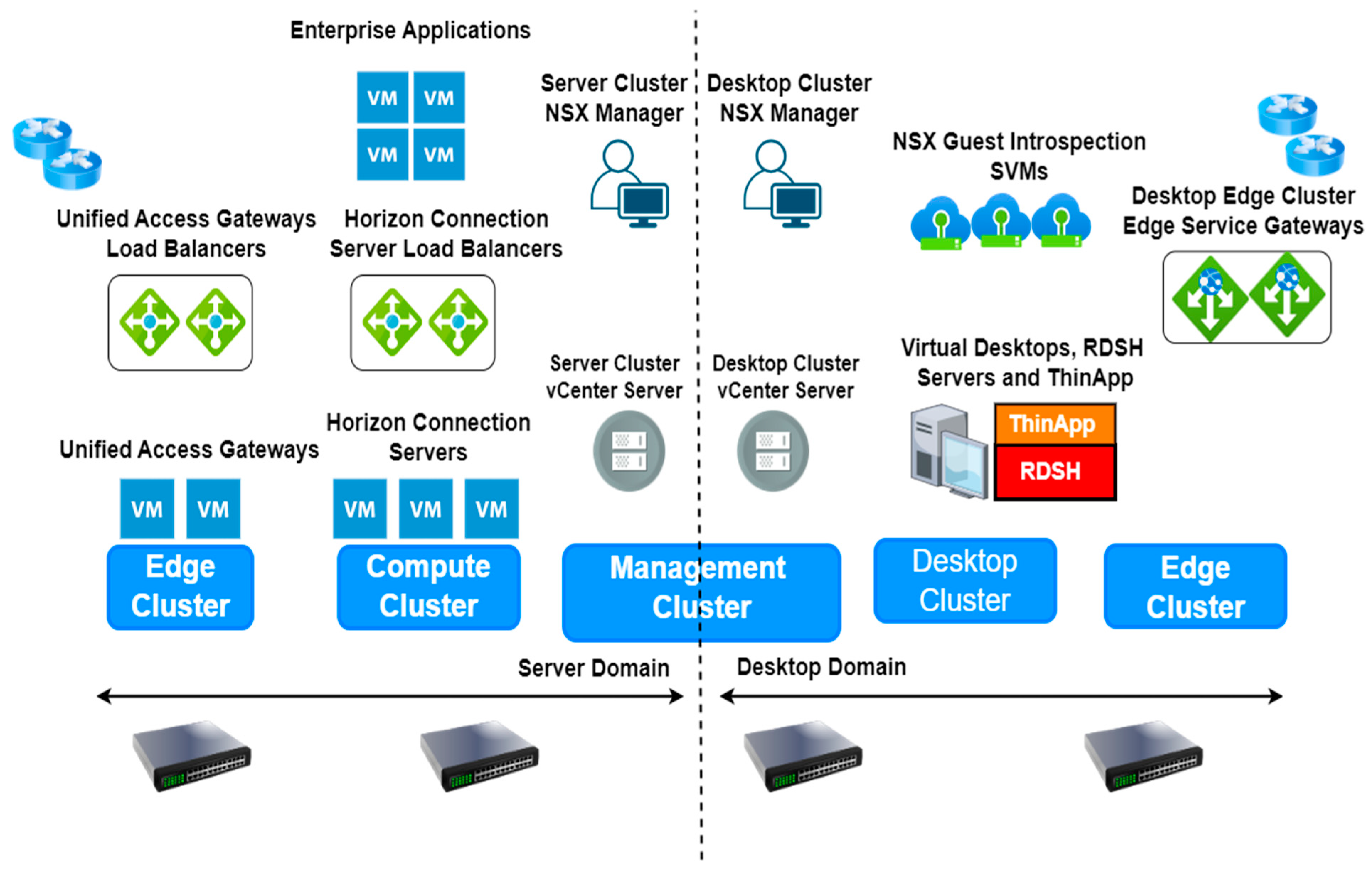

The VMware NSX model, based on Zero Trust principles, offers network virtualisation technology that includes various components for the development, security, and management of virtual networks, as shown in

Figure 10. The core principle of the NSX Data Centre is micro-segmentation, which allows for precise control over traffic flow across different operational environments.

The VMware NSX model demonstrates a virtualised desktop approach that effectively thwarts attackers’ attempts to establish a persistent presence within the network. The network virtualisation technology and focus on micro-segmentation align with Zero Trust principles and provide organisations with a robust framework for network security. However, the requirement for virtualisation in the model can present challenges, particularly in IoT systems where virtualisation may be necessary for sensors and operational technology [

62].

2.5.5. Comparative Analysis of the Real-World Zero Trust Model Implementations

Table 1 effectively aligns practical implementations of the Zero Trust model with the main pillars of the Zero Trust model, offering a comprehensive view of the performance, benefits, and limitations of each implementation. This comparative analysis provides a solid base for identifying the most fitting Zero Trust strategy across different organisational scenarios, with a focus on the financial sector.

It is evident from

Table 1 that BeyondCorp excels in network segmentation and strong user and device verification processes, making it suitable for cloud-hosted applications. VMware NSX shows proficiency in micro-segmentation and transport encryption alongside virtualised desktop solutions, but it can be costly. The SDP model stands out for its cost-effective application integration and strong access control mechanisms, though it requires a significant initial setup effort. Forrester’s NGFW/ZTX framework, while offering simplified deployment in BYOD environments, faces challenges in direct user authentication with its segmentation engine.

2.6. Real-World Applications of Blockchain Technology in Financial Institutions

Blockchain technology has been increasingly adopted in the banking and finance industries, transforming established practices. It has decentralised and streamlined vital institutional functions, including supply chain management, marketing, and finance [

8]. Financial institutions globally are increasingly adopting blockchain to transform conventional operations, streamline processes, and offer innovative services. This section explores the real-world uses of blockchain in the finance industry, highlighting innovators and the advantages and challenges of adopting blockchain technology.

Blockchain technology has found significant success in direct financing, bank credit, and supply chain finance, offering transparency and financial data security [

63]. Blockchain has become the focus of global attention, presenting unprecedented opportunities and challenges for traditional credit businesses in commercial banks [

64].

Among the pioneers, Santander Bank has significantly marked its presence by leveraging blockchain for international payments. In 2018, Santander unveiled the Santander One Pay FX service, utilising Ripple’s blockchain technology to facilitate faster, more transparent, and cost-efficient cross-border transactions, setting a benchmark in the industry [

65]. Similarly, HSBC’s venture into blockchain for trade finance transactions in 2018 stands as a testament to the technology’s potential to condense the traditional processing timeline from days to mere hours, thereby enhancing operational efficiency and reducing risks [

66].

The application of blockchain extends beyond payments and trade finance. Institutions such as Barclays and Deutsche Bank are exploring blockchain for identity verification and Know-Your-Customer (KYC) processes. These efforts aim to establish a shared, immutable ledger for KYC, potentially reducing redundancy and costs while improving the customer onboarding experience and compliance with regulatory mandates [

67,

68]. Furthermore, JPMorgan Chase’s initiation of the Interbank Information Network (IIN), rebranded as Liink, showcases blockchain’s capability to refine interbank communications and settlements. By employing a blockchain-based network, Liink facilitates quicker and more secure payment validations among participating banks, illustrating the efficiency gains achievable through blockchain adoption [

69].

Blockchain technology has extended the traditional functions of banking applications and infrastructure, offering more convenient and efficient financial management. Therefore, the adoption of blockchain technology in the banking and finance industry has brought about significant advancements, offering transparency, security, and efficiency in various financial applications.

Despite the clear benefits, including enhanced security, reduced transaction times, and increased transparency, the journey towards widespread blockchain adoption in finance is not devoid of challenges. Scalability concerns, integration complexities with legacy banking systems, and strict regulatory requirements persist, emphasising the need for continued innovation and regulatory engagement.

2.7. Current Security Models in the Finance Industry

The security infrastructure of the finance industry plays a crucial role in protecting sensitive data and financial assets. Over time, various security models have been developed and implemented to address these challenges. This section discusses the Castle-and-Moat model, Layered Security model, Defence in Depth, Bell–LaPadula model, and Biba Integrity model, each offering unique mechanisms for protecting financial institutions.

2.7.1. Castle-and-Moat Model

The Castle-and-Moat model in the finance industry is a traditional security paradigm that emphasises strong perimeter defence to protect resources within. Similar to how mediaeval castles were safeguarded by surrounding moats, this model aims to create a formidable barrier against external threats. However, it operates under the assumption that once inside the perimeter, entities are trusted, which, in modern cybersecurity landscapes, can be a significant vulnerability.

This model focuses primarily on establishing robust perimeter defences such as firewalls, intrusion detection systems, and boundary routers. The goal is to scrutinise and control incoming and outgoing network traffic, thereby preventing unauthorised access to the institution’s internal networks and systems [

70].

One of the critical aspects of the Castle-and-Moat model is its emphasis on external threats. It is built on the premise that attacks are likely to originate from outside the organisation. Consequently, considerable resources are allocated to fortifying external defences. While effective against direct external attacks, this model often overlooks the potential for internal threats or breaches that occur due to compromised credentials.

In the context of financial institutions, where the protection of sensitive data and financial assets is crucial, the Castle-and-Moat model has been a longstanding approach. It provides a fundamental level of security by creating a well-defined boundary around the institution’s digital assets. However, the increasing sophistication of cyber threats and the rise of insider threats have exposed limitations to this model. The Castle-and-Moat approach is less effective in a landscape where attackers can bypass perimeter defences through social engineering, phishing attacks, or by exploiting insiders. Once inside the perimeter, attackers can move laterally with little resistance, as internal security is often less stringent [

71].

2.7.2. Layered Security Model

The Layered Security model, distinct from the Defence-in-Depth strategy, is a specific approach to cybersecurity focusing on implementing multiple layers of protection across different aspects of the IT infrastructure. In the finance industry, the Layered Security model is essential for protecting sensitive data and systems against a range of cyber threats. This model operates on the premise that no single defence measure is sufficient to thwart all types of cyber threats. Instead, security is enhanced by integrating various protective measures at different layers within the IT environment. The key components of the Layered Security model typically include the following:

Perimeter Security: This is the outermost layer, involving technologies such as firewalls and intrusion detection systems to monitor and control incoming and outgoing network traffic, acting as a barrier to external threats;

Network Security: Within the network, measures such as secure VPNs, network segmentation, and intrusion prevention systems are used to safeguard data in transit and to limit the spread of attacks within the network [

72];

Endpoint Security: At the device level, endpoint security solutions like antivirus software, anti-malware programs, and personal firewalls are employed to protect individual devices that access the network;

Application Security: This layer focuses on protecting software applications from threats. It involves secure coding practices, regular vulnerability scanning, and application firewalls to defend against application-level attacks [

73];

Data Security: The innermost layer focuses on safeguarding the data itself, irrespective of where it is stored or how it is transmitted. This involves encryption, access controls, and data loss prevention strategies to ensure data confidentiality, integrity, and availability;

Physical security: The outermost layer involves measures such as access control systems, surveillance cameras, and secure facilities, aiming to prevent unauthorised physical access to critical systems and data centres.

In the financial sector, the Layered Security model is particularly effective due to its comprehensive nature. It ensures that if a threat bypasses one layer of security, additional layers are in place to mitigate the risk. This model is crucial for protecting against a variety of threats, ranging from external hacking attempts to internal data leaks. While this model addresses some limitations of the Castle-and-Moat model by implementing multiple defence layers across the IT infrastructure, it is still not inadequate for dynamically responding to the evolving and sophisticated nature of modern cyber threats.

2.7.3. Defence in Depth

The Defence-in-Depth approach is crucial in the finance industry to protect against a wide range of threats. The authors in [

74] argue that the legal environment, particularly as constructed by the enforcement activities of regulators, significantly influences the likelihood that organisations will effectively implement self-regulatory commitments, highlighting the importance of legal and regulatory layers in the Defence-in-Depth strategy for financial security. Furthermore, the authors in [

75] propose a 16-component model of financial security management, emphasising the systemic nature of financial security. This comprehensive model aligns with the concept of Defence in Depth by incorporating multiple layers of security parameters, including organisational culture, sustainable development, and systemic optimisation, to fortify the financial infrastructure against potential threats.

This model is based on the concept that no single defence mechanism is sufficient against the variety of threats faced in the financial sector. For example, if there was a physical theft, how could information be guarded against a forensic data recovery? Among other concerns are threat delay, rapid notification, and response when attacks and disasters are underway. The key components of the Defence-in-Depth strategy include the following:

Layered Security Components: Incorporating the elements of the Layered Security model, such as perimeter, network, endpoint, application, and data security;

Monitoring and Alerting: Continuously surveilling systems to detect and alert suspicious activities, an essential component for early threat detection;

Emergency Response: Readiness for immediate action during security incidents, ensuring rapid containment and mitigation;

Authorised Personnel Activity: Managing and monitoring actions of authorised users to prevent insider threats and unauthorised access;

Disaster Recovery: Developing robust processes to ensure business continuity and data integrity in the event of significant disruptions or disasters;

Criminal Activity Reporting: Implementing procedures for the reporting and handling of criminal activities essential for legal compliance and threat intelligence;

Forensic Analysis: Conducting detailed investigations post-breach, including scenarios like physical theft, to understand attack vectors and prevent future incidents.

Although this model offers a more comprehensive defence through a multi-layered strategy, there are still gaps in addressing real-time threats and ensuring seamless integration of various security components.

2.7.4. Bell–LaPadula Model

In the finance sector, the Bell–LaPadula model’s principles are particularly relevant. Financial institutions often handle sensitive client data across various levels of confidentiality. The model maintains data confidentiality by categorising both users (subjects) and data files (objects) in a non-discretionary manner [

76]. This approach aligns with the industry’s need for a robust framework to handle multiple data categorisations securely. Developed by physicists David Elliot Bell and Leonard J. LaPadula, the model is recognised as the first mathematical framework aimed at restricting unauthorised access to confidential information. Its core features include an access matrix for discretionary access control (ds-property), the “simple security” or “no read-up” rule (ss-property), and the “star property” or “no write-down” rule. These properties ensure that a system adheres to strict confidentiality protocols.

The primary benefit of using this security model is that subjects and objects cannot change their security levels after they have been created. Another advantage is that subjects and objects cannot degrade information [

77]. Despite its theoretical soundness, the Bell–LaPadula model has seen limited practical implementation, with Honeywell Multics being a notable but ultimately unsuccessful case. The model’s primary focus on maintaining confidentiality, without addressing other aspects like access control or covert channels, presents certain challenges. Additionally, the model does not prevent the creation of higher-categorisation objects by any user, posing a risk in environments like finance where data integrity is crucial.

2.7.5. Biba Integrity Model

The Biba model, named after its creator, scientist Kenneth J. Biba, is a critical framework in the realm of information security, particularly focusing on the aspect of integrity. In the finance industry, where the accuracy and consistency of data are paramount, the Biba model’s principles are highly relevant. In financial settings, the stringent approach to maintaining the data integrity of the Biba model is crucial. It categorises users (subjects) and data files (objects) without discretion, ensuring that integrity levels are strictly adhered to. This model is a response to the limitations of the Bell–LaPadula model, which primarily addresses data confidentiality but lacks the ability to ensure complete system integrity.

The Biba model operates on fundamental principles distinct from the Bell–LaPadula model. It enforces “no read-down” and “no write-up” policies, meaning higher integrity levels cannot read data from lower integrity levels, and subjects cannot transmit data from lower to higher security environments [

77]. This approach is especially pertinent in the finance industry, where the integrity of transactional data and financial records is critical.

Currently, some high-assurance systems in production are utilising a combination of the Biba and Bell–LaPadula models. This synergy creates a robust security framework capable of ensuring both the integrity and confidentiality of data, a requirement increasingly significant in the finance sector’s move towards models like Zero Trust [

78]. The Biba Model’s primary advantages are its simplicity and its compatibility with the Bell–LaPadula model, which forms a comprehensive security framework. However, one significant limitation is its lack of mechanisms for authorisation control and confidentiality provision. This drawback requires financial institutions to supplement the Biba model with other security measures to achieve a holistic security posture.

2.8. Comparative Analysis of the Current Security Models Used in the Finance Industry

Table 2 compares the existing security models used in the finance industry based on their strengths, weaknesses, and applications in the finance industry. It provides insights into which security model or combination of models best aligns with specific institutional needs, considering factors like the nature of data, threat landscape, and compliance requirements.

Each of these models plays a significant role in the overarching security strategy of financial institutions. The Layered Security and Castle-and-Moat models provide robust perimeter defences, while Defence in Depth offers a more comprehensive, multi-layered approach. The Bell–LaPadula and Biba models, on the other hand, focus on specific aspects of security: confidentiality and integrity, respectively. The effectiveness of these models in the finance industry lies in their strategic implementation and integration into a cohesive security architecture.

3. Banking Application without Zero Trust Security

This section offers a comprehensive overview of a banking application that lacks Zero Trust security measures, highlighting potential vulnerabilities and emphasising the need for incorporating Zero Trust principles to safeguard sensitive financial data.

3.1. Identity and Access Management (IAM)

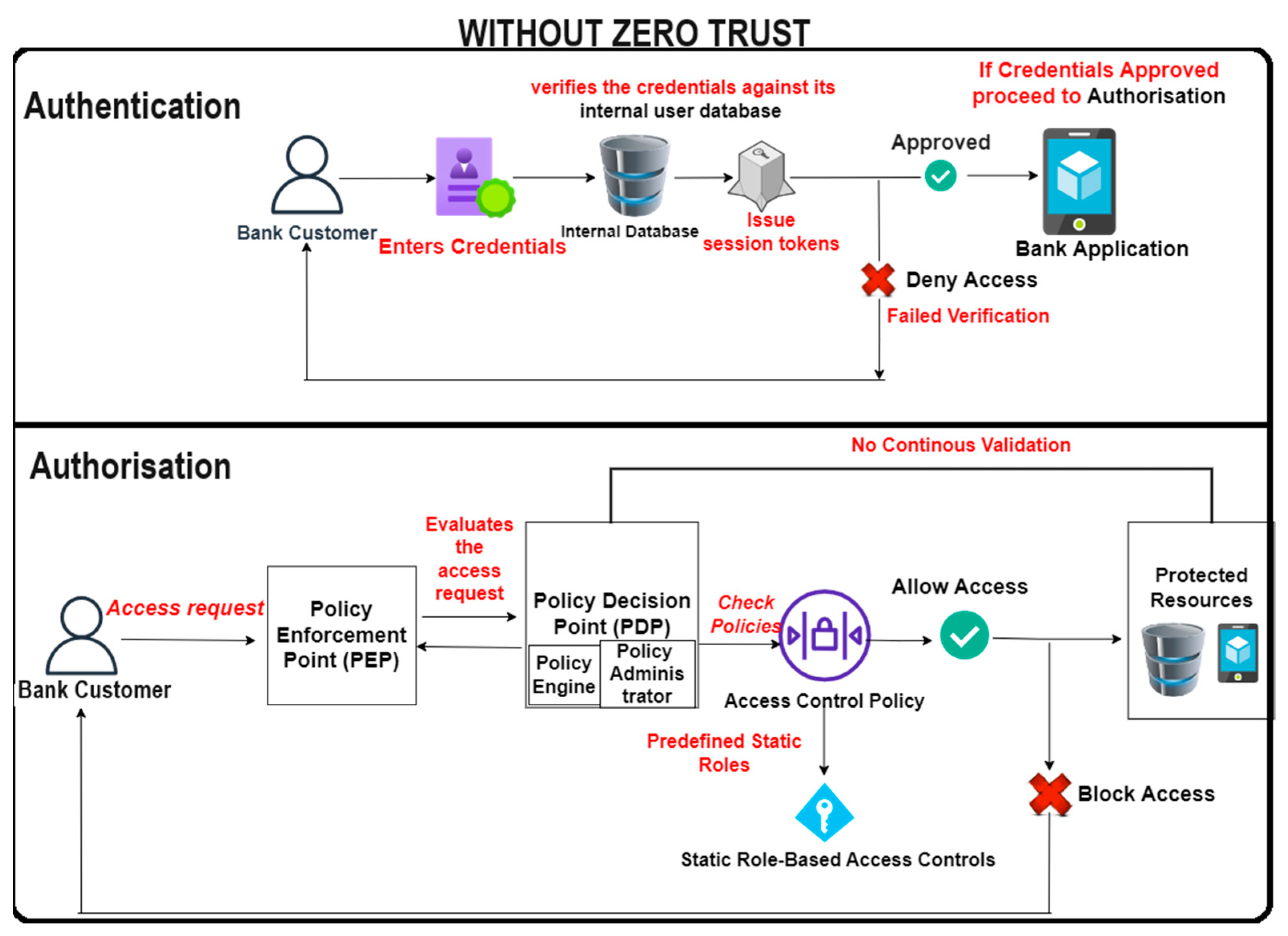

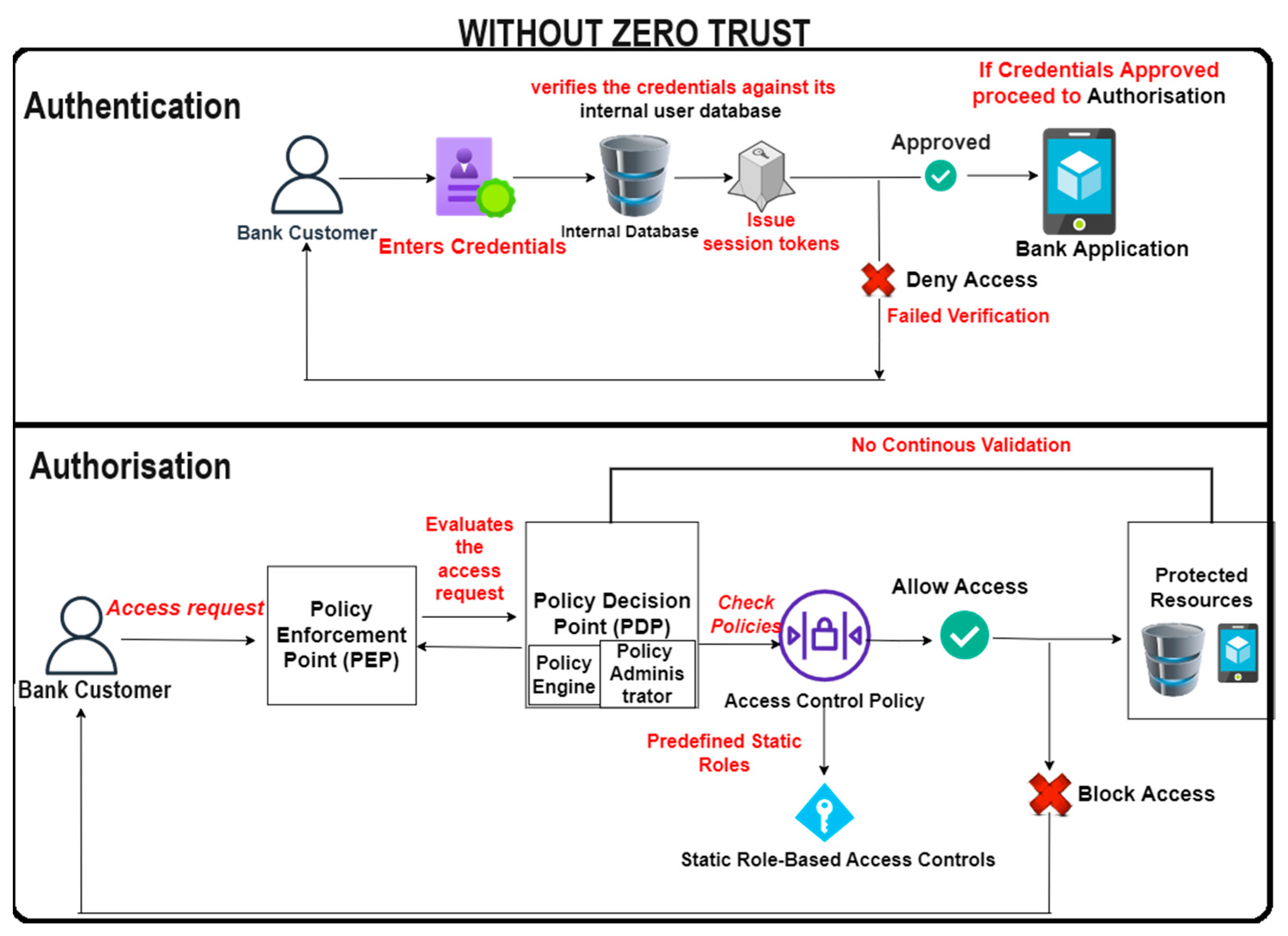

Prior to the adoption of Zero Trust principles, the IAM framework was founded on traditional security models that emphasise perimeter defence. The process begins with the authentication phase, where bank customers enter their credentials to be verified against the internal user database. If the credentials are confirmed as valid, the system issues session tokens, thereby granting access to the bank application. Should the verification fail, access is consequently denied.

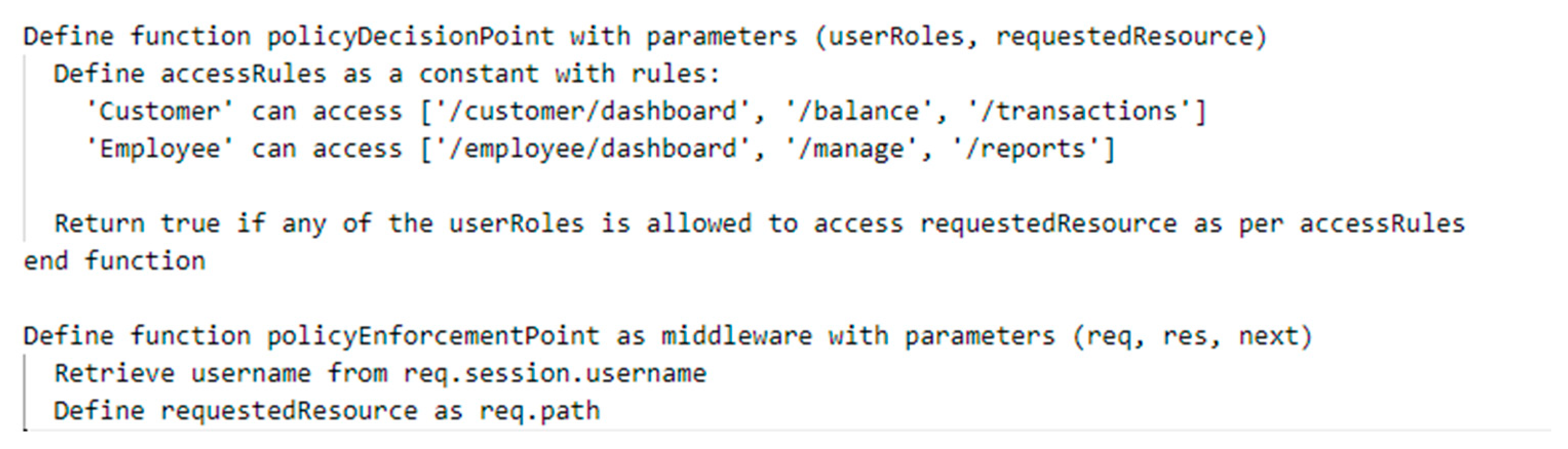

Following authentication, the authorisation phase commences. The policy enforcement point (PEP) handles the customer’s access request and sends it to the policy decision point (PDP). The PDP evaluates the request against a set of predefined roles and access control policies managed by the policy administrator. If the request complies with the access control policy, the customer is granted access to protected resources. However, if the request is non-compliant, the customer is denied access to these resources.

This IAM framework operates under the assumption that the network’s interior is secure once access is granted, demonstrating a notable lack of continuous validation, as shown in

Figure 11. It relies on static Role-Based Access Controls (RBAC), where user roles are fixed and do not dynamically adapt to evolving contexts or security threats. Therefore, it may not be equipped to handle the current digital landscape, highlighting the need for an adaptive approach, such as Zero Trust frameworks.

3.2. Device and Network Security

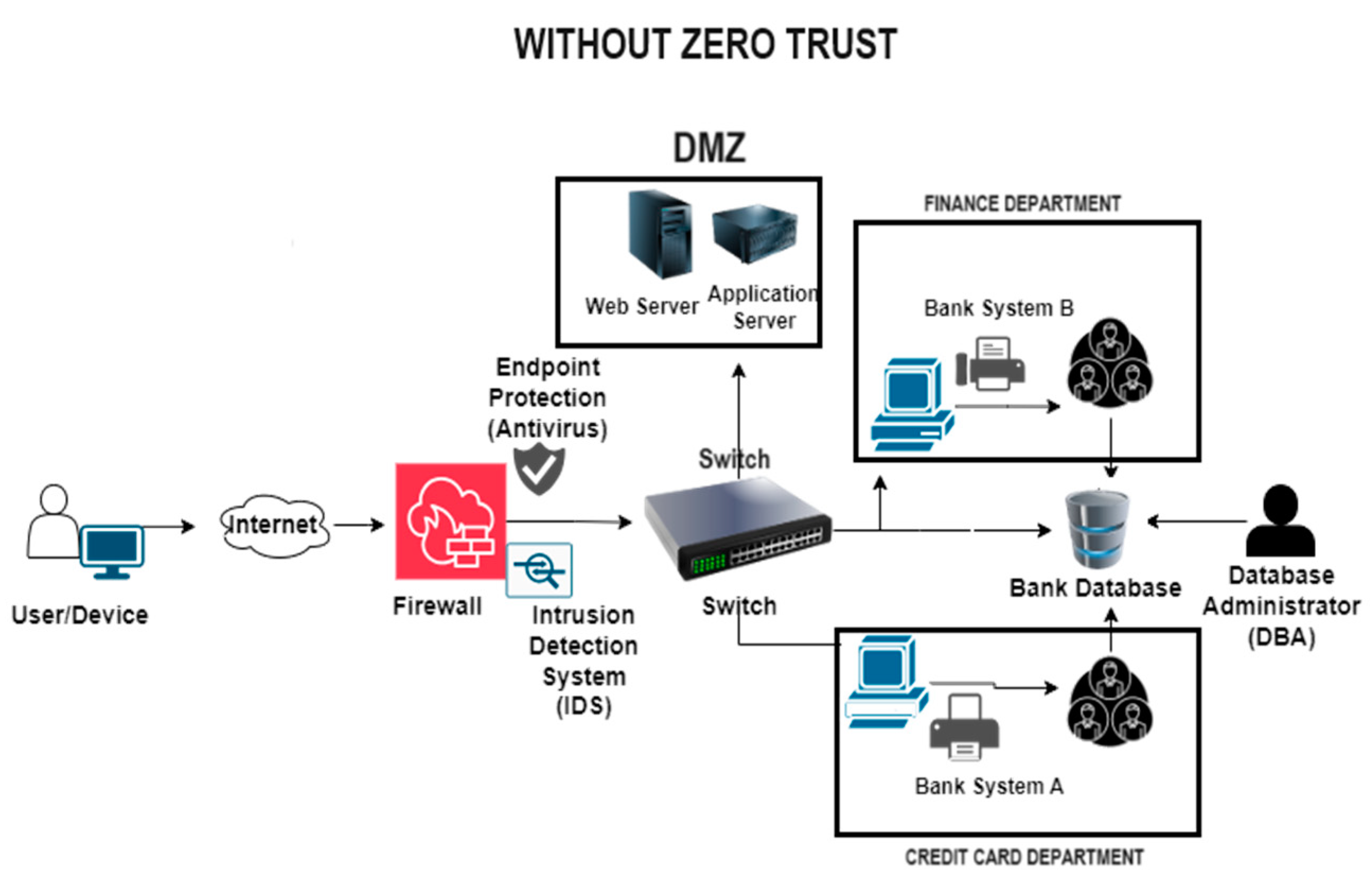

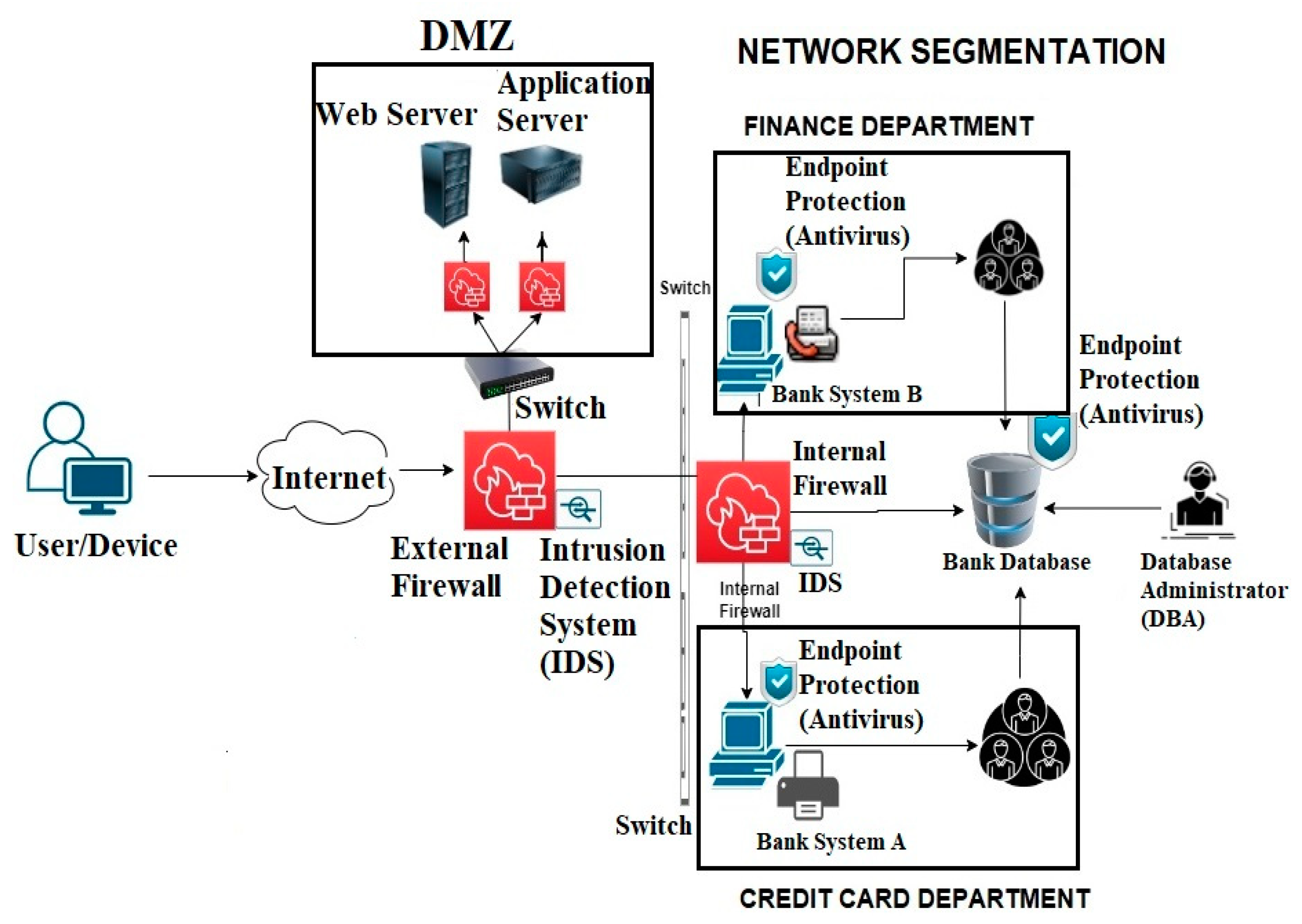

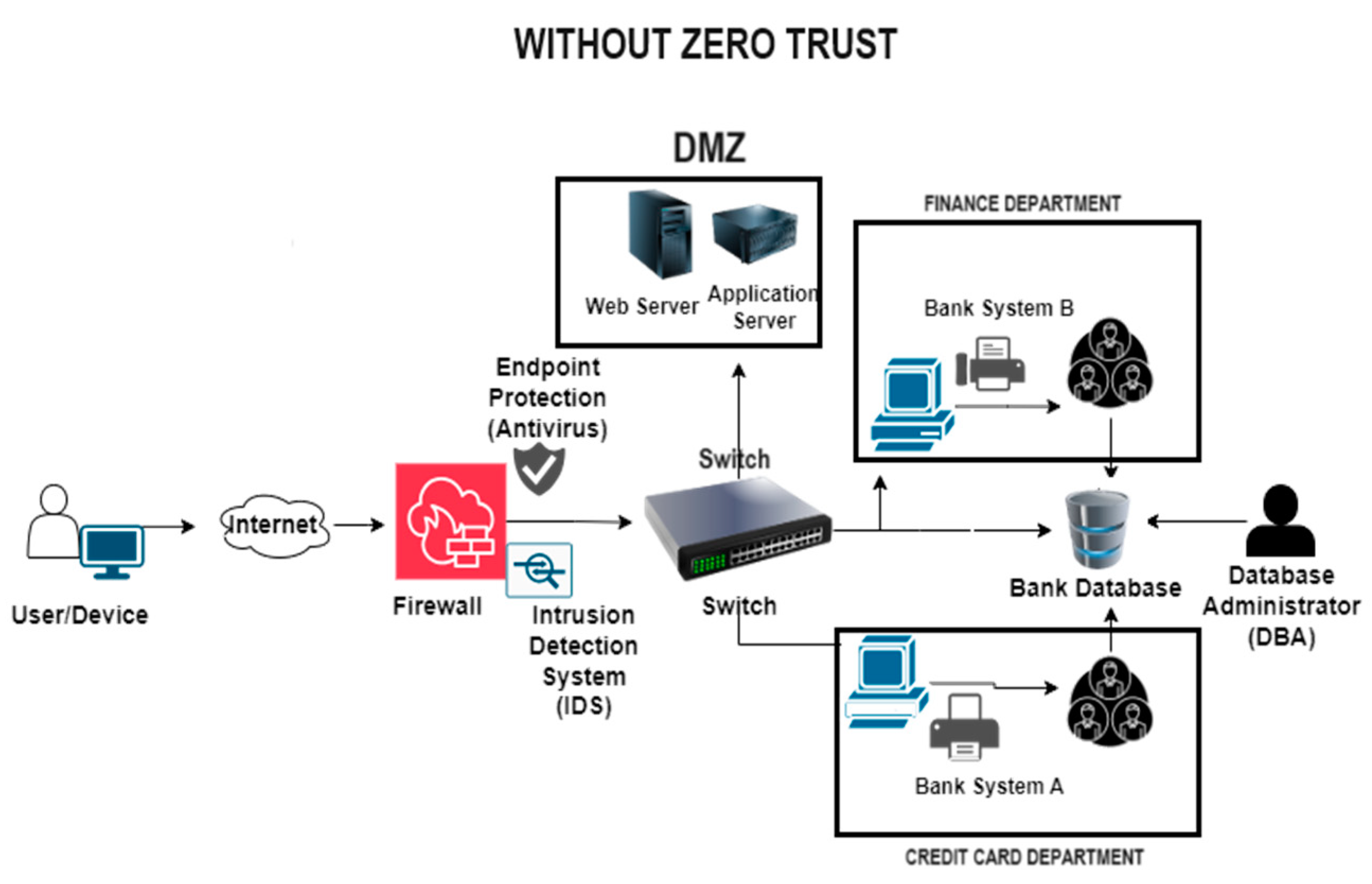

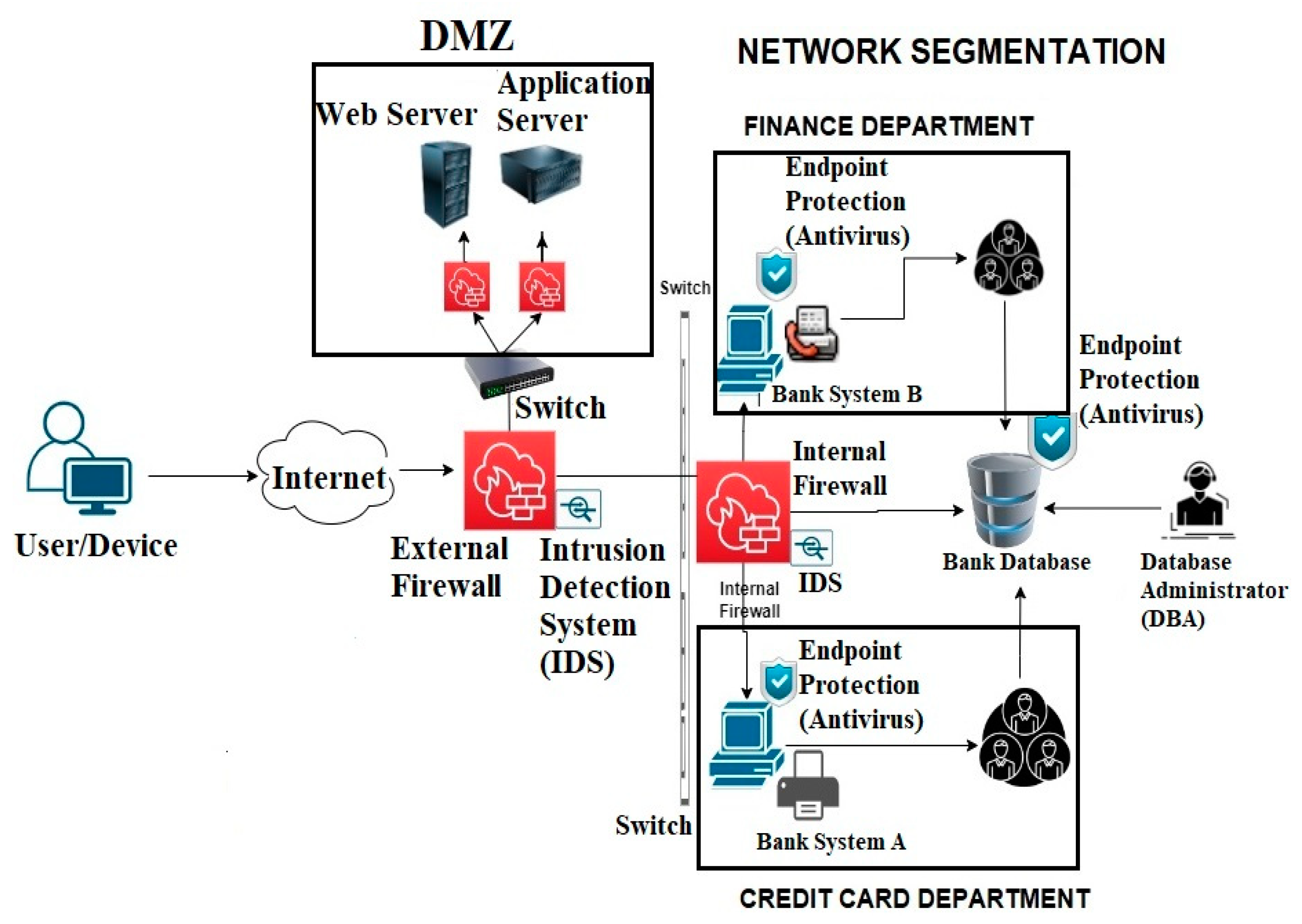

The device and network security framework prior to the implementation of Zero Trust principles relied on a perimeter-based defence strategy, as shown in

Figure 12. This model is characterised by its emphasis on securing the boundaries of the network rather than focusing on the security within the network itself. In the traditional setup, the DMZ serves as a buffer zone between the untrusted public internet and the internal network. It hosts public-facing servers such as the Web server and the Application server, which are exposed to internet traffic but isolated from the internal network to mitigate risk. Perimeter defences, such as firewalls, are deployed to scrutinise incoming and outgoing traffic. The firewalls operate based on predefined security rules to block or allow data packets, acting as the first line of defence against external threats. Endpoint protection (antivirus) software is also used on devices to protect against malware and other cybersecurity threats.

The IDS complements the firewall by monitoring network traffic for suspicious patterns that may indicate a security breach. It serves as a watchdog, alerting administrators to potential intrusions. The network is segmented according to departmental functions, such as the Finance and Credit Card departments, each with its own bank systems and databases, but it does not have its own end-point protections, internal firewalls, or IDS to monitor for unauthorised data transmissions or infiltration attempts and also to prevent cross-segment breaches.

Databases, which store sensitive financial information, are secured and managed by database administrators (DBAs). The DBAs are responsible for maintaining the integrity and confidentiality of the data stored within these databases. In this pre-Zero Trust device and network security framework, trust is implicitly granted to users and devices within the network perimeter, which has been identified as a vulnerability. The assumption that the internal network is secure once access is granted through the perimeter defences does not account for the lateral movement of threats that bypass the initial barriers.

The outlined framework serves as a foundation upon which the more dynamic and granular Zero Trust approach is built. The Zero Trust model assumes that threats may exist both outside and inside the network perimeter, leading to a more thorough and continuous verification process for devices and users, regardless of their location relative to the network infrastructure.

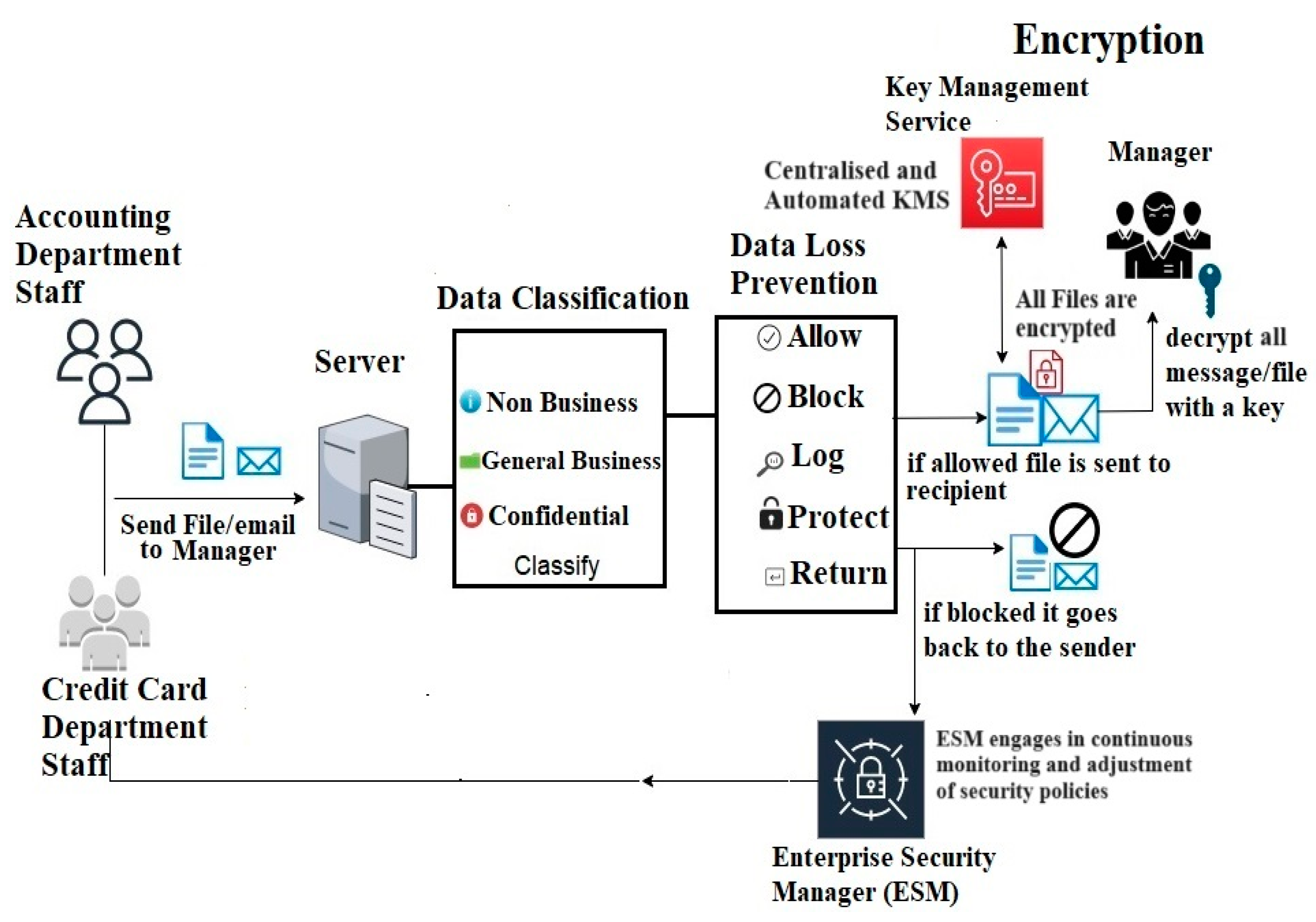

3.3. Data Protection

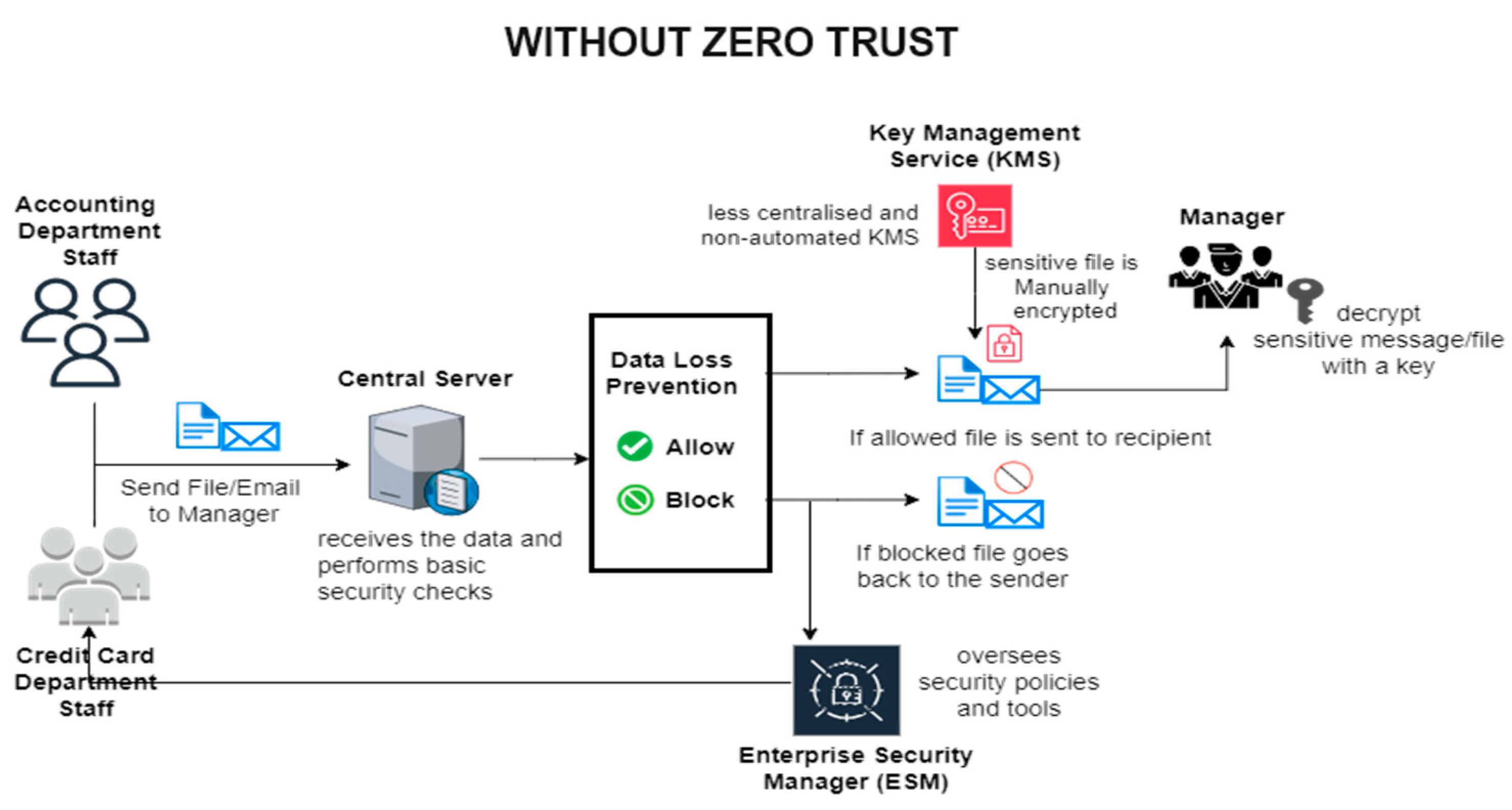

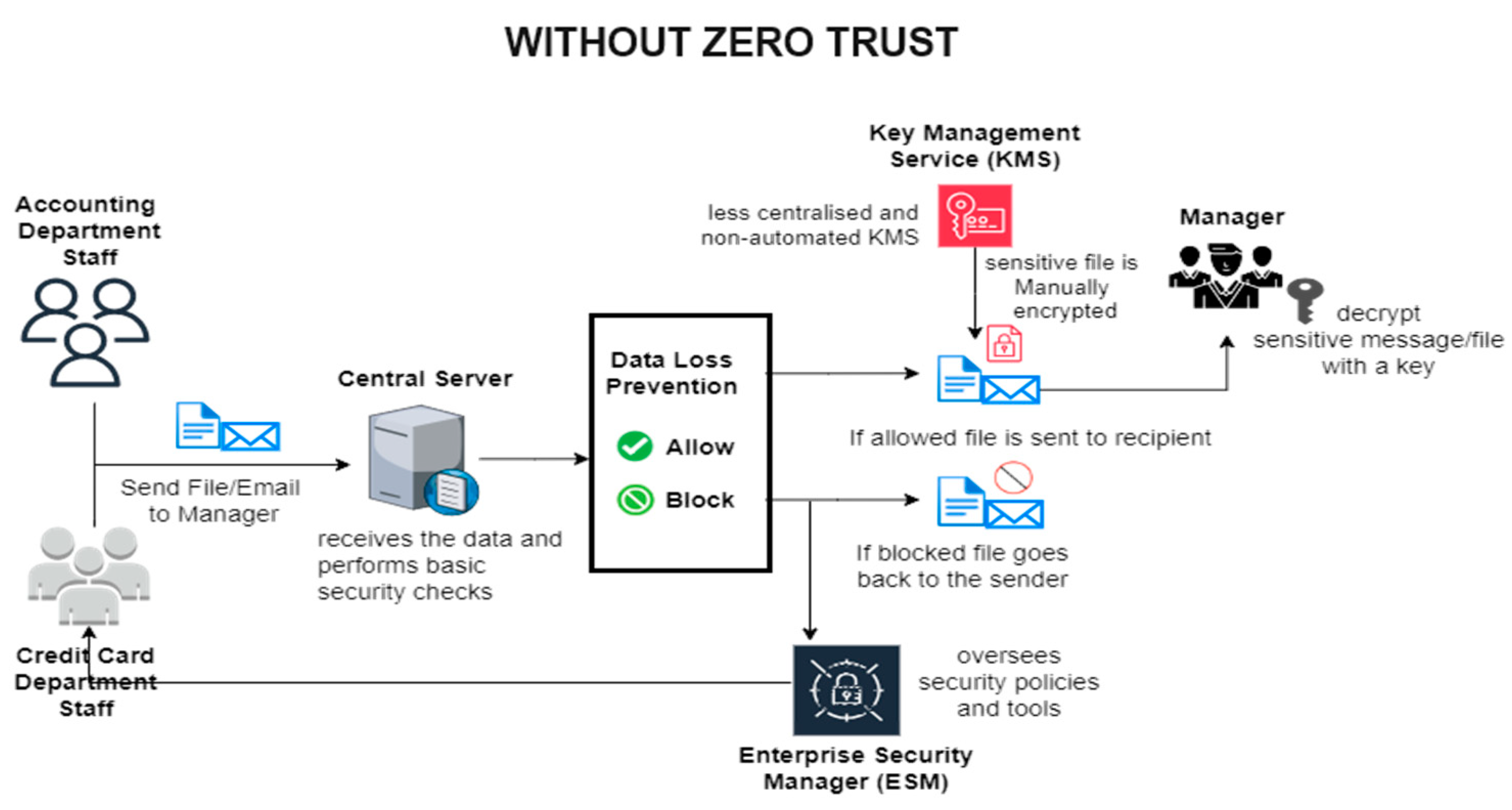

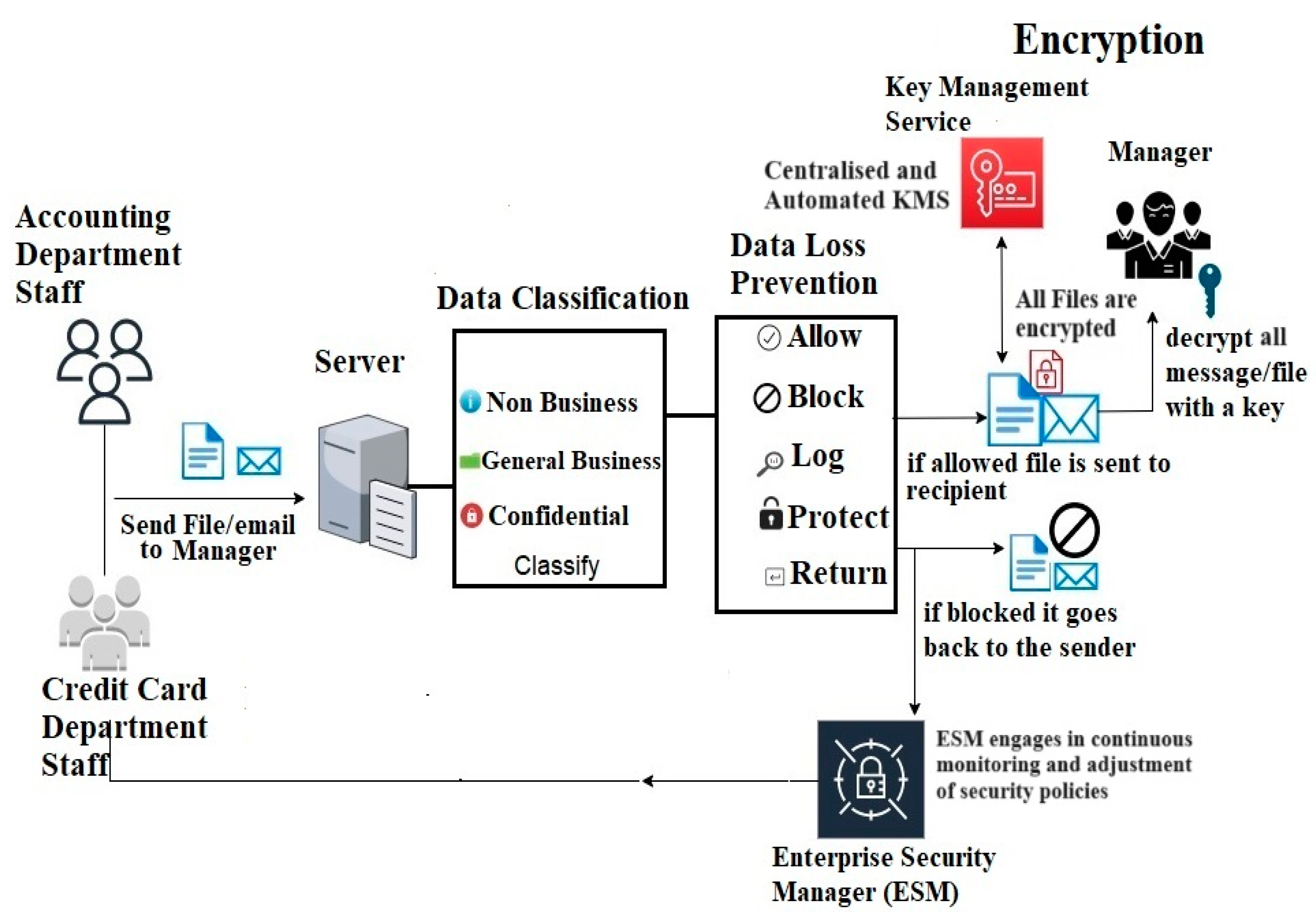

The data protection strategy in place prior to the adoption of Zero Trust principles was built on a foundation of perimeter defence and static security measures. The key components of this strategy involved less centralised key management and a basic level of data loss prevention (DLP). Staff from various departments, such as Accounting and Credit Card, would initiate data transactions by sending files or emails to their managers. This process was not governed by real-time security checks or dynamic policy enforcement. The central server played a vital role in receiving data and conducting basic security checks. However, these checks were relatively simple and not designed to adapt to the constantly evolving threat landscape.

The pre-Zero Trust approach utilised a DLP system to monitor and control data transfer based on static rules.

Figure 13 shows how the system worked, with the ability to log activities for compliance and auditing purposes. The key management service was less centralised and largely manual. Encryption applies to only sensitive files without the aid of automated systems to ensure consistency and reduce human error. Managers were responsible for the decryption of only sensitive files using keys. This manual intervention added a layer of security but also introduced potential delays and inefficiencies in the data handling process. The enterprise security manager (ESM) oversaw the security policies and tools. While providing a level of oversight, the ESM in a pre-Zero Trust framework was not equipped with the tools necessary for continuous monitoring or enforcement of adaptive security policies.

In summary, the pre-Zero Trust data protection model was characterised by its reliance on fixed roles and static security measures. This model lacked the flexibility to respond to sophisticated cyber threats effectively, as it did not incorporate the granular controls or the principle of least privilege inherent in Zero Trust frameworks. The transition to a Zero Trust model was driven by the need for a more resilient and dynamic approach to data protection capable of countering the threats within an ever-changing cyber environment.

4. Proposed Zero Trust Framework

This section presents a Zero Trust framework for financial institutions, encompassing three key areas: identity and access management (IAM) with blockchain, device and network security, and data protection. This proposed framework is designed to address the limitations inherent in traditional cybersecurity models like Bell–LaPadula and Biba, including Castle-and-Moat, Layered Security, and even Defence-in-Depth approaches, which are commonly employed in the finance industry.

4.1. Security Assumptions

In implementing this framework, several security assumptions are made:

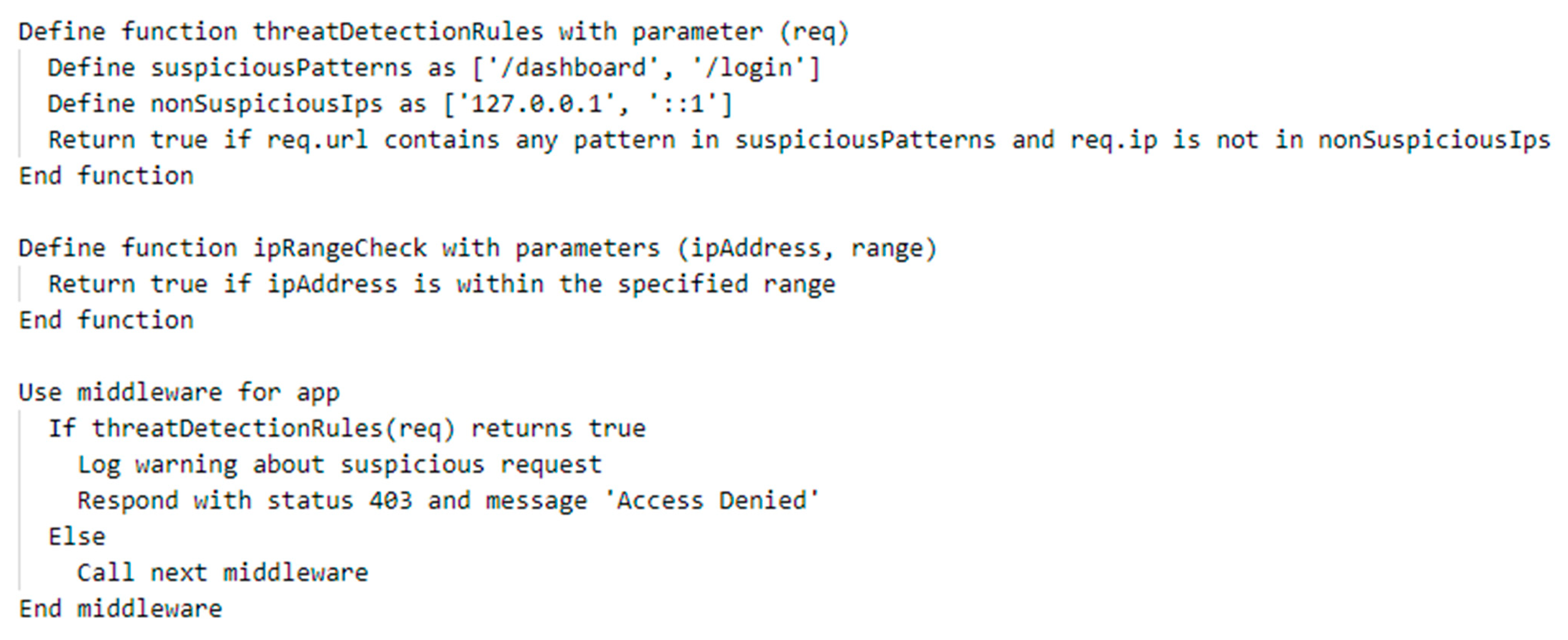

Continuous Verification: It is assumed that continuous verification of all users and devices within the network can significantly mitigate the risk of internal and external threats associated with unauthorised access, such as phishing attacks. This assumption underlies the application of the Zero Trust model;

Immutable Record with Ethereum: The framework utilises Ethereum blockchain technology to establish a secure, immutable record for IAM processes. This enhancement is predicated on Ethereum’s capability to enforce the integrity of user authentication and authorisation, thereby fortifying the trust layer essential to the Zero Trust model;

Comprehensive Threat Detection: The framework assumes that the integration of various security components like IDS, firewalls, and DLP tools will effectively detect and mitigate a wide range of cyber threats, including XSS and CSRF attacks;

Adaptive Security Posture: The framework is based on the assumption that an adaptive security posture, responsive to evolving threats such as brute-force and MiTM attacks, is critical in the dynamic landscape of financial cybersecurity;

Data Integrity and Confidentiality: The assumption is that through data classification and encryption, the integrity and confidentiality of sensitive data can be maintained effectively, reducing the risk of data breaches and unauthorised access.

4.2. Threat Model

Following the security assumptions, our proposed framework addresses multiple threats that could compromise various components of financial institutions’ cybersecurity landscapes. Each threat is analysed for its potential impact.

Man-in-the-Middle Attack: It could compromise the integrity of data in transit between users and services, particularly affecting the network security component;

Phishing Attack: It directly targets user authentication processes, jeopardising the IAM component by attempting to steal credentials;

SQL Injection: It threatens the data protection component by potentially allowing unauthorised access to or manipulation of the database;

Cross-Site Scripting (XSS): It endangers client-side data and can lead to unauthorised actions, impacting the data protection and network security modules;

Cross-Site Request Forgery (CSRF): It could manipulate authenticated sessions, affecting transaction processing within IAM;

Brute-force Attack: It targets the robustness of user authentication, putting the IAM system at risk;

Insider Threat: It puts at risk all components by potentially bypassing internal security measures due to authorised access.

Our framework includes specific security measures to address each threat, ensuring complete protection across IAM, data protection, and network security.

4.3. Security Implementation/Mitigation Strategies

After identifying potential threats to financial institutions’ cybersecurity, our proposed framework implements a robust set of security measures tailored to safeguard critical components and ensure data integrity and confidentiality.

IAM: We integrate strict access control mechanisms, including role-based access controls and dynamic permissions, to mitigate the risk of unauthorised access and insider threats. Using blockchain technology, which offers an unchangeable and verifiable record of user activity and access patterns, authentication processes are enhanced;

Device and Network Security: To protect against external breaches and internal vulnerabilities, our framework employs advanced encryption standards, intrusion detection systems, and continuous network monitoring. These measures are designed to detect and prevent man-in-the-middle and brute-force attacks, ensuring secure communication channels and device integrity;

Data Protection: Sensitive data are protected through end-to-end encryption, both at rest and in transit. SQL injection and XSS threats are mitigated by implementing stringent input validation, parameterised queries, and content security policies. Additionally, regular security audits are conducted to identify and rectify potential vulnerabilities, ensuring the resilience of data protection measures;

Adaptive Threat Response: The framework is engineered to adapt dynamically to emerging threats. By continuously analysing threat intelligence, the system can apply real-time updates to security configurations, ensuring a state of preparedness against evolving cyber threats.

When a threat is detected, our framework engages a predefined mitigation strategy based on a set of criteria that include the type of threat, its severity, the system’s current state, and the potential impact on operations. This decision-making process involves an automated evaluation using threat intelligence and real-time system monitoring to determine the most effective response. For example, if the system saw an attempt to get in without permission, it would tighten access controls and start an immediate audit trail review through the blockchain’s immutable records. This would effectively find and stop the threat vector. This protocol ensures a rapid and precise security response, minimising risk exposure and system vulnerability.

Each of these strategies is systematically illustrated in

Figure 14,

Figure 15 and

Figure 16, which depict the Zero Trust mechanisms across IAM, data protection, and network security, demonstrating the practical application of our security measures.

4.4. Identity and Access Management with Blockchain

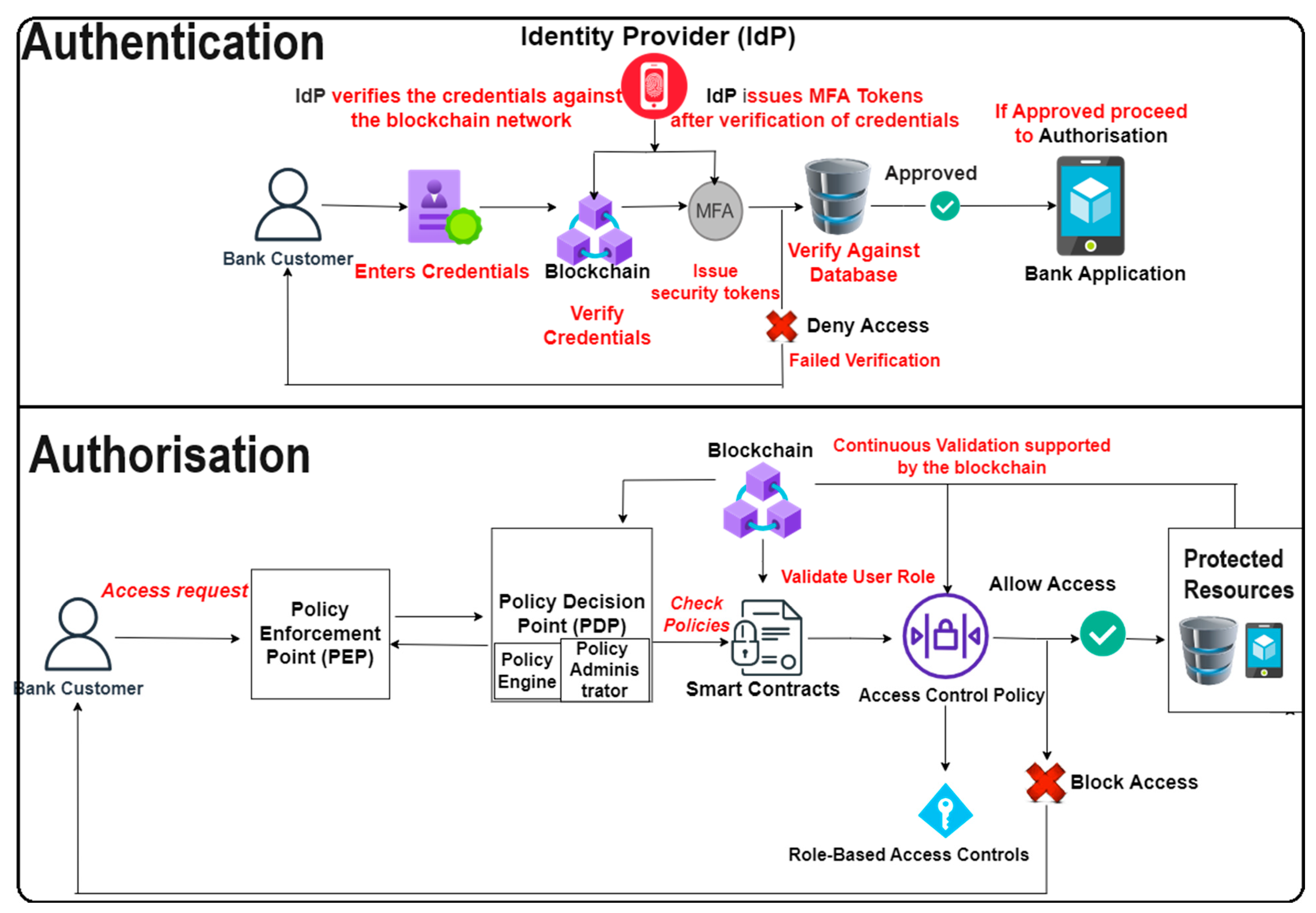

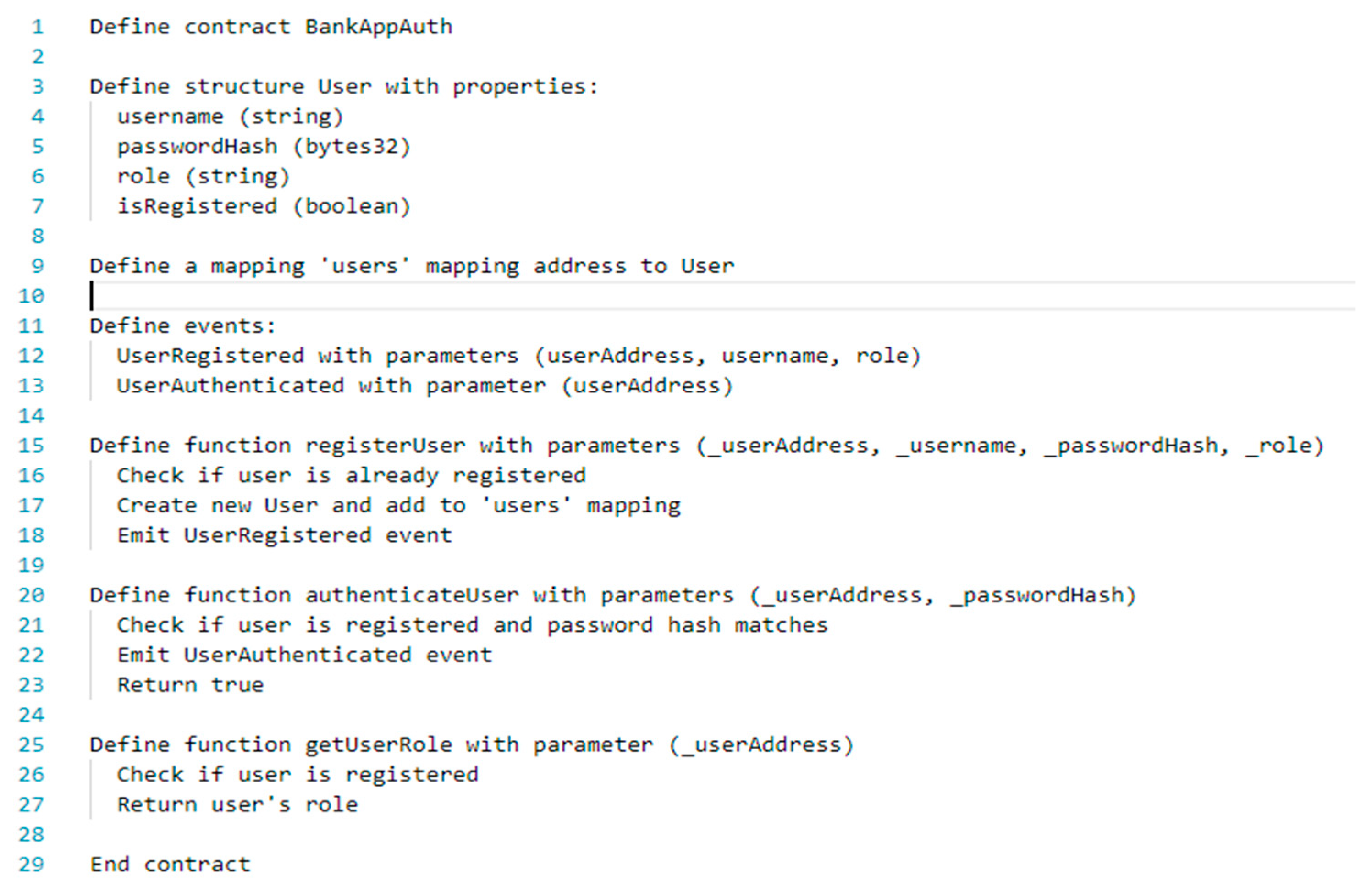

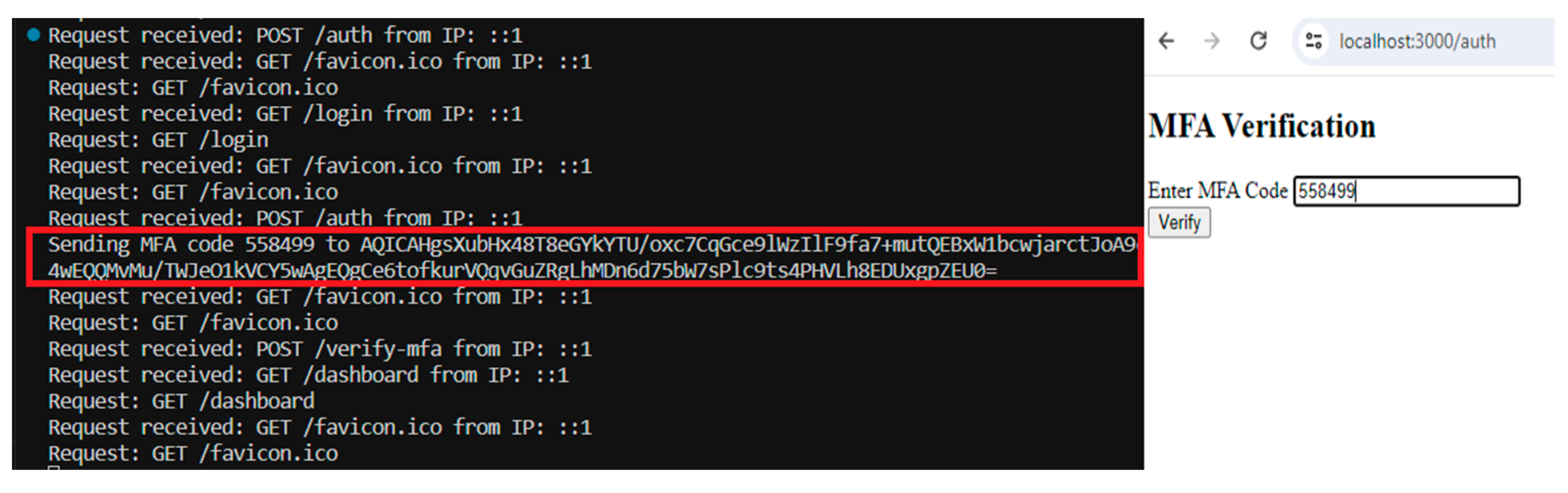

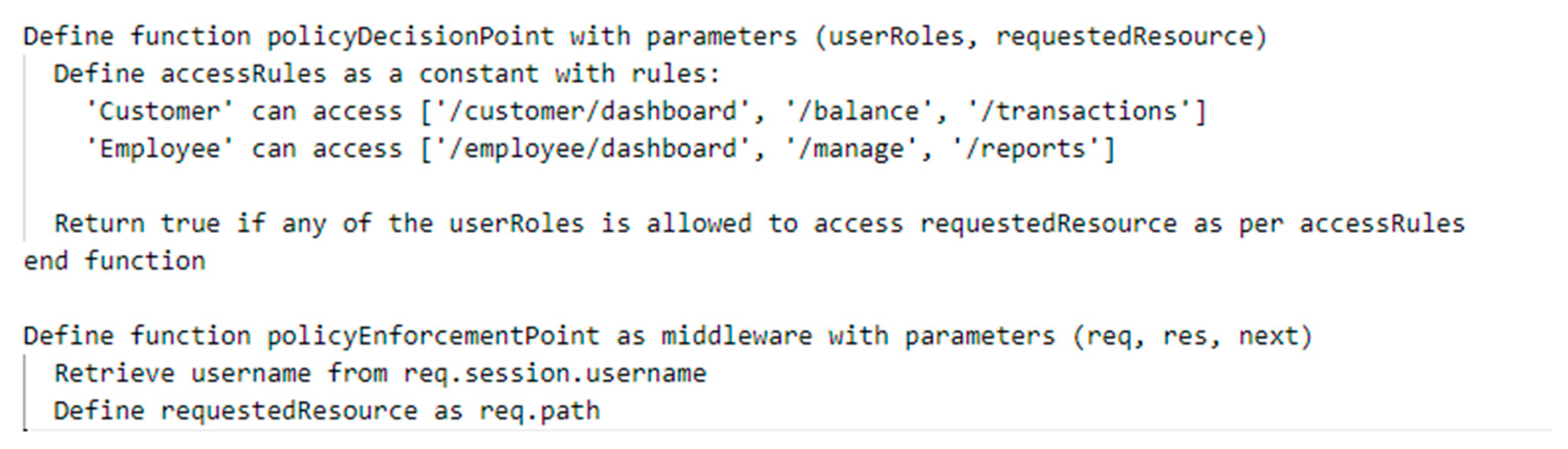

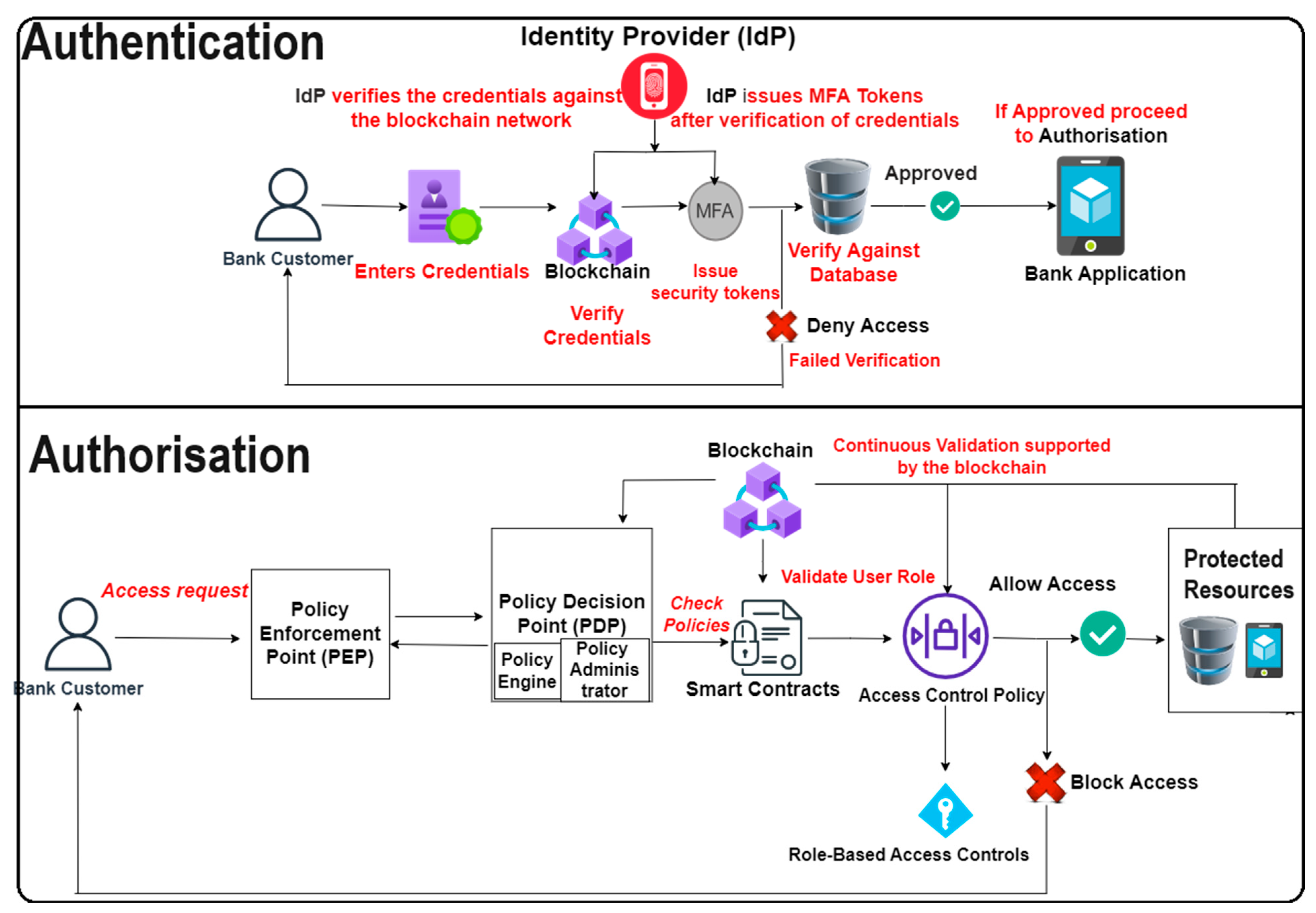

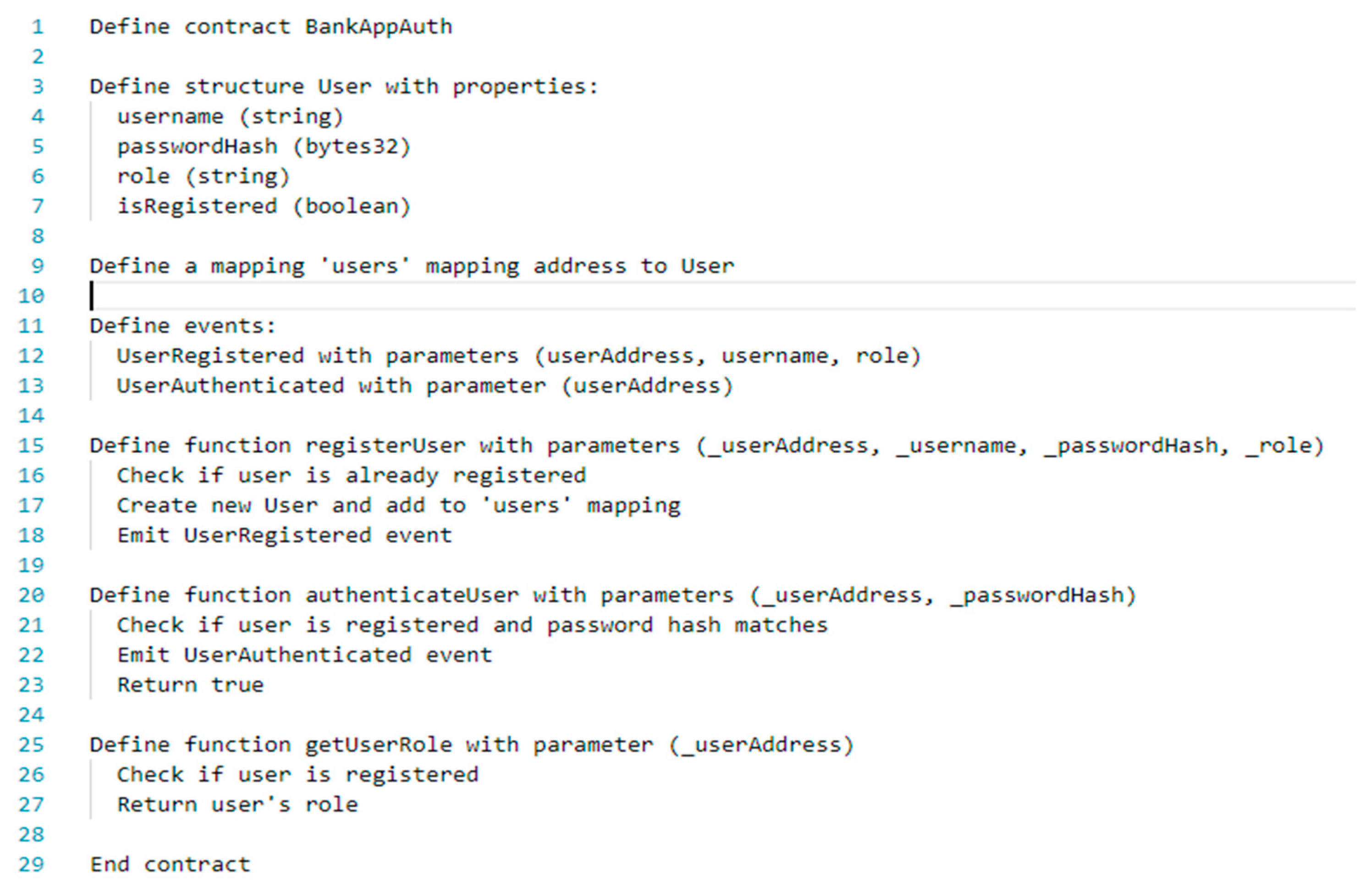

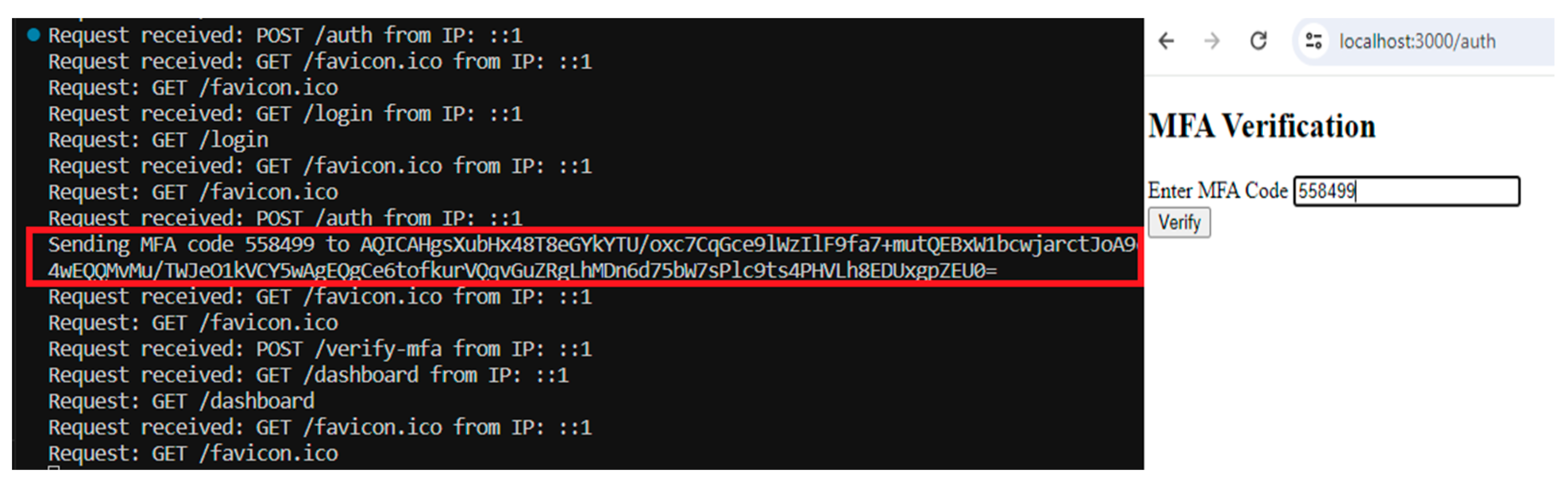

The IAM component is crucial in ensuring that only authorised users are granted access to an organisation’s resources, particularly in financial institutions where sensitive data and transactions are involved. It is important to implement robust authentication and authorisation mechanisms such as Multi-factor authentication (MFA), Role-Based Access Controls (RBACs), and access control policies. Integrating blockchain technology as a trust layer is also essential in maintaining security.

Figure 14 illustrates the proposed IAM process, in which users first enter their credentials, which are then verified by the authentication server or identity provider (IdP), potentially using a blockchain to check the validity of the credentials in a secure and tamper-proof manner. Blockchain’s distributed ledger technology ensures that user credentials are not centrally stored, thus mitigating the risk of a single point of failure. Upon successfully verifying the user’s credentials, the IdP issues MFA tokens, which may include blockchain-based security tokens that provide cryptographic proof of the user’s identity.

The MFA phase ensures an added layer of security by requiring proof of identity that is verifiable via blockchain, making the authentication process more resistant to fraud and unauthorised access. After verifying the MFA token, the system moves to the authorisation phase, where the PEP intercepts the user’s request and forwards it to the PDP for evaluation against the defined access control policies. These policies, underpinned by the trust layer, ensure that the rights and credentials exchanged during the process are immutable and verifiable through blockchain records.

The PDP defines access rules for different roles, such as customers and employees, specifying which endpoints these roles can access. For instance, customers may only access their dashboard and transaction history, while employees can manage accounts or generate reports. These policies are encoded as smart contracts within a blockchain platform, ensuring tamper-proof, immutable, and enforceable rules that reflect the organisation’s access control structure. The PEP acts as a middleware that checks if a user’s role, fetched from the session and verified against the blockchain, permits access to the requested resource. If a role does not have access, it denies the request.

RBAC is applied at this stage, granting customers and employees access to the resources and actions they are authorised to perform based on their assigned roles. These roles are recorded on the blockchain, ensuring they cannot be altered without consensus, adding an additional layer of security. Finally, the system provides access to the resources and continuously monitors and audits user activities to ensure compliance with security policies and detect potential threats or anomalies. This constant monitoring makes it possible to find and fix security risks in real-time, which makes the financial institution even safer overall.

In conclusion, integrating a trust layer using blockchain technology into the IAM systems aligns with financial regulations and data protection laws, such as the General Data Protection Regulation (GDPR) for data privacy, the Payment Card Industry Data Security Standard (PCI DSS) for transaction security, and other relevant financial industry standards. By using blockchain, the financial institution ensures that access logs are immutable and traceable, which is paramount for audits and regulatory compliance. Furthermore, the decentralised nature of blockchain addresses the concentration risk, where a central repository of sensitive data might present a lucrative target for cyberattacks.

The IAM system integrated with blockchain technology offers a robust and adaptive solution to the challenges identified in the pre-Zero Trust model IAM shown in

Figure 11, establishing a forward-thinking security stance that aligns with the evolving demands of the financial sector’s cybersecurity needs.

4.5. Device and Network Security

Device and network security are integral to the Zero Trust model, designed to protect against internal and external threats. This is achieved by incorporating various security components such as firewalls, IDS, DMZ, and network segmentation.

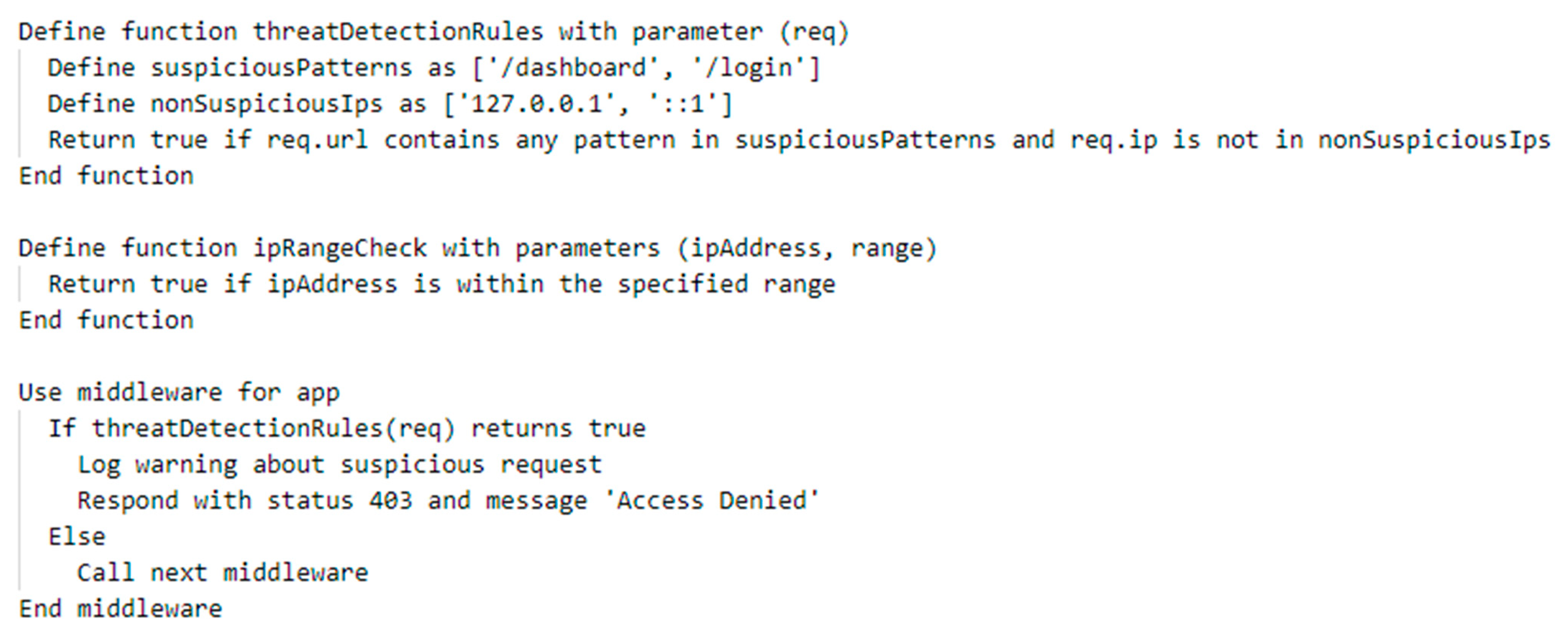

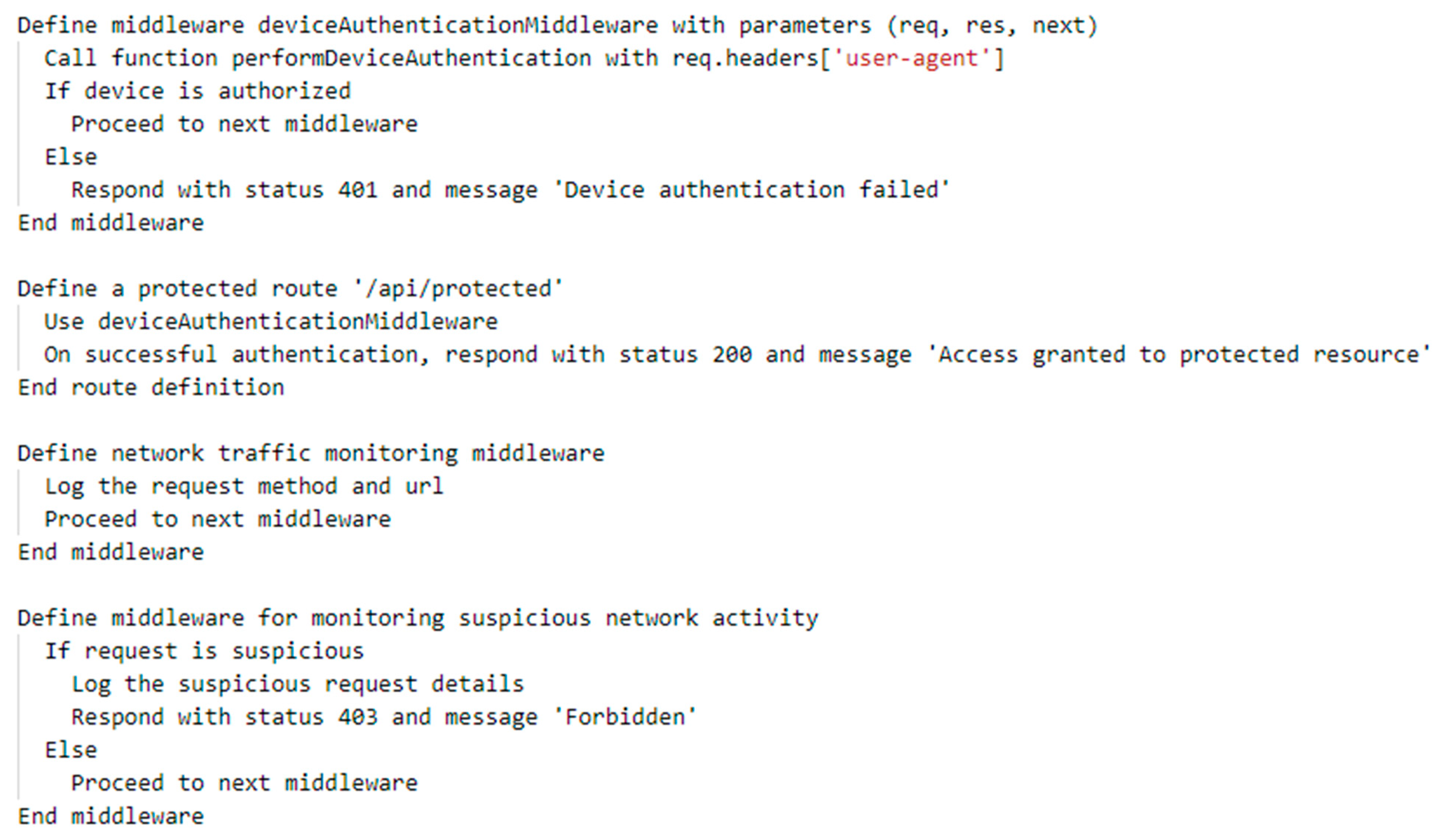

Financial institutions are highly susceptible to security threats due to the sensitive data they manage and the value of their transactions. To mitigate such risks, the implementation of robust security measures is essential. For instance, IDS can detect and stop advanced threats that target organisations.

Figure 15 illustrates the proposed device and network security mechanism, in which all user and device traffic is treated as untrusted and verified before accessing any network resources. The framework begins by implementing an external firewall, which regulates incoming and outgoing traffic to allow legitimate traffic while blocking unauthorised traffic. IDS is also deployed to detect and prevent intrusion attempts into the network, providing a reactive security posture to complement the firewall’s preventative measures.

Network segmentation is implemented by dividing the network into separate segments based on functionality and security requirements. For instance, the finance department would be cordoned off, possessing its own internal firewalls and IDS to monitor for unauthorised data transmissions or infiltration attempts, while the credit card department would have similar but separate defences to prevent cross-segment breaches. Each segment incorporates endpoint protection to defend against malware and other malicious activities. This layer of security operates at the device level, ensuring that all terminals, whether they are workstations or servers within the segment, maintain integrity against compromise.

A DMZ is created to act as a segregated network buffer, containing and controlling access to public-facing services such as web and application servers. Each server is scrutinised and monitored continuously, ensuring that any communication with these servers, whether entering or leaving, is authenticated and authorised in real time. This isolation from the core internal network is critical, as it limits the exposure of sensitive internal resources to external vulnerabilities and attacks.

The database component is crucial for financial institutions, and its security is maintained through endpoint protection and database administration. Endpoint protection ensures database servers are immune to malware, while DBAs manage access controls, monitor database activity, and enforce policies to defend against unauthorised access or data exfiltration. The vulnerability scanning is conducted using automated scanning tools such as Nessus and OpenVAS. These tools scan the network infrastructure to detect and remediate potential security vulnerabilities, thereby enabling timely remediation before exploitation.

The device and network security component of our proposed Zero Trust framework in

Figure 15 represents a strategic shift from the pre-Zero Trust static, perimeter-oriented defences in

Figure 12 to dynamic, context-aware, and adaptive security mechanisms. This ensures that the finance industry’s network infrastructure remains secure and resilient against cyber threats.

4.6. Data Protection

Data protection is critical to the Zero Trust model, particularly for financial institutions that handle sensitive customer data and financial transactions. Implementing effective data protection measures ensures that sensitive information is secure from potential data breaches and unauthorised access. The framework is designed to address vulnerabilities inherent in the pre-Zero trust data protection strategies shown in

Figure 13 by incorporating automated processes and continuous validation.

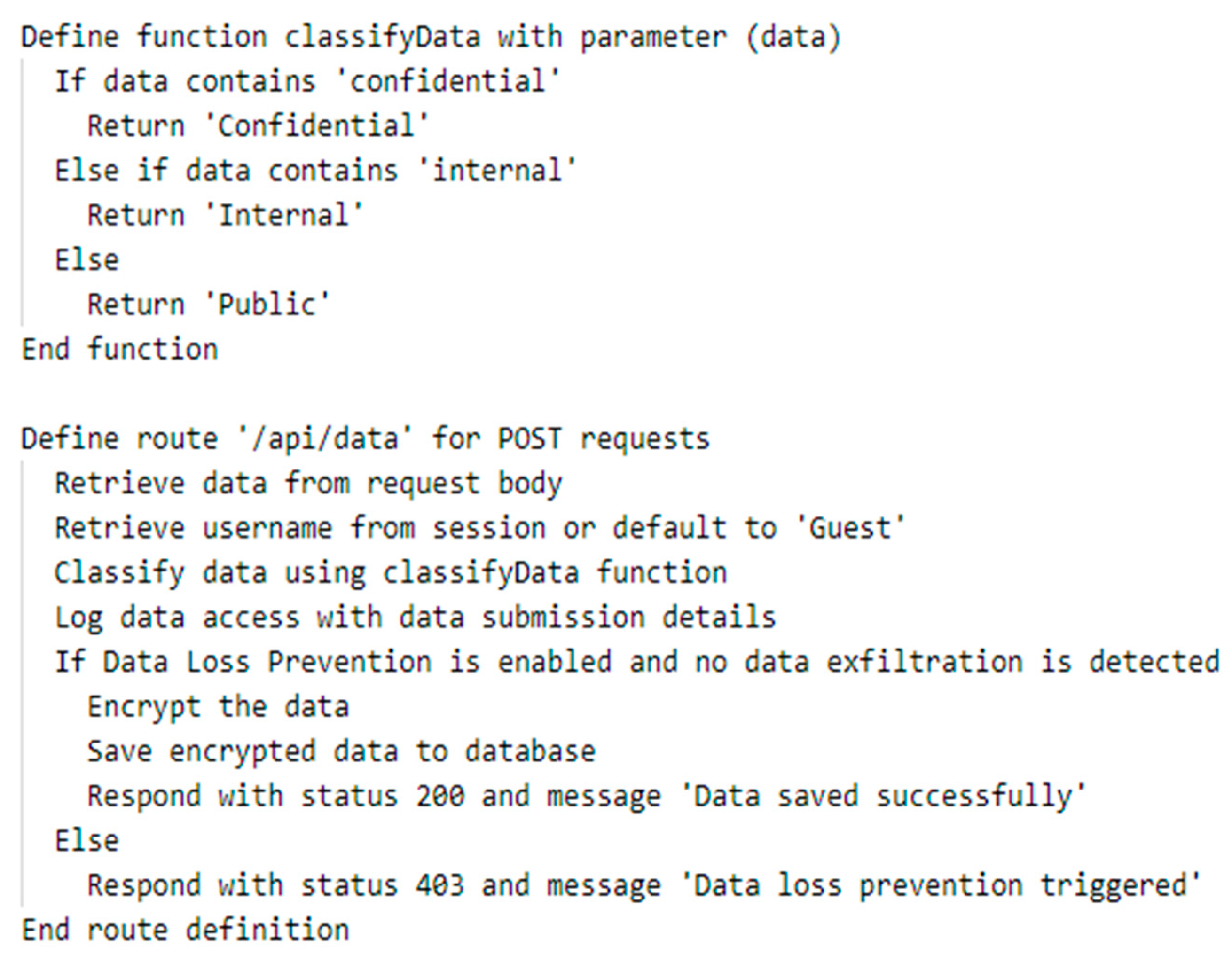

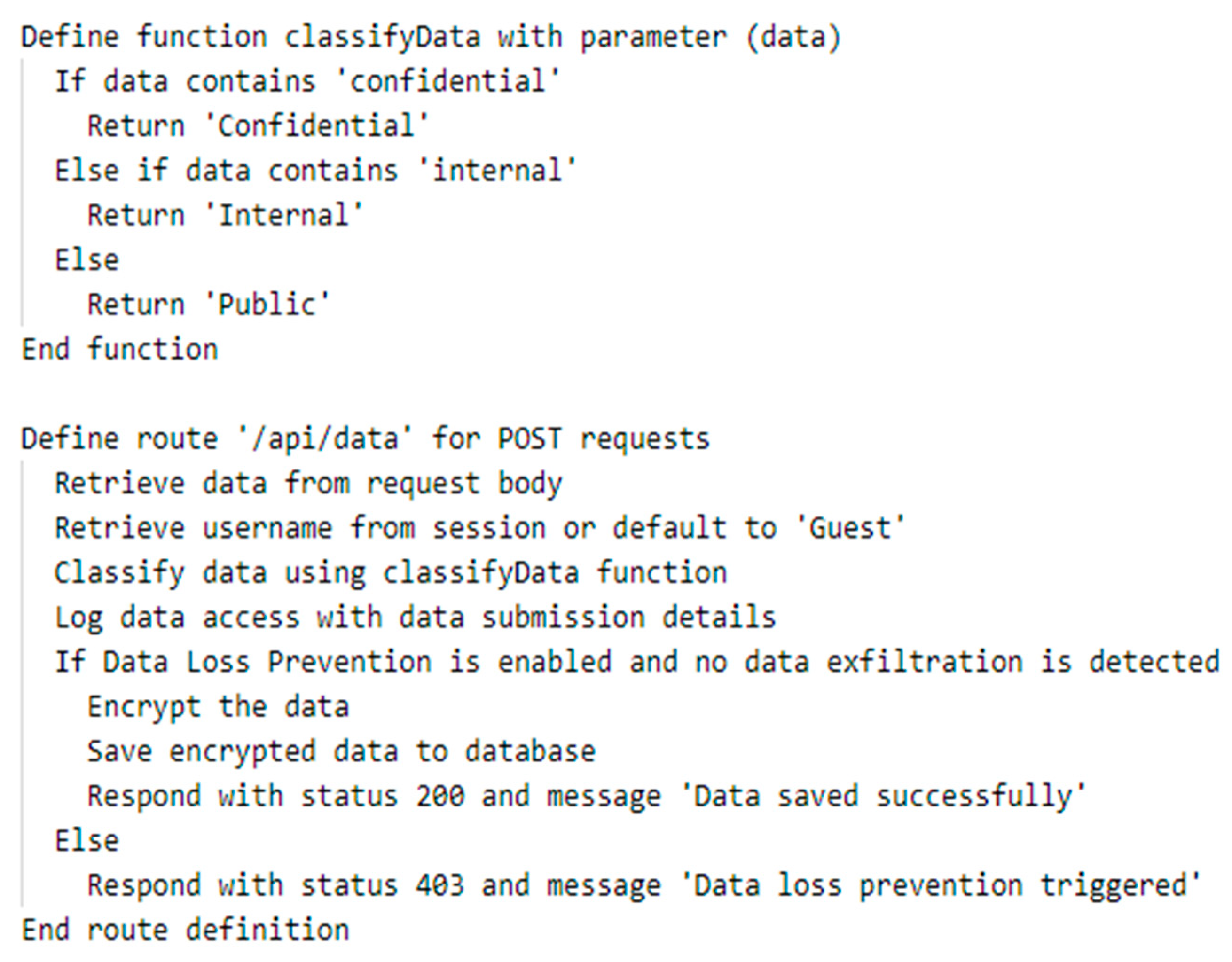

Figure 16 shows the proposed data protection method, which includes data classification, DLP, encryption, and ESM. The first step in data protection is to classify the data based on its sensitivity level. This can range from non-business data to confidential data, requiring the highest protection level. Non-business data, which are less sensitive, might include everyday internal communications. General business data include operational information that might be sensitive but is not critical. Confidential data, which could include customer financial details, require the highest level of security. Data classification helps organisations identify the types of data they hold and prioritise security measures accordingly.

DLP is a set of technologies and policies that help prevent data from leaving an organisation’s network. These tools work by setting rules that can block, log, or allow the transfer of data based on its classification. For example, if an employee tries to send confidential data outside the network, the DLP tool can block the transfer and notify the security team. This not only prevents data breaches but also provides a traceable log for audits and compliance checks.

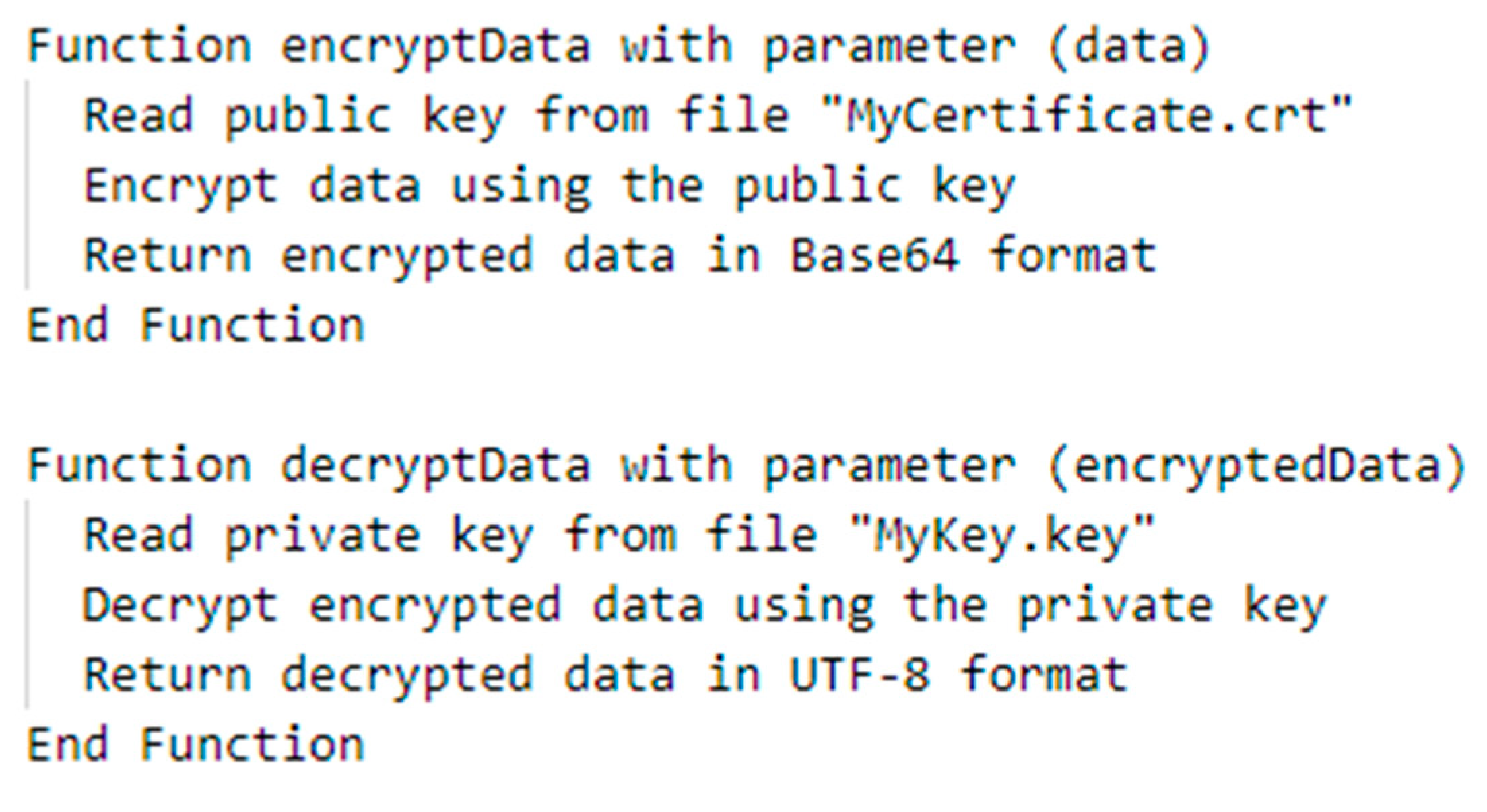

Encryption is another essential data protection technique used to secure data and information. This protects all data at rest, in transit, and in use, ensuring that it remains confidential even if intercepted or accessed by unauthorised parties. Key management services and managers play a crucial role in the encryption process, helping to ensure that encryption keys are generated, stored, and managed securely. The right encryption and key management can make data almost useless to attackers. The encryption–decryption process is streamlined and automated to minimise errors and reduce the administrative burden.

The ESM is a centralised management platform that provides visibility and control over an organisation’s security infrastructure, unlike the static policies of the past. This includes monitoring and managing security events, policies, and configurations; analysing security data; and generating reports. It is like the command centre for data protection, where all the monitoring, management, and analysis happen. The ESM helps financial institutions proactively identify and respond to security threats and vulnerabilities. This ensures that sensitive data remain secure and confidential, reducing the risk of data breaches and ensuring compliance with data protection regulations.

By implementing these data protection measures, the finance industry moves away from the perimeter defence and static security measures in

Figure 13 towards a framework where trust levels are continuously evaluated. No entity within or outside the network is inherently trusted, and verification is a constant process. This approach significantly enhances the security posture, ensuring that data protection measures are resilient, responsive, and capable of defending against sophisticated cyber threats in a proactive manner.

By addressing the security assumptions and integrating the key components effectively, the proposed framework offers a robust approach to implementing the Zero Trust model in financial institutions, ensuring a secure and compliant environment for handling sensitive financial data.

5. Implementation and Evaluation

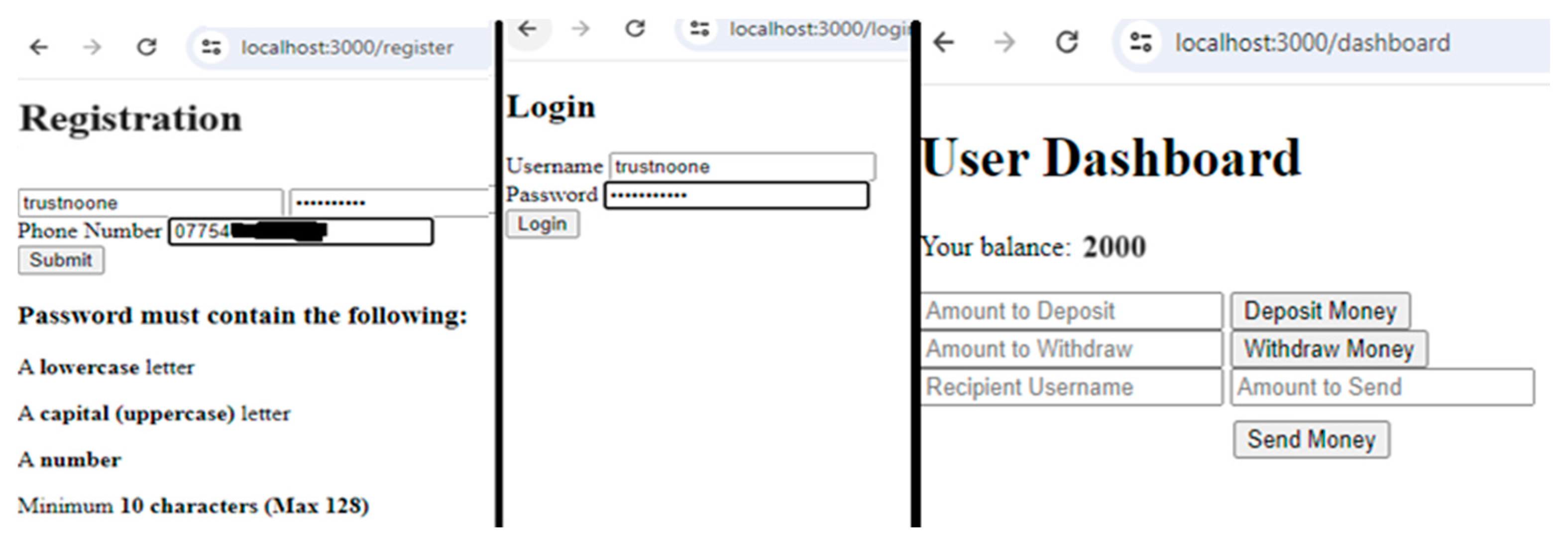

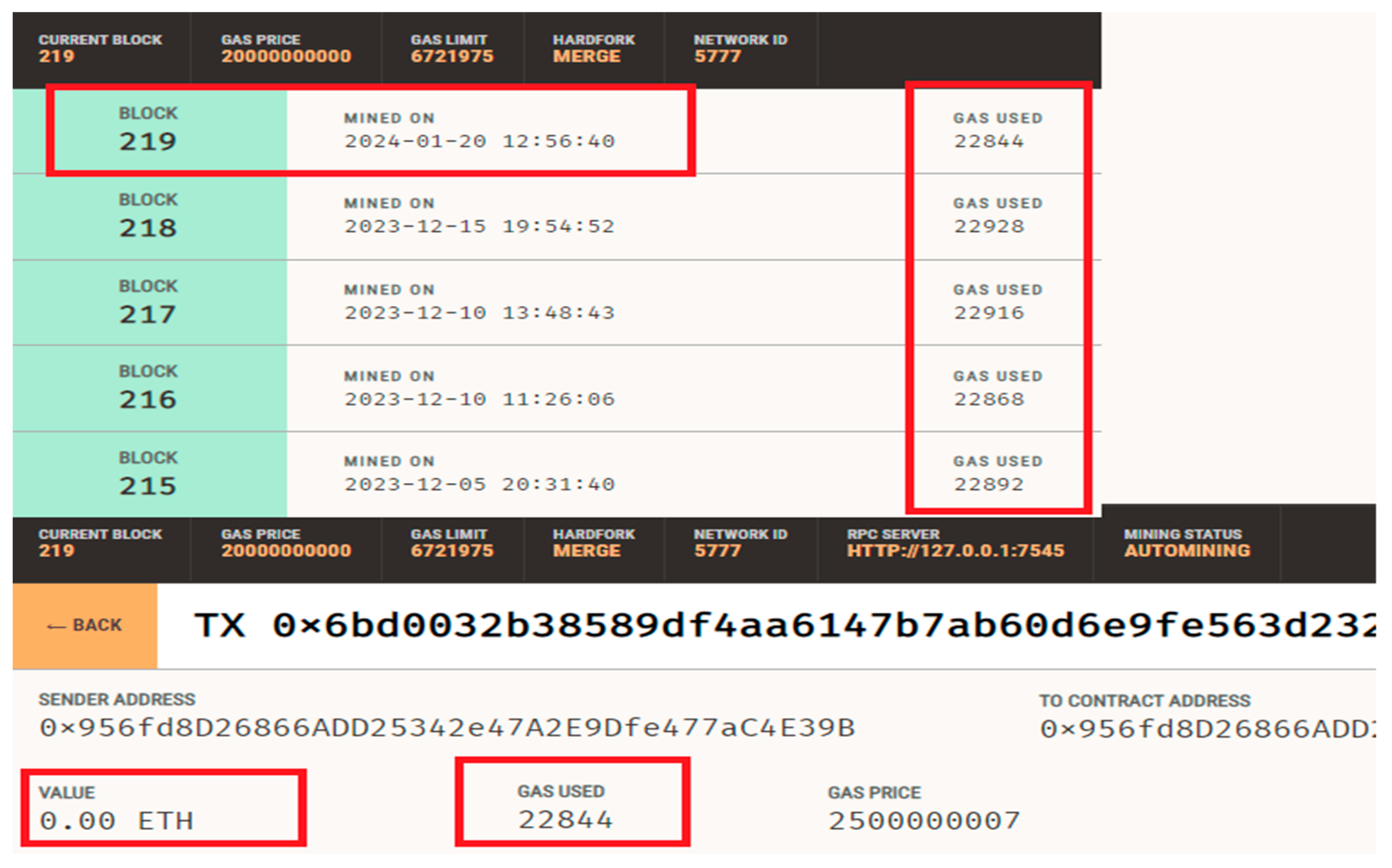

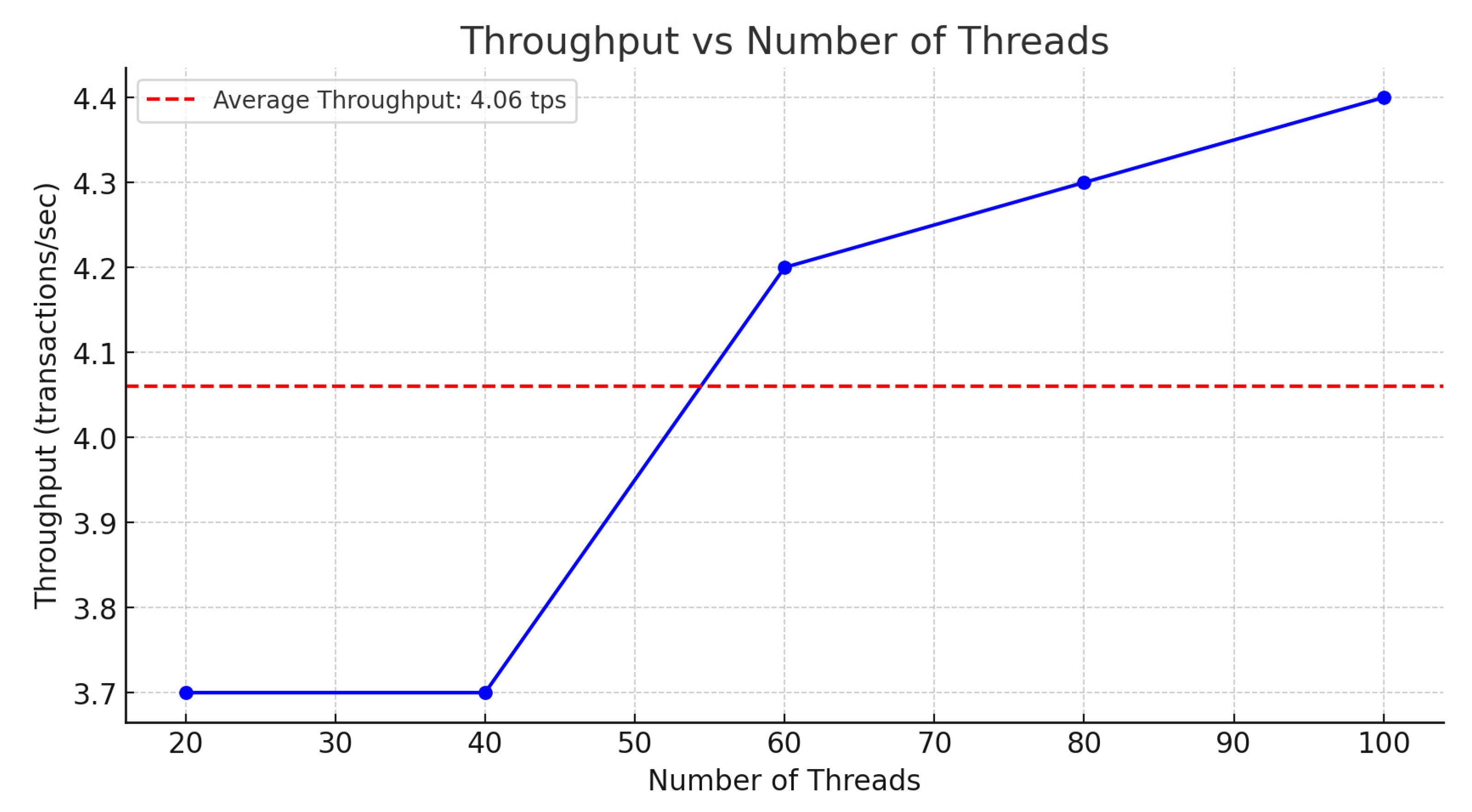

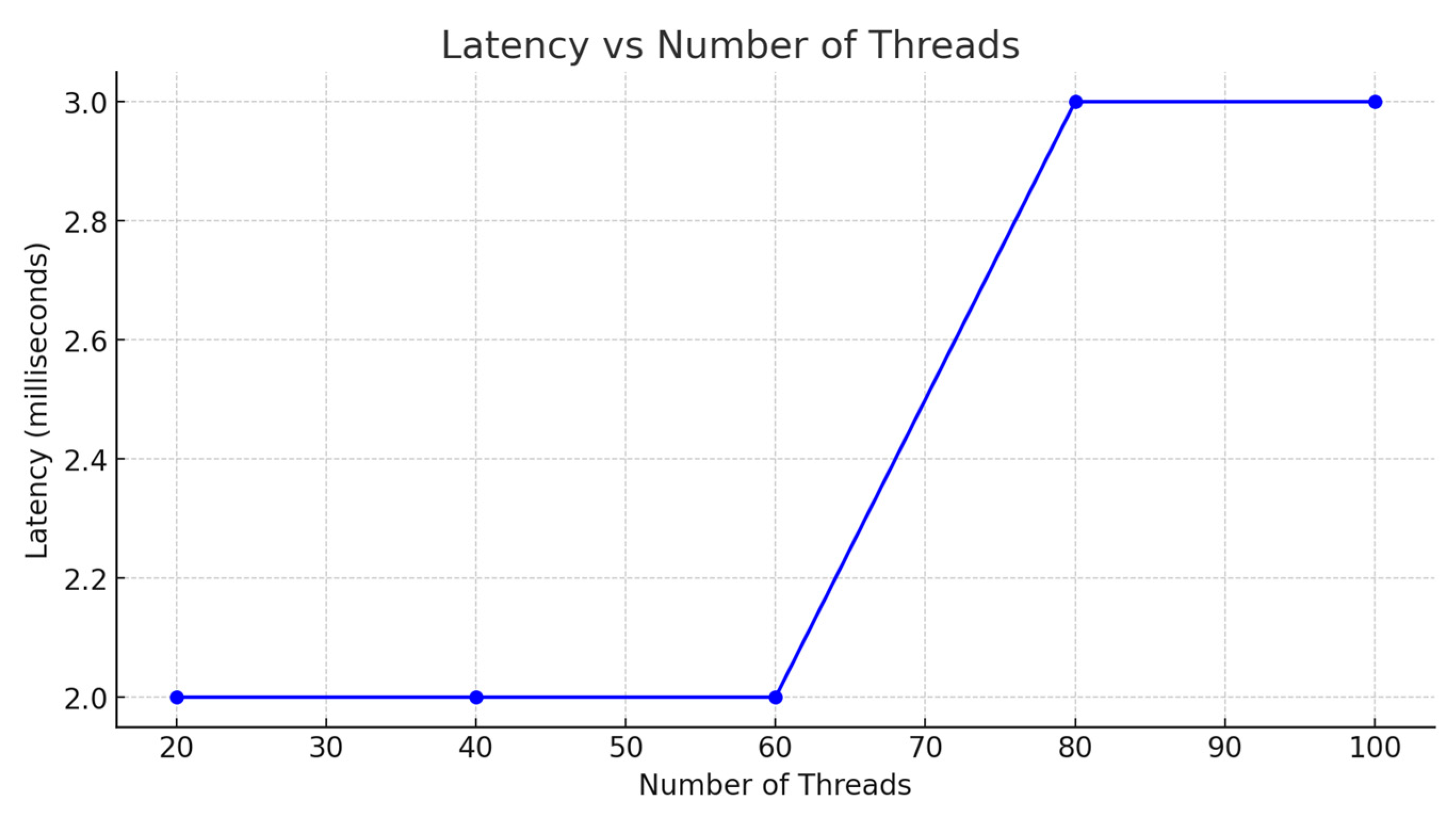

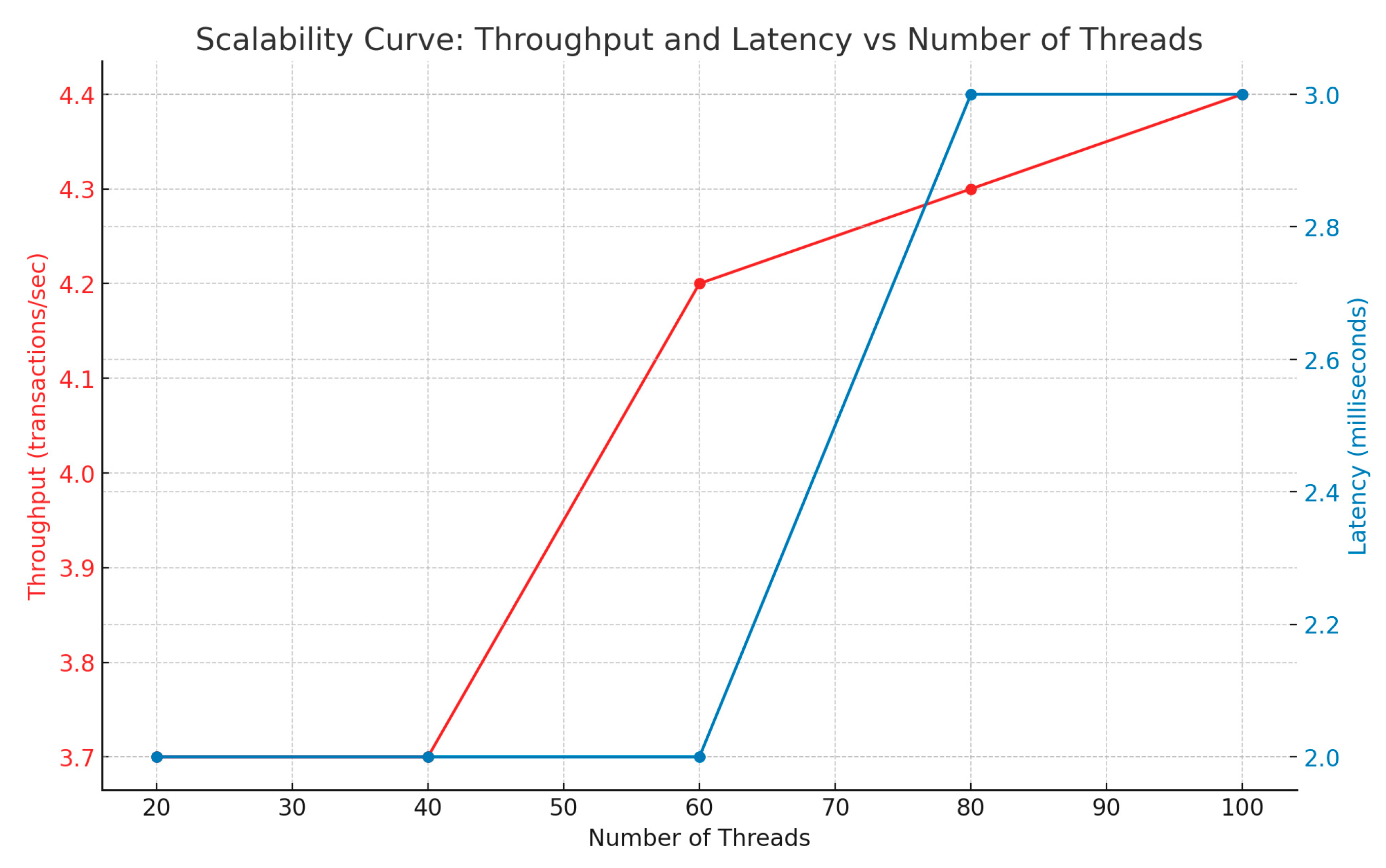

To validate the proposed framework, we developed a prototype bank application using JavaScript (version 1.8.5), HTML5, and CSS3 for the front-end development, Node.js (version 14.17.0) as the runtime environment, and Express.js (version 4.17.1) served as the web application framework, together enabling efficient processing and routing of server-side requests. Data storage and management were handled using MySQL (version 8.0.23), a robust relational database management system that ensures secure and scalable storage of sensitive customer and transaction data. Additionally, the application integrated the AWS KMS for cryptographic key management and the AWS SDK for interfacing with AWS services. Web3.js was used for interactions with the Ethereum blockchain, particularly for smart contract functionalities associated with user authentication. Ethereum-Ganache (v. 2.7.1), part of the Truffle Suite, provided a local blockchain environment for Ethereum development, facilitating the testing and development of smart contract functionalities. Truffle was employed as a comprehensive environment for the development, testing, and deployment of Ethereum smart contracts.

Security measures were a paramount consideration, with the application incorporating client sessions for secure session management, bcrypt (v. 5.0.1) for robust password hashing, Helmet for setting secure HTTP headers, express rate limit for mitigating brute-force attacks, and XSS filters and Bleach for sanitising user inputs to prevent cross-site scripting attacks. The HTTPS module was used to establish a secure server, encrypting data exchanged between the client and the server, thus reinforcing the application’s adherence to the Zero Trust model principles.