The Impact of Digital Finance on Farmers’ Adoption of Eco-Agricultural Technology: Evidence from Rice-Crayfish Co-Cultivation Technology in China

Abstract

1. Introduction

2. Theoretical Analysis

2.1. Theoretical Framework

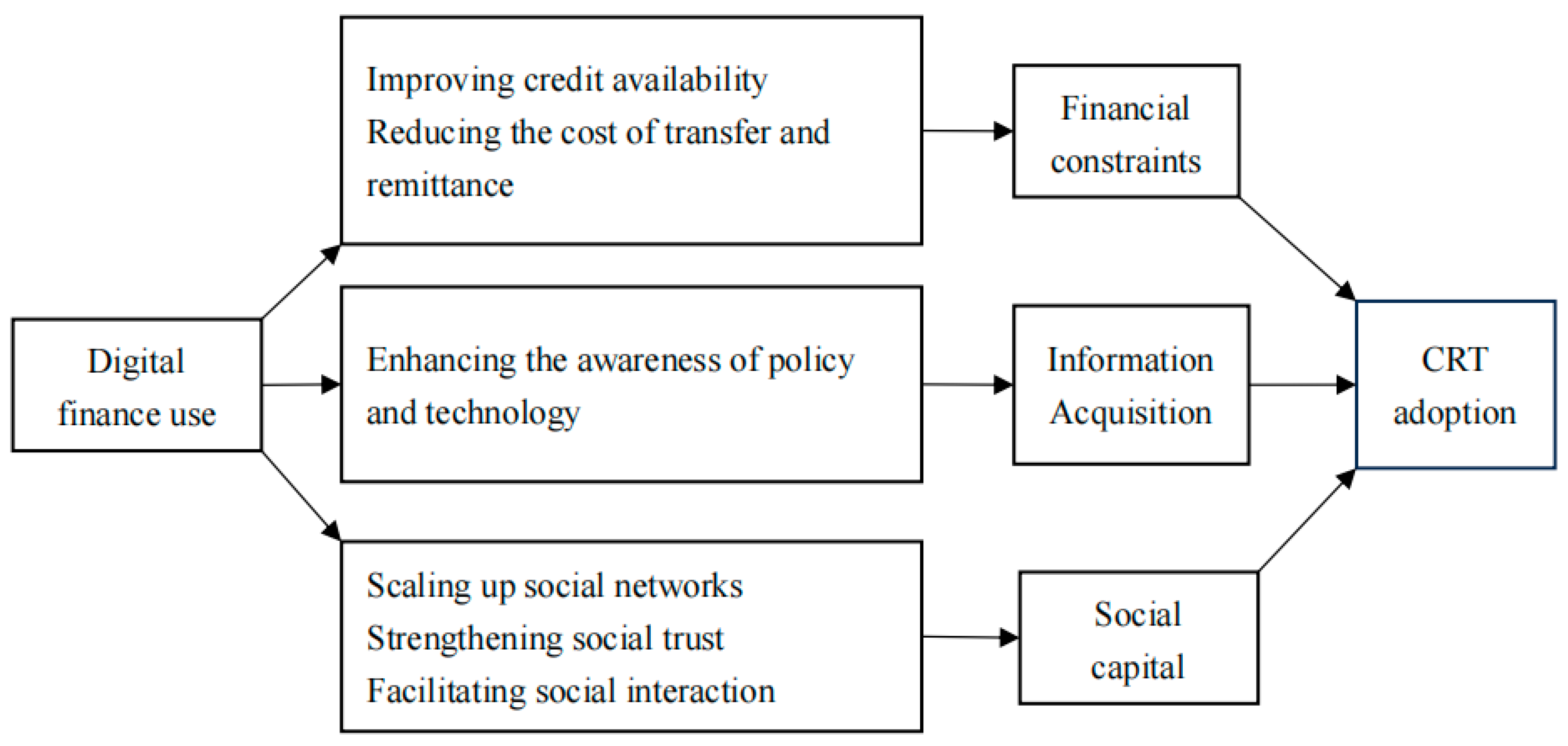

2.2. Mechanisms of Digital Finance on Farmers’ Adoption of Ecological Agricultural Technologies

2.2.1. Alleviating Financial Constraints

2.2.2. Expanding Information Channels

2.2.3. Increasing Social Capital Accumulation

3. Materials and Methods

3.1. Data

3.2. Variable Settings

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Control Variables

3.2.4. Mediating Variables

3.2.5. Instrumental Variable

3.3. Descriptive Statistics

3.4. Empirical Model

3.4.1. Endogenous Switching Probit Model

3.4.2. Mediation Effect Model

4. Results

4.1. Simultaneous Estimation Results

4.1.1. Factors Influencing Household Digital Finance Usage Decision

4.1.2. Factors Influencing the Adoption of CRT by Households

4.2. Average Treatment Effect (ATT) Estimation

4.3. Robustness Check

4.4. Heterogeneity Analysis

4.5. Mechanism Analysis

4.5.1. Alleviating Financial Constraints

4.5.2. Expanding Information Channels

4.5.3. Increasing Social Capital Accumulation

5. Conclusions and Discussion

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Lockeretz, W. Problems in evaluating the economics of ecological agriculture. Agr. Ecosyst. Environ. 1989, 27, 67–75. [Google Scholar] [CrossRef]

- Shah, S.I.A.; Zhou, J.H.; Shah, A.A. Ecosystem-based Adaptation (EbA) practices in smallholder agriculture: Emerging evidence from rural Pakistan. J. Clean. Prod. 2019, 218, 673–684. [Google Scholar] [CrossRef]

- Priyadarshini, P.; Abhilash, P.C. Policy recommendations for enabling transition towards sustainable agriculture in India. Land Use Policy 2020, 96, 104718. [Google Scholar] [CrossRef]

- Cao, C.; Wang, Y.; Wang, J.P.; Yuan, P.L.; Chen, S.W. “Dual character” of rice-crayfish culture and strategy for its sustainable development. Chin. J. Eco-Agric. 2017, 25, 1245–1253. (In Chinese) [Google Scholar]

- Wei, Y.B.; Lu, M.; Yu, Q.Y.; Xie, A.K.; Hu, Q.; Wu, W.B. Understanding the dynamics of integrated rice–crawfish farming in Qianjiang county, China using Landsat time series images. Agric. Syst. 2021, 191, 103167. [Google Scholar] [CrossRef]

- Chen, Y.L.; Yu, P.H.; Chen, Y.Y.; Chen, Z.Y. Spatiotemporal dynamics of rice–crayfish field in Mid-China and its socioeconomic benefits on rural revitalization. Appl. Geogr. 2021, 139, 102636. [Google Scholar] [CrossRef]

- Xie, J.; Hu, L.L.; Tang, J.J.; Wu, X.; Li, N.N.; Yuan, Y.G.; Yang, H.S.; Zhang, J.E.; Luo, S.M.; Chen, X. Ecological mechanisms underlying the sustainability of the agricultural heritage rice–fish coculture system. Proc. Natl. Acad. Sci. USA 2011, 108, 1381–1387. [Google Scholar] [CrossRef] [PubMed]

- Ge, L.; Sun, Y.; Li, Y.J.; Wang, L.Y.; Guo, G.Q.; Song, L.L.; Wang, C.; Wu, G.G.; Zang, X.Y.; Cai, X.M.; et al. Ecosystem sustainability of rice and aquatic animal co-culture systems and a synthesis of its underlying mechanisms. Sci. Total Environ. 2023, 880, 163314. [Google Scholar] [CrossRef] [PubMed]

- Li, L.W.; Li, N.; Lu, D.S.; Chen, Y.Y. Mapping Moso bamboo forest and its on-year and off-year distribution in a subtropical region using time-series Sentinel-2 and Landsat 8 data. Remote Sens. Environ. 2019, 231, 111265. [Google Scholar] [CrossRef]

- Zhou, Y.; Yan, X.Y.; Gong, S.L.; Li, C.W.; Zhu, R.; Zhu, B.; Liu, Z.Y.; Wang, X.L.; Cao, P. Changes in paddy cropping system enhanced economic profit and ecological sustainability in central China. J. Integr. Agric. 2022, 21, 566–577. [Google Scholar] [CrossRef]

- Kabir, J.; Cramb, R.; Alauddin, M.; Gaydon, D.S.; Roth, C.H. Farmers’ perceptions and management of risk in rice/shrimp farming systems in South-West Coastal Bangladesh. Land Use Policy 2020, 95, 104577. [Google Scholar] [CrossRef]

- Bashir, M.A.; Liu, J.; Geng, Y.C.; Wang, H.Y.; Pan, J.T.; Zhang, D.; Rehim, A.; Aon, M.; Liu, H.B. Co-culture of rice and aquatic animals: An integrated system to achieve production and environmental sustainability. J. Clean. Prod. 2020, 249, 119310. [Google Scholar] [CrossRef]

- Cafer, A.M.; Rikoon, J.S. Adoption of new technologies by smallholder farmers: The contributions of extension, research institutes, cooperatives, and access to cash for improving tef production in Ethiopia. Agric. Hum. Values 2018, 35, 685–699. [Google Scholar] [CrossRef]

- Sieber, S.; Graef, F.; Amjath-Babu, T.S.; Mutabazi, K.D.; Tumbo, S.D.; Fasse, A.; Paloma, S.G.Y.; Rybak, C.; Lana, M.A.; Ndah, H.T.; et al. Trans-SEC’s food security research in Tanzania: From constraints to adoption for out- and upscaling of agricultural innovations. Food Secur. 2018, 10, 775–783. [Google Scholar] [CrossRef]

- Boucher, S.R.; Carter, M.R.; Guirkinger, C. Risk rationing and wealth effects in credit markets: Theory and implications for agricultural development. Am. J. Agric. Econ. 2008, 90, 409–423. [Google Scholar] [CrossRef]

- Bruhn, M.; Love, I. The real impact of improved access to finance: Evidence from mexico. J. Financ. 2014, 69, 1347–1376. [Google Scholar] [CrossRef]

- Mbiti, I.; Weil, D.N. The home economics of e-money: Velocity, cash management, and discount rates of m-pesa users. Am. Econ. Rev. 2013, 103, 369–374. [Google Scholar] [CrossRef] [PubMed]

- Auci, S.; Pronti, A. Irrigation technology adaptation for a sustainable agriculture: A panel endogenous switching analysis on the Italian farmland productivity. Resour. Energy Econ. 2023, 74, 101391. [Google Scholar] [CrossRef]

- Jack, W.; Suri, T. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. Am. Econ. Rev. 2014, 104, 183–223. [Google Scholar] [CrossRef]

- Lee, C.C.; Wang, F.H.; Lou, R.C.; Wang, K.Y. How does green finance drive the decarbonization of the economy? Empirical evidence from China. Renew. Energy 2023, 204, 671–684. [Google Scholar] [CrossRef]

- Yu, L.L.; Zhao, D.Y.; Xue, Z.H.; Gao, Y. Research on the use of digital finance and the adoption of green control techniques by family farms in China. Technol. Soc. 2020, 62, 101323. [Google Scholar] [CrossRef]

- Rasoulinezhad, E.; Taghizadeh-Hesary, F. Role of green finance in improving energy efficiency and renewable energy development. Energy Effic. 2022, 15, 14. [Google Scholar] [CrossRef] [PubMed]

- Ellison, N.B.; Vitak, J.; Gray, R.; Lampe, C. Cultivating social resources on social network sites: Facebook relationship maintenance behaviors and their role in social capital processes. J. Comput. Mediat. Commun. 2014, 19, 855–870. [Google Scholar] [CrossRef]

- Abdul-Rahaman, A.; Abdulai, A. Mobile money adoption, input use, and farm output among smallholder rice farmers in Ghana. Agribusiness 2021, 38, 236–255. [Google Scholar] [CrossRef]

- Lagakos, D.; Marshall, S.; Mobarak, A.M.; Vernot, C.; Waugh, M.E. Migration costs and observational returns to migration in the developing world. J. Monetary Econ. 2020, 113, 138–154. [Google Scholar] [CrossRef]

- Liu, D.; Li, Y.S.; You, J.; Balezentis, T.; Shen, Z.Y. Digital inclusive finance and green total factor productivity growth in rural areas. J. Clean. Prod. 2023, 418, 138159. [Google Scholar] [CrossRef]

- Kromidha, E. Identity mediation strategies for digital inclusion in entrepreneurial finance. Int. J. Inf. Manag. 2023, 72, 102658. [Google Scholar] [CrossRef]

- Zhao, P.P.; Zhang, W.; Cai, W.C.; Liu, T.J. The impact of digital finance use on sustainable agricultural practices adoption among smallholder farmers: An evidence from rural China. Environ. Sci. Pollut. Res. 2022, 29, 39281–39294. [Google Scholar] [CrossRef] [PubMed]

- Aparo, N.O.; Odongo, W.; De Steur, H. Unraveling heterogeneity in farmer’s adoption of mobile phone technologies: A systematic review. Technol. Forecast. Soc. Chang. 2022, 185, 122048. [Google Scholar] [CrossRef]

- Song, K.; Wu, P.Z.; Zou, S.R. The adoption and use of mobile payment: Determinants and relationship with bank access☆. China Econ. Rev. 2023, 77, 101907. [Google Scholar] [CrossRef]

- Koulayev, S.; Rysman, M.; Schuh, S.; Stavins, J. Explaining adoption and use of payment instruments by US consumers. Rand J. Econ. 2016, 47, 293–325. [Google Scholar] [CrossRef]

- Carter, M.R.; Olinto, P. Getting institutions “right” for whom? Credit constraints and the impact of property rights on the quantity and composition of investment. Am. J. Agric. Econ. 2003, 85, 173–186. [Google Scholar] [CrossRef]

- Su, L.L.; Peng, Y.L.; Kong, R.; Chen, Q. Impact of e-commerce adoption on farmers’ participation in the digital financial market: Evidence from rural China. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1434–1457. [Google Scholar] [CrossRef]

- Bressan, S.; Pace, N.; Pelizzon, L. Health status and portfolio choice: Is their relationship economically relevant? Int. Rev. Financ. Anal. 2014, 32, 109–122. [Google Scholar] [CrossRef]

- Jack, W.; Ray, A.; Suri, T. Transaction networks: Evidence from mobile money in Kenya. Am. Econ. Rev. 2013, 103, 356–361. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inform. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Beck, T.; Pamuk, H.; Ramrattan, R.; Uras, B.R. Payment instruments, finance and development. J. Dev. Econ. 2018, 133, 162–186. [Google Scholar] [CrossRef]

- Giné, X. Access to capital in rural Thailand: An estimated model of formal vs. informal credit. J. Dev. Econ. 2011, 96, 16–29. [Google Scholar] [CrossRef]

- Girma, Y. Credit access and agricultural technology adoption nexus in Ethiopia: A systematic review and meta-analysis. J. Agric. Food Res. 2022, 10, 100362. [Google Scholar] [CrossRef]

- Croppenstedt, A.; Demeke, M.; Meschi, M.M. Technology adoption in the presence of constraints: The case of fertilizer demand in Ethiopia. Rev. Dev. Econ. 2003, 7, 58–70. [Google Scholar] [CrossRef]

- Yang, X.; Zhou, X.H.; Deng, X.Z. Modeling farmers’ adoption of low-carbon agricultural technology in Jianghan Plain, China: An examination of the theory of planned behavior. Technol. Forecast. Soc. Chang. 2022, 180, 121726. [Google Scholar] [CrossRef]

- Narayan, D.; Cassidy, M.F. A dimensional approach to measuring social capital: Development and validation of a social capital inventory. Current Sociol. 2016, 49, 59–102. [Google Scholar] [CrossRef]

- Hunecke, C.; Engler, A.; Jara-Rojas, R.; Poortvliet, P.M. Understanding the role of social capital in adoption decisions: An application to irrigation technology. Agric. Syst. 2017, 153, 221–231. [Google Scholar] [CrossRef]

- Ellison, N.B.; Steinfield, C.; Lampe, C. Connection strategies: Social capital implications of Facebook-enabled communication practices. New Media Soc. 2011, 13, 873–892. [Google Scholar] [CrossRef]

- Bandie, R.; Rasul, I. Social networks and technology adoption in northern Mozambique. Econ. J. 2006, 116, 869–902. [Google Scholar] [CrossRef]

- Satar, M.S.; Alarifi, G.; Alrubaishi, D. Exploring the entrepreneurial competencies of E-commerce entrepreneurs. Int. J. Manag. Educ. 2023, 21, 100799. [Google Scholar] [CrossRef]

- Deng, X.; Xu, D.D.; Zeng, M.; Qi, Y.B. Does internet use help reduce rural cropland abandonment? Evidence from China. Land Use Policy 2019, 89, 104243. [Google Scholar] [CrossRef]

- Lokshin, M.; Sajaia, Z. Impact of interventions on discrete outcomes: Maximum likelihood estimation of the binary choice models with binary endogenous regressors. Stata J. 2011, 11, 368–385. [Google Scholar] [CrossRef]

- Heckman, J.J.; Ichimura, H.; Todd, P. Matching as an econometric evaluation estimator: Evidence from evaluating a job training programme. Rev. Econom. Stud. 1997, 64, 605–654. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Atella, V.; Brunetti, M.; Maestas, N. Household portfolio choices, health status and health care systems: A cross- country analysis based on SHARE. J. Bank. Financ. 2012, 36, 1320–1335. [Google Scholar] [CrossRef] [PubMed]

- Lusardi, A.; Mitchell, O.S. The economic importance of financial literacy: Theory and evidence. J. Econ. Lit. 2014, 52, 5–44. [Google Scholar] [CrossRef] [PubMed]

- Wu, H.X.; Song, Y.; Yu, L.S.; Ge, Y. Uncertainty aversion and farmers’ innovative seed adoption: Evidence from a field experiment in rural China. J. Integr. Agric. 2023, 22, 1928–1944. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Definition | Digital Finance Users | Non-Users | Mean Difference (t-test) |

|---|---|---|---|---|

| Mean | Mean | |||

| Digital finance use | 1 If household uses any one of digital payment, digital credit or digital investment, 0 otherwise | 1.000 | - | 1.000 |

| CRT adoption | 1 if household adopt CRT in 2020, 0 otherwise | 0.773 | 0.584 | −0.189 *** |

| Male | 1 if household head is male, 0 female | 0.986 | 0.977 | −0.009 |

| Age | Household head’s age (in years) | 52.896 | 61.737 | 8.841 *** |

| Health status | Health status of the household head, 5-point Likert-type scale, 1 = very poor, 5 = very good | 4.458 | 3.998 | −0.460 *** |

| Education-level | Years of education of the household head | 8.689 | 6.872 | −1.817 *** |

| Party membership | 1 if household head has party membership, 0 otherwise | 0.216 | 0.102 | −0.114 *** |

| Risk appetite | According to the farmers’ preferences for different investment projects, assign values from 0 to 5, with higher values indicating a greater preference for risk. | 1.959 | 1.121 | −0.838 *** |

| Planting area | Total planting area (ha) | 32.180 | 18.930 | −13.250 *** |

| Soil fertility | Soil fertility of household, 5-point Likert-type scale, 1 = very bad, 5 = very good | 3.417 | 3.258 | −0.159 *** |

| Agricultural labor | Number of laborers engaged in agriculture in the household | 1.943 | 1.812 | −0.132 *** |

| Share of agricultural income | The ratio of a farmer’s agricultural income to his/her total household income (%) | 0.633 | 0.544 | −0.089 |

| New agricultural business entity | Whether the household engages in large-scale farming, family farm, and agricultural business: No = 0, any one organization member = 1, any two organization members = 2, three organization members = 3. | 0.190 | 0.063 | −0.127 *** |

| Irrigation condition | Proportion of effective irrigated area in the village canal system (%). | 98.462 | 99.023 | 0.561 |

| E-commerce service platform | 1 if village has e-commerce service platform, 0 otherwise | 0.359 | 0.319 | −0.040 |

| Distance to nearest township | Distance from the village committee to the nearest township (km) | 6.433 | 6.553 | 0.120 |

| Jingzhou | 1 if the household head is located in Jingzhou City, 0 otherwise | 0.629 | 0.735 | 0.106 *** |

| Instrumental variable | The mean value of “digital finance use” of other households in the same village, excluding the interviewed households | 0.636 | 0.539 | −0.097 *** |

| Financial constraints | Do you think the financial threshold for CRT is high? High = 1, No = 0. | 0.453 | 0.523 | 0.070 ** |

| Information acquisition | The level of attention to agricultural economy and financial information, 5-point Likert-type scale, 1 = very little, 5 = very much | 3.153 | 3.016 | −0.149 ** |

| Social capital | The household’s expenditure on interpersonal communication and postal communication in 2020 (Yuan) | 1.495 | 1.079 | −0.415 *** |

| Observations | — | 633 | 430 | — |

| Adoption of CRT (740) | No Adoption of CRT (323) | |||

|---|---|---|---|---|

| Observations | Proportion | Observations | Proportion | |

| Used digital finance | 489 | 66.08% | 144 | 44.59% |

| No digital finance | 251 | 33.92% | 179 | 55.41% |

| Variable | Selection Equation | Digital Finance Users’ Adoption | Non-Users’ Adoption |

|---|---|---|---|

| Coefficient | Coefficient | Coefficient | |

| Male | −0.167 * (0.345) | 0.239 (0.411) | 0.034 (0.403) |

| Age (years) | −0.067 *** (0.006) | 0.010 (0.008) | −0.004 (0.015) |

| Health status (1 = very poor, 5 = very good) | 0.199 *** (0.059) | −0.044 (0.079) | −0.108 * (0.075) |

| Education (years) | 0.074 *** (0.018) | −0.045 *** (0.017) | −0.048 * (0.024) |

| Party membership (1 = yes) | 0.513 ** (0.134) | −0.330 *** (0.134) | −0.387 *** (0.200) |

| Risk appetite (0 = risk aversion, 5 = risk appetite) | 0.058 ** (0.026) | 0.079 ** (0.033) | −0.021 (0.038) |

| Planting area (ha) | 0.002 (0.002) | 0.009 *** (0.003) | 0.005 (0.004) |

| Soil fertility (1 = very bad, 5 = very good) | 0.073 (0.061) | 0.143 * (0.075) | 0.243 *** (0.09) |

| Agricultural labor (Number) | 0.232 *** (0.084) | 0.052 (0.089) | 0.118 (0.139) |

| Share of agricultural income (%) | 0.024 (0.045) | −0.032 (0.041) | −0.082 (0.086) |

| New agricultural business entity (Number) | 0.298 * (0.158) | −0.199 (0.152) | −0.396 (0.252) |

| Irrigation condition (%) | −0.014 * (0.007) | 0.004 (0.007) | 0.013 (0.011) |

| E-commerce service platform (1 = yes) | 0.093 (0.010) | 0.129 (0.120) | −0.128 (0.129) |

| Distance to nearest township (km) | −0.02 * (0.011) | 0.045 *** (0.014) | 0.075 *** (0.017) |

| Jingzhou (1 = yes) | −0.152 (0.111) | 0.049 ** (0.126) | 0.290 * (0.157) |

| Instrumental variable | 1.443 *** (0.240) | ||

| Constant | 2.592 *** (0.966) | −0.730 (0.963) | −2.116 (1.562) |

| −0.755 *** (0.174) | |||

| −0.668 *** (0.209) | |||

| LR-test of independent equations: Chi-squared | 13.79 *** | ||

| Log likelihood | −1069.356 | ||

| Ward chi (2) | 289.67 *** | ||

| Observations | 1063 | 633 | 430 |

| Farmer Type | Probability of Adopting CRT | ATT | Changes (%) | |

|---|---|---|---|---|

| Digital Finance Users’ Adoption | Non-Users’ Adoption | |||

| Digital finance use | 0.772 (0.005) | 0.257 (0.007) | 0.515 *** (0.005) | 200 |

| Outcome by Estimation Technique | CRT Adoption | Average Treatment Effects on the Treated (ATT) | Changes (%) | |

|---|---|---|---|---|

| Digital Finance Users’ Adoption | Non-Users’ Adoption | |||

| Mean | Mean | Coefficient | ||

| Endogenous Switching Probit | 0.772 | 0.257 | 0.515 *** (0.005) | 200 |

| Propensity Score Matching Nearest neighbor-matching | 0.758 | 0.657 | 0.101 ** (0.051) | 15.37 |

| Radius-matching | 0.758 | 0.589 | 0.169 *** (0.025) | 28.69 |

| Kernel-matching | 0.758 | 0.655 | 0.103 *** (0.048) | 15.73 |

| Grouping Variable | Observations | CRT Adoption | Average Treatment Effects on the Treated (ATT) | Change (%) | ||

|---|---|---|---|---|---|---|

| Digital Finance Users’ Adoption | Non-Users’ Adoption | |||||

| Mean | Mean | Coefficient | ||||

| Age | Low | 517 | 0.806 | 0.700 | 0.106 (0.066) | 15.14 |

| High | 546 | 0.701 | 0.599 | 0.102 * (0.060) | 17.03 | |

| Education | Low | 409 | 0.762 | 0.646 | 0.116 * (0.061) | 17.96 |

| High | 654 | 0.764 | 0.686 | 0.078 (0.067) | 11.37 | |

| Share of agricultural income | Low | 701 | 0.728 | 0.641 | 0.086 * (0.052) | 13.57 |

| High | 363 | 0.825 | 0.612 | 0.213 * (0.117) | 34.80 | |

| Chanel 1 | Chanel 2 | Chanel 3 | ||||

|---|---|---|---|---|---|---|

| Financial CONSTRAINTS (1 = Yes) | CRT Adoption (1 = Yes) | Information Acquisition (1 = Very Little Attention, 5 = A Lot of Attention) | CRT Adoption (1 = Yes) | Social Capital (Yuan) | CRT Adoption (1 = Yes) | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Digital finance use | 0.121 *** (0.036) | 0.104 *** (0.033) | 0.110 *** (0.036) | 0.095 *** (0.032) | 0.097 ** (0.023) | 0.095 *** (0.033) |

| Financial constraints | 0.051 * (0.028) | |||||

| Information Acquisition | 0.135 *** (0.027) | |||||

| Social capital | 0.154 *** (0.044) | |||||

| Constant | −0.339 *** (0.289) | 0.543 ** (0.264) | 2.661 *** (0.295) | −0.165 (0.271) | 0.01 (0.185) | 0.524 ** (0.263) |

| R2 | 0.083 | 0.132 | 0.130 | 0.149 | 0.088 | 0.139 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Z.; Qi, Z.; Tian, Q.; Clark, J.S.; Zhang, Z. The Impact of Digital Finance on Farmers’ Adoption of Eco-Agricultural Technology: Evidence from Rice-Crayfish Co-Cultivation Technology in China. Agriculture 2024, 14, 611. https://doi.org/10.3390/agriculture14040611

Liu Z, Qi Z, Tian Q, Clark JS, Zhang Z. The Impact of Digital Finance on Farmers’ Adoption of Eco-Agricultural Technology: Evidence from Rice-Crayfish Co-Cultivation Technology in China. Agriculture. 2024; 14(4):611. https://doi.org/10.3390/agriculture14040611

Chicago/Turabian StyleLiu, Zhe, Zhenhong Qi, Qingsong Tian, John Stephen Clark, and Zeyu Zhang. 2024. "The Impact of Digital Finance on Farmers’ Adoption of Eco-Agricultural Technology: Evidence from Rice-Crayfish Co-Cultivation Technology in China" Agriculture 14, no. 4: 611. https://doi.org/10.3390/agriculture14040611

APA StyleLiu, Z., Qi, Z., Tian, Q., Clark, J. S., & Zhang, Z. (2024). The Impact of Digital Finance on Farmers’ Adoption of Eco-Agricultural Technology: Evidence from Rice-Crayfish Co-Cultivation Technology in China. Agriculture, 14(4), 611. https://doi.org/10.3390/agriculture14040611