1. Introduction

Shaping prices on agricultural markets is one of the most important problems of modern economies and is the subject of research in the economics of agriculture. It is neither a simple market mechanism nor a fully regulated market. This mechanism is more like a hybrid that combines free market with regulation. The behavior of prices in the agricultural market is different than in the market of industrial goods or services; in particular, they are distinguished by greater price volatility than other markets [

1].

In the early years of research on futures markets, the situation was uncomplicated. It was generally argued that these markets were established to hedge real prices by shifting risk [

2]. There was practically no interest in the speculative function, and hedging was equated with insurance against risk [

3], although it was noted that the role of speculators is significant, and losses of the hedging parties are the premium they pay to speculators for taking the risk [

4,

5,

6].

Until the middle of the last century, the dominant approach was hedging the risk, treating the futures markets as insurance. This approach has gradually evolved towards treating futures markets as a place to make a profit. In 1944 it was argued that future changes in commodity prices were unknown and therefore uncertain, which made regular insurance impossible, but little attention was paid to the profit motive [

7]. However, in 1953, there was fairly loud criticism of the idea of futures markets as a hedge against risk. It has been argued that it is not the motive of hedging against risk that drives investors to the futures markets, but the desire for profit. Investors with certain expectations about future prices try to maximize their profit, which is generated by predicting price fluctuations in the futures market in relation to price fluctuations in the spot market [

8].

The introduction of modern portfolio theory at the turn of the 1950s and 1960s marked the beginning of research on the issue of risk reduction in the theory of the futures market. The portfolio approach sees the one hedging against risk as the person who maximizes the expected utility of a portfolio of spot and futures contracts. According to this theory, the risk manager clearly weighs the risk and the expected return. Using modern portfolio theory, one can objectively justify participants’ motives in futures trading [

9,

10].

Until 1980, the risk hedging theory did not consider alternative risk management instruments. It was considered that futures contracts concluded in organized markets were better than informal forward contracts. Although futures contracts impose certain restrictions, as they are subject to various rules and cannot be applied in every situation, and access to them is not easy for everyone, they are based on the mutual trust of both parties, which is additionally secured by appropriate regulations and conditions. Due to their standardization, futures contracts ensure a high degree of liquidity and eliminate the risk of insolvency. Thus, it was considered that risk reduction could be a motive for their use, but alternative solutions were also indicated.

In general, the essence of the problem concerns the price relationship between the futures and cash markets. The effectiveness of individual futures instruments will largely depend on this relationship. The question of how these markets interact is a subject of ongoing research [

11].

The price of the product to be delivered in the future may be determined in two ways: at the time of concluding a future transaction, on the basis of the price in force on that day on the cash market, or in the process of earlier negotiations, i.e., forward contracts. In practice, the terms of forward contracts are determined by the strength of the counterparties, although as it turns out, the advantage is usually on the side of corporations [

12]. Tensions between enterprises resulting from different transaction preferences can be resolved with the use of services offered on the futures markets. These services can supplement the price element of the transaction so that it becomes mutually acceptable. This could be described as being able to buy or sell products in the future at a fixed price without forcing a monetary transaction [

13]. It can be said that without insurance services, some of the business-to-business transactions would not take place. Thus, transactions on the futures market expand the sales channels and thus affect the effective organization of production [

14].

Risk management in agricultural production is all the more important as the agricultural sector affects other areas of the country’s economy. By means of futures contracts for agricultural products, it is possible to effectively set prices for the future, plan production, manage risk, and minimize the effects of seasonality of production and consumption, which means that the efficiency of investments in agricultural production can be high [

15,

16]. These agreements can contribute to reducing uncertainty in the market of agricultural products and can be an important risk-reduction measure for industries that use agricultural products as raw materials [

17].

Changes taking place in the economic environment, new production technologies, increasing the number of market participants, changes in the demand and supply of agricultural products and increasing international competition require a wider use of futures markets in the agricultural sector. That is why the futures markets in many countries have been created and supported by public institutions. Currently, the dynamic development of the derivatives segment is observed, which is a positive sign of its development, and the importance of these markets in price formation is the subject of research and discussion [

18].

The futures market has two important functions in setting prices and managing the price risk of a given product. These functions are extremely useful for all segments of the economy, in particular for producers who can find out about the likely price at a later date and can therefore choose between different competing commodities and implement those that best meet their future income expectations and will guarantee sales. Likewise, consumers can see at what price the product will be available at a later point in time and choose the right moment to buy it. Futures trading is also useful for exporters as it enables them to secure an export contract [

19].

Futures markets attract investors encouraged by risk management opportunities, but they compete with each other because better positions will be taken by those investors who have more complete market information and the ability to analyze prices in trading the commodities in question. While hedging against price movements, a long-term market perspective is required, while traders or arbitrations prefer the current view of the market. However, all these market users are involved in buying and selling goods, and make their decisions based on various national and global parameters such as price, demand and supply, climatic conditions, and other market information. The resultant of all these reasons for participation in the market and expectations is the price. At the same time, the opportunities offered by the futures market attract a large number of buyers and sellers on these exchanges [

20]. Futures markets offer the possibility of long-term price hedging, while avoiding the immediate purchase of a physical commodity, blocking cash funds, and incurring high storage costs. They will only be able to perform an effective hedging function if they are effective in terms of price formation [

21].

Futures prices rise or fall due to countless factors that influence buyers and sellers’ expectations of what a commodity will be worth at a certain time in the future. If there is new information or there are changes in supply and demand, expectations will also change and the price of the contract will swing up or down. There is some continuity in this pricing process [

22]. On any given day, the contract price will reflect the buyers’ and sellers’ consensus on the future value of the good. New or more accurate information emerging will change these expectations and the price of the contracts will go up or down. Price formation by futures markets is one of the more important economic functions, and even the main economic benefits of these markets. Thanks to this, information on the future value of a commodity is available, and each participant has full access to the same information at the same time [

23]. In theory, therefore, futures markets play an important role in the hedging strategies of companies operating in the real economy.

From the point of view of a hedging strategy, the most important issue is the process of aligning futures and cash prices. This process may be disrupted by various fundamental factors related to the economy and speculative factors related to investors’ decisions. All this means that the process of achieving the equalization of cash and futures prices does not proceed in a straight line. During the quotation period of a given contract, its greater or lesser volatility is observed. Previous studies on the price relationship between futures contracts and cash prices for agricultural products show that unexpected volatility of contract prices causes instability in the cash prices of most commodities. The causality tests showed a two-way flow of information, but the impulses from futures to cash were clearly stronger than those from cash to futures. A stronger flow of impulses from volatility in futures contracts to the cash market is a general pattern in financial markets [

24,

25].

Research carried out for 2000–2008 shows a rather disturbing phenomenon of nonconvergence of spot and futures prices in the maize, soybean, and wheat markets. This inconsistency is highly controversial because of the use of contracts for hedging purposes. The reasons for this state of affairs are seen in the lack of sufficient liquidity on the spot market and the excessive number of open positions on the futures market [

26]. It should be noted, however, that the nonconvergence of spot and futures prices does not necessarily preclude the use of contracts in hedging strategies, because in their case it is enough for the difference between spot and futures prices at the time of contract settlement to be constant.

The situation did not change in the following years (2008–2009). An analysis of the cash prices of grain in more than one hundred locations other than the place of delivery indicated that prices vary with distance from the place of delivery, as theory predicts. Spot prices in different markets took into account transport costs between local suppliers and buyers, but these relationships were disrupted by the discrepancy between futures and spot prices. The lack of convergence of prices between the main place of delivery and the futures market meant that prices in other places also did not converge. These results were explained by the specificity of the futures contract, which, however, undermined the effectiveness of futures markets in conducting hedging strategies and shaping supply prices. Meanwhile, no discrepancy between spot prices and fundamental factors was found, which gave additional grounds to consider the futures market, as opposed to the cash market, as a speculative market [

27].

Subsequent studies also highlighted the problem of price convergence, especially for wheat and, to a lesser extent, for soybeans and maize. To this end, certain decisions have been made to improve the efficiency of price hedging through futures contracts and restore the basic functions of futures markets such as price formation, risk management and inventory allocation over time. The Chicago Board of Trade (CBOT) and the Kansas City Board of Trade (KCBT) have modified their contracts to better reflect market conditions for these products by changing storage rates, strengthening wheat quality requirements, and others that should help improve convergence between expiring futures and money prices [

28].

Research in other agricultural product markets shows similar results. For example, in the coffee market it has been shown that there is a strong correlation between spot prices and futures prices. Moreover, the two main coffee futures markets (Inter-Continental Exchange (ICE) in New York for Arabica and NYSE Liffe Futures and Options in London for Robusta) are closely related to each other, which is reflected in similar movements in futures prices. In addition, the difference between cash and forward prices that serves as the basis for hedging and arbitration is volatile, independent of the price level and the expiry date of the contract, and therefore a source of risk [

29].

Taking into account the above observations, the problems discussed in this study will focus on the relationship between wheat futures contracts on the American market (data from the CBOT exchange) and wheat prices obtained by entrepreneurs on the real market (PPI index of wheat producers). The research will aim to assess the effectiveness of the futures market in terms of discovering prices in the cash market. This is the basis for building a hedging strategy. Monthly nominal data for the period 01.2010–01.2022 were analyzed. The following hypothesis was put forward:

3. Results

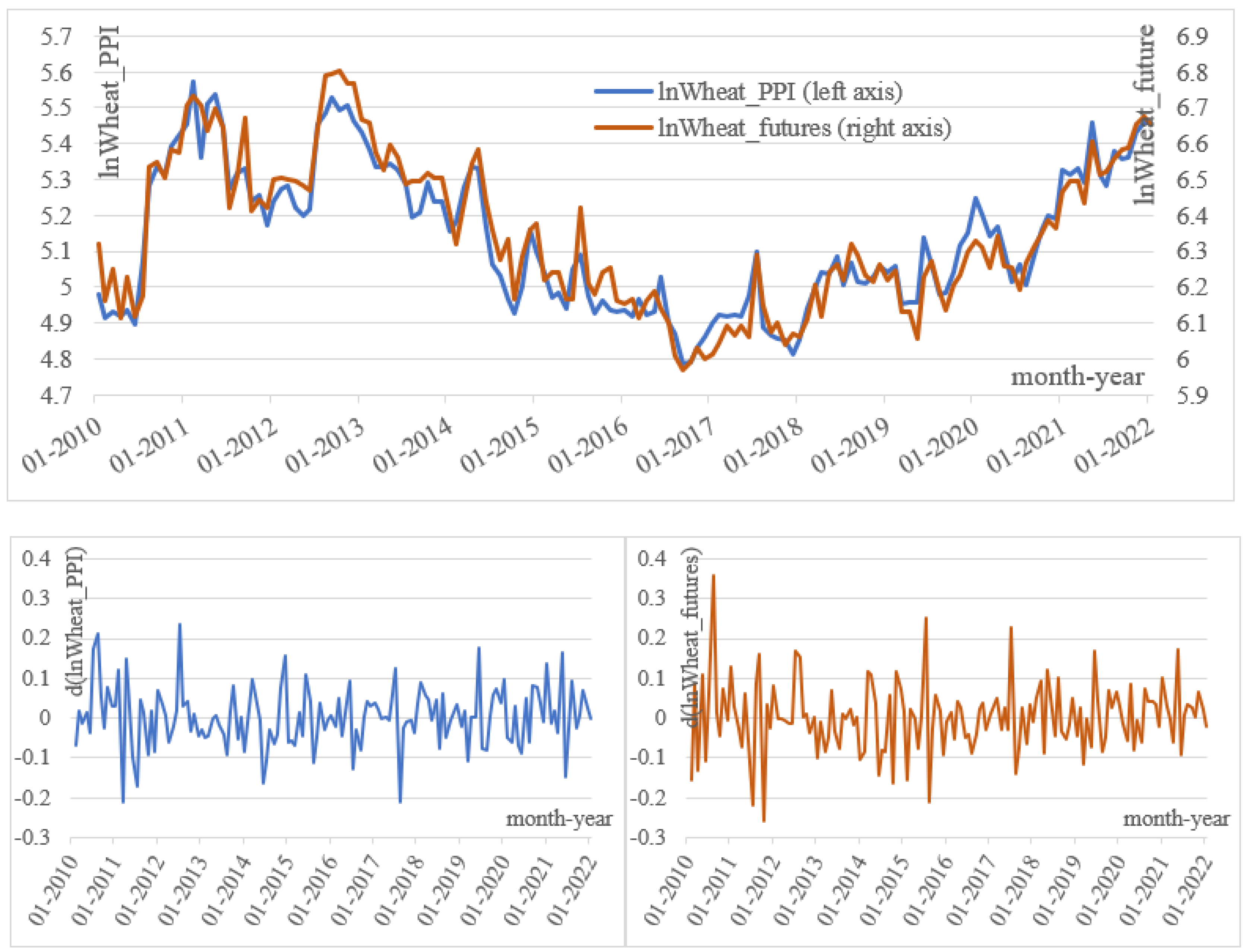

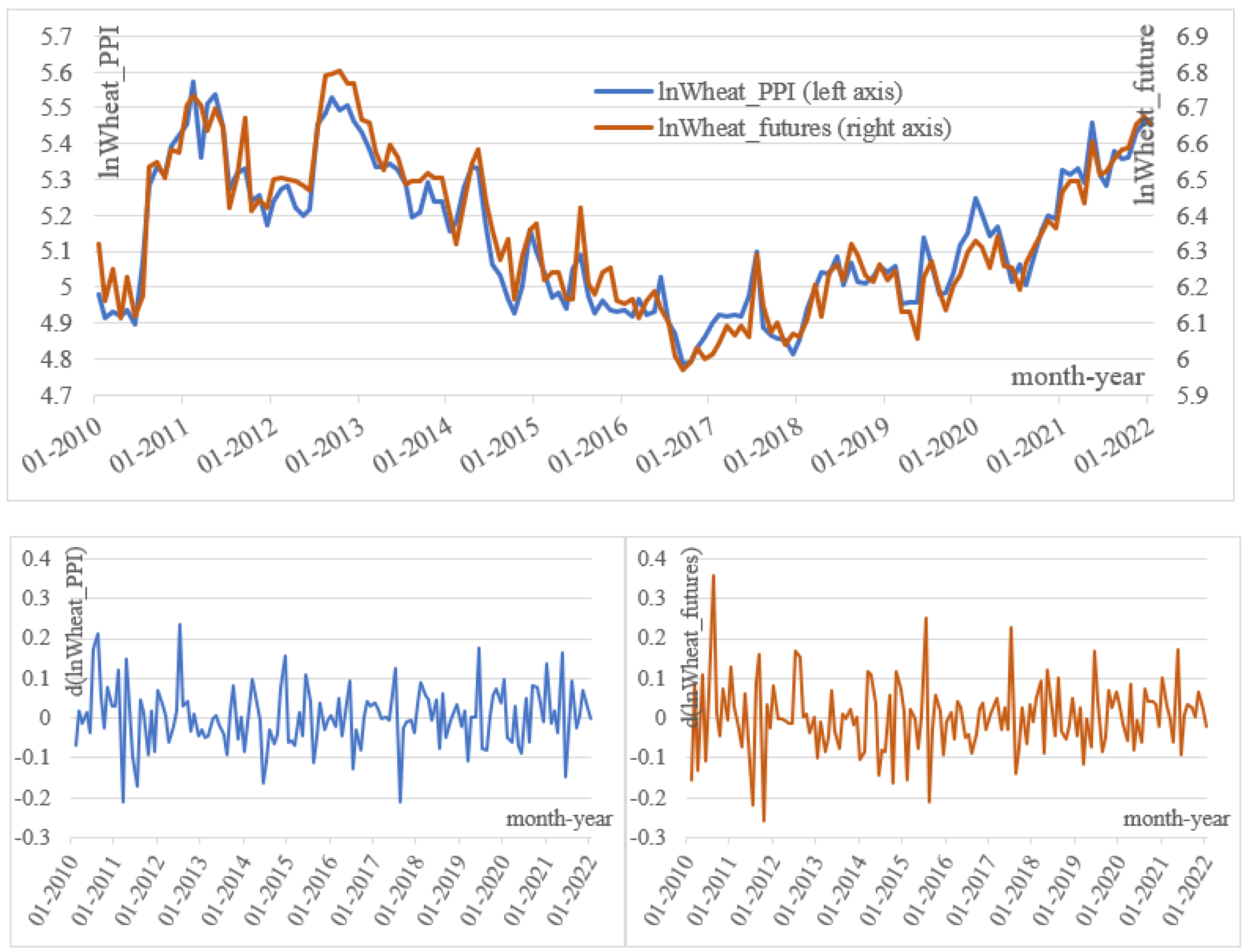

The series of futures prices (

Figure 1) arose from contracts with the highest trading volume. Therefore, it is possible to present data in such a long time series. Futures quotes are quoted in the continuous trading system; here is the first quotation in a given month.

Figure 1 also shows the wheat price PPI. Both series were expressed as logarithms.

There is a very strong relationship between cash prices and futures prices in the chart. These prices are very close to each other, as are the turning points of the periods of rising and falling prices, and the periods of ups and downs coincide at the same time. Generally, very strong long-term relationships can be noticed here.

Less similarity is observed in the series of increments. First of all, the scale of fluctuations is not the same, but also the periods in which extreme fluctuations occur are different. It does not preclude a positive relationship, but it can be seen that in the short term it is clearly weaker than in the long term.

The series of increases in cash and futures prices are described by means of descriptive statistics (

Table 1).

The presented descriptive characteristics show quite important differences in the formation of time series of increases in cash and futures prices. They are quite distinct. First of all, the average monthly change for cash prices is 0.0033 pp, and for futures prices it is much lower and amounted to 0.0023 pp, but cash prices were more stable as their increases were characterized by a lower value of the standard deviation, i.e., 0.0748 pp, and 0.0872 for futures prices. At the same time, the range of min-max volatility of increases in cash prices is smaller than in futures.

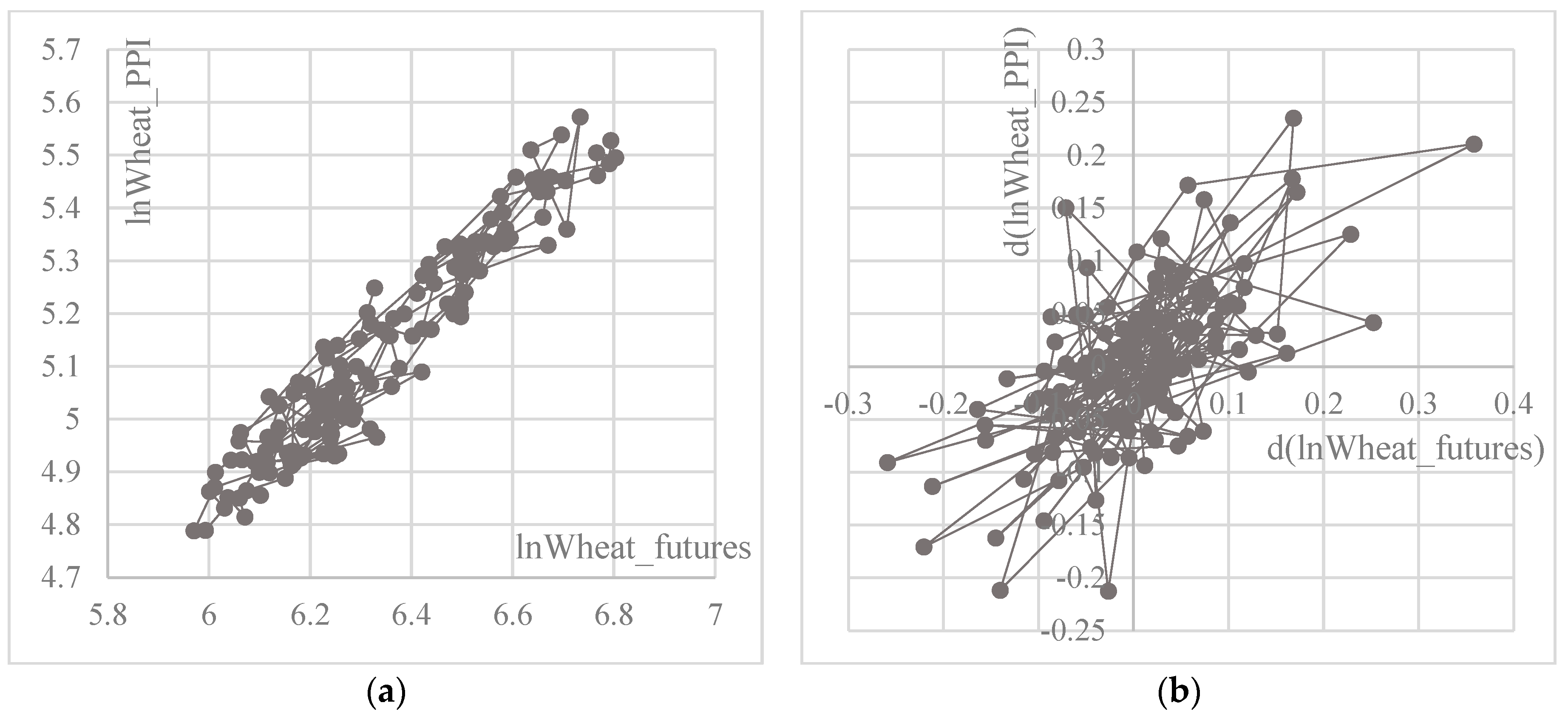

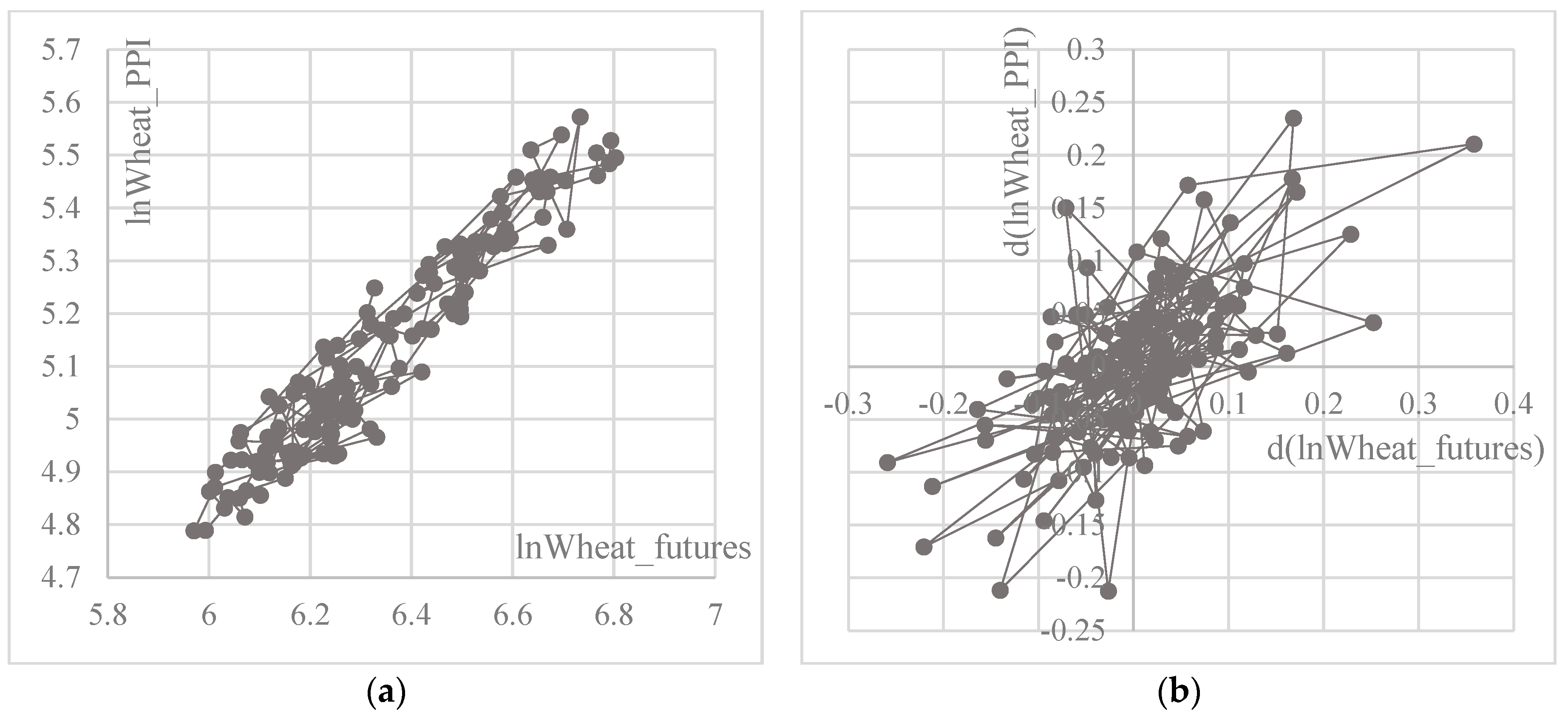

The noticed similarity of the time series of futures and cash prices in

Figure 1 means that there is a strong correlation between the values of these series (

Figure 2a). The value of this relationship, measured with the correlation coefficient, can be estimated at 0.9579. Thus, long-term price trends are strongly consistent.

The situation in the short term is slightly different, which is illustrated by the correlation of the series of price increases (

Figure 2b). This dependence, measured by the correlation coefficient, can be estimated at 0.6373, so it is also positive, but its strength is average. Interestingly, however, the relationship between the increase in cash prices and the increase in futures prices in the next month (cash prices are ahead of futures prices) is 0.2600, while the relationship between the increase in futures prices and the increase in cash prices in the next month (futures prices are ahead of cash prices) is −0.0784. Thus, there is a strong influence from an increase in cash prices to an increase in futures prices. This is the first indication that the stated hypothesis is not true.

The proper modeling of the relationship between wheat futures and cash prices began with the assessment of the stationarity of time series (

Table 2).

The stationarity tests gave a classic result for economic variables. The logarithmized time series of cash prices turn out to be non-stationary series (significance level of the non-stationarity test for cash prices p = 0.8102, and for futures prices 0.8246), while their first differences appear to be stationary (significance level of the non-stationarity test p = 0.0000). Such results suggest that modeling of the relationship should be done on price increments, not levels.

The next stage of the research was to conduct the Granger causality test. Its results may be important in terms of establishing the explanatory and dependent variables (

Table 3). This test was performed for different amounts of lags k (Formulas (1) and (2)). The presented results refer to the situation where k = 1. The results confirm the correlation study, as it turns out that the increases in wheat cash prices are a statistically significant cause of the increase in wheat futures prices (

p = 0.0000). The opposite relationship, i.e., the impact of increases in futures prices on increases in cash prices, was not found (

p = 0.3359).

The adoption of a different value of k changed the significance levels of the test but did not change the impact classification; there was always a one-sided effect from increases in cash prices to increases in futures prices.

The results obtained suggest that futures prices should be more dependent on cash prices than the other way round. This phenomenon will be observed on the basis of the VAR model (

Table 4).

The shaping of cash price increases Y = d(lnWheat_PPI) can be considered independent of delayed increases in futures prices and delayed increases in cash prices, as in each case low values of t-statistics were obtained for the X variables. Thus, what happens month to month with cash prices does not depend on the short-term history of quotations.

The situation is different in the case of increments of futures prices Y = d(lnWheat_futures), where there is a significant dependence on its own lags, and this relationship is negative. In the case of time series of increases in economic variables, negative auto-dependence is expected. However, what is most important from the point of view of research and investment practice is that there is a significant dependence of increases in futures prices on delayed increases in cash prices, and it is a positive relationship. The relationship with a delay of 1 month is very strong, with the regression coefficient being 0.8972, with a t-statistic of 7.9136. Thus, it can be said that increases in futures prices turn out to be a derivative of increases in cash prices.

4. Conclusions

Forecasting crops and prices of cereals is one of the most important problems of food markets [

31]. There are numerous studies that do not agree on the price formation processes as to whether prices in agricultural markets are world or regional [

32]. Different groups of interested parties have different information resources, while entrepreneurs, farmers and financial investors have different knowledge [

33]. The activity of the financial investors is particularly criticized as they are often blamed for speculative trading in futures contracts, which destabilizes the market and leads to higher prices. In this context, it is important to define the process of shaping agricultural commodity prices, and a number of different analytical methods are used [

34,

35].

The following factors are usually highlighted as those which influence wheat price: supply, demand, and stock values [

36]; former wheat price, oil price, and climate factors and exchange rates and stock market parameters [

37]. Futures prices are also cited as the reason for the formation of cash prices, i.e., in line with the idea of futures trading, the futures market should discover future cash prices. Additionally, the far-reaching impacts of a changing climate, the increasing demand for fuels, both traditional and renewable, and the implications of an integrated global economy all play a part in wheat price determination [

38]. All this shapes the broadly understood food security [

39], and today, rising energy prices are the biggest challenge [

40,

41]. The problems that concern food markets, including the wheat market, are therefore very wide, and while the paper presents the problem more narrowly, i.e., the interaction between spot and futures prices is examined, this study is important in the context of the financialization of agricultural markets.

The obtained results unambiguously allow us to conclude that the time series of futures contracts are influenced by cash prices of wheat. The obtained conclusion is statistically significant. Thus, the hypothesis that the wheat futures market is the cause of price formation in the wheat cash market has been verified negatively.

Wheat futures prices are assumed to show the expectations of market participants as to future cash prices. Thus, if market participants expect that there will be a surplus of wheat in the future, prices should fall, and if there is a shortage, futures prices should rise. In contrast, cash prices should depend on current supply and demand. Thus, futures prices should be ahead of cash prices. Such results have been obtained in many studies, some of which were quoted in the introduction. The research carried out here shows that it is otherwise, because it is cash prices, or more precisely, increases in cash prices, that precede changes in futures prices.

One may wonder where these results come from, and whether they are not accidental. It should be noted here that due to statistical significance, it is difficult to call them accidental. Moreover, some studies conducted in the past showed that the relationship between the futures market and the cash market may be two-sided, though there were also those that found a similar conclusion to this study: the cash market is the cause of the futures market. First, it is worth considering whether it is true that today’s cash price is actually a reflection of the current supply and demand, and whether it is balancing the current supply and demand, in accordance with economic principles. Perhaps entrepreneurs buying grain as well as agricultural producers, who are aware of how large the stocks are and what time is left until the next harvest, adjust prices based on this information and not the current supply and demand. In such a situation, the cash price essentially expresses expectations about the future. This view seems to be rational. The second thing is that the futures market is increasingly becoming a speculative market in which financial institutions, rather than processors and agricultural producers, play the dominant role. For speculators, the cash price can be an indicator of value and they base their investment decisions on it. In such a setting, the futures market would lose its original hedging function.

{kind=link}

{kind=link}