Implications of Emerging Vehicle Technologies on Rare Earth Supply and Demand in the United States

Abstract

1. Introduction

- What could be the demand for rare earth elements by the AEV sector until 2050?

- How does historical US domestic production compare to these demands?

- What role could end-of-life vehicles play as a secondary source of these materials?

- How would new critical material intensive-technologies impact supply and demand?

2. Materials and Methods

2.1. Vehicle Inflows

2.2. Vehicle Stocks and Outflows

2.3. Material Intensities and the Mass of Materials in Vehicles

2.4. Scenarios of Technological Change

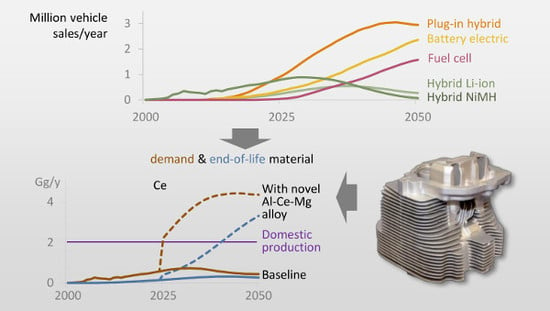

3. Results

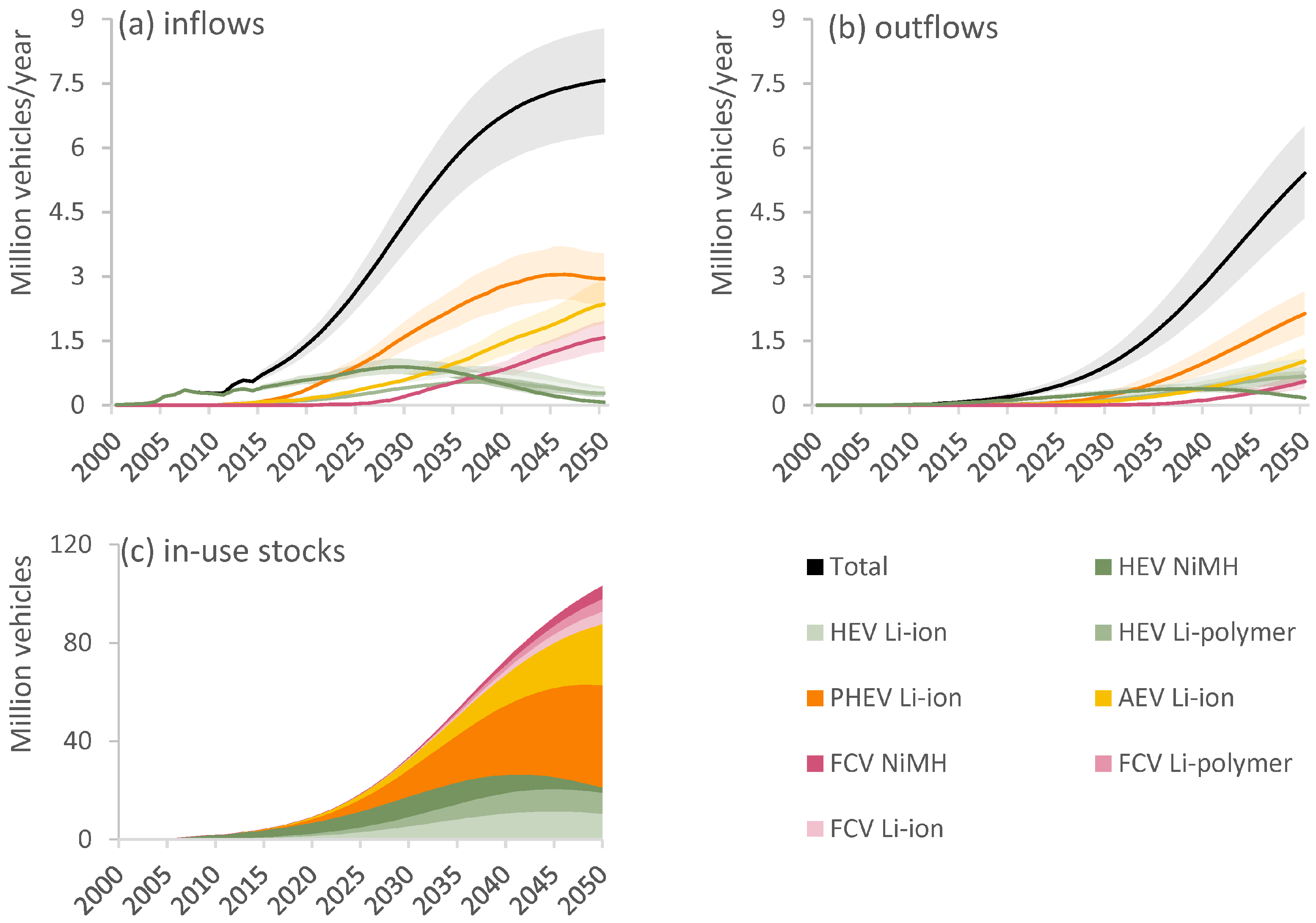

3.1. Vehicle Trends

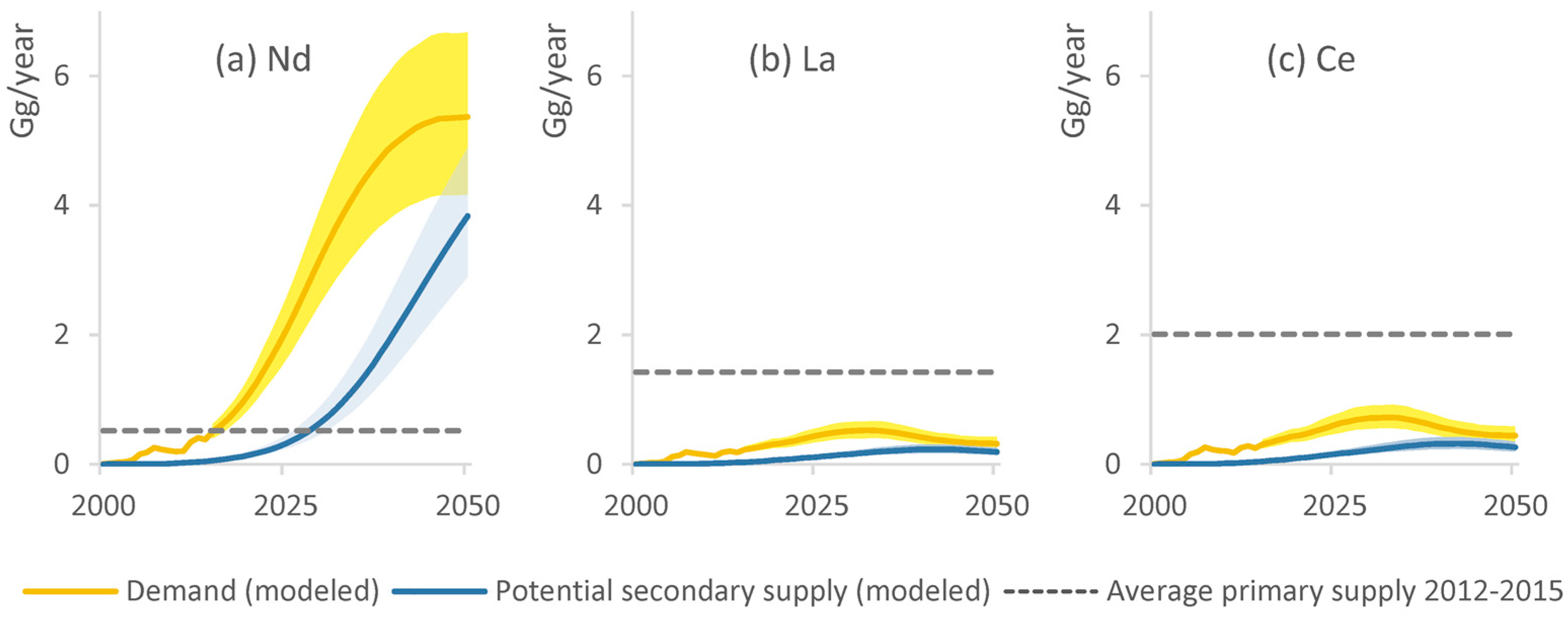

3.2. Supply and Demand of Rare Earth Elements

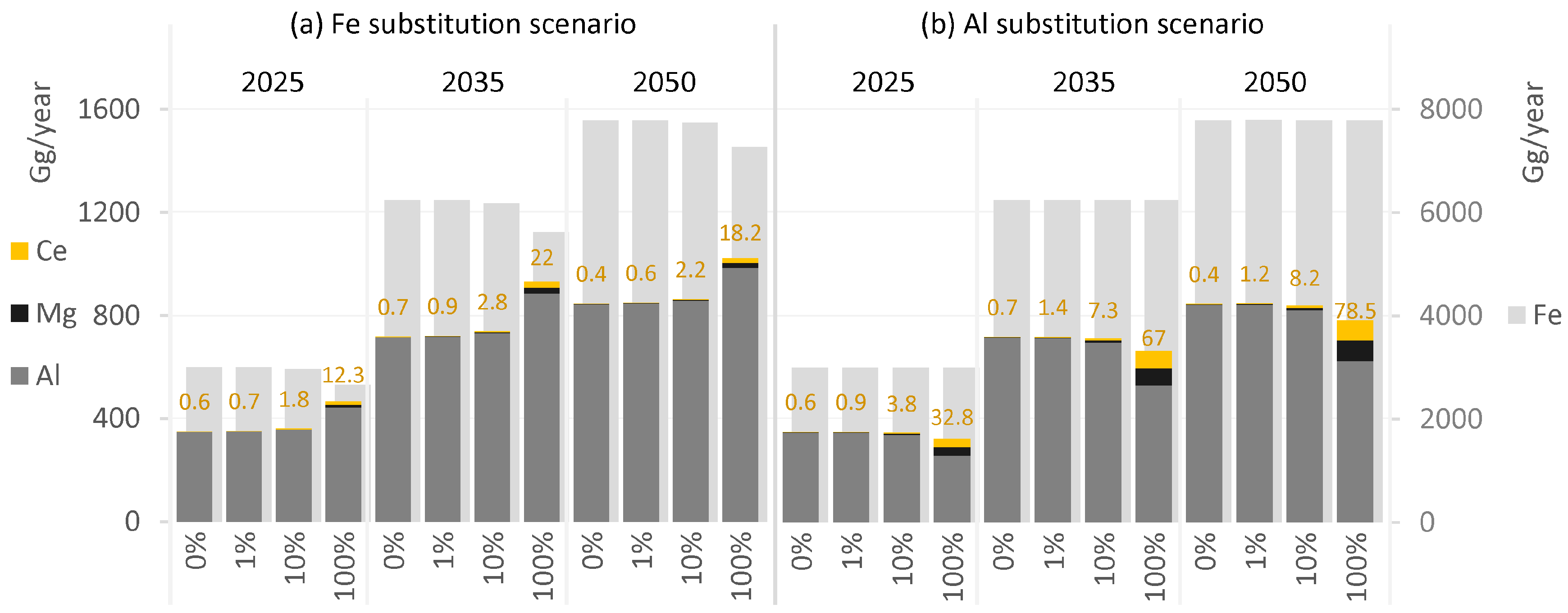

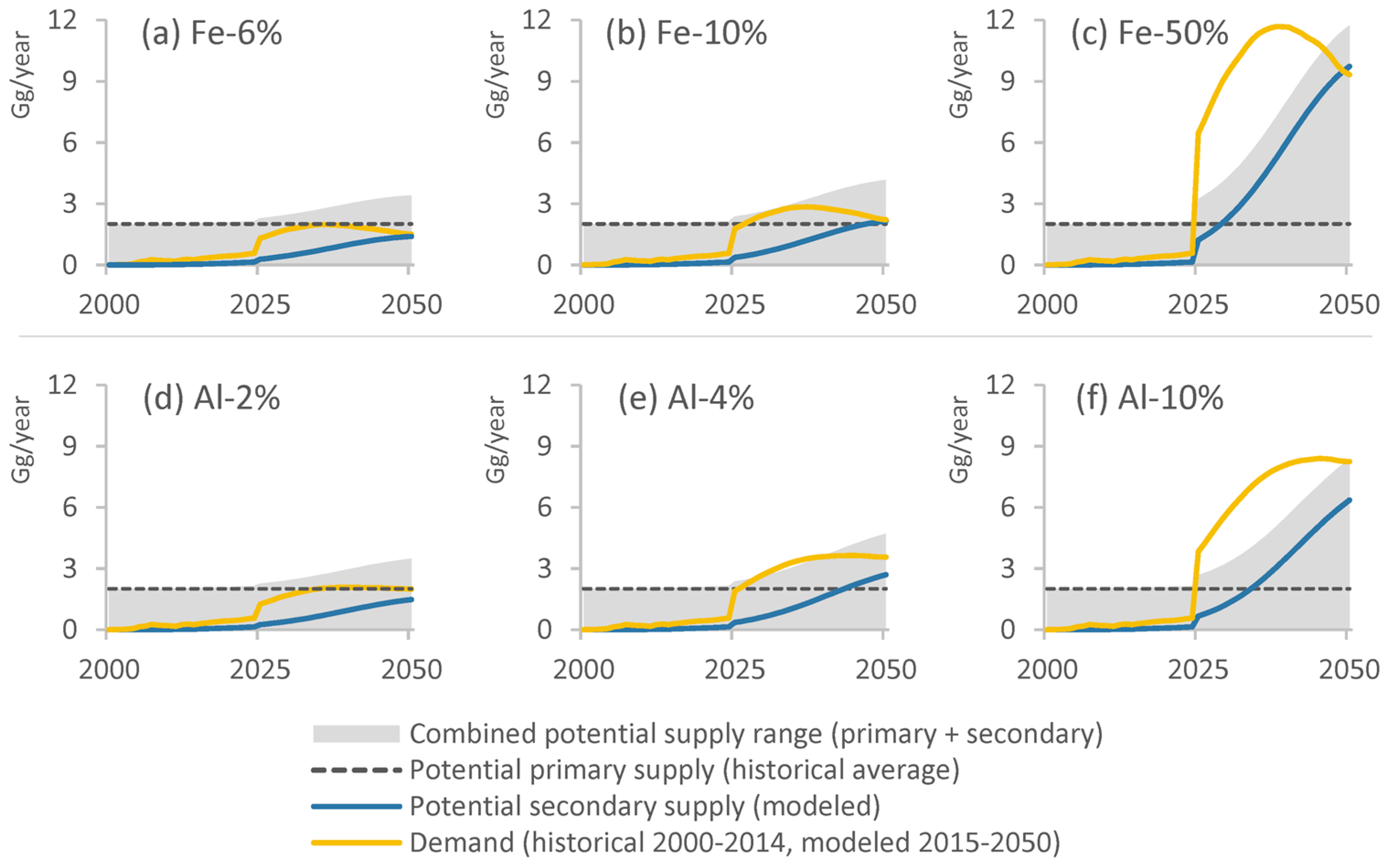

3.3. Introduction of AlCeMg Alloy Technology

3.4. Can Demands and Supplies Reach Equilibrium?

4. Discussion

4.1. Outlook for REEs in AEVs

4.2. Shifting Stocks

4.3. Technological Changes

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- U.S. Department of Transportation. National Transportation Statistics; Bureau of Transportation Statistics: Washington, DC, USA, 2016.

- U.S. Department of Energy. HEV Sales by Model. Available online: https://www.afdc.energy.gov/uploads/data/data_source/10301/10301_hev_sales.xlsx (accessed on 27 January 2017).

- International Energy Agency. Technology Roadmap: Electric and Plug-In Hybrid Electric Vehicles (2011 Update); IEA Publications: Paris, France, 2011. [Google Scholar]

- Miotti, M.; Supran, G.J.; Kim, E.J.; Trancik, J.E. Personal Vehicles Evaluated against Climate Change Mitigation Targets. Environ. Sci. Technol. 2016, 50, 10795–10804. [Google Scholar] [CrossRef] [PubMed]

- U.S. Energy Information Administration. Annual Energy Outlook 2017; U.S. Energy Information Administration: Washington, DC, USA, 2017. Available online: https://www.eia.gov/outlooks/aeo (accessed on 4 May 2017).

- U.S. Department of Energy. 2011 Critical Materials Strategy. 2011. Available online: https://energy.gov/epsa/downloads/2011-critical-materials-strategy (accessed on 6 July 2017).

- Du, X.; Graedel, T.E. Global In-Use Stocks of the Rare Earth Elements: A First Estimate. Environ. Sci. Technol. 2011, 45, 4096–4101. [Google Scholar] [CrossRef] [PubMed]

- Sprecher, B.; Daigo, I.; Murakami, S.; Kleijn, R.; Vos, M.; Kramer, G.J. Framework for Resilience in Material Supply Chains, With a Case Study from the 2010 Rare Earth Crisis. Environ. Sci. Technol. 2015, 49, 6740–6750. [Google Scholar] [CrossRef] [PubMed]

- Imholte, D.D.; Nguyen, R.T.; Vedantam, A.; Brown, M.; Iyer, A.; Smith, B.J.; Collins, J.W.; Anderson, C.G.; O’Kelley, B. An assessment of U.S. rare earth availability for supporting U.S. wind energy growth targets. Energy Policy 2018, 113, 294–305. [Google Scholar] [CrossRef]

- Graedel, T.E.; Harper, E.M.; Nassar, N.T.; Nuss, P.; Reck, B.K. Criticality of metals and metalloids. Proc. Natl. Acad. Sci. USA 2015, 112, 4257–4262. [Google Scholar] [CrossRef] [PubMed]

- Massari, S.; Ruberti, M. Rare earth elements as critical raw materials: Focus on international markets and future strategies. Resour. Policy 2013, 38, 36–43. [Google Scholar] [CrossRef]

- Eggert, R.G. Minerals go critical. Nat. Chem. 2011, 3, 688–691. [Google Scholar] [CrossRef] [PubMed]

- Lovins, A. Clean energy and rare earths: Why not to worry. Bulletin of the Atomic Scientists. 2017. Available online: https://thebulletin.org/clean-energy-and-rare-earths-why-not-worry10785 (accessed on 17 July 2017).

- Du, X.; Graedel, T.E. Uncovering the end uses of the rare earth elements. Sci. Total Environ. 2013, 461–462, 781–784. [Google Scholar] [CrossRef] [PubMed]

- Shigetomi, Y.; Nansai, K.; Kagawa, S.; Kondo, Y.; Tohno, S. Economic and social determinants of global physical flows of critical metals. Resour. Policy 2017, 52, 107–113. [Google Scholar] [CrossRef]

- Ciacci, L.; Reck, B.K.; Nassar, N.T.; Graedel, T.E. Lost by Design. Environ. Sci. Technol. 2015, 49, 9443–9451. [Google Scholar] [CrossRef] [PubMed]

- Graedel, T.E.; Allwood, J.; Birat, J.-P.; Buchert, M.; Hagelüken, C.; Reck, B.K.; Sibley, S.F.; Sonnemann, G. What Do We Know About Metal Recycling Rates? J. Ind. Ecol. 2011, 15, 355–366. [Google Scholar] [CrossRef]

- Fridstrøm, L.; Østli, V.; Johansen, K.W. A stock-flow cohort model of the national car fleet. Eur. Transp. Res. Rev. 2016, 8, 22. [Google Scholar] [CrossRef]

- Modaresi, R.; Pauliuk, S.; Løvik, A.N.; Müller, D.B. Global Carbon Benefits of Material Substitution in Passenger Cars until 2050 and the Impact on the Steel and Aluminum Industries. Environ. Sci. Technol. 2014, 48, 10776–10784. [Google Scholar] [CrossRef] [PubMed]

- Serrenho, A.C.; Allwood, J.M. Material Stock Demographics: Cars in Great Britain. Environ. Sci. Technol. 2016, 50, 3002–3009. [Google Scholar] [CrossRef]

- Busch, J.; Steinberger, J.K.; Dawson, D.A.; Purnell, P.; Roelich, K. Managing Critical Materials with a Technology-Specific Stocks and Flows Model. Environ. Sci. Technol. 2014, 48, 1298–1305. [Google Scholar] [CrossRef] [PubMed]

- Busch, J.; Dawson, D.; Roelich, K. Closing the low-carbon material loop using a dynamic whole system approach. J. Clean. Prod. 2017, 149, 751–761. [Google Scholar] [CrossRef]

- Elshkaki, A. An analysis of future platinum resources, emissions and waste streams using a system dynamic model of its intentional and non-intentional flows and stocks. Resour. Policy 2013, 38, 241–251. [Google Scholar] [CrossRef]

- Majeau-Bettez, G.; Hawkins, T.R.; Strømman, A.H. Life Cycle Environmental Assessment of Lithium-Ion and Nickel Metal Hydride Batteries for Plug-In Hybrid and Battery Electric Vehicles. Environ. Sci. Technol. 2011, 45, 4548–4554. [Google Scholar] [CrossRef] [PubMed]

- Restrepo, E.; Løvik, A.N.; Wäger, P.; Widmer, R.; Lonka, R.; Müller, D.B. Stocks, Flows, and Distribution of Critical Metals in Embedded Electronics in Passenger Vehicles. Environ. Sci. Technol. 2017, 51, 1129–1139. [Google Scholar] [CrossRef] [PubMed]

- Sun, Y.; Delucchi, M.; Ogden, J. The impact of widespread deployment of fuel cell vehicles on platinum demand and price. Int. J. Hydrogen Energy 2011, 36, 11116–11127. [Google Scholar] [CrossRef]

- Yano, J.; Muroi, T.; Sakai, S. Rare earth element recovery potentials from end-of-life hybrid electric vehicle components in 2010–2030. J. Mater. Cycles Waste Manag. 2016, 18, 655–664. [Google Scholar] [CrossRef]

- The Economist. The Driverless, Car-Sharing Road Ahead. The Economist, 9 January 2016. Available online: https://www.economist.com/news/business/21685459-carmakers-increasingly-fret-their-industry-brink-huge-disruption (accessed on 17 January 2018).

- Musk, E. Hyperloop Alpha; SpaceX: Hawthorne, CA, USA, 2013; Available online: http://www.spacex.com/sites/spacex/files/hyperloop_alpha.pdf (accessed on 17 January 2018).

- Sims, Z.C.; Weiss, D.; McCall, S.K.; McGuire, M.A.; Ott, R.T.; Geer, T.; Rios, O.; Turchi, P.A.E. Cerium-Based, Intermetallic-Strengthened Aluminum Casting Alloy: High-Volume Co-product Development. JOM 2016, 68, 1940–1947. [Google Scholar] [CrossRef]

- Sims, Z.C.; Rios, O.R.; Weiss, D.; Turchi, P.E.A.; Perron, A.; Lee, J.R.I.; Li, T.T.; Hammons, J.A.; Bagge-Hansen, M.; Willey, T.M.; et al. High performance aluminum-cerium alloys for high-temperature applications. Mater. Horiz. 2017, 4, 1070–1078. [Google Scholar] [CrossRef]

- Modaresi, R.; Løvik, A.N.; Müller, D.B. Component- and Alloy-Specific Modeling for Evaluating Aluminum Recycling Strategies for Vehicles. JOM 2014, 66, 2262–2271. [Google Scholar] [CrossRef]

- U.S. Geological Survey. Rare Earth Elements—Critical Resources for High Technology; U.S. Geological Survey: Reston, VA, USA, 2002.

- Nguyen, R.T.; Imholte, D.D. China’s Rare Earth Supply Chain: Illegal Production, and Response to new Cerium Demand. JOM 2016, 68, 1948–1956. [Google Scholar] [CrossRef]

- Elshkaki, A.; van der Voet, E.; Timmermans, V.; Holderbeke, M.V. Dynamic stock modelling: A method for the identification and estimation of future waste streams and emissions based on past production and product stock characteristics. Energy 2005, 30, 1353–1363. [Google Scholar] [CrossRef]

- Fishman, T.; Schandl, H.; Tanikawa, H.; Walker, P.; Krausmann, F. Accounting for the Material Stock of Nations. J. Ind. Ecol. 2014, 18, 407–420. [Google Scholar] [CrossRef] [PubMed]

- Hatayama, H.; Daigo, I.; Matsuno, Y.; Adachi, Y. Outlook of the World Steel Cycle Based on the Stock and Flow Dynamics. Environ. Sci. Technol. 2010, 44, 6457–6463. [Google Scholar] [CrossRef] [PubMed]

- Krausmann, F.; Wiedenhofer, D.; Lauk, C.; Haas, W.; Tanikawa, H.; Fishman, T.; Miatto, A.; Schandl, H.; Haberl, H. Global socioeconomic material stocks rise 23-fold over the 20th century and require half of annual resource use. Proc. Natl. Acad. Sci. USA 2017, 114, 1880–1885. [Google Scholar] [CrossRef] [PubMed]

- Van der Voet, E.; Kleijn, R.; Huele, R.; Ishikawa, M.; Verkuijlen, E. Predicting future emissions based on characteristics of stocks. Ecol. Econ. 2002, 41, 223–234. [Google Scholar] [CrossRef]

- Laner, D.; Rechberger, H.; Astrup, T. Systematic Evaluation of Uncertainty in Material Flow Analysis. J. Ind. Ecol. 2014, 18, 859–870. [Google Scholar] [CrossRef]

- Liu, G.; Müller, D.B. Centennial Evolution of Aluminum In-Use Stocks on Our Aluminized Planet. Environ. Sci. Technol. 2013, 47, 4882–4888. [Google Scholar] [CrossRef] [PubMed]

- OECD/International Transport Forum. Long-run Trends in Car Use. In ITF Round Tables; No. 152; OECD Publishing/ITF: Paris, France, 2013; ISBN 978-92-821-0593-1. [Google Scholar] [CrossRef]

- Volvo Car Group. Volvo Cars to Go All Electric. 5 July 2017. Available online: https://www.media.volvocars.com/global/en-gb/media/pressreleases/210058/volvo-cars-to-go-all-electric (accessed on 15 October 2017).

- General Motors. GM Outlines All-Electric Path to Zero Emissions. 2 October 2017. Available online: http://www.gm.com/mol/m-2017-oct-1002-electric.html (accessed on 15 October 2017).

- Reuters. Automakers Get Serious about Electric Cars. Reuters, 17 November 2017. Available online: https://www.reuters.com/article/us-autos-electric-factbox/factbox-automakers-get-serious-about-electric-cars-idUSKBN1DH28A (accessed on 18 November 2017).

- National Conference of State Legislatures State Efforts to Promote Hybrid and Electric Vehicles. Available online: http://www.ncsl.org/research/energy/state-electric-vehicle-incentives-state-chart.aspx (accessed on 15 October 2017).

- International Energy Agency. Energy Technology Perspectives 2008: Scenarios & Strategies to 2050; IEA Publications: Paris, France, 2008. [Google Scholar]

- Miatto, A.; Schandl, H.; Tanikawa, H. How important are realistic building lifespan assumptions for material stock and demolition waste accounts? Resour. Conserv. Recycl. 2017, 122, 143–154. [Google Scholar] [CrossRef]

- National Highway Traffic Safety Administration. Vehicle Survivability and Travel Milage Schedules; NHTSA Technical Report; U.S. Department of Transportation: Springfield, VA, USA, 2006.

- Alonso, E.; Wallington, T.; Sherman, A.; Everson, M.; Field, F.; Roth, R.; Kirchain, R. An assessment of the rare earth element content of conventional and electric vehicles. SAE Int. J. Mater. Manuf. 2012, 5, 473–477. [Google Scholar] [CrossRef]

- Alonso, E.; Sherman, A.M.; Wallington, T.J.; Everson, M.P.; Field, F.R.; Roth, R.; Kirchain, R.E. Evaluating Rare Earth Element Availability: A Case with Revolutionary Demand from Clean Technologies. Environ. Sci. Technol. 2012, 46, 3406–3414. [Google Scholar] [CrossRef] [PubMed]

- Borgwardt, R.H. Platinum, fuel cells, and future US road transport. Transp. Res. Part D Transp. Environ. 2001, 6, 199–207. [Google Scholar] [CrossRef]

- Chan, C.C.; Bouscayrol, A.; Chen, K. Electric, hybrid, and fuel-cell vehicles: Architectures and modeling. IEEE Trans. Veh. Technol. 2010, 59, 589–598. [Google Scholar] [CrossRef]

- Cheah, L.; Heywood, J.; Kirchain, R. The energy impact of US passenger vehicle fuel economy standards. In Proceedings of the IEEE International Symposium on Sustainable Systems and Technology (ISSST), Arlington, VA, USA, 17–19 May 2010; pp. 1–6. [Google Scholar]

- Cullbrand, K.; Magnusson, O. The Use of Potentially Critical Materials in Passenger Cars; Chalmers University of Technology: Gothenburg, Sweden, 2012. [Google Scholar]

- Du, X.; Restrepo, E.; Widmer, R.; Wäger, P. Quantifying the distribution of critical metals in conventional passenger vehicles using input-driven and output-driven approaches: A comparative study. J. Mater. Cycles Waste Manag. 2015, 17, 218–228. [Google Scholar] [CrossRef]

- Ellingsen, L.A.-W.; Majeau-Bettez, G.; Singh, B.; Srivastava, A.K.; Valøen, L.O.; Strømman, A.H. Life Cycle Assessment of a Lithium-Ion Battery Vehicle Pack. J. Ind. Ecol. 2014, 18, 113–124. [Google Scholar] [CrossRef]

- Hawkins, T.R.; Singh, B.; Majeau-Bettez, G.; Strømman, A.H. Comparative Environmental Life Cycle Assessment of Conventional and Electric Vehicles. J. Ind. Ecol. 2013, 17, 53–64. [Google Scholar] [CrossRef]

- Hawkins, T.R.; Singh, B.; Majeau-Bettez, G.; Strømman, A.H. Corrigendum to: Comparative environmental life cycle assessment of conventional and electric vehicles. Ind. Ecol. 2013, 17, 158–160. [Google Scholar] [CrossRef]

- TIAX LLC. Platinum Availability and Economics for PEMFC Commercialization; Report to US Department of Energy; TIAX LLC: Cambridge, MA, USA, 2003. Available online: http://www1.eere.energy.gov/hydrogenandfuelcells/pdfs/tiax_platinum.pdf (accessed on 15 September 2016).

- Tollefson, J. Worth its weight in platinum: Booming mineral prices leave car makers scrambling to eke more catalytic performance out of precious metals. Nature 2007, 450, 334–336. [Google Scholar] [CrossRef] [PubMed]

- U.S. Department of Energy. Alternative Fuels Data Center. Available online: https://www.afdc.energy.gov/data/ (accessed on 20 November 2016).

- U.S. Department of Energy. AVTA: Light Duty Alternative Fuel and Advanced Vehicle Data. Available online: https://energy.gov/eere/vehicles/avta-light-duty-alternative-fuel-and-advanced-vehicle-data (accessed on 20 November 2016).

- Kelly, T.D.; Matos, G.R. Historical Statistics for Mineral and Material Commodities in the United States. U.S. Geological Survey Rare Earth Statistics [Through 2015, Last Modified 19 January 2017]. Available online: https://minerals.usgs.gov/minerals/pubs/historical-statistics//#rareearths (accessed on 8 June 2017).

- U.S. Geological Survey. Mineral Commodity Summaries 2017, 2017th ed.; U.S. Geological Survey: Reston, VA, USA, 2017.

- Goonan, T.G. Rare Earth Elements—End Use and Recyclability: U.S. Geological Survey Scientific Investigations Report 2011-5094; U.S. Geological Survey: Reston, VA, USA, 2011.

- Binnemans, K.; Jones, P.T. Rare Earths and the Balance Problem. J. Sustain. Metall. 2015, 1, 29–38. [Google Scholar] [CrossRef]

- Elshkaki, A.; Graedel, T.E. Dysprosium, the balance problem, and wind power technology. Appl. Energy 2014, 136, 548–559. [Google Scholar] [CrossRef]

- Gordon, R.B.; Bertram, M.; Graedel, T. Metal stocks and sustainability. Proc. Natl. Acad. Sci. USA 2006, 103, 1209–1214. [Google Scholar] [CrossRef] [PubMed]

- Rauch, J.N. Global mapping of Al, Cu, Fe, and Zn in-use stocks and in-ground resources. Proc. Natl. Acad. Sci. USA 2009, 106, 18920–18925. [Google Scholar] [CrossRef] [PubMed]

- Sverdrup, H.U.; Ragnarsdottir, K.V.; Koca, D. Aluminium for the future: Modelling the global production, market supply, demand, price and long term development of the global reserves. Resour. Conserv. Recycl. 2015, 103, 139–154. [Google Scholar] [CrossRef]

- Gruber, P.W.; Medina, P.A.; Keoleian, G.A.; Kesler, S.E.; Everson, M.P.; Wallington, T.J. Global Lithium Availability. J. Ind. Ecol. 2011, 15, 760–775. [Google Scholar] [CrossRef]

- Simon, B.; Ziemann, S.; Weil, M. Potential metal requirement of active materials in lithium-ion battery cells of electric vehicles and its impact on reserves: Focus on Europe. Resour. Conserv. Recycl. 2015, 104, 300–310. [Google Scholar] [CrossRef]

- Narins, T.P. The battery business: Lithium availability and the growth of the global electric car industry. Extr. Ind. Soc. 2017, 4, 321–328. [Google Scholar] [CrossRef]

- Ali, S.H.; Giurco, D.; Arndt, N.; Nickless, E.; Brown, G.; Demetriades, A.; Durrheim, R.; Enriquez, M.A.; Kinnaird, J.; Littleboy, A.; et al. Mineral supply for sustainable development requires resource governance. Nature 2017, 543, 367–372. [Google Scholar] [CrossRef] [PubMed]

- Simas, M.; Pauliuk, S.; Wood, R.; Hertwich, E.G.; Stadler, K. Correlation between production and consumption-based environmental indicators: The link to affluence and the effect on ranking environmental performance of countries. Ecol. Indic. 2017, 76, 317–323. [Google Scholar] [CrossRef]

- Wiedmann, T.O.; Schandl, H.; Lenzen, M.; Moran, D.; Suh, S.; West, J.; Kanemoto, K. The material footprint of nations. Proc. Natl. Acad. Sci. USA 2015, 122, 6271–6276. [Google Scholar] [CrossRef] [PubMed]

- RTTNews. Reuters: GM May Cancel Six Car Models In U.S., Including Chevrolet Volt. Business Insider. 2017. Available online: http://markets.businessinsider.com/news/stocks/Reuters-GM-May-Cancel-Six-Car-Models-In-U-S-Including-Chevrolet-Volt-1002196631 (accessed on 3 August 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Material | Baseline Scenario | Fe Substitution Scenario | Al Substitution Scenario |

|---|---|---|---|

| Fe | |||

| Al | |||

| Mg | |||

| Ce |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fishman, T.; Myers, R.J.; Rios, O.; Graedel, T.E. Implications of Emerging Vehicle Technologies on Rare Earth Supply and Demand in the United States. Resources 2018, 7, 9. https://doi.org/10.3390/resources7010009

Fishman T, Myers RJ, Rios O, Graedel TE. Implications of Emerging Vehicle Technologies on Rare Earth Supply and Demand in the United States. Resources. 2018; 7(1):9. https://doi.org/10.3390/resources7010009

Chicago/Turabian StyleFishman, Tomer, Rupert J. Myers, Orlando Rios, and T.E. Graedel. 2018. "Implications of Emerging Vehicle Technologies on Rare Earth Supply and Demand in the United States" Resources 7, no. 1: 9. https://doi.org/10.3390/resources7010009

APA StyleFishman, T., Myers, R. J., Rios, O., & Graedel, T. E. (2018). Implications of Emerging Vehicle Technologies on Rare Earth Supply and Demand in the United States. Resources, 7(1), 9. https://doi.org/10.3390/resources7010009