Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study

,

,  , ,

, ,  , and

, and

Abstract

1. Introduction

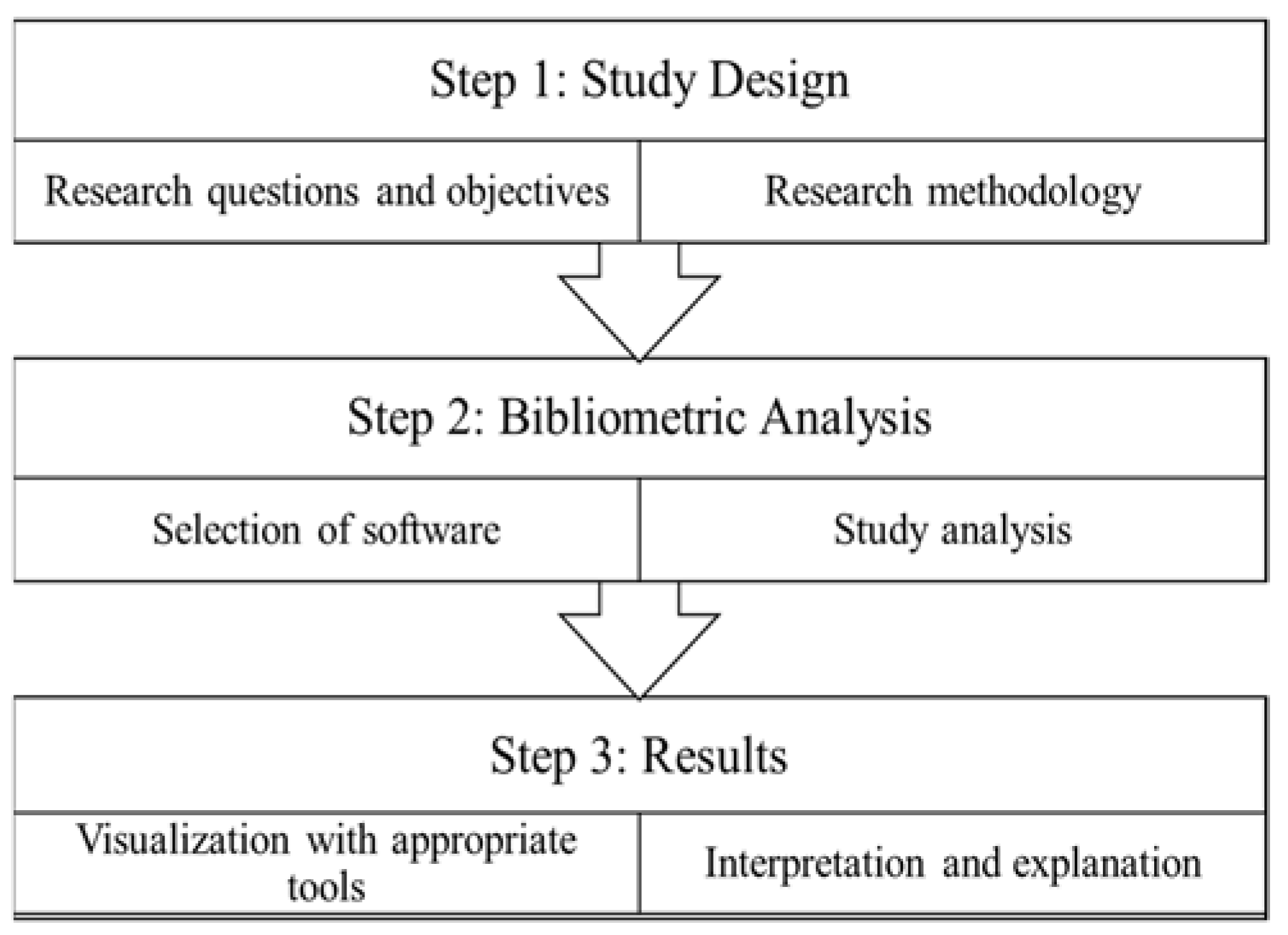

2. Study Design and Descriptive Outlook

3. Bibliometric Analysis

3.1. Influential Aspects

3.1.1. Core Sources

3.1.2. Influential Authors in Fintech Literature

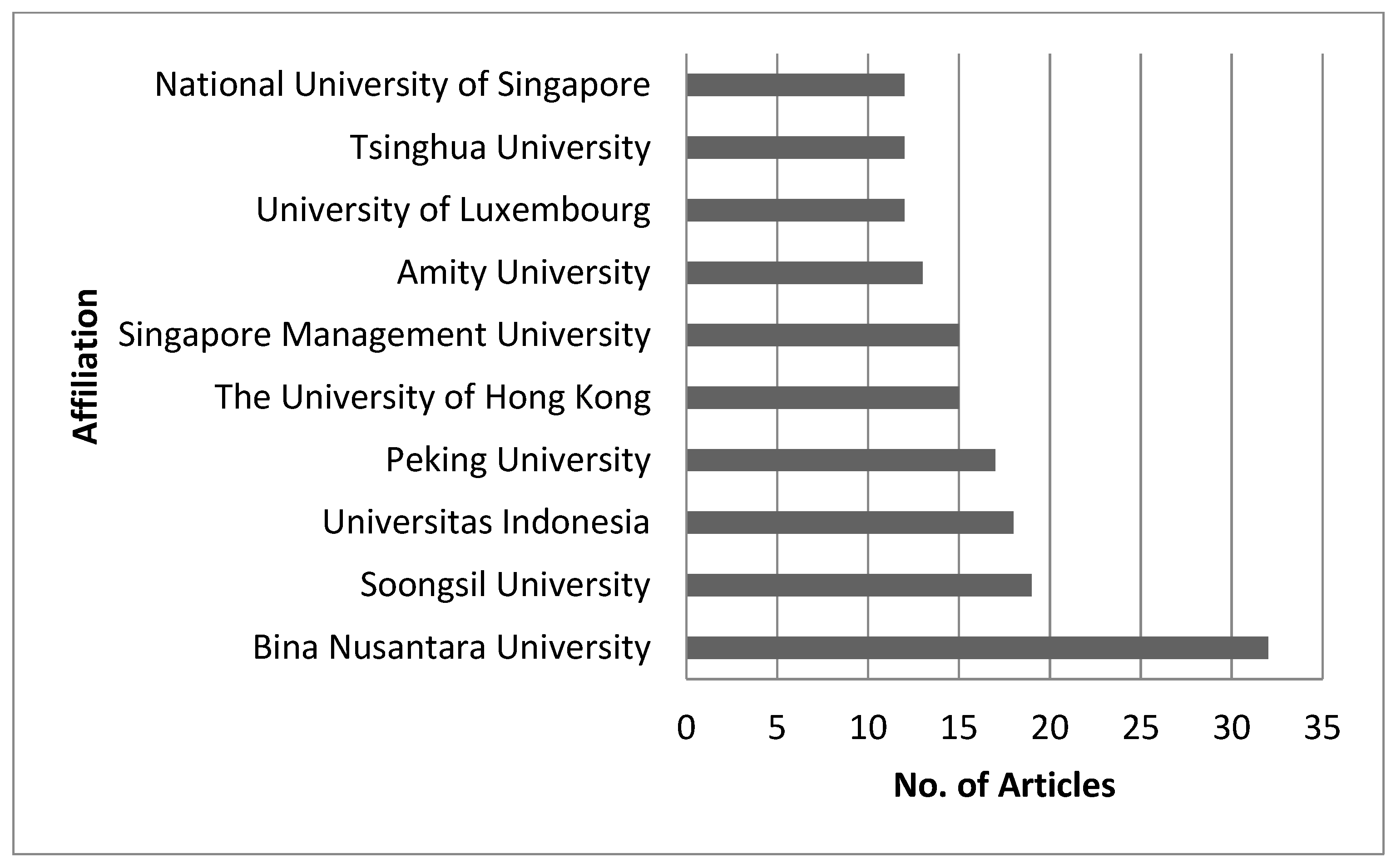

3.1.3. Most Relevant Affiliations

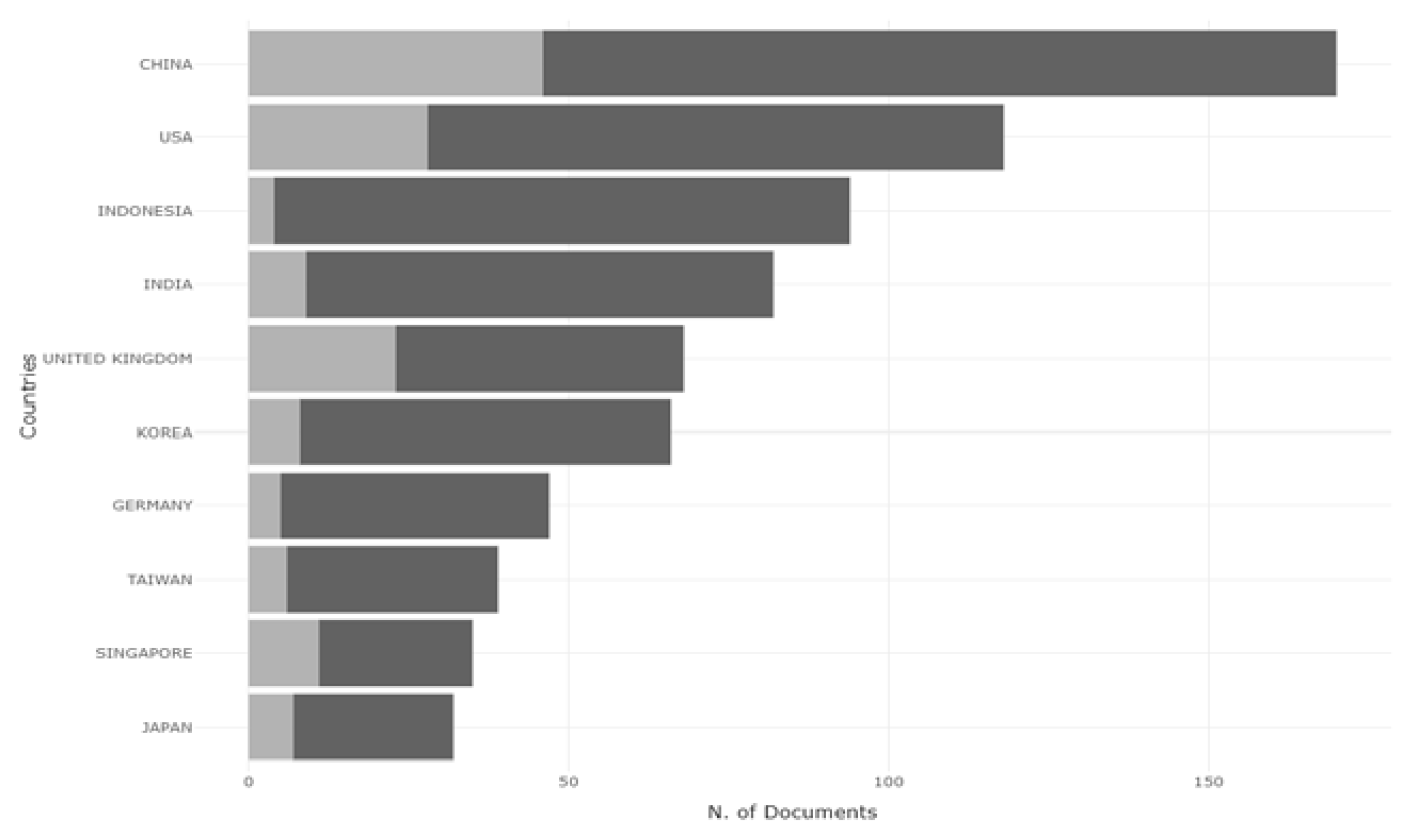

3.1.4. Influential Countries

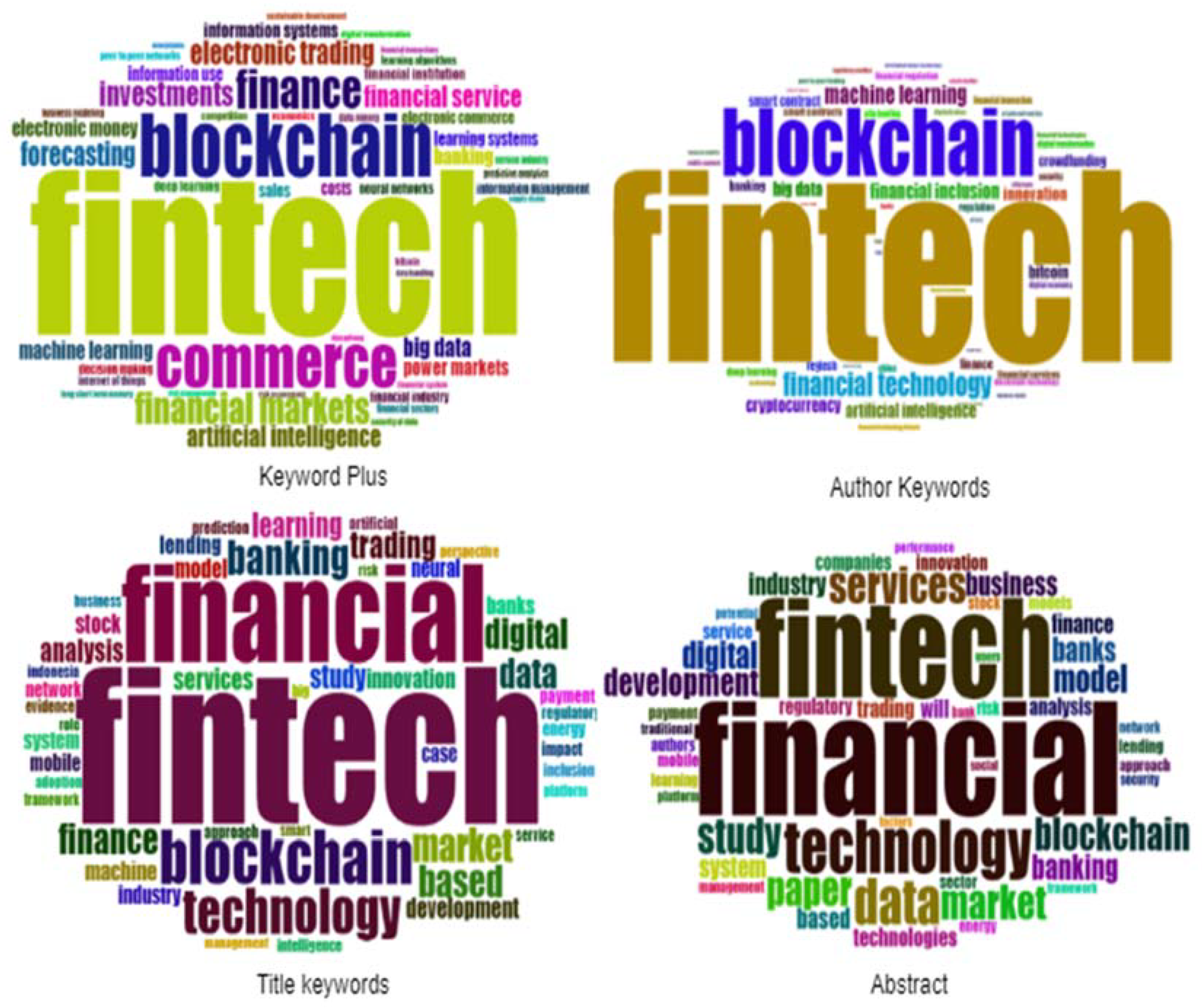

3.1.5. Keyword Analysis

3.2. Conceptual Framework

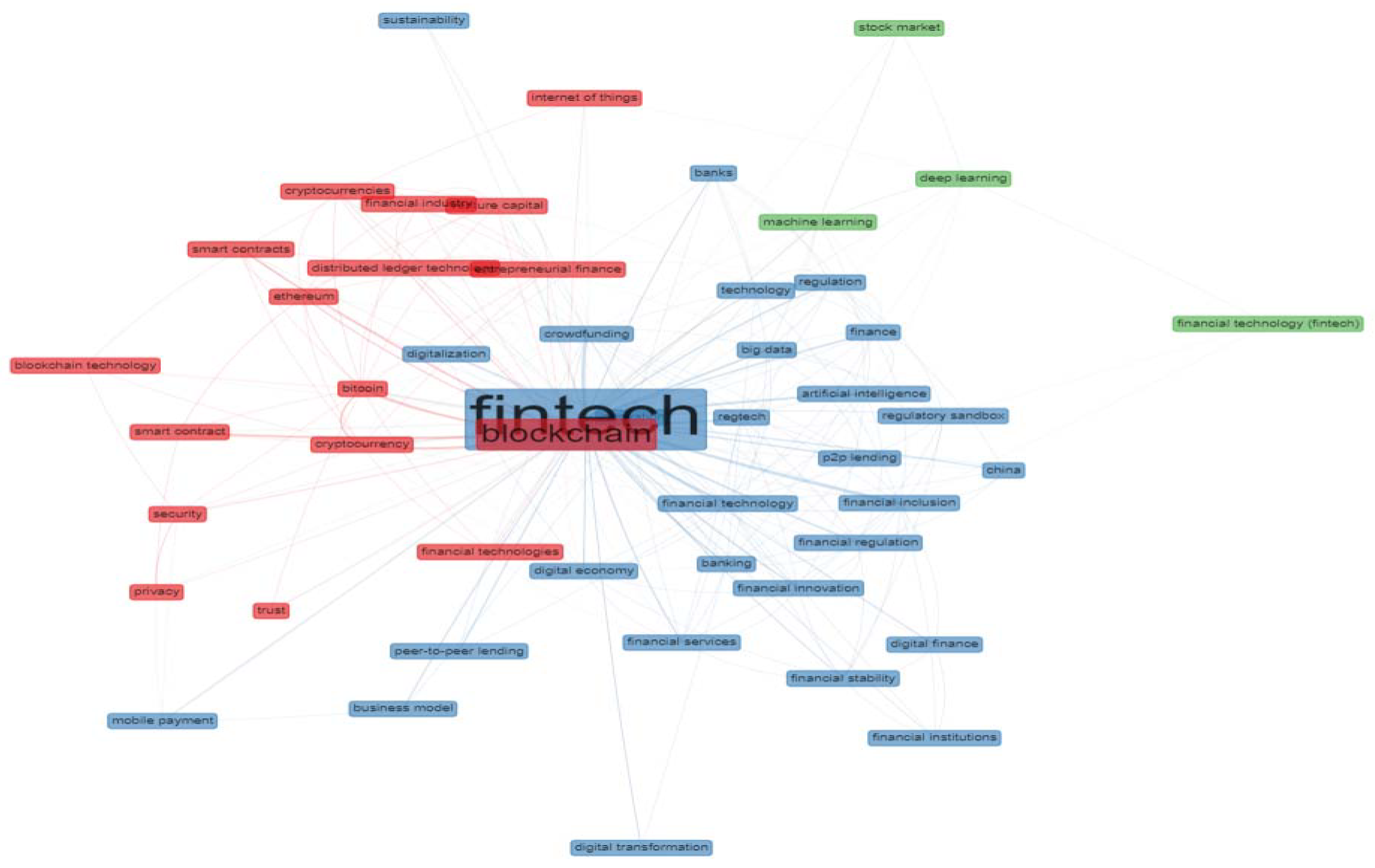

3.2.1. Co-Occurrence Network

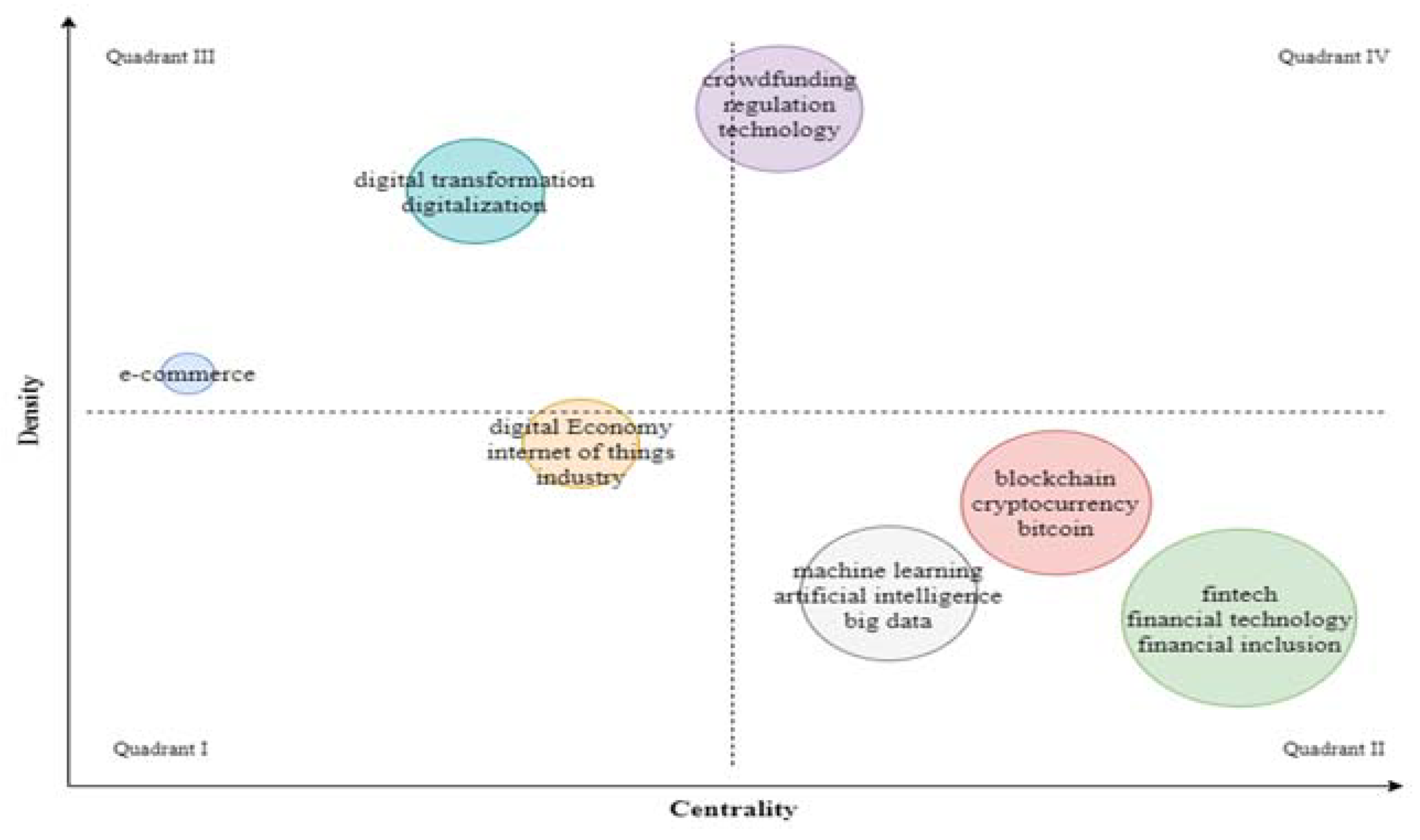

3.2.2. Thematic Map

4. Future Research

- Using financial technology to achieve sustainable development goals;

- Identify limitations and proliferate industry 4.0 with the internet of things, blockchain, and digital transformation mechanism;

- Will the world see fintech as the opportunity for a new era after the COVID-19 outbreak, or are there challenges ahead;

- Ecommerce proliferation: gap-filling regarding government regulations regarding online payments, supply chain management, blockchain and bitcoin penetration, product differentiation, logistic financial methods, fraud detection, safety policies, law enforcement, ease of startups, and reshaping financial orders;

- Identify and implement various crowdfunding techniques such as blockchain and bitcoin investment with proper regulations to fund multiple new ventures;

- Implementing fintech tools in Islamic banking and finance. Digital transformation of Islamic instruments such as Mudarabah, Musharakah, Islisna, Salam, Ijarah, Sukuk, and Takaful;

- In developing models, applications of fintech technologies, especially blockchains, ensure standard recording, reporting, and companies’ disclosure requirements such as technological transformation regarding corporate governance-related recordings [123];

- Using fintech, such as machine learning and neural networks tools, develops banking operations such as know-your-customer, risk management, and forecasting;

- Identify opportunities, gaps, and challenges for implementing and developing regulatory technology.

5. Limitation of Study

- The search query is conducted at one point in time, i.e., 17 March 2021; this is a limitation because these studies may change as new literature may be added on future dates.

- There is limited literature available on fintech literature related to social and environmental sciences. More literature will refine the concept.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Qi, B.Y.; Xiao, J. Fintech: AI powers financial services to improve people’s lives. Commun. ACM 2018, 61, 65–69. [Google Scholar] [CrossRef]

- Wang, Y.; Sui, X.P.; Zhang, Q. Can fintech improve the efficiency of commercial banks?—An analysis based on big data. Res. Int. Bus. Financ. 2021, 55, 101338. [Google Scholar] [CrossRef]

- Dranev, Y.; Frolova, K.; Ochirova, E. The impact of fintech M&A on stock returns. Res. Int. Bus. Financ. 2019, 48, 353–364. [Google Scholar] [CrossRef]

- Legowo, M.B.; Subanidja, S.; Sorongan, F.A. Fintech and bank: Past, present, and future. J. Tek. Komput. 2021, 7, 94–99. [Google Scholar] [CrossRef]

- Puschmann, T. Fintech. Bus. Inf. Syst. Eng. 2017, 59, 69–76. [Google Scholar] [CrossRef]

- Nüesch, R.; Alt, R.; Puschmann, T. Hybrid customer interaction. Bus. Inf. Syst. Eng. 2015, 57, 73–78. [Google Scholar] [CrossRef]

- Martínez-Plumed, F.; Gómez, E.; Hernández-Orallo, J. Futures of artificial intelligence through technology readiness levels. Telemat. Inform. 2021, 58, 101525. [Google Scholar] [CrossRef]

- Veilleux, M.; Sénécal, S.; Demolin, B.; Bouvier, F.; Di Fabio, M.-L.; Coursaris, C.; Léger, P.-M. Visualizing a user’s cognitive and emotional journeys: A fintech case. In Design, User Experience, and Usability. Interaction Design; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; Volume 12200, pp. 549–566. [Google Scholar] [CrossRef]

- Rabhi, F.A.; Mehandjiev, N.; Baghdadi, A. State-of-the-Art in Applying Machine Learning to Electronic Trading. In Enterprise Applications, Markets and Services in the Finance Industry; Lecture Notes in Business Information Processing; Springer: Cham, Switzerland, 2020; Volume 401, pp. 3–20. [Google Scholar] [CrossRef]

- Li, W.; Bao, R.; Harimoto, K.; Chen, D.; Xu, J.; Su, Q. Modeling the stock relation with graph network for overnight stock movement prediction. In Proceedings of the IJCAI International Joint Conference on Artificial Intelligence, Yokohama, Japan, 11–17 July 2020; pp. 4541–4547. [Google Scholar]

- Oprea, S.-V.; Bara, A.; Andreescu, A.I. Two Novel Blockchain-Based Market Settlement Mechanisms Embedded into Smart Contracts for Securely Trading Renewable Energy. IEEE Access 2020, 8, 212548–212556. [Google Scholar] [CrossRef]

- Erosa, V.E. Online Money Flows: Exploring the Nature of the Relation of Technology’s New Creature to Money Supply—A Suggested Conceptual Framework and Research Propositions. Am. J. Ind. Bus. Manag. 2018, 8, 250–305. [Google Scholar] [CrossRef][Green Version]

- Broto Legowo, M.; Subanija, S.; Sorongan, F.A. Role of FinTech mechanism to technological innovation: A conceptual framework. Int. J. Innov. Sci. Res. Technol. 2020, 5, 1–6. [Google Scholar]

- Nasir, A.; Shaukat, K.; Hameed, I.A.; Luo, S.; Alam, T.M.; Iqbal, F. A Bibliometric Analysis of Corona Pandemic in Social Sciences: A Review of Influential Aspects and Conceptual Structure. IEEE Access 2020, 8, 133377–133402. [Google Scholar] [CrossRef]

- Aria, M.; Cuccurullo, C. Bibliometrix: An R-tool for comprehensive science mapping analysis. J. Informetr. 2017, 11, 959–975. [Google Scholar] [CrossRef]

- Salameh, A.; Bass, J.M. Heterogeneous Tailoring Approach Using the Spotify Model. In ACM International Conference Proceeding Series; Association for Computing Machinery: New York, NY, USA, 2020; pp. 293–298. [Google Scholar]

- Kumarathunga, M.; Calheiros, R.; Ginige, A. Towards Trust Enabled Commodity Market for Farmers with Blockchain Smart Contracts. In ACM International Conference Proceeding Series; Association for Computing Machinery: New York, NY, USA, 2020; pp. 75–82. [Google Scholar]

- Paulson-Luna, M.; Reily, K. The Financial Derivative Ecosystem is Old-Decentralized Ledger Technology is its Fountain of Youth. In ACM International Conference Proceeding Series; Association for Computing Machinery: New York, NY, USA, 2020; pp. 105–112. [Google Scholar]

- Chakravaram, V.; Ratnakaram, S.; Vihari, N.S.; Tatikonda, N. The Role of Technologies on Banking and Insurance Sectors in the Digitalization and Globalization Era—A Select Study. Adv. Intell. Syst. Comput. 2021, 1245, 145–156. [Google Scholar] [CrossRef]

- Nam, G. Bringing the QR Code to Canada: The Rise of AliPay and WeChatPay in Canadian e-Commerce Markets. Adv. Intell. Syst. Comput. 2021, 1290, 622–628. [Google Scholar] [CrossRef]

- Rao, V.; Singh, A.; Rudra, B. Ethereum Blockchain Enabled Secure and Transparent E-Voting. Adv. Intell. Syst. Comput. 2021, 1290, 683–702. [Google Scholar] [CrossRef]

- Xu, L.; Lu, X.; Yang, G.; Shi, B. Identifying fintech innovations with patent data: A combination of textual analysis and machine-learning techniques. In Sustainable Digital Communities; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; Volume 12051, pp. 835–843. [Google Scholar] [CrossRef]

- Mamonov, S. The Role of Information Technology in Fintech Innovation: Insights from the New York City Ecosystem. Responsible Des. Implement. Use Inf. Commun. Technol. 2020, 12066, 313–324. [Google Scholar] [CrossRef]

- Li, L.; Zhao, T.; Xie, Y.; Feng, Y. Interpretable Machine Learning Based on Integration of NLP and Psychology in Peer-to-Peer Lending Risk Evaluation. In Natural Language Processing and Chinese Computing; Zhu, X., Zhang, M., Hong, Y., He, R., Eds.; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; pp. 429–441. [Google Scholar]

- Liu, B.; Wang, M.; Men, J.; Yang, D. Microgrid Trading Game Model Based on Blockchain Technology and Optimized Particle Swarm Algorithm. IEEE Access 2020, 8, 225602–225612. [Google Scholar] [CrossRef]

- Masaud, T.M.; Warner, J.; El-Saadany, E.F. A Blockchain-Enabled Decentralized Energy Trading Mechanism for Islanded Networked Microgrids. IEEE Access 2020, 8, 211291–211302. [Google Scholar] [CrossRef]

- Liao, C.-H.; Lin, H.-E.; Yuan, S.-M. Blockchain-Enabled Integrated Market Platform for Contract Production. IEEE Access 2020, 8, 211007–211027. [Google Scholar] [CrossRef]

- Chen, R.R.; Chen, K. A 2020 perspective on “Information asymmetry in initial coin offerings (ICOs): Investigating the effects of multiple channel signals”. Electron. Commer. Res. Appl. 2020, 40, 100936. [Google Scholar] [CrossRef]

- Jocevski, M.; Ghezzi, A.; Arvidsson, N. Exploring the growth challenge of mobile payment platforms: A business model perspective. Electron. Commer. Res. Appl. 2020, 40, 100908. [Google Scholar] [CrossRef]

- Ferrer-Gomila, J.-L.; Hinarejos, M.F. A 2020 perspective on “A fair contract signing protocol with blockchain support”. Electron. Commer. Res. Appl. 2020, 42, 100981. [Google Scholar] [CrossRef]

- Tritto, A.; He, Y.; Junaedi, V.A. Governing the gold rush into emerging markets: A case study of Indonesia’s regulatory responses to the expansion of Chinese-backed online P2P lending. Financ. Innov. 2020, 6, 51. [Google Scholar] [CrossRef]

- Yan, J.; Yu, W.; Zhao, J.L. How signaling and search costs affect information asymmetry in P2P lending: The economics of big data. Financ. Innov. 2015, 1, 19. [Google Scholar] [CrossRef]

- Li, Y.; Spigt, R.; Swinkels, L. The impact of FinTech startups on incumbent retail banks’ share prices. Financ. Innov. 2017, 3, 26. [Google Scholar] [CrossRef]

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and Financial Inclusion. Eur. Bus. Organ. Law Rev. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Arner, D.W.; Zetzsche, D.A.; Buckley, R.P.; Barberis, J.N. The Identity Challenge in Finance: From Analogue Identity to Digitized Identification to Digital KYC Utilities. Eur. Bus. Organ. Law Rev. 2019, 20, 55–80. [Google Scholar] [CrossRef]

- Donald, D.C. Smart Precision Finance for Small Businesses Funding. Eur. Bus. Organ. Law Rev. 2020, 21, 199–217. [Google Scholar] [CrossRef]

- Donald, D.C. Hong Kong’s fintech automation: Economic benefits and social risks. In Regulating FinTech in Asia; Perspectives in Law, Business and Innovation; Springer: Singapore, 2020; pp. 31–50. [Google Scholar] [CrossRef]

- Arner, D.W.; Barberis, J.; Buckley, R.P. FinTech, regTech, and the reconceptualization of financial regulation. Northwest J. Int. Law Bus. 2017, 37, 373–415. [Google Scholar]

- Arner, D.W.; Barberis, J.; Buckley, R.P. RegTech: Building a Better Financial System. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Buckley, R.P.; Arner, D.W.; Zetzsche, D.A.; Selga, E.K. Techrisk. Singap. J. Leg. Stud. 2020, pp. 35–62. Available online: http://hub.hku.hk/handle/10722/293372 (accessed on 2 September 2021).

- Buckley, R.P.; Arner, D.W.; Zetzsche, D.A.; Weber, R.H. The road to RegTech: The (astonishing) example of the European Union. J. Bank. Regul. 2020, 21, 26–36. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Kauffman, R.J.; Kim, K.; Lee, S.-Y.T.; Hoang, A.-P.; Ren, J. Combining machine-based and econometrics methods for policy analytics insights. Electron. Commer. Res. Appl. 2017, 25, 115–140. [Google Scholar] [CrossRef]

- Kauffman, R.J.; Ma, D. Special issue: Contemporary research on payments and cards in the global fintech revolution. Electron. Commer. Res. Appl. 2015, 14, 261–264. [Google Scholar] [CrossRef]

- Adhami, S.; Giudici, G.; Martinazzi, S. Why do businesses go crypto? An empirical analysis of initial coin offerings. J. Econ. Bus. 2018, 100, 64–75. [Google Scholar] [CrossRef]

- History | BINUS UNIVERSITY. Available online: https://binus.ac.id/history/ (accessed on 2 September 2021).

- Richard; Heryadi, Y.; Lukas; Trisetyarso, A. Leverage from Blockchain in Commodity Exchange: Asset-Backed Token with Ethereum Blockchain Network and Smart Contract. In Smart Trends in Computing and Communications: Proceedings of SmartCom 2020; Zhang, Y.-D., Senjyu, T., So-In, C., Joshi, A., Eds.; Smart Innovation, Systems and Technologies; Springer: Singapore, 2021; pp. 301–309. [Google Scholar]

- Yuniarti, S.; Rasyid, A. Consumer Protection in Lending Fintech Transaction in Indonesia: Opportunities and Challenges. Phys. Conf. Ser. 2020, 1477, 052016. [Google Scholar] [CrossRef]

- Candra, S.; Nuruttarwiyah, F.; Hapsari, I.H. Revisited the Technology Acceptance Model with E-Trust for Peer-to-Peer Lending in Indonesia (Perspective from Fintech Users). Int. J. Technol. 2020, 11, 710–721. [Google Scholar] [CrossRef]

- Abdullah, E.M.E.; Rahman, A.A.; Rahim, R.A. Adoption of financial technology (Fintech) in mutual fund/ unit trust investment among Malaysians: Unified Theory of Acceptance and Use of Technology (UTAUT). Int. J. Eng. Technol. 2018, 7, 110–118. [Google Scholar] [CrossRef]

- Yohanes, K.; Junius, K.; Saputra, Y.; Sari, R.; Lisanti, Y.; Luhukay, D. Unified Theory of Acceptance and Use of Technology (UTAUT) model perspective to enhance user acceptance of fintech application. In Proceedings of the 2020 International Conference on Information Management and Technology, ICIMTech 2020, Bandung, Indonesia, 13–14 August 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 643–648. [Google Scholar]

- Soongsil University. Available online: http://www.ssu.ac.kr/web/eng/home (accessed on 2 September 2021).

- Kim, J.-H.; Jo, S.-I.; Hong, S.-W.; Gim, G.-Y. Small foreign currency remittance based on block chain in Korea and Vietnam. Asia Life Sci. 2019, pp. 57–67. Available online: https://scholarworks.bwise.kr/ssu/handle/2018.sw.ssu/34793 (accessed on 2 September 2021).

- La, H.J.; Kim, S.D. A machine learning framework for adaptive FinTech security provisioning. J. Internet Technol. 2018, 19, 1545–1553. [Google Scholar] [CrossRef]

- Lee, H.J.; Han, K.S. A study on mobile easy payment service based on fintech to reduce smart divide and income gap. Int. J. Adv. Sci. Technol. 2018, 116, 35–48. [Google Scholar] [CrossRef]

- Tran, T.A.; Han, K.S.; Yun, S.Y. Factors influencing the intention to use mobile payment service using fintech systems: Focused on Vietnam. Asia Life Sci. 2018, pp. 1731–1747. Available online: https://scholarworks.bwise.kr/ssu/handle/2018.sw.ssu/34383 (accessed on 2 September 2021).

- Lee, S. Evaluation of mobile application in user’s perspective: Case of P2P lending apps in FinTech industry. KSII Trans. Internet Inf. Syst. 2017, 11, 1105–1115. [Google Scholar] [CrossRef]

- Asmarani, S.C.; Wijaya, C. Effects of fintech on stock return: Evidence from retail banks listed in Indonesia stock exchange. J. Asian Financ. Econ. Bus. 2020, 7, 95–104. [Google Scholar] [CrossRef]

- Yulianita Gitaharie, B.; Abbas, Y.; Dewi, M.K.; Handayani, D. Research on Firm Financial Performance and Consumer Behavior; Nova Science Publishers, Inc.: Hauppauge, NY, USA, 2020. [Google Scholar]

- Saputra, A.D.; Burnia, I.J.; Shihab, M.R.; Anggraini, R.S.A.; Purnomo, P.H.; Azzahro, F. Empowering Women Through Peer to Peer Lending: Case Study of Amartha.com. In Proceedings of the 2019 International Conference on Information Management and Technology, ICIMTech 2019, Jakarta/Bali, Indonesia, 19–20 August 2019; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2019; pp. 618–622. [Google Scholar]

- Nasir, A.; Shaukat, K.; Khan, K.I.; Hameed, I.A.; Alam, T.M.; Luo, S. What is core and what future holds for blockchain technologies and cryptocurrencies: A bibliometric analysis. IEEE Access 2021, 9, 989–1004. [Google Scholar] [CrossRef]

- Michaels, L.; Homer, M. Regulation and Supervision in a Digital and Inclusive World. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Birch, D.G.W.; Parulava, S. Ambient Accountability: Shared Ledger Technology and Radical Transparency for Next Generation Digital Financial Services. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Ebenhoch, P. Blockchain Compliance. Jusletter IT. 2018. Available online: https://jusletter-it.weblaw.ch/en/issues/2018/IRIS/blockchain-complianc_04fc310f86.html__ONCE&login=false (accessed on 2 September 2021).

- Tsai, C.-H.; Peng, K.-J. The FinTech Revolution and Financial Regulation: The Case of Online Supply-Chain Financing. Asian J. Law Soc. 2017, 4, 109–132. [Google Scholar] [CrossRef]

- Fan, P.S. Singapore Approach to Develop and Regulate FinTech. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Fenwick, M.; Vermeulen, E.P.M.; Corrales, M. Business and regulatory responses to artificial intelligence: Dynamic regulation, innovation ecosystems and the strategic management of disruptive technology. In Robotics, AI and the Future of Law; Perspectives in Law, Business and Innovation; Springer: Singapore, 2018; pp. 81–103. [Google Scholar] [CrossRef]

- Fenwick, M.; Kaal, W.A.; Vermeulen, E.P.M. Regulation tomorrow: Strategies for regulating new technologies. In Transnational Commercial and Consumer Law; Perspectives in Law, Business and Innovation; Springer: Singapore, 2018; pp. 153–174. [Google Scholar] [CrossRef]

- Gerlach, J.M.; Rugilo, D. The predicament of fintechs in the environment of traditional banking sector regulation—An analysis of regulatory sandboxes as a possible solution. Credit Cap. Mark. 2019, 52, 323–373. [Google Scholar] [CrossRef]

- Sangwan, V.; Harshita; Prakash, P.; Singh, S. Financial technology: A review of extant literature. Stud. Econ. Financ. 2020, 37, 71–88. [Google Scholar] [CrossRef]

- Makarov, V.O.; Davydova, M.L. On the concept of regulatory sandboxes. In “Smart Technologies” for Society, State and Economy. ISC 2020; Lecture Notes in Networks and Systems; Springer: Cham, Switzerland, 2021; pp. 1014–1020. [Google Scholar]

- Liao, F. Does china need the regulatory sandbox? A preliminary analysis of its desirability as an appropriate mechanism for regulating fintech in China. In Regulating FinTech in Asia; Perspectives in Law, Businsess and Innovation; Springer: Singapore, 2020; pp. 81–95. [Google Scholar] [CrossRef]

- Le, T.N.-L.; Abakah, E.J.A.; Tiwari, A.K. Time and frequency domain connectedness and spill-over among fintech, green bonds and cryptocurrencies in the age of the fourth industrial revolution. Technol. Forecast. Soc. Chang. 2021, 162, 120382. [Google Scholar] [CrossRef]

- Petrov, N.A. Main Trends in the Market of Electronic Financial Services in Russia. In Economic Systems in the New Era: Stable Systems in an Unstable World. IES 2020; Ashmarina, S.I., Horak, J., Vrbka, J., Suler, P., Eds.; Lecture Notes in Networks and Systems; Springer: Cham, Switzerland, 2021; pp. 708–712. [Google Scholar]

- Teeluck, R.; Durjan, S.; Bassoo, V. Blockchain technology and emerging communications applications. In Security and Privacy Applications for Smart City Development; Studies in Systems, Decision and Control; Springer: Cham, Switzerland, 2021; pp. 207–256. [Google Scholar]

- Mbodji, F.N.; Mendy, G.; Mbacke, A.B.; Ouya, S. Proof of concept of blockchain integration in P2P lending for developing countries. In Infrastructure and e-Services for Developing Countries. AFRICOMM 2019; Zitouni, R., Agueh, M., Houngue, P., Soude, H., Eds.; Lecture Notes of the Institute for Computer Sciences, Social-Informatics and Telecommunications Engineering; Springer: Cham, Switzerland, 2020; pp. 59–70. [Google Scholar]

- Hu, Z.; Du, Y.; Rao, C.; Goh, M. Delegated Proof of Reputation Consensus Mechanism for Blockchain-Enabled Distributed Carbon Emission Trading System. IEEE Access 2020, 8, 214932–214944. [Google Scholar] [CrossRef]

- De Oliveira, A.D.C.M.; Pinto, P.F.A.; Colcher, S. Stocks Clustering Based on Textual Embeddings for Price Forecasting. In Intelligent Systems. BRACIS 2020; Cerri, R., Prati, R.C., Eds.; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; pp. 665–678. [Google Scholar]

- Abe, M.; Nakagawa, K. Deep Learning for Multi-factor Models in Regional and Global Stock Markets. In New Frontiers in Artificial Intelligence. JSAI-isAI 2019; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; Volume 12331, pp. 87–102. [Google Scholar] [CrossRef]

- Nabipour, M.; Nayyeri, P.; Jabani, H.; Shahab, S.; Mosavi, A. Predicting Stock Market Trends Using Machine Learning and Deep Learning Algorithms Via Continuous and Binary Data; A Comparative Analysis. IEEE Access 2020, 8, 150199–150212. [Google Scholar] [CrossRef]

- Chen, Y.; Liu, K.; Xie, Y.; Hu, M. Financial Trading Strategy System Based on Machine Learning. Math. Probl. Eng. 2020, 2020, 3589198. [Google Scholar] [CrossRef]

- Obthong, M.; Tantisantiwong, N.; Jeamwatthanachai, W.; Wills, G. A survey on machine learning for stock price prediction: Algorithms and techniques. In Proceedings of the FEMIB 2020—2nd International Conference on Finance, Economics, Management and IT Business, Prague, Czech Republic, 5–6 May 2020; SciTePress: Prague, Czech Republic, 2020; pp. 63–71. [Google Scholar]

- Lozano-Medina, J.I.; Hervert-Escobar, L.; Hernandez-Gress, N. Risk profiles of financial service portfolio for women segment using machine learning algorithms. In Computational Science—ICCS 2020. ICCS 2020; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2020; Volume 12143, pp. 561–574. [Google Scholar] [CrossRef]

- Rozi, M.F.; Sucahyo, Y.G.; Gandhi, A.; Ruldeviyani, Y. Appraising Personal Data Protection in Startup Companies in Financial Technology: A Case Study of ABC Corp. In ACM International Conference Proceeding Series; Association for Computing Machinery: New York, NY, USA, 2020; pp. 9–14. [Google Scholar]

- Jiang, H.; Zhang, J. Discovering systemic risks of China’s Listed Banks by CoVaR approach in the digital economy era. Mathematics 2020, 8, 180. [Google Scholar] [CrossRef]

- Li, M.; Hu, D.; Lal, C.; Conti, M.; Zhang, Z. Blockchain-Enabled Secure Energy Trading with Verifiable Fairness in Industrial Internet of Things. IEEE Trans. Ind. Inform. 2020, 16, 6564–6574. [Google Scholar] [CrossRef]

- Yao, S.; Li, J.; Liu, D.; Wang, T.; Liu, S.; Shao, H.; Abdelzaher, T. Deep compressive offloading: Speeding up neural network inference by trading edge computation for network latency. In SenSys 2020—Proceedings of the 2020 18th ACM Conference on Embedded Networked Sensor Systems; Association for Computing Machinery, Inc.: New York, NY, USA, 2020; pp. 476–488. [Google Scholar]

- Cui, Y.; Pan, B.; Sun, Y. A Survey of Privacy-Preserving Techniques for Blockchain. In Artificial Intelligence and Security. ICAIS 2019; Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics); Springer: Cham, Switzerland, 2019; Volume 11635, pp. 225–234. [Google Scholar] [CrossRef]

- Gayathri, S.; Mohana, R.S. Optical Character Recognition in Banking Sectors Using Convolutional Neural Network. In Proceedings of the 3rd International Conference on I-SMAC IoT in Social, Mobile, Analytics and Cloud, I-SMAC 2019, Palladam, India, 12–14 December 2019; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2019; pp. 753–756. [Google Scholar]

- Hasegawa, T. Toward the mobility-oriented heterogeneous transport system based on new ICT environments—Understanding from a viewpoint of the systems innovation theory. IATSS Res. 2018, 42, 40–48. [Google Scholar] [CrossRef]

- Garrido, G.M.; Miehle, D.; Luckow, A.; Matthes, F. A Blockchain-based Flexibility Market Platform for EV Fleets. In Proceedings of the Clemson University Power Systems Conference, PSC 2020, Clemson, SC, USA, 10–13 March 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020. [Google Scholar]

- Gupta, S.; Sharma, H.; Hassija, V.; Saxena, V. BitCom: A Commerce Model on Blockchain. In Proceedings of the 6th International Conference on Signal Processing and Communication, ICSC 2020, Noida, India, 5–7 March 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 64–70. [Google Scholar]

- He, T.; Gui, X.; Zhang, Z.; Zhou, D.; Hu, Z.; Chen, J.; Li, W. Blockchain-Based Distributed Energy Trading Scheme. In Proceedings of the 2020 Asia Energy and Electrical Engineering Symposium, AEEES 2020, Chengdu, China, 29–31 May 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 919–924. [Google Scholar]

- Ozili, P.K. Contesting digital finance for the poor. Digit. Policy Regul. Gov. 2020, 22, 135–151. [Google Scholar] [CrossRef]

- Liu, J.; Li, X.; Wang, S. What have we learnt from 10 years of fintech research? A scientometric analysis. Technol. Forecast. Soc. Change 2020, 155, 120022. [Google Scholar] [CrossRef]

- Ravikumar, S.; Saraf, P. Prediction of stock prices using machine learning (regression, classification) Algorithms. In Proceedings of the 2020 International Conference for Emerging Technology, INCET 2020, Belgaum, India, 5–7 June 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020. [Google Scholar]

- Ampomah, E.K.; Qin, Z.; Nyame, G. Evaluation of tree-based ensemble machine learning models in predicting stock price direction of movement. Information 2020, 11, 332. [Google Scholar] [CrossRef]

- Harahap, L.A.; Lipikorn, R.; Kitamoto, A. Nikkei Stock Market Price Index Prediction Using Machine Learning. J. Phys. Conf. Ser. 2020, 1566, 012043. [Google Scholar] [CrossRef]

- Ismail, M.S.; Md Noorani, M.S.; Ismail, M.; Abdul Razak, F.; Alias, M.A. Predicting next day direction of stock price movement using machine learning methods with persistent homology: Evidence from Kuala Lumpur Stock Exchange. Appl. Soft Comput. J. 2020, 93, 106422. [Google Scholar] [CrossRef]

- Saifan, R.; Sharif, K.; Abu-Ghazaleh, M.; Abdel-Majeed, M. Investigating algorithmic stock market trading using ensemble machine learning methods. Informatica 2020, 44, 311–325. [Google Scholar] [CrossRef]

- Zhang, M. Artificial Intelligence and Application in Finance. In ACM International Conference Proceeding Series; Association for Computing Machinery: New York, NY, USA, 2020; pp. 317–322. [Google Scholar]

- Chang, J.; Ding, Y.; Tu, W. FollowAKOInvestor: Using Machine Learning to Hear Voices from All Kinds of Investors. In Proceedings of the International Conference on Tools with Artificial Intelligence, ICTAI, Baltimore, MD, USA, 9–11 November 2020; IEEE Computer Society: Washington, DC, USA, 2020; pp. 875–882. [Google Scholar]

- Kulshrestha, N.; Srivastava, V.K. Synthesizing Technical Analysis, Fundamental Analysis Artificial Intelligence—An Applied Approach to Portfolio Optimisation Performance Analysis of Stock Prices in India. In Proceedings of the ICRITO 2020—IEEE 8th International Conference on Reliability, Infocom Technologies and Optimization (Trends and Future Directions), Noida, India, 4–5 June 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 1185–1188. [Google Scholar]

- Wong, K.Y.; Wong, R.K. Big data quality prediction on banking applications: Extended abstract. In Proceedings of the 2020 IEEE 7th International Conference on Data Science and Advanced Analytics, DSAA 2020, Sydney, NSW, Australia, 6–9 October 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 791–792. [Google Scholar]

- Ceaparu, C. IT solutions for big data processing and analysis in the finance and banking sectors. Adv. Intell. Syst. Comput. 2021, 1243, 133–144. [Google Scholar] [CrossRef]

- Zhang, Q.; Liu, F. Research on channel model and price dispersion of E-commerce market based on blockchain technology. Wirel. Commun. Mob. Comput. 2020, 2020, 8824754. [Google Scholar] [CrossRef]

- Delger, O.; Tseveenbayar, M.; Namsrai, E.; Tsendsuren, G. Current State of E-Commerce in Mongolia: Payment and Delivery. In Advances in Intelligent Information Hiding and Multimedia Signal Processing; Pan, J.-S., Li, J., Tsai, P.-W., Jain, L., Eds.; Smart Innovation, Systems and Technologies; Springer: Singapore, 2020; pp. 289–297. [Google Scholar]

- Almuhammadi, A. An overview of mobile payments, fintech, and digital wallet in Saudi Arabia. In Proceedings of the 7th International Conference on Computing for Sustainable Global Development, INDIACom 2020, New Delhi, India, 12–14 March 2020; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2020; pp. 271–278. [Google Scholar]

- Kennedyd, S.I.; Guo, Y.; Fu, Z.; Liu, K. The Cashless Society Has Arrived: How Mobile Phone Payment Dominance Emerged in China. Int. J. Electron. Gov. Res. 2020, 16, 94–112. [Google Scholar] [CrossRef]

- Li, M.; Shao, S.; Ye, Q.; Xu, G.; Huang, G.Q. Blockchain-enabled logistics finance execution platform for capital-constrained E-commerce retail. Robot. Comput. Integr. Manuf. 2020, 65, 101962. [Google Scholar] [CrossRef]

- Ferrer-Gomila, J.-L.; Francisca Hinarejos, M.; Isern-Deyà, A.-P. A fair contract signing protocol with blockchain support. Electron. Commer. Res. Appl. 2019, 36, 100869. [Google Scholar] [CrossRef]

- Najdawi, A.; Chabani, Z.; Said, R.; Starkova, O. Analysing the Adoption of E-Payment Technologies in UAE Based on Demographic Variables. In Proceedings of the 2019 International Conference on Digitization: Landscaping Artificial Intelligence, ICD 2019, Sharjah, United Arab Emirates, 18–19 November 2019; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2019; pp. 244–248. [Google Scholar]

- Ding, D.; Chong, G.; Chuen, D.L.K.; Cheng, T.L. From Ant Financial to Alibaba’s Rural Taobao Strategy—How Fintech Is Transforming Social Inclusion. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Dula, C.; Chuen, D.L.K. Reshaping the Financial Order. In Handbook of Blockhain, Digital Finance and Inclusion; Elsevier Inc.: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Jin, B.H.; Li, Y.M.; Li, Z.W. Study on crowdfunding patterns and factors in different phases. In Proceedings of the Americas Conference on Information Systems 2018: Digital Disruption, AMCIS 2018, New Orleans, LA, USA, 16–18 August 2018; Association for Information Systems: Atlanta, GA, USA, 2018. [Google Scholar]

- Stasik, A.; Wilczyńska, E. How do we study crowdfunding? An overview of methods and introduction to new research agenda. J. Manag. Bus. Adm. Cent. Eur. 2018, 26, 49–78. [Google Scholar] [CrossRef]

- Zetzsche, D.; Preiner, C. Cross-Border Crowdfunding: Towards a Single Crowdlending and Crowdinvesting Market for Europe. Eur. Bus. Organ. Law Rev. 2018, 19, 217–251. [Google Scholar] [CrossRef]

- Ferreira, F.; Pereira, L. Success Factors in a Reward and Equity Based Crowdfunding Campaign. In Proceedings of the 2018 IEEE International Conference on Engineering, Technology and Innovation, ICE/ITMC 2018, Stuttgart, Germany, 17–20 June 2018; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2018. [Google Scholar]

- Pokrovskaya, M. Risk mitigation based on innovative solutions. In Proceedings of the International Astronautical Congress, IAC. International Astronautical Federation, IAF (2019), Washington, DC, USA, 21–25 October 2019. [Google Scholar]

- Miraz, M.H.; Donald, D.C. Application of Blockchain in Booking and Registration Systems of Securities Exchanges. In Proceedings of the 2018 International Conference on Computing, Electronics and Communications Engineering, iCCECE 2018, Southend, UK, 16–17 August 2018; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2019; pp. 35–40. [Google Scholar]

- Nasir, F.; Saeedi, M. ‘RegTech’ as a Solution for Compliance Challenge: A Review Article. J. Adv. Res. Dyn. Control Syst. 2019, 11, 912–919. [Google Scholar] [CrossRef]

- Goul, M. Services computing and regtech. In Proceedings of the 2019 IEEE World Congress on Services, SERVICES 2019, Milan, Italy, 8–13 July 2019; Institute of Electrical and Electronics Engineers Inc.: Piscataway, NJ, USA, 2019; pp. 219–223. [Google Scholar]

- Singh, H.; Jain, G.; Munjal, A.; Rakesh, S. Blockchain technology in corporate governance: Disrupting chain reaction or not? Corp. Gov. 2019, 20, 67–86. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. The Cross-Section of Expected Stock Returns. J. Financ. 1992, 47, 427–465. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. A five-factor asset pricing model. J. Financ. Econ. 2014, 116, 1–22. [Google Scholar] [CrossRef]

- Nasir, A.; Khan, K.I.; Mata, M.N.; Mata, P.N.; Martins, J.N. Optimisation of Time-Varying Asset Pricing Models with Penetration of Value at Risk and Expected Shortfall. Mathematics 2021, 9, 394. [Google Scholar] [CrossRef]

- Shaukat, K.; Iqbal, F.; Alam, T.M.; Aujla, G.K.; Devnath, L.; Khan, A.G.; Iqbal, R.; Shahzadi, I.; Rubab, A. The impact of artificial intelligence and robotics on the future employment opportunities. Trends Comput. Sci. Inf. Technol. 2020, 5, 50–54. [Google Scholar]

- Shaukat, K.; Alam, T.M.; Hameed, I.A.; Luo, S.; Li, J.; Aujla, G.K.; Iqbal, F. A comprehensive dataset for bibliometric analysis of SARS and coronavirus impact on social sciences. Data Brief 2020, 33, 106520. [Google Scholar] [CrossRef] [PubMed]

- Alam, T.M.; Mushtaq, M.; Shaukat, K.; Hameed, I.A.; Sarwar, M.U.; Luo, S. A Novel Method for Performance Measurement of Public Educational Institutions Using Machine Learning Models. Appl. Sci. 2021, 11, 9296. [Google Scholar] [CrossRef]

- Shaukat, K.; Luo, S.; Varadharajan, V.; Hameed, I.A.; Xu, M. A survey on machine learning techniques for cyber security in the last decade. IEEE Access 2020, 8, 222310–222354. [Google Scholar] [CrossRef]

- Shaukat, K.; Luo, S.; Varadharajan, V.; Hameed, I.A.; Chen, S.; Liu, D.; Li, J. Performance comparison and current challenges of using machine learning techniques in cybersecurity. Energies 2020, 13, 2509. [Google Scholar] [CrossRef]

- Shaukat, K.; Luo, S.; Chen, S.; Liu, D. Cyber Threat Detection Using Machine Learning Techniques: A Performance Evaluation Perspective. In Proceedings of the 2020 International Conference on Cyber Warfare and Security (ICCWS), Islamabad, Pakistan, 20–21 October 2020; pp. 1–6. [Google Scholar]

- Shaukat, K.; Masood, N.; Khushi, M. A Novel Approach to Data Extraction on Hyperlinked Webpages. Appl. Sci. 2019, 9, 5102. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Results |

|---|---|

| Documents | 1556 |

| Sources (Journals, Books, etc.) | 759 |

| Keywords Plus (ID) | 4453 |

| Author’s Keywords (DE) | 3454 |

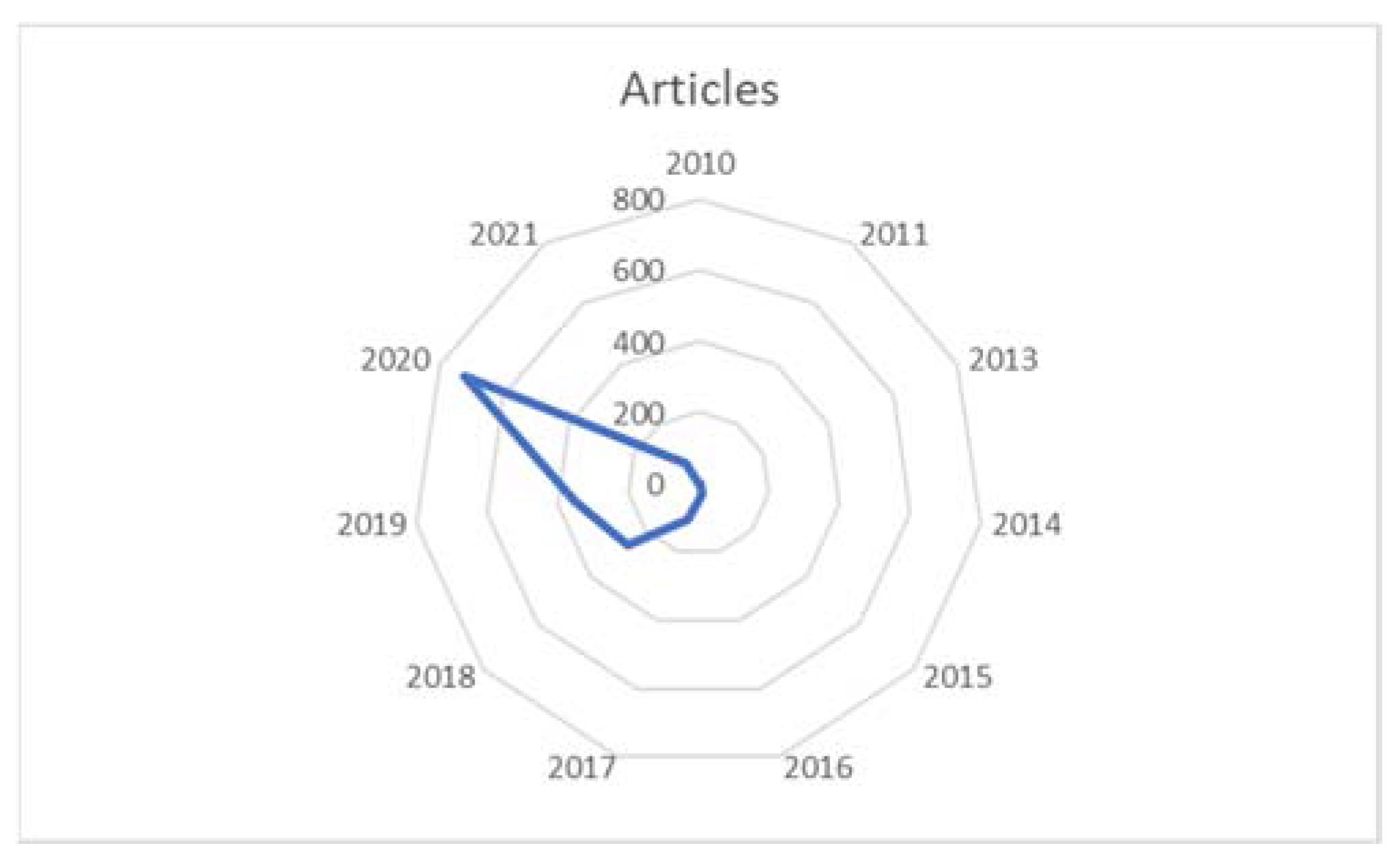

| Period | 2010–2021 |

| Average citations per document | 3.611 |

| Authors | 3483 |

| Author Appearances | 4325 |

| Authors of single-authored documents | 298 |

| Authors of multi-authored documents | 3185 |

| Single-authored documents | 373 |

| Documents per Author | 0.447 |

| Authors per Document | 2.24 |

| Co-Authors per Documents | 2.78 |

| Collaboration Index | 2.69 |

| Document types | |

| Article | 786 |

| Book | 26 |

| Book chapter | 86 |

| Conference paper | 553 |

| Conference review | 22 |

| Editorial | 22 |

| Review | 61 |

| Source | h_Index | g_Index | m_Index | TC | NP | PY_Start |

|---|---|---|---|---|---|---|

| Electronic commerce research and applications | 7 | 13 | 1 | 186 | 15 | 2015 |

| Financial innovation | 7 | 9 | 1 | 148 | 9 | 2015 |

| Technological forecasting and social change | 5 | 9 | 1.25 | 89 | 11 | 2018 |

| European business organisation law review | 5 | 7 | 1.25 | 53 | 9 | 2018 |

| Handbook of blockchain, digital finance, and inclusion | 5 | 5 | 1 | 38 | 9 | 2017 |

| IT professional | 5 | 7 | 1 | 150 | 7 | 2017 |

| Electronic markets | 5 | 6 | 1.25 | 124 | 6 | 2018 |

| Industrial management and data systems | 5 | 6 | 1.25 | 85 | 6 | 2018 |

| Journal of economics and business | 5 | 6 | 1.25 | 231 | 6 | 2018 |

| Journal of management information systems | 5 | 6 | 1.25 | 204 | 6 | 2018 |

| Authors | h_Index | g_Index | m_Index | TC | NP | PY_Start |

|---|---|---|---|---|---|---|

| Panel A: Ranked according to h,g,m index | ||||||

| Arner DW | 4 | 8 | 0.67 | 79 | 10 | 2016 |

| Buckley RP | 4 | 8 | 0.80 | 77 | 8 | 2017 |

| Kauffman RI | 4 | 5 | 0.57 | 150 | 5 | 2015 |

| Li Y | 3 | 7 | 0.60 | 51 | 11 | 2017 |

| Wang S | 3 | 3 | 0.60 | 14 | 8 | 2017 |

| Panel B: Ranked according to total citations | ||||||

| Gomber P | 3 | 3 | 0.60 | 223 | 3 | 2017 |

| Kauffman RI | 4 | 5 | 0.57 | 150 | 5 | 2015 |

| Giudici G | 1 | 2 | 0.25 | 127 | 2 | 2018 |

| Martinazzi S | 1 | 2 | 0.25 | 127 | 2 | 2018 |

| Adhami S | 1 | 1 | 0.25 | 126 | 1 | 2018 |

| Country | Total Citations | Country | Number of Publications |

|---|---|---|---|

| USA | 742 | China | 419 |

| China | 457 | USA | 296 |

| South Korea | 411 | UK | 189 |

| United Kingdom (UK) | 394 | Indonesia | 171 |

| Germany | 376 | India | 157 |

| Italy | 288 | Germany | 117 |

| Taiwan | 211 | South Korea | 114 |

| Switzerland | 185 | Australia | 97 |

| Hong Kong | 168 | Taiwan | 87 |

| Spain | 144 | Italy | 75 |

| Keywords | Clusters | Research Stream |

|---|---|---|

| Blockchain, bitcoin, cryptocurrency, entrepreneurial finance, smart contracts, security, internet of things, venture capital, the financial industry | Red | Cryptocurrencies, smart contracts, and financial technology |

| Fintech, financial inclusion, regulatory sandbox, innovation, financial technology, big data, regulations, regtech, banking, artificial intelligence, financial# (regulations, innovations, service, and stability), digital economy, digitalisation, mobile payment, p2p lending, business model, digital finance. | Blue | Financial industry stability, service, innovation, and regulatory technology (regtech) |

| Deep learning, machine learning, financial technology, stock market. | Green | Machine learning, deep learning and artificial intelligence |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nasir, A.; Shaukat, K.; Iqbal Khan, K.; A. Hameed, I.; Alam, T.M.; Luo, S. Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study. Appl. Sci. 2021, 11, 10353. https://doi.org/10.3390/app112110353

Nasir A, Shaukat K, Iqbal Khan K, A. Hameed I, Alam TM, Luo S. Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study. Applied Sciences. 2021; 11(21):10353. https://doi.org/10.3390/app112110353

Chicago/Turabian StyleNasir, Adeel, Kamran Shaukat, Kanwal Iqbal Khan, Ibrahim A. Hameed, Talha Mahboob Alam, and Suhuai Luo. 2021. "Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study" Applied Sciences 11, no. 21: 10353. https://doi.org/10.3390/app112110353

APA StyleNasir, A., Shaukat, K., Iqbal Khan, K., A. Hameed, I., Alam, T. M., & Luo, S. (2021). Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study. Applied Sciences, 11(21), 10353. https://doi.org/10.3390/app112110353